Uncategorized

Reuters: Telcos draft proposal to charge Big Tech for EU 5G rollout; Meta offers a rebuttal

Big tech companies accounting for more than 5% of a telecoms provider’s peak average internet traffic should help fund the rollout of 5G and broadband across Europe, according to a draft proposal by the telecoms industry. The proposal is part of feedback to the European Commission which launched a consultation into the issue in February. The deadline for responses is Friday.

Alphabet’s Google, Apple Facebook-owner Meta, Amazon, Netflix and TikTok would most likely be hit with fees, according to industry estimates. Google, Apple, Meta, Netflix, Amazon and Microsoft together account for more than half of data internet traffic.

The document, which was reviewed by Reuters and has not been published, was compiled by telecoms lobbying groups GSMA and ETNO. They represent 160 operators in Europe, including Deutsche Telekom, Orange, Telefonica and Telecom Italia. Telecom operators have lobbied for years for leading technology companies to help foot the bill for 5G and broadband roll-out, saying that they create a huge part of the region’s internet traffic. This is the first time they have tried to define a threshold for who should pay.

“We propose a clear threshold to ensure that only large traffic generators, who impact substantially on operators’ networks, fall within the scope,” the draft stated. “Large traffic generators would only be those companies that account for more than 5% of an operator’s yearly average busy hour traffic measured at the individual network level,” it said. The European Commission declined to comment.

Meta on Wednesday urged Brussels to reject any proposals to charge Big Tech for additional network costs. In a Facebook blog post, Markus Reinisch, Meta’s VP for Public Policy for Europe, described potential fees as a “private sector handout for selected telecom operators” that would disincentivize innovation and investment, and distort competition. “We urge the Commission to consider the evidence, listen to the range of organizations who have voiced concerns, and abandon these misguided proposals as quickly as possible,” he said. Here are Meta’s takeaways:

- Network fee proposals misunderstand the value that content platforms bring to the digital ecosystem.

- We support the Commission’s goal of “ensuring access to excellent connectivity for everyone,” but network fee proposals will hurt European consumers and businesses.

- We urge the Commission to consider the evidence, listen to the range of organizations who have voiced concern, and drop these proposals.

References:

Network Fee Proposals Will Ultimately Hurt European Businesses and Consumers

https://www.euractiv.com/section/5g/news/eu-telcos-call-for-big-tech-to-share-5g-network-costs/

GSMA: Europe’s 5G rollout is too slow at 6% of mobile customer base

European telcos need to address very high 5G energy consumption

Strand Consult: Market for 5G RAN in Europe: Share of Chinese and Non-Chinese Vendors in 31 European Countries

MTN Consulting: Satellite network operators to focus on Direct-to-device (D2D), Internet of Things (IoT), and cloud-based services

Satellite network operators are being forced to expand their addressable markets in the near term, due to several factors: rising competition, with the emergence of players such as SpaceX along with several upstarts including AST SpaceMobile and Lynk. A difficult funding climate resulting from a grim economic outlook and rising interest rates is a challenge. There are also market concentration risks arising from the current focus on satellite broadband internet.

To address these challenges, satellite network operators are raising stakes in new pursuits and developing new offerings. MTN Consulting expects three new potential addressable markets to provide transformational opportunities for satellite operators in the next 2-4 years. These include Direct-to-device (D2D), Internet of Things (IoT), and cloud-based services.

Looking at these market opportunities, a thought may arise whether satellite operators are trying to disrupt the traditional telecom market. But the reality is that telcos will continue to be the primary service provider for wireless access. Telcos are also going to benefit from partnerships with satellite operators as they will aid in providing an enhanced experience for telco customers, reinforced by ubiquitous coverage. For satellite operators though, navigating the regulatory hurdles and ensuring constant capital flow are key concerns; several players from the current herd will vanish in the next 3-5 years.

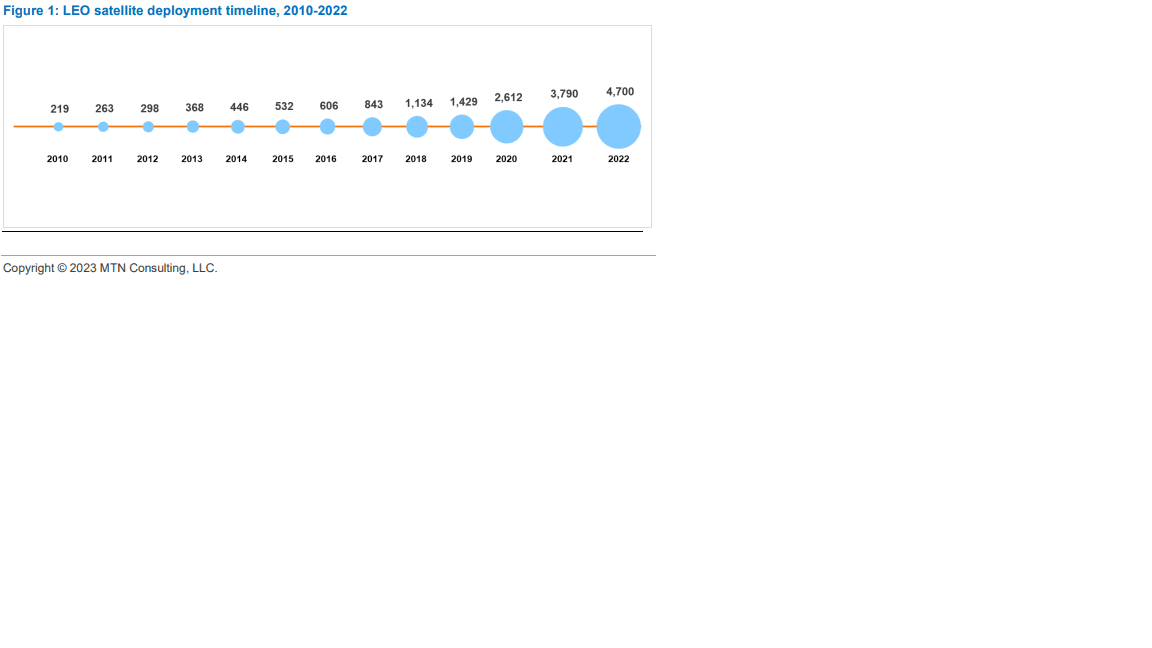

The battle for space based Internet gained momentum in the year 2022 as several satellite operators, notwithstanding their size and years of operations, shifted gears with the launch of commercial broadband internet through low earth orbit (LEO) satellites. The space rush, aided by the advancement in satellite development and large-scale manufacturing, witnessed the sudden surge in large fleets of LEO satellites being deployed in recent years, as shown in Figure 1. As of May 2022, about 4,700 active LEO satellites are girdling the planet; that’s 16x the number of active LEO satellites deployed a decade ago.

Separately, MTN found that a number of large telcos have high debt, low margins, and/or weak top line growth, and may have to curtail spending in 2023-2024 in order to cope with this reality. In particular:

- Total telco debt in 4Q22 was $1.14 trillion, 17% due in next year

- Software capex as a % of revenues was 1.9% in 2022, up a bit from 1.8% in 2021.

- Spending on acquisitions amounted to 0.5% of revenues in 2022, the lowest figure since 2012.

- At the industry level, the ratio of net debt to EBITDA in 2022 was 1.9, a bit up from 2021 but down from 2020.

- A number of large telcos face short-term debt levels over 30% of total debt

- Average margins for the industry in 2022 disappointed: free cash flow margin for the telco industry in 2022 was 11.4%, down from 12.6% in 2021; EBITDA margin was 33.7% (2021: 34.0%), and EBIT margin was 14.4% (2021: 14.9%).

References:

Satellite players bet on direct-to-device (D2D), IoT, and cloud for next big liftoff

Omdia Surveys: PON will be a key part of network operator energy reduction strategies

Omdia (owned by Informa) surveys have found a “very high” number of telcos regarded PON as a key part of their energy savings programs. Omdia’s chief analyst Julie Kunstler said PON technology is fiber-asset efficient, easy to upgrade, and highly secure.

Speaking at a Light Reading webinar Thursday, Kunstler said another large cohort of network operator execs said they believed PON would play some role in their energy reduction strategies. “PON is energy efficient and this is definitely gaining attention.” Kunstler said “a very strong movement” by operators was underway toward next gen PON, in particular XGS PON. “But perhaps more importantly, PONs are also supporting other types of customers and applications.” She also noted PON technology was fiber-asset efficient, easy to upgrade, highly secure and allowed operators to choose when to upgrade. But she cautioned that in many telcos PON faced organizational obstacles because of the belief that it was for consumer services only and because of the silos between residential and business.

Anuradha Udunuwara, a senior enterprise solutions architect at Sri Lanka Telecom, said energy costs had become a bigger concern in the past 12 months following sharp hikes in power tariffs. He agreed that PON “definitely has an advantage… it is passive, so there is no energy consumption there.”

Udunuwara described PON as an “architectural option” that could support FTTX deployment. He said it was a myth about PON that it was for FTTH only. “It’s not confined to any of the variations of FTTX.” He expected that in the long run services would converge on to a single access technology.

“Oftentimes, sales and marketing teams don’t feel comfortable about PON, simply because they don’t understand it,” Kunstler said. “Many believe its point to multipoint topology is for residential only and that it’s simply best effort and there’s no technical ability to support enterprise services.”

“A lot of education is needed within some operators to explain to the sales and marketing team that PON is not just best effort and that you can actually commit to rates,” she pointed out.

“Not all enterprises need point to point. They don’t all need their own dedicated fiber, and many of them really don’t want to have to pay for dedicated fiber.”

Kunstler said selling business services over PON increased the ROI over that access infrastructure. “With 10G PON, you can easily support one gig symmetrical, two gig symmetrical five gig symmetrical and so forth, and 50 GPON, which will be here within a couple of years, can even support more bandwidth.

By using that optical distribution network for more than just residential, operators were already moving to a converged access approach. “You have more revenues over a single access network. You have a single network to upgrade. You have improved optics and you have improved energy savings.”

References:

Dell’Oro: XGS, 25G, and Early 50G PON Rollouts to Fuel Broadband Spending

AT&T to deploy FTTP network based on XGS-PON in Amarillo, TX

ZTE PON ONT obtains EasyMesh R3 certification from WiFi Alliance

Dell’Oro: PONs boost Broadband Access; Total Telecom & Enterprise Network Equipment Markets

Omdia: Consumer Telco Opportunity Challenged by Global Tech Giants

Market research firm Omdia (owned by Informa) says all growth areas for telcos will experience significant competition from hyperscalers – specifically the global tech giants Google, Amazon, Meta/Facebook, and Apple.

Omdia’s Quantifying the Consumer Telco Opportunity – 2023 report is an in-depth report providing analysis and insights drawn from Omdia’s related data tools as well as individual operator case studies. The market research firm says that other than core fixed-line and mobile data services, almost all of the potential growth for telcos in the consumer sector over the next few years will come from ‘non-traditional categories. Those include video streaming, digital gaming, streaming music, and smart home (whatever that means).

“Service providers must look beyond data and diversify into adjacent digital markets to enable continued growth of their telco consumer businesses,” said Omdia’s Jonathan Doran. “Many have already invested in TV and online video entertainment, but there are other fast-growing markets telcos can also explore. Adopting the right go-to-market strategy and business model for each individual service area will be critical to striking the balance between achieving market success and mitigating financial risk. In many areas, telcos will need to accept that competing head-on is unrealistic and developing partnerships with such players is not only more pragmatic but will also serve to strengthen their own products and brands” observes Doran.

“Omdia’s Digital Consumer Operator Strategy Benchmark shows that the more service providers actively invest in a given service area – including through partnerships – the bigger market impact they have, which in turn better positions them to take a bigger slice of overall market revenue”

Big tech is already there and doing a decent job of selling all these digital goodies direct to consumers without the help of operators. Every time telcos have tried to compete directly in adjacent markets is has all gone horribly wrong so, as well as picking their fights more carefully, they are advised to consider an ‘if you can’t beat em, join em’ approach.

“In many areas, telcos will need to accept that competing head-on is unrealistic and developing partnerships with such players is not only more pragmatic but will also serve to strengthen their own products and brands,” said Doran. “Omdia’s Digital Consumer Operator Strategy Benchmark shows that the more service providers actively invest in a given service area – including through partnerships – the bigger market impact they have, which in turn better positions them to take a bigger slice of overall market revenue.”

The Omdia chart below illustrates product types by growth potential (horizontal axis), relevance to the Communications Service Provider (CSP) core proposition (vertical axis) and forecasted relative 2027 market size. As you can see, most consumer digital products are pretty far from the CSP core proposition, but Omdia forecasts they will collectively amount to a $500 billion market by 2027. How much of that will find its way into the pockets of telcos as a result of partnering with Big Tech remains to be seen, but even a small fraction is better than nothing.

Amazon, Microsoft and Google are not only three of the biggest players in the digital consumer space, they also dominate the public cloud market, which network operators are constantly urged to turn to for its efficiencies and flexibility. It’s possible to imagine a time most of what we get from and operator is actually supplied, and monetized, buy one of a small number of hyperscalers. It’s not clear whether that represents a positive development for the telecoms industry.

References:

https://telecoms.com/521154/study-highlights-increasing-dependence-of-operators-on-hyperscalers/

IEEE Techblog recognized by Feedspot!

The IEEE ComSoc Techblog was voted #2 best broadband blog:

https://blog.feedspot.com/broadband_blogs/

2. The IEEE ComSoc Technology Blog

Piscataway, New Jersey, US

Piscataway, New Jersey, US

Featuring the latest in breaking telecom/networking news and analysis, the IEEE ComSoc blog is written by several expert bloggers. IEEE Communications Society is a global community of professionals with a common interest in advancing all communications and networking technologies.

Also in Telecom Blogs

techblog.comsoc.org+ Follow

…………………………………………………………………………………………………

..and #13 best telecom blog in the world:

https://blog.feedspot.com/telecom_blogs/?_src=alsoin

Many thanks to Vinny Rodriquez and Khanh Luh for making our blog so successful!

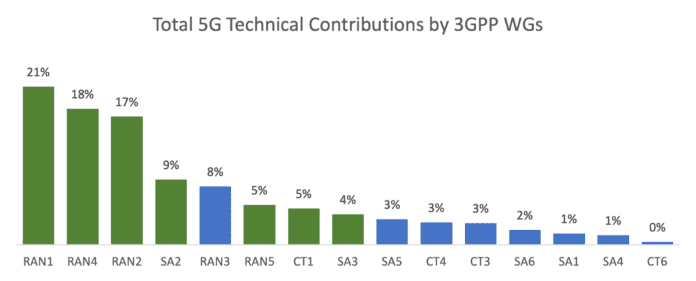

ABI Research: Major contributors to 3GPP; How 3GPP specs become standards

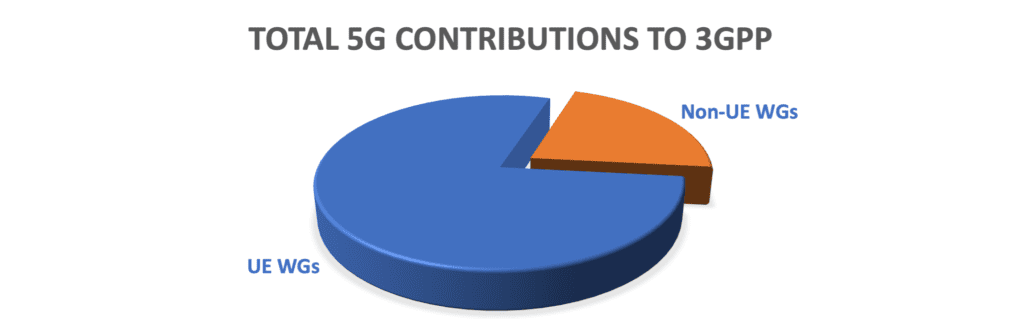

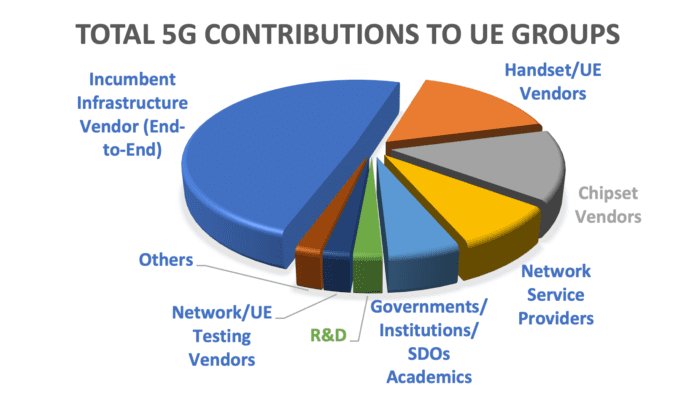

Three large network equipment vendors (Huawei, Ericsson, and Nokia) have been leading in both the number of contributions and approved contributions for 5G technologies to The 3rd Generation Partnership Project (3GPP). This is particularly the case with specifications related to User Equipment (UE) specifications and functionalities that are developed under RAN1, RAN2, RAN4, RAN5, SA2, SA3, and CT1 Working Groups (WGs).

Editor’s Note:

The 3GPP Organizational Partners (OP) are the seven Standards Developing Organizations (SDOs) – from China, Europe, India, Japan, Korea and the United States. The OPs are:

ARIB The Association of Radio Industries and Businesses, Japan

ATIS The Alliance for Telecommunications Industry Solutions, USA

CCSA China Communications Standards Association

ETSI The European Telecommunications Standards Institute

TSDSI Telecommunications Standards Development Society, India

TTA Telecommunications Technology Association, Korea

TTC Telecommunication Technology Committee, Japan

Participation in 3GPP is made possible by companies and organizations becoming Individual Members (IM) of one of the OPs.

- 3GPP specifications are not standards, they have no legal standing. They become “official” standards once one or more of the OPs transposes them, as ETSI has done many times.

- 3GPP specs become ITU-R recommendations when they are submitted to ITU-R WP5D by ATIS, discussed and agreed upon, then sent to WP5 plenary in November for final approval. That procedure was followed to create the ITU-R M.2150 recommendation which features 5G-NR.

……………………………………………………………………………………………………………………………………………………………………………………………………………….

The list of the most active companies within 5G 3GPP standards is listed in the table below:

| Top Ranked by Total Contributions | Approved Contributions | Total Contributions | Company Category |

| Huawei | 15,266 | 43,753 | Incumbent Infrastructure Vendor (End-to-End) |

| Ericsson | 11,601 | 36,375 | Incumbent Infrastructure Vendor (End-to-End) |

| Nokia | 7,553 | 23,112 | Incumbent Infrastructure Vendor (End-to-End) |

| Qualcomm | 5,523 | 18,471 | Chipset |

| Samsung | 3,548 | 16,464 | Incumbent Infrastructure Vendor (End-to-End) |

| ZTE | 3,415 | 15,291 | Incumbent Infrastructure Vendor (End-to-End) |

| Intel | 2,151 | 10,770 | Chipset |

| LGE | 1,396 | 10,139 | Handset/UE Vendor |

| CATT | 1,934 | 9,792 | Government/Institution/SDO/Academics |

| vivo | 1,205 | 8,367 | Handset/UE Vendor |

| MediaTek | 1,848 | 7,766 | Chipset |

Source: ABI Research

Key Takeaways:

- Counting contributions alone is insufficient to identify leaders in 3GPP standardization processes. However, it is a crucial step in recognizing active contributors and identifying innovation.

- More than 400 companies from the industry have participated in 3GPP standardization; however, only a handful of companies are consistently active in driving 3GPP 5G standards.

- Huawei, Ericsson, and Nokia have, so far, been leading in both the number of total and approved contributions for 5G technologies to 3GPP.

- Network infrastructure vendors are significantly more active than any other company categories, followed by handset vendors, chipset vendors, network service providers, and government research institutions.

- UE-related WGs (i.e., RAN1, RAN2, RAN4, RAN5, SA2, SA3, and CT1) take 80% of total contributions. RAN1, RAN2, RAN4, and SA2 are the most important WGs, impacting the entire mobile industry and receiving massive interest.

References:

https://www.3gpp.org/about-us/partners

ITU-R M.2150-1 (5G RAN standard) will include 3GPP Release 17 enhancements; future revisions by 2025

Busting a Myth: 3GPP Roadmap to true 5G (IMT 2020) vs AT&T “standards-based 5G” in Austin, TX

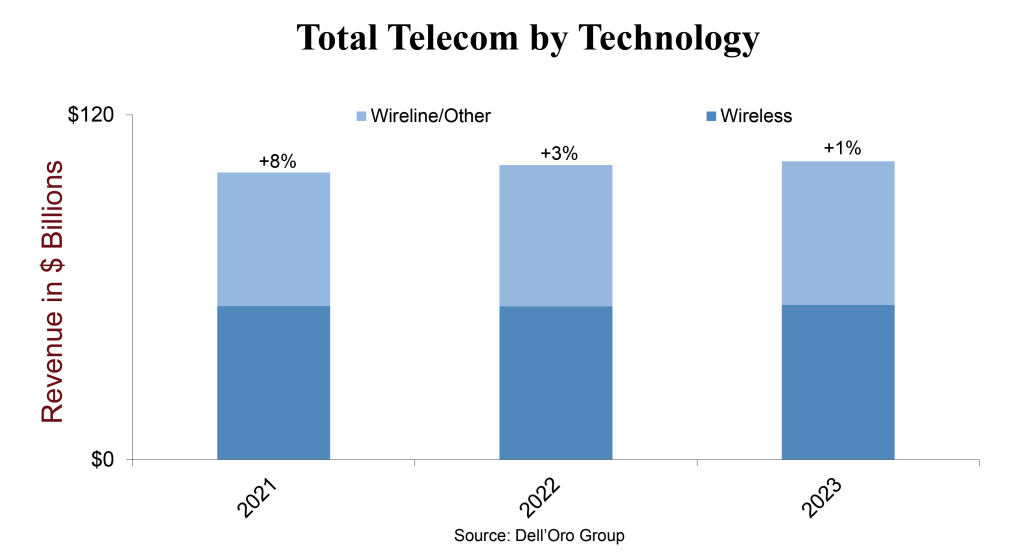

Dell’Oro: Worldwide Telecom Equipment Market Growth +3% in 2022; MTN: +2% Network Infrastructure Growth in 2022

by Stefan Pongratz, VP Dell’Oro Group

Following four consecutive years of modest telecom equipment growth across the six telecom programs tracked at the Dell’Oro Group, preliminary findings show that the aggregate telecom equipment market moderated somewhat from the 8% revenue increase in 2021 to 3% year-over-year (Y/Y) in 2022.

Looking back at the full year, the results were slightly lower than the 4% growth rate we projected a year ago going into 2022. In addition to more challenging comparisons in the advanced 5G markets and the supplier exits in Russia, the strengthening USD weighed on the broader telecom equipment market. Supply issues also impacted the market negatively during 1H22 but eased somewhat in the second half.

Regional developments were mixed, underpinned by strong growth in North America and CALA, which was enough to offset more challenging conditions in EMEA and the Asia Pacific. With China growing around 4%, we estimate global telecom equipment revenues excluding China increase around 3% in 2022.

From a technology perspective, there is a bit of capex shift now underway between wireless and wireline. Multiple indicators suggest Broadband Access revenues surged in 2022, however, this double-digit growth was offset by stable or low-single-digit growth across the other five segments (Microwave Transport, Mobile Core Network, Optical Transport, RAN, SP Router & Switch).

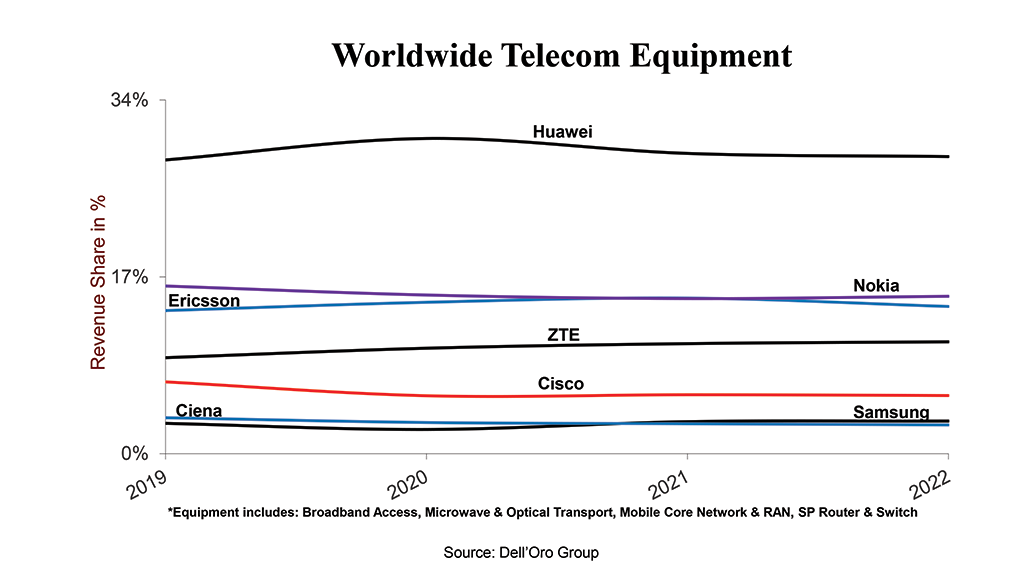

Vendor dynamics were relatively stable between 2021 and 2022, with the top 7 suppliers (Huawei, Ericsson, Nokia, ZTE, Cisco, Ciena and Samsung) driving around 80% of the overall market. Despite on-going efforts by the US government to limit Huawei’s TAM and access to the latest silicon, our assessment is that Huawei still leads the global telecom equipment market, in part because Huawei remains the #1 supplier in five out of the six telecom segments we track. At the same time, Huawei has lost some ground outside of China. Still, Nokia, Ericsson, and Huawei were the top 3 suppliers outside of China in 2022, accounting for around 20%, 18%, and 18% of the market, respectively.

Editor’s Note:

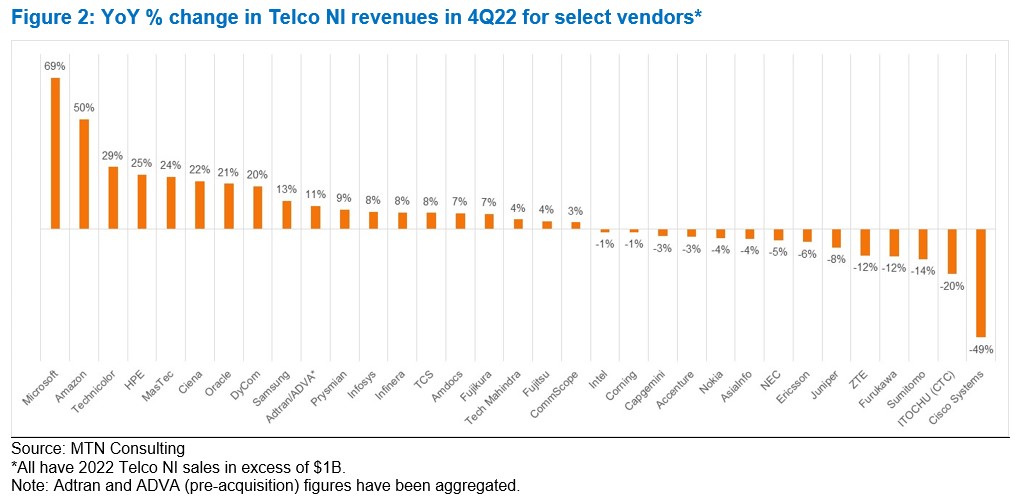

MTN Consulting recently noted that network spending was starting to flatten in the telco segment. In 3Q22, telco capex dipped 5% YoY, the first decline since 4Q20. The vendor market also weakened in 3Q22, as Telco Network Infrastructure (NI) vendor revenues grew just 2% after seven straight quarters of much stronger growth. Now we have a solid set of preliminary results for 2022’s final three months, 4Q22. For the 105 vendors available, Telco NI revenues fell by 1% YoY in 4Q22; this is the first decline for this group of Telco NI vendors since 2Q20, when COVID shut down economies. For CY2022, Telco NI grew just 2% YoY, down from +9% in 2021, when telcos splurged post-COVID, and the 5G RAN market saw a nice run-up. Among the larger reporting vendors, the best 4Q22 Telco NI growth was recorded at the three cloud providers (AWS, Azure, and GCP); engineering services companies Dycom and MasTec; NEPs Calix, Ciena, Samsung, and Technicolor (now Vantiva). New vendor Rakuten Symphony recorded the best overall growth rate in 4Q-2022, with revenues of $180M up 193% YoY. On the other side, Cisco, Ericsson, and ZTE saw the worst declines in 4Q-2022, due in part to a downswing in spending among their largest customers.

For the overall market, some of the decline seen in 4Q-2022 was inevitable, as telcos slow down their initial 5G network buildouts. Other negatives include higher interest rates, higher energy costs, weak economic growth, cloud alternatives to network builds, and 5G’s inability to deliver services revenue growth. Revenue guidance for 2023 from key vendors suggests a flat to slightly down market, as telcos absorb capacity and continue to wrestle with these challenges. Capex guidance from telcos is consistent.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Following five consecutive years of growth, the Dell’Oro Group believes there is more room left in the tank. Collectively the analyst team is forecasting the overall telecom equipment market to increase 1% in 2023 and record a sixth consecutive year of growth. Risks are broadly balanced and the analysts will continue to monitor the 5G rollouts in India, capex cuts in the US, and 5G slowdown in China (preliminary data by MIIT suggest new 5G BTS volumes will drop by a third in 2023 relative to 2022), wireless and broadband investments in Europe, forex fluctuations, and inventory optimization.

*Telecommunications Infrastructure programs covered at Dell’Oro Group, include Broadband Access, Microwave & Optical Transport, Mobile Core Network (MCN), Radio Access Network (RAN), and SP Router & Switch.

References:

Dell’Oro: PONs boost Broadband Access; Total Telecom & Enterprise Network Equipment Markets

UAE’s “etisalat by e&” announces first software defined quantum satellite network

Dubai’s etisalat by e& today announced the implementation of the Eutelsat quantum satellite solution, becoming the first telco in the country to expand “5G” network capabilities (NOTE: there are no standards for satellite 5G RAN- only for terrestrial RAN, e.g. ITU-R M.2150 and 3GPP Release 15-17) over a software-defined satellite network.

This deployment was a result of rigorous testing with customers for over a year to rapidly scale up the 5G mobile network deployment. etisalat by e& implemented Eutelsat’s latest technology Quantum satellite with the recently installed state-of-the-art Newtech Dialog Hub enhancing the mobile network capability.

“With the demand for ‘always-on’ connectivity as technologies like IoT, AI and blockchain make a bigger impact on consumer lives, satellite connectivity can empower communities and business in this rapidly evolving digital landscape,” said Khalid Murshed, Chief Technology and Information Officer, etisalat by e& UAE. “With the deployment of this satellite solution and technology, our customers will be able to access their data at 5G speeds even when terrestrial connectivity is unavailable, marking another important step towards the regions’ 5G adoption and bridging the digital divide,” he added.

Image Credit: e&, formerly known as Etisalat Group

………………………………………………………………………………………………………………………………………………………………………

“Eutelsat are proud to partner with etisalat by e& to deploy this 5G use case on the world’s first Software Defined satellite network,” said Ghassan Murat, Head of Connectivity Business Unit for Middle East, Africa and Asia Pacific, Eutelsat. “Our fully steerable beams are capable of meeting the most rigorous demands of Next Generation mobile and satellite networks.”

Oscar Garcia, Business Marketing and Product Innovation, etisalat by e&, said, “The need for connectivity has grown beyond traditional communications with customers wanting to access the highest speeds in the network to meet their requirements and demands for bandwidth-intensive applications such as GSM services, Remote IT, Unified communications, OTT, and media streaming among others.. The testing and implementation of this satellite solution greatly enhances the mobile network capability to address the futuristic development of new age applications while being able to build and deploy 5G use cases for various industry verticals and business.”

References:

https://eand.com/en/etisalat-uae.jsp

AST SpaceMobile Deploys Largest-Ever LEO Satellite Communications Array

European Space Agency & UK Space Agency chose EnSilica to develop satellite communications chip for terminals

FCC grants Amazon’s Kuiper license for NGSO satellite constellation for internet services

Bullitt Group & Motorola Mobility unveil satellite-to-mobile messaging service device

China Tower had ~2.1M telecom towers installed with 3.36M tower tenants at end of 2022

China Tower ended 2022 with 2.05 million telecom towers installed, representing a net increase of 17,000 sites from the end of 2021. The company installed approximately 745,000 5G base-stations during the year, with more than 96 percent of sites delivered through sharing existing network infrastructure. Through the end of 2022, China Tower reported that it has received cumulative orders of nearly 1.8 million new 5G cell sites. The total tower tenants rose by 102,000 in the year to 3.36 million, pushing the average number per tower from 1.62 as of the end of 2021 to 1.65 at end-2022.

China Tower primarily serves the country’s state-owned telecommunications service providers (TSP) – China Mobile, China Telecom, China Unicom, and China Broadnet. The four TSPs accounted for a total of nearly 3.4 million tower tenants, a 102,000 year-over-year increase. The TSP tenancy ratio increased from 1.60 to 1.65 over the same period last year, showing a continuous increase in the level of site colocation.

Operating revenue for 2022 reached $13.4 billion, up 6.5 percent YoY. Revenue from the TSP segment was $12.0 billion, up by 3.5 percent over the same period last year, and accounting for 90 percent of operating revenue. The TSP business comprises revenue from towers and indoor distributed antenna system (DAS) business. Towers contributed $11.3 billion, up nearly 2 percent, while DAS revenue was $845 million, a 34 percent YoY increase. Capital expenditures for new tower builds and site augmentation was $3.0 billion in 2022, up 5 percent over nearly $2.9 billion in 2021.

The company sees “5G + DAS” as its dual-growth engines, with DAS as the fastest growing segment. The DAS business focuses on providing 5G coverage under various scenarios in key sectors including education, cultural tourism, transportation, and healthcare, with an integrated approach to coordinating resources and demands.

At year-end 2022, China Tower’s DAS deployments covered buildings with a cumulative area of 7,390 million square meters, representing a 48 percent YoY increase. The company expanded DAS coverage to 10,429 kilometers in high-speed railway tunnels and to 9,611 kilometers in subways, coverage reaching a cumulative length of 20,040 kilometers, up 19 percent from a year ago.

China Tower has Commercial Pricing Agreements and Service Agreements with each of the TSPs. In a statement, the company reiterated its commitment to meeting its TSP customer network construction needs using innovative construction and service models that provide low-cost and efficient coverage.

Zhang Zhiyong, chairman of China Tower said: “Looking ahead, we will remain focused on grasping the opportunities brought by the development of 5G new infrastructure, the digital economy, and the green-oriented transition of energy. With a focus on “Digital Tower,” our Smart Tower business growth accelerated. Serving the national strategic goals.”

Tower business. China Tower advocated for the inclusion of 5G base-station sites in development planning and played an active role in setting the wireless communications specifications for buildings. Complying with these specifications, we have been included in the administrative approval process for new construction projects, further strengthening our ability to coordinate and share resources. We launched innovative low-cost construction solutions to sharpen our capability in providing integrated wireless communications coverage solutions. A higher level of resource sharing enabled us to comprehensively satisfy customer demand for 5G construction. We completed approximately 745,000 5G base-stations during the year, of which more than 96% were delivered through sharing existing resources. In addition, we focused our efforts on tackling difficult sites and continued to enhance our service quality. Alongside an improving capability in site maintenance, customer satisfaction grew. In 2022, our Tower business generated revenue of RMB77,204 million, or year-on-year growth of 1.8%. As of 31 December 2022, we managed 2.055 million tower sites, representing a net increase of 17,000 sites from the end of 2021. The number of TSP tenants reached 3.362 million, an increase of 102,000 from the end of 2021, and the TSP tenancy ratio also increased from 1.60 to 1.65 over the same period of last year, showing a continuous increase in the level of site co-location.

DAS business. China Tower focused on providing 5G coverage for key scenarios and key sectors including education, cultural tourism, transportation and healthcare, with an integrated approach to coordinating resources and demands. Playing an important role in coordinating site entry and construction, we were able to take up all DAS construction demand for key venues, scenarios and sectors, providing customers with differentiated and diversified indoor coverage solutions. In addition, we stepped up innovation to develop sharable DAS products and solutions. We enhanced our professional capabilities to optimize our advantages in providing low-cost and green and low-carbon DAS solutions, complemented by our quality services, driving accelerated growth in the DAS business. This business has increasingly become the second growth engine of our development. In 2022, our DAS business recorded revenue of RMB5,827 million, representing a year-on-year increase of 34.3%. As of 31 December 2022, we had covered buildings with a cumulative area of 7,390 million square meters, representing a year-on-year increase of 48.1%. Our high-speed railway tunnels and subway coverage reached a cumulative length of 20,040.2 kilometers, a year-on-year increase of 18.5%.

Grasping strategic opportunities to boost strong growth in Two Wings business:

By leveraging the opportunities brought forth by the growth of the “digital economy” and the “dual carbon” goals, we focused on product innovation and business optimization to fortify our competitive advantages. As a result, the Two Wings business sustained a robust growth trajectory with revenue in 2022 reaching RMB8,904 and accounting for 9.7% of our overall operating revenue, an increase of 2.6 percentage points from the same period in 2021. The business contributed 49.7% to our incremental operating revenue for the year, an increase of 9.7 percentage points year-on-year, further solidifying our multi-pillar business development structure.

Image courtesy of China Tower

…………………………………………………………………………………………………………………………………………………………………………………………

China’s wireless network operators had deployed a total of 2.29 million 5G base stations nationwide as of the end of November, according to the latest available data from China’s Ministry of Industry and Information Technology. This figure represents an increase of 862,000 compared to the end of 2021 and accounts for 21.1% of all mobile base stations in the country.

Chinese operators recorded a net gain of 16.53 million 5G subscribers in January, according to the operators’ latest available statistics. China Mobile, the world’s largest operator in terms of subscribers, added a total of 8.46 million 5G subscribers during the first month of the year. The carrier said it ended last month with 622.47 million 5G subscribers. China Mobile added a total of 227.2 million subscribers in the 5G segment during 2022.

Meanwhile, China Telecom added 5 million 5G subscribers last month to take its total 5G subscribers base to 273 million. During 2022, the telco added a total of 80.16 million 5G subscribers.

Rival operator China Unicom said it added a total of 3.07 million 5G subscribers during last month. The carrier ended January with 215.8 million 5G subscribers. China Unicom added over 42 million subscribers in the 5G segment during 2022.

…………………………………………………………………………………………………………………………………………………………………………………………

References:

China MIIT claim: 475M 5G mobile users, 1.97M 5G base stations at end of July 2022

China’s MIIT to prioritize 6G project, accelerate 5G and gigabit optical network deployments in 2023

Nokia and Kyndryl extend partnership to deliver 4G/5G private networks and MEC to manufacturing companies

Following their first partnership one year ago, Nokia and Kyndryl have extended it for three years after acquiring more than 100 customers for automating factories using 4G/5G private wireless networks as well as multi-access edge computing (MEC) technologies. Nokia is one of the few companies that have been able to get any traction in the private 4G/5G business which is expected to grow by billions of dollars every year. The size of the global private 5G network market is expected to reach $41.02 billion by 2030 from 1.38 billion in 2021, according to a study by Grand View Research.

The companies said some customers were now coming back to put private networks into more of their factories after the initial one. “We grew the business significantly last year with the number of customers and number of networks,” Chris Johnson, head of Nokia’s enterprise business, told Reuters.

According to the companies, 90% of those engagements—which span “from advisory or testing, to piloting, to full implementation”—are with manufacturing firms. In Dow Chemical’s Freeport, Texas, manufacturing facility which is leveraging a private LTE network using CBRS frequencies to cover 40 production plants over 50-square-kilometers. The private wireless network increased worker safety, enabled remote audio and video collaboration, personnel tracking, and vehicle telematics, the companies said. Dow Chemical is now planning to expand the same coverage to dozens of its factories, said Paul Savill, Kyndryl’s [1.] global practice leader. “Our pipeline has been growing fundamentally faster than it has been in the last 12 months,” he said. “We now have over 100 customers that we’re working with in the private wireless space … in around 24 different countries.”

Note 1. After getting spun off from IBM in 2021, Kyndryl has focused on building its wireless network business and has signed several agreements with cloud providers.

The current active engagements are across more than 24 countries, including markets like the U.S. where regulators have set aside spectrum assets for direct use by enterprises; this means it’s increasingly possible for buyers to access spectrum without the involvement of mobile network operators.

“As enterprises seek to accelerate and deliver on their journeys towards Industry 4.0 and digitalization, the effective integration and deployment of advanced LTE and 5G private wireless networking technologies becomes instrumental to integrate all enterprise operations in a seamless, reliable, efficient and built in a secure manner,” said Alejandro Cadenas, Associate Vice President of Telco and Mobility Research at IDC. “This expanding, powerful, relationship between Nokia and Kyndryl is a unique combination of vertical and horizontal capabilities, and offers IT, OT and business leaders access to the innovation, tools, and expert resources they need to digitally transform their operations. The partnership offers a compelling shared vision and execution that will enable customers across all industries and geographies to access the ingredients they need to deliver against the promise of digital acceleration, powered by network and edge computing.”

The expanded effort will be enhanced with Kyndryl’s achievement of Nokia Digital Automation Cloud (DAC) Advanced accreditation status, which helps ensure that enterprise customers benefit from an expanded lineup of expert resources and skilled practitioners who have extensive training and deep understanding of Nokia products and solutions. In addition, customers will gain access to Kyndryl’s accelerated network deployment capabilities and support of Nokia cellular radio expertise in selected markets.

In response to a question about how direct enterprise access to spectrum has informed market-by-market activity, Kyndryl Global Practice Leader of Network and Edge Paul Savill told RCR Wireless News in a statement, “Spectrum availability is rapidly becoming less of a barrier, with governments allocating licensed spectrum for industrial use and the emergence of unlicensed wireless networking options (such as CBRS in the US, and MulteFire).”

The companies have also developed automated industrial drones that can monitor a site with different kinds of sensors such as identifying chemicals and video recognition as part of surveillance. While drones have not yet been deployed commercially yet, customers are showing interest in rugged, industrialized non-stop automated drone surveillance, Johnson said.

References: