Verizon faces tough times as 5G fails to generate a decent ROI

In 2021, Verizon spent more than $50 billion at FCC auctions to acquire mid-band C-band spectrum licenses for 5G. Along with AT&T, it negotiated a high-profile battle with the U.S. airline industry and FAA to put those spectrum licenses into commercial operations at the beginning of this year.

Verizon launched a C-band 5G network covering 130 million people – almost half of the U.S. population- in the 1st quarter of 2022. By the end of the first quarter, around 40% of Verizon‘s customers owned 5G gadgets capable of accessing the network, and it’s already carrying almost a third of all of Verizon‘s data traffic where it is available.

According to results from network-monitoring company Ookla, Verizon‘s 5G download speeds doubled via to its C-band network launch. However, the effort has been costly. Verizon‘s quarterly capital expenses (capex) spiked during the first quarter thanks to the $1.5 billion it spent during the period on the network equipment necessary to put its C-band licenses into action. That figure doesn’t include the extra money Verizon spent on its massive marketing campaign, which included $1,000 handset subsidies and a $1,000 switcher credit, during the quarter to promote the new network.

What does Verizon have to show for all its mid-band 5G investments? So very much as Moody wrote in a report skeptical on 5G monetization.

In the 1st quarter of 2022, Verizon lost 36,000 postpaid phone customers. While that’s certainly an improvement over the operator’s quarterly performance from a year ago, and also better than some financial analyst expectations, it stands in stark contrast to the 691,000 new postpaid phone customers AT&T netted during the period. AT&T, for its part, has delayed slightly its own big mid-band 5G network buildout until next year.

Moreover, Verizon executives acknowledged that the company saw a slowdown in new customers signing up for Verizon service starting in February and accelerating into March, just as the operator’s C-band marketing campaign ramped up.

David Barden, a financial analyst with Bank of America Merrill Lynch, called out the situation during Verizon‘s quarterly conference call on Friday. “There was a time when Verizon had the best network and could charge the highest prices. And on these calls we would talk about margins and obtainable market share,” he said. “You guys are now [market] share donors. And we’re celebrating how many 5G phones we have and how much C-band we’re deploying, but it’s not obvious that that’s translating into something tangible that investors can celebrate in terms of financial reward. So can we talk a little about that?”

Verizon‘s management team, including CEO Hans Vestberg, argued that “our focus over time is to grow this business.”

“We’re going to compete well,” Vestberg said, adding that “we see more excitement in the market where we offer C-band.”

“This is going to pay off big time in 5-10 years,” he said of Verizon‘s broad 5G investments.

However, he also conceded that Verizon could suffer from inflationary pressures on its labor and energy costs. And, like AT&T CEO John Stankey, he said Verizon may consider raising service prices as a result.

Verizon has lowered their 2022 guidance to the low end of their previous range on every key metric, and they cut their forecast for service and other revenue growth to flat (from +1.0-1.5% previously). The company warned that it now expects its full-year 2022 financial results to come in at the low end of its previously announced guidance. Nonetheless, “we remain well positioned to achieve our long-term growth targets,” Vestberg said.

Analysts don’t seem to agree with Vestberg’s optimism:

“Verizon is growing neither its subscriber base nor its ARPU [average revenue per user]. At a time of rising inflationary pressures, pricing power is nowhere to be found,” wrote the colleague Craig Moffett at MoffettNathanson in a note to clients following the release of Verizon‘s first-quarter results. “And on the unit side, Verizon is already losing share. Unless something changes for 5G revenues that still seem rather intangible (IoT, MEC [multiaccess edge computing], or private networks), the growth runway for Verizon would appear rather weak.”

“There are areas for concern outside of the Wireless segment. Again like AT&T, their Wireline segment is a drag on growth that is only getting worse (their results in Business Wireline, in particular, were – like AT&T’s yesterday – shockingly weak). That puts even more of an onus on the Wireless unit to grow.”

“Things aren’t likely to get easier. Consolidated operating revenue (as reported) of $33.6B was 0.3% below consensus of $33.7B. With such anemic growth, the inflation backdrop is a troubling one. Costs will rise faster than revenues.”

Moffett sees “no easy answers” for Verizon. It could “bow to the pressure” and increase promotions, but he noted that this would further constrain average revenue per user growth for both Verizon and the broader industry. The company could stay disciplined with its pricing and promotional strategies, but doing so would risk further subscriber losses at a time when Verizon’s network advantage over rivals is in jeopardy. “In summary, the path forward remains a challenging one,” Craig concluded.

Financial analysts with New Street Research wrote: “We do remain concerned about Verizon‘s longer-term prospects in wireless, fueled by T-Mobile‘s lead over Verizon on deploying upper mid-band [spectrum] and big lead on total holdings in mid-band spectrum. Verizon management’s aspirations for strong service revenue growth driven by rising ARPU and growing subscribers also still seem way too optimistic in the face of rising competition from a challenger [T-Mobile] with a similar (if not soon-to-be better) network offering priced at a steep discount.”

The New Street analysts also acknowledged that there are widespread expectations that overall growth in the U.S. wireless industry will start to slow sometime this year and that Verizon could be the first 5G operator to suffer from that trend that may eventually affect all of the market’s players.

References:

https://www.lightreading.com/5g/is-verizons-big-5g-gamble-falling-apart/d/d-id/776998?

Huawei to expand consumer products to include smartphones, PCs and other consumer-oriented devices

Huawei Technologies said on Wednesday it will step up efforts to expand its presence in the commercial hardware market in its latest effort to pursue new growth opportunities beyond smartphones amid foreign government restrictions. Richard Yu Chengdong, a member of Huawei‘s executive board, said: “The company has rebranded its consumer business group that includes smartphones, PCs and other consumer-oriented businesses, into a device business group, to showcase its determination to tap into enterprise-oriented businesses such as PCs used in offices, desktops and large displays for industry customers.”

Huawei‘s new group will focus on providing office hardware and software solutions for key sectors including education, healthcare, manufacturing, transportation, finance and energy, Huawei said. Huawei‘s consumer business group used to contribute the most to the overall revenue of the company. But due to tough US government restrictions on Huawei‘s access to crucial technologies including semiconductors, the company’s smartphone sales plunged.

In the fourth quarter of 2021, Huawei‘s consumer business group revenue dropped nearly 50 percent to 243.4 billion yuan ($38 billion).

According to market research company Counterpoint, the company’s global smartphone market share fell below 4 percent since the first quarter of 2021, compared with its peak of 20 percent in the second quarter of 2020.

Amid such a context, Huawei has been working hard to find new growth engines to offset its declining smartphone business.

At an online product launch on Wednesday, Huawei unveiled its latest commercial tablets, smart wearables and displays equipped with its self-developed HarmonyOS. Huawei also provides a customized full-scenario payment solution called Huawei Payment for government clients and small and medium-sized enterprises.

Xiang Ligang, director-general of the Information Consumption Alliance, an industry association, said sales channels constitute the biggest difference between consumer-oriented and enterprise-oriented businesses. The former relies on retail stores, while the latter depends on close partnerships with customers from industries.

Huawei‘s advantages in product performance, quality as well as research and development can still give it an edge in enterprise-oriented business, Xiang said, adding that Huawei has accumulated experience in targeting industrial customers in its 5G base station business. Huawei is also continuing its drive for development of the OpenEuler operating system as part of its broader push to solve China’s lack of homegrown operating systems for fundamental digital technologies.

OpenEuler is designed for enterprise customers and can be used in devices such as servers and cloud computing. Last year, Huawei donated its Euler operating system to the OpenAtom Foundation, a major open source foundation in China, to become an open-source OS.

Jiang Dayong, director of the OpenEuler Community, said the OpenEuler open source community has attracted more than 8,000 developers and 330 partners such as chip makers, software companies and hardware makers. At present, the cumulative installed capacity of OpenEuler stands at more than 1.3 million in industries such as finance, transportation and telecom, which means the system is ready for faster growth. Jiang said he expects about 2 million new installations of OpenEuler in 2022.

Computer products at a Huawei store in Foshan, Guangdong province, on April 4, 2022. Photo: VCG

……………………………………………………………………………………………………………………………………………………………………….

References:

Comcast Deploys Advanced Hollowcore Fiber With Faster Speed, Lower Latency

Comcast today announced what is believed to be the first-ever end-to-end deployment of advanced “hollowcore” fiber optics in the world by an Internet Service Provider (ISP). Hollowcore fibers deliver significantly lower latency than traditional fibers and over time will provide critical performance attributes. These fibers will help power Comcast’s network and support the delivery of multigigabit speeds through 10G b/sec.

Unlike traditional fibers, in which laser light travels over a solid glass core, “hollowcore” fibers are empty inside with air-filled channels. Since light travels nearly 50 percent faster through air than glass, data travels about 150 percent faster with up to 33 percent lower latency through “hollowcore” fiber compared to traditional fiber. The faster speed of light can be used to double the reach for latency critical applications or can speed up the transaction rates by around 47 percent.

For the deployment announced today, Comcast worked with hollowcore fiber cable solutions provider, Lumenisity.

“Hollowcore fiber is a leap forward in how we deliver ultra-fast, ultra-low latency and ultra-reliable services to customers,” said Elad Nafshi, EVP & Chief Network Officer at Comcast Cable. “As we continue to develop and deploy technology to deliver 10G, multigigabit performance to tens of millions of homes, hollowcore fiber will help to ensure that the network powering those experiences is among the most advanced and highest performing in the world.”

“The reality is that light travelling through air is about 50% faster than travelling through glass. The data throughput and the latency is greatly improved when you have a hollowcore fiber … The advantage is you can extend your reach at equal performance,” Nafshi said. Hollowcore fiber, like traditional fiber, can be used in the access, metro or core network, and is compatible with legacy fiber.

Comcast connected two locations in Philadelphia, which enables network engineers to continue to test and observe the performance and physical compatibility of hollowcore fiber in a real-world deployment. This 40-kilometer hybrid deployment of hollowcore and traditional fiber is believed to be the longest in the world by an Internet provider. Comcast successfully tested bidirectional transmission (upstream and downstream traffic traveling on a single fiber), used coherent and direct-detect systems (allowing for forward and backward technology compatibility), and produced traffic rates ranging from 10 gigabits per second (Gbps) to 400 Gbps all simultaneously on a single strand of hollowcore fiber.

“We are proud to be working with Comcast on the next generation hollowcore fiber, which we believe unlocks exciting new potential for connectivity around the world,” said David Parker, Executive Chairman of Lumenisity.

Hollowcore fiber will help to power the next generation of ultra-low latency technologies to support network virtualization, telemedicine, augmented and virtual reality, and other emerging services. Moving forward, Comcast is exploring opportunities to strategically deploy hollowcore fiber in select core- and access-network deployments. From 2017 to 2021, Comcast added more than 50,000 new route miles of fiber to its network and is actively building more fiber into cities and towns across the United States.

Comcast’s ongoing work to expand and evolve its fiber deployments – including this groundbreaking step forward with hollowcore fiber – helps to power Comcast’s ongoing 10G evolution, which will deliver reliable multigigabit upload and download speeds over the connections already installed in tens of millions of homes and businesses.

An illustration of the air-filled channels utilized in hollowcore fiber.

Source: Comcast

………………………………………………………………………………………………………………..

Comcast deployed more than 50,000 new route miles of fiber to its network from 2017 to 2021. The operator isn’t revealing how or when it might commercialize its use of hollowcore fiber, but the operator sees it playing a role for certain apps and use cases, such as telemedicine, AR/VR and network virtualization.

The operator might also use the technology to target new customer segments that are seeking greater throughputs and lower latencies.

From a broader standpoint, hollowfiber could provide a conduit for “10G,” an industry initiative focused on delivering symmetrical 10Gbit/s speeds, low latencies and enhanced security over fiber-to-the-premises (FTTP), hybrid fiber/coax (HFC) and wireless networks.

Citing its 40km connection in Philadelphia, Comcast is billing this as the world’s longest ISP deployment of hollowcore fiber so far.

But Comcast isn’t the only major operator working closely with Lumenisity. Last year, the startup announced BT was trialing its new optical fiber technology at its labs in Adastral Park, Ipswich. That trial involved a 10km-long hollowcore fiber from Lumenisity.

Lumenisity was spun out of the Optoelectronics Research Centre at the University of Southampton in 2017, with an aim to commercialize the development of hollowcore fiber.

In 2020, the startup closed a £7.5 million ($9.77 million) funding round from a group of investors that included BGF and Parkwalk Advisors and existing industrial strategic investors. Lumenisity has raised £12.5 million (US$16.28 million), according to Crunchbase.

Some key application areas Lumenisity has identified for its technology include financial, data center connectivity and connectivity for the separation of remote radio units and baseband units in 5G networks.

About Comcast Corporation:

Comcast Corporation (Nasdaq: CMCSA) is a global media and technology company that connects people to moments that matter. We are principally focused on broadband, aggregation, and streaming with 57 million customer relationships across the United States and Europe. We deliver broadband, wireless, and video through our Xfinity, Comcast Business, and Sky brands; create, distribute, and stream leading entertainment, sports, and news through Universal Filmed Entertainment Group, Universal Studio Group, Sky Studios, the NBC and Telemundo broadcast networks, multiple cable networks, Peacock, NBCUniversal News Group, NBC Sports, Sky News, and Sky Sports; and provide memorable experiences at Universal Parks and Resorts in the United States and Asia. Visit www.comcastcorporation.com for more information.

Media Contact:

David McGuire 215-422-2732

[email protected]

About Luminosity:

Lumenisity® Limited was formed in early 2017 as a spin-out from the world-renowned Optoelectronics Research Centre (ORC) at the University of Southampton (UK) to commercialize breakthroughs in the development of hollowcore optical fibre. We have built a team of industry leaders and experts to realise our goal to be the world’s premier high-performance Hollowcore fibre optic cable solutions provider, offering customers reliable, deployable, low latency and high bandwidth connections that unlock new capabilities in communication networks.

Lumenisity is well funded by a consortium of industrial and private investors. We recently relocated our headquarters to Romsey, UK after a substantial investment was made in developing a state of the art manufacturing and testing facility. Our vision is to be the world’s premier high-performance hollowcore fibre optic cable solutions provider offering our customers reliable, deployable, low latency and high bandwidth connections that unlock new capabilities in communication networks.

References:

Comcast 2021 Network Report: Data Traffic Increased Over Historic 2020 Levels; 10G Coming

Comcast broadband subscriber growth slows; Business services and Xfinity Mobile gain

Comcast Business Announces $28 Million Investment to Expand Fiber Broadband Network in Eastern U.S.

Comcast Earnings Report: Record Broadband Growth; 3 Core Strategy Tenets; Wireless Expansion

New broadcast TV standard ATSC 3.0 “Next Gen TV” to cover 82% of U.S. households by end of 2022

Pearl TV, a consortium of U.S. broadcasters operating more than 820 TV stations, said that it is making progress with hardware and software that wants to accelerate the rollout and adoption of ATSC 3.0, the new broadcast TV signaling standard that’s been branded as “NextGen TV.” ATSC 3.0 has been in the works for many years, but only now seems to be gaining a wide following.

Pearl TV has collaborated with Taiwan wireless telecom semiconductor company MediaTek on a reference design for smart TVs and other devices that support the new standard. On the software front, the consortium has formally introduced RUN3TV, a web-based platform that enables broadcasters to deliver interactive and on-demand apps and services over ATSC 3.0.

The new IP-based standard – which supports 4K video, enhanced audio and interactive apps – are expected to take center stage. Pearl TV’s members include Cox Media Group, the E.W. Scripps Company, Graham Media Group, Hearst Television, Nexstar Media Group, Gray Television, Sinclair Broadcast Group and Tegna.

Sinclair Broadcast Group and USSI Global said they will partner to offer the nation’s first commercial datacasting service using the NextGen Broadcast standard (ATSC 3.0). The pilot program will deliver local content, advertising, and data files to the rapidly growing Electric Vehicle Charging station market.

The ATSC 3.0 reference design – billed as the “FastTrack to NextGen TV” platform – includes a TV system-on-chip (SoC), ATSC 3.0 demodulators and a software stack. It will be pre-certified for compliance with the Consumer Technology Association’s (CTA’s) NextGen TV logo requirements, A3SA security (which uses IP-based encryption protocols, device certificates and rights management technology) and the RUN3TV application platform.

It’s hoped that the ATSC 3.0 reference design will open up the market for lower-cost ASTC 3.0-based TVs and drive more volume into the NextGen TV ecosystem. MediaTek already provides TV SoCs to about 90% of all TV brands, according to Pearl TV and MediaTek. The program stems from a partnership between them announced in January 2022. CTA expects NextGen TV sales to double this year, rise by 75% in 2023 and then double again in 2024.

About 70 TV models from Samsung, Sony and LG Electronics support ASTC 3.0 today, with Hisense on deck to build sets that utilize the new standard. More than 100 TV models are expected to support ATSC 3.0 by later this year, Anne Schelle, managing director of Pearl TV, recently told Light Reading.

The official launch of RUN3TV brings to market a web platform that supports interactive apps delivered via ATSC 3.0, such as targeted advertising, weather widgets, live sports scores, TV-based commerce and enhanced emergency alerts. It is arriving on the scene as the deployment of the new standard reaches about 60 markets.

Pearl TV is launching the RUN3TV platform through a subsidiary, ATSC 3.0 Framework Alliance LLC, with development partners that include Kineton, MadHive, IBM Weather, Freewheel (the Comcast-owned ad-tech company) and Google. Gray Television.

The E.W. Scripps Company, Graham Media, Tegna, Hearst and Howard University’s WHUT are among the platform’s early adopters.

“With NextGen TV and RUN3TV, broadcasters can now bring the OTA environment into the digital world,” Schelle said in a statement.

The reference design and interactive platform are coming together amid an ongoing expansion of ATSC 3.0. It’s expected that NextGen TV will cover about 82% of all U.S. households by the end of 2022. Large markets set for launches later this year include Boston, New York, Philadelphia, Chicago and Miami.

References:

Gartner: Public Cloud End-User Spending to approach $500B in 2022; $600B in 2023

Gartner forecasts that public cloud end user spending will reach nearly $600 billion by the end of 2023. The market research firm says public cloud services will continue in 2022, and nearly capture $494.7 billion in global spending this year – up from $410.9 billion in 2021. That represents a 20.4% increase in spending from 2021.

“Cloud is the powerhouse that drives today’s digital organizations,” said Sid Nag, research vice president at Gartner. “CIOs are beyond the era of irrational exuberance of procuring cloud services and are being thoughtful in their choice of public cloud providers to drive specific, desired business and technology outcomes in their digital transformation journey.”

Infrastructure-as-a-service (IaaS) is forecast to experience the highest end-user spending growth in 2022 at 30.6%, followed by desktop-as-a-service (DaaS) at 26.6% and platform-as-a-service (PaaS) at 26.1% (see Table 1). The new reality of hybrid work is prompting organizations to move away from powering their workforce with traditional client computing solutions, such as desktops and other physical in-office tools, and toward DaaS, which is driving spending to reach $2.6 billion in 2022. Demand for cloud-native capabilities by end-users accounts for PaaS growing to $109.6 billion in spending.

Table 1. Worldwide Public Cloud Services End-User Spending Forecast (Millions of U.S. Dollars)

| 2021 | 2022 | 2023 | |

| Cloud Business Process Services (BPaaS) | 51,410 | 55,598 | 60,619 |

| Cloud Application Infrastructure Services (PaaS) | 86,943 | 109,623 | 136,404 |

| Cloud Application Services (SaaS) | 152,184 | 176,622 | 208,080 |

| Cloud Management and Security Services | 26,665 | 30,471 | 35,218 |

| Cloud System Infrastructure Services (IaaS) | 91,642 | 119,717 | 156,276 |

| Desktop as a Service (DaaS) | 2,072 | 2,623 | 3,244 |

| Total Market | 410,915 | 494,654 | 599,840 |

BPaaS = business process as a service; IaaS = infrastructure as a service; PaaS = platform as a service; SaaS = software as a service. Note: Totals may not add up due to rounding. Source: Gartner (April 2022)

“Cloud native capabilities such as containerization, database platform-as-a-service (dbPaaS) and artificial intelligence/machine learning contain richer features than commoditized compute such as IaaS or network-as-a-service,” said Nag. “As a result, they are generally more expensive which is fueling spending growth.”

SaaS remains the largest public cloud services market segment, forecasted to reach $176.6 billion in end-user spending in 2022. Gartner expects steady growth within this segment as enterprises take multiple routes to market with SaaS, for example via cloud marketplaces, and continue to break up larger, monolithic applications into composable parts for more efficient DevOps processes.

Emerging technologies in cloud computing such as hyperscale edge computing and secure access service edge (SASE) are disrupting adjacent markets and forming new product categories, creating additional revenue streams for public cloud providers.

“Driven by maturation of core cloud services, the focus of differentiation is gradually shifting to capabilities that can disrupt digital businesses and operations in enterprises directly,” said Nag. “Public cloud services have become so integral that providers are now forced to address social and political challenges, such as sustainability and data sovereignty.

“IT leaders who view the cloud as an enabler rather than an end state will be most successful in their digital transformational journeys,” said Nag. “The organizations combining cloud with other adjacent, emerging technologies will fare even better.”

Gartner clients can read more in Forecast: Public Cloud Services, Worldwide, 2020-2026, 1Q22 Update. Lean more in the complimentary Gartner webinar Cloud Computing Scenario: The Future of Cloud.

References:

Gartner: Accelerated Move to Public Cloud to Overtake Traditional IT Spending in 2025

Strong growth for global cloud infrastructure spending by hyperscalers and enterprise customers

Gartner: Global public cloud spending to reach $332.3 billion in 2021; 23.1% YoY increase

Omdia: VMware and Versa Networks are SD-WAN revenue leaders; SD-WAN market to hit $6.7B by 2026

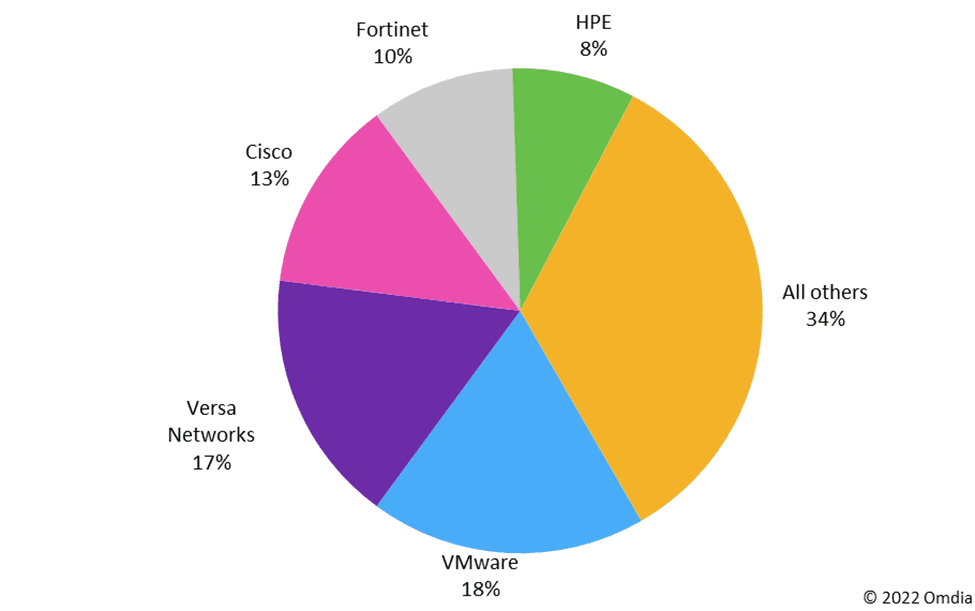

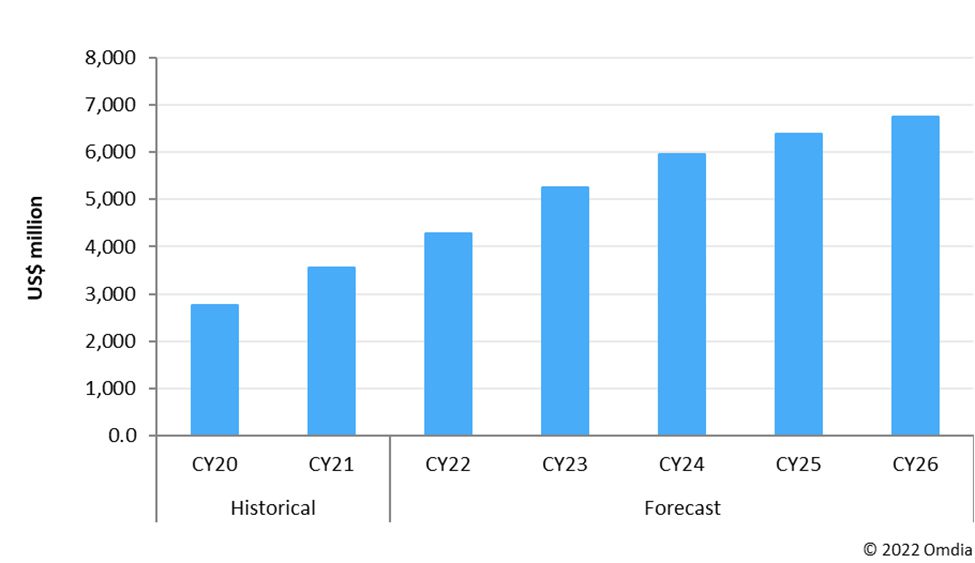

According to a new report by market research firm Omdia (owned by Informa in the UK ), SD-WAN revenue remained on track with forecasts reaching $3.6 billion in 2021. Edge computing, an increased use of machine learning (ML) and artificial intelligence (AI), and growth in IoT are also increasing demand for SD-WAN services, Omdia said. The SD-WAN market exceeded $1 billion in total revenue for Q4 2021, up 24% year-over-year. Amongst SD-WAN vendors, VMware led in 2021 with 18% market share for Q4, followed closely by Versa Networks (17%) and Cisco (13%). Both VMware and Cisco got to the top through various SD-WAN acquisitions. More importantly, SD-WANs (with application aware routing and an overlay network) seem to have totally replaced classical SDN based WANs (with strict separation of Data and Control place, centralized Network layer routing, and NO overlay networks) as we don’t hear anything about that previously ultra-hyped “pie in the sky” technology.

Omidia says that vendors which managed their supply chain, shipping, logistics or relied heavily on uCPE hardware fared the best in 2021. Power management integrated circuits (PMIC) remain the biggest bottleneck for server vendors; interface integrated circuits (ICs), microcontrollers and networking application-specific ICs (ASICs) are among the components in short supply impacting SD-WAN vendors, said Omdia. There are also growing opportunities for vendors and service providers to work together on delivering SD-WAN as a managed service as customer demand trends away from DIY (do it yourself) SD-WAN.

“There is a new opportunity for vendors and CSPs as the market transitions from providing optimization of application packet streams on single links with WAN optimization appliances to agility and cost savings enabled by virtualizing the WAN across multiple link types with SD-WAN,” added Omdia.

The SD-WAN market has also benefitted from increased deployment of cloud and multi-cloud services as a result of enterprise efforts to support a more distributed workforce. Omdia cites adoption of 5G as another driver for SD-WAN demand to “help deploy and manage network capability, connectivity and security cost-effectively.”

“Service providers are beginning to look to SD-WAN to provide traffic steering over 5G LTE links for use cases such as the Industrial Internet of Things (IIoT),” said Omdia. Security is also front-of-mind to protect remote workers but is frequently viewed more as “an additional layer than a priority when selecting an SD-WAN provider,” Omdia added.

SD-WAN deployments in the healthcare industry have also experienced significant growth due to increased reliance on mobile health devices and telehealth services.

Over the next two years, Omdia predicts that SD-WAN vendors will further integrate services to provide vendor interoperability for enterprise customers, and that AI automation technology will be added to SD-WAN software for automated real-time analysis and network optimization for application traffic.

By 2026, the SD-WAN market will reach $6.7 billion in revenue, according to Omdia’s forecast. That’s up from $3.6 billion revenue in 2021 and results in a CAGR of almost 20%.

References:

https://www.lightreading.com/sd-wan/omdia-sd-wan-boosted-by-5g-edge-computing-growth/d/d-id/776851?

Dell’Oro: SD-WAN market grew 45% YoY; Frost & Sullivan: Fortinet wins SD-WAN leadership award

AT&T tops VSG’s U.S. Carrier Managed SD-WAN Leaderboard for 4th year

India’s Trai: Coexistence essential for efficient use of mmWave band spectrum

India’s telecom regulator (Trai) believes that its suggestion of coexistence between terrestrial network operators and satellite service providers in the millimeter wave (mmWave) band of 27.5- 28.5 GHz is essential for the “optimum use of airwaves.”

Trai has recommended the mmWave band – 24.25 GHz to 28.5 GHz – be put to auction. It has recommended a base price of Rs 7 crore a unit.

“Both International Mobile Telecommunications (IMT) and satellite bands can co-exist. That has to happen for the efficient use of spectrum,” said a senior Telecom regulator who did not want to be identified by name.

“The Satellite Earth Station Gateway (for satcom) should be permitted to be established in the frequency range 27.5-28.5 GHz at uninhabited or remote locations on a case-to-to-case basis, where there is less likelihood of 5G IMT services to come up,” the Trai official said.

Trai said that such a move would encourage buyers – both telcos and satcom players and eliminate the possibility of a major chunk of such airwaves to remain idle.

Editor’s Note:

As we’ve noted many times, the WRC 19 specified 5G mmWave frequency arrangements have yet to be standardized in the ITU-R M.1036 revision. Hence, it’s a 5G frequency free for all.

…………………………………………………………………………………………..

Why are telecom companies upset with TRAI despite its proposal to cut spectrum prices by 40%?

The Telecom Regulatory Authority of India (TRAI) this week released recommendations on auction of spectrum, including those likely to be used for offering 5G services. The telecom regulator has suggested cutting prices of airwaves across various bands by 35-40% from its earlier proposed base price. However, the Cellular Operators Association of India, whose members include the three private telcos, Bharti Airtel, Reliance Jio and Vodafone Idea, has expressed disappointment, given the industry’s demand for a 90% reduction in the prices.

The telecom regulator has recommended that all available spectrum in the existing bands — 700 MHz, 800 MHz, 900 MHz, 1800 MHz, 2100 MHz, 2300 MHz, 2500 MHz — should be put up for auction, along with airwaves in new bands such as 600 MHz, 3300-3670 MHz and 24.25-28.5 GHz. In all, more than 1,00,000 MHz of airwaves have been recommended to be put up for auction. The total spectrum on offer at reserve price is valued at about ₹5 lakh crore for 20 years.

For the 3300-3670 MHz band, which has emerged as the prime spectrum for 5G and is likely to be used for deploying 5G in India, the all-India reserve price has been lowered by about 35.5% to ₹317 crore/MHz, from ₹492 crore/MHz recommended earlier. Similarly, the reserve price for the premium 700 MHz band, which saw no takers in the previous auction, has been cut by 40% to ₹3,927 crore/MHz, from about ₹6,568 crore/MHz.

TRAI has determined the reserve price for spectrum bands based on a 20-year spectrum holding period. The reserve price for the increase in spectrum holding period to 30 years would be 1.5x the recommended reserve price for 20 years.

It has also recommended several options for the uptake of Captive Wireless Private Networks (CWPNs), including private networks through telcos, independent isolated network in an enterprise’s premises using telcos’ spectrum, allowing enterprise to take spectrum on lease from telcos or directly from Department of Telecom (DoT) to establish their own isolated captive private networks. TRAI also suggested that enterprises may obtain the spectrum directly from the government and establish their own isolated CWPN.

Given the financial stress in the sector, the government had in November, written to the regulator emphasising the need to strike a balance between generating revenue and the sustainability of the telecom sector in a way that telecom service providers are in good health with sufficient capacities to make regular and substantial capital expenditure for transitioning to 5G technology. It had also highlighted that spectrum lying idle was a waste for the economy.

Further, in the last spectrum auction, held in March 2021, only 37.1% of the spectrum put to auction was acquired by the telecom services providers, largely due to high prices.

“The inputs received by the Authority during the consultation process also point to the need for further rationalisation of the reserve price,” the regulator said in the recommendation running to more than 400 pages.

In its recommendations, the regulator has asserted that the “valuation exercise (and the setting of the reserve prices) is grounded in a techno-economic methodology that is time-tested. The valuation is intended to elicit spectrum prices that encourage buyers to procure radio frequencies in different bands, while at the same time ensuring that bidders are discouraged from collusive behaviour.”

The telecom services providers have via the industry body COAI expressed disappointment with TRAI’s recommendations for auction of 5G spectrum bands.

In a strongly worded reaction, COAI called the recommendation a “step backwards” than forward towards building a digitally connected India.

COAI maintained that the spectrum pricing recommended by TRAI was too high, and noted that throughout the consultation process, the industry had presented extensive arguments based on global research and benchmarks, for significant reduction in spectrum prices. “Industry recommended 90% lower price, and to see only about 35-40% reduction recommended in prices, therefore is deeply disappointing,” it said.

It added that charging a 1.5x price for spectrum for a 30-year period will nullify the relief provided by the Union Cabinet in 2021. The industry body pointed out that by introducing mandatory rollout obligations for 5G networks without factoring the huge cost of such a rollout, TRAI has “delinked itself from reality and is running counter to the Government’s efforts of enhancing ease of doing business”.

On allowing private captive networks for enterprises, COAI argued that TRAI was dramatically altering the industry dynamics and hurting the financial health of the industry rather than improving it. Private networks would be a disincentive for the telecom industry to invest in networks and continue paying high levies and taxes, it contended.

Reference:

Intel quietly acquires private 5G software provider Ananki

Intel has acquired private 5G network provider Ananki, several months after the startup spun out of the non-profit Open Networking Foundation (ONF) to commercialize open-source network technologies.

The acquisition was confirmed Monday on LinkedIn by Guru Parulkar, PhD, who was co-founder and CEO of Ananki and executive director of the Open Networking Foundation.

–>His ONF successor was not disclosed, despite my LI comment enquiring about it.

Intel declined to comment on the Ananki acquisition and instead only confirmed a development that Parulkar said was related: that the ONF’s development team has joined Intel’s Networking and Edge Group. Intel’s statement echoed a quote provided by top Intel networking executive and former Stanford Professor Nick McKeown, PhD in a press release published by the non-profit. McKeown was previously a part-time Intel Senior Fellow who joined the company after its 2019 acquisition of Barefoot Networks, which he co-founded.

“The addition of these developers will support [Intel’s Network and Edge Group’s] mission to drive the shift toward software-defined and fully programmable infrastructure – from the cloud, through the Internet and 5G networks, all the way out to the Intelligent Edge. Intel intends to continue to support and contribute to ONF’s open-source efforts,” an Intel spokesperson said. No financial terms were disclosed.

Ananki provides an open-source, software-defined service that aims to make private 5G networks “as easy to consume as Wi-Fi” for enterprises working on so-called Industry 4.0 projects. This involves connecting a variety of things, including cameras, sensors, robots, and autonomous vehicles, over high-speed networks in various settings, from factories to retail stores.

Ananki has a diverse range of products, including a SaaS-based 5G software stack, small cell radios, SIM cards, and a dashboard for monitoring and analyzing network activity. These are provided through a subscription-based service that charges organizations based on how much 5G coverage they need.

Source: Ananki

If Intel continues to offer Ananki’s products as a subscription service, it would fall in line with the semiconductor giant’s plan to buoy hardware sales with a significant increase in software revenue, as The Register has previously reported. Less than two weeks ago, The Register reported that Intel plans to offer the cloud optimization software of Granulate, another startup it plans to acquire, in Xeon CPU sales pitches.

The Ananki transaction is part of a broader effort by the Open Networking Foundation to support the increasing commercialization of its open-source, software-defined networking technologies, which it originally developed with the financial support of its more than 100 members. Those include Intel as well as several other prominent tech companies, such as AMD, AT&T, Broadcom, Cisco, Google, Microsoft, Nvidia, and T-Mobile.

The Open Networking Foundation said this new commercialization shift involves open-sourcing the entirety of its production-ready software, which includes private 5G, SD-RAN, SD-Fabric and SD-Core technologies that serve as the basis of Ananki’s products. The nonprofit has also made its software-defined broadband and P4 programmable network technologies available as open source.

“We have built platforms that naysayers said were doomed to fail, we’ve proven what’s possible, and today a number of our platforms have been deployed in production networks and others are now production ready and expected to be broadly adopted,” said Parulkar, who is now vice president of software within Intel’s Network and Edge Group.

The ONF seems to want to move development from internal open source teams to member organizations. As such, the nonprofit is transitioning a majority of its development team to Intel’s Network and Edge Group, which is also the new home of Ananki.

References:

https://www.theregister.com/2022/04/12/intel_ananki_5g/

https://www.intel.com/content/www/us/en/edge-computing/what-is-the-network-edge.html

https://networkbuilders.intel.com/events2022/big-5g-event

ONF Enters a New Era Focused on Growing Adoption and Community for its Leading Open Source Projects

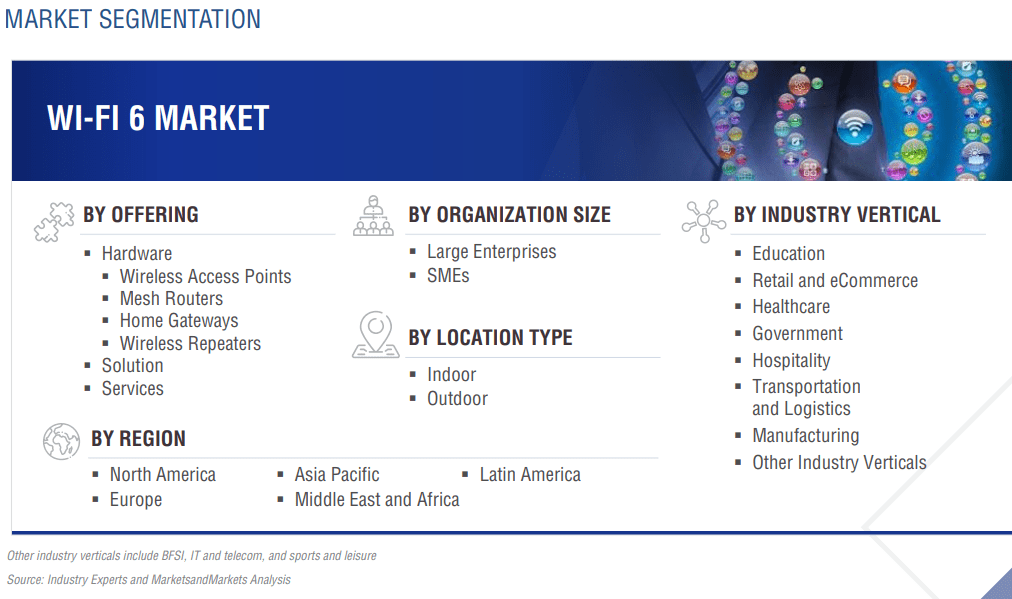

Global Wi-Fi 6 market forecast to grow from $11.5B in 2022 to $26.2B by 2027; CAGR=17.9%

According to a new research report “Wi-Fi 6 Market Global Forecast to 2027,” published by MarketsandMarkets™, the global Wi-Fi 6 market size is expected to grow from $11.5 billion in 2022 to $26.2 billion by 2027, at a Compound Annual Growth Rate (CAGR) of 17.9% during the forecast period.

……………………………………………………………………………………………………………………………………

Editor’s Note:

Wi-Fi 6 is an acronym for the IEEE 802.11ax standard. Prior to the release of Wi-Fi 6, Wi-Fi standards were identified by version numbers ranging from 802.11b to 802.11ac.

…………………………………………………………………………………………………………………….

The managed services Wi-Fi 6 market segment is expected to grow at a higher CAGR than enterprise or consumer Wi-Fi 6 during the forecast period. Managed Service Providers (MSPs) offer are third–party IT service providers that remotely manage the IT infrastructure and systems of clients for backup and recovery of business–critical data. These service providers carry out 24/7 remote monitoring of Wi–Fi 6 networks for their commercial clients. Enterprises opt for managed services to overcome the challenges of budget constraints and technical expertise as managed service providers have skilled human resources, infrastructure, and industry certifications. They offer services to monitor and manage hardware devices and manage the availability and the performance of networks. They also ensure smooth operations and security of networks. The growth of the Wi–Fi 6 market is being driven by the increasing reliance by businesses on the use of IT to improve business productivity, coupled with a continuing rise in demand for specialized MSPs and cloud–based managed Wi–Fi 6 services.

Asia Pacific (APAC) region to record the highest growing region in the Wi-Fi 6 Market. Important countries include Australia, Japan, Singapore, India, China, and New Zealand. The region is expected to witness the fast-paced adoption of Wi-Fi 6 software. The Asia Pacific region is estimated to be the fastest-growing Wi-Fi 6 Market owing to the rise in the adoption of new technologies, high investments for digital transformation, the rapid expansion of domestic enterprises, extensive development of infrastructures, and increasing GDP of various countries. Rapidly growing economies, such as China, Japan, Singapore, and India, are implementing Wi-Fi 6 solutions across multiple business processes to provide effective solutions.

Key and innovative vendors in the Wi-Fi 6 market are:

Cisco Systems (US), Intel Corporation (US), Huawei Technologies (China), NETGEAR (US), Juniper Networks (US), Broadcom (US), Qualcomm Inc. (US), Extreme Networks (US), Ubiquiti Networks (US), Fortinet Inc. (US), Aruba Networks (US), NXP Semiconductors (Netherlands), AT&T (US), Cambium Networks (US), D-Link Corporation (China), Alcatel-Lucent (US), TP-Link (China), MediaTek (China), Telstra (Australia), Murata (Japan), Sterlite Technologies Limited (India), Celeno (Israel), H3C (China), Senscomm Semiconductor (China), XUNISON (Ireland), Redway Networks (UK), VSORA (France), NEWRACOM (US), WILUS Group (South Korea), Federated Wireless (US).

References:

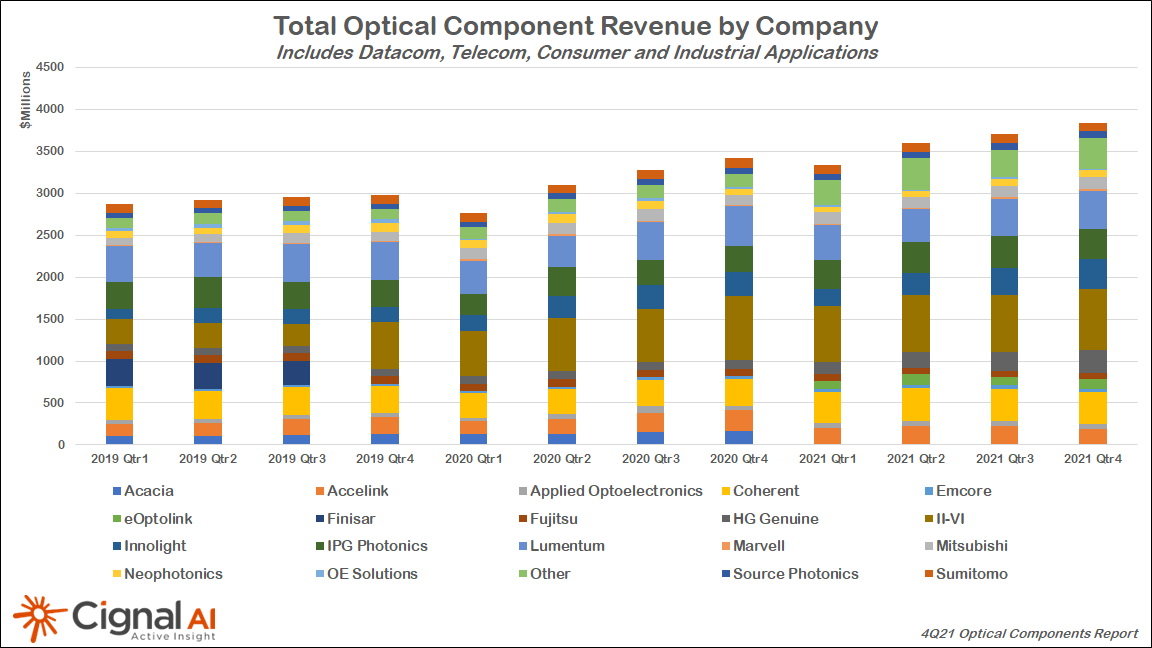

Cignal AI: Datacom optical component revenue +27% to reach $4.7B in 2021

Cignal AI reports that total revenue for optical components, a category that includes optical transceivers, grew 15% in 2021. Components for datacom optical network applications led the way, growing 27% to account for $4.7 billion of the total $14.5 billion component sales registered for the year within the datacom, telecom, industrial, and consumer markets, the market research firm states in its latest Optical Components Report.

A transition by large cloud service providers and some enterprise network operators toward 400-Gbps transmission helped spur this growth. For example, 1.8 million QSFP-DD and OSFP datacom modules shipped during 2021, most of which were DR4 format. Meanwhile, more than 60,000 400G pluggable coherent modules shipped at the same time, with QSFP-DD ZR devices accounting for the majority.

“The transition to 400GbE is well underway, and pluggable coherent 400Gbps technology is revolutionizing the design of the optical networks that connect datacenters,” said Scott Wilkinson, Lead Optical Component Analyst at Cignal AI. “400Gbps speeds will drive spending and bandwidth growth both inside and outside the datacenter in 2022,” Scott added.

More Key Findings from the 4Q21 Optical Components Report:

- Supply chain difficulties limited Telecom optical components market growth the most in 2021. However, the segment is forecast to grow more than 8% in 2022.

- Consumer component revenue for 3D sensing applications was flat YoY as lower-cost components offset higher unit shipments.

- Industrial optical components used for welding and medical applications grew 18% in 2021, following a weak 2020. Following the acquisition of Coherent, II-VI is poised to control over 50% of this market.

- 1.8M QSFP-DD Datacom modules shipped during 2021, most of which were DR4 format. The report also tracks SR4, FR4, and LR4 Datacom transceivers.

- Over 60k 400Gbps pluggable coherent modules shipped last year, the majority of which were QSFP-DD ZR. The report captures the shipment details of all the emerging derivatives of this format, including ZR, ZR+, 0dB ZR+, and CFP2 based ZR+.

- Shipments of 200Gbps coherent CFP2 modules grew 17% to just over 200k units during 2021 as Chinese OEMs ramp this speed (which is less dependent on western technology) for longer distance metro and long haul applications.

References: