Open AI raises $8.3B and is valued at $8.3B; AI speculative mania rivals Dot-com bubble

According to the Financial Times (FT), OpenAI (the inventor of Chat GPT) has raised another $8.3 billion in a massively over-subscribed funding round, including $2.8 billion from Dragoneer Investment Group, a San Francisco-based technology-focused fund. Please use the sharing tools found via the share button at the top or side of articles. Copying articles to share with others is a breach of FT.com T&Cs and Copyright Policy. Email [email protected] to buy additionLeading VCs that also participated included Founders Fund, Sequoia Capital, Andreessen Horowitz, Coatue Management, Altimeter Capital, D1 Capital Partners, Tiger Global and Thrive Capital, according to the people with knowledge of the deal. The Chat GPT private company is now valued at $300 billion.

OpenAI’s annual recurring revenue has surged to $12bn, according to a person with knowledge of OpenAI’s finances, and the group is set to release its latest model, GPT-5, this month.

OpenAI is in the midst of complex negotiations with Microsoft that will determine its corporate structure. Rewriting the terms of the pair’s current contract, which runs until 2030, is seen as a prerequisite to OpenAI simplifying its structure and eventually going public. The two companies have yet to agree on key issues such as how long Microsoft will have access to OpenAI’s intellectual property. Another sticking point is the future of an “AGI clause”, which allows OpenAI’s board to declare that the company has achieved a breakthrough in capability called “artificial general intelligence,” which would then end Microsoft’s access to new models.

An additional risk is the increasing competition from rivals such as Anthropic — which is itself in talks for a multibillion-dollar fundraising — and is also in a continuing legal battle with Elon Musk. The FT also reported that Amazon is set to increase its already massive investment in Anthropic.

OpenAI CEO Sam Altman. The funding forms part of a round announced in March that values the ChatGPT maker at $300bn © Yuichi Yamazaki/AFP via Getty Images

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

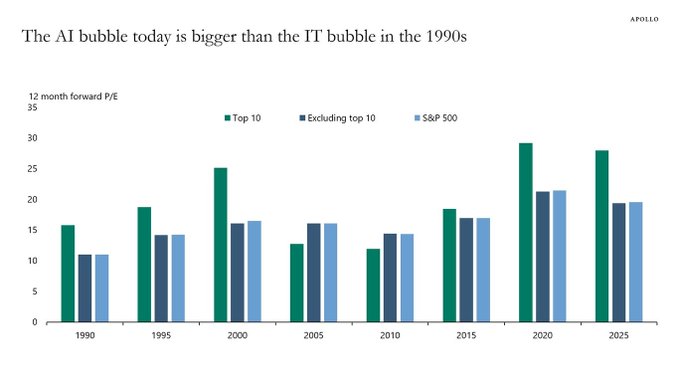

While AI is the transformative technology of this generation, comparisons are increasingly being made with the Dot-com bubble. 1999 saw such a speculative frenzy for anything with a ‘.com’ at the end that valuations and stock markets reached unrealistic and clearly unsustainable levels. When that speculative bubble burst, the global economy fell into an extended recession in 2001-2002. As a result, analysts are now questioning the wisdom of the current AI speculative bubble and fearing dire consequences when it eventually bursts. Just as with the Dot-com bubble, AI revenues are nowhere near justifying AI company valuations, especially for private AI companies that are losing tons of money (see Open AI losses detailed below).

Torsten Slok, Partner and Chief Economist at Apollo Global Management via ZERO HEDGE on X: “The difference between the IT bubble in the 1990s and the AI bubble today is that the top 10 companies in the S&P 500 today (including Nvidia, Microsoft, Amazon, Google, and Meta) are more overvalued than the IT companies were in the 1990s.”

AI private companies may take a lot longer to reach the lofty profit projections institutional investors have assumed. Their reliance on projected future profits over current fundamentals is a dire warning sign to this author. OpenAI, for example, faces significant losses and aggressive revenue targets to become profitable. OpenAI reported an estimated loss of $5 billion in 2024, despite generating $3.7 billion in revenue. The company is projected to lose $14 billion in 2026 while total projected losses from 2023 to 2028 are expected to reach $44 billion.

Other AI bubble data points (publicly traded stocks):

- The proportion of the S&P 500 represented by the 10 largest companies is significantly higher now (almost 40%) compared to 25% in 1999. This indicates a more concentrated market driven by a few large technology companies deeply involved in AI development and adoption.

- Investment in AI infrastructure has reportedly exceeded the spending on telecom and internet infrastructure during the dot-com boom and continues to grow, suggesting a potentially larger scale of investment in AI relative to the prior period.

- Some indices tracking AI stocks have demonstrated exceptionally high gains in a short period, potentially surpassing the rates of the dot-com era, suggesting a faster build-up in valuations.

- The leading hyperscalers, such as Amazon, Microsoft, Google, and Meta, are investing vast sums in AI infrastructure to capitalize on the burgeoning AI market. Forecasts suggest these companies will collectively spend $381 billion in 2025 on AI-ready infrastructure, a significant increase from an estimated $270 billion in 2024.

Check out this YouTube video: “How AI Became the New Dot-Com Bubble”

References:

https://www.ft.com/content/76dd6aed-f60e-487b-be1b-e3ec92168c11

https://www.telecoms.com/ai/openai-funding-frenzy-inflates-the-ai-bubble-even-further

https://x.com/zerohedge/status/1945450061334216905

AI spending is surging; companies accelerate AI adoption, but job cuts loom large

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Canalys & Gartner: AI investments drive growth in cloud infrastructure spending

AI Echo Chamber: “Upstream AI” companies huge spending fuels profit growth for “Downstream AI” firms

Huawei launches CloudMatrix 384 AI System to rival Nvidia’s most advanced AI system

Gen AI eroding critical thinking skills; AI threatens more telecom job losses

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Emerging Cybersecurity Risks in Modern Manufacturing Factory Networks

By Omkar Ashok Bhalekar with Ajay Lotan Thakur

Introduction

With the advent of new industry 5.0 standards and ongoing advancements in the field of Industry 4.0, the manufacturing landscape is facing a revolutionary challenge which not only demands sustainable use of environmental resources but also compels us to make constant changes in industrial security postures to tackle modern threats. Technologies such as Internet of Things (IoT) in Manufacturing, Private 4G/5G, Cloud-hosted applications, Edge-computing, and Real-time streaming telemetry are effectively fueling smart factories and making them more productive.

Although this evolution facilitates industrial automation, innovation and high productivity, it also greatly makes the exposure footprint more vulnerable for cyberattacks. Industrial Cybersecurity is quintessential for mission critical manufacturing operations; it is a key cornerstone to safeguard factories and avoid major downtimes.

With the rapid amalgamation of IT and OT (Operational Technology), a hack or a data breach can cause operational disruptions like line down situations, halt in production lines, theft or loss of critical data, and huge financial damage to an organization.

Industrial Networking

Why does Modern Manufacturing demand Cybersecurity? Below outlines a few reasons why cybersecurity is essential in modern manufacturing:

- Convergence of IT and OT: Industrial control systems (ICS) which used to be isolated or air-gapped are now all inter-connected and hence vulnerable to breaches.

- Enlarged Attack Surface: Every device or component in the factory which is on the network is susceptible to threats and attacks.

- Financial Loss: Cyberattacks such as WannaCry or targeted BSOD Blue Screen of Death (BSOD) can cost millions of dollars per minute and result in complete shutdown of operations.

- Disruptions in Logistics Network: Supply chain can be greatly disarrayed due to hacks or cyberattacks causing essential parts shortage.

- Legislative Compliance: Strict laws and regulations such as CISA, NIST, and ISA/IEC 62443 are proving crucial and mandating frameworks to safeguard industries

It is important to understand and adapt to the changing trends in the cybersecurity domain, especially when there are several significant factors at risk. Historically, it has been observed that mankind always has had some lessons learned from their past mistakes while not only advances at fast pace, but the risks from external threats would limit us from making advancements without taking cognizance.

This attitude of adaptability or malleability needs to become an integral part of the mindset and practices in cybersecurity spheres and should not be limited to just industrial security. Such practices can scale across other technological fields. Moreover, securing industries does not just mean physical security, but it also opens avenues for cybersecurity experts to learn and innovate in the field of applications and software such as Manufacturing Execution System (MES) which are crucial for critical operations.

Greatest Cyberattacks in Manufacturing of all times:

Familiarizing and acknowledging different categories of attacks and their scales which have historically hampered the manufacturing domain is pivotal. In this section we would highlight some of the Real-World cybersecurity incidents.

Ransomware (Colonial Pipeline, WannaCry, y.2021):

These attacks brought the US east coast to a standstill due to extreme shortage of fuel and gasoline after hacking employee credentials.

Cause: The root cause for this was compromised VPN account credentials. An VPN account which wasn’t used for a long time and lacked Multi-factor Authentication (MFA) was breached and the credentials were part of a password leak on dark web. The Ransomware group “Darkside” exploited this entry point to gain access to Colonial Pipeline’s IT systems. They did not initially penetrate operational technology systems. However, the interdependence of IT and OT systems caused operational impacts. Once inside, attackers escalated privileges and exfiltrated 100 GB of data within 2 hours. Ransomware was deployed to encrypt critical business systems. Colonial Pipeline proactively shut down the pipeline fearing lateral movement into OT networks.

Effect: The pipeline, which supplies nearly 45% of the fuel to the U.S. East Coast, was shut down for 6 days. Mass fuel shortages occurred across several U.S. states, leading to public panic and fuel hoarding. Colonial Pipeline paid $4.4 million ransom. Later, approximately $2.3 million was recovered by the FBI. Led to a Presidential Executive Order on Cybersecurity and heightened regulations around critical infrastructure cybersecurity. Exposed how business IT network vulnerabilities can lead to real-world critical infrastructure impacts, even without OT being directly targeted.

Industrial Sabotage (Stuxnet, y.2009):

This unprecedented and novel software worm was able to hijack an entire critical facility and sabotage all the machines rendering them defunct.

Cause: Nation-state-developed malware specifically targeting Industrial Control Systems (ICS), with an unprecedented level of sophistication. Stuxnet was developed jointly by the U.S. (NSA) and Israel (Unit 8200) under operation “Olympic Games”. The target was Iran’s uranium enrichment program at Natanz Nuclear Facility. The worm was introduced via USB drives (air-gapped network). Exploited four zero-day vulnerabilities in Windows systems at that time, unprecedented. Specifically targeted Siemens Step7 software running on Windows, which controls Siemens S7-300 PLCs. Stuxnet would identify systems controlling centrifuges used for uranium enrichment. Reprogrammed the PLCs to intermittently change the rotational speed of centrifuges, causing mechanical stress and failure, while reporting normal operations to operators. Used rootkits for both Windows and PLC-level to remain stealthy.

Effect: Destroyed approximately 1,000 IR-1 centrifuges (~10% of Iran’s nuclear capability). Set back Iran’s nuclear program by 1-2 years. Introduced a new era of cyberwarfare, where malware caused physical destruction. Raised global awareness about the vulnerabilities in industrial control systems (ICS). Iran responded by accelerating its cyber capabilities, forming the Iranian Cyber Army. ICS/SCADA security became a top global priority, especially in energy and defense sectors.

Upgrade spoofing (SolarWinds Orion Supply chain Attack, y.2020):

Attackers injected malicious pieces of software into the software updates which infected millions of users.

Cause: Compromise of the SolarWinds build environment leading to a supply chain attack. Attackers known as Russian Cozy Bear, linked to Russia’s foreign intelligence agency, gained access to SolarWinds’ development pipeline. Malicious code was inserted into Orion Platform updates, released between March to June 2020 Customers who downloaded the update installed malware known as SUNBURST. Attackers compromised SolarWinds build infrastructure. It created a backdoor in Orion’s signed DLLs. Over 18,000 customers were potentially affected, including 100 high-value targets. After the exploit, attackers used manual lateral movement, privilege escalation, and custom C2 (command-and-control) infrastructure to exfiltrate data.

Effect: Breach included major U.S. government agencies: DHS, DoE, DoJ, Treasury, State Department, and more. Affected top corporations: Cisco, Intel, Microsoft, FireEye, and others FireEye discovered the breach after noticing unusual two-factor authentication activity. Exposed critical supply chain vulnerabilities and demonstrated how a single point of compromise could lead to nationwide espionage. Promoted the creation of Cybersecurity Executive Order 14028, Zero Trust mandates, and widespread adoption of Software Bill of Materials (SBOM) practices.

Spywares (Pegasus, y.2016-2021):

Cause: Zero-click and zero-day exploits leveraged by NSO Group’s Pegasus spyware, sold to governments. Pegasus can infect phones without any user interaction also known as zero-click exploits. It acquires malicious access to WhatsApp, iMessage or browsers like Safari’s vulnerabilities on iOS, including zero-days attacks on Android devices. Delivered via SMS, WhatsApp messages, or silent push notifications. Once installed, it provides complete surveillance capability such as access to microphones, camera, GPS, calls, photos, texts, and encrypted apps. Zero-click iOS exploit ForcedEntry allows complete compromise of an iPhone. Malware is extremely stealthy, often removing itself after execution. Bypassed Apple’s BlastDoor sandbox and Android’s hardened security modules.

Effect: Used by multiple governments to surveil activists, journalists, lawyers, opposition leaders, even heads of state. The 2021 Pegasus Project, led by Amnesty International and Forbidden Stories, revealed a leaked list of 50,000 potential targets. Phones of high-profile individuals including international journalists, associates, specifically French president, and Indian opposition figures were allegedly targeted which triggered legal and political fallout. NSO Group was blacklisted by the U.S. Department of Commerce. Apple filed a lawsuit against NSO Group in 2021. Renewed debates over the ethics and regulation of commercial spyware.

Other common types of attacks:

Phishing and Smishing: These attacks send out links or emails that appear to be legitimate but are crafted by bad actors for financial means or identity theft.

Social Engineering: Shoulder surfing though sounds funny; it’s the tale of time where the most expert security personnel have been outsmarted and faced data or credential leaks. Rather than relying on technical vulnerabilities, this attack targets human psychology to gain access or break into systems. The attacker manipulates people into revealing confidential information using techniques such as Reconnaissance, Engagement, Baiting or offering Quid pro quo services.

Security Runbook for Manufacturing Industries:

To ensure ongoing enhancements to industrial security postures and preserve critical manufacturing operations, following are 11 security procedures and tactics which will ensure 360-degree protection based on established frameworks:

A. Incident Handling Tactics (First Line of Defense) Team should continuously improve incident response with the help of documentation and response apps. Co-ordination between teams, communications root, cause analysis and reference documentation are the key to successful Incident response.

B. Zero Trust Principles (Trust but verify) Use strong security device management tools to ensure all end devices are in compliance such as trusted certificates, NAC, and enforcement policies. Regular and random checks on users’ official data patterns and assign role-based policy limiting full access to critical resources.

C. Secure Communication and Data Protection Use endpoint or cloud-based security session with IPSec VPN tunnels to make sure all traffic can be controlled and monitored. All user data must be encrypted using data protection and recovery software such as BitLocker.

D. Secure IT Infrastructure Hardening of network equipment such switches, routers, WAPs with dot1x, port-security and EAP-TLS or PEAP. Implement edge-based monitoring solutions to detect anomalies and redundant network infrastructure to ensure least MTTR.

E. Physical Security Locks, badge readers or biometric systems for all critical rooms and network cabinets are a must. A security operations room (SOC) can help monitor internal thefts or sabotage incidents.

F. North-South and East-West Traffic Isolation Safety traffic and external traffic can be rate limited using Firewalls or edge compute devices. 100% isolation is a good wishful thought, but measures need to be taken to constantly monitor any security punch-holes.

G. Industrial Hardware for Industrial applications Use appropriate Industrial grade IP67 or IP68 rated network equipment to avoid breakdowns due to environmental factors. Localized industrial firewalls can provide desired granularity on the edge thereby skipping the need to follow Purdue model.

H. Next-Generation Firewalls with Application-Level Visibility Incorporate Stateful Application Aware Firewalls, which can help provide more control over zones and policies and differentiate application’s behavioral characteristics. Deploy Tools which can perform deep packet inspection and function as platforms for Intrusion prevention (IPS/IDS).

I. Threat and Traffic Analyzer Tools such as network traffic analyzers can help achieve network Layer1-Layer7 security monitoring by detecting and responding to malicious traffic patterns. Self-healing networks with automation and monitoring tools which can detect traffic anomalies and rectify the network incompliance.

J. Information security and Software management Companies must maintain a repo of trust certificates, software and releases and keep pushing regular patches for critical bugs. Keep a constant track of release notes and CVEs (Common Vulnerabilities and exposures) for all vendor software.

K. Idiot-Proofing (How to NOT get Hacked) Regular training to employees and familiarizing them with cyber-attacks and jargons like CryptoJacking or HoneyNets can help create awareness. Encourage and provide a platform for employees or workers to voice their opinions and resolve their queries regarding security threats.

Current Industry Perspective and Software Response

In response to the escalating tide of cyberattacks in manufacturing, from the Triton malware striking industrial safety controls to LockerGoga shutting down production at Norsk Hydro, there has been a sea change in how the software industry is facilitating operational resilience. Security companies are combining cutting-edge threat detection with ICS/SCADA systems, delivering purpose-designed solutions like zero-trust network access, behavior-based anomaly detection, and encrypted machine-to-machine communications. Companies such as Siemens and Claroty are leading the way, bringing security by design rather than an afterthought. A prime example is Dragos OT-specific threat intelligence and incident response solutions, which have become the focal point in the fight against nation-state attacks and ransomware operations against critical infrastructure.

Bridging the Divide between IT and OT: Two way street

With the intensification of OT and IT convergence, perimeter-based defense is no longer sufficient. Manufacturers are embracing emerging strategies such as Cybersecurity Mesh Architecture (CSMA) and applying IT-centric philosophies such as DevSecOps within the OT environment to foster secure by default deployment habits. The trend also brings attention to IEC 62443 conformity as well as NIST based risk assessment frameworks catering to manufacturing. Legacy PLCs having been networked and exposed to internet-borne threats, companies are embracing micro-segmentation, secure remote access, and real-time monitoring solutions that unify security across both environments. Learn how Schneider Electric is empowering manufacturers to securely link IT/OT systems with scalable cybersecurity programs.

Conclusion

In a nutshell, Modern manufacturing, contrary to the past, is not just about quick input and quick output systems which can scale and be productive, but it is an ecosystem, where cybersecurity and manufacturing harmonize and just like healthcare system is considered critical to humans, modern factories are considered quintessential to manufacturing. So many experiences with cyberattacks on critical infrastructure such as pipelines, nuclear plants, power-grids over the past 30 years not only warrant world’s attention but also calls to action the need to devise regulatory standards which must be followed by each and every entity in manufacturing.

As mankind keeps making progress and sprinting towards the next industrial revolution, it’s an absolute exigency to emphasize making Industrial Cybersecurity a keystone in building upcoming critical manufacturing facilities and building a strong foundation for operational excellency. Now is the right time to buy into the trend of Industrial security, sure enough the leaders who choose to be “Cyberfacturers” will survive to tell the tale, and the rest may just serve as stark reminders of what happens when pace outperforms security.

References

- https://www.cisa.gov/topics/industrial-control-systems

- https://www.nist.gov/cyberframework

- https://www.isa.org/standards-and-publications/isa-standards/isa-standards-committees/isa99

- https://www.cisa.gov/news-events/news/attack-colonial-pipeline-what-weve-learned-what-weve-done-over-past-two-years

- https://www.law.georgetown.edu/environmental-law-review/blog/cybersecurity-policy-responses-to-the-colonial-pipeline-ransomware-attack/

- https://www.hbs.edu/faculty/Pages/item.aspx?num=63756

- https://spectrum.ieee.org/the-real-story-of-stuxnet

- https://www.washingtonpost.com/world/national-security/stuxnet-was-work-of-us-and-israeli-experts-officials-say/2012/06/01/gJQAlnEy6U_story.html

- https://www.kaspersky.com/resource-center/definitions/what-is-stuxnet

- https://www.malwarebytes.com/stuxnet

- https://www.zscaler.com/resources/security-terms-glossary/what-is-the-solarwinds-cyberattack

- https://www.gao.gov/blog/solarwinds-cyberattack-demands-significant-federal-and-private-sector-response-infographic

- https://www.rapid7.com/blog/post/2020/12/14/solarwinds-sunburst-backdoor-supply-chain-attack-what-you-need-to-know/

- https://www.fortinet.com/resources/cyberglossary/solarwinds-cyber-attack

- https://www.amnesty.org/en/latest/research/2021/07/forensic-methodology-report-how-to-catch-nso-groups-pegasus/

- https://citizenlab.ca/2023/04/nso-groups-pegasus-spyware-returns-in-2022/

- https://thehackernews.com/2023/04/nso-group-used-3-zero-click-iphone.html

- https://www.securityweek.com/google-says-nso-pegasus-zero-click-most-technically-sophisticated-exploit-ever-seen/

- https://www.nist.gov/itl/smallbusinesscyber/guidance-topic/phishing

- https://www.blumira.com/blog/social-engineering-the-human-element-in-cybersecurity

- https://www.nist.gov/cyberframework

- https://www.dragos.com/cyber-threat-intelligence/

- https://mesh.security/security/what-is-csma/

- https://download.schneider-electric.com/files?p_Doc_Ref=IT_OT&p_enDocType=User+guide&p_File_Name=998-20244304_Schneider+Electric+Cybersecurity+White+Paper.pdf

- https://insanecyber.com/understanding-the-differences-in-ot-cybersecurity-standards-nist-csf-vs-62443/

- https://blog.se.com/sustainability/2021/04/13/it-ot-convergence-in-the-new-world-of-digital-industries/

About Author:

Omkar Bhalekar is a senior network engineer and technology enthusiast specializing in Data center architecture, Manufacturing infrastructure, and Sustainable solutions with extensive experience in designing resilient industrial networks and building smart factories and AI data centers with scalable networks. He is also the author of the Book Autonomous and Predictive Networks: The future of Networking in the Age of AI and co-author of Quantum Ops – Bridging Quantum Computing & IT Operations. Omkar writes to simplify complex technical topics for engineers, researchers, and industry leaders.

China gaining on U.S. in AI technology arms race- silicon, models and research

Introduction:

According to the Wall Street Journal, the U.S. maintains its early lead in AI technology with Silicon Valley home to the most popular AI models and the most powerful AI chips (from Santa Clara based Nvidia and AMD). However, China has shown a willingness to spend whatever it takes to take the lead in AI models and silicon.

The rising popularity of DeepSeek, the Chinese AI startup, has buoyed Beijing’s hopes that it can become more self-sufficient. Huawei has published several papers this year detailing how its researchers used its homegrown AI chips to build large language models without relying on American technology.

“China is obviously making progress in hardening its AI and computing ecosystem,” said Michael Frank, founder of think tank Seldon Strategies.

AI Silicon:

Morgan Stanley analysts forecast that China will have 82% of AI chips from domestic makers by 2027, up from 34% in 2024. China’s government has played an important role, funding new chip initiatives and other projects. In July, the local government in Shenzhen, where Huawei is based, said it was raising around $700 million to invest in strengthening an “independent and controllable” semiconductor supply chain.

During a meeting with President Xi Jinping in February, Huawei Chief Executive Officer Ren Zhengfei told Xi about “Project Spare Tire,” an effort by Huawei and 2,000 other enterprises to help China’s semiconductor sector achieve a self-sufficiency rate of 70% by 2028, according to people familiar with the meeting.

……………………………………………………………………………………………………………………………………………

AI Models:

Prodded by Beijing, Chinese financial institutions, state-owned companies and government agencies have rushed to deploy Chinese-made AI models, including DeepSeek [1.] and Alibaba’s Qwen. That has fueled demand for homegrown AI technologies and fostered domestic supply chains.

Note 1. DeepSeek’s V3 large language model matched many performance benchmarks of rival AI programs developed in the U.S. at a fraction of the cost. DeepSeek’s open-weight models have been integrated into many hospitals in China for various medical applications.

In recent weeks, a flurry of Chinese companies have flooded the market with open-source AI models, many of which are claiming to surpass DeepSeek’s performance in certain use cases. Open source models are freely accessible for modification and deployment.

The Chinese government is actively supporting AI development through funding and policy initiatives, including promoting the use of Chinese-made AI models in various sectors.

Meanwhile, OpenAI’s CEO Sam Altman said his company had pushed back the release of its open-source AI model indefinitely for further safety testing.

AI Research:

China has taken a commanding lead in the exploding field of artificial intelligence (AI) research, despite U.S. restrictions on exporting key computing chips to its rival, finds a new report.

The analysis of the proprietary Dimensions database, released yesterday, finds that the number of AI-related research papers has grown from less than 8500 published in 2000 to more than 57,000 in 2024. In 2000, China-based scholars produced just 671 AI papers, but in 2024 their 23,695 AI-related publications topped the combined output of the United States (6378), the United Kingdom (2747), and the European Union (10,055).

“U.S. influence in AI research is declining, with China now dominating,” Daniel Hook, CEO of Digital Science, which owns the Dimensions database, writes in the report DeepSeek and the New Geopolitics of AI: China’s ascent to research pre-eminence in AI.

In 2024, China’s researchers filed 35,423 AI-related patent applications, more than 13 times the 2678 patents filed in total by the U.S., the U.K., Canada, Japan, and South Korea.

References:

https://www.wsj.com/tech/ai/how-china-is-girding-for-an-ai-battle-with-the-u-s-5b23af51

Huawei launches CloudMatrix 384 AI System to rival Nvidia’s most advanced AI system

U.S. export controls on Nvidia H20 AI chips enables Huawei’s 910C GPU to be favored by AI tech giants in China

Goldman Sachs: Big 3 China telecom operators are the biggest beneficiaries of China’s AI boom via DeepSeek models; China Mobile’s ‘AI+NETWORK’ strategy

Gen AI eroding critical thinking skills; AI threatens more telecom job losses

Softbank developing autonomous AI agents; an AI model that can predict and capture human cognition

AI spending is surging; companies accelerate AI adoption, but job cuts loom large

Big Tech and VCs invest hundreds of billions in AI while salaries of AI experts reach the stratosphere

ZTE’s AI infrastructure and AI-powered terminals revealed at MWC Shanghai

Deloitte and TM Forum : How AI could revitalize the ailing telecom industry?

Ericsson completes Aduna joint venture with 12 telcos to drive network API adoption

Today, Ericsson announced the completion of the equity investments by twelve global communication service providers (CSPs) into its subsidiary Aduna, formally establishing Aduna as a 50:50 joint venture. Aduna was created to combine and sell aggregated network Application Programming Interfaces (APIs) globally. It has been operational since the deal signed on 11 September 2024. Aduna is now owned by AT&T, Bharti Airtel, Deutsche Telekom, Ericsson, KDDI, Orange, Reliance Jio, Singtel, Telefonica, Telstra, T-Mobile, Verizon and Vodafone.

The network APIs, based on the CAMARA open source project of the GSMA and Linux Foundation, are designed to enable network operators to offer services such as service level assurance, fraud prevention and authentication programmatically to application developers, similar to how those same application developers can easily spin up cloud compute instances on cloud providers like Google Cloud and Microsoft Azure. For telcos and other network operators, network APIs promise the potential to leverage 5G networks for new business models and revenue streams.

The Aduna ecosystem includes additional CSPs worldwide, as well as major developer platform companies, global system integration (GSI) companies, communication platform-as-a-service (CPaaS) companies, and independent software vendor (ISV) companies. To date these include: e& (in UAE -formerly Etisalat), Bouygues Telecom, Free, CelcomDigi, Softbank, NTT DOCOMO, Google Cloud, Vonage, Sinch, Infobip, Enstream, Bridge Alliance, Syniverse, JT Global, Microsoft, Wipro and Tech Mahindra – each playing a vital role in advancing the reach and impact of network APIs worldwide.

Former Vonage COO Anthony Bartolo, became Aduna CEO this past January. He said in a statement:

“The closing of the transaction is another important step for Aduna. In just ten months we have built an impressive ecosystem comprising the biggest names in telecoms and the wider ICT industry. The closing provides renewed motivation for Aduna to accelerate the adoption of network APIs by developers on a global scale. This includes encouraging more telecom operators to join the new company, further driving the industry and developer experience.”

………………………………………………………………………………………………………………………………………………………………………………………………………….

A Febuary 2024 McKinsey article stated:

Network APIs are the interlocking puzzle pieces that connect applications to one another and to telecom networks. As such, they are critical to companies seamlessly tapping into 5G’s powerful capabilities for hundreds of potential use cases, such as credit card fraud prevention, glitch-free videoconferencing, metaverse interactions, and entertainment. If developers have access to the right network APIs, enterprises can create 5G-driven applications that leverage features like speed on demand, low-latency connections, speed tiering, and edge compute discovery.

In addition to enhancing today’s use cases, network APIs can lay the foundation for entirely new ones. Remotely operated equipment, semi-autonomous vehicles in production environments, augmented reality gaming, and other use cases could create substantial value in a broad range of industries. By enabling these innovations, telecom operators can position themselves as essential partners to enterprises seeking to accelerate their digital transformations.

Over the next five to seven years, we estimate the network API market could unlock around $100 billion to $300 billion in connectivity- and edge-computing-related revenue for operators while generating an additional $10 billion to $30 billion from APIs themselves. But telcos won’t be the only ones vying for this lucrative pool. In fact, with the market structure currently in place, they would cede as much as two-thirds of the value creation to other players in the ecosystem, such as cloud providers and API aggregators—repeating the industry’s frustrating experience of the past two decades.

……………………………………………………………………………………………………………………………………………………………………………………………………………..

Telecom API Market Size and Forecast 2025 to 2034 by Precedence Research:

The global telecom API market size was estimated at USD 252.10 billion in 2024 and is anticipated to reach around USD 1741.39 billion by 2034, expanding at a CAGR of 21.32% from 2025 to 2034.

Aduna Global can potentially scale network APIs across regions, and maybe even globally, Leonard Lee, executive analyst at neXt Curve, told Fierce Network. Aduna can potentially help deliver trust and regulatory clients that network APIs need for widespread adoption. Aduna itself won’t directly offer services Aduna partners such as JT Global, Vonage and AWS already offer fraud prevention services that leverage relevant security and authentication-related network APIs, Lee said.

“You won’t likely see Aduna Global offer a fraud prevention service,” he added. “You need to look at Vonage, Infobip, Tech Mahindra and the like to offer these solutions that will likely be accessible to developers through APIs.”

……………………………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://www.ericsson.com/en/press-releases/2025/7/ericsson-announces-completion-of-aduna-transaction

New venture to sell Network Application Programming Interfaces (APIs) on a global scale

https://www.precedenceresearch.com/telecom-api-market

Telefónica and Nokia partner to boost use of 5G SA network APIs

Countdown to Q-day: How modern-day Quantum and AI collusion could lead to The Death of Encryption

By Omkar Ashok Bhalekar with Ajay Lotan Thakur

Behind the quiet corridors of research laboratories and the whir of supercomputer data centers, a stealth revolution is gathering force, one with the potential to reshape the very building blocks of cybersecurity. At its heart are qubits, the building blocks of quantum computing, and the accelerant force of generative AI. Combined, they form a double-edged sword capable of breaking today’s encryption and opening the door to an era of both vast opportunity and unprecedented danger.

Modern Cryptography is Fragile

Modern-day computer security relies on the un-sinking complexity of certain mathematical problems. RSA encryption, introduced for the first time in 1977 by Rivest, Shamir, and Adleman, relies on the principle that factorization of a 2048-bit number into primes is computationally impossible for ordinary computers (RSA paper, 1978). Also, Diffie-Hellman key exchange, which was described by Whitfield Diffie and Martin Hellman in 1976, offers key exchange in a secure manner over an insecure channel based on the discrete logarithm problem (Diffie-Hellman paper, 1976). Elliptic-Curve Cryptography (ECC) was described in 1985 independently by Victor Miller and Neal Koblitz, based on the hardness of elliptic curve discrete logarithms, and remains resistant to brute-force attacks but with smaller key sizes for the same level of security (Koblitz ECC paper, 1987).

But quantum computing flips the script. Thanks to algorithms like Shor’s Algorithm, a sufficiently powerful quantum computer could factor large numbers exponentially faster than regular computers rendering RSA and ECC utterly useless. Meanwhile, Grover’s Algorithm provides symmetric key systems like AES with a quadratic boost.

What would take millennia or centuries to classical computers, quantum computers could boil down to days or even hours with the right scale. In fact, experts reckon that cracking RSA-2048 using Shor’s Algorithm could take just 20 million physical qubits which is a number that’s diminishing each year.

Generative AI adds fuel to the fire

While quantum computing threatens to undermine encryption itself, generative AI is playing an equally insidious but no less revolutionary role. By mass-producing activities such as the development of malware, phishing emails, and synthetic identities, generative AI models, large language models, and diffusion-based visual synthesizers, for example, are lowering the bar on sophisticated cyberattacks.

Even worse, generative AI can be applied to model and experiment with vulnerabilities in implementations of cryptography, including post-quantum cryptography. It can be employed to assist with training reinforcement learning agents that optimize attacks against side channels or profile quantum circuits to uncover new behaviors.

With quantum computing on the horizon, generative AI is both a sophisticated research tool and a player to watch when it comes to weaponization. On the one hand, security researchers utilize generative AI to produce, examine, and predict vulnerabilities in cryptography systems to inform the development of post-quantum-resistant algorithms. Meanwhile, it is exploited by malicious individuals for their ability to automate the production of complex attack vectors like advanced malware, phishing attacks, and synthetic identities radically reducing the barrier to conducting high impact cyberattacks. This dual-use application of generative AI radically shortens the timeline for adversaries to take advantage of breached or transitional cryptographic infrastructures, practically bridging the window of opportunity for defenders to deploy effective quantum-safe security solutions.

Real-World Implications

The impact of busted cryptography is real, and it puts at risk the foundations of everyday life:

1. Online Banking (TLS/HTTPS)

When you use your bank’s web site, the “https” in the address bar signifies encrypted communication over TLS (Transport Layer Security). Most TLS implementations rely on RSA or ECC keys to securely exchange session keys. A quantum attack would decrypt those exchanges, allowing an attacker to decrypt all internet traffic, including sensitive banking data.

2. Cryptocurrencies

Bitcoin, Ethereum, and other cryptocurrencies use ECDSA (Elliptic Curve Digital Signature Algorithm) for signing transactions. If quantum computers can crack ECDSA, a hacker would be able to forge signatures and steal digital assets. In fact, scientists have already performed simulations in which a quantum computer might be able to extract private keys from public blockchain data, enabling theft or rewriting the history of transactions.

3. Government Secrets and Intelligence Archives

National security agencies all over the world rely heavily on encryption algorithms such as RSA and AES to protect sensitive information, including secret messages, intelligence briefs, and critical infrastructure data. Of these, AES-256 is one that is secure even in the presence of quantum computing since it is a symmetric-key cipher that enjoys quantum resistance simply because Grover’s algorithm can only give a quadratic speedup against it, brute-force attacks remain gigantic in terms of resources and time. Conversely, asymmetric cryptographic algorithms like RSA and ECC, which underpin the majority of public key infrastructures, are fundamentally vulnerable to quantum attacks that can solve the hard mathematical problems they rely on for security.

Such a disparity offers a huge security gap. Information obtained today, even though it is in such excellent safekeeping now, might not be so in the future when sufficiently powerful quantum computers will be accessible, a scenario that is sometimes referred to as the “harvest now, decrypt later” threat. Both intelligence agencies and adversaries could be quietly hoarding and storing encrypted communications, confident that quantum technology will soon have the capability to decrypt this stockpile of sensitive information. The Snowden disclosures placed this threat in the limelight by revealing that the NSA catches and keeps vast amounts of global internet traffic, such as diplomatic cables, military orders, and personal communications. These repositories of encrypted data, unreadable as they stand now, are an unseen vulnerability; when Q-Day which is the onset of available, practical quantum computers that can defeat RSA and ECC, come around, confidentiality of decades’ worth of sensitive communications can be irretrievably lost.

Such a compromise would have apocalyptic consequences for national security and geopolitical stability, exposing classified negotiations, intelligence operations, and war plans to adversaries. Such a specter has compelled governments and security entities to accelerate the transition to post-quantum cryptography standards and explore quantum-resistant encryption schemes in an effort to safeguard the confidentiality and integrity of information in the era of quantum computing.

Arms Race Toward Post-Quantum Cryptography

In response, organizations like NIST are leading the development of post-quantum cryptographic standards, selecting algorithms believed to be quantum resistant. But migration is glacial. Implementing backfitting systems with new cryptographic foundations into billions of devices and services is a logistical nightmare. This is not a process of merely software updates but of hardware upgrades, re-certifications, interoperability testing, and compatibility testing with worldwide networks and critical infrastructure systems, all within a mode of minimizing downtime and security vulnerabilities.

Building such a large quantum computer that can factor RSA-2048 is an enormous task. It would require millions of logical qubits with very low error rates, it’s estimated. Today’s high-end quantum boxes have less than 100 operational qubits, and their error rates are too high to support complicated processes over a long period of time. However, with continued development of quantum correction methods, materials research, and qubit coherence times, specialists warn that effective quantum decryption capability may appear more quickly than the majority of organizations are prepared to deal with.

This convergence time frame, when old and new environments coexist, is where danger is most present. Attackers can use generative AI to look for these hybrid environments in which legacy encryption is employed, by botching the identification of old crypto implementations, producing targeted exploits en masse, and choreographing multi-step attacks that overwhelm conventional security monitoring and patching mechanisms.

Preparing for the Convergence

In order to be able to defend against this coming storm, the security strategy must evolve:

- Inventory Cryptographic Assets: Firms must take stock of where and how encryption is being used across their environments.

- Adopt Crypto-Agility: System needs to be designed so it can easily switch between encryption algorithms without full redesign.

- Quantum Test Threats: Use AI tools to stress-test quantum-like threats in encryption schemes.

Adopt PQC and Zero-Trust Models: Shift towards quantum-resistant cryptography and architectures with breach as the new default state.

In Summary

Quantum computing is not only a looming threat, it is a countdown to a new cryptographic arms race. Generative AI has already reshaped the cyber threat landscape, and in conjunction with quantum power, it is a force multiplier. It is a two-front challenge that requires more than incremental adjustment; it requires a change of cybersecurity paradigm.

Panic will not help us. Preparation will.

Abbreviations

RSA – Rivest, Shamir, and Adleman

ECC – Elliptic-Curve Cryptography

AES – Advanced Encryption Standard

TLS – Transport Layer Security

HTTPS – Hypertext Transfer Protocol Secure

ECDSA – Elliptic Curve Digital Signature Algorithm

NSA – National Security Agency

NIST – National Institute of Standards and Technology

PQC – Post-Quantum Cryptography

References

- https://arxiv.org/abs/2104.07603

- https://www.researchgate.net/publication/382853518_CryptoGenSec_A_Hybrid_Generative_AI_Algorithm_for_Dynamic_Cryptographic_Cyber_Defence

- https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5185525

- https://www.classiq.io/insights/shors-algorithm-explained

- https://www.theguardian.com/world/interactive/2013/nov/01/snowden-nsa-files-surveillance-revelations-decoded

- https://arxiv.org/abs/2307.00691

- https://secureframe.com/blog/generative-ai-cybersecurity

- https://www.techtarget.com/searchsecurity/news/365531559/How-hackers-can-abuse-ChatGPT-to-create-malware

- https://arxiv.org/abs/1802.07228

- https://www.technologyreview.com/2019/05/30/65724/how-a-quantum-computer-could-break-2048-bit-rsa-encryption-in-8-hours/

- https://arxiv.org/pdf/1710.10377

- https://thequantuminsider.com/2025/05/24/google-researcher-lowers-quantum-bar-to-crack-rsa-encryption/

- https://csrc.nist.gov/projects/post-quantum-cryptography

***Google’s Gemini is used in this post to paraphrase some sentences to add more context. ***

About Author:

Omkar Bhalekar is a senior network engineer and technology enthusiast specializing in Data center architecture, Manufacturing infrastructure, and Sustainable solutions with extensive experience in designing resilient industrial networks and building smart factories and AI data centers with scalable networks. He is also the author of the Book Autonomous and Predictive Networks: The future of Networking in the Age of AI and co-author of Quantum Ops – Bridging Quantum Computing & IT Operations. Omkar writes to simplify complex technical topics for engineers, researchers, and industry leaders.

Huawei launches CloudMatrix 384 AI System to rival Nvidia’s most advanced AI system

On Saturday, Huawei Technologies displayed an advanced AI computing system in China, as the Chinese technology giant seeks to capture market share in the country’s growing artificial intelligence sector. Huawei’s CloudMatrix 384 system made its first public debut at the World Artificial Intelligence Conference (WAIC), a three-day event in Shanghai where companies showcase their latest AI innovations, drawing a large crowd to the company’s booth.

The Huawei CloudMatrix 384 is a high-density AI computing system featuring 384 Huawei Ascend 910C chips, designed to rival Nvidia’s GB200 NVL72 (more below). The AI system employs a “supernode” architecture with high-speed internal chip interconnects. The system is built with optical links for low-latency, high-bandwidth communication. Huawei has also integrated the CloudMatrix 384 into its cloud platform. The system has drawn close attention from the global AI community since Huawei first announced it in April.

The CloudMatrix 384 resides on the super-node Ascend platform and uses high-speed bus interconnection capability, resulting in low latency linkage between 384 Ascend NPUs. Huawei says that “compared to traditional AI clusters that often stack servers, storage, network technology, and other resources, Huawei CloudMatrix has a super-organized setup. As a result, it also reduces the chance of facing failures at times of large-scale training.

Huawei staff at its WAIC booth declined to comment when asked to introduce the CloudMatrix 384 system. A spokesperson for Huawei did not respond to questions. However, Huawei says that “early reports revealed that the CloudMatrix 384 can offer 300 PFLOPs of dense BF16 computing. That’s double of Nvidia GB200 NVL72 AI tech system. It also excels in terms of memory capacity (3.6x) and bandwidth (2.1x).” Indeed, industry analysts view the CloudMatrix 384 as a direct competitor to Nvidia’s GB200 NVL72, the U.S. GPU chipmaker’s most advanced system-level product currently available in the market.

One industry expert has said the CloudMatrix 384 system rivals Nvidia’s most advanced offerings. Dylan Patel, founder of semiconductor research group SemiAnalysis, said in an April article that Huawei now had AI system capabilities that could beat Nvidia’s AI system. The CloudMatrix 384 incorporates 384 of Huawei’s latest 910C chips and outperforms Nvidia’s GB200 NVL72 on some metrics, which uses 72 B200 chips, according to SemiAnalysis. The performance stems from Huawei’s system design capabilities, which compensate for weaker individual chip performance through the use of more chips and system-level innovations, SemiAnalysis said.

Huawei has become widely regarded as China’s most promising domestic supplier of chips essential for AI development, even though the company faces U.S. export restrictions. Nvidia CEO Jensen Huang told Bloomberg in May that Huawei had been “moving quite fast” and named the CloudMatrix as an example.

Huawei says the system uses “supernode” architecture that allows the chips to interconnect at super-high speeds and in June, Huawei Cloud CEO Zhang Pingan said the CloudMatrix 384 system was operational on Huawei’s cloud platform.

According to Huawei, the Ascend AI chip-based CloudMatrix 384 with three important benefits:

- Ultra-large bandwidth

- Ultra-Low Latency

- Ultra-Strong Performance

These three perks can help enterprises achieve better AI training as well as stable reasoning performance for models. They could further retain long-term reliability.

References:

https://www.huaweicentral.com/huawei-launches-cloudmatrix-384-ai-chip-cluster-against-nvidia-nvl72/

https://semianalysis.com/2025/04/16/huawei-ai-cloudmatrix-384-chinas-answer-to-nvidia-gb200-nvl72/

U.S. export controls on Nvidia H20 AI chips enables Huawei’s 910C GPU to be favored by AI tech giants in China

Huawei’s “FOUR NEW strategy” for carriers to be successful in AI era

FT: Nvidia invested $1bn in AI start-ups in 2024

Intel to spin off its Networking & Edge Group into a stand-alone business

As originally reported by CRN, Intel revealed its plan to spin off its Network and Edge Group in a memo addressed to customers and said it will seek outside investment for the business unit. Intel will be an anchor investor in the stand-alone business. The memo, seen by CRN, was authored by Sachin Katti, who has led the Network and Edge Group, abbreviated as NEX, since early 2023. He was given the extra role of chief technology and AI officer by Intel CEO Lip-Bu Tan in April to lead the chipmaker’s AI strategy. An Intel spokesperson confirmed the contents of the memo to CRN.

“We plan to establish key elements of our Networking and Communications business as a stand-alone company and we have begun the process of identifying strategic investors,” the representative said in a statement. “Like Altera, we will remain an anchor investor enabling us to benefit from future upside as we position the business for future growth,” the spokesperson added.

The NEX spin-off plan was announced to Intel customers and employees the same day the semiconductor giant revealed more changes under Tan’s leadership, including a 15% workforce reduction and a more conservative approach to its foundry business. “We are laser-focused on strengthening our core product portfolio and our AI roadmap to better serve customers,” Tan said in a statement.

In Katti’s memo, he said Intel “internally announced” on Thursday its plan to “establish its NEX business as a stand-alone company.” This will result in a “new, independent entity focused exclusively on delivering leading silicon solutions for critical communications, enterprise networking and ethernet connectivity infrastructure,” he added.

Katti did not give a timeline for when Intel could spin off NEX, which has been mainly focused on networking and communications products after the company moved its edge computing business to the Client Computing Group last September. Intel also shifted its integrated photonics solutions to the Data Center Group that same month. Similar to other businesses Intel has spun off, the company plans to maintain a stake in the stand-alone NEX company as it seeks out other investors, according to Katti. “While Intel will remain an anchor investor in the new company, we have begun the process of identifying additional strategic and capital partners to support the growth and development of the new company,” he wrote.

Katti said the move is “rooted in our commitment to serving” Intel’s customers better and promised that there will be “no change in service or the support” they rely on. He added that it will also help NEX “expand into new segments more effectively. Backed by Intel, this new, independent company will be positioned to accelerate its customer-facing strategy and product road map by innovating faster and investing in new offerings.”

Katti said he expects the transition to be “seamless” for Intel’s customers. “What we expect to change is our ability to operate with greater focus, speed and flexibility—all to better meet your needs,” he wrote.

…………………………………………………………………………………………………………………………………………………..

Intel was rumored to be looking for a buyer for its Network and Edge group in May. This business produced $5.8 billion in revenue in 2024.

This strategy seems similar to the company’s decision to spin off RealSense, its former stereoscopic imaging technology business, earlier this month. Intel decided to spin RealSense out during former CEO Pat Gelsinger’s tenure and the company struck out on its own with $50 million in venture funding.

…………………………………………………………………………………………………………………………………………………..

Shortly after Tan became Intel’s CEO in March, the leader made clear that he would seek to spin off businesses he considers not core to its strategy. Then in May, Reuters reported that the company was exploring a sale of the NEX business unit as part of that plan.

While Tan didn’t reference Intel’s decision to spin off NEX in the company’s Thursday earnings call, he discussed other actions it has taken to monetize “non-core assets,” including the sale of a portion of Intel’s stake in Mobileye earlier this month.

The company is also expected to complete its majority stake sale of the Altera programmable chip business to private equity firm Silver Lake by late September, according to Tan. Silver Lake will gain a 51 percent stake in the business while Intel will own the remaining 49%. “I will evaluate other opportunities as we continue to sharpen our focus around our core business and strategy,” Tan said on the earnings call.

………………………………………………………………………………………………………………………………………………………….

In 2019, Apple acquired the majority of Intel’s smartphone modem business for $1 billion. This deal included approximately 2,200 Intel employees, intellectual property, equipment, leases, and over 17,000 wireless technology patents. The acquisition allowed Apple to accelerate its development of 5G modem technology for its iPhones, reducing reliance on third-party suppliers like Qualcomm. Intel, in turn, refocused its 5G efforts on areas like network infrastructure, PCs, and IoT devices

References:

https://www.crn.com/news/networking/2025/intel-reveals-plan-to-spin-off-networking-business-in-memo

https://techcrunch.com/2025/07/25/intel-is-spinning-off-its-network-and-edge-group/

https://www.lightreading.com/semiconductors/intel-sale-of-networks-sounds-like-an-ericsson-problem

CES 2025: Intel announces edge compute processors with AI inferencing capabilities

Massive layoffs and cost cutting will decimate Intel’s already tiny 5G network business

Nokia utilizes Intel technology to drive greater 5G SA core network energy savings

Nokia selects Intel’s Justin Hotard as new CEO to increase growth in IP networking and data center connections

T-Mobile’s growth trajectory increases: 5G FWA, Metronet acquisition and MVNO deals with Charter & Comcast

T-Mobile US is having a banner year. The “uncarrier” has again increased its annual earnings outlook, supported by the acquisition of fiber network operator Metronet and strong mobile customer growth in Q2. After gaining another 1.73 million postpaid customers in the quarter, T-Mobile now expects total postpaid net additions this year of 6.1-6.4 million, up from its previous guidance of 5.5-6.0 million. Postpaid customer growth strengthened compared to the first quarter and included 830,000 new phone customers and 902,000 other devices, while churn was little changed at 0.90 percent. Prepaid growth was more muted, with just 39,000 net additions. T-Mobile counted 132.778 million mobile customers at the end of June, up by around 1.9 million from a year ago. 5G broadband customers rose by 454,000 in the three months to 7.308 million.

In the three months to June, the company posted service revenues up 6% year-on-year to $17.4 billion, and core adjusted EBITDA (after leases) also was up 6% to $8.5 billion. The net profit rose 10 percent to a record $3.2 billion, and adjusted free cash flow increased 4% to $4.6 billion. Cash CAPEX rose 17.5 percent to $2.4 billion in Q2 and is still expected to reach $9.5 billion over the full year. The company also spent $2.5 billion buying back its own shares in Q2.

“T-Mobile crushed our own growth records with the best-ever total postpaid and postpaid phone nets in a Q2 in our history,” said Mike Sievert, CEO of T-Mobile. “T-Mobile is now America’s Best Network. When you combine that with the incredible value that we have always been famous for, it should surprise no one that customers are switching to the Un-carrier at a record pace. These durable advantages enabled us to once again translate customer growth into financial growth, with the industry’s best service revenue growth by a wide mile and record Q2 Adjusted Free Cash Flow.”

![]()

The new forecast includes the expected close of the Metronet acquisition on July 24th (today). The Metronet deal – crafted as a joint venture with KKR – will expand T-Mobile’s fiber reach by about 2 million homes across 17 states. It follows the completion of the deal with EQT to buy fiber operator Lumos.

T-Mobile plans to close the UScellular buyout and “become one team” on August 1st. “The combination gives us an expected 50% or more increase in capacity, in the combined footprint, and our site coverage will expand by a third from 9,000 to 12,000 sites,” CEO Mike Sievert said, noting that this will be in addition to 4,000 greenfield sites planned for this year, of which 1,000 have already been “lit up” to date.

T-Mobile stands at a critical juncture in its history, as it prepares to absorb more wireless and fiber assets, build a fiber network access business and enter a new market with the launch of T-Satellite in collaboration with Elon Musk’s Starlink. T-Mobile has already launched T-Mobile Fiber Home Internet and has forecast 100,000 fiber net customer adds in the second half of 2025 following the Lumos and Metronet deals. Sievert also reiterated that T-Mobile would continue to “keep an open mind” about any further fiber M&A.

T-Mobile is now the market’s fifth-largest ISP. Currently, the operator’s goals are to reach 12 million fixed wireless access subscribers by 2028 and to pass 12 million to 15 million households with fiber by the end of 2030, through both the fiber joint ventures and wholesale partnerships.

COO Srini Gopalan said on the earnings call, “We’re positioned to be a scale player in broadband,” claiming that the combined FWA and fiber targets would be equivalent to 40 million to 45 million homes passed as a broadband player, “and that’s before we go make other investments. As we’ve said before, we’re very open to looking at investments in fiber,” he added.

Separately, Charter Communications and Comcast announced Tuesday that they’ve cut a multi-year MVNO agreement with T-Mobile focused on their respective business customers. As the telecom industry growth rate is very low (real growth rate is barely positive), this additional source of revenue will be most welcome by the uncarrier. T-Mobile is expected to generate $850 million in incremental after tax income from its MVNO deals with Charter and Comcast. This revenue is included in the company’s updated guidance, but that guidance excludes the planned acquisition of UScellular assets.

T-Mobile Recognized as Network Leader by Third Parties:

- Ookla awarded T-Mobile as the only carrier in the country to win back-to-back Best Mobile Network awards in the largest, most-comprehensive tests of their kind, each leveraging half a billion real world data points on millions of devices measuring speed and experience

- Recognized by Opensignal for best Overall Experience for the fourth consecutive year and blew away the competition in best download speeds, nearly 200% faster than the nearest competitor, and upload speeds, approximately 65% faster than the nearest competitor

References:

https://www.lightreading.com/fttx/t-mobile-readies-for-the-next-stage-after-a-record-breaking-q2

Evercore: T-Mobile’s fiber business to boost revenue and achieve 40% penetration rate after 2 years

T-Mobile posts impressive wireless growth stats in 2Q-2024; fiber optic network acquisition binge to complement its FWA business

T-Mobile to acquire UScellular’s wireless operations in $4.4 billion deal

T-Mobile & EQT Joint Venture (JV) to acquire Lumos and build out T-Mobile Fiber footprint

T-Mobile US, Ericsson, and Qualcomm test 5G carrier aggregation with 6 component carriers

ITU-R WP5D IMT 2030 Submission & Evaluation Guidelines vs 6G specs in 3GPP Release 20 & 21

Like previous generations of international mobile telecommunications (IMT) recommendations, ITU-R defines the 6G terrestrial radio access network requirements while 3GPP develops the standardized technology specifications that will be the project’s candidate to the ITU-R process. The target date for “Technology proposals for IMT-2030 RIT/SRITs” has been defined by ITU-R to be early 2029, and resulting specifications (i.e. full system definition) are to be submitted by mid-2030 at the latest. 3GPP contributions to ITU-R WP 5D are made via ATIS – its North American partner standards organization. That is effectively how IMT 2020 RIT/SRIT became standardized in ITU-R M.2150 (5G RIT/SRITs).

At it’s July 2025 meeting in Japan, ITU-R WP 5D generated an outline of a working document that, when completed, will specify the requirements, evaluation criteria and submission templates for the development of IMT-2030 recommendation(s) sometime in 2030. The structure of this working document is based on Report ITU-R M.2411, and the sections and contents of each section are to be further discussed. This meeting also discussed 16 contributions on evaluation guidelines for IMT-2030 and that working document was updated

Meanwhile, 3GPP has concluded that two 3GPP Releases are needed to specify 6G: Release 20 for Studies and Release 21 for the normative work that will produce 6G specs. Technical studies on the 6G radio interface and 6G core network architecture within the RAN and SA Working Group to start in June 2025. Release 21 will be the official start of normative 6G work.

Juan Montojo, Qualcomm’s vice president of technical standards, told Light Reading that all of today’s 3GPP 6G contributors are committed. “I can say I’m very confident that every player that comes to the 3GPP is a full believer in the value of having a single, global standard,” he told Light Reading. “I’ve not seen any exception, or any [other] indication.” 3GPP Release 20 lays an important foundation for 6G, said Montojo in a blog post.

Huawei had way more delegates attending 3GPP 5G sessions than any other company which raised concerns that the company might exert undue influence on the development of 3GPP 5G specs to its advantage. However, it has now become much harder for companies from a particular region to dominate proceedings, according to Montojo. “There are very recent decisions where working group officials cannot all come from the same region,” he explained. The system has also been changed so that companies with operations in multiple geographies, such as Huawei and Qualcomm, cannot claim to be from any region except that of their headquarters, Montojo said.

Future 6G Patents:

While the standardization process remains open to new entrants, the likelihood is that 6G’s ultimate patent owners will be drawn heavily from the ranks of today’s 5G network equipment vendors, chipmakers and smartphone companies that actively participate at 3GPP and ITU-R meetings. Several independent assessments forecast that Qualcomm and Huawei will likely remain at or near the top for the forthcoming 6G related patents,. In January, a LexisNexis study ranked Huawei first in 5G based on patent ownership and standards contributions. A separate LexisNexis ranking called the Patent Asset Index, which attempted to score organizations based on the value of their patents, gave the top spot to Qualcomm. In 2024, patent licensing accounted for only 14% of Qualcomm’s revenues but ~39% of its pre-tax earnings.

- Huawei (China): Huawei holds a significant share of 5G patents and is actively developing 6G technology, according to Williams IP Law. They are also a strong contributor to 5G technical standards.

- Qualcomm (US): Qualcomm is evolving its research from 4G and 5G towards 6G, holding a notable percentage of global 5G patents. They are also a major player in software-defined network solutions for 6G.

- Samsung (South Korea): Samsung is a prominent player in 5G patent ownership and is leading efforts in 6G standardization, including chairing the ITU-R 6G Vision Group. They are also investing heavily in terahertz communication technologies for 6G.

- Ericsson (Sweden): Ericsson is recognized for its strong 5G patent portfolio and contributions to technical standards. They are actively engaged in 6G research and development, including collaborations and investments in areas like network compute fabric and trustworthy systems.

- Nokia (Finland): Nokia is another key player in 5G patent ownership and a significant contributor to 5G technical standards. They identified key technologies for 6G early on and are actively testing and setting 6G standards through collaborations and research labs.

Higher Spectrum Bands for 6G:

Much of the industry’s recent attention has been captured by the upper 6GHz band and the 7GHz to 15GHz range. Unfortunately, signals do not travel as far or penetrate walls and other obstacles as effectively in these higher bands. To compensate, 6G’s active antenna systems are set to include four times as many elements as today’s most advanced 5G technologies, according to Montojo.

“It is part of the requirement in 3GPP to reduce the site grid of the existing C-band,” he said. “You would not want to require a densification beyond the levels that we currently have but can actually guarantee reuse of the site grid of the C-band into these higher bands.” Some analysts, however, remain dubious. A so-called massive MIMO (multiple input, multiple output) radio loaded with an even bigger number of antennas is likely to be expensive, meaning the deployment of 6G for mass-market mobile services in higher spectrum bands might not be economically viable.

6G Core Network (3GPP only- no ITU involvement):

“The best-case scenario, and I would say default scenario, is that 6G radio will be connected to 6G core as basically the standards-based approach,” said Montojo. “What 6G core will be is TBD, but there is a lot of desire from the operator community to have a 6G core that is an evolved 5G core with some level, to be defined, of backwards compatibility.”

Here’s an AI generated speculation on the 6G core network to be specified by 3GPP in Release 21:

- AI and Machine Learning (ML) will be fundamental to the 6G core, moving beyond supplementary roles to become an inherent part of the network’s design and operation.

- Every network function may be AI-powered, enabling advanced decision-making, predictive maintenance, and real-time optimization.

- 6G core will be designed to support the full lifecycle of AI components, including data collection, model training, validation, deployment, and performance monitoring.

- Network slicing will evolve further in 6G, enabling even more flexible, customized, and isolated network slices tailored to the diverse requirements of emerging applications.

- The 6G core will likely leverage a streamlined, unified, and future-proof exposure framework, potentially building on the 3GPP Common API Framework (CAPIF), to enable new value creation and monetization opportunities through network service exposure to third parties.

- The 6G core will be designed with a strong focus on energy efficiency and sustainability, considering the growing demands and environmental impact of network operations.

- It will need to be resilient to handle high mobility conditions of devices across various networks and administrative domains, including terrestrial and non-terrestrial networks (NTNs) like satellites & drones.

- Security and trustworthiness will be paramount, requiring a strong emphasis on authentication, data privacy, integrity, and operational resilience.

- The 6G core will likely incorporate quantum-safe cryptography to address the threat of quantum computing.

- While many in the industry favor an evolutionary path building upon the 5G core, some in the Chinese telecom ecosystem have advocated for a completely new 6G core network architecture.

- This suggests a potential for divergence in the early stages of 6G development, with discussions and debates within 3GPP shaping the ultimate architectural choices.

In summary, the 6G core network to be specified by 3GPP is anticipated to be a highly intelligent, flexible, and efficient platform, deeply integrated with AI/ML, supporting diverse services through enhanced network slicing and exposure, while addressing critical challenges in security, sustainability, and global connectivity.

…………………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.3gpp.org/specifications-technologies/releases/release-20

The SA1 road to 6G: https://www.3gpp.org/news-events/3gpp-news/sa1-6g-road

Introduction to 3GPP Release 19 and 6G Planning – Contains an introduction to the preparation for 6G in 3GPP: https://atis.org/webinars/introduction-to-3gpp-release-19-and-6g-planning/

Advancing 5G towards 6G, TSDSI Workshops (Jan 2023): https://www.3gpp.org/news-events/partner-news/tsdsi-workshops

https://www.lightreading.com/6g/qualcomm-is-optimistic-geopolitics-won-t-tear-6g-apart

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

Highlights of 3GPP Stage 1 Workshop on IMT 2030 (6G) Use Cases

ITU-R: IMT-2030 (6G) Backgrounder and Envisioned Capabilities

ITU-R WP5D invites IMT-2030 RIT/SRIT contributions

NGMN issues ITU-R framework for IMT-2030 vs ITU-R WP5D Timeline for RIT/SRIT Standardization

IMT-2030 Technical Performance Requirements (TPR) from ITU-R WP5D

Draft new ITU-R recommendation (not yet approved): M.[IMT.FRAMEWORK FOR 2030 AND BEYOND]

IMT Vision – Framework and overall objectives of the future development of IMT for 2030 and beyond

Gen AI eroding critical thinking skills; AI threatens more telecom job losses

Two alarming research studies this year have drawn attention to the damage that Gen AI agents like ChatGPT are doing to our brains:

The first study, published in February, by Microsoft and Carnegie Mellon University, surveyed 319 knowledge workers and concluded that “while GenAI can improve worker efficiency, it can inhibit critical engagement with work and can potentially lead to long-term overreliance on the tool and diminished skills for independent problem-solving.”

An MIT study divided participants into three essay-writing groups. One group had access to Gen AI and another to Internet search engines while the third group had access to neither. This “brain” group, as MIT’s researchers called it, outperformed the others on measures of cognitive ability. By contrast, participants in the group using a Gen AI large language model (LLM) did the worst. “Brain connectivity systematically scaled down with the amount of external support,” said the report’s authors.

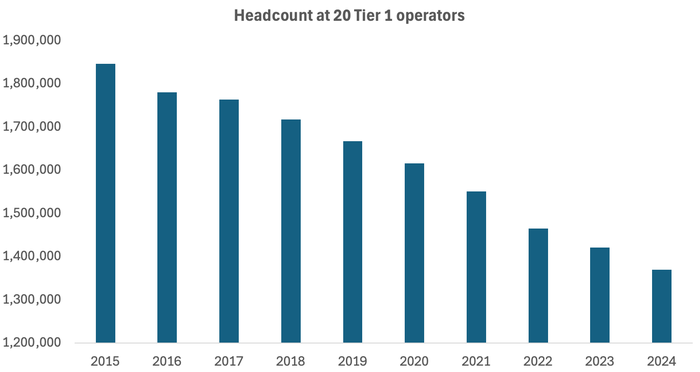

Across the 20 companies regularly tracked by Light Reading, headcount fell by 51,700 last year. Since 2015, it has dropped by more than 476,600, more than a quarter of the previous total.

Source: Light Reading

………………………………………………………………………………………………………………………………………………

Doing More with Less:

- In 2015, Verizon generated sales of $131.6 billion with a workforce of 177,700 employees. Last year, it made $134.8 billion with fewer than 100,000. Revenues per employee, accordingly, have risen from about $741,000 to more than $1.35 million over this period.

- AT&T made nearly $868,000 per employee last year, compared with less than $522,000 in 2015.

- Deutsche Telekom, buoyed by its T-Mobile US business, has grown its revenue per employee from about $356,000 to more than $677,000 over the same time period.

- Orange’s revenue per employee has risen from $298,000 to $368,000.

Significant workforce reductions have happened at all those companies, especially AT&T which finished last year with 141,000 employees – about half the number it had in 2015!

Not to be outdone, headcount at network equipment companies are also shrinking. Ericsson, Europe’s biggest 5G vendor, cut 6,000 jobs or 6% of its workforce last year and has slashed 13,000 jobs since 2023. Nokia’s headcount fell from 86,700 in 2023 to 75,600 at the end of last year. The latest message from Börje Ekholm, Ericsson’s CEO, is that AI will help the company operate with an even smaller workforce in future. “We also see and expect big benefits from the use of AI, and that is one reason why we expect restructuring costs to remain elevated during the year,” he said on this week’s earnings call with analysts.

………………………………………………………………………………………………………………………………………………

Other Voices:

Light Reading’s Iain Morris wrote, “An erosion of brainpower and ceding of tasks to AI would entail a loss of control as people are taken out of the mix. If AI can substitute for a junior coder, as experts say it can, the entry-level job for programming will vanish with inevitable consequences for the entire profession. And as AI assumes responsibility for the jobs once done by humans, a shrinking pool of individuals will understand how networks function.

“If you can’t understand how the AI is making that decision, and why it is making that decision, we could end up with scenarios where when something goes wrong, we simply just can’t understand it,” said Nik Willetts, the CEO of a standards group called the TM Forum, during a recent conversation with Light Reading. “It is a bit of an extreme to just assume no one understands how it works,” he added. “It is a risk, though.”

………………………………………………………………………………………………………………………………………………

References:

AI spending is surging; companies accelerate AI adoption, but job cuts loom large

Verizon and AT&T cut 5,100 more jobs with a combined 214,350 fewer employees than 2015

Big Tech post strong earnings and revenue growth, but cuts jobs along with Telecom Vendors

Nokia (like Ericsson) announces fresh wave of job cuts; Ericsson lays off 240 more in China

Deutsche Telekom exec: AI poses massive challenges for telecom industry