Month: June 2020

Bell Canada Announces Largest 5G Network in Canada

Bell Canada has announced the launch of what it says is Canada’s largest 5G mobile network. Bell’s 5G services have launched in Montreal, the Greater Toronto area, Calgary, Edmonton and Vancouver and will expand to more cities in the future.

Bell Canada is selling a number of compatible 5G devices, including the Samsung Galaxy S20 5G series, the LG V60 ThinQ 5G Dual Screen and the Motorola Edge+, all from CAD 0 upfront with Bell SmartPay. 5G access is CAD 10 a month on any Bell Mobility postpaid plan and will be free as a bonus until the end of March 2021.

“Bell has built the country’s best networks since 1880 with a goal to advance how Canadians connect with each other and the world, and we’re proud to take the next step forward with the country’s largest 5G network,” said Mirko Bibic, President and CEO of BCE and Bell Canada. “As the world rapidly embraces the Fifth Generation of wireless, Bell is ready to ensure Canada remains at the forefront of 5G innovation and accessibility. The COVID-19 crisis has clearly underscored the critical importance of high-quality networks to keeping consumers, businesses and governments connected and informed, and Bell remains committed to building the best as we take wireless into the next generation.”

“With 5G coverage that is 6 times greater than the next largest network, the biggest selection of 5G-capable devices available and faster data speeds than even our award-winning Advanced LTE network, Bell Mobility has once again raised the bar in Canadian wireless,” said Claire Gillies, President of Bell Mobility. “As the scale, speed and capabilities of our next-generation network continue to grow, Bell Mobility will champion the 5G customer experience in every part of our business.”

The first company to trial mobile 5G technology in Canada, Bell is working with a range of leading global and domestic 5G partners, including Ericsson and Nokia, to accelerate Canada’s 5G innovation ecosystem. This includes continued funding of R&D at Canadian institutions, such as the partnership announced today between Western University and Bell to create a new academic centre for research into 5G applications across health, agriculture, transportation, manufacturing and other sectors. On the international stage, Bell is a leader in the setting of global 5G standards with our participation in the Next Generation Mobile Networks (NGMN) consortium and Third Generation Partnership Program (3GPP).

…………………..………………………………………………………………………………

Bell also announced a partnership with Western University, to create an advanced 5G research centre, including the deployment of a campus-wide 5G network. The Canadian carrier will invest CAD 2.7 million into the centre but also help fund research and development initiatives with the university, including training opportunities and tech innovations.

Specifically, the centre will study 5G applications, including virtual and augmented reality use, smart vehicle and city applications, autonomous vehicles, industrial IoT applications, multi-access edge computing, batter and small cell research, machine learning, artificial intelligence and other system for use in fields such as medicine, agriculture, transportation and communications.

…………………..…………………………………………………………………………..

Bell Canada is the largest communications company in Canada. With more than 22 million consumer and business connections, Bell provides advanced broadband wireless, TV, Internet and business communication services throughout the country.

Bell Media is Canada’s premier multimedia company with leading assets in television, radio, out of home and digital media.

References:

Nokia study of consumer & enterprise users: FWA and Video are top 5G services

In a study of wireless consumer users conducted with Parks Associates, Nokia found that fixed wireless access (FWA) services as the top-ranked use case by global consumers (76% of all respondents), although with the caveat that mobile network operators must prove that 5G can perform as well as fixed broadband.

We find that quite interesting, as FWA is NOT a use case for IMT 2020– the global 5G standard (yet to be completed).

The study of enterprise users found that businesses identify video as the most attractive 5G WAN and LAN applications, with 83% finding it appealing and 48% citing 5G-enhanced video monitoring as a near-term opportunity. 90 percent of consumers said that uninterrupted video calls will be a “very valuable” part of 5G connectivity. 83 percent of businesses said that video calls are a “compelling” use case for 5G.

Two-thirds of the enterprises surveyed in the study (65%) said they are familiar with 5G, and one-third (34%) report they are already using 5G and are highly satisfied with the service. The report also noted that while nearly half (47%) of IT decision-makers say their organizations have already started planning for 5G, others are waiting for more widespread 5G availability (54%), and nearly one-third (30%) reported they would also like to better understand the value of 5G before developing a strategy to use it in their organization.

Nokia noted that the research was carried out before the COVID-19 pandemic, but claimed the results were still valid, “perhaps more so in this new environment,” said Josh Aroner, vice president of communication service provider marketing at Nokia. “While current networks are performing well, consumers are newly appreciating the value of quality networking.”

The consumer study surveyed 3,000 people in the UK, US and South Korea, while the enterprise study surveyed over 1,000 IT decision-makers in segments including energy, manufacturing, government/ public safety and automotive/transportation.

Josh Aroner, Vice President of Communication Service Provider Marketing, commented: “Nokia commissioned this research prior to the current global coronavirus pandemic but its insights are still valid and applicable, perhaps moreso in this new environment. While current networks are performing well, consumers are newly appreciating the value of quality networking.

“Video has been a bedrock of social interaction and 5G can greatly improve this capability, while social isolation and remote work likely increase appeal for immersive experience applications. FWA is an attractive early use case for 5G, especially with remote install, but operators must make an informed decision about how to invest in it and in which geographic location.”

Additional report findings:

- Nearly half of those who work remotely indicate a strong willingness to switch providers for 5G service and more likely to intend to purchase a 5G phone. Greatly expanded remote work experience may drive plan and phone upgrades.

- Nearly two-thirds of early 5G users are highly satisfied with the speeds they experience on 5G networks, compared with less than half of 4G users.

- 45 percent of all consumers find connected car concepts appealing with navigation and safety capabilities seen as most valuable, but this jumps to 73 percent amongst vehicle owners. 53 percent of vehicle owners said they would be interested in bundling car connectivity with a 5G data plan.

- Two-thirds of consumers find 5G-enabled Augmented Reality and Virtual Reality services appealing and 56 percent were drawn to cloud gaming. Mandatory physical distancing may be the inflection point for these use cases.

- 77 percent of companies using connected equipment find 5G-enabled remote control machinery appealing. 82 percent of respondents with existing cloud robotics deployments find the idea of 5G-enabled cloud robotics “highly appealing”

Network operators will no doubt be pleased to learn that there is demand among consumers for 5G, although they should note that customers would be prepared to switch operator if their current provider is slow to launch 5G services.

Methodology:

This survey fielded 3,000 smartphone owners across the US, UK, and Korea. Demographic quotas set for age, gender, and household income ensure the sample is representative of the population of each market surveyed. Respondent Characteristics: Adults, ages 18 and older; Smartphone owners; Broadband internet users; Primary decision makers.

Resources:

- To download the research, please go here: The value of 5G services: Consumer perceptions and the opportunity for CSPs

- To download images please go to the Media Library

- Infographic: 5G opportunities for consumers

- Webpage: Extraordinary opportunities for 5G

- Webpage: Nokia FWA

- Webpage: Nokia 5G

About Nokia

We create the technology to connect the world. Only Nokia offers a comprehensive portfolio of network equipment, software, services and licensing opportunities across the globe. With our commitment to innovation, driven by the award-winning Nokia Bell Labs, we are a leader in the development and deployment of 5G networks.

Our communications service provider customers support more than 6.4 billion subscriptions with our radio networks, and our enterprise customers have deployed over 1,300 industrial networks worldwide. Adhering to the highest ethical standards, we transform how people live, work and communicate. For our latest updates, please visit us online www.nokia.com and follow us on Twitter @nokia.

Media Inquiries:

Nokia

Communications

Phone: +358 10 448 4900

Email: [email protected]

References:

Nokia: Video is still the 5G ‘killer app’ for both consumers and enterprises

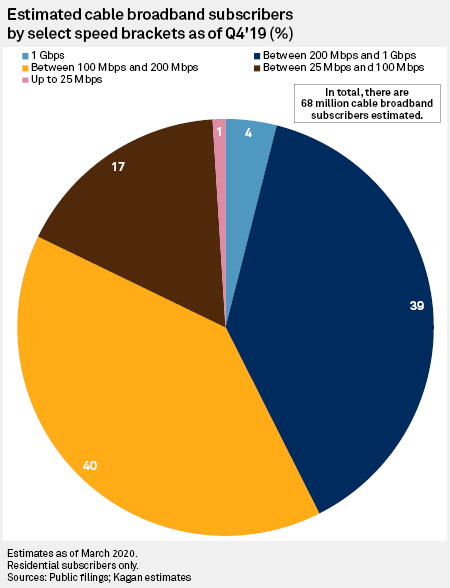

Dell’Oro: Broadband Access Equipment Revenue -15% YoY; Radical Change Coming

A new report by the Dell’Oro Group found that total global revenue for wireline Broadband Access equipment (=Cable, DSL, and PON equipment) dropped to $2.5 B, down 15 percent year-over-year (YoY) from 1Q 2019. The first quarter activity, which is seasonally slow to begin with, was hurt by supply chain disruptions throughout Asia-Pacific as a result of the COVID-19 pandemic.

“The first half of 2020 will give way to a sustained rebound in broadband equipment spending in the second half of the year,” said Jeff Heynen, Senior Research Director, Broadband Access and Home Networking. “The need to expand residential broadband speeds and availability will ultimately win out over the current macroeconomic slowdown,” explained Heynen.

Following are additional highlights from the 1Q 2020 Broadband Access Quarterly Report:

- Total cable access concentrator revenue decreased 22 percent YoY to $211 M, driven by a slowdown in CCAP license purchases in North America.

- Total DOCSIS 3.1 CPE shipments remained strong and increased to 5.8 M, representing 67 percent of total Cable CPE shipments. It’s forecast to reach 70 percent of shipments by the end of 2020.

- Total PON ONT (passive optical network/optical network terminal) unit shipments decreased 15 percent YoY, as new installations were limited by the pandemic.

Heynen also expects cable access revenues to rebound a bit in the second quarter as cable operators boost upstream capacity by purchasing additional channel capacity on traditional CCAPs and move ahead with mid-split and high-split projects that expand the amount of spectrum dedicated for the cable network upstream.

Cable remote PHY deployments remain slow today but could pick up as operators begin to touch amplifiers and other parts of the network for future expansions of the cable network upstream. In those cases, “you’re almost required to upgrade to remote PHY at some point,” explains Heynen.

Q1 didn’t produce a major swing in cable access market share among CommScope/Arris, Casa Systems and Cisco Systems. Harmonic, meanwhile, has already warned that some cable network virtualization projects have been pushed out a bit as cable operators reassessed their near-term network-facing priorities during the pandemic.

Regarding the fiber-to-the-premises (FTTP) market, Dell’Oro found that total PON ONT (optical network terminal) unit shipments dropped 15% year-over-year as new installations were hindered by the pandemic. However, OLT (optical line terminal) ports were relatively flat over that period, indicating that there is sustained investment being placed in FTTP infrastructure in regions such as Europe, says Heynen.

Heynen expects that activity centered on the Rural Digital Opportunity Fund (RDOF) could provide some lift to the FTTP sector in the US next year.

The Dell’Oro Group Broadband Access and Home Networking Quarterly Report provides a complete overview of the Broadband Access market with tables covering manufacturers’ revenue, average selling prices, and port/unit shipments for Cable, DSL, and PON equipment. Covered equipment includes Converged Cable Access Platforms (CCAP) and Distributed Access Architectures (DAA); Digital Subscriber Line Access Multiplexers ([DSLAMs] by technology ADSL/ADSL2+, G.SHDSL, VDSL, VDSL Profile 35b, and G.FAST); PON Optical Line Terminals (OLTs), Cable, DSL, and PON CPE (Customer Premises Equipment); and SOHO WLAN Equipment, including Mesh Routers. For more information about the report, please contact [email protected].

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, networks, and data center IT markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions. For more information, contact Dell’Oro Group at +1.650.622.9400 or visit www.delloro.com.

………………………………………………………………………………………………………………………………………………………

Source: S&P Global

………………………………………………………………………………………………………………………….

References:

………………………………………………………………………………………………………………………….

Addendum: Cable network undergoing a ‘radical transformation’

Belal Hamzeh, CTO and SVP at CableLabs, told a Light Reading virtual audience that the evolution of the network and a rethinking of HFC are necessary to prepare the cable industry to support a wave of new requirements for a broader set of high-capacity, low-latency applications. These next-gen applications will span everything from augmented and virtual reality and remote healthcare to mobile backhaul and edge computing and others that are still being thought of.

“The requirements of the network are becoming quite diverse,” he said. “For us to efficiently and effectively handle that, we have to look at entirely new perspectives … Rather than looking at the platform as a connectivity platform, we need to start looking at the platform as a connectivity and compute platform.”

Virtualization, Hamzeh added, is a “huge enabler for this transformation.” To address that critical piece, CableLabs has teamed with partners, including Altran, on an open source project nicknamed “Adrenaline” that aims to provide a centrally managed distributed and heterogeneous computing platform that supports the deployment of workloads across the operator’s infrastructure.

“It’s a cable-first initiative, but this is also a general purpose platform,” said Shamik Mishra, VP of research and innovation at Altran, a company that’s primarily focused on engineering and R&D services for multiple industries, including the telecom sector.

“We’re not trying to constrain what use cases there are [for Adrenaline],” added Randy Levensalor, principal architect with CableLabs’s future infrastructure group in the office of the CTO.

Telcos need to fill in gaps to be Edge Computing (5G, IIoT) leaders

The rapidly expanding edge computing space represents a $17 billion opportunity for telecom service providers over the next three years, but those companies are being overlooked by enterprises when it comes to deployments, according to a recent study by World Wide Technology done in conjuction with Analysys Mason.

“The Edge Disconnect” report found that service providers’ deep connectivity expertise and investments in 5G infrastructure are advantages, but that they need to fill gaps in their offerings to become a one-stop shop for enterprises looking to expand to the edge with connectivity, infrastructure, and applications.

“Service providers are under immense pressure to monetize 5G infrastructure investments and create cost-reducing efficiencies,” said Dan Graham, global product leader for edge computing at WWT. “Edge computing provides services as close to the end user or device as possible and is essential to the value proposition of 5G. Next-gen applications, including self-driving vehicles, remote surgery, Industrial Internet of Things (IIoT), will all hinge on the edge.”

The report found that IT companies and tech companies, rather than telecoms service providers, are invariably seen as the “edge experts.” In particular, the report authors wrote:

“Connectivity is the cornerstone of an enterprise edge strategy, yet enterprises don’t see connectivity providers as the partner they need to make their strategy a success.”

How can carriers better show off their edge muscles in front of enterprises? WWT makes a number of suggestions based on the research, which, it insisted, “reflected the market’s view and was in no way influenced by WWT’s own perspective on edge.”

By developing a “pre-packaged edge solution” composed of connectivity and system integration capabilities, as well as an application platform (which WWT thinks will generate nearly 60% of the resulting revenue) “telecoms service providers can cement their place in the new era of enterprise data management.”

“Cloud service providers and systems integrators may talk up to their ability to satisfy customers’ connectivity needs, but telecoms service providers have been delivering these services for decades,” reassured the authors. “They have an innate understanding of the intricacies involved, and how these can be optimized.”

……………………………………………………………………………………………………………………………………………..

Industries covered by the research include transport, public sector, manufacturing, retail, financial services and healthcare. In each of these sectors, distributing computing through Edge implementations presents an opportunity to transform data management in line with the realities of an increasingly connected digital economy, as well as introducing new cost efficiencies and improvements to data security and compliance.

The report also identifies the 30 industry-specific Edge use cases likely to deliver the greatest revenue potential, all of which benefit from Edge’s suitability for transformative, data-intensive applications.

Key findings in the report:

- Options: Only 6% of enterprise decision-makers would choose service providers for their edge implementations. Instead, 41% would primarily opt for a technology company, while 31% would go with a public cloud provider.

- Demand: 59% of the $17 billion opportunity is at the level of user-facing application and service platforms, far more than connectivity-focused roles telecom service providers play. Telecom service providers need to expand what they offer beyond connectivity to capture more of the opportunity.

- Edge drivers: Across multiple industries, the top reasons organizers are embracing the edge are newer or enhanced customer experiences, data security and privacy, and cost efficiencies.

- Data management: Enterprises see the edge as a way of reducing data management costs by up to 20%.

The edge continues to be a promising opportunity for telecom service providers, cloud service providers, and channel partners. The report says that service providers’ deep understanding of connectivity is a key advantage. With the assistance of a partner who can bridge any gaps in their knowledge of vertical-specific use cases, they can develop pre-packaged solutions covering all three of the above requirements. Achieve this, and service providers will be on the road to changing enterprise perceptions, increasingly cementing themselves as the de facto partners for enterprise Edge deployments.

Grand View Research analysts predict that the global market for edge computing will grow 37.4% a year through 2027, when it will grow to $43.4 billion. A key catalyst for that growth will be 5G technology, which promises significantly faster speeds and more bandwidth and capacity than current 4G LTE networks.

…………………………………………………………………………………………………………………………………………………

References:

https://channelnomics.com/2020/06/09/ingram-micro-cloud-simplifies-complex-aws-world/

https://www.lightreading.com/the-edge/telcos-need-to-up-their-edge-game—report/d/d-id/761562?

Broadband Forum and LAN Laboratory Expand Certification Program to include XGS-PON

As demand for fiber networks continues to grow, the Broadband Forum has expanded its BBF.247 Optical Network Unit (ONU) Certification Program to include XGS-PON.

This latest update extends the program to a variety of key features needed by operators deploying XGS-PON networks. The certification is just one piece of Broadband Forum’s vision to provide network operators with the tools, open specifications, and open source references necessary to bring new services and technologies to their customers more rapidly. Certified ONU products can be deployed quickly, with improved interoperability to existing Optical Line Terminal (OLT) equipment already deployed. Similarly, certified ONU products will also work directly with newer Broadband Forum specifications, including the forthcoming virtual OMCI specifications and software defined access networks.

The XGS-PON extensions add to the BBF.247 G-PON initiative – which has now certified nearly 100 products since its launch in 2011. The new test plan will see ONUs undergo rigorous testing at Broadband Forum’s official certification program test laboratory Laboratoire des Applications Numeriques (LAN Laboratory), using MT2’s ONU testing solution. The work will confirm conformance to the latest PON ITU-T standards, providing network operators with assurance that they can deliver efficient networks and a high-quality customer experience. New additions to the technology are also now tested, including extended OMCI messages format, Enhanced Unicast & Multicast Operations, and Capacity Tests & Performance Monitoring. This increases the number of certification test cases by more than 50% compared to the previous version.

Eight products, including single or multi-user port ONUs/L2 and Residential Gateways from Altice Labs, CommScope, Huawei, Humax, KAONMEDIA, Sagemcom, Sercomm and ZTE have already been certified under the new BBF.247 certification program.

“The introduction of XGS-PON certification by Broadband Forum is a significant and positive step for the PON ecosystem as interoperability will encourage growth,” said Jaeseok Kim, Head of Infra Planning at SK Broadband. “This will become increasingly important as more operators look to upgrade existing network to meet consumer demand for Gigabit + speeds.”

Claudio Mathys, Product Manager Wireline Access Networks at Swisscom (Schweiz) AG, added: “Establishing interoperability and testing requirements are key elements in a liberated market. The introduction of XGS-PON from Swisscom as a technology leader – in conjunction with the certification and testing program from Broadband Forum – will significantly enhance the confidence from our competitors for CPE certification as based on industry standards and independent references. Achieving Broadband Forum certification is the entry ticket for connectivity to our network. We will definitely avoid the painful experience made with xDSL interoperability/complexity – right from the beginning.”

Hugues Le Bras, Network Engineer in Fixed Access Networks at Orange, said: “The role of interoperability and standards has only become more important as broadband grows in popularity and operators upgrade their networks to meet consumer demand. Orange already requests BBF.247 certification for each ONU deployed on the field. However, this expansion of Broadband Forum’s certification program will give us confidence when deploying next-generation technology that will enable the future era of connectivity. The latest additions to the certification also bring new features, such as flexibility and monitoring, which are essential for Orange throughout the ONU life.”

A future XGS-PON interoperability test event will take place at LAN Laboratory, in Tauxigny, France, from October 5 to 9, 2020, allowing vendors worldwide to exercise their OLT or Optical Network Terminal (ONT) solutions against each other. The event will give all equipment vendors the opportunity to improve the interoperability of their products by testing them against the other solutions presented at the event.

“Our existing G-PON certification has made a significant impact on ensuring products meet standards, and this latest expansion of the program will give operators the confidence to roll out mass XGS-PON deployments,” said Robin Mersh, CEO at Broadband Forum. “We now want to instill this same assurance in the industry for upcoming ITU PON technology, including XGS-PON and NG-PON2. XGS-PON is a major step in network evolution, supporting the expansion of 5G and through BBF.247 certification, we can ensure network interoperability.”

Thierry Doligez, Director of LAN Laboratory, said: “Both operators and vendors increasingly recognize the importance of certification in order to speed up deployment and we are proud to partner with Broadband Forum on this extension of its G-PON certification program. As operators move to upgrade their networks to meet increasing consumer demand, the new testing will make sure they are investing in trusted products which will guarantee a certain level of service. ONU manufacturers will also benefit from this substantial program update as it will give them the chance to prove their conformance against enhanced features.”

For more information or to actively get involved with Broadband Forum’s work on higher speed PON technologies, visit: www.broadband-forum.org.

……………………………………………………………………………………………………………………………………….

BBF.247 certification program is open to all GPON, XG-PON and XGS-PON ONU products with Ethernet Interfaces and is based on the Broadband Forum’s TP-247/IR-247 test plan. It tests conformance to TR-156 and TR-280 using OMCI as defined in the ITU G.988, which are the most critical standards to interoperable implementations.

The Broadband Forum has reviewed and authorized the following independent testing agency to administer the approved BBF.247 tests and assess eligibility of products for the Broadband Forum Certification. For more information or to schedule testing, please contact the laboratory directly:

- LAN www.lanpark.eu

-

- Since 2009, the BBF has collaborated with FSAN (Full Service Access Network) on interoperability testing plugfests on the physical, TC and upper layers for GPON, with FSAN leading on the first two and BBF on the last.

……………………………………………………………………………………………………………………………………………….

About Broadband Forum

Broadband Forum is the communications industry’s leading organization focused on accelerating broadband innovation, standards, and ecosystem development. Our members’ passion – delivering on the promise of broadband by enabling smarter and faster broadband networks and a thriving broadband ecosystem.

A non-profit industry organization composed of the industry’s leading broadband operators, vendors, and thought leaders, our work to date has been the foundation for broadband’s global proliferation and innovation. For example, the Forum’s flagship TR-069 CPE WAN Management Protocol has nearly 1 billion installations worldwide.

Broadband Forum working groups collaborate to define best practices for global networks, enable new revenue-generating service and content delivery, establish technology migration strategies, and engineer critical device, service & development management tools in the home and business IP networking infrastructure. We develop multi-service broadband packet networking specifications addressing architecture, device and service management, software data models, interoperability and certification in the broadband market.

Our free technical reports and white papers can be found at https://www.broadband-forum.org/

About Laboratoire des Applications Numeriques (LAN Laboratory)

The Laboratoire des Applications Numeriques (LAN) is a unique independent laboratory specialized in conformance, interoperability and coexistence tests of devices deployed by telecom operators in the access and home networks (DSL, G-PON, Broadband-PLC, …), by DSOs in Smartgrids networks using powerline communications (G3-PLC), and by the industry in video security networks (E&PoC). LAN also offers on-demand test services dedicated to PON network operators, addressing their needs in terms of pre-deployment qualification tests for each specific network they operate. LAN is one of the Broadband Forum’s Approved Test Laboratory (ATL), the unique one accredited by the Broadband Forum to conduct the worldwide recognized BBF.247 certification tests for G-PON, XG-PON and XGS-PON terminals.

For more information on Laboratoire des Applications Numeriques, please go to www.lanpark.eu, follow @Laboratoire_LAN on Twitter, or send an Email to [email protected].

About MT2

MT2 leads the industry in FTTH G-PON and XGS-PON network test, offering troubleshoot, monitoring deep analysis of products, and ‘single-click’ automated test suite solutions. MT2’s analyzers and OLT emulators have the unique powerful features to allow the user to simply ‘software-select’, and switch between GPON, XG-PON, XGS-PON or NG-PON2, all within the same single system. MT2 ensures the complicated protocols and subscriber internet access traffic complies with every spec, automatically, using a powerful and intuitive user interface, high precision and innovative design. MT2 actively contributes to the Broadband Forum activity, as a test-tool vendor, and developed its FTTH automated test suites for functionality and performance testing, covering BBF.247, TR-309 and TR-255, critical to ensure system quality and full validation of any operator’s FFTH network.

For more information on MT2, please go to www.mt2.fr, follow MT2ftth on LinkedIn, or send an Email to [email protected]

…………………………………………………………………………………………………………………………………………….

References:

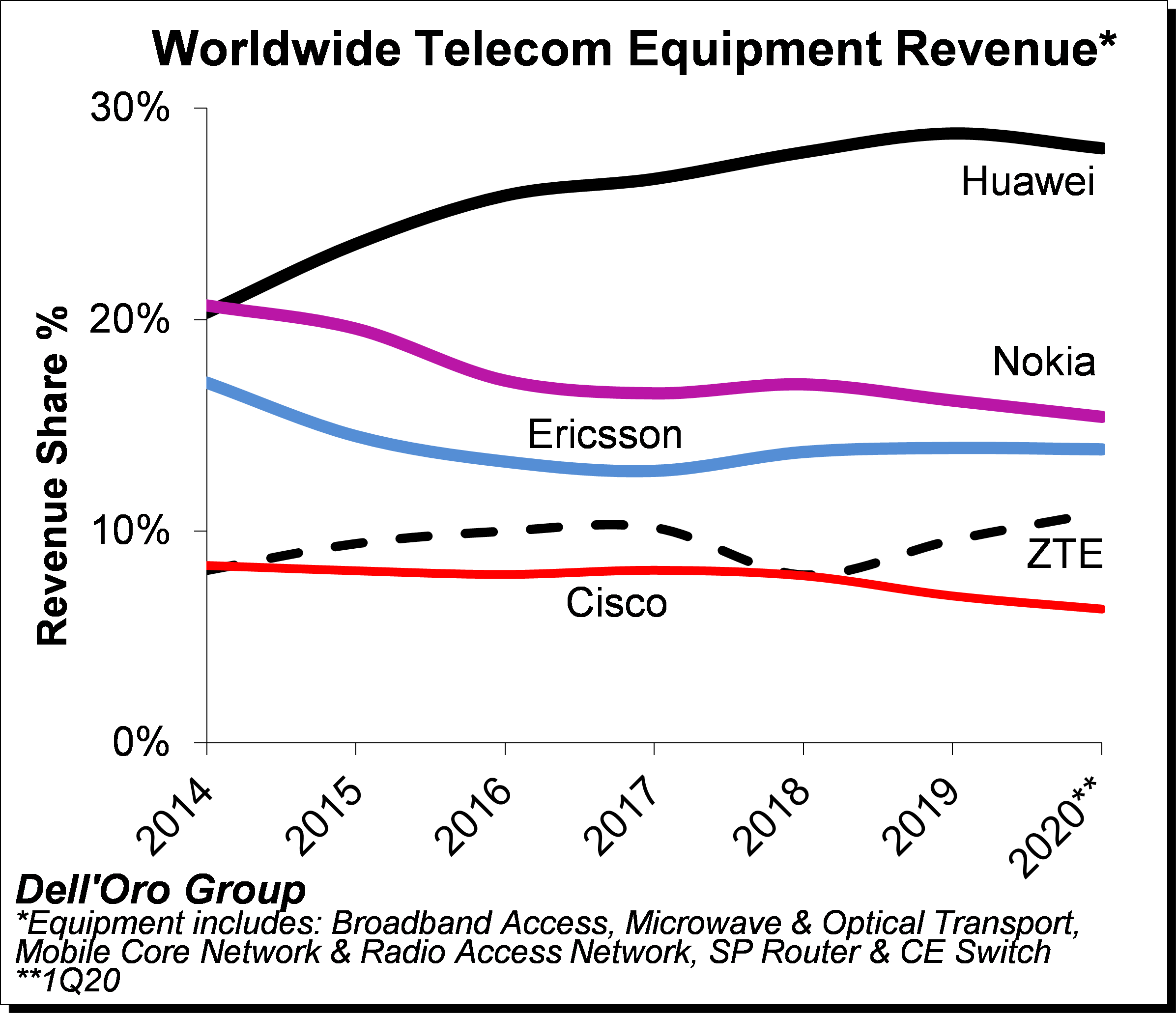

Dell’Oro: Telecom Equipment Market declined 4% YoY; Statista: $49.3B revenues in 2020

Preliminary estimates suggest 1Q20 revenue shares relative to 2019 revenue shares for the top five suppliers – the latter indicated herein parenthesis – show that Huawei, Nokia, Ericsson, ZTE, and Cisco comprised 28% (29%), 15% (16%), 14% (14%), 11% (10%), 6% (7%), respectively.

Table 1: Telecom equipment market shares

| Vendor | 2019 market share | Q1 2020 market share |

| Huawei | 29% | 28% |

| Nokia | 16% | 15% |

| Ericsson | 14% | 14% |

| ZTE | 10% | 11% |

| Cisco | 7% | 6% |

| Source: Dell’Oro Group | ||

Additional key takeaways from the 1Q2020 reporting period include:

- Following two years of consecutive growth in 2018 and 2019, the overall telecom equipment market started the year on a weaker note, reflecting mixed market conditions as the positive market sentiment with mobile-related segments, including RAN and Core, was not enough to offset reduced demand for Broadband Access, Routers and CE Switch, and Optical/Microwave Transport.

- While healthy end-user fundamentals and positive 5G momentum outweighed downward risks associated with the COVID-19 pandemic for both RAN and Core investments, the pandemic had a more material impact on some of the non-wireless related segments, driven partly by supply chain disruptions and weakened demand as a result of increased macroeconomic uncertainty.

- Within the technology segments, Mobile RAN and Core revenues together advanced at a single-digit rate, accounting for nearly half of the overall telecom equipment market during 1Q20. At the same time, the combined revenues for Broadband Access, Microwave Transport, and Routers and CE Switch declined at a double-digit pace Y/Y, accounting for about a third of the overall market.

- In contrast to previous recessions, the COVID-19 slowdown is shifting and transforming the way we use the network. But a shift in how users are consuming data doesn’t necessarily result in a corresponding increase in spending on new infrastructure to support that traffic growth. Some suppliers and service providers indicated that network capacity upgrades were required to accommodate data traffic growth, however, traffic surges did not lead to significant demand for network capacity upgrades across all the telecom equipment segments.

- Even though the pandemic is still inflicting high human and economic losses, the Dell’Oro analyst team collectively expect market conditions and supply chain risks to be more favorable in the second half of 2020, propelling the overall telecom equipment market to advance 1% in 2020, reflecting a downward revision from the previous 2% growth outlook.

Dell’Oro Group telecommunication infrastructure research programs consist of: Broadband Access, Microwave Transmission & Mobile Backhaul, Mobile Core Networks, Mobile Radio Access Network, Optical Transport, and Service Provider (SP) Router & Carrier Ethernet Switch.

…………………………………………………………………………………………………….

Separately, Statista reports that telecom equipment spending is projected to increase from 44.8 billion U.S. dollars in 2015 to around 49.3 billion U.S. dollars in 2020. In 2019, the estimated revenue of the entire global telecommunications industry was US $610.4 billion.

Ericsson, Cisco Systems, Fujitsu, Nokia, NEC Corporation and Qualcomm are the leading telecom equipment companies worldwide. Cisco Systems is the leading Ethernet switch vendor, with more than 50 percent of the market share. Ethernet switches are an important and profitable part of the industry, as they are an integral part of IT infrastructure. They are used to receive, process and transmit data between two devices connected by a physical layer. Together, the top 5 vendors of Ethernet switches generated more than 25 billion U.S. dollars in revenue in 2017. Cisco is also the main vendor of enterprise WLAN, accounting for 45 percent of the global market share. HPE/Aruba, Arris/Ruckus, Ubiquiti and Huawei are also important vendors of enterprise WLAN worldwide.

Ethernet switch, WLAN and telecom towers are only a few examples of telecom equipment. This industry is vast, and includes other important markets such as smartphones. More than 1.5 billion smartphones were sold worldwide in 2017. Samsung, the global mobile market leader since 2012, sold about 20 percent of this total. Apple and Huawei are Samsung’s closest competitors in the market, with around 14 percent and 10 percent of the global smartphone market share respectively.

References:

OMDIA: South Korea is 5G market leader amongst 22 countries

Market research firm OMDIA – formerly known as Ovum (including IHS-Markit IT acquisition) – has released the first version of its 5G Market Progress Assessment (end-2019) report, showing that South Korea is the undisputed leading country for 5G deployment in the twenty two leading 5G countries analyzed for their deployment of 5G technology.

The OMDIA research assessed the deployment progress of 5G based on operator launches, network coverage, subscriber take-up as well as 5G spectrum availability and regulatory ecosystem.

Based on these factors OMDIA’s research concluded that South Korea – as it did in the 4G era – has established itself as the early market-leader for 5G technology deployment. South Korea, Kuwait, and Switzerland are among a small group of markets notable for 5G coverage exceeding 50% of their subscriber base.

According to the report, South Korea is leading the way with adoption reaching 4.67 million subscribers at the end of December, which equates to about seven per cent of wireless services in the market. That number is now over 6 million as we reported in this article.

- Spectrum – 2,680 MHz across the 3.5 and 28 GHz bands

- Service launches – all three Korean service providers have commercial offerings available to the mass market, and MVNO services have been launched

- Network coverage – approximately 90% population coverage

- 5G take-up – 4.67 million 5G subscribers, or 7% of the mobile market

- Ecosystem – Strong government support and leading local vendor ecosystem

South Korea has exceeded expectations in each of the above criteria, a trend which should continue over the next few years in light of the government’s intention to make a further 2,640 MHz of bandwidth available for 5G networks by 2026.

Editor’s Note: South Korea’s IMT 2020 RIT submission (see Document IMT-2020/25) is being progressed by ITU-R WP5D, even though an ATIS sponsored evaluation group [ATIS WTSC IMT-2020 Independent Evaluation Group (IEG)] found that it is technically identical to the 3GPP submission.

…………………………………………………………………………………………………………………………………………..

“Limited coverage, device availability and cautious launches has limited take-up in other global markets,” said Stephen Myers, OMDIA Principal Analyst. “However, expansive coverage rolled out by Sunrise and Swisscom in Switzerland, Ooredoo and Vodafone in Qatar and Kuwait’s three service providers has rivalled Korea for breadth of market coverage.”

The report is based on data relating to the end-December period and was originally due for publication in mid-March but was delayed because of the impact of COVID-19.

Omdia Principal Analyst Stephen Myers said:

The global market is steadily gearing up for 5G deployment but right now South Korea is leading the way – although markets like Switzerland have also made steady progress.

Across the world we are seeing governments and regulators fine-tuning their 5G spectrum allocations and operators get ready for their 5G launches and expand network coverage in those countries where 5G has already launched.

We can expect to see a much larger number of commercial 5G launches in major global markets in the next 12-18 months as more spectrum is released across the world.

The full 5G Market Progress Assessment, end-2019 report can be purchased from OMDIA by contacting [email protected].

References:

https://www.realwire.com/releases/OMDIA-ranks-South-Korea-as-top-global-5G-market

https://www.omdia.com/resources/product-content/5g-market-progress-assessment-end2019-glb007-000395

South Korea 5G subscribers top 6 million at end of April 2020

Dell’Oro: Data Center Switch market declined 9% YoY; SD-WAN market increased at slower rate than in 2019

Market research firm Dell’Oro Group reported today that the worldwide Data Center Switch market recorded its first decline in nine years, dropping 9 percent year-over-year in the first quarter. 1Q 2020 revenue level was also the lowest in three years. The softness was broad-based across all major branded vendors, except Juniper Networks and white box vendors. Revenue from white box vendors was propelled mainly by strong demand from Google and Amazon.

“The COVID-19 pandemic has created some positive impact on the market as some customers pulled in orders in anticipation of supply shortage and elongated lead times,” said Sameh Boujelbene, Senior Director at Dell’Oro Group. “Yet this upside dynamic was more than offset by the pandemic’s more pronounced negative impact on customer demand as they paused purchases due to macro-economic uncertainties. Supply constraints were not major headwinds during the first quarter but expected to become more apparent in the next quarter,” added Boujelbene.

Additional highlights from the 1Q 2020 Ethernet Switch – Data Center Report:

- The revenue decline was broad-based across all regions but was less pronounced in North America.

- We expect revenue in the market to decline high single-digit in 2020, despite some pockets of strength from certain segments.

The Dell’Oro Group Ethernet Switch – Data Center Quarterly Report offers a detailed view of the market, including Ethernet switches for server access, server aggregation, and data center core. (Software is addressed separately.) The report contains in-depth market and vendor-level information on manufacturers’ revenue; ports shipped; average selling prices for both Modular and Fixed Managed and Unmanaged Ethernet Switches (1000 Mbps,10, 25, 40, 50, 100, 200, and 400 GE); and regional breakouts. To purchase these reports, please contact us by email at [email protected].

…………………………………………………………………………………………………………………………………………………

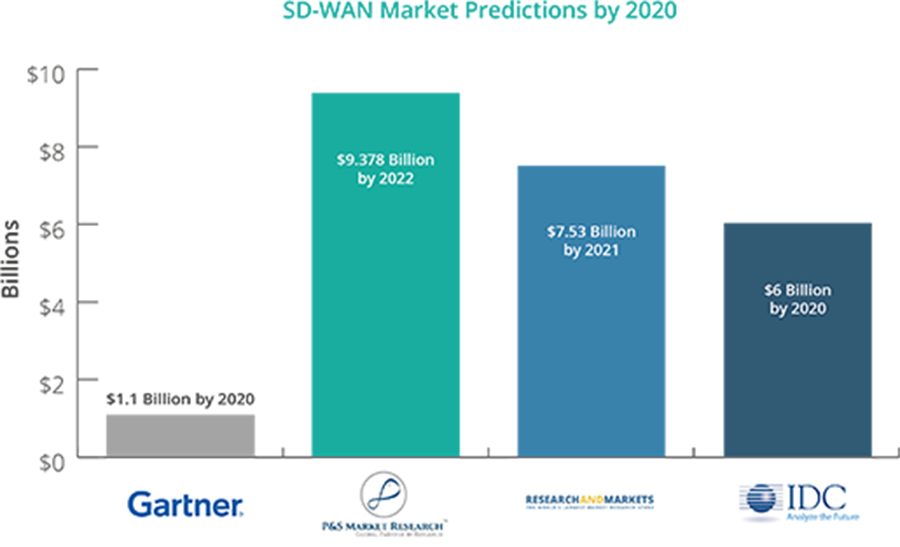

Separately, Dell’Oro Group reported that the market for software-defined (SD)-WAN equipment increased by 24% in the first quarter (year-to-year), which was significantly below the 64% growth seen in 2019. Citing supply chain issues created by the coronavirus pandemic, the market research firm’s Shin Umeda predicted the market will post double-digit growth in 2020 despite “macroeconomic uncertainty.”

- Supply chain disruptions accounted for the majority of the Service Provider (SP) Router and CES Switch market decline in 1Q 2020.

- The SP Router and CES market in China showed a modest decline in 1Q 2020, but upgrades for 5G infrastructure are expected to drive strong demand over the rest of 2020.

Rakuten Mobile, Inc. and NEC to jointly develop the containerized standalone (SA) 5G core network

Japanese upstart carrier Rakuten Mobile, Inc. and NEC Corporation today announced that they have reached an agreement to jointly develop the containerized standalone (SA) 5G core network (5GC) to be utilized in Rakuten Mobile’s fully virtualized cloud native 5G network.

Based on the agreement, Rakuten Mobile and NEC will jointly develop the containerized SA 5G mobile core to be made available on the Rakuten Communications Platform (RCP), Rakuten Mobile’s fully virtualized and containerized cloud-native mobile network platform. The two companies will collaborate to build a Japan-made, highly reliable 5GC, based on the 5GC software source code developed by NEC. Subsequent to the launch of its non-standalone (NSA) 5G service in 2020, Rakuten Mobile aims to provide its SA 5G service in Japan in 2021.

The containerized 5GC will also play a key role in the global expansion of RCP, a platform aimed at offering solutions and services for the deployment of virtualized networks at speed and low cost by telecom companies and enterprises around the world, tailored for their unique needs. The 5GC will be offered as an application on the RCP Marketplace, allowing customers to quickly and easily “click, purchase and deploy” a fully virtualized SA 5G core network solution.

…………………………………………………………………………………………………….

Editor’s Note: The two companies don’t state what spec they’re using for their container based SA 5G Core Network.

–Please see Tareq Amin’s Comment below.

The only standards work we know of related to SA 5G Core Network is in 3GPP (5GCN), but it’s based on a NFV enabled network cloud and a service based architecture, rather than containers.

We suggest that NEC contribute this spec to both 3GPP and ITU-T (for IMT 2020 non-radio aspects). However, neither ITU-R or ITU-T has any serious ongoing work related to the 5G Core Network at this point in time.

The 3GPP specified 5G core network covers both wire-line and wireless access. Key characteristics:

Control plane is separated from the data plane and implemented in a virtualized environment

Fully distributed network architecture with single level of hierarchy

GW to GW interface to support seamless mobility between 5G-GW

Traffic of the same flow can be delivered over multiple RITs

From the latest 3GPP Release 16 – TS.23501 5G Systems Architecture-V16.4.0 (2020-03):

The 5G System architecture is defined to support data connectivity and services enabling deployments to use techniques such as e.g. Network Function Virtualization and Software Defined Networking. The 5G System architecture shall leverage service-based interactions between Control Plane (CP) Network Functions where identified. Some key principles and concept are to:

– Separate the User Plane (UP) functions from the Control Plane (CP) functions, allowing independent scalability, evolution and flexible deployments e.g. centralized location or distributed (remote) location.

– Modularize the function design, e.g. to enable flexible and efficient network slicing.

– Wherever applicable, define procedures (i.e. the set of interactions between network functions) as services, so that their re-use is possible.

– Enable each Network Function and its Network Function Services to interact with other NF and its Network Function Services directly or indirectly via a Service Communication Proxy if required. The architecture does not preclude the use of another intermediate function to help route Control Plane messages (e.g. like a DRA).

– Minimize dependencies between the Access Network (AN) and the Core Network (CN). The architecture is defined with a converged core network with a common AN – CN interface which integrates different Access Types e.g. 3GPP access and non-3GPP access.

– Support a unified authentication framework.

– Support “stateless” NFs, where the “compute” resource is decoupled from the “storage” resource.

– Support capability exposure.

– Support concurrent access to local and centralized services. To support low latency services and access to local data networks, UP functions can be deployed close to the Access Network.

ITU-T SG13 is working on IMT 2020 non-radio aspects, but are heavily dependent on 3GPP documents to be liased in order to drive their future standards work in that area. Unfortunately that has not happened.

Please see Comment in box underneath this article for GSMA Feb 2020 document on SA 5G Core option 2 guidelines for implementation.

………………………………………………………………………………………………………………………………..

“We are very excited to collaborate with NEC on the development of our standalone 5G core network,” commented Tareq Amin, Representative Director, Executive Vice President and CTO of Rakuten Mobile. “Our partnership with NEC represents a joint collaboration to build an open, secure and highly scalable 4G and 5G cloud native converged core, that will also become a key feature of the highly competitive services we will offer to global customers through the Rakuten Communications Platform.”

“NEC is proud to be the 5GC development partner for Rakuten Mobile’s advanced, fully virtualized, cloud-native network. Following the BSS/OSS for the 4G network and 5G radio equipment that we have already begun offering, we look forward to providing a high-quality, highly reliable 5GC and contributing to Rakuten Mobile’s 5G services,” said Atsuo Kawamura, Executive Vice President and President of the Network Services Business Unit, NEC.

Through the joint development of the SA 5GC, Rakuten Mobile and NEC aim to drive innovation in global mobile technology and provide high quality 5G network technology to customers both in Japan and around the world.

Rakuten Mobile CTO Tareq Amin clarification comments; via edited email to this author:

NEC/Rakuten 5GC is 3GPP standardized software for network service and a de facto standard container basis infrastructure (“infrastructure agnostic”). It is a forward looking approach, but not proprietary.

1. 3GPP standardized software for network service:

NEC/Rakuten 5GC openness are realized by implementation of “Open Interface” defined in 3GPP specifications (TS 23.501, 502, 503 and related stage 3 specifications).

2. Containerization/Cloud native:

3GPP 5GC specification requires cloud native 5G core (5GC) architecture as the general concept (service based architecture). It should be distributed, stateless, and scalable. However, an explicit reference model is out of scope for the 3GPP specification. Therefore NEC 5GC cloud native architecture is based on above mentioned 3GPP concept as well as ETSI NFV treats “container” and “cloud native”, which NEC is also actively investigating to apply its product.

3. Reference To Open RAN in the press release:

This has no relationship to 5G Core, but only an indication that our Radio Access Network (RAN) architecture is O-RAN Compliant.

……………………………………………………………………………………………………………………………………….

Press Release:

Forward Reference:

Rakuten Communications Platform (RCP) defacto standard for 5G core and OpenRAN?

About Rakuten Mobile

Rakuten Mobile, Inc. is a Rakuten Group company responsible for mobile communications, including mobile network operator (MNO) and mobile virtual network operator (MVNO) businesses, as well as ICT and energy. Through continuous innovation and the deployment of advanced technology, Rakuten Mobile aims to redefine expectations in the mobile communications industry in order to provide appealing and convenient services that respond to diverse customer needs.

About NEC Corporation

NEC Corporation has established itself as a leader in the integration of IT and network technologies while promoting the brand statement of “Orchestrating a brighter world.” NEC enables businesses and communities to adapt to rapid changes taking place in both society and the market as it provides for the social values of safety, security, fairness and efficiency to promote a more sustainable world where everyone has the chance to reach their full potential.

more information, visit NEC at http://www.nec.com.

Contacts:

Rakuten, Inc. Corporate Communications Department

[email protected]

NEC Corporation Corporate Communications Division

[email protected]

South Korea 5G subscribers top 6 million at end of April 2020

More than 6 million South Koreans were subscribed to 5G mobile networks as of April, a year after the country adopted the service, according to government data reported Monday, June 1st. The number of 5G users in the nation reached 6.34 million as of the end of April, up 7.8 percent from a month earlier, according to the data compiled by the Ministry of Science and ICT.

South Korea’s three carriers — SK Telecom Co., KT Corp. and LG Uplus Corp. — rolled out the commercial 5G network last April and have aggressively promoted their new service for premium smartphones.

SK Telecom’s 5G customers accounted for 45 percent as of April, trailed by KT with 30.3 percent and LG Uplus with 24.7 percent, the ministry said.

The number of mobile subscribers between 2G and 5G came to 69.35 million as of the end of April, the ministry said.

In May, South Korean operator KT added 360,000 5G subscribers in the first quarter of the year, the telco said in its earnings statement. KT, which launched commercial 5G services in April 2019, ended Q1 with a total of 1.78 million 5G customers.

“Since the launch of KT’s 5G services, we are currently maintaining a much higher market share in 5G compared to the market share we have for the LTE handsets,” Kyung-Keun Yoon, KT’s CFO, said during a conference call with investors.

It’s important to note that Korea has its own version of IMT 2020 RIT/SRIT being progressed by ITU-R WP 5D. The country’s IMT 2020 submission is based on 3GPP Release 15 “5G NR.” It is not clear if there are any technical differences between Korea and 3GPP IMT 2020 submissions and if so, what they are.

References:

https://en.yna.co.kr/view/AEN20200601006000320