Uncategorized

SKT-Samsung Electronics to Optimize 5G Base Station Performance using AI

SK Telecom (SKT) has partnered with Samsung Electronics to use AI to improve the performance of its 5G base stations in order to upgrade its wireless network. Specifically, they will use AI-based 5G base station quality optimization technology (AI-RAN Parameter Recommender) to commercial 5G networks.

The two companies have been working throughout the year to learn from past mobile network operation experiences using AI and deep learning, and recently completed the development of technology that automatically recommends optimal parameters for each base station environment. When applied to SKT’s commercial network, the new technology was able to bring out the potential performance of 5G base stations and improve the customer experience.

Mobile base stations are affected by different wireless environments depending on their geographical location and surrounding facilities. For the same reason, there can be significant differences in the quality of 5G mobile communication services in different areas using the same standard equipment.

Accordingly, SKT utilized deep learning, which analyzes and learns the correlation between statistical data accumulated in existing wireless networks and AI operating parameters, to predict various wireless environments and service characteristics and successfully automatically derive optimal parameters for improving perceived quality.

Samsung Electronics’ ‘Network Parameter Optimization AI Model’ used in this demonstration improves the efficiency of resources invested in optimizing the wireless network environment and performance, and enables optimal management of mobile communication networks extensively organized in cluster units.

The two companies are conducting additional learning and verification by diversifying the parameters applied to the optimized AI model and expanding the application to subways where traffic patterns change frequently.

SKT is pursuing advancements in the method of improving quality by automatically adjusting the output of base station radio waves or resetting the range of radio retransmission allowance when radio signals are weak or data transmission errors occur due to interference.

In addition, we plan to continuously improve the perfection of the technology by expanding the scope of targets that can be optimized with AI, such as parameters related to future beamforming*, and developing real-time application functions.

* Beamforming: A technology that focuses the signal received through the antenna toward a specific receiving device to transmit and receive the signal strongly.

SKT is expanding the application of AI technology to various areas of the telecommunications network, including ‘Telco Edge AI’, network power saving, spam blocking, and operation automation, including this base station quality improvement. In particular, AI-based network power saving technology was recently selected as an excellent technology at the world-renowned ‘Network X Award 2024’.

Ryu Tak-ki, head of SK Telecom’s infrastructure technology division, said, “This is a meaningful achievement that has confirmed that the potential performance of individual base stations can be maximized by incorporating AI,” and emphasized, “We will accelerate the evolution into an AI-Native Network that provides differentiated customer experiences through the convergence of telecommunications and AI technologies.”

“AI is a key technology for innovation in various industrial fields, and it is also playing a decisive role in the evolution to next-generation networks,” said Choi Sung-hyun, head of the advanced development team at Samsung Electronics’ network business division. “Samsung Electronics will continue to take the lead in developing intelligent and automated technologies for AI-based next-generation networks.”

SK Telecom and Samsung Electronics researchers discussing verification of AI-based 5G base station quality optimization technology.

SK Telecom and Samsung Electronics researchers discussing verification of AI-based 5G base station quality optimization technology.

SK Telecom and Samsung Electronics researchers discussing verification of AI-based 5G base station quality optimization technology.

SK Telecom and Samsung Electronics researchers discussing verification of AI-based 5G base station quality optimization technology.

…………………………………………………………………………………………………………………………………….

SKT said it is expanding the use of AI to various areas of its communications network, such as “Telco Edge AI,” network power reduction, spam blocking and operation automation, including basestation quality improvement.

…………………………………………………………………………………………………………………………………….

References:

SK Telecom (SKT) and Nokia to work on AI assisted “fiber sensing”

South Korea has 30 million 5G users, but did not meet expectations; KT and SKT AI initiatives

SKT Develops Technology for Integration of Heterogeneous Quantum Cryptography Communication Networks

India Mobile Congress 2024 dominated by AI with over 750 use cases

Dell’Oro: Private RAN revenue declines slightly, but still doing relatively better than public RAN and WLAN markets

Dell’Oro Group reports that Private Wireless Radio Access Network (RAN) revenue growth slowed slightly in the second quarter on a year-over-year basis relative to the ~40 percent increase in 2023. Still, the tapering is in line with expectations and private wireless is performing significantly better on a relative basis than both public RAN and enterprise WLAN. [However, it’s a much smaller market.]

“With public MBB investments slowing, the expectations with new growth opportunities such as Fixed Wireless Access and private wireless are rising,” said Stefan Pongratz, Vice President at Dell’Oro Group. “The results in the quarter and the trends over the past year validate this message that we have communicated now for some time, namely that the enterprise is a very large and mostly untapped opportunity. The market will continue to grow faster than both public RAN and enterprise WLAN, but because of the lower starting point, it will take some time before enterprise RAN revenues are large enough to stabilize public MBB swings,” continued Pongratz.

Additional highlights from the September 2024 Private Wireless Report:

- Contract activity is slowing but the quality of the contracts is improving and increasingly includes larger, multi-site, and even multi-country agreements.

- Regional activity is mostly stable. The three largest regions in 1H24 from a revenue perspective include China, North America, and EMEA.

- Vendor rankings did not change in 1H24. The evolving scope of private wireless taken together with the fact that the $20 B+ enterprise RAN opportunity remains largely untapped is spurring interest from a broad array of participants across the ecosystem. Still, the traditional RAN suppliers are currently well-positioned in this initial phase.

- Top 3 Private Wireless RAN suppliers in 1H24 are Huawei, Nokia, and Ericsson.

- Top 3 Private Wireless RAN suppliers in 1H24 excluding China are Nokia, Ericsson, and Samsung.

- Projections are mostly unchanged. Private wireless RAN revenues are projected to grow at a 21 percent CAGR over the next five years, while public RAN revenues are set to decline at a 3 percent CAGR over the same time period.

Dell’Oro Group’s Private Wireless Advanced Research Report includes both quarterly vendors share data and a 5-year forecast for Private Wireless RAN by RF Output Power, technology, spectrum, and region. To purchase this report, please contact us at [email protected].

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, security, enterprise networks, and data center markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions. For more information, contact Dell’Oro Group at +1.650.622.9400 or visit https://www.delloro.com.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Ericsson and Nokia – Private Wireless Network Initiatives:

- Last week, Ericsson shared details of its enterprise 5G strategy, formulated after its 2020 Cradlepoint acquisition which provides both private 5G and neutral host solutions. “Ericsson’s strategic and comprehensive approach to evolving its private networking portfolio is addressing the growing demand for secure, high-performance connectivity in enterprises,” the vendor quoted Pablo Tomasi, Principal Analyst for Private Networks and Enterprise 5G at Omdia, as saying in its strategy announcement. “Ericsson’s ability to meet customers where they are in their 5G journey with a unified experience will be critical in helping the market scale and enabling enterprises leveraging 5G to transform in a meaningful way,” Tomasi added.

- Nokia has made myriad private networking deal announcements in the past couple of years and recently revealed the results of a market study it commissioned that paints the sector in a very positive light. Early adopters have been scaling up deployments, adding new locations for example, and the vast majority of those surveyed – 93%, to be exact – claimed to have generated a return on investment within a year; almost a quarter did so in just one month. That’s a strong message and one designed to help drive the market forwards.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

References:

Private Wireless RAN Revenues up 24 percent in 2Q 2024, According to Dell’Oro Group

https://www.telecoms.com/telecoms-infrastructure/private-ran-revenues-continue-to-grow-amid-vendor-push

Dell’Oro: RAN market still declining with Huawei, Ericsson, Nokia, ZTE and Samsung top vendors

Highlights of Dell’Oro’s 5-year RAN forecast

Dell’Oro: 2023 global telecom equipment revenues declined 5% YoY; Huawei increases its #1 position

Dell’Oro & Omdia: Global RAN market declined in 2023 and again in 2024

Dell’Oro: Private 5G ecosystem is evolving; vRAN gaining momentum; skepticism increasing

HPE Aruba Launches “Cloud Native” Private 5G Network with 4G/5G Small Cell Radios

SNS Telecom & IT: Private 5G Network market annual spending will be $3.5 Billion by 2027

Ericsson and Vodafone enable Irish rugby team to use Private 5G SA network for 2023 Rugby World Cup

Wipro and Cisco Launch Managed Private 5G Network-as-a-Service Solution

Japan to support telecom infrastructure in South Pacific using Open RAN technology

Japan’s government and private sector will offer support for telecommunications infrastructure in Pacific island countries, starting with a data center and telecom project in Palau, in an effort to improve the security of vital networks connecting Asia and North America. The initiative will be led by Japan’s Ministry of Internal Affairs and Communications and is expected to include telecom company NTT Group, internet service provider Internet Initiative Japan and other companies. It aims to increase Japan’s participation in the South Pacific, a region crisscrossed with undersea communications cables linking East Asia, the U.S., Australia and Southeast Asia. Funding will come from the ministry’s international cooperation budget. Several billion yen (1 billion yen equals $7.1 million) in public-private investment is expected to be mobilized over the first two years.

The infrastructure improvements will use Open Radio Access network (RAN) technology, which Japan has sought to promote as a low-cost way of building wireless networks from components made by different manufacturers.

Japan, the U.S., and Australia — which, along with India, make up the security dialogue known as the Quad — all support improving communications security in Pacific island countries. These island countries are reliant on equipment from Chinese telecom company Huawei Technologies for their land-based networks. The U.S. and others say Huawei has ties to the Chinese military and poses a security risk. Western officials have raised concerns about the potential for eavesdropping on communications and other activities. Huawei denies such accusations.

Quad members have agreed to support the modernization of Palau’s telecommunications infrastructure. Japan’s communications ministry will start putting this initiative to work as early as fiscal 2025, which begins in April. It will then seek to expand aid in fiscal 2026 to other countries in the region. Tuvalu and the Marshall Islands — two of the dwindling number of countries to maintain formal diplomatic relations with Taiwan — are likely to be candidates for such support. The effort will also seek to train cybersecurity personnel. Island countries with understaffed cybersecurity capabilities are seen as a potential vulnerability that can be exploited to launch attacks against Japan, experts say.

Tuvalu-an island country roughly halfway between Australia and Hawaii-is expected to be a candidate to receive Japanese support for telecommunications infrastructure. © Reuters

……………………………………………………………………………………………………………………………………………………………………………………………………..

China has worked to extend its influence in the South Pacific. In recent years, the Solomon Islands, Kiribati and Nauru have all cut diplomatic ties with Taiwan in favor of relations with Beijing. The Solomon Islands also formed a security agreement with China. Including Palau, only three countries in the region still maintain diplomatic relations with Taiwan.

Telecommunications infrastructure is becoming increasingly important for island countries in their own right.

“A stable network connecting a country with the rest of the world is essential for receiving remittances from migrant workers. Better telecommunications infrastructure is of great significance in improving ties between countries,” said Motohiro Tsuchiya, a professor at the Keio University Graduate School of Media and Governance in Japan.

……………………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://market.us/report/open-ran-market/

https://www.o-ran.org/otics/japan-otic

https://www.lowyinstitute.org/the-interpreter/japan-s-5g-ambitions-quad

NTT advert in WSJ: Why O-RAN Will Change Everything; AT&T selects Ericsson for its O-RAN

NTT DOCOMO OREX brand offers a pre-integrated solution for Open RAN

New venture to sell Network Application Programming Interfaces (APIs) on a global scale

Overview:

Some of the world’s largest telecom operators, including América Móvil, AT&T, Bharti Airtel, Deutsche Telekom, Orange, Reliance Jio, Singtel, Telefonica, Telstra, T-Mobile, Verizon and Vodafone, together with network gear maker Ericsson (the largest shareholder) are announcing a new venture to combine and sell network Application Programming Interfaces (APIs) on a global scale to spur innovation in digital services. Network APIs are the way to easily access, use and pay for network capabilities. The venture will drive implementation and access to common APIs from multiple telecom service providers to a broader ecosystem of developer platforms. All the APIs on offer will be based on CAMARA – the open source API project led by the GSMA and the Linux Foundation.

Modern mobile networks have advanced and intelligent capabilities, which have historically been inaccessible to developers. Additionally, it has been impractical for developers to integrate the different capabilities of hundreds of individual telecom operators. The newly formed company will combine network APIs globally, with a vision that new applications will work anywhere and on any network, making it easier and quicker for developers to innovate.

Easily accessible advanced network capabilities will open up the next frontier in app development and empower developers to create new use cases across many sectors. These could include anti-fraud verification for financial transactions and the ability to check device status so streaming providers can dynamically adjust video quality.

The newly formed company will provide network APIs to a broad ecosystem of developer platforms, including hyperscalers (HCPs), Communications Platform as a Service (CPaaS) providers, System Integrators (SIs) and Independent Software Vendors (ISVs), based on existing industry-wide CAMARA APIs (the open-source project driven by the GSMA and the Linux Foundation). Vonage and Google Cloud will partner with the new company, providing access to their ecosystems of millions of developers as well as their partners. The new venture shareholders will bring funding and important assets, including Ericsson’s platform and network expertise, global telecom operator relationships, knowledge of the developer community and each telecom operator’s network APIs, expertise and marketing.

Ericsson-owned Vonage and Google Cloud have already agreed to partner with the new venture, providing access to their respective ecosystems of millions of developers as well as their partners.

“We have a common concern that we’ve made it difficult for developers to program on wireless networks,” said Niklas Heuveldop, CEO of Vonage, stressing that this initiative is all about removing any friction and roadblocks that may be preventing developers taking full advantage of the programmable networks opportunity. He added that, for Vonage, this means a smaller piece of a bigger network API pie.

Closing of the transaction is expected early 2025, subject to regulatory approvals and other customary conditions. Upon closing, Ericsson will hold 50% of the equity in the venture while the telecom providers will hold 50% in total. Built on a deep understanding of developer and enterprise needs and in keeping with the industry-body GSMA Open Gateway principles, the new venture’s platform and partner ecosystem will remain open and non-discriminatory to maximize value creation across the industry.

Comment and Analysis:

Much has already been made of the industry’s decision to open up and (attempt) to monetize network APIs. Optimistic estimates, like the one proffered by McKinsey, claim that network APIs represent a $300 billion opportunity for telcos between now and the end of the decade. However, some like Kearney, have warned that all will be for naught without proper industry coordination and collaboration to drive software developer uptake.

“Today’s announcement is an important step in that direction by addressing one of the major challenges for developers seeking to engage with mobile operators – sector fragmentation,” said Kester Mann, director of consumer and connectivity at CCS Insight. “In the past, the telecom industry – with many competing players each deploying different strategies for their specific regions – has struggled to present a united and coherent front.” Despite their dubious track record, Mann reckons this particular venture stands a better chance of success than most, thanks to the urgent need for operators to earn a return on 5G, and due to the involvement of major technology partners in the form of Google and Ericsson. “There should be fresh optimism that the new company unveiled will enjoy more success than previous failed ventures,” he added.

While open network APIs will work on compatible hardware from any vendor – whether it’s Nokia or Ericsson or Huawei – this new venture represents an opportunity for Ericsson to play a central role in the emerging ecosystem.

Quotes from the partners:

América Móvil

Daniel Hajj, Chief Executive Officer, AMX: “We are very excited to join Ericsson and other key players in our industry in this innovative global platform initiative that will benefit the digital ecosystem as a whole. New API solutions will establish exciting value-added offerings to our customers on the top of our networks’ infrastructure.”

AT&T

Jeremy Legg, Chief Technology Officer, AT&T: “At AT&T, we’ve been creating API tools to empower developers for well over a decade. Now, with a broad-based, interoperable API platform, we’re giving innovators a new global toolbox where the world’s best app developers can create exciting user experiences at scale. This high-performance mobile ecosystem will usher in a new era of greater possibility for customers and mobile users around the world.”

Bharti Airtel

Gopal Vittal, Managing Director and CEO, Bharti Airtel: “Today marks a defining moment as the industry comes together to form a unified platform that will allow more developers and businesses to utilize our networks and explore API opportunities through open gateway principles. This move will enhance network monetization opportunities. Airtel is delighted to partner in this initiative that will help enable the telecom sector to drive growth and innovation across the ecosystem.”

Deutsche Telekom

Tim Höttges, CEO of Deutsche Telekom: “The new company accelerates our leading work with MagentaBusiness APIs to expose our network capabilities for customers and developers. We believe that this company will open up new monetization opportunities for the industry. We encourage and look forward to more telecom operators joining us to expand and develop this ecosystem.”

Ericsson

Börje Ekholm, President and CEO, Ericsson: “Today is a defining moment for the industry and milestone in our strategy to open up the network for increased monetization opportunities. A global platform built on Ericsson’s deep technical capabilities and with a comprehensive ecosystem, that provides millions of developers with a single connection, will enable the telecom industry to invest deeper into the network API opportunity, driving growth and innovation for everyone.”

Orange

Christel Heydemann, Chief Executive Officer, Orange: “This is a critical first step in our innovation journey to fully harness the power of our networks at scale, providing secure access to new on-demand network services and advanced network capabilities. By delivering a common and simple set of network APIs for developers globally, we can unleash this network value for businesses, large and small. This is a definitive gamechanger for businesses, opening up the possibility of a new wave of digital services.”

Reliance Jio

Mathew Oommen, President, Reliance Jio: “We spearheaded the transformation of both mobile and fixed home broadband by delivering affordable, high-quality broadband to everyone, across India. As we rapidly adopt an AI and API-driven technology ecosystem—by collaborating with global leaders, Jio is thrilled to offer a suite of innovative and transformative APIs to enterprises and developers worldwide. Together, we are not just building networks; we are laying the foundation for a smarter, more connected, and inclusive world in the AI era.”

Singtel

Mr Yuen Kuan Moon, Group Chief Executive Officer, Singtel: “This unified platform and global eco-system will enable even more developers and businesses to leverage 5G quality networks to exploit API opportunities using GSMA’s open gateway principles. We look forward to helping even more enterprises and organizations in Asia to use network API solutions to drive growth and innovation through this timely collaboration.”

Telefonica

José María Álvarez-Pallete, Chairman & CEO of Telefónica: “This collaboration will drive the GSMA Open Gateway initiative and provide customers with a consistent set of Camara APIs. Our belief is that this industry movement, which will be open to all networks, can set the stage for unprecedented innovation and value creation for the sector, by unlocking the potential of network capabilities.”

Telstra

Vicki Brady, CEO of Telstra: “This is a groundbreaking initiative for our industry. This new global venture will create an ecosystem that provides developers, partners and customers with access to programmable, advanced network capabilities that will unleash a new wave of innovation in digital services and further unlocks the benefits of our 5G network. We’ve been making good progress locally with Ericsson and other partners, and we look forward to further accelerating digital transformation for our Australian customers and bringing value and simplicity to application developers around the world.”

T-Mobile

Ulf Ewaldsson, President of Technology, T-Mobile: “At T-Mobile, we’ve always been laser focused on championing change across the industry to create the best customer experiences, while fueling growth and innovation across the entire wireless ecosystem. That level of transformation takes unprecedented collaboration and expertise. We are excited about the possibilities this venture will create for developers and wireless customers around the world.”

Verizon

Joe Russo, EVP & President, Global Network and Technology of Verizon: “The depth and value of the services and data insights accessible through Verizon’s renowned 5G network are practically boundless. Verizon has been at the forefront of developing various network APIs to assist developers in enhancing customer security, reducing pain points in customer interactions, and enabling the creation of novel experiences. This exciting collaboration with global partners will broaden the availability of these services and accelerate adoption of APIs worldwide.”

Vodafone

Margherita Della Valle, Vodafone Group Chief Executive, said: “Network APIs are reshaping our industry. This pioneering partnership will enable businesses and developers to use the collective strength of our global networks to develop applications that drive growth, create jobs, and improve public services. Just as 4G and smartphones made apps integral to our everyday life, the power of our 5G network will stimulate the next wave of digital services.”

Google Cloud

Thomas Kurian, CEO of Google Cloud: “We understand the power of an open platform and ecosystem in driving innovation. We are proud to participate in this important partnership in the telco industry to create value for our global customers via network APIs – and ultimately deliver on the promise of the public cloud.”

Vonage

Niklas Heuveldop, CEO Vonage: “This groundbreaking, open industry collaboration effectively removes the single largest barrier for developers to leverage mobile networks to their full potential. Developers across the world’s leading developer platforms will benefit from accessing advanced network capabilities in partner networks globally through common APIs, accelerating the digital transformation of businesses and the public sector. As one of the leading developer platforms, we look forward to engaging our developer community as we grow the network API business.”

……………………………………………………………………………………………………………………………………………………….

References:

Telefónica and Nokia partner to boost use of 5G SA network APIs

Analysts: Telco CAPEX crash looks to continue: mobile core network, RAN, and optical all expected to decline

Analysys Mason Open Network Index: survey of 50 tier 1 network operators

Ericsson expects continuing network equipment sales challenges in 2024

Nvidia enters Data Center Ethernet market with its Spectrum-X networking platform

Nvidia is planning a big push into the Data Center Ethernet market. CFO Colette Kress said the Spectrum-X Ethernet-based networking solution it launched in May 2023 is “well on track to begin a multi-billion-dollar product line within a year.” The Spectrum-X platform includes: Ethernet switches, optics, cables and network interface cards (NICs). Nvidia already has a multi-billion-dollar play in this space in the form of its Ethernet NIC product. Kress said during Nvidia’s earnings call that “hundreds of customers have already adopted the platform.” And that Nvidia plans to “launch new Spectrum-X products every year to support demand for scaling compute clusters from tens of thousands of GPUs today to millions of DPUs in the near future.”

- With Spectrum-X, Nvidia will be competing with Arista, Cisco, and Juniper at the system level along with “bare metal switches” from Taiwanese ODMs running DriveNets network cloud software.

- With respect to high performance Ethernet switching silicon, Nvidia competitors include Broadcom, Marvell, Microchip, and Cisco (which uses Silicon One internally and also sells it on the merchant semiconductor market).

Image by Midjourney for Fierce Network

…………………………………………………………………………………………………………………………………………………………………………..

In November 2023, Nvidia said it would work with Dell Technologies, Hewlett Packard Enterprise and Lenovo to incorporate Spectrum-X capabilities into their compute servers. Nvidia is now targeting tier-2 cloud service providers and enterprise customers looking for bundled solutions.

Dell’Oro Group VP Sameh Boujelbene told Fierce Network that “Nvidia is positioning Spectrum-X for AI back-end network deployments as an alternative fabric to InfiniBand. While InfiniBand currently dominates AI back-end networks with over 80% market share, Ethernet switches optimized for AI deployments have been gaining ground very quickly.” Boujelbene added Nvidia’s success with Spectrum-X thus far has largely been driven “by one major 100,000-GPU cluster, along with several smaller deployments by Cloud Service Providers.” By 2028, Boujelbene said Dell’Oro expects Ethernet switches to surpass InfiniBand for AI in the back-end network market, with revenues exceeding $10 billion.

………………………………………………………………………………………………………………………………………………………………………………

In a recent IEEE Techblog post we wrote:

While InfiniBand currently has the edge in the data center networking market, but several factors point to increased Ethernet adoption for AI clusters in the future. Recent innovations are addressing Ethernet’s shortcomings compared to InfiniBand:

- Lossless Ethernet technologies

- RDMA over Converged Ethernet (RoCE)

- Ultra Ethernet Consortium’s AI-focused specifications

Some real-world tests have shown Ethernet offering up to 10% improvement in job completion performance across all packet sizes compared to InfiniBand in complex AI training tasks. By 2028, it’s estimated that: 1] 45% of generative AI workloads will run on Ethernet (up from <20% now) and 2] 30% will run on InfiniBand (up from <20% now).

………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.fierce-network.com/cloud/data-center-ethernet-nvidias-next-multi-billion-dollar-business

https://www.nvidia.com/en-us/networking/spectrumx/

Will AI clusters be interconnected via Infiniband or Ethernet: NVIDIA doesn’t care, but Broadcom sure does!

Data Center Networking Market to grow at a CAGR of 6.22% during 2022-2027 to reach $35.6 billion by 2027

LightCounting: Optical Ethernet Transceiver sales will increase by 40% in 2024

Huawei’s First-Half Net Profit Rose on Strong Smartphone Sales, Car Business

Huawei Technologies Co.’s revenue grew for the sixth straight quarter as its smartphones gained significant market share in China. Net profit climbed 18% in the first half of the year, thanks to strong smartphone sales and robust growth in its car business. Huawei reports a handful of unaudited financial figures throughout the year and releases a more detailed audited annual report each spring. It didn’t provide data broken down by business segment for the first half.

The Chinese networking and electronics behemoth posted revenue of 239 billion yuan ($33.6 billion) in the June quarter, up 33.7% from a year earlier, according to calculations based on the company’s six-month financial figures. Implied net profit was 35.5 billion yuan, a drop of 18.6% from a year ago when Huawei recorded one-time gains from divestments. The company sold mobile maker Honor Device Co. to a consortium in 2020 and parts of its server business in 2021, with proceeds from both paid out in installments.

The Shenzhen-based company’s smartphone shipments rose by 50% last quarter as it and other local players like Vivo and Xiaomi Corp. beat out Apple, which dropped to sixth place among handset makers in China, according to market tracker IDC. Apple’s sales in China fell 6.5% in the June quarter, missing Wall Street projections, even as overall shipments in China grew.

Huawei’s next flagship Mate 70 will be closely watched for any processor upgrades when the device is introduced later this year. The Mate 60 roiled US policymakers when it debuted a China-made 7-nanometer chip a year ago, despite US-imposed sanctions and export controls geared to stem advances in China’s chip technologies.

Last year, Huawei more than doubled its net profit as it rebuilt the market share of its core businesses in consumer electronics and cloud computing, which were severely eroded by several years of U.S. sanctions that limited its access to advanced semiconductors.

In the second quarter, Huawei was the No. 2 smartphone seller in China, the world’s largest smartphone market, with an 18.1% market share, according to market-research firm International Data Corp. Counterpoint Research said Huawei’s sales jumped 44.5% in the quarter from a year earlier, the fastest growth among Chinese original equipment manufacturers, thanks to the Pura 70 and Nova 12 series. The company launched its Pura 70 series in April.

Huawei and other local smartphone makers like Vivo and Xiaomi Corp. beat out Apple, which dropped to sixth place among handset makers in China, according to market tracker IDC.

………………………………………………………………………………………………………………………..

Huawei has invested in its car business as Beijing ramps up support for high-tech industries as part of efforts to reduce the economy’s reliance on the property sector for growth.

The company’s automotive unit, which offers self-driving technology to electric vehicle makers, earned a revenue of 10 billion yuan as of early July, according to a report by a Chinese media outlet, more than the combined revenue in the previous two years. Huawei didn’t provide a breakdown of its sales.

Changan Automobile-backed Avatr Technology said in an exchange filing last week that it will acquire a 10% stake in Yinwang Smart Technology, Huawei’s car unit that provides autonomous-driving technology to automakers, valuing the company at 115 billion yuan. Seres on Monday said it will acquire a 10% stake in Yinwang.

……………………………………………………………………………………………………………………………………………

References:

Despite U.S. sanctions, Huawei has come “roaring back,” due to massive China government support and policies

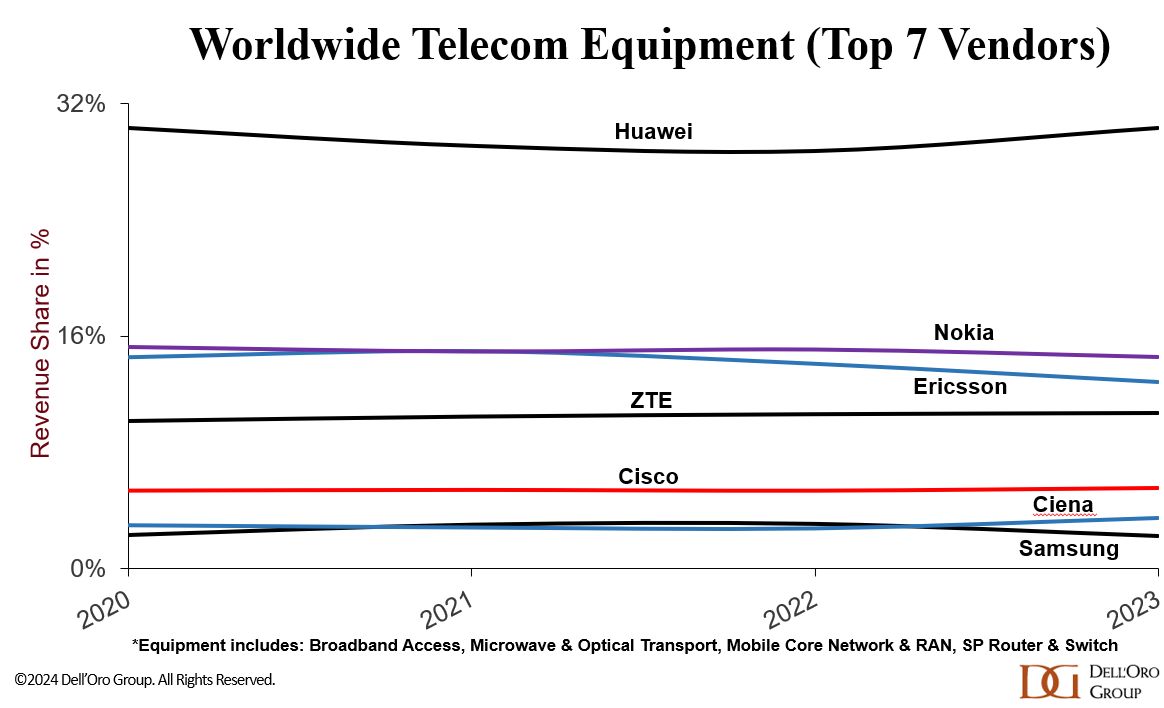

Dell’Oro: RAN market still declining with Huawei, Ericsson, Nokia, ZTE and Samsung top vendors

China Unicom-Beijing and Huawei build “5.5G network” using 3 component carrier aggregation (3CC)

ZTE reports H1-2024 revenue of RMB 62.49 billion (+2.9% YoY) and net profit of RMB 5.73 billion (+4.8% YoY)

China’s ZTE reported a 2.9% rise in total revenue to RMB62.5 billion ($8.76 billion), with net profit attributable to holders of ordinary shares of the Hong Kong listed company at RMB 5.73 billion, up 4.8% year-over-year (YoY). The biggest growth surge was in the corporate and government unit, which boosted revenue by 56% to RMB9.2 billion yuan ($1.29 billion), mainly through stronger server and storage sales. However, that was offset by a 68% hike in costs, depressing the gross margin by 5.7 points – a result of “changes in revenue mix,” the company said.

The company’s core carrier network equipment business declined 8.6% in the first half of 2024, holding back underlying earnings to 4.96 billion Chinese yuan (US$700 million) – a gain of just 1.1% over last year. The carrier unit, which accounted for 60% of the company’s total revenue, brought in RMB37 billion ($5.18 billion) in sales in H1, the company revealed in its stock exchange filing.

ZTE said demand from Chinese telecom operators had been constrained by “overall investment sentiments,” but it pointed to improved sales of indoor distribution, high-speed rail and metro networking equipment. ZTE’s consumer business, which includes mostly handsets and home routers, grew 14% to RMB16 billion ($2.24 billion). R&D spending remained flat at RMB12.7 billion ($1.78 billion).

_International_Software_Products.jpeg?width=1280&auto=webp&quality=95&format=jpg&disable=upscale)

Source: Cynthia Lee/Alamy Stock Photo

China’s domestic market accounted for 69% of total sales, roughly the same as last year. The biggest offshore growth region was Asia (excluding China), which grew 23%. ZTE said it is positioning itself as a “path-builder for the digital economy” and aimed to further expand its legacy connectivity business while growing its computing business. Its AI portfolio includes full-stack intelligent solutions, backed by key technologies such as high-speed networking, network computing and data processing.

ZTE is developing their own custom silicon. In the first half of 2024, the company continued to increase investment in advanced semiconductor process technologies, advanced architecture and seal packaging design, core intellectual properties and digitalized efficient development platform on the back of close to 30 years’ R&D build-up. We are an industry leader in terms of the ability to design the whole process of chip. On top of a solid foundation in the R&D of base-level technology for DICT chip, the Group has also constructed an ultra-efficient, green and intelligent full-stack computing network base pivoting on “data, computing and network” in line with developments in computing-network integration. The creation of a product regime meeting the core requirements of the diversified scenarios of “cloud, edge, terminal” has supported our ongoing leading position in terms of competitiveness.

ZTE has used its expertise in communication software and hardware development, engineering capabilities and industrialization to intensify its investment in computing power products and solutions. The company has launched a comprehensive suite of full-stack, full-scenario intelligent computing solutions, covering computing, networks, capabilities, intelligence and applications. These solutions include a full range of general computing servers, high-performance AI training servers, inference servers, liquid-cooled servers, distributed storage systems, high-end multi-control magnetic arrays, integrated training-inference machines and high-speed lossless switches.

In the terminal sector, ZTE has introduced the concept of “AI for All”, focusing on five core consumer scenarios: sports and health, audio and video entertainment, business and travel, home and education, and smart driving. The company has launched a full range of AI-driven terminal products, including smartphones, tablets, laptops and mobile internet devices, as part of its Full-Scenario Intelligent Ecosystem 3.0. This ecosystem promotes the integration of AI technology across mobile terminal devices, smart home devices, cloud computing and automotive electronics.

Moving forward, ZTE is dedicated to advancing its core technological innovations and accelerating its expansion into the “connectivity + computing + capability + intelligence” domain. The company will focus on strengthening its digital and intelligent infrastructure. By fostering open collaboration and pursuing diverse, mutually beneficial partnerships, ZTE aims to build a highly efficient and intelligent digital future with industry partners. The company said it expects: gradual adoption of 5G-Advanced, further rollout of 400G optical and construction of intelligent computing centers to drive the China’s telecom carrier market in the second half. Offshore, it will continue to focus on large national markets and big telcos for its wirelines and wireless product lines.

References:

https://www.lightreading.com/finance/zte-s-carrier-sales-slump-9-in-h1

https://www1.hkexnews.hk/listedco/listconews/sehk/2024/0816/2024081601602.pdf

ZTE reports H1 2024 revenue of RMB 62.49 billion and net profit of RMB 5.73 billion

ZTE reports higher earnings & revenue in 1Q-2024; wins 2023 climate leadership award

China Telecom with ZTE demo single-wavelength 1.2T bps hollow-core fiber transmission system over 100T bps

China Mobile & ZTE use digital twin technology with 5G-Advanced on high-speed railway in China

Türk Telekom and ZTE trial 50G PON, but commercial deployment is not imminent

ZTE sees demand for fixed broadband and smart home solutions while 5G lags

Tech layoffs continue unabated: pink slip season in hard-hit SF Bay Area

A combination of strategic pivots toward the red-hot AI sector and corrections after pandemic-era over hiring have pushed companies across the tech sector to lay off massive number of employees, according to outplacement firm Challenger, Grey & Christmas. Tech companies including Cisco Systems, Intel and Dell have cut tens of thousands of jobs in August, the latest in a year that began with layoffs at companies such as Amazon and Google.

On Wednesday, Cisco announced in a notice posted with the Securities and Exchange Commission that it was laying off 5,500 workers (7% of its employees) as part of an effort to invest more in AI. In a short statement, CEO Chuck Robbins used the term “AI” five times, highlighting the company’s efforts to keep up in the ongoing AI race. Earlier this year, Cisco also laid off 4,000 or 5% of its workforce, saying that the company wanted to “realign the organization and enable further investment in key priority areas.” Cisco joins a litany of other companies like Microsoft and Intuit that have used AI as the justification for mass layoffs.

- As of August 17, 2024, 404 tech companies have laid off 132,498 workers this year, according to layoffs.fyi, a website that tracks tech industry job cuts. This includes major tech companies like Amazon, Google, Microsoft, Tesla, TikTok, and Snap, as well as smaller startups and apps.

- Crunchbase says that in 2023, more than 191,000 workers in U.S.-based tech companies (or tech companies with a large U.S. workforce) were laid off in mass job cuts. In 2022, more than 93,000 jobs were slashed from public and private tech companies in the U.S.

The SF Bay Area has been particularly hard-hit, with companies such as Twitter, Meta, and Salesforce announcing significant job cuts. The layoffs are sending shockwaves through the region’s economy. The tech industry has long been a major driver of growth and employment in the Bay Area, accounting for a significant portion of tax revenue and supporting numerous ancillary businesses. The sudden loss of jobs has raised concerns about a potential economic downturn. Many of the affected workers are highly skilled in areas such as software engineering, product development, and data science.

Here are the largest Bay Area tech company layoffs in 2024 and 2023:

| March 14, 2023 | Meta/FB |

21,000

|

13% | Menlo Park |

| August 1, 2024 | Intel |

18,720

|

15% | Santa Clara |

| January 20, 2023 | Alphabet |

12,000

|

6% | Mountain View |

| Feb 14 & Aug14, 2024 | Cisco Systems | 9,500 | 13% | San Jose |

The tech layoffs have created a fiercely competitive job market, with many qualified individuals seeking new employment. This has put pressure on salaries and benefits, further exacerbating the economic impact. The tech layoffs have also had a psychological toll on the Bay Area community. Many workers have lost their sense of stability and are worried about their financial future. The uncertainty has created a climate of anxiety and stress, particularly among those who are still employed.

Government officials and economic development agencies are working to mitigate the effects of the layoffs. They are providing support services to displaced workers, such as job retraining and placement assistance. However, the full extent of the economic impact remains to be seen. The surge in tech layoffs underscores the cyclical nature of the industry. While the Bay Area has weathered economic downturns in the past, the unprecedented scale of the current tech job cuts raises questions about the long-term health of the tech sector. As companies adapt to a changing economic landscape, the region’s economy is struggling to evolve to meet the challenges and perceived opportunities (e.g. AI).

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.wsj.com/finance/investing/tech-media-telecom-roundup-market-talk-12947dd6

https://futurism.com/the-byte/cisco-layoff-ai-profit

https://news.crunchbase.com/startups/tech-layoffs/

https://www.challengergray.com/tags/job-cut-report/

Massive layoffs and cost cutting will decimate Intel’s already tiny 5G network business

Cisco to lay off more than 4,000 as it shifts focus to AI and Cybersecurity

Cisco restructuring plan will result in ~4100 layoffs; focus on security and cloud based products

Massive layoffs and cost cutting will decimate Intel’s already tiny 5G network business

Huge Loss & Restructuring:

In its August 1st press release detailing a $1.6 billion 2Q-2024 loss (mainly from it’s foundry business) [1.] Intel announced it was cutting more than 15% of its workforce by 2025 with most of those coming by year end. The company is also suspending its dividend starting in the fourth quarter of 2024.

Note 1. Intel Foundry, which reported a $2.5bn operating loss during the first quarter of 2024, lost an additional $2.8bn in Q2-2024. That business is seen as a U.S. strategic asset in a major move to bring back chip making to the U.S. from Taiwan, China and South Korea.

“Our Q2 financial performance was disappointing, even as we hit key product and process technology milestones. Second-half trends are more challenging than we previously expected, and we are leveraging our new operating model to take decisive actions that will improve operating and capital efficiencies while accelerating our IDM 2.0 transformation,” said Pat Gelsinger, Intel CEO. “These actions, combined with the launch of Intel 18A next year to regain process technology leadership, will strengthen our position in the market, improve our profitability and create shareholder value.”

CEO/CFO Earnings Call prepared remarks:

“We are targeting a headcount reduction of greater than 15% by the end of 2025, with the majority of this action completed by the end of this year. We do not do this lightly, and we have carefully considered the impact this will have on the Intel family. These are hard but necessary decisions. Our actions will reduce OpEx (operating expenses) to approximately $20 billion in 2024, and we see a bigger impact next year, with 2025 OpEx targeted at $17.5 billion, more than 20% below prior estimates. We expect further benefits in 2026, with OpEx to decline in absolute dollars yet again. Even as we lower overall spending, we will continue to fund the investments needed to deliver our strategy.”

The company’s latest filing with the Securities and Exchange Commission (SEC) stated there were 124,800 employees as of December 2023, down from 131,900 a year before. Therefore, a 15% reduction could translate to the loss of 18,720 employees and we wouldn’t be surprised by total job cuts exceeding 20,000! In addition to layoffs, Intel is pushing older employees to retire.

CEO Pat Gelsinger wrote in a letter to Intel employees:

“Next week, we’ll announce a companywide enhanced retirement offering for eligible employees and broadly offer an application program for voluntary departures. I believe that how we implement these changes is just as important as the changes themselves, and we will adhere to Intel values throughout this process.”

The objective is to greatly reduce various operational costs (research and development plus marketing, general and administrative expenses) to about $20 billion this year and $17.5 billion in 2025, “with further reductions planned in 2026,” said Intel. That $17.5 billion would be about $4.2 billion less than Intel booked for these expenses in 2023, according to its last annual SEC filing, and a reduction of $7 billion compared with the figure for 2022.

Fitch Ratings downgraded Intel’s Long-Term Issuer Default Rating to ‘BBB+’ from “A-,” citing execution risks and potential negative rating actions. Fitch also affirmed Intel’s Short-Term IDR and commercial paper rating at ‘F2’. Fitch believes execution risk remains significant for Intel and that missteps could result in further negative rating actions.

……………………………………………………………………………………………………………………………………

Analyst Comments:

Rosenblatt Securities analyst Hans Mosesmann reiterated his sell rating on Intel stock with a price target of 17. “We anticipate that the company (Intel) will continue to lose share to AMD as its manufacturing roadmap is tepid compared to that of the leading-edge player,” Mosesmann said in a client note.

Bernstein analyst Stacy Rasgon was particularly grim about Intel’s prospects.

“The company’s issues are now approaching the existential,” he said in a client note. “In other circumstances we believe we would now be having ‘going concern’ conversations with clients.”

Impact on Intel’s 5G Business:

The company’s website states: “From Cloud to Network to Edge: 5G Is Powered by Intel Intel-powered 5G networks deliver a powerful data-centric future where compute is fluid, intelligent, and pervasive—creating an evolutionary leap in agility and scalability.”

PHOTO Credit: Intel

Intel incorrectly states, “Intel is embedded throughout the 5G value chain, offering flexible performance, Intel® Xeon® Scalable processors, custom RAN configurations, accelerators, software, and a common toolchain.” Does anyone really believe that?

Intel wants 5G network equipment vendors to switch from custom ASIC silicon they design to its general-purpose processors (GPPs). But there has been very limited adoption of those processors in the radio access network (RAN) to date. Many telco executives remain unconvinced GPPs, especially based on x86, can measure up. Arguments about using the same platforms for multiple needs look spurious when most RAN compute is at the mast site, where it cannot realistically be shared with anything else.

Of the big three 5G kit vendors, only Ericsson says Intel is a good option for Layer 1 (PHY), the category of most demanding RAN software. Huawei and Nokia remain vehemently opposed to using Intel silicon in this area. As expected, most of Ericsson’s 5G products today are based on its own custom silicon, not Intel’s GPPs.

References:

https://www.intel.com/content/www/us/en/newsroom/news/actions-accelerate-our-progress.html#gs.d2jtpn

https://download.intel.com/newsroom/2024/corporate/Earnings-Call-2Q2024-080124.pdf

https://www.intel.com/content/www/us/en/wireless-network/5g-overview.html

Despite U.S. sanctions, Huawei has come “roaring back,” due to massive China government support and policies

On March 30th we wrote that Huawei Technologies was back, with its net profit more than doubled from the same period last year (2023). Today, a Wall Street Journal (WSJ) news story reaffirmed that with reasons which were really no surprise! Huawei’s profit more than doubled last year, the largest jump in at least two decades. Roughly two-thirds of its revenue comes from domestic (China) clients.

Five years ago, the U.S. sanctioned Huawei, cutting off the Chinese company’s access to advanced U.S. technologies like semiconductors and the Android OS for its smartphones. Initially, the company struggled. In 2021, its revenue dropped almost 30% from the year before. Its core telecom equipment business was suffering. Apple’s iPhone was taking over Huawei market share in smartphones.

Yet in the last year, Huawei has come roaring back, boosted by billions of dollars in China government support. Huawei has expanded into new businesses, boosted its profitability and found fresh ways to curb its dependence on U.S. suppliers. It has held on to its leading position in the global telecom-equipment market, despite American efforts to squeeze Huawei out of its allies’ networks. Also, it’s making a big comeback in high-end smartphones, using sophisticated new chips developed in-house, such that it has captured 15% market share in China (knocking Apple out of the top five smartphone brands).

“The U.S. government’s campaign against Huawei is inadvertently bolstering the company’s resilience, echoing the age-old adage that what doesn’t kill you makes you stronger,” said Sameh Boujelbene, an analyst at research firm Dell’Oro Group.

China state support has paid off big time! After the U.S. imposed restrictions, Huawei and China’s government grew closer. Soon, Huawei leaders declared that every product they made going forward should be able to rely entirely on components developed by Chinese companies. China government contracts and company registration records, as well as WSJ interviews with former and current employees, reveal that billions of dollars flowed from the Chinese government to Huawei through preferential buying contracts and subsidies. State-owned enterprises, government agencies and Communist Party bodies sought Huawei chips, smartphones, cloud services and software, with some procurement contracts calling for Huawei gear by name.

Local governments have bought Huawei businesses, providing cash injections. Once reliant on Google’s Android for its consumer devices, Huawei built its own operating system. It has even made a foray into electric vehicles, a task that Apple gave up on, and developed its own version of Bluetooth. Huawei still faces challenges. Its most advanced semiconductors remain a step behind industry leaders such as Nvidia, whose chips are made by TSMC in Taiwan, which Huawei no longer has access to due to U.S. sanctions. U.S. export restrictions, which effectively barred Huawei from using American technology anywhere along the chipmaking process, meant the Chinese company could no longer source its chips from TSMC. Some analysts believe it will be hard for Huawei to keep innovating without access to more advanced Western technologies, especially chip making equipment and software.

One current U.S. official said Washington is closely tracking Huawei’s efforts to make its own semiconductors, in case more actions are needed to block China from manufacturing artificial-intelligence-focused chips that can give Beijing a military edge.

On May 16, 2019, China’s local government in Shenzhen, where Huawei is based, registered an investment company Shenzhen Major Industry Investment Group (SMII), focused on semiconductors, investing in foundries, manufacturing equipment and materials that would help ensure Huawei was supplied with enough domestically made chips and other technologies. Two companies established by SMII, including a chip foundry, employed former Huawei executives, according to people familiar with the matter. One received around a dozen patented technologies transferred from Huawei. Huawei human-resources managers had asked company researchers if they would work at that entity, promising them they could keep their benefits if they moved, according to people familiar with the matter. Shenzhen’s imports of semiconductor manufacturing equipment surged after SMII’s inception, official data shows. Through various state-backed funds, the Chinese government has invested in more than two dozen chip-related startups, over the past five years, according to corporate database Tianyancha.

That’s in addition to government investments in Huawei’s HiSilicon chip unit (more below), which made the silicon used in the company’s popular Mate 60 Pro smartphone. HiSilicon became an independent, wholly owned Huawei subsidiary in 2004. It was founded in 1991 as Huawei’s ASIC Design Center.

A majority-owned Shenzhen company also bought Huawei’s Honor smartphone business, which was struggling because of the U.S. sanctions. The deal was worth several billions of dollars, a person familiar with the transaction said. The cash allowed Huawei to focus on other businesses, including its higher-end Mate series of phones.

“We’ve been through a lot over the past few years. But through one challenge after another, we’ve managed to grow,” Huawei said in a written statement, adding that the company owed its survival and development to the trust and support of global customers, partners and “all sectors of society.” Sustaining R&D investment will be crucial going forward, the company said.

“We’ve been through a lot over the past few years, but through one challenge after another, we’ve managed to grow,” Huawei said in a written statement, adding that the company owed its survival and development to the trust and support of global customers, partners and “all sectors of society.” Sustaining R&D investment will be crucial going forward, the company said.

Huawei focused on building out more of its own supply chain and expanding into new areas that could generate revenue to help keep the company going, including cloud computing and other services, according to Chris Peirera, a former Huawei senior director in public affairs. “In the past, we chased the ideal of globalization, determined to serve mankind. What are our goals now? It’s to survive. We will make money wherever we can,” Huawei founder Ren Zhengfei later told the company’s staff in an internal letter.

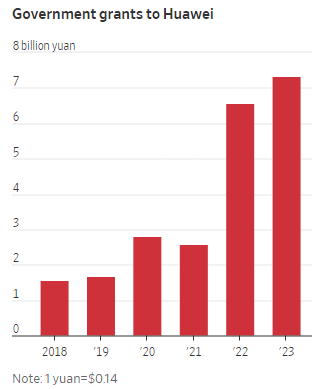

Huawei received over $1 billion in China government grants in 2023, more than quadruple the amount it received in 2019, according to Huawei’s financial reports. In all, Huawei received nearly $3 billion in the past five years, accounting for 3% of its total R&D expenses.

Source: Huawei via WSJ

China’s government directed state agencies to buy more of Huawei’s software, chips and mobile devices, a policy that boosted Huawei while reducing China’s reliance on American companies, including Apple, whose iPhones are no longer allowed in the workplace for many government employees. A Chinese government research unit named Huawei as one of four tech giants spearheading the nation’s push to wean itself off foreign technology, while another government body singled out Huawei as a preferred state supplier of AI chips, servers and other enterprise software.

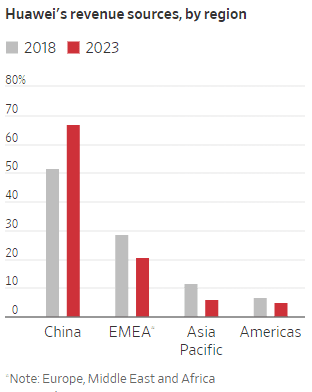

Though Huawei is still seeking to sell its products abroad in places such as Southeast Asia and Africa, it is more reliant on China’s market than ever, with 67% of revenue last year coming from domestic clients. The company often portrays itself as a national champion that gives priority to serving China.

Source: Huawei via WSJ

A WSJ investigation found more than 300 government procurement contracts worth around $5 billion specifically calling for the purchase of servers and other tech infrastructure powered by Huawei’s Kunpeng central processing units, or CPUs, in 2023. Other contracts listed Huawei CPUs among a handful of preferred local vendors. All of this was a sharp contrast to five years ago, when government agencies specifically requested products from U.S. chip makers Intel or AMD.

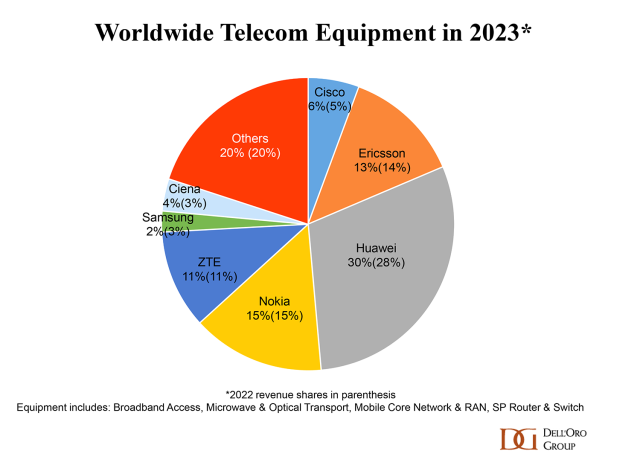

China’s buy-local policy is even more pronounced in the telecom-equipment space, Huawei’s largest revenue source. State-owned Chinese wireless carriers have largely stopped buying equipment from Huawei’s foreign rivals, Sweden’s Ericsson and Finland’s Nokia, even when one of them priced their contracts more cheaply than Chinese companies. The shift came while Sweden and other European countries indicated that they would cut Huawei and another Chinese equipment maker, ZTE, from their networks. Ericsson and Nokia held about 15% of China’s cellular network equipment market before 5G began rolling out in 2019. In China’s current 5G cellular-equipment market, Huawei holds about 4% to 5%, according to market research firm Dell’Oro.

They peg Huawei’s 2023 global telecom market share (#1) at 30% – double that of #2 Nokia as per this pie chart:

With so much government support, Huawei was able to avoid massive job and spending cuts that would have gutted its R&D or led to a talent exodus. Huawei boosted R&D spending to almost 165 billion yuan, or $23 billion, last year, up from 102 billion yuan in 2018. More than half of Huawei’s 207,000 employees are in R&D.

Huawei is now at the vanguard of China’s push to develop cutting-edge chips to wean reliance on Nvidia and Intel, as the Biden administration seeks to curb China’s ability to develop advanced chips and technology that could aid its warfare and surveillance. U.S. chip juggernaut Nvidia singled out Huawei as a top competitor in February.

Huawei is leading a government-funded project to develop memory units for advanced AI chips, people familiar with the matter said, with at least 11 national AI data centers now using Huawei chips. WSJ reports that last summer, a group of Huawei researchers gathered at a barbecue restaurant on the outskirts of Beijing to congratulate engineers who worked on the Mate 60 Pro chip set at Huawei owned HiSilicon.

“You HiSilicon people kick ass,” one of the Huawei researchers said, according to a person who attended. “Managers tell us daily that our work helps the country fight against foreign oppression,” a HiSilicon engineer who was present responded. “We’re becoming more and more like a state-owned company, aren’t we?” another researcher chimed in.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.wsj.com/business/telecom/huawei-china-technology-us-sanctions-76462031

Huawei is back – net profits more than doubled in 2023!

Dell’Oro: 2023 global telecom equipment revenues declined 5% YoY; Huawei increases its #1 position

Huawei to revolutionize network operations and maintenance

Huawei pushes 5.5G (aka 5G Advanced) but there are no completed 3GPP specs or ITU-R standards!

China’s mobile data consumption slumps; Apple’s market share shrinks-no longer among top 5 vendors