Fixed Wireless Access (FWA)

Broadcom with Samsung Electronics: Integrated 5G and Wi-Fi 8 FWA Platform

Broadcom has announced a collaboration with Samsung Electronics Co., Ltd. to develop a reference platform for fixed wireless access (FWA) deployments, combining Broadcom’s BCM6776 Wi-Fi system-on-chip (SoC) with Samsung’s B1320 5G modem. The platform is designed to integrate 3GPP Release 17 5G connectivity with emerging IEEE 802.11bn (Wi-Fi 8) capabilities, supporting convergence between wide-area and local-area broadband technologies.

The reference design targets global FWA use cases, where operators seek to deliver high-throughput broadband services using 5G radio access in conjunction with advanced in-home wireless distribution. By aligning 5G and Wi-Fi 8 performance characteristics, the platform addresses requirements for sustained throughput, low latency, and reliability under variable radio conditions. The design also emphasizes scalability for high-volume deployments, with integration intended to reduce system complexity and cost.

The Broadcom BCM6776 is a tri-band Wi-Fi 8 SoC designed for residential and small enterprise access points. It integrates a quad-core Arm-based network processor with Wi-Fi 8 radio functionality in a single device. The SoC supports 2-stream operation with 40 MHz channels in the 2.4 GHz band, and 4-stream operation with up to 160 MHz channels in the 5 GHz and 6 GHz bands. This configuration enables multi-gigabit aggregate throughput while maintaining compatibility with evolving IEEE 802.11bn features.

Integration of compute and radio subsystems within a single SoC reduces bill of materials (BOM) requirements and simplifies hardware design. Power efficiency is also improved relative to prior architectures that relied on discrete components, supporting deployment in thermally constrained residential environments.

Image Credit: Broadcom

…………………………………………………………………………………………………………………………………………………

The Samsung B1320 modem is a 5 nm-class integrated 5G chipset compliant with 3GPP Release 17. It supports peak downlink throughput of up to 3.43 Gbps and uplink throughput of up to 1.17 Gbps, depending on deployment configuration. The modem incorporates a quad-core Arm CPU, RF transceiver, power management functions, and a global navigation satellite system (GNSS) receiver.

The platform further supports non-terrestrial network (NTN) operation, including both NR-NTN and NB-NTN modes, enabling compatibility with satellite-based extensions of 5G coverage.

The combined architecture is designed to sustain end-to-end throughput between the 5G access link and the in-home Wi-Fi network, minimizing bottlenecks between the wide-area and local domains. This is particularly relevant for FWA deployments, where performance is constrained by both radio access conditions and in-premises distribution efficiency.

By providing a pre-integrated reference design, the platform enables original equipment manufacturers (OEMs) and operators to accelerate development cycles and standardize system performance across deployments. This approach supports broader adoption of FWA as a complement to fixed broadband infrastructure, particularly in scenarios where fiber deployment is limited or economically constrained.

“At Computex 2026, we are highlighting that the future of home internet can be both accessible and affordable,” said Joonsuk Kim, Executive Vice President and Head of CP Development at Samsung Electronics. “This platform is designed to deliver reliable performance across a wide range of environments, helping operators bring high-quality connectivity experiences to subscribers.”

“Broadcom is proud to lead the Wi-Fi 8 transition alongside Samsung and our valued ODM partners,” said Vijay Nagarajan, Vice President of Marketing, Wireless and Broadband Communications Division at Broadcom. “This partnership is a game-changer for the FWA market. The combination of Wi-Fi 8 and 5G prioritizes coordinated reliability, giving operators a tool that delivers a consistent experience to every corner of the home.”

Product Features:

The Samsung B1320 is a broadband-optimized 5G platform with the following features:

- 3GPP Release 17

- 4Rx/2Tx radio chain support

- Power Class 1.5 support (TDD bands)

- LPDDR4x / LPDDR5x support

- 1.6 GHz quad-core ARM Cortex-A55 CPU

- 5 Gbps USXGMII, PCIe Gen 3, USB 2.0

- GNSS

- NR-NTN and NB-NTN support for n255 and n256 (L- and S-bands)

The Broadcom BCM6776 is a single-chip Wi-Fi SoC and multi-band radio supporting the following:

- High performance quad-core CPU complex

- Dedicated network processing engine freeing the CPU complex for operator-specific applications and utilities

- Integrated 2×2 2.4 GHz and 4×4 5 GHz and 6 GHz Wi-Fi 8 MAC/PHY/Radio functionality, simplifying system design and lowering cost

- On-chip 2.4 GHz power amplifiers (PAs) and support for third-generation digital pre-distortion for reduced external components and improved RF efficiency

- Versatile memory controller supporting DDR4, LPDDR4, DDR5, and LPDDR5

- Dual PCIe Gen3 controllers to enable simultaneous tri-band applications with a single additional chip

- Integrated multi-gig PHY

A Global Ecosystem of Support:

The launch is supported by the world’s leading original equipment manufacturers (OEMs), who are already integrating the B1320 / BCM6776 platform into their next-generation gateway portfolios.

“HUMAX Networks is delighted to pioneer the next-generation 5G CPE market alongside global technology leaders Broadcom and Samsung. At the recent MWC 2026, we successfully showcased the industry’s first Wi-Fi 8 solution, which integrates Samsung’s cutting-edge 5G technology with Broadcom’s next-generation silicon. Through our ongoing partnership, we remain committed to driving market innovation and consistently delivering top-tier experiences and innovative devices to our global customers,” said Jerry Lee, CEO of Humax Networks.

“We are delighted to collaborate with Broadcom and Samsung to develop our next generation Wi-Fi 8 gateway addressing MSO CBU/FWA market. This solution is capable of delivering a smarter, more secure, and future-ready network optimized solution to meet MSO/FWA customers’ increasing demands of cost competitive 5G NR connectivity,” said Johnson Hsu, SVP & GM of WNC’s Connectivity & Solutions BG.

Availability:

Global carrier trials and OEM sampling of the Samsung B1320 / Broadcom BCM6776 FWA platform are underway.

About Broadcom:

Broadcom Inc. (NASDAQ: AVGO) is a technology leader that designs, develops, and supplies semiconductors and infrastructure software for global organizations’ complex, mission-critical needs. Broadcom combines long-term R&D investment with superb execution to deliver the best technology, at scale. Broadcom is a Delaware corporation headquartered in Palo Alto, CA. For more information, visit www.broadcom.com.

Broadcom, the pulse logo, and Connecting everything are among the trademarks of Broadcom. The term “Broadcom” refers to Broadcom Inc., and/or its subsidiaries. Other trademarks are the property of their respective owners.

…………………………………………………………………………………………………………………..

References:

Extreme Networks deploys Wi‑Fi 7 (IEEE 802.11be) at University of Florida’s “Swamp”

Ookla: FWA Speed Test Results for big 3 U.S. Carriers & Wireless Connectivity Performance at Busy Airports

Aviat Networks and Intracom Telecom partner to deliver 5G mmWave FWA in North America

T-Mobile’s growth trajectory increases: 5G FWA, Metronet acquisition and MVNO deals with Charter & Comcast

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

Analysis: Broadcom’s end-to-end 50G PON Edge AI portfolio with WiFi 8 support

Broadcom has announced the BCM68850, a 50G ITU-T PON home gateway system-on-chip (SoC) that integrates a neural processing unit (NPU) and provides native support for emerging Wi-Fi 8 (IEEE 802.11bn) capabilities. The device extends the evolution of broadband access silicon toward higher-capacity passive optical network (PON) standards while maintaining alignment with next-generation in-home wireless technologies. Broadcom is currently sampling the BCM68850 and BCM55050 to its early access customers and partners. Please contact your local Broadcom sales representative for samples and pricing.

The integration of NPU functionality within the gateway reflects an architectural trend toward distributing compute resources closer to the network edge. This enables localized processing of AI-driven workloads within customer premises equipment (CPE), which can reduce upstream bandwidth demand and improve responsiveness for latency-sensitive applications.

Migration to 50G PON, as defined within ongoing ITU-T standardization efforts (e.g., Higher Speed PON), provides increased access capacity and improved latency characteristics relative to earlier generations such as XGS-PON. These enhancements support more deterministic service delivery, particularly in environments where traffic patterns are becoming increasingly burst-oriented and driven by compute-intensive applications.

Image Credit: ADTRAN

…………………………………………………………………………………………………………………………………………………………………………………………………………………………..

In residential networks, traffic is expected to increasingly consist of short-duration, high-throughput bursts associated with edge processing, real-time analytics, and interactive services. A 50G PON gateway can accommodate these patterns by transmitting high-density payloads over sub-millisecond intervals, after which shared channel resources are rapidly released for other users. This behavior contributes to improved utilization efficiency on shared fiber infrastructure.

Low-latency and low-jitter performance are important for emerging application classes, including distributed AI inference, synchronized edge workloads, and multi-stream ultra-high-definition media. These requirements extend across both the access network and the in-home wireless domain, reinforcing the need for coordinated evolution of PON and Wi-Fi technologies.

From a deployment perspective, introduction of 50G-capable CPE provides operators with additional capacity headroom and supports alignment with future service requirements. Coupled with advancements in IEEE 802.11bn, this approach enables continued scaling of residential broadband performance while maintaining consistency across access and local network segments.

BCM68850 – 50G PON Edge AI Gateway SoC:

The BCM68850 is a standalone 50G PON Gateway SoC that provides an industry-standard ITU-T path for operators to future-proof their networks. The device features:

- High-Performance Application Engine: A dedicated CPU for third-party and operator applications leveraging industry available middleware.

- Integrated Neural Engine: A dedicated NPU that accelerates Edge AI inference, reducing cloud latency and enhancing data privacy by keeping sensitive information on premises.

- Symmetric 50G Performance: Delivers full 50G throughput to meet the insatiable appetite for reliable, multi-gigabit bandwidth.

- Wi-Fi 8 Ready: Native compatibility with Wi-Fi 8 standards to ensure the highest reliability and real-world consistency at the broadband edge.

- Intelligent Self-Healing: Enables operators to implement real-time anomaly detection and predictive bandwidth optimization, reducing OpEx and improving ARPU.

- Advanced Security: Incorporates enhanced security algorithms, including Post-Quantum Cryptography (PQC).

“The BCM68850 is a defining milestone for global fiber networks; we are reshaping the broadband edge as the central intelligence hub of the home,” said Philip Radtke, vice president of product marketing for Broadcom’s Wireless and Broadband Communications Division. “This flagship SoC joins our established lineup of NPU-accelerated fiber, cable, set-top box, and Wi-Fi solutions, ensuring operators can efficiently deploy edge-intelligent broadband regardless of the access medium and extend that intelligence all the way to the edge.”

“With ever increasing consumer and enterprise demand for bandwidth and ultra-reliable connectivity, operators are upgrading the Central Office and End Points with 50G PON capability. Next-generation solutions such as Broadcom’s BCM68850 SoC are critical to unlocking the value of this investment by future-proofing the network edge and ensuring high service levels at every node and premise,” said Jaimie Lenderman, practice leader for Optical, IP, and Broadband Infrastructure market research at Omdia.”By establishing a true end-to-end 50G pipe, operators can deliver the massive capacity and deterministic low latency required to support the rigors of the imminent Wi-Fi 8 deployment cycle.”

This end-to-end 50G offering completes the path from Broadcom’s BCM68660 OLT to the edge, providing a seamless and technically robust ecosystem comprising the BCM55050 ONT or the BCM68850 CPE gateway. This architecture introduces a new level of efficiency by optimizing CPU and memory resources for the AI era, ensuring that the home gateway can handle the massive data pipes required for the next decade of digital innovation.

About Broadcom:

Broadcom Inc. (NASDAQ: AVGO) is a technology leader that designs, develops, and supplies semiconductors and infrastructure software for global organizations’ complex, mission-critical needs. Broadcom combines long-term R&D investment with superb execution to deliver the best technology, at scale. Broadcom is a Delaware corporation headquartered in Palo Alto, CA. For more information, visit www.broadcom.com.

Broadcom, the pulse logo, and Connecting Everything are among the trademarks of Broadcom. The term “Broadcom” refers to Broadcom Inc., and/or its subsidiaries. Other trademarks are the property of their respective owners.

References:

https://www.broadcom.com/company/news/product-releases/64341

2026 Fiber Connect Keynote: “The Future of Fiber Optics: AI and the Quantum”

Nokia and Google Fiber trial 50G PON – first in the U.S.

HKT is first to deploy 50G PON technology in Hong Kong

Türk Telekom and ZTE trial 50G PON, but commercial deployment is not imminent

Ooredoo Qatar is first operator in the world to deploy 50G PON

Highlights of FiberConnect 2024: PON-related products dominate

Fiber Connect 2023: Telcos vs Cablecos; fiber symmetric speeds vs. DOCSIS 4.0?

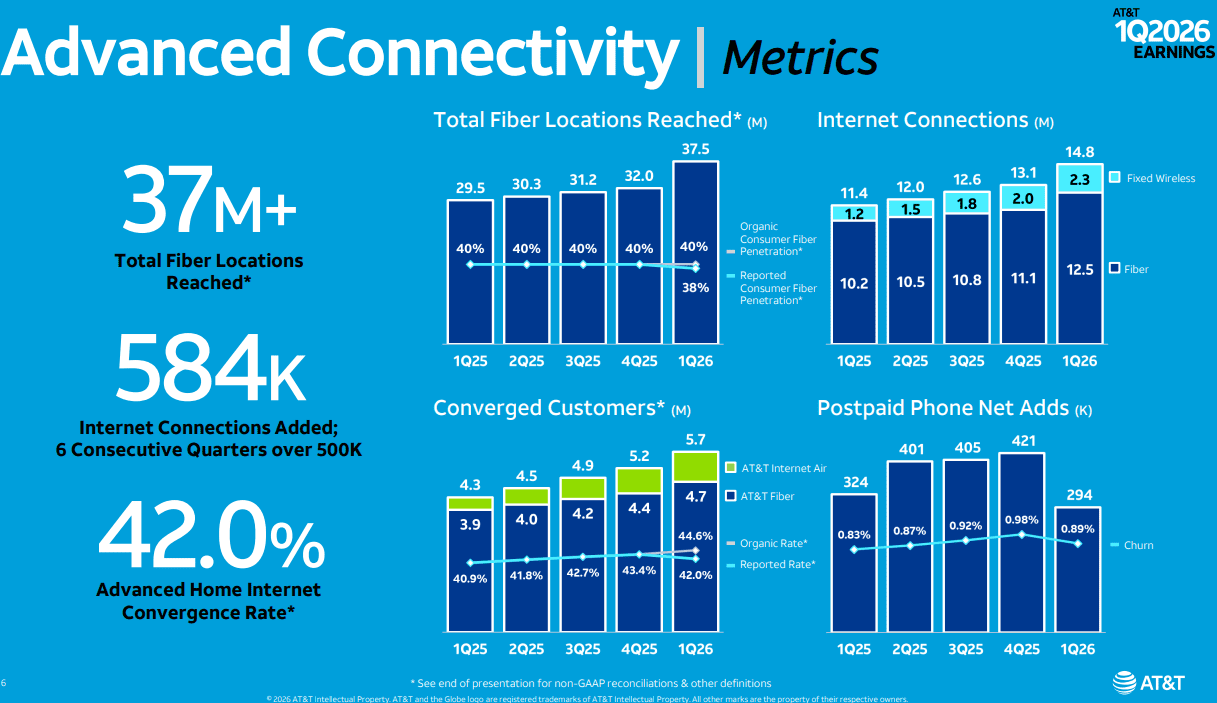

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

AT&T reported first-quarter results today, achieving its fastest-ever year-over-year organic growth in its advanced connectivity convergence rate, with nearly 45% of advanced home internet subscribers also choosing AT&T wireless. Customers are increasingly purchasing their internet and wireless together from AT&T, highlighting the strength of the company’s differentiated, investment-led strategy to drive converged advanced connectivity at scale.

“We saw our best first quarter ever for Advanced Connectivity internet customer net additions, demonstrating the solid foundation of assets we have built,” said John Stankey, AT&T Chairman and CEO. “We’re uniquely positioned to deliver more of what customers want — fiber and 5G all from one provider on the nation’s largest advanced converged network, backed by the AT&T Guarantee. The actions we’ve taken this quarter are evidence of how we are improving the customer value proposition, scaling faster, and accelerating growth.”

AT&T reported $31.5 billion in consolidated operating revenues, representing a 2.9% year-over-year (YoY) increase and outperforming Street estimates of $31.22 billion. This growth was largely driven by the Advanced Connectivity segment, which generated $22.15 billion in consumer revenues, up from $20.97 billion in the prior-year period.

- Wireless Performance: Mobility services posted mostly flat $16.94 billion in revenue, compared to $16.65 billion in Q1 2025.

- Legacy Decommissioning: Legacy revenues fell 25.3% YoY to $1.8 billion. The aggressive copper-to-fiber migration continues, with 85% of wire centers now approved for legacy service cessation.

- Strategic Sunsetting: 30% of these wire centers are slated for total decommissioning by late 2026, coinciding with the loss of 270,000 DSL subscribers this quarter.

The shift toward high-speed, durable connectivity is evidenced by the growth of AT&T’s Fiber and Fixed Wireless Access (FWA) portfolios.

- Fiber Penetration: AT&T recorded 292,000 fiber net additions, bringing the total subscriber base to 12.5 million. The current passings stand at 37.5 million locations, with 32.7 million owned/operated and 4.8 million via joint ventures (JVs).

- FWA Momentum: AT&T Internet Air added 239,000 customers in the quarter (up from 181,000 in Q1 2025), reaching a total of 1.73 million subscribers.

- Roadmap to 60 Million: AT&T remains on track to reach 60 million fiber locations by 2030 through organic expansion, the Gigapower JV, and open-access agreements.

AT&T is evolving its “NetworkCo” model to optimize capital intensity and market reach.

- Lumen Asset Integration: Recently acquired fiber assets from Lumen will be transferred into a JV structure. CFO Pascal Desroches expects to finalize an agreement with an equity partner for these assets in 2H 2026.

- Convergence and “One Connect”: The “One Connect” platform is the cornerstone of AT&T’s converged strategy.

- Bundle Adoption: 42% of advanced home internet customers (5.68 million) also subscribe to mobile services.

- Fiber-Mobile Synergy: Among fiber-specific customers, the mobility bundle penetration rate is 40.2% (4.74 million).

- The “One Connect” Roadmap: CEO John Stankey views the platform as an iterative engine, beginning with BYOD (Bring Your Own Device) and eventually expanding into tailored family plans.

“We made further progress at positioning AT&T as the preferred provider for connecting consumers and businesses to the internet. We closed our transaction with Lumen, ahead of schedule, adding 1.1 million fiber customers, and over 4 million fiber locations. We’re pleased with the progress we’re making as we integrate these assets in several major metro areas and position the business for faster growth. Early indicators are positive. We now offer fiber services throughout our distribution channels in these areas, which has driven sales activity well above pre-transaction trends. We’re executing the steps to scale engineering, construction and service delivery in the acquired geographies, expected as we move into the back half of the year, will achieve steady improvement in fiber and wireless customer growth in these areas. When we focus on customers needs and invest in the experience and products they want, we find success, and in the first quarter, we gave customers more reasons to choose AT&T. We expanded the AT&T guarantee to cover internet Air and launched a new flagship app to deliver a simple digital-first experience to customers.

We also launched AT&T OneConnect, which enables customers to easily connect all their eligible devices at home and on the go, and eliminates the need to buy internet access twice. We refreshed our Unlimited Your Way plans to deliver more value. All these moves are based on a consistent set of principles that drive our approach to serving customers the way they want to be served, with offers that deliver simplicity, value and choice and converged connectivity.

After years of industry-leading investments in our fiber and wireless network, we believe that we have now established a structural advantage that others will not catch. We reached more than 90 million customer locations across the country with our advanced internet services, over either fiber or 5G. We believe this provides us with more scalable reach and converged connectivity than any of our peers, including a meaningful scale and performance advantage in fiber. This is an advantage we’re growing as we ramp our deployment at a faster pace than anyone else. Today, we reach over 37 million customer locations with fiber, and we’re on track to reach 60 million plus locations by the end of the decade.”

NTNs and D2D:

Regarding its choice of AST SpaceMobile for direct-to-device (D2D) connectivity for its smartphones, Stankey said, “I think it’s natural that we work with LEO partners that have the capabilities to solve that problem, to integrate those offerings into our services,” Stankey said Tuesday on AT&T’s Q1 2026 earnings call. “My goal would be that I have a good, strong wholesale relationship, and it may not just be with one of them. It may be with more than one of them.”

Besides AST SpaceMobile, Stankey said he expects SpaceX/Starlink to have a “robust direct-to-device capability,” as well as Amazon Leo and potentially a fourth NTN satellite internet company. SpaceX is developing a next-generation D2D offering with spectrum it’s acquiring from EchoStar, and Amazon plans to introduce a new D2D offering in 2028 amid its recent deal to acquire Globalstar. AT&T has a deal with Amazon Leo to connect business customers that are out of reach of terrestrial wireless and wireline networks, but it has not yet signed a D2D-specific deal with Amazon’s satellite and services unit.

Market Analysis – The Fiber Coverage Gap:

Despite strong growth, analysts remain cautious regarding AT&T’s convergence ceiling. With fiber currently available in only about 20% of the U.S., the primary concern is whether AT&T can maintain competitive parity in non-fiber regions.

- Potential Underperformance Risk: In markets where AT&T relies on legacy copper or wholesale third-party access, it may struggle to match the churn reduction and ARPU (Average Revenue Per User) lift seen in its “Fiber + Wireless” footprint.

- Mitigation Strategy: The success of the “60-million-locations fiber by 2030” roadmap which is the primary driver of AT&Ts increased spending. Also, the scaling of Internet Air as a “bridge” technology will be critical in preventing regional underperformance.

- 2026 Milestone: AT&T expects to exceed 40 million total fiber locations by the end of 2026.

- Build Cadence: The company is targeting an organic deployment pace of 4 million new locations per year by the end of 2026. After 2026, this rate is projected to increase to approximately 5 million additional spots annually.

- Funding Mechanism: To support this acceleration, AT&T plans to reinvest $3.5 billion in cost savings specifically into the fiber build-out over the 2026–2027 period.

- “There’s no path for AT&T to have a fiber footprint that will cover more than a third of the country. Will AT&T be consigned to losing share in the other two thirds?” MoffettNathanson analyst Craig Moffett asked in a research note to clients posted after AT&T’s earnings call.

Despite the high CapEx, AT&T CFO Pascal Desroches reaffirmed that the company remains on track to deliver $18 billion+ in free cash flow (FCF) for 2026.

………………………………………………………………………………………………………………………………………………………………………

References:

https://www.lightreading.com/satellite/at-t-might-look-beyond-ast-spacemobile-for-d2d

Analysis: AT&T’s $250B network investment to advance U.S. connectivity

AT&T and AWS to deliver last mile connectivity for AI workloads; AT&T Geo Modeler™ AI simulation tool

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

AT&T’s convergence strategy is working as per its 3Q 2025 earnings report

AT&T deploys nationwide 5G SA while Verizon lags and T-Mobile leads

AT&T to buy spectrum licenses from EchoStar for $23 billion

AT&T grows fiber revenue 19%, 261K net fiber adds and 29.5M locations passed by its fiber optic network

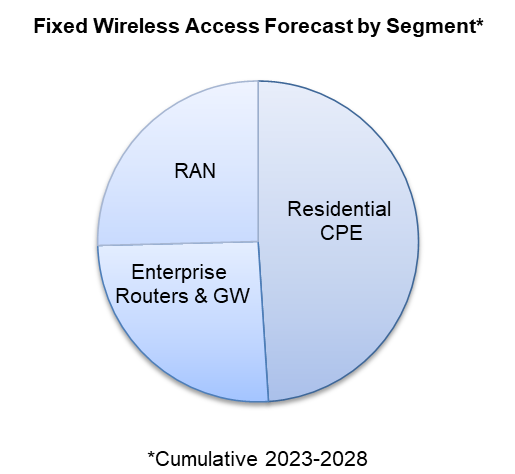

Dell’Oro: Fixed Wireless Access revenues +10% in 2025 & will continue to grow 10% annually through 2029

Additional highlights from the Fixed Wireless Access Infrastructure and CPE Advanced Research Report:

- Total FWA subscriptions, which include residential, SMB, and large enterprises, are expected to grow steadily, surpassing 191 million by 2029.

- 5G Sub-6GHz and mmWave units will dominate the global residential CPE market.

The Dell’Oro Group Fixed Wireless Access Infrastructure and CPE Report includes 5-year market forecasts for FWA CPE (Residential and Enterprise) and RAN infrastructure, segmented by technology, including 802.11/Other, 4G LTE, CBRS, 5G sub-6GHz, 5G mmWave, and 60GHz technologies. The report also includes regional forecasts for FWA subscriptions, including for both residential and enterprise markets, with the enterprise subscriptions segmented by SMB and Large Enterprise. To purchase this report, please contact us by email at [email protected].

………………………………………………………………………………………………………………………………………………………………………

Independent Analysis via Perplexity.ai:

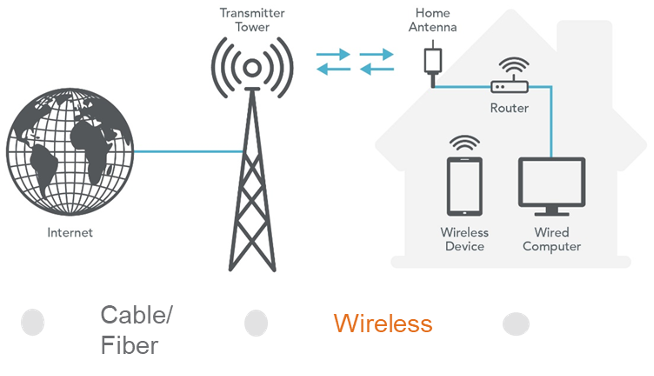

Fixed Wireless Access Schematic Diagrams

……………………………………………………………………………………………………………………………………………………………

Demand-side drivers:

-

Rising demand for high‑speed home and enterprise broadband, including video streaming, gaming, and cloud/SaaS, in areas poorly served by DSL or legacy cable.

-

Customer appetite for quick‑install, no‑truck‑roll broadband that can be activated using wireless CPE instead of waiting for fiber construction.

-

Growing need for reliable connectivity for remote work, distance learning, and SME digitization, especially in suburban and rural regions.

Supply-side / operator economics:

-

Ability to leverage existing 4G LTE macro grids and sub‑6 GHz spectrum, with incremental capex mainly in CPE and software rather than full new access builds.

-

Refarming of LTE spectrum and overlay of 5G NR on the same bands allows operators to run both mobile broadband and FWA on a common RAN/core.

-

Attractive ROI relative to fiber in low‑density areas, since one macro site at sub‑6 GHz can cover large rural or ex‑urban footprints.

Technology and spectrum factors (4G & sub‑6 GHz 5G):

-

4G LTE coverage ubiquity: years of investment mean LTE already reaches most urban, suburban, and many rural markets, making LTE‑FWA immediately deployable.

-

Sub‑6 GHz 5G propagation: better penetration through buildings and walls than higher bands, enabling more reliable indoor FWA without extensive outdoor CPE alignment.

-

Massive MIMO and beamforming on sub‑6 GHz bands increase sector capacity and improve non‑line‑of‑sight performance, which is critical for FWA quality at cell edge.

Competitive and regulatory drivers:

-

Mobile operators using FWA to attack cable and DSL bases; in several markets FWA contributes a high share of net broadband additions, pressuring incumbents on price and speed.

-

Government rural‑broadband programs and subsidies (e.g., U.S. RDOF‑type initiatives) encourage use of FWA as a cost‑effective tool to close the digital divide.

-

Regulatory allocation of additional mid‑band and sub‑6 GHz spectrum (e.g., 3–4 GHz bands) increases usable capacity and supports scaling FWA to millions of homes.

Market growth indicators:

-

FWA market value is growing at double‑digit CAGRs, with 4G still a large share today but 5G FWA projected to dominate new subscriptions by the late 2020s.

-

Sub‑6 GHz FWA gateways and CPE are a rapidly expanding device segment, driven by operator deployments targeting residential and SME broadband.

…………………………………………………………………………………………………………………………………………………………………….

References:

https://www.delloro.com/news/fwa-infrastructure-and-cpe-spending-will-remain-above-10-billion-annually-through-2029/

Fiber and Fixed Wireless Access are the fastest growing fixed broadband technologies in the OECD

Ookla: FWA Speed Test Results for big 3 U.S. Carriers & Wireless Connectivity Performance at Busy Airports

Point Topic: Global Broadband Subscribers in Q2 2025: 5G FWA, DSL, satellite and FTTP

Aviat Networks and Intracom Telecom partner to deliver 5G mmWave FWA in North America

T-Mobile’s growth trajectory increases: 5G FWA, Metronet acquisition and MVNO deals with Charter & Comcast

Dell’Oro: 4G and 5G FWA revenue grew 7% in 2024; MRFR: FWA worth $182.27B by 2032

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

Highlights of Qualcomm 5G Fixed Wireless Access Platform Gen 3; FWA and Cisco converged mobile core network

Ericsson: Over 300 million Fixed Wireless Access (FWA) connections by 2028

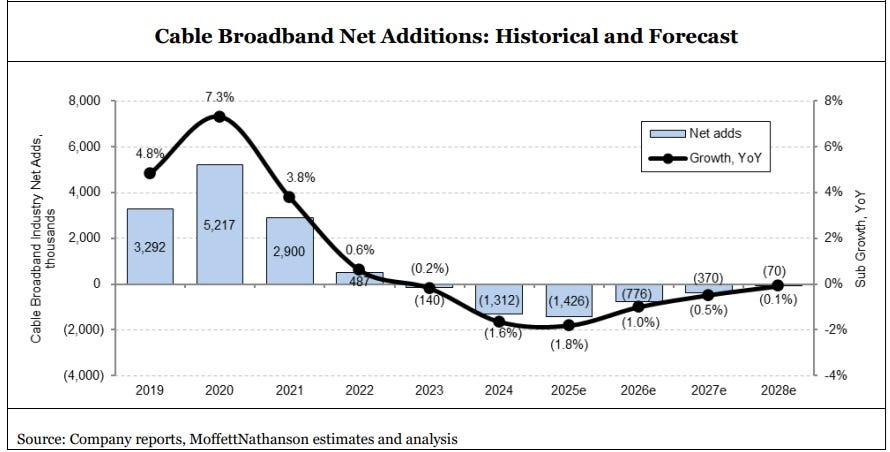

New Street Research study: Cable broadband will continue its decline, but total broadband access subscribers will increase

A recent New Street Research broadband trends study suggests that U.S. cablecos (previously called MSOs) aren’t likely to increase the net number of broadband internet subscribers during this decade, but their broadband losses are expected to decrease. The financial market research firm doesn’t anticipate cable broadband subscriber growth to be positive for at least another four to five years. Under New Street’s “base case,” cable broadband net adds will remain negative each year until 2030. Cable broadband is facing fierce competition on the high end from fiber to the premises (e.g. AT&T, Frontier/Verizon) and on the lower end from 5G FWA (e.g. T-MobileUS, Verizon).

Cable “is the new copper,” New Street Research analysts David Barden and Vikash Harlalka wrote, implying declining subscribers for xDSL based broadband will also happen to cablecos. Obviously, cablecos won’t like that characterization given that their hybrid fiber/coax (HFC) networks are mostly comprised of fiber. However, declining subscriber trends is not a commentary about the cable industry’s underlying broadband access network technology.

“While we expect cable losses to improve over time, we never have cable adds in aggregate turning positive,” New Street analysts David Barden and Vikash Harlalka wrote in a Tuesday report. “We think most investors agree with us and are not modeling positive subscriber growth for any of the large cable operators over the next 5 years.”

“With industry growth remaining below pre-pandemic levels and FWA adds remaining strong, we don’t expect Cable to grow subscribers this decade. Cable needs industry growth to improve and FWA adds to slow down to return to growth,” New Street’s analysts write in their 140-page report (subscribers only).

New Street outlines potential scenarios for how cable’s share of the broadband market will look by 2030:

-

Best case scenario – cable has 42% of the market as 84% of the market is divvied up between cable and fiber, while FWA gets 16%.

-

Plausible scenario – cable retains 32% share of the broadband market, with 80% of it being shared with fiber, and FWA capturing 20%.

-

Optimistic scenario – cable captures 50% of the broadband market, fueled by “superior marketing and cheaper mobile bundles,” compared to fiber (41%) and FWA (10%).

New Street expects cable’s “steady state terminal market share” to be just a bit higher than 40% across its footprint, down from 62% today.

The report also takes a look at how cable will fare in markets that overlap with fiber. New Street estimates that 75% of cable markets will have a fiber competitor in the years to come. When combining non-fiber and fiber markets, cable is expected to capture about 41% of the share in their footprints. That compares to fiber (34%), FWA (20%), DSL (2%) and satellite broadband (3%).

It only gets worse for cablecos, as their customer net promoter scores (NPS) [1.] are lower than their competitors (mostly telcos). Using data from Recon Analytics’ weekly survey of about 10,000 respondents, New Street’s study notes there’s a pronounced customer NPS gap for cable against its primary broadband rivals. Customer NPS scores from Comcast (2) and Charter (1) are just above water compared to Cox Communications (-1) and Optimum Communications (-8). Fiber providers are doing much better: AT&T Fiber (25), Verizon Fios (21), Frontier (17) and Lumen Fiber (1). FWA also holds a sizable customer NPS advantage: T-Mobile (31) and Verizon FWA (29).

Note 1. NPS is a customer loyalty metric that measures the likelihood of customers recommending a company to a friend or colleague, using a scale of \(0\)-\(10\). The score is calculated by subtracting the percentage of “detractors” (those who score \(0\)-\(6\)) from the percentage of “promoters” (those who score \(9\)-\(10\)), with “passives” (those who score \(7\)-\(8\)) not being factored into the final score. NPS is a single, easy-to-understand number that ranges from \(-100\) to \(+100\) and is used to gauge customer satisfaction and predict business growth. Customers are asked, “On a scale of \(0\)-\(10\), how likely are you to recommend [company] to a friend or colleague?”

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

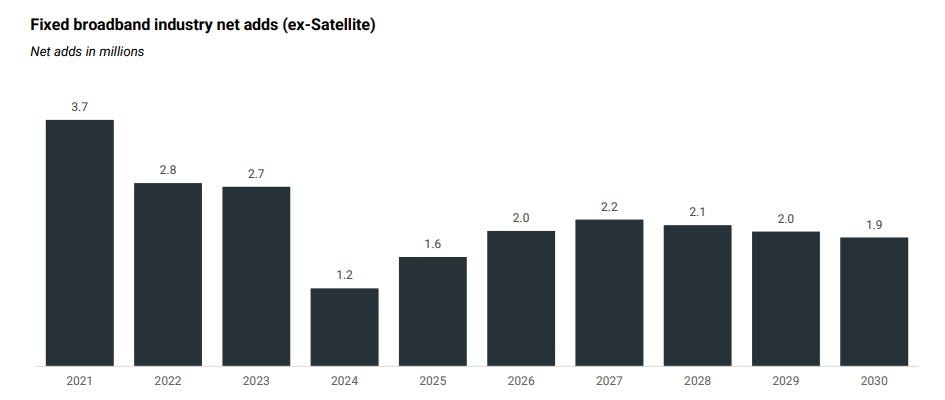

Considering all types of broadband access, New Street expects total net U.S. broadband net adds of 1.6 million, up from the 1.2 million from an earlier estimate. Fueled by fiber and FWA, net broadband subscriber adds are expected to continue above that level through 2030.

That growth will continue even as the market becomes increasingly saturated. New Street forecasts 139 million Internet households in 2030, up from 133 million at the end of 2025. Broadband penetration is expected to reach 93% by 2030, up from 87.7% at the end of 2025.

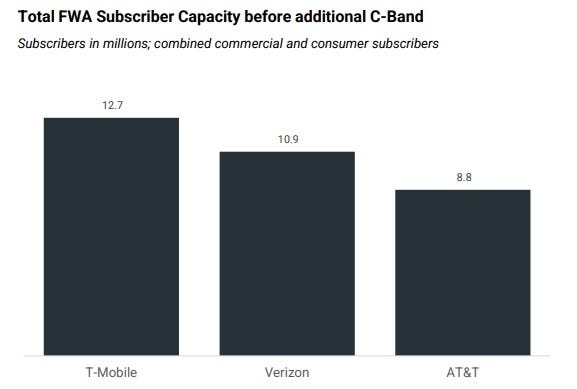

New Street expects U.S. network service providers to have 32 million to 36 million FWA subscribers in the coming years. However, the forecast expects a slight slowdown in FWA sub adds in 2026, coming in just below the range of 3.7 million to 3.8 million seen over the past three years. Next year, New Street expects FWA subscriber adds of 3.6 million (1.7 million for T-Mobile, 1 million for Verizon and 900,000 for AT&T). The analysts estimate that the carriers currently have enough capacity to support about 32 million FWA subs, estimating that carriers have already consumed about 55% of total capacity with new subs. That estimate does not include potential capacity coming from the upcoming auction of upper C-Band spectrum. That auction could provide capacity for another 4 million or so additional FWA subs, New Street said.

- Intense Competition: Cable operators are losing subscribers to FTTH, which offers faster speeds and higher reliability, and FWA services, which often appeal to customers seeking lower-priced or easily installed options.

- Market Saturation and Demographics: The broadband market is becoming increasingly saturated, and a slowdown in new household formation and people moving is curbing a key driver of new broadband connections.

- End of Government Subsidies: The expiration of government programs like the Affordable Connectivity Program (ACP) is impacting subscriber numbers, with major cable operators losing customers who relied on the subsidy.

- Network Upgrades: Cable companies are investing in network upgrades, such as DOCSIS 4.0, to improve speeds and performance, but it is not yet clear if these upgrades will significantly boost subscriber numbers.

Other Analyst Opinions:

- MoffettNathanson sees flattish cable broadband subscriber growth for the next couple of years, with a small gain in 2028. The firm projects subscriber losses in legacy markets will be eventually offset by gains from rural expansions and edge-out builds. “The conclusion for the two [Comcast and Charter] is about the same: even a near worst-case scenario yields roughly flat subscribership over the next five years or so,” Moffett wrote. “That’s a far cry from the doomsday scenarios we typically hear for the bear case.”

- In February 2025, Wolfe Research estimated that total industry net broadband additions for 2025 would be under 2 million, with cable providers bearing much of the slowdown.

- Grand View Research forecasts the global broadband services market (all connection types) to reach ~ US$ 875 billion by 2030, growing ~ 9.8% per year from 2025. In North America, broadband services revenue is expected to grow at ~ 8.3% CAGR from 2025 to 2030.

- Mordor Intelligence forecasts that the global market for hybrid-fiber coaxial (HFC — the backbone for many cable networks) will grow a 7.6% CAGR from $14.96 billion in 2025 to ~ $21.58 billion in 2030.

- An Ericsson analysis noted a projected decline of around 150 million DSL and cable connections globally between 2024 and 2030, with most growth coming from fiber, FWA, and satellite.

References:

https://www.lightreading.com/cable-technology/ouch-broadband-study-casts-cable-as-the-new-copper-

https://www.lightreading.com/cable-technology/cable-broadband-faces-a-flat-future-not-doomsday

https://telcomagazine.com/top10/top-10-global-fxxt-companies-in-telecoms

https://broadbandbreakfast.com/cable-unlikely-to-grow-subscribers-this-decade-new-street/

Highlights of 2025 Broadband Nation Expo: Comcast, T-Mobile keynotes + selected quotes

Dell’Oro: Abysmal revenue results continue: Ethernet Campus Switch and Worldwide Telecom Equipment + Telco Convergence Moves to Counter Cable Broadband

Cable broadband subscriber growth slows while FTTx and FWA gain ground

Aviat Networks and Intracom Telecom partner to deliver 5G mmWave FWA in North America

Aviat Networks, a wireless transport and access company, today announced a partnership with Intracom Telecom, a global technology systems and solutions provider, to deliver Fixed Wireless Access (FWA) technology using high-capacity 28 and 39 GHz millimeter wave (mmWave) bands, conforming to FCC requirements for mmWave bands intended for 5G use.

Aviat will initially focus on select North American service providers to address the growing need for multi-Gigabit consumer and enterprise 5G use cases as an alternative to the high cost, delays and complexity of using fiber, but with fiber-like performance. In addition, Aviat will offer software solutions along with a comprehensive set of design, planning, deployment and support services thanks to its extensive presence in North America.

Intracom Telecom’s WiBAS G5 platform is the only commercially available point-to-multipoint FWA solution operating in the 28 and 39 GHz mmWave bands that can address the growing demand for high-capacity Fixed Wireless Access, cost effectively delivering over 22Gbps from the same base station site, using Multi-User MIMO and Hybrid Massive Beamforming, over distances of up to 5 miles and more.

“We are very excited at this significant opportunity to extend our wireless expertise to provide advanced mmWave FWA solutions,” Pete Smith, CEO of Aviat Networks said, “Wireless can be deployed rapidly and cost effectively, and is perfectly suited to support high speed connectivity combined with excellent reliability.”

“I am very proud of Intracom Telecom’s R&D team for creating a solution that sets a new benchmark for FWA. Through this strategic partnership with Aviat Networks, we’re excited to help U.S. operators accelerate broadband expansion and deliver a true multi-gigabit experience, and more, over wireless,” said Kartlos Edilashvili, CEO of Intracom Telecom.

Image Source: Aviat Networks

In the U.S., Verizon, AT&T, and T-Mobile (including UScellular‘s retail wireless operations) use 28 GHz and 39 GHz millimeter wave (mmWave) bands for 5G services in densely populated areas and venues. mmWave signal propagation characteristics limit range/coverage and have a high susceptibility to blockage by physical objects and weather. These limitations significantly increase deployment costs and constrain coverage to densely populated areas.

About Aviat Networks:

Aviat, based in Austin, TX, is a leading expert in wireless transport and access solutions and works to provide dependable products, services and support to its customers. With more than one million systems sold into 170 countries worldwide, communications service providers and private network operators including state/local government, utility, federal government and defense organizations trust Aviat with their critical applications. Coupled with a long history of microwave innovations, Aviat provides a comprehensive suite of localized professional and support services enabling customers to drastically simplify both their networks and their lives. For more than 70 years, the experts at Aviat have delivered high performance products, simplified operations, and the best overall customer experience. Aviat is headquartered in Austin, Texas. For more information, visit www.aviatnetworks.com or connect with Aviat Networks on LinkedIn and Facebook.

About Intracom Telecom:

Intracom Telecom is a global technology systems and solutions provider operating for over 45 years in the market. The company is the benchmark in fixed wireless access, and it successfully innovates in the wireless access & transmission field. Furthermore, the company offers a comprehensive software solutions portfolio and a complete range of ICT services. Intracom Telecom serves telecom operators, public authorities and large public and private enterprises. The Group maintains its own R&D and production facilities, operates subsidiaries worldwide and has been active in the North American market since 2001, through its subsidiary, Intracom Telecom USA, based in Atlanta, Georgia. The parent company is located in Athens, Greece. For more information, visit www.intracom-telecom.com

References:

T-Mobile’s growth trajectory increases: 5G FWA, Metronet acquisition and MVNO deals with Charter & Comcast

Dell’Oro: 4G and 5G FWA revenue grew 7% in 2024; MRFR: FWA worth $182.27B by 2032

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

Aviat Sells TIP compliant 5G-Ready Disaggregated Transmission Network to Africell

U.S. Home Internet prices DECLINE amidst fierce competition between wireless carriers and cablecos

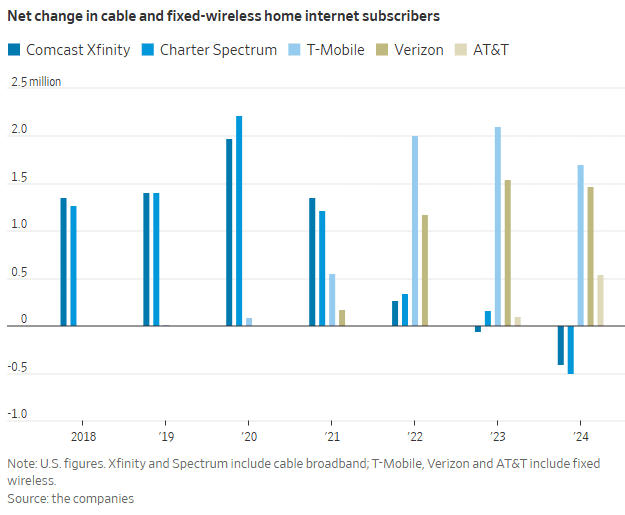

Home internet prices in the U.S. are being driven down by fierce competition between mobile carriers offering Fixed Wireless Access (FWA) and cable internet companies offering legacy Hybrid Fiber Coax connections. The increased competition has driven down the cost of home internet service, a welcome break for consumers when prices are rising for many other essential products. The price of home internet service fell 3.1% in May from a year earlier, while the overall consumer-price index rose 2.4%, according to the Labor Department.

The WSJ reports that major home-internet service providers including Verizon VZ, Comcast/Xfinity and T-Mobile launched a flurry of price-lock guarantees, promising steady rates for as long as five years. CableCos Charter, which is acquiring Cox, unveiled a three-year deal last year.

Cable companies have struggled to retain broadband internet subscribers since mobile carriers began offering more affordable 5G fixed-wireless access (FWA) internet service in 2018. FWA, which relies on over the air transmission to cell towers instead of HFC access, brought competition into markets where cable companies had long enjoyed being the only game in town. Now both types of providers are growing more aggressive to attract—and keep—customers.

“The cable companies went from gaining subscribers and raising rates every year to declining subscribers and giving people price locks,” said John Hodulik, a UBS analyst. “They’re seeing churn rise in their broadband subscriber base. And they’re trying to nip that in the bud.” Fixed wireless can sometimes cost half as much as a cable-provided internet plan. Though network congestion and other connectivity issues can be an issue for some users, the lower price point has been luring cable customers away.

T-Mobile, Verizon and AT&T added a combined 3.7 million FWA customers in 2024. In sharp contrast, Comcast’s Xfinity and Charter’s Spectrum lost more than 900,000 home internet subscribers. That’s depicted in this graph:

“Our pricing wasn’t breaking through in the marketplace,” said Steve Croney, chief operating officer for Comcast’s connectivity and platforms business. He said the company’s five-year price lock, introduced in April, competes well against the telecom companies’ offerings.

Frank Boulben, chief revenue officer at Verizon’s consumer group, said his company has been trying to address the “pain points” customers have with cable companies, such as price hikes. That’s why the telco is emphasizing FWA vs its FiOS fiber to the home based service. Boulben said his company would focus on selling fiber service to customers as it becomes available to them.

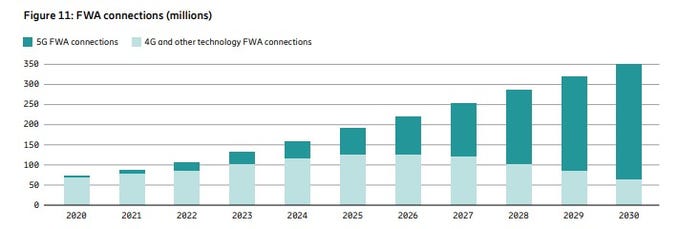

Is FWA the ONLY real killer application for 5G? Even though it was NOT one of the envisioned use cases? Ericsson’s recently released Mobility Report says FWA will account for more than 35% of all new fixed broadband connections, with an expected increase to 350 million by the end of 2030. The report states that more than half of all network service providers (wireless telcos) who offer FWA now do so with “speed-based monetization benefits enhanced by 5G.”

About 80% of the global network operators sampled by Ericsson currently offer FWA, with the most rapid area of growth among CSPs (communications service providers) offering 5G-enabled speed-based tariff plans. These opportunities are about the ability to offer a range of subscriber packages with different downlink and uplink data options with 5G FWA. As with fiber deals, “increasing monetization opportunities for CSPs compared to earlier generations of FWA.” 51% of operators with FWA offerings now include these speed-based options, which is up from 40% on the same period in June 2024 and represents a 27.5% increase. The June 2024 number had grown 50% on the June 2023 equivalent.

Source: Ericsson Mobility Report

…………………………………………………………………………………………………………………………………………………………………..

“We are at an inflection point, where 5G and the ecosystem are set to unleash a wave of innovation,” said Erik Ekudden, Ericsson Senior Vice President and Chief Technology Officer. “The recent advancements in 5G standalone (SA) networks, coupled with the progress in 5G-enabled devices, have led to an ecosystem poised to unlock transformative opportunities for connected creativity. Service providers have recognized this potential of 5G and are beginning to monetize it through innovative service offerings that extend beyond merely selling data plans. To fully realize the potential of 5G, it is essential to continue deploying 5G SA and to further build out mid-band sites. 5G SA capabilities serve as a catalyst for driving new business growth opportunities.”

Fixed-wireless doesn’t work everywhere. Besides congestion weak signals can make coverage spotty. If your cell phone doesn’t pick up 5G coverage smoothly, fixed-wireless from the same company probably won’t work either.

Verizon, AT&T and T-Mobile are winning converts to FWA at a faster pace than many anticipated, said Jonathan Chaplin, a managing partner at equity research firm New Street Research. Charter agreed to buy Cox last month for $21.9 billion in equity and assume $12 billion of its outstanding debt, in part to acquire scale to better compete with fixed wireless access. However, fixed-wireless growth can’t last indefinitely. The wireless networks on which they run will eventually hit capacity, limiting how many subscribers they can add. Chaplin estimates the networks can support around 19 million total fixed-wireless subscribers—which he predicts they will reach in about five years, accounting for planned network expansions that the companies have announced. When that limit is reached, cable companies may regain the upper hand and keep growing their fiber customer base, Chaplin said.

The big three wireless carriers (AT&T, Verizon and T-Mobile) have all been investing in fiber-based wired networks via build-outs and acquisitions. AT&T is bringing new customers in via FWA, with the long-term goal to convert them to fiber-based service, said Erin Scarborough, who runs that company’s broadband and connectivity initiatives.

References:

https://www.telecoms.com/5g-6g/ericsson-says-fwa-is-boosting-telco-monetization-opportunities

https://www.ericsson.com/en/reports-and-papers/mobility-report

https://www.consumeraffairs.com/news/cable-vs-wireless-war-is-driving-prices-down-062525.html

Dell’Oro: 4G and 5G FWA revenue grew 7% in 2024; MRFR: FWA worth $182.27B by 2032

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

T-Mobile posts impressive wireless growth stats in 2Q-2024; fiber optic network acquisition binge to complement its FWA business

5G Advanced offers opportunities for new revenue streams; 3GPP specs for 5G FWA?

FWA a bright spot in otherwise gloomy Internet access market

Dell’Oro: 4G and 5G FWA revenue grew 7% in 2024; MRFR: FWA worth $182.27B by 2032

According to Dell’Oro Group, Fixed Wireless Access (FWA) has surged in recent years to support both residential and enterprise connectivity due to its ease of deployment along with the more widespread availability of 4G LTE and 5G Sub-6GHz networks. Preliminary findings suggest total FWA revenues, including RAN equipment, residential CPE, and enterprise router and gateway revenue remain on track to advance 7% in 2024, driven largely by residential subscriber growth in North America and India, as well as growing branch office connectivity more globally.

“Initially viewed as a way to monetize under-utilized spectrum, FWA has grown to become a major tool for connecting homes and businesses with broadband,” said Jeff Heynen, Vice President with the Dell’Oro Group. “What started in the U.S. is now expanding to India, Southeast Asia, Europe, and the Middle East, as mobile operators continue to expand their 5G-based FWA offerings to both residential and enterprise customers,” added Heynen.

Additional highlights from the Fixed Wireless Access Infrastructure and CPE Advanced Research Report:

- Total FWA equipment revenue for the 2023-2027 period have been revised upward by 17 percent, reflecting continued positive subscriber growth in North America and India.

- Long-term subscriber growth is expected to occur in emerging markets in Southeast Asia and MEA, due to upgrades to existing 3G and LTE networks and a need to connect subscribers economically.

- The Satellite Broadband market will also be a key enabler of broadband connectivity in emerging markets as well as rural markets where existing infrastructure either doesn’t exist or is cost-prohibitive to deploy. Subscriber growth will generally come from LEOS-based providers including Starlink, OneWeb, and Project Kuiper.

The Dell’Oro Group Fixed Wireless Access Infrastructure and CPE Report includes 5-year market forecasts for FWA CPE (Residential and Enterprise) and RAN infrastructure, segmented by technology, including 802.11/Other, 4G LTE, CBRS, 5G sub-6GHz, 5G mmWave, and 60GHz technologies. The report also includes regional subscriber forecasts for FWA and satellite broadband technologies, as well as Residential Gateway forecasts for satellite broadband deployments. To purchase this report, please contact us by email at [email protected].

In a related Dell’Oro post, Stefan Pongratz wrote that Dedicated FWA RAN < $1B:

The market opportunity for DSL and fiber replacements or alternative solutions is vast. According to the ITU and Ericsson’s Mobility Report, approximately 35% of the world’s two billion households remain underserved, lacking broadband connectivity. Beyond these unconnected households, FWA technologies can also address the needs of secondary homes and small businesses. With nearly half of 5G operators supporting 5G FWA (GSA), fixed wireless is already a mature technology, boosting both the RAN and the broadband markets.

Despite these advancements, the fundamental economics driving FWA are not expected to shift significantly in 2025. While technological improvements are expanding the TAM, the business case remains constrained by the mobile network’s capacity and the ROI of dedicated FWA RAN deployments. Operators continue refining their targets, but the existing mobile network infrastructure offers the most favorable RAN economics.

Although operators are gradually increasing their investments in dedicated RAN solutions for high-traffic areas, mobile networks are expected to maintain dominance in the near term. According to our latest FWA report, which covers the broader FWA ecosystem—including 3GPP and non-3GPP RAN and devices—dedicated FWA RAN investments are projected to stay below $1 billion in 2025.

…………………………………………………………………………………………………………………

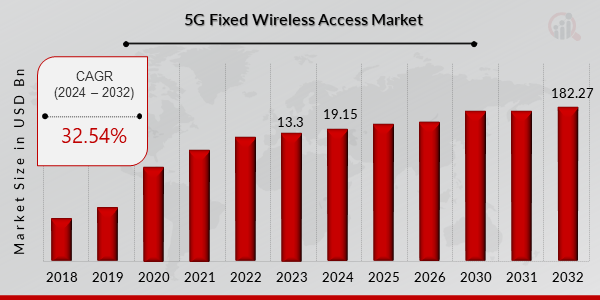

Separately, MRFR says the FWA market will be worth $182.27 Billion by 2032. Here’s a chart of 5G Fixed Wireless Access Market Growth:

FWA Growth Drivers:

Rising Demand for High-Speed Internet: With the increasing reliance on digital infrastructure and applications, there is a surging demand for high-speed and reliable internet connectivity. 5G FWA solutions offer ultra-fast broadband to underserved and remote areas, addressing connectivity gaps effectively.

Growing Adoption of IoT and Advanced Technologies: The proliferation of IoT devices and the need for seamless connectivity are driving the adoption of 5G FWA solutions. Additionally, advancements in mmWave technology enhance bandwidth efficiency, boosting market adoption.

Cost-Effective Alternative to Fiber Networks: 5G FWA provides a cost-efficient and rapid deployment option compared to traditional fiber-based internet, making it an attractive solution for internet service providers and enterprises.

References:

https://www.delloro.com/what-to-expect-from-ran-in-2025/

https://www.marketresearchfuture.com/reports/5g-fixed-wireless-access-market-7561

Latest Ericsson Mobility Report talks up 5G SA networks (?) and FWA (!)

Fiber and Fixed Wireless Access are the fastest growing fixed broadband technologies in the OECD

Ericsson: Over 300 million Fixed Wireless Access (FWA) connections by 2028

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

Ericsson’s November 2024 Mobility Report predicts that global 5G standalone (SA) connections will top 3.6 billion by 2030. That compares to 890 million at the end of 2023. Over that same period of time, 5G SA as a proportion of global mobile subscriptions is expected to increase from 10.5% to 38.4%, while average monthly smartphone data consumption will grow to 40 GB from 17.2 GB. By the end of the decade, 80% of total mobile data traffic will be carried by 5G networks.

That rosy forecast is in sharp contrast to the extremely slow and disappointing pace of 5G SA deployments to date. In January, Dell’Oro counted only 12 new 5G SA deployments in 2023, compared to the 18 in 2022. “The biggest surprise for 2023 was the lack of 5G SA deployments by AT&T, Verizon, British Telecom EE, Deutsche Telekom, and other Mobile Network Operators (MNOs) around the globe. As we’ve stated for years, 5G SA is required to realize 5G features like security, network slicing, and MEC to name a few.”

Fifty 5G Standalone enhanced Mobile Broadband (eMBB) networks commercially deployed (2020 – 2023):

The report states, “Although 5G population coverage is growing worldwide, 5G mid-band is only deployed in around 30% of all sites globally outside of mainland China. Further densification is required to harness the full potential of 5G.” Among the report highlights:

- Global 5G subscriptions will reach around 6.3 billion in 2030, equaling 67% of total mobile subscriptions.

- 5G subscriptions will overtake 4G subs in 2027.

- 5G is expected to carry 80% of total mobile data traffic by the end of 2030.

- 5G SA subscriptions are projected to reach around 3.6 billion in 2030.

Source: Ericsson Mobility Report -Nov 2024

“Service differentiation and performance-based opportunities are crucial as our industry evolves,” said Fredrik Jejdling, EVP and head of Ericsson’s networks division. “The shift towards high-performing programmable networks, enabled by openness and cloud, will empower service providers to offer and charge for services based on the value delivered, not merely data volume,” he added.

The Mobility Report provides two case studies in T-Mobile US and Finland’s Elisa – both of which have rolled out network slicing on their 5G SA networks and co-authored that section of the report:

- T-Mobile has been testing a high priority network slice to carry mission-critical data during special events.

- Elisa has configured a slice to support stable, high-capacity throughput for users of its premium fixed-wireless access (FWA) service, called Omakaista.

The Mobility Report doesn’t say if those two telcos are deriving any monetary benefit from network slicing, or more broadly from their 5G SA networks.

……………………………………………………………………………………………………………………………………………………………………………………………………………..

The Fixed Wireless Access (FWA) market has momentum:

- Ericsson predicts FWA connections will reach 159 million this year, up from 131 million in 2023.

- By 2030, connections are expected to hit 350 million, with 80% carried by 5G networks.

- In four out of six regions, 83% or more wireless telcos now offer FWA.

- The number of FWA service providers offering speed-based tariff plans – with downlink and uplink data parameters similar to cable or fiber offerings – has increased from 30% to 43% in the last year alone.

- An updated Ericsson study of retail packages offered by mobile service providers reveals that 79% have a FWA offering.

- There are 131 service providers offering FWA services over 5G, representing 54 percent of all FWA service providers.

- In the past 12 months, Europe has accounted for 73%of all new 5G FWA launches globally.

- Currently, 94% of service providers in the Gulf Cooperation Council region offer 5G FWA services.

- In the U.S. two service providers (T-Mobile US and Verizon) originally set a goal to achieve a combined 11–13 million 5G FWA connections by 2025. After reaching this target ahead of schedule, they have now revised their goal to 20–21 million connections by 2028.

- The market in India is rapidly accelerating, with 5G FWA connections reaching nearly 3 million in just over a year since launch. • An increasing number of service providers are launching FWA based on 5G standalone (SA).

References:

https://www.ericsson.com/en/reports-and-papers/mobility-report/reports/november-2024

https://www.ericsson.com/4ad0df/assets/local/reports-papers/mobility-report/documents/2024/ericsson-mobility-report-november-2024.pdf

5G Advanced offers opportunities for new revenue streams; 3GPP specs for 5G FWA?

FWA a bright spot in otherwise gloomy Internet access market

Where Have You Gone 5G? Midband spectrum, FWA, 2024 decline in CAPEX and RAN revenue

GSA: More 5G SA devices, but commercial 5G SA deployments lag

Vodafone UK report touts benefits of 5G SA for Small Biz; cover for proposed merger with Three UK?

Building and Operating a Cloud Native 5G SA Core Network

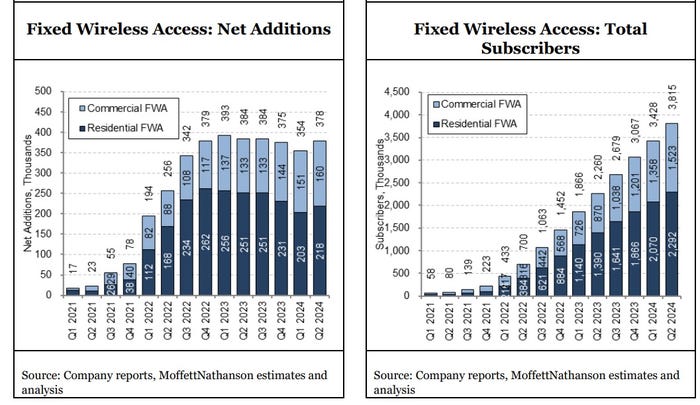

Verizon Q2-2024: strong wireless service revenue and broadband subscriber growth, but consumer FWA lags

Verizon Communications wireless and wireline subscriber growth expectations in the second quarter beat estimates with 148K postpaid phone net additions vs. 118K expected. There were 391,000 total broadband wireline net additions. The company ended the quarter with 11.5 million broadband subscribers, up 17.2% year over year. However, the telecom company posted lower operating revenue that was below expectations. Earnings mostly matched expectations, but were below the year ago level.

“Demand for the service is strengthening as small businesses and enterprises continue to trust the reliability of the product and the speed and east of deployment,” Verizon CFO Tony Skiadas said on Monday’s earnings call.

- Verizon added 160,000 business Fixed Wireless Access (FWA) subs in 2Q-2024 – a record quarterly gain in the category that was better than the 138,000 expected by analysts. That quarterly intake was up from a gain of 133,000 in the year-ago quarter and improved from a gain of 151,000 in the prior quarter. Verizon ended Q2 with 1.52 million business FWA subs.

- The company added 218,000 residential FWA subs in Q2 2024, down from a gain of 251,000 in the year-ago quarter, but ahead of the 208,000 residential FWA subs added in the prior quarter. Verizon ended the period with 2.29 million residential FWA subs.

A recent OpenSignal study revealed that Verizon’s 5G customers are rarely connected to the 5G network – in range just 7.7% of the time compared to AT&T (11.8%) and T-Mobile (67.9%). Verizon has not come close to adding as many FWA subs as T-Mobile has each quarter, particularly in the residential market.

New Street Research expects Verizon to cross the 4 million FWA subscriber mark in mid-August. In New Street’s follow-up note, analyst Jonathan Chaplin points to a recent estimate from the firm that data consumption among consumer FWA subs could be four to five time greater than business subscribers. On that basis, an estimate of FWA capacity for 4.1 million Verizon subs would really equate to 6.1 million total customers, he wrote.

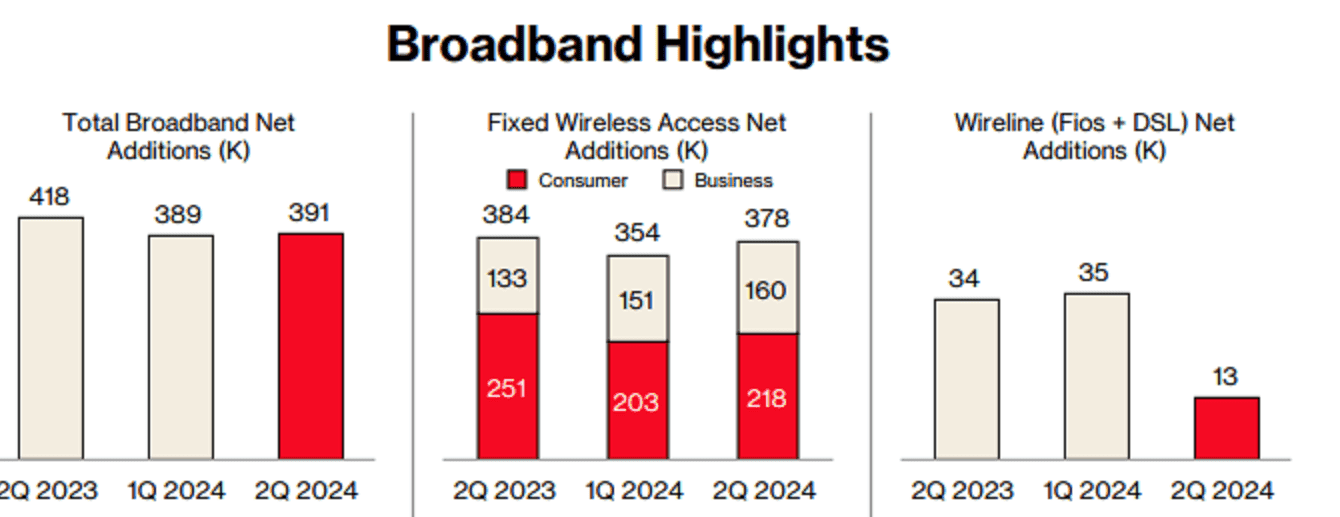

2Q 2024 Highlights:

Wireless: Accelerated growth in wireless service revenue

- Total wireless service revenue1 of $19.8 billion, a 3.5 percent increase year over year.

- Retail postpaid phone net additions of 148,000, and retail postpaid net additions of 340,000.

- Retail postpaid phone churn of 0.85 percent, and retail postpaid churn of 1.11 percent.

Broadband: Double-digit broadband subscriber growth

- Total broadband net additions of 391,000. This was the eighth consecutive quarter with more than 375,000 broadband net additions.

- Total fixed wireless net additions of 378,000. At the end of second-quarter 2024, the company had a base of more than 3.8 million fixed wireless subscribers, representing an increase of nearly 69 percent year over year.

- 11.5 million total broadband subscribers as of the end of second-quarter 2024, representing a 17.2 percent increase year over year.

- Fixed wireless revenue for second-quarter 2024 was $514 million, up more than $200 million year over year.

Other results and FY 2024 forecast:

- Verizon reported adjusted earnings of $1.15 a share for the quarter, in line with analyst expectations, but a slowdown from last year’s adjusted earnings of $1.21 a share. This was also the lowest earnings per share for a second quarter since 2017.

- Total operating revenue came in at $32.8 billion, 0.6% higher than a year ago, but below estimates of $33.8 billion.

- Total wireless service revenue was $19.8 billion, up 3.5% year over year, driven primarily by growth in Consumer wireless service revenue.

- FY-2024 Outlook: Verizon reiterated a 2.0% – 3.5% wireless service revenue growth. It maintained an adjusted EPS of $4.50 – $4.70 versus consensus of $4.58.

References: