Month: December 2021

Algar Telecom deploys 1st 5G network in Brazil using 2.3GHz band

Brazilian network operator Algar Telecom announced that it launched what it claims to be the first commercial 5G network in the country. It’s a commercial Non Standalone (NSA) 5G service using its newly acquired 2.3GHz spectrum. The 5G network went live on 15 December and covers selected parts of Uberlandia and Uberaba, as well as Franca in Sao Paulo, with initial coverage reaching some 40 districts in these three cities.

Algar had carried out demonstrations of 5G technology two weeks ago in Uberaba via an implementation carried out together with Nokia and with a focus on agribusiness. According to the company, investments were made in transport network structures, network core and service platforms.

Brazil’s Minister of Communications, Fábio Faria, had anticipated in his hearing before the Senate last week that Algar would be the first telco to launch 5G services in the country.

“For this almost immediate launch to be possible, intensive planning prior to the 5G auction was essential, ensuring the acquisition of the 2.3 GHz frequency, which does not require spectrum cleaning. In addition, the company already had a good part of its infrastructure adequate or easily adapted to offer 5G. We made investments in backhaul structures, network core and service platforms,” the telco said in a release.

In the 5G auction, which ended on November 5, Algar Telecom had secured seven regional slots: five on the 26 GHz frequency, one on the 3.5 GHz frequency and one on the 2.3 GHz frequency. All slots obtained are in Algar Telecom’s original area of operation, where the company has operated since 1954, and which covers 87 municipalities in the states of Minas Gerais, São Paulo, Goiás and Mato Grosso do Sul.

The government of Brazil raised a total of 47.2 billion reals ($8.5 billion) in its recent 5G spectrum auction, making it the second largest auction of assets in the country’s history, according to the government.

Through this auction, the government offered spectrum in the 700 MHz, 2.3 GHz, 3.5 GHZ and 26 GHz bands.

The country’s main mobile operators, Vivo, Claro and TIM, secured 5G spectrum as well as telecoms operators Algar Telecom and Sercomtel. Also, six new entrants secured 5G spectrum in the auction.

The new entrants that secured licenses in the auction are Winity II Telecom, Brisanet, Fly Link, Neko Serviços e Comunicações and Entertainment and Education, Consórcio 5G Sul and Cloud2U Indústria e Comércio de Equipamentos Eletrônicos.

Brazilian Communications Minister Fabio Faria said that the government will schedule a new 5G spectrum auction in 2022 to sell batches that did not attract interest, mainly in the 26 GHZ spectrum band. Faria noted that the 26 GHZ spectrum did not attract interest due to uncertainties in the business model.

The rules previously approved by telecommunications watchdog Anatel stipulate that 5G should be deployed across Brazilian state capitals by July 31, 2022.

Brazilian cities with more than 500,000 inhabitants will have 5G by July 31, 2025, while the deadline for the rollout of the service in locations with more than 200,000 inhabitants is July 31, 2026. Also, Brazilian cities with more than 100,000 inhabitants will have 5G by July 31 2027, and the service will be available in locations with more than 30,000 inhabitants by July 31, 2028.

TeleGeography notes that Algar acquired regional spectrum in the 2.3GHz, 3.5GHz and 26GHz bands in the country’s 5G spectrum auction. Unlike the 3.5GHz band, the 2.3GHz band does not require cleaning for interference before 5G use. Algar executive Marcio De Jesus commented: “The company already had a good part of its infrastructure adequate or easy to adapt to the 5G offer. We made investments in backhaul structures, network core and service platforms.”

References:

https://www.rcrwireless.com/20211216/5g/algar-telecom-activates-first-5g-network-brazil

https://www.commsupdate.com/articles/2021/12/16/algar-telecom-launches-5g-using-2-3ghz-band/

https://www.gsma.com/spectrum/wp-content/uploads/2020/11/5G-and-3.5-GHz-Range-in-Latam.pdf

https://www.rcrwireless.com/20211108/5g/brazil-raises-total-8-billion-5g-spectrum-auction

Multi-access Edge Computing (MEC) Market, Applications and ETSI MEC Standard-Part I

by Dario Sabella, Intel, ETSI MEC Chair, with Alan J Weissberger

Introduction (by Alan J Weissberger):

According to Research & Markets, the global Multi-access Edge Computing (MEC) market size is anticipated to reach $23.36 billion by 2028, producing a CAGR of 42.6%. Reduced Total Cost of Ownership (TCO) due to integration of MEC in network systems as compared to legacy systems and subsequent ability to generate faster Return on Investment (RoI) is further expected to encourage smaller retail chains to leverage MEC technology.

Multi-access Edge Computing Market Highlights (from Research & Markets):

- The software segment is anticipated to be the fastest-growing segment owing to emerging demand among service providers to use software that can be deployed for various applications without making changes to existing 3GPP hardware infrastructure specifications.

- The energy and utilities segment is expected to witness the fastest growth rate over the forecast period owing to increasing demand among companies to quickly access insights and analyze data generated from remote locations

- The Asia Pacific region is expected to emerge as the fastest-growing regional market due to strong support from the government to encourage advanced network infrastructure

A few important MEC applications/ use cases include:

- Streaming video and pay TV: Increasing number of users adopting the Over the Top (OTT) video delivery model is expected to promote telecom companies and mobile networks to upgrade their existing infrastructure to cache video/audio content closer to the user. Using the multi-access edge computing (MEC) architecture system brings backend functionality closer to the user network, which is expected to aid Multichannel Video Programming Distributors (MVPD) to meet their customers’ demands. Users pay subscription fees for a specified duration of time to access the content offered by the MVPD.

- Deployment of MEC technology is expected to enable retail and on line stores to improve the performance of in-store systems and reduce data processing time, thus ensuring faster resolving of customer grievances. Furthermore, adoption of this technology is expected to reduce the load on external macro sites, thus offering a seamless in-store experience for users.

- Increasing number of IoT devices and the emerging need to gain access to real-time analysis of data generated by them is expected to drive MEC market growth. Leveraging this technology in IoT can facilitate reduced pressure on cloud networks and result in lower energy consumption, which is expected to offer significant growth opportunities to the market.

- Multi-access edge computing is expected to enhance manufacturing practices and thus facilitate the advent of connected cars ecosystem. Connected cars are equipped with computing systems, wireless devices, and sensing, which have to work together in a coordinated fashion, thus facilitating the need to adopt MEC.

- 5G MEC technology can be used to exchange critical operational and safety information to enhance efficiency, safety, and enhance value-added services such as smart parking and car finder.

Previously referred to as Mobile Edge Computing, MEC raises a lot of questions. For example:

- Can MEC be used with wireline and fixed access networks?

- Is 5G Stand Alone (SA) core network with separate control, data, and management planes required for MEC to be effective?

- Finally, why should MEC (and multi-cloud) matter to infrastructure owners and application developers?

Dario Sabella, Intel, ETSI MEC Chair, answers those questions and provides more context and color in his two part article.

………………………………………………………………………………………………..

ETSI MEC Standard Explained, by Dario Sabella, Intel, ETSI MEC Chair

ETSI MEC – Foundation for Edge Computing:

MEC (Multi-access Edge Computing) “offers to application developers and content providers cloud-computing capabilities and an IT service environment at the edge of the network” [1].

The MEC ISG (Industry Specification Group) was established by ETSI to create an open standard for edge computing, allowing multiple implementations and ensuring interoperability across a diverse ecosystem of stakeholders: from mobile operators, application developers, Over the Top (OTT) players, Independent Software Vendors (ISVs), telecom equipment vendors, IT platform vendors, system integrators, and technology providers; all of these parties are interested in delivering services based on Multi-access Edge Computing concepts.

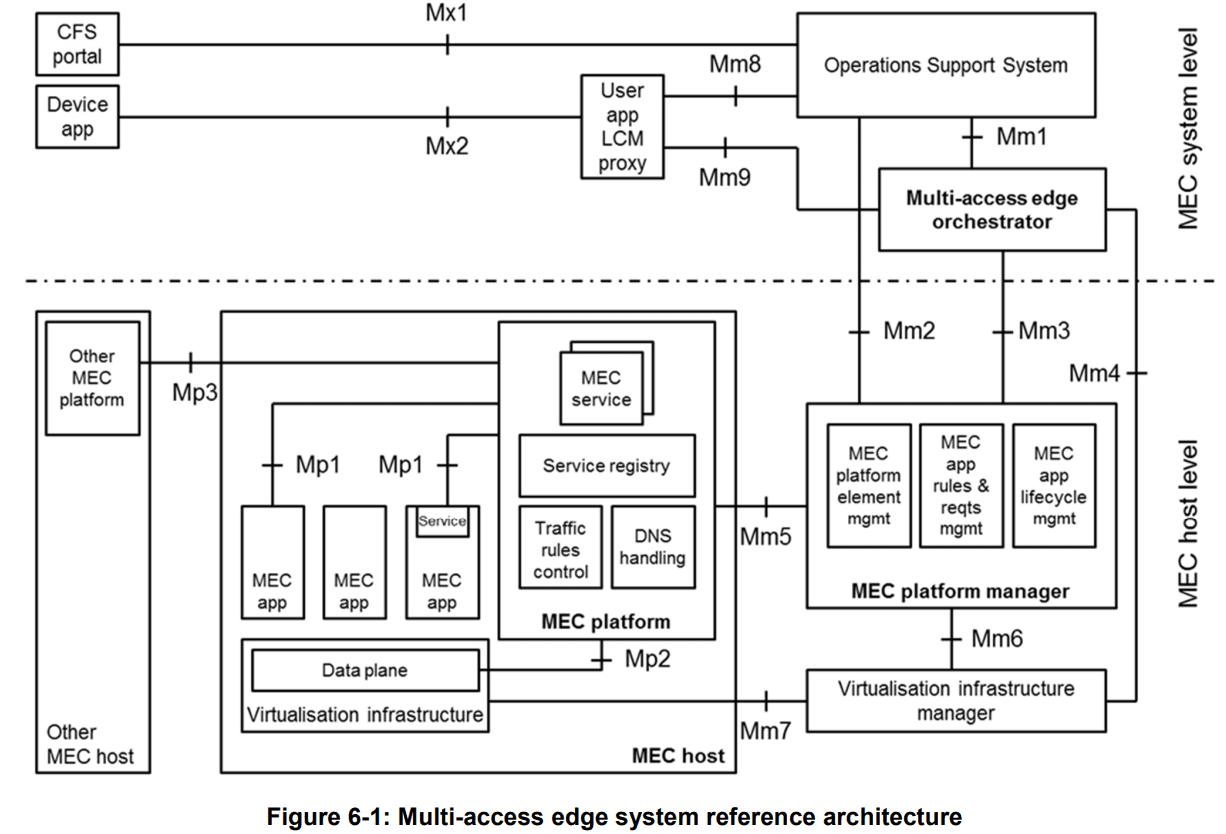

The work of the MEC initiative (see the architecture in Figure 1. above) aims to unite the telco and IT-cloud worlds, providing IT and cloud-computing capabilities at the edge: operators can open their network edge to authorized third parties, allowing them to flexibly and rapidly deploy innovative applications and services towards mobile subscribers, enterprises and vertical segments (e.g. automotive).

Author’s Note:

From a deployment point of view, a natural question is “where exactly is the edge?” In this perspective, the ETSI MEC architecture supports all possible options, ranging from customer premises, 1st wireless base station/small cell, 1st network compute point of presence, internet resident data center/compute server or edge of the core network. The MEC standard is flexible, and the actual and specific MEC deployment is really an implementation choice from the infrastructure owners.

Additionally, the MEC architecture (shown in Figure 2 and defined in the MEC 003 specification [2]) has been designed in such a way that a number of different deployment options of MEC systems are possible:

- The MEC 003 specification includes also a MEC in NFV (Network Functions Virtualization) variant, which is a MEC architecture that instantiates MEC applications and NFV virtualized network functions on the same virtualization infrastructure, and to reuse ETSI NFV MANO components to fulfil a part of the MEC management and orchestration tasks. This MEC deployment in NFV (Network Functions Virtualization) is also coherent with the progressive virtualization of networks.

- In that perspective, MEC deployment in 5G networks is a main scenario of applicability (note that the MEC standard is aligned with 3GPP specifications [3]).

- On the other hand, the nature of the ETSI MEC Standard (as emphasized by the term “Multi-access” in the MEC acronym) is access agnostic and can be applicable to any kind of deployment, from Wi-Fi to fixed networks.

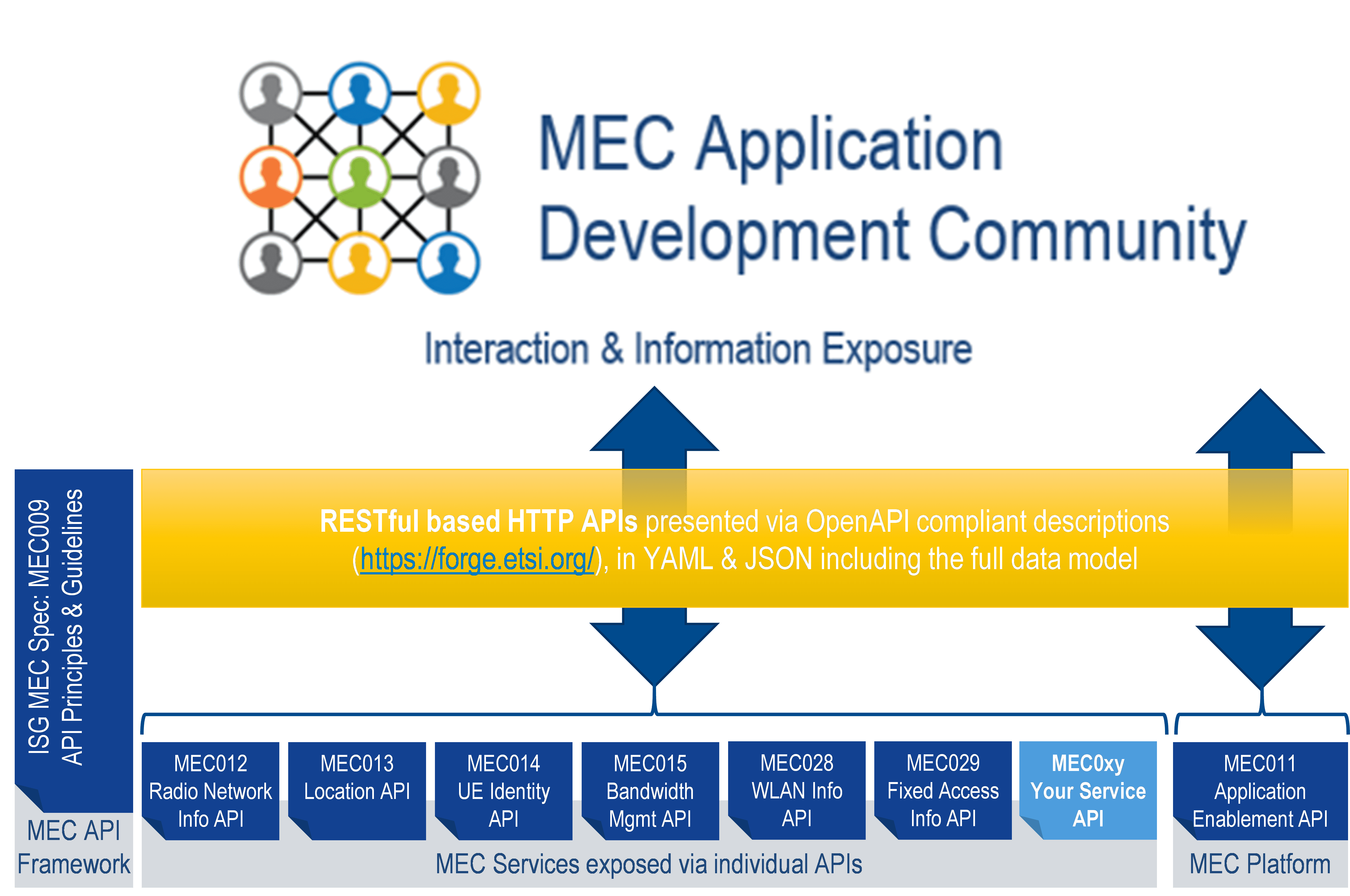

- A major effort of the MEC standardization work is dedicated to publishing relevant and industry-driven exemplary specifications of MEC service APIs, that are using RESTful principles, thus exposed to application developers in a universally recognized language.

Figure 2. MEC Application Development Community

The ETSI MEC initiative is focused on Applications at the Edge, and the specified MEC APIs (see above Figure 2.) include meaningful information exposed to application developers at the network edge, ranging from RNI (Radio Network Information) API (MEC 012), WLAN API (MEC 029), Fixed Access API (MEC 028), Location API (MEC 013), Traffic Management APIs (MEC015) and many others.

Additionally, new APIs (compliant with the basic MEC API principles [4]) can be added, without the need of being standardized in ETSI.

In this perspective, MEC truly provides a new ecosystem and value chain, by opening up the market to third parties, and allowing not only operators and cloud providers but any authorized software developers that can flexibly and rapidly deploy innovative applications and services towards mobile subscribers, enterprises and vertical segments.

MEC in 4G (and 5G NSA) Deployments:

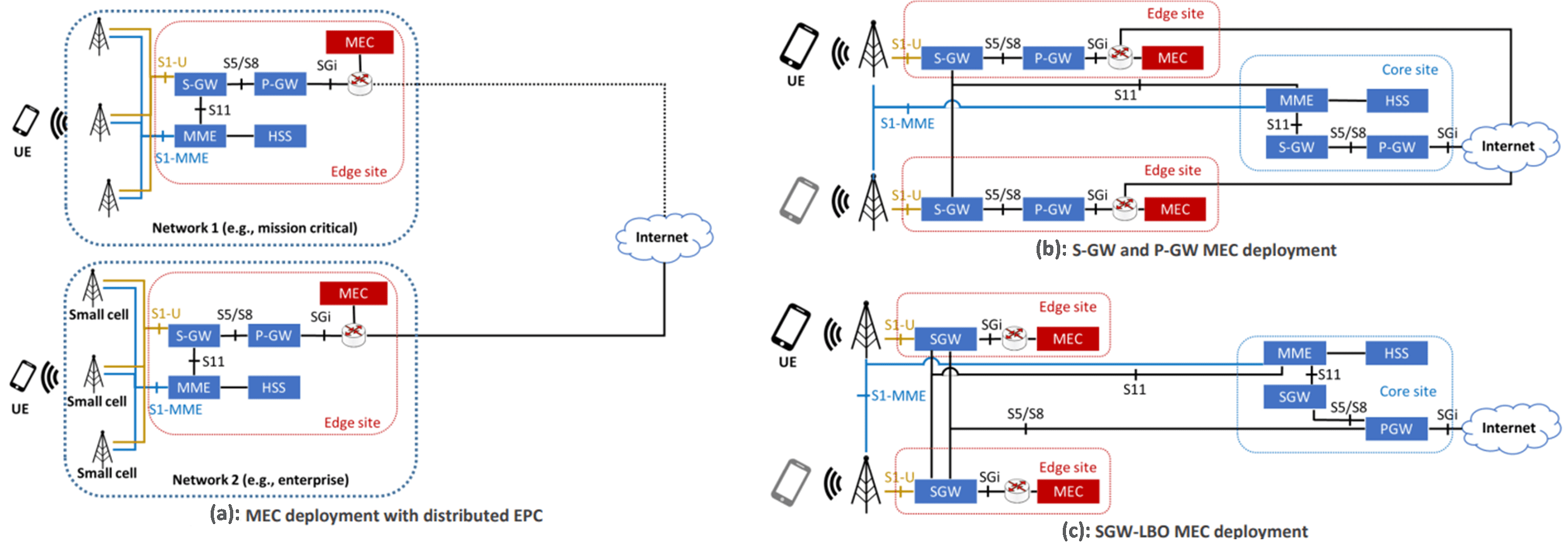

ETSI has already clarified how MEC can be deployed in 4G networks, given its access-agnostic nature [5], with many approaches:

From “bump in the wire” (where the MEC sits on the S1 interface of the 4G system architecture), to “distributed 4G-Evolved Packet Core” (EPC -where the MEC data plane sits on the SGi interface), to “distributed S/PGW” (where the control plane functions such as the MME and HSS are located at the operator’s core site) and “distributed SGW with Local Breakout” (SGW-LBO) -where the MEC system and the distributed SGW are co-located at the network’s edge.

Figure 3. MEC deployment options with distributed EPC (a), distributed S/PGW (b) and SGW-LBO (c)

Depending on the selected solution, MEC Handover is executed in different ways:

In the “bump in the wire approach,” mobility is not natively supported. Instead, in the EPC MEC, SGW + PGW MEC, and CUPS MEC, the MEC handover is supported using 3GPP specified S1 Handover with SGW relocation by maintaining the original PGW as anchor.

The same considerations apply for the SGW-LBO MEC deployment. In the latter case, the target SGW enforces the same policy towards the local MEC application.

Finally, the solutions that include an EPC gateway, such as EPC MEC, SGW+PGW MEC, SGW-LBO MEC, and CUPS MEC are compliant with LI (Lawful Interception) requirements.

This last aspect is also very relevant for MEC adoption, since public telecommunications network and service providers are legally required to make available to law enforcement authorities information from their retained data which is necessary for the authorities to be able to monitor telecommunications traffic as part of criminal investigations.

In that perspective, MEC deployment options are also chosen by infrastructure owners in the view of their compliance to Lawful Interception requirements.

Distributed SGW with Local Breakout (SGW-LBO):

A mainstream for the adoption of MEC is given by the progressive introduction of 5G networks.

Among the various 5G deployment options, local breakout at the SGWs (Figure 3c above) is a solution for MEC that originated from operators’ desire to have a greater control on the granularity of the traffic that needs to be steered. This principle was dictated by the need to have the users able to reach both the MEC applications and the operator’s core site application in a selective manner over the same APN.

The traffic steering uses the SGi – Local Break Out interface which supports traffic separation and allows the same level of security as the network operator expects from a 3GPP-compliant solution.

This solution allows the operator to specify traffic filters similar to the uplink classifiers in 5G, which are used for traffic steering. The local breakout architecture also supports MEC host mobility, extension to the edge of CDN, push applications that requires paging and ultra-low latency use cases.

The SGW selection process performed by MMEs is according to the 3GPP specifications and based on the geographical location of UEs (Tracking Areas) as provisioned in the operator’s DNS.

The SGW-LBO offers the possibility to steer traffic based on any operator-chosen combination of the policy sets, such as APN and user identifier, packet’s 5-tuple, and other IP level parameters including IP version and DSCP marking.

Integrated MEC deployment in 5G networks (3GPP Release 15 and later):

Edge computing has been identified as one of the key technologies required to support low latency together with mission critical and future IoT services. This was considered in the initial 3GPP requirements, and the 5G system was designed from the beginning to provide efficient and flexible support for edge computing to enable superior performance and quality of experience.

In that perspective, the design approach taken by 3GPP allows the mapping of MEC onto Application Functions (AF) that can use the services and information offered by other 3GPP network functions based on the configured policies.

In addition, a number of enabling functionalities were defined to provide flexible support for different deployments of MEC and to support MEC in case of user mobility events. The new 5G architecture (and MEC deployment as AF) is depicted in the Figure 4 below.

Figure 4. – MEC as an AF (Application Function) in 5G system architecture

In this deployment scenario, MEC as an AF (Application Function) can request the 5GC (5G Core network) to select a local UPF (User Plane Function) near the target RAN node. Then use the local UPF for PDU sessions of the target UE(s) and to control the traffic forwarding from the local UPF so that the UL traffic matching with the traffic filters received from MEC (AF) is diverted towards MEC hosts while other traffic is sent to the Central Cloud.

In case of UE mobility, the 5GC can re-select a new local UPF more suitable to handle application traffic identified by MEC (AF) and notify the AF about the new serving UPF.

In summary, MEC as an AF can provide the following services with a 5GC:

- Traffic filters identifying MEC applications deployed locally on MEC hosts in Edge Cloud

- Target UEs (one UE identified by its IP/MAC address, a group of UE, any UE)

- Information about forwarding the identified traffic further e.g. references to tunnels toward MEC hosts

………………………………………………………………………………………………………………………………………………………………………………………….

Part II. of this two part article will illustrate and explain concurrent access to local and central Data Networks. The enablement of MEC deployments and ecosystem development will also be presented.

Importantly, Part II will explain how MEC is evolving to the next phase of 5G– 3GPP Release 17. In particular, ETSI MEC is aligning with 3GPP SA6 which is defining an EDGEAPP architecture (ref. 3GPP TS 23.558).

Part II will also explain how MEC is evolving to multi-cloud support in alignment with GSMA OPG requirements for the MEC Federation work.

ETSI MEC Standard Explained – Part II

…………………………………………………………………………………………………………………………………………………………………………………………..

References:

1. Introduction:

https://www.accenture.com/_acnmedia/PDF-128/Accenute-MEC-for-Pervasive-Networks-PoV.pdf

PowerPoint Presentation (etsi.org)

2. Main body of this article (Part I and II):

[1] ETSI MEC website, https://www.etsi.org/technologies/multi-access-edge-computing

[2] ETSI GS MEC 003 V2.1.1 (2019-01): “Multi-access Edge Computing (MEC); Framework and Reference Architecture”, https://www.etsi.org/deliver/etsi_gs/mec/001_099/003/02.01.01_60/gs_mec003v020101p.pdf

[3] ETSI White Paper #36, “Harmonizing standards for edge computing – A synergized architecture leveraging ETSI ISG MEC and 3GPP specifications”, First Edition, July 2020, https://www.etsi.org/images/files/ETSIWhitePapers/ETSI_wp36_Harmonizing-standards-for-edge-computing.pdf

[4] ETSI GS MEC 009 V3.1.1 (2021-06), “Multi-access Edge Computing (MEC); General principles, patterns and common aspects of MEC Service APIs”, https://www.etsi.org/deliver/etsi_gs/MEC/001_099/009/03.01.01_60/gs_MEC009v030101p.pdf

[5] ETSI White Paper No. 24, “MEC Deployments in 4G and Evolution Towards 5G”, February 2018, https://www.etsi.org/images/files/ETSIWhitePapers/etsi_wp24_MEC_deployment_in_4G_5G_FINAL.pdf

[6] ETSI White Paper No. 28, “MEC in 5G network”, June 2018, https://www.etsi.org/images/files/ETSIWhitePapers/etsi_wp28_mec_in_5G_FINAL.pdf

[7] ETSI GR MEC 031 V2.1.1 (2020-10), “Multi-access Edge Computing (MEC); MEC 5G Integration”, https://www.etsi.org/deliver/etsi_gr/MEC/001_099/031/02.01.01_60/gr_MEC031v020101p.pdf

[8] ETSI GR MEC 035 V3.1.1 (2021-06), “Multi-access Edge Computing (MEC); Study on Inter-MEC systems and MEC-Cloud systems coordination”, https://www.etsi.org/deliver/etsi_gr/MEC/001_099/035/03.01.01_60/gr_mec035v030101p.pdf

[9] ETSI DGS/MEC-0040FederationAPI’ Work Item, “Multi-access Edge Computing (MEC); Federation enablement APIs”, https://portal.etsi.org/webapp/WorkProgram/Report_WorkItem.asp?WKI_ID=63022

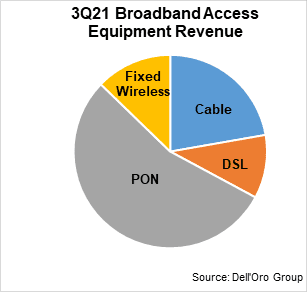

Dell’Oro: PON ONT spending +15% Year over Year

According to a newly published report by Dell’Oro Group, total global revenue for the Broadband Access equipment market increased to $3.9 B in 3Q 2021, up 7% year-over-year (Y/Y). Growth came from spending on both PON infrastructure and fixed wireless CPE. Please see chart below.

“5G fixed wireless deployments joined fiber as the primary drivers for spending this quarter,” noted Jeff Heynen, Vice President, Broadband Access and Home Networking at Dell’Oro Group. “Despite supply chain constraints and increased costs, operators continue to focus on expanding broadband connectivity,” explained Heynen.

Additional highlights from the 3Q 2021 Broadband Access and Home Networking quarterly report:

- Total cable access concentrator revenue decreased 27 percent Y/Y to $257 M. There was a clear mix shift this quarter to remote PHY and remote MACPHY devices, both of which saw Y/Y revenue increases.

- Total PON ONT unit shipments reached 32 M units, marking the fourth quarter in row-unit shipments have exceeded 30 M globally.

- Component shortages are clearly impacting cable CPE and home networking device sales, with unit shipments down markedly Y/Y.

The Dell’Oro Group Broadband Access and Home Networking Quarterly Report provides a complete overview of the Broadband Access market with tables covering manufacturers’ revenue, average selling prices, and port/unit shipments for Cable, DSL, and PON equipment. Covered equipment includes Converged Cable Access Platforms (CCAP) and Distributed Access Architectures (DAA); Digital Subscriber Line Access Multiplexers ([DSLAMs] by technology ADSL/ADSL2+, G.SHDSL, VDSL, VDSL Profile 35b, and G.FAST); PON Optical Line Terminals (OLTs), Cable, DSL, and PON CPE (Customer Premises Equipment); and SOHO WLAN Equipment, including Mesh Routers. For more information about the report, please contact [email protected].

Separately, Dell’Oro reports that the worldwide Campus Switch market revenue reached a record level in 3Q 2021. Growth was mostly propelled by 1 Gbps, which reached a record level in shipments during the quarter, while Ethernet NBase-T ports were down Y/Y.

“We have been predicting the demand in the market to remain strong, but what surprised us is the level of shipments and revenues that vendors were able to achieve during the quarter, despite ongoing supply challenges,” said Sameh Boujelbene, Senior Director at Dell’Oro Group. “It appears, however, that these supply challenges are impacting the newer technologies more than the older ones, due to a less diversified ecosystem, and in some cases, a less mature supply chain,” added Boujelbene.

Additional highlights from the 3Q 2021 Ethernet Switch – Campus Report:

- Extreme, HPE, and Juniper each gained more than one point of revenue share in Europe, Middle East and Africa (EMEA)

- H3C outperformed the market and captured the revenue leading position in China

- Power-over-Ethernet (PoE) ports up strong double-digits and comprised 30 percent of the total ports

The Dell’Oro Group Ethernet Switch – Campus Quarterly Report offers a detailed view of Ethernet switches built and optimized for deployment outside the data center, to connect users and things to the Local Area Networks. The report contains in-depth market and vendor-level information on manufacturers’ revenue, ports shipped and average selling prices for both Modular and Fixed, and Fixed Managed and Unmanaged Ethernet Switches (100 Mbps, 1, 2.5, 5, 10, 25, 40, 50, 100 Gbps), Power-over-Ethernet, plus regional breakouts as well as split by customer size (Enterprise vs. SMB) and vertical segments. To purchase these reports, please contact us by email at [email protected].

About Dell’Oro Group

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, networks, and data center IT markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions. For more information, contact Dell’Oro Group at +1.650.622.9400 or visit www.delloro.com.

References:

Vodafone and Mavenir complete VoLTE call over a containerized Open RAN lab environment

Upstart network software provider Mavenir, announced today that it completed the first data and Voice over LTE (VoLTE) call across a containerized 4G small cell Open RAN solution in a Vodafone lab environment. The completed tests are the latest steps forward to delivering an open and vendor-interoperable 4G connectivity solution for small to medium-sized office locations.

Having first started work on a containerized indoor enterprise connectivity solution in January 2021, Vodafone has completed tests for an important stage of the technology roadmap. The plug-and-play small cell equipment can ensure comprehensive mobile coverage in every corner of the office. The solution will provide 4G coverage initially, making use of radio hardware from Sercomm and software from Mavenir (Open RAN). Containerization means that software can be seamlessly transferred between equipment, platforms, and applications. Wind River provided its Containers as a Service (CaaS) software, part of Wind River Studio.

This demonstration of a containerized solution is a major milestone in the evolution of connectivity equipment away from physical infrastructure to a digital cloud-based environment. Containerization provides greater flexibility for customers, but also significant benefits in terms of speed and cost of deployment.

Open RAN technology separates software from hardware, meaning more flexibility for mobile operators and customers. This approach aims to see many companies providing the components that make up a mobile network site, where previously one vendor would have delivered the whole solution. The technology is controversial, but accepted by many as a potential disruptor for the telecommunications industry. Vodafone claims to be one of the industry leaders in supporting the development of the Open RAN vendor ecosystem.

Whereas much of the focus for Open RAN has been directed towards network infrastructure deployment on mobile sites throughout the UK, the technology can be implemented in an enterprise environment to support local connectivity requirements. As an interoperable and standardized (there are no standards for Open RAN!) technology, Open RAN solutions can be integrated with little disruption in a “plug and play” manner, interoperable with other Open RAN compliant vendors.

Andrea Dona, Chief Network Officer, Vodafone UK, said: “Open RAN is opening doors to simplified and intuitive connectivity solutions. For our wider network deployment strategy, Open RAN is enabling us to work with a wider pool of suppliers and to avoid vendor lock-in scenarios that might prevent us from taking advantage of the latest innovations. The same could be said for enterprise connectivity solutions.”

“From the moment Open RAN is deployed in an office environment, customers are no-longer locked into a single upgrade path. Working alongside Vodafone, customers can be more flexible in how connectivity solutions are adapted and upgraded as demands evolve in the future.”

Stefano Cantarelli, Executive Vice President and Chief Marketing Officer, Mavenir, said; “Cloud Native and Open Solutions are becoming the new reality of the mobile world, and these include Radio Access and its containerized implementation. Open vRAN is a very flexible architecture that can serve any type of segment and Mavenir is really pleased to work with Vodafone in the enterprise business and achieved another first together. It is an opportunity to show that automated and AI controlled systems will simplify life to business and industry.”

“Mavenir is delighted to partner with Vodafone in Open RAN and to work in the U.K. on their radio network transformation initiative, proving the extreme flexibility of Open vRAN,” Virtyt Koshi, SVP of Mavenir EMEA, said. “We are particularly proud in working in the field within the Vodafone commercial network and in the Newbury Open RAN Test and Verification lab, supporting the Vodafone effort to boost the ecosystem.”

Moving forward, Vodafone and Mavenir will focus on finalizing the packaging and automation of the solution before beginning trials with selected customers.

References:

Vodafone and Mavenir create indoor OpenRAN solution for business customers

Vodafone partners with Mavenir to leverage Open RAN for in-building enterprise 4G

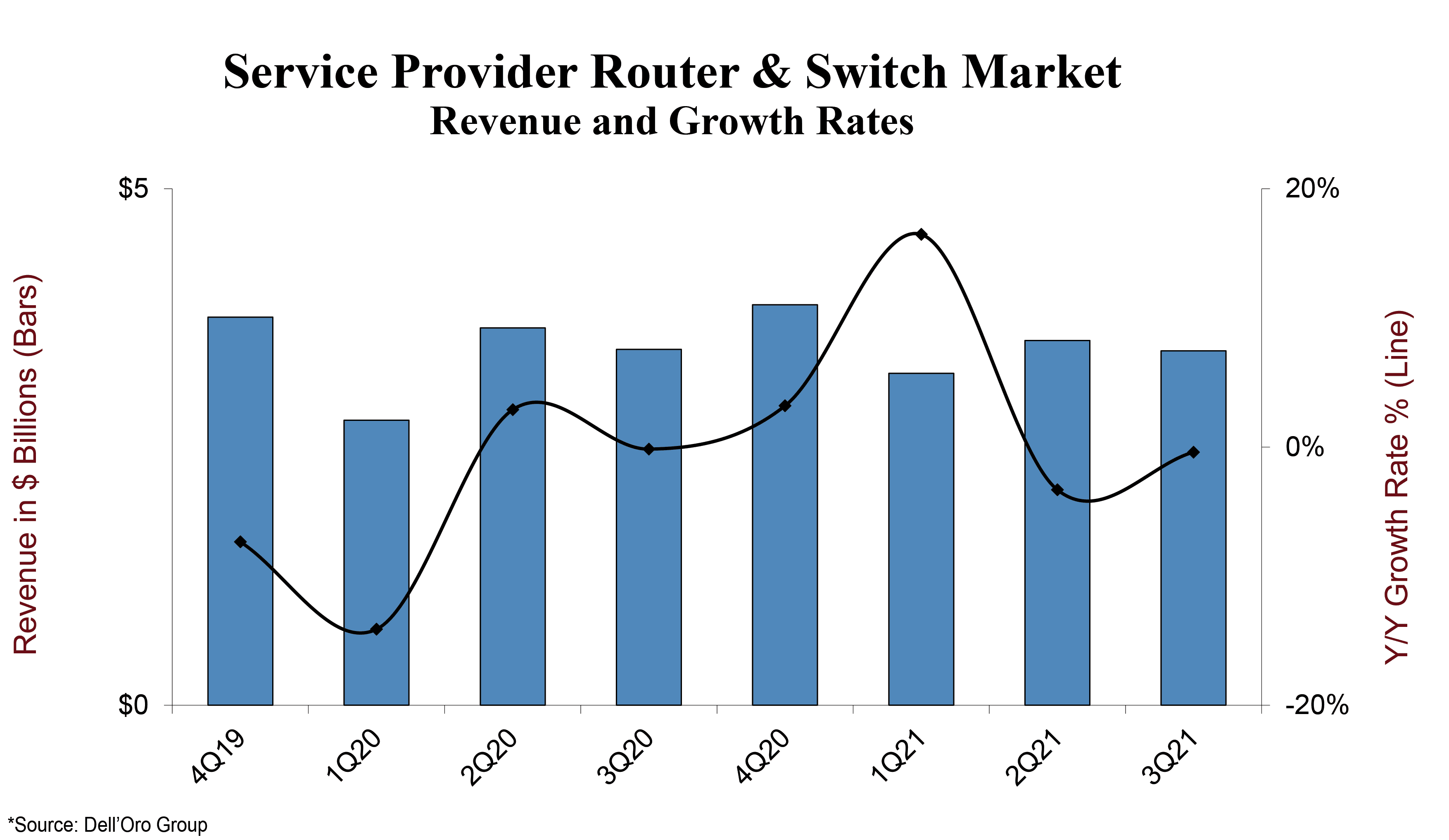

Dell Oro and IDC on the Global Service Provider Router and Switch market in 3Q-2021

According to a new report by Dell’Oro Group, the worldwide Service Provider Router and Switch market was flat in 3Q 2021. Market growth was stifled during the quarter due in large part to global supply chain constraints that affected vendors’ ability to deliver products to customers.

“Despite global supply chain problems, the underlying demand to upgrade backbone and 5G transport networks remains strong,” said Shin Umeda, Vice President at Dell’Oro Group. “Service providers are transitioning to new network architectures, and demand for 400 Gbps capable systems and enhanced edge routers offer the networking capabilities required to achieve the transformations,” added Umeda.

Additional highlights from the 3Q 2021 Service Provider Router and Switch Report:

- Cisco was the top-ranked vendor for the first three quarters of 2021, followed by Huawei, Nokia, Juniper, and ZTE.

- The Service Provider Router and Switch market is projected to grow at a slightly lower rate for 2021 due to the negative effect of supply chain constraints.

- The North American region outperformed all other regions with double-digit revenue growth through the first three quarters of 2021.

The Dell’Oro Group Service Provider Router and Switch Quarterly Report offers complete, in-depth coverage of the Service Provider Router and Switch market for future current and historical periods. The report includes qualitative analysis and detailed statistics for manufacture revenue by regions, customer types, and use cases, average selling prices, and unit and port shipments. To purchase these reports, please contact us by email at [email protected].

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, networks, and data center IT markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions. For more information, contact Dell’Oro Group at +1.650.622.9400 or visit www.delloro.com.

……………………………………………………………………………………..

On December 8th, IDC reported that the worldwide Ethernet switch market recorded $8.1 billion in revenue in the third quarter of 2021 (3Q21), an increase of 7.5% year over year.

Meanwhile, worldwide total enterprise and service provider (SP) router market revenues grew 4.7% year over year in 3Q21 to $3.8 billion. These growth rates are according to results published in the International Data Corporation (IDC) Worldwide Quarterly Ethernet Switch Tracker and IDC Worldwide Quarterly Router Tracker.

Ethernet Switch Market Highlights

The Ethernet switch market’s 7.5% annualized growth in 3Q21 builds on growth in the first half of the year. Year-to-date through the first three quarters of 2021, the market is up 8.6% compared to the first three quarters of 2020. On a sequential basis, the 3Q21 Ethernet switch market revenues were up 9.3% from the previous quarter. And compared to the third quarter of 2019, which was before the COVID-19 pandemic, revenues increased 9.6%, indicating strong organic growth in the market.

From a geographic perspective, the 3Q21 Ethernet switch market had strong results across most parts of the world. In the Asia/Pacific region, the People’s Republic of China increased 18.1% year over year while Japan’s market declined 13.6%. In the rest of Asia/Pacific (excluding China and Japan) (APeJC), the market rose 7.3% year over year, buoyed by the market in Korea growing 22.3% annually. In Europe, results were mixed: Western Europe’s market rose 16.7% year over year with strength from Germany, which grew 18.3%. Central and Eastern Europe’s market rose 3.3%. In the Middle East & Africa, the market declined 8.9% year over year. Across the Americas, the market in the United States rose 5.5%; Canada’s market fell 0.2%, and Latin America’s market increased 16.0% year over year with Brazil rising 43.6% compared to 3Q20.

“The Ethernet switching market continues to demonstrate impressive resilience. Through the first three quarters of 2021, the market has recorded healthy growth compared to 2020, driven by demand in both the enterprise campus and branch markets, as well as from hyperscalers and other cloud providers, which continue to invest in datacenter switching capacity,” notes Brad Casemore, research vice president, Datacenter and Multicloud Networking. “There are some headwinds in the market, though: supply-chain constraints occasioned by the COVID-19 pandemic mean that customers and vendors must plan accordingly as they look to the year ahead, and the pandemic itself continues to sow uncertainty among technology buyers, especially enterprises in certain industries.”

Overall port shipments increased 9.1% with growth in both the non-datacenter and datacenter portions of the Ethernet switch market. Non-datacenter Ethernet switch revenues grew 6.5% in 3Q21 year over year with port shipments increasing 9.1%. The non-datacenter Ethernet switch portion of the market makes up 87.1% of port shipments and 56.7% of total market revenues with the balance of revenues and port shipments in the datacenter portion of the market. In the datacenter segment, revenues rose 8.8% year over year while port shipments increased 8.7%.

The higher-speed segments of the Ethernet switch market continue to see significant growth driven by hyperscalers and cloud providers. Market revenues for 200/400 GbE switches grew 70.4% from the second quarter to the third quarter of 2021 with port shipments more than doubling (+118.1%) on a sequential basis. 100GbE revenues increased 13.8% on an annualized basis while port shipments rose 13.1% year over year. 100GbE revenues make up 24.5% of the Ethernet switch market’s total revenues. 25/50 GbE revenues declined 1.1% annually while port shipments declined 7.8%.

Lower-speed switches, a more mature part of the market, saw mixed results. 10GbE port shipments declined 1.5% year over year with revenue dropping 6.0% annually; 10GbE switches make up 23.0% of the market’s total revenue. 1GbE switches increased 10.5% year over year in port shipments and increased 7.6% in revenue. 1GbE accounts for 34.4% of the total Ethernet switch market’s revenue. 2.5/5GbE switch revenue increased 7.3% sequentially from 2Q21 to 3Q21 while port shipments rose 6.7% quarter-over-quarter.

Router Market Highlights

The worldwide enterprise and service provider router market increased 4.7% year over year in 3Q21 with the major service provider segment, which accounts for 76.4% of revenues, increasing 3.6% and the enterprise segment increasing 8.3%. From a regional perspective, the combined service provider and enterprise router market increased 15.4% in APeJC. Japan’s market declined 6.1% while the People’s Republic of China market was up 2.2% year over year. Revenues in Western Europe were off 1.6% compared to 3Q20 while the Central and Eastern Europe the combined enterprise and service provider declined 4.9% annually. The Middle East & Africa region declined 1.7%. In the U.S., the enterprise segment increased 27.6% while the service provider revenues increased 5.4% giving the combined markets a 10.6% increase on an annualized basis. The Latin American market grew 7.3% on an annualized basis and Canada’s market increased 6.2% year over year.

Vendor Highlights

Cisco finished 3Q21 with a year-over-year decline of 1.3% in overall Ethernet switch revenues and market share of 45.4%. Meanwhile, Cisco’s combined service provider and enterprise router revenue grew 10.7% year over year with enterprise router revenue increasing 14.1% and SP revenues increasing 8.7%. Cisco’s combined SP and enterprise router market share stands at 37.5% in the quarter.

Huawei’s Ethernet switch revenue increased 11.4% on an annualized basis in 3Q21 giving the company market share of 10.7%. The company’s combined SP and enterprise router revenue increased 4.0% year over year giving the company a market share of 28.1%.

Arista Networks saw its Ethernet switch revenues increase 23.0% in 3Q21, bringing its share of the total market to 7.3%.

H3C’s Ethernet switch revenue increased 18.6% year over year giving the company market share of 6.2% in the quarter. In the combined service provider and enterprise routing market, H3C’s revenues grew 31.3%, giving the company a 2.2% market share.

HPE‘s Ethernet switch revenue increased 23.6% year over year in 3Q21, giving the company a market share of 5.8%.

Juniper‘s Ethernet switch revenue, which includes the company’s cloud-managed, enterprise campus Mist portfolio as well as its EX and QFX switch portfolios, increased 25.6% year over year in 3Q21, bringing its Ethernet switch market share to 3.2%. Juniper saw an 11.0% decline in combined enterprise and SP router sales, bringing its market share in the router market to 10.0%.

“Results in the Ethernet switch market were generally strong across the globe, indicating that most regions of the world continue to recover from the COVID-19 pandemic that caused decreased spending on network infrastructure,” noted Petr Jirovsky, research director, IDC Networking Trackers. “The growth in the third quarter of 2021 compared to the same period in 2019 indicates strong fundamentals for the market, which is a positive sign for the future.”

The Worldwide Quarterly Ethernet Switch Tracker and the Worldwide Quarterly Router Tracker provide total market size and vendor shares for the Ethernet switch and router technologies in an easy-to-use Excel pivot table format. The geographic coverage for both the Ethernet switch market and the router market includes nine major regions (USA, Canada, Latin America, People’s Republic of China, Asia/Pacific (excluding Japan & China), Japan, Western Europe, Central and Eastern Europe, and Middle East and Africa) and 60 countries. The Ethernet switch market is further segmented by speed (100Mb, 1000Mb, 2.5Gb/5Gb, 10Gb, 25Gb/50Gb, 50Gb, 100Gb, 200Gb/400Gb), product (fixed managed, fixed unmanaged, modular), and layer (Ethernet switch, ADC). Measurement for the Ethernet switch market is provided in vendor revenue, value, and port shipments. The router market is further split by product (high-end, mid-range, low-end, SOHO), deployment (service provider, enterprise), connectivity (core, edge), and the measurements are in vendor revenue, value, and unit shipments.

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,100 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 110 countries. IDC’s analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly owned subsidiary of International Data Group (IDG), the world’s leading tech media, data, and marketing services company. To learn more about IDC, please visit www.idc.com. Follow IDC on Twitter at @IDC and LinkedIn. Subscribe to the IDC Blog for industry news and insights.

Samsung and Viettel launch 5G RAN trial in Da Nang, Vietnam

Samsung has launched a commercial trial of its 5G radio access network technology with Viettel in Vietnam. The network operator will use Samsung’s advanced 5G solutions to power its commercial network and to enable users in Da Nang to “experience the full benefits of 5G services. The companies will verify the high-performance and advanced capabilities made possible by Samsung’s 4G and 5G network solutions,” Samsung said in this statement.

“Viettel has continued to prioritize building 5G infrastructure in key areas of the city,” said Tao Duc Thang, Deputy General Director from Viettel. “Viettel will join hands to make smart city development in Da Nang more synchronous and modern, to connect broadband in multi-dimensional and safe ways, ensuring best network infrastructure for digital government development, supporting for business and growth of Da Nan,” Tao added.

Viettel is Vietnam’s largest telecom operator. Its 4G infrastructure covers 97% of the Vietnamese population. The company also provided the first 5G service in Vietnam.

Currently, 11 provinces/cities of Vietnam have 5G Viettel coverage (including Hanoi, Bac Ninh, Bac Giang, Vinh Phuc, Dong Nai, Ho Chi Minh City, Ba Ria–Vung Tau, Binh Phuoc, Thua Thien–Hue and Da Nang). People in these areas can experience 5G for free with unlimited capacity, on many 5G support devices. The 5G Viettel network in the above areas has a stable data download speed of 600-700 Mbps, the highest of up to more than 1Gbps.

For the commercial trial in Da Nang, Samsung provided its latest 4G and 5G solutions, which include its baseband unit as well as 64T64R Massive MIMO radios and radios on mid-band spectrum. Samsung’s latest baseband unit offers improved performance with industry leading capacity and throughput, while supporting both 4G and 5G technologies.

Samsung says its 64T64R 5G Massive MIMO radio has the capability to power highly-congested and populated areas, delivering increased coverage and data speeds for enhanced 5G end-user experiences.

“We are excited to work with Viettel to bring immersive and reliable 5G services to consumers, and demonstrate Samsung’s technical leadership in Vietnam. This trial marks a big first step for the two companies’ collaborative efforts in Vietnam,” said Ho Chi Dung, Vice President, Network Business, Samsung VINA. “We look forward to supporting Viettel with a network that is ready to unlock the future of mobile connectivity in Vietnam, and that brings a new level of 5G experiences to the country’s increasing number of mobile users.”

Samsung has successfully delivered 5G end-to-end solutions including chipsets, radios and core. Through ongoing research and development, Samsung drives the industry to advance 5G networks with its market-leading product portfolio from fully virtualized RAN and Core to private network solutions and AI-powered automation tools. The company is currently providing network solutions to mobile operators that deliver connectivity to hundreds of millions of users around the world.

References:

https://news.samsung.com/global/samsung-and-viettel-to-launch-5g-commercial-trial-in-da-nang-vietnam

https://www.channelasia.tech/article/693891/viettel-kicks-off-da-nang-5g-trials-samsung/

Globe Telecom and Linksys deploy dual band mesh WiFi 6 system

Philippines network operator Globe Telecom has partnered with Linksys, a provider of home and business WiFi services, to provide Globe At Home subscribers with Linksys’ Atlas Pro 6 Dual-Band Mesh WiFi 6 system.

All Globe At Home subscribers can now pre-order the Linksys WiFi 6 Mesh device. Powered by Velop Intelligent Mesh, this dual-band WiFi 6 router is designed to allow more than 30 devices to connect across three bedrooms. It is best recommended for subscribers to Globe At Home’s Unli Fiber Up 70 Mbps plan and up, the operator added.

Globe customers can take up the Linksys Atlas Pro 6 (MX5502 – two units) for PHP 1,099 per month or for a one-time payment of PHP 19,995. For a limited time only, every pre-order will come with a bonus Samsung SmartThings camera worth PHP 5,500, Globe said.

“As a company whose mission is to give Filipinos the tools they need to keep winning in life despite all the challenges we face, we are always on the lookout for emerging technologies that can help us do just this,” says Barbie Dapul, Vice President for Marketing of Globe At Home. “From our improved unli, fiber internet plans to Globe Streamwatch 2-in-1 Entertainment Box, and now the Linksys Atlas Pro 6 WiFi Mesh, all of our efforts are geared towards turning Filipino houses into powerhouses; homes that are capable of enriching familial bonds and at the same time, fulfilling dreams.”

The Linksys Atlas Pro 6 makes so much sense especially in the post-pandemic setting with the internet becoming more central in people’s lives and the home becoming a central venue for work, school, gaming, and family entertainment. The WiFi 6 competency is designed to deliver gigabit WiFi speeds to every corner of the home, including balconies and outdoor areas, offering the best home mesh WiFi coverage to date.

“With more people working from home, and attending school online, home networks are becoming increasingly constrained, especially when used for video or other streaming applications,” said Kingsley Chan, Business Development Director, Linksys. “The new Linksys Atlas Pro 6 is designed to address this and provides all of the heavy WiFi lifting at a reasonable price.”

Access to 160 MHz unleashes the true power of WiFi 6 technology—the least-congested channels on the 5 GHz band offer incredibly fast connectivity. Faster peak data rates allow work-from-home, online learning, streaming, and gaming devices to operate simultaneously without diminished bandwidth. Meanwhile, advanced security and parental controls all add to the essentiality of this upgrade to any home.

Additional Features and Benefits

- 4X Faster Speed than WiFi 5, Powerful WiFi 6 Mesh Coverage: WiFi 6 sends and receives multiple streams of data simultaneously, providing up to 4X more WiFi capacity to handle more mobile, streaming, gaming, and smart home devices.

- Increased WiFi Range by 50%: Expands WIFI coverage up and lessens dead spots.

- Ultra-Low Latency: Faster WiFi performance for lag-free online gaming and HD streaming to any device, providing 4X more speed compared to WiFi 5.

- Easy set-up and WIFI controls with Linksys app let you access your network from anywhere, and view or prioritize which connected devices are using the most WiFi.

References:

https://www.globe.com.ph/about-us/newsroom/consumer/better-wider-wifi-globe-at-home-linksys.html

For more information, please visit shop.globe.com.ph/linksys-atlas-pro6-pre-order. You can also download the Globe At Home app and follow Globe At Home on Facebook.

https://www.linksys.com/us/velop/

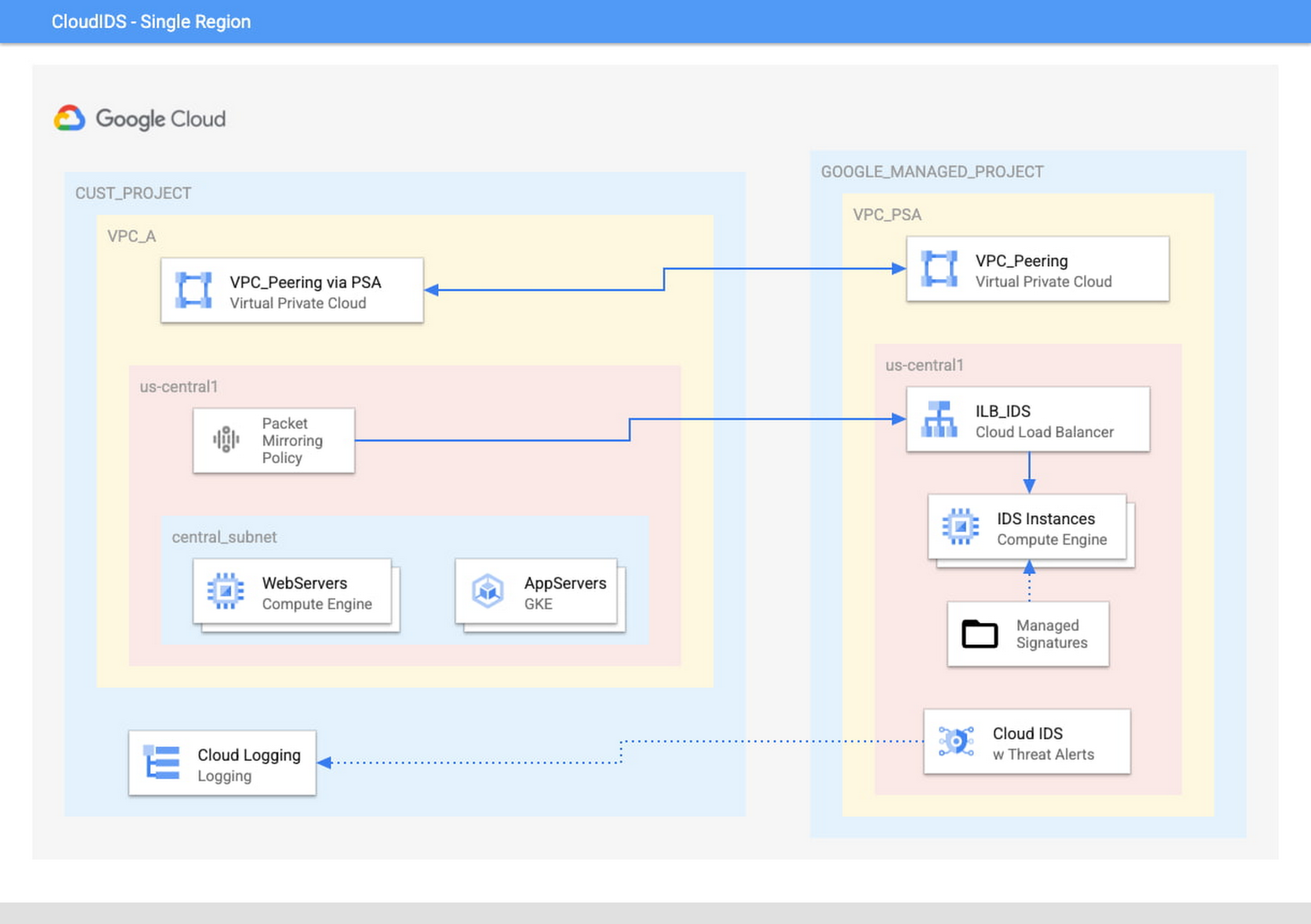

Google Cloud Intrusion Detection System (IDS) now available worldwide

As more and more applications move to the cloud, cloud network security teams have to keep them secure against an ever-evolving threat landscape. Shielding applications against network threats is also one of the most important criteria for regulatory compliance. To address these challenges, many cloud network security teams build their own complex network threat detection solutions based on open source or third-party IDS components. These customized solutions can be difficult and costly to operate, and they often lack the scalability that is required to protect dynamic cloud applications.

To meet this challenge, Google Cloud has announced the general availability of Google Cloud Intrusion Detection System (IDS) – a cloud-native managed network security solution, where key security capabilities are continuously engineered into our trusted cloud platform. This core network security offering helps detect network-based threats and helps organizations meet compliance standards that call for the use of an intrusion detection system.

Cloud IDS is built with Palo Alto Networks’ industry-leading threat detection technologies, providing high levels of security efficacy that enable you to detect malicious activity with few false positives. The general availability release includes these enhancements:

- Service availability in all regions

- Auto-scaling available in all regions

- Detection signatures automatically updated daily

- Support for customers’ HIPAA compliance requirements (under the Google Cloud HIPAA Business Associate Agreement)

- ISO27001 certification (and in the audit process to support customers’ PCI-DSS compliance requirements by year end)

- Integration with Chronicle, Google’s security analytics platform, to help organizations investigate threats surfaced by Cloud IDS.

Managed network threat detection with full traffic visibility:

Cloud IDS delivers cloud-native, managed, network-based threat detection. It features simple setup and deployment, and gives customers visibility into traffic entering their cloud environment (north-south traffic) and into traffic between workloads (east-west traffic). Cloud IDS empowers security teams to focus their resources on high priority issues instead of designing and operating complex network threat detection solutions.4

“Cloud IDS delivers cloud-native, managed, network-based threat detection. It features simple setup and deployment, and gives customers visibility into traffic entering their cloud environment (north-south traffic) and into traffic between workloads (east-west traffic). Cloud IDS empowers security teams to focus their resources on high priority issues instead of designing and operating complex network threat detection solutions,” according to Google.

“Google Cloud customers will be able to deploy on-demand application visibility and threat detection between workloads or containers in any Google Cloud virtual private cloud (VPC) to support their compliance goals and protect applications,” said Palo Alto Networks Senior Vice President Muninder Singh Sambi in a separate post.

Google Cloud VPC threat detection preceding Google Cloud IDS was limited in its scope, he said. It was also complex to design and implement, and—most crucially for cloud-native businesses—couldn’t scale dynamically to handle cloud bursting events, which are necessary to handle peaks in IT demand.

“Until now, detecting threats in traffic between workloads within the trust boundary of a VPC has been a significant hurdle for cloud network security teams, leading to compliance challenges and blind spots for the Security Operations Center (SOC),” he said.

“The Palo Alto Networks ML-powered threat analysis engine processes over 15 trillion transactions per day, automatically collected from across our global network of firewalls and endpoint agents. The result is 4.3 million unique security updates made per day to ensure you’re covered against the latest threats,” Sambi added.

Google Cloud IDS comes at at time when hyper-scalers, including Google, Amazon and Microsoft, are rapidly increasing their global Wide Area Network (WAN) reach. Businesses are increasingly turning to the public cloud and multi-cloud as more companies pivot to being cloud-native or at least cloud-adjacent.

In December Google announced plans to move into Germany, Israel, and Saudi Arabia with new cloud regions planned for 2022. Those join 29 cloud regions and 88 zones already in use.

Cloud IDS is now available in all regions. It provides protection against malware, virus and spyware, command and control (C2) attacks, and vulnerabilities such as buffer overflow and illegal code execution attacks. Auto-scaling capability dynamically adjusts Cloud IDS as needed when your traffic throughput changes so that you can automatically keep up with your scale needs. Threat signature updates are applied daily so you can stay ahead of the new threat variants. You can now use Chronicle to investigate the threats surfaced in Cloud IDS. With Chronicle’s integration, you can store and analyze Cloud IDS threat logs along with all your security telemetry data in one place so that you can effectively investigate and respond to threats at scale.

Google has patented their IDS, which is defined as follows:

An intrusion detection system for detection of intrusion or attempted intrusion by an unauthorized party or entity to a computer system or network, the intrusion detection system comprising means for monitoring the activity relative to the computer system or network, means for receiving and storing one or more general rules, each of the general rules being representative of characteristics associated with a plurality of specific instances of intrusion or attempted intrusion, and matching means for receiving data relating to activity relative to said computer system or network from the monitoring means and for comparing, in a semantic manner, sets of actions forming the activity against the one or more general rules to identify an intrusion or attempted intrusion. Inductive logic techniques are proposed for suggesting new intrusion detection rules for inclusion into the system, based on examples of sinister traffic.

References:

https://www.paloaltonetworks.com/blog/2021/07/google-cloud-network-threat-detection/

https://patents.google.com/patent/WO2003090046A2

Google Cloud IDS simplifies virtual private cloud network threat detection

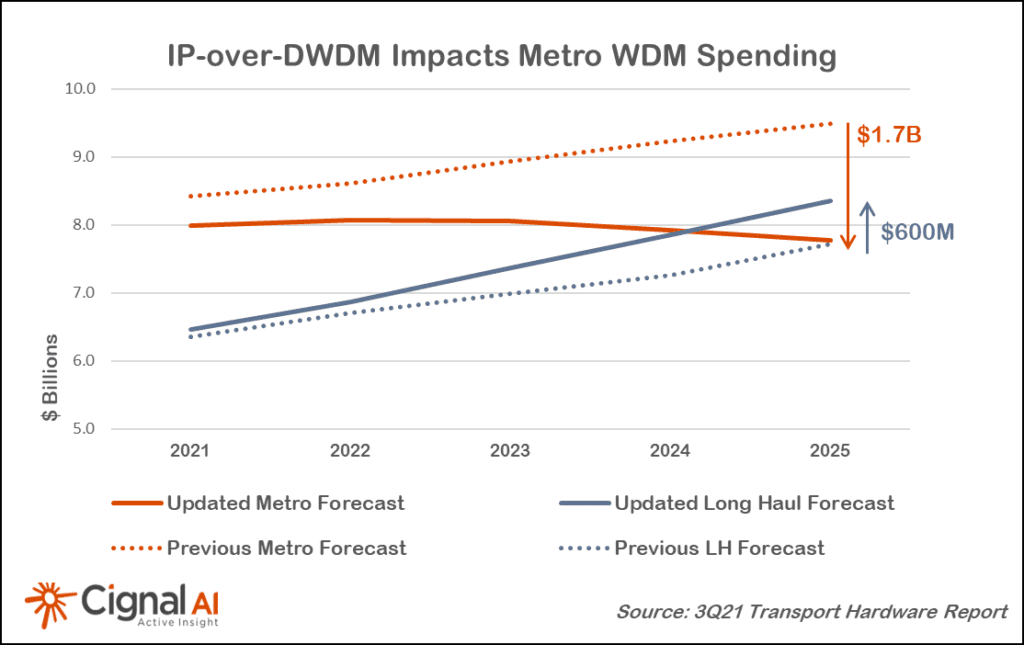

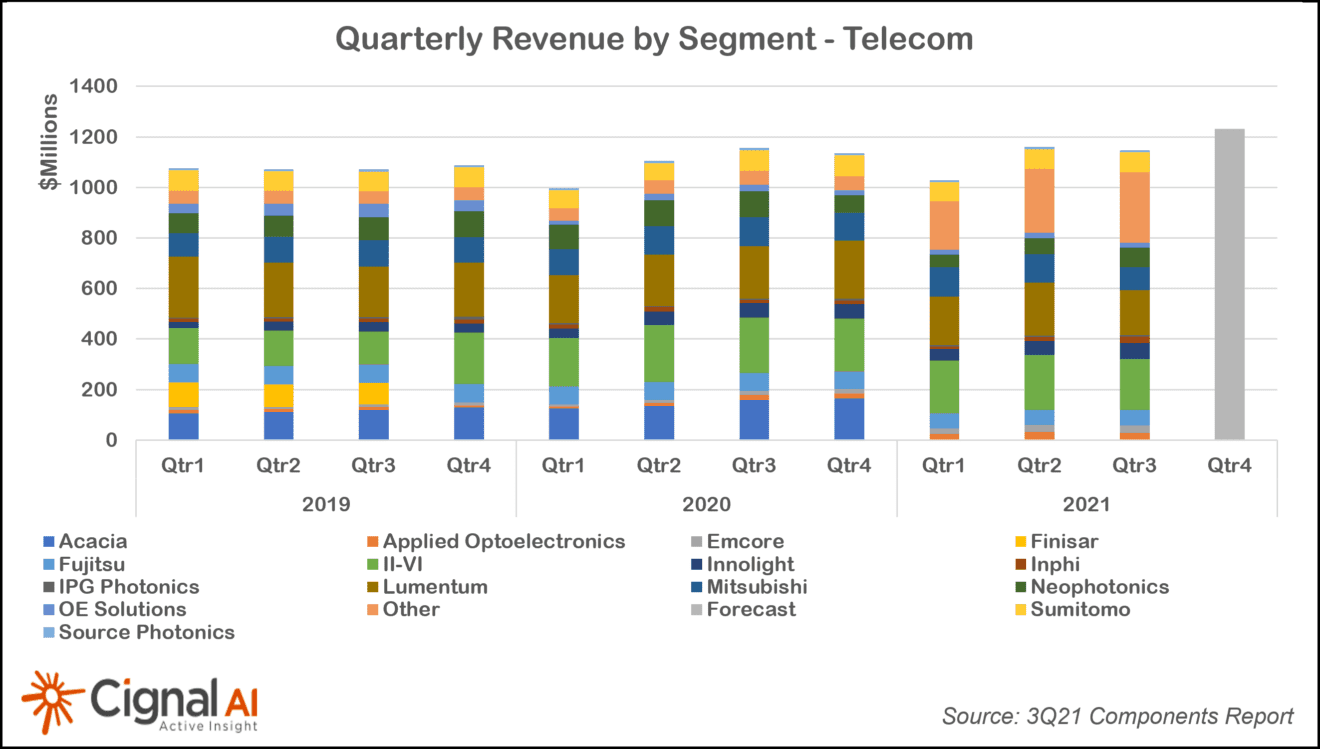

Cignal AI: Metro WDM forecast cut; IP-over-DWDM and Coherent Pluggables to impact market

Optical transport equipment deployment faces increasing headwinds as a broad number of network operators embrace IP-over-DWDM in Metro WDM applications, according to the most recent Transport Hardware Report from research firm Cignal AI. The impact of IP-over-DWDM on capex is expected to be moderate until 2023 when implementation of the new approach gathers momentum.

“IP-over-DWDM is a concept two decades old, but technical compromises, operational challenges, and high cost have prevented its widespread adoption. Gen60C 400ZR/ZR+ pluggable optics can solve these problems with availability well-timed to the 400 Gigabit Ethernet investment cycle,” said Kyle Hollasch, Lead Analyst for Transport Hardware at Cignal AI. “Hyperscale data center interconnect will drive early volumes, but service providers – who are responsible for 75% of optical CAPEX – should get on board in 2023 as the cost savings of IP-over-DWDM becomes impossible to ignore.”

| Cignal AI has cut forecasted spending on standalone optical transport hardware by $1.1B in 2025 as operators introduce pluggable coherent optics into routing and switching equipment to replace standalone traditional and compact modular equipment. This decline will be partially offset by greater sales of IP Routing and Switching hardware, open line systems, and long haul WDM, as well as direct sales of coherent optics to hyperscale operators. Clients can read 400ZR IPoDWDM Market Impact and Forecast for more detail. |

| Additional 3Q21 Transport Hardware Report Findings: |

- Total transport hardware (Optical and IP Switching & Routing) revenue declined -2.5%, with sales in China declining double digits for the second consecutive quarter.

- North American optical revenue grew for the 4th consecutive quarter and registered its first quarter of YoY growth since COVID impacted 2Q20. Fujitsu and Cisco led in revenue growth.

- Sales of optical hardware in EMEA increased YoY as the region registered its 6th consecutive quarter of growth. Regional market leaders Huawei and Nokia declined while ADVA, Infinera, and ZTE grew double digits.

- North American packet transport sales grew 6%, its third straight quarter of growth. Nokia and Cisco led this growth.

- Japanese packet sales continued to grow, up nearly 10% YoY. Cisco increased its lead in the region, with YoY sales growth of 42%.

Dell’Oro: SD-WAN market grew 45% YoY; Frost & Sullivan: Fortinet wins SD-WAN leadership award

According to a recently published report by Dell’Oro Group, the worldwide SD-WAN market grew 45% in the third quarter of 2021 compared to the prior year. Cisco maintained the top position for the revenue share for the quarter and was followed by Fortinet and VMware in the second and third spots.

“Enterprises are upgrading network infrastructures at accelerated rates compared to pre-pandemic times, and our research finds that the SD-WAN market is growing at strong double-digit rates in all regions of the world,” said Shin Umeda, Vice President at Dell’Oro Group. “Because SD-WAN is software-based technology, the global supply chain disruptions have had less of an effect compared to hardware-based networking products,” added Umeda.

Additional highlights from the 3Q 2021 SD-WAN Report:

- The SD-WAN market continues to consolidate around a small number of vendors with the top six vendors accounting for 69 percent market share in 3Q 2021.

- Cisco’s quarterly SD-WAN revenue nearly doubled in 3Q 2021 with especially strong growth in the North America region.

- The market for hardware-based Access Routers grew quarterly revenues for the first time in almost two years.

The Dell’Oro Group SD-WAN & Enterprise Router Quarterly Report offers complete, in-depth coverage of the SD-WAN and Enterprise Router markets for future current and historical periods. The report includes qualitative analysis and detailed statistics for manufacture revenue by regions, customer types, and use cases, average selling prices, and unit and port shipments. To purchase these reports, please contact us by email at [email protected].

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, networks, and data center IT markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions. For more information, contact Dell’Oro Group at +1.650.622.9400 or visit www.delloro.com.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Separately, Frost & Sullivan recently analyzed the global SD-WAN vendor market, and recognized Fortinet with the 2021 Global SD-WAN Vendor Product Leadership Award for transforming and securing the WAN. Fortinet’s Security-driven Networking approach to SD-WAN enables a wide range of use cases including secure and optimized connections to cloud-based applications. The company’s Secure SD-WAN solution integrates SD-WAN capabilities, advanced routing functions, next-generation firewall (NGFW), and zero trust network access (ZTNA) proxy on a single appliance or a single virtual machine (VM) to deliver secure networking capability. The solution can be deployed in a virtual or physical format on-premise or as a VM in the cloud, with a throughput of 20 Gbps, the highest available in the industry.

Fortinet’s Secure SD-WAN solution, powered by the industry’s first SOC4 SD-WAN ASIC [1.] for accelerated performance, features an unrestricted WAN bandwidth consumption model on appliances that is unique in the industry. Cloud adoption continues to grow, but enterprises have generally struggled to implement and maintain a secure, high-performing WAN that allows for efficient access to cloud-based applications across their user base. With the rise in remote working and with distributed users accessing cloud-hosted applications, the enterprise perimeter is no longer limited to users within the company site. Fortinet’s solution securely connects users to cloud-based applications delivering consistent policies off- and on-network.

Note 1. On Apr 9, 2019 John Maddison, EVP of product and solutions, Fortinet said:

“The WAN edge is now a part of digital attack surfaces, but the edge of your network must never be a bottleneck. For branch offices, the ability to provide best-of-breed WAN Edge — including SD-WAN, WAN optimization, security and orchestration — with optimal performance and security is critical to enable the digital experience. Fortinet’s SoC4 SD-WAN ASIC allows organizations to realize security-driven networking whether they have 100 or 10,000 branch offices.”

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Roopa Honnachari, VP of Research, Network Services & Edge, explained that “Fortinet has been a long-time leader in the network security market, which has enabled them to deliver a solution that tightly knits advanced security features with SD-WAN. Though Fortinet is best known as a security company, they have shown their strength and innovation in networking as one of the top SD-WAN solutions on the market capable of supporting enterprise digital transformation.”

To break the perception that it is a security vendor that also does SD-WAN and to eliminate the risk of not appealing to enterprise infrastructure or network decision makers, the company has consciously focused on highlighting its routing and networking capabilities in marketing activities and proofs of concept.”

With its focus on SD-WAN with integrated advanced security and ability to deliver multiple functions in a single hardware appliance or VM, Fortinet has experienced significant growth in the last three years. The company sells 100% through channel partners, including large telcos, such as AT&T, Verizon, British Telecom, Masergy, GTT, KDDI, Orange, and Windstream, that are looking to add secure SD-WAN to their portfolios. As a result, Fortinet has nearly doubled its revenue.

Honnachari added that “Fortinet has emerged as a formidable competitor in the enterprise secure networking space. While the company has always served as a leading competitor in the network security space, the transformation to adding SD-WAN, NGFW, ZTNA access proxy, and advanced routing capabilities on a single operating system and managed by a single console is highly commendable.”

Gartner’s Magic Quadrant for WAN Edge Infrastructure

Cisco is a leader in this Magic Quadrant. It has two branded offerings: Cisco SD-WAN powered by Viptela and Cisco SD-WAN powered by Meraki. Both include hardware and software appliances, and associated orchestration and management. Cisco also provides optional additional security via the Cisco Umbrella Security Internet Gateway (SIG) platform. Cisco is based in California, U.S., and has more than 40,000 WAN edge customers. The vendor operates globally and addresses customers of all sizes, in all verticals. We expect the vendor to continue to invest in this market, particularly in the areas of improved self-healing capabilities, new consumption-based pricing models and integrated security to enable a single-vendor SASE offering.

Fortinet is a leader in this Magic Quadrant. Its offering is the FortiGate Secure SD-WAN product, which includes physical, virtual appliances and cloud-based services managed with FortiManager orchestrator. Fortinet is based in Sunnyvale, California, U.S., and Gartner estimates that it has more than 34,000 WAN edge customers with more than 10,000 SD-WAN customers. FortiOS v.7.0 combines ZTNA to its broad WAN and network security functionalities to deliver a capable SASE offering. It has a wide global presence, addressing customers across multiple verticals and sizes. We expect the vendor to continue investing in SASE, artificial intelligence for IT operations (AIOps) and 5G functionality.

VMware is a leader in this Magic Quadrant. Its offering is branded as VMware SD-WAN, and is part of VMware SASE. The offering includes edge appliances (hardware and software), gateways — VMware points of presence (POPs) offering various services — and an orchestrator and its Edge Network Intelligence. VMware provides additional optional security via VMware Cloud Web Security and VMware Secure Access. Based in California, U.S., it has more than 14,000 SD-WAN customers. The vendor operates globally and addresses customers of all sizes, and in all verticals. Gartner expects the vendor to continue investments in this market, including enhancing options for remote workers and building out its SASE offering.

………………………………………………………………………………………………………………………

Each year, Frost & Sullivan presents this award to the company that has developed a product with innovative features and functionality that is gaining rapid market acceptance. The award recognizes the quality of the solution and the customer value enhancements it enables.

About Frost & Sullivan:

For six decades, Frost & Sullivan has been world-renowned for its role in helping investors, corporate leaders, and governments navigate economic changes and identify disruptive technologies, Mega Trends, new business models, and companies to action, resulting in a continuous flow of growth opportunities to drive future success. Contact us: Start the discussion. Contact us: Start the discussion.

Contact: Bianca Torres

P: 1.210.477.8418

E: [email protected]

References:

https://www.gartner.com/doc/reprints?id=1-27EGPR7B&ct=210909&st=sb