Uncategorized

Business Research Company: Double Digit Growth Forecast for China’s Telecom Market

Overview:

China’s telecom market grew from $289.6 billion in 2014 to $418.8 billion in 2018 at a compound annual growth rate (CAGR) of 9.7%. The market is expected to grow from $418.8 billion in 2018 to $649.3 billion in 2022 at a CAGR of 11.6% according to The Business Research Company (TBRC’s) Global Market Model.

[Switzerland is expected to be the fastest growing country within the telecom market at a CAGR of 16.5% followed by Denmark at 14.5% and Iraq at 13.2% respectively.]

China was the second largest country in the global telecom market. It was worth $418.8 billion in 2018, accounting for 15.6% of the global telecom market, followed by Japan at 8.3% and India at 3 % respectively. China’s telecom market accounts for 42.5 % of the Asia Pacific’s telecom market in 2018.

Major telecom companies in China include: China Mobile, China Telecom, China Unicom, China Netcom, Companhia de Telecomunicações de Macau (Macau was previously a Portuguese colony now owned by China), and UTStarcom.

Editor’s Note: The first three companies listed (China Mobile, China Telecom, China Unicom) are all state owned and are by far the largest telecom companies in China. We have no idea why neither Huawei or ZTE are listed as major telecom infrastructure companies like UTStarcom.

…………………………………………………………………………………………………………………………

Market Definition:

The telecoms market consists of sales of telecommunications goods and services by entities (organizations, sole traders and partnerships) that apply communication hardware equipment and software for the transmission and switching of voice, data, text and video. This market includes segments such as wired telecommunications carriers, wireless telecommunications carriers and communications hardware. The telecoms market also includes sales of goods such as GPS equipment, cellular telephones, switching equipment.

………………………………………………………………………………………………………………………………………………..

Discussion:

The satellite and telecommunication resellers was the fastest growing segment within China’s telecom market at a CAGR of 14.6% followed by wired telecommunication carriers at 11.2% and wireless telecommunication carriers at 10.4% from 2014 to 2018. The satellite and telecommunication resellers is expected to be the fastest growing segment during the forecast period from 2018 to 2022 at a CAGR of 16.2% followed by wired telecommunication carriers at 12.8% and wireless telecommunication carriers at 11.9%.

The telecom market is segmented in to wireless telecommunication carriers, wired telecommunication carriers, communications hardware, and satellite and telecommunication resellers. The wireless telecommunication carriers market mainly consists of sub segments such as cellular/mobile telephone services, and wireless internet services. the wired telecommunication carriers market consists of sub segments such as broadband internet services, fixed telephony services, and direct-to-home(DTH) services. The communications hardware market includes sub segments such as general communication equipment, broadcast communications equipment, and telecom infrastructure equipment. The satellite and telecommunication resellers market has satellite telecommunications, telecommunication resellers, and others – satellite and telecommunication resellers as its sub segments.

China’s Telecom Accounts For More Than 3% Of The Country’s GDP in 2018:

The table below shows telecom market size as a proportion of China’s GDP during 2014 – 2022.

Year 2014 2015 2016 2017 2018 2019 2020 2021 2022 HCAGR FCAGR Percentage of GDP 2.74% 2.96% 3.00% 3.04% 3.08% 3.13% 3.18% 3.23% 3.28% 2.98% 1.58%

China’s telecom market grew at a CAGR of 9.7% from 2014 to 2018, while China’s GDP grew at a CAGR of 6.49% during the same period. China’s telecom percentage share in China’s GDP increased from 2.74% to 3.08% during the same period. China’s telecom share of China’s GDP is expected to reach to 3.28% in 2022.

China’s Per Capita Expenditure On Telecom Was Less Than That Of Global Expenditure In 2018

The table below shows China’s per capita expenditure on telecom during 2014 – 2022.

Year 2014 2015 2016 2017 2018 2019 2020 2021 2022 HCAGR FCAGR Per capita Expenditure ($) 211.73 241.26 248.03 271.63 301.28 334.74 373.84 415.20 461.29 9.22% 11.24%

China’s telecom market grew at a CAGR of 9.7% from 2014 to 2018, while China’s population grew at a CAGR of 0.41% during the same period. China’s per capita expenditure on telecom increased from $211.73 to $301.28 from 2014 to 2018 and expected to reach to $461.29 in 2022.

…………………………………………………………………………………………………………………

Major Trends Shaping The Telecom Market Include:

1. Over-The-Top Services Are Becoming Popular

OTT services are becoming popular as this technology enables customers to access audio and video content through internet. Over-the-Top (OTT) services refers to accessing film or TV content via Internet without subscribing to cable or paytv services. It delivers messaging, voice and video content directly to the consumers over the internet.

2. Investments In Cyber Security

Telecommunication providers are investing in cyber security solutions to protect telecom infrastructure and datafrom cyberattacks. Cybersecurity refers to the set of techniques used to protect the network integrity and data from unauthorized access. Telecom operators are investing more into cybersecurity solutions to manage cyber security. For Instance, leading telecommunication companies like Telefonica, Softbank, Etisalat and SingTel have signed an agreement to create the first global cyber security partnership

3. Software Defined Wide Area Networking

Software defined wide area networking (SD-WAN) application is widely used in enterprise networking to reduce the network traffic. Software defined wide area networking (SD-WAN) is a specific application of software-defined networking (SDN) technology applied in WAN connections which connects enterprise networks over large distances. It improves connectivity and security in a cloud environment due to its scalability across numerous locations. It also provides encrypted data across the connectivity points, firewalls and application-based security.i For Instance, some of the major companies providing this technology include Silver Peak, Cisco, VMware, Riverbed and Citrix.

4. Green Wireless Network

A rapid increase in energy consumption in wireless networks has been recognized as a major threat for environmental protection and sustainable development. Due to access to the high-speed internet provided by the next generation wireless networks and increased smartphone usage, the requirement for global access to data has risen sharply, triggering a dramatic expansion of network infrastructures and escalating energy demand. To meet these challenges green evolution has become an urgent priority for wireless network service providers.

5. Voice over IP (VoIP) services:

VoIP is the transmission of voice and multimedia content over Internet Protocol (IP) networks. VoIP services are becoming popular as the audio quality is superior than traditional wired networks. With more networks investing to upgrade to 5G, there has been a substantial improvement in the quality of VoIP. 5G will eliminate common troubleshooting issues like call jitter, echoes and packet loss. AI is also beginning to be an integral part of system restoration. With the latest advancements in AI, identifying and adjusting poor quality calls even before answering them has become much easier. AI helps in restoring call quality quickly and efficiently without the need for human intervention.

…………………………………………………………………………………………………………………………………………

IDC on China’s Telecom Market:

In 2018, the capital expenditure of China’s three major operators (China Mobile, China Telecom, China Unicom) was US$4.34 billion and China was the second-largest operator expenditure market. In addition, in 2018, Chinese mobile subscribers reached 1.57 billion, which is the largest single mobile communication market in the world. On June 6, 2019, China formally issued 5G licenses, and the construction of 5G will accelerate.

With the business transformation and network transformation of operators, the impact of telecommunications industry on traditional infrastructure is also growing. SDN/NFV, cloud, and edge computing are becoming the new mainstream technology, and the operator market has great potential for IT vendors.

…………………………………………………………………………………………………………………………………………

………………………………………………………………………………………………………………………………………….

The Business Research Company’s reports are based on the methodology below:

Our data sets are created using a wide range of proprietary and public sources including leading government bodies, associations, trade journals, market intelligence reports and trade magazines. Data is modeled based on hard data, extrapolation, regression analysis based on known macro data inputs, interpolation between hard figures, comparisons with other geographies and markets, price estimations, and qualitative inputs. Data is triangulated within our unique market data model covering an exhaustive list of 600+ markets across 48 countries and 7 regions. Comparable data is used for sanity check and trend analysis. For example, our global market value data is compared to unit sales and price data for the relevant market as well as relevant macro-economic data sets in order to establish validity.

Market value is defined as the revenues earned by organizations for products and services within the specified market. The break down by geography is revenue generated within the specific industry by organizations in the specified geography, irrespective of where they are produced.

Market value and forecasts used in market share calculation and potential gain of the company is sourced from TBRC’s Global Market Model (more below).

…………………………………………………………………………………………………………………………………………….

The Global Market Model is a comprehensive database of integrated market information which covers historic, current and forecast market information. This database helps in drawing multiple conclusions, exploring market opportunities and taking effective business decisions.

Global Market Model’s methodology ensures that the data is of the highest quality. It starts with high standard data sources and correlation based modelling techniques. This is supported by TBRC’s market expertise and thousands of expert interviews conducted each year to verify the data.

The data sets on the global market model are created using a wide range of proprietary and public sources including leading government bodies, associations, trade journals, market intelligence reports and trade magazines. Data is modeled based on hard data, extrapolation, regression analysis based on known macro data inputs, interpolation between hard figures, comparisons with other geographies and markets, price estimations, and qualitative inputs. Data is triangulated within our unique market data model covering an exhaustive list of 600+ markets across 48 countries and 7 regions. Comparable data is used for sanity check and trend analysis. For example, our global market value data is compared to unit sales and price data for the relevant market as well as relevant macro-economic datasets in order to establish validity.

Analysis is drawn from our Consultants’ wide range of industry and research experience as well as public and proprietary sources. Consultants are trained in research techniques and ethics by the Market Research Society.

Every year The Business Research Company carries out thousands of interviews with senior executives and industry experts across hundreds of markets. Through these interviews we develop our internal understanding of markets and geographies and cross reference our understanding of global markets with expert feedback utilizing ‘Delphic’ research methodologies.

The Business Research Company prides itself on the quality and validity of its data and analysis. Our unique ‘end noted’ referencing approach allows the user to trace our market numbers and analysis back to the specific data sources they were derived from.

Note: All currency conversions are done on the basis of 2018 exchange rates.

………………………………………………………………………………………………………………………………

References:

TBRC Business Research Pvt Ltd-Document BRCOMM0020200213eg2d0000f

https://en.wikipedia.org/wiki/Telecommunications_industry_in_China

NEC and Mavenir collaborate to deliver 5G Open vRAN platform

NEC Corp. and Mavenir entered a collaboration agreement to deliver a 5G Open virtualized RAN (vRAN) platform to the Japanese enterprise market. This move will open up Local/Private 5G Network opportunities for enterprises, regional authorities and other organizations, according to the companies.

Under this collaboration, NEC and Mavenir said they will jointly work on 5G Open vRAN and Local 5G business developments and create a simple and cost-efficient ecosystem in the market. The collaboration will bring together NEC’s expertise in IT, network and system integration and Mavenir’s cloud-native network technology.

Editor’s Note:

Moving to a virtual RAN (vRAN) may offer operators important benefits, including a reduced capital expenditure (CAPEX) and operational expenditure (OPEX) over time. Additionally, RAN transformation can be boosted by network functions virtualization (NFV) technology, which changes the typical network architecture from hardware-based to software-defined infrastructure and decouples the baseband functions from the underlying hardware. In turn, the architecture is more flexible, agile, and easier to maintain, allowing operators to launch new services to market faster than ever before.

Cisco created and announced Open vRAN at Mobile World Congress 2018. Conversations with key network operator customers, as well as our partners, made it apparent that something needed to change and they thought we could help. Since then, it’s been a whirlwind ride – working with customers to better define this future and the key elements, building solutions with our partners, innovating in the market to explore new service designs, and contributing to the process of defining industry specifications.

On that last topic, sometimes there is a little confusion between Open vRAN and O-RAN due to the similar names and similar principles. The naming similarity was coincidental, but not surprising, given both are fairly descriptive of the opportunity. O-RAN (Open RAN Alliance) describes themselves well on their website: “The O-RAN Alliance was founded by operators to clearly define requirements and help build a supply chain eco-system to realize its objectives.” They have extensive details available on their website and in their whitepaper.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Mavenir delivers an Open vRAN platform that provides strategic differentiation by enabling multi-source Remote Radio Units (RRUs) to interwork with the virtualized, containerized, Cloud Base Band software over Ethernet Fronthaul (FH), using the O-RAN open interface, overcoming the traditional constraints of the proprietary walled garden specifications used by the other traditional equipment vendors.

![]()

“We are excited to collaborate with NEC, as we move together toward open, virtualized networks,” said Pardeep Kohli, Mavenir’s President and CEO. “Mavenir’s vRAN and NEC’s radio naturally come together to quickly and easily bring new and innovative solutions to the Japanese Enterprise Market.”

NEC actively promotes an open, virtualized infrastructure model in support of the 5G era, using IT, orchestration and network expertise. Moreover, the NEC ecosystem contributes to vRAN via inter-operability testing between multiple vendors’ equipment that is compliant with O-RAN fronthaul specifications.

![]()

“The combination of advanced assets and expertise from Mavenir and NEC will enable us to offer end-to-end one-stop 5G Open vRAN and Local/Private 5G solutions, including an advanced 5G network solution for the ecosystem, and vertical solutions that meet the needs of a great variety of Enterprise customers.” said Nozomu Watanabe, senior vice president at NEC.

This joint collaboration will continue to provide value-added products for customers worldwide. An overview of this collaboration will be introduced during MWC Barcelona 2020 (assuming the event is not cancelled as is rumored now) at the NEC booth, Hall 3, 3M30.

……………………………………………………………………………………………………………………………………………………….

About Mavenir:

Mavenir is the industry’s only end-to-end, cloud-native Network Software Provider focused on accelerating software network transformation and redefining network economics for Communications Service Providers (CSPs) by offering a comprehensive end-to-end product portfolio across every layer of the network infrastructure stack. From 5G application/service layers to packet core and RAN, Mavenir leads the way in evolved, cloud-native networking solutions enabling innovative and secure experiences for end users. Leveraging industry-leading firsts in VoLTE, VoWiFi, Advanced Messaging (RCS), Multi-ID, vEPC and OpenRAN vRAN, Mavenir accelerates network transformation for more than 250+ CSP customers in over 140 countries, which serve over 50% of the world’s subscribers.

We embrace disruptive, innovative technology architectures and business models that drive service agility, flexibility, and velocity. With solutions that propel NFV evolution to achieve webscale economics, Mavenir offers solutions to help CSPs with revenue generation, cost reduction, and revenue protection. Learn more at www.mavenir.com

References:

https://mavenir.com/press-releases/nec-and-mavenir-deliver-5g-open-vran-solution/

https://www.telecompaper.com/news/nec-mavenir-collaborate-to-deliver-5g-open-vran-platform–1326379

https://blogs.cisco.com/sp/the-open-vran-wave-is-building

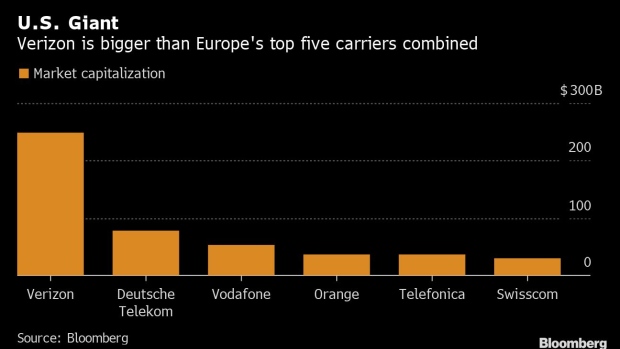

Verizon enters 5G market in Europe with London tech lab to open this April

Verizon Communications plans to advance its 5G efforts by opening a 5G tech lab in London this April as a way of displaying the services the company can offer. The production studio and showroom, Verizon’s first outside the U.S., is also aimed at attracting partners for 5G-related projects. The new Verizon lab will showcase services enabled by 5G wireless broadband and invites partners to collaborate on developing new ways to use it. The studio will use 5G to speed up data-intensive content production like motion-capture for entertainment and marketing. It’s all part of the company’s bet on the new tech.

- New facility offers first Verizon 5G-enabled development and collaboration space outside the United States

- Showcases existing 5G use cases and experiences & offers co-creation space for 5G-enabled application development

- 5G-enabled production studio brings next-generation content experiences to Verizon Media customers

- European investment enables Verizon to more easily share 5G leadership and expertise with companies based outside the U.S.

- Co-located Verizon Business & Media expertise offers unique, holistic approach to both 5G infrastructure & content

“Verizon has proven expertise in delivering 5G in the U.S.,” said Tami Erwin, Group CEO, Verizon Business. “One of the best ways of unleashing the true possibilities of 5G is getting it into the hands of innovators and visionaries. Our London facility enables our international customers to benefit from this expertise as they look to deploy 5G-enabled applications and experiences.”

“We’ve pretty much bet the company on this — it’s not like we’re dabbling,” said Toby Redshaw, vice president of innovation at Verizon’s business unit.

The outlook is still early, uncertain and competitive for these 5G services. And European carriers will have significant home field advantages: they already have relationships with the continent’s biggest businesses, local cultural and regulatory know-how, and own more local network assets.

But Redshaw says Verizon’s advantages include a head start from testing 5G in the field for years back in the U.S., and its larger scale. He was visiting London for the lab’s opening and to woo prospective clients, and said he’s had recent conversations with a Formula One team and other businesses. The company said the fresh London investment is “significant” but declined to give a number.

Examples of tech on display include cybersecurity visualization software, which lets a user fly around a virtual 3D landscape that represents their company’s network to spot potential anomalies. A service called BriefCam can instantly crunch reams of video and apply searches for a range of objects, such as all the red cars in a day’s worth of traffic footage, something a police force could find useful.

References:

https://www.verizon.com/about/news/verizon-expands-international-5g-ecosystem

https://www.bnnbloomberg.ca/verizon-muscles-into-europe-s-5g-race-with-u-k-outpost-1.1387674

T-Mobile Earnings Beat + 5G Network Status + 600 MHz and Spectrum Position

T-Mobile US beat analysts’ estimates for quarterly revenue and profit on Thursday, as the wireless carrier added more mobile phone subscribers to its monthly plans, some of which come bundled with a Netflix Inc service.

The third-largest U.S. wireless carrier by subscribers has been awaiting a decision on its proposed merger with Sprint Corp. The two U.S. telcos delivered closing arguments in a federal court last month against a multi-state lawsuit that argues the merger will increase prices for the consumers.

T-Mobile’s fourth-quarter net income rose to $751 million from $640 million, a year earlier. Excluding items, the company earned 87 cents, beating analysts’ average estimate of 83 cents. Revenue rose to $11.88 billion from $11.45 billion, edging past analysts’ average estimate of $11.83 billion, according to IBES data from Refinitiv.

………………………………………………………………………………………………………………………………………………………………………………………

Highlights from the T-Mobile Investor Factbook website:

Strong Customer Growth:

• 1.9 million total net additions in Q4 2019 – 7.0 million in 2019 – 6th year in a row of more than 5 million total net additions

• 1.3 million branded postpaid net additions in Q4 2019, best in industry – 4.5 million in 2019, best in industry

• 1.0 million branded postpaid phone net additions in Q4 2019, best in industry – 3.1 million in 2019, best in industry

• 77,000 branded prepaid net additions in Q4 2019 – 339,000 in 2019

• Branded postpaid phone churn of 1.01% in Q4 2019, up 2 bps YoY – 0.89% in 2019, down 12 bps from 2018

First Nationwide 5G Network:

• Launched the first nationwide 5G network utilizing 600 MHz spectrum, forming the foundational 5G coverage layer for

New T-Mobile; network covers more than 200 million people and more than 5,000 cities and towns

• 4G LTE on 600 MHz now covers 248 million people and 1.5 million square miles

• Currently, more than 33 million 600 MHz compatible devices already on our network

Strong Standalone Outlook for 2020:

• Branded postpaid net additions of 2.6 to 3.6 million

• Net income is not available on a forward-looking basis(2)

• Adjusted EBITDA target of $13.7 to $14.0 billion, which includes leasing revenues of $450 to $550 million

• Cash purchases of property and equipment, including capitalized interest of approximately $400 million, are expected

to be $5.9 to $6.2 billion. Cash purchases of property and equipment, excluding capitalized interest, are expected to

be $5.5 to $5.8 billion

• In Q1 2020, pre-close merger-related costs are expected to be $200 to $300 million before taxes

• Net cash provided by operating activities, excluding payments for merger-related costs and any settlement of interest

rate swaps, is expected to be in the range of $7.9 to $8.5 billion

• Free Cash Flow, excluding payments for merger-related costs and any settlement of interest rate swaps, is expected

to be in the range of $5.4 to $5.8 billion

Total Customers:

• Total net customer additions were 1,863,000 in Q4 2019, compared to 1,747,000 in Q3 2019 and 2,402,000 in Q4 2018. This is the 27th consecutive quarter in which TMobile added more than one million total net customers.

• T-Mobile ended Q4 2019 with 86.0 million total customers, of which 67.9 million were total branded customers.

• For the full-year 2019, total net customer additions were 7,011,000 compared to 7,044,000 in 2018. This was the sixth consecutive year in which total net customer additions exceeded 5 million.

______________________________________________________________

5G NETWORK:

On December 2, 2019, T-Mobile launched America’s first nationwide 5G network, including prepaid 5G with Metro by T-Mobile, covering more than 200 million people and more than 5,000 cities and towns across over 1 million square miles with 5G. In addition, we introduced two new 600 MHz 5G capable superphones, the exclusive OnePlus 7T Pro 5G McLaren and the Samsung Galaxy Note10+ 5G and anticipate offering an industry-leading smartphone portfolio built to work on nationwide 5G in 2020. This 5G network is our foundational layer of 5G coverage on 600 MHz low-band spectrum.

Should we close our merger with Sprint, we will rapidly deploy 5G on Sprint’s 2.5 GHz spectrum, completing the “layer cake” of spectrum and providing consumers with an unmatched 5G experience. On June 28, 2019, T-Mobile introduced its 5G network using high-band millimeter wave (mmWave) spectrum in conjunction with the introduction of our first 5G handset, the Samsung Galaxy S10 5G. The 5G network on mmWave spectrum has been rolled out in parts of seven cities (New York City, Los Angeles, Dallas, Atlanta, Cleveland, Las Vegas and Miami).

600 MHz Spectrum:

- At the end of Q4 2019, T-Mobile owned a nationwide average of 31 MHz of 600 MHz low-band spectrum. In total, T-Mobile owns approximately 41 MHz of low-band spectrum (600 MHz and 700 MHz). The spectrum covers 100% of the U.S.

- As of the end of Q4 2019, T-Mobile had cleared 275 million POPs and expects to clear the remaining 600 MHz spectrum POPs in 2020.

- T-Mobile continues its deployment of LTE on 600 MHz spectrum using 5G-ready equipment. At the end of Q4 2019, we were live with 4G LTE in nearly 8,900 cities and towns in 49 states and Puerto Rico covering 1.5 million square miles and 248 million POPs.

- Combining 600 and 700 MHz spectrum, we have deployed 4G LTE in low-band spectrum to 316 million POPs.

Currently, more than 33 million devices on T-Mobile’s network are compatible with 600 MHz spectrum.

Spectrum Position:

- At the end of Q4 2019, T-Mobile owned an average of 111 MHz of spectrum nationwide, not including mmWave spectrum. The spectrum comprises an average of 31 MHz in the 600 MHz band, 10 MHz in the 700 MHz band, 29 MHz in the 1900 MHz PCS band, and 41 MHz in the AWS band. On June 3, 2019, the FCC announced the results of Auctions 101 (28 GHz spectrum) and 102 (24 GHz spectrum). In the combined auctions, T-Mobile spent $842 million to more than quadruple its nationwide average total mmWave spectrum holdings from 104 MHz to 471 MHz.

- We will evaluate future spectrum purchases in upcoming auctions and in the secondary market to further augment our current spectrum position. We are not aware of any such spectrum purchase options that come close to matching the efficiencies and synergies possible from merging with Sprint.

Network Coverage Growth:

- T-Mobile continues to expand its coverage breadth and covered 327 million people with 4G LTE at the end of Q4 2019.

- At the end of Q4 2019, T-Mobile had equipment deployed on approximately 66,000 macro cell sites and 25,000 small cell/ distributed antenna system sites.

Network Capacity Growth:

- Due to industry spectrum limitations (especially in mid-band), T-Mobile continues to make efforts to expand its capacity and increase the quality of its network through the re-farming of existing spectrum and implementation of new technologies including Voice over LTE (“VoLTE”), Carrier Aggregation, 4×4 multiple-input and multiple-output (“MIMO”), 256 Quadrature Amplitude Modulation (“QAM”) and License Assisted Access (“LAA”).

- VoLTE comprised 90% of total voice calls in Q4 2019, flat with 90% in Q3 2019 and up from 87% in Q4 2018. Carrier aggregation is live for T-Mobile customers in 969 markets, up from 956 markets in Q3 2019 and 923 in Q4 2018.

- 4×4 MIMO is currently available in 708 markets, up from 683 markets in Q3 2019 and 564 in Q4 2018.

- T-Mobile customers have 256 QAM available across the Un-carrier’s entire 4G LTE footprint.

Source: Opensignal USA Mobile Network Experience Report January 2020, based on data collection period from 9/16/2019 to 12/14/2019 - T-Mobile is the first carrier globally to have rolled out the combination of carrier aggregation, 4×4 MIMO and 256 QAM. This trifecta of standards has been rolled out to 701 markets, up from 674 markets in Q3 2019 and 549 markets in Q4 2018.

- LAA has been deployed to 30 cities including Atlanta, Austin, Chicago, Denver, Houston, Las Vegas, Los Angeles, Miami, New Orleans, New York, Philadelphia, Sacramento, San Diego, Seattle, and Washington, DC.

Network Speed:

- Based on data from Opensignal for Q4 2019, T-Mobile’s average download speed was 25.8 Mbps, AT&T at 27.5 Mbps, Verizon at 25.3 Mbps, and Sprint at 23.9 Mbps.

- Based on data from Opensignal for Q4 2019, T-Mobile’s average upload speed was 8.6 Mbps, compared to Verizon at 7.9 Mbps, AT&T at 6.0 Mbps, and Sprint at 2.7 Mbps.

…………………………………………………………………………………………………………………………………………………………………………

References:

https://investor.t-mobile.com/financial-performance/quarterly-results/default.aspx

https://www.youtube.com/watch?v=CHPuI289U-Q&feature=youtu.be

BICS: 4G roaming traffic doubles for the third consecutive year

4G roaming traffic doubled in 2019 for the third consecutive year, according to a BICS report. Subscriber demand for high-capacity borderless connectivity continues to boom. The findings were from sourced from BICS’ global network, which connects over 700 operators and 500 digital service providers and carries over 50% of global data roaming traffic. The report show an uplift in roaming traffic across all continents, fueled by increased global travel, adoption of roaming tariffs, travel SIMs, and IoT devices.

“The exponential growth in roaming traffic highlights how important international connectivity has become to the subscriber experience,” commented Mikaël Schachne, CMO and VP Mobility & IoT Business at BICS. “Through the provision of seamless, cross-border 5G connectivity, operators will be able to create new revenue streams and support a wide range of new and innovative use cases in areas such as automotive, gaming, telemedicine and logistics. As carriers launch 5G networks, roaming must be at the heart of their offerings to deliver maximum value for subscribers.”

Carrying over a third of all global roaming traffic, BICS is connected to every single mobile network and has a presence in over 180 countries. Through BICS’ IPX platform, service providers can establish roaming and inter-working agreements with over 600 members on the network, enabling them to offer subscribers high-quality data roaming with other mobile and fixed network operators globally. In 2019 BICS consolidated its position at the center of the global connectivity ecosystem, with one in three operators worldwide now utilizing its 4G roaming services.

Last year also saw momentum build for both national and international 5G; approximately 50 national 5G networks are now live, while BICS pioneered several live 5G roaming services, including a 5G intercontinental roaming service between Europe and Asia. In 2020 BICS predicts 5G roaming will gain further traction, as service providers progress 5G deployments and launch 5G roaming to support increasing demand from both subscribers and industries requiring high-speed, ultra-low latency 5G data connectivity.

In July of last year, BICS launched a 5G roaming service between Swiss operator Swisscom and South Korean carrier SK Telecom. The 5G roaming service delivers high-speed, low latency 5G data connectivity between two continents, with operators using BICS’ 5G global IPX network.

Editor’s Caveat:

There won’t be much if any roaming on 5G until the industry agrees on IMT 2020 standards which must include a legitimate 5G Core network (as per 3GPP Release 16).

References:

https://bics.com/news/4g-roaming-traffic-doubles-for-the-third-year-as-industry-gears-up-for-5g/

CES 2020: Lenovo Yoga 5G claims to be the first 5G laptop PC

Lenovo has displayed the world’s first “5G” laptop at CES 2020 in Las Vegas, NV. The Chinese company says the Lenovo Yoga 5G is the first PC to be able to connect to (pre-IMT 2020 standard) 5G mmWave networks. However, neither the spectrum used nor the “5G” networks supported were disclosed. The Yoga 5G also supports Bluetooth 5.0 wireless connectivity, but (astonishingly) WiFi is not listed in the data sheet.

The Lenovo Yoga 5G will go on sale in the first quarter of 2020, starting at $1,499 (around £1,200, AU$2,100), and in North America will be known as the Lenovo Flex 5G.

The Lenovo Yoga 5G was previously known as Project Limitless before its official name was unveiled yesterday at CES 2000. As with other Yoga laptops, this is an ultra-portable 2-in-1 device, with a screen that can be folded backwards to turn it into a tablet.

The Lenovo Yoga 5G is also the first laptop to run on the Qualcomm Snapdragon 8cx platform, which includes built-in support for 5G connections, allowing the Yoga 5G to connect via a service provider and access super-fast mobile internet. According to Lenovo, this will allow the user to download large files easily, with download speeds of around 4Gb/s. The company says its 5G laptop is “up to 10 times faster than 4G through a 5G service provider when on the move and reliable WiFi access at home.” That’s quite impressive!

Lenovo said in a press release “5G technology will change entire industries as we know them, disrupting some while helping to launch others.”

Lenovo NOTES:

- Requires 5G network service and separately purchased cellular data plan that may vary by location. Additional terms, conditions and/or charges apply. Connection speeds will vary due to location, environment, network conditions and other factors.

- “5G” Download speeds vary by region and service provider, e.g. Verizon in U.S. offers up to 4Gbs/second. Network strength also varies by 5G service provider.

References:

Lenovo Breaks Barriers with New Consumer Technology Unveiled at CES 2020

https://news.lenovo.com/wp-content/uploads/2020/01/Lenovo-Yoga-5G_14Inch_Qualcomm.pdf

Samsung #1 in Global 5G smartphone sales with 6.7 Million Galaxy 5G Devices in 2019

Samsung Electronics Co., Ltd. said that it shipped more than 6.7 million Galaxy 5G smartphones globally in 2019, giving consumers the ability to experience next-generation speed and performance. As of November 2019, Samsung accounted for 53.9% of the global 5G smartphone market and led the industry in offering consumers five Galaxy 5G devices globally, including the Galaxy S10 5G, Note10 5G and Note10+ 5G, as well as the recently launched Galaxy A90 5G and Galaxy Fold 5G.

The 6.7 million in Samsung 5G smartphone sales eclipses the 4 million target the firm set itself, though as its main Android competitor (Huawei) is being stifled by political friction, it is hardly surprising Samsung has stormed into the lead. Note also that Apple has not announced a 5G smartphone and probably will not do so till late 2020. In the absence of main competitors, Samsung is maintaining its leadership position in the 5G segment as well as 4G-LTE.

“Consumers can’t wait to experience 5G and we are proud to offer a diverse portfolio of devices that deliver the best 5G experience possible,” said TM Roh, President and Head of Research and Development at IT & Mobile Communications Division, Samsung Electronics. “For Samsung, 2020 will be the year of Galaxy 5G and we are excited to bring 5G to even more device categories and introduce people to mobile experiences they never thought possible,” he added.

The Galaxy Tab S6 5G, which will be available in Korea in the first quarter of 2020, will be the world’s first 5G tablet bringing ultra-fast speeds together with the power and performance of the Galaxy Tab series. With its premium display, multimedia capabilities and now, 5G, the Galaxy Tab S6 5G offers high-quality video conferencing, as well as a premium experience for watching live and pre-recorded video streams or playing cloud and online games with friends.

“5G smartphones contributed to 1% of global smartphone sales in 2019. However, 2020 will be the breakout year, with 5G smartphones poised to grow 1,687% with contribution rising to 18% of the total global smartphone sales volumes,” said Neil Shah, VP of Research at Counterpoint Research. “Samsung has been one of the leading players catalyzing the 5G market development in 2019 with end-to-end 5G offerings from 3GPP standards contribution, semiconductors, mobile devices to networking equipment. With tremendous 5G growth opportunities on the horizon, Samsung, over the next decade, is in a great position to capitalize by further investing and building on the early lead and momentum, ” Shah added.

………………………………………………………………………………………………………………………………………………………………………………………….

Sidebar: Qualcomm or Samsung 5G silicon in future 5G devices?

It has become widely accepted that the latest Qualcomm chipset features in the majority of flagship smartphone devices throughout the year. Only two smartphone makers – Samsung and Huawei – have said they were making their own 5G chipsets which would be integrated into their 5G smartphones. Will Samsung use both its own silicon as well as Qualcomm’s in future 5G devices?

Over the next few months Qualcomm will begin shipping both the Snapdragon 865 and Snapdragon 765 chipsets. The Snapdragon 865 is more powerful, though 5G is on a separate modem, potentially decreasing the power efficiency of devices. The Snapdragon 765 has 5G connectivity integrated, though is notably less powerful. Whichever chipset OEMs elect for, there will be a trade-off to stomach.

Looking at the rumours spreading through the press, it does appear many of the smartphone manufacturers are electing for the Snapdragon 865 and a paired 5G modem in the device. Samsung’s Galaxy S11, Sony Xperia 2 and the Google Pixel 5 are only some of the launches suggested to feature the Snapdragon 865 as opposed to its 5G integrated sister chipset.

With Mobile World Congress 2020 in Barcelona just two months away, there is amble opportunity for new 5G devices to be launched prior, during and just after the event. It will be interesting to see what 5G silicon is used in them.

Incomplete (or non existent) 5G Standards:

Of critical importance is that there are currently no standards for 5G implementations. The closest is IMT 2020.SPECS which won’t be completed and approved till November 23-24, 2020 ITU-R SG5 meeting or later. That spec will likely not include the 5G packet core (5GC), network slicing, virtualization, automation/orchestration/provisioning, network management, security, etc which will either be proprietary or use 4G LTE infrastructure. It also might not include signaling, ultra low latency or ultra high reliability, depending on completion of those items in 3GPP Release 16 and its disposition to ITU-R WP 5D.

………………………………………………………………………………………………………………………………………………………………………………………..

For nearly a decade, Samsung has worked to bring 5G from the lab to real life by working closely with carrier partners, regulatory groups and government agencies to develop the best 5G experience possible. As a leading contributor to industry groups like 3GPP and O-RAN Alliance, Samsung is committed to an open, collaborative approach to networking, which has helped to accelerate delivery of 5G to consumers and businesses. Over the past year, in addition to launching a robust 5G device portfolio, the company reached several historical milestones including providing network equipment for the world’s first 5G commercial service in Korea as well as working closely with global carrier partners to expand 5G networks and introduce 5G experiences and use cases.

In the year ahead, Samsung says they will continue to lead the market in 5G innovation by introducing new advancements that will improve the speed, performance and security of Galaxy 5G devices even further. In 2020, these advancements will give even more people access to new mobile experiences that change the way they watch and interact with movies, TV and sports, play games and talk with friends and family.

For more information about Samsung Galaxy 5G devices please visit news.samsung.com/us/galaxy-5g/, www.samsungmobilepress.com or www.samsung.com/galaxy.

References:

https://news.samsung.com/us/samsung-galaxy-5g-devices-shipping-more-than-6-million-2019/

https://telecoms.com/501580/samsung-claims-the-5g-lead-after-6-7-million-shipments/

https://www.extremetech.com/mobile/304091-samsung-shipped-over-6-7-million-5g-phones-in-2019

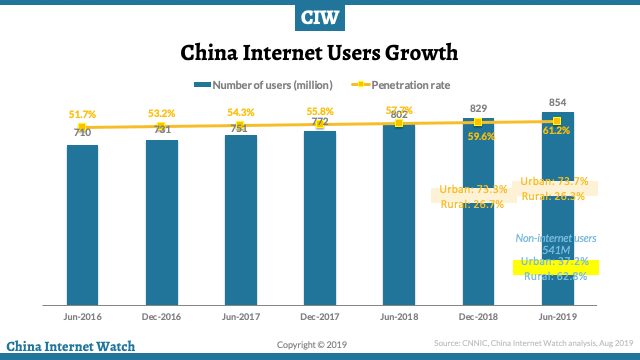

China Internet penetration reached 61.2% in 1st half 2019; 99.1% access Internet via mobile phones!

Internet penetration in China reached 61.2 percent in the first half of the year, with 854 million internet users at end June, according to China government-backed research institute MIC (Market Intelligence & Consulting Institute) and reported by China Internet Watch.

China internet users in urban areas account for 73.7% of total internet users. Among the Chinese population who don’t access the internet (which is 541 million), rural areas account for 62.8%. Internet user growth is mainly relying on mobile terminals, which is also very slow.

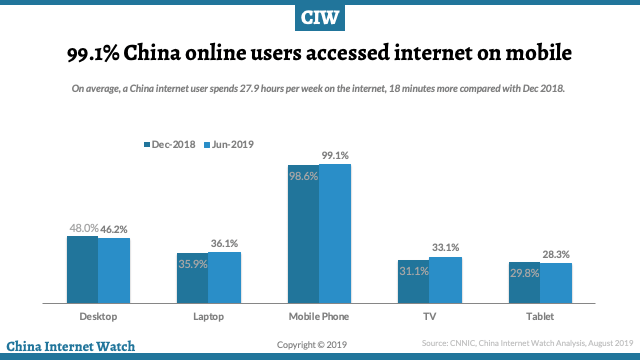

The number of internet users on mobile phones is 847 million, accounting for over 99% of internet users in China. Smartphones have become the top internet access devices in China.

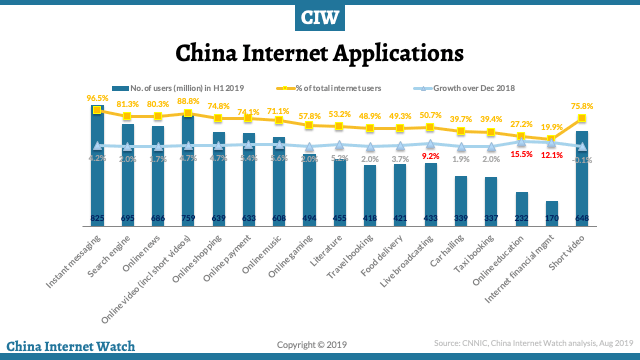

Short video consumers made up 88.8 percent of all internet users, about 760 million, breaking past the 490 million online gamers.

Top online applications by total number of users in the first half of 2019 are instant messaging, search engines, online news, online videos, and online shopping.

About 80.2 percent of internet users on the country’s three major platforms – iQiyi, Tencent, and Youku, watch OTT content. Bilibili, Sohu Video, and Mango TV were also very popular. These platforms are making big investments into exclusive content.

“Content quality has become the key to competitiveness,” MIC said.

References:

https://www.chinainternetwatch.com/statistics/china-internet-users/

https://app.box.com/s/jz9iet7vja58ciqw51j31bxeib986ms1?

ITU Hosted ICT CxO Meeting: achieving ‘self-driving’ IMT-2020/5G networks

Introduction:

Innovation to achieve ‘self-driving’ IMT-2020/5G networks, collaboration in the interests of 5G security and the value of ‘open’ network concepts were among the key topics discussed at an invitation-only meeting of ICT industry executives (‘CxOs’) held last week in Dubai, UAE, in conjunction with the Telecom Review Leaders’ Summit. The CxO meeting’s discussions revolved around industry preparations for IMT-2020/5G.

CxOs shared insights gained from early 5G deployments and trials of 5G–enabled industrial Internet of Things (IoT) applications. They also discussed the importance of building public trust in autonomous driving and the safety-critical radiocommunications supporting Intelligent Transport Systems.

With a view to discussing industry needs and associated standardization priorities, the meeting brought together representatives of companies including du, Etisalat, Facebook, Fujitsu, Korek Telecom, Krypton Security, Nokia, Orange, Roborace, Rohde & Schwarz, SES Networks and TELUS.

The trends discussed at the CxO meeting reflect the evolution of ITU membership, in particular that of ITU’s standardization arm (ITU-T). ITU-T has welcomed 51 new members in 2019, following 45 new members in 2018.

New ITU-T members include companies in energy and utilities, shipping and logistics, mobile payments, over-the-top applications, automotive, IoT connectivity, blockchain and distributed ledger technologies, quantum communications, cybersecurity, and artificial intelligence and machine learning.

The meeting issued a communiqué summarizing ICT trends of growing relevance to ITU standardization.

< Download the CxO meeting communiqué >

The optimization of network management and orchestration – capitalizing on real-time network performance data, machine learning for prediction and self-learning, and the automated build and configuration of virtual network functions – will improve ICT services and introduce new cost efficiencies, said CxOs.

ITU-R WP 5D will produce a draft new Report ITU-R M.[IMT.C-V2X] on “Application of the Terrestrial Component of IMT for Cellular-V2X.”

3GPP intends to contribute to the draft new Report and plans to submit relevant material at WP 5D meeting #36. 3GPP looks forward to the continuous collaboration with ITU-R WP 5D for the finalization of Report ITU-R M.[IMT.C-V2X].

This optimization is becoming increasingly challenging, and increasingly important, as networks gain in complexity to support the coexistence of a diverse range of ICT services.

CxOs encouraged ITU to study the evolution of network operation and maintenance in view of increasing network complexity and the resulting importance of automation informed by machine learning.

CxOs discussed the progress achieved in responding to the ‘Ottawa Accord’ considered by ITU’s annual Chief Technology Officer (CTO) meeting in Budapest, Hungary, 8 September 2019.

The Ottawa Accord is a set of security priorities developed in June 2019 by network operators, standards bodies and industry associations.

The Budapest CTO meeting endorsed the findings of the Ottawa Accord in relation to three security priorities:

- Global threat exchange: Common understanding of security threats and common terminology to enable the sharing of threat intelligence.

- Best practices for operational security: Best practices for 5G security and widespread commitment to infrastructure protection.

- Security incentives: Measurement schemes based on agreed metrics could bring attention to prevailing levels of security and create incentives for investment in security.

CxOs echoed the sentiment of the Budapest CTO meeting that a holistic approach to 5G security could receive valuable support from a global centre for the development of security solutions and their testing and assurance. Such a ‘living lab’ open to multiple vendors, said CTOs in Budapest, could bring cohesion to 5G security efforts as well as reduce the costs of testing security solutions.

CxOs with experience in the early commercial deployment of 5G reiterated the importance of investment in fibre. Fibre-optic networks form the ‘backbone’ of the ICT ecosystem. Investment in fibre continues to rise, recognizing the importance of this investment to the 5G vision.

Experience with industrial IoT applications as part of the development of 5G-enabled smart sea ports and smart factories, said CxOs, has highlighted the importance of network slicing and shown edge computing to be capable of supporting low latencies. CxOs’ experience with 5G-enabled smart factories, in particular, has shown such factories to be capable of highly efficient production and quality control.

Infrastructure sharing has the potential to assist network operators in reducing time-to-market for new solutions, gaining cost efficiencies and increasing coverage in certain network deployment scenarios.

CxOs illustrated possible scenarios for the sharing of infrastructure such as core networks, central offices, backhaul infrastructure, towers, and RANs.

The meeting considered an example of ‘Multi-Core Operator Networks’, networks said to be capable of reducing an operator’s infrastructure investments through sharing, while improving network performance.

General-purpose ‘white box’ hardware, standardized interfaces and virtualized network elements are the foundations of the ‘open RAN’ concept, said CxOs.

Open RAN could support industry in avoiding the challenges that may result from proprietary RAN interfaces, challenges such as RAN equipment vendor lock-in, limited interoperability between different vendors’ RAN equipment, and limited scope for active RAN sharing.

CxOs offered the view that the standardization of open, interoperable RAN interfaces and RAN functional architecture could support a diverse business ecosystem in deploying and operating RANs with considerable cost efficiency.

ITU has established a new Focus Group on ‘Artificial intelligence for autonomous and assisted driving’ to work towards the establishment of international standards to monitor and assess the performance of the AI ‘Drivers’ in control of automated vehicles.

CxOs discussed the ITU Focus Group’s aim to devise a ‘Driving Test’ for AI ‘Drivers’. The proposed test could become the basis for an International Driving Permit for AI. The right to hold this permit would be assessed continuously, based on the AI Driver’s behavioural performance on the road.

CxOs highlighted their support for the Focus Group’s expected contribution to public trust in automated vehicles as well as the value of ITU collaboration with UNECE in this regard.

Recognizing the importance of new radio technology and applications to Intelligent Transport Systems (ITS), CxOs highlighted the importance of conformance assessment based on harmonized test requirements.

According to the CxOs, compliance, conformance and quality testing will make a key contribution to industry and consumer confidence in safety-critical radiocommunications in the ITS context. Conformance assessment would also support ITS interoperability and cost efficiency, said CxOs.

…………………………………………………………………………………………………………………………………………………………

The participating organizations were:

Arab Information & Communication Technologies Organization (AICTO), du, Etisalat, Facebook,

Fujitsu, Korek Telecom, Krypton Security, Nokia, Orange, Roborace, Rohde and Schwarz, SES

Networks, Telecom Review North America, Telecommunication Industry Association (TIA), TELUS

References:

Intelligence, security and cost efficiency: Industry executives highlight priorities for the 5G era

https://www.itu.int/en/ITU-T/tsbdir/CxO/Documents/Communique%20-%20CxO%20-%20Dubai%202019.pdf

Zayo’s largest capacity wavelengths deal likely for cloud data center interconnection (DCI)

Zayo Group Holdings announced it has signed a deal for the largest amount of capacity sold on any fiber route in the company’s history. The deal with the unnamed customer will provide approximately 5 terabits of capacity that can be used to connect mega scale data centers. While Zayo didn’t disclose the customer, large hyperscale cloud providers, such as Amazon Web Services, Microsoft Azure and Google Cloud Project, and webscale companies such as Facebook, seem to be likely candidates.

Zayo provides a 133,000-mile fiber network in the U.S., Canada and Europe. Earlier this year it agreed to be acquired by affiliates of Digital Colony Partners and the EQT Infrastructure IV fund. That deal is slated to close in the first half of next year.

“Our customers [1] are no longer talking gigabits — they’re talking terabits on multiple diverse routes,” said Julia Robin, senior vice president of Transport at Zayo. “Zayo’s owned infrastructure, scalable capacity on unique routes and ability to turn up services quickly positions us to be the provider of choice for high-capacity infrastructure.”

Note 1. Zayo’s primary customer segments include data centers, wireless carriers, national carriers, ISPs, enterprises and government agencies.

Zayo to extend fiber-optic network in central Florida: The new fiber network infrastructure, comprising more than 2300 route miles, will open Tampa and Orlando as new markets for the fiber-optic network services company.

…………………………………………………………………………………………………………………………………………………………………………………………….

Zayo’s extensive wavelength network provides dedicated bandwidth to major data centers, carrier hotels, cable landing stations and enterprise locations across our long-haul and metro networks. Zayo continues to invest in the network, adding new routes and optronics to eliminate local stops, reduce the distance between essential markets and minimize regeneration points. Options include express, ultra-low and low-latency routes and private dedicated networks.

Zayo says it “leverages its deep, dense fiber assets in almost all North American and Western European metro markets to deliver a premier metro wavelength offering. Increasingly, enterprises across multiple sectors including finance, retail, pharma and others, are leveraging this network for dedicated connectivity as they seek ways to have more control over their growing bandwidth needs.”

According to a report by market research firm IDC, data created, captured and replicated worldwide will be 175 zettabytes by 2025 and 30% of it will be in real time. A large chunk of that amount will be driven by webscale, content and cloud providers that require diverse, high capacity connections between their data centers. In order to provision high bandwidth amounts, service providers and webscale companies are turning to dedicated wavelength solutions.

Zayo’s wavelength network provides dedicated bandwidth to major data centers, carrier hotels, cable landing stations and enterprise locations across its long-haul and metro networks. Its communications infrastructure offerings include dark fiber, private data networks, wavelengths, Ethernet, dedicated internet access and data center co-location services. Zayo also owns and operates a Tier 1 IP backbone and 51 carrier-neutral data centers.

References:

For more information on Zayo, please visit zayo.com

https://www.fiercetelecom.com/telecom/zayo-lands-largest-wavelengths-deal-its-history-at-5-terabits