LightCounting: Optical components market to hit $20 billion by 2027+ Ethernet Switch ASIC Market Booms

|

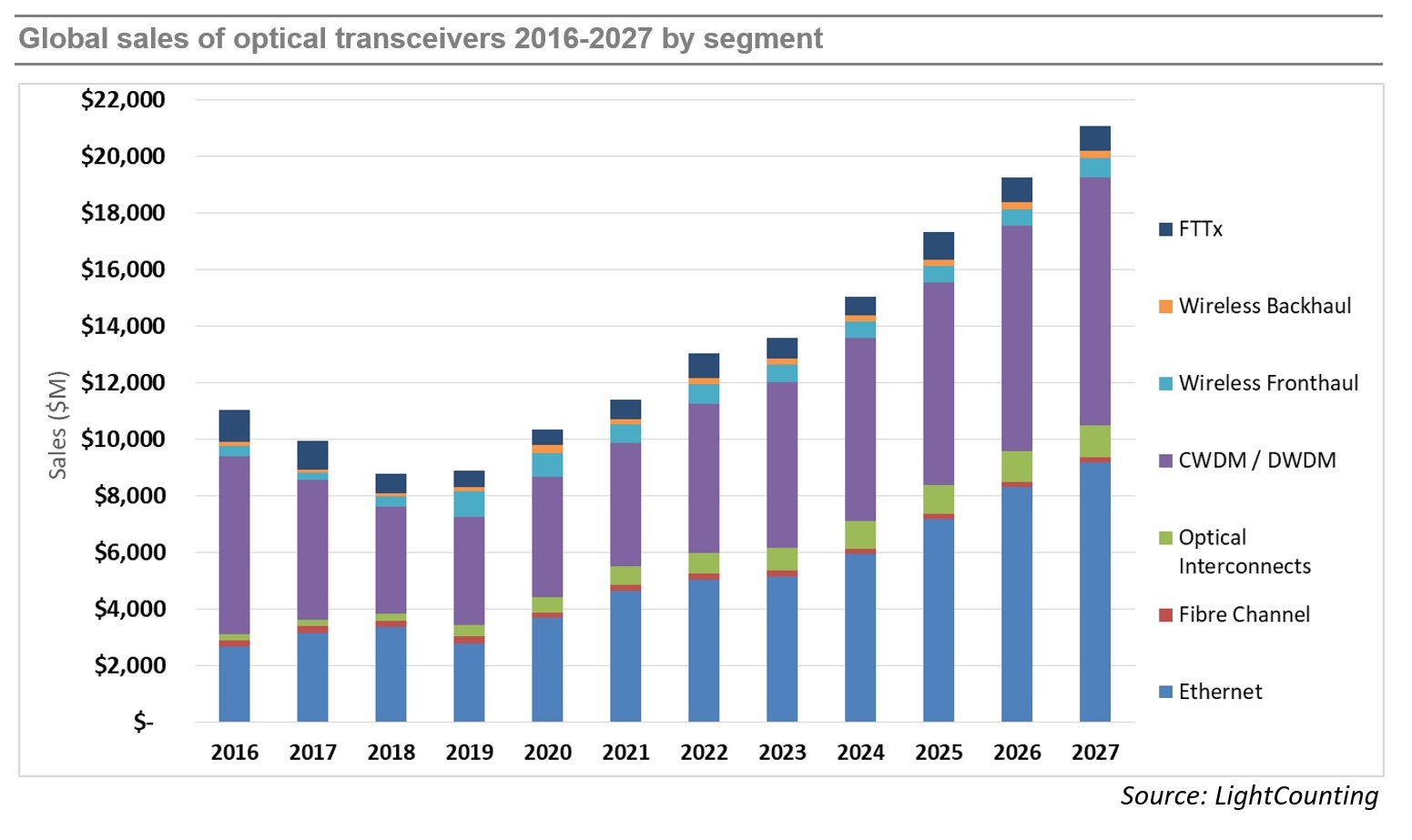

The optical communications industry entered 2020 with very strong momentum. Demand for DWDM, Ethernet, and wireless fronthaul connectivity surged at the end of 2019, and major shifts to work-at-home and school-at-home in 2020 and 2021 due to the COVID-19 pandemic created even stronger demand for faster, more ubiquitous, higher reliability networks.

While supply chain disruptions continued, the industry was able to largely overcome them, and the market for optical components and modules saw strong growth in 2020 and 2021, as shown in the figure below. Light Counting believes the transceiver market is on track for another year of strong (14%) revenue growth in 2022, after increasing by 10% in 2021, and 17% in 2020. However, market growth is projected to slow to 4% in 2023, prior to recovering in 2024-2025.

Demand for optics is strong across all market segments, but continuing bottlenecks in the global supply chain negatively impacted sales of 400G DR4 and 100G DR1+ transceivers to Amazon in the first 9 month of 2022. Meta increased its deployments of optics sharply this year, but its latest forecast for 2023 has been reduced substantially. We suspect that Amazon and other cloud companies may moderate their investments in 2023, if the current economic slowdown continues to negatively impact their advertising, streaming, and retail businesses.

|

|

|

LightCounting’s latest forecast projects a 11% CAGR in 2022-2027, not very different from the 13% CAGR in the forecast published in October 2021. Strong sales of DWDM and Ethernet optics accounted for most of the market growth in 2021 and these segments are projected to lead the growth in 2022-2027. Sales of optical interconnects, mostly Active Optical Cables (AOCs), will also increase at double digit rates over the next 5 years. PON sales for FTTx networks will remain steady, as the China market ends its 10G cycle and North America and Europe ramp up 10G PON deployments, driven by government funding programs. 25G and 50G PON provide new growth later in the forecast period. Wireless fronthaul is one area of weakness, since 5G network deployments in China are reaching completion. This segment will return to growth in 2026-2027 with the onset of 6G deployments (which we don’t think will happen till many years later).

…………………………………………………………………………………………………………………………………………………………….

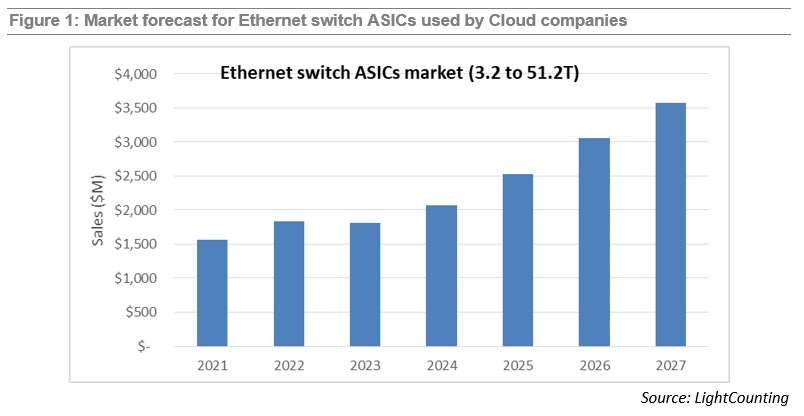

Demand for Ethernet switches from Cloud companies created a new market segment for very high bandwidth switches and switch ASICs. It also transformed the industry supply chain as Cloud companies started using internally designed Ethernet switches and opening these “white box” designs to a broader community. LightCounting’s report on Ethernet switch ASICs was first published in April 2022, and today the first update has been released. The report covers the most interesting segment of the switching ASIC market – high bandwidth (3.2T and above), low latency chips deployed in Cloud datacenters. The report offers brief profiles of the leading suppliers of merchant switch ASIC and system integrators, offering products to Cloud companies, and includes a forecast for sales of 3.2 to 51.2T switch ASICs. The updated report now includes 3.2T/6.4T chips in addition to the higher speed products. This change added close to $1 billion to the total market size compared to our April estimate. The forecast includes chips sold in the merchant market as well as chips used by Cisco in their own equipment (captive market). A lower forecast for 2023 compared to our April 2022 edition reflects reduced guidance by the leading Cloud companies for datacenter upgrades planned for next year. Despite a reduced forecast, the overall market is expected to roughly double in size from $1.8 billion in 2023 to $3.6 billion in 2027.

References:

|

5G FWA launched by South Africa’s Telkom, rather than 5G Mobile

South African telecommunications operator Telkom [1.] has launched its 5G high speed Internet network using technology from China’s Huawei Technologies. The partially state-owned operator said it will initially use the network to provide fixed wireless Internet via 5G rather than focusing on mobile 5G.

“At launch Telkom will primarily focus on providing super fast 5G fixed wireless access solutions, as the demand for mobile 5G increases, we will supplement this with suitable mobile propositions,” Telkom Consumer and Business CEO Lunga Siyo explained.

Note 1. Telkom is South Africa’s third largest network operator with 17.6 million users in the third quarter of 2022, according to statistics from market research company Omdia. Vodacom remains South Africa’s largest operator with over 52 million users while MTN has about 36 million customers.

……………………………………………………………………………………………………………………………………………

Telkom joins its competitors Vodacom, MTN and Rain in the quest to provide high speed Internet in South Africa. Data-only network Rain rolled out its 5G services in 2019 and Vodacom and MTN followed with commercial launches in 2020.

Telkom said it will use its 125 5G base stations located in the provinces of Gauteng, KwaZulu-Natal, Eastern Cape and Western Cape at launch.

The telco’s managing executive Lebo Masalesa said the company is rolling out 5G nationally and in smaller towns, with the intention to build network where it is needed.

“Once there is a greater proliferation of 5G capable mobile devices on Telkom’s network, it will launch 5G services for mobile users,” he added.

“5G stands head and shoulders above 4G and LTE through faster and more reliable connection it provides, however it was critical for us to make sure that our existing 4G ecosystem remains strong whilst introducing 5G into the market,” continued Siyo.

The South African network operator invested 2.1 billion South African rand (US$116 million) for 42MHz of frequencies in the spectrum auction by the Independent Communications Authority of South Africa (ICASA), supporting its network upgrades.

“The COVID pandemic has driven significant lifestyle changes for South Africans, due to work from home or school from home, online shopping and an ‘always on’ kind of culture,” said Fortune Wang, Carrier Business Director for Huawei South Africa.

“At launch Telkom will primarily focus on providing super fast 5G fixed wireless access solutions, as the demand for mobile 5G increases, we will supplement this with suitable mobile propositions,” said Lunga Siyo, chief executive officer of Telkom Consumer and Business.

Shunned in the global north due to security concerns, which Huawei has denied, the Chinese company dominates in Africa as a supplier of equipment to many telecoms operators.

Telkom SA’s commercial 5G rollout comes on the back of Safaricom in Kenya making a similar announcement last week about a focus on retail and enterprise customers for 5G rather than mobile, as it launched its 5G Internet service following trials that started in March 2021.

Furthermore, the commercial 5G launch comes after MTN walked away from talks to acquire Telkom. The talks between the two companies stalled when the data-only network operator Rain offered its network up to Telkom SA to acquire, in a move that stood in the way of MTN’s plans to buy Telkom.

References:

https://www.euronews.com/next/2022/10/27/telkom-sa-huawei-tech-5g

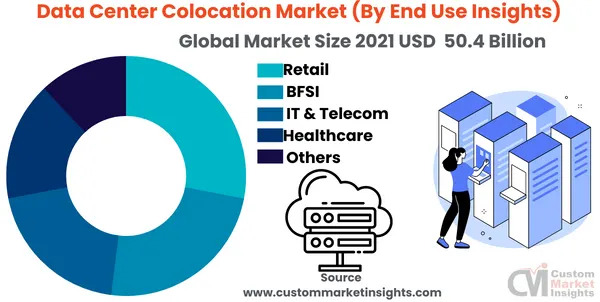

Global Data Center Colocation Market Size forecast = $131.8 Billion by 2030 at a 14.2% CAGR

According to a market research study published by Custom Market Insights, the Global Data Center Colocation Market size and share revenue was valued at approximately USD $50.4 Billion in 2021 and is expected to reach USD $57.2 billion in 2022 and is expected to reach around USD $131.8 Billion by 2030, at a CAGR of 14.2% between 2022 and 2030.

The key market players listed in the report with their sales, revenues and strategies are China Telecom Corp. Ltd., CoreSite Realty Corp., CyrusOne Inc., NaviSite, NTT Communications Corp., Cyxtera Technologies Inc., Digital Realty Trust Inc., Equinix Inc., Global Switch, Telehouse, and others.

“According to the latest research study, the demand for global Data Center Colocation Market size & share was valued at approximately USD 50.4 Billion in 2021 and is expected to reach USD 57.2 billion in 2022 and is expected to reach a value of around USD 131.8 Billion by 2030, at a compound annual growth rate (CAGR) of about 14.2% during the forecast period 2022 to 2030.”

Data center colocation market offers a comprehensive and deep evaluation of the market stature. Also, the market report estimates the market size, revenue, price, market share, market forecast, growth rate, and competitive analysis.

Data center colocation is when a service provider rents out vast amounts of floor space, internet bandwidth, and network from an existing data center to establish its own data center, store massive amounts of data, and oversee the server operations of big businesses. It enables data center colocation by sharing the existing infrastructure of data center resources.

As a result of the Covid-19 outbreak, colocation is becoming an essential component of staying connected, collaborating, and moving forward cost-effectively and safely. Healthcare organizations analyze patient outcomes using data and anticipate the spread of diseases using artificial intelligence. Robust network connectivity at Telehouse colocation centers in New York enables them to provide a range of commercial solutions.

Over the projected period, it is predicted that the fast expansion of structured and unstructured data and the rising demand for cloud computing will drive the growth of the global data center colocation market. Another factor anticipated to accelerate the development of colocation data centers is the rising capital expense associated with owning and maintaining sizable computing facilities.

A trend that is anticipated to continue during the projected period is that predictable prices, high dependability, simple scalability, and overall reduced costs are some of the primary reasons impacting colocation demand. High-capacity networks are becoming increasingly crucial as edge computing applications take off. Multi-locational hybrid data architectures have developed due to network latency challenges and the need for instantaneous real-time insights.

Data transmission between data centers or private exchange points has therefore become crucial. Additionally, as more companies move their operations to the cloud, more bandwidth is needed to support quicker data processing and smoother data transfer. The growth of immersive technologies like augmented reality, virtual reality, and artificial intelligence (AI), as well as 5G technology, has further contributed to the requirement for providing larger bandwidths for data transfer across organizations.

The continuous use of several disruptive technologies, including cloud computing, IoT, autonomous cars, and sophisticated robotics, is another factor driving the growing demand for colocation in data centers. In addition, lower latency has become increasingly in the market due to the ongoing development of these technologies and the ensuing adoption of intelligent devices. As a result, colocation gives cloud service providers a chance to relocate their data center facilities close to the consumers, resulting in high bandwidth and low latency in data transfer.

Key questions answered in this report:

- What is the size of the Data Center Colocation market and what is its expected growth rate?

- What are the primary driving factors that push the Data Center Colocation market forward?

- What are the Data Center Colocation Industry’s top companies?

- What are the different categories that the Data Center Colocation Market caters to?

- What will be the fastest-growing segment or region?

- In the value chain, what role do essential players play?

- What is the procedure for getting a free copy of the Data Center Colocation market sample report and company profiles?

Click Here to Access a Free Sample Report of the Global Data Center Colocation Market @ https://www.custommarketinsights.com/report/data-center-colocation-market/

Segmental Overview

The data center colocation market is segmented into type, enterprise size, and end-use insights. According to the class, the retail colocation category is expected to increase quickly. Numerous advantages this kind offers, including managed service, which results in cheaper costs for data center maintenance, high data security, and others, are credited with the segment’s rise.

The global market is divided into small and minimum-scale enterprises and large enterprises, depending on the enterprise size. However, large-scale organizations had the majority of the market share for data center colocation and are anticipated to keep expanding over the projected period. Heavy investment by big-size organizations in data centers is credited with this increase. Additionally, the worldwide market for data center colocation is being driven by significant enterprises’ increasing need for substantial data storage.

The market is divided into IT & Telecom, BFSI, Healthcare, and others. The IT and telecom industries had the most significant proportion in 2021, followed by the banking, financial, and insurance sectors. In the projection term, the CAGR for the IT & Telecom category is expected to be high. In addition, due to ongoing patient data monitoring and storage, which have greatly expanded since the COVID-19 pandemic in 2021, the healthcare subsegment also offers significant development potential throughout the projection period.

North America held the most significant market share in the data center colocation market. This is because several necessary cloud service providers are well-represented in the area, and SMEs also set up colocation data centers there. Additionally, rising e-commerce sales in the United States foster regional market expansion. To determine client buying habits and product requests based on several categories, such as area, gender, and age group, retailers are investing extensively in their IT infrastructure to keep customer data.

……………………………………………………………………………………………………………………………………………………..

Another forecast is even more bullish, predicting a Global Data Center Colocation market size of $202.71 Billion by 2030 as per this chart:

References:

https://www.yahoo.com/now/latest-global-data-center-colocation-023000887.html

Canalysis & Counterpoint: Global Smartphone shipments plunge 9% YoY in 3Q-2022

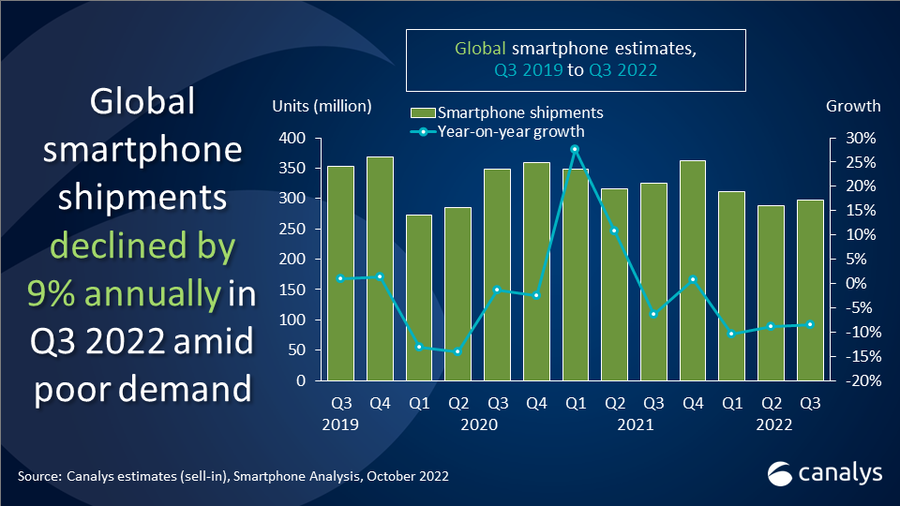

Canalys smartphone analysis indicates weak demand in 3Q-2022 caused worldwide smartphone shipments to decline by 9% year-on-year to 297.8 million units. Samsung defended its first place in the market despite an 8% decline, shipping 64.1 million units. Apple, the only leading vendor to increase year-on-year driven by robust demand, grew 8% and shipped 53.0 million units. Following two quarters of double-digit declines, Xiaomi leveraged its global scale to find opportunities helping it strengthen its position to only decline 8%, shipping 40.5 million units. OPPO and Vivo took fourth and fifth place despite having over 20% declines, shipping 28.5 million and 27.4 million units respectively in Q3 2022.

“Performance of the high-end segment was the only highlight this quarter,” said Canalys Research Analyst Runar Bjørhovde. “Apple reached its highest Q3 market share yet, driven by both the iPhone 13 and newly launched iPhone 14 series. The popularity of the iPhone 14 Pro and Pro Max, in particular, will contribute to a higher ASP and stable revenue for Apple. On the Android side, Samsung refreshed its foldable portfolio and increased its marketing initiatives significantly to generate interest and demand for its new flagships. Mid-to-low-end demand has been hit making it challenging for vendors to navigate in a competitive segment. Xiaomi managed to leverage its global scale with a refreshed product line to offset declines in its home market. OPPO and vivo are still significantly impacted by the drop in the China market but have both shown small signs of recovery.”

“Europe and Asia Pacific outperformed the rest of the world in Q3,” said Canalys Analyst Sanyam Chaurasia. “Europe avoided a significant drop helped by a spike in shipments to Russia. Here, Chinese vendors leveraged short-term opportunities to stock up the channel in a market that has been undersupplied during previous quarters. APAC had a huge variation between different markets, but sequentially improving demand in India, Indonesia and the Philippines helped the region stabilize its performance. Carrier dominated markets such as North America and Latin America presented increasingly cautious sentiments on managing inventory before heading into big holiday seasons, contrasting a much more optimistic view in Q3 last year.”

“Moving into Q4, ongoing global disruptions are hampering the performance of entire ecosystem portfolios for vendors,” said Canalys Analyst Toby Zhu. “The upstream supply chain is entering a long winter sooner than expected where OEMs’ order targets are slashed heavily. Also, slow inventory turnover and poor economic figures have affected the channel’s confidence, falling back to major brands with iconic devices to generate traffic for the most important revenue quarter. Vendors are entering Q4 with cautious strategies to handle the persisting difficulties. Managing the gloomiest Q4 outlook in over a decade will show which vendors are well-positioned for the long-term.”

|

Worldwide smartphone shipments and annual growth Canalys Smartphone Market Pulse: Q3 2022 |

|||||||

|

Vendor |

Q3 2022 shipments (million) |

Q3 2022 |

Q3 2021 |

Q3 2021 |

Annual |

||

|

Samsung |

64.1 |

22% |

69.4 |

22% |

-8% |

||

|

Apple |

53.0 |

18% |

49.2 |

16% |

8% |

||

|

Xiaomi |

40.5 |

14% |

44.0 |

14% |

-8% |

||

|

OPPO |

28.5 |

10% |

36.7 |

12% |

-22% |

||

|

Vivo |

27.4 |

9% |

34.2 |

11% |

-20% |

||

|

Others |

84.3 |

27% |

92.1 |

25% |

-6% |

||

|

Total |

297.8 |

100% |

325.6 |

100% |

-9% |

||

|

Note: percentages may not add up to 100% due to rounding |

|||||||

Source: Canalys

…………………………………………………………………………………………………………………………………

Counterpoint: Global Smartphone Market at Lowest Q3 Level Since 2014

- The global smartphone market declined by 12% YoY even as it grew by 2% QoQ to reach 301 million units in Q3 2022.

- While quarterly growth in Apple and Samsung pushed the global smartphone market above 300 million units, a level it failed to reach last quarter, political and economic instability drove negative consumer sentiment.

- Apple was the only top-five smartphone brand to grow YoY, with shipments increasing 2% YoY, growing market share by two percentage points to 16%.

- Samsung’s shipments declined by 8% YoY but grew 5% QoQ to 64 million.

- Xiaomi, OPPO* and vivo, recovered slightly after receiving heavy beatings due to lockdowns in China in Q2, and as they captured more of the market ceded by Apple and Samsung’s exit from Russia.

Senior Analyst Harmeet Singh Walia said, “Most major vendors continued experiencing annual shipment declines in the third quarter of 2022. Russia’s escalating war in Ukraine, ongoing China-US political distrust and tensions, growing inflationary pressures across regions, a growing fear of recession, and weakening national currencies all caused a further dent in consumer sentiment, hitting already weakened demand. This is also adding to a slow but sustained lengthening of smartphone replacement cycles with smartphones becoming more durable and as technology advancement slows. This is accompanying, and to a smaller degree advancing, a fall in the shipments of mid- and lower-end smartphones, even as the premium segment weathers the economic storm better. Consequently, and thanks to an earlier launch of the latest iPhone series this year, Apple emerged as the only top-five smartphone vendor to manage annual shipment growth in the quarter.”

While Samsung grew QoQ in Q3 2022 thanks to record presales of its premium fold and flip smartphones, compared with the same quarter last year, however, its shipments fell by 8% YoY. This is primarily down to dampening consumer sentiment in several of its key markets. This also affected top Chinese brands, whose shipments remained low compared with last year as they were getting rid of excess inventory and at the same time managing a slowdown in the home market, China. However, they were able to capitalise on Apple and Samsung’s exit from the Russian market, in which their share increased substantially.

Associate Director Jan Stryjak noted, “With the full force of the latest iPhone launch being felt in Q4, we expect further quarterly improvement in the coming quarter, although central banks’ attempts to control inflation will further reduce consumer demand. The channel inventory is still higher, and the OEMs will focus on getting rid of excess inventory in Q4 as well. Hence, shipments are unlikely to reach last year’s levels, let alone pre-pandemic Q4 levels of over 400 million units. Looking further ahead into 2023, we expect sluggish demand with lengthening replacement rates, especially in the first half of the year.”

*OPPO includes OnePlus from Q3 2021

References:

Clearwave Fiber Expands Fiber Buildout in Savannah, Hinesville and Richmond Hill, GA

Clearwave Fiber [1.] continues its construction of a state-of-the art, all-Fiber Internet network in the “Coastal Empire.” This latest expansion for the Savannah-based operation marks a continuation of almost 6,000 route miles of Fiber in the Southeast and Midwest. The company’s goal is to bring the most advanced and fastest Internet available to more than 500,000 homes and businesses across the United States by the end of 2026.

Note 1. Clearwave Fiber was formed in January of 2022 as a rebranding of Hargray Fiber, which has been serving the Southeast for 70+ years. Senior leadership and operations management have a long history with Hargray and now lead Clearwave Fiber during this rapid expansion.

![]()

………………………………………………………………………………………………………………………………………………………..

“Clearwave Fiber is excited to contribute to the continual growth in Southeast Georgia and provide such a crucial resource to residents and commercial operations,” said Clearwave Fiber General Manager John Robertson. “We’re committed to providing communities with the high-speed connectivity that is essential for families, businesses and local economies.”

“We’re ingrained in the fabric of Savannah and its surrounding communities,” said Clearwave Fiber Chief Operating Officer Gwynne Lastinger. “Our sales and technical support staff live and work in the Coastal Empire and we continue to add to our team of more than 500 throughout the Southeast and Midwest.”

With gigabit download and upload speeds, Clearwave Fiber will bring 10 times more speed to consumer doorsteps at a time when fast, reliable Internet is becoming increasingly critical to modern households and businesses. Remote work, streaming, gaming, smart home technology and multiple device connectivity all require robust, reliable connections. Clearwave Fiber is committed to providing hassle-free, high-quality Fiber data connection to every location of its growing footprint.

“We’re seeing an increase in households where multiple online activities are occurring at the same time. Many Internet connections aren’t up to the task of keeping it all running at top speeds,” said Robertson. “Clearwave Fiber solves the problem of the bandwidth issues that happen when everyone in the house is connected. We also have solutions for businesses that keep them operating on a fast, reliable network.”

For many consumers, Internet touches every facet of daily life. Remote work, telehealth, and virtual learning all require robust, reliable connections. A 2022 study by Deloitte indicated that 45 percent of surveyed households include one or more remote workers, and 23 percent include at least one or more household member attending school from home. Additionally, 49 percent of U.S. adults had virtual medical appointments in the past year.

In addition, the Deloitte report noted that the average U.S. household now utilizes a total of 22 connected devices, including laptops, tablets, smartphones, smart TVs, game consoles, home concierge systems like Amazon Echo and Google Nest, fitness trackers, camera and security systems, and smart home devices such as connected exercise machines and thermostats.

Supporting this burgeoning ecosystem of household devices can challenge companies serving customers over DSL or cable systems. “Older copper wire and coaxial networks worked just fine for the technologies they were built for. Copper lines are great for telephone calls and coax worked well for cable TV, but those networks struggle to deliver the kind of bandwidth possible with fiber,” noted Lastinger. “Fiber optic technology is the future. Fiber networks are more durable, more consistent, and they move data at the speed of light. Best of all, our network easily keeps pace with technology innovations, exponentially increasing demands for bandwidth, and evolving customer needs. The options are almost limitless.”

Fiber networks are currently being installed on Wilmington and Whitemarsh Islands, Windsor Forest, Hinesville, Rincon, Pooler and Richmond Hill. Clearwave Fiber is scheduled to complete these projects by the end of November and will continue working in other areas in the region into 2023 and beyond.

For more information, visit ClearwaveFiber.com

References:

Synergy: Q3 Cloud Spending Up Over $11 Billion YoY; Google Cloud gained market share in 3Q-2022

Synergy Research estimates the cloud infrastructure market at $57B in Q3-2022. That was up by well over $11 billion from the third quarter of last year despite two fierce headwinds – historically strong U.S. dollar and a severely restricted Chinese market. The incremental spending represents year-on-year growth of 24%. If exchange rates had remained constant over the last year, the growth rate would have been over 30%. As the market continues on a strong growth trajectory,

Google is alone among the hyper-scaler giants to be gaining market share. Google Cloud increased its market share in Q3 compared to the prior quarter, while Amazon and Microsoft market shares remained relatively unchanged. Compared to a year ago all three have increased their market share by at least a percentage point. Amazon, Microsoft and Google combined had a 66% share of the worldwide market in the quarter, up from 61% a year ago. In aggregate all other cloud providers have tripled their revenues since late 2017, though their collective market share has plunged from 50% to 34% as their growth rates remain far below the market leaders.

Synergy estimates that quarterly cloud infrastructure service revenues (including IaaS, PaaS and hosted private cloud services) were $57.5 billion, with trailing twelve-month revenues reaching $217 billion. Public IaaS and PaaS services account for the bulk of the market and those grew by 26% in Q3. The dominance of the major cloud providers is even more pronounced in public cloud, where the top three control 72% of the market. Geographically, the cloud market continues to grow strongly in all regions of the world.

“It is a strong testament to the benefits of cloud computing that despite two major obstacles to growth the worldwide market still expanded by 24% from last year. Had exchange rates remained stable and had the Chinese market remained on a more normal path then the growth rate percentage would have been well into the thirties,” said John Dinsdale, a Chief Analyst at Synergy Research Group. “The three leading cloud providers all report their financials in US dollars so their growth rates are all beaten down by the historic strength of their home currency. Despite that all three have increased their share of a rapidly growing market over the last year, which is a strong testament to their strategies and performance. Beyond these three, all other cloud providers in aggregate have been losing around three percentage points of market share per year but are still seeing strong double-digit revenue growth. The key for these companies is to focus on specific portions of the market where they can outperform the big three.”

Synergy provides quarterly market tracking and segmentation data on IT and Cloud related markets, including vendor revenues by segment and by region. Market shares and forecasts are provided via Synergy’s uniquely designed online database SIA™, which enables easy access to complex data sets. Synergy’s Competitive Matrix™ and CustomView™ take this research capability one step further, enabling our clients to receive on-going quantitative market research that matches their internal, executive view of the market segments they compete in.

References:

Synergy Research: public cloud service and infrastructure market hit $126B in 1Q-2022

Cloud Computing Giants Growth Slows; Recession Looms, Layoffs Begin

Highlights of ITU-R report: IMT TERRESTRIAL BROADBAND REMOTE COVERAGE

Introduction:

Almost three years in the making (see References below), this ITU-R report on IMT TERRESTRIAL BROADBAND REMOTE COVERAGE provides details on scenarios associated with the provisioning of enhanced mobile broadband services in sparsely populated and underserved remote areas with a discussion on enhancements of user and network equipment. Mobile broadband access in rural and remote areas can be done by various existing user equipment and additionally, broadband can be delivered also by FWA (Fixed Wireless Access) type of consumer premises equipment (CPEs). It offers technical solutions for certain deployment scenarios prevailing in developing countries and is meant to be used in accordance with the existing regulations in those countries.

In many countries, national policymakers have recognized the necessity to introduce polices and solutions to ensure connectivity in underserved and remote areas.

Further challenges that limit the reach of mobile broadband in sparsely populated areas are, for example, infrastructure requirements, backhaul connectivity, operation and maintenance, sparse distribution of population and so on. However, some of the remote areas have industrial plants, excavation units and mining with temporary human occupancy or shelters, which would benefit from broadband connectivity.

Remote coverage might in the future be driven by the need for national security and public safety connectivity, intelligent traffic systems, internet of things, industry automation and end users need for home and commercial broadband services as an alternative to fiber connections. In order to fulfil the needs of remote coverage, it is important to identify viable solutions for mobile and fixed wireless broadband services.

Solutions that support remote sparsely populated areas providing high data rate coverage:

Possible technical solutions to achieve both extended coverage as well as high capacity in remote areas could be to use dual frequency bands at the same time, one lower band for the uplink (UL) and one higher band for the downlink (DL), in aggregated configurations.

Combining spectrum bands in the mid-band range (1-6 GHz) and the low-band range (below 1 GHz) on an existing grid can provide extended capacity compared to a network only using the low-band range.

An alternative technical solution to provide extended coverage in a remote area using existing or reduced number of terrestrial base station (BS) sites requires careful selection of proper locations and technical characteristics compared to configurations of suburban networks. Realizing such extended network configuration for coverage, several considerations need to be taken into account, both at a BS site and at customer premises. Considerations of accommodating BSs on high towers

in sparsely populated areas could be further studied1. Performance limitations usually arise in the uplink, arising from the handset designs : higher noise figure and, (due to regulation) limited transmission power of 23 dBm. Such large cell designs therefore typically rely on the use of external customer premises equipment (CPE) with large gain antennas, and high processing and computation power and stable power supply.

In order to extend broadband services to remote areas, IMT systems can benefit by employing high gain antennas.. One proposed solution is to use a few high-gain (up to 29.5 dBi), narrow beam x-pole antennas on a strategically placed high ground tower, where power and backhaul exist. Each of the very high gain antennas (VEGA) can cover a 15 to 35 km range, depending on deployment parameters like frequency, antenna height, ground surface and vegetation. See also in ITU-D 2021 final Report ‘Telecommunications/ICTs for rural and remote areas). The directive antennas improve the quality of service by increasing the signal-to-noise ratio (SNR) and Eb/N0 of the downlink (DL) and uplink (UL) signals.

Note 1. Such opportunities rest with traditionally high tower used for analogue or digital television with an average inter-site distance (ISD) of the order of 60 km to 80 km designed to provide blanket coverage of national terrestrial television services.

…………………………………………………………………………………………………………………………………………………………………….

Such very high gain multi-beam antennas provide gain, wider combined beamwidth, as well as broadband with a three-fold capacity, wherever needed. One tower implementing several high-gain beam-antennas, each providing high quality service to its dedicated target area, saves the necessity of additional building, maintaining (and guarding) several towers, each with a full BS and microwave backhaul or a fiber link. For these reasons, these antennas operate in remote sites, to cover those distant underserved communities at a shorter time.

With potential enhancements of base station (BS), user equipment (UE), and customer premises broadband configurations, it is deemed feasible to deploy a standalone network in the bands identified for IMT within the in 1-6 GHz range (see revision 6. of Recommendation ITU-R M.1036 -not yet completed/agreed) providing high capacity and coverage over tens of kilometres in remote sites. This could potentially be a promising solution for bringing IMT broadband (e.g., IMT‑2020/5G) in remote sites.

Aggregation of carriers from existing 4G LTE in low-band with 5G New Radio (NR) in the bands identified for IMT within the mid-range (~1-6 GHz) can provide such extended coverage along with capacity enhancement.

Generally, at a BS site, the antenna height, the radio frequency output power and antenna gain impact the coverage and capacity performance. Effective performance solutions are also represented by a high level of antenna sectorization, high antenna beamforming gain, and the use of Multiple Input Multiple Output (MIMO) antennas, as well as the use of carrier-aggregation. Furthermore, additional spectrum bands and bandwidth, and usage of redundant signalling protocol will improve performance.

Extending cell-coverage is limited by the uplink performance. Enhancing UE transmission capabilities is key to enabling extended coverage along with the Downlink coverage. For a fixed wireless broadband deployment in a “wireless fibre” configuration, using an outdoor directional antenna mounted line-of-sight (LOS) to the BS antenna site extends the coverage range significantly by avoiding building penetration losses. Conventional, mobile devices are UEs with power class of maximum 23 dBm transmit power. At higher carrier frequencies in the mid-band (between 1-6 GHz), a standalone network will be limited by uplink coverage than the downlink when deployed for extended coverage in remote areas. Hence, it is important to provide adequate extended coverage in the UL direction for the users located at the cell edge along with DL enhancements by using the dual band carriers in the deployment.

It is assumed that conventional IMT antenna arrangements are used for the UL system. For the DL, IMT-2020/5G bands identified for IMT within the in 1-6 GHz range, an antenna array is assumed to have 64 dual-polarized antenna elements installed on very high television towers. The considered ISD is regarded to be representative for a conventional 2G network grid. For extended coverage, adding a new band from bands identified for IMT within the 1-6 GHz range for mobile and fixed wireless broadband connectivity, networks can clearly deliver on the promise to increase on the coverage requirements for IMT-2020/5G services, but only adequately in the DL direction. This additional band also helps distribute the UL traffic through the 4G low-band at the cell-edge.

With dual bands, a very high gain antenna covering all lower bands as well as bands in 1-6 GHz enables easy implementation of the carrier aggregation, as well as strong DL on the higher bands (and good UL using the lower bands). The solutions employing a higher BS or UE power or other parameters/values different than typical deployments, should be used in accordance with the existing regulations of those countries.

Figure 1. Remote Coverage using High Gain Multi Beam Antenna

References:

ITU-R Report: Terrestrial IMT for remote sparsely populated areas providing high data rate coverage

Telecom Infra Project introduces Open FAN to promote multi-vendor interoperability

The Telecom Infra Project (TIP) has announced a new initiative for “open fixed access networks (FAN)” at the FYUZ conference in in Madrid, Spain. The Open FAN initiative is being led by Telefónica, Telecom Italia, and Vodafone. As in the mobile radio access network, the goal is to ensure products from competing vendors can be combined in the same fixed access network. That is the essence of true interoperability.

The work will focus on improving interoperability and diversity in the access network, accelerating innovation and boosting capacity in the last mile through the transition from GPON to XGS-PON. Specifically, Open FAN is targeting the link between optical line terminals (OLTs) and optical network terminals (ONTs), the boxes that sit at either end of a fiber connection. Integration with SDN controllers, the traffic cops of the network, is another priority. Open FAN has just become the latest TIP sub-group, part of the fixed access project group.

……………………………………………………………………………………………………………………………………………………….

TIPs Fixed Broadband Project Group is developing a new generation of open and disaggregated technologies that help operators increase the availability of fast and reliable broadband services across the world. The goal of the TIP fixed access sub-group is to build access networks capable of delivering high speed connectivity over the last mile. The primary objective for this group is to achieve a high degree of interoperability in the access domain, including:

- East-west interworking and integration between network elements

- Northbound integrations to OSS and network management systems

……………………………………………………………………………………………………………………………………………………….

Participants are currently drawing up technical requirements for a so-called “pizza box” OLT that can be delivered to the local telco. They will issue a request for information later this year as they assess the technical capabilities of vendors and their “readiness” for open FAN.

“The disaggregation of OLTs represents a valuable opportunity to broaden the telecom supply chain, which we’ve seen has become more important than ever during recent times,” said Paolo Pellegrini, TIM’s access innovation project manager, in telling remarks. “TIM is excited about the opportunities to work with a new generation of hardware and software suppliers who can bring innovative solutions that will help us build more cost-effective and efficient networks.”

Data from Omdia, owned by Informa, shows that just three vendors controlled 85% of the market for OLTs last year. Two of them, Huawei and ZTE, are Chinese, leaving Nokia as the only other supplier. The lack of alternatives explains why the UK government was less restrictive in fixed than it was in mobile when clamping down on Chinese vendors.

TIP probably hopes interoperability will boost competition in a market for passive optical network (PON) products worth about $8 billion in sales last year. If operators could more easily buy OLTs separately from ONTs, developers could focus resources on one area. An OLT specialist would not require an ONT capability to compete.

Today, mixing FAN products from different vendors is problematic, said a source at TIP, and Nokia seems to agree.

“It is not easy to do, but it is something that we do,” said Federico Guillén, the head of Nokia’s network infrastructure business group, during an interview at the recent Network X event in Amsterdam. “If you do this, you have to put in some rules for how the OLT and the ONT communicate and set a lower denominator, which means you are missing some features. Interoperability doesn’t come for free.”

Telecom already has an interface for connecting OLTs to ONTs, called OMCI (for ONT management control interface). But when it comes to multi-vendor interoperability, this does not seem to have delivered. “It was perfectly standardized, and everyone was implementing and following, but they were choosing different options,” said Stefaan Vanhastel, the chief technology officer for Nokia’s fixed network unit.

Nokia served about 24% of the global PON market last year, according to Omdia’s data, but has increased its presence in OLTs, according to Guillén. A backlash against Huawei in many countries outside China has probably helped. “Our market share is growing, especially where we want it to grow, which is the OLT side,” he told Light Reading. “The ONT side is a very crowded space.”

Specialists may find that challenging Nokia in the FAN is just as hard as it is in the RAN. Last year it pumped €4.2 billion (US$4.2 billion) into research and development, including investments in the silicon platforms that support higher-speed broadband services. At Network X, it announced a new OLT, branded Lightspan MF-14, that provides an upgrade path to 100G-capable networks. “Operators have a solution that will be reusable as line cards are upgraded over time,” said Julie Kunstler, chief analyst with Omdia. “This has lots of capacity and ONTs will be upgraded as needed.”

The new TIP Open FAN subgroup expects to issue an RFI to establish the technical capabilities and readiness of suppliers to deliver such a solution later in the year, with test and validation to follow.However, there was no mention of network equipment vendor support for open FAN in the TIP’s statement and without that it could struggle. If enough operators urge change, those vendors may have to budge – but the wariness of Ericsson and Nokia about open RAN illustrates just how difficult that could be. Open FAN also appears to lack an equivalent of the O-RAN Alliance, the group developing open RAN specifications. TIP has previously distanced itself from specifications development. If an alternative to OMCI is needed, who takes the lead?

Whether open FAN becomes as big a deal as open RAN is doubtful. For one thing, operators spent about $37 billion less on FAN products last year than on RAN kit, according to Omdia’s numbers. Most of their fixed-line capex goes into civil engineering, and no amount of interoperability or virtualization will save money there.

Despite the muscle of Huawei, Nokia and ZTE, the market was also growing more competitive before open FAN was a thing, according to Omdia’s Kunstler. Ciena, an optical equipment vendor based in the US, and Sterlite, an Indian firm that sells fiber-optic cable, are just two examples of companies moving into a PON market forecast to generate nearly $16 billion in annual sales by 2027.

References:

https://telecominfraproject.com/wp-content/uploads/Fixed-Access-UCD_v1.0_20220628.pdf

CableLabs to bring mobility to WiFi for a better user experience

Introduction:

CableLabs said it has developed a new technology that brings mobile, cellular-like capabilities to Wi-Fi networks. That, of course goes beyond the charter of IEEE 802.11 Working Group[1.]. CableLabs also believes its technology will enable cable operators to cut down on MVNO costs by offloading even more data to their Wi-Fi networks (this author frequently uses Xfinity WiFi when away from home for mobile Internet access).

The cable networks research organization is focusing the technology on home networks that are comprised of multiple Wi-Fi access points (APs) and extenders, but also believes the pieces are in place to support other use-cases, such as Wi-Fi network deployments in commercial buildings and the Cable Wi-Fi roaming initiative that now comprises about 4 million hotspots.

There have been many attempts to do this over the years, typically relying on coercing the device to reconnect to the new AP, but this frequently seems not to work quite right. Sometimes, there’s a lag before a device switches APs, and sometimes the device never switches APs. Or sometimes, the device insists that an AP is still present, even though it no longer is—for example, when you leave your house in your car and your phone insists it’s still connected to your home Wi-Fi.

Note 1. The IEEE 802.11™ Working Group (WG) is responsible for developing Wireless Local Area Network (WLAN) standards under the authority of the IEEE® Project 802 LAN/MAN Standards Committee (802 LMSC). The 802.11 WG is one of several WGs that comprise the Project 802 LAN/MAN Standards Committee (such as IEEE 802.3 Ethernet).

How Does CableLabs Mobile Wi-Fi Work?

CableLabs Mobile Wi-Fi uses a central controller to group multiple access points or APs (WiFi routers) into one continuous network. The central controller detects which AP your device is closest to and connects your device to that AP. If you move—for example, getting up and walking to a different room—then the controller evaluates whether you would get the best experience by staying connected to the old AP or if your experience would be better by switching to a new one. If it’s the latter, the controller moves your device to the new AP without you even noticing.

Instead of asking the phone to reconnect to a different AP, CableLabs Mobile Wi-Fi moves the network itself to the new AP. It does this using a virtual Basic Service Set, or VBSS. A VBSS is a network set up exclusively for use by one device and can be moved from AP to AP without the device disconnecting and reconnecting. This makes the transitions between APs seamless and transparent to the phone.

So now, as you walk around your house with your device, the CableLabs Mobile Wi-Fi controller is moving your VBSS such that it follows along with you, hopping from one AP to another as you go. If you wander too far and go outside the range of all your APs (like when you drive away in your car), the CableLabs Mobile Wi-Fi controller detects this, closes your connection and tears down your VBSS so that your phone immediately knows there is no longer a Wi-Fi connection. The phone will then immediately switch to cellular data.

The result is that your device will be consistently connected to the best available AP in your space. Gone will be the days of being connected to an AP across the house instead of the one right next to you. Your Wi-Fi will be better and faster.

When Can I Get It?

CableLabs Mobile Wi-Fi is not yet available to end consumers. For the next step toward a commercial implementation of CableLabs Mobile Wi-Fi, CableLabs has joined and is working with the prpl Foundation to include Mobile Wi-Fi in the open-source prplMesh implementation of Wi-Fi Alliance EasyMesh™️. Go to the prpl website for more information about prplMesh and access to the prplMesh codebase. CableLabs is also working in Wi-Fi Alliance to support Wi-Fi CERTIFIED EasyMesh.

For more information on CableLabs Mobile Wi-Fi, reach out to Steve Arendt, Principal Architect & Director, Advanced Technology Group, CableLabs.

…………………………………………………………………………………………………………………………………………………………………………………………………………………….

Steve Glennon, a distinguished technologist at CableLabs, told Light Reading that Wi-Fi has done well in new iterations to beef up physical data rates as home broadband speeds continue to climb to 1 Gbit/s and beyond. But he argues that Wi-Fi has fallen short of the mark in attempts to seamlessly connect smartphones to the best link in multiple-AP environments after the initial Wi-Fi connection is established.

“In general, phones go down the path of saying, ‘I’m connected, life is good.’ And they spend a bunch of battery and compute trying to scan and work out what’s around and when should I switch,” Glennon said. “You might be sitting right next to a Wi-Fi extender and your phone is still getting cruddy throughput. The problem is it’s associated with the main AP back in the living room of the house and in fact you’re upstairs in the bedroom sitting right next to the extender.”

Glennon said Wi-Fi roaming work around 802.11k, 802.11r, and 802.11v help to recognize this issue, but suggests they’ve not been super-successful at fixing it by giving the phone more information to help select the best AP.

Instead of putting a bunch of focus on the smartphone and requiring that device to be constantly scanning, CableLabs wants to flip things around by treating multiple APs like a mobile network. And instead of having the phone associate with a physical AP, the approach proposed by CableLabs is to create a virtual access point that moves from AP to AP without requiring the phone to know what’s going on.

CableLabs says it accomplishes that through a Virtual Basic Service Set (VBSS), which aims to virtualize the concept of an access point being a piece of hardware. The VBSS effectively is a network that is set up exclusively for use by one device and can be moved from AP to AP without the device (the smartphone, in this case) disconnecting and reconnecting.

“It’s like the binary version of the SSID [service set identifier],” Glennon explained. “It’s kind of like the magic, unique identifier for the access point. And rather than having physical access points, we virtualized the access point. You’re no longer associating with a physical access point; you’re associating with a virtual one. And because it’s virtual, we can move that virtualized access point between different pieces of hardware, without the phone even knowing … We can take the virtual access point and move it around between different physical access points.”

Glennon said the new Mobile Wi-Fi tech also has the smarts to automatically kick the phone off the Wi-Fi link if performance on the closest AP is degrading and to shift the phone to the cellular network. And when the Wi-Fi environment improves, the system will flip the phone back to Wi-Fi.

The broad aim here is to improve the customer experience when the phone connects to Wi-Fi as the user moves about. But Glennon notes there’s also some big, potential benefits to cable operators that are now in the mobile game: offloading more data on Wi-Fi and lowering MVNO costs.

“Offloading your mobile connection to Wi-Fi as frequently and as completely as possible is the best financial outcome for the cable operator who’s offering mobile service,” he said. “The whole point here is make the Wi-Fi experience be really good, because then you’ll do more Wi-Fi offload and there’s more financial benefit to our [members].”

Glennon said the project started about five years ago. The initial use case is for multiple APs in the home, but the pieces are there to extend the capability to commercial businesses and other venues where cable operators have set up Wi-Fi networks, he said.

References:

CableLabs Brings Mobile Wi-Fi’s Power to Wi-Fi Industry for a Better User Experience

https://www.lightreading.com/broadband/cablelabs-aims-to-bring-mobility-to-wi-fi-/d/d-id/781328?

https://www.ieee802.org/11/QuickGuide_IEEE_802_WG_and_Activities.htm

Juniper Research: 5G Fixed Wireless Access to Generate $2.5 Billion in Operator Revenue by 2023

Global telco revenues from 5G Fixed Wireless Access (FWA) will rise from $515 million in 2022 to $2.5 billion next year, according to a new report from Juniper Research. FWA includes services that provide high-speed Internet connectivity through cellular‑enabled CPE (Customer Premises Equipment) for uses including broadband and IoT networks.

The research predicts that operators’ 5G FWA revenue will reach $24 billion globally by 2027. It identified the consumer market as the sector generating the highest revenue for network operators, representing 96% of global 5G FWA revenue. However, it warns that operators must provide a compelling user proposition for FWA solutions through the bundling of services such as video streaming, gaming and smart home security to enrich user experience and gain competitive advantage against incumbent high‑speed connectivity technologies, such as FTTP (Fibre‑to‑the‑Premises).

| Key Market Statistics | |

| Market size in 2022: | $515m |

| Market size in 2023: | $2.5bn |

| 2022 – 2027 Market Growth: | 480% |

Juniper Research author Elisha Sudlow-Poole remarked: “The benefits of FWA are now comparable with services using fibre-based networks. Operators have an immediate opportunity to generate revenue from broadband subscriptions directly to end users by providing last-mile solutions underpinned by their existing 5G infrastructure.”

Juniper Research notes that the increase in 5G subscribers will be driven mainly by “the accelerating migration of cellular subscriptions to 5G networks, owing to operator strategies that minimize or remove any premium over existing 4G subscription offerings,” and that 600 million additional 5G subscriptions are expected be created next year, “despite the anticipated economic downturn in 2023.”

The report predicts that the growth of 5G networks will continue, and over 80% of global operator‑billed revenue will be attributable to 5G connections by 2027. The telecommunications industry demonstrated its robustness against the impact of the COVID-19 pandemic, and the report forecasts that the growth of 5G will also be resilient against this economic downturn due to the vital importance of mobile Internet connectivity today.

Juniper Research co-author Olivia Williams noted: “Despite the growth of the Internet of Things, revenue from consumer connections will continue to be the cornerstone of 5G operator revenue increase. Over 95% of global 5G connections in 2027 will be connected personal devices such as smartphones, tablets and mobile broadband routers.”

Private 5G Networks Represent a Key Opportunity for Operators:

In addition, the report predicts that the ability of standalone 5G networks to offer ‘network slicing’ will act as the ideal platform for the growth of 5G private network revenue. 5G Standalone (SA) uses 5G core networks supporting network slicing technology, which can be used to take a ‘slice’ of public 5G infrastructure and provide it to private network users. In turn, this helps mitigate the cost of private 5G network hardware and increase its overall value proposition, all against a background of deteriorating macro-economic conditions.

The report recommends that operators use 5G FWA to facilitate the last mile-solution by treating the relationship between FWA and fibre networks as wholly collaborative to maximize network performance and return on investment.

References:

https://www.juniperresearch.com/whitepapers/how-operators-will-capitalise-on-5g-fixed-wireless

5G Service Revenue to Reach $315 Billion Globally in 2023 | TelecomTV