Cloud Computing Giants Growth Slows; Recession Looms, Layoffs Begin

Among the megatrends driving the technology industry, cloud computing has been a major force. But for the first time in its brief history, the cloud has grown stormy as third-quarter cloud giant earnings details made very clear:

- Amazon Web Services (AWS) fell short of the mark on both earnings and revenue. Reports say parent Amazon.com (AMZN) has frozen hiring at its cloud computing unit and will be laying off 10,000 employees.

- Microsoft’s (MSFT) Azure cloud business at posted an unexpected slowdown in cloud computing growth. At Microsoft, “Intelligent Cloud” revenue rose 24% to $25.7 billion during the company’s fiscal first quarter, including Azure’s 35% growth to $14.4 billion. Excluding the impact of currency exchange rates, Azure revenue climbed 42%

- Alphabet’s (GOOGL) Google Cloud business came in ahead of forecasts, but Oppenheimer analyst Tim Horan said in a note to clients that it has “no line of sight to meaningful profits.”

Note: We don’t consider Facebook/Meta Platforms a cloud service provider, even though they build the IT infrastructure for their cloud resident data centers. They are first and foremost a social network provider that’s now desperately trying to create a market for the Metaverse, which really does not exist and may never be!

In late October, Synergy Research reported that Amazon, Microsoft and Google combined had a 66% share of the worldwide cloud services market in the 3rd quarter, up from 61% a year ago. Alibaba and IBM placed fourth and fifth, respectively according to Synergy. In aggregate, all cloud service providers excluding the big three have tripled their revenues since late 2017, yet their collective market share has plunged from 50% to 34% as their growth rates remain far below the market leaders.

In 2022, capital spending on internet data centers by the three big cloud computing companies will jump a healthy 25% to $74 billion, estimates Dell’Oro Group. In 2023, spending on warehouse-size data centers packed with computer servers and data storage gear is expected to slow. Dell’Oro puts growth at just 7%, which would take the market up to $79 billion.

Oppenheimer’s Horan wrote, “Cloud providers remain very bullish on long-term trends, but investors have been surprised at how economically sensitive the sector is. “Sales cycles in cloud services have elongated and customers are looking to cut cloud spending by becoming more efficient. Despite the deceleration, cloud is now a $160 billion-plus industry. But investors will be concerned given this is our first real cloud recession, which makes forecasts difficult.”

“This macro slowdown clearly will impact all aspects of tech spending over the next 12 to 18 months. Cloud spending is not immune to the dark macro backdrop as seen during earnings season over the past few weeks,” Wedbush analyst Daniel Ives told Investor’s Business Daily via an email. “That said, we estimate 45% of workloads have moved to the cloud globally and (the share is) poised to hit 70% by 2025 in a massive $1 trillion shift. Enterprises will aggressively push to the cloud and we do not believe this near-term period takes that broader thesis off course. The near-term environment is more of a speed bump rather than a brick wall on the cloud transformation underway. Microsoft, Amazon, Google, IBM (IBM) and Oracle (ORCL) will be clear beneficiaries of this cloud shift over the coming years and will power through this Category 5 (hurricane) economic storm.”

Bank of America expects a boost from next-generation cloud services that cater to “edge computing.” Amazon, Microsoft and Google are “treating the edge as an extension of their public cloud,” said a BofA report. The giant cloud computing companies have all partnered with telecom firms AT&T (T), Verizon (VZ) and T-Mobile US (TMUS). Their aim to embed their cloud services within 5G wireless networks. “Telcos are leveraging the hyperscale cloud to launch their own edge compute businesses,” BofA said.

At BMO Capital Markets, analyst Keith Bachman says investors need to reset their expectations as the coronavirus pandemic eases. The corporate switch to working from home spurred demand for cloud services. Online shopping boomed. And consumers turned to internet video and online gaming for entertainment.

“We think many organizations accelerated the journey to the cloud as Covid and hybrid work requirements exposed weaknesses in existing on-premise IT capabilities,” Bachman said in a note. “While spend remains healthy in the cloud category, growth has decelerated for the past few quarters. We believe economic forces are at work as well as a slower pace of cloud migrations post-Covid.”

Market research heavyweight Gartner updated its global cloud computing growth forecast Oct. 31. The new forecast was completed before third-quarter earnings were released by Amazon, Microsoft and Google. Gartner forecasted worldwide end-user spending on public cloud services will grow 20.7% in 2023 to $591.8 billion. That’s up from 18.8% growth in 2022.

In a press release, Gartner analyst Sid Nag cautioned: “Organizations can only spend what they have. Cloud spending could decrease if overall IT budgets shrink, given that cloud continues to be the largest chunk of IT spend and proportionate budget growth.

AWS, Microsoft Azure and Google’s cloud computing units are all growing at an above-industry-average rate. Still, AWS and Azure are slowing, perhaps a bit due to size as well as the economy.

- At Wolfe Research, MSFT stock analyst Alex Zukin said in his note: “The damage in Microsoft’s case came from another Azure miss in the quarter, but the bigger surprise was the guide of 37%. That is the largest sequential growth deceleration on record.”

- Google’s cloud computing revenue rose 38% to $6.28 billion. That’s up 2% from the previous quarter and topped estimates from GOOGL stock analysts by 4%. However, the company reported an operating loss of $644 million for the cloud business versus a $699 million loss a year earlier. Hoping to take market share from bigger AWS and Microsoft’s Azure, Google has priced cloud services aggressively, analysts say. It also stepped up hiring and spending on data centers. And it acquired cybersecurity firm Mandiant for $5.4 billion.

- “Amazon noted it has seen an uptick in AWS customers focused on controlling costs and is working to help customers cost-optimize,” Amazon stock analyst Youssef Squali at Truist Securities said in a report to clients. “The company is also seeing slower growth from certain industries (financial services, mortgage and crypto sectors),” he added.

- Oppenheimer’s Horan estimates that AWS will produce $13.9 billion in free cash flow in 2022. But he sees Google’s cloud unit having $10.6 billion in negative free cash flow.

Nonetheless, Deutsche Bank analyst Brad Zelnick remains upbeat on the cloud computing business. He wrote in a research note:

“We see a temporary slowdown in bringing new workloads to the cloud, though importantly not a change in organizations’ long-term cloud ambitions. The near-term forces of optimization can obscure what we believe remain very supportive underlying trends. We remain confident that we are in the early innings of a generational shift to cloud.”

References:

The First Real Cloud Computing Recession Is Here — What It Means For Tech Stocks

Synergy: Q3 Cloud Spending Up Over $11 Billion YoY; Google Cloud gained market share in 3Q-2022

AST SpaceMobile Deploys Largest-Ever LEO Satellite Communications Array

AST SpaceMobile, the company building the first and only space-based cellular broadband network accessible directly by standard mobile phones, announced today that it had successfully completed deployment of the communications array for its test satellite, BlueWalker 3 (“BW3”), in orbit.

BW3 is the largest-ever commercial communications array deployed in Low Earth Orbit (LEO) and is designed to communicate directly with cellular devices via 5G frequencies (which have yet to be standardized by ITU-R in M.1036 revision 6).

The satellite spans 693 square feet in size, a design feature critical to support a space-based cellular broadband network. The satellite is expected to have a field of view of over 300,000 square miles on the surface of the Earth.

The unfolding of BW3 was made possible by years of R&D, testing and operational preparation. AST SpaceMobile has a portfolio of more than 2,400 patent and patent-pending claims supporting its space-based cellular broadband technology. Additional details on the BlueWalker 3 mission can be seen in this video.

“Every person should have the right to access cellular broadband, regardless of where they live or work. Our goal is to close the connectivity gaps that negatively impact billions of lives around the world,” said Abel Avellan, Chairman and Chief Executive Officer of AST SpaceMobile. “The successful unfolding of BlueWalker 3 is a major step forward for our patented space-based cellular broadband technology and paves the way for the ongoing production of our BlueBird satellites.”

AST SpaceMobile has agreements and understandings with mobile network operators (“MNOs”) globally that have over 1.8 billion existing subscribers, including a mutual exclusivity with Vodafone in 24 countries. Interconnecting with AST SpaceMobile’s planned network will allow MNOs, including Vodafone Group, Rakuten Mobile, AT&T, Bell Canada, MTN Group, Orange, Telefonica, Etisalat, Indosat Ooredoo Hutchison, Smart Communications, Globe Telecom, Millicom, Smartfren, Telecom Argentina, Telstra, Africell, Liberty Latin America and others, the ability to offer extended cellular broadband coverage to their customers who live, work and travel in areas with poor or non-existent cell coverage, with the goal of eliminating dead zones with cellular broadband from space.

“We want to close coverage gaps in our markets, particularly in territories where terrain makes it extremely challenging to reach with a traditional ground-based network. Our partnership with AST SpaceMobile – connecting satellite directly to conventional mobile devices – will help in our efforts to close the digital divide,” said Luke Ibbetson, Head of Group R&D, Vodafone and an AST SpaceMobile director.

Tareq Amin, CEO of Rakuten Mobile and Rakuten Symphony and an AST SpaceMobile director, added “Our mission is to democratize access to mobile connectivity: That is why we are so excited about the potential of AST SpaceMobile to support disaster-readiness and meet our goal of 100% geographical coverage to our customers in Japan. I look forward not only to testing BW3 on our world-leading cloud-native network in Japan, but also working with AST SpaceMobile on integrating our virtualized radio network technology to help bring connectivity to the world.”

Chris Sambar, President – Network, AT&T, added “We’re excited to see AST SpaceMobile reach this significant milestone. AT&T’s core mission is connecting people to greater possibilities on the largest wireless network in America. Working with AST SpaceMobile, we believe there is a future opportunity to even further extend our network reach including to otherwise remote and off-grid locations.”

About AST SpaceMobile:

AST SpaceMobile is building the first and only global cellular broadband network in space to operate directly with standard, unmodified mobile devices based on our extensive IP and patent portfolio. Our engineers and space scientists are on a mission to eliminate the connectivity gaps faced by today’s five billion mobile subscribers and finally bring broadband to the billions who remain unconnected. For more information, follow AST SpaceMobile on YouTube, Twitter, LinkedIn and Facebook. Watch this video for an overview of the SpaceMobile mission.

References:

Musk’s SpaceX and T-Mobile plan to connect mobile phones to LEO satellites in 2023

New developments from satellite internet companies challenging SpaceX and Amazon Kuiper

Quantum Technologies Update: U.S. vs China now and in the future

The quantum computing market could be worth up to $5 billion by 2025, driven by competition between the US and China, according to London-based data analytics fir GlobalData whose Patent Analytics Database reveals that the U.S. is the global leader in quantum computing. The analytics company notes that China is currently about five years behind the U.S., and the recently passed U.S. CHIPS and Science Act will enhance U.S. quantum capabilities while hindering China.

Sidebar; What is a Quantum Computer:

Unlike a classical computer, which performs calculations one bit or word at a time, a quantum computer can perform many calculations concurrently. Quantum computers use a basic memory unit called a qubit, which has the flexibility to represent either zero, one or both at the same time. This ability of an object to exist in more than one form at the same time is known as superposition. The concept of entanglement is when multiple particles in a quantum system are connected and affect each other. If two particles become entangled, they can theoretically transmit and receive information over very long distances. However, the transmission error rates have yet to be determined.

Because quantum computers’ basic information units can represent all possibilities at the same time, they are theoretically much faster and more powerful than the regular computers we are used to.

Physicists in China recently launched a quantum computer they said took 1 millisecond to perform a task that would take a conventional computer 30 trillion years.

The aforementioned U.S. CHIPS and Science Act, signed into law in August 2022, represents an escalation in the growing tech war between the U.S. and China. The act includes measures designed to cut off China’s access to US-made technology. In addition, new export restrictions were announced on October 10, some of which took immediate effect. These restrictions prevent the export of semiconductors manufactured using US equipment to China. Currently, the U.S. is negotiating with allied nations to implement similar restrictions. Included in the CHIPS Act is a detailed package of domestic funding to support US quantum computing initiatives, including discovery, infrastructure, and workforce.

Among the many commercial companies researching the technology, IBM, Alphabet (parent company of Google), and Northrop Grumman have filed the most patents, with a respective 1,885, 1,000, and 623 total publications.

Earlier this week, IBM unveiled the largest quantum bit count (433 qubits) of its quantum computers to date, named Osprey, at this week’s IBM Quantum Summit. The company also introduced its latest modular quantum computing system.

“The new 433 qubit ‘Osprey’ processor brings us a step closer to the point where quantum computers will be used to tackle previously unsolvable problems,” IBM SVP Darío Gil said in a statement.

The IBM Osprey more than tripled the qubit count of its predecessor — the 127-qubit Eagle processor, launched in 2021. “Like Eagle, Osprey includes multi-level wiring to provide flexibility for signal routing and device layout, while also adding in integrated filtering to reduce noise and improve stability,” Jay Gambetta, VP of IBM Quantum wrote in a blog post.

The company claims Osprey is more powerful to run complex computations and the number of classical bits needed to represent a state on this latest processor far exceeds the total number of atoms in the known universe.

Gambetta noted IBM has been following along its quantum technology development roadmap. The company put its first quantum computer on the cloud in 2016 and aims to launch its first 1000-plus qubit quantum processor (Condor) next year and a 4000-plus qubit processor around 2025.

The US government has committed $3 billion in funding for federal quantum projects, which are either being planned or already underway, including the $1.2 billion National Quantum Computing initiative. In addition, the U.S. government almost certainly conducts quantum projects in secret through the Defense Advanced Research Projects Agency (DARPA) and the National Security Agency (NSA).

The U.S. government has committed $3bn in funding to federal quantum projects that are either already in train or being planned. The biggest project is the $1.2bn U.S. National Quantum Computing Initiative. Of course, the military and security services will be assiduously tending their own quantum gardens.

As expected, considerably less is known about China’s advancements and investments in quantum technology. The country proclaims itself to be the world-leader in secure quantum satcoms. The CCP (which runs the People’s Republic of China or PRC) can devote huge resources to any technology perceived to give the PRC a strategic geo-political advantage – such as global quantum supremacy.

“Quantum computing has become the latest battleground between the U.S. and China,” GlobalData associate analyst Benjamin Chin said in a statement. “Both countries want to claim quantum supremacy, not only as a matter of national pride but also because of the financial, industrial, scientific, and military advantages quantum computing can offer. “China has already established itself as a world leader in secure quantum satellite communications. Moreover, thanks to its autocratic economic model, it can pool resources from institutions, corporations, and the government. This gives China a distinct advantage as it can work collectively to achieve a single aim – quantum supremacy.”

China has already developed quantum equipment with potential military applications:

- This year, scientists from Tsinghua University developed a quantum radar that could detect stealth aircraft by generating a small electromagnetic storm.

- In 2017, the Chinese Academy of Sciences also developed a quantum submarine detector that could spot submarines from far away.

- In December 2021, China created a quantum communication network in space to protect its electric power grid against attacks, according to scientists involved in the project. Part of the network links the power grid of Fujian, the southeastern province closest to Taiwan, to a national emergency command centre in Beijing.

Consider Alibaba’s innocuously named DAMO Academy (Discovery, Adventure, Momentum and Outlook), which has already invested $15bn in quantum technology and will continue to plough more and more money into the venture. The Chinese government has also invested at least $10bn in the National Laboratory for Quantum Information Science, whose sole purpose is to conduct R&D only into quantum technologies with “direct military applications.”

Photo: Shutterstock Images

Swiss company ID Quantique, a spin-off from the Group of Applied Physics at the University of Geneva, is launching technology to make satellite security quantum proof. The company was founded in 2011 and has more than a decade of experience in quantum key distribution systems, quantum safe network encryption, single photon counters and hardware random number generators. The latest additions to its portfolio are two extremely robust, ruggedized and radiation-hardened QRNG (Quantum Random Number Generator) chips designed and fabricated especially for space applications.

The generation of genuine randomness is a vital component of cybersecurity: Systems that rely on deterministic processes, such as Pseudo Random Number Generators (PRNGs), to generate randomness are insecure because they rely on deterministic algorithms and these are, by their nature, predictable and therefore crackable. The most reliable way to generate random numbers is based on quantum physics, which is fundamentally random. Indeed, the intrinsic randomness of the behaviour of subatomic particles at the quantum level is one of the very few absolutely random processes known to exist. Thus, by linking the outputs of a random number generator to the utterly random behaviour of a quantum particle, a truly unbiased and unpredictable system is guaranteed and can be assured via live verification of the numbers and monitoring of the hardware to ensure it is operating properly.

The two new space-hardened microprocessors, the snappily named IDQ20MC1-S1 and IDQ20MC1-S3, are certified to the equally instantly memorable ECSS-Q-ST-60-13, the standard that defines the requirements for selection, control, procurement and usage of electrical, electronic and electro-mechanical (EEE) commercial components for space projects. The IDQ20MC1-S3 is a Class 3 device, predominantly for use in low-earth orbit (LEO) missions. The IDQ20MC1-S1 is a Class 1 device, for use in MEO and GEO mission systems. IDQ is the first to enable satellite security designers to upgrade their encryption keys to quantum enhanced keys.

References:

https://ibm-com-qc-dev.quantum-computing.ibm.com/quantum/summit

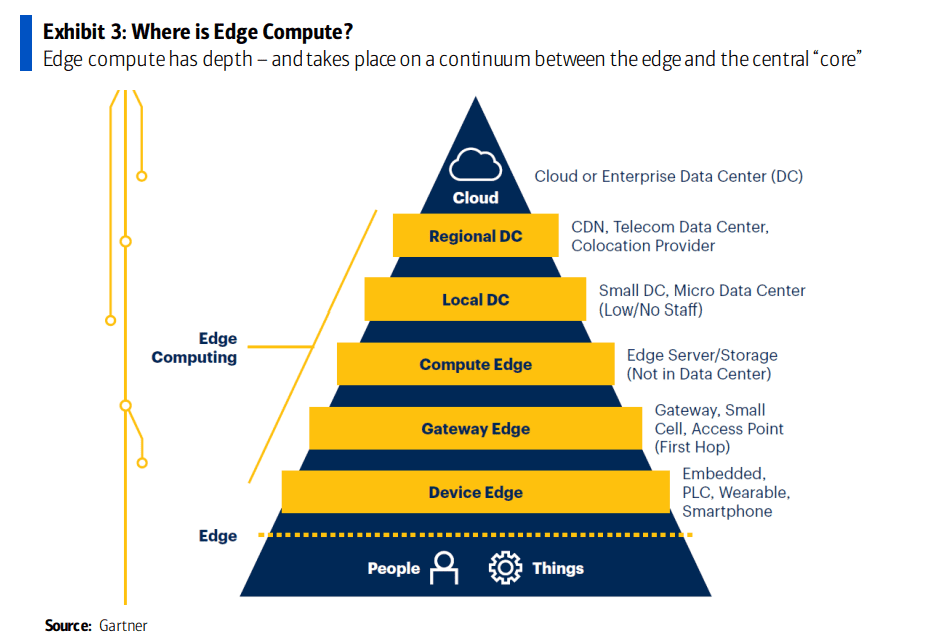

Has Edge Computing Lived Up to Its Potential? Barriers to Deployment

Despite years of touting and hype, edge computing (aka Multi-access Edge Computing or MEC) has not yet provided the payoff promised by its many cheerleaders. Here are a few rosy forecasts and company endorsements:

In an October 27th report, Markets and Markets forecast the Edge Computing Market size is to grow from $44.7 billion in 2022 to $101.3 billion by 2027, which is a Compound Annual Growth Rate (CAGR) of 17.8% over those five years.

IDC defines edge computing as the technology-related actions that are performed outside of the centralized datacenter, where edge is the intermediary between the connected endpoints and the core IT environment.

“Edge computing continues to gain momentum as digital-first organizations seek to innovate outside of the datacenter,” said Dave McCarthy, research vice president, Cloud and Edge Infrastructure Services at IDC. “The diverse needs of edge deployments have created a tremendous market opportunity for technology suppliers as they bring new solutions to market, increasingly through partnerships and alliances.”

IDC has identified more than 150 use cases for edge computing across various industries and domains. The two edge use cases that will see the largest investments in 2022 – content delivery networks and virtual network functions – are both foundational to service providers’ edge services offerings. Combined, these two use cases will generate nearly $26 billion in spending this year (2022). In total, service providers will invest more than $38 billion in enabling edge offerings this year. The market research firm believes spending on edge compute could reach $274 billion globally by 2025 – though that figure would be inclusive of a wide range of products and services.

HPE CEO Antonio Neri recently told Yahoo Finance that edge computing is “the next big opportunity for us because we live in a much more distributed enterprise than ever before.”

DigitalBridge CEO Marc Ganzi said his company continues to see growth in demand for edge computing capabilities, with site leasing rates up 10% to 12% in the company’s most recent quarter. “So this notion of having highly interconnected data centers on the edge is where you want to be,” he said, according to a Seeking Alpha transcript.

Equinix CEO Charles Meyers said his company recently signed a “major design win” to provide edge computing services to an unnamed pediatric treatment and research operation across a number of major US cities. Equinix is one of the world’s largest data center operators, and has recently begun touting its edge computing operations.

……………………………………………………………………………………………………………………………………………………………..

In 2019, Verizon CEO Hans Vestberg said his company would generate “meaningful” revenues from edge computing within a year. But it still hasn’t happened yet!

BofA Global Research wrote in an October 25th report to clients, “Verizon, the largest US wireless provider and the second largest wireline provider, has invested more resources in this [edge computing] topic than any other carrier over the last seven years, yet still cannot articulate how it can make material money in this space over an investable timeframe. Verizon is in year 2 of its beta test of ‘edge compute’ applications and has no material revenue to point to nor any conviction in where real demand may emerge.”

“Gartner believes that communications and manufacturing will be the main drivers of the edge market, given they are infrastructure-intensive segments. We highlight existing use cases, like content delivery in communications, or

‘device control’ in manufacturing, as driving edge compute proliferation. However, as noted above, the market is still undefined and these are only two possible outcomes of many.”

Raymond James wrote in an August research note, “Regarding the edge, carriers and infrastructure companies are still trying to define, size and time the opportunity. But as data demand (and specifically demand for low-latency applications) grows, it seems inevitable that compute power will continue to move toward the customer.”

……………………………………………………………………………………………………………………………………………

BofA Global Research – Challenges with Edge Compute:

The distributed nature of edge compute can pose several risks to enterprises. The number of nodes needed between stores, factories, automobiles, homes, etc. can vary wildly. Different geographies may have different environmental issues, regulatory requirements, and network access. Furthermore, the distributed scale in edge compute puts a greater burden on ensuring that edge compute nodes are secured and that the enterprise is protected. Real-time decision making on the edge device requires a platform to be able to anonymize data used in analytics, and secure data in transit and information stored on the edge device. As more devices are added to the network, each one becomes a potential vulnerability target and as data entry points expand across a corporate network, so do opportunities for intrusion.

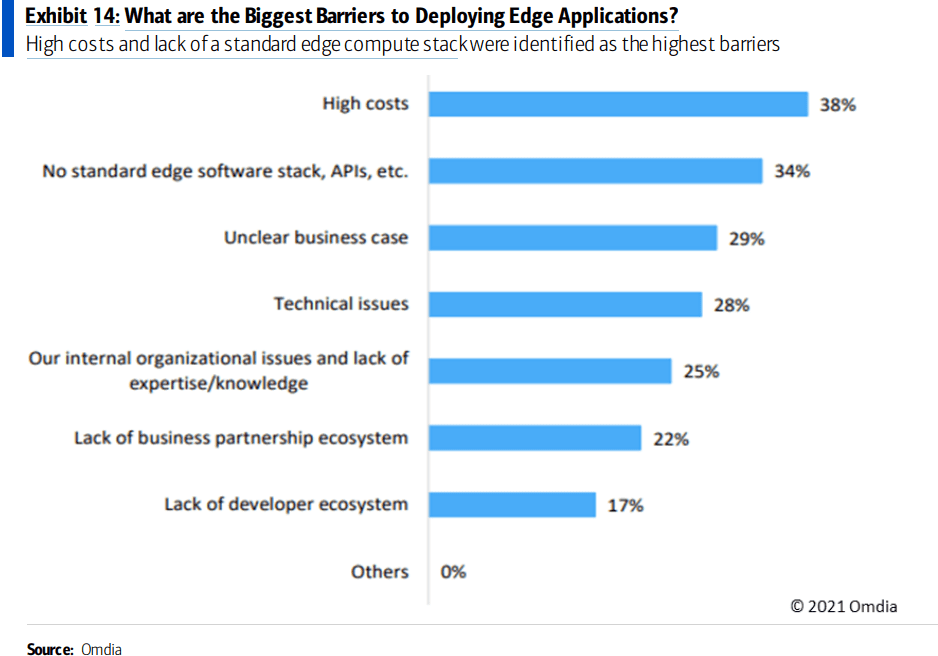

On the other hand, the risk is somewhat double-sided as some security risk is mitigated by keeping the data distributed so that a data breach only impacts a fraction of the data or applications. Other barriers to deploying edge applications include high costs as a result of its distributed nature, as well as a lack of a standard edge compute stack and APIs.

Another challenge to edge compute is the issue of extensibility. Edge computing nodes have historically been very purpose-specific and use-case dependent to environments and workloads in order to meet specific requirements and keep costs down. However, workloads will continuously change and new ones will emerge, and existing edge compute nodes may not adequately cover additional use cases. Edge computing platforms need to be both special-purpose and extensible. While enterprises typically start their edge compute journey on a use-case basis, we expect that as the market matures, edge compute will increasingly be purchased on a vertical and horizontal basis to keep up with expanding use cases.

References:

The Amorphous “Edge” as in Edge Computing or Edge Networking?

Edge computing refuses to mature | Light Reading

Multi-access Edge Computing (MEC) Market, Applications and ETSI MEC Standard-Part I

ETSI MEC Standard Explained – Part II

Lumen Technologies expands Edge Computing Solutions into Europe

Dell’Oro: FWA revenues on track to advance 35% in 2022 led by North America

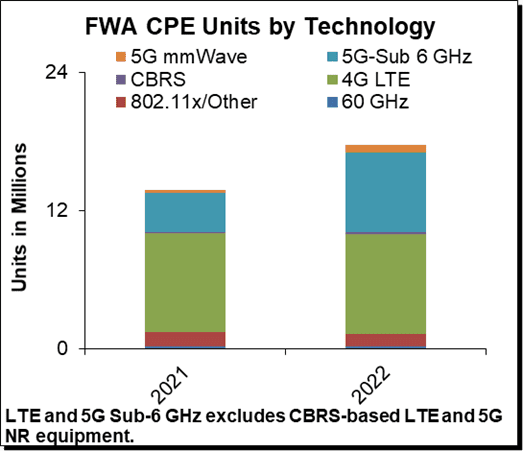

Dell’Oro Group announced today the launch of its new Fixed Wireless Access Infrastructure and CPE advanced research report (ARR). Preliminary findings suggest total Fixed Wireless Access (FWA) revenues, including both RAN equipment and CPE revenue remain on track to advance 35% in 2022, driven largely by subscriber growth in North America.

“Fixed Wireless Access has become a key component to bridging the digital divide and connecting rural and underserved markets globally. What we are also seeing is that FWA can effectively compete with existing fixed broadband technologies, especially with the advent of 5G and other higher-throughput, non-3GPP technologies,” said Jeff Heynen, Vice President and analyst with the Dell’Oro Group.

“Right now, CPE for fixed wireless access using 5G sub-6GHz technologies are growing the fastest. We do expect these units to tail off over time as current investments in fiber networks, along with cable’s DOCSIS 4.0 and fiber upgrades, will limit the addressable market for large-scale fixed wireless services,” Jeff added.

Additional highlights from the Fixed Wireless Access Infrastructure and CPE Advanced Research Report:

- Global FWA revenues are projected to surpass $5 B by 2026, reflecting sustained investment and subscriber growth in both 3GPP- and non-3GPP-based network deployments.

- The North American market remains the most dynamic in terms of deployed FWA technology options, with CBRS and other sub-6GHz options growing alongside 5G NR and 60GHz options.

- Long-term subscriber growth is expected to occur in emerging markets in Southeast Asia and MEA, due to upgrades to existing LTE networks and a need to connect subscribers economically.

- The Satellite Broadband market will also be a key enabler of broadband connectivity in emerging markets, thanks to LEOS-based providers including Starlink, OneWeb, and Project Kuiper.

The Dell’Oro Group Fixed Wireless Access Infrastructure and CPE Report includes 5-year market forecasts for FWA CPE and RAN infrastructure, segmented by technology, including 802.11/Other, 4G LTE, CBRS, 5G sub-6GHz, 5G mmWave, and 60GHz technologies. The report also includes regional subscriber forecasts for FWA and satellite broadband technologies, as well as Gateway forecasts for satellite broadband deployments. To purchase this report, please contact us by email at [email protected].

Note: The IEEE Techblog has featured many FWA success stories and that FWA is probably the top 5G use case to date. The main reason is that a 5G FWA network doesn’t involve roaming or a 5G SA core network for which there are no ITU/ETSI standards or 3GPP implementation specs. As long as the FWA CPE supports 5G NR (via ITU M.2150 recommendation or 3GPP Release 16) all the other functions can be customized in software which only has to work with the network provider offering the FWA service.

References:

JC Market Research: 5G FWA market to reach $21.7 billion in 2029 for a CAGR of 65.6%

Juniper Research: 5G Fixed Wireless Access (FWA) to Generate $2.5 Billion in Global Network Operator Revenue by 2023

Samsung achieves record speeds over 10km 5G mmWave FWA trial in Australia

5G FWA launched by South Africa’s Telkom, rather than 5G Mobile

Nokia and Safaricom complete Africa’s first Fixed Wireless Access (FWA) 5G network slicing trial

Huawei aims to lead Africa’s 5G digital transformation, as U.S. and Europe lockouts continue

Faced with continuing bans in the U.S. and Europe, Huawei is focusing network equipment sales in Africa, which in turn is emphasizing “digital transformation.”

“As the third wave of the global 5G market, Africa will open the 5G era in 2023,” Benjamin Hou, president of Huawei’s northern Africa business, told the Africa 5G summit, that took place in Bangkok, Thailand on October 24th. The event was seen as a platform to draw African countries to 5G tech powered by Shenzhen-based Huawei.

Hou said: “Huawei will further increase its investment in Africa to support the steady development of 5G to facilitate digital transformation in the region. In Africa, for Africa, Huawei will continue to deepen cooperation with industry partners to support customers’ business success in the 5G era.”

Huawei has already built massive information and communications technology (ICT) infrastructure across Africa, but faces challenges in the United States and other Western countries in the northern hemisphere over security concerns. The Trump administration banned tech exports to Chinese companies including Huawei Technologies, ZTE and China Telecom over alleged ties to Chinese military or surveillance networks, and lobbied allied nations to do the same. President Biden took his predecessor’s restrictions forward last year, signing a law to block Chinese companies including Huawei. The Federal Communications Commission (FCC) has named Chinese telecoms firms China Unicom and Pacific Networks Corp as threats to U.S. national security, with a formal ban likely to go through soon.

China’s foreign ministry said: “What the U.S. did violates the rules of the market economy … and seriously hurts the interests of Chinese companies.” “China firmly rejects this. We urge the U.S. side to immediately change its wrong course of action and stop hobbling and suppressing Chinese companies.” In Africa, however, local operators have invested heavily in Chinese equipment and infrastructure, with Beijing often providing funding to build ICT infrastructure including data centers, fiber optic cables and cloud services.

Huawei also faces headwinds in Europe, where Britain and some European Union countries have blacklisted the company from supplier lists for mobile networks, including 5G.

Delivering the keynote speech at the Bangkok summit, Coulibaly Yacouba, CEO of the Ivory Coast mobile spectrum authority, hailed the advent of the 5G era in his country – due to host the Africa Cup of Nations in early 2024.

“The government and local operators are making comprehensive preparations for the commercial launch of 5G in the country. People are expected to enjoy the ultimate service experience brought by innovative 5G technologies during the next Africa Cup of Nations,” he said.

Late last month, two more African mobile network operators – in South Africa and Kenya – launched 5G networks powered by Huawei. South Africa’s partly state-owned Telkom followed smaller data-only network Rain – which in 2019 became Africa’s first telecoms to deploy a commercial 5G network using Huawei. In Kenya, largest mobile network operator Safaricom became East Africa’s first telecoms company to commercially launch 5G high-speed internet services, with infrastructure built by Huawei and Finland’s Nokia.

Deploying multiple vendors, as Safaricom has done, is seen as a way for African operators to get around US or European sanctions and calls to avoid Chinese technology. In South Africa, Vodacom – a subsidiary of Britain’s Vodafone – uses Nokia alongside Huawei as a network provider, while MTN uses tech from Sweden’s Ericsson as well as Huawei and ZTE.

Abishur Prakash, co-founder and geopolitical futurist at the Centre for Innovating the Future, a Canada-based advisory firm, said the Western pushback had made Huawei realise that some countries were “off limits”, with its most lucrative business lines, like 5G, being banned or restricted from India to Japan to Britain. “Now, Huawei is focusing on markets that are less under the thumb of the West – like Africa and the Middle East,” Prakash said. What Huawei was experiencing was part of a new era of “vertical globalisation”, he said. “The world is no longer open and accessible, as it has been for decades … In this new design of the world, Huawei cannot operate freely, the way [America’s] IBM and GE once did.” The US-China rivalry was revealing a new African position, Prakash noted. “African nations are willing to put their own interests first. Take Kenya. It will continue buying from Huawei, even if the US doesn’t want this. It’s this attitude, where Africa is willing to ignore the US, that’s encouraging Huawei to focus more on the continent. Of course, none of this comes without challenges.” Prakash said that while Africa was acting independently, it was also ceding sovereignty as U.S. and Chinese technology companies dominated their societies.

“[As] for the West, it will have to contend with the footprint China is building in Africa, and how this drives Chinese power in the 21st century.”

No government in Africa has banned operators from using Huawei technology. In 2019, South African President Cyril Ramaphosa hinted his country would choose Huawei for its 5G roll-out, and also criticized the U.S. government. “Because they have been outstripped, they must now punish that company and use it as a pawn in the fight they have with China. We want 5G and we know where we can get 5G.”

Those sentiments are also supported by operators in Africa. According to Stephane Richard, CEO of French telecoms giant Orange, Africa’s No 2 operator after MTN: “We’re working more and more with Chinese vendors in Africa, not because we like China, but we have an excellent business relationship with Huawei. They’ve invested in Africa while the European vendors have been hesitating,” Richard told Reuters during last year’s Mobile World Congress in Barcelona, Spain.

New Zealand-based Kenyan telecoms and IT consultant, Peter Wanyonyi, said US and European warnings to African and other developing countries against using Huawei had nothing to do with security or spying. “It’s all about geopolitical power and protectionism – and the West’s fear of a rising China,” Wanyonyi said.

He maintains that the West saw Huawei – and other leading Chinese companies – as threats to the dominance that Western companies had enjoyed in Africa and the Global South for 200 years. The economies of scale meant Huawei could bring leading-edge products onto the market much faster than Western rivals could, and China’s pro-business outlook encouraged investment in research and development at rates that the West simply could not match, he said. “The result is that Huawei technologies are more affordable and now more robust than what the West has to offer, and African countries are jumping at the opportunity afforded by Huawei to modernise their technology infrastructure.” Chinese investments in Africa were not charity, he added.

“To many Africans, it is a relief to just be able to do business without having to deal with the paternalism and historical baggage that Western companies carry around with them when doing business in Africa. “Huawei technology is affordable, available, unconditional and does the job – and will thus continue to be the technology of choice for many African telecoms.” Dobek Pater, business development director at the market research firm Africa Analysis, said Huawei equipment has improved significantly over the years and was very competitive in terms of quality and price with traditional “Western” equipment.

“Particularly in the case of 5G, Huawei has invested a lot in R&D. This makes Huawei often a preferred supplier,” Pater said. “Moreover, in many instances the mobile network operators or fixed-line operators already have quite a bit of Huawei kit installed in their networks and it makes sense to continue building out networks with Huawei equipment,” Pater said. He said some of the operators followed a strategy of using multiple suppliers of new technologies.

“In the case of 5G, there are only really three main providers of [radio access network] equipment. Huawei is one of them. Therefore, it naturally becomes a choice in many instances,” Pater said. Another advantage for Huawei was the Chinese government’s willingness to advance soft loans to help in infrastructure development. However, Huawei has not gone without controversy in Africa, he added.

n 2018, French newspaper Le Monde reported Huawei had bugged the African Union headquarters in Addis Ababa, Ethiopia – claims that were rejected by the company. The following year, Huawei lodged a protest with The Wall Street Journal after it reported that the Chinese company had helped the Ugandan and Zambian governments spy on political opponents. Huawei denied the allegations.

References:

https://www.huawei.com/en/technology-insights/publications/huawei-tech/202203/5g-business-success

https://www.connectingafrica.com/author.asp?section_id=728&doc_id=778960

Samsung achieves record speeds over 10km 5G mmWave FWA trial in Australia

South Korea’s Samsung Electronics says it has achieved record-setting average downlink speeds of 1.75 Gbps and uplink speeds of 61.5 Mbps over a 10 km (6.2 miles) 5G mmWave network in a recent field trial conducted with Australia’s NBN Co. As the farthest 28 GHz 5G mmWave Fixed Wireless Access (FWA) connection recorded by Samsung, this milestone demonstrates the expanded reach possible with this powerful spectrum, and its ability to efficiently deliver widespread broadband coverage across the country.

Source: Accton

To achieve average downlink speeds of 1.75 Gbps at such extended range, the trial by Samsung and NBN utilized eight component carriers (8CC), which is an aggregation of 800MHz of mmWave spectrum. The potential to support large amounts of bandwidth is a key advantage of the mmWave spectrum and Samsung’s beamforming technology enables the aggregation of such large amounts of bandwidth at long distance. At its peak, the company also reached a top downlink speed of 2.7Gbps over a 10km distance from the radio.

“The results of these trials with Samsung are a significant milestone and demonstrate how we are pushing the boundaries of innovation in support of the digital capabilities in Australia,” said Ray Owen, Chief Technology Officer at NBN Co. “As we roll out the next evolution of our network to extend its reach for the benefit of homes and businesses across the country, we are excited to demonstrate the potential for 5G mmWave. nbn will be among the first in the world to deploy 5G mmWave technology at this scale, and achievements like Samsung’s 10km milestone will pave the way for further developments in the ecosystem.”

There’s a total of AUD $750 million investment in the nbn Fixed Wireless network (made up of AUD $480 million from the Australian Government and supported by an additional AUD $270 million from nbn). NBN will use software enhancements and advances in 5G technology, and in particular 5G mmWave technology, to extend the reach of the existing fixed wireless footprint by up to 50 percent and introduce two new wholesale high-speed tiers. The nbn FWA network covers nearly 650,000 premises in the country. The company wants to add at least 120,000 locations in Australia that are currently served by a satellite-based service.

“This new 5G record proves the massive potential of mmWave technology, and its ability to deliver enhanced connectivity and capacity for addressing the last mile challenges in rural areas,” said Junehee Lee, Executive Vice President and Head of R&D, Networks Business at Samsung Electronics. “We are excited to work with nbn to push the boundaries of 5G technology even further in Australia and tap the power of mmWave for customer benefit.”

As demonstrated in the trials, 5G mmWave spectrum is not only viable for the deployment of high-capacity 5G networks in dense urban areas, but also for wider FWA coverage. Extending the effective range of 5G data signals on mmWave will help address the connectivity gap, providing access to rural and remote areas where fiber cannot reach.

For the trial, Samsung used its 28GHz Compact Macro and third-party 5G mmWave customer premise equipment (CPE). Samsung’s Compact Macro is the industry’s first integrated radio for mmWave spectrum, bringing together a baseband, radio and antenna into a single form factor. This compact and lightweight solution can support all frequencies within the mmWave spectrum, simplifying deployment, and is currently deployed in commercial 5G networks across the globe, including Japan, Korea and the U.S.

Since launching the world’s first 5G mmWave FWA services in 2018 in the U.S., Samsung has been leading the industry, offering an end-to-end portfolio of 5G mmWave solutions — including in-house chipsets and radios — and advancing the 5G mmWave momentum globally.

The nbn® network is Australia’s digital backbone that helps deliver reliable and resilient broadband across a continent spanning more than seven million square kilometers. nbn is committed to responding to the digital connectivity needs of people across Australia, working with industry, governments, regulators and community partners to increase the digital capability of Australia.

Samsung has pioneered the successful delivery of 5G end-to-end solutions including chipsets, radios and core. Through ongoing research and development, Samsung drives the industry to advance 5G networks with its market-leading product portfolio from RAN and Core to private network solutions and AI-powered automation tools. The company is currently providing network solutions to mobile operators that deliver connectivity to hundreds of millions of users around the world.

Nokia had previously announced it was supplying 5G FWA mmWave CPE equipment for nbn’s efforts that also operates in the 28 GHz band with similar performance characteristics stated by Samsung for its test, including a range of up to 6.2 miles from the transmission tower. However, Samsung said that Nokia’s equipment was not part of its test.

Nokia noted that its CPE includes an antenna installed on the roof of a premises that is linked using a 2.5 Gb/s power over Ethernet (PoE) connection to an indoor unit that powers the on-premises internet connectivity.

Related Articles:

- Samsung Electronics Supports NTT East’s Continued Expansion of Private 5G Networks in Japan

- Samsung Electronics Tapped To Support Comcast’s 5G Connectivity Efforts

- Samsung Electronics To Deliver Private 5G Network Solutions to Korea’s Public and Private Sectors

References:

https://www.sdxcentral.com/articles/news/samsung-nokia-power-5g-mmwave-potential/2022/11/

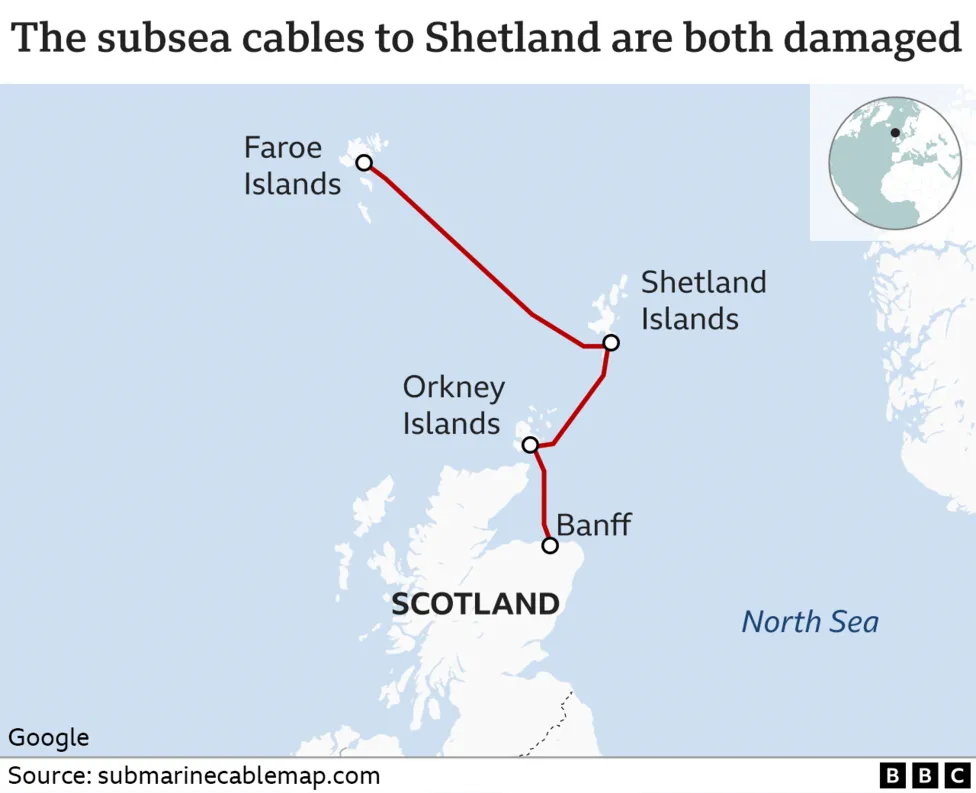

Sabotage or Accident: Was Russia or a fishing trawler responsible for Shetland Island cable cut?

Most telecom professionals, analysts, and media don’t realize how dependent the world is on a limited number of fiber-optic subsea cables that form the internet’s spine and electronically link our continents and islands. Currently 95% of international internet traffic is transmitted by undersea cables. Satellites, in comparison, convey very little internet traffic.

There are still only about 200 cables around the world, each the size of a large hose pipe and capable of data transfers at about 200 terabytes per second. These cables lie on the ocean floor, while nearer to the shore they are buried under the seabed for additional protection. They carry an estimated $10 trillion worth of financial transactions every day and come together at 10 or so international chokepoints, which are particularly vulnerable.

On October 20th, the subsea cable connecting Shetland and the Faroe Islands was damaged with a separate cable linking Shetland with the Scottish mainland also being cut. BT Group, which provides communications services through the cables, said engineers had been working “flat out” to repair the damage – which had primarily impacted mobile and broadband connections.

A BT spokesperson said: “While both cable links are being repaired by subsea engineers, engineers were able to reconnect all services via a temporary solution on Thursday afternoon.”

Although the BBC attributed the Shetland subsea cable damage to a fishing trawler, there is speculation that Moscow may have been the culprit. The Financial Times (and other sources) reported that Russia’s Boris Petrov scientific research ship, was tracked in the vicinity of the Shetland Isles cables when they were cut. Since it’s designated a ‘vessel of interest’ by western navies, there’s every chance the fault could have been an example of Russia’s hybrid warfare.

The FT wrote: “The presence of a Russian underwater research ship, and the recent trio of underwater explosions that severed the Nordstream gas pipeline, make Moscow sabotage far more plausible.

Lord West, the former head of the Royal Navy, told Talk Radio: “In the Shetlands recently, where power was lost a couple of times and I’m sure it was probably a dredger or a trawler did it. “But actually there was a Russian ship of the type that can cause damage to damaged pipelines in that region. And hopefully, we are monitoring very closely making sure we’re seeing what they are doing.”

Alexander Lord, a Europe and Eurasia analyst at Sibylline told Express.co.uk: “I think in the instance of the Shetland Islands I think that’s a really interesting one to watch. Obviously, accidents do happen, and these undersea cables do occasionally get damaged by fishing trawlers, for example.

“But I think it is notable and indeed local officials have noted that it’s highly unusual that two cables were damaged in quick succession and that’s what we’ve seen this week, it is what’s caused some of the problems in Shetland. In terms of the vulnerability of European critical infrastructure, maritime assets, for example, including undersea cables will remain particularly vulnerable, undersea pipelines as well.”

The FT noted that UK Prime Minister Rishi Sunak wrote a paper in 2017 on the growing sabotage threat to subsea cables. From that paper: “In the digital age of cloud computing, the idea that steel and plastic pipes are integral to our life seems anachronistic,’ wrote Rishi Sunak. ‘But our ability to transmit confidential information, to conduct financial transactions and to communicate internationally all depend upon a global network of physical cables lying under the sea.’ And what if those cables are cut? The threat is nothing short of existential.”

In his 2017 paper, Sunak made several recommendations for fortifying the security of undersea cables. These included incentivising private businesses such as Google and Facebook, which own or finance much of the global cable network, to back up systems and distribute cables more widely. But nothing was done.

The UK has around 60 undersea cables. If several of these were cut or disrupted, the consequences would be disastrous. Now that Sunak is the UK PM, will he invest in protective maritime and submarine capabilities as he recommended in his 2017 paper?

This past January, Admiral Tony Radakin, the head of the British Armed Forces, observed that ‘Russia has grown the capability to put at threat those undersea cables and potentially exploit undersea cables.’ It’s now crunch time for the UK!

References:

https://www.bbc.com/news/uk-scotland-north-east-orkney-shetland-63337473

https://www.ft.com/content/0ddc5b48-b255-401b-8e9f-8660f4eab37b

https://www.spectator.co.uk/article/the-threat-to-britains-undersea-cables/

Cable One invests $50 million in Ziply Fiber after its JV called Clearwire Fiber

Cable One [1.] has invested $50 million to acquire a minority stake in northwestern U.S. wireline network operator Ziply Fiber [2.]. Although the investment was made on September 6th, it was first announced Thursday November 3rd when Cable One Chair and CEO Julie Laulis revealed the investment during the company’s Q3 2022 earnings call. She referred to Ziply Fiber as Cable One’s “newest strategic growth partner.” A Ziply representative confirmed the sum from Cable One was part of the $450 million in new funding it announced on September 8th.

Note 1. Cable One is an American broadband communications provider. Under the Sparklight brand, it provides service to 21 states and 900,000 residential and business customers. It is headquartered in Phoenix, Arizona, though it does not serve that metro area.

Note 2. Ziply Fiber was formed from the acquisition of Frontier Communications operations in Washington, Oregon and Montana. Ziply has an ambitious fiber buildout/upgrade plan with the launch of symmetrical, multi-gigabit broadband speed tiers.

…………………………………………………………………………………………………………………………………………………………..

In a 10-Q filing, Cable One stated it invested an initial $22.2 million in Ziply in November 2022 and expects to invest the remaining $27.8 million before the end of September 2023. Its investment netted the company less than a 10% equity interest in Ziply.

“We are investing alongside proven operational and financial leaders that we have maintained long-term trusted relationships with and they continue to demonstrate the ability to deliver strong results and shareholder returns that align with our rigorous standards,” a Cable One spokesman told Light Reading.

Other highlights from Cable One’s Q3-2022 results and earnings call:

- Total revenues were $424.7 million in the third quarter of 2022 compared to $430.2 million in the third quarter of 2021. Year-over-year, residential data revenues increased 6.3% and business services revenues decreased 11.5%. Revenues for the third quarter of 2022 included $4.9 million from CableAmerica(1) operations. Revenues for the third quarter of 2021 included $16.3 million from operations that were contributed to Clearwave Fiber(1) and from the Divested Operations, of which a substantial majority consisted of business services revenues.

- Net income was $70.6 million in the third quarter of 2022, an increase of 35.1% year-over-year. Adjusted EBITDA was $224.6 million in the third quarter of 2022, an increase of 1.9% year-over-year. Net profit margin was 16.6% and Adjusted EBITDA margin(2) was 52.9%.

- Revenues decreased $5.5 million, or 1.3%, to $424.7 million for the third quarter of 2022 due primarily to the contribution of operations to Clearwave Fiber and the disposition of the Divested Operations during 2022 that collectively generated $16.3 million of revenues in the prior year quarter, predominantly consisting of business services revenues, and decreases in residential video and residential voice revenues. The decrease was partially offset by increases in higher margin residential data and business services revenues from continuing operations and the addition of CableAmerica operations.

- Cable One, like other cable operators, is seeing a slowdown in consumer move activity across its footprint. The operator posted an organic gain of just 1,800 broadband subs in the quarter, according to MoffettNathanson, a division of SVB Securities.

- Sell-in for 1-Gig service has accelerated to nearly 32%.

- Cable One’s average revenue per user (ARPU) rose 15%, to $80.46, as customers migrated to faster, higher-priced services or took an unlimited data plan.

- Rate increases are “absolutely on the table,” Laulis said.

- Average data usage reached about 580 gigabytes per month in Q3, up 19% year-over-year.

- Cable One, which has DOCSIS 4.0 on its roadmap, has tested symmetrical multi-gigabit speeds, but did not say when it might launch such services.

- FWA adoption in Cable One’s markets “remains low,” Laulis said.

- Video losses hit 18,000, widened from a year-ago loss of 8,000. Reflecting Cable One’s de-emphasis on video and its laser-focus on broadband, the company’s video base eroded by another 28% year-over-year.

At the start of 2022, Cable One along with three private equity companies formed a joint venture called Clearwave Fiber, aiming to reach 500,000 rural locations by 2027. Cable One contributed assets from its Illinois-focused Clearwave Communications and South Carolina-based Hargray Communications businesses as part of the deal. Shortly after its formation, Clearwave Fiber acquired the assets of Kansas-based operator RG Fiber to gain a foothold in the state.

Earlier this week, Clearwave Fiber revealed it has already crossed the 100,000 passings mark. By the end of this year, the company said its services will be available in a total of 35 markets across four states: Illinois, Kansas, Georgia and Florida.

References:

Cable One joint venture to expand fiber based internet access via FTTP

Ziply Fiber deploys 2 Gig & 5 Gig fiber internet tiers in 60 cities – AT&T can now top that!

Frontier Communications and Ziply Fiber to raise funds for fiber optic network buildouts

https://www.lightreading.com/cable-tech/cable-one-invests-$50m-in-ziply-fiber/d/d-id/781591

https://www.fiercetelecom.com/broadband/cable-one-doubles-down-fiber-50m-ziply-investment

FCC establishes Space Bureau dedicated to satellite industry oversight

The Federal Communications Commission (FCC) has set up a new bureau dedicated to improving the agency’s oversight of the satellite industry. It is one of two new offices to come out of an internal reorganization at the FCC, which has also created a standalone office of international affairs.

According to the FCC, the changes will help the agency fulfill its statutory obligations and to keep pace with the rapidly changing satellite industry and global communications policy. Establishing a standalone Space Bureau will elevate the importance of satellite programs and policy internally, and will also acknowledge the role of satellite communications in advancing domestic communications policy, according to the agency.

“The satellite industry is growing at a record pace, but here on the ground our regulatory frameworks for licensing them have not kept up. Over the past two years the agency has received applications for 64,000 new satellites. In addition, we are seeing new commercial models, new players, and new technologies coming together to pioneer a wide-range of new satellite services and space-based activities that need access to wireless airwaves,” said FCC Chairwoman Rosenworcel in her prepared remarks.

After identifying space tourism, satellite broadband, disaster recovery efforts and more, Rosenworcel said the interest in space as a new market for investment and a home for new kinds of services is vast. She noted that “private investment in space companies has reached more than $10 billion in the last year, the highest it has ever been.”

She also said that “the space sector has been on a monumental run. Satellite operators set a new record last year for the number of satellites launched into orbit, a record they will surpass again.”

Under the Communications Act of 1934, the FCC licenses radio frequency uses by satellites and ensures that space systems reviewed by the agency have sufficient plans to mitigate orbital debris.

The FCC said also that creating the two new separate offices will allow expertise to be more consistently leveraged across the organization’s different bureaus.

Commenting on the reorganization, FCC Chairwoman Rosenworcel said: “The satellite industry is growing at a record pace, but here on the ground our regulatory frameworks for licensing them have not kept up. Over the past two years, the agency has received applications for 64,000 new satellites. In addition, we are seeing new commercial models, new players, and new technologies coming together to pioneer a wide-range of new satellite services and space-based activities that need access to wireless airwaves.”

“Today, I announced a plan to build on this success and prepare for what comes next,” she added. “A new Space Bureau at the FCC will ensure that the agency’s resources are appropriately aligned to fulfill its statutory obligations, improve its coordination across the federal government, and support the 21st century satellite industry.”

Jennifer Warren, VP of technology, policy and regulation at Lockheed Martin, said during a panel following Rosenworcel’s announcement that the stakes are much bigger than broadband satellite launches. This new regulatory framework can clear the way for the US to be a leader in “the commercialization of space,” she said. “It’s not for the faint-hearted.”

The FCC bureau reorg “also gives encouragement to new space actors that there will be staff accessible to answer the many questions they must have as they try to enter this exciting industry,” according to Julie Zoller, Head of Global Regulatory Affairs, Project Kuiper at Amazon. “It’s a complex process, but it is one that is full of opportunity and benefits to consumers, as Chairwoman Rosenworcel mentioned. The number of broadband satellite systems is really supercharging the ability to bridge the digital divide curve at home and abroad.”

In August, the FCC signed a joint memorandum of understanding with the NTIA aimed at improving the coordination of federal spectrum management and efficient use of radio frequencies.

References:

FCC establishes new bureau dedicated to satellite industry oversight

https://www.lightreading.com/satellite/the-fcc-takes-its-bureaucracy-beyond-stars/d/d-id/781568