Nvidia

Will “AI at the Edge” transform telecom or be yet another telco monetization failure?

New Telco Opportunity – AI at the Edge:

At MWC 2026 last week, there were a flurry of claims that “AI at the Edge” would transform the telecom industry. One of many examples is an article titled, “The AI edge boom is giving telecom a new strategic role.” In that piece, Jeff Aaron, vice president of product and solutions marketing at Hewlett Packard Enterprise (HPE) spoke with theCUBE’s John Furrier at MWC Barcelona, during an exclusive broadcast on theCUBE, SiliconANGLE Media’s livestreaming studio. They discussed telecom edge AI and why networking is becoming a strategic foundation for data-centric services. Aaron said:

“A big reason for [reignited interest in routing] is AI workloads. They’re moving everywhere now. They have to move to the edge. For them to move to the edge, you’ve got to get them outside of the factory and to all the locations. We’re right in the core of that, and it’s super exciting.”

As AI expands to the edge, data will need to move not only to local compute, but also between many distributed edge sites, making routing paramount. There are four ways AI infrastructure is scaling — inside data centers and across distributed edge locations, according to Aaron.

“There’s scale-out, scale-across, scale-up, and on-ramp. Two are within the data center — scale-out and scale-up — but scale-across and edge on-ramp basically mean you got to figure out how to connect to those areas, and those are just networking,” he added.

Scale-across refers to connecting distributed data centers and edge locations, while edge on-ramp brings remote sites such as factories or branch locations into the network to access AI services. Supporting those distributed environments creates an opportunity for HPE to bring networking and compute together into a more integrated infrastructure stack. At MWC 2026 Barcelona, those trends are clearly coming into focus, according to Aaron.

“Data is moving everywhere right now, and the network is back. The network isn’t just plumbing. The network is how you build a value-added service using an AI workload as a telco infrastructure,” he added.

Telecom carriers are now urgently trying to move from being “dumb data pipes” to becoming “AI performance platforms” by leveraging their geographically distributed infrastructure to host AI closer to the end user. They urgently want to pivot from selling just bandwidth and connectivity to selling outcomes and intelligence with a heavy focus on industrial and enterprise-specific edge deployments. They are considering the following services and business models:

- Infrastructure as a Service (IaaS) & GPUaaS: Offering raw computing power, specifically GPUs, from edge data centers to enterprises that need low-latency processing without building their own facilities.

- Sovereign AI Clouds: Providing AI services that guarantee data remains within national borders, appealing to government and highly regulated sectors like finance and healthcare.

- API Monetization: Exposing real-time network data (e.g., location intelligence, predictive network quality, fraud risk scoring) via APIs that enterprises pay to integrate into their own applications.

- Outcome-Based Pricing: Charging for specific business results, such as a “guaranteed video call quality” or “fraud loss reduction share,” rather than just data usage.

- AI-as-a-Service (AIaaS): Bundling pre-trained models or specialized AI agents (e.g., for customer service or industrial monitoring) with connectivity

Major Carrier AI Edge Deployment Plans:

- AT&T:

- Launched Connected AI for Manufacturing in March 2026, which unifies 5G, IoT, and generative AI to provide real-time fault detection (claiming a 70% reduction in waste).

- Deploying “Edge Zones” in major U.S. cities (Detroit, LA, Dallas) to allow developers to run low-latency, cloud-based software locally.

- Partnering with AWS to link fiber and 5G directly into AWS environments for distributed AI workloads.

- Verizon:

- Unveiled Verizon AI Connect, a suite of products designed to manage resource-intensive AI workloads for hyperscalers like Google Cloud and Meta.

- Trialing V2X (Vehicle-to-Everything) platforms to provide carmakers with standardized APIs for low-latency edge processing in autonomous driving.

- Collaborating with NVIDIA to integrate GPUs into private 5G networks for on-premise AI inferencing in robotics and AR.

- SK Telecom (SKT):

- Announced an “AI Native” strategy at MWC 2026, including a roadmap for AI-RAN (Radio Access Network) that uses GPUs to optimize network performance and host user AI apps simultaneously.

- Building a Manufacturing AI Cloud powered by over 2,000 NVIDIA RTX GPUs to support digital twin simulations and robotics.

- Expanding AI Data Centers (AIDC) across South Korea and Southeast Asia (Vietnam, Malaysia) using energy-optimized LNG-powered facilities.

- Orange & Deutsche Telekom:

- Deploying AI-powered planning tools to cut fiber rollout costs and optimize site power consumption by up to 33% using AI “Deep Sleep” modes.

- Focusing on Sovereign AI strategies to ensure data governance for European enterprise customers.

- Vodafone:

- Utilizing AI/ML applications for daily power reduction at 5G sites and testing autonomous network healing via AI agents

- BT:

- Offers 5G-connected VR for manufacturing design teams (e.g., Hyperbat) to collaborate on 3D models in real-time.

| Product Category | Primary Target | Key Value Proposition |

|---|---|---|

| AI-RAN | Industry 4.0 | Seamless, ultra-low latency for robotics and sensing. |

| Connected AI Platforms | Manufacturing | Real-time predictive maintenance and waste reduction. |

| AI-as-a-Service (AIaaS) | Developers/SMBs | Access to GPU power and pre-trained models via telco edge nodes. |

| Network Slicing APIs | App Developers | Programmatic control over bandwidth for AR/VR and gaming. |

…………………………………………………………………………………………………………………………………………………………………………………………..

A Dissenting View of “AI at the Edge”:

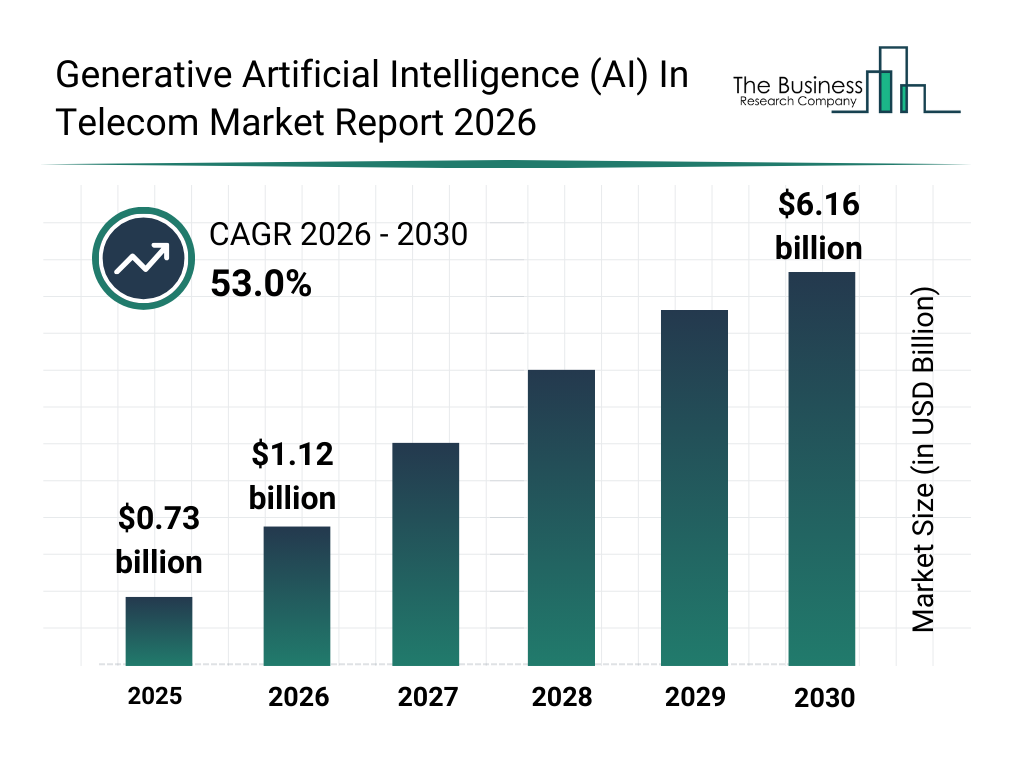

The global market for AI within the global telecommunications sector is valued at $6.69 billion in 2026, growing at a compound annual rate (CAGR) of 41.9% from 2025. The broader edge AI market—including hardware, software, and services—is forecast to reach $29.98 billion in 2026, according to The Business Research Company. We think those estimates are way too high.

The market research firm states:

………………………………………………………………………………………………………

Author’s Opinion:

Unless telcos change their corporate culture along with slowing the footprint growth of cloud service providers/hyperscalers, we think that AI at the Edge will be yet another telco monetization failure. Just like their failure to monetize: 4G LTE apps, the telco cloud, 5G, multi-access edge computing (MEC), OpenRAN, LPWANs and other telecom technologies that never lived up to their promise and potential.

That’s largely because telcos are very weak: developing IT platforms, compute services, killer applications, and rapid execution of new services (e.g. 5G services require a 5G SA core network which telcos were very slow to deploy). Telecom execs themselves cite cultural and speed‑of‑change issues: the industry is not organized like a software company, so it struggles to iterate products at AI/cloud pace. Also, telcos historically struggle with software. Managing distributed GPU clusters is vastly different from managing cell towers.

After spending billions on 5G with very little or no ROI, investors are skeptical of the increased capex required for AI-grade edge servers which must be maintained by telcos. Those servers will be expensive (especially if they contain clusters of Nvidia GPUs) and consume a lot of power, which is a critical issue at the edge of the carrier’s network.

Many network operators frame AI/edge as “network optimization” or “utilizing underused sites,” not as building monetizable AI platforms with APIs, SDKs, and ecosystems. This mirrors 5G, where huge RAN/core builds were not matched by a clear product and platform strategy, leaving value to OTTs and hyperscalers which are extending their control planes and protocol stacks to the network edge (local zones, operator co‑lo, on‑premises stacks).

Telcos risk becoming “dumb pipes” for AI traffic if they can’t provide a superior developer ecosystem. If they only sell space/power/connectivity, the cloud service providers will continue to own the developer and AI value chain. Analysts warn that edge is a “right to participate, not a right to win.” As such, value accrues to whoever owns the AI platform, tools, marketplace, and pricing power, not the entity that provides connectivity, PoP or cell towers.

Data fragmentation and weak “intelligence” layer:

-

AI monetization depends on high‑quality, cross‑domain data, but telco data is fragmented across OSS, BSS, probes, and partner systems; without unification, it is hard to expose compelling network/edge intelligence services.

-

Analysts emphasize that failure here reduces telcos to generic GPU landlords, while higher‑margin offers (real‑time quality, fraud, identity, mobility/context APIs) remain unrealized.

Narrow internal focus on cost savings:

-

Many operators’ early AI focus is inward (Opex reduction in assurance, planning, customer care) rather than building external, revenue‑generating products, echoing how early 5G was justified mainly on cost/efficiency.

-

Commentators warn that if AI/edge remains a “network efficiency” play, the commercial upside will go to cloud/AI natives that turn similar capabilities into products sold to enterprises.

What analysts say telcos must do differently:

-

Build “Sovereign AI factories” and edge AI clouds: GPU‑enabled sites with cloud‑like developer experience (APIs, self‑service portals, metering, SLAs) and clear sovereign/regional guarantees.

-

Combine differentiated connectivity with AI services (latency‑backed SLAs, AI‑on‑RAN, domain‑specific models for verticals) and use modern, flexible commercial models instead of just selling bandwidth or colocation.

Conclusions:

In summary, the main risk for telcos is to successfully transition from owning and maintaining network infrastructure to owning and operating AI platforms and products at software industry speed. AI at the edge is less of a new service or product and more an architectural upgrade. The two ways telcos can benefit are from:

- Internal cost reduction: If telcos use it to lower their own costs (fraud prevention, risk management, predictive maintenance, fault isolation, self-healing networks, etc.), it’s an automatic win but won’t increase the top line.

- Revenue from new AI -Edge services, e.g. Verizon uses edge-based video analytics in warehouses to improve inventory turnover by up to 40%. If they expect to charge a massive premium for “AI-enabled 5G,” they face the same monetization wall that has doomed them for the past 20 years!

References:

https://siliconangle.com/2026/03/04/telecom-edge-ai-makes-networking-strategic-mwc26/

https://www.nvidia.com/en-us/lp/ai/the-blueprint-for-ai-success-ebook/

AT&T and AWS to deliver last mile connectivity for AI workloads; AT&T Geo Modeler™ AI simulation tool

Analysis: Edge AI and Qualcomm’s AI Program for Innovators 2026 – APAC for startups to lead in AI innovation

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Private 5G networks move to include automation, autonomous systems, edge computing & AI operations

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

Nvidia AI-RAN survey results; AI inferencing as a reinvention of edge computing?

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

CES 2025: Intel announces edge compute processors with AI inferencing capabilities

Indosat Ooredoo Hutchison, Nokia and Nvidia AI-RAN research center in Indonesia amongst telco skepticism

Indosat Ooredoo Hutchison (Indosat) Nokia, and Nvidia have officially launched the AI-RAN Research Centre in Surabaya, a strategic collaboration designed to advance AI-native wireless networks and edge AI applications across Indonesia. This collaboration, aims to support Indonesia’s digital transformation goals and its “Golden Indonesia Vision 2045.” The facility will allow researchers and engineers to experiment with combining Nokia’s RAN technologies with Nvidia’s accelerated computing platforms and Indosat’s 5G network.

According to the partners, the research facility will serve as a collaborative environment for engineers, researchers, and future digital leaders to experiment, learn, and co-create AI-powered solutions. Its work will centre on integrating Nokia’s advanced RAN technologies with Nvidia’s accelerated computing platforms and Indosat’s commercial 5G network. The three companies view the project as a foundation for AI-driven growth, with applications spanning education, agriculture, and healthcare.

The AI-RAN infrastructure enables high-performance software-defined RAN and AI workloads on a single platform, leveraging Nvidia’s Aerial RAN Computer 1 (ARC-1). The facility will also act as a distributed computing extension of Indosat’s sovereign AI Factory, a national AI platform powered by Nvidia, creating an “AI Grid” that connects datacentres and distributed 5G nodes to deliver intelligence closer to users.

Nezar Patria, vice minister of communication and digital affairs of the Republic of Indonesia said: “The inauguration of the AI-RAN Research Centre marks a concrete step in strengthening Indonesia’s digital sovereignty. The collaboration between the government, industry, and global partners such as Indosat, Nokia, and Nvidia demonstrates that Indonesia is not merely a user but also a creator of AI technology. This initiative supports the acceleration of the Indonesia Emas 2045 vision by building an inclusive, secure, and globally competitive AI ecosystem.”

Vikram Sinha, president director and CEO of Indosat Ooredoo Hutchison said: “As Indonesia accelerates its digital transformation, the AI-RAN Research Centre reflects Indosat’s larger purpose of empowering Indonesia. When connectivity meets compute, it creates intelligence, delivered at the edge, in a sovereign manner. This is how AI unlocks real impact, from personalised tutors for children in rural areas to precision farming powered by drones. Together with Nokia and Nvidia, we’re building the foundation for AI-driven growth that strengthens Indonesia’s digital future.”

From a network perspective, the project demonstrates how AI-RAN architectures can optimize wireless network performance, energy efficiency, and scalability through machine learning–based radio signal processing.

Ronnie Vasishta, senior vice president of telecom at Nvidia added: “The AI Grid is the biggest opportunity for telecom providers to make AI as ubiquitous as connectivity and distribute intelligence at scale by tapping into their nationwide wireless networks.”

Pallavi Mahajan, chief technology and AI officer at Nokia said: “This initiative represents a major milestone in our journey toward the future of AI-native networks by bringing AI-powered intelligence into the hands of every Indonesian.”

………………………………………………………………………………………………………………………………………………………..

Wireless Telcos are Skeptical about AI-RAN:

According to Light Reading, the AI RAN uptake is facing resistance from telcos. The problem is Nvidia’s AI GPUs are very costly and not GPUs power-efficient enough to reside in wireless base stations, central offices or even small telco data centers.

Nvidia references 300 watts for the power consumption of ARC-Pro, which is much higher than the peak of 40 watts that Qualcomm claimed more than two years ago for its own RAN silicon when supporting throughput of 24 Gbit/s. How ARC-Pro would measure up on a like-for-like basis in a commercial network is obviously unclear.

Nvidia also claims a Gbit/s-per-watt performance “on par with” today’s traditional custom silicon. Yet the huge energy consumption of GPU-filled telco data centers does not bear that out.

“Is there a case for a wide-area indiscriminate rollout? I am not sure,” said Verizon CTO Yago Tenorio, during the Brooklyn 6G Summit, another telecom event, last week. “It depends on the unit cost of the GPU, on the power efficiency of the GPU, and the main factor will always be just doing what’s best for the basestation. Don’t try to just overcomplicate the whole thing monetizing that platform, as there are easier ways to do it.”

“We have no way to justify a business case like that,” said Bernard Bureau, the vice president of wireless strategy for Canada’s Telus, at FYUZ. “Our COs [central offices] are not necessarily the best places to run a data center. It would mean huge investments in space and power upgrades for those locations, and we’ve got sunk investment that can be leveraged in our cell sites.”

Light Reading’s Iain Morris wrote, “Besides turning COs into data centers, operators would need to invest in fiber connections between those facilities and their masts.”

How much spectral efficiency can be gained by using Nvidia GPUs as RAN silicon?

“It’s debatable if it’s going to improve the spectral efficiency by 50% or even 100%. It depends on the case,” said Tenorio. Whatever the exact improvement, it would be “really good” and is something the industry needs, he told the audience.

In April, Nokia’s rival Ericsson said it had tested “AI-native” link adaptation, a RAN algorithm, in the network of Bell Canada without needing any GPU. “That’s an algorithm we have optimized for decades,” said Per Narvinger, the head of Ericsson’s mobile networks business group. “Despite that, through a large language model, but a really small one, we gained 10% of spectral efficiency.”

Before Nvidia invested in Nokia, the latter claimed to have sufficient AI and machine-learning capabilities in the custom silicon provided by Marvell Technology, its historical supplier of 5G base station chips.

Executives at Cohere Technology praises Nvidia’s investment in Nokia, seeing it as an important AI spur for telecom. Yet their own software does not run on Nvidia GPUs. It promises to boost spectral efficiency on today’s 5G networks, massively reducing what telcos would have to spend on new radios. It has won plaudits from Vodafone’s Pignatelli as well as Bell Canada and Telstra, both of which have invested in Cohere. The challenge is getting the kit vendors to accommodate a technology that could hurt their own sales. Regardless, Bell Canada’s recent field trials of Cohere have used a standard Dell server without GPUs.

Finally, if GPUs are so critical in AI for RAN, why has neither Ericsson or Samsung using Nvidia GPU’s in their RAN equipment?

Morris sums up:

“Currently, the AI-RAN strategy adopted by Nokia looks like a massive gamble on the future. “The world is developing on Nvidia,” Vasishta told Light Reading in the summer, before the company’s share price had gained another 35%. That vast and expanding ecosystem holds attractions for RAN developers bothered by the diminishing returns on investment in custom silicon.”

“Intel’s general-purpose chips and virtual RAN approach drew interest several years ago for all the same reasons. But Intel’s recent decline has made Nvidia shine even more brightly. Telcos might not have to worry. Nvidia is already paying a big 5G vendor (Nokia) to use its technology. For a company that is so outrageously wealthy, paying a big operator to deploy it would be the next logical step.

…………………………………………………………………………………………………………………………………………………

References:

https://capacityglobal.com/news/indosat-nokia-and-nvidia-launch-ai-ran-research-centre-in-indonesia/

https://www.telecoms.com/ai/indosat-nokia-and-nvidia-open-ai-ran-research-centre-in-indonesia

https://www.lightreading.com/5g/nokia-and-nvidia-s-ai-ran-plan-hits-telco-resistance

https://resources.nvidia.com/en-us-aerial-ran-computer-pro

Nvidia pays $1 billion for a stake in Nokia to collaborate on AI networking solutions

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Nvidia AI-RAN survey results; AI inferencing as a reinvention of edge computing?

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

The case for and against AI-RAN technology using Nvidia or AMD GPUs

AI RAN Alliance selects Alex Choi as Chairman

Amdocs and NVIDIA to Accelerate Adoption of Generative AI for $1.7 Trillion Telecom Industry

Amdocs and NVIDIA today announced they are collaborating to optimize large language models (LLMs) to speed adoption of generative AI applications and services across the $1.7 trillion telecommunications and media industries.(1)

Amdocs and NVIDIA will customize enterprise-grade LLMs running on NVIDIA accelerated computing as part of the Amdocs amAIz framework. The collaboration will empower communications service providers to efficiently deploy generative AI use cases across their businesses, from customer experiences to network provisioning.

Amdocs will use NVIDIA DGX Cloud AI supercomputing and NVIDIA AI Enterprise software to support flexible adoption strategies and help ensure service providers can simply and safely use generative AI applications.

Aligned with the Amdocs strategy of advancing generative AI use cases across the industry, the collaboration with NVIDIA builds on the previously announced Amdocs-Microsoft partnership. Service providers and media companies can adopt these applications in secure and trusted environments, including on premises and in the cloud.

With these new capabilities — including the NVIDIA NeMo framework for custom LLM development and guardrail features — service providers can benefit from enhanced performance, optimized resource utilization and flexible scalability to support emerging and future needs.

“NVIDIA and Amdocs are partnering to bring a unique platform and unmatched value proposition to customers,” said Shuky Sheffer, Amdocs Management Limited president and CEO. “By combining NVIDIA’s cutting-edge AI infrastructure, software and ecosystem and Amdocs’ industry-first amAlz AI framework, we believe that we have an unmatched offering that is both future-ready and value-additive for our customers.”

“Across a broad range of industries, enterprises are looking for the fastest, safest path to apply generative AI to boost productivity,” said Jensen Huang, founder and CEO of NVIDIA. “Our collaboration with Amdocs will help telco service providers automate personalized assistants, service ticket routing and other use cases for their billions of customers, and help the telcos analyze and optimize their operations.”

Amdocs counts more than 350 of the world’s leading telecom and media companies as customers, including 27 of the world’s top 30 service providers.(2) With more than 1.7 billion daily digital journeys, Amdocs platforms impact more than 3 billion people around the world.

NVIDIA and Amdocs are exploring a number of generative AI use cases to simplify and improve operations by providing secure, cost-effective and high-performance generative AI capabilities.

Initial use cases span customer care, including accelerating customer inquiry resolution by drawing information from across company data. On the network operations side, the companies are exploring how to proactively generate solutions that aid configuration, coverage or performance issues as they arise.

(1) Source: IDC, OMDIA, Factset analyses of Telecom 2022-2023 revenue.

(2) Source: OMDIA 2022 revenue estimates, excludes China.

Editor’s Note:

- Language models: These models, like OpenAI’s GPT-3, generate human-like text. One of the most popular examples of language-based generative models are called large language models (LLMs).

- Large language models are being leveraged for a wide variety of tasks, including essay generation, code development, translation, and even understanding genetic sequences.

- Generative adversarial networks (GANs): These models use two neural networks, a generator, and a discriminator.

- Unimodal models: These models only accept one data input format.

- Multimodal models: These models accept multiple types of inputs and prompts. For example, GPT-4 can accept both text and images as inputs.

- Variational autoencoders (VAEs): These deep learning architectures are frequently used to build generative AI models.

- Foundation models: These models generate output from one or more inputs (prompts) in the form of human language instructions.

https://www.nvidia.com/en-us/glossary/data-science/generative-ai/

https://blogs.nvidia.com/blog/2023/01/26/what-are-large-language-models-used-for/

Cloud Service Providers struggle with Generative AI; Users face vendor lock-in; “The hype is here, the revenue is not”

Global Telco AI Alliance to progress generative AI for telcos

Bain & Co, McKinsey & Co, AWS suggest how telcos can use and adapt Generative AI

Generative AI Unicorns Rule the Startup Roost; OpenAI in the Spotlight

Generative AI in telecom; ChatGPT as a manager? ChatGPT vs Google Search

Generative AI could put telecom jobs in jeopardy; compelling AI in telecom use cases

Nvidia Survey Reveals How Telcos Plan to Use AI; Quantifying ROI is a Challenge

A Nvidia sponsored survey of more than 400 telecommunications industry professionals from around the world found a cautious tone in how they plan to define and execute on their AI strategies. Virtually every telco is already engaged with AI in some way, although mostly at an early stage. NVIDIA’s first “State of AI in Telecommunications” survey consisted of questions covering a range of AI topics, infrastructure spending, top use cases, biggest challenges and deployment models. The survey was conducted over eight weeks between mid-November 2022 and mid-January 2023.

Amid skepticism about the money-making potential of 5G, telecoms see efficiencies driven by AI as the most likely path for returns on investment. 93% of those responding to questions about undertaking AI projects at their own companies appear to be substantially underinvesting in AI as a percentage of annual capital spending.

Some 50% of respondents reported spending less than $1 million last year on AI projects; a year earlier, 60% of respondents said they spent less than $1 million on AI. Just 3% of respondents spent over $50 million on AI in 2022.

The reasons cited for such cautious spending? Some 44% of respondents reported an inability to adequately quantify return on investment, which illustrates a mismatch between aspirations and the reality in introducing AI-driven solutions. 34% cited an insufficient number of data scientists as the second-biggest challenge.

The biggest telco objectives for AI are to: optimize operations (60%), lower costs (44%) and enhance customer engagement (35%). Respondents cited use cases ranging from cell site planning and truck-route optimization to recommendation engines.

Just over a third of respondents said they had been using AI for more than six months. 31% said they’re still weighing different options, 18% reported being still in a trial phase and only 5% said they had no AI plans at all. Most industry execs say they see AI technologies will positively impact their business – 65% agreed AI was important to their company’s success, and 59% said it would become a source of competitive advantage.

Operators are spending a fraction of their capex budgets on AI projects – last year half said they spent less than $1 million on AI. At the top end, 2% spent more than $50 million in 2021, with that number rising to 3% in 2022.

The latest AI Index compiled by Stanford University puts telcos at the forefront of AI deployment. Using its own data and that from a McKinsey study, it found that the highest level of AI adoption is in product or service development by hi-tech companies and telcos (45%), followed by AI in service operations (45%).

The biggest single application in any industry was natural language text understanding deployed by 34% of hi-tech and telco firms, with 28% implementing AI-based computer vision and 25% using virtual agents.

- Moving from proof of concept to production/scale 47%

- Economic uncertainty 46%

- Infrasctructure upgrades 46%

- Market differentiation 34%

- Change in priority of data science 20%

- 92% will either increase or maintain their AI spend in 2023.

References:

https://blogs.nvidia.com/blog/2023/02/21/telco-survey-ai/

https://www.nvidia.com/en-us/lp/industries/telecommunications/state-of-ai-in-telecom-survey-report/

https://aiindex.stanford.edu/wp-content/uploads/2022/03/2022-AI-Index-Report_Master.pdf

Allied Market Research: Global AI in telecom market forecast to reach $38.8 by 2031 with CAGR of 41.4% (from 2022 to 2031)

Global AI in Telecommunication Market at CAGR ~ 40% through 2026 – 2027

The case for and against AI in telecommunications; record quarter for AI venture funding and M&A deals

SK Telecom inspects cell towers for safety using drones and AI

Summary of ITU-R Workshop on “IMT for 2030 and beyond” (aka “6G”)