FTTP

T-Mobile expands FTTH footprint via 50-50 JVs with Oak Hill Capital and Wren House

T-Mobile US is expanding its fiber-to-the-home (FTTH) footprint by investing ~$2.7 billion in two new 50-50 joint ventures (JVs) with Oak Hill Capital ($2 billion for GoNetspeed and Greenlight Networks) and Wren House ($700 million for i3 Broadband). These partnerships aim to pass around 1.8 million homes, largely in the northeastern U.S., accelerating T-Mobile’s fixed broadband expansion alongside their 5G network. Those deals are expected to close in the first half of 2027. T-Mobile, which markets fiber services under the brand name “T-Fiber,” said the deals are part of a plan to serve 18 million to 19 million total broadband customers – including 3 million to 4 million fiber customers – by the end of 2030.

- GoNetspeed offers voice and broadband services to residential and business customers (including multiple-dwelling units, or MDUs) in parts of Alabama, Connecticut, Maine, Massachusetts, Missouri, New York, Pennsylvania and Vermont, with plans to light up networks in cities in New Jersey and Rhode Island. GoNetspeed sells a handful of fiber-fed broadband tiers up to 6 Gbit/s and offers DSL in some areas.

- Greenlight Networks, founded in 2011, supports speeds up to 10 Gbit/s for residential and business customers in New York (Rochester, Buffalo, Binghamton, Capital Region and Hudson Valley), Pennsylvania (Scranton, Wilkes-Barre and Lehigh Valley), and Baltimore, Maryland. It serves about 225,000 homes and nearly 10,000 small businesses.

- i3 Broadband serves parts of Illinois and Missouri with broadband and voice services.

T-Mobile said GoNetspeed and Greenlight are expected to pass a combined 1.3 million households by the end of 2026, with i3 Broadband expected to pass roughly 500,000 households by that time. As it is with T-Mobile’s prior fiber JVs, the service providers involved in this new pair of transactions will operate under wholesale models that enable T-Mobile to offer “simple” plans with no annual service contracts.

- Target: ~1.8 million new homes passed, primarily in the Northeast.

- Partners: Joint ventures with investment firms Oak Hill Capital and Wren House.

- Strategic Goal: Deepen fiber footprint to support a target of 18-19 million broadband customers by 2030, with 3-4 million on fiber.

- Starlink Business Backup: T-Mobile is introducing a Starlink-powered backup option to provide comprehensive, resilient connectivity for business customers, enhancing their “SuperBroadband” offerings.

- Broadband Strategy: This move follows earlier 2025 moves, including the joint venture with EQT to acquire Lumos and the takeover of Metronet, strengthening T-Mobile’s position as a major fiber competitor.

Image Credit: Panther Media GmbH/Alamy Stock Photo

……………………………………………………………………………………………………………………………………………………………

New Street Research analysts David Barden and Vikash Harlalka (via Light Reading) said GoNetspeed passed about 770,000 locations in June 2025, with 725,000 of them passed with fiber, and the rest passed by copper and hybrid fiber/coax (HFC). They also estimate that Greenlight passed about 330,000 locations and i3 Broadband passed roughly 370,000 with fiber as of June 2025. Combined, the three operators involved in the proposed T-Mobile JVs pass nearly 1.5 million total locations, including 1.4 million fiber locations, according to NSR.

Based on an assumption that each fiber network operator has achieved penetration levels of about 25%, New Street said this implies that the Oak Hill JV has about 275,000 customers while the Wren House JV has about 75,000. At that level, they said that means T-Mobile is paying about $725 million for customers from the Oak Hill JV and $250 million for customers from the Wren House JV. The New Street analysts said today’s announcement shows that T-Mobile continues to have interest in acquiring “pure-play fiber operators.” As such, they also believe that the odds of a reported T-Mobile-Uniti deal have dropped.

The analysts also believe that the new fiber-focused JVs will also lower the odds of a potential combination with a major US cable operators such as Charter Communications. “A larger fiber footprint also makes it more difficult to get a deal approved by regulators,” they explained.

……………………………………………………………………………………………………………………………………………………………..

Even with the two new JV’s, T-Mobile’s fiber footprint will still be dwarfed by those of AT&T and Verizon,

- AT&T is targeting a 60 million fiber-to-the-premises (FTTP) footprint by 2030, leveraging joint ventures to accelerate deployment.

- Verizon, following acquisitions of Frontier and Eaton Fiber, projects 32 million fiber passings by 2026, with plans to reach 40–50 million via further partnerships and inorganic growth. Verizon, which also struck a deal to acquire Eaton Fiber last fall, is on track to end 2026 with more than 32 million fiber passings. CEO Dan Schulman reiterated that Verizon plans to broaden its fiber footprint to 40 million-50 million “over the medium term,” but did not provide a more specific timeframe. “There’s no question that fiber is a key differentiator … against competitors that don’t have it,” Schulman said, noting that the attachment rate of Verizon mobile customers who also get broadband from Verizon is hovering at about 55%.

……………………………………………………………………………………………………………………………………………………………..

References:

https://www.lightreading.com/broadband/t-mobile-s-new-jvs-fixate-on-fiber

https://www.lightreading.com/broadband/verizon-surpasses-6m-fwa-subs-as-priority-shifts-to-fiber

T-Mobile US announces new broadband wireless and fiber targets, 5G-A with agentic AI and live voice call translation

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

Evercore: T-Mobile’s fiber business to boost revenue and achieve 40% penetration rate after 2 years

T-Mobile & EQT Joint Venture (JV) to acquire Lumos and build out T-Mobile Fiber footprint

Highlights of 2025 Broadband Nation Expo: Comcast, T-Mobile keynotes + selected quotes

T-Mobile posts impressive wireless growth stats in 2Q-2024; fiber optic network acquisition binge to complement its FWA business

Australia’s NBN and Nokia demonstrate multi-generation optical technologies concurrently over existing FTTP infrastructure

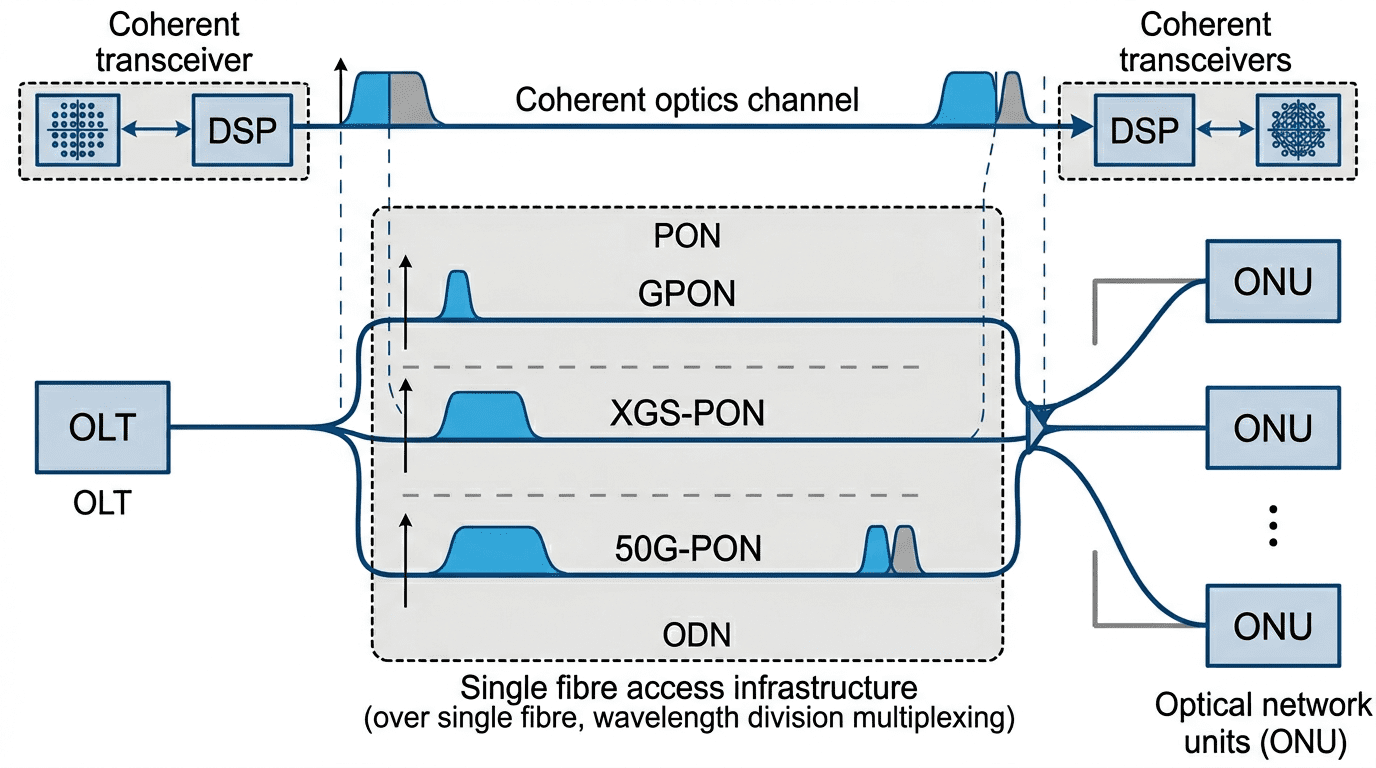

NBN Co, in collaboration with Nokia, has successfully conducted a laboratory demonstration of multiple generations of optical access and coherent transmission technologies operating concurrently over its existing Fiber‑to‑the‑Premises (FTTP) network. The technical trial validates the long‑term scalability of NBN Co’s national full‑fibre infrastructure and its capacity to accommodate the sustained growth of residential, enterprise, and industrial data demand anticipated over the coming decades.

The “Supercharging Fibre” trial, presented at the Broadband Forum Spring Member Meeting—held in Australia for the first time and hosted by NBN Co—demonstrated aggregate transmission rates exceeding 230 Gbit/s using multiple optical technologies over a single physical fiber link in a controlled laboratory environment. The experimental setup also established a pathway toward achieving terabit‑class capacities in future trials through the evolution of optical modulation formats and channel aggregation techniques.

A key outcome of the trial was the successful integration of coherent optical transmission with multiple generations of passive optical network (PON) technologies—GPON, XGS‑PON, and 50G‑PON—operating simultaneously over the same fiber infrastructure currently in service across Australia. Coherent optics, traditionally deployed within metropolitan, core, and data center interconnect networks, employ advanced modulation and digital signal processing to deliver extended reach, low latency, and high spectral efficiency. Their introduction into the access network domain represents a significant step toward the convergence of access and transport technologies, offering an efficient route to enhanced capacity and service flexibility without extensive physical network replacement.

The demonstration (see illustration below) underscores the technical viability of leveraging existing passive optical infrastructure to support future bandwidth requirements driven by the proliferation of cloud computing, immersive digital experiences, artificial intelligence applications, and industrial IoT systems. The results further illustrate the potential of FTTP systems to evolve into a highly scalable, future‑ready broadband platform capable of sustaining national connectivity objectives.

Image Credit: Perplexity.ai

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

By 31 December 2025, more than 1 million customers had transitioned from copper‑based services to high‑speed full‑fiber connections, positioning FTTP as NBN Co’s dominant fixed‑line technology at approximately 35% of total connections. The company achieved its commitment to enable 10 million premises, representing about 90% of the NBN fixed‑line footprint, to order multi‑gigabit‑capable wholesale broadband services. Ongoing upgrade activities encompass over 228,000 premises, as part of an initiative to extend full‑fiber access to 95% of the remaining ~622,000 copper‑served locations by 2030.

These developments reflect NBN Co’s strategic focus on access network modernization and underscore the continuing evolution of optical access technologies toward achieving the performance, flexibility, and resilience required to support Australia’s transition to a digital and cloud‑centric economy.

NBN Co. was established in 2009 by the Commonwealth of Australia as a Government Business Enterprise (GBE) with a clear direction – to design, build and operate a wholesale broadband access network for Australia.

And we’ve done just that – creating a network that criss-crosses a country, and allowing internet retailers to provide reasonably priced broadband services to consumers and businesses.

The network is the digital backbone of Australia and is constantly evolving to keep communities and businesses connected and our nation productive.

References:

https://www.nbnco.com.au/corporate-information/about-nbn-co

https://www.broadband-forum.org/events/spring-2026-member-meeting/

Dell’Oro: Optical Transport Systems market +15% year-over-year in 3Q2025 driven by Cloud Service Providers

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

Point Topic: FTTP broadband subs to reach 1.12bn by 2030 in 29 largest markets

Nokia and Hong Kong Broadband Network Ltd deploy 25G PON

Nokia’s launches symmetrical 25G PON modem

Google Fiber planning 20 Gig symmetrical service via Nokia’s 25G-PON system

NTT to launch 25 Gps FTTH service in Tokyo starting March 2026

NTT East plans to launch a 25 Gbps Fiber-to-the-Home (FTTH) service in Tokyo starting March 2026, according to Telecompaper, The service will offer significantly faster residential broadband, building on their existing fiber services and recent developments in higher-speed business options. Currently, the highest speed Fiber-to-the-Home (FTTH) access plan commercially available in Japan is 10 Gbps offered by multiple fiber optic network providers, including NTT East/West and Sony-backed NURO Hikari.

NTT’s forthcoming Flet Hikari 25G service will be a best-effort FTTH access product, utilizing shared subscriber fiber to connect customers to their chosen Internet Service Providers (ISPs).

The launch is part of NTT’s broader initiative to develop next-generation digital infrastructure, which also includes the development of key devices for an ultrafast optical network under its “Innovative Optical and Wireless Network” (IOWN) project in 2026.

Source: NTT Access Service Systems Laboratories

Separately, researchers in Japan have set world records for internet transmission speeds using experimental fiber optic technology, reaching speeds of over 1 petabit per second (which is over a million gigabits per second) in laboratory settings. These are research achievements and not a commercially available service for everyday use.

References:

https://www.ntt-review.jp/archive/ntttechnical.php?contents=ntr201604fa6.html

https://www.telecompaper.com/news/ntt-east-and-west-launch-10-gbps-service–1538339

NTT’s IOWN provides ultra low latency and energy efficiency in Japan and Hong Kong

NTT Data and Google Cloud partner to offer industry-specific cloud and AI solutions

Sony and NTT (with IOWN) collaborate on remote broadcast production platform

NTT & Yomiuri: ‘Social Order Could Collapse’ in AI Era

T‑Mobile and EQT close JV to acquire FTTH network provider Lumos

T-Mobile and EQT (a purpose-driven global investment organization) announced the successful close of their joint venture (JV) to acquire fiber-to-the-home provider Lumos. As part of the transaction, many Lumos customers will soon become T-Mobile Fiber customers and begin enjoying new offers and benefits as they’re welcomed into the Magenta family.

This deal marks a major milestone in T-Mobile’s broadband growth and builds on the Un-carrier’s success in delivering best-in-class connectivity. By bringing more value and choice to the millions of Americans who have previously been underserved, T-Mobile continues to deliver on its mission to change broadband for good. T-Mobile will take full ownership of the customer experience, using its proven brand, nationwide retail footprint, differentiated marketing and customer-first service model to attract new subscribers.

Currently, Lumos operates a 7,500-mile fiber network, providing high-speed connectivity to 475,000 homes across the Mid-Atlantic. The joint venture combines the Un-carrier’s unique assets with EQT’s fiber infrastructure expertise, and Lumos’ scalable build capabilities to drive rapid network expansion, with the goal of reaching 3.5 million homes by the end of 2028. To fuel this growth, T-Mobile invested $950 million into the joint venture, with an additional $500 million planned between 2027 and 2028 to support further expansion. T-Mobile will provide an update to its full year 2025 guidance resulting from this transaction during its Q1 earnings call.

“T-Mobile is already the fastest-growing broadband provider in America, and expanding into fiber helps us take the next big step in delivering what customers truly want – faster, more reliable internet that simply works,” said Mike Katz, T-Mobile President of Marketing, Strategy and Products. “People deserve better when it comes to their home internet: fewer disruptions, more value, and support that actually feels supportive. We’re excited to welcome Lumos customers to the T-Mobile family and bring them the Un-carrier experience – built around their needs, fueled by innovation, and focused on making life easier.”

As Lumos customers continue to enjoy the same high-speed fiber internet they rely on today at low monthly prices, they’ll now also enjoy the value-add benefits they get from simply being a part of the T-Mobile family. They will have access to T-Mobile’s best-in-class customer experience and nationwide retail presence. Every plan also comes with unlimited data plus Wi-Fi equipment and installation included, so customers can enjoy the freedom and flexibility of reliable internet. Additionally, new and existing customers will enjoy VIP treatment through Magenta Status, which includes exclusive benefits like discounts on food, gas, entertainment and top brands, plus freebies every Tuesday in the T-Life app. All with T-Mobile’s standard ‘no exploding bills’ pricing structure.

“We’re excited to begin this joint venture and even more energized about what’s ahead,” said Brian Stading, CEO of Lumos. “Partnering with EQT and T-Mobile, we’re ready to scale faster, deliver cutting-edge fiber technology to more people, and change even more lives. This is about more than just internet – it’s about building the infrastructure of the future and creating lasting opportunity, connection, and impact for communities.”

“We are thrilled to officially embark on this next chapter of growth with Lumos alongside our partners at T-Mobile,” said Nirav Shah, Partner within EQT’s Infrastructure Advisory team. “This joint venture represents a powerful combination of EQT’s digital infrastructure expertise, Lumos’ proven fiber deployment capabilities, and T-Mobile’s customer-first approach and national reach. Together, we are well-positioned to accelerate access to high-quality fiber broadband to millions of underserved Americans and look forward to executing on our plans to deliver the critical connectivity that empowers communities across the country.”

As the fifth-largest and fastest-growing Internet service provider in the U.S., T-Mobile offers 5G Home Internet to 70 million homes, serving more than 6.4 million customers nationwide as of the end of 2024, and has introduced T-Mobile Fiber in parts of 32 U.S. markets. Fiber-to-the-home complements T-Mobile’s successful 5G Home Internet offering, which currently has over 1 million customers on its waitlist. This expansion in fiber opens an additional avenue to meet the growing demand for T-Mobile broadband. Through its strategic fiber partnerships and joint ventures, the Un-carrier expects to reach 12 to 15 million households, or more, with fiber by the end of 2030.

References:

https://www.t-mobile.com/news/business/t-mobile-eqt-close-lumos-fiber-jv

T-Mobile & EQT Joint Venture (JV) to acquire Lumos and build out T-Mobile Fiber footprint

T-Mobile posts impressive wireless growth stats in 2Q-2024; fiber optic network acquisition binge to complement its FWA business

AT&T’s leads the pack of U.S. fiber optic network service providers

Fiber and Fixed Wireless Access are the fastest growing fixed broadband technologies in the OECD

Verizon to buy Frontier Communications

Wall Street Journal reported today that Verizon is on the verge of buying Frontier Communications for as much as $7 billion in a deal that would bolster the company’s fiber network to compete with rivals notably AT&T. With a market value of over $7 billion, Dallas, TX based Frontier provides broadband (mostly fiber optic) connections to about three million locations across 25 states. Frontier is in the midst of upgrading its legacy copper landline network to cutting-edge fiber. Rising interest rates sparked fears among investors, however, that the business would run out of cash and not be able to raise more before completing those upgrades. Frontier has a 25-state footprint and serves largely rural areas. It reported sales of $5.8 billion in 2023, with about 52% of total revenue from activities related to its fiber-optic products and bills itself as “largest pure-play fiber internet company in the US.”

An all-cash deal between the two companies could be announced as soon as Thursday, a person familiar with the negotiations told Bloomberg.

Fiber M&A has heated up as telecom companies and financial firms pour capital into neighborhoods that lack high-speed broadband or offer only one internet provider, usually from a cable-TV company. New fiber-optic construction is expensive and time-consuming, making existing broadband providers attractive takeover targets.

Verizon, with a market valuation of around $175 billion, will be under pressure from shareholders to justify any big purchase after the company paid more than $45 billion to secure C-band 5G wireless spectrum licenses and spent billions more to use them. Executives have said they are focused on trimming the telecom giant’s leverage to put it on a firmer financial footing.

Verizon, the top cellphone carrier by subscribers, has faced increased pressure from competitors and from cable-TV companies that offer discounted wireless service backed by Verizon’s own cellular network. Faced with slowing wireless revenue growth and an expensive dividend, Verizon has invested in expanding its home-internet footprint. It has both 5G fixed wireless access (FWA) and its Fios-branded fiber to the premises network.

T-Mobile is the only major U.S. cellphone carrier that lacks a large landline business. Since its 2020 takeover of rival carrier Sprint, the company has focused on 5G dominance and succeeded in growing its cellphone business faster than rivals. That network has also linked millions of customers to its fixed 5G broadband service, which offers cablelike service over the air. T-Mobile’s strategy has shifted in recent months, however, as the company dabbles in partnerships and wholesale leasing agreements with companies that build fiber lines to homes and businesses. The wireless “un-carrier” in July agreed to spend about $4.9 billion through a joint venture with private-equity giant KKR to buy Metronet, a Midwestern broadband provider.

Photo Credit: Jeenah Moon/Bloomberg News

…………………………………………………………………………………………………………………………………………………………

A deal for Frontier would be a round trip of sorts for some of the network infrastructure that Frontier bought from Verizon in 2016 for $10.54 billion in cash. Frontier later filed for Chapter 11 bankruptcy in April 2020 as it burned through cash and was burdened by a heavy debt load. It emerged as a leaner business in 2021 with about $11 billion less debt and focused on building a next-generation fiber optic network.

Frontier’s biggest investors today include private-equity firms Ares Management and Cerberus Capital Management. The company drew the attention of activist Jana Partners last year, which built a stake in the business. Jana delivered a letter to Frontier’s board late last year asking the company to take steps immediately to help reverse its sinking share price, including a possible outright sale.

…………………………………………………………………………………………………………………………………………………………..

AT&T has focused on expanding its fiber network since spinning off its WarnerMedia assets in 2022 to Warner Brothers Discovery. AT&T has 27.8 million fiber homes/businesses passed, growing at ~2.4 million per year, plus more locations passed via its Gigapower joint venture. AT&T’s fiber internet business is expected to contribute to an increase in consumer broadband and wireline revenue. AT&T expects broadband revenue to increase by at least 7% in 2024, which is more than double the rate of growth for wireless service revenue. In contrast, Verizon only has about 18 million fiber locations, growing at about 500,000 per year.

Other recent deals in the fiber transport market sector include the $3.1 billion acquisition, including debt, of fiber provider Consolidated Communications in late 2023 by Searchlight Capital Partners and British Columbia Investment Management.

………………………………………………………………………………………………………………………………………………………….

It’s All About Convergence (fiber based home internet combined with mobile service):

Speaking at a Bank of America investors conference today, Verizon’s CEO for the Consumer Group Sowmyanarayan Sampath said when Verizon bundles Fios with wireless, it sees a 50% reduction in mobile churn and a 40% reduction in broadband churn. He said they don’t see the same benefits with FWA. Sampath was scheduled to speak at the Mobile Future Forward conference tomorrow, but he canceled at the last minute, which may be a sign that this deal for Frontier is imminent.

The analysts at New Street Research led by Jonathan Chaplin said Verizon’s rationale for the purchase is “convergence baby.” They wrote, wrote, “Verizon seemed complacent. No longer.” Indeed, Verizon CEO Hans Vestberg was challenged on the company’s second quarter 2024 earnings call by analysts who questioned whether Verizon had a big enough fiber footprint to compete in the future. The New Street analysts said Sampath’s comments today “marked a shift in rhetoric from: ‘convergence is important, but we can do it with FWA.”

The analysts at New Street wrote today, “We have been arguing for a couple of years that all the fiber assets would eventually be rolled up into the three big national carriers (AT&T, Verizon, T-Mobile). We always knew that if one carrier started the process, others would have to follow swiftly because there are three wireless carriers and only one fiber asset in every market with a fiber asset.”

Other potential fiber companies that the big three national carriers might be eyeing include Google Fiber, Windstream, Stealth Communications and TDS Telecom.

After its annual summer conference in August in Boulder, Colorado, the analysts at TD Cowen, led by Michael Elias, said there was a lot of conversation about the wireline-wireless “convergence” frenzy. “We believe convergence is a race to the bottom, but if one player is going in with a slight advantage (AT&T), the others must reluctantly follow,” wrote TD Cowen. In the mid-term they speculated that T-Mobile might look at fiber roll-ups with Ziply or Lumen (formerly or other regional players.

References:

https://www.wsj.com/business/deals/verizon-nearing-deal-for-frontier-communications-9e402bb4

https://www.fierce-network.com/broadband/verizon-rumored-buy-frontier-its-convergence-game

https://finance.yahoo.com/news/verizon-talks-buy-frontier-communications-180419091.html

https://videos.frontier.com/detail/videos/internet/video/6322692427112/why-fiber

Building out Frontier Communications fiber network via $1.05 B securitized debt offering

Fiber builds propels Frontier Communication’s record 4th Quarter; unveils Fiber Innovation Labs

Frontier Communications fiber build-out boom continues: record number of fiber subscribers added in the 1st quarter of 2023

Frontier’s Big Fiber Build-Out Continued in Q3-2022 with 351,000 fiber optic premises added

AT&T and BlackRock’s Gigapower fiber JV may alter the U.S. broadband landscape

AT&T Highlights: 5G mid-band spectrum, AT&T Fiber, Gigapower joint venture with BlackRock/disaggregation traffic milestone

AT&T to use Frontier’s fiber infrastructure for 4G/5G backhaul in 25 states

Frontier Communications offers first network-wide symmetrical 5 Gig fiber internet service

Frontier Communications adds record fiber broadband customers in Q4 2022

Verizon Q2-2024: strong wireless service revenue and broadband subscriber growth, but consumer FWA lags

Summary of Verizon Consumer, FWA & Business Segment 1Q-2024 results

Highlights of FiberConnect 2024: PON-related products dominate

The Fiber Broadband Association’s flagship conference, FiberConnect 2024, concluded July 31, 2024, in Nashville, Tennessee. It featuring 275 speakers and 286 exhibitors in the Expo Hall, with about half the attendees from operators and half representing vendors. The show provided a great opportunity to gauge the pulse of the fiber based broadband industry in North America.

AT&T’s fiber business grows along with FWA “Internet Air” in Q4-2023

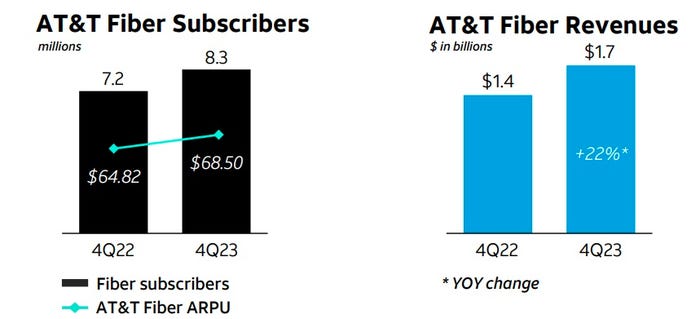

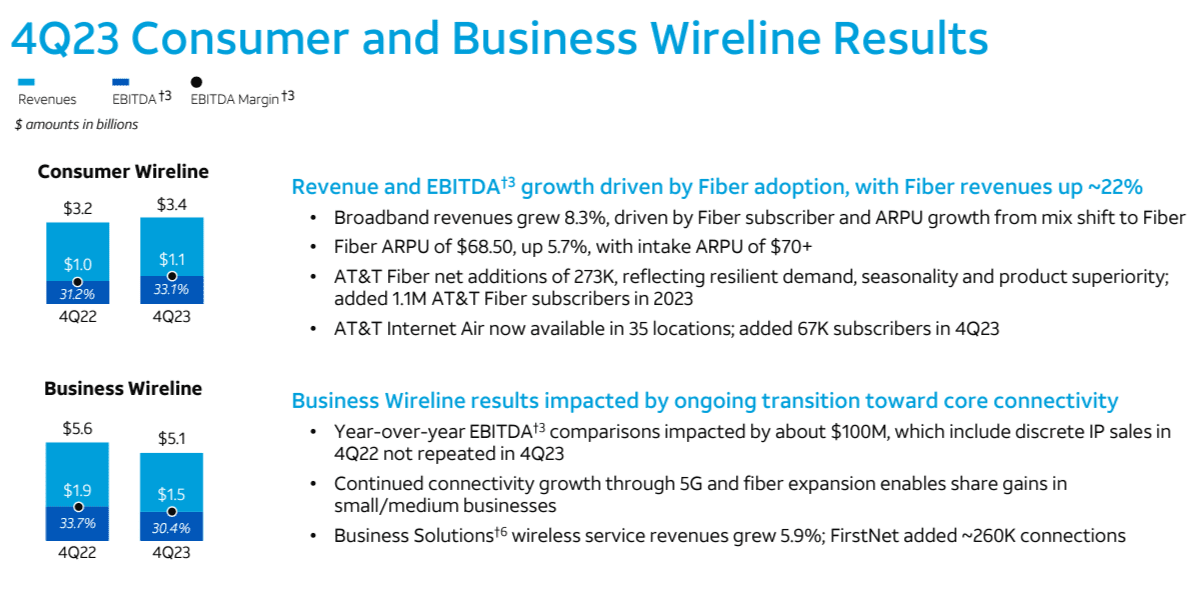

AT&T added 273,000 residential fiber subs in Q4, down slightly from year-ago adds of +280,000 and a gain of +296,000 in the prior quarter. AT&T ended 2023 with 8.3 million fiber subs. The U.S. based carrier added about 400,000 fiber locations in Q4, extending that reach to 21.1 million. AT&T remains committed to expanding its fiber-to-the-premises (FTTP) footprint to 30 million locations by 2025, Stankey said.

Fiber-related revenues hit $1.67 billion, up from $1.37 billion in the year-ago quarter. Fiber average revenue per user (ARPU) reached $68.50, up from $64.82 a year earlier.

AT&T says it has the nation’s largest fiber network, which now passes 26 million+ consumer and business locations; on track to pass 30 million+ locations with fiber by the end of 2025.

…………………………………………………………………………………………………………………

AT&T’s new fixed wireless access (FWA) service dubbed “Internet Air” gained ground in the fourth quarter of 2023. Internet Air added 67,000 subscribers in Q4 of 2023, extending its total to 93,000. Those quarterly FWA subscriber additions were a “surprise,” New Street Research analyst Jonathan Chaplin said in a research note issued after AT&T posted earnings. Yet they are way below Verizon’s FWA numbers which came in at 375,000 FWA subs added in the Q4 of 2023.

However, AT&T’s FWA offering will remain a limited and targeted product in the operator’s home broadband arsenal. “I don’t expect that we are going to be pushing the [Internet Air] product the same way that some others in the market are pushing it today,” AT&T CEO John Stankey said on today’s earnings call. “We made a conscious choice as a company that we want to dedicate capital to invest in fiber, which we believe is a more sustainable long-term means to deal with stationary and fixed broadband needs.”

AT&T will continue to use Internet Air on a selective basis, relying on it as an alternative for customers transitioning off of the telco’s aging copper plant, in pockets of some markets where AT&T offers fiber service, as well as markets where AT&T has no existing wireline business.

……………………………………………………………………………………………………………………….

AT&T claims it has the largest and most reliable wireless network in North America. Its mid-band 5G spectrum now covers 210 million+ people, achieving its end-of-year targets. It expects wireless service revenue growth in the 3% range for 2024.

Stankey said 2024 will be the “proving year” for the Gigapower joint venture with BlackRock that will initially bring open access fiber networks to about 1.5 million locations outside of AT&T’s legacy wireline footprint. Initial Gigapower markets include Las Vegas, three cities in Arizona (Mesa, Chandler and Gilbert), parts of northeastern Pennsylvania (including Wilkes-Barre and Scranton) and segments of Alabama and Florida.

AT&T also said that it now has a FirstNet customer base consisting of more than 5.5 million connections.

“We accomplished exactly what we said we would in 2023, delivering sustainable growth and consistent business performance, resulting in full-year free cash flow of $16.8 billion, ahead of our raised guidance. As we advance our lead in converged connectivity, we will continue to scale our best-in-class 5G and fiber networks to meet customers’ growing demand for seamless, ubiquitous broadband, and drive durable growth for shareholders,” said CEO John Stankey.

References:

https://about.att.com/story/2024/q4-earnings-2023.html

https://edge.media-server.com/mmc/p/keicd3et/ (4Q 2023 earnings call)

https://investors.att.com/news-and-events/events-and-presentations

https://www.lightreading.com/fixed-wireless-access/at-t-nears-100k-internet-air-subs

AT&T and BlackRock’s Gigapower fiber JV may alter the U.S. broadband landscape

Telecom layoffs continue unabated as AT&T leads the pack – a growth engine with only 1% YoY growth?

NTT advert in WSJ: Why O-RAN Will Change Everything; AT&T selects Ericsson for its O-RAN

Deutsche Telekom Network Day: Fiber, Mobile Network, Open RAN and 5G SA Launch in 2024

2023 Deutsche Telekom (DT) Highlights:

- Fiber offensive: more than 2.5 million new fiber connections made possible in 2023, reaching a total of more than ten million fiber households in 2024

- 5G front-runner: 5G population coverage of 96%, 5G Standalone also for private customers in 2024

- State-of-the-art technologies: Artificial intelligence supports fiber and mobile rollout

- EURO 2024: Deutsche Telekom connects all stadiums, fan zones & team quarters, data gift for all mobile customers

………………………………………………………………………………………………………………………………………

Deutsche Telekom announced that it has successfully enabled more than 2.5 million new fiber connections this year, thereby realizing its fiber plant expansion target. The company invested EUR 2.5 billion in fiber expansion, expanding coverage in almost 3,500 towns and municipalities. According to the announcement, the company projects a total investment of EUR 30 billion in the fiber optic rollout by 2030.

Its Fiber-to-the-home (FTTH) network is set to reach eight million households by the end of the year, with plans to extend this to ten million fiber optic connections by 2024.

………………………………………………………………………………………………………………………………………..

In mobile, Deutsche Telekom currently provides 5G coverage to 96 percent of the population, serving 80 million people through a network of over 80,000 5G antennas, including 10,000 in the 3.5 GHz band spread across more than 800 cities and municipalities. The network delivers download speeds of up to 1 Gbps.

The company aims to achieve 99 percent 5G coverage for the German population by 2025 and plans to launch 5G Standalone (SA) core network for private customers in 2024. DT indicates that 10,000 antennas are compatible with 5G SA in the 3.6 GHz band, covering more than 800 cities and municipalities. This is up from 9,700 antennas in August 2023.

Deutsche Telekom’s business customers are already using 5G SA technology with functions such as network slicing. For example, for live TV transmission of media or in 5G campus networks for industry and research. “In the coming year, 5G SA should then offer all customers real added value,” DT said.

Meanwhile, rival operators Telefónica Deutschland (O2 Germany) and Vodafone Germany already offer standalone 5G services.

…………………………………………………………………………………………………………………………

DT began the deployment of its open radio access network (O-RAN) in Germany in December, in collaboration with Nokia and Fujitsu. The first O-RAN commercial deployment will be in Neubrandenburg. Nokia and Fujitsu are supplying the necessary technology components.

“Open RAN increases the choice of manufacturers and therefore our flexibility. The open access network enables more automation. And makes our networks even more resilient. This benefits the people that our mobile network connects,” says Claudia Nemat.

The German telco expects to have 3,000 O-RAN compatible antennas by the end of 2026.

…………………………………………………………………………………………………………………………

Deutsche Telekom also says it’s using Artificial Intelligence (AI) in network expansion and mobile communications. AI aids in analyzing and evaluating cell usage and capacity utilization, with the ongoing development of a large language model for telco-specific applications in collaboration with SK Telekom. Additionally, AI contributes to enhanced network security through automated pattern recognition, according to the company.

References:

https://www.telekom.com/en/media/media-information/archive/telekom-network-day-2023-1055364

https://www.fiercewireless.com/wireless/deutsche-telekom-plans-5g-standalone-launch-2024

Building out Frontier Communications fiber network via $1.05 B securitized debt offering

Frontier Communications has nearly three million broadband internet subscribers across 25 states, on a network that reaches about 5.5 million homes and businesses via fiber and another 10 million via copper. About a third of Frontier’s potential fiber customers subscribe, three times the rate of those on copper lines. Frontier built fiber to an additional 339,000 locations in Q1 2023, ending the quarter with 5.5 million fiber passings and 15.4 million total passings. The company also added a record 87,000 fiber subs in the period, extending that customer total to 1.76 million (1.65 million residential and 110,000 business customers).

However, building out its fiber network will cost more than Frontier’s management forecast when the company emerged from bankruptcy in early 2021. Its latest two million locations cost an average of $830 to deploy. In May, management said it expects the remainder of this year’s build to cost between $1,000 and $1,100 per location. It costs Frontier another $600 or so to send a technician to a customer’s home to plug in all the necessary equipment and the like.

Light Reading reports that Vikash Harlalka, telecom analyst at New Street Research, estimates that Frontier’s fiber buildout plan faces a funding gap of about $2.3 billion. However, Frontier Communications’ plan to offer $1.05 billion in securitized debt, with the potential to upsize it, will significantly cut down the company’s funding gap to build fiber to 10 million locations by 2025. The company said:

An indirect subsidiary of the Company intends to offer approximately $1.05 billion aggregate principal amount of secured fiber network revenue term notes (the “Notes”), with the potential to upsize, subject to market conditions and other factors. The Notes will be secured by certain of Frontier’s fiber assets and associated customer contracts in the Dallas metropolitan area and constitute the first offering of green bonds by a Frontier subsidiary.

“The offering should close nearly half the gap (more than half, if the offering is upsized. It takes most of the funding risk off the table,” Harlalka explained in a research note, adding that the move also unlocks a new market for Frontier to tap into for its funding needs. Harlalka noted that Frontier had about $2.7 billion in liquidity at the end of the first quarter of 2023 – enough to meet the company’s capital needs until mid-2024. “This new debt raise should extend that beyond 2024,” he added.

Frontier said the debt offer will be secured by a portion of the company’s fiber assets and associated customer contracts in the Dallas metropolitan area, and marks the first offering of “green bonds” by a Frontier subsidiary. The offer will go toward capital expenditures and research and development, “in line with Frontier’s fiber expansion and copper migration strategies,” the company said.

Last week, Frontier stock dropped 21.3% after The Wall Street Journal reported on potential health risks posed by lead-sheathed copper wires in old networks across the U.S. Frontier declined to comment. The stock decline continued on Monday July 17th with FYBR hitting a low of $11.65 on huge volume of 12,063,100 shares. It rebounded 43.95% in the next four trading days to close at $16.77 on Friday July 21st (albeit on very light volume).

New Street analyst Jonathan Chaplin estimates that remediation costs to Frontier could reach $6 billion if it is required to rip out all the lead-covered copper on its own dime within five years. But there’s overlap with upgrading those same lines to fiber, and Chaplin calculates a $75 fair value for the stock in this unlikely scenario. “Even if it comes to pass, we see upside to the stock,” he writes.

Frontier is scheduled to announce Q2 2023 results on Friday, August 4th.

References:

https://www.barrons.com/articles/buy-frontier-communications-stock-price-pick-a2f82599

Frontier Communications fiber build-out boom continues: record number of fiber subscribers added in the 1st quarter of 2023

Fiber builds propels Frontier Communication’s record 4th Quarter; unveils Fiber Innovation Labs

AT&T to use Frontier’s fiber infrastructure for 4G/5G backhaul in 25 states

Frontier Communications offers first network-wide symmetrical 5 Gig fiber internet service

Frontier Communications adds record fiber broadband customers in Q4 2022

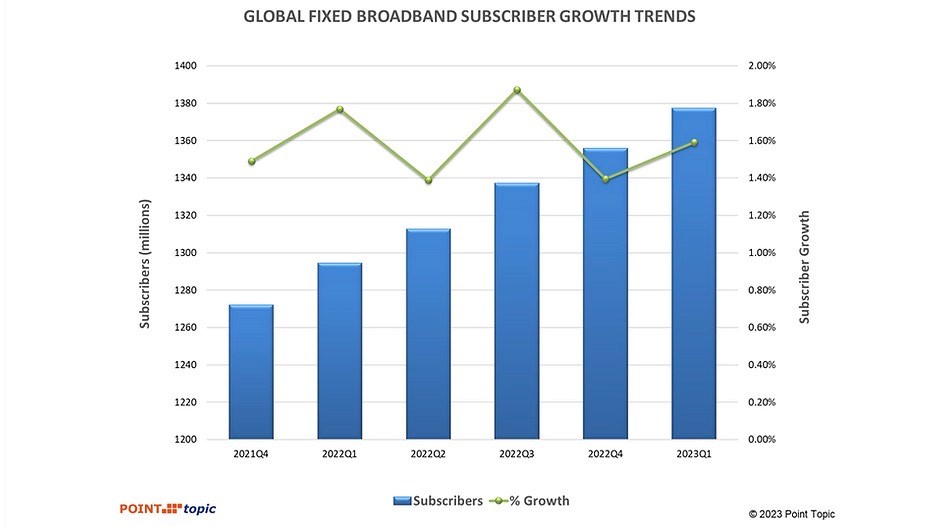

Point Topic Comprehensive Report: Global Fixed Broadband Connections at 1.377B as of Q1-2023

Global fixed broadband connections reached 1.377 billion as of Q1-2023, up by 83 million from a year earlier and reflecting an annual growth rate of 1.59%, according to Point Topic.

There was a decline in fixed broadband subscriptions in 18 countries[1] which mainly include emerging markets, as well as some saturated markets such as Singapore. However, while there were fluctuations in growth rates across regions and markets, the overall trend indicates a steady expansion of global broadband connectivity.

Highlights:

-

Among global regions, Africa, East Asia and America Other saw the fastest growth in broadband connections (2.9%, 2.2% and 1.8%), not least due to healthy increases in broadband subscribers in the vast markets of Egypt, Brazil and China.

-

The share of FTTH/B in the total fixed broadband subscriptions continued to increase and stood at 66.7%. Broadband connections based on other technologies saw their market shares shrink further, with an exception of satellite and wireless (mainly FWA).

-

VDSL subscriber numbers grew in ten countries, while they dropped in at least 22 markets as consumers migrated to FTTH/B.

-

The highest FTTH/B broadband subscriber growth rates in Q1 2023 were in Algeria, Peru and UK.

At 21.6 million, the quarterly net adds were close to the figure we recorded a year ago, though the growth rate (1.59%) was slower, compared to 1.77% in Q1 2022, with global inflation and economic instability having an impact.

East Asia continued to dominate in Q1 2023, maintaining its position as the largest market with a 49.6% share of global fixed broadband subscribers. This substantial market share is primarily driven by China with its vast population.

In Q1 2023, broadband subscriber base grew faster in China, Hong Kong and Korea, compared to Q4 2022. As a result, the region’s net adds share globally went up from 63.2% to 68.8%. Asia Other accounted for 10.8% of the global broadband market, similarly to the previous quarter, though the region’s net adds share went down from 12.8% to 9.4%.

Europe’s market shares remained rather consistent, though Eastern Europe saw their net adds share decline from 3.4% to 0.5%, as a result of slower growth in almost all markets and the decline in broadband subscribers in Russia having an especially significant impact due to its market size.

Similarly, Americas maintained relatively stable market shares of 10.3% and 8.1% respectively, while America – Other’s net adds share increased from 7.8% to 9%, driven by higher growth in such sizeable markets as Brazil, Mexico, Colombia and Chile, to name a few.

Next Point Topic looks at fixed broadband penetration among population, comparing it to growth rates across the regions.

Africa and Asia Other continue to have relatively low fixed broadband penetration rates among their populations. In Q1 2023, this metric in Africa stood at 4.6%, while Asia Other reached 5.6%. These figures indicate the potential for future expansion in these regions. Not surprisingly, Africa also recorded the highest quarterly growth rate of 2.9%.

The markets of East Asia and America Other followed closely with growth rates of 2.2% and 1.8% respectively, despite East Asia already having the highest population penetration at 41.9%. This reflects a widespread adoption of fixed broadband services in East Asia, while America Other showcases steady growth in a region with significant potential, where broadband penetration is among the lowest, at 17.2%.

Eastern Europe displayed a modest growth rate of 0.2% with a population penetration of 24.8%. Some markets in this region still have a lot of headspace when it comes to broadband adoption but the growth was sluggish, likely due to economic pressures. Other European regions showed a slightly higher growth rate, with Europe Other at 0.5%, coupled with the second highest population penetration of 39.4%. These figures indicate a mature market with limited growth opportunities.

Among the largest twenty broadband markets all but one saw fixed broadband subscribers grow in Q1 2023, although in ten of them the growth was slower than in the Q4 2022. There was a slight drop in broadband subscribers in Russia which is under international sanctions.

The less saturated broadband markets of India, Egypt, Brazil and Mexico recorded the highest quarterly growth rates in Q1 2023, all higher than 2%. China recorded an above 2% growth as well. At the other end of the spectrum, the mature markets of Germany, France, Japan, UK, and Italy saw modest growth rates at below 0.5%. At the same time, Italy was among the countries that saw one of the largest improvements in growth rates, from -0.44% in Q4 2022 to 0.04% in Q1 2023, as its GDP growth also went from negative to positive in that period[2]. Mexico, China and Brazil recorded the largest improvements in their growth rates, at +1.14.%, +0.52% and +0.41% respectively.

Between Q4 2022 and Q1 2023, the share of FTTH/B connections in the total fixed broadband subscriptions went up by 0.7% and stood at 66.7%. Broadband connections based on other technologies saw their market shares shrink further, with an exception of satellite and wireless (mainly FWA), which remained stable.

FTTx (mainly VDSL) share stood at 6.7%[3]. VDSL subscriber numbers grew in ten countries (including modest quarterly increase in the large VDSL markets of Turkey, Czech Republic, Greece and Germany, for example), while they fell in 22 other markets as consumers migrated to FTTH/B.

It remains to be seen whether consumers will continue to gravitate toward fibre broadband offerings, particularly as global economies face potential slowdown and inflationary pressures.

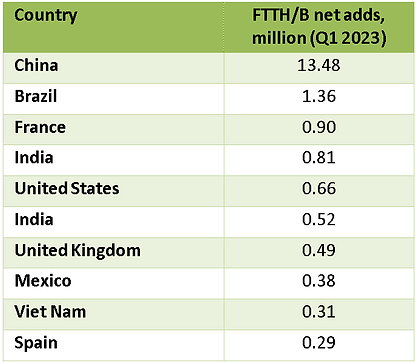

In terms of FTTH/B broadband net additions in Q1 2023, China continued to maintain a significant lead with 13.5 million while Brazil added 1.4 million. Mexico is back in the top ten league, having pushed out Argentina this quarter.

Satellite broadband also saw a modest growth of 1.3% while wireless broadband demonstrated continued relevance with a respectable growth rate of 4.9%. These trends can be attributed to the demand for connectivity in remote or underserved areas where traditional broadband infrastructure is not feasible.

The diverse growth rates among different broadband technologies highlight the dynamic nature of the industry as consumers seek more reliable and high-speed connections. The significant increase in FTTH/B connections and the growth of satellite and wireless broadband underline the ongoing efforts to bridge the digital divide and ensure connectivity for all.

The top ten countries by fixed broadband subscribers remained unchanged (Figure 5). As of Q1 2023, China exceeded 0.6 billion fixed broadband subscribers, having added 14.6 million in the quarter. Also, the country is approaching 1.2 billion 5G subscribers, with the service now being used by 84% of the population.

Overall, the latest fixed broadband subscriber data reveals a clear trend towards advanced, high-speed broadband solutions like FTTH/B, while older technologies such as copper-based broadband (ADSL and VDSL) are experiencing a decline, suggesting that the broadband landscape is continuously evolving to meet the growing demand for faster and more reliable connectivity.

References:

https://www.point-topic.com/post/global-broadband-subscriptions-q1-2023

Point Topic: Global Broadband Tariff Benchmark Report- 2Q-2022

Point Topic: Global fixed broadband connections up 1.7% in 1Q-2022, FTTH at 58% market share