Author: Alan Weissberger

Vestaspace Technology joins SpaceX in launching Internet Satellites

Commercial space-tech company Vestaspace Technology will launch 35+ 5G satellites this September for pilot to build 5G speed network connections and IoT functionalities for industries.

Editor’s Note:

Sounds a lot like what Elon Musk’s SpaceX plans to do with its Starlink internet satellites. The satellite constellation will consist of thousands of mass-produced small satellites in low Earth orbit (LEO), working in combination with ground transceivers. Starlink is targeting service in the Northern U.S. and Canada in 2020, rapidly expanding to near global coverage of the populated world by 2021.

Image Credit: SpaceX

…………………………………………………………………………………………………………………………………..

In a statement Tuesday, Vestaspace said it will release beta version of satellite constellations pan-India in September and fully-operational version early next year into Low-Earth-Orbit or Geosynchronous Equatorial Orbit.

“The company plans to replace traditional fiber networks with all the satellite constellations and to provide high-speed 5G network connections PAN India with its unmanned Software Data processing,” it said.

The company has tested a live-streamed video of 1080p (Full HD) with less than 34 milliseconds latency with the speed of more than 400 Mbps.

With regards to data privacy and security issues, Vestaspace has put 10 layer firewall that does immediate remediation if any false data is found.

Arun Kumar Sureban, Founder & CEO, Vestaspace Technology said, “To solve the complex system and to provide 5G internet network solutions to the Urban, Rural and unserved regions, we have positioned 8 Ground Stations and 31,000 data receptors all over India. This is made possible with the help of accurate positioning and telemetry related activities.”

The Pune, India-based startup has secured USD 10 million funding from an American investment and advisory firm Next Capital LLC, and has been working with ISRO, NASA and other leading space agencies on various strategic projects.

However, we don’t think these Internet satellites have anything to do with 5G which is defined as a terrestial wireless interface (at least that’s true for IMT 2020).

References:

Sweden Telecom Operators Announce 5G Network Launches and Details

Three major telecom companies in Sweden –Tele 2, Telia, and Tre Sweden– have announced their upcoming 5G network launches and areas covered. Sections of Stockholm, the nation’s capital, already have 5G service, with many more being added to the list as the year goes on, as well as other cities and towns in Sweden.

On May 24th, Tele 2 switched its network to 5G, with availability opening up to customers as of June 24 in Stockholm, Gothenburg, and Malmö. The Tele2 network will offer service at more than 1 Gbps through 80 MHz bandwidth on the C-band.

Customers with a Tele2 Unlimited subscription and a compatible handset from Samsung’s Galaxy S20 series will get free access to Tele2’s 5G network from 24 June. Other offers and cooperations with other phone manufacturers will be presented later, and Tele2 will gradually phase in 5G throughout Sweden.

Telia inaugurated its first major 5G commercial network in Stockholm today (May 25th) even though it had already been up and running for a few weeks. It has 15 base stations that are already in place, and 60 more will be built in June hand in hand with Ericsson, who will be powering the network for Telia. Initial services on the 700Mhz band will cover most of central Stockholm by mid-June, including the Norrmalm, Östermalm and Vasastan districts (more below).

Tre Sweden is jumping on the 5G board by bringing its network in the centers of Malmö, Lund, Helsingborg, Vasteras, Uppsala, and western parts of Stockholm in June. Tre said that it would activate 5G in Stockholm city centre after the summer. The earlier start in western Stockholm will include Kungsholmen, Bromma and parts of Solna. This will be an expansion of its already-launched 5G network back in December 2019, when it announced testing.

…………………………………………………………………………………………………………………………………………

Telia takes center stage to promote 5G:

Telia aims to enhance and supplement its low-band 5G commercial services with additional nationwide 5G coverage, including mid- and high-bands, following the auction of the related spectrum by the Swedish government later this year. For this launch Telia is using its existing 700MHz spectrum, boosted by LTE and New Radio (NR) carrier aggregation.

Fredrik Jejdling Executive Vice President and Head of Networks, Ericsson; Allison Kirkby, CEO, Telia Company; Anders Ygeman, Sweden’s Minister of Energy and Digital Development, at the Telia Company 5G launch in Stockholm.

……………………………………………………………………………………………………………………………………………………

Having already partnered successfully on 5G in Sweden – including enabling the country’s first live 5G network at the KTH Royal Institute of Technology and partnering with Volvo to operate Sweden’s first industrial 5G network – Telia selected Ericsson as its 5G partner for the launch network. Ericsson President and CEO, Börje Ekholm, said 5G will transform Swedish life, society and business for the better.

Earlier this month Telia’s sister company Telia Norway also launched its first commercial 5G services, with Ericsson as its sole 5G RAN supplier.

Allison Kirkby, CEO of Telia, said in a press release: “Our networks have never been more important to lives and livelihoods, than now. Telia’s 5G launch lays the foundations for the next phase of digital transformation, with innovation, sustainability, and security as three critical pillars, and we are proud to be doing this launch in partnership with Ericsson.”

Kirkby continued “As we roll-out 5G across Sweden, we will open up new user experiences and accelerated innovation in areas such as entertainment, healthcare, manufacturing, and transport, that will collectively strengthen and protect everyone living and working in Sweden, and Swedish competitiveness in the world.”

Telia’s 5G network is due to power most of Stockholm’s city center by June 21, and its private customers that are within range and have a 5G-ready smartphone and Jobbmobil contract will be able to enable the new 5G network. Moreover, its network is run 100% on renewable energy certified by the Swedish Society for Nature Conservation.

5G launches are scheduled for later in the year in other major cities in Sweden including Gothenburg and Malmö.

References:

https://interestingengineering.com/sweden-sets-up-first-5g-network-with-its-major-telecom-companies

https://www.tele2.com/about/who-we-are/tele2-5g

https://www.telecompaper.com/news/tele2-telia-and-3-sweden-announce-5g-networks-launches–1339788

https://www.teliacompany.com/en/news/news-articles/2018/swedens-first-5g-network-goes-live/

COVID-19 has changed how we look at telecom infrastructure, cloud and AI

by John Strand, Strand Consult, Denmark; edited for clarity by Alan J Weissberger

The coronavirus (COVID-19) crisis has proven that telecom infrastructure is critically important. Telecommunications networks delivered service during the lockdown, enabling many to continue to work, learn, shop, and access healthcare.

Policymakers will likely revisit regulation for telecom networks, not only to optimize network investment, but to improve security. Indeed, policymakers will also realize that security which has focused to date on the transport layer of networks is leaving the access and applications layers vulnerable.

While the focus on Huawei is long overdue, the discussion of network security and Huawei’s role are oversimplified. It is insufficient to address only one aspect of conventional components of networks: access, core, and transport.

The bigger issues are how end-user data will be protected while stored in the network/cloud and processed by artificial intelligence (AI) agents? Also, how will connected devices on Internet of Things (IoT) networks and other applications (such as smart city solutions) can be secured?

Historically network connectivity was likened to the dumb pipe, the medium which transmits data. The “smart parts” of the network were the edge and the core, where users access networks and where information processing occurs. These actions have become more complex with third party providers of AI and cloud computing. Naturally, these models don’t fit 5G because intelligence must exist throughout the network. However, telecom regulation has been associated with these three traditional functions.

Now that networks have evolved, it’s time for telecom regulation to evolve. If the goal of security measures is to reduce the risk and vulnerability of exposure to Chinese state-owned and affiliated firms, then policymakers need holistic frameworks that address the multiple aspects of network security at its various layers: application, transport, and access.

Indeed, the singular focus on Huawei in connectivity misses the fact that Huawei sells products for the other layers, and that many other Chinese state-owned firms should be scrutinized. For example, Baidu, WeChat, Alibaba, and Huawei provide AI solutions in the Applications layer; Huawei and ZTE in transport; and Huawei smartphones and laptops by Lenovo (the world’s leading maker of laptops as well as a leader in servers).

Strand Consult has described this in the research note The debate about network security is more complex than Huawei. Look at Lenovo laptops and servers and the many other devices connected to the internet.

The EU’s 5G Toolbox is the first step towards greater security and accountability for a discrete part of 5G network transport, but it does not address all elements of 5G security nor other layers. In performing its security assessment, the United Kingdom looked beyond 5G mobile Radio Access Networks (RAN) and Core to other network layers, types and technology, notably wireline networks. Policymakers need a broader focus than 5G when assessing the security of telecommunications networks in the future. Policymakers need to look at Huawei’s movement into cloud and AI solutions in the application layer as well as the many state-owned Chinese firms in the access layer like Lenovo.

In China, Huawei is vertically integrated and delivers a suite of products and services for all the layers of a network: it transports the data; it provides access through end user devices, and it provides the applications in the form of AI and cloud solutions. While European policymakers debate issues of RAN and core, Huawei is busy selling other solutions for the rest of the network: smartphones, routers, AI, and cloud solutions. As restrictions tighten on Huawei’s network products, the company will naturally push other business lines to compensate for lost revenue. A large operator in Europe works with Huawei on a joint Chinese-German cloud platform, and the reference customer for this solution is the European Organization for Nuclear Research, CERN in Switzerland. It is not logical how Huawei which can be deemed high risk for telecommunications and military networks, but somehow neutral for nuclear research. The agreement for the project is four years old; the question is whether such a project will be acceptable for political and security standards going forward.

Vertical integration was the standard model for traditional state-owned telecommunications. The government built a telephone network (the wires and switches); it delivered a single service – telephony; and it sold the end user device, typically a classic phone. Privatizing networks was about opening up the value chain to different kinds of providers. This worked well in mobile networks; different firms specialized for different parts of the value chain. However, Huawei is driving the decentralized chain back to the state-centered concept, perhaps fitting for its practice in China where it partners with the government to deliver full-service surveillance solutions.

Policymakers, regulators, and competition authorities have long been skeptical of vertical integration in telecommunications, and it was frequently a way to control traditional telecom operators by demanding that the divest certain parts of their business or by prohibiting certain acquisitions.

COVID-19 has proven that telecommunications networks are vital infrastructure at all layers and levels. It’s not just military and public safety networks that need to be secure. Everyone needs to have secure networks if we are live in a digital society. If politicians and telecom operators don’t recognize this, network users do. Change is being driven by companies which themselves are increasingly victims of cyber-attacks. Companies are putting increased pressure on telecom operators and governments to do more to make networks secure.

John Strand of Strand Consult

…………………………………………………………………………………………………………………..

Six big issues on the future of telecom regulation:

Strand Consult believes that governments will take a broader view about network security. Here are six categories of issues for policymakers to consider.

- What is critical infrastructure, and how will it be defined in the future? Historically, critical infrastructure had to do with physical and digital network assets which are required for physical and economic security, health, and safety. Indeed, there are many vital network assets deemed “critical” including those for chemicals, communications, manufacturing, dams, defense, emergency services, energy, financials, food/agriculture, government facilities, healthcare, information technology, nuclear reactors, transportations systems, and water/wastewater. Are these networks equally prioritized? What are the security concerns and protocols for each, both on the physical and cyber fronts? Do some have greater security than others? How does this change in the COVID-19 world?

- What are the government’s responsibilities to ensure the security of communications infrastructure?What are the minimum requirements to restrict a vendor? How is this balanced with requirements for fair and open processes for bids and tenders?

- What are the relevant communications networks to secure? Is it enough to focus on 5G mobile RAN and core or should security requirements apply to wireline networks, satellite, Wi-Fi, 3G/4G and so on?

- Is it sufficient only to address the transport element of network security? How will security be ensured for the storage and processing of data, for example on the computers, laptops, and servers provided by Chinese state-owned Lenovo where China’s rules for surveillance and espionage also apply? What about apps like TikTok and Huawei’s AI and cloud solutions?

- Who should perform the security assessment? Telecom operators, military departments, intelligence agencies, private security consultants, law enforcement, or some other actor?

- How will shareholders account for increased security risk in networks? Have shareholder asked relevant questions about operators’ security practices and the associated risk?

Strand Consult believes it is dangerous for telecom operators to make the decision about Huawei themselves without involving the authorities.

There are a lot of arguments for why telecommunications companies should involve the competent and relevant authorities. Telecom operators must understand that If telecommunications companies assume responsibility as those who assess each supplier in relation to national security, they will be held responsible when things go wrong.

When you take on a responsibility, you also take on risk. Thus, shareholders are exposed to increasing risk when using high risk vendors. The historical facts show that telecommunications companies have been wrong in the past when assessing cooperation with partners which have proven to be corrupt. Some partnerships have cost shareholders billions of euros. In practice, operators are limited in their ability to judge whether partners and vendors are trustworthy.

Strand Consult’s research shows that is not only government, intelligence, and security officials who are concerned about companies like Huawei. Nor is it just telecom operators which build and run networks. It is the small, medium, and large enterprises that use networks that fear that their valuable data will be surveyed, sabotaged, or stolen by actors associated with the Chinese government and military. Consequently, it is the clients of telecom operators which push to restrict Chinese made equipment from networks. This is described in this research note, The pressure to restrict Huawei from telecom networks is driven not by governments, but the many companies which have experienced hacking, IP theft, or espionage.

What the future looks like – just ask the banks:

If you want to see the future of the telecom industry, look at what happened with banking. European banks have been required to implement Anti-Money Laundering (AML) and the Counter Terrorist Financing (CFT). About 10% of European banks employees are today working with compliance. Telecom authorities, defense officials, and other policymakers and will likely see cybersecurity is vital for Europe and that telecom infrastructure is critically important. So just as the banks have been put under a heavy regulatory regime to address corruption and financial crimes, the telecom industry will be required to implement deterrence of cyberattacks.

In practical terms, the authorities in the EU and in each nation state will likely make some demands that challenge the network paradigm that telecommunications companies operate today. The rules will likely be so rigid that they will effectively eliminate Huawei and other Chinese companies from being vendors without making explicit bans. However, it won’t be governments alone driving the charge. Corporate customers of telecom networks, companies that have experienced hacking, IP theft, or espionage, will also join the effort. This is described in this research note, The biggest taboo in European telecom industry is the cost of cybersecurity – just ask the banks.

Copyright 2020. All rights reserved

………………………………………………………………………………………………

About Strand Consult:

Strand Consult, an independent company, produces strategic reports, research notes and workshops on the mobile telecom industry.

For 25 years, Strand Consult has held strategic workshops for boards of directors and other leaders in the telecom industry. We offer strategic knowledge on global regulatory trends and the experience of operators worldwide packaged it into a workshop for professionals with responsibility for policy, public affairs, regulation, communications, strategy and related roles.

Learn more about John Strand: www.understandingmobile.com

Learn more about Strand Consult: www.strandreports.com

Strand Consult

Gammel Mønt 14

Copenhagen 1117 K

Denmark

[email protected]

U.S. Government on 5G Integrated and Open Networks + ATIS on U.S. 6G Leadership

In a speech he was scheduled to deliver (but didn’t) Thursday at a Global CTO Roundtable on 5G Integrated and Open Networks (ION), U.S. Attorney General William Barr wrote (bold font added):

The United States and our partners are in an urgent race against the People’s Republic of China (PRC) to develop and build 5G infrastructure around the world. Our national security and the flourishing of our liberal democratic values here and around the world depend on our winning it.

Future 5G networks will be a critical piece of global infrastructure, the central nervous system of the global economy. Unfortunately, the PRC is well on its way to seizing a decisive 5G advantage. If the PRC wins the 5G race, the geopolitical, economic, and national security consequences will be staggering. The PRC knows this, which explains why it is using every lever of power to expand its 5G market share around the globe. The community of free and democratic nations must do the same.

To compete and win against the PRC juggernaut, the United States and its partners must work closely with trusted vendors to pursue practical and realistic strategies that can turn the tide now. Although the ‘Open RAN’ approach is not a solution to our immediate problem, the concept of Integrated and Open Networks (ION), which was the topic of yesterday’s roundtable, holds promise and should be explored. We can win the race, but we must act now.

From Mung Chiang of the U.S. Office of Science and Technology Advisor:

With a broad, inclusive tent of what “open” means, a nuanced appreciation of network deployment reality, and a more solid view on architectural choices, ION becomes one of the areas where the United States and partner countries can lead in 5G innovation. We invite technology leaders in the industry to help make that happen. Speed is the key to winning the 5G race.

While technology should not be mistaken as a solution to the fundamental problem of a distorted market, its exploration is still useful. ION and Edge Computing, for example, are two areas of innovation to realize 5G’s promise of a new level of responsiveness and scale. Such innovation leadership, along with the Clean Networks initiative and supply chain security form three prongs in a global strategy for 5G.

………………………………………………………………………………………………………………………………………………….

Separately, the Alliance for Telecommunications Industry Solutions (ATIS) has issued a call to action to promote U.S. 6G leadership.

“While innovation can be triggered in reaction to current market needs, technology leadership at a national level requires an early commitment and development that addresses U.S. needs as well as a common vision and set of objectives,” said Susan Miller, President and CEO of ATIS, possibly in acknowledgement of the panic the U.S. has got itself into over 5G and of recent developments in China.

………………………………………………………………………………………………………………………………………………….

Comment, analysis and assessment:

Mobile standards are global in nature, so talk of regional races seems disingenuous if not counter-productive. It is bad enough that there are six competing IMT 2020 RITs (Radio Interface Technologies) from five different countries/regions being progressed by ITU-R WP5D for IMT 2020.specs with three based on 3GPP 5G NR (Release 15 and 16): China, Korea, India (TSDSI). In addition to 3GPPs RIT/SRIT submissions (from ATIS), there are also the DECT/ETSI IMT 2020 RIT submission based on DECT NR and the Nufront (Chinese company) submission based on their own 5G radio which supposedly supports ultra low latency.

What Attorney General Barr probably means is that he’s worried U.S. 5G networks are going to be second rate compared to the Chinese equivalent from Huawei and ZTE. However, he said that Open RAN is NOT a solution to the U.S.’ current “5G problem.” Barr and Ms Chiang say that ION is a more viable approach (what the *&^%$** is ION?). In particular, “ION becomes one of the areas where the United States and partner countries can lead in 5G innovation.”

Telecoms.com author Scott Bicheno wrote: “Any non-Chinese telecoms company with a few bright ideas would be well advised to stick close to the U.S. government as the public money tap seems to be well and truly open.”

References:

https://www.state.gov/remarks-at-global-chief-technology-officers-roundtable-on-5g-ion/

India telecom revenue to slow through March 2021; 5G spectrum auction delayed yet again

Revenue and profit growth at Indian telecom operators during the financial year ending March 2021 will slow due to lower data growth and weaker economic activity amid the coronavirus pandemic, according to Fitch Ratings.

Mobile service EBITDA will increase by about 15 percent in fiscal 2021 from 25 percent in fiscal 2020, as the industry will realise the full-year benefit of industry-wide tariff hikes of around 30 percent, effective from December 2019.

India telecom operators’ Q4FY2020 EBITDA growth was driven by tariff hikes and 4G data growth, which will decelerate in FY2021, as lockdowns were only implemented from 24 March 2020, Fitch Ratings reported.

Market leader, Reliance Jio, a subsidiary of Reliance Industries Ltd, reported sequential revenue and EBITDA growth of 6% and 11%, respectively, as ARPU growth was less pronounced, at 2%, to INR 131. This was due to the significant proportion of Jio’s customers being on long-tenor plans, on which tariff hikes will be implemented only in 1QFY21. In addition, sale of incremental Jiophones led to slower growth in ARPU. Its monthly data and voice usage per user was at 11.3GB and 771 minutes, respectively. Jio continued to gain market share at the expense of India’s third-largest telco, Vodafone-Idea Limited, as it added 18 million subscribers to reach a customer base of 388 million, the industry’s highest. We expect Jio’s FY21 mobile revenue to increase by at least 20%, led by higher monthly ARPU of INR147 and subscriber additions of 30 million (FY20: 80 million).

Bharti Airtel’s Indian mobile segment’s EBITDA will improve by 15-20 percent, on lower data growth, as smartphone sales are likely to drop significantly in 1HFY21 as feature-phone users are unable to upgrade to 4G smartphones during the lockdowns.

Airtel will be adding around 15 million new subscribers in fiscal 2021 as compared with the earlier prediction of 30 million, as users are unable to port their numbers during the lockdowns.

The pandemic-led economic slowdown will mostly affect lower-revenue users – those who spend INR 50-100 a month – which could prevent further improvements in monthly average revenue per user (ARPU), Fitch Ratings said.

Bharti Airtel management, headed by India CEO Gopal Vittal, is confident that the pandemic will have limited impact on FY21 EBITDA growth, which it forecasts to be at least 25 percent as compared with 25 percent in FY20, supported by ARPU growth to INR 170-175 a month.

Management says that data growth has increased by 20-25 percent in the short-term as users work from home and upgrade to higher-ARPU plans.

Airtel will generate small positive free cash flow in FY21, as Capex / revenue is likely to decline to around 26-27 percent on lower core Capex, interest costs and the government’s two-year moratorium on the payment of existing spectrum dues, which will defer about $840 million in each of FY21 and FY22.

Airtel has almost completed the shutdown of its 3G network across India and has redirected its 900MHz and 2100MHz spectrum for 4G usage. Telecom sector Capex peaked in 2019, as both Airtel and Jio front-laded Capex to expand 4G coverage and capacity and invested in fibre networks and in-building coverage.

Revenue market share is consolidating fast at Jio and Bharti, with Vodafone Idea rapidly losing market share. Vodafone Idea lost about 131 million subscribers in the last six quarters and is struggling to service its debt due to stagnant EBITDA generation, which is insufficient to cover its interest costs. The telco’s subscriber base is shrinking due to its deteriorating network on limited capex. Vodafone Idea has paid only USD 926 million in adjusted gross revenue dues, against the department’s demand of USD 6 billion, and has not yet reported its 4QFY2020 results.

……………………………………………………………………………………………………………………………….

5G Auction to be Delayed:

Fitch Ratings believes a 5G spectrum auction looks increasingly improbable in 2020 in light of incumbent telcos’ limited financial flexibility, a high base price of USD 7 billion for pan-India 5G spectrum in 3.3GHz-3.6GHz bandwidth and a limited business case for 5G, when 4G penetration is only around 50%. Bharti and Vodafone Idea have publicly stated that they will not participate in 5G auctions at such high prices.

A report in The Economic Times of India claims that the government will go ahead with the auction of additional 4G spectrum as planned, later this year but will defer the 5G spectrum sale until 2021.

Bharti Airtel and Vodafone Idea, who were both hit with multi-billion dollar AGR dues by the country’s Supreme Court last October, have both called for the auction to be delayed, as they battle to rein in expenses.

Sources familiar with the matter told journalists at The Economic Times of India that the country’s Digital Communications Commission had met on Monday to discuss postponing the 5G auction.

“Discussions are on to hold the 5G auctions later as some of the telcos need to buy spectrum but 5G may not be the priority now,” a source told the ET.

Light Reading reports that all the Indian telecom providers (including Reliance Jio, Airtel and Vodafone Idea) have asked the government to lower the high base price for 5G spectrum. Airtel says it will not participate in the auction at the current reserve prices. The Department of Telecommunications has attached a base price of INR4.92 billion ($64.9 million) per MHz to spectrum in the 5G band.

Besides the negative effects of the COVID-19 pandemic, another possible reason for India postponing the sale of 5G spectrum is the deteriorating financial position of the telcos. That makes it unlikely the government would generate decent proceeds from the sale of 5G spectrum at this time. A recent court ruling about fees the telcos owe the government has further harmed their financial health, making it harder for them to participate in the auction.

Equally important is that the 5G ecosystem is far from developed. The lack of “use cases” [1.] for the new technology means telcos are unable to justify the high spectrum costs to investors. This was the main reason Vodafone Idea gave when it pushed for a reduction in fees.

Note 1.: The important 5G use cases of Ultra High Reliability and Ultra Low Latency will not be realized anytime in 2021 as it is only 27% complete at this time in 3GPP Release 16. You can’t implement something which hasn’t been specified yet!

………………………………………………………………………………………………………………………………………………..

India to Miss “5G Bus”:

Muntazir Abbas wrote in a May 23rd ETTelecom post:

India is set to miss the ‘5G bus‘ following the lack of preparedness, unavailability of sufficient spectrum, absence of encouraging use cases, and uncertainty around radiowaves sale for the next generation of telecom services.“The Department of Telecommunications (DoT) is yet to form relevant study groups and revise the National Frequency Allocation Plan (NFAP) 2018 to include more bands including mmWave frequencies as a part of 5G roadmap,” an industry executive aware of the developments said.

In the past, Prime Minister Narendra Modi-led government maintained that it “won’t afford to miss 5G bus” like in the case of 2G, 3G, and 4G technologies that were deployed in India way later than many countries.

The executive further said that the quantum of spectrum availability in the 3300 – 3600 Mhz range also remains uncertain, while the department has not sought views on 26 GHz from the regulator despite agreeing to its viability for the commercial launch of fifth-generation or 5G networks.

The India government-backed high-level 5G Forum headed by the Stanford University Professor Emeritus AJ Paulraj anticipated the first 5G commercial launch by 2020, while suggesting that most guidelines on regulatory matters be promulgated by March 2019 to facilitate early 5G deployment. That will clearly not happen!

India government authorities have yet to decide whether the 5G market is open to Chinese vendors Huawei and ZTE. Huawei has been banned from several countries, including Australia and the U.S,, over security concerns. Initially, Chinese vendors were not invited to participate in India’s 5G trials, although this was later changed. Now, India’s government is under immense pressure from the US to ban Huawei.

The current backlash against China over coronavirus, which originated in the Chinese city of Wuhan, makes the decision even harder for India’s government. That lack of clarity may have been the main factor in the postponement of the 5G auction, said Gagandeep Kaur, contributing editor to Light Reading

References:

https://www.lightreading.com/asia/india-postpones-5g-spectrum-sale-to-2021/d/d-id/759852?

https://www.telecomlead.com/4g-lte/india-telecom-revenue-will-face-slow-growth-fitch-ratings-95298

Omdia: High-speed data-center Ethernet adapter market at $1.7 billion in 2019

Executive Summary:

The market for Ethernet adapters with speeds of 25 gigabits (25GE) and faster deployed by enterprises, cloud service providers and telecommunication network providers at data centers topped $1 billion for the first time in 2019, according to Omdia.

The total Ethernet adapter market size stood at $1.7 billion for the year. This result was in line with Omdia’s long term server and storage connectivity forecast. Factors driving that forecast include the growth in data sets, such as those computed by analytics algorithms looking for patterns, and the adoption of new software technologies like AI and ML which must examine large data sets to be effective, driving larger movement of data.

“Server virtualization and containerization reached new highs in 2019 and drove up server utilization. This increased server connectivity bandwidth requirements, and the need for higher speed Ethernet adapters” said Vlad Galabov, principal analyst for data center IT, at Omdia. “The popularization of data-intensive workloads, like analytics and AI, were also strong drivers for higher speed adapters in 2019”

25GE Ethernet adapters represented more than 25 percent of total data-center Ethernet adapter ports and revenue in 2019, as reported by Omdia’s Ethernet Network Adapter Equipment Market Tracker. Omdia also found that the price per each 25GE port is continued to decline. A single 25GE port cost an average of $81 in 2019, a decrease of $9 from 2018.

Despite representing a small portion of the market, 100GE Ethernet adapters are increasingly deployed by cloud service providers and enterprises running high-performance computing clusters. Shipments and revenue for 100GE Ethernet adapter ports both grew by more than 60 percent in 2019. Each 100GE adapter port is also becoming more affordable. In 2019, an individual 100GE Ethernet adapter port cost $321 on average, a decrease of $34 from 2018.

“Cloud service providers (CSPs) are leading the transition to faster networks as they run multi-tenant servers with a large number of virtual machines and/or containers per server. This is driving high traffic and bandwidth needs,” Galabov said. “Omdia expects telcos to invest more in higher speeds going forward—including 100GE—driven by network function virtualization (NFV) and increased bandwidth requirements from HD video, social media, AR/VR and expanded IoT use cases.”

The Ethernet outlook:

Omdia expects Ethernet adapter revenue to grow 21 percent on average each year through 2024. Despite the COVID-19 lockdown, the Ethernet adapter market is set to remain close to this growth curve in 2020.

Ethernet adapters that can provide complete on-card processing of network, storage or memory protocols, data-plane offload or that can offload server memory access will account for half of the total market revenue in 2020, or $1.1 billion. Ethernet adapters that have an onboard field customizable processor such as a field-programmable gate array (FPGA) or system on chip (SoC), will account for slightly more than than a quarter of 2020 adapter revenue, totaling $557 million. Adapters that only provide Ethernet connectivity will make up a minority share of the market, at just $475 million.

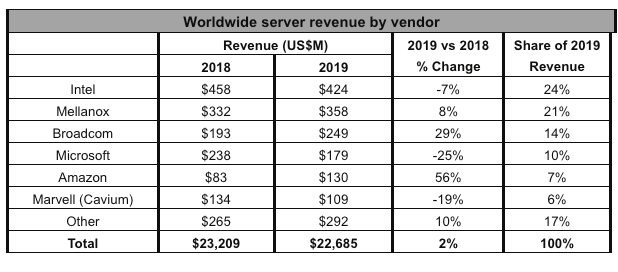

Intel maintains lead:

Looking at semiconductor vendor market share, Intel held 24 percent of the 2019 Ethernet adapter market, shipping adapters worth $424 million in 2019. This represents a 2.5-point decrease from 2018 that Omdia attributes to the aging Intel Ethernet adapter portfolio which consists primarily of 1GE and 10GE adapters with Ethernet connectivity only. Intel indicated it will introduce adapters with offload functionality in 2020 that will help it remain competitive in the market.

Mellanox (now part of NVIDIA) captured 21 percent of the 2019 Ethernet adapter market, a 1-point increase compared to 2018. The vendor reported strong growth of its 25GE and 100GE offload adapters driven by strong cloud service provider demand and growing demand among enterprises for 25GE networking.

Broadcom was the third largest Ethernet adapter vendor in 2019, commanding a 14 percent share of the market, an increase of 3 points from 2018. Broadcom’s revenue growth was driven by strong demand for high-speed offload and programmable adapters at hyperscale CSPs.

In 2019, Microsoft and Amazon continued to adopt in-house-developed Ethernet adapters. Given their large scale and the high value of their high-speed offload and programmable adapters, the companies cumulatively deployed Ethernet adapters worth over $300 million. This made them the fourth and fifth largest makers of Ethernet adapters in 2019. As both service providers deploy 100GE adapters in larger numbers in 2020, they’re set to remain key trendsetters in the market.

Amazon AWS and Microsoft Azure continued to use in-house-developed Ethernet adapters. Given their large scale and the high value of their high-speed offload and programmable adapters, the companies cumulatively deployed Ethernet adapters worth over $300 million, according to Omdia. This made Microsoft and Amazon, respectively, the fourth and fifth largest makers of Ethernet adapters in 2019. As both service providers deploy 100GE adapters in larger numbers in 2020, Omdia expects them to continue to be key trendsetters in the market going forward.

About Omdia:

Omdia is a global technology research powerhouse, established following the merger of the research division of Informa Tech (Ovum, Heavy Reading and Tractica) and the acquired IHS Markit technology research portfolio*.

We combine the expertise of over 400 analysts across the entire technology spectrum, analyzing 150 markets publishing 3,000 research solutions, reaching over 14,000 subscribers, and covering thousands of technology, media & telecommunications companies.

Our exhaustive intelligence and deep technology expertise allow us to uncover actionable insights that help our customers connect the dots in today’s constantly evolving technology environment and empower them to improve their businesses – today and tomorrow.

………………………………………………………………………………………………………………………………………………..

Omdia is a registered trademark of Informa PLC and/or its affiliates. All other company and product names may be trademarks of their respective owners. Informa PLC registered in England & Wales with number 8860726, registered office and head office 5 Howick Place, London, SW1P 1WG, UK. Copyright © 2020 Omdia. All rights reserved.

*The majority of IHS Markit technology research products and solutions were acquired by Informa in August 2019 and are now part of Omdia.

Fastest 5G network in the U.S.? T-Mobile vs Verizon; Nokia’s fastest 5G claim

T-Mobile’s Salim Kouidri tweeted on Tuesday (see below) that their 5G network in New York City recently hit 1G bit/sec download speeds, at least in one recent test. Surprisingly, that 1 Gig connection didn’t even make use of T-Mobile’s low-band or millimeter wave (mmWave) spectrum holdings.

Salim Kouidri@salimkouidriA big milestone was achieved today @TMobile NYC. The team recorded a 1 Gigabit/s speed test on our newly launched 2.5Ghz 5G network in Manhattan @NevilleRay @MikeSievert #layercake #nationwide5G #wewontstop

- N41 (the 2.5GHz spectrum T-Mobile acquired from Sprint)

- B66 (the AWS spectrum T-Mobile is using to broadcast both 5G and 4G using EN-DC technology)

- And Band 46 (the unlicensed 5GHz band that T-Mobile is using to deploy LAA technology)

Therefore, the operator’s 1Gbit/s 5G connection didn’t even make use of T-Mobile’s low-band or high-band, mmWave spectrum holdings. Moreover, T-Mobile officials have said the operator is initially deploying only 60MHz of the roughly 150MHz it now owns in the 2.5GHz band. The inclusion of transmissions in those additional bands would undoubtedly increase users’ download speeds.

Although Australia’s Telstra, all three of South Korea’s operators, Sprint in the U.S. and the U.K.’s EE and Vodafone have all deployed 5G on mid-band spectrum, users’ speeds differed greatly from well over 200 Mbps on all three Korean operators, to 114.2 Mbps on Sprint. In part, this speed difference is because of the amount of 5G spectrum available to deploy — wider channels are better, ideally 100Mhz in a single 5G band — but it’s also due to other differences in the networks such as the capacity of the onward connection from each cell site or the performance of each operator’s core network.

As the new T-Mobile combines the assets of Sprint, we expect to see the average 5G speed of new T-Mobile users rising as they benefit from the mid-band 5G spectrum which Sprint has deployed.

The record speed was achieved by combining eight 100 MHz channels of millimeter wave spectrum on the 28 GHz and 39GHz bands, providing 800 MHz of bandwidth, and 40 MHz of LTE spectrum using the EN-DC functionality available on Nokia’s AirScale solution. EN-DC allows devices to connect simultaneously to 5G and LTE networks, transmitting and receiving data across both air-interface technologies. This means devices can achieve a higher throughput than when connecting to 5G or LTE alone. The speeds were achieved on both 5G cloud-based (vRAN) and classic baseband configurations.

Nokia’s AirScale Radio Access is an industry-leading, commercial end-to-end 5G solution enabling operators globally to capitalize on their 5G spectrum assets. It offers huge capacity scaling and market-leading latency and connectivity by enabling all air-interface technologies on the same radio access equipment.

Stéphane Téral, Chief Analyst at LightCounting Market Research, said: “This is a substantial achievement that reflects the careful workings of a brilliant and subtle team with the deepest appreciation for detail and circumstance. In other words, 8-component carrier aggregation in the millimeter wave domain shows the world that there is more than massive MIMO and open RAN to not only truly deliver the promise of commercial 5G, but also pave the way for future Terahertz system.”

Tommi Uitto, President of Mobile Networks at Nokia, commented: “This is an important and significant milestone in the development of 5G services in the U.S., particularly at a time when connectivity and capacity is so crucial. It demonstrates the confidence operators have in our global end-to-end portfolio and the progress we have made to deliver the best possible 5G experiences to customers. We already supply our mmWave radios to all of the major U.S. carriers and we look forward to continuing to work closely with them moving forward.”

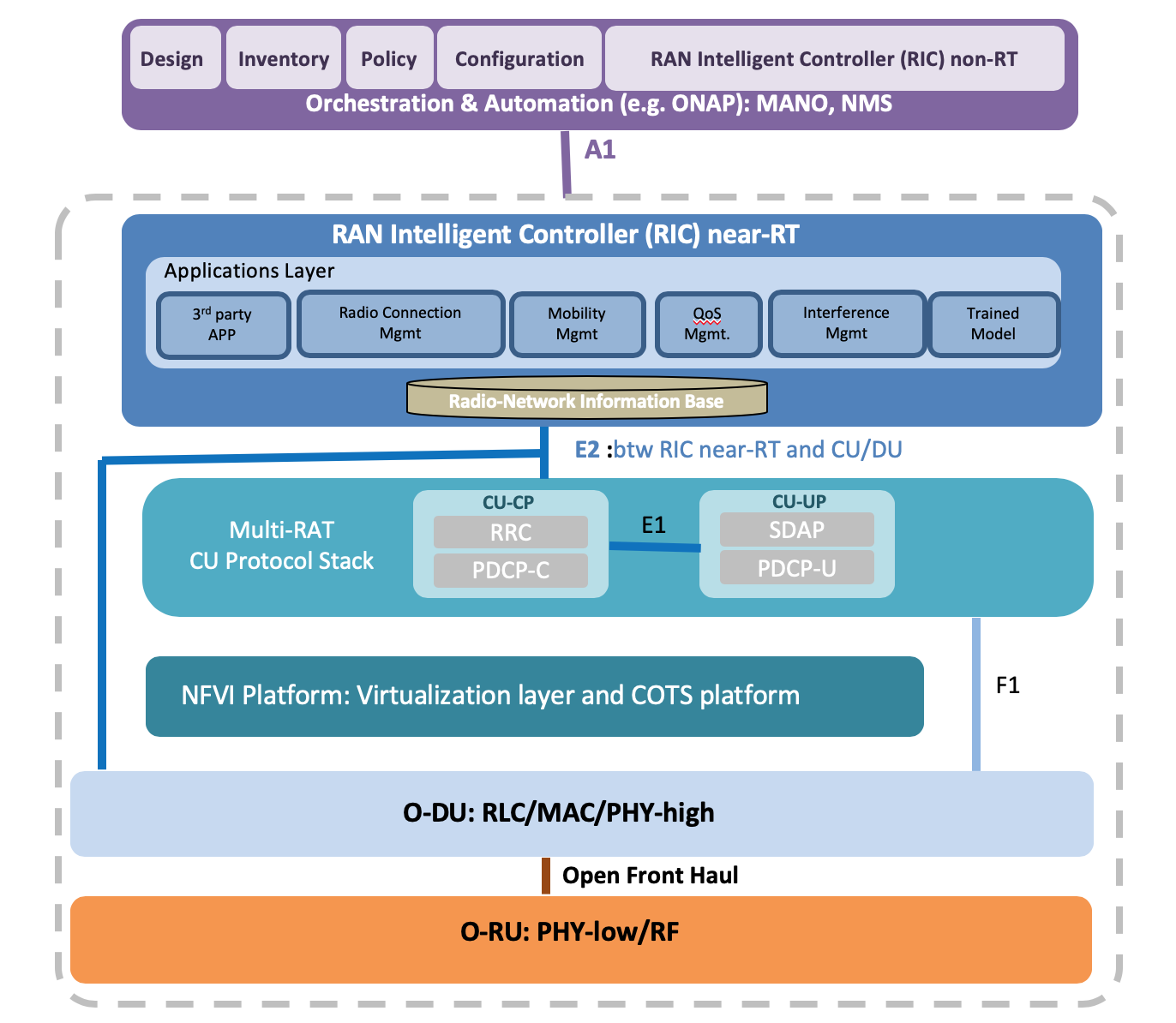

Altiostar testing O-RAN Compliant 5G Massive MIMO with NEC and Rakuten Mobile

Altiostar announced testing of massive MIMO 5G over a virtual Radio Access Network (vRAN) in collaboration with NEC and Rakuten Mobile. The tests aim to ensure interoperability of multi-vendor systems based on the open RAN specifications from the O-RAN alliance.

Open RAN Layered Architecture from the O-RAN Alliance

……………………………………………………………………………………………………………………………….

Altiostar is integrating the O-RAN Distributed Unit (O-DU) functionality of its virtual radio access network (vRAN) software with NEC’s O-RAN Radio Unit (O-RU) using fully compliant control, user, synchronization and management (C/U/S/M) plane protocols based on O-RAN Alliance guidelines. The 5G layer is built using container network functions (CNF) that leverage Rakuten Mobile’s cloud infrastructure platform that is part of its 4G network build out.

As part of management-plane integration, Altiostar is following a hierarchical model that allows the O-DU software to manage the NEC O-RU, including providing software upgrades, RU configuration, fault management and performance monitoring. This interoperability is being performed for 5G new radio (NR) sub-6 GHz massive MIMO O-RU and meets all the 3GPP downlink/uplink (DL/UL) requirements.

Altiostar says they have “pioneered RAN disaggregation since 2013 when it first introduced a split between the higher non-real-time layers of the protocol stack and the lower layers of the stack. The industry then standardized this concept in the 3GPP and what is now known as the option-2 split between the centralized unit and the distributed unit. This paved the way for operators to think differently when it comes to disaggregation and network deployment,” according to Altiostar.

Further disaggregation was introduced by Altiostar in the form of a radio interface unit. The RIU incorporates lower L1 functionality and provides a gateway function that converts Common Public Radio Interface to/from Ethernet. By eliminating the high bandwidth and proprietary CPRI interface to the radio, Altiostar took a key step towards integrating legacy Remote Radio Head over an Ethernet transport network to O-DU functionality.

Using this technology, the first multi-vendor RAN was deployed at a commercial scale and paved the way for operators to engage radio vendors to build O-RAN compliant radios. Rakuten Mobile’s adoption of the platform has helped move forward the ecosystem and open interfaces in the industry.

“Open RAN as a concept is one that the whole industry is now actively pursuing as a means to introduce supply chain diversity into mobile networks globally,” said Ashraf Dahod, CEO of Altiostar Networks. “Altiostar is leading the industry with this network transformation by ensuring interoperability, integration and most importantly extensive testing to ensure that we have a commercial, carrier-grade solution for both 4G and 5G while keeping the principles of Open RAN in place.”

“Rakuten Mobile is a big supporter of O-RAN principles and has seen the benefit of supply chain diversity in our own network,” said Tareq Amin, Representative Director, Executive Vice President and Chief Technology Officer of Rakuten Mobile. “By combining the spectral efficiency of massive MIMO along with an advanced cloud-based RAN, we are leveraging and introducing advanced innovative technology from both NEC and Altiostar, who are specialists in these respective fields.”

…………………………………………………………………………………………………………………………………..

References:

Verizon misleading 5G commercials called out by NAD after AT&T complaint

The National Advertising Division (NAD) has condemned Verizon for misleading consumers over the quality of its 5G network across the country. NAD recommended Verizon stop using the claim that it’s delivering “the most powerful 5G experience for America” in two previously aired TV commercials touting the carrier’s 5G service rollout in sports stadiums were challenged by 5G competitor AT&T.

Editor’s Note: NAD is an investigative unit of the advertising industry’s system of self-regulation and is a division of the BBB National Programs’ self-regulatory and dispute resolution programs.

……………………………………………………………………………………………………………………………………………….

“The National Advertising Division has determined that, in the context of two challenged television commercials touting Verizon’s rollout of 5G service in sports venues, the claim that ‘Verizon is building the most powerful 5G experience for America’ reasonably communicates a message about the consumer experience of using 5G mobile service that was not supported by the evidence in the record,” according to statement from NAD.

The message is apparently that Verizon was not fairly representing its network in advertisements and promotions broadcast at sporting venues.

Verizon plans to appeal the ruling to the National Advertising Review Board.

……………………………………………………………………………………………………………………………….

Verizon is building 5G networks in sporting venues across the U.S., though the NAD believes the way the advertisements have been created suggests a similar experience would be offered outside the sports venues themselves.

The express claim stated in the ads is that “Verizon is building the most powerful 5G experience for America,” a message the carrier indicated is clear to consumers, despite NAD’s finding that Verizon’s use of past and present tense conveys the message that it currently delivers the most powerful 5G experience.

“The intent of the commercial is to inform consumers about the billions of dollars Verizon is investing in its 5G buildout. Verizon strongly believes that consumers understand that this is the only message that is reasonably conveyed,” said Verizon in its advertiser’s statement.

NAD pointed to wording like “This is happening now,” for the NFL spots and said Verizon’s “unqualified superiority claim…goes beyond touting Verizon’s spectrum portfolio.” Instead, sending the message of 5G consumer experiences that include capacity to serve many people at once and using Verizon’s 5G network to post content, along with resilience, coverage and latency – which NAD said Verizon didn’t provide sufficient evidence to support its present tense “most powerful network” claim.

Based on the context, one commercial the NAD release appears to be referring to is a Verizon NFL 5G Built Right ad, which Jeffrey Moore, principal at Wave7 Research, confirmed ran heavily in September 2019 in line with the start of NFL season and stopped airing November 18.

“5G branding efforts from Verizon, AT&T, and T-Mobile shifted to pandemic-related branding, showing that Verizon, AT&T, and T-Mobile are doing what they can to keep customers connected and safe,” Moore told Fierce Wireless.

Verizon announced last September it was expanding 5G service to 13 NFL stadiums. Given current restrictions on large public gatherings in many places though, it’s unclear when ads depicting massive crowds might come back into favor.

…………………………………………………………………………………………………………..

U.S. based wireless telcos are facing a difficult challenge in delivering the desired “5G experience.” Despite the telcos preaching about the benefits of mmWave spectrum to underpin 5G networks, the telcos are performing woefully according to many critics/pundits.

T-Mobile has been blasted for the speeds which have been delivered over the 600 MHz spectrum it has been offering, while AT&T and Verizon has been failing at coverage. In a recent Rootmetrics gaming study in Los Angeles, none met the minimum requirements for latency.

Moore noted that Metro By T-Mobile’s “Rule Your Day” campaign, was halted for a period, but restarted May 6. On the postpaid side, T-Mobile’s message for a time was “We’re with you,” but has now returned to the tagline of “Are you with us?”

This “slap on the wrist” by NAD implies that the U.S. is failing to even come close to meeting its own inflated promises in the delivery of 5G service.

For an excellent analysis and comparison of exaggerated 5G claims by Verizon vs AT&T, please see this blog post by Adrian Diaconescu.

……………………………………………………………………………………………………………………………………….

References:

https://telecoms.com/504372/verizon-gets-wrist-slap-for-misleading-5g-claims/

https://www.phonearena.com/news/verizon-misleading-5g-advertisingatt-complaint_id124706

Verizon misleading 5G commercials called out by NAD after AT&T complaint

The National Advertising Division (NAD) has condemned Verizon for misleading consumers over the quality of its 5G network across the country. NAD recommended Verizon stop using the claim that it’s delivering “the most powerful 5G experience for America” in two previously aired TV commercials touting the carrier’s 5G service rollout in sports stadiums were challenged by 5G competitor AT&T.

Editor’s Note: NAD is an investigative unit of the advertising industry’s system of self-regulation and is a division of the BBB National Programs’ self-regulatory and dispute resolution programs.

……………………………………………………………………………………………………………………………………………….

“The National Advertising Division has determined that, in the context of two challenged television commercials touting Verizon’s rollout of 5G service in sports venues, the claim that ‘Verizon is building the most powerful 5G experience for America’ reasonably communicates a message about the consumer experience of using 5G mobile service that was not supported by the evidence in the record,” according to statement from NAD.

The message is apparently that Verizon was not fairly representing its network in advertisements and promotions broadcast at sporting venues.

Verizon plans to appeal the ruling to the National Advertising Review Board.

……………………………………………………………………………………………………………………………….

Verizon is building 5G networks in sporting venues across the U.S., though the NAD believes the way the advertisements have been created suggests a similar experience would be offered outside the sports venues themselves.

The express claim stated in the ads is that “Verizon is building the most powerful 5G experience for America,” a message the carrier indicated is clear to consumers, despite NAD’s finding that Verizon’s use of past and present tense conveys the message that it currently delivers the most powerful 5G experience.

“The intent of the commercial is to inform consumers about the billions of dollars Verizon is investing in its 5G buildout. Verizon strongly believes that consumers understand that this is the only message that is reasonably conveyed,” said Verizon in its advertiser’s statement.

NAD pointed to wording like “This is happening now,” for the NFL spots and said Verizon’s “unqualified superiority claim…goes beyond touting Verizon’s spectrum portfolio.” Instead, sending the message of 5G consumer experiences that include capacity to serve many people at once and using Verizon’s 5G network to post content, along with resilience, coverage and latency – which NAD said Verizon didn’t provide sufficient evidence to support its present tense “most powerful network” claim.

Based on the context, one commercial the NAD release appears to be referring to is a Verizon NFL 5G Built Right ad, which Jeffrey Moore, principal at Wave7 Research, confirmed ran heavily in September 2019 in line with the start of NFL season and stopped airing November 18.

“5G branding efforts from Verizon, AT&T, and T-Mobile shifted to pandemic-related branding, showing that Verizon, AT&T, and T-Mobile are doing what they can to keep customers connected and safe,” Moore told Fierce Wireless.

Verizon announced last September it was expanding 5G service to 13 NFL stadiums. Given current restrictions on large public gatherings in many places though, it’s unclear when ads depicting massive crowds might come back into favor.

…………………………………………………………………………………………………………..

U.S. based wireless telcos are facing a difficult challenge in delivering the desired “5G experience.” Despite the telcos preaching about the benefits of mmWave spectrum to underpin 5G networks, the telcos are performing woefully according to many critics/pundits.

T-Mobile has been blasted for the speeds which have been delivered over the 600 MHz spectrum it has been offering, while AT&T and Verizon has been failing at coverage. In a recent Rootmetrics gaming study in Los Angeles, none met the minimum requirements for latency.

Moore noted that Metro By T-Mobile’s “Rule Your Day” campaign, was halted for a period, but restarted May 6. On the postpaid side, T-Mobile’s message for a time was “We’re with you,” but has now returned to the tagline of “Are you with us?”

This “slap on the wrist” by NAD implies that the U.S. is failing to even come close to meeting its own inflated promises in the delivery of 5G service.

For an excellent analysis and comparison of exaggerated 5G claims by Verizon vs AT&T, please see this blog post by Adrian Diaconescu.

……………………………………………………………………………………………………………………………………….

References:

https://telecoms.com/504372/verizon-gets-wrist-slap-for-misleading-5g-claims/

https://www.phonearena.com/news/verizon-misleading-5g-advertisingatt-complaint_id124706