AI Bubble

Nvidia CEO Huang: AI is the largest infrastructure buildout in human history; AI Data Center CAPEX will generate new revenue streams for operators

Executive Summary:

In a February 6, 2026 CNBC interview with with Scott Wapner, Nvidia CEO Jensen Huang [1.] characterized the current AI build‑out as “the largest infrastructure buildout in human history,” driven by exceptionally high demand for compute from hyperscalers and AI companies. “Through the roof” is how he described AI infrastructure spending. It’s a “once-in-a-generation infrastructure buildout,” specifically highlighting that demand for Nvidia’s Blackwell chips and the upcoming Vera Rubin platform is “sky-high.” He emphasized that the shift from experimental AI to AI as a fundamental utility has reached a definitive inflection point for every major industry.

Jensen forecasts aa roughly 7–to- 8‑year AI investment cycle lies ahead, with capital intensity justified because deployed AI infrastructure is already generating rising cash flows for operators. He maintains that the widely cited ~$660 billion AI data center capex pipeline is sustainable, on the grounds that GPUs and surrounding systems are revenue‑generating assets, not speculative overbuild. In his view, as long as customers can monetize AI workloads profitably, they will “keep multiplying their investments,” which underpins continued multi‑year GPU demand, including for prior‑generation parts that remain fully leased.

Note 1. Being the undisputed leader of AI hardware (GPU chips and networking equipment via its Mellanox acquisition), Nvidia MUST ALWAYS MAKE POSITIVE REMARKS AND FORECASTS related to the AI build out boom. Reader discretion is advised regarding Huang’s extremely bullish, “all-in on AI” remarks.

Huang reiterated that AI will “fundamentally change how we compute everything,” shifting data centers from general‑purpose CPU‑centric architectures to accelerated computing built around GPUs and dense networking. He emphasizes Nvidia’s positioning as a full‑stack infrastructure and computing platform provider—chips, systems, networking, and software—rather than a standalone chip vendor. He accuratedly stated that Nvidia designs “all components of AI infrastructure” so that system‑level optimization (GPU, NIC, interconnect, software stack) can deliver performance gains that outpace what is possible with a single chip under a slowing Moore’s Law. The installed base is presented as productive: even six‑year‑old A100‑class GPUs are described as fully utilized through leasing, underscoring persistent elasticity of AI compute demand across generations.

AI Poster Childs – OpenAI and Anthropic:

Huang praised OpenAI and Anthropic, the two leading artificial intelligence labs, which both use Nvidia chips through cloud providers. Nvidia invested $10 billion in Anthropic last year, and Huang said earlier this week that the chipmaker will invest heavily in OpenAI’s next fundraising round.

“Anthropic is making great money. Open AI is making great money,” Huang said. “If they could have twice as much compute, the revenues would go up four times as much.”

He said that all the graphics processing units that Nvidia has sold in the past — even six-year old chips such as the A100 — are currently being rented, reflecting sustained demand for AI computing power.

“To the extent that people continue to pay for the AI and the AI companies are able to generate a profit from that, they’re going to keep on doubling, doubling, doubling, doubling,” Huang said.

Economics, utilization, and returns:

On economics, Huang’s central claim is that AI capex converts into recurring, growing revenue streams for cloud providers and AI platforms, which differentiates this cycle from prior overbuilds. He highlights very high utilization: GPUs from multiple generations remain in service, with cloud operators effectively turning them into yield‑bearing infrastructure.

This utilization and monetization profile underlies his view that the capex “arms race” is rational: when AI services are profitable, incremental racks of GPUs, network fabric, and storage can be modeled as NPV‑positive infrastructure projects rather than speculative capacity. He implies that concerns about a near‑term capex cliff are misplaced so long as end‑market AI adoption continues to inflect.

Competitive and geopolitical context:

Huang acknowledges intensifying global competition in AI chips and infrastructure, including from Chinese vendors such as Huawei, especially under U.S. export controls that have reduced Nvidia’s China revenue share to roughly half of pre‑control levels. He frames Nvidia’s strategy as maintaining an innovation lead so that developers worldwide depend on its leading‑edge AI platforms, which he sees as key to U.S. leadership in the AI race.

He also ties AI infrastructure to national‑scale priorities in energy and industrial policy, suggesting that AI data centers are becoming a foundational layer of economic productivity, analogous to past buildouts in electricity and the internet.

Implications for hyperscalers and chips:

Hyperscalers (and also Nvidia customers) Meta , Amazon, Google/Alphabet and Microsoft recently stated that they plan to dramatically increase spending on AI infrastructure in the years ahead. In total, these hyperscalers could spend $660 billion on capital expenditures in 2026 [2.] , with much of that spending going toward buying Nvidia’s chips. Huang’s message to them is that AI data centers are evolving into “AI factories” where each gigawatt of capacity represents tens of billions of dollars of investment spanning land, compute, and networking. He suggests that the hyperscaler industry—roughly a $2.5 trillion sector with about $500 billion in annual capex transitioning from CPU to GPU‑centric generative AI—still has substantial room to run.

Note 2. An understated point is that while these hyperscalers are spending hundered of billions of dollars on AI data centers and Nvidia chips/equipment they are simultaneously laying off tens of thousands of employees. For example, Amazon recently announced 16,000 job cuts this year after 14,000 layoffs last October.

From a chip‑level perspective, he argues that Nvidia’s competitive moat stems from tightly integrated hardware, networking, and software ecosystems rather than any single component, positioning the company as the systems architect of AI infrastructure rather than just a merchant GPU vendor.

References:

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

Analysis: Cisco, HPE/Juniper, and Nvidia network equipment for AI data centers

Networking chips and modules for AI data centers: Infiniband, Ultra Ethernet, Optical Connections

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Superclusters of Nvidia GPU/AI chips combined with end-to-end network platforms to create next generation data centers

184K global tech layoffs in 2025 to date; ~27.3% related to AI replacing workers

Analysis: SpaceX FCC filing to launch up to 1M LEO satellites for solar powered AI data centers in space

SpaceX has applied to the Federal Communications Commission (FCC) for permission to launch up to 1 million LEO satellites for a new solar-powered AI data center system in space. The private company, 40% owned by Elon Musk, envisions an orbital data center system with “unprecedented computing capacity” needed to run large-scale AI inference and applications for billions of users, according to SpaceX’s filing entered late on Friday.

Credit: Blueee/Alamy Stock Photo

The proposed new satellites would operate in “narrow orbital shells” of up to 50 kilometers each. The satellites would operate at altitudes of between 500 kilometers and 2,000 kilometers, and 30 degrees, and “sun-synchronous orbit inclinations” to capture power from the sun. The system is designed to be interconnected via optical links with existing Starlink broadband satellites, which would transmit data traffic back to ground Earth stations.

“Fortunately, the development of fully reusable launch vehicles like Starship that can deploy millions of tons of mass per year to orbit when launching at rate, means on-orbit processing capacity can reach unprecedented scale and speed compared to terrestrial buildouts, with significantly reduced environmental impact,” SpaceX said.

- Energy Density & Sustainability: By tapping into “near-constant solar power,” SpaceX aims to utilize a fraction of the Sun’s output—noting that even a millionth of its energy exceeds current civilizational demand by four orders of magnitude.

- Thermal Management: To address the cooling requirements of high-density AI clusters, these satellites will utilize radiative heat dissipation, eliminating the water-intensive cooling loops required by terrestrial facilities.

- Opex & Scalability: The financial viability of this orbital layer is tethered to the Starship launch platform. SpaceX anticipates that the radical reduction in $/kg launch costs provided by a fully reusable heavy-lift vehicle will enable rapid scaling and ensure that, within years, the lowest LCOA (Levelized Cost of AI) will be achieved in orbit.

- Vacuum-Speed Data Transmission: In a vacuum, light propagates roughly 50% faster than through terrestrial fiber optic cables. By utilizing Starlink’s optical inter-satellite links (OISLs)—a “petabit” laser mesh—data can bypass terrestrial bottlenecks and subsea cables. This potentially reduces intercontinental latency for AI inference to under 50ms, surpassing many long-haul terrestrial routes.

- Edge-Native Processing & Data Gravity: Current workflows require downlinking massive raw datasets (e.g., Synthetic Aperture Radar imagery) for terrestrial processing, a process that can take hours. Shifting to orbital edge computing allows for “in-situ” AI inference, processing data onboard to deliver actionable insights in minutes rather than hours. This “Space Cloud” architecture eliminates the need to route raw data back to the Earth’s internet backbone, reducing data transmission volumes by up to 90%.

- LEO Proximity vs. Terrestrial Hops: While terrestrial fiber remains the “gold standard” for short-range latency (typically 1–10ms), it is often hindered by inefficient routing and multiple hops. SpaceX’s LEO constellation, operating at altitudes between 340km and 614km, currently delivers median peak-hour latencies of ~26ms in the US. Future orbital configurations may feature clusters at varying 50km intervals to optimize for specific workload and latency tiers.

………………………………………………………………………………………………………………………………………………………………………………………

The SpaceX FCC filing on Friday follows an exclusive report by Reuters that Elon Musk is considering merging SpaceX with his xAI (Grok chatbot) company ahead of an IPO later this year. Under the proposed merger, shares of xAI would be exchanged for shares in SpaceX. Two entities have been set up in Nevada to facilitate the transaction, Reuters said. Musk also runs electric automaker Tesla, tunnel company The Boring Co. and neurotechnology company Neuralink.

………………………………………………………………………………………………………………………………………………………………………………………

References:

Google’s Project Suncatcher: a moonshot project to power ML/AI compute from space

Blue Origin announces TeraWave – satellite internet rival for Starlink and Amazon Leo

China ITU filing to put ~200K satellites in low earth orbit while FCC authorizes 7.5K additional Starlink LEO satellites

Amazon Leo (formerly Project Kuiper) unveils satellite broadband for enterprises; Competitive analysis with Starlink

Telecoms.com’s survey: 5G NTNs to highlight service reliability and network redundancy

Huge significance of EchoStar’s AWS-4 spectrum sale to SpaceX

U.S. BEAD overhaul to benefit Starlink/SpaceX at the expense of fiber broadband providers

Telstra selects SpaceX’s Starlink to bring Satellite-to-Mobile text messaging to its customers in Australia

SpaceX launches first set of Starlink satellites with direct-to-cell capabilities

AST SpaceMobile to deliver U.S. nationwide LEO satellite services in 2026

GEO satellite internet from HughesNet and Viasat can’t compete with LEO Starlink in speed or latency

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Subsea cable systems: the new high-capacity, high-resilience backbone of the AI-driven global network

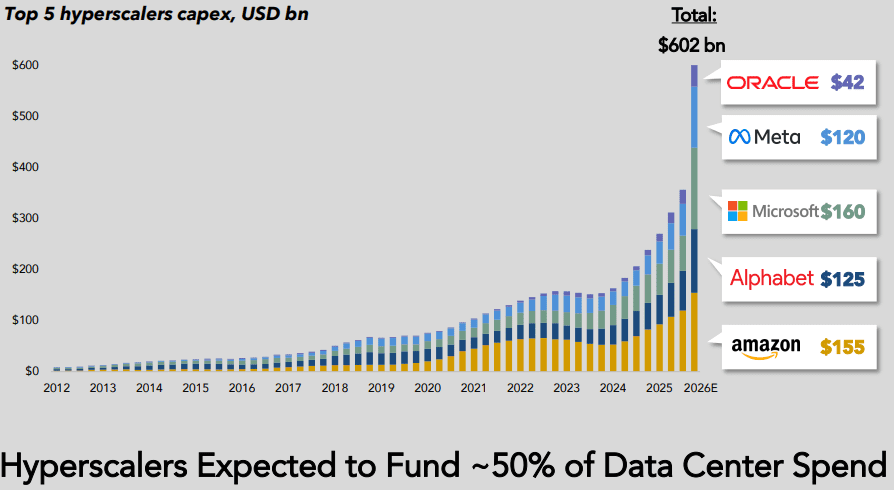

Hyperscaler capex > $600 bn in 2026 a 36% increase over 2025 while global spending on cloud infrastructure services skyrockets

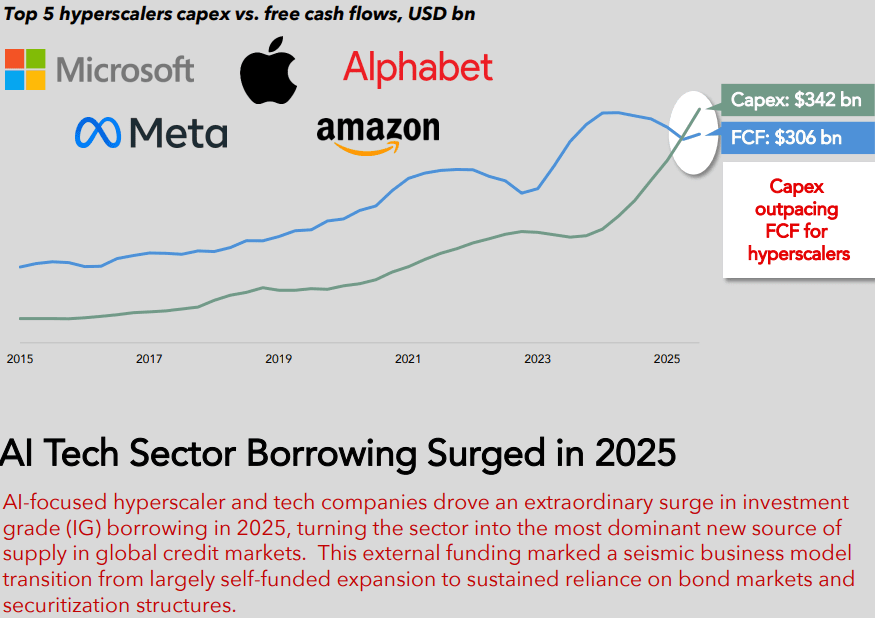

Hyperscaler capex for the “big five” (Amazon, Alphabet/Google, Microsoft, Meta/Facebook, Oracle) is now widely forecast to exceed $600 bn in 2026, a 36% increase over 2025. Roughly 75%, or $450 bn, of that spend is directly tied to AI infrastructure (i.e., servers, GPUs, datacenters, equipment), rather than traditional cloud. Hyperscalers are increasingly leaning on debt markets to bridge the gap between rapidly rising AI capex budgets and internal free cash flow, transforming historically cash-funded business models into ones utilizing leverage, albeit with still very strong balance sheets. Aggregate capex for “the big five”, after buybacks and dividends are included, are now above projected cash flows, thereby necessitating external funding needs.

……………………………………………………………………………………………………………………………………………………………………………………………………………………..

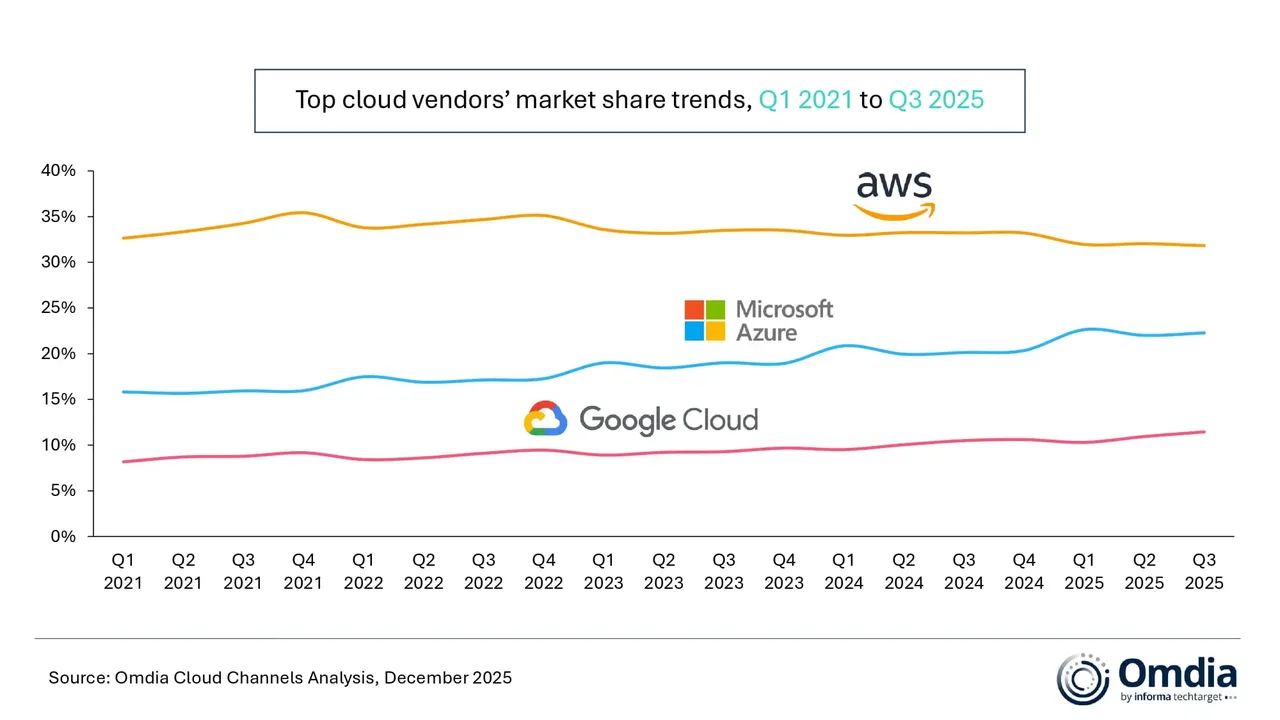

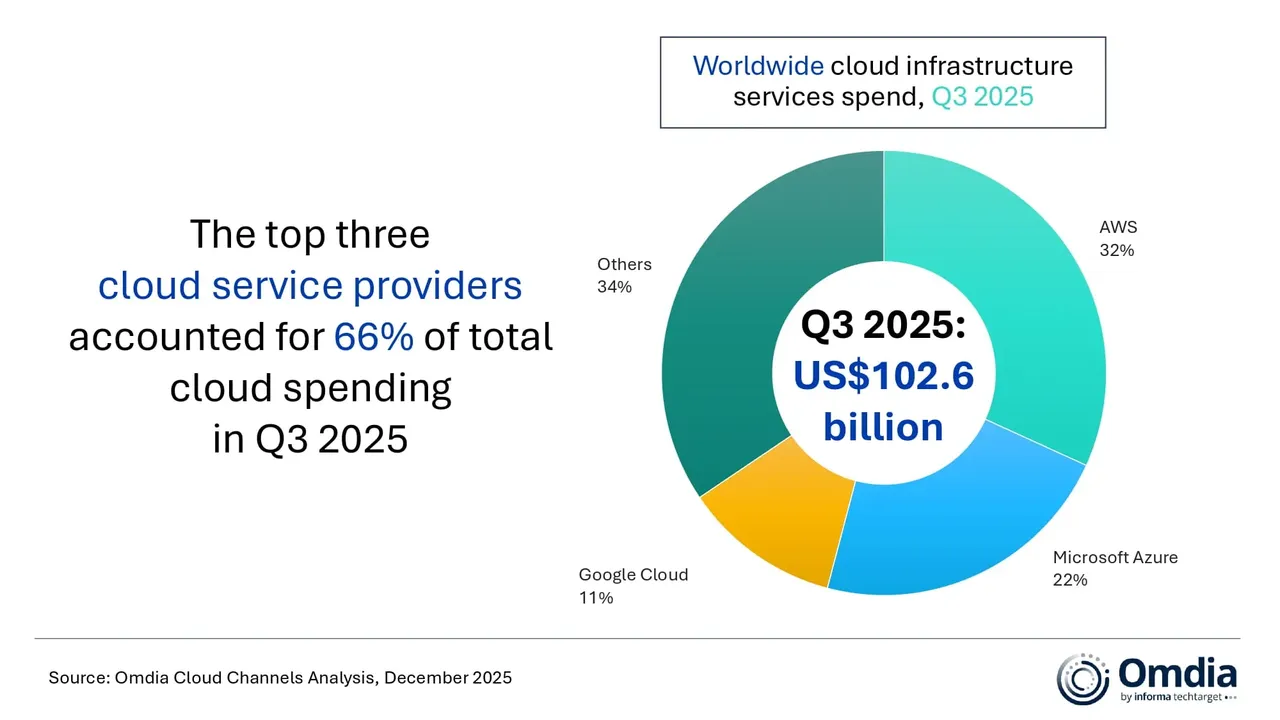

According to market research from Omdia (owned by Informa) global spending on cloud infrastructure services reached $102.6 billion in Q3 2025 — a 25% year-on-year increase. It was the fifth consecutive quarter in which cloud spending growth remained above 20%. Omdia says it “reflects a significant shift in the technology landscape as enterprise demand for AI moves beyond early experimentation toward scaled production deployment.” AWS, Microsoft Azure, and Google Cloud – maintained their market rankings from the previous quarter, and collectively accounted for 66% of global cloud infrastructure spending. Together, the three firms had 29% year-on-year growth in their cloud spending.

Hyperscaler AI strategies are shifting from a focus on incremental model performance to platform-driven, production-ready approaches. Enterprises are now evaluating AI platforms based not solely on model capabilities, but also on their support for multi-model strategies and agent-based applications. This evolution is accelerating hyperscalers’ move toward platform-level AI capabilities. According to the report, Amazon Web Services (AWS), Microsoft Azure, and Google Cloud are integrating proprietary foundation models with a growing range of third-party and open-weight models to meet these new demands.

“Collaboration across the ecosystem remains critical,” said Rachel Brindley, Senior Director at Omdia. “Multi-model support is increasingly viewed as a production requirement rather than a feature, as enterprises seek resilience, cost control, and deployment flexibility across generative AI workloads.”

Facing challenges with practical application, major cloud providers are boosting resources for AI agent lifecycle management, including creation and operationalization, as enterprise-level deployment proves more intricate than anticipated.

Yi Zhang, Senior Analyst at Omdia, said, “Many enterprises still lack standardized building blocks that can support business continuity, customer experience, and compliance at the same time, which is slowing the real-world deployment of AI agents. This is where hyperscalers are increasingly stepping in, using platform-led approaches to make it easier for enterprises to build and run agents in production environments.”

This past October, Omdia released a report forecasting that growth of cloud adoption among communications service providers (CSPs) will double this year. It also forecasted a compound annual growth rate (CAGR) of 7.3% to 2030, resulting in the telco cloud market being worth $24.8 billion.

………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Editor’s Note: Does anyone remember the stupendous increase in fiber optic spending from 1998-2001 till that bubble burst? Caveat Emptor!

………………………………………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://www.telecoms.com/public-cloud/global-cloud-infrastructure-spend-up-25-in-q3

https://www.telecoms.com/public-cloud/telco-investment-in-cloud-infrastructure-is-accelerating-omdia

AI infrastructure spending boom: a path towards AGI or speculative bubble?

Expose: AI is more than a bubble; it’s a data center debt bomb

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

Gartner: AI spending >$2 trillion in 2026 driven by hyperscalers data center investments

AI spending is surging; companies accelerate AI adoption, but job cuts loom large

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

Canalys & Gartner: AI investments drive growth in cloud infrastructure spending

Sovereign AI infrastructure for telecom companies: implementation and challenges

AI Echo Chamber: “Upstream AI” companies huge spending fuels profit growth for “Downstream AI” firms

Custom AI Chips: Powering the next wave of Intelligent Computing

AI infrastructure spending boom: a path towards AGI or speculative bubble?

by Rahul Sharma, Indxx with Alan J Weissberger, IEEE Techblog

Introduction:

The ongoing wave of artificial intelligence (AI) infrastructure investment by U.S. mega-cap tech firms marks one of the largest corporate spending cycles in history. Aggregate annual AI investments, mostly for cloud resident mega-data centers, are expected to exceed $400 billion in 2025, potentially surpassing $500 billion by 2026 — the scale of this buildout rivals that of past industrial revolutions — from railroads to the internet era.[1]

At its core, this spending surge represents a strategic arms race for computational dominance. Meta, Alphabet, Amazon and Microsoft are racing to secure leadership in artificial intelligence capabilities — a contest where access to data, energy, and compute capacity are the new determinants of market power.

AI Spending & Debt Financing:

Leading technology firms are racing to secure dominance in compute capacity — the new cornerstone of digital power:

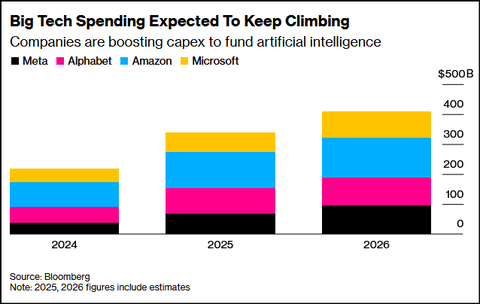

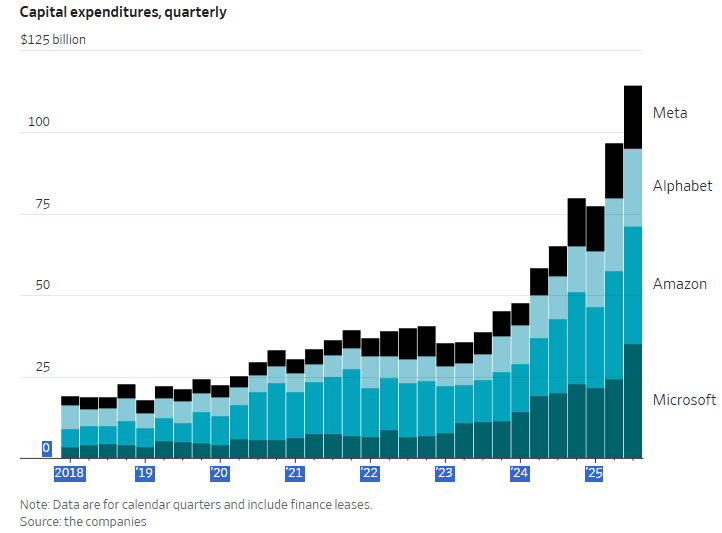

- Meta plans to spend $72 billion on AI infrastructure in 2025.

- Alphabet (Google) has expanded its capex guidance to $91–93 billion.[3]

- Microsoft and Amazon are doubling data center capacity, while AWS will drive most of Amazon’s $125 billion 2026 investment.[4]

- Even Apple, typically conservative in R&D, has accelerated AI infrastructure spending.

Their capex is shown in the chart below:

Analysts estimate that AI could add up to 0.5% to U.S. GDP annually over the next several years. Reflecting this optimism, Morgan Stanley forecasts $2.9 trillion in AI-related investments between 2025 and 2028. The scale of commitment from Big Tech is reshaping expectations across financial markets, enterprise strategies, and public policy, marking one of the most intense capital spending cycles in corporate history.[2]

Meanwhile, OpenAI’s trillion-dollar partnerships with Nvidia, Oracle, and Broadcom have redefined the scale of ambition, turning compute infrastructure into a strategic asset comparable to energy independence or semiconductor sovereignty.[5]

Growth Engine or Speculative Bubble?

As Big Tech pours hundreds of billions of dollars into AI infrastructure, analysts and investors remain divided — some view it as a rational, long-term investment cycle, while others warn of a potential speculative bubble. Yet uncertainty remains — especially around Meta’s long-term monetization of AGI-related efforts.[8]

Some analysts view this huge AI spending as a necessary step towards achieving Artificial General Intelligence (AGI) – an unrealized type of AI that possesses human-level cognitive abilities, allowing it to understand, learn, and adapt to any intellectual task a human can. Unlike narrow AI, which is designed for specific functions like playing chess or image recognition, AGI could apply its knowledge to a wide range of different situations and problems without needing to be explicitly programmed for each one.

Other analysts believe this is a speculative bubble, fueled by debt that can never be repaid. Tech sector valuations have soared to dot-com era levels – and, based on price-to-sales ratios, are well beyond them. Some of AI’s biggest proponents acknowledge the fact that valuations are overinflated, including OpenAI chairman Bret Taylor: “AI will transform the economy… and create huge amounts of economic value in the future,” Taylor told The Verge. “I think we’re also in a bubble, and a lot of people will lose a lot of money,” he added.

Here are a few AI bubble points and charts:

- AI-related capex is projected to consume up to 94% of operating cash flows by 2026, according to Bank of America.[6]

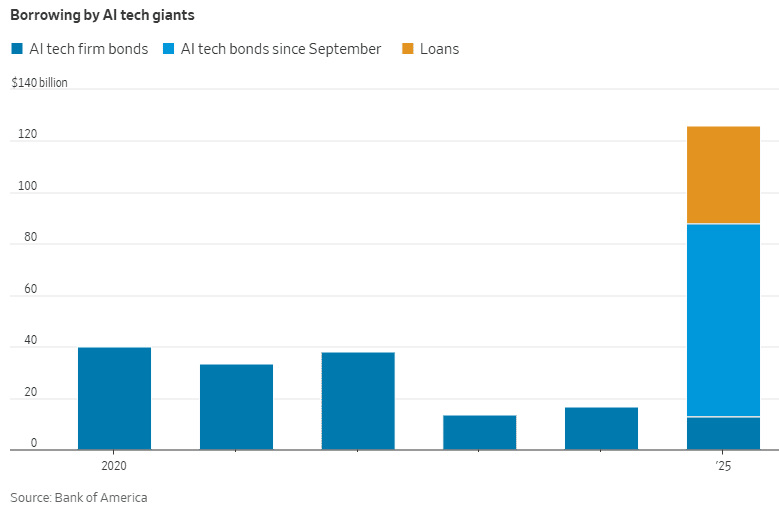

- Over $75 billion in AI-linked corporate bonds have been issued in just two months — a signal of mounting leverage. Still, strong revenue growth from AI services (particularly cloud and enterprise AI) keeps optimism alive.[7]

- Meta, Google, Microsoft, Amazon and xAI (Elon Musk’s company) are all using off-balance-sheet debt vehicles, including special-purpose vehicles (SPVs) to fund part of their AI investments. A slowdown in AI demand could render the debt tied to these SPVs worthless, potentially triggering another financial crisis.

- Alphabet’s (Google’s parent company) CEO Sundar Pichai sees “elements of irrationality” in the current scale of AI investing which is much more than excessive investments during the dot-com/fiber optic built-out boom of the late 1990s. If the AI bubble bursts, Pichai said that no company will be immune, including Alphabet, despite its breakthrough technology, Gemini, fueling gains in the company’s stock price.

…………………………………………………………………………………………………………………..

From Infrastructure to Intelligence:

Executives justify the massive spend by citing acute compute shortages and exponential demand growth:

- Microsoft’s CFO Amy Hood admitted, “We’ve been short on capacity for many quarters” and confirmed that the company will increase its spending on GPUs and CPUs in 2026 to meet surging demand.

- Amazon’s Andy Jassy noted that “every new tranche of capacity is immediately monetized”, underscoring strong and sustained demand for AI and cloud services.

- Google reported billions in quarterly AI revenue, offering early evidence of commercial payoff.

Macro Ripple Effects – Industrializing Intelligence:

AI data centers have become the factories of the digital age, fueling demand for:

- Semiconductors, especially GPUs (Nvidia, AMD, Broadcom)

- Cloud and networking infrastructure (Oracle, Cisco)

- Energy and advanced cooling systems for AI data centers (Vertiv, Schneider Electric, Johnson Controls, and other specialists such as Liquid Stack and Green Revolution Cooling).

| Company Name | Core Expertise | Key Solutions for AI Data Centers |

|---|---|---|

| Vertiv | Critical infrastructure (power & cooling) | Offers full-stack solutions with air and liquid cooling, power distribution units (PDUs), and monitoring systems, including the AI-ready Vertiv 360AI portfolio. |

| Schneider Electric | Energy management & automation | Provides integrated power and thermal management via its EcoStruxure platform, specializing in modular and liquid cooling solutions for HPC and AI applications. |

| Johnson Controls | HVAC & building solutions | Offers integrated, energy-efficient solutions from design to maintenance, including Silent-Aire cooling and YORK chillers, with a focus on large-scale operations. |

| Eaton | Power management | Specializes in electrical distribution systems, uninterruptible power supplies (UPS), and switchgear, which are crucial for reliable energy delivery to high-density AI racks. |

- LiquidStack: A leader in two-phase and modular immersion cooling and direct-to-chip systems, trusted by large cloud and hardware providers.

- Green Revolution Cooling (GRC): Pioneers in single-phase immersion cooling solutions that help simplify thermal management and improve energy efficiency.

- Iceotope: Focuses on chassis-level precision liquid cooling, delivering dielectric fluid directly to components for maximum efficiency and reduced operational costs.

- Asetek: Specializes in direct-to-chip (D2C) liquid cooling solutions and rack-level Coolant Distribution Units (CDUs) for high-performance computing.

- CoolIT Systems: Known for its custom direct liquid cooling technologies, working closely with server OEMs (Original Equipment Manufacturers) to integrate cold plates and CDUs for AI and HPC workloads.

–>This new AI ecosystem is reshaping global supply chains — but also straining local energy and water resources. For example, Meta’s massive data center in Georgia has already triggered environmental concerns over energy and water usage.

Global Spending Outlook:

- According to UBS, global AI capex will reach $423 billion in 2025, $571 billion by 2026 and $1.3 trillion by 2030, growing at a 25% CAGR during the period 2025-2030.

Compute demand is outpacing expectations, with Google’s Gemini saw 130 times rise in AI token usage over the past 18 months, highlighting soaring compute and Meta’s infrastructure needs expanding sharply.[9]

Conclusions:

The AI infrastructure boom reflects a bold, forward-looking strategy by Big Tech, built on the belief that compute capacity will define the next decade’s leaders. If Artificial General Intelligence (AGI) or large-scale AI monetization unfolds as expected, today’s investments will be seen as visionary and transformative. Either way, the AI era is well underway — and the race for computational excellence is reshaping the future of global markets and innovation.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Footnotes:

[1] https://www.investing.com/news/stock-market-news/ai-capex-to-exceed-half-a-trillion-in-2026-ubs-4343520?utm_medium=feed&utm_source=yahoo&utm_campaign=yahoo-www

[2] https://www.venturepulsemag.com/2025/08/01/big-techs-400-billion-ai-bet-the-race-thats-reshaping-global-technology/#:~:text=Big%20Tech’s%20$400%20Billion%20AI%20Bet:%20The%20Race%20That’s%20Reshaping%20Global%20Technology,-3%20months%20ago&text=The%20world’s%20largest%20technology%20companies,enterprise%20strategy%2C%20and%20public%20policy.

[3] https://www.businessinsider.com/big-tech-capex-spending-ai-earnings-2025-10?

[4] https://www.investing.com/analysis/meta-plunged-12-amazon-jumped-11–same-ai-race-different-economics-200669410

[5] https://www.cnbc.com/2025/10/15/a-guide-to-1-trillion-worth-of-ai-deals-between-openai-nvidia.html

[6] https://finance.yahoo.com/news/bank-america-just-issued-stark-152422714.html

[7] https://news.futunn.com/en/post/64706046/from-cash-rich-to-collective-debt-how-does-wall-street?level=1&data_ticket=1763038546393561

[8] https://www.businessinsider.com/big-tech-capex-spending-ai-earnings-2025-10?

[9] https://finance.yahoo.com/news/ai-capex-exceed-half-trillion-093015889.html

……………………………………………………………………………………………………………………………………………………………………………………………………………………………

About the Author:

Rahul Sharma is President & Co-Chief Executive Officer at Indxx – a provider of end-to-end indexing services, data and technology products. He has been instrumental in leading the firm’s growth since 2011. Raul manages Indxx’s Sales, Client Engagement, Marketing and Branding teams while also helping to set the firm’s overall strategic objectives and vision.

Rahul holds a BS from Boston College and an MBA with Beta Gamma Sigma honors from Georgetown University’s McDonough School of Business.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………

References:

Curmudgeon/Sperandeo: New AI Era Thinking and Circular Financing Deals

Expose: AI is more than a bubble; it’s a data center debt bomb

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

FT: Scale of AI private company valuations dwarfs dot-com boom

Amazon’s Jeff Bezos at Italian Tech Week: “AI is a kind of industrial bubble”

AI Data Center Boom Carries Huge Default and Demand Risks

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Nokia in major pivot from traditional telecom to AI, cloud infrastructure, data center networking and 6G

Reuters: US Department of Energy forms $1 billion AI supercomputer partnership with AMD

………………………………………………………………………………………………………………………………………………………………………….

Expose: AI is more than a bubble; it’s a data center debt bomb

We’ve previously described the tremendous debt that AI companies have assumed, expressing serious doubts that it will ever be repaid. This article expands on that by pointing out the huge losses incurred by the AI startup darlings and that AI poster child Open AI won’t have the cash to cover its costs 9which are greater than most analysts assume). Also, we quote from the Wall Street Journal, Financial Times, Barron’s, along with a dire forecast from the Center for Public Enterprise.

In Saturday’s print edition, The Wall Street Journal notes:

OpenAI and Anthropic are the two largest suppliers of generative AI with their chatbots ChatGPT and Claude, respectively, and founders Sam Altman and Dario Amodei have become tech celebrities.

What’s only starting to become clear is that those companies are also sinkholes for AI losses that are the flip side of chunks of the public-company profits.

OpenAI hopes to turn profitable only in 2030, while Anthropic is targeting 2028. Meanwhile, the amounts of money being lost are extraordinary.

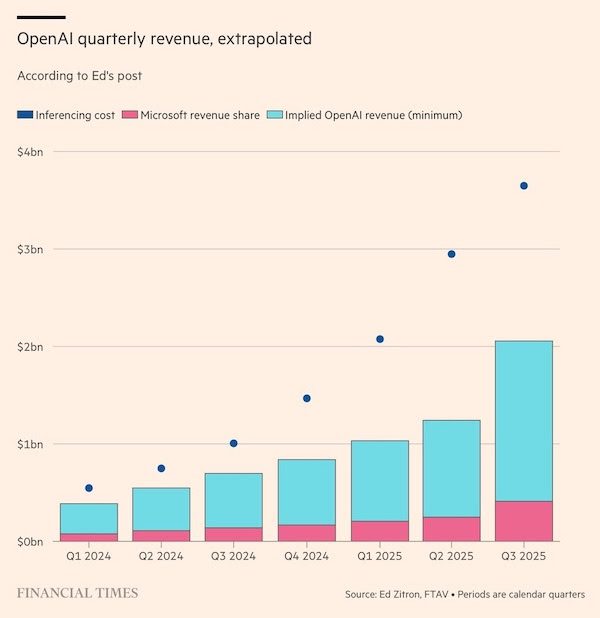

It’s impossible to quantify how much cash flowed from OpenAI to big tech companies. But OpenAI’s loss in the quarter equates to 65% of the rise in underlying earnings of Microsoft, Nvidia, Alphabet, Amazon and Meta together. That ignores Anthropic, from which Amazon recorded a profit of $9.5B from its holding in the loss-making company in the quarter.

OpenAI committed to spend $250 billion more on Microsoft’s cloud and has signed a $300 billion deal with Oracle, $22 billion with CoreWeave and $38 billion with Amazon, which is a big investor in rival Anthropic.

OpenAI doesn’t have the income to cover its costs. It expects revenue of $13 billion this year to more than double to $30 billion next year, then to double again in 2027, according to figures provided to shareholders. Costs are expected to rise even faster, and losses are predicted to roughly triple to more than $40 billion by 2027. Things don’t come back into balance even in OpenAI’s own forecasts until total computing costs finally level off in 2029, allowing it to scrape into profit in 2030.

The losses at OpenAI that has helped boost the profits of Big Tech may, in fact, understate the true nature of the problem. According to the Financial Times:

OpenAI’s running costs may be a lot more than previously thought, and that its main backer Microsoft is doing very nicely out of their revenue share agreement.

OpenAI appears to have spent more than $12.4bn at Azure on inference compute alone in the last seven calendar quarters. Its implied revenue for the period was a minimum of $6.8bn. Even allowing for some fudging between annualised run rates and period-end totals, the apparent gap between revenues and running costs is a lot more than has been reported previously.

The apparent gap between revenues and running costs is a lot more than has been reported previously. If the data is accurate, then it would call into question the business model of OpenAI and nearly every other general-purpose LLM vendor.

Also, the financing needed to build out the data centers at the heart of the AI boom is increasingly becoming an exercise in creative accounting. The Wall Street Journal reports:

The Hyperion deal is a Frankenstein financing that combines elements of private-equity, project finance and investment-grade bonds. Meta needed such financial wizardry because it already issued a $30B bond in October that roughly doubled its debt load overnight.

Enter Morgan Stanley, with a plan to have someone else borrow the money for Hyperion. Blue Owl invested about $3 billion for an 80% private-equity stake in the data center, while Meta retained 20% for the $1.3 billion it had already spent. The joint venture, named Beignet Investor after the New Orleans pastry, got another $27 billion by issuing bonds that pay off in 2049, $18 billion of which Pimco purchased. That debt is on Beignet’s balance sheet, not Meta’s.

Dan Fuss, vice chairman of Loomis Sayles told Barrons: “We are good at taking credit risk,” Dan said, cheerfully admitting to having the scars to show for it. That is, he added, if they know the credit. But that’s become less clear with the recent spate of mind-bendingly complex megadeals, with myriad entities funding multibillion-dollar data centers. Fuss thinks current data-center deals are too speculative. The risk is too great and future revenue too uncertain. And yields aren’t enough to compensate, he concluded.

Increased wariness about monster hyper-scaler borrowings has sent the cost of insuring their debt against default soaring. Credit default swaps (CDS) more than doubled for Oracle since September, after it issued $18 billion in public bonds and took out a $38 billion private loan. CoreWeave’s CDS gapped higher this past week, mirroring the slide of the data-center company’s stock.

According to the Bank Credit Analyst (BCA), capex busts weigh on the economy, which further hits asset prices, the firm says. Following the dot-com bust, a housing bubble grew, which burst in the 2008-09 financial crisis. “It is far from certain that a new bubble will emerge (after the AI bubble bursts) this time around, in which case the resulting recession could be more severe than the one in 2001,” BCA notes.

………………………………………………………………………………………………………………………………………………

The widening gap between the expenditures needed to build out AI data centers and the cash flows generated by the products they enable creates a colossal risk which could crash asset values of AI companies. The Center for Public Enterprise reports that it’s “Bubble or Nothing.”

Should economic conditions in the tech sector sour, the burgeoning artificial intelligence (AI) boom may evaporate—and, with it, the economic activity associated with the boom in data center development.

Circular financing, or “roundabouting,” among so-called hyperscaler tenants—the leading tech companies and AI service providers—create an interlocking liability structure across the sector. These tenants comprise an incredibly large share of the market and are financing each others’ expansion, creating concentration risks for lenders and shareholders.

Debt is playing an increasingly large role in the financing of data centers. While debt is a quotidian aspect of project finance, and while it seems like hyperscaler tech companies can self-finance their growth through equity and cash, the lack of transparency in some recent debt-financed transactions and the interlocked liability structure of the sector are cause for concern.

If there is a sudden stop in new lending to data centers, Ponzi finance units ‘with cash flow shortfalls will be forced to try to make position by selling out position’—in other words to force a fire sale—which is ‘likely to lead to a collapse of asset values.’

The fact that the data center boom is threatened by, at its core, a lack of consumer demand and the resulting unstable investment pathways, is itself an ironic miniature of the U.S. economy as a whole. Just as stable investment demand is the linchpin of sectoral planning, stable aggregate demand is the keystone in national economic planning. Without it, capital investment crumbles.

……………………………………………………………………………………………………………..

Postscript (November 23, 2025):

In addition to cloud/hyperscaler AI spending, AI start-ups (especially OpenAI) and newer IT infrastructure companies (like Oracle) play a prominent role. It’s often a “scratch my back and I’ll scratch yours” type of deal. Let’s look at the “circular financing” arrangement between Nvidia and OpenAI where capital flows from Nvidia to OpenAI and then back to Nvidia. That ensures Nvidia a massive, long-term customer and providing OpenAI with the necessary capital and guaranteed access to critical, high-demand hardware. Here’s the scoop:

- Nvidia has agreed to invest up to $100 billion in OpenAI over time. This investment will be in cash, likely for non-voting equity shares, and will be made in stages as specific data center deployment milestones are met.

- OpenAIhas committed to building and deploying at least 10 gigawatts of AI data center capacity using Nvidia’s silicon and equipment, which will involve purchasing millions of Nvidia expensive GPU chips.

Here’s the Circular Flow of this deal:

- Nvidia provides a cash investment to OpenAI.

- OpenAI uses that capital (and potentially raises additional debt using the commitment as collateral) to build new data centers.

- OpenAI then uses the funds to purchase Nvidia GPUs and other data center infrastructure.

- The revenue from these massive sales flows back to Nvidia, helping to justify its soaring stock price and funding further investments.

What’s wrong with such an arrangement you ask? Anyone remember the dot-com/fiber optic boom and bust? Critics have drawn parallels to the “vendor financing” practices of the dot-com era, arguing these interconnected deals could create a “mirage of growth” and potentially an AI bubble, as the actual organic demand for the products is difficult to assess when companies are essentially funding their own sales.

However, supporters note that, unlike the dot-com bubble, these deals involve the creation of tangible physical assets (data centers and chips) and reflect genuine, booming demand for AI compute capacity although it’s not at all certain how they’ll be paid for.

There’s a similar cozy relationship with the $1B Nvidia invested in Nokia with the Finnish company now planning to ditch Marvell’s silicon and replace it by buying the more expensive, power hungry Nvidia GPUs for its wireless network equipment. Nokia, has only now become a strong supporter of Nvidia’s AI RAN (Radio Access Network), which has many telco skeptics.

………………………………………………………………………………………………………………………………………………….

References:

https://www.wsj.com/tech/ai/big-techs-soaring-profits-have-an-ugly-underside-openais-losses-fe7e3184

https://www.ft.com/content/fce77ba4-6231-4920-9e99-693a6c38e7d5

https://www.wsj.com/tech/ai/three-ai-megadeals-are-breaking-new-ground-on-wall-street-896e0023

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

AI Data Center Boom Carries Huge Default and Demand Risks

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

Gartner: AI spending >$2 trillion in 2026 driven by hyperscalers data center investments

Amazon’s Jeff Bezos at Italian Tech Week: “AI is a kind of industrial bubble”

FT: Scale of AI private company valuations dwarfs dot-com boom

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

- Meta Platforms says it continues to experience capacity constraints as it simultaneously trains new AI models and supports existing product infrastructure. Meta CEO Mark Zuckerberg described an unsatiated appetite for more computing resources that Meta must work to fulfill to ensure it’s a leader in a fast-moving AI race. “We want to make sure we’re not underinvesting,” he said on an earnings call with analysts Wednesday after posting third-quarter results. Meta signaled in the earnings report that capital expenditures would be “notably larger” next year than in 2025, during which Meta expects to spend as much as $72 billion. He indicated that the company’s existing advertising business and platforms are operating in a “compute-starved state.” This condition persists because Meta is allocating more resources toward AI research and development efforts rather than bolstering existing operations.

- Microsoft reported substantial customer demand for its data-center-driven services, prompting plans to double its data center footprint over the next two years. Concurrently, Amazon is working aggressively to deploy additional cloud capacity to meet demand. Amy Hood, Microsoft’s chief financial officer, said: “We’ve been short [on computing power] now for many quarters. I thought we were going to catch up. We are not. Demand is increasing.” She further elaborated, “When you see these kinds of demand signals and we know we’re behind, we do need to spend.”

- Alphabet (Google’s parent company) reported that capital expenditures will jump from $85 billion to between $91 billion and $93 billion. Google CFO Anat Ashkenazi said the investments are already yielding returns: “We already are generating billions of dollars from AI in the quarter. But then across the board, we have a rigorous framework and approach by which we evaluate these long-term investments.”

- Amazon has not provided a specific total dollar figure for its planned AI investment in 2026. However, the company has announced it expects its total capital expenditures (capex) in 2026 to be even higher than its 2025 projection of $125 billion, with the vast majority of this spending dedicated to AI and related infrastructure for Amazon Web Services (AWS).

- Apple: Announced it is also increasing its AI investments, though its overall spending remains smaller in comparison to the other tech giants.

As big as the spending projections were this week, they look pedestrian compared with OpenAI, which has announced roughly $1 trillion worth of AI infrastructure deals of late with partners including Nvidia , Oracle and Broadcom.

Despite the big capex tax write-offs (due to the 2025 GOP tax act) there is a large degree of uncertainty regarding the eventual outcomes of this substantial AI infrastructure spending. The companies themselves, along with numerous AI proponents, assert that these investments are essential for machine-learning systems to achieve artificial general intelligence (AGI), a state where they surpass human intelligence.

Yet skeptics question whether investing billions in large-language models (LLMs), the most prevalent AI system, will ultimately achieve that objective. They also highlight the limited number of paying users for existing technology and the prolonged training period required before a global workforce can effectively utilize it.

During investor calls following the earnings announcements, analysts directed incisive questions at company executives. On Microsoft’s call, one analyst voiced a central market concern, asking: “Are we in a bubble?” Similarly, on the call for Google’s parent company, Alphabet, another analyst questioned: “What early signs are you seeing that gives you confidence that the spending is really driving better returns longer term?”

Bank of America (BofA) credit strategists Yuri Seliger and Sohyun Marie Lee write in a client note that capital spending by five of the Magnificent Seven megacap tech companies (Amazon.com, Alphabet, and Microsoft, along with Meta and Oracle) has been growing even faster than their prodigious cash flows. “These companies collectively may be reaching a limit to how much AI capex they are willing to fund purely from cash flows,” they write. Consensus estimates of AI capex suggest will climb to 94% of operating cash flows, minus dividends and share repurchases, in 2025 and 2026, up from 76% in 2024. That’s still less than 100% of cash flows, so they don’t need to borrow to fund spending, “but it’s getting close,” they add.

………………………………………………………………………………………………………………………………………………………………….

Google, which projected a rise in its full-year capital expenditures from $85 billion to a range of $91 billion to $93 billion, indicated that these investments were already proving profitable. Google’s Ashkenazi stated: “We already are generating billions of dollars from AI in the quarter. But then across the board, we have a rigorous framework and approach by which we evaluate these long-term investments.”

Microsoft reported that it expects to face capacity shortages that will affect its ability to power both its current businesses and AI research needs until at least the first half of the next year. The company noted that its cloud computing division, Azure, is absorbing “most of the revenue impact.”

Amazon informed investors of its expedited efforts to bring new capacity online, citing its ability to immediately monetize these investments.

“You’re going to see us continue to be very aggressive in investing capacity because we see the demand,” said Amazon Chief Executive Andy Jassy. “As fast as we’re adding capacity right now, we’re monetizing it.”

Meta’s chief financial officer, Susan Li, stated that the company’s capital expenditures—which have already nearly doubled from last year to $72 billion this year—will grow “notably larger” in 2026, though specific figures were not provided. Meta brought this year’s biggest investment-grade corporate bond deal to market, totaling some $30 billion, the latest in a parade of recent data-center borrowing.

Apple confirmed during its earnings call it is also increasing investments in AI . However, its total spending levels remain significantly lower compared to the outlays planned by the other major technology firms.

Skepticism and Risk:

While proponents argue the investments are necessary for AGI and offer a competitive advantage, skeptics question if huge spending (capex) on AI infrastructure and large-language models will achieve this goal and point to limited paying users for current AI technology. Meta CEO Zuckerberg addressed this by telling investors the company would “simply pivot” if its AGI spending strategy proves incorrect.

The mad scramble by mega tech companies and Open AI to build AI data centers is largely relying on debt markets, with a slew of public and private mega deals since September. Hyperscalers would have to spend 94% of operating cash flow to pay for their AI buildouts so are turning to debt financing to help defray some of that cost, according to Bank of America. Unlike earnings per share, cash flow can’t be manipulated by companies. If they spend more on AI than they generate internally, they have to finance the difference.

Hyperscaler debt taken on so far this year have raised almost as much money as all debt financings done between 2020 and 2024, the BofA research said. BofA calculates $75 billion of AI-related public debt offerings just in the past two months!

In bubbles, everyone gets caught up in the idea that spending on the hot theme will deliver vast profits — eventually. When the bubble is big enough, it shifts the focus of the market as a whole from disliking capital expenditure, and hating speculative capital spending in particular, to loving it. That certainly seems the case today with surging AI spending. For much more, please check-out the References below.

Postscript: November 23, 2025:

In this new AI era, consumers and workers are not what drives the economy anymore. Instead, it’s spending on all things AI, mostly with borrowed money or circular financing deals.

BofA Research noted that Meta and Oracle issued $75 billion in bonds and loans in September and October 2025 alone to fund AI data center build outs, an amount more than double the annual average over the past decade. They warned that “The AI boom is hitting a money wall” as capital expenditures consume a large portion of free cash flow. Separately, a recent Bank of America Global Fund Manager Survey found that 53% of participating fund managers felt that AI stocks had reached bubble proportions. This marked a slight decrease from a record 54% in the prior month’s survey, but the concern has grown over time, with the “AI bubble” cited as the top “tail risk” by 45% of respondents in the November 2025 poll.

JP Morgan Chase estimates up to $7 trillion of AI spending will be with borrowed money. “The question is not ‘which market will finance the AI-boom?’ Rather, the question is ‘how will financings be structured to access every capital market?’ according to strategists at the bank led by Tarek Hamid.

As an example of AI debt financing, Meta did a $27 billion bond offering. It wasn’t on their balance sheet. They paid 100 basis points over what it would cost to put it on their balance sheet. Special purpose vehicles happen at the tail end of the cycle, not the early part of the cycle, notes Rajiv Jain of GQG Partners.

References:

IBM and Groq Partner to Accelerate Enterprise AI Inference Capabilities

IBM and Groq [1.] today announced a strategic market and technology partnership designed to give clients immediate access to Groq’s inference technology — GroqCloud, on watsonx Orchestrate – providing clients high-speed AI inference capabilities at a cost that helps accelerate agentic AI deployment. As part of the partnership, Groq and IBM plan to integrate and enhance RedHat open source vLLM technology with Groq’s LPU architecture. IBM Granite models are also planned to be supported on GroqCloud for IBM clients.

………………………………………………………………………………………………………………………………………………….

Note 1. Groq is a privately held company founded by Jonathan Ross in 2016. As a startup, its ownership is distributed among its founders, employees, and a variety of venture capital and institutional investors including BlackRock Private Equity Partners. Groq developed the LPU and GroqCloud to make compute faster and more affordable. The company says it is trusted by over two million developers and teams worldwide and is a core part of the American AI Stack.

NOTE that Grok, a conversational AI assistant developed by Elon Musk’s xAI is a completely different entity.

………………………………………………………………………………………………………………………………………………….

Enterprises moving AI agents from pilot to production still face challenges with speed, cost, and reliability, especially in mission-critical sectors like healthcare, finance, government, retail, and manufacturing. This partnership combines Groq’s inference speed, cost efficiency, and access to the latest open-source models with IBM’s agentic AI orchestration to deliver the infrastructure needed to help enterprises scale.

Powered by its custom LPU, GroqCloud delivers over 5X faster and more cost-efficient inference than traditional GPU systems. The result is consistently low latency and dependable performance, even as workloads scale globally. This is especially powerful for agentic AI in regulated industries.

For example, IBM’s healthcare clients receive thousands of complex patient questions simultaneously. With Groq, IBM’s AI agents can analyze information in real-time and deliver accurate answers immediately to enhance customer experiences and allow organizations to make faster, smarter decisions.

This technology is also being applied in non-regulated industries. IBM clients across retail and consumer packaged goods are using Groq for HR agents to help enhance automation of HR processes and increase employee productivity.

“Many large enterprise organizations have a range of options with AI inferencing when they’re experimenting, but when they want to go into production, they must ensure complex workflows can be deployed successfully to ensure high-quality experiences,” said Rob Thomas, SVP, Software and Chief Commercial Officer at IBM. “Our partnership with Groq underscores IBM’s commitment to providing clients with the most advanced technologies to achieve AI deployment and drive business value.”

“With Groq’s speed and IBM’s enterprise expertise, we’re making agentic AI real for business. Together, we’re enabling organizations to unlock the full potential of AI-driven responses with the performance needed to scale,” said Jonathan Ross, CEO & Founder at Groq. “Beyond speed and resilience, this partnership is about transforming how enterprises work with AI, moving from experimentation to enterprise-wide adoption with confidence, and opening the door to new patterns where AI can act instantly and learn continuously.”

IBM will offer access to GroqCloud’s capabilities starting immediately and the joint teams will focus on delivering the following capabilities to IBM clients, including:

- High speed and high-performance inference that unlocks the full potential of AI models and agentic AI, powering use cases such as customer care, employee support and productivity enhancement.

- Security and privacy-focused AI deployment designed to support the most stringent regulatory and security requirements, enabling effective execution of complex workflows.

- Seamless integration with IBM’s agentic product, watsonx Orchestrate, providing clients flexibility to adopt purpose-built agentic patterns tailored to diverse use cases.

The partnership also plans to integrate and enhance RedHat open source vLLM technology with Groq’s LPU architecture to offer different approaches to common AI challenges developers face during inference. The solution is expected to enable watsonx to leverage capabilities in a familiar way and let customers stay in their preferred tools while accelerating inference with GroqCloud. This integration will address key AI developer needs, including inference orchestration, load balancing, and hardware acceleration, ultimately streamlining the inference process.

Together, IBM and Groq provide enhanced access to the full potential of enterprise AI, one that is fast, intelligent, and built for real-world impact.

References:

FT: Scale of AI private company valuations dwarfs dot-com boom

AI adoption to accelerate growth in the $215 billion Data Center market

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

FT: Scale of AI private company valuations dwarfs dot-com boom

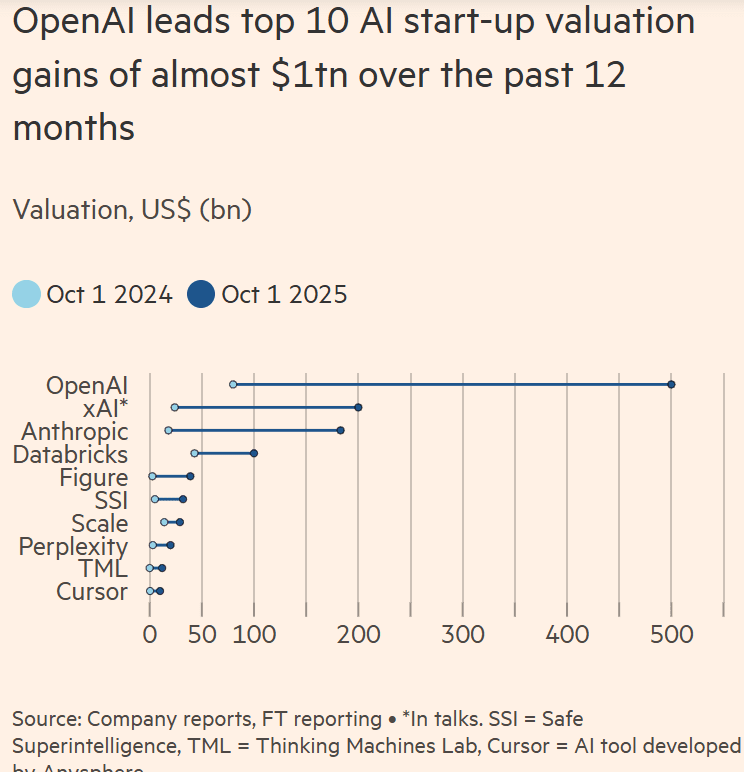

The Financial Times reports that ten loss making artificial intelligence (AI) start-ups have gained close to $1 trillion in private market valuation in the past 12 months, fuelling fears about a bubble in private markets that is much greater than the dot com bubble at the end of the 20th century. OpenAI leads the pack with a $500 billion valuation, but Anthropic and xAI have also seen their values march higher amid a mad scramble to buy into emerging AI companies. Smaller firms building AI applications have also surged, while more established businesses, like Databricks, have soared after embracing the technology.

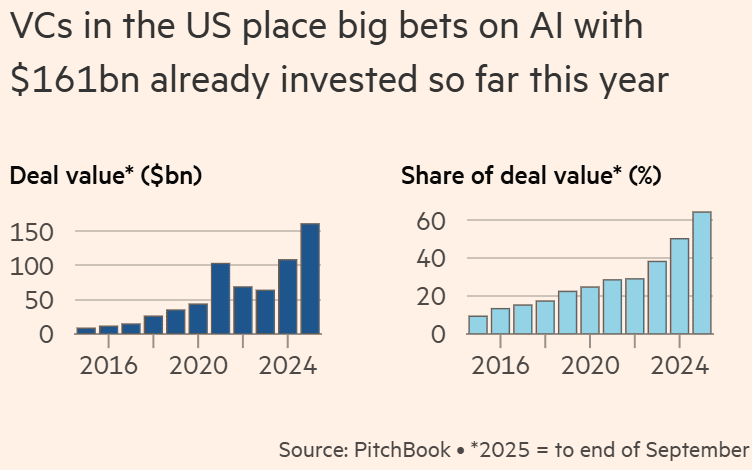

U.S. venture capitalists (VCs) have poured $161 billion into artificial intelligence startups this year — roughly two-thirds of all venture spending, according to PitchBook — even as the technology’s commercial payoff remains elusive. VCs are on track to spend well over $200bn on AI companies this year.

Most of that money has gone to just 10 companies, including OpenAI, Anthropic, Databricks, xAI, Perplexity, Scale AI, and Figure AI, whose combined valuations have swelled by nearly $1 trillion, Financial Times calculations show. Those AI start-ups are all burning cash with no profits forecasted for many years.

Start-ups with about $5mn in annual recurring revenue, a metric used by fast-growing young businesses to provide a snapshot of their earnings, are seeking valuations of more than $500mn, according to a senior Silicon Valley venture capitalist.

Valuing unproven businesses at 100 times their earnings or more dwarfs the excesses of 2021, he added: “Even during peak Zirp [zero-interest rate policies], these would have been $250mn-$300mn valuations.”

“The market is investing as if all these companies are outliers. That’s generally not the way it works out,” he said. VCs typically expect to lose money on most of their bets, but see one or two pay the rest off many times over.

“There will be casualties. Just like there always will be, just like there always is in the tech industry,” said Marc Benioff, co-founder and chief executive of Salesforce, which has invested heavily in AI. He estimates $1tn of investment on AI might be wasted, but that the technology will ultimately yield 10 times that in new value.

“The only way we know how to build great technology is to throw as much against the wall as possible, see what sticks, and then focus on the winners,” he added.

“Of course there’s a bubble,” said Hemant Taneja, chief executive of General Catalyst, which raised an $8 billion fund last year and has backed Anthropic and Mistral. “Bubbles align capital and talent around new trends. There’s always some destruction, but they also produce lasting innovation.”

Venture investors have weathered cycles of boom and bust before — from the dot-com crash in 2000 to the software downturn in 2022 — but the current wave of AI funding is unprecedented. In 2000, VCs invested $10.5 billion in internet startups; in 2021, they deployed $135 billion into software firms. This year, they are on pace to exceed $200 billion in AI. “We’ve gone from the doldrums to full-on FOMO,” said one investment executive.

OpenAI and its start-up peers are competing with Meta, Google, Microsoft, Amazon, IBM, and others in a hugely capital-intensive race to train ever-better models, meaning the path to profitability is also likely to be longer than for previous generations of start-ups.

Backers are betting that AI will open multi-trillion-dollar markets, from automated coding to AI friends or companionship. Yet some valuations are testing credulity. Startups generating about $5 million in annual recurring revenue are seeking valuations above $500 million, a Silicon Valley investor said — 100 times revenue, surpassing even the excesses of 2021. “The market is behaving as if every company will be an outlier,” he said. “That’s rarely how it works.”

The enthusiasm has spilled into public markets. Shares of Nvidia, AMD, Broadcom, and Oracle have collectively gained hundreds of billions in market value from their ties to OpenAI. But those gains could unwind quickly if questions about the startup’s mounting losses and financial sustainability persist.

Sebastian Mallaby, author of The Power Law, summed it up beautifully:

“The logic among investors is simple — if we get AGI (Artificial General Intelligence, which would match or exceed human thinking), it’s all worth it. If we don’t, it isn’t…. “It comes down to these articles of faith about Sam’s (Sam Altman of OpenAI) ability to work it out.”

References:

https://www.ft.com/content/59baba74-c039-4fa7-9d63-b14f8b2bb9e2

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

Amazon’s Jeff Bezos at Italian Tech Week: “AI is a kind of industrial bubble”

Gartner: AI spending >$2 trillion in 2026 driven by hyperscalers data center investments

AI Data Center Boom Carries Huge Default and Demand Risks

Canalys & Gartner: AI investments drive growth in cloud infrastructure spending