Telcos need to fill in gaps to be Edge Computing (5G, IIoT) leaders

The rapidly expanding edge computing space represents a $17 billion opportunity for telecom service providers over the next three years, but those companies are being overlooked by enterprises when it comes to deployments, according to a recent study by World Wide Technology done in conjuction with Analysys Mason.

“The Edge Disconnect” report found that service providers’ deep connectivity expertise and investments in 5G infrastructure are advantages, but that they need to fill gaps in their offerings to become a one-stop shop for enterprises looking to expand to the edge with connectivity, infrastructure, and applications.

“Service providers are under immense pressure to monetize 5G infrastructure investments and create cost-reducing efficiencies,” said Dan Graham, global product leader for edge computing at WWT. “Edge computing provides services as close to the end user or device as possible and is essential to the value proposition of 5G. Next-gen applications, including self-driving vehicles, remote surgery, Industrial Internet of Things (IIoT), will all hinge on the edge.”

The report found that IT companies and tech companies, rather than telecoms service providers, are invariably seen as the “edge experts.” In particular, the report authors wrote:

“Connectivity is the cornerstone of an enterprise edge strategy, yet enterprises don’t see connectivity providers as the partner they need to make their strategy a success.”

How can carriers better show off their edge muscles in front of enterprises? WWT makes a number of suggestions based on the research, which, it insisted, “reflected the market’s view and was in no way influenced by WWT’s own perspective on edge.”

By developing a “pre-packaged edge solution” composed of connectivity and system integration capabilities, as well as an application platform (which WWT thinks will generate nearly 60% of the resulting revenue) “telecoms service providers can cement their place in the new era of enterprise data management.”

“Cloud service providers and systems integrators may talk up to their ability to satisfy customers’ connectivity needs, but telecoms service providers have been delivering these services for decades,” reassured the authors. “They have an innate understanding of the intricacies involved, and how these can be optimized.”

……………………………………………………………………………………………………………………………………………..

Industries covered by the research include transport, public sector, manufacturing, retail, financial services and healthcare. In each of these sectors, distributing computing through Edge implementations presents an opportunity to transform data management in line with the realities of an increasingly connected digital economy, as well as introducing new cost efficiencies and improvements to data security and compliance.

The report also identifies the 30 industry-specific Edge use cases likely to deliver the greatest revenue potential, all of which benefit from Edge’s suitability for transformative, data-intensive applications.

Key findings in the report:

- Options: Only 6% of enterprise decision-makers would choose service providers for their edge implementations. Instead, 41% would primarily opt for a technology company, while 31% would go with a public cloud provider.

- Demand: 59% of the $17 billion opportunity is at the level of user-facing application and service platforms, far more than connectivity-focused roles telecom service providers play. Telecom service providers need to expand what they offer beyond connectivity to capture more of the opportunity.

- Edge drivers: Across multiple industries, the top reasons organizers are embracing the edge are newer or enhanced customer experiences, data security and privacy, and cost efficiencies.

- Data management: Enterprises see the edge as a way of reducing data management costs by up to 20%.

The edge continues to be a promising opportunity for telecom service providers, cloud service providers, and channel partners. The report says that service providers’ deep understanding of connectivity is a key advantage. With the assistance of a partner who can bridge any gaps in their knowledge of vertical-specific use cases, they can develop pre-packaged solutions covering all three of the above requirements. Achieve this, and service providers will be on the road to changing enterprise perceptions, increasingly cementing themselves as the de facto partners for enterprise Edge deployments.

Grand View Research analysts predict that the global market for edge computing will grow 37.4% a year through 2027, when it will grow to $43.4 billion. A key catalyst for that growth will be 5G technology, which promises significantly faster speeds and more bandwidth and capacity than current 4G LTE networks.

…………………………………………………………………………………………………………………………………………………

References:

https://channelnomics.com/2020/06/09/ingram-micro-cloud-simplifies-complex-aws-world/

https://www.lightreading.com/the-edge/telcos-need-to-up-their-edge-game—report/d/d-id/761562?

Broadband Forum and LAN Laboratory Expand Certification Program to include XGS-PON

As demand for fiber networks continues to grow, the Broadband Forum has expanded its BBF.247 Optical Network Unit (ONU) Certification Program to include XGS-PON.

This latest update extends the program to a variety of key features needed by operators deploying XGS-PON networks. The certification is just one piece of Broadband Forum’s vision to provide network operators with the tools, open specifications, and open source references necessary to bring new services and technologies to their customers more rapidly. Certified ONU products can be deployed quickly, with improved interoperability to existing Optical Line Terminal (OLT) equipment already deployed. Similarly, certified ONU products will also work directly with newer Broadband Forum specifications, including the forthcoming virtual OMCI specifications and software defined access networks.

The XGS-PON extensions add to the BBF.247 G-PON initiative – which has now certified nearly 100 products since its launch in 2011. The new test plan will see ONUs undergo rigorous testing at Broadband Forum’s official certification program test laboratory Laboratoire des Applications Numeriques (LAN Laboratory), using MT2’s ONU testing solution. The work will confirm conformance to the latest PON ITU-T standards, providing network operators with assurance that they can deliver efficient networks and a high-quality customer experience. New additions to the technology are also now tested, including extended OMCI messages format, Enhanced Unicast & Multicast Operations, and Capacity Tests & Performance Monitoring. This increases the number of certification test cases by more than 50% compared to the previous version.

Eight products, including single or multi-user port ONUs/L2 and Residential Gateways from Altice Labs, CommScope, Huawei, Humax, KAONMEDIA, Sagemcom, Sercomm and ZTE have already been certified under the new BBF.247 certification program.

“The introduction of XGS-PON certification by Broadband Forum is a significant and positive step for the PON ecosystem as interoperability will encourage growth,” said Jaeseok Kim, Head of Infra Planning at SK Broadband. “This will become increasingly important as more operators look to upgrade existing network to meet consumer demand for Gigabit + speeds.”

Claudio Mathys, Product Manager Wireline Access Networks at Swisscom (Schweiz) AG, added: “Establishing interoperability and testing requirements are key elements in a liberated market. The introduction of XGS-PON from Swisscom as a technology leader – in conjunction with the certification and testing program from Broadband Forum – will significantly enhance the confidence from our competitors for CPE certification as based on industry standards and independent references. Achieving Broadband Forum certification is the entry ticket for connectivity to our network. We will definitely avoid the painful experience made with xDSL interoperability/complexity – right from the beginning.”

Hugues Le Bras, Network Engineer in Fixed Access Networks at Orange, said: “The role of interoperability and standards has only become more important as broadband grows in popularity and operators upgrade their networks to meet consumer demand. Orange already requests BBF.247 certification for each ONU deployed on the field. However, this expansion of Broadband Forum’s certification program will give us confidence when deploying next-generation technology that will enable the future era of connectivity. The latest additions to the certification also bring new features, such as flexibility and monitoring, which are essential for Orange throughout the ONU life.”

A future XGS-PON interoperability test event will take place at LAN Laboratory, in Tauxigny, France, from October 5 to 9, 2020, allowing vendors worldwide to exercise their OLT or Optical Network Terminal (ONT) solutions against each other. The event will give all equipment vendors the opportunity to improve the interoperability of their products by testing them against the other solutions presented at the event.

“Our existing G-PON certification has made a significant impact on ensuring products meet standards, and this latest expansion of the program will give operators the confidence to roll out mass XGS-PON deployments,” said Robin Mersh, CEO at Broadband Forum. “We now want to instill this same assurance in the industry for upcoming ITU PON technology, including XGS-PON and NG-PON2. XGS-PON is a major step in network evolution, supporting the expansion of 5G and through BBF.247 certification, we can ensure network interoperability.”

Thierry Doligez, Director of LAN Laboratory, said: “Both operators and vendors increasingly recognize the importance of certification in order to speed up deployment and we are proud to partner with Broadband Forum on this extension of its G-PON certification program. As operators move to upgrade their networks to meet increasing consumer demand, the new testing will make sure they are investing in trusted products which will guarantee a certain level of service. ONU manufacturers will also benefit from this substantial program update as it will give them the chance to prove their conformance against enhanced features.”

For more information or to actively get involved with Broadband Forum’s work on higher speed PON technologies, visit: www.broadband-forum.org.

……………………………………………………………………………………………………………………………………….

BBF.247 certification program is open to all GPON, XG-PON and XGS-PON ONU products with Ethernet Interfaces and is based on the Broadband Forum’s TP-247/IR-247 test plan. It tests conformance to TR-156 and TR-280 using OMCI as defined in the ITU G.988, which are the most critical standards to interoperable implementations.

The Broadband Forum has reviewed and authorized the following independent testing agency to administer the approved BBF.247 tests and assess eligibility of products for the Broadband Forum Certification. For more information or to schedule testing, please contact the laboratory directly:

- LAN www.lanpark.eu

-

- Since 2009, the BBF has collaborated with FSAN (Full Service Access Network) on interoperability testing plugfests on the physical, TC and upper layers for GPON, with FSAN leading on the first two and BBF on the last.

……………………………………………………………………………………………………………………………………………….

About Broadband Forum

Broadband Forum is the communications industry’s leading organization focused on accelerating broadband innovation, standards, and ecosystem development. Our members’ passion – delivering on the promise of broadband by enabling smarter and faster broadband networks and a thriving broadband ecosystem.

A non-profit industry organization composed of the industry’s leading broadband operators, vendors, and thought leaders, our work to date has been the foundation for broadband’s global proliferation and innovation. For example, the Forum’s flagship TR-069 CPE WAN Management Protocol has nearly 1 billion installations worldwide.

Broadband Forum working groups collaborate to define best practices for global networks, enable new revenue-generating service and content delivery, establish technology migration strategies, and engineer critical device, service & development management tools in the home and business IP networking infrastructure. We develop multi-service broadband packet networking specifications addressing architecture, device and service management, software data models, interoperability and certification in the broadband market.

Our free technical reports and white papers can be found at https://www.broadband-forum.org/

About Laboratoire des Applications Numeriques (LAN Laboratory)

The Laboratoire des Applications Numeriques (LAN) is a unique independent laboratory specialized in conformance, interoperability and coexistence tests of devices deployed by telecom operators in the access and home networks (DSL, G-PON, Broadband-PLC, …), by DSOs in Smartgrids networks using powerline communications (G3-PLC), and by the industry in video security networks (E&PoC). LAN also offers on-demand test services dedicated to PON network operators, addressing their needs in terms of pre-deployment qualification tests for each specific network they operate. LAN is one of the Broadband Forum’s Approved Test Laboratory (ATL), the unique one accredited by the Broadband Forum to conduct the worldwide recognized BBF.247 certification tests for G-PON, XG-PON and XGS-PON terminals.

For more information on Laboratoire des Applications Numeriques, please go to www.lanpark.eu, follow @Laboratoire_LAN on Twitter, or send an Email to [email protected].

About MT2

MT2 leads the industry in FTTH G-PON and XGS-PON network test, offering troubleshoot, monitoring deep analysis of products, and ‘single-click’ automated test suite solutions. MT2’s analyzers and OLT emulators have the unique powerful features to allow the user to simply ‘software-select’, and switch between GPON, XG-PON, XGS-PON or NG-PON2, all within the same single system. MT2 ensures the complicated protocols and subscriber internet access traffic complies with every spec, automatically, using a powerful and intuitive user interface, high precision and innovative design. MT2 actively contributes to the Broadband Forum activity, as a test-tool vendor, and developed its FTTH automated test suites for functionality and performance testing, covering BBF.247, TR-309 and TR-255, critical to ensure system quality and full validation of any operator’s FFTH network.

For more information on MT2, please go to www.mt2.fr, follow MT2ftth on LinkedIn, or send an Email to [email protected]

…………………………………………………………………………………………………………………………………………….

References:

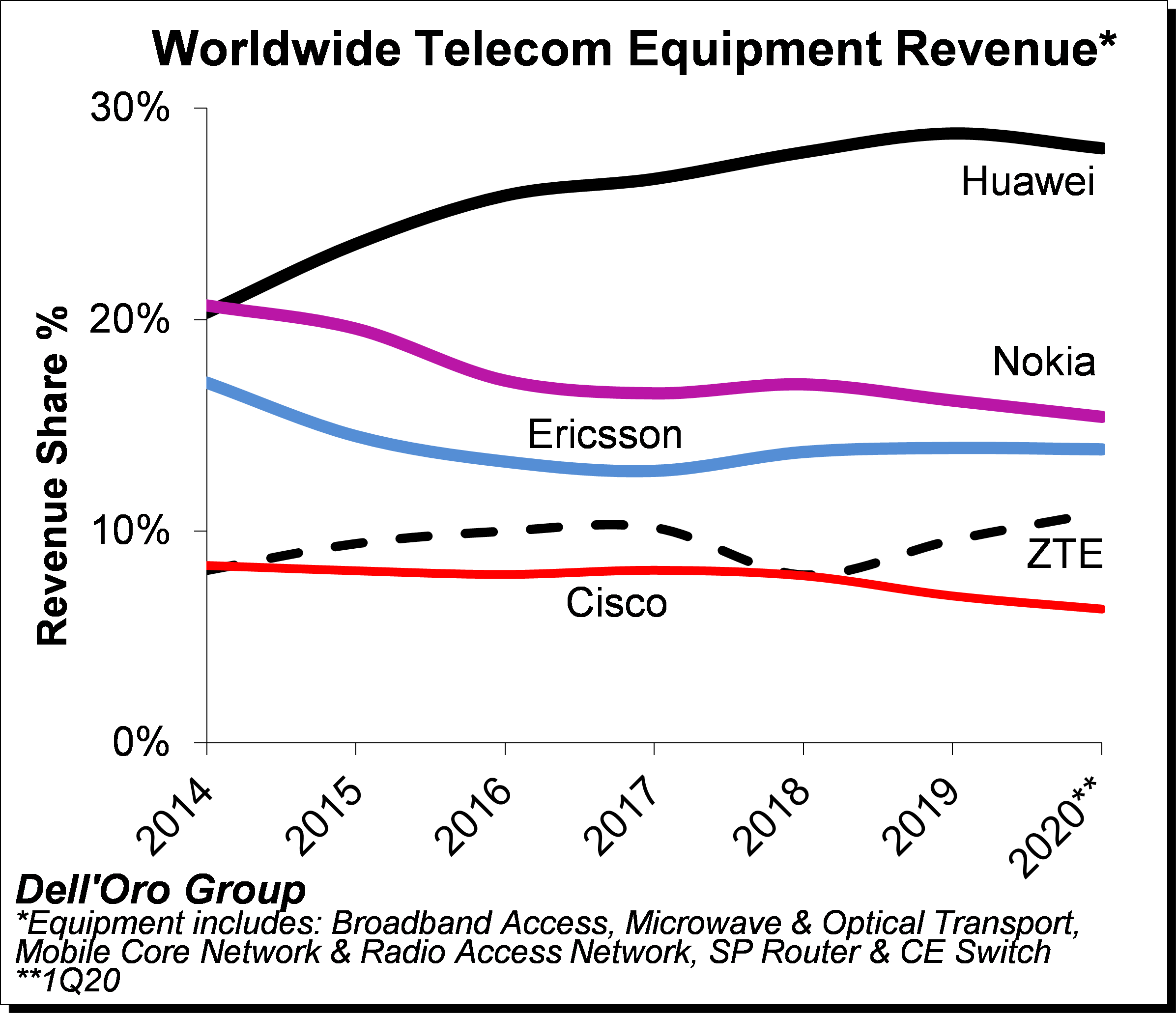

Dell’Oro: Telecom Equipment Market declined 4% YoY; Statista: $49.3B revenues in 2020

Preliminary estimates suggest 1Q20 revenue shares relative to 2019 revenue shares for the top five suppliers – the latter indicated herein parenthesis – show that Huawei, Nokia, Ericsson, ZTE, and Cisco comprised 28% (29%), 15% (16%), 14% (14%), 11% (10%), 6% (7%), respectively.

Table 1: Telecom equipment market shares

| Vendor | 2019 market share | Q1 2020 market share |

| Huawei | 29% | 28% |

| Nokia | 16% | 15% |

| Ericsson | 14% | 14% |

| ZTE | 10% | 11% |

| Cisco | 7% | 6% |

| Source: Dell’Oro Group | ||

Additional key takeaways from the 1Q2020 reporting period include:

- Following two years of consecutive growth in 2018 and 2019, the overall telecom equipment market started the year on a weaker note, reflecting mixed market conditions as the positive market sentiment with mobile-related segments, including RAN and Core, was not enough to offset reduced demand for Broadband Access, Routers and CE Switch, and Optical/Microwave Transport.

- While healthy end-user fundamentals and positive 5G momentum outweighed downward risks associated with the COVID-19 pandemic for both RAN and Core investments, the pandemic had a more material impact on some of the non-wireless related segments, driven partly by supply chain disruptions and weakened demand as a result of increased macroeconomic uncertainty.

- Within the technology segments, Mobile RAN and Core revenues together advanced at a single-digit rate, accounting for nearly half of the overall telecom equipment market during 1Q20. At the same time, the combined revenues for Broadband Access, Microwave Transport, and Routers and CE Switch declined at a double-digit pace Y/Y, accounting for about a third of the overall market.

- In contrast to previous recessions, the COVID-19 slowdown is shifting and transforming the way we use the network. But a shift in how users are consuming data doesn’t necessarily result in a corresponding increase in spending on new infrastructure to support that traffic growth. Some suppliers and service providers indicated that network capacity upgrades were required to accommodate data traffic growth, however, traffic surges did not lead to significant demand for network capacity upgrades across all the telecom equipment segments.

- Even though the pandemic is still inflicting high human and economic losses, the Dell’Oro analyst team collectively expect market conditions and supply chain risks to be more favorable in the second half of 2020, propelling the overall telecom equipment market to advance 1% in 2020, reflecting a downward revision from the previous 2% growth outlook.

Dell’Oro Group telecommunication infrastructure research programs consist of: Broadband Access, Microwave Transmission & Mobile Backhaul, Mobile Core Networks, Mobile Radio Access Network, Optical Transport, and Service Provider (SP) Router & Carrier Ethernet Switch.

…………………………………………………………………………………………………….

Separately, Statista reports that telecom equipment spending is projected to increase from 44.8 billion U.S. dollars in 2015 to around 49.3 billion U.S. dollars in 2020. In 2019, the estimated revenue of the entire global telecommunications industry was US $610.4 billion.

Ericsson, Cisco Systems, Fujitsu, Nokia, NEC Corporation and Qualcomm are the leading telecom equipment companies worldwide. Cisco Systems is the leading Ethernet switch vendor, with more than 50 percent of the market share. Ethernet switches are an important and profitable part of the industry, as they are an integral part of IT infrastructure. They are used to receive, process and transmit data between two devices connected by a physical layer. Together, the top 5 vendors of Ethernet switches generated more than 25 billion U.S. dollars in revenue in 2017. Cisco is also the main vendor of enterprise WLAN, accounting for 45 percent of the global market share. HPE/Aruba, Arris/Ruckus, Ubiquiti and Huawei are also important vendors of enterprise WLAN worldwide.

Ethernet switch, WLAN and telecom towers are only a few examples of telecom equipment. This industry is vast, and includes other important markets such as smartphones. More than 1.5 billion smartphones were sold worldwide in 2017. Samsung, the global mobile market leader since 2012, sold about 20 percent of this total. Apple and Huawei are Samsung’s closest competitors in the market, with around 14 percent and 10 percent of the global smartphone market share respectively.

References:

OMDIA: South Korea is 5G market leader amongst 22 countries

Market research firm OMDIA – formerly known as Ovum (including IHS-Markit IT acquisition) – has released the first version of its 5G Market Progress Assessment (end-2019) report, showing that South Korea is the undisputed leading country for 5G deployment in the twenty two leading 5G countries analyzed for their deployment of 5G technology.

The OMDIA research assessed the deployment progress of 5G based on operator launches, network coverage, subscriber take-up as well as 5G spectrum availability and regulatory ecosystem.

Based on these factors OMDIA’s research concluded that South Korea – as it did in the 4G era – has established itself as the early market-leader for 5G technology deployment. South Korea, Kuwait, and Switzerland are among a small group of markets notable for 5G coverage exceeding 50% of their subscriber base.

According to the report, South Korea is leading the way with adoption reaching 4.67 million subscribers at the end of December, which equates to about seven per cent of wireless services in the market. That number is now over 6 million as we reported in this article.

- Spectrum – 2,680 MHz across the 3.5 and 28 GHz bands

- Service launches – all three Korean service providers have commercial offerings available to the mass market, and MVNO services have been launched

- Network coverage – approximately 90% population coverage

- 5G take-up – 4.67 million 5G subscribers, or 7% of the mobile market

- Ecosystem – Strong government support and leading local vendor ecosystem

South Korea has exceeded expectations in each of the above criteria, a trend which should continue over the next few years in light of the government’s intention to make a further 2,640 MHz of bandwidth available for 5G networks by 2026.

Editor’s Note: South Korea’s IMT 2020 RIT submission (see Document IMT-2020/25) is being progressed by ITU-R WP5D, even though an ATIS sponsored evaluation group [ATIS WTSC IMT-2020 Independent Evaluation Group (IEG)] found that it is technically identical to the 3GPP submission.

…………………………………………………………………………………………………………………………………………..

“Limited coverage, device availability and cautious launches has limited take-up in other global markets,” said Stephen Myers, OMDIA Principal Analyst. “However, expansive coverage rolled out by Sunrise and Swisscom in Switzerland, Ooredoo and Vodafone in Qatar and Kuwait’s three service providers has rivalled Korea for breadth of market coverage.”

The report is based on data relating to the end-December period and was originally due for publication in mid-March but was delayed because of the impact of COVID-19.

Omdia Principal Analyst Stephen Myers said:

The global market is steadily gearing up for 5G deployment but right now South Korea is leading the way – although markets like Switzerland have also made steady progress.

Across the world we are seeing governments and regulators fine-tuning their 5G spectrum allocations and operators get ready for their 5G launches and expand network coverage in those countries where 5G has already launched.

We can expect to see a much larger number of commercial 5G launches in major global markets in the next 12-18 months as more spectrum is released across the world.

The full 5G Market Progress Assessment, end-2019 report can be purchased from OMDIA by contacting [email protected].

References:

https://www.realwire.com/releases/OMDIA-ranks-South-Korea-as-top-global-5G-market

https://www.omdia.com/resources/product-content/5g-market-progress-assessment-end2019-glb007-000395

South Korea 5G subscribers top 6 million at end of April 2020

Dell’Oro: Data Center Switch market declined 9% YoY; SD-WAN market increased at slower rate than in 2019

Market research firm Dell’Oro Group reported today that the worldwide Data Center Switch market recorded its first decline in nine years, dropping 9 percent year-over-year in the first quarter. 1Q 2020 revenue level was also the lowest in three years. The softness was broad-based across all major branded vendors, except Juniper Networks and white box vendors. Revenue from white box vendors was propelled mainly by strong demand from Google and Amazon.

“The COVID-19 pandemic has created some positive impact on the market as some customers pulled in orders in anticipation of supply shortage and elongated lead times,” said Sameh Boujelbene, Senior Director at Dell’Oro Group. “Yet this upside dynamic was more than offset by the pandemic’s more pronounced negative impact on customer demand as they paused purchases due to macro-economic uncertainties. Supply constraints were not major headwinds during the first quarter but expected to become more apparent in the next quarter,” added Boujelbene.

Additional highlights from the 1Q 2020 Ethernet Switch – Data Center Report:

- The revenue decline was broad-based across all regions but was less pronounced in North America.

- We expect revenue in the market to decline high single-digit in 2020, despite some pockets of strength from certain segments.

The Dell’Oro Group Ethernet Switch – Data Center Quarterly Report offers a detailed view of the market, including Ethernet switches for server access, server aggregation, and data center core. (Software is addressed separately.) The report contains in-depth market and vendor-level information on manufacturers’ revenue; ports shipped; average selling prices for both Modular and Fixed Managed and Unmanaged Ethernet Switches (1000 Mbps,10, 25, 40, 50, 100, 200, and 400 GE); and regional breakouts. To purchase these reports, please contact us by email at [email protected].

…………………………………………………………………………………………………………………………………………………

Separately, Dell’Oro Group reported that the market for software-defined (SD)-WAN equipment increased by 24% in the first quarter (year-to-year), which was significantly below the 64% growth seen in 2019. Citing supply chain issues created by the coronavirus pandemic, the market research firm’s Shin Umeda predicted the market will post double-digit growth in 2020 despite “macroeconomic uncertainty.”

- Supply chain disruptions accounted for the majority of the Service Provider (SP) Router and CES Switch market decline in 1Q 2020.

- The SP Router and CES market in China showed a modest decline in 1Q 2020, but upgrades for 5G infrastructure are expected to drive strong demand over the rest of 2020.

Rakuten Mobile, Inc. and NEC to jointly develop the containerized standalone (SA) 5G core network

Japanese upstart carrier Rakuten Mobile, Inc. and NEC Corporation today announced that they have reached an agreement to jointly develop the containerized standalone (SA) 5G core network (5GC) to be utilized in Rakuten Mobile’s fully virtualized cloud native 5G network.

Based on the agreement, Rakuten Mobile and NEC will jointly develop the containerized SA 5G mobile core to be made available on the Rakuten Communications Platform (RCP), Rakuten Mobile’s fully virtualized and containerized cloud-native mobile network platform. The two companies will collaborate to build a Japan-made, highly reliable 5GC, based on the 5GC software source code developed by NEC. Subsequent to the launch of its non-standalone (NSA) 5G service in 2020, Rakuten Mobile aims to provide its SA 5G service in Japan in 2021.

The containerized 5GC will also play a key role in the global expansion of RCP, a platform aimed at offering solutions and services for the deployment of virtualized networks at speed and low cost by telecom companies and enterprises around the world, tailored for their unique needs. The 5GC will be offered as an application on the RCP Marketplace, allowing customers to quickly and easily “click, purchase and deploy” a fully virtualized SA 5G core network solution.

…………………………………………………………………………………………………….

Editor’s Note: The two companies don’t state what spec they’re using for their container based SA 5G Core Network.

–Please see Tareq Amin’s Comment below.

The only standards work we know of related to SA 5G Core Network is in 3GPP (5GCN), but it’s based on a NFV enabled network cloud and a service based architecture, rather than containers.

We suggest that NEC contribute this spec to both 3GPP and ITU-T (for IMT 2020 non-radio aspects). However, neither ITU-R or ITU-T has any serious ongoing work related to the 5G Core Network at this point in time.

The 3GPP specified 5G core network covers both wire-line and wireless access. Key characteristics:

Control plane is separated from the data plane and implemented in a virtualized environment

Fully distributed network architecture with single level of hierarchy

GW to GW interface to support seamless mobility between 5G-GW

Traffic of the same flow can be delivered over multiple RITs

From the latest 3GPP Release 16 – TS.23501 5G Systems Architecture-V16.4.0 (2020-03):

The 5G System architecture is defined to support data connectivity and services enabling deployments to use techniques such as e.g. Network Function Virtualization and Software Defined Networking. The 5G System architecture shall leverage service-based interactions between Control Plane (CP) Network Functions where identified. Some key principles and concept are to:

– Separate the User Plane (UP) functions from the Control Plane (CP) functions, allowing independent scalability, evolution and flexible deployments e.g. centralized location or distributed (remote) location.

– Modularize the function design, e.g. to enable flexible and efficient network slicing.

– Wherever applicable, define procedures (i.e. the set of interactions between network functions) as services, so that their re-use is possible.

– Enable each Network Function and its Network Function Services to interact with other NF and its Network Function Services directly or indirectly via a Service Communication Proxy if required. The architecture does not preclude the use of another intermediate function to help route Control Plane messages (e.g. like a DRA).

– Minimize dependencies between the Access Network (AN) and the Core Network (CN). The architecture is defined with a converged core network with a common AN – CN interface which integrates different Access Types e.g. 3GPP access and non-3GPP access.

– Support a unified authentication framework.

– Support “stateless” NFs, where the “compute” resource is decoupled from the “storage” resource.

– Support capability exposure.

– Support concurrent access to local and centralized services. To support low latency services and access to local data networks, UP functions can be deployed close to the Access Network.

ITU-T SG13 is working on IMT 2020 non-radio aspects, but are heavily dependent on 3GPP documents to be liased in order to drive their future standards work in that area. Unfortunately that has not happened.

Please see Comment in box underneath this article for GSMA Feb 2020 document on SA 5G Core option 2 guidelines for implementation.

………………………………………………………………………………………………………………………………..

“We are very excited to collaborate with NEC on the development of our standalone 5G core network,” commented Tareq Amin, Representative Director, Executive Vice President and CTO of Rakuten Mobile. “Our partnership with NEC represents a joint collaboration to build an open, secure and highly scalable 4G and 5G cloud native converged core, that will also become a key feature of the highly competitive services we will offer to global customers through the Rakuten Communications Platform.”

“NEC is proud to be the 5GC development partner for Rakuten Mobile’s advanced, fully virtualized, cloud-native network. Following the BSS/OSS for the 4G network and 5G radio equipment that we have already begun offering, we look forward to providing a high-quality, highly reliable 5GC and contributing to Rakuten Mobile’s 5G services,” said Atsuo Kawamura, Executive Vice President and President of the Network Services Business Unit, NEC.

Through the joint development of the SA 5GC, Rakuten Mobile and NEC aim to drive innovation in global mobile technology and provide high quality 5G network technology to customers both in Japan and around the world.

Rakuten Mobile CTO Tareq Amin clarification comments; via edited email to this author:

NEC/Rakuten 5GC is 3GPP standardized software for network service and a de facto standard container basis infrastructure (“infrastructure agnostic”). It is a forward looking approach, but not proprietary.

1. 3GPP standardized software for network service:

NEC/Rakuten 5GC openness are realized by implementation of “Open Interface” defined in 3GPP specifications (TS 23.501, 502, 503 and related stage 3 specifications).

2. Containerization/Cloud native:

3GPP 5GC specification requires cloud native 5G core (5GC) architecture as the general concept (service based architecture). It should be distributed, stateless, and scalable. However, an explicit reference model is out of scope for the 3GPP specification. Therefore NEC 5GC cloud native architecture is based on above mentioned 3GPP concept as well as ETSI NFV treats “container” and “cloud native”, which NEC is also actively investigating to apply its product.

3. Reference To Open RAN in the press release:

This has no relationship to 5G Core, but only an indication that our Radio Access Network (RAN) architecture is O-RAN Compliant.

……………………………………………………………………………………………………………………………………….

Press Release:

Forward Reference:

Rakuten Communications Platform (RCP) defacto standard for 5G core and OpenRAN?

About Rakuten Mobile

Rakuten Mobile, Inc. is a Rakuten Group company responsible for mobile communications, including mobile network operator (MNO) and mobile virtual network operator (MVNO) businesses, as well as ICT and energy. Through continuous innovation and the deployment of advanced technology, Rakuten Mobile aims to redefine expectations in the mobile communications industry in order to provide appealing and convenient services that respond to diverse customer needs.

About NEC Corporation

NEC Corporation has established itself as a leader in the integration of IT and network technologies while promoting the brand statement of “Orchestrating a brighter world.” NEC enables businesses and communities to adapt to rapid changes taking place in both society and the market as it provides for the social values of safety, security, fairness and efficiency to promote a more sustainable world where everyone has the chance to reach their full potential.

more information, visit NEC at http://www.nec.com.

Contacts:

Rakuten, Inc. Corporate Communications Department

[email protected]

NEC Corporation Corporate Communications Division

[email protected]

South Korea 5G subscribers top 6 million at end of April 2020

More than 6 million South Koreans were subscribed to 5G mobile networks as of April, a year after the country adopted the service, according to government data reported Monday, June 1st. The number of 5G users in the nation reached 6.34 million as of the end of April, up 7.8 percent from a month earlier, according to the data compiled by the Ministry of Science and ICT.

South Korea’s three carriers — SK Telecom Co., KT Corp. and LG Uplus Corp. — rolled out the commercial 5G network last April and have aggressively promoted their new service for premium smartphones.

SK Telecom’s 5G customers accounted for 45 percent as of April, trailed by KT with 30.3 percent and LG Uplus with 24.7 percent, the ministry said.

The number of mobile subscribers between 2G and 5G came to 69.35 million as of the end of April, the ministry said.

In May, South Korean operator KT added 360,000 5G subscribers in the first quarter of the year, the telco said in its earnings statement. KT, which launched commercial 5G services in April 2019, ended Q1 with a total of 1.78 million 5G customers.

“Since the launch of KT’s 5G services, we are currently maintaining a much higher market share in 5G compared to the market share we have for the LTE handsets,” Kyung-Keun Yoon, KT’s CFO, said during a conference call with investors.

It’s important to note that Korea has its own version of IMT 2020 RIT/SRIT being progressed by ITU-R WP 5D. The country’s IMT 2020 submission is based on 3GPP Release 15 “5G NR.” It is not clear if there are any technical differences between Korea and 3GPP IMT 2020 submissions and if so, what they are.

References:

https://en.yna.co.kr/view/AEN20200601006000320

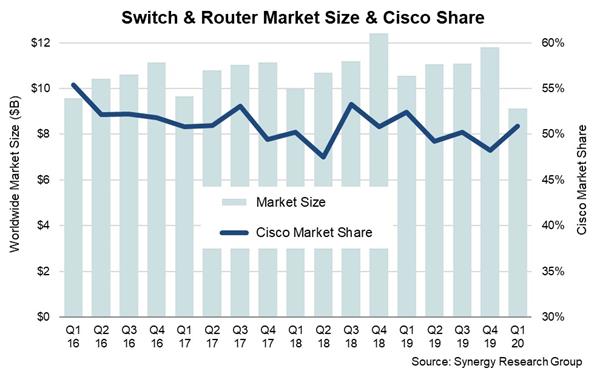

Synergy Research: Ethernet Switch & Router revenues drop to 7 year low in Q1-2020

Revenues from the Ethernet switch and router market fell 14 percent to a seven-year low of $9.1 billion in Q1 2020, according to Synergy Research Group. Ethernet switches, enterprise routers and service provider routers all saw double digit declines in Q1-2020.

Ethernet switching is the largest of the three segments accounting for 62% of the total Q1 market. While GbE switches remain the largest segment in both fixed and modular Ethernet switches, the most notable feature of the market is the rapid deployment of 100 GbE and 25 GbE fixed switches. Both of these segments actually grew in the first quarter.

In Q1-2020, revenues from enterprise routers were down 15% from 2019, but on a trailing twelve month basis the market still grew thanks to strong numbers in the previous three quarters. Service Provider routers saw the biggest decline in the first quarter, down 19% from 2019. In Q1 North America remained the biggest region accounting for almost 40% of worldwide revenues, followed by APAC, EMEA and Latin America. In aggregate across all switch and router segments, year-on-year revenue declines were broadly similar across the major regions.

Comment from IEEE 802.3 Ethernet standards veteran Geoff Thompson:

Revenue is deceptive in this market which has been characterized by falling prices per function for many years. In a market where the dominant function is trunk switching and higher speeds per lane are coming on line every year that is a very difficult ride.

You have to keep the functional volume growing enough to overcome both the price erosion per transistor and the higher cost efficiency of faster lanes as well as maintain your market share in order to grow your revenue. That is very, very tough.

Cisco’s market share in switches and routers was 51% in Q1, meaning that for eight of the last twelve quarters it has been over the 50% mark. Across the three main markets, Cisco’s Q1 share was 57% for Ethernet switches, 65% for enterprise routers and 35% for service provider routers. Behind Cisco the ranking of vendors was different in each of the three markets, but in aggregate Cisco is followed by Huawei, Nokia, Juniper, Arista Networks and HPE. Beyond this leading group, other active vendors include Ericsson, Extreme, H3C and ZTE.

“In a market that is usually characterized by relative stability and predictability, the first quarter represented a sharp change from the norm, clearly as a result of COVID-19. In a pre-pandemic world we’d have expected total vendor revenues from switches and routers to have been a billion dollars higher that what we actually saw,” said John Dinsdale, a Chief Analyst at Synergy Research Group.

“On balance the Q1 hit was driven more by supply chain issues rather than by soft demand. We’d expect supply chain problems to be resolved reasonably quickly, but demand is a different story. On the service provider side demand remains robust as network traffic continues to grow, but enterprise demand will be a much spottier picture and some sectors will take several months before returning to some form of normality.”

![]()

……………………………………………………………………………………………………………………………

About Synergy Research Group

Synergy provides quarterly market sizing and segmentation data on networking, IT and cloud-related markets, including company revenues by segment and by region. Synergy Research Group ( www.srgresearch.com ) helps marketing and strategic decision makers around the world via its unique insights and in-depth analytics.

To speak to an analyst or to find out more about how to access Synergy’s market data, please contact Heather Gallo @ [email protected] or at 775-852-3330 extension 101.

Press Release:

Ultra Oxymoron: GSMA teams up with O-RAN Alliance without liaison with 3GPP or ITU

The GSMA and O-RAN Alliance are cooperating to accelerate the adoption of Open Radio Access Network (RAN) products and solutions that take advantage of new open virtualized architectures, software and hardware. The organizations will work together to harmonize the open networking ecosystem and agree on an industry roadmap for network solutions, thereby making access networks as open and flexible as possible for new market entrants.

GSMA. made up with established wireless telcos and incumbent network equipment vendors, says that “5G will facilitate the opportunity to create even more agile, purpose-built networks tailored to the different needs of citizens, enterprises and society. For example, 5G is an essential ingredient of the European Commission’s recently launched Industrial Strategy and will help shape its future.”

O-RAN Alliance is a world-wide community of more than 170 mobile operators, vendors, and research & academic institutions operating in the Radio Access Network (RAN) industry. It’s mission is to re-shape the industry towards more intelligent, open, virtualized and fully interoperable mobile networks. The new O-RAN standards will enable a more competitive and vibrant RAN supplier ecosystem with faster innovation to improve user experience. O-RAN-compliant mobile networks will at the same time improve the efficiency of RAN deployments as well as operations by the mobile operators.

……………………………………………………………………………………………………………………………………………….

Author’s Opinion:

So here we have an upstart consortium (O-RAN Alliance), cooperating with an established mobile ecosystem marketing machine (GSMA) to promote “open and interoperable mobile networks.” Yet the only way for that to be realized is through adherence to “open” standards and cooperating closely with recognized standards bodies. That is the way interoperability is obtained- by defining open interfaces, layers and protocols!

Instead, O-RAN is making their own specifications (e.g. virtual RAN) that are not part of any 5G standard or 3GPP spec! In particular, the O-RAN Alliance has no liaisons with either 3GPP or ITU-R or ITU-T. How is then possible to specify open hardware and software without any inter-change of documents with those standards organizations? One would think that liaisons, spec iterations, close cooperation with feedback would be essential for success, e.g. a closed loop ecosystem between standards bodies and open source consortiums is urgently needed!

……………………………………………………………………………………………………………………………………………….

In its latest Mobile Economy Report, the GSMA predicts that operators will invest more than a trillion dollars over the next five years globally to serve both consumer and enterprise customers, 80 per cent of which will be on 5G networks.

“When 5G reaches its potential, it will become the first generation of mobile networks to have a bigger impact on enterprises than consumers,” said Alex Sinclair, Chief Technology Officer, GSMA. “In the enterprise sector alone, we forecast $700 billion worth of economic value to be created by the 5G opportunity. The growth of the open networking ecosystem will be essential to meeting enterprise coverage and services needs in the 5G era.”

“As the demand for data and vastly expanded mobile communications grow in the 5G era, a global, cross-border approach is needed to rethink the RAN,” said Andre Fuetsch, Chairman of the O-RAN ALLIANCE, and Executive Vice President and Chief Technology Officer, AT&T. “The GSMA collaboration with the O-RAN ALLIANCE is exactly the sort of global effort that’s needed for everyone, operators and vendors alike, to succeed in this new generation.”

Mobile operators are re-evaluating the way that their networks are deployed. New virtualised architectures with open interfaces can drive cost efficiencies and allow operators to accelerate the deployment of 5G networks. Also, open interfaces can help diversify and reinvigorate the supply chain promoting competition and innovation – for example, by building and operating a RAN based on mix-and-match components from different vendors.

The GSMA and O-RAN ALLIANCE collaboration complements the recently announced inter-working between the GSMA and Telecom Infra Project (TIP), and the O-RAN Alliance and TIP. The goal for these collaborations is to help avoid fragmentation and accelerate the successful evolution of the industry towards a more intelligent, open, virtualized and fully interoperable RAN (see Author’s Opinion above) why this is highly unlikely to happen).

Image Credit: O-RAN Alliance

…………………………………………………………………………………………………………………………………………………

June 12, 2020 Update: Press Release from Mavenir and Aliostar:

“Very few companies are participating in the current (OpenRAN) supply chain and mostly offering proprietary radio solutions lacking open interfaces that are not interoperable with other network elements. In addition, the requirement to procure products from trusted vendors in the US market is also causing operators to reconsider supplier options. OpenRAN radios provide new possibilities for operators to implement a secure, cost effective and best of breed solution as networks move to 5G and beyond.”

Mavenir and Altiostar Collaborate to Deliver OpenRAN Radios for US Market

……………………………………………………………………………………………………………………………………………………….About the GSMA

The GSMA represents the interests of mobile operators worldwide, uniting nearly 750 operators with almost 300 companies in the broader mobile ecosystem, including handset and device makers, software companies, equipment providers and internet companies, as well as organisations in adjacent industry sectors. The GSMA also produces industry-leading events such as Mobile World Congress, Mobile World Congress Shanghai, Mobile World Congress Americas and the Mobile 360 Series of conferences.

For more information, please visit the GSMA corporate website at www.gsma.com. Follow the GSMA on Twitter: @GSMA.

About O-RAN ALLIANCE

O-RAN ALLIANCE is a world-wide community of more than 170 mobile operators, vendors, and research & academic institutions operating in the Radio Access Network (RAN) industry. As the RAN is an essential part of any mobile network, O-RAN ALLIANCE’s mission is to re-shape the industry towards more intelligent, open, virtualized and fully interoperable mobile networks. The new O-RAN standards will enable a more competitive and vibrant RAN supplier ecosystem with faster innovation to improve user experience. O-RAN-compliant mobile networks will at the same time improve the efficiency of RAN deployments as well as operations by the mobile operators. To achieve this, O-RAN ALLIANCE publishes new RAN specifications, releases open software for the RAN, and supports its members in integration and testing of their implementations.

For a short video describing O-RAN’s progress, see www.o-ran.org/videos

For more information please visit www.o-ran.org

Media Contacts:

For the GSMA

Alia Ilyas

+44 (0) 7970 637622

[email protected]

GSMA Press Office

[email protected]

O-RAN ALLIANCE:

Zbynek Dalecky

[email protected]

O-RAN Alliance e.V.

Buschkauler Weg 27

53347 Alfter/Germany

……………………………………………………………………………………………………………………………………………..

References:

GSMA and O-RAN Alliance Collaborate on Opening up 5G Networks

5G breaks from proprietary systems, embraces open source RANs

Qualcomm SoCs for Wi-Fi 6E in 6GHz band and Bluetooth 5.2 with superior performance

Qualcomm has launched a new portfolio of flagship mobile system on a chip (SoC) featuring support for Wi-Fi 6E (aka IEEE 802.11ax), which will soon be operational in the 6 GHz band. The first products to be launched are two SoCs, the Qualcomm FastConnect 6900 and the Qualcomm FastConnect 67000.

The FastConnect 6900 will provide speeds of up to 3.6 Gbps, implementation of 4-stream Dual Band Simultaneous (DBS) with multiband (including 6 GHz) capabilities. The FastConnect 6700 chip will meanwhile deliver speeds approaching 3 Gbps. The Verge noted that one of the chips will be for smartphones and the other for routers.

Both chips will both support Wi-Fi 6, low latency, and Bluetooth audio features for classic and new use cases. They will sport Qualcomm 4K QAM for enhanced gaming and ultra HD streaming and 160 MH channels support in both 5 and 6 GHz bands, expanding throughput while reducing congestion. They will also help save power, by generating less channel congestion. The chips are now sampling and will ship in production during the second half of 2020.

“Wi-Fi 6E delivers an unprecedented improvement in capacity to meet the rapid growth of connected devices and data demand. The introduction of supporting chipsets so soon after the FCC ruling ensures customers will see the benefits quickly and is an indicator of both Qualcomm Technologies’ investment and broad industry collaboration,” said Geoff Blaber, vice president, research, Americas, CCS Insights.

“Wi-Fi Alliance® members have mobilized around 6 GHz in an unprecedented way, and we’re excited to see Wi-Fi 6E solutions rapidly coming to market with the availability of new unlicensed spectrum in the U.S.,” said Kevin Robinson, Senior VP of Marketing, Wi-Fi Alliance. “Solutions like these from Qualcomm will help users fully experience Wi-Fi® in 6 GHz and quickly benefit from faster speeds, higher capacity, and lower latency applications.”

Next-Generation Wi-Fi 6E for Mobile and Computing

New portfolio extends advanced Wi-Fi 6 feature implementations into the 6 GHz band. Key features include:

Unmatched Wi-Fi Speed:

- FastConnect 6900 offers the fastest available Wi-Fi 6 speed, up to 3.6 Gbps, of any mobile Wi-Fi offering in the industry.

- FastConnect 6700 delivers impressive peak speeds approaching 3 Gbps.

Driving this performance for both FastConnect systems are differentiated features such as:

- Qualcomm® 4K QAM (2.4, 5, 6 GHz) – an industry first implementation of this advanced modulation technique can extend the maximum QAM rate, across any supported band, from 1K to 4K for enhanced gaming and ultra HD streaming.

- 160 MHz channels support in both 5 and 6GHz bands, dramatically expanding throughput while reducing congestion.

FastConnect 6900 delivers an extra boost of performance through additional unique feature implementation of 4-stream Dual Band Simultaneous (DBS) with multi-band (including 6 GHz) capabilities.

Essential Improvement of Capacity and Network Efficiency: Delivering reliable performance, even in the most congested home, enterprise and public networks.

- 6 GHz dramatically expands Wi-Fi capacity by adding up to 1200 MHz of additional spectrum, more than doubling the number of pathways currently available for sending and receiving data.

- Dual band 160 MHz supports up to seven additional non-overlapping channels in the 6 GHz band, in addition to 160 MHz channels available in the 5 GHz band.

- Deploys high-performance Uplink / Downlink MU-MIMO and OFDMA mobile technologies across all available bands.

- New Wi-Fi 6 Uplink MU-MIMO capability can increase network capacity by more than 2.5x.

Ultra-Low Latency: A new class of low latency and high speed for emerging mobile applications, providing the foundation for explosive growth in mobile gaming and XR application.

- Feature implementation delivers latency reduction up to 8x in congested environments for dramatically improved mobile gaming experiences.

- Wireless VR-class latency (<3ms) for Head Mounted Displays (HMD) provides a strong foundation for this rapidly growing industry segment.

Advanced Technology and Power Efficiency: Power savings due to less channel congestion and improved scheduling.

- 14nm process node combined with advanced power-management architecture provides up to 50 percent improvement in power efficiency, compared to previous generation solutions.

Bluetooth 5.2 with Advanced Audio

FastConnect 6900 and 6700 integrate Bluetooth 5.2 with the latest audio advancements for greatly improved wireless experiences. Key features include:

Bluetooth 5.2 Above and Beyond

- Leading Bluetooth 5.2 implementation includes a second Bluetooth antenna with intelligent switching capabilities, overcoming common signal shadowing issues for unparalleled Bluetooth reliability and range.

- Engineered to be ready to address emerging LE Audio experiences such as multi-point audio sharing and broadcast audio, enabling multiple audio connections simultaneously.

Superior Bluetooth Audio

- Qualcomm® aptX™ Adaptive supporting wire-equivalent audio (up to 96kHz) and Qualcomm® aptX™ Voice providing super-wideband quality calls.

End-to-End Enhanced Experiences

- When paired with the premium features of Qualcomm® QCC5141, QCC5144, QCC3046 and QCC3040 Audio SoCs, users can expect robust, premium audio quality with low power consumption.

- Innovative transmit power and coexistence algorithms deliver materially improved range and link robustness.

………………………………………………………………………………………………………………………………………………

“Leveraging decades of focused research and development, our second-generation Wi-Fi 6 platforms set a new performance benchmark for home and enterprise networking applications,” said Nick Kucharewski, vice president and general manager, wireless infrastructure and networking, Qualcomm Technologies, Inc. “With Tri-Band Wi-Fi 6 and scaling to 16 streams, Qualcomm Networking Pro Series Platforms pair wireless expertise with robust architecture designed to deliver Gigabit speeds, massive capacity, and stable-as-wire reliability our customers depend on.”

“The new 6 GHz band and Wi-Fi 6E standard ushers in a new age in wireless connectivity – a dramatic advance in performance and a new paradigm in wireless networking. Industry-leading Wi-Fi 6E technology – including Qualcomm’s new Wi-Fi 6E platforms – will transform every use case segment, from home to the enterprise, industrial applications, and even fixed wireless access, with new unbelievable applications sure to follow. The Wi-Fi 6E future looks very bright indeed,” said Claus Hetting, CEO & Chairman, Wi-Fi Now.

“Wi-Fi Alliance® members have mobilized around 6 GHz in an unprecedented way, and we’re excited to see Wi-Fi 6E solutions rapidly coming to market with the availability of new unlicensed spectrum in the U.S.,” said Kevin Robinson, Senior VP of Marketing, Wi-Fi Alliance. “Solutions like these from Qualcomm will help users fully experience Wi-Fi® in 6 GHz and quickly benefit from faster speeds, higher capacity, and lower latency applications.”

Qualcomm Tri-Band Wi-Fi 6 expands the capabilities of the Qualcomm Networking Pro Series portfolio, whose hallmark is the delivery of consistent high performance in the most densely congested environments:

- Qualcomm® Max User Architecture: Industry-first architecture to manage and maintain connectivity for up to 2,000 clients simultaneously, with network stability and sustained throughput.

- Qualcomm® Multi-User Traffic Management: Provides advanced scheduling algorithms and buffering with universal uplink data support. Advanced multi-user implementations specialized for high user counts include up to 37-user OFDMA support per channel and 8-user MU-MIMO support per channel.

- Qualcomm® 4K QAM technology: Designed to deliver 20% higher throughput compared to standard Wi-Fi 6E, helping achieve device-to-device transfers of up to 2.4 Gbps per link to compatible mobile and compute devices.

- Qualcomm® Tri-Band Wi-Fi 6 for Mesh Networks: Qualcomm® Wi-Fi SON has been enhanced to interconnect the Mesh Nodes using the 6 GHz band.

- Qualcomm® Wi-Fi Security Suite: Comprehensive WPA3 implementation coupled with state-of-the-art embedded crypto accelerators designed to provide secure transactions across a full range of Wi-Fi data touchpoints.

“Aruba’s enterprise customers demand high-performance, reliable and secure Wi-Fi connectivity solutions that can be scaled to deliver extreme density and capacity. Through our collaboration with Qualcomm Technologies, we’ve utilized their advanced Wi-Fi technology to continuously evolve the seamless, connected experiences that our customers demand,” said Onno Harms, senior director of Product Management for WLAN Platforms at Aruba, a Hewlett Packard Enterprise company. “The newly opened 6 GHz spectrum and the advent of Wi-Fi 6E are important industry milestones that promise to usher in a new wave of Wi-Fi innovation that will bring exceptional wireless experiences to life.”

“We see this announcement from Qualcomm Technologies as a positive step forward in what’s possible for networking across the industry,” said David Henry, senior vice president of Connected Home Products and Services for NETGEAR. “We look forward to continuing our collaboration with Qualcomm Technologies as we incorporate the Networking Pro Series to deliver robust and seamless experiences that enable us to expand the ecosystem.”

“Our recent announcement highlighting CommScope’s RUCKUS Wi-Fi 6 Certified access points is a great example of pushing the boundaries of what’s possible for wireless communications. Integrating the Qualcomm Technologies Networking Pro Series platform into the RUCKUS portfolio enables customers to benefit from the latest improvements in security, speed and Wi-Fi connectivity, creating a more powerful and robust product that will strengthen the rich suite of solutions available in the industry,” said Pramod Badjate, senior vice president for CommScope’s RUCKUS portfolio.

Qualcomm Networking Pro Series platforms are shipping now with commercial availability expected this year.

For more information about our Wi-Fi 6E products, visit qualcomm.com/wi-fi-6e

*All peak speeds refer to maximum physical layer (PHY) rate.

About Qualcomm

Qualcomm is the world’s leading wireless technology innovator and the driving force behind the development, launch, and expansion of 5G. When we connected the phone to the internet, the mobile revolution was born. Today, our foundational technologies enable the mobile ecosystem and are found in every 3G, 4G and 5G smartphone. We bring the benefits of mobile to new industries, including automotive, the internet of things, and computing, and are leading the way to a world where everything and everyone can communicate and interact seamlessly.

Qualcomm Incorporated includes our licensing business, QTL, and the vast majority of our patent portfolio. Qualcomm Technologies, Inc., a subsidiary of Qualcomm Incorporated, operates, along with its subsidiaries, substantially all of our engineering, research and development functions, and substantially all of our products and services businesses, including our QCT semiconductor business.

https://www.qualcomm.com/wi-fi-6e