capex

MTN Consulting: Generative AI hype grips telecom industry; telco CAPEX decreases while vendor revenue plummets

Ever since Generative (Gen) AI burst into the mainstream through public-facing platforms (e.g. ChatGPT) late last year, its promising capabilities have caught the attention of many. Not surprisingly, telecom industry execs are among the curious observers wanting to try Gen AI even as it continues to evolve at a rapid pace.

MTN Consulting says the telecom industry’s bond with AI is not new though. Many telcos have deployed conventional AI tools and applications in the past several years, but Gen AI presents opportunities for telcos to deliver significant incremental value over existing AI. A few large telcos have kickstarted their quest for Gen AI by focusing on “localization.” Through localization of processes using Gen AI, telcos vow to eliminate language barriers and improve customer engagement in their respective operating markets, especially where English as a spoken language is not dominant.

Telcos can harness the power of Gen AI across a wide range of different functions, but the two vital telco domains likely to witness transformative potential of Gen AI are networks and customer service. Both these domains are crucial: network demands are rising at an unprecedented pace with increased complexity, and delivering differentiated customer experiences remains an unrealized ambition for telcos.

Several Gen AI use cases are emerging within these two telco domains to address these challenges. In the network domain, these include topology optimization, network capacity planning, and predictive maintenance, for example. In the customer support domain, they include localized virtual assistants, personalized support, and contact center documentation.

Most of the use cases leveraging Gen AI applications involve dealing with sensitive data, be it network-related or customer-related. This will have major implications from the regulatory point of view, and regulatory concerns will constrain telcos’ Gen AI adoption and deployment strategies. The big challenge is the mosaic of complex and strict regulations prevalent in different markets that telcos will have to understand and adhere to when implementing Gen AI use cases in such markets. This is an area where third-party vendors will try to cash in by offering Gen AI solutions that are compliant with regulations in the respective markets.

Vendors will also play a key role for small- and medium-sized telcos in Gen AI implementation, by eliminating constraints due to the lack of technical expertise and HW/SW resources, skilled manpower, along with opex costs burden. Key vendors to watch out for in the Gen AI space are webscale providers who possess the ideal combination of providing cloud computing resources required to train large language models (LLM) coupled with their Gen AI expertise offered through pre-trained models.

Other key points from MTN Consulting on Gen AI in the telecom industry:

- Network operations and customer support will be key transformative areas.

- Telco workforce will become leaner but smarter in the Gen AI era.

- Strict regulations will be a major barrier for telcos.

- Vendors key to Gen AI integration; webscale providers set for more telco gains.

- Lock-in risks and rising software costs are key considerations in choosing vendors.

………………………………………………………………………………………………………………………………

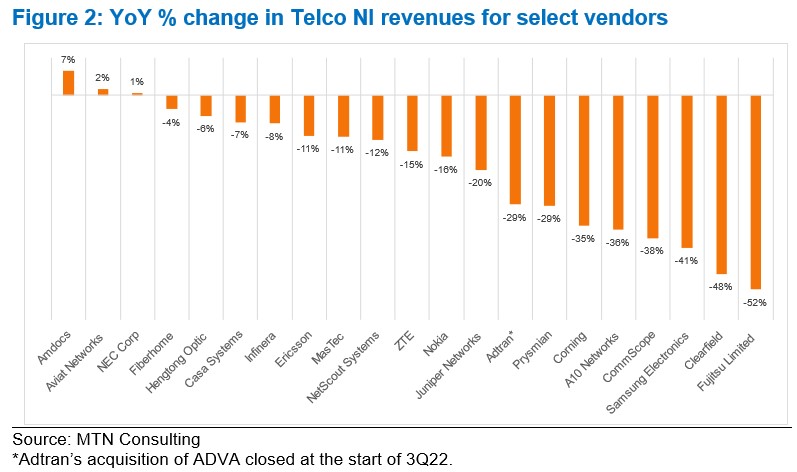

Separately, MTN Consulting’s latest forecast called for $320B of telco capex in 2023, down only slightly from the $328B recorded in 2022. Early 3Q23 revenue reports from vendors selling into the telco market call this forecast into question. The dip in the Americas is worse than expected, and Asia’s expected 2023 growth has not materialized.

Key vendors are reporting significant YoY drops in revenue, pointing to inventory corrections, macroeconomic uncertainty (interest rates, in particular), and weaker telco spending. Network infrastructure sales to telcos (Telco NI) for key vendors Ericsson and Nokia dropped 11% and 16% YoY in 3Q23, respectively, measured in US dollars. By the same metric, NEC, Fujitsu and Samsung saw +1%, -52%, and -41% YoY growth; Adtran, Casa, and Juniper declined 29%, 7%, and 20%; fiber-centric vendors Clearfield, Corning, CommScope, and Prysmian all saw double digit declines.

MTN Consulting will update its operator forecast formally next month. In advance, this comment flags a weaker spending outlook than expected. Telco capex for 2023 is likely to come in around $300-$310B.

MTN Consulting’s Network Operator Forecast Through 2027: “Telecom is essentially a zero-growth industry”

MTN Consulting: Top Telco Network Infrastructure (equipment) vendors + revenue growth changes favor cloud service providers

Proposed solutions to high energy consumption of Generative AI LLMs: optimized hardware, new algorithms, green data centers

Cloud Service Providers struggle with Generative AI; Users face vendor lock-in; “The hype is here, the revenue is not”

Global Telco AI Alliance to progress generative AI for telcos

Amdocs and NVIDIA to Accelerate Adoption of Generative AI for $1.7 Trillion Telecom Industry

Bain & Co, McKinsey & Co, AWS suggest how telcos can use and adapt Generative AI

Generative AI Unicorns Rule the Startup Roost; OpenAI in the Spotlight

Generative AI in telecom; ChatGPT as a manager? ChatGPT vs Google Search

Generative AI could put telecom jobs in jeopardy; compelling AI in telecom use cases

MTN Consulting: Satellite network operators to focus on Direct-to-device (D2D), Internet of Things (IoT), and cloud-based services

MTN Consulting on Telco Network Infrastructure: Cisco, Samsung, and ZTE benefit (but only slightly)

MTN Consulting: : 4Q2021 review of Telco & Webscale Network Operators Capex

Synergy Research: Growth in Hyperscale and Enterprise IT Infrastructure Spending; Telcos Remain in the Doldrums

Hyperscale cloud companies are spending more and more money on Capex IT infrastructure compared with the largest telecommunication companies as overall IT infrastructure spending in 2022 reached $700 billion. In 2022, hyperscale operators spent roughly $200 billion on Capex IT infrastructure such as network switches and data center hardware and software, representing a 9 percent increase annually and led by Amazon, Google and Microsoft, according to new data from IT market research firm Synergy Research Group.

Comparatively, telecom spending on IT infrastructure by companies like Verizon, AT&T and China Mobile dropped 4 percent in 2022 to approximately $290 billion, Synergy Research Group reported.

Hyperscale operator share of total spending has continued to rise steadily over the last few years, as continued growth in cloud and other digital services drive ever-higher spending levels. Telco spending remains heavily crimped by lack of meaningful growth in their revenue streams. Enterprise spending has also bounced back in the last two years after a soft spell in 2019 and 2020. The main drivers in the enterprise have been the continued long-term growth of hosted and cloud collaboration solutions, increased spending on network security, and a post-pandemic bounce back for both enterprise data centers and switches. In some segments, higher ASPs have also contributed, as cost increases due to supply chain issues are passed on to the customers of tech vendors.

Telcos remain locked in a low-to-no-growth world and their Capex reflects that. For hyperscale operators, the boom in cloud services and continued growth in other digital services is driving ongoing growth in spending. Telecom companies’ share of Capex IT infrastructure spending was 42 percent in 2022, down from 58 percent share in 2016. The largest telco spenders on technology infrastructure last year were China Mobile, Deutsche Telekom, Verizon, AT&T, NTT and China Telecom.

In 2022, hyperscale operators accounted for 29 percent share of the total Capex infrastructure spending market, up significantly from 13 percent share in 2016. Some of the biggest spenders in 2022 were Amazon, Apple, Google, Microsoft and Alibaba.

Overall spending by both fixed and mobile telco operators has been relatively flat over the past eight years, with annual spending levels for infrastructure hovering around $290 billion each year. Synergy market data covers total capital expenditure for telco and hyperscale operators mostly around networking and data center hardware and software.

The final market segment covered in Synergy’s new data is enterprise spending on IT infrastructure, which grew 9 percent year over year in 2022 to roughly $210 billion. The enterprise spend accounted for 29 percent of the total Capex infrastructure market in 2022.

“Enterprise spending has also bounced back a bit in the last two years after a soft spell in 2019 and 2020,” said Dinsdale. ince 2016, enterprise IT spending has grown by an average of over 6 percent annually. Synergy said to make the market data numbers more comparable, enterprise spending covers data center hardware and software, networking and collaboration tools. It excludes enterprise spending on communication and IT services, devices and business software.

“There has also been something of a post-pandemic bounce back for both enterprise data centers and switches, the former being helped by higher costs due to supply chain issues that are being passed on in the form of higher ASPs [average selling price],” said Dinsdale. “For equipment and software vendors, the good news is that overall IT infrastructure spending will continue to grow steadily over the next five years,” he added.

…………………………………………………………………………………………………………………………………………………………………………………………………..

About Synergy Research Group:

Synergy provides quarterly market tracking and segmentation data on IT and Cloud related markets, including vendor revenues by segment and by region. Market shares and forecasts are provided via Synergy’s uniquely designed online database SIA ™, which enables easy access to complex data sets. Synergy’s Competitive Matrix ™ and CustomView ™ take this research capability one step further, enabling our clients to receive on-going quantitative market research that matches their internal, executive view of the market segments they compete in.

Synergy Research Group helps marketing and strategic decision makers around the world via its syndicated market research programs and custom consulting projects. For nearly two decades, Synergy has been a trusted source for quantitative research and market intelligence.

To speak to an analyst or to find out how to receive a copy of a Synergy report, please contact [email protected] or 775-852-3330 extension 101.

…………………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://www.crn.com/news/cloud/cloud-provider-spend-on-it-capex-climbs-as-telecom-falls

Synergy Research: public cloud service and infrastructure market hit $126B in 1Q-2022

Synergy Research: Microsoft and Amazon (AWS) Dominate IT Vendor Revenue & Growth; Popularity of Multi-cloud in 2021

Synergy Research: Hyperscale Operator Capex at New Record in Q3-2020

Synergy Research: Strong demand for Colocation with Equinix, Digital Realty and NTT top providers

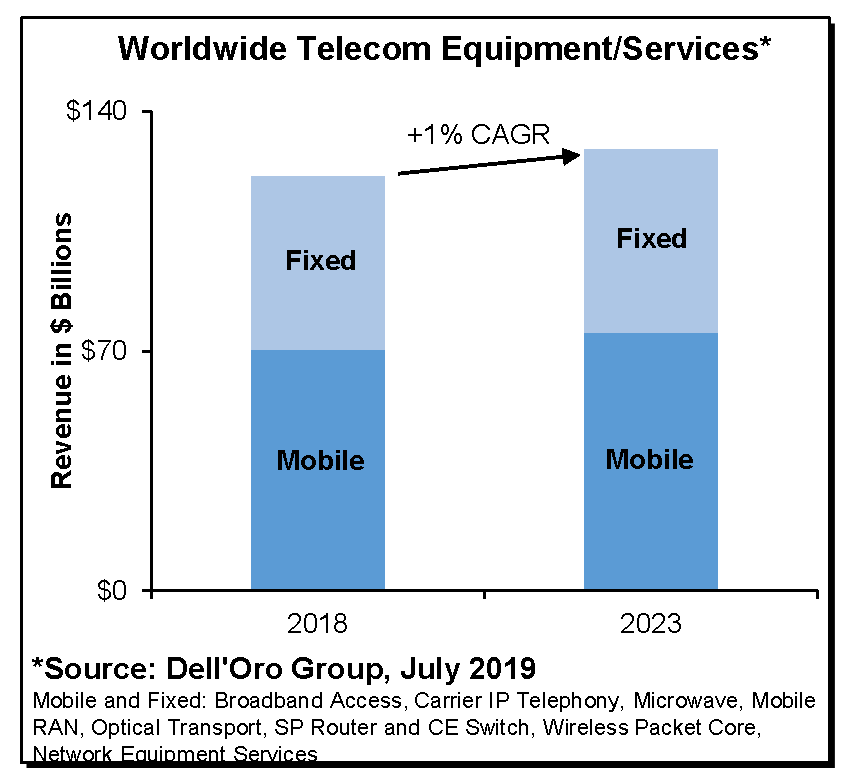

Dell’Oro: Telecom Capex Growth to Slow in calendar years 2022-2024

Dell’Oro Group forecasts that telco capex growth will taper off in 2023 and 2024 after increasing 9% year-over-year in nominal USD terms and on track to advance 3% in 2022.

The market research firm states that the top fifty carriers in the world collectively generated combined annual revenue and investments of well over $1.4 T this past year. They estimate that these carriers account for roughly 80% of worldwide capex and revenue.

Dell’Oro’s Telecom Capex bi-annual reports (previously called Carrier Economics bi-annual reports) track the revenue and capital expenditure (capex) trends for these fifty-plus carriers.

“Telco investments, in general, have shown remarkable resilience to external factors including Covid-19 containment measures, supply chain disruptions, and economic uncertainties,” said Stefan Pongratz, Vice President and analyst with the Dell’Oro Group. “Surging wireless investments in the US taken together with non-mobile capex expansions in China will keep the momentum going in 2022,” continued Pongratz.

Stefan believes carrier revenue and capex trends can to some degree explain telecom equipment manufacturer revenue trends. The highly granular information provided in this report will enable carriers, system and component vendors, equity researchers, and regulatory bodies to assess growth opportunities and to observe performance practices in the telecom sector.

Additional highlights from the March 2022 3-year Telecom Capex forecast report:

- Global capex growth is expected to moderate from 9 percent in 2021 to 3 percent in 2022, before tapering off in 2023 and 2024.

- The coupling between carrier investments and manufacturing infrastructure revenues is expected to prevail over the short-term—capex and telecom equipment are on track to advance 3 percent and 4 percent in 2022, respectively.

- Short-term output acceleration is expected to be relatively broad-based, with investments growing in China and the US. At the same time, challenging comparisons in the US are expected to drag down the overall capex in the outer part of the forecast.

- Following a strong showing in 2021, capex growth prospects across Europe will be more muted in 2022.

Editor’s Note:

MTN Consulting estimates a nearly $325B annualized global capex in 2021, or nearly double the webscale total of $175B. The ratio of capex to revenues, or capital intensity, reached 17.2% in 2021, the highest level since 2015.

Excluding China/HK-based companies (which haven’t finished reporting), the top 10 biggest telco capex spenders in 2021 were AT&T, DT, Verizon, NTT, Comcast, Vodafone, Orange, Charter, America Movil, and Telefonica. The biggest capex gains in 2021 were seen at America Movil (+$2.54B versus 2020 total), Telecom Italia (+$2.49B), Verizon (+$2.09B), AT&T (+$1.93B), Deutsche Telekom (+$1.74B), BT (+$1.63B), and Rakuten ($1.47B). The DT jump is inflated slightly by its Sprint acquisition, which closed in April 2020.

MTN’s latest official global capex forecast is for $328B in 2022, a bit higher than 2021. “We are maintaining this target for now, but there is a high level of uncertainty and considerable downside risk.” No forecast beyond 2022 was provided.

The Dell’Oro Group Telecom Capex Report provides in-depth coverage of more than 50 telecom operators highlighting carrier revenue, capital expenditure, and capital intensity trends. The report provides actual and 3-year forecast details by carrier, by region by country (United States, Canada, China, India, Japan, and South Korea), and by technology (wireless/wireline). To purchase this report, please contact by email at [email protected].

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications and enterprise networks infrastructure, network security and data center IT markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions. For more information, please contact Dell’Oro Group at +1.650.622.9400 or visit www.delloro.com.

China is already showing signs of slowing its 5G investment – China Telecom plans to reduce 5G investment by nearly 11% to 34 billion yuan (US$5.34 billion) this year, reported Light Reading’s Robert Clark in March. China Mobile has budgeted 110 billion yuan (US$17.3 billion) for spending on 5G networks in 2022, a 3.5% decline.

In the US, Dish Network is among service providers upping their 5G investments this year. Dish spent $1 billion on 5G-related capex in 2021 and plans to spend $2.5 billion in 2022 , reported Light Reading’s Jeff Baumgartner in February.

On the other hand, IDC doesn’t expect telecom capex to drop until 2024:

“COVID-19 has shown no long-term negative effects on telecommunications capex. IDC expects 2021 capex will grow versus 2020 and show no decline until at least 2024. If anything, COVID-19 has led to communications service providers increasing their network investments to sustain increase demand for connectivity and the speeds associated with it.” said Daryl Schoolar, IDC research director, Worldwide Telecommunications Insights.

References:

Worldwide Telecom Capex Growth to Taper Off in 2023, According to Dell’Oro Group

https://www.lightreading.com/5g/telco-capex-could-level-out-in-2023-delloro-reports/d/d-id/776610?

MTN Consulting: : 4Q2021 review of Telco & Webscale Network Operators Capex

https://www.idc.com/getdoc.jsp?containerId=US48465621

MTN Consulting: : 4Q2021 review of Telco & Webscale Network Operators Capex

by Matt Walker

Webscale revenues surge 25% to $2.1 trillion in 2021; capex of $175B drives global data center demand.

Introduction:

Revenues for the webscale sector of network operators ended 2021 at $2.14 trillion. That’s up 25% from 2020, and nearly 3x the total recorded in 2011. One reason for this is a dramatic uptick in cloud services revenues: cloud revenues for the top 3 (AWS, GCP and Azure) climbed 42% YoY, to $120.3B (per MTN Consulting). Still, this accounts for less than 6% of total webscale sector revenues. Larger factors behind 2021’s growth include: digital ad revenues for Alphabet and Facebook (Meta); ecommerce sales at Amazon, JD.Com, and Alibaba; and, 5G device revenue sales at Apple. The webscale sector is now comfortably larger than telecom, which recorded just under $1.9 trillion in 2021 revenues.

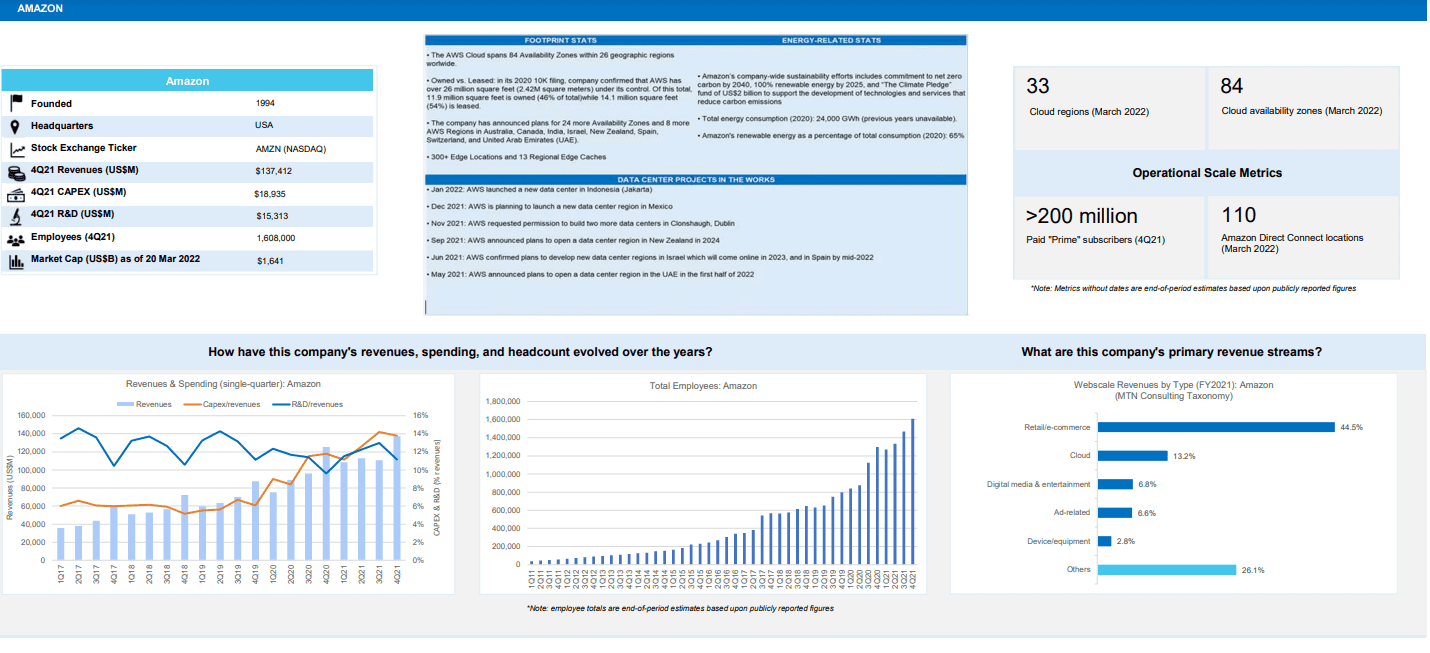

Here’s the profile for Amazon:

Capex- Telcos vs Webscalers:

On a capex basis, telecom remains far ahead, with nearly $325B in 2021 annualized capex, or nearly double the webscale total of $175B. Excluding China/HK-based companies (which haven’t finished reporting), the top 10 biggest telco capex spenders in 2021 were AT&T, DT, Verizon, NTT, Comcast, Vodafone, Orange, Charter, America Movil, and Telefonica. The biggest capex gains in 2021 were seen at America Movil (+$2.54B versus 2020 total), Telecom Italia (+$2.49B), Verizon (+$2.09B), AT&T (+$1.93B), Deutsche Telekom (+$1.74B), BT (+$1.63B), and Rakuten ($1.47B). The DT jump is inflated slightly by its Sprint acquisition, which closed in April 2020.

However, webscale is gradually bridging the capex gap with telcos: webscale capex spiked 30% YoY in 2021, versus an approximate 10% rise for telco capex. Capex in 4Q21 for webscalers was $50B, up 23% YoY. Webscalers also invest heavily in R&D, and have bleeding-edge requirements for the technology they deploy in their network. That has led them to drive the creation of many new innovations in network infrastructure over the last few years. These span semiconductors, optical transmission and components, intent-based routing, network automation, and other areas.

Facebook (Meta) is perhaps the most influential of all webscalers due in part to its openness and support for the OCP and TIP organizations.

Asia Pacific records best recent revenue growth in 2021

Regionally, the strongest growth in 2021 was in Asia Pacific, where revenues grew 29% YoY. The more mature Americas region lagged, with growth of just over 21% YoY. That pushed Americas down to about 44% of global webscale revenues, from 45% in 2020. Asia Pacific follows, with a 36% global revenue share, then Europe (17%) and MEA (3%). The Americas still account for the majority of webscale capex, with the US at the center. For instance, both Alphabet and Facebook (Meta) say well over 70% of their “long-lived assets” are in the US. Going forward, the non-US portion should rise as the cloud providers within the webscale market build out their global data center footprints. In January 2022, for example, AWS launched its first data center in Jakarta, Indonesia, and is planning a new region in Mexico.

Profitability still relatively high, but weaker than 2020:

Using a standardized definition of free cash flow (cash from operations less capex), the webscale sector’s FCF was $347.4B in 2021, or 16.2% of revenues. That is down significantly from a 19.7% margin in 2020. This ratio is still high relative to many sectors, however. The decline is due largely to a webscaler choice to accelerate capex during the COVID dislocation; that should pay off over the long run. Oracle, for instance, saw its FCF drop from 30.8% in 2020 to 17.2% in 2021, due mainly to its rapid cloud expansion. Nonetheless, Oracle says it will continue capex at a roughly $1B per quarter run rate, as it aspires to be the fourth major cloud provider with global scope. Amazon is actually the worst hit company in terms of FCF margin drop, due directly to its enormous 2021 capex outlays: Amazon’s FCF in 2021 was -3.1%, from 6.7% in 2020. Amazon, however, says its 2022 infrastructure (AWS) capex will likely rise.

Cash on hand, including short-term liquid investments, amounted to $747B for the webscale sector at the end of 4Q21, down 2% from the end of 2020. Total debt increased by 7%, to $518B. As a result, net debt (debt minus cash) in Dec. 2021 was -$228B for the webscale sector, from -$280B in December 2020. The companies with the biggest stockpiles of cash (and equivalents) are Alphabet ($139.6B), Microsoft ($125.4B), Amazon ($96.0B), and Apple ($63.9B). Facebook has just $48B, but no debt at all. Apple, IBM, and Oracle all have significantly more debt than cash.

Top 8 webscalers remain the biggest spenders, but Oracle and Twitter also important

This webscale tracker considers a “Top 8” group of companies as being, traditionally, the most influential in the market’s overall technology development and investments. These include three Chinese Internet companies (Alibaba, Baidu and Tencent), the world’s leading smartphone provider (Apple), the world’s biggest social media company (Facebook), and the leading three cloud providers: Alphabet, Amazon, and Microsoft. Ranking webscalers based on their share of tech capex, Amazon tops the list easily, accounting for 27.0% of network/IT capex in 2021. Amazon is followed by Alphabet (16.2%), Microsoft (14.0%), Facebook (10.0%), Tencent (6.3%), Apple (5.0%), Alibaba (4.1%), Oracle (2.9%), Baidu (2.1%), IBM (1.7%), HPE (1.5%), and Twitter (1.3%). Amazon’s recent capex surge is well known, and has supported expansion of the company’s AWS footprint and service offerings. Oracle has been quieter but its capex growth is equally impressive, from a smaller base: 2021 capex was $3.1B, up 70% from 2020. Twitter, a new addition to our webscale coverage, spends more on network/IT capex as a percentage of revenues (over 19%) than all other webscalers, due to ongoing software development and construction of its first owned data center.

The facilities these webscale players are building can be immense. For instance, Microsoft started construction recently on two new data centers in Des Moines Iowa, each of which costs over $1B and measures over 167K square meters (1.8 million square feet). These two are part of a cluster in the area, as is often the case; Microsoft already has three facilities around Des Moines. Facebook is working on a project in DeKalb, Illinois, roughly half the size at 84.2K square meters, costing US$800M and spreading across 500 acres of land. This construction project was announced in 2020 but won’t complete until 2023. These are just two examples of the many big facilities in the works in the webscale sector.

Who benefits from webscale capex?

The network spending of big webscalers is centered around immense, “hyperscale” data centers and undersea cable systems that support network traffic from the tech companies’ online retail, video, and social media platforms, along with cloud services. Webscale network operators (WNOs) may also own access networks, typically using fiber, microwave or mmWave, and even fixed satellite. WNOs exploring outer space for providing connectivity include Amazon, Apple, Alphabet, Facebook, and Microsoft.

A broad set of vendors are benefiting from WNO capex spending – from semiconductor players selling into the data center market (Intel, AMD, Nvidia, Broadcom, etc), to optical components & transport vendors selling into data center interconnect markets (e.g. Infinera, II-VI, Lumentum/Neophotonics), to contract manufacturers of white box/OCP servers (e.g. Wistron and Quanta). Cisco, for instance, recorded approximately $4.0B in 2021 sales to the webscale sector, up from about $2.1B in 2020. The construction industry also sees webscale as important, as much of their capex is for development of data center properties.

Network investment outlook:

Our current forecast calls for $187B of webscale capex in 2022, and further growth in the out-years until capex hits about $252B in 2026. For now, we are maintaining these targets. Despite a modest slippage in profitability, cash/debt and top-line growth in 4Q21, the sector retains many strengths which won’t go away overnight. Cloud services revenue growth remains strong, as does profitability for most players. Moreover, 2022 capex guidance from the major webscalers suggests modest growth; a summary follows:

- Amazon: 4Q21 earnings call confirmed that network/IT (“infrastructure” for AWS) is about 40% of total, consistent with MTN Consulting assumptions. Other components are fulfillment/logistics and transportation. For future capex, it says “we’re still working through some of our plans for 2022, but it’s coming into focus a bit. We see the CapEx for infrastructure going up…we’re adding regions and capacity to handle usage that still exceeds revenue growth in that business. So we feel good about making those investments.”

- Facebook (Meta): still calling for 2022 capex, including principal payments on finance leases, in the range of $29-34 billion (2021 actual: $19.2 billion). Says capex is driven by investments in data centers, servers, network infrastructure, and office facilities, and next year’s figure “reflects a significant increase in our AI and Machine Learning investments, which will support a number of areas across our Family of Apps.”

- Alphabet: projects a “meaningful increase in CapEx” for 2022, due to both technical infrastructure (mainly servers) and office facilities, where the company says it is “reaccelerating investment in fit-outs and ground-up construction.”

- Microsoft: expects 1Q22 capex to decline sequentially versus 4Q21, a change from the prior year period when 1Q21’s total capex was up 22% versus 4Q20. Does not provide any longer-term guidance. Its pending acquisition of Activision Blizzard is likely a factor in future plans, for two reasons. First, the deal consumes a lot of cash, and second, absorbing Activision would likely come with some changes in data center strategy. Currently Activision does not have any of its own data centers, rather, it rents colocation space in third-party facilities. The combined company will clearly want to see benefits from Microsoft’s data center footprint.

- Oracle: expects capex to continue in the roughly $1B per quarter range through the end of its current fiscal year (May 2022).

- Tencent: no concrete guidance but has hinted at Facebook-like investments in the “metaverse,” says it has a lot of the building blocks needed, for example, “a lot of gaming experiences…very strong social networking experience…engine capability, we have AI capability, we have the capability to build a large server architecture that can serve a huge number of concurrent users. We are very experienced in managing digital content economies as well as real-life digital assets.”

- Apple: nothing concrete on capex specifically, but in April 2021 it announced “$430 billion in contributions to the US economy include direct spend with American suppliers, data center investments, capital expenditures in the US, and other domestic spend…”

- Alibaba: no concrete guidance but 4Q21 call said it will continue to “invest in expanding its international infrastructure,” saying it now provides cloud services in 25 regions globally and that it is “committed to serving the real economy for the long term and the digitalization of all industries”. At its Apsara conference in October 2021, the company unveiled several new proprietary products, including Yitian 710 server chip, the X-Dragon architecture, Panjiu cloud-native server series, Alibaba AI and big data platform and a new generation of PolarDB database. It has global aspirations for its IaaS and PaaS services.

- Baidu: hasn’t addressed capex recently but on 4Q21 earnings call cited strong cloud demand growth, and said it is “trying to retain rapid revenue growth for 2022 and beyond,” which will require infrastructure investments.

- Twitter: its capex appears to be moderating now that it has (largely) completed construction of its new data center.

While we are maintaining the forecast outlook as published in Dec 2021, Amazon is a wildcard. It provides no specific guidance, and is clearly the market leader. Its quarterly outlays will be watched carefully. Even if its total capex does moderate, it is possible that the network/IT % of total will rise.

Implications for carrier-neutral market segment:

Webscalers with cloud operations are building out their data center footprints, and most webscalers are deploying more complex functionality into their networks (video, gaming, AI, metaverse). However, webscalers do have some financial pressures, and more important have an increasingly rich range of options for how they expand. The carrier-neutral segment (CNNO) of data center players is investing heavily in larger, more hyperscale-friendly and energy efficient facilities. Further, the sector is consolidating with help from private equity. MTN Consulting expects webscalers to continue to lean heavily on these third-parties for expansion in 2022 and beyond. As a result, data center CNNOs like Digital Realty, Equinix and its JV partners, QTS/Blackstone, CyrusOne/KKR/GIP, American Tower/CoreSite, and GDS will become more attractive to vendors as they invest more in network technology of their own.

References:

MTN Consulting: Network Infrastructure market grew 5.1% YoY; Telco revenues surge 12.2% YoY

MTN Consulting: Network operator capex forecast at $520B in 2025

Will AT&T’s huge fiber build-out win broadband market share from cablecos/MSOs?

AT&T added 235,000 fiber connections in the first quarter, ending the period with nearly 5.2 million total fiber customers. AT&T says they have a total of around 15 million fiber and non-fiber customers, so fiber access is approximately 1/3 of total customers now.

The company recently announced it plans to build fiber to 3 million new customer locations this year and 4 million next year. AT&T plans to double the number of locations where it offers fiber Internet, from approximately 15 million to about 30 million, by 2025. To do that, AT&T is planning to increase its annual capital expenses from $21 billion to around $24 billion.

AT&T’s new focus on connectivity over content is a direct result of its spinning off Warner Media to Discovery, as we chronicled in this IEEE Techblog post. Thaddeus Arroyo, head of AT&T’s consumer business, made that crystal clear at a recent BoA investor event:

“We expect capital expenditures of about $24 billion a year after the Warner Media discovery transaction closes. That’s an incremental investment that’s going to go to fiber to 5G capacity and 5G C-band deployment.

We have another great opportunity, the one we continue to talk around fiber. So as part of this capital, we’re going to be investing in fiber expansion to meet the growing needs for bandwidth that require a much more robust fiber network regardless of the last mile serving technology. Fiber is the foundation that fuels our network. Expanding our fiber reach serves multiple services hanging off at each strand of fiber. It includes macro cell sites, small cell sites, wholesale services, enterprise, small business, and fiber that’s extended directly into our customers’ homes and into businesses.

We plan to reach 30 million customer locations passed with fiber by the end of 2025. That’s going to double our existing fiber footprint. And investing in fiber drives solid returns because it’s a superior product. Where we have fiber we win, we’re improving share in our fiber footprint, and the penetration rates are accelerating and growing, given our increased financial flexibility. We’re comfortable in our ability to invest and achieve our leverage targets that we outlined of getting to 2.6% at close and below 2.5% by the end of 2023.”

Mo Katibeh, the AT&T executive responsible for fiber and 5G build-outs, added on via a recent post on LinkedIn: “We are building MORE Fiber to MORE homes and businesses. And we’re talking A LOT of fiber – MILLIONS of new locations every year, planning to cover 30 MILLION customer locations by the end of 2025! And you know what comes with all that investment in America? JOBS. Our AT&T Network Build team is GROWING..”

Previously, Katibeh wrote on LinkedIn : “Contributing to a large portion of the $105B Capital spend between 2016 and 2020 – our team is building out AT&T #Fiber to MILLIONS of new customer locations in 2021, as well as augmenting America’s best mobility network with more capacity, more speed – and more #5G (you know I love 5G!).”

…………………………………………………………………………………………………………………………………………………………..

So with all that said, will AT&T’s fiber build-out keep pace with cable companies/MSOs DOCSIS networks?

Tom Rutledge, Charter’s CEO, made a brief comment about plant upgrades on the earnings call (note – Dave Watson made similar comments on the Comcast earnings call):

“We’re continuously increasing the capacity in our core and hubs and augmenting our network to improve speed and performance at a pace dictated by customers in the marketplace. We have a cost-effective approach to using DOCSIS 3.1, which we’ve already deployed, to expand our network capacity 1.2 gigahertz, which gives us the ability to offer multi-gigabit speeds in the downstream and at least 1 gigabit per second in the upstream.”

According to Leichtman Research Group, the top cable companies had 68 million broadband subscribers, and top wireline telecom companies had 33.2 million subscribers at the end of 2019.

“Based on the currently available information, cable stole wired broadband market share in Verizon and AT&T markets as well. Oy vey!” said Jim Patterson of Patterson Advisory Group in his May 2, 2021 newsletter. “Think about Comcast and AT&T as having roughly the same number of homes passed (AT&T probably closer to 57 million homes versus the nearly 60 million shown for Comcast),” he added. Patterson noted that top cable companies Comcast, Charter and Altice managed to capture 86% of broadband customer growth in the U.S. in the first quarter of this year.

“(AT&T) fiber connections simply aren’t growing fast enough to keep up,” wrote colleague Craig Moffett of MoffettNathanson in a recent note to clients. Here’s more:

To be sure, there are questions about the extent to which these deployments will overlap cable (or will instead be focused on unserved rural communities), and the extent to which labor and supply chain contraints might limit acheivability of announced targets. Still, taken together, these deployments suggest that, after a precipitous decline in new fiber construction in 2020, planned fiber deployments do, indeed, rise over the next two years; we expect that both 2021 and 2022 will represent new all-time peaks in total number of fiber homes passed. Typically, the competitive impact from overbuilds is felt with some lag, suggesting the impact on cable operators will peak in 2024/2025.

At the same time, we expect that federal stimulus to accelerate broadband market growth in 2021 and 2022, perhaps significantly, with new household formation, in particular, driving upside to 2021 and 2022 forecasts.

Longer term, however, Cable operators will have to contend with more fiber overbuilds, as TelCos increasingly see both more favorable economics for fiber deployment and increasingly acknowledge that their copper plant faces imminent obsolescence without it. The forecasts for fiber deployment in this note suggest that 2021 will be a record for fiber construction – assuming labor and materials capacity can accommodate the TelCos’ own forecasts – and 2022 will step up higher still. After that, deployments are expected to abate, at least to a degree.

“Cable can upgrade its plant quickly and at low cost to offer at least 4.6Gbit/s down and 1.5Gbit/s up, well beyond current fiber offerings. They can do this before the move to DOCSIS 4.0, which is still years off,” wrote the financial analysts at New Street Research in a recent note to investors. The result, according to the New Street analysts, is that fiber providers like AT&T won’t necessarily be able to dominate the fiber market with a 1 Gbit/s FTTH/FTTP connection and take market share from cable incumbents.

“Cable will face new fiber competition in more of its markets over the next few years; however, there is little to no prospect of fiber delivering a service in those markets that cable can’t easily match or beat,” New Street concluded.

…………………………………………………………………………………………………………………………………………………………….

“Looking back and being a little critical, we probably allowed the cable companies to execute and to take share in that market in a significant way,” AT&T CFO Pascal Desroches said at a recent Credit Suisse investor event.

AT&T executives have said that the company’s fiber investment ultimately will generate internal returns of around 15%. Desroches said that return on investment will be due to a variety of factors. Fiber “supports not only consumer needs, it supports needs for our enterprise businesses as well as needs for potentially our reseller business. So being able to look across and integrate the planning for fiber deployment such that it not only serves consumer needs, but it serves these other market adjacencies as well is something that we haven’t been very good at historically, That’s why we’re really bullish and we believe we’re going to be able to execute really well here,” AT&T’s CFO concluded.

References:

https://www.lightreading.com/opticalip/is-atandts-fiber-investment-good-idea/d/d-id/770468?

https://www.linkedin.com/feed/update/urn:li:activity:6813211481950318592/

MTN Consulting: Network operator capex forecast at $520B in 2025

Executive Summary:

Telco, webscale and carrier-neutral capex will total $520 billion by 2025 according to a report from MTN Consulting.. That’s compared with $420 billion in 2019.

- Telecom operators (telco) will account for 53% of industry Capex by 2025 vs 9% in 2019;

- Webscale operators will grow from 25% to 39%;

- Carrier-neutral [1.] providers will add 8% of total Capex in 2025 from 6% in 2019.

Note 1. A Carrier-neutral data center is a data center (or carrier hotel) which allows interconnection between multiple telecommunication carriers and/or colocation providers. It is not owned and operated by a single ISP, but instead offers a wide variety of connection options to its colocation customers.

Adequate power density, efficient use of server space, physical and digital security, and cooling system are some of the key attributes organizations look for in a colocation center. Some facilities distinguish themselves from others by offering additional benefits like smart monitoring, scalability, and additional on-site security.

……………………………………………………………………………………………………………………………………………………….

The number of telco employees will decrease from 5.1 million in 2019 to 4.5 million in 2025 as telcos deploy automation more widely and spin off parts of their network to the carrier-neutral sector.

By 2025, the webscale sector will dominate with revenues of approximately $2.51 trillion, followed by $1.88 trillion for the telco sector and $108 billion for carrier-neutral operators (CNNOs).

KEY FINDINGS from the report:

Revenue growth for telco, webscale and carrier-neutral sector will average 1, 10, and 7% through 2025

Telecom network operator (TNO, or telco) revenues are on track for a significant decline in 2020, with the industry hit by COVID-19 even as webscale operators (WNOs) experienced yet another growth surge as much of the world was forced to work and study from home. For 2020, telco, webscale, and carrier-neutral revenues are likely to reach $1.75 trillion (T), $1.63T, and $71 billion (B), amounting to YoY growth of -3.7%, +12.2%, and 5.0%, respectively. Telcos will recover and webscale will slow down, but this range of growth rates will persist for several years. By 2025, the webscale sector will dominate with revenues of approximately $2.51 trillion, followed by $1.88 trillion for the telco sector and $108 billion for carrier-neutral operators (CNNOs).

Network operator capex will grow to $520B by 2025

In 2019, telco, webscale and carrier-neutral capex totaled $420 billion, a total which is set to grow to $520 billion by 2025. The composition will change starkly though: telcos will account for 53% of industry capex by 2025, from 9% in 2019; webscale operators will grow from 25% to 39% in the same timeframe; and, carrier-neutral providers will add 8% of total capex in 2025 from their 2019 level of 6%.

By 2025, the webscale sector will employ more than the telecom industry

As telcos deploy automation more widely and cast off parts of their network to the carrier-neutral sector, their employee base should decline from 5.1 million in 2019 to 4.5 million in 2025. The cost of the average telco employee will rise significantly in the same timeframe, as they will require many of the same software and IT skills currently prevalent in the webscale workforce. For their part, webscale operators have already grown from 1.3 million staff in 2011 to 2.8 million in 2019, but continued rapid growth in the sector (especially its ecommerce arms) will spur further growth in employment to reach roughly 4.8 million by 2025. The carrier-neutral sector’s headcount will grow far more modestly, rising from 90 million in 2019 to about 119 million in 2025. Managing physical assets like towers tends to involve a far lighter human touch than managing network equipment and software.

Example of a Carrier Neutral Colo Data Center

RECOMMENDATIONS:

Telcos: embrace collaboration with the webscale sector

Telcos remain constrained at the top line and will remain in the “running to stand still” mode that has characterized their last decade. They will continue to shift towards more software-centric operations and automation of networks and customer touch points. What will become far more important is for telcos to actively collaborate with webscale operators and the carrier-neutral sector in order to operate profitable businesses. The webscale sector is now targeting the telecom sector actively as a vertical market. Successful telcos will embrace the new webscale offerings to lower their network costs, digitally transform their internal operations, and develop new services more rapidly. Using the carrier-neutral sector to minimize the money and time spent on building and operating physical assets not viewed as strategic will be another key to success through 2025.

Vendors: to survive you must improve your partnership and integration capabilities

Collaboration across the telco/webscale/carrier-neutral segments has implications for how vendors serve their customers. Some of the biggest telcos will source much of their physical infrastructure from carrier-neutral providers and lean heavily on webscale partners to manage their clouds and support new enterprise and 5G services. Yet telcos spend next to nothing on R&D, especially when compared to the 10% or more of revenues spent on R&D by their vendors and the webscale sector. Vendors who develop customized offerings for telcos in partnership with either their internal cloud divisions (e.g. Oracle, HPE, IBM) or AWS/GCP/Azure/Alibaba will have a leg up. This is not just good for growing telco business, but also for helping webscale operators pursue 5G-based opportunities. One of the earliest examples of a traditional telco vendor aligning with a cloud player for the telco market is NEC’s 2019 development of a mobile core solution for the cloud that can be operated on the AWS network; there will be many more such partnerships going forward.

All sectors: M&A is often not the answer, despite what the bankers urge

M&A will be an important part of the network infrastructure sector’s evolution over the next 5 years. However, the difficulty of successfully executing and integrating a large transaction is almost always underappreciated. There is incredible pressure from bankers to choose M&A, and the best ones are persuasive in arguing that M&A is the best way to improve your competitiveness, enter a new market, or lower your cost base. Many chief executives love to make the big announcements and take credit for bringing the parties together. But making the deal actually work in practice falls to staff way down the chain of command, and to customers’ willingness to cope with the inevitable hiccups and delays brought about by the transaction. And the bankers are long gone by then, busy spending their bonuses and working on their next deal pitch. Be extremely skeptical about M&A. Few big tech companies have a history of doing it well.

Webscale: stop abusing privacy rights and trampling on rules and norms of fair competition

The big tech companies that make up the webscale sector tracked by MTN Consulting have been rightly abused in the press recently for their disregard for consumer privacy rights, and overly aggressive, anti-competitive practices. After years of avoiding increased regulatory oversight through aggressive lobbying and careful brand management, the chickens are coming home to roost in 2021. Public concerns about abuses of privacy, facilitation of fake news, and monopolistic or (at the least) oligopolistic behavior will make it nearly impossible for these companies to stem the increased oversight likely to come soon from policymakers.

Australia’s pending law, the “News Media and Digital Platforms Bargaining Code,” could foreshadow things to come for the webscale sector, as do recent antitrust lawsuits against Facebook and Alphabet. Given that webscale companies are supposed to be fast moving and innovative, they should get out ahead of these problems. They need to implement wholesale, transparent changes to how they treat consumer privacy and commit to (and actually follow) a code of conduct that is conducive to innovation and competition. The billionaires leading the companies may even consider encouraging fairer tax codes so that some of their excessive wealth can be spread across the countries that actually fostered their growth.

ABOUT THIS REPORT:

This report presents MTN Consulting’s first annual forecast of network operator capex. The scope includes telecommunications, webscale and carrier-neutral network operators. The forecast presents revenue, capex and employee figures for each market, both historical and projected, and discusses the likely evolution of the three sectors through 2025. In the discussion of the individual sectors, some additional data series are projected and analyzed; for example, network operations opex in the telco sector. The forecast report presents a baseline, most likely case of industry growth, taking into account the significant upheaval in communication markets experienced during 2020. Based on our analysis, we project that total network operator capex will grow from $420 billion in 2020 to $520 billion in 2025, driven by substantial gains in the webscale and (much less so) carrier-neutral segments. The primary audience for the report is technology vendors, with telcos and webscale/cloud operators a secondary audience.

References:

………………………………………………………………………………………………………………………………………………….

January 8, 2021 Update:

Analysys Mason: Cloud technology will pervade the 5G mobile network, from the core to the RAN and edge

“Communications Service Providers (CSPs) spending on multi-cloud network infrastructure software, hardware and professional services will grow from USD4.3 billion in 2019 to USD32 billion by 2025, at a CAGR of 40%.”

5G and edge computing are spurring CSPs to build multi-cloud, cloud-native mobile network infrastructure

Many CSPs acknowledge the need to use cloud-native technology to transform their networks into multi-cloud platforms in order to maximise the benefits of rolling out 5G. Traditional network function virtualisation (NFV) has only partly enabled the software-isation and disaggregation of the network, and as such, limited progress has been made on cloudifying the network to date. Indeed, Analysys Mason estimates that network virtualisation reached only 6% of its total addressable market for mobile networks in 2019.

The telecoms industry is now entering a new phase of network cloudification because 5G calls for ‘true’ clouds that are defined by cloud-native technologies. This will require radical changes to the way in which networks are designed, deployed and operated, and we expect that investments will shift to support this new paradigm. The digital infrastructure used for 5G will be increasingly built as horizontal, open network platforms comprising multiple cloud domains such as mobile core cloud, vRAN cloud and network and enterprise edge clouds. As a result, we have split the spending on network cloud into spending on multiple cloud domains (Figure 1) for the first time in our new network cloud infrastructure report. We forecast that CSP spending on multi-cloud network infrastructure software, hardware and professional services will grow from USD4.3 billion in 2019 to USD32 billion by 2025, at a CAGR of 40%.

https://www.analysysmason.com/research/content/comments/network-cloud-forecast-comment-rma16/

Synergy Research: Hyperscale Operator Capex at New Record in Q3-2020

Hyperscale cloud operator capex topped $37 billion in Q3-2020, which easily set a new quarterly record for spending, according to Synergy Research Group (SRG). Total spending for the first three quarters of 2020 reached $99 billion, which was a 16% increase over the same period last year.

The top-four hyperscale spenders in the first three quarters of this year were Amazon, Google, Microsoft and Facebook. Those four easily exceeded the spending by the rest of the hyperscale operators. The next biggest cloud spenders were Apple, Alibaba, Tencent, IBM, JD.com, Baidu, Oracle, and NTT.

SRG’s data found that capex growth was particularly strong across Amazon, Microsoft, Tencent and Alibaba while Apple’s spend dropped off sharply and Google’s also declined.

Much of the hyperscale capex goes towards building, expanding and equipping huge data centers, which grew in number to 573 at the end of Q3. The hyperscale data is based on analysis of the capex and data center footprint of 20 of the world’s major cloud and internet service firms, including the largest operators in IaaS, PaaS, SaaS, search, social networking and e-commerce. In aggregate these twenty companies generated revenues of over $1.1 trillion in the first three quarters of the year, up 15% from 2019.

“As expected the hyperscale operators are having little difficulty weathering the pandemic storm. Their revenues and capex have both grown by strong double-digit amounts this year and this has flowed down to strong growth in spending on data centers, up 18% from 2019,” said John Dinsdale, a Chief Analyst at Synergy Research Group. “They generate well over 80% of their revenues from cloud, digital services and online activities, all of which have seen COVID-19 related boosts. As these companies go from strength to strength they need an ever-larger footprint of data centers to support their rapidly expanding digital activities. This is good news for companies in the data center ecosystem who can ride along in the slipstream of the hyperscale operators.”

Separately, Google Cloud announced it is set to add three new ‘regions,’ which provide faster and more reliable services in targeted locations, to its global footprint. The new regions in Chile, Germany and Saudi Arabia will take the total to 27 for Google Cloud.

About Synergy Research Group:

Synergy provides quarterly market tracking and segmentation data on IT and Cloud related markets, including vendor revenues by segment and by region. Market shares and forecasts are provided via Synergy’s uniquely designed online database tool, which enables easy access to complex data sets. Synergy’s CustomView ™ takes this research capability one step further, enabling our clients to receive on-going quantitative market research that matches their internal, executive view of the market segments they compete in.

Synergy Research Group helps marketing and strategic decision makers around the world via its syndicated market research programs and custom consulting projects. For nearly two decades, Synergy has been a trusted source for quantitative research and market intelligence. Synergy is a strategic partner of TeleGeography.

To speak to an analyst or to find out how to receive a copy of a Synergy report, please contact [email protected] or 775-852-3330 extension 101.

References:

AT&T Earnings Down; Cost Cutting & Lower CAPEX for Remainder of 2020, 5G Uncertainty?

As expected, AT&T reported first quarter (Q1) 2020 revenues down 4.6 percent to $42.8 billion. The mega telco/media company continued to lose pay-TV subscribers while its WarnerMedia division suffered from the Covid-19 outbreak’s impact on the film and TV industry.

AT&T estimates the coronavirus pandemic reduced EPS 5 cents in the first quarter, which otherwise would have been in line with analyst expectations. Adjusted EPS fell to $0.84 from $0.86 a year ago, but would have increased to $0.89 without the extraordinary virus effect. The adjusted operating profit margin reached 21.2 percent in Q1, down slightly from 21.4 percent a year ago.

- Telecom business revenues were down 2.6 percent to $34.2 billion, while adjusted EBITDA rose 2.1 percent to $12.8 billion.

- AT&T Wireless grew service revenues 2.5 percent.

- Revenues continued lower at the Entertainment group as AT&T lost another 1.035 million pay-TV subscribers in the quarter.

- Mobile subscriber growth slowed to 27,000 postpaid net adds (+163,000 with phones), and the broadband base fell by another 73,000 customers in the three months.

Highlights from today’s AT&T earnings call transcript:

In Mobility, service revenue grew by 2.5% in the quarter. EBITDA of $7.8 billion grew by more than $500 million or 7%, and EBITDA margins expanded by 280 basis points. COVID did impact our top line revenue numbers in the quarter by about $200 million due to lower equipment and roaming revenues. Our subscriber counts for wireless, video and broadband this quarter exclude customers who we agreed not to terminate service for non-payment. For reporting purposes, we are treating those subscribers has disconnects. Even with that, our industry-leading network and FirstNet drove postpaid phone net adds of 163,000. Postpaid phone churn was down 6 basis points to 0.86% and our 5G deployment continues. We now cover more than 120 million people in 190 markets, and we expect we’ll be nationwide this summer.

In our Entertainment Group, cash generation remains a focus. We added 209,000 AT&T Fiber subscribers and now serve more than 4 million. We continue to drive ARPU growth in both video and IP broadband. In fact, premium video ARPU was up about 10% as we continue to focus on long-term value customers. We launched AT&T TV nationally late in the quarter and subscriber growth was in line with our expectations even with COVID impacts. Premium video net losses again improved sequentially.

Business Wireline performance was solid, with EBITDA and EBITDA margins remaining stable. Revenues were consistent with recent trends as declines in legacy products were partially offset by growth in strategic and managed services. Business Wireline continued to be an effective channel for our Mobility sales. Including wireless, total business revenues grew 1.7%.

………………………………………………………………………………………………………..

The negative coronavirus financial impact was palpable at WarnerMedia, which lost around $1 billion in revenue year-on-year and over $500 million in adjusted EBITDA. The unit suffered from the suspension of key events such as the NCAA basketball tournament and new cinema releases, a slowdown in advertising due to the reduced economic activity and a halt to most production activities.

Operating cash flow totaled $8.9 billion in the quarter, and capital expenditure (CAPEX) reached $5.8 billion, leaving free cash flow of USD 3.9 billion. Net debt was at about 2.6x EBITDA at the end of the quarter.

AT&T said its liquidity position and balance sheet remained strong and it had already adjusted capital spending plans and suspended its share buybacks. It will continue investing in critical growth areas like 5G, fiber broadband and HBO Max, while maintaining its dividend commitment and paying down debt,

AT&T President & COO John Stankey said during AT&T’s earnings call:

Our 5G deployment continues, although we continue to navigate workforce and permitting delays. We expect nationwide coverage this summer. We also continue to be opportunistic with our fiber build beyond the 14 million household locations we reach today.

Stankey said the operator would encourage customers to install their own equipment and would shift customers to its fiber network. He also said the operator would use artificial intelligence (AI) and other capabilities to reduce initial “truck rolls” (technician visits to customer locations) and to eliminate the need for a second visit.

“These efficiencies will enhance our ability to continue to invest in our key growth initiatives,” including HBO Max and 5G, Stankey said of AT&T’s cost-cutting program.

Regarding CAPEX, before the coronavirus pandemic, AT&T said it would spend around $20 billion on CAPEX throughout 2020, which is significantly lower than the $23 billion it spent in 2019 and the $22 billion that most Wall Street analysts had expected AT&T to spend in 2020. AT&T CEO Randall Stephenson gave mixed messages on CAPEX plans for the remainder of the year on today’s earnings call:

“It’s not just writing checks for CAPEX. There’s people out doing things,” he said, explaining that some technicians may not be able to visit cell sites due to the spread of COVID-19, while some local officials may not be able to issue cell site construction permits.

“While we have no intention of slowing down on 5G and fiber deployment, the reality is that a lot of it is not in our control,” Stephenson said. “So there’s probably going to be – relative to the targets we gave you in CAPEX – some downward proclivity on that number, just because of the logistical issues we’re running into.”

AT&T declined to provide any financial guidance for the remainder of 2020 due to the pandemic. The operator/media giant spent roughly $5 billion on CAPEX during its most recent quarter, slightly above some Wall Street estimates.

AT&T’s management said the company had begun a cost-cutting program that the operator hopes will trim $6 billion from its budget by 2023. The huge cost cutting effort may include layoffs. Stankey didn’t specifically mention that word, but instead said the operator would enact a “headcount rationalization,” a term that could include layoffs as well as reductions by not hiring replacements for workers who retire or leave. That program, he said, would reduce the operator’s labor expenses by 4%, or roughly $1.5 billion, by the end of 2020. He added that the reduction would target employees in AT&T’s call centers, management structures and distribution strategy. AT&T employed roughly 252,000 people at the end of September.

CEO Stephenson made the following illuminating comments during the call:

In Mobility, the most immediate impacts are the reduction of roaming revenues as well as a reduction in late fees. The waiving of late fees is a commitment to our customers during these difficult economic times and roaming should gradually increase as people start to travel more. The first quarter impact of these items was approximately $50 million, with virtually all of it in the second half of March. We’re augmenting our digital sales team to mitigate the impact of store closures on equipment and service revenues, but we’re still forecasting lower wireless gross adds and upgrades. In fact, equipment revenues were down nearly 25% year-over-year in March. As a result of COVID, we anticipate an increase in bad debt expense across the various businesses, and accordingly, have recorded a $250 million incremental reserve in anticipation of that.

In our Entertainment Group, we anticipate increases in premium TV subscriber cord-cutting as well as lower revenues from commercial locations such as hotels, bars, and restaurants. Labor unit costs will increase temporarily from the 20% boost in pay we’re providing our frontline employees.

At WarnerMedia, content production has been placed on hiatus. Theatrical releases have been postponed and we’re seeing lower advertising revenues and lower costs from sports rights. This crisis has shown the value of premium streaming entertainment and we anticipate strong demand for HBO Max when it launches next month.

Fiber and broadband are more important than ever and we saw a pickup in demand for both in the quarter. We’re also seeing higher demand for VPN bandwidth and security. We do expect a negative impact on small business, which makes up about 15% of our total business wireline revenues. A detailed schedule of the COVID impacts is included in our investor briefing.

………………………………………………………………………………………………………………………………………………………………..

Lightreading’s Mike Dano made the following comments on AT&T’s 5G deployments and CAPEX in a blog post:

One Wall Street analyst wondered if AT&T is moving its 5G goal posts slightly for 2020. Jennifer Fritzsche at Wells Fargo pointed out that AT&T executives now promise nationwide low band 5G by “summer” 2020. In contrast, during previous calls they had said the operator would reach that target by the “middle” of 2020.

AT&T’s low band 5G offering works on its 850MHz spectrum and doesn’t provide speeds that are much faster than its 4G LTE network. The operator also operates faster 5G services in millimeter wave (mmWave) spectrum in parts of roughly 30 cities, but AT&T executives have remained conspicuously silent on that effort.

Verizon, in contrast, has promised to expand its own mmWave 5G network to an additional 30 cities this year.

AT&T’s 2020 CAPEX warning, on its network in general and on 5G specifically, has been echoed by some other players in the industry.

“COVID-19 and actions taken by governments to slow down the spread are making our service delivery and supply harder due to lockdowns and travel restrictions in many countries,” Ericsson CEO Börje Ekholm said earlier on Wednesday. Ericsson sells 4G and 5G equipment to a wide range of global operators, including AT&T. “In addition, while we have seen no material effects on our demand situation, it is prudent to believe that the slowdown in the general economy may lead some operators to delay investment programs.”

Ekholm said some operators are accelerating their investments in 5G and 4G capacity, pointing to providers in China specifically. Those comments dovetail with concerns of a 5G slowdown in Europe, largely due to decisions by some officials there to delay 5G spectrum auctions.

“We’re having to understand better what will happen as we exit the COVID pandemic in terms of [5G] investment,” noted EXFO CEO Philippe Morin in response to a question about how the pandemic might affect US operators’ 5G spending, according to a transcript of his remarks. He made his comments during his company’s recent quarterly conference call with investors. EXFO sells network testing equipment, including for 5G, to mobile network operators globally.

“In certain other countries in Europe, we’ve seen actually some of the [5G] spectrum auctions to be delayed as the countries have to deal with the virus,” Morin continued. “So, we’re going to – this is part of the discussions we’re having and dialogs we are having with our customers to better understand how – once we emerge out of the crisis, how the investments and where are the priorities are going to be.”

Stephenson acknowledged that it’s “pretty difficult” to predict what’s going to happen next as Americans and the rest of the world fight COVID-19. He said the world’s smartest economists disagree about what’s going to happen in the next quarter, much less the rest of the year.

AT&T’s CFO John Stephens said that mobile service remains an essential expense to most people. “The last thing that people don’t want to pay is probably their cellphone bill,” he said.

Indeed, in its most recent quarter – which suffered from the initial effects of widespread stay-at-home orders – AT&T reported postpaid phone net customer additions of 163,000, ahead of most Wall Street expectations. AT&T executives said the operator’s mobility business would help bolster its troubled media operation.

“The bottom line here is that Mobility performed its role admirably in Q1,” wrote the analysts at Wall Street research firm MoffettNathanson of AT&T’s financial performance, in a note to investors Wednesday.

However, AT&T executives warned that if an economic recession deepens wireless users may look to reduce their spending by paying less for their service or holding onto an existing phone longer rather than upgrading to a new phone.

References:

https://www.lightreading.com/services/atandt-starts-$6b-cost-cutting-program/d/d-id/759075?

…………………………………………………………………………………………………………………………………….

UPDATE:

April 24 (Reuters) – AT&T Inc said Friday that Chief Operating Officer John Stankey will take over as chief executive officer, effective July 1. The announcement was made during AT&T’s annual meeting.

AT&T Earnings Down; Cost Cutting & Lower CAPEX for Remainder of 2020, 5G Uncertainty?

As expected, AT&T reported first quarter (Q1) 2020 revenues down 4.6 percent to $42.8 billion. The mega telco/media company continued to lose pay-TV subscribers while its WarnerMedia division suffered from the Covid-19 outbreak’s impact on the film and TV industry.

AT&T estimates the coronavirus pandemic reduced EPS 5 cents in the first quarter, which otherwise would have been in line with analyst expectations. Adjusted EPS fell to $0.84 from $0.86 a year ago, but would have increased to $0.89 without the extraordinary virus effect. The adjusted operating profit margin reached 21.2 percent in Q1, down slightly from 21.4 percent a year ago.

- Telecom business revenues were down 2.6 percent to $34.2 billion, while adjusted EBITDA rose 2.1 percent to $12.8 billion.

- AT&T Wireless grew service revenues 2.5 percent.

- Revenues continued lower at the Entertainment group as AT&T lost another 1.035 million pay-TV subscribers in the quarter.

- Mobile subscriber growth slowed to 27,000 postpaid net adds (+163,000 with phones), and the broadband base fell by another 73,000 customers in the three months.

Highlights from today’s AT&T earnings call transcript:

In Mobility, service revenue grew by 2.5% in the quarter. EBITDA of $7.8 billion grew by more than $500 million or 7%, and EBITDA margins expanded by 280 basis points. COVID did impact our top line revenue numbers in the quarter by about $200 million due to lower equipment and roaming revenues. Our subscriber counts for wireless, video and broadband this quarter exclude customers who we agreed not to terminate service for non-payment. For reporting purposes, we are treating those subscribers has disconnects. Even with that, our industry-leading network and FirstNet drove postpaid phone net adds of 163,000. Postpaid phone churn was down 6 basis points to 0.86% and our 5G deployment continues. We now cover more than 120 million people in 190 markets, and we expect we’ll be nationwide this summer.

In our Entertainment Group, cash generation remains a focus. We added 209,000 AT&T Fiber subscribers and now serve more than 4 million. We continue to drive ARPU growth in both video and IP broadband. In fact, premium video ARPU was up about 10% as we continue to focus on long-term value customers. We launched AT&T TV nationally late in the quarter and subscriber growth was in line with our expectations even with COVID impacts. Premium video net losses again improved sequentially.

Business Wireline performance was solid, with EBITDA and EBITDA margins remaining stable. Revenues were consistent with recent trends as declines in legacy products were partially offset by growth in strategic and managed services. Business Wireline continued to be an effective channel for our Mobility sales. Including wireless, total business revenues grew 1.7%.

………………………………………………………………………………………………………..

The negative coronavirus financial impact was palpable at WarnerMedia, which lost around $1 billion in revenue year-on-year and over $500 million in adjusted EBITDA. The unit suffered from the suspension of key events such as the NCAA basketball tournament and new cinema releases, a slowdown in advertising due to the reduced economic activity and a halt to most production activities.

Operating cash flow totaled $8.9 billion in the quarter, and capital expenditure (CAPEX) reached $5.8 billion, leaving free cash flow of USD 3.9 billion. Net debt was at about 2.6x EBITDA at the end of the quarter.

AT&T said its liquidity position and balance sheet remained strong and it had already adjusted capital spending plans and suspended its share buybacks. It will continue investing in critical growth areas like 5G, fiber broadband and HBO Max, while maintaining its dividend commitment and paying down debt,

AT&T President & COO John Stankey said during AT&T’s earnings call:

Our 5G deployment continues, although we continue to navigate workforce and permitting delays. We expect nationwide coverage this summer. We also continue to be opportunistic with our fiber build beyond the 14 million household locations we reach today.

Stankey said the operator would encourage customers to install their own equipment and would shift customers to its fiber network. He also said the operator would use artificial intelligence (AI) and other capabilities to reduce initial “truck rolls” (technician visits to customer locations) and to eliminate the need for a second visit.

“These efficiencies will enhance our ability to continue to invest in our key growth initiatives,” including HBO Max and 5G, Stankey said of AT&T’s cost-cutting program.

Regarding CAPEX, before the coronavirus pandemic, AT&T said it would spend around $20 billion on CAPEX throughout 2020, which is significantly lower than the $23 billion it spent in 2019 and the $22 billion that most Wall Street analysts had expected AT&T to spend in 2020. AT&T CEO Randall Stephenson gave mixed messages on CAPEX plans for the remainder of the year on today’s earnings call:

“It’s not just writing checks for CAPEX. There’s people out doing things,” he said, explaining that some technicians may not be able to visit cell sites due to the spread of COVID-19, while some local officials may not be able to issue cell site construction permits.

“While we have no intention of slowing down on 5G and fiber deployment, the reality is that a lot of it is not in our control,” Stephenson said. “So there’s probably going to be – relative to the targets we gave you in CAPEX – some downward proclivity on that number, just because of the logistical issues we’re running into.”

AT&T declined to provide any financial guidance for the remainder of 2020 due to the pandemic. The operator/media giant spent roughly $5 billion on CAPEX during its most recent quarter, slightly above some Wall Street estimates.

AT&T’s management said the company had begun a cost-cutting program that the operator hopes will trim $6 billion from its budget by 2023. The huge cost cutting effort may include layoffs. Stankey didn’t specifically mention that word, but instead said the operator would enact a “headcount rationalization,” a term that could include layoffs as well as reductions by not hiring replacements for workers who retire or leave. That program, he said, would reduce the operator’s labor expenses by 4%, or roughly $1.5 billion, by the end of 2020. He added that the reduction would target employees in AT&T’s call centers, management structures and distribution strategy. AT&T employed roughly 252,000 people at the end of September.

CEO Stephenson made the following illuminating comments during the call:

In Mobility, the most immediate impacts are the reduction of roaming revenues as well as a reduction in late fees. The waiving of late fees is a commitment to our customers during these difficult economic times and roaming should gradually increase as people start to travel more. The first quarter impact of these items was approximately $50 million, with virtually all of it in the second half of March. We’re augmenting our digital sales team to mitigate the impact of store closures on equipment and service revenues, but we’re still forecasting lower wireless gross adds and upgrades. In fact, equipment revenues were down nearly 25% year-over-year in March. As a result of COVID, we anticipate an increase in bad debt expense across the various businesses, and accordingly, have recorded a $250 million incremental reserve in anticipation of that.

In our Entertainment Group, we anticipate increases in premium TV subscriber cord-cutting as well as lower revenues from commercial locations such as hotels, bars, and restaurants. Labor unit costs will increase temporarily from the 20% boost in pay we’re providing our frontline employees.

At WarnerMedia, content production has been placed on hiatus. Theatrical releases have been postponed and we’re seeing lower advertising revenues and lower costs from sports rights. This crisis has shown the value of premium streaming entertainment and we anticipate strong demand for HBO Max when it launches next month.

Fiber and broadband are more important than ever and we saw a pickup in demand for both in the quarter. We’re also seeing higher demand for VPN bandwidth and security. We do expect a negative impact on small business, which makes up about 15% of our total business wireline revenues. A detailed schedule of the COVID impacts is included in our investor briefing.

………………………………………………………………………………………………………………………………………………………………..

Lightreading’s Mike Dano made the following comments on AT&T’s 5G deployments and CAPEX in a blog post:

One Wall Street analyst wondered if AT&T is moving its 5G goal posts slightly for 2020. Jennifer Fritzsche at Wells Fargo pointed out that AT&T executives now promise nationwide low band 5G by “summer” 2020. In contrast, during previous calls they had said the operator would reach that target by the “middle” of 2020.

AT&T’s low band 5G offering works on its 850MHz spectrum and doesn’t provide speeds that are much faster than its 4G LTE network. The operator also operates faster 5G services in millimeter wave (mmWave) spectrum in parts of roughly 30 cities, but AT&T executives have remained conspicuously silent on that effort.

Verizon, in contrast, has promised to expand its own mmWave 5G network to an additional 30 cities this year.

AT&T’s 2020 CAPEX warning, on its network in general and on 5G specifically, has been echoed by some other players in the industry.

“COVID-19 and actions taken by governments to slow down the spread are making our service delivery and supply harder due to lockdowns and travel restrictions in many countries,” Ericsson CEO Börje Ekholm said earlier on Wednesday. Ericsson sells 4G and 5G equipment to a wide range of global operators, including AT&T. “In addition, while we have seen no material effects on our demand situation, it is prudent to believe that the slowdown in the general economy may lead some operators to delay investment programs.”

Ekholm said some operators are accelerating their investments in 5G and 4G capacity, pointing to providers in China specifically. Those comments dovetail with concerns of a 5G slowdown in Europe, largely due to decisions by some officials there to delay 5G spectrum auctions.

“We’re having to understand better what will happen as we exit the COVID pandemic in terms of [5G] investment,” noted EXFO CEO Philippe Morin in response to a question about how the pandemic might affect US operators’ 5G spending, according to a transcript of his remarks. He made his comments during his company’s recent quarterly conference call with investors. EXFO sells network testing equipment, including for 5G, to mobile network operators globally.

“In certain other countries in Europe, we’ve seen actually some of the [5G] spectrum auctions to be delayed as the countries have to deal with the virus,” Morin continued. “So, we’re going to – this is part of the discussions we’re having and dialogs we are having with our customers to better understand how – once we emerge out of the crisis, how the investments and where are the priorities are going to be.”

Stephenson acknowledged that it’s “pretty difficult” to predict what’s going to happen next as Americans and the rest of the world fight COVID-19. He said the world’s smartest economists disagree about what’s going to happen in the next quarter, much less the rest of the year.

AT&T’s CFO John Stephens said that mobile service remains an essential expense to most people. “The last thing that people don’t want to pay is probably their cellphone bill,” he said.

Indeed, in its most recent quarter – which suffered from the initial effects of widespread stay-at-home orders – AT&T reported postpaid phone net customer additions of 163,000, ahead of most Wall Street expectations. AT&T executives said the operator’s mobility business would help bolster its troubled media operation.