5G in Europe

Lack of wireless network operator consolidation & EU over-regulation weakened mobile network infrastructure investments

by John Strand of Strand Consult

Over-regulation in the European Union (EU) has had a negative impact on mobile network operator’s investment in both fixed and mobile infrastructure. Years ago, the EU identified a €100 billion investment gap in telecommunications. By 2025, this gap has reportedly doubled to €200 billion. Why did that happen?

The EU telecom market has a large number of operators, many of whom lack the subscriber base to generate sufficient returns on capital to justify large infrastructure investments. In contrast, countries like the US and China have a smaller number of larger operators, allowing for greater economies of scale and more investment per operator.

Regulatory Complexity and Costly Landscape: Overregulation and fragmented national rules create a complex and costly environment that stifles innovation and adds uncertainty for telecom companies, says the ECIPE. This impacts the ability to attract investment, according to the European Investment Bank.

Mobile operators around the world would like to merge four mobile networks in their respective nations into three. This would improve the business case for investment by eliminating duplicative administrations, improving spectrum synergies, and upgrading customers to better networks. Strand Consult has studied mobile industry consolidation since 2000 with the groundbreaking case of South Korea merging five operators into three and being first in the world to launch 3G. South Korea has remained at the forefront of mobile industry innovation, investment, and rollout ever since.

Unfortunately, during the period 2014 to 2024 European Union Vice President for Competition Margrethe Vestager had a crude view on in market consolidation. She did not understand that market consolidation could have a positive impact on the wireless infrastructure that citizens have access to.

The result is that this proceeding appears to overlook that critical lever—making it unlikely to achieve its core goal of boosting private-sector investment in broadband, fiber, and next-generation networks like 5G and 6G. While reducing compliance and reporting burdens is welcome, if the overarching regulatory model remains flawed, the fundamental barriers to investment will persist.

If you look at countries such as the United States, India and Brazil, the in-market consolidation has had a positive impact on the infrastructure to which citizens have access. Today, in a country like India, there is better 5G infrastructure than there is in large parts of Europe.

There is no requirement that EU Competition authorities justify their merger decisions empirically. Only occasionally are official post-mortems issued examining whether their decision was right. Generally, such reports conclude that prices remain low. However, in a world in which mobile prices are flat or falling anyway, a merger rejection is not needed to ensure competitive prices. Competing voice technologies like WhatsApp and Telegram drive down mobile prices, as do the competitive wireless offerings by fixed line providers.

Notably few, if any, competition authorities have studied how the length of merger review impacts network investment. When companies request permission to merge, it’s as if time stops. Operators must hold back on critical capital decisions while authorities assess the merger request.

In the United Kingdom, some analysts have blamed poor mobile coverage on new restrictions placed on Huawei and ZTE. This is nonsense. Operators across the EU have switched and upgraded to trusted equipment vendors without impacting coverage. See TDC Denmark, Telenor and Telia in Norway, T-Mobile in the Netherlands (Odido), and Proximus in Belgium.

The UK has had two recent mobile merger attempts: O2/Hutchison (2015-2016), which Vestager blocked in May 2016. The parties sued the Commission and won in 2020. However, the EC appealed and won in 2023. By that point, the issue was moot as the UK had left the Union. Most competition authorities don’t care that their review of transactions can take years, but markets do. Few companies can afford to tie up so much capital for so long, and fewer still can afford to challenge such decisions when they are unfavorable. Hence the Draghi report is on to something.

Vodafone and Hutchison have tried to merge since June 2023. Upon leaving the EU, UK merger decisions were restored to local authorities. The UK Competition and Markets Authority issued a favorable decision last year.

Slow merger review process is almost as bad as a merger rejection. Before firms announce a merger, they have done their internal due diligence, perhaps over 12-18 months. Once submitted, a merger review can take 12 to 24 months. If approved, the merger can take another 18 to 24 months to implement. This process can take from 36-66 months from start to finish. This period of planning, submission, review, merger, and implementation puts network investment on hold. The numbers speak for themselves just look at Ookla´s numbers for the UK.

T-Mobile – Sprint Merger:

In US, it’s a wonder that the merger of #3 T-Mobile and operator #4 Sprint happened at all. Depending on the asset and transfer, telecom merger review can include the Department of Justice, the Federal Communications Commission, the Attorneys General of the 50 states and other gatekeepers, all of whom want to extract concessions from the transaction. While there are fewer authorities in the case of Vodafone and Hutchison, it still takes time.

With the Sprint acquisition, T-Mobile wanted to create an operator to compete at scale with AT&T and Verizon. Today the merger is an unqualified success; customers have gained access to a better network, while T-Mobile today has grown the muscle to compete head on with AT&T and Verizon.

The military needs to get access to 5G SA:

In the telecommunications industry, there has been talk for many years about how mobile companies can gain access to new sources of revenue. 5G and not least 5G SA and 5G private networks have received a lot of attention. Conversely, there has not been much talk about what communication solutions the defense system needs in the future.

The war in Ukraine and shifting geopolitical realities have dramatically changed perspectives in recent years. There is now a fundamentally different understanding of why and how defense investments must be made. We live in a world in which Russia has invaded Ukraine; China counts Russia, North Korea, and Iran as allies; and these countries support Russia’s invasion of Ukraine

All countries across NATO are in the process of modernizing the defense systems, gigantic sums will be invested in new and advanced equipment. The shopping list is very long, on the other hand, all these new defense solutions have in common that they need access to modern communication solutions.

Modern militaries cannot function without secure, advanced, and integrated communications. 5G SA is the go-to solution for its speed, security, and adaptability. When it comes to the limited rollout of 5G SA in Europe, it has major implications for NATO´s access to access to a single national network free from untrusted vendors like Huawei and ZTE.

At the same time NATO does not use equipment from countries like China, Russia, North Korea, or Iran. Indeed, NATO’s procurement rules prohibit its contracting with communist countries. NATO would not purchase Chinese fighter jets from Chengdu Aircraft Corporation and Shenyang Aircraft Corporation, nor Huawei network equipment. The rationale is that ill-advised to acquire critical supplies from one’s adversary.

One of NATO´s key problems in Europe is a large number of operators have chosen to use equipment from suppliers like Huawei and ZTE there are unlikely to meet the security requirements from NATO. The qualification review and exercise which will be undertaken among the 32 NATO countries and many other nations around the world aligned with NATO, countries like Japan, the Philippines, and others. Countries which consider China a military partner (Pakistan, Belarus, and Cambodia) use Huawei and ZTE equipment.

The European Commission wants to transform telecom regulation in Europe:

The EU will have a public consultation regarding The Digital Networks Act (DNA). It is EU’s initiative to modernize telecom regulation by harmonizing rules, spurring infrastructure investment, and cutting red tape. It seeks to streamline spectrum licensing, network authorizations, and reporting across member states, while promoting sustainability and consumer protection. These are worthy aims—but past experience suggests the European Commission lacks the resolve, or the “DNA,” to turn vision into action. While Strand Consult supports the effort to bring telecom policy into the 21st century, the proposals arrive too little, too late to inspire investors, entrepreneurs, or citizens. Outside of standout digital performers like Denmark, Europe’s digital sector has long trailed the U.S., South Korea, Norway, and Switzerland by most competitive benchmarks.

At Strand Consult, we are concerned that the EU’s ongoing regulatory reforms will once again fail to address the fundamental challenges. Years ago, the EU identified a €100 billion investment gap in telecommunications. By 2025, this gap has reportedly doubled to €200 billion.

The EU’s record on AI is similarly illustrative. In 2018, the EU announced its ambition to lead in AI. However, by 2023, it had passed legislation that imposed significant constraints on AI development. In 2025, despite limited presence in the global AI landscape, the EU reiterated its ambition to lead, this time with an “AI Continent Action Plan.”

These historical examples suggest that the European Commission excels at producing regulations that slow technological development and deter investment. There are few—if any—notable technology firms that owe their success to EU regulatory frameworks. In contrast, we see a steady decline in key sectors like telecommunications and hardware, driven by regulatory missteps.

The European Commission has now pledged to transform telecom regulation in Europe. It may be too little, too late to address the deep-rooted challenges the EU itself has acknowledged and in part, created.

The bottom line is that The European figures from Ookla speak for themselves. The problem that they have uncovered is a problem that many of us have talked about a lot for many years.

………………………………………………………………………………………………………………………………………………………………………………………………

References:

Consolidation would renew European telecoms, says digital industry chief

https://www.eib.org/files/publications/thematic/accelerating_the_5g_transition_in_europe_en.pdf

………………………………………………………………………………………………………………………………………………………………………………………………..

John Strand is the CEO of Strand Consult. He founded Strand Consult in 1995. Strand Consult is an independent telecom consultancy known for its expert knowledge and many reports which help mobile operators and their shareholders navigate an increasing complex world. It has 170 mobile operators from around the world on its client list.

Ookla: Uneven 5G deployment in Europe, 5G SA remains sluggish; Ofcom: 28% of UK connections on 5G with only 2% 5G SA

According to Ookla, Europe is a “two-speed” 5G competitiveness landscape,” with some countries surging ahead and others falling well behind, In Q2-2025, Nordic and southern Europe countries maintained a substantial lead in 5G availability, helped by recent 700MHz band deployments in countries such as Sweden and Italy. By contrast, 5G availability in central and western European laggard countries such as Belgium, the UK and Hungary remains less than half that of the 5G pacemakers, says the study. On average, mobile subscribers in the EU spent 44.5% of their time connected to 5G networks in Q2 2025, up from 32.8% a year earlier.

The deployment and adoption of 5G SA in Europe remain sluggish, increasing slowly from a very low base and further widening the region’s gap with North America and Asia. Spain stands out as a clear leader in 5G SA deployment, reaching an 8% Speedtest® sample share compared with the EU average of just 1.3% as of Q2 2025. This progress has been driven by Spain’s proactive use of EU recovery funds to subsidize 5G SA rollouts in underserved areas, with a particular focus on bridging the rural-urban digital divide. However, the U.S. and China are still far ahead, with 5G SA sample shares above 20% and 80% respectively, reflecting a much greater pace of coverage and adoption in those markets.

Northern Europe Maintains 5G Availability Lead – Speed Test Intelligence Q2-2025:

Fragmented 5G Availability across Europe is driven by a complex mix of national policies on spectrum assignment and broader economic factors, rather than by simple geographic or demographic differences. 5G Availability is more strongly correlated with policy-driven factors such as spectrum allocation timelines and costs, coverage obligations, subsidy mechanisms, and regulations for infrastructure sharing and permitting, than with structural factors like urbanization rates or the number of operators. This indicates that 5G competitiveness is shaped less by technology gaps or inherent market imbalances and more by effective policy execution.

Northern Europe Maintains 5G Availability Lead; Other Countries Lag:

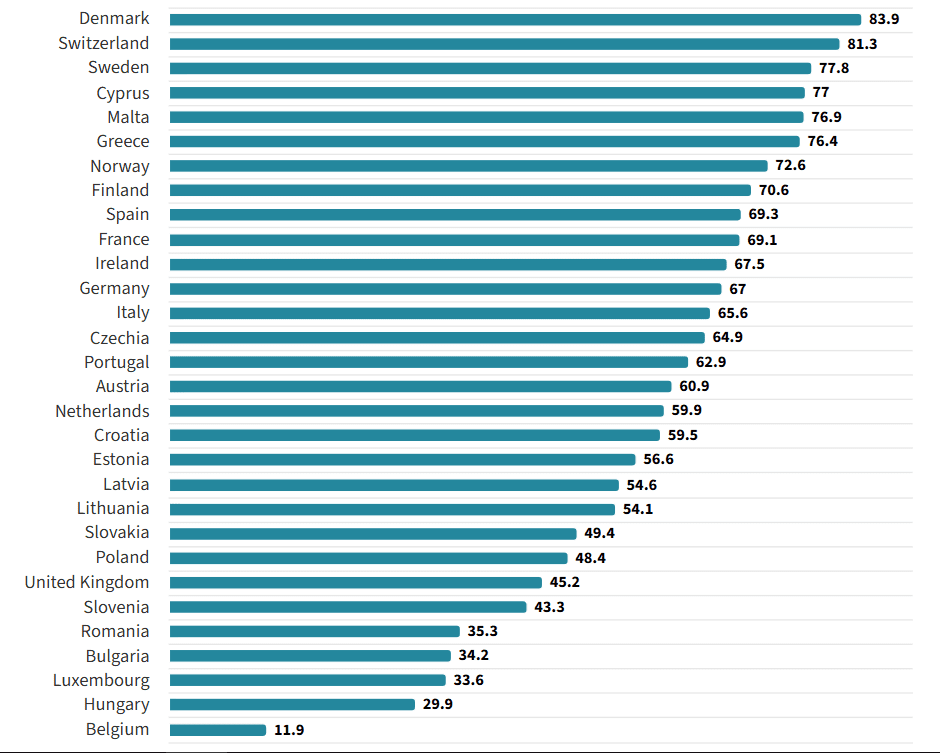

Fragmentation remains a persistent theme, shaping stark 5G deployment asymmetries that cannot be explained by geography or demographics alone. Northern and Southern European countries such as Denmark (83.9%), Sweden (77.8%), and Greece (76.4%) are disproportionately represented among the countries with the highest 5G Availability in Q2 2025, with coverage rates up to twice as high as those in Western and Eastern countries like the United Kingdom (45.2%), Hungary (29.9%), and Belgium (11.9%).

Low-band deployment and DSS use continue to lift 5G availability in lagging countries:

Recent advances in 5G Availability have been driven by low-band deployments and the use of DSS, raising the average proportion of time spent on 5G networks in the EU from 32.8% in Q2 2024 to 44.5% in Q2 2025. The pace of coverage growth, and the corresponding increase in 5G usage, has primarily reflected each country’s starting point. Lagging countries like Latvia, Poland, and Slovenia have seen double-digit gains in 5G Availability from a low base. By contrast, leading countries such as Switzerland and Denmark, where 5G coverage is now nearly ubiquitous, have shifted their focus to targeted capacity upgrades through site densification and mid-band expansion.

About Ookla:

Ookla, a global leader in connectivity intelligence, brings together the trusted expertise of Speedtest®, Downdetector®, Ekahau®, and RootMetrics® to deliver unmatched network and connectivity insights. By combining multi-source data with industry-leading expertise, we transform network performance metrics into strategic, actionable insights. Solutions empower service providers, enterprises, and governments with the critical data and insights needed to optimize networks, enhance digital experiences, and help close the digital divide. At the same time, we amplify the real-world experiences of individuals and businesses that rely on connectivity to work, learn, and communicate. From measuring and analyzing connectivity to driving industry innovation, Ookla helps the world stay connected.

Ookla is a division of Ziff Davis, a vertically focused digital media and internet company whose portfolio includes leading brands in technology, entertainment, shopping, health, cybersecurity, and martech.

……………………………………………………………………………………………………………………………………………………………………………………

Mobile Matters report from communications regulator Ofcom discusses 5G’s share of network connections in UK. Ofcom’s analysis – based on crowdsourced data collected by Opensignal and covering the period October 2024 to March 2025 – showed that 28% of connections were on 5G, with 71% still on 4G, 0.7% on 3G and a holdout 0.2% on 2G. In terms of mobile network operators, BT-owned EE had the highest proportion of network connections on 5G, at 32%, while Vodafone had the lowest, at 24%. O2, which is now the mobile arm of Virgin Media, had the lowest share of 4G connections (68%) and the highest proportion on 3G (3%).

5G standalone vs 5G non-standalone performance:

• 5G standalone (SA) accounted for 2% of all 5G connection attempts in the six months to March 2025. UK MNOs have started to offer 5G SA but its use is currently low.

• Standalone 5G’s average response time (latency) was about 15% lower (better) than for 5G NSA. However, our analysis also indicated that 5G SA had a lower average connection success rate (95.9%) than 5G NSA (97.6%), although this was slightly higher than 4G’s.

• 5G SA provided significantly higher download speeds than 5G NSA. Seventy per cent of 5G SA download speeds measurements were at 100 Mbit/s or higher, compared to 46% for 5G NSA, and 2MB, 5MB and 10MB file download times, on average, were about 45% faster on 5G SA than over 5G NSA.

• The picture was more mixed for uploads. While 5G NSA had a higher proportion of low-speed connections (18% of 5G NSA upload speeds provided less than 2 Mbit/s compared to 10% on 5G SA) it also had a slightly higher share of higher-speed connections (30% of 5G NSA uploads were 20 Mbit/s or higher vs 28% on 5G SA).

References:

https://www.ookla.com/articles/europe-5g-q2-2025

Ookla: Europe severely lagging in 5G SA deployments and performance

Téral Research: 5G SA core network deployments accelerate after a very slow start

Ookla: Europe severely lagging in 5G SA deployments and performance

According to a new joint study from Omdia and Ookla, Europe has had the poorest 5G SA availability and performance among major regions. In Q4 2024, China (80%), India (52%), and the United States (24%) led the world in 5G SA availability based on Speedtest® sample share, markedly ahead of Europe (2%).

The European region also lagged behind its peers in performance, with the median European consumer experiencing 5G SA download speeds of 221.17 Mbps—lower than those in the Americas (384.42 Mbps) and both Developed (237.04 Mbps) and Emerging (259.73 Mbps) Asia Pacific. The interplay of earlier deployments, a more diversified multi-band spectrum strategy, and greater operator willingness to invest in the 5G core to monetize new use cases have driven rollouts at a faster pace in regions outside Europe.

The European Commission has championed measures to accelerate private investment in 5G SA, highlighting network slicing—a flagship capability of cloud-native core networks—as a key potential driver of its broader industrial strategy in sectors such as precision manufacturing, defense and clean energy. Up until this point, high-quality public data examining Europe’s progress in 5G SA—and benchmarking its competitive position relative to other global regions—has been scarce. In its latest annual report, Connect Europe, the trade body representing Europe’s telecoms operators, noted that “there is limited information available about the extent of operators’ rollout of 5G SA.”

Advanced network capabilities enabled by the technology remain stubbornly limited to just a few operators in leading markets such as the U.S., according to the study, while Europe lags behind its peers on several 5G SA performance indicators, “raising concerns about the bloc’s competitiveness in the technology.”

Network operator investment per capita also lags in Europe as per the below chart:

When faced with choices among investments in fiber, 5G RAN, and 5G SA core, the latter frequently loses out, since operators can still launch a “5G” network by leveraging alternative technologies. There is also a lack of 5G SA-compatible devices, especially devices with User Equipment Routing Selection Policy (URSP) technology, which allows a device to dynamically select a slice (or multiple slices) provisioned by an operator. However, only Android 12/iOS 17 mobile devices support that largely unknown technology.

While capital spending on the 5G core transition is now increasing rapidly, European network operators will remain committed to strict cost discipline Based on Omdia’s Q3 2024 quarterly core software market share and forecast, the research firm believes that the global core market revenue from both 4G and 5G network functions will grow with a five-year CAGR of 3.2% between 2023 and 2028. When considering the spending in 5G core software, the forecasted growth with a five-year CAGR during the same period is of 17.0%.

Omdia now forecasts that 5G SA core spending in EMEA will grow with a five-year CAGR of 26.2% between 2023 and 2028. Nonetheless, as a prerequisite, deploying the 5G core also requires a good 5G radio coverage, to avoid a degraded experience where the 5G coverage is limited or nonexistent, and where the user falls back on 4G-LTE or 2G/3G. This means operators must invest in 5G RAN, which is usually considered the highest capex draining activity for an operator. While 5G is known for very high throughput speeds using mid-band (and particularly C-band) spectrum, these bands need to be complemented by sub-GHz spectrum deployment, in order to offer improved in-building and wide area coverage. This rollout has been slow in many European markets, with 5G availability in all countries outside the Nordics remaining significantly lower than that in the United States and China, according to Ookla’s Q4 2024 Speedtest Intelligence® data.

One bright spot is that Europe has made progress on achieving low latency on its 5G networks. In Q4 2024, the average country-wide median latency in Europe was 32 milliseconds (ms) compared to 35 ms in the Americas and 36 ms in Emerging Asia Pacific region.

References:

https://www.lightreading.com/5g/eurobites-europe-behind-on-5g-sa-study

https://www.ookla.com/s/media/2025/02/ookla_omdia-5GSA_0225.pdf

Building and Operating a Cloud Native 5G SA Core Network

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

GSA 5G SA Core Network Update Report

ABI Research: Expansion of 5G SA Core Networks key to 5G subscription growth

Vision of 5G SA core on public cloud fails; replaced by private or hybrid cloud?

Nokia and Eolo deploy 5G SA mmWave “Cloud RAN” network

Nokia, BT Group & Qualcomm achieve enhanced 5G SA downlink speeds using 5G Carrier Aggregation with 5 Component Carriers

Telefónica launches 5G SA in >700 towns and cities in Spain

Telefónica has followed Orange with the official launch of a 5G standalone (SA) network in more than 700 towns and cities throughout Spain. The service is branded Movistar 5G+ even though it is just 3GPP defined real 5G (with its own core network , rather than 5G NSA which uses LTE core network). The new Telefónica 5G SA network uses Ericsson and Nokia network equipment. Huawei has been excluded from it because the European Commission wants to ban Huawei in the EU for its alleged espionage work for the Chinese government.

Telefonica said its 5G NSA service in the 700 MHz band is currently available to around 85 percent of the Spanish population across 2,200 municipalities. The Spanish operator also uses the 3.5 GHz band for 5G and invested EUR 20 million to secure the maximum possible 1 GHz of spectrum in the 2.6 GHz band.

![]()

“Movistar customers will be able to enjoy 5G+ automatically and at no additional cost both in large cities and in small municipalities thanks to a highly capillarity deployment that will allow ultra-fast speeds and very low latency to be obtained in practically all of Spain,” the company explained in a statement.

The launch of 5G+, which offers greater coverage and browsing speeds of up to 1,600 megabits per second (Mbps), will take place within the scope of Movistar’s deployment in the 3,500 MHz band. In practice, 5G+ translates into better mobile experience in content downloads at the speed of fiber optics, streaming High quality and uninterrupted gaming. It also offers greater coverage in crowded spaces such as a sporting event or a music concert, according to Telefónica.

Movistar currently covers a total of 11 cities with 5G SA: Madrid, Barcelona, Malaga, Seville, Palma de Mallorca, Las Palmas de Gran Canaria, Ávila, Segovia, Castellón, El Ferrol and Vigo. The goal for the end of the year is to have “extensive 5G SA coverage in most cities with more than 250,000 inhabitants,” as well as in smaller towns, so that the capillarity of the service continues to be consolidated. However, in order to enjoy this service it is necessary to have a mobile that supports 5G SA. For the moment, Movistar has the new Xiaomi terminals to which new brands will be added.

Gabriel Brown, principal analyst at Heavy Reading, notes that Movistar operates the biggest network in Spain and has the largest number of live 3.5GHz sites, according to the independent AntenasMoviles website.

Said deployment is completed with the coverage in the 700 MHz band that Movistar has been offering since last year and currently reaches more than 2,200 municipalities, with advantages such as improved indoor coverage. The so-called low band is complemented in 5G with that of 3,500 MHz, ideal for services that require a user experience at a very high transmission speed, both for rural areas and large urban centers. In this way, Movistar already offers 5G coverage to more than 85% of the population, reports the company.–

Orange leads 5G SA coverage as it already reaches more than twenty cities that cover 30% of the population in Spain. In the case of Vodafone and MásMóvil, 5G SA is expected to be available before March 2024.

Heavy Reading’s Brown said, “It will be interesting to see if this gives it an edge in SA. Orange Spain, meanwhile, says it will launch network slicing before the end of the year.”

References:

https://euro.eseuro.com/business/572316.html

Telefónica – Nokia alliance for private mobile networks to accelerate digital transformation for enterprises in Latin America

Orange-Spain deploys 5G SA network (“5G+”) in Madrid, Barcelona, Valencia and Seville

Kearney’s “5G Readiness Index 2022” and How to Monetize 5G

A new report from management consultancy Kearney analyzes a year of 5G progress across 33 countries around the world. The Kearney “5G Readiness Index 2022” assesses 5G and how close countries are to realizing all the potential and benefits of widespread 5G in the context of the overall maturity of a country’s telecoms market and its socio-economic position. The report covers 33 countries, all of which had launched 5G by the third quarter of 2022. To be included, countries must have launched 5G by the fourth quarter of 2021.

“Europe is falling behind on 5G!” is a cry we heard at the latest Mobile World Congress. The Kearney 5G Readiness Index 2021 reflected it, and our 2022 Index confirms it, at least for now (see Figure 1).

11 out of 28 countries tracked have at least one operator with a standalone 5G core network launched. Asia leads with seven countries, while Europe trails with just Finland and Germany reaching this point. Only in two countries have all operators launched standalone cores—Singapore and China—opening up their markets for a 5G transformation.

This year’s Index reveals that only 10 countries have made high band spectrum available, and operators in just five of them (the United States, Australia, South Korea, Thailand, and Japan) have launched full commercial services within it. So far, no European countries have gotten this far, although select services have been launched on limited mmWave licenses, including in Germany. The lack of availability of mmWave spectrum is disappointing because its advantages are the cornerstone of new, high speed 5G-enabled services.

The Index identified more key developments during the past year:

- The United States continues to push ahead of other countries. Its regulator has provided spectrum in all three band classes, and national operators have made the most of it by launching services. One operator has launched a standalone 5G core. Canada also has an operator offering 5G services via its new standalone core.

- South Korea, which ranked second in the 2021 Index, has dropped to fifth because it has not made low band spectrum available, despite high subscriber penetration.

- Most Nordic countries are pulling ahead, thanks to wider spectrum availability and broader deployment across bands, but Sweden is held back by the lack of mmWave spectrum as full availability of 26 GHz isn’t planned before 2025. This slows Sweden down and risks muting consumer excitement.

- Germany moved from laggard to leader of the EU4 (France, Germany, Italy, and Spain) plus the United Kingdom, thanks to operators launching 5G in multiple bands. Only one operator has launched a 5G standalone core.

- France now trails other larger European countries because of its late launch of 5G (November 2020) and customers’ apparent limited interest in it.

- A strong showing in the Middle East (Saudi Arabia, United Arab Emirates, and Qatar) is a testament to their networks’ quality and strong rollouts. Penetration is 9 to 11 percent. A Saudi operator has launched a standalone 5G core.

- Australia was one of the first countries to launch 5G, has continuously expanded spectrum access across all bands, and enjoys successful commercialization. It has 18 percent 5G penetration, the second highest in the Index.

Kearney also uncovered the following findings:

- Take-up (as a percentage of total subscribers in the first quarter, 2022) is paltry across Europe. Switzerland is the best with 13 percent but launched in April 2019. Belgium is the worst offender at 1.7 percent of connections. Take-up is 31 percent in South Korea.

- In South Korea, the government has announced a push for creating an ecosystem of companies that innovate and leverage 5G (aiming for 1,800 5G service firms by 2026). They understand operators won’t be solo drivers but enablers.

- Rollout of new capacity in the United States allows operators to launch impactful services, such as 5G fixed wireless access (FWA). One operator is using

- 5G to equip ambulances with high-quality video feeds that medical professionals can view while patients are en route.

Europe is behind, but not irreparably so. Vigilance and focus are required, together with operators’ preparation to win with 5G when their countries have reached ready status.

Monetize 5G step-by-step, building up to an ecosystem of products, services, and partners:

Currently, 5G lacks killer uses cases to drive customer uptake. Without seductive 5G products or services, people won’t see its benefits. Yet, operators wonder whether advancing investment in 5G is wise. It’s classic chicken-and-egg, but it will start somewhere, spearheaded by first-mover operators along with third-party providers that will figure out what will make everyone want 5G. Plan monetization first with small steps, and then plan the ecosystem to realize its potential.

It still may seem like early days in the 5G journey, but time grows shorter for European telcos to catch up with the United States and other markets. Getting your strategy rolling now is the only way to take advantage of the European market when it becomes fully 5G ready.

References:

Ericsson Mobility Report: 5G monetization depends on network performance

Moody’s skeptical on 5G monetization; Heavy Reading: hyperscalers role in MEC and telecom infrastructure

ABI Research: Expansion of 5G SA Core Networks key to 5G subscription growth

PwC report on Monetizing 5G should be a wake up call to network operators!

How 5G network operators can stay competitive and grow their business

Reuters: Telcos draft proposal to charge Big Tech for EU 5G rollout; Meta offers a rebuttal

Big tech companies accounting for more than 5% of a telecoms provider’s peak average internet traffic should help fund the rollout of 5G and broadband across Europe, according to a draft proposal by the telecoms industry. The proposal is part of feedback to the European Commission which launched a consultation into the issue in February. The deadline for responses is Friday.

Alphabet’s Google, Apple Facebook-owner Meta, Amazon, Netflix and TikTok would most likely be hit with fees, according to industry estimates. Google, Apple, Meta, Netflix, Amazon and Microsoft together account for more than half of data internet traffic.

The document, which was reviewed by Reuters and has not been published, was compiled by telecoms lobbying groups GSMA and ETNO. They represent 160 operators in Europe, including Deutsche Telekom, Orange, Telefonica and Telecom Italia. Telecom operators have lobbied for years for leading technology companies to help foot the bill for 5G and broadband roll-out, saying that they create a huge part of the region’s internet traffic. This is the first time they have tried to define a threshold for who should pay.

“We propose a clear threshold to ensure that only large traffic generators, who impact substantially on operators’ networks, fall within the scope,” the draft stated. “Large traffic generators would only be those companies that account for more than 5% of an operator’s yearly average busy hour traffic measured at the individual network level,” it said. The European Commission declined to comment.

Meta on Wednesday urged Brussels to reject any proposals to charge Big Tech for additional network costs. In a Facebook blog post, Markus Reinisch, Meta’s VP for Public Policy for Europe, described potential fees as a “private sector handout for selected telecom operators” that would disincentivize innovation and investment, and distort competition. “We urge the Commission to consider the evidence, listen to the range of organizations who have voiced concerns, and abandon these misguided proposals as quickly as possible,” he said. Here are Meta’s takeaways:

- Network fee proposals misunderstand the value that content platforms bring to the digital ecosystem.

- We support the Commission’s goal of “ensuring access to excellent connectivity for everyone,” but network fee proposals will hurt European consumers and businesses.

- We urge the Commission to consider the evidence, listen to the range of organizations who have voiced concern, and drop these proposals.

References:

Network Fee Proposals Will Ultimately Hurt European Businesses and Consumers

https://www.euractiv.com/section/5g/news/eu-telcos-call-for-big-tech-to-share-5g-network-costs/

GSMA: Europe’s 5G rollout is too slow at 6% of mobile customer base

European telcos need to address very high 5G energy consumption

Strand Consult: Market for 5G RAN in Europe: Share of Chinese and Non-Chinese Vendors in 31 European Countries

GSMA: Europe’s 5G rollout is too slow at 6% of mobile customer base

GSMA says in order to stay competitive European economies must ‘digitalize’ themselves through faster 5G rollouts and make a fair contribution. The telco trade body and owner of MWC event has released its 2022 Mobile Economy Report for Europe, in which it states the EU will not meet its ‘digital decade goals’ unless it starts rolling out 5G faster across the continent.

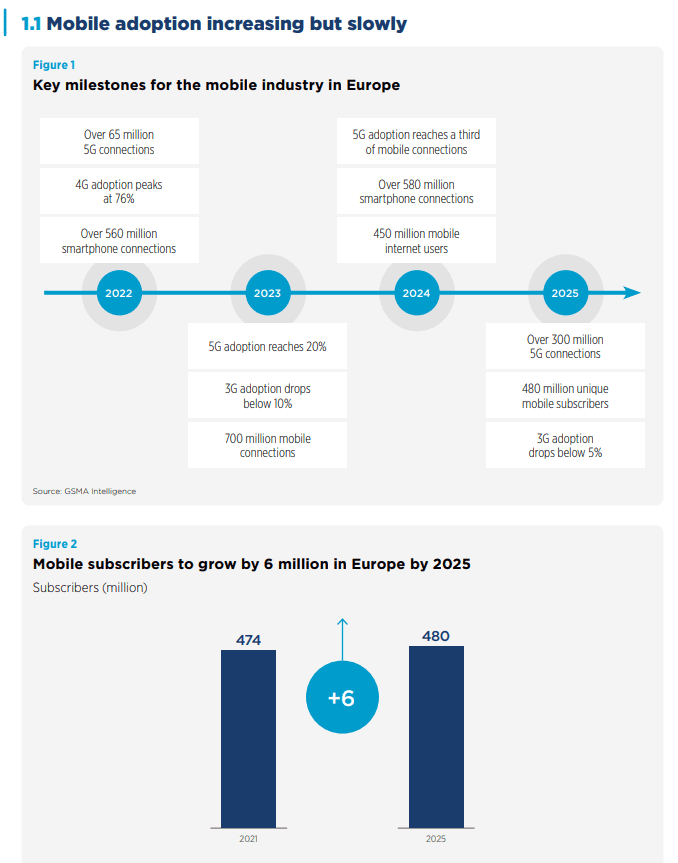

In 2021, 474 million people in Europe (86% of the population) were subscribed to mobile services, and this is expected to grow to 480 million by 2025.

The majority of countries in Europe have now deployed commercial 5G services, and nearly two thirds of wireless network operators in the region have launched 5G networks. At the end of June 2022, 108 operators in 34 markets across Europe had launched commercial 5G services, while consumer uptake was at 6% of the mobile customer base. Norway trended above this with 16% of its citizens using 5G, followed by Switzerland (14%), Finland (13%), the UK (11%) and Germany (10%).

GSMA forecasts that by 2025, there will be 311 million 5G connections across Europe, a 44% adoption rate. However, European markets still lag behind global peers such as Japan, South Korea and the U.S. in the adoption of 5G technology. In 2025, the UK and Germany will have the highest 5G adoption rates in Europe at 61% and 59% respectively, compared to 73% in South Korea and 68% in Japan and the U.S. 4G adoption in Europe will peak in 2022 and then decline. However, it is set to remain the dominant technology across the region, accounting for just over half of total connections by 2025.

The pace of 5G coverage expansion across Europe will be a key factor in the transition from 4G to 5G. Although 5G network coverage in Europe will rise to 70% in 2025 (from 47% in 2021), nearly a third of the population will remain without 5G coverage. This compares to 2% or less in South Korea and the U.S.

SOURCE: GSMA

“Europe is adopting 5G faster than ever before, but greater focus on creating the right market conditions for infrastructure investment is needed to keep pace with other world markets. This should include the implementation of the principle of fair contribution to network costs,” said Daniel Pataki, GSMA Vice President for Policy & Regulation, and Head of Europe.

Which of course is a reference to the ‘fair contribution’ argument that telcos and now the GSMA itself has been making for some time now, which in a nutshell says that since internet firms like Netflix and Facebook make tons of money, they should contribute to the building of physical network infrastructure because it is expensive and telcos don’t make as much cash as they used to.

This announcement from the GSMA goes a bit further than saying it’s unfair that content providers make much more margin streaming TV shows that telcos do on digging holes and dragging up cell towers, and seems to be asserting that unless something is done about all this then the entire continent of Europe will become uncompetitive on the world stage.

As economies and societies around the world digitalize, the acceleration of 5G in Europe is necessary to ensure that traditional industrial and manufacturing strengths are not dragged down by weaknesses in the ICT sector. To achieve this, it is vital to create the right conditions for private infrastructure investment, network modernization and digital innovation. A financially sustainable mobile sector is key to the delivery of innovative services and the deployment of new networks.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

References:

https://www.gsma.com/mobileeconomy/wp-content/uploads/2022/10/051022-Mobile-Economy-Europe-2022.pdf