Author: Alan Weissberger

Huawei: XR industry to realize exponential growth with 5G; ‘Spatial Internet’ will be the next big thing

The world of Extended Reality or XR, which covers Virtual Reality, Augmented Reality and Mixed Reality, offers infinite potential, said Dr. Philip Song, Chief Marketing Officer, Huawei Carrier, during his keynote speech “5G + XR: Bringing Imagination into Reality,” at the 2022 Mobile World Congress (MWC) in Barcelona.

According to a survey, the XR industry will contribute US$1.5 trillion to the global GDP by 2030. In 2021, more than 10 million units of Quest 2 were shipped. These 10 million users will be the critical mass for the XR ecosystem to take off. Dr. Song added that following the mobile internet, ‘Spatial Internet’ [1.] will be the next big thing.

Note 1. While there’s no clear definition, the Spatial Web or Spatial Internet refers to a computing atmosphere that exists in a 3D space. It is a pairing of real and virtual realities, enabled via billions of connected devices, and accessed through the interface of Virtual and Augmented Reality.

…………………………………………………………………………………………………………………………………………………………………………………………………………..

Song introduced how Huawei held VR-enabled annual meetings and uses AR to assist with 5G base station delivery. Huawei and third-party data shows that the XR market will generate US$1.5 trillion in GDP by 2030, which is roughly equivalent to the current 5G market.

Comparing the XR industry’s progress to how the smartphone industry developed, Song said many vendors are now offering XR devices for under US$300, making the technology more affordable while still offering next-gen user experiences. XR development tools are being increasingly adopted. The new OPEN XR standard is now supported by almost every major hardware, platform, and engine company, making multi-platform deployment possible without multiple rounds of development.

What is more noteworthy is that a number of global XR pioneer carriers have made commercial breakthroughs in recent years. Carriers in countries like South Korea, Thailand, and China have led the deployment of VR/AR services and gained significant returns through three steps: selecting industries, setting business models, and developing capabilities. A carrier said, “If XR was launched three months later, it might take three years to catch up.”

XR Industry to Grow Rapidly:

The world is on the cusp of witnessing the fast-paced growth of the XR industry, he said. VR headset shipments are accelerating. In 2021, more than 10 million units of Oculus Quest 2, a VR headset, were shipped. Ten million users will be the critical mass for the XR ecosystem to take off. The growth of VR devices will mirror that of smartphones and mobile devices. From 1983 to 1994, it took 11 years to sell the first 10 million cellphones. However, the cellphone shipment touched 20 million in 1995, and 100 million were sold over the next three years. According to market forecast, VR headset shipment will reach 100 million units by 2025.

Also, the price of VR devices continues to drop, making them affordable for more people. Lastly, continuous innovation in XR technologies has made it possible to deliver a generational leap in user experience.

Huawei launched its next-generation, innovative AR-HUD, expanding XR applications. In terms of XR data transmission, Huawei presented innovative solutions such as 5G Massive MIMO and FTTR. The company has publicly committed to supporting a “Gigaverse” that provides ubiquitous gigabit access to support XR experiences anytime, anywhere. Huawei also launched its “Cloud-network Express” solution to help XR industry partners quickly access multiple clouds and use cloud-based development and rendering capabilities.

As he closed out his presentation, Song called on industry partners to work together in line with the “new Moore’s Law” and seize this great development opportunity for the XR industry. “I do believe that with industry-wide collaboration, 5G+XR will have a bright future. The best way to predict the future is to create it. The time to act is now,” concluded Dr. Song.

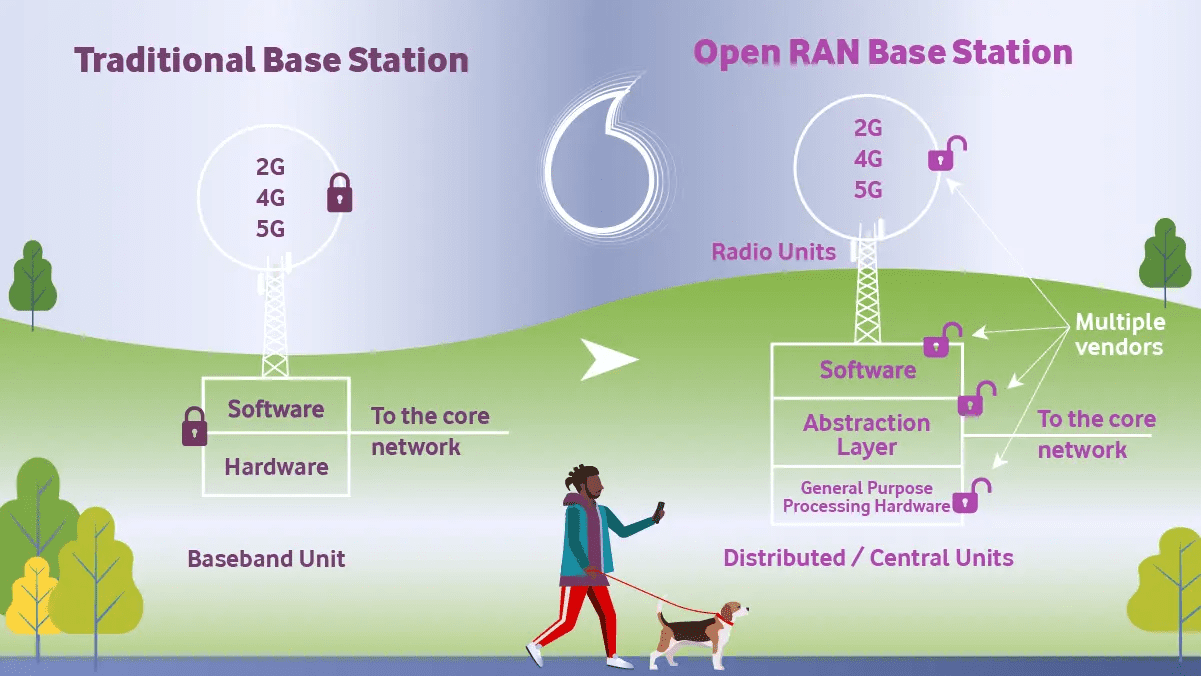

Telefónica Germany and NEC partner to deliver 1st Open RAN with small cells in Germany

Telefónica Germany and NEC Corporation announced their successful collaboration in launching the first Open and virtual RAN architecture-based small cells in Germany. The service has initially launched in the city center of Munich to enhance the customer experience by providing increased capacity to the existing mobile network in this dense, urban area. NEC serves as the prime system integrator in the four countries of Telefónica S.A. and NEC’s program to explore ways to apply Open RAN in various geographies (urban, sub-urban, rural) and use cases. Telefónica Germany had previously said it planned to deploy pure 5G Open RAN mini-radio cells in Munich later this year.

In this German deployment, the flexibility of Open RAN is leveraged through the use of small cells to improve capacity in dense, urban areas. One of the key advantages of Open RAN over a traditional architecture is that it allows wider choice of vendor options. NEC integrated a multi-vendor architecture that includes Airspan Networks* unique Airspeed plug-and-play solution and Rakuten Symphony’s Open vRAN software for O2 / Telefónica Germany’s small cells to complement the existing multi-vendor based macro cells in its network.

The adoption of Open RAN small cells combined with macro cells will pave the way for 5G network densification. This will be especially beneficial in Germany, where multiple industries and enterprises are seeking ways to utilize cellular service functionalities in a particular area or in shared physical spaces.

Source: Telecom Infra Project

……………………………………………………………………………………………………………………………………………………

O2 / Telefónica Germany and NEC will continue their collaboration leveraging innovative Open RAN technologies, as well as automation, to validate and deploy advanced networks that efficiently deliver superior customer experiences in the 5G era, with collaboration from key partners.

“We are proud to have launched Germany’s first small cells built on innovative Open RAN technologies that help to complete the delivery of granular, high-quality connectivity in dense urban areas,” said Matthias Sauder, Director Mobile Access & Transport at O2 / Telefónica Germany. “NEC became our partner in this innovative project, with its underlying technological background and experiences of Open RAN technologies.”

“The potential of Open RAN technologies in the 5G era is infinite,” said Shigeru Okuya, Senior Vice President, NEC Corporation. “NEC is honored to be the strategic partner to O2 / Telefónica Germany, jointly leading the industry with practical and effective use cases that prove the value of Open RAN.”

………………………………………………………………………………………………………..

Germany seems to be a focal point for OpenRAN deployments. For example, greenfield operator 1 & 1 is deploying a fully-virtualized, Open RAN mobile network built by Rakuten Symphony. That partnership began in the fourth quarter of 2021.

At Mobile World Congress this week, Vodafone announced that it plans to use OpenRAN in 30 percent of its masts in Europe – which includes Germany, of course – by 2030. Last November it emerged that it is working with Nokia and network software provider Mavenir to transform Plauen in Germany into a so-called ‘OpenRAN city’ that will be a live testbed for new OpenRAN-based products.

Deutsche Telekom is also a big fan of OpenRAN. Last June it claimed Europe’s first live OpenRAN deployment in Neubrandenburg, which has been dubbed ‘O-RAN Town’. It has partnered with a broad range of suppliers, including NEC, Fujitsu, Dell, Intel, Mavenir and SuperMicro.

Last December, semiconductor/SoC start-up Picocom made headlines in the Open RAN community by releasing the “industrt’s first” 5G NR small cell SoC for Open RAN. This new product, dubbed the PC802, is described as PHY SoC for 5G NR and LTE small cell decentralized and integrated RAN architectures, including support for leading Open RAN specifications. The PC802 allows for interfacing to radio units using either the O-RAN Open Fronthaul eCPRI interface or a JESD204B high-speed serial interface. Optimized explicitly for decentralized small cells, the PC082 employs a FAPI protocol to allow communication and physical layer services to the MAC.

…………………………………………………………………………………………………………………………………………………………..

OpenRAN has been a recurring topic at this week’s Mobile World Congress in Barcelona, with Mavenir, Qualcomm, and Rakuten Symphony, etc. all making product pitches. However, it remains to be seen if Open RAN will actually be able to deliver on its promise of mix and match network modules and lower the cost of network deployment with the performance, security and reliability that network operators must provide to their customers.

…………………………………………………………………………………………………………………………………………………………..

References:

https://www.nec.com/en/press/202203/global_20220302_04.html

Mavenir at MWC 2022: Nokia and Ericsson are not serious OpenRAN vendors

Picocom PC802 SoC: 1st 5G NR/LTE small cell SoC designed for Open RAN

South Korean telcos to double 5G network bandwidth with massive MIMO; Private 5G

South Korea is on course to become the first country in the world where its mobile carriers scale up its 5G network capacity to more than 100 MHz-bandwidth for a single network operator.

At the Mobile World Congress 2022 exhibitions, three network equipment suppliers — Huawei Technologies, Ericsson-LG and Nokia — unveiled the most recent updates of their 5G equipment. Representatives say these could help South Korean telcos improve the quality of 5G delivery by doubling the bandwidth of their allocated network with a single piece of equipment.

The new massive MIMO antenna, allows a telecom carrier to use up to 200 MHz of a 400 MHz spectrum. It also enables bandwidths to be used on separate parts of the 400MHz range, so a carrier could use two 100 MHz bandwidths 200 MHz apart, or even three or more smaller bandwidths. Without the massive MIMO, Korean telcos would have to buy additional equipment to use more than one bandwidth slot or a bandwidth exceeding 100 MHz.

“Korea will become the first country to have its telcos occupy more than 100 MHz in terms of bandwidth (for a mid-range 5G network),” James Han, head of 5G sales Korea at Finland-based Nokia, told reporters at its MWC 2022 exhibition. “The world will be watching, and we are seeing the new market coming,” Han added.

Some of these products are not only showcased but are also being deployed in Seoul. Han said the investment has been underway to deploy its cutting-edge massive MIMO antenna in downtown Seoul, starting this year, as the deployment should be done prior to the forthcoming 5G spectrum auction by the government and the licensing procedures.

Caption: Massive MIMO technology can be mutually beneficial and complementary with ultra-dense networking technology and high-frequency band technology.

Source: Research Gate

………………………………………………………………………………………………………………………………………………………………………

Seoul-based joint venture Ericsson-LG is also testing its newest equipment with Korean telecom carriers. According to Lee Young-jo, vice president at Ericsson-LG, the deployment of a new antenna is expected to kick off in the second quarter. “A telco would have been forced to buy two outdated pieces of equipment to (use) two separate slots, and this would have been a cost burden on the telco,” Lee told reporters.

Nokia and Ericsson-LG have both supplied their products to network infrastructure of Korean carriers KT and SK Telecom. Another partner of the two, Samsung Electronics’ network division, did not unveil new equipment at MWC 2022 as it did not host a booth for its network solutions.

On the other hand, Huawei Technologies, which supplies its equipment to LG Uplus, also showcased at MWC 2022 its massive MIMO solution that supports the 400 MHz bandwidth scope and 200 MHz spectrum availability. The solution, however, has yet to be deployed for LG Uplus.

Meanwhile, the new 5G technology indicated that a successful deployment could settle a heated debate between Korean telecom firms over spectrum allocations. If the deployment is complete, all three companies — SK Telecom, KT and LG Uplus — are likely to be given the same opportunity to claim rights for the new 100 MHz spectrum.

Currently, Korean carriers were allocated the 5G spectrum for mid-band range at between 3.42 GHz and 3.7 GHz bandwidth.

The government in June 2018 allocated an 80 MHz spectrum to LG Uplus, while its rivals KT and SK Telecom both won auctions for 100 MHz spectrums.

The auction effectively gave birth to the world‘s first commercial 5G smartphones in April 2019. It also launched a 5G-powered commercial smart factory in July 2020.

For the last three years, South Korean telcos have been at odds over how the auction of additional bandwidth slots should be carried out. So far, Korea’s 280 MHz bandwidth combined were allocated to telcos, while 320 MHz is to be auctioned before 2023, but details regarding the auction have yet to be determined.

The targeted 5G spectrum includes a 20 MHz slot adjacent to LG Uplus‘ allocated spectrum that was left out at the 2018 auction due to interference with neighboring frequencies.

Addressing the problem, the government sought to put the slot back up for auction, only to face opposition from SK Telecom and KT, arguing they were effectively deprived of opportunities to use the spectrum without additional infrastructure investment, because of technological limitations.

Source: Korea Herald

…………………………………………………………………………………………………………………………

Separately, LG CNS, the information technology wing of South Korea’s LG Group, has applied for government permission to become the second domestic operator of a private 5G network. It will be customized for services in specific regions that affords numerous advantages for modern enterprises as it can deliver ultra-low latency and incredibly high bandwidth connections supporting artificial intelligence-driven applications.

LG CNS said on March 3 that it would accelerate the digital transformation of manufacturing customers by combining 5G with smart factories. The company has released Factova, an integrated smart factory platform based on artificial intelligence, big data, and the internet of things (IoT).

Source: LG CNS

South Korea has commercialized a 5G mobile telecom service using the frequency band of 3.5 GHz. For private 5G networks, the government will provide the 28 GHz band that makes data transmission speed faster especially in areas where traffic is concentrated.

Without borrowing 5G networks built by mobile carriers for businesses in factories or buildings, companies that want to provide 5G-based convergence services can build private 5G networks in specific regions. The private 5G network affords numerous advantages for modern enterprises as it can deliver ultra-low latency and incredibly high bandwidth connections supporting artificial intelligence-driven applications.

Unlike mobile telecommunication companies that developed nationwide business-to-consumer (B2C) communication businesses based on frequency monopoly rights, the ministry said that private 5G network operators can use regional monopoly rights to conduct business-to-business (B2B) communication services in limited areas.

In December 2021, Naver Cloud, a cloud computing service wing of South Korea’s top web portal operator and IT company, has become the country’s first operator of a private 5G network. Naver Cloud will establish a smart office using a private 5G network at a new robot-friendly building under construction in Bundang in the southern satellite city of Seoul.

For services to other companies, Naver Cloud will provide cloud data centers and private 5G networks, while Naver Labs will offer ultra-large AI and 5G brainless robots. Naver will use the robot-friendly building as a global reference space where 5G networks, cloud, robots, autonomous driving, digital twin, and AI are connected and fused into one.

References:

http://www.koreaherald.com/view.php?ud=20220303000733

Rootmetrics: U.S. 5G carriers in close race; South Korea 5G is worldwide #1

https://www.ajudaily.com/view/20220303172314627

https://www.lgcns.com/En/Solution/Factova-MES

Comcast 2021 Network Report: Data Traffic Increased Over Historic 2020 Levels; 10G Coming

After hitting historic peaks in 2020, traffic on the Comcast network grew again in 2021, according to the Comcast 2021 Network Report, released today. Key takeaways:

- In 2021 alone, Comcast invested more than $4.2 billion to strengthen, expand and evolve the network – more than any previous year.

- Traffic patterns remained highly asymmetrical, as peak downstream traffic grew 2x faster than upstream traffic, more closely mirroring pre-pandemic trends.

- In 2021, downstream traffic rose 11% over 2020 levels, while peak upstream traffic rose just 5%. By comparison, 2020 network traffic levels spiked considerably – peak downstream traffic rose 38% while upstream traffic surged 56%

- Similar to last year, entertainment activities dominated peak network traffic, with video streaming accounting for 71 percent of downstream traffic.

“Over the past two years, our network has been a powerful and reliable pillar for our customers as they’ve navigated dramatic changes in how we live, learn, play and work,” said Charlie Herrin, President of Technology, Product, Experience at Comcast Cable. “The outstanding performance of the network throughout this time is a testament to our commitment to strategic investment, unceasing innovation, and the incredible talent and dedication of our technology teams across the country.”

Regarding traffic content, video streaming, at 71%, dominated peak network traffic on Comcast’s network in 2021, compared to 11% for gaming apps, 9% for web browsing and 2% for software updates.

2021 Network Traffic:

Comcast increased speeds for its most popular Xfinity speed tiers in 2021, including increasing gig speeds to 1.2 gigabits-per-second In 2021 alone, Comcast invested more than $4.2 billion to strengthen, expand and evolve the network – more than any previous year.

In addition to smart software and virtualization technologies that increase performance and reliability, Comcast took major steps in 2021 toward the next phase of network evolution. 10G technology will allow Comcast to deliver multi-gigabit upload and download speeds over the connections already in tens of millions of American homes. In 2021, Comcast completed successful tests of key technologies required to deliver 10G, including a world-first demonstration of a complete 10G connection from network to modem.

“Network investment is important, but the network architects and software engineers across Comcast are also innovating at the speed of software,” said Elad Nafshi, EVP & Chief Network Officer at Comcast Cable. “Our colleagues leading these innovations are creating the future for our customers.”

“We certainly haven’t had time to sit still during the past two years, but thanks to billions of investment, continuous innovation, and most importantly the incredible team we have working on the network at every level, we have stayed well ahead of demand, which is really borne out by our performance delivering above-advertised speeds to customers throughout the pandemic,” Nafshi said via email in response to questions from Light Reading.

Xfinity Gigabit Pro is a targeted, residential fiber-to-the-premises (FTTP) service that was recently upgraded to deliver symmetrical speeds of 3 Gbit/s. The cable operator also offers up to 1.2Gbit/s downstream and 35Mbit/s upstream on its DOCSIS 3.1 network.

“We’re always building our network in anticipation of whatever our customers may need in the future, so while traffic today remains heavily asymmetrical – with downstream accounting for 14.5x as much volume as upstream in the last six months of 2021 – we continue to be really excited about the multi-gig symmetrical capacity we are developing for our HFC plant, because it offers a unique path to provide those experiences to customers at scale,” Nafshi explained.

Comcast and other cable operators are now starting to focus on DOCSIS 4.0, a new platform for hybrid fiber/coax (HFC) networks that can deliver up to 10Gbit/s downstream and 6Gbit/s upstream. Recent Comcast tests have generated symmetrical speeds of 4 Gbit/s. Comcast has not announced when it expects DOCSIS 4.0-based services to be ready for prime time.

References:

https://corporate.comcast.com/press/releases/comcast-2021-network-report

https://corporate.comcast.com/press/releases/world-first-test-10g-modem-technology-multigigabit-speeds-to-homes

https://www.lightreading.com/cable-tech/comcast-says-network-traffic-still-rising-but-shifting-to-pre-pandemic-patterns/d/d-id/775741?

https://techblog.comsoc.org/2021/10/28/comcast-broadband-subscriber-growth-slows-business-services-and-xfinity-mobile-gain/

https://techblog.comsoc.org/2021/10/06/comcast-business-announces-28-million-investment-to-expand-fiber-broadband-network/

https://techblog.comsoc.org/2021/07/29/comcast-cable-business-firing-on-all-cylinders-wireless-doing-well-video-revenue-up/

Mavenir at MWC 2022: Nokia and Ericsson are not serious OpenRAN vendors

Andrew Wooden of telecoms.com talked with Mavenir’s SVP of business development John Baker and CMO Stefano Cantarelli to gauge how industry is feeling towards OpenRAN. Here are a few quotes:

“Clearly the (OpenRAN) train has left the station, there’s a lot of buzz about OpenRAN – it’s back to the haves and have nots,” Baker told us. “I see a lot of interest from network operators and a lot of interest from the component suppliers. But on the other side of it, about [Nokia’s recent statement about OpenRAN] – they’re full of it. Because they’re a startup in OpenRAN themselves but are not doing anything. They’re trying to pass on a message that the OpenRAN community is confused, that there are no real OpenRAN players out there, and they’re trying to position themselves as the real OpenRAN player. Digging underneath that, we’re having to call out the Nokia’s and Ericsson’s for confusing the story and trying to keep the confusion running around the marketplace, about the status of OpenRAN.”

“Ericsson has been clear right up front that [they’re] not going to participate in OpenRAN. They name their products as Cloud RAN but you can’t mix and match, so they don’t they don’t meet the OpenRAN requirements. I stand very firm that unless you’ve got two suppliers interworked, then you haven’t got OpenRAN.” Of course, this author agrees 100%!

Regarding Nokia, Baker said: “We’ve been asking for the last two years, every month almost, we’re ready to interwork, when are you ready? And they never get there. So our view is Nokia doesn’t have anything, they’re just trying to protect an old silicon strategy. And that’s their problem. They’ve had two failed attempts, in my opinion, of their silicon strategy – first time they got it completely wrong. Second time they got it too late for the industry because software is now replacing where they are with silicon. I think at the end of the day those two logos are going to disappear in the distance.”

Cantarelli added: “I think Ericsson and Nokia are not stupid. They know OpenRAN is the future, it’s just at the beginning they didn’t think about it, and now they’re a bit late. So they’re protecting their legacy. And they’re waiting for when they’re going to be ready, so it’s purely a delaying technique.”

Some observers think OpenRAN is immediate, and of singular importance, but others don’t think it will be as disruptive as that, at least not right now. This author is in the latter camp. We’ve explained why many times why: without implementation standards there is no interoperability!

References:

Mavenir slams Nokia and Ericsson for confusing the OpenRAN story

Ericsson expresses concerns about O-RAN Alliance and Open RAN performance vs. costs

Vodafone and Mavenir create indoor OpenRAN solution for business customers

https://www.nokia.com/networks/radio-access-networks/open-ran/

Rakuten Communications Platform (RCP) defacto standard for 5G core and OpenRAN?

Strand Consult: Open RAN hype vs reality leaves many questions unanswered

CableLabs to host NTIA’s 5G Challenge – includes 5G SA core network, testing and measurement

The U.S. Department of Commerce announced that CableLabs will host the NTIA- Information Administration’s Institute for Telecommunication Sciences (NTIA-ITS) 5G Challenge, in support of the U.S. Department of Defense (DoD), which seeks to advance open 5G networks with the goal of interoperability and plug-and-play operation from different vendor components. NTIA-ITS will leverage CableLabs’ state-of-the-art lab deployment of fully virtualized 5G networks, including multiple cores, multiple radio access network and new network emulation equipment.

The competition requires a 5G SA core network, testing and measurement capabilities. An important goal of the competition is to help spur a growing 5G supplier community with interoperable, multi-vendor solutions – and CableLabs says its facility has all the right makings to see participants compete in testing and validation on-site.

NTIA launched an inquiry in early 2021 seeking input on a 5G Challenge as it explored ways to speed up development and interoperability of the open 5G ecosystem to support DoD missions. It’s still working on design and execution of the competition, and previously received input from major vendors such as Ericsson and groups including the Open RAN Policy Coalition, which were among 51 responses submitted by a range of industry stakeholders.

“The Department of Defense recognizes that 5G technologies are foundational to strengthening our Nation’s warfighting capabilities as well as U.S. economic competitiveness. Open 5G systems would greatly bolster the Department’s ability to deliver on its missions, and we look forward to exploring new and innovative opportunities for their development,” said Michael Kratsios, Acting Under Secretary of Defense for Research and Engineering.

The effort is going to leverage the CableLabs 17,000-square-foot lab, where it has deployed fully virtualized 5G networks that include multiple cores, radio access network and new network emulation equipment. CableLabs has a 5G SA network prototype with engineering capabilities to integrate multiple vendors at the same time while also testing and measuring technical performance metrics.

In a blog post Wednesday, CableLabs VP of Wireless David Debrecht highlighted the group’s growing expertise focused on mobile networks, such as involvement in industry efforts to build flexible 5G technologies including at 3GPP, the O-RAN Alliance and the Telecom Infra Project. “CableLabs is well situated to host the 5G Challenge, given our long-standing role in the industry and our work with multiple vendors to drive interoperable network technologies,” Debrecht wrote.

CableLabs is deeply involved in the industry’s work to develop flexible 5G technologies—including at 3GPP, O-RAN Alliance and the Telecom Infra Project (TIP)—to enable new vendor opportunities, enhance network security and streamline integration and interoperability.

In a statement, CableLabs president and CEO Phil McKinney indicated work would continue beyond the challenge, as it’s committed to ongoing R&D and interoperability testing in mobile network technologies.

“CableLabs is honored to be the host lab for the 5G Challenge,” McKinney commented. “The recognition from the US Department of Commerce is a testament to CableLab’s continued and increasing investment in mobile wireless network technologies, and particularly, our focus on open and interoperable network technologies.”

The NTIA issued its initial notice of inquiry in support of the DoD’s 5G Initiative, the latter which has committed $600 million for 5G testbeds to see how the military could use the technology for its networking needs. The DoD’s focus on 5G is aimed at technology that will enable both military and commercial deployments.

The 5G challenge, meanwhile, is meant to specifically address the shift toward using open implementations of different components for a 5G system, and NTIA had said an aim is to maximize benefits for both 5G stakeholders and the DoD on an accelerated timeline.

It received feedback across standards and industry groups, equipment vendors, major operators, and others who weighed with comments on the NOI to help inform NTIA about how to structure the challenge and goals, incentives and scope, and timeframe and infrastructure.

Further information:

- Written comments may be submitted by email to [email protected]

- To receive updates, send an email request to [email protected]

About CableLabs:

As the leading innovation and R&D lab for the broadband cable industry, CableLabs creates global impact through its member companies around the world and its subsidiaries, Kyrio and SCTE. With a state-of-the-art research and innovation facility and collaborative ecosystem with thousands of vendors, CableLabs delivers impactful network technologies for the entire industry.

References:

https://www.ntia.doc.gov/5g-challenge

https://www.federalregister.gov/documents/2021/01/11/2021-00202/5g-challenge-notice-of-inquiry

Accelerating 5G Network Innovation: CableLabs Named Host Lab for 5G Challenge

https://www.fiercewireless.com/tech/cablelabs-chosen-host-ntia-dod-5g-challenge

https://www.fiercewireless.com/5g/ericsson-open-ran-coalition-weigh-ntia-5g-challenge

OpenRAN in 30% of Vodafone European network by 2030; Europe way behind China and South Korea in 5G deployments

Vodafone will use OpenRAN technology in 30% of its masts across Europe by 2030, said Johan Wibergh, Vodafone Group Chief Technology Officer, in a speech at Mobile World Congress (MWC) 2022 in Barcelona.

Around 30,000 Vodafone cell sites across Europe will eventually use OpenRAN, he said, with rural areas the first to benefit from the new 4G and 5G masts that use the more flexible radio technology.

When the roll-out reaches cities, the equipment from any existing 5G masts being replaced will then be reused elsewhere to reduce unnecessary wastage, he said.

Vodafone has been one of the key drivers behind the development and use of OpenRAN, building one of the first-ever live OpenRAN masts in Wales. This was followed by the construction of OpenRAN masts in Cornwall, as well as the UK’s first 5G OpenRAN site.

At MWC 2022, Vodafone announced new smartphone sustainability initiatives, as well as the trial of new Internet of Things technology to enable cars to pay automatically for their own refueling.

……………………………………………………………………………………………………………………………………………………………………………………………..

Earlier this week, Vodafone Group CEO Nick Read addressed MWC 2022 attendees in a keynote speech, highlighting the challenges and opportunities facing the mobile industry. Among them are the following:

Europe needs to be digital to remain globally competitive and maintain its leadership role in key sectors such as automotive, aerospace, defence, and agriculture. The regions that have 5G first, will be the regions that innovate fastest.

Yet, at current rates, it will take until at least the end of the decade, for Europe to match the transformational “full 5G experience” that China will already have achieved this year. If we look at 5G population coverage around the world – South Korea is over 90%, China 60%, USA 45%, and Europe under 10% – and with Africa hardly even at the starting line. Europe will only catch up if we reverse the ill-health and hyper-fragmentation of our sector. We must have local scale to close the investment gap. Otherwise, we will be the passive by-stander of the new tech order.

Local scale is needed to close the investment gap and ensure we can deploy 5G at pace. Regional scale is needed to close the digitalisation gap. The combination of local and regional scale ensures our economies and societies can enjoy the full benefits of digital innovation and industrialisation.

We have all seen the impact of global digital platforms. Platforms that change the way we conduct our daily lives. Vodafone continues to invest in regional platforms – let me just give you a few examples. In Europe we created our IoT platform which connects more than 140m devices, across 180 countries. The SIM based IoT market has tripled in the last five years, – and in the next 5 years, will hit 5bn connections. 62% of Europe’s leading automotive brands rely on Vodafone IOT. And with that scale, we are able to evolve from the “Internet of Things” to the “Economy of Things.”

References:

https://newscentre.vodafone.co.uk/news/openran-in-30-percent-of-vodafone-european-network-by-2030/

https://www.vodafone.com/news/digital-society/mwc22-new-tech-order

https://newscentre.vodafone.co.uk/press-release/switches-on-first-5g-openran-site/

Cincinnati Bell rebrands as Altafiber after takeover by Macquarie Infrastructure

Consistent with the strong fiber build-out megatrend, Cincinnati Bell [1.] said it will now be doing business in Ohio, Kentucky and Indiana under the new Altafiber brand. With its takeover by Macquarie Infrastructure now complete, the company will continue to put attention on expanding its geographic reach and investing into its broadband network. Cincinnati Bell will transition to the Altafiber brand over the next 6-9 months. The change will not impact Hawaiian Telcom and the IT services business, branded as CBTS.

Note 1. Cincinnati Bell was founded in 1873 as the City and Suburban Telegraph Association and later called the Cincinnati and Suburban Bell Telephone Company starting in 1903.

“The investment in fiber, our geographic expansion, and our partnership with Macquarie mark a clear inflection point for the company. And it’s all incredibly exciting and positive for our employees and for the communities and customers that we serve,” said Leigh Fox, President and CEO of altafiber.

“The word ‘alta’ is rooted in a word that means elevated, and that’s what altafiber is doing: We’re providing an elevated connection through fiber and raising the standard of service to our customers and the communities,” the company said. Cincinnati Bell said the new Altafiber brand and mission statement embodies the company’s tagline, “Connecting What Matters,” while capturing its transformation into a fiber optic based carrier positioned to support customers over the next 150 years.

As the leading supplier of fibre services in Greater Cincinnati, Altafiber has invested over USD 1 billion into the fiber optic network and now offers Fiber-to-the-Premises (FTTP) connectivity to 60 percent of all locations in the area. The idea is to provide the services to all of the addresses in the area over the next fibre years.

Altafiber will also bring fiber beyond its traditional operating area through partnerships with Greene County in Ohio, and City of Greendale, Indiana. Altafiber has established a regional headquarter in the Dayton market, including a retail store and business office in the city.

Fox noted that the he company’s commitment to the community, its customers, and leadership continues:

• Commitment to the community. altafiber and its employees will continue to support community initiatives – particularly those that provide increased access to education, employment, and healthcare opportunities – and increase investments into sustainability, safety, and diversity and inclusion initiatives.

•Commitment to customers. altafiber will continue to provide customers with the same great service they have come to expect from the company.

• Leadership. The current executive team will continue to lead the company. altafiber will also honor its legacy through the recently launched “Bell Charitable Foundation,” an exciting new platform for corporate giving that will allow the company to more strategically support

organizations that are focused on Economic, Environmental, Social, Technology, and Health & Wellbeing initiatives.

“We are proud of the Cincinnati Bell name, and it will always be a part of our history,” said Fox. “We are still the local hometown company, with 2,000 employees across Greater Cincinnati who are dedicated to connecting our customers with what matters most through technology for the next 150 years,” Fox said.

About altafiber:

Cincinnati Bell is now doing business as “altafiber” in Ohio, Kentucky, and Indiana. The Company delivers integrated communications solutions to residential and business customers over its fiber-optic network including high-speed internet, video, voice and data. The Company also provides service in Hawai’i under the brand Hawaiian Telcom. In addition, the Company’s enterprise customers across the United States and Canada rely on CBTS and OnX, wholly-owned subsidiaries, for efficient, scalable office communications systems and end-to-end IT solutions.

References:

https://info.cincinnatibell.com/altafiber

https://www.telecompaper.com/news/cincinnati-bell-rebrands-to-altafiber–1416259

Qualcomm FastConnect 7800 combining WiFi 7 and Bluetooth in single chip

Qualcomm Technologies has announced its first Wi-Fi 7 chip, the FastConnect 7800. Bundling the latest Wi-Fi (IEEE 802.11) and Bluetooth specifications, the new chip is sampling already and expected to be available for commercial products in the second half of 2022. Qualcomm said this should be the first Wi-Fi 7 chip to launch commercially, pending the start of certification of Wi-Fi 7 products.

Wi-Fi 7, also known as IEEE 802.11be, is still in development so has not yet been approved as an IEEE standard. It includes features like 4k QAM, 320MHz channel bandwidth, and multi-link capabilities. Though, as with every standard, implementation is where truly differentiated performance is achieved. For example, multi-link can be implemented with simultaneous links or alternating links. Further, one of those links may be implemented using the narrow and congested 2.4GHz band (which could otherwise be reserved for Bluetooth or IoT devices). Design choices such as these will dictate how well your next devices will be able to harness Wi-Fi 7 speed and latency benefits, so Qualcomm Technologies’ approach is to offer a flexible solution that will include all the options.

Qualcomm said it expects the WiFi 7 system to deliver peak speeds up to 5.8Gbps, via single 320MHz or paired 160MHz channels, falling to 4.3Gbps when the 6GHz band is not be available. Latency should be less than 2ms.

One of the key features of the new system is High Band Simultaneous (HBS) Multi-Link technology. This simultaneously leverages two Wi-Fi radios for four streams of high band connectivity in the 5GHz and/or 6GHz bands. These connections can deliver the highest throughput and lowest sustained latency, while reserving high-traffic 2.4GHz spectrum for Bluetooth and lower-bandwidth Wi-Fi applications.

In addition, the new chip extends 4-Stream Dual-Band Simultaneous (DBS) into the high bands. This builds on Qualcomm’s 4-Stream DBS (2×2 + 2×2) with 5 and/or 6GHz Wi-Fi links used in concert for extreme low latency performance between access point and client or independently for multi-client scenarios. For instance, a mobile device connecting to a Wi-Fi 6/6E access point (for 2×2 backhaul in high band spectrum) can concurrently connect to an XR headset (for 2×2 fronthaul also in high band spectrum), free from the low bandwidth and congestion of the 2.4GHz band.

Qualcomm also promises high-quality Bluetooth audio with the new chip, which includes support for Snapdragon Sound. Its Intelligent Dual Bluetooth offers two radios with enhanced connections, enabling Bluetooth accessories to work up to twice the range, to pair in half the time, and speed up changing a Bluetooth connection between devices, according to the company.

Special attention was given to ensure that FastConnect 7800 maintains compatibility with all prior generation devices. Whatever generation of Wi-Fi or Bluetooth being used, FastConnect 7800 is built to provide the best connectivity. Sampling is already underway, with commercial availability rolling out in the second half of 2022.

At the launch at MWC, several companies including Honor, Meta, Xiaomi, Vivo and Oppo said they plan to use the new chip in future products.

https://www.qualcomm.com/products/fastconnect-7800

Lumen Technologies tops Vertical Systems Group’s 2021 U.S. Wavelength Services Leaderboard

- Customer demand for retail wavelength circuits exceeded wholesale deployments in 2021.

- Revenue for U.S. Wavelength Services is projected to grow at a 13% CAGR between 2021 and 2026. This projection incorporates the effects of the COVID pandemic, including installation disruptions and chip shortages.

- Six providers on the U.S. Wavelength Services LEADERBOARD also hold a rank position on the latest U.S. Fiber Lit Buildings LEADERBOARD – Lumen, Zayo, Verizon, AT&T, Crown Castle and Cox. Additionally, Windstream achieved a Challenge Tier citation.

- Five U.S. Wavelength Services LEADERBOARD providers are also top ranked on the Mid-2021 U.S. Ethernet LEADERBOARD– Lumen, Verizon, AT&T, Windstream and Cox. Zayo has a Challenge Tier citation.

………………………………………………………………………………………………………………………………….

References:

VSG LEADERBOARD : AT&T #1 in Fiber Lit Buildings- Year end 2020