2Q-2018 Status & Direction of AT&T Communications, by CEO John Donovan

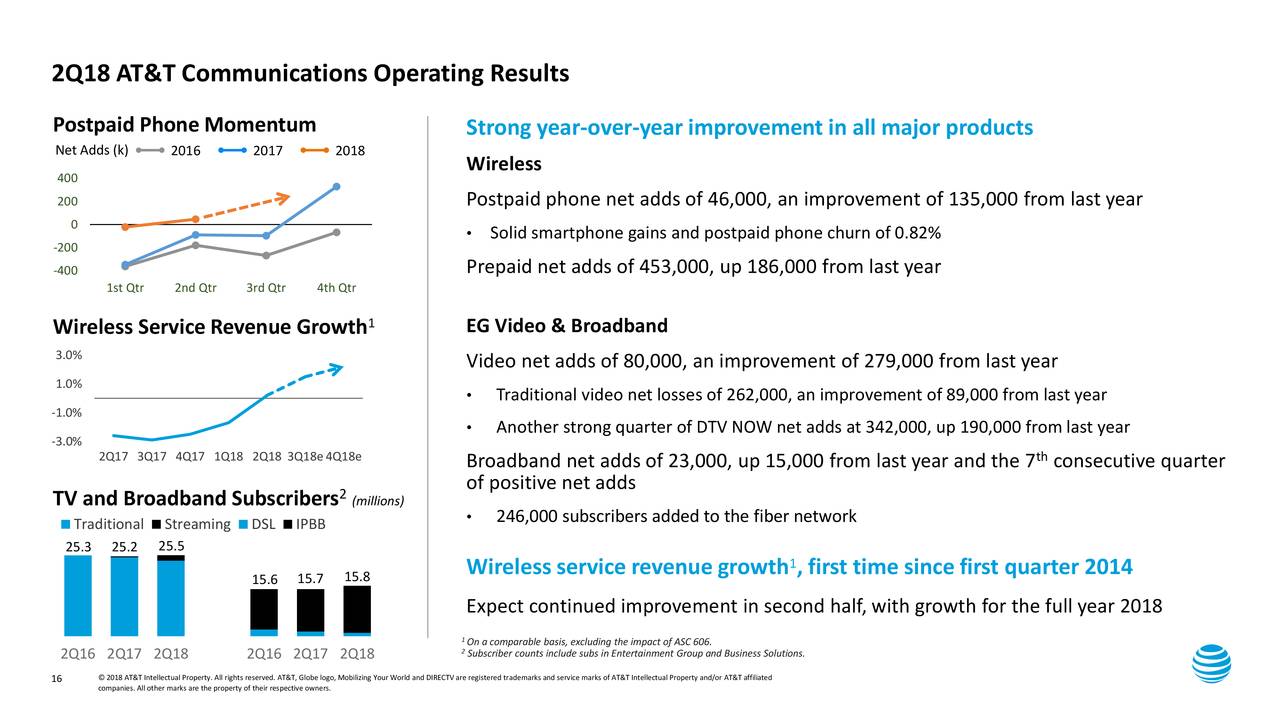

2Q-2018 for AT&T had 76,000 IP broadband net adds with 23,000 total broadband net adds. That’s the seventh consecutive quarter of broadband growth for AT&T Communications. About 95% of our consumer broadband base is now on our IP broadband as our transition from DSL is drawing to a close. Our fiber build continues at a fast clip, now passing more than 9 million customer locations, and we expect that this time next year to reach 14 million locations.

This gives us a long runway for broadband growth. We’re doing very well in our fiber markets, including a 246,000 net increase in subs on our fiber network in the second quarter.

Now I’d like to update you on several key initiatives we have underway, so we’ll turn to Slide 17. Evolving our video portfolio is top priority for us. We believe we’re well positioned as our customers move toward a more personalized set of streaming products.

Our new platform was launched in May as the DIRECTV NOW user interface, and it’s now live on all supported device operating systems and has been well received with strong engagement by customers. It offers a new cloud-based DVR and more robust video-on-demand experience with new pay-per-view options. Over time, it will bring additional advertising and data insight opportunities. This new video platform gives us flexibility to adapt to the market with new offerings and products. Late in the quarter, we added our third video offering called WatchTV, a small package of 30 live channels and 15,000 on-demand titles.

We include WatchTV in our unlimited, more wireless plans where you can purchase it for $15 a month, making it perfect for customers who want video but not at the cost of a large package. This complements DIRECTV NOW where we continue to see success in attracting cord cutters and cord severs. And later this year, we will begin testing a premium product extension, which is a streaming product that will give the full DIRECTV experience over any broadband, ours or competitors’. It will have additional benefits of an improved search and discovery feature and an enhanced user interface. We’re excited that this will complement our top-end product for those who don’t want or can’t have a satellite dish.

Our open-video platform also dovetails nicely with our ongoing focus on driving the industry’s leading cost structure. The new platform is low touch with lower acquisition costs as streaming services becomes a bigger part of our business.

Digital sales are a cost-efficient way of customer engagement, and we’re seeing double-digit growth in our digital sales and service. We’re also seeing operating expense savings from our move to a virtualized software-defined network.

More than 55% of our network functions were virtualized at the end of 2017, and we’re well on our way to meet or exceed our goal of 75% virtualized by 2020. These and other cost management initiatives have helped drive 13 straight quarters of cost reductions in our technology and infrastructure group.

Finally, I’d like to give an update on our FirstNet build and other network investments. Our FirstNet network build is accelerating. We expect to have between 12,000 and 15,000 band 14 sites on air by the end of this year 2018, and we’re ahead of our contractual commitment. And don’t forget, when we’re putting in equipment for FirstNet, we’re also deploying our AWS and WCS spectrum, utilizing the one touch, one tower approach. This approach allows all customers access to our improved network. FirstNet also gives us an opportunity to sell to first responders. So far, more than 1,500 public safety agencies across 52 states and territories have joined FirstNet, nearly doubling the network’s adoption since April.

In addition to our efforts with FirstNet, 5G and 5G Evolution work continues its development in several different areas that will pave the way to the next generation of higher speeds for our customers.

We now have 5G Evolution in more than 140 markets, covering nearly 100 million people with theoretical peak speeds of at least 400 megabits per second with plans to cover 400-plus markets by the end of this year. Our millimeter wave mobile 5G trials are also going well, and we’re on track to launch service in parts of 12 markets by the end of this year.

References:

https://seekingalpha.com/article/4189949-t-inc-2018-q2-results-earnings-call-slides

Singtel, Ericsson to launch “5G” pilot network in Singapore this year

Singtel and Ericsson will launch what is touted as Singapore’s first “5G” pilot network later this year. The 5G pilot network, scheduled to go live by the fourth quarter this year, will be deployed at one-north in Buona Vista, the city-state’s science, business and IT hub. Later this year, the network will support trials of drones and autonomous vehicle wireless communications – applications where very low latency is required.

Singtel and Ericsson will also work with enterprises at one-north to develop new 5G use cases and tap into the business potential of 5G.

NOTE: The press release incorrectly states: “Ericsson’s 3GPP standards compliant 5G technology….” As we have noted in many, many posts, 3GPP specifications are not standards and the 3GPP “5G” submission to ITU-R WP 5D for IMT 2020 won’t be completed till July 2019.

……………………………………………………………………………………………………………………………………………………………………………………………………

“5G has the potential to accelerate the digital transformation of industries, as well as empower consumers with innovative applications,” Singtel CTO Mark Chong said. “We are pleased to take another bold step in our journey to 5G with our 5G pilot network at one-north and invite enterprises to start shaping their digital future with us,” Chong added.

He told The Straights Times (see photo below):

“The location is in line with the government’s initiative to designate one-north as a test bed for autonomous vehicles and unmanned aircraft systems. For a start, we plan to conduct a drone trial on the pilot network to showcase network slicing capability.”

Aileen Chia, deputy chief executive and director-general (Telecoms & Post) at Info-Communications Media Development Authority (IMDA), described the 5G pilot network as “an encouraging step towards commercialization, with live 5G trial networks made possible with the regulatory sandbox IMDA has in place…IMDA will continue to work closely with mobile service providers such as Singtel in their journey to build communication capabilities of the future and complement Singapore’s efforts towards a vibrant digital economy.”

Last year, IMDA announced plans to let Singapore telcos test 5G services for free over two years and waived frequency fees for 5G trials until December 2019, as part of efforts to fuel 5G development in Singapore.

At the launch event on Monday, July 23rd, Singtel and Ericsson demonstrated a range of potential 5G use cases, including cutting-edge 3D augmented reality (AR) streaming over a 5G network operating in the 28-GHz millimeter wave spectrum. Participants were able to view and interact with lifelike virtual objects such as a photorealistic human anatomy and a 360-degree image of the world. The immersive experience was then streamed in real-time to a remote audience via 5G.

“5G represents a key mobile technology evolution, opening up new possibilities and applications,” said Mr Martin Wiktorin, Country Manager for Ericsson Singapore, Brunei & the Philippines. “We believe that 5G will play a key role in the digital transformation of the Singapore economy. Demonstrating the possibilities in this showcase event will be a catalyst for engagements with Singapore enterprises.”

Image courtesy of Singapore Straights Times.

……………………………………………………………………………………………………………………………………………………………………………………………………..

The 5G pilot network is the result of a joint 5G initiative Singtel and Ericsson formed last year. In October 2017, the two companies set up a joint Certificate of Entitlement (CoE) to develop 5G technology, with an initial investment of $2 million to be deployed over three years.

Besides Singtel, Singapore’s other mobile carriers have also begun conducting their own 5G trials. M1 said last month it has partnered with Huawei to run tests in the 28-GHz mmWave spectrum, with plans to conduct the first 3.5-GHz non-standalone standards compliant field trial in Southeast Asia by the end of the year, and a 28-GHz and 3.5-GHz standalone field trial by mid-2019. StarHub is also working with Huawei on its 5G network trials.’

Reference:

China Permits Virtual Telecom Operators vs Amazon Virtual Private Cloud (VPC)

China has granted the official go ahead for virtual telecom operator businesses after piloting the practice for almost five years. The China Ministry of Industry and Information Technology has issued official licenses to 15 private virtual telecoms to resell internet access, the ministry said in a statement released Monday on its website. These virtual operators, including Chinese tech giants Alibaba and Xiaomi, do not maintain the network infrastructure but rent wholesale services like roaming and text messages from the country’s three major telecom infrastructure operators China Mobile, China Unicom, and China Telecom.

In a move to further open up the telecom sector, China started to issue pilot licenses in May 2013 to private companies to allow them to offer repackaged mobile services to users. It issued pilot operation licenses to eleven ‘mobile virtual network operators’, or MVNOs, at the end of 2013 which has gradually increased to A 42 virtual telecom businesses.

Granting virtual telecom operators official licenses is aimed at encouraging mobile telecom business innovation and improving the sector’s overall service quality, the statement said.

Reference:

http://usa.chinadaily.com.cn/a/201807/23/WS5b559eb4a310796df4df82ed.html

………………………………………………………………………………………………………………………..

While Amazon is not a virtual ISP, they do offer Virtual Private Cloud (VPC) service:

To securely transfer data between an on-premises data center and Amazon Web Services (AWS), consider implementing a transit Virtual Private Cloud (VPC). Transit VPCs not only manage your networks more efficiently, but also add dynamic routing and secure connectivity in your cloud environment. Because these transit VPCs are deployed with high availability on AWS, downtime is limited.

Amazon’s VPC lets a company or enterprise provision a logically isolated section of the AWS Cloud where you can launch AWS resources in a virtual network that the user defines. The user has complete control over the enterprise virtual networking environment, including selection of IP address range, creation of subnets, and configuration of route tables and network gateways. You can use both IPv4 and IPv6 in your VPC for secure and easy access to resources and applications.

These AWS resource requests are implemented virtually and can be used to connect Amazon VPCs, whether they are running in different parts of the world and/or running in separate AWS accounts, to a common Amazon VPC that serves as a global network transit center. This approach uses host-based Virtual Private Network (VPN) appliances in a dedicated Amazon VPC and helps to simplify network management by reducing the amount of connections required to connect multiple Amazon VPCs and remote networks.

Simplify network management and reduce your total number of connections by deploying a highly available, scalable, and secure transit Virtual Private Cloud (VPC) on AWS.

Download the eBook to learn more about:

- How to build a private network that spans two or more AWS Regions

- Sharing connectivity between multiple Amazon VPCs and on-premises data centers

- How transit VPCs enable you to share Amazon VPCs and AWS resources across multiple AWS accounts

For more info please refer to https://aws.amazon.com/networking/partner-solutions/featured-partner-solutions/

Will IEEE 802.11ax be a “5G” Contender?

Note: Neither IEEE 802.11ax or 802.11ay have been presented to ITU-R WP 5D for consideration as an IMT 2020 Radio Interface Technology (RIT), which will be first evaluated at their July 2019 meeting. Hence, those future IEEE 802.11 standards will be orthogonal to IMT 2020 (the only real standard for mobile 5G). There are no official standards for 5G fixed Broadband Wireless Access (BWA). Despite what you may have read, all such “5G” BWA deployments (e.g. Verizon, C-Spire, etc) are proprietary.

IEEE 802.11ax-2019 will replace both IEEE 802.11n-2009 and IEEE 802.11ac-2013 as the next high-throughput WLAN amendment.

Summary:

The future IEEE 802.11ax standard will provide users with 5G-level speeds over Wi-Fi networks and be more economical, says a report from GlobalData. Equipment that supports a pre-standard version of IEEE 802.11ax is rolling out this year.

“The 802.11ax standard will drive a significant boost in capacity, efficiency and flexibility that should make Wi-Fi align closely with emerging 5G priorities,” GlobalData Technology Analyst John Byrne said in a press release. “The ability to support up to 12 simultaneous user streams from a single access point, 8×8 multi-user multiple input multiple output, and the use of much larger 80 MHz channels of wireless spectrum represent dramatic upgrades from the current state-of-the-art standard, 802.11ac.”

Byrne continued: “However, once the cost curve comes down, 802.11ax Wi-Fi has the potential to deliver 5G-like user experiences at a fraction of the cost of similar cellular gear. The ability to deploy Wi-Fi access points at significantly lower cost than 5G small cells offering similar performance characteristics could represent a significant selling point for Wi-Fi gear vendors.”

IEEE 802.11ax Carrier Wi-Fi:

The forthcoming IEEE standard will address challenges faced by carrier-provided Wi-Fi, including unreliability, suspect security and difficulty in integrating with cellular networks. The shift from 802.11ac to 802.11ax access points will begin as the cost curve falls through 2022. The equalization of 5G and Wi-Fi technology and 802.11ax’s lower cost could “represent a significant selling point for Wi-Fi gear vendors,” Byrne said.

Technology vendors believe that IEEE 802.11ax could be a big commercial success . In January 2018, Starry and Marvel said they would team to develop fixed wireless technologies. The deal includes the Starry millimeter wave integrated circuit and cloud management software and Marvel’s 802.11ax chipsets.

Aerohive plans to deliver its first 802.11ax access points in mid-2018. PCTel said in January that it haddeveloped a reference design for 802.11ax antennas for an unnamed “major 802.11ax Wi-Fi chipset manufacturer.” There’s a lot of chipset activity in particular, with Qualcomm already having launched its “802.11ax-ready” Atheros WCN3998 chipset in February and other companies like Intel laying out plans to begin offering chips this year. Chip company Skyworks is collaborating with Broadcom with modules integrated into Broadcom’s Max Wi-Fi 802.11ax solution and claims that its 2.4 and 5 GHz 802.11ax modules and Broadcom’s Max WiFi solutions “provide four times faster download speeds, six times faster upload speeds, enhanced coverage and up to seven times longer battery life when compared to 802.11ac Wi-Fi products available in the market today.” ABI Research has noted that in addition to those vendors, Marvell, Quantenna and Celeno have also made 802.11ax chipset announcements — mostly targeting the access point space — and that AP companies such as Asus, D-Link and Huawei have already put out 802.11ax-ready APs and gateways.

References:

http://en.ctimes.com.tw/DispNews.asp?O=HK27J9UJV4CSAA00NT

http://www.ieee802.org/11/Reports/tgax_update.htm

https://ieeexplore.ieee.org/document/7792393/

https://ieeexplore.ieee.org/document/7422404/

https://www.rcrwireless.com/20180322/wireless/802-11ax-is-on-its-way

South Korean Mobile Operators to Launch 5G Simultaneously on Korea 5G Day

South Korea is said to be just behind China in the race to be first to deploy 5G service at scale. South Korean mobile operators have now all agreed to launch 5G services on the same day in order to avoid excessive competition.

SK Telecom, KT and LG Uplus will all launch services on “Korea 5G Day,” which they expect to hold some time around March next year, the Korea JoongAng Daily reported.

The arrangement was fostered by the nation’s Ministry of Science and ICT during a meeting on Tuesday, July 17th. Minister You Young-min asked the operators to co-operate closely to ensure that Korea is the world’s first country to commercialize 5G, and to avoid excessive competition. At the meeting, representatives of the operators urged the government to introduce measures to help operators cope with the major investments required to deploy 5G networks and support the introduction of future technologies such as automated vehicles. Other suggestions included tax benefits for 5G investments, the newspaper report states.

From left, LG U+ CEO and Vice Chairman Ha Hyun-hwoi, KT CEO Hwang Chang-gyu, Minister of Science and ICT You Young-min and SK Telecom CEO Park Jung-ho meet in Yeouido, western Seoul, on Tuesday. [MINISTRY OF SCIENCE AND ICT]

…………………………………………………………………………………………………………………………………………………………………………………………………….

Minister You added that the government’s push toward lowering household phone bills will hold even in the 5G era and asked carriers to come up with wise phone plan options.

During the meeting, KT CEO Hwang Chang-gyu said 5G commercialization calls for big investments as the network will be used to support many business-to-business services, unlike the current 4G network that was used mostly to support services targeting consumers. The 5G networks are expected to be the backbone of future businesses like self-driving cars and Internet of Things technology, where network stability is crucial to guaranteeing safety and security.

“The government should help ease some difficulties faced by the telecommunications industry and support investment in 5G,” Hwang added.

According to the Science Ministry, Hwang asked for tax benefits when setting up 5G network infrastructure to ease the burden on companies and the minister said he will consider the possible options.

SK Telecom CEO Park Jung-ho said the company is researching what changes 5G could bring to the world and added that he is particularly interested in 5G’s possible impact on the media industry.

LG U+ CEO Ha Hyun-hwoi, on his first full day on the job, showed up for the meeting. Though former CEO Kwon Young-soo was originally scheduled to take part, Ha said he decided to participate considering the importance of 5G business and to listen to the policy directions of the Science Ministry regarding the network.

Telstra, Ericsson, Intel complete “5G” data call using 3GPP New Radio

Australian network operator Telstra, Ericsson and Intel announced they have jointly completed the first end-to-end 3GPP non-standalone “5G” data call on a commercial network in a multi-vendor setup. The trial at Telstra’s 5G Innovation Centre on Australia’s Gold Coast used licensed 3.5-GHz spectrum, and Ericsson’s “5G” New Radio, baseband and packet core solution, a Telstra SIM and the Intel 5G Mobile Trial Platform. It involved a network connection to an Ericsson virtualized 5G packet core running on Ericsson’s network functions virtualization (NFV) infrastructure. The 5G slice was then connected into the existing Telstra 4G mobile network.

Ericsson and Intel jointly completed the first lab-based end-to-end non-standalone 5G data call earlier this month, and the live demonstration builds on this milestone.

“Demonstrating this 5G data call end-to-end using my own personal SIM card on Telstra’s mobile network is the closest any provider has come to making a ’true’ 5G call in the real world-environment, and marks another 5G first for Telstra,” Telstra group managing director for networks Mike Wright said.

Previous “5G” experiments have included the first 5G data call over 26-GHz spectrum, Australia’s first 5G connected vehicle trial and its first 5G mobile gaming demonstration.

“We continue to work with global technology companies Ericsson and Intel as well as global standards bodies to advance the deployment of commercial 5G capability in Australia,” Wright concluded.

Intel Next Generation and Standards vice president and general manager Asha Keddy said the tech giant would continue working on 5G use cases and trials ahead of the launch of Telstra’s 5G network in 2019.

References:

Analysys Mason: Public WiFi to add $20B to India’s GDP

Public Wi-Fi can play a key role in driving ubiquitous connectivity and digital inclusion in India, as explored in an Analysys Mason report – ‘Accelerating connectivity through public Wi-Fi: Early lessons from the railway Wi-Fi project.’

Despite fast increases in number of people connected (316 million at the end of 2017, compared to 200 million the previous year), mobile broadband penetration in India stood at only 31% at the end of 2017, still significantly behind many of India’s peers. The report, prepared through the lens of Google and Railtel Public Wi-Fi project, support the Government’s ambition under the draft NDCP to reach 5 million access points in 2020 and 10 million in 2022, to provide an all-pervasive coverage and internet connectivity, for 600 million Indians.

David Abecassis, partner at Analysys Mason, said: “In the last few years, India has made significant progress in driving mobile data usage, thanks to improved networks, and low cost data. But to really achieve the connected India vision, India will need to further invest in developing public Wi-Fi as a complement to mobile and fiber broadband.”

According to Abecassis, the Google and RailWire project to deploy high speed Wi-Fi across 400 stations has shown that there was a technical and operational solution to providing high-quality public Wi-Fi to millions of Indians nationwide, on affordable terms.

“The success of this rollout and Reliance Jio’s 80,000 public Wi-Fi access points as of mid-2017 provided valuable insights in further developing public Wi-Fi as a service that can truly achieve the Digital India vision,” he added.

The report further outlines an opportunity to develop a wider connectivity ecosystem with Public Wi-Fi as a key component, which can not only benefit users and wireless ISPs, but also telecom service providers, handset manufacturers and venue owners. ISPs can benefit by monetizing demand for faster mobile broadband and higher data volumes on their networks, as people get used to fast speeds and ubiquitous connectivity.

Analysis Mason found that around 100 million people would be willing to spend an additional USD 2 to 3 billion per year on handsets and cellular mobile broadband services, as a result of experiencing fast broadband on public Wi-Fi. In addition to driving productivity improvements from high speed Wi-Fi for the overall economy, public Wi-Fi can also translate into tangible benefits to GDP, by around USD 20 billion between 2017-19 and at least billion per annum thereafter.

References:

Google’s Internet Access for Emerging Markets – Managed WiFi Network for India Railways

Brookings Institute 5G Game Plan for the U.S. vs Opinion

Can the U.S. catch up with China and South Korea, which are paving the way forward to deploy 5G wireless networks (whatever that means?)

Here’s what the Brookings Institute recommends for the U.S. 5G effort:

U.S. 5G deployment process is slowed by outdated regulatory processes, spectrum scarcity, and local bureaucracy related to building local towers and other infrastructure. The U.S. faces unique challenges associated with the deployment of small cells, which are antennae the size of a pizza box that enable 5G’s signal strength and resiliency. Deployment delays also result from approval times on small cell applications, permitting, and zoning processes at the local level.

While the U.S. has correctly identified 5G leadership as an important goal, a coordinated, comprehensive, and focused approach by Congress, state and local leaders, and the private sector will be needed. Currently, municipalities, states, industry, and other government agencies in the U.S. lack a comprehensive and synchronized strategy, or what I call a “5G game plan,” that harmonizes the goals of public policies, investments, and the public interest.

While having a common goal should be the foundation of any proposed 5G game plan, the framework for this discussion should also prioritize the following three points.

1. The U.S. must rapidly adopt complementary public policies with timelines that address ongoing spectrum shortage concerns.

Higher frequency spectrum will be the lifeblood for advanced wireless networks. Both the House and Senate have recently introduced the bipartisan AIRWAVES Act to expedite the creation of a pipeline of spectrum for 5G by requiring the FCC and the National Telecommunications and Information Administration to make it available across a variety of frequencies, including low-, mid-, and high-bands. While the current legislation has broad bipartisan appeal, it’s important for Congress to act in a timely way. The AIRWAVES Act complements the recent enactment of the RAYBAUM and MOBILE NOW Acts as part of the 2018 omnibus appropriations bill, which paves the way for future auctions and speeds up 5G infrastructure.

Concurrently, the FCC also has the opportunity to bring much-needed mid-band spectrum to market by adopting rules for the 3.5 gigahertz band that will promote 5G deployments. At its July meeting, the FCC launched a proceeding that has the potential to free up hundreds of megahertz of mid-band spectrum in the 3.7 to 4.2 gigahertz band. The agency is also making available high-band spectrum that will, among other things, help free up more millimeter-wave spectrum bands, improve operability requirements within 24 gigahertz bands, and adopt a sharing framework for terrestrial and fixed satellite services.

While all of these actions can address spectrum scarcity concerns, U.S. policymakers and agencies at all levels need to collaborate to hasten the availability of spectrum for commercial wireless use. They also need to work toward short- and long-term coordinated plans that may render even better and faster results.

2. The deployment of small cell technologies must become a priority to accelerate 5G infrastructure.

It is equally important that local, federal, and industry stakeholders work collaboratively on small cell deployment, which is the technical architecture required at the local level. With more than 89,000 local governments in the U.S., policymakers must strike a balance that harmonizes and expedites processes and approvals, and still provides specific localities, especially tribal lands, the ability to provide guidance on safety and aesthetics.

To this end, policymakers should identify and work on laws and regulations at the municipal, state, and federal levels that effectuate a 5G game plan. Jurisdictions without a plan should employ strategies for advancing wireless networks rather than delay the deployment of next-generation mobile networks for their residents, including updates to the guiderails for state and local siting. As of June 1, 2018, 20 states have enacted legislation modernizing regulations to facilitate small cell deployment, and more should follow suit.

Congress is also taking its own steps to expedite 5G readiness. Last month, Senate Commerce Committee Chairman John Thune (R-SD) and Communications Subcommittee Ranking Member Brian Schatz (D-HI) introduced legislation to speed up small cell deployment called the Streamlining the Rapid Evolution and Modernization of Leading-Edge Infrastructure Necessary to Enhance Small Cell Deployment Act (or STREAMLINE Small Cell Deployment Act). The legislation creates a shot clock between 60 and 90 days for state and local governments to decide on industry applications for small cell installation. If the entity misses the deadline, the application would be automatically approved. The legislation also ensures that localities don’t foot the bill for installation of small cells, and requires reasonable cost-based fees for processing applications. Finally, the bill calls for a GAO study on the important issue of identifying barriers to broadband deployment on tribal lands.

While there are legitimate concerns from municipalities about unfair burdens and deadlines, political dogma should not overtake this issue. If passed, the STREAMLINE Small Cell Deployment Act may go a long way toward finding a balance between local entities, the federal government, and the private sector to avoid burdensome application processes, unfair and disparate fee structures between localities, and difficult compliance requirements for municipalities. Moving forward, these issues require a multi-stakeholder approach where policymakers and practitioners can embrace the ultimate benefits of 5G deployment, particularly those that will accrue social and economic value back to constituents.

3. Stakeholders involved in 5G deployment must keep top of mind the economic and social good that these next-generation networks can deliver.

The final leg of the 5G game plan is to ensure that efforts are ultimately promoting economic and social good. For example, 5G networks can enhance healthcare through the integration of electronic and digital devices (e.g., sensors, smartphones), in upward of $650 billion savings by 2025 provided that faster and more reliable networks enable new technologies, according to a report commissioned by Qualcomm. From medical internet of things devices to online consultations, the capture of real-time medical information and data analytics will empower the healthcare sector, patients, and government to find remedies for skyrocketing costs.

In the healthcare industry and other sectors, 5G can reduce costs for the governments that deploy these networks, the consumers who are in need of additional savings (especially for public interest applications and services), and the enterprises that desire a faster access to the global marketplace.

These three points are not meant to be exhaustive, but a starting point for building a sustainable, competitive, and resilient 5G game plan. The game plan should also include proposals on policies that accelerate fiber availability and regulatory permissions that should go to wireline providers that are also critical to 5G deployment.

But what should be evident is that without a plan that addresses both the priorities of multiple stakeholders as well as the technical requisites of this emerging technology, the U.S. will not be 5G-ready, thereby falling behind our global competitors who seek dominance in the ecology driving the next-generation of wireless networks.

Christoph Mergerson contributed research to this blog post.

Alan’s Opinion:

First, we have to define and classify 5G while identifying the critically important use cases. Instead of doing that, wireless carriers have been making noise, promoting nonsense, hype and spin over their proprietary higher speed wireless networks, e.g. fixed BWA, mobile 5G, 5G backhaul from a WiFi hotspot, etc.

Next, carriers MUST respect and not ignore the true 5G standards, from accredited standards bodies such as ITU-R, ITU-T, and IEEE 802.11. The 5G standards (especially IMT 2020 radio and non radio aspects) from those organizations won’t be completed for a couple more years but they will eventually take over from all the proprietary 5G offerings from 2018-to-2020. If that doesn’t happen, 5G won’t scale to serve a large number of users and the technology will be DOA!

IHS Markit: CSPs accelerate high speed Ethernet adapter adoption; Mellanox doubles switch sales

by Vladimir Galabov, senior analyst, IHS Markit

Summary:

High speed Ethernet adapter ports (25GE to 100GE) grew 45% in 1Q18, tripling compared to 1Q17, with cloud service provider (CSP) adoption accelerating the industry transition. 25GE represented a third of adapter ports shipped to CSPs in 1Q18, doubling compared to 4Q17. Telcos follow CSPs in their transition to higher networking speeds and while they are ramping 25GE adapters, they are still using predominantly 10GE adapters, while enterprises continue to opt for 1GE, according to the Data Center Ethernet Adapter Equipment report from IHS Markit.

“We expect higher speeds (25GE+) to be most prevalent at CSPs out to 2022, driven by high traffic and bandwidth needs in large-scale data centers. By 2022 we expect all Ethernet adapter at CSP data centers to be 25GE and above. Tier 1 CSPs are currently opting for 100GE at ToR with 4x25GE breakout cables for server connectivity,” said Vladimir Galabov, senior analyst, IHS Markit. “Telcos will invest more in higher speeds, including 100GE out to 2022, driven by NFV and increased bandwidth requirements from HD video, social media, AR/VR, and expanded IoT use cases. By 2022 over two thirds of adapters shipped to telcos will be 25GE and above.”

CSP adoption of higher speeds drives data center Ethernet adapter capacity (measured in 1GE port equivalents) shipped to CSPs to hit 60% of total capacity by 2022 (up from 55% in 2017). Telco will reach 23% of adapter capacity shipped by 2022 (up from 15% in 2017) and enterprise will drop to 17% (down from 35% in 2017).

“Prices per 1GE ($/1GE) are lowest for CSPs as higher speed adapters result in better per gig economies. Large DC cloud environments with high compute utilization requirements continually tax their networking infrastructure, requiring CSPs to adopt high speeds at a fast rate,” Galabov said.

Additional data center Ethernet adapter equipment market highlights:

· Offload NIC revenue was up 6% QoQ and up 55% YoY, hitting $160M in 1Q18. Annual offload NIC revenue will grow at a 27% CAGR out to 2022.

· Programmable NIC revenue was down 5% QoQ and up 14% YoY, hitting $26M in 1Q18. Annual programmable NIC revenue will grow at a 58% CAGR out to 2022.

· Open compute Ethernet adapter form factor revenue was up 11% QoQ and up 56% YoY, hitting $54M in 1Q18. By 2022, 21% of all ports shipped will be open compute form factor.

· In 1Q18, Intel was #1 in revenue market share (34%), Mellanox was #2 (23%), and Broadcom was #3 (14%)

Data Center Compute Intelligence Service:

The quarterly IHS Markit “Data Center Compute Intelligence Service” provides analysis and trends for data center servers, including form factors, server profiles, market segments and servers by CPU type and co-processors. The report also includes information about Ethernet network adapters, including analysis by adapter speed, CPU offload, form factors, use cases and market segments. Other information includes analysis and trends of multi-tenant server software by type (e.g., server virtualization and container software), market segments and server attach rates. Vendors tracked in this Intelligence Service include Broadcom, Canonical, Cavium, Cisco, Cray, Dell EMC, Docker, HPE, IBM, Huawei, Inspur, Intel, Lenovo, Mellanox, Microsoft, Red Hat, Supermicro, SuSE, VMware, and White Box OEM (e.g., QCT and WiWynn).

………………………………………………………………………………………………………………………………………….

Mellanox Ethernet Switches for the Data Center:

In the Q1 2018 earnings call, Mellanox reported that its Ethernet switch product line revenue more than doubled year over year. Mellanox Spectrum Ethernet switches are getting strong traction in the data center market. The recent inclusion in the Gartner Magic Quadrant is yet another milestone. There are a few underlying market trends that is driving this strong adoption.

Network Disaggregation has gone mainstream

Mellanox Spectrum switches are based off its highly differentiated homegrown silicon technology. Mellanox disaggregates Ethernet switches by investing heavily in open source technology, software and partnerships. In fact, Mellanox is the only switch vendor that is part of the top-10 contributors to open source Linux. In addition to native Linux, Spectrum switches can run Cumulus Linux or Mellanox Onyx operating systems. Network disaggregation brings transparent pricing and provides customers a choice to build their infrastructure with the best silicon and best fit for purpose software that would meet their specific needs.

25/100GbE is the new 10/40GbE

25/100GbE infrastructure provides better RoI and the market is adopting these newer speeds at record pace. Mellanox Spectrum silicon outperforms other 25GbE switches in the market in terms of every standard switch attribute.

FCC: 5G-High Band Spectrum Auctions Coming this November

FCC Chairman Ajit Pai says the first two 5G-specific high-band spectrum auctions in the U.S. will be in November, with more to follow in 2019. The FCC auctions will sell off the 28GHz millimeter wave (mmWave) band, with the bidding expected to start November 14, and the 24GHz band to be sold off “immediately afterward,” Pai said. He announced the auctions on a blog on Medium. The Federal Communications Commission (FCC) will vote to finalize the rules on the auctions at meeting on August 2.

“With so many wanting so much spectrum for 5G, we’re moving as quickly as possible to make these bands available for commercial use,” the FCC chairman wrote. Pai expects to hold 3 more millimeter wave auctions in the 2nd half of 2019 in the 37GHz, 39GHz, and 47GHz bands. “To help facilitate that auction on this timeline, I’m proposing rules to clean up the 39 GHz band and move incumbents into rationalized license holdings,” Pai writes. He didn’t say exactly how much spectrum will be auctioned yet, but the scale and scope of these planned high-band auctions appear to promise to open up the largest tranche of spectrum for wireless broadband yet seen in the U.S.

“5G has the potential to have an enormously positive impact on American consumers,” Pai said in a statement to USA TODAY. “High-speed, high-capacity wireless connectivity will unleash new innovations to improve our quality of life. It’s the building block to a world where everything that can be connected will be connected — where driverless cars talk to smart transportation networks and where wireless sensors can monitor your health and transmit data to your doctor. That’s a snapshot of what the 5G world will look like.”

The FCC is focused on making additional low-, mid-, and high-band spectrum available for 5G services.

- Low-band: Deploying service in 600 MHz bands post incentive auction.

- Mid-band: Exploring a shared service framework in the 3.5 GHz band and developing next steps for terrestrial use in the 3.7 GHz band.

- High-band: Unleashing spectrum at the frontiers of the spectrum chart, including pursuing millimeter wave spectrum for 5G terrestrial use and looking forward to spectrum auctions in 28 and 24 GHz bands.

At its regular monthly meeting Thursday, the FCC will also vote on on a proposal to allow 5G use for mid-band spectrum. This Fall’s upcoming series of high-band spectrum auctions, Pai said, will “make it easier to deploy the physical infrastructure that will be critical to the 5G networks of the future, I believe that the United States is well positioned to lead the world in 5G. … The large amount of spectrum that the FCC will make available for commercial use will enable the private sector to bring the next generation of wireless connectivity to American consumers.”

In July 2016, the FCC said that it planned to open up 3.85GHz of licensed spectrum in the 28GHz, 37GHz, and 39GHz band. The agency later voted to add 700MHz in the 24GHz band, and nearly 1GHz in the 47GHz band.

This would be an embarrassment of radio riches compared to earlier low-band 4G auctions. The 600MHz auction in 2017 offered 108MHz of spectrum nationwide.

High-band millimeter wave spectrum is expected to be a cornerstone of future gigabit-speed 5G network services. AT&T Inc, Verizon Wireless and T-Mobile US Inc. have all tested 28GHz spectrum for fixed or mobile services, sometimes both.

The August FCC meeting should further clarify exactly what will be offered in the forthcoming auctions. One question is whether T-Mobile and Sprint will be allowed to participate in the new auctions, which would likely enable them to build out a 5G pre-standard network in 2019 and in later years.

References:

https://www.lightreading.com/first-5g-specific-us-spectrum-auctions-coming-november/d/d-id/744609?