Huawei to ship over 2 million “5G” base stations by 2020; Android vs HarmonyOS?

Huawei’s 5G network equipment business:

Ren Zhengfei, Huawei’s founder and CEO, says that his company will produce more than 2 million base stations over the next 18 months, regardless of whether the US decides to remove it from the Entity List. Zhengfei said that while the US’ decision to add Huawei to the entity list was profoundly unjust, it would have little impact on the company’s productivity – particularly with regards to its 5G network equipment.

How many more will they ship after IMT 2020 RIT/SRIT has been standardized by ITU-R in late 2020?

“First of all, please note that adding us to the Entity List was not fair. Huawei has not done anything wrong but was still placed on this list. This list didn’t have that much impact on us. Most of our more advanced equipment does not contain U.S. components, despite the fact that we used their components in the past. These newest versions of our equipment even function 30% more efficiently than before,” he said.

“In August and September, we will undergo a run-in period before we can mass produce these new versions. So, we can only produce around 5,000 base stations each month during that period. Following that, we will be able to produce 600,000 5G base stations this year and at least 1.5 million next year. That means we don’t need to rely on U.S. companies for our survival in this area,” Ren explained.

Ren Zhengfei, Huawei’s founder and CEO says the conflict with the U.S. has exceeded what he had previously thought.

…………………………………………………………………………………………………………………………………………………………………………………………….

While the impact on Huawei’s network infrastructure business is expected to be minimal, being added to the Entity List does create problems for Huawei’s handset business, particularly as the company looks to reel in its rival Samsung and claim top spot in the market. If Huawei were to be permanently added to the Entity List, it would lose access to Google’s Android operating system, which the company uses as standard on all its smartphone handsets.

“I could never have expected this controversy to be so intense though,” Ren said in a recent interview with Sky. “We knew that if there were two teams climbing up the same mountain from opposing sides, we would eventually meet on the peak and we may clash. We just didn’t expect this clash to be so intense and lead to this kind of conflict between the state apparatus of a country and a company.”

Ren has reportedly sent out another memo detailing the fallout of the conflict, which does finally seem to be hitting home. Job cuts are on the horizon, with replicative staff facing the axe and a simplified management structure promised. Contracts and payments will face higher scrutiny also, to keep an eye on free cash flow, while R&D seems to have been impacted also.

Android vs HarmonyOS on Huawei smartphones:

Huawei’s preference has always been to continue to use the Android operating system on its handsets, however, the US’ latest political campaign has forced the company to bring forward the release of its own OS, HarmonyOS.

“Google is a great company. We have a sound relationship with Google. We have signed many agreements with Google over the years. We still want to use Google’s system in our devices and develop within its ecosystem. Because of this, we hope that the U.S. government will approve the sale of Google’s system to us. There are billions of Android system users and billions of Windows system users around the world. Banning one or two companies from using these systems won’t help ensure the security of the U.S. as a country, so they should keep their doors open.”

“If the U.S. doesn’t want to sell the Android system to us, we will have no choice but to develop our own ecosystem. This isn’t something that can be achieved overnight. We estimate that it will take us two or three years to build this ecosystem. In light of all this, we don’t believe we will be able to become the number one player in the device sector any time soon,” Ren added.

Conclusions:

Huawei is already the undisputed leader in optical network and cellular network equipment. They are destined to be #1 in 5G network gear sales, independent of the U.S. sanctions and bans. Huawei is also #2 in global smartphone sales (Samsung is #1). And they’ve introduced a host of new innovative products like the Honor Vision smart screen.

While Americans shamefully excuse the isolation of Huawei as a wise action rooted in “national security” and an aversion to thievery, they don’t realize that Huawei has 80,000 R&D employees (mostly in China) and it spent $15 billion on R&D in 2018 alone. Of course, the Chinese government may have directly or indirectly funded much of that R&D but it is what’s contributed hugely to Huawei’s success.

References:

http://telecoms.com/499224/huawei-founder-has-been-expecting-5g-conflict-for-a-decade/

https://news.sky.com/video/huawei-chief-executive-speaks-to-sky-news-11786209 (video)

…………………………………………………………………………………………………………………………………………………………………………………………………………..

T-Mobile opens new Test Lab optimized for 5G, but also includes 4G LTE, 3G, LAA, NB-IoT, etc

T-Mobile US just opened a brand-new device lab designed to analyze performance and pressure test devices across the Un-carrier’s range of current and future 5G spectrum, as well as all current technologies. The new, 20,000 square foot facility will test 5G devices as well as devices which enable License Assisted Access, narrowband IoT, LTE and 3G. The new T-Mo test facility, known as the Launch Pad, also houses the carrier’s 5G Tech Experience showcase for 4G and 5G, in addition to T-Mobile US’ network lab.

Why it matters: New technology requires new and innovative approaches to testing, and the new lab will help T-Mobile ensure customers have the best experience possible with their new 5G devices.

The Un-carrier said in a press release that the new lab consists of more than a dozen testing areas, ranging from radio frequency signal testing to voice call/sound quality, video optimization and data throughput testing; “in-depth testing” of software, applications and services; and durability testing including drop-testing, water testing and sensitivity to heat. Further, the lab has equipment to test devices across a range of frequencies from low-band and mid-band to millimeter wave — in both its “current and planned” 5G spectrum, which is expected to expand considerably, if its proposed merger with Sprint is finalized.

T-Mo said the new device lab “is equipped with new, rigorous tests to ensure smartphones, IoT devices and any other connected devices take full advantage of the high-, mid- and low-band spectrum from New T-Mobile 5G, if the merger is approved.”

T-Mobile US said that the Launch Pad is designed to bring device and network quality engineers together to innovate and refine technologies from end-to-end before delivering them to customers” — which it said it critical for 5G, which is a combination of new tech in both devices and the network itself.

“5G will unlock SO MANY new capabilities and opportunities for innovation. And with that comes new complexities in delivering the technology to customers,” said Neville Ray, Chief Technology Officer at T-Mobile. “We’ve evolved in this new era of wireless to deliver continuous innovation and the best 5G experience possible — from the network to the devices in their hands — which is why I’m So. Damn. Proud. of this amazing team and cutting-edge lab,” he emphatically added.

The lab includes:

–Sub-6 GHz 5G Radio Performance Chamber: A test chamber for sub-6 GHz 5G testing, which has more than 50 antennas at different angles in order to assess signal quality transmission and reception.

–5G Millimeter Wave Antenna Range: A mmWave test chamber, complete with magenta “T” logo.

–Multi-band 5G SmartLab Chambers: A series of what the Un-carrier calls “5G SmartLab Chambers,” which support all of its current and planned 5G spectrum. T-Mo said that within those chambers, engineers can test devices across different combinations of spectrum and technologies.

–Software Performance Lab: A device software testing area, which contains machines that the carrier said are capable of “simulating a week’s worth of customer usage in just 24 hours,” including testing the device keyboard, battery life, and applications from voice calls and music to gaming, videos, texting, email and more. Devices have to run continuously for 24 hours and perform hundreds of tasks without any glitches or freezes, T-Mobile US added.

–Hardware Pressure Testing Room: A room for testing the durability of device hardware, where devices are put in machines which tumble and drop them, or that subject them to a wide range of temperatures to ensure that they continue to operate.

Reference:

https://www.t-mobile.com/news/5g-device-lab

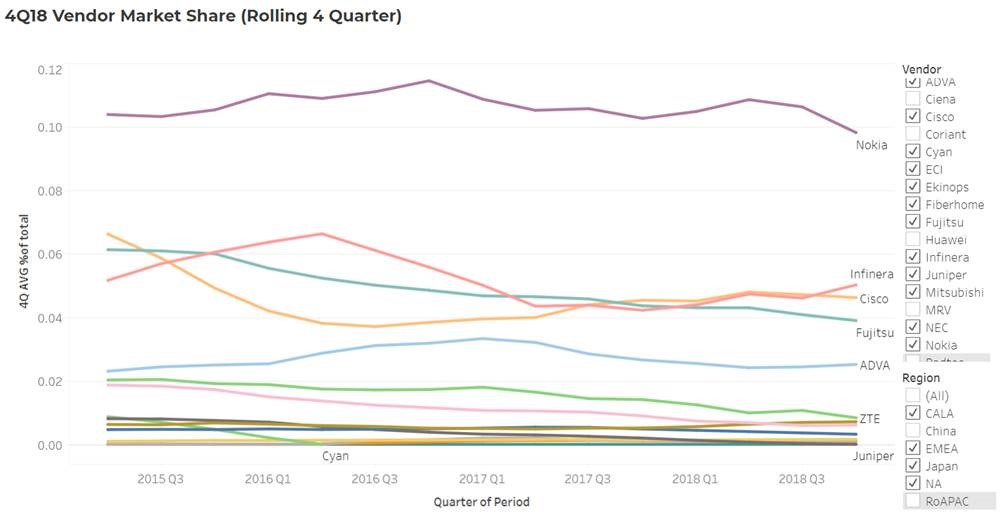

Cignal AI: Worldwide Optical Hardware Spending Increases; Huawei Remains #1 Vendor

|

||||

|

||||

|

||||

|

||||

|

| About Cignal AI |

| Cignal AI provides active and insightful market research for the networking component and equipment market and the market’s end customers. Our work blends expertise from a variety of disciplines to create a uniquely informed perspective on the evolution of networking communications. |

| Contact Us/Purchase Report: |

| [email protected] |

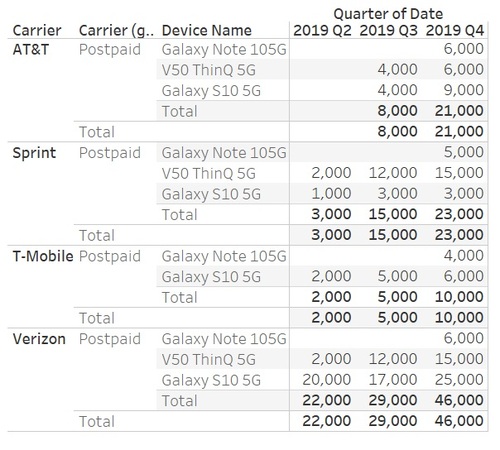

U.S. 5G Smartphone Sales Disappoint; Sticker Shock Pricing for 1st Wave of 5G phones

5G Smartphone Sales in U.S. are minuscule:

According to BayStreet Research via Lightreading, U.S. wireless network operators sold just 29,000 5G devices by the end of the second quarter. And the firm predicts that the number won’t grow much throughout 2019.

“It’s very small volume,” said Cliff Maldonado, the firm’s founder. “The value proposition [for 5G devices] isn’t clear.”

Pre-standard 5G is definitely in its infancy in the U.S. It only launched a few months ago, and it’s only available in a handful of cities on just a few phones. And those phones aren’t cheap: The Samsung Galaxy S10 5G for Verizon starts at an eye-popping $1,300, for example.

BayStreet Research says 5G phones haven’t been selling very well.

……………………………………………………………………………………………………………………………………………………………………………………………………….

Unlisted in the above chart is the 5G Moto Mod, an accessory that customers can snap on to a handful of existing Motorola smartphones that will allow them to access Verizon’s 5G network. Maldonado estimated just 1,000 to 2,000 sales of that gadget.

BayStreet obtains its figures from public and private data sources. Maldonado pointed out that the company’s third and fourth quarter figures are estimates. He also noted that the forecasts of 5G phone sales in the coming quarters don’t — and can’t — include as-yet-unannounced devices.

Many in the industry have argued that the rollout of 5G in the US could ultimately take up to ten years, considering operators will need to deploy 5G across more potentially millions more small cells, using a wide range of spectrum bands and will have to invest in technologies like mobile edge computing. For now, in the early days of 5G, most potential customers are staying on the sidelines.

Editor’s Note:

It’s extremely important to realize that a given 5G smartphone will only work on one carrier’s network, e.g. an AT&T 5G phone won’t work on Verizon’s 5G network. That’s because each pre-standard 5G wireless carrier uses different RIT specs (most are based on 3GPP Rel 15 NR NSA for the data plane with LTE signaling for the control plane and EPC for the mobile packet core) and different frequencies. So your so called 5G phone will fall back to 4G if you are not in range of your carrier’s pre-standard 5G network. That means limited mobility and certainly none when you travel to a city where your carrier doesn’t have 5G coverage.

All these pre-standard 5G deployments will be trashed and ditched when the IMT 2020 standard is completed and implemented in new standard IMT 2020 phones and base stations/small cells.

………………………………………………………………………………………………………………………………………………………………………………………..

Separately, IHS-Markit reports that the cost of the initial wave of 5G phones is dramatically exceeding expectations, with the price premium as much as 29 times higher than many consumers anticipate, according to a new IHS Markit survey examining consumer perceptions regarding the technology.

A total of 91 percent of survey respondents said they expect to pay more for 5G devices compared to existing 4G LTE smartphones. Three quarters of respondents stated they foresee paying an additional 10 to 25 percent for a 5G-capable phone. With the average sales price (ASP) of a smartphone amounting to $319 in 2019, a 10 percent hike in pricing would add $32 to the cost, while a 25 percent increase would boost it by $80.

However, the actual pricing of the first wave of 5G phones is far higher. For instance, Samsung’s S10 5G phone is retail priced at $1,300, a 335 percent premium compared to the $388 average for the company’s existing 4G smartphone models. In dollar terms, this would represent a $912 increase in price, an order of magnitude higher than consumers’ expectations.

It should be noted that this comparison is of a flagship smartphone price against an industry ASP. Naturally, newer technologies almost always come first to premium smartphones, which typically are two to three times as much as industry ASP. Also, given the nature of 5G radio design, these early 5G smartphones are configured with larger-than-typical displays and packed with extra features such as time-of-flight (ToF) cameras to enable AR applications. All of these extras do contribute to a higher-than-expected retail price from a consumer perspective.

In another example, the Huawei Mate 20 X 5G smartphone carries a retail price of $1,200, a more than 400 percent premium compared to $295 for the company’s 4G models.

This pricing discrepancy could instill sticker shock among many consumers. While such pricing premium is not likely to impact early adopters, it could slow sales of 5G devices to the wider, more mainstream consumer market.

“The 5G market is primed for massive growth, with the transition to the new technology expected to occur at a much faster pace than any previous wireless generation during the first five years of deployment,” said Joshua Builta, senior principal analyst at IHS Markit. “However, as with each new wireless generation, the first wave of phones carries sky-high costs because of the additional electronics required to support the enhanced features. With smartphone brands passing these additional costs down to consumers, many buyers will be turned off by the high prices and will wait until they come down before purchasing a 5G phone.”

Expectation of price premium for 5G smartphones:

Fast wireless technology makes slow initial progress:

Global 5G handset shipments are expected to soar to 424.5 million units in 2023. However, shipments will start rather modestly, amounting to just 9.5 million in 2019—the first year of deployment—and only 73.7 million in 2020. This represents a slower initial rate than for 4G LTE when it first deployed a decade ago, although the longer-term outlook for subscriber growth for 5G is more optimistic than for 4G.

The early 5G smartphones analyzed by IHS Markit demonstrate why their cost and pricing is so elevated. For example, some 5G phones include a highly complex radio-frequency (RF) subsystem designed to support millimeter wave capability for high-speed data transfer. Specifically, in the U.S., the Moto Z3 with 5G Mod and a version of the Samsung Galaxy S10 5G both integrate multiple separate millimeter wave antenna modules that are strategically placed throughout the device to allow clear signal reception. When considering that most smartphone designs employ just one antenna module, it’s easy to see how this redundant design drives up costs significantly.

Lower prices for a bigger market:

However, just as occurred in the 4G LTE era, 5G phone pricing is expected to decline quickly. Prices will begin to decrease next year as phone OEMs use more efficient designs employing multimode modems. Within the next few years, prices will fall to between the $700 to $800 range, making them more affordable for price-conscious consumers. Elsewhere, markets such as China will deploy a standalone (SA) 5G network which will further simplify RF front-end design requirements to further push down the industry ASP.

Consumer expectations:

Many consumers equate 5G with faster data speeds and aren’t aware of the technology’s other benefits. As a result, their low expectations for pricing premiums may not take into account all of the advantages and allures of 5G technology.

For example, improved immersive entertainment experiences like virtual reality (VR) have been cited as a key benefit of 5G. The 5G standard eventually can provide the kind of ultra-low latency that VR requires. However, fewer than 30 percent of survey respondents said they would increase their use of VR with the arrival of 5G.

As the market waits for prices to decline, brands may be able to overcome consumer reticence regarding pricing by promoting the other attributes of 5G beyond speed.

About IHS Markit Digital Orbit:

IHS Markit’s Digital Orbit report summarizes the results of a survey on how consumers perceive 5G and how they intend to use the new technology. The survey was conducted May 22-27 among 2,031 respondents, 95 percent of whom were US-based. The median age of the survey respondents was 43, and 63 percent lived in urban areas.

Park Place Technologies on network monitoring, predictive fault diagnosis and repair; Entuity acquisition adds analytics

by Michael Cantor, CIO, Park Place Technologies

Introduction:

While network monitoring is a key component of predictive fault diagnosis and repair, it’s just one part of an overall solution to the network maintenance problem. Network monitoring, depending on the level of sophistication, can supply multiple data streams that contribute to fault diagnosis and repair. At the simplest level, a network monitor can notify on circuit up/down, overall bandwidth utilization on particular circuits, and individual network gear parameters, such as CPU usage. At the next level of sophistication, a network monitor can perform flow analysis and deep packet inspection to look for configuration issues or unexpected application traffic. And last, a network monitor may provide service delivery monitoring, combining all of the above to arrive at fault diagnosis from end-to-end across the network.

Network monitoring currently lags for the various cloud vendors, so providing coverage for IaaS (Infrastructure as a Service) installations in the cloud as part of the overall solution is the next major area of development among the network monitors. That said, to get a truly useful picture of IT operations, an overall platform is needed to combine the data streams from all types of monitoring: hardware, operating system, database, and application, along with network monitoring to really get predictive of a fault.

For example, a performance problem is likely to be noted in the application first, and it can take days of effort to trace that performance problem to a defective or over-utilized piece of network gear that is intermittently losing packets. Combining all these inputs together, along with an AI layer, results in a platform that can make a difference in daily IT operations: accelerating fault diagnosis and reducing false alarms.

…………………………………………………………………………………………………………………………………………

The ParkView™ platform:

It monitors customer hardware 24/7. When a fault is detected, ParkView™ instantly creates a ticket including the details necessary to resolve the issue, so there’s no need to call. ParkView™ identifies the exact nature of the issue and all relevant details to resolve it. ParkView™ will suppress all non-vital events including soft errors and status updates – only notifying you of issues that are pressing in nature.

Over time, ParkView™ leverages machine learning to detect faults before they even occur (i.e. predictive fault detection).

Other ParkView™ features include:

- Vendor-agnostic interface supports a wide range of OEMs, platforms, OS and generations

- Real-time visibility via Central Park customer portal

- Security features are based on your company’s unique requirements and all data transmitted to ParkView™ is SSL encrypted

……………………………………………………………………………………………………………………………………………………………………….

Case Study –Proactive detection of hardware faults in a telco environment:

Cincinnati Bell has seen demonstrable savings of time and money since adopting ParkView™, a service that proactively detects faults in storage, server and networking hardware.

ParkView™ is a revolutionary new remote service that proactively detects equipment hardware faults 24/7 across storage, server, and networking products. The related alerts are then securely transmitted to Park Place Technologies’ technical operations, enabling more timely and accurate failure diagnosis, part identification, and necessary repair actions. The company was able to save 8 hours per week not having to travel to remote data center to search for flaws.

A video describing the case study can be viewed here.

……………………………………………………………………………………………………………………………………………………………………….

Importance of Entuity Acquisition:

Earlier this month, Park Place Technologies acquired Entuity, a specialist firm that offers networking monitoring and visibility, as well as asset control software. Entuity has offices in Boston and London. It’s s an established player in the network performance monitoring sector, where it provides the software analytics needed to keep networks performing, as well as visibility into issues before they impact business services.

For over 20 years, Entuity has focused on network performance monitoring to ensure uninterrupted service delivery. Entuity provides the analytics needed to keep networks performing and visibility into issues before they impact business services. Entuity is a perfect complement to Park Place Technologies as both organizations are customer-centric, have a deep-seated commitment to their employees and are laser-focused on maximizing customer up-time.

Park Place Technologies is the global leader in third-party maintenance for data center hardware, and this software acquisition will be a key component of its multi-vendor service delivery model. Following the acquisition, Park Place will be the only multi-vendor, global hardware maintenance provider that offers customers monitoring, automated maintenance, Network Operations Center (NOC) services, event management, probable cause and IT Data Analytics across a single pane of glass.

“This acquisition represents a milestone for Park Place Technologies as we welcome Entuity, a highly regarded network performance monitoring provider into the Park Place family,” said Chris Adams, President and CEO, Park Place Technologies. “When Entuity is integrated with our award winning ParkView™ monitoring product, we will deliver enhanced network visibility and NOC services, driving uptime for our global customer base.”

“It is exciting to see how this partnership will yield mutual benefits for both companies and their customers across the globe,” said Stephen Woodard, President and CEO, Entuity. “Entuity’s auto discovery and inventory capabilities, live topology, event management and probable cause analysis strengthens Park Place’s existing innovations and industry-leading solutions such as ParkView™.”

……………………………………………………………………………………………………………………………………………………………………….

Acknowledgement:

Thanks to Catie Gehlert of Global KWT for facilitating publication of this article.

CenturyLink CTO on Network Virtualization; Major Investment in Edge Compute Services

Andrew Dugan, senior vice president and chief technology officer, CenturyLink, Inc. presented his company’s views on network virtualization and related topics at the Cowen and Company 5th Annual Communications Infrastructure Summit in Boulder CO., on Aug. 13th. You can listen to the audio webcast replay here.

Dugan said he doesn’t know what AT&T means when the mega carrier says it’s virtualizing 75% of its core network by the end of 2020. “I’d like to figure out what AT&T means by 75% virtualization,” said Dugan. “I don’t get it. The concept of virtualizing the core router or an optical platform, that’s a lot of cost of your network to provide services. We’re not working on virtualizing that stuff.”

Dugan said CenturyLink is focused on virtualizing systems that enable its customers to turn up and turn down services on demand, and it’s also focused on virtualization at the edge of its network. He said the company likes the benefits of putting a white box device on the customer premises and “letting a customer turn up a firewall or an SD-WAN appliance or a WAN accelerator whenever they want.”

Earlier this week, CenturyLink announced the rollout of its edge compute-focused strategy, beginning with a several hundred-million-dollar investment to build out and support edge compute services. This effort – which includes creating more than 100 initial edge compute locations across the U.S., and providing a range of hybrid cloud solutions and managed services – enables customers to advance their next-gen digital initiatives with technology that integrates high performance, low-latency networking with leading cloud service provider platforms in customized configurations.

“Customers are increasingly coming to us for help with applications where latency, bandwidth and geography are critical considerations,” said Paul Savill, senior vice president, product management, CenturyLink. “This investment creates the platform for CenturyLink to enable enterprises, hyperscalers, wireless carriers, and system integrators with the technology elements to drive years of innovation where workloads get placed closer to customers’ digital interactions.”

This expansion allows businesses and government agencies to leverage a highly diverse, global fiber network with edge facilities designed to serve their local locations within 5 milliseconds of latency. With this infrastructure, companies will be able to complete the linkage from office location to market edge compute aggregation to public cloud and data centers with redundant and dynamically consumable network.

“Digital transformation is gaining momentum as enterprises across all verticals look to technology to improve operational efficiency and enhance the customer experience,” said Melanie Posey, Research Vice President and General Manager at 451 Research. “As business processes become increasingly distributed, data-intensive, and transaction-based, the IT systems they depend on must be equally distributed to provide the necessary compute, storage and network resources to far-flung business value chains.”

Dugan said the edge compute platform plays into the company’s virtualization efforts, allowing customers the ability to turn up and turn down Ethernet services, increase capacity, change vLANs, and configure their services on-demand.

“That, to me, is where NFV and SDN comes in. We haven’t put a number on the percent of the network. We’re more focused on that customer enablement,” he said.

“When you build out an NFV platform, you’ve got the cost of the white box, you have the cost of the management or virtualization software that runs within the white box, and you have the cost of the virtual functions themselves. If you’re running one or two applications on premise, it’s not cheaper. The real value from NFV comes in the flexibility that it provides you to be able to put a box out there and be able to turn up and turn down services. It’s not a capex reduction…It’s a reduction in operating costs because you’re not having to roll trucks and put boxes out,” Dugan added.

CenturyLink says its “thousands of secure technical facilities combined with its network of 450,000-global route miles of fiber, expertise in high-performance cloud networking, and extensive cloud management expertise make this investment in the rapidly emerging edge compute market a natural evolution for the company.”

Key Facts (source: CenturyLink):

- CenturyLink today connects to over 2,200 public and private data centers and over 150,000 on-net, fiber-fed enterprise buildings.

- CenturyLink’s robust fiber network is one of the most deeply peered and well-connected in the world, with over 450,000 route-miles of coverage.

- CenturyLink is expanding access to its services by expanding network colocation services in many key markets to enable customers and partners to run distributed IT workloads close to the edge of the network.

……………………………………………………………………………………………………………..

CenturyLink References:

IHS Markit: CenturyLink #1 in the 2019 North American SIP Trunking Scorecard

VSG’s U.S. Carrier Ethernet LEADERBOARD: CenturyLink #1, AT&T #2; U.S. CE port base grew >12%

CenturyLink offers Multi Cloud Connect L2 Service for Fiber-fed Buildings

Samsung (with AT&T) Tests How 5G Can Improve Chip-Making

By Sara Castellanos of the Wall Street Journal

Samsung Electronics Co. is testing how 5G wireless networks can speed up connections at its chip-making factory in Austin, Texas, a pilot that aims to prove 5G is more than a buzzword. The company is experimenting with the new technology to show what ultra-fast speeds can do at its Austin chip factory

The company has teamed up with AT&T Inc. ’s communications division to develop a customized 5G network to experiment with how it could be used in chip manufacturing.

The fifth generation of cellular networking, 5G is designed to replace current 4G technology, also known as LTE. The ultrafast speeds and reduced lag that will come with 5G will buttress new applications such as augmented reality and self-driving cars. Peak download speeds using 5G are expected to be about 100 times as fast as with 4G.

The transformation that will come from widespread commercial 5G deployments in manufacturing, logistics, transportation and energy is still about a decade away, experts have said. That’s partly because it will take time to roll out the infrastructure to achieve full 5G coverage.

In the meantime, Samsung and other companies are testing 5G’s potential in limited pilots to show what the technology can do.

“We’re still in the experimentation phase, but we’re hopeful there’s value,” said Alok Shah, vice president of networks strategy, business development and marketing at Samsung Electronics America, the company’s U.S. unit.

Factories will be a big beneficiary of 5G connections, said Andre Fuetsch, chief technology officer for AT&T Communications, AT&T’s biggest division.

“We see 5G being a great solution for solving a lot of the Wi-Fi issues that typical factories have today,” he said. The technology, for example, could be used on manufacturing floors to power more reliable connections for computer-vision-scanning equipment that checks product quality.

AT&T has also rolled out consumer 5G networks in about 20 U.S. cities.

Samsung Electronics America and AT&T have invested millions of dollars in 5G innovation at Samsung’s chip-manufacturing facility in Austin. Thousands of employees work at the chip factory, which is the size of about 10 football fields, Mr. Shah said.

Chip-making uses a lot of water and toxic chemicals; 5G could help chip factories cut waste and alert workers to safety hazards.

For example, 5G would allow more sensors to be installed to detect air quality, Mr. Shah said. Streaming real-time data from the sensors over 5G networks would mean that a control center can immediately detect serious air-quality hazards and move people out of harm’s way. Sensors in factories today can’t rely on existing wireless networks to pass along warnings to a control center, Mr. Shah said.

“Being able to put thousands of sensors within a relatively small space is hard for other [networking] technologies to support,” Mr. Shah said. Certain networks can only support a finite number of devices. Fifth-generation wireless networks could support 1 million devices per square kilometer, up from about 100,000 devices per square kilometer with 4G LTE, he said.

Sensors on pumps and valves could also stream data about water usage over 5G networks so the facility can improve the efficiency of its water usage in real time and reduce waste.

Using 5G connections, workers could also learn how to repair equipment on the factory floor through augmented and virtual-reality headsets without any buffering or lags.

Other companies including New York Times Co. and German engineering firm Robert Bosch GmbH are testing 5G in pilots. The market for 5G, including related network infrastructure, is forecast to grow to $26 billion in 2022 from $528 million in 2018, according to research firm International Data Corp.

The tests are often “showcase demonstration pieces,” useful for proving that 5G could generate revenue through new services or make processes more efficient, said Jason Leigh, research manager for mobility and 5G at IDC.

“The sooner you can get something tangible, it makes it easier to have that discussion at a C-suite and board level about what 5G really is, and it’s not just this fad,” Mr. Leigh said.

Write to Sara Castellanos at [email protected]

https://www.wsj.com/articles/samsung-tests-how-5g-can-improve-chip-making-11565813658

…………………………………………………………………………………………………………………………….

Last September, AT&T and Samsung created the US’s first manufacturing-focused 5G “Innovation Zone” in Austin, TX. The zone, designed to test 5th generation wireless broadband technology, will be on Samsung Austin Semiconductor’s 160-acre campus in north Austin. The site will feature AT&T’s 5G wireless technology along with Samsung’s 5G network equipment, according to an announcement Wednesday from the two companies.

Technology experts say 5G — which is essentially ultra high-speed wireless connections — will not only power future waves of mobile devices, but also will evolve technology in other industries like automotive and health care. Companies expect 5G to be up to 100 times faster than the current 4G networks.

“This collaboration with Samsung Electronics America and AT&T will help us test how a 5G network can improve mobility, performance and efficiencies within our plant,” Sang-Pil Sim, president of Samsung Austin Semiconductor, said in a statement.

South Korea-based Samsung has operated in Austin since 1997. About 3,000 employees work in the 2.45 million-square-foot Austin chip making plant. Samsung has invested $17 billion in its Austin campus through the years.

Kagan: Broadband Wireline Internet growth slowing with cable leading telcos; U.S. vs Europe cord cutters compared

Broadband service providers continued to gain customers ahead of widespread competition from pre-standard 5G wireless offerings, but growth is slowing as nearly four out of five homes in the U.S. now subscribe to a wireline internet connection, according to a new report released today.

Kagan, a media research group within S&P Global Market Intelligence, estimates cable and telecom providers combined added 339,000 residential subscribers in the second quarter. The momentum was largely driven by the cable industry. Cable operators saw the rate of growth shrink on a sequential and annual basis, but they did not however lack market share gains, adding nearly half a million new residential customers versus a net loss for the telecoms of 155,000 customers.

Ian Olgeirson, Research Director at Kagan commented: “We estimate wireline broadband penetration increased slightly to 78.5% of occupied households. Cable’s residential gains did not match the levels from the previous or year-ago quarters, but net adds in the trailing 12 months are still higher at 2.8 million when compared to the same period in 2018. Telco broadband slumped in the second quarter, returning to a pattern of six-figure losses after holding steady in the first quarter. Growth in telco fiber-to-the-home connections was not sufficient to overcome losses to legacy copper and fiber-to-the-node DSL connections.”

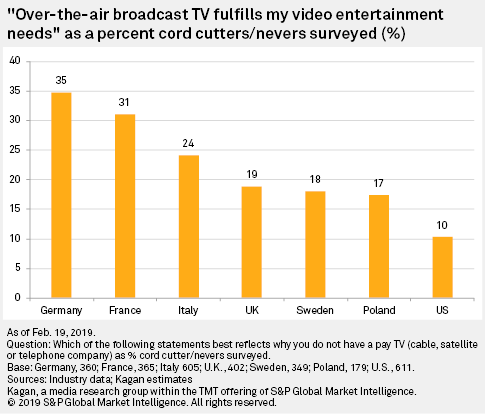

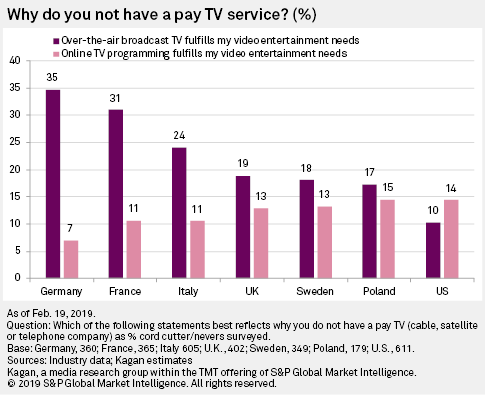

Separately, Kagan says that Americans are not the only ones cutting the cord. The vibrant and free-to-air broadcasting options available in most of the EU countries we surveyed makes paying for TV a hard sell, subscription video on demand or otherwise.

For instance, when Kagan asked cord cutters and “cord nevers” why they cut the cord or never added a video service, 35% of German cord cutters/nevers answered that “rabbit ears” fulfill their video entertainment needs. All respondents from EU countries surveyed scored above 15% on this metric. But just 10% of U.S. survey-takers felt the same way.

Kagan thinks the longer history with pay TV in the U.S., one that was forecast by Paul Kagan in the late 1960s, has left Americans with more paid TV options than Europeans, leading to fewer viewers stateside who mostly use over the air, or OTA.

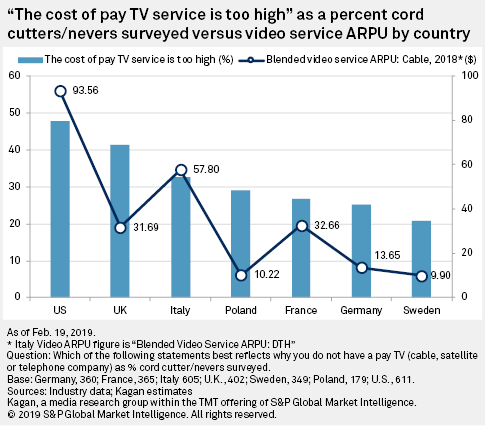

But the longer pay TV history in the U.S. does not imply Americans like paying for the service.

Nearly half of American cord cutters/nevers said price was the main reason they cut the cord or never connected, the highest rate among all seven countries we reviewed. Americans pay close to $100 per month on average for traditional multichannel video services, with EU countries coming in lower. Sweden’s average monthly fee for video is under $10 and survey-takers there were consequently less concerned with pricing. A significant factor in lower pay TV access prices in Europe is that sports and premium channels are only included in top TV tiers, with basic packages boosted by a large number of OTA (over the air) channels.

U.S. survey-takers were also the only ones to say online video services were more important than free OTA in terms of why they cut the cord or never added a cord. For instance, while 10% of Americans said rabbit ears were enough reason to cut the cord, 14% said the same about online video services, including Netflix. Again, this could be a case of the U.S. being first to market with online video services and remaining relatively ahead of the pack.

As traditional media companies look towards a digital future it’s important to remember that what matters to US consumers might matter less overseas.

About S&P Global Market Intelligence:

At S&P Global Market Intelligence, we know that not all information is important—some of it is vital. We integrate financial and industry data, research and news into tools that help clients track performance, generate alpha, identify investment ideas, understand competitive and industry dynamics, perform valuations and assess credit risk. Investment professionals, government agencies, corporations and universities globally can gain the intelligence essential to making business and financial decisions with conviction.

S&P Global Market Intelligence is a division of S&P Global (NYSE: SPGI). For more information, visit www.spglobal.com/marketintelligence

GSA Update and Analysis: 5G Devices Ecosystem – August 2019

- The GSA Research team has identified 100 announced 5G devices in total, excluding regional variants and prototypes not expected to be commercialised.In the first half of 2019, the number of announced 5G devices grew rapidly, starting with a few announcements and then gathering pace as operators in various parts of the world launched their first commercial 5G services. We can expect the device ecosystem to continue to grow quickly and GSA will be tracking and reporting regularly on 5G device launch announcements. Its GAMBoD database will contain key details about device form factors, features and support for spectrum bands. Summary statistics are released in this regular publication. By the first week of August, GSA had identified:

- Thirteen announced form factors (phones, hotspots, indoor CPE, outdoor CPE, laptops, modules, snap-on dongles/adapters, enterprise routers, IoT routers, drones, a switch, a USB terminal and robot).

- Forty-one vendors that had announced available or forthcoming 5G devices, including sub-brands separately (plus four in partnership with Sunsea).

- One hundred announced devices, up from 90 at the end of June (excluding regional variants, re-badged devices, phones that can be upgraded using a separate adapter, and prototypes not expected to be commercialised):

- 26 phones (plus regional variants); at least nine of which are now commercially available

- eight hotspots (plus regional variants); at least three of which are now commercially available

- 26 CPE devices (indoor and outdoor, including two Verizon-spec compliant devices) at least eight of which are now believed to be commercially available

- 28 modules

- two snap-on dongles/adapters

- two routers,

- two IoT routers

- two drones

- one laptop

- one switch

- one USB terminal

- one robot

Here are the commercially available 5G devices as listed in the GSA’s latest report August 2019:

- HTC 5G Hub (hotspot)

- Huawei 5G CPE 2.0 (indoor and outdoor customer premises equipment, or CPE)

- Huawei 5G CPE Win (outdoor and window CPE)

- Huawei 5G CPE Pro (indoor CPE)

- Huawei Mate X (phone)

- Huawei Mate 20x 5G (phone)

- Inseego R1000 Home Router/MiFi IQ 5G (fixed wireless indoor CPE)

- Inseego MiFi M1000 5G Mobile Hotspot (hotspot)

- LG V50 ThinQ (phone)

- Motorola 5G Moto Mod Snap-on (dongle)

- Netgear Nighthawk M5 Fusion MR5000 (aka Nighthawk 5G Mobile Hotspot) (hotspot)

- Nokia Fastmile 5G Gateway CPE (indoor/ outdoor CPE)

- OnePlus OnePlus 7Pro 5G (phone)

- Oppo Reno 5G (phone)

- Percepto Drone-in-abox (drone)

- Samsung SFG-D0100 (indoor CPE)

- Samsung Galaxy S10 5G (phone)

- SIMCom Wireless SIM8200- EA-M2 (module)

- SIMCom Wireless SIM8200G (module)

- Xiaomi Mi Mix 3 5G (phone)

- ZTE Axon 10 Pro 5G (phone)

- ZTE 5G Indoor CPE MC801 (indoor CPE)

……………………………………………………………………………………

What versions of 5G have been deployed/announced?

After downloading and reading the GSA report, I noticed a huge omission: the version of 5G is not disclosed for any of the “pre-IMT 2020 standard 5G” deployments. Most are likely to be based on 3GPP release 15 “5G NR” for the data plane NSA (LTE signaling and EPC). However, many of the 5G fixed wireless deployments (like Verizon’s and C-Spire) are proprietary.

5G silicon?

Also of note is that within the 5G devices, there are only four 5G silicon vendors chipsets – Qualcomm is by far the largest selling 5G SoC’s/IP, then Mediatek selling on the merchant market, whereas Huawei and Samsung design their own silicon for their 5G terminals/handsets and base stations.

Note while there is not yet any “Intel inside” 5G, Intel has sold its 5G smartphone modem silicon business to Apple recently for $1B.

If 5G were truly such a hot market, why aren’t there other semiconductor vendors pursuing it?

IHS Markit: CenturyLink #1 in the 2019 North American SIP Trunking Scorecard

By Diane Myers, senior research director, IHS Markit

Highlights:

- CenturyLink leads the market for session initiation protocol (SIP) trunking with the largest installed base of all North American providers.

- Twilio has been a disruptor in the SIP trunking market and placed second in the scorecard due to solid market momentum.

- Verizon and AT&T were #3 and #4, respectively.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………

Editor’s Note:

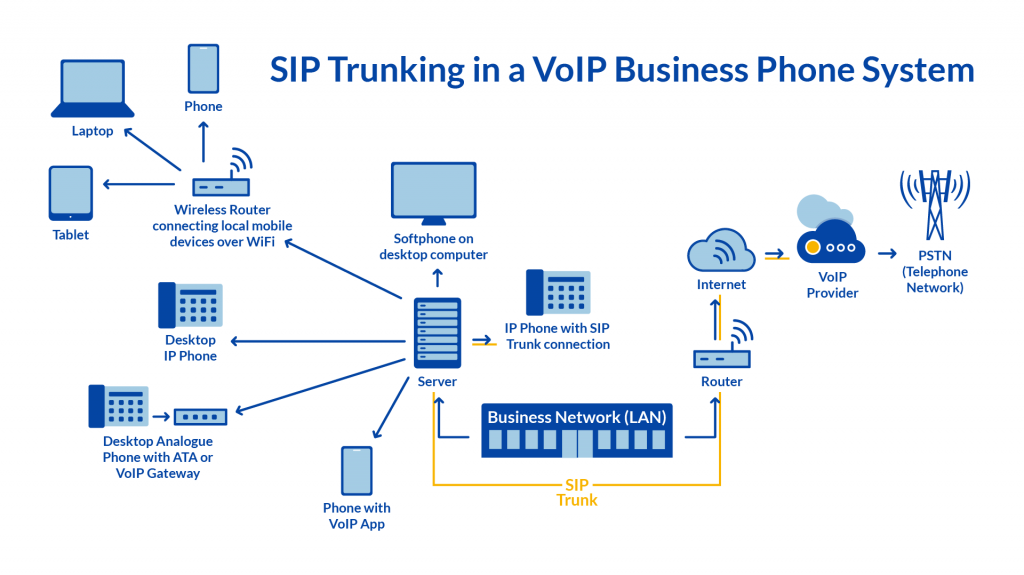

SIP (Session Initiated Protocol) trunking is a method of sending voice and other unified communications services over the internet. It works with an IP-enabled PBX (private branch exchange). SIP trunking replaces traditional telephone lines or PRIs (Primary Rate Interface).connects both IP and analog devices via the Internet, eliminating the need to maintain separate voice circuits or replace legacy equipment.

Before SIP became a popular and reliable method of transmitting voice signals, telephone calls were carried over the Public Switched Telephone Network (PSTN). The PSTN is a circuit switched network, which requires a physical connection between two points to complete a call.

SIP trunks are virtual phone lines that enable users to make and receive phone calls over the internet to anyone in the world with a phone number. SIP trunks utilize a packet switch network, in which voice calls are broken down into digital packets and sent across a network to the final destination.

Each SIP trunk supports SIP channels. A SIP channel is equivalent to one incoming or outgoing call. A SIP trunk can hold an unlimited number of channels, so users only need one SIP trunk no matter how many concurrent calls they expect. The number of channels required depends on how many calls the business will make at any one time.

References:

https://www.sip.us/blog/latest-news/sip-trunking-101-the-fundamentals/

https://www.nextiva.com/blog/sip-trunking.html

…………………………………………………………………………………………………………………………………………………………………………………………………………………………….

IHS Markit analysis:

In its 2019 SIP Trunking North America Scorecard, IHS Markit analyzed and ranked the top SIP trunking providers in North America. For the fourth year in a row, CenturyLink leads the SIP trunking market with solid growth and the largest installed base of trunks. CenturyLink has done extensive work over the past two years bringing together its assets with those of Level 3, a company it acquired in 2017, to build a market-leading service portfolio and customer base.

In this year’s scorecard, Twilio made another jump to the second-ranked position because of its strong financial score and the continued growth of its installed base. Twilio has been a market disruptor with its Elastic SIP Trunking service, which has grown to attain a sizable installed base. The strong growth of Twilio’s Elastic SIP Trunking service reflects the widespread appeal of flexible consumption-based pricing.

Just a few years ago, there was little differentiation in the SIP trunking market. Fast forward to today, and there is a stark difference between traditional trunking services and the new on-demand trunks. Traditional trunking remains grounded in the old world of contracting for voice networking. In contrast, with on-demand trunks, customers simply pay for what they use and never need to worry about capacity planning.

SIP Trunking North America Scorecard:

In the 11th annual SIP Trunking North America Scorecard, IHS Markit analyzes the top-10 North American SIP trunking service providers: CenturyLink, Twilio, Verizon, AT&T, IntelePeer, Fusion, Rogers, Voyant, Windstream and Sprint. The criteria used in this analysis include market share, financial strength, market share momentum, service development and support options.