MoffettNathanson: AT&T, Verizon set to lose wireless market share to Cablecos; 5G to disappoint – no real use cases

Our esteemed colleague Craig Moffett of MoffettNathanson says that the wireless market is now growing fast enough for both telcos and cablecos to meet their expectations. However, longer term growth that’s much above population growth is clearly unsustainable.

The market research firm has long argued that above-population phone growth in a more or less fully penetrated

market owes to the industry’s willingness to give away free phones in return for additional lines, even when those additional lines aren’t needed and won’t be used.

MoffettNathanson had earlier reported that it expects cablecos to continue to take wireless market share from telcos, bolstered by what is now much more competitive pricing from Comcast.

Craig wrote in a note to clients [we recommend you become one if not truly interested in telecom and/or cable]:

That leaves AT&T and Verizon to bear the brunt of the impact. AT&T has been growing its market share of late, but only because Verizon had been slow to match their aggressive retention offer. Now that Verizon has finally introduced its own, similar, retention offer, the two are likely to be in closer equilibrium… …which is to say, we believe they are likely to now both lose equally. Both companies have guided to low-single digit consolidated revenue growth in the near term, accelerating to the mid-single digits over the coming years.

With continued contraction in the Business Wireline segment all but a given, that means growth in wireless will have to be even faster than that. How? Their guidance seems awfully optimistic to us. We are also projecting significant losses for prepaid as low-priced post-paid plans accelerate pre-paid to post-paid conversions.

Moffett’s revised estimates are for mobile phone subscriber net additions to drop from about 6 million this year to approximately 4.5 million per year in the next few years. That works out to 5.8 million postpaid net adds vs. a loss of 1.3 million prepaid subscribers.

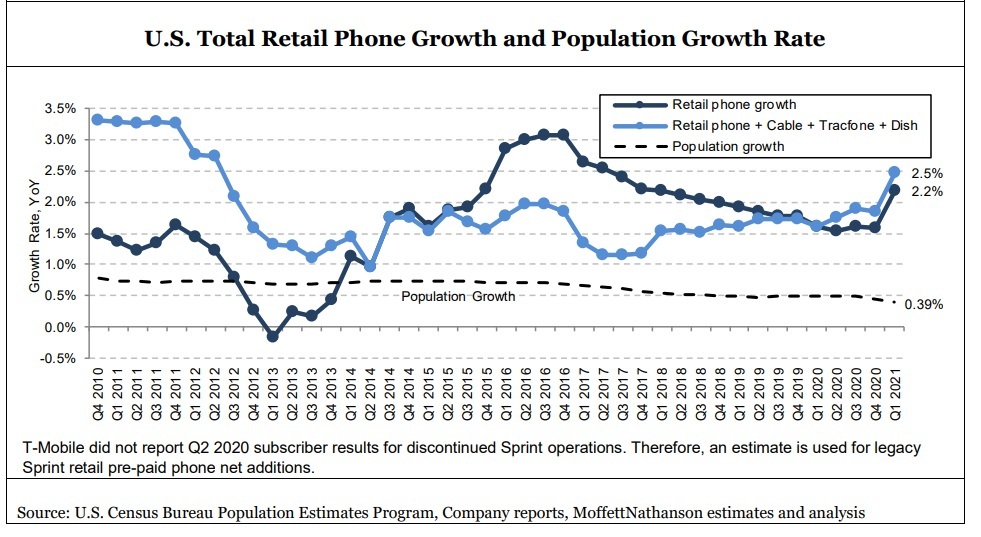

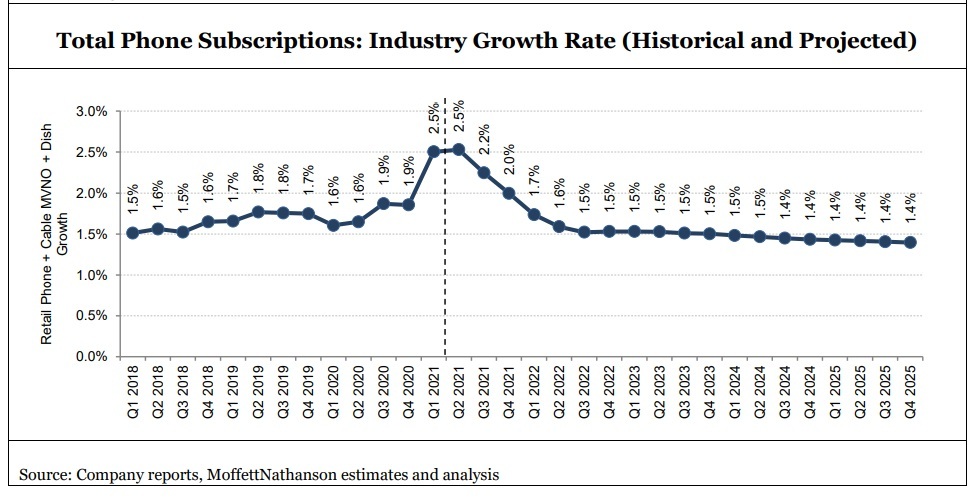

Moreover, the phone subscriber loss for mobile telcos will become more acute if the growth rate recedes from a recent increase of 2.5% year-over-year (a number five times higher than population growth), to more moderate levels – down to about 1.4% by 2025, according to Moffett’s forecast.

Moffett has significantly lowered his estimates for postpaid phone net adds for both AT&T and Verizon. T-Mobile’s sub growth will slow to a smaller degree, reflecting “greater competition from cable operators,” Moffett wrote.

- AT&T: For 2022, Moffett has cut an original forecast of 1.05 million postpaid net adds, to net adds of 505,000. Looking to 2025, he has lowered an original forecast of 888,000 postpaid adds, to 261,000.

- Verizon: For 2022, the analyst cut original expected postpaid adds of 1.03 million to 673,000. For 2025, he now expects Verizon, which does benefit from Comcast’s and Charter’s mobile businesses thanks to the aforementioned MVNO agreements, to pull in postpaid adds of 306,000, versus an original 1.09 million.

- T-Mobile: For 2022, Moffett has reduced his original postpaid net adds of 2.93 million, to 2.73 million. For 2025, he has lowered T-Mobile’s expected postpaid net adds to 2.97 million, versus an original 3.35 million.

Ahead of its national 5G network build, Dish Network remains largely a prepaid operator following its acquisiton of the Boost business from T-Mobile, along with a mix of pre- and post-paid subs coming from last year’s Ting deal. Moffett expects to see a faster decline at Dish’s Boost prepaid business as the company prepared to “compete more vigorously in post-paid.”

The wireless industry hasn’t grown mid-single digits in years, and, with competitive intensity rising, there is little reason to expect that to change. Unfortunately, MoffettNathanson is skeptical (to say the least) that 5G will create incremental revenue streams that fundamentally alter the industry’s growth trajectory. [1.]

Note 1. With URLLC performance requirements not met by either 3GPP Release 16 or IMT 2020 (M.2150), no ITU standard or 3GPP implementation spec for 5G SA core network (which is required for all 5G features like network slicing), no 5G SA roaming, and no ITU-R agreement on 5G mmWave frequencies (revision to M.1036 companion recommendation for M.2150), we think there are very few legitimate use cases for 5G at this time. Furthermore, the network build out costs, especially for hundreds of thousands of small cells with fiber backhaul) will overwhelm any revenue increases and result in a net LOSS for almost all wireless telcos that deploy 5G SA (T-Mobile may be an exception for many reasons).

…………………………………………………………………………………………………………………………………………………………………………….

Craig continues:

And if AT&T and Verizon are both going to be share losers – this seems to us to be a relatively non-controversial assertion – in an industry that barely grows, then how on earth will they achieve faster than mid-single digit growth?

In sum, our calculation suggests industry phone growth – again, to be clear, this is before the minting of unneeded and unused additional lines – should be about 1.2% per year.

With Cablecos taking a bite out of that smaller pie, Craig expects growth of incumbent telco’s – AT&T and Verizon, in particular – to suffer.

References:

MoffetNathanson July 6, 2021 Report: Cable Wireless: The Impact on TelCos (subscribers only)

Nokia and TPG Telecom launch 5G SA 700MHz network in Australia; 700MHz 5G status report

Nokia and TPG Telecom today announced that they have switched on a live 5G standalone (SA) network in Australia on the 700MHz spectrum band – the first time this has happened in the world. Low band 5G coverage at 700MHz, which is the lowest 5G frequency band deployed in Australia with the largest range, will enable TPG Telecom to provide wide outdoor 5G services, as well as deep indoor 5G coverage in urban and suburban areas to its customers.

Under the partnership, Nokia is supplying equipment from its latest ReefShark based AirScale product range including its unique triple band remote radio unit that supports 700, 850 and 900 MHz bands. The unit also supports 3G, 4G and 5G simultaneously across all TPG Telecom’s low-band frequencies. TPG Telecom’s 5G SA service is now successfully activated in parts of Sydney and this means that the operator’s customers will benefit from having 5G available in more places.

Low band 5G goes further outdoor and deeper into buildings than existing 5G deployments and will allow operators like TPG Telecom to bring 5G to even more customers. TPG Telecom may be targeting the Internet of Things (IoT) with its 700MHz service, because that frequency provides a broader coverage area. Australian homes will contain over 47 million smart devices by 2022, estimates the country’s National Science and Technology Council.

………………………………………………………………………………………………………………………………………………………………..

Other network operators are pursuing 700MHz 5G service.

- Japan’s KDDI said in March that it is using Samsung equipment operating in the 700MHz spectrum as part of its goal of covering 90% of Japan’s population by early 2022.

- CBN/China Mobile have put out tender requests bids for 480,397 5G macro base stations in the 700 MHz band. China granted a 5G license for use of the 700 MHz frequency to CBN, the country’s fourth telecoms operator, in June 2019.

- AT&T’s 5G “low band” network mostly uses 850MHz, but its 700 MHz FirstNet public safety network uses hardware “that can be upgraded to 5G with a simple software release.” AT&T has not publicly announce when that might be done.

The 700MHz spectrum provides “deep indoor penetration, a reliable uplink and large coverage,” notes a Nokia white paper. 700Mhz spectrum was referred to as “beachfront property” in 2007-2008.

………………………………………………………………………………………………………………………………………………………………..

Barry Kezik, Executive General Manager Mobile and Fixed Networks at TPG Telecom, said: “We’re excited to be the first network in the world to realize the true potential of low band 5G SA at 700MHz. TPG Telecom’s low band 5G will expand our 5G coverage, supporting our goal of reaching 85% of the population in Australia’s top six cities by the end of the year and changing the way people and things connect to the TPG Telecom 5G network.”

Dr Robert Joyce, Chief Technology Officer at Nokia Oceania, said: “Nokia is proud to support another 5G world first. We have a long-standing partnership with TPG Telecom, and we have jointly developed our unique triple band radio solution specifically for them. Today we get to see the result of that joint effort and collaboration which will deliver premium wide area 5G SA coverage for TPG Telecom and its customers.”

Other 5G networks in Australia: Telstra’s 5G covers 200 towns and cities, and Optus recently announcing it has connected 1 million 5G devices to its network

References:

https://www.rrt.lt/wp-content/uploads/2018/10/Nokia_5G_Deployment_below_6GHz_White_Paper_EN.pdf

Other Resources:

Activate massive 5G capacity with Nokia AirScale

AirScale baseband | Nokia

AirScale Active Antennas | Nokia

AirScale Radio | Nokia

Facebook and Liquid Intelligent Technologies to build huge fiber network in Africa

Facebook Inc. and Africa’s largest fiber optics company, Liquid Intelligent Technologies, are extending their reach on the continent by laying 2,000 kilometers (1,243 miles) of fiber in the Democratic Republic of Congo. The two companies intend to build an extensive long haul and metro fiber network. Apparently, this is part of Facebook’s effort to “connect the unconnected,” especially in 3rd world countries.

The move will make Facebook one of the biggest investors in fiber networks in the region. The cable will eventually extend the reach of 2Africa, a major sub-sea line that’s also been co-developed by Facebook, the two companies said in a July 5th statement.

Facebook will invest in the fiber build and support network planning. Liquid Technologies will own, build and operate the fiber network, and provide wholesale services to mobile network operators and internet service providers. The network will help create a digital corridor from the Atlantic Ocean through the Congo Rainforest, the second largest rainforest after the Amazon, to East Africa, and onto the Indian Ocean. Liquid Technologies has been working on the digital corridor for more than two years, which now reaches Central DRC. This corridor will connect DRC to its neighboring countries including Angola, Congo Brazzaville, Rwanda, Tanzania, Uganda, and Zambia.

The new build will stretch from Central DRC to the Eastern border with Rwanda and extend the reach of 2Africa, a major undersea cable that will land along both the East and West African coasts, and better connect Africa to the Middle East and Europe. Additionally, Liquid will employ more than 5,000 people from local communities to build the fiber network.

“This is one of the most difficult fiber builds ever undertaken, crossing more than 2,000 kilometers of some of the most challenging terrain in the world” said Nic Rudnick, Group CEO of Liquid Intelligent Technologies. “Liquid Technologies and Facebook have a common mission to provide affordable infrastructure to bridge connectivity gaps, and we believe our work together will have a tremendous impact on internet accessibility across the region.”

Liquid Intelligent Technologies is present in more than 20 countries in Africa, with a vision of a digitally connected future that leaves no African behind.

“This fiber build with Liquid Technologies is one of the most exciting projects we have worked on,” said Ibrahima Ba, Director of Network Investments, Emerging Markets at Facebook. “We know that deploying fibre in this region is not easy, but it is a crucial part of extending broadband access to under-connected areas. We look forward to seeing how our fibre build will help increase the availability and improve the affordability of high-quality internet in DRC.”

Facebook has been striving to improve connectivity in Africa to take advantage of a young population and the increasing availability and affordability of smartphones. The social-media giant switched to a predominantly fiber strategy following the failed launch of a satellite to beam signal around the continent in 2016.

About Liquid Intelligent Technologies:

Liquid Intelligent Technologies is a pan-African technology group present in more than 20 countries, mainly in Sub-Saharan Africa. Liquid has firmly established itself as the leading provider of pan-African digital infrastructure with an extensive network covering over 100,000 km. Liquid Intelligent Technologies is redefining network, cloud, and cybersecurity offerings through strategic partnerships with leading global players, innovative business applications, smart cloud services and world-class security on the African continent. Liquid Intelligent Technologies is now a comprehensive, one-stop technology group that provides customized digital solutions to public and private sector companies across the continent under several business units including Liquid Networks, Liquid Cloud and CyberSecurity and Africa Data Centers. For more information contact: Angela Chandy [email protected]

References:

Huawei investment subsidiary buys 40 companies in 3 years to reconstruct semiconductor supply chain

According to financial magazine Caijing (Chinese), Huawei has been building an independent and controllable silicon industrial capability in the last two years as it attempts to rebuild its supply chain. Investments cover virtually every part of the semiconductor industry, including IC design, electronic design automation (EDA) software, packaging and testing, and materials.

On June 23rd, Tianyancha, an enterprise information query platform, revealed that Shenzhen Hubble Investment Partnership (Limited Partnership), a subsidiary of Huawei Technologies Co., Ltd [1.], became a shareholder of Qiangyi Semiconductor (Suzhou) Co., Ltd. The registered capital of the latter increased from 65.943 million yuan to 73.165 million yuan. This is the first company in mainland China that has the ability to independently design vertical probe cards and has achieved mass production of MEMS probe cards.

The probe card is the core component of the chip test link, accounting for 70% of the total cost of the entire test fixture. As a test interface, the probe card will test the bare chip and screen out defective products. For a long time, the semiconductor test probe market has been monopolized by foreign manufacturers.

Note 1. Shenzhen Hubble Investment Partnership (Limited Partnership), which was established in April this year and is an investment institution controlled by Huawei Investment Holdings Co., Ltd., which is the same as Hubble Technology Investment Co., Ltd., which was established in April 2019.

…………………………………………………………………………………………………………………………………………………………………………………

Hubble Technology Investment Co., Ltd., which has been established for three years, has made faster and more detailed investments. In May, it invested in Shenzhen Yunyinggu Technology. On June 23 and 24, it successively invested in Qiangyi Semiconductor and Chongqing Xinjing Special Glass. There are 37 companies in its investment portfolio, of which 34 are related to semiconductors, involving chip design, EDA, testing, packaging, materials and equipment All links.

Before the establishment of Hubble Investment in 2019, Huawei had always followed the long-term principle of not investing in any company. Hubble’s mission is closely linked to the production of Huawei chips via wholly-owned subsidiary HiSilicon. Huawei CEO Ren Zhengfei had insisted the company would not invest in or partner with suppliers in order to ensure it was free to choose the best technologies.

In 2019, after Huawei was sanctioned by the U.S. government, the chips designed by HiSilicon could not find a foundry company (e.g. TMSC, Samsung, etc) that would make those chips for them. Those U.S. sanctions have changed Ren’s stance on investments/acquisitions. So Hubble Investment’s mission was directed at Huawei’s survival needs.

According to market research firm Strategy Analytics report, in the first quarter of 2021, the global smartphone processor market grew by 21% year-on-year, and Huawei HiSilicon’s smartphone processor shipments dropped by 88% compared to the same period last year. The sharp decline in data also indicates the urgency of self-help to make HiSilicon designed chips.

As tech blogger Kevin Xu pointed out: “Habo is a way to find and invest in the best companies in China who can be suppliers and partners, and groom them to be world class quality. That’s why Huawei gives them its business — there’s no better training than serving a real (and big) customer.”

Huawei’s executive director and CEO of consumer business, Yu Chengdong, once admitted that it was a mistake to only choose the field of chip research and development and ignore the asset-heavy chip manufacturing field.

The investment focus has shifted several times as it has built out its prospective supply chain partners, Caijing says. In late 2019 and the first half of 2020, its targets were materials and opto-electronic chip firms. In the latter part of 2020 and early 2021, it shifted to EDA software. In recent months it has targeted advanced equipment. In early June it invested 82 million yuan (US$12.7 million) in Beijing RSLaser Opto-Electronics Technology Co, specialist in light source systems for lithography machines.

Caijing confirmed with many people familiar with the matter that Huawei will build its first wafer fab in Wuhan. It will need a series of related materials, equipment, software, etc., which cannot be researched by Huawei alone. This means that Hubble’s investment in the semiconductor industry chain in the past three years will play an important role, and this will also be a crucial step for Huawei to achieve self-help in the supply chain.

Most of the companies invested by Hubble are in the early stages, and their scale is still far from the leading companies in the industry. Huawei tends to grow together with a company. Therefore, even some technologies that have not yet been commercialized in large quantities will receive investment from Huawei. This is for the controllable layout of Huawei’s industrial chain.

Although the information released to the outside world is extremely limited, many sources indicate that Hubble is closely connected with Huawei’s overall strategic plan. Bai Yi, the chairman and general manager of Hubble Investment, is also the president of Huawei’s Global Financial Risk Control Center and formerly vice president of Huawei’s strategy department.

A Huawei employee revealed to a reporter from Caijing that Hubble’s personnel are simple, “only a few dozen people”, but some of them also belong to Huawei’s strategic department in terms of administrative planning. For a long time before this, the decision-making power of Hubble’s foreign investment was not in the hands of the investment company itself, but was determined by the business department related to the invested company.

A semiconductor investor told a reporter from Caijing that sometimes they will look at projects with Hubble Investment. In many projects, Huawei’s procurement VP will directly participate in investment negotiations. At the same time, some of the invested companies are also Huawei’s upstream suppliers. . Some companies have business cooperation with Huawei, but Hubble has only deepened business cooperation.

The most obvious manifestation of the in-depth business cooperation is the order. In addition to investment, Huawei will also support the invested companies in order.

Take analog chip manufacturer Si Ruipu as an example. In the prospectus disclosed, customer A is the number one customer of Si Ruipu, which accounts for 57.13% of the operating income of the company. According to some related information, it is speculated that this customer A is Huawei. According to the prospectus, Si Ruipu established a cooperative relationship with Huawei in 2016 and obtained the certification of Huawei as a qualified supplier in 2017. In 2019, Hubble Investment, a subsidiary of Huawei, through private placement, became a shareholder of Seripul, and furthered the cooperation, and Huawei became the number one customer of Siripul.

Another example is Can Qin Technology. In 2019, Can Qin Technology became Huawei’s strategic core supplier and the largest supplier of Huawei’s 5G base station filters. Its orders from Huawei accounted for 91.34% of its operating income. In 2020, Hubble Investment will invest in Canqin Technology through equity transfer, with a shareholding ratio of 4.58%.

For small and medium-sized start-ups, the most worrying thing before is that no manufacturers are willing to use the product. Obtaining Huawei’s orders means stable sales revenue and strong ecological support, and it also gives these companies the opportunity for iterative trial and error. Many semiconductor companies in the United States have gradually developed by relying on powerful semiconductor manufacturers.

As previously noted, Huawei was not receptive to domestic suppliers in the early days. In addition to its strong style, Huawei did not give many domestic companies opportunities in the early years of the company. Their suppliers will still be the world’s first-class manufacturers. Today, the situation is quite different, but it gives tech companies in mainland China a rare opportunity.

In addition to orders, if some companies say that products or technologies may not be developed until next year, Huawei will also say that as long as the company can produce products in the future, Huawei promises to use it. This is a strong driving force for China’s independent semiconductor industry chain.

Once Huawei’s wafer fab is completed, its IDM model will go through, and a closed loop of the ecological industry chain will be realized. Now, Huawei is hiring talents in chip manufacturing and equipment. At the same time, Huawei is also paying attention to some domestic material companies, such as photoresist, silicon wafer, gas and other companies, which will serve for the construction of fabs in 2 to 3 years.

Becoming a supplier of Huawei is not an easy task. Huawei has very high requirements on suppliers. Accepting Huawei’s orders is a very energy-consuming task. At the same time, invested companies may also face the choice of giving up other customers. If there is a problem with Huawei, a major customer, the company’s operations will also be strained.

Today, Huawei is planning to build its own wafer fab and adopt the IDM model. If completed, Huawei’s semiconductor ecosystem will gradually form a closed loop. Huawei also hopes that the companies it invests in will be used for its production lines in the next 3 to 5 years.

References:

https://mp.weixin.qq.com/s/16JJ4h5JXckwoowvLe4gYw

OneWeb Launches 36 LEO satellites, 254 in orbit, funding deals & UK coverage too!

OneWeb, the Low Earth Orbit (LEO) satellite communications company, announced the successful launch of another 36 satellites to mark the completion of its ‘Five to 50’ mission.

The latest launch takes OneWeb’s in-orbit constellation to 254 satellites, or 40% of OneWeb’s planned fleet of 648 LEO satellites that will deliver high-speed, low-latency global connectivity. OneWeb intends to make global service available in 2022.

With this major milestone, the company is ready to deliver connectivity across the United Kingdom, Canada, Alaska, Northern Europe, Greenland, and the Arctic Region. Commercial satellite Internet service should be rolled out by the end of 2021 with a global service following next year, the company said.

Service demonstrations will begin this summer in several key locations – including Alaska and Canada – as OneWeb prepares for commercial service in the next six months. Offering enterprise-grade connectivity services, the Company has already announced distribution partnerships across several industries and businesses including with BT, ROCK Network, AST Group, PDI, Alaska Communications and others, as OneWeb expands its global capabilities.

The company continues to engage with telecommunications providers, ISPs, and governments worldwide to offer its low-latency, high-speed connectivity services and sees growing demand for new solutions to connect the hardest to reach places.

The launch of the latest 36 satellites was conducted by Arianespace from the Vostochny Cosmodrom. Liftoff occurred on 1 July at 13:48 BST. OneWeb’s satellites separated from the rocket and were dispensed in 9 batches over a period of 3 hours 52 minutes with signal acquisition on all 36 satellites confirmed.

Image Source: Source: Roscosmos, Space-Center-Vostochny and TsENKi

………………………………………………………………………………………………………………………………………………………………………….

The Prime Minister of the United Kingdom, the Rt. Hon. Boris Johnson, MP, said: “This latest launch of OneWeb satellites will put high-speed broadband within reach of the whole Northern Hemisphere later this year, including improving connectivity in the remotest parts of the UK.

“Backed by the British Government, OneWeb proves what is possible when public and private investment come together, putting the UK at the forefront of the latest technologies, opening up new markets, and ultimately transforming the lives of people around the world.”

Sunil Bharti Mittal, Founder and Chairman of Bharti Enterprises, Executive Chairman of OneWeb, said: “Today’s momentous milestone demonstrates that OneWeb is now a leader in LEO broadband connectivity, serving a wide range of stakeholders across the Northern Hemisphere. This fifth launch amid the unprecedented global pandemic is truly remarkable and I congratulate the management team and fellow shareholders on the success.

“Bharti’s doubling of its investment earlier this week is testament to the commitment to OneWeb’s mission. We now look forward to the next chapter in OneWeb’s story, preparing the company for commercial service in the less than six months to deliver our global connectivity solutions to communities around the world.”

The Rt. Hon. Kwasi Kwarteng, MP, Secretary of State, BEIS, added: “Today’s launch is an exciting milestone in providing some of the world’s most remote locations with fast, UK-backed broadband less than a year since British government investment made this possible. With yet another successful mission, the people of the UK can be proud that this country is at the heart of the latest advances in small satellite technology.

“OneWeb’s coverage across the Northern Hemisphere now puts the United Kingdom at the forefront of the latest developments in Low Earth Orbit technology, and we will capitalise on the company’s unique position within this growing market to build a strong domestic space industry and cement our status as a global science and technology superpower.”

Neil Masterson, OneWeb CEO, said: “This is a truly historic moment for OneWeb, the culmination of months of positive momentum in our ‘Five to 50’ programme, increased investment from our global partners and the rapid onboarding of new customers. We are incredibly excited to start delivering high-speed, low-latency connectivity first to the UK and the Arctic region and to see our network scale over the coming months as we continue building to global service. Thanks to all our incredible partners who have been with us on this journey and are instrumental to making OneWeb’s mission a success.”

……………………………………………………………………………………………………………………………………………………………..

Funding Deals:

OneWeb resumed satellite launches in December 2020 after emerging from bankruptcy protection with $1 billion in equity investment from a consortium of the British government and India’s Bharti Enterprises. It has also received investment from Japan’s Softbank and Eutelsat Communications, and further financing from Bharti. OneWeb said on Tuesday it was fully-funded and had secured $2.4 billion in total.

Earlier this week, OneWeb secured another $500 million in funding, bringing its total funding to $2.4 billion. This new cash injection came from Bharti under a Call Option agreement and is expected to be completed in the second half of this year. According to the BBC, the funding will see Bharti take a 39% stake in OneWeb, making it the company’s biggest shareholder. The UK government, Eutelsat and SoftBank will each own 19.3% of the firm.

“In just a year and during a global pandemic, together we have transformed OneWeb, bringing the operation back to full-scale,” said Bharti Global’s managing director Shravin Mittal. “With this round of financing, we complete the funding requirements.”

The funding announcement came on the heels of news that OneWeb had struck a deal with BT as the UK incumbent operator looks to improve its coverage of more remote areas.

References:

https://www.oneweb.world/media-center/oneweb-completes-its-five-to-50-mission

Webcast playback Launch highlights available View on OneWeb YouTube

Launch Imagery Launch #8 Media Kit

Launch Partner Arianespace and Glavkosmos

Launch Facility Soyuz Launch Complex, Vostochny Cosmodrome

RootMetrics touts 5G performance in Korea while users complain; No 5G SA in Korea!

A new report released by RootMetrics (owned by IHS Markit), shared the 5G performance results in four major South Korean cities in the first half of 2021. Three South Korean operators, KT, LG Uplus and SK Telecom, claim to have provided users with widespread access to 5G, remarkable speeds, and low latency.

According to the report, LG Uplus’s 5G network in Seoul has the fastest speed, the shortest latency, and the best coverage, providing end users with an optimal 5G experience. This is the third consecutive year that LG Uplus has maintained their position as a 5G industry leader. Of note, the report stated that LG Uplus made the most efficient use of the spectrum, despite only 80 MHz of 5G bandwidth, less than that of KT and SK Telecom, with 100 MHz each.

South Korea’s 5G availability and user speed, which are the two key components of a consumer’s 5G experience, are ahead of most of the rest of the world. RootMetrics considers LG Uplus in Seoul to be the best 5G network based on the 5G report results in four cities (see image below):

- Best 5G coverage: LG Uplus provides coverage in all scenarios, including outdoor, indoor, high-speed railway, metro, hot spots etc., with 95.2% 5G availability. That means the network is providing ubiquitous 5G access, far more than cities like New York and London city.

- Fastest 5G speed: The median speed of 5G users is 640.7 Mbps, which is much higher than in other cities with 5G access.

LG Uplus has built 5G networks with high-bandwidth massive MIMO, deployed 64TRx Massive MIMO at scale for outdoor scenarios and LampSite+distributed Massive MIMO for indoor scenarios to build “Everywhere” Massive MIMO. In addition, 5G AI+ has also been introduced. Together these technology build the strongest and most intelligent 5G network, according to RootMetrics.

The report says that the performance of the other two major operators in South Korea is also impressive. The 5G availability of the three operators has increased to over 93% and the median speed is over 461 Mbps, which means end users can access the 5G network no matter their location to enjoy the ultimate 5G experience. RootMetrics can’t help praise: South Korea is winning the global 5G race, with availability and speeds that are far, far ahead of others.

“5G is becoming the foundation of our connected communities and as important a piece of infrastructure as is water, roads, or electricity. We’ve tested performance in South Korea over many years. Our results continue to show that South Korean operators have taken a leading position in delivering the type of 5G experience that can help fuel new consumer and business activity,” said Patrick Linder, Chief Marketing Officer at RootMetrics. “As 5G continues to expand across the globe, the implementation strategies and performance seen in South Korea have set an impressive standard for other operators to follow.”

Reference:

https://rootmetrics.com/en-US/content/5g-in-south-korea-1H-2021

………………………………………………………………………………………………………………………………………………………………………

In sharp contrast to RootMetrics’ glowing praise for 5G in South Korea, many 5G customers there are extremely dissatisfied as per this Light Reading article:

Their gripe is that 5G is little better than 4G in terms of speed, while coverage is annoyingly patchy. Worst of all, they’re locked into much more expensive two-year contracts when compared to LTE tariffs.

Rather than just put up with their 5G lot, this unhappy crew is intending to take part in a collective lawsuit and seek compensation of at least KRW1 million ($890) each. South Korean law firm Joowon is spearheading the legal action.

“Considering that monthly 5G plans are around 50,000 won more expensive than 4G LTE plans, we expect around 1 million won in compensation for users subscribed to two-year plans,” explained Kim Jin-wook, a Joowon lawyer.

Kim indicated that South Korea’s “big three” had a case to answer. They initially advertised 5G download speeds as being 20 times faster than 4G LTE, when they first came out of the 5G traps in April 2019, but a government report last year apparently found that average 5G download speeds were just four times faster than 4G.

Korea Bizwire points out that the Korea National Council of Consumer Organizations, a consumer advocacy group, recommended last October that carriers pay as much as KRW350,000 ($309) in compensation to users who filed for mediation over what they saw as a mediocre 5G service.

As of January the number of 5G subscribers in South Korea was just shy of 13 million, which was less than 20% of all mobile network users in the country.

5G customer dissatisfaction is a worldwide phenomenon. In May, Reuters reported that “about 70% of (global 5G) users are dissatisfied with the apps and services bundled with their 5G plans, according to a study carried out by Ericsson ConsumerLab in 26 markets around the world.

“While early adopters are pleased with 5G network speeds, they are already expressing dissatisfaction with a lack of bundled new and innovative apps and services, which they feel were promised in the marketing pitch for 5G,” Ericsson said.

“Service providers need to offer exclusive content and services that could differentiate a 5G experience from 4G and promote a sense of novelty and exclusivity,” Ericsson said.

……………………………………………………………………………………………………………………………………………………………

Finally, none of the South Korea carriers have deployed a 5G SA/Core network, despite Samsung’s bogus claim of November 4, 2020: “Samsung and KT announced they have successfully deployed Korea’s first 5G Standalone (SA) and Non-Standalone (NSA) common core in KT’s commercial network. KT will commercially launch its SA network when 5G SA-capable devices become available in the market.”

Well, that hasn’t happened yet, so KT’s 5G SA network has yet to be deployed! The major benefits of 5G, like network slicing, automation, secure communications, new QoS model, etc. are ONLY realized via a 5G SA core network.

The 5G SA architecture connects the 5G Radio (base station or small cell) directly to the 5G core network, and the control signaling does not depend on the 4G network as it does in 5G NSA. The full set of 5G Phase 1 services (defined in 3GPP Release 15) are ONLY supported in 5G SA mode.

GSMA has identified 12 5G SA networks worldwide. None are in South Korea:

At least 12 operators in nine countries/territories are understood to have launched (or close to launch) public 5G SA networks:

- China Mobile, China Telecom and China Unicom have all launched 5G SA networks (China Telecom and China Unicom sharing some of the network construction). China Mobile has deployed or upgraded 400,000 base stations to support standalone services, while China Telecom announced its service launch covering more than 300 cities.

- T-Mobile in the USA has launched 5G SA nationwide using spectrum at 600 MHz.

- RAIN has launched 5G SA in parts of Cape Town in South Africa to support 5G FWA services and DIRECTV in Colombia has launched 5G SA for FWA in parts of Bogota. China Mobile Hong Kong announced the launch of 5G SA in late 2020.

- Mass Response (Spusu) has launched a limited network in Austria and is progressing with a wider regional deployment and, most recently.

- Telefonica and Vodafone have launched 5G SA networks in Germany.

- STC has announced a commercial launch in Kuwait.

- Singtel has announced its launch in Singapore (with other operators in Singapore expected to go live very soon).

- In Saudi Arabia, STC has announced that it has activated its 5G SA networks, although GSA is waiting for confirmation of availability of commercial services for customers before classifying its 5G SA networks as launched. Also, in Saudi Arabia, ITC has announced a soft launch of a 5G SA network.

- In Australia, Telstra has deployed a 5G core network and has stated it is ready to launch its 5G SA network once a sufficient range of suitable devices is available in the Australian market.

…………………………………………………………………………………………………………………………………………………………………….

Qualcomm’s designing custom CPU’s for dominance in laptop markets; CEO: “We will go big in China”

Qualcomm’s new CEO believes that by next year his company will supply CPU chips for laptop makers competing with Apple. Last year, the Cupertino, CA based company introduced laptops using a custom-designed central processor chip that boasts longer battery life. Longtime processor suppliers Intel Corp and Advanced Micro Devices have no chips as energy efficient as Apple’s.

Qualcomm Chief Executive Cristiano Amon told Reuters on Thursday he believes his company can have the best chip on the market, with help from a team of chip architects who formerly worked on the Apple chip but now work at Qualcomm. In his first interview since taking the top job at Qualcomm, Amon also said the company is also counting on revenue growth from China to power its core smartphone chip business despite political tensions.

“We will go big in China,” he said, noting that U.S. sanctions on Huawei Technologies Co Ltd (HWT.UL) give Qualcomm an opportunity to generate a lot more revenue.

Amon said a cornerstone of his strategy comes from a lesson learned in the smartphone chip market: It was not enough just to provide modem chips for phones’ wireless data connectivity. Qualcomm also needed to provide the brains to turn the phone into a computer, which it now does for most premium Android devices.

Now, as Qualcomm looks to push 5G connectivity into laptops, it is pairing modems with a powerful central processor unit, or CPU, Amon said. Instead of using computing core blueprints from longtime partner ARM Ltd, as it now does for smartphones, Qualcomm concluded it needed custom-designed chips if its customers were to rival new laptops from Apple.

As head of Qualcomm’s chip division, Amon this year led the $1.4 billion acquisition of startup, whose ex-Apple founders help design some those Apple laptop chips before leaving to form the startup. Qualcom will start selling Nuvia-based laptop chips next year.

“We needed to have the leading performance for a battery-powered device,” Amon said. “If ARM, which we’ve had a relationship with for years, eventually develops a CPU that’s better than what we can build ourselves, then we always have the option to license from ARM.”

ARM is in the midst of being purchased by Nvidia Corp for $40 billion, a merger that Qualcomm has objected to with regulators.

Amon said Qualcomm has no plans to build its own products to enter the other big market for CPUs – data centers for cloud computing companies. But it will license Nuvia’s designs to cloud computing companies that want to build their own chips, which could put it in competition with parts of ARM.

“We are more than willing to leverage the Nuvia CPU assets to partner with companies that are interested as they build their data center solutions,” Amon said.

Smartphone chips accounted for $12.8 billion of its $16.5 billion in chip revenue in its most recent fiscal year. Some of Qualcomm’s best customers, such as phone maker Xiaomi Corp are in China.

Qualcomm is counting on revenue growth as its Android handset customers swoop in on former users of phones from Huawei, which was forced out of the handset market by Washington’s sanctions.

Kevin Krewell, principal analyst at TIRIAS Research, called it a “political minefield” due to rising U.S.-China tensions. But Amon said the company could do business as usual there.

“We license our technology – we don’t have to do forced joint ventures with technology transfers. Our customers in China are current with their agreements, so you see respect for American intellectual property,” he said.

Another major challenge for Amon will be hanging on to Apple as a customer. Qualcomm’s modem chips are now in all Apple iPhone 12 models after a bruising legal battle. Apple sued Qualcomm in 2017 but eventually dropped its claims and signed chip supply and patent license agreements with Qualcomm in 2019. Apple is now designing chips to displace Qualcomm’s communications chips in iPhones.

“The biggest overhang for Qualcomm’s long-term stock multiple is the worry that right now, it’s as good as it gets, because they’re shipping into all the iPhones, but someday, Apple will do those chips internally,” said Michael Walkley, a senior analyst at Canaccord Genuity Group.

Amon said that Qualcomm has decades of experience designing modem chips that will be hard for any rival to replicate and that the void in the Android market left by Huawei creates new revenue opportunities for Qualcomm.

Another challenge for Amon, a gregarious executive who is energetic onstage during keynote presentations, will be that Qualcomm is not well known to consumers in the way that Intel or Nvidia are, even in Qualcomm’s hometown.

“I flew into San Diego and got an Uber driver at the airport and told him I was going to Qualcomm. He said, ‘You mean the stadium?'” Krewell said, referring to the football arena formerly home to the San Diego Chargers.

Amon has started a new branding program for the company’s Snapdragon smartphone chips to try to change that. “We have a mature smartphone industry today. People care what’s behind the glass,” he said.

References:

https://www.reuters.com/technology/qualcomms-new-ceo-eyes-dominance-laptop-markets-2021-07-01/

China Broadcasting Network tender for 480,400 5G macro base stations & multi-band antenna products

China Broadcasting Network (CBN), China’s fourth mobile operator, has issued a tender for the radio access portion of its national 5G network via its network partner China Mobile. Previously, the two companies entered into a 5G Network Co-construction and Sharing Collaboration Agreement along with other 5G collaborations.

The CBN/China Mobile tender requests bids for 480,397 5G macro base stations in the 700 MHz band which is roughly equivalent to the number of 2.6 GHz base stations already deployed by China Mobile. Based on past big 3 (China Mobile, China Telecom, China Unicom) tender results, Huawei and ZTE are expected to win approximately 85% of the business. That would leave only 15% for Ericsson or other well known 5G base station vendor, but probably NOT Nokia which was shut out of the last China 5G contract awards.

China granted a 5G license for use of the 700 MHz frequency to CBN, the country’s fourth telecoms operator, in June 2019. The other three obtained 5G licenses for 2.6 GHz and 4.9 GHz. Founded in 2014, Beijing-based CBN is the most recently established, so lacks users and infrastructure, which is partly why it is cooperating with China Mobile on 5G.

Concurrently, a bidding announcement for the centralized procurement of multi-band (including 700MHz) antenna products was also issued. This project is a centralized bidding project. The purchased products are multi-band (including 700M) antenna products. There are three types of 6 antennas: 4+4+4 antennas (700/900/1800MHz), divided into ordinary gain and high gain; 4+4+ 4+8 antennas (700/900/1800/FA), divided into long and short models; single 4 antenna (700MHz), divided into normal gain and high gain. The procurement scale is approximately 1.74 million antennas, of which 4.448 antennas require 1.14 million antennas, and the remaining model antennas such as 444 are 600,000 antennas.

China Mobile will complete the deployment of 700MHz 400,000 stations within this year. In the first half of 2022, they plan to open 480,000 seats and fully support 5G broadcasting services. Within two years full network coverage will be achieved.

There are now nearly 100 5G mobile phones supporting the 700MHz frequency band, covering high, middle and low end consumer groups. China Mobile earlier made it clear that in 2021, it will promote the joint construction and sharing of 700MHz to achieve 700MHz commercialization. It requires: starting from March 1, 2021, terminals of 4,000 yuan and above must support 700MHz; from October 1, 2021, The newly added terminal must support 700MHz.

The tender is a milestone for the China telecom sector, marking the start of the rollout of the new entrant, who is also the first network operator not linked to the Ministry of Industry and IT. CBN said the network will be configured around video and streaming to serve its existing cable TV customer base and to provide differentiation from the incumbent telcos. The rollout will include 5G mobile broadcasting capabilities, including 3,000 transmission towers.

The 700MHz frequency band is part of the wider ultra-high frequency (UHF) band used previously for terrestrial broadcasting. The 700MHz frequency band will improve connectivity in rural areas thanks to its ability to support better coverage in open spaces. Moreover, with its wide territorial reach and good penetration in buildings, the 700MHz band will help service providers meet the rising consumer demand for audiovisual content and other broadband services over wireless networks.

Li Shuang, Deputy Director of Department of Technology Development, CBN, said: “CBN always extensively cooperates with domestic and international industry partners with innovation-driven, open and win-win concepts in mind, promoting continuous maturation of the global industry chain of 5G 700MHz network and committed to building a high-quality nationwide 5G network in China. The successful test by Ericsson based on the 3GPP 5G specifications contributed by CBN, including the 700MHz technology standard and n28 band terminal enhancements standard, has improved the 700MHz network capability efficiently, which is of great significance to the innovation of low-band 5G networks in various scenarios.”

…………………………………………………………………………………………………………………………………………………………………………….

CBN and China Mobile are reportedly promising to deploy 400,000 base stations this year.

Robert Clark of Light Reading wrote, “That seems unlikely – it took the incumbent operators nearly two years to reach that mark – but it seems certain that CBN will offer its first commercial services late this year or early 2022. The bid documents state that the tender is fully funded, a positive sign for the cash-strapped CBN.

As Rakuten in Japan is learning, it is not easy to compete against big legacy players each with a large installed base and deep marketing channels. Even in the capital markets, CBN may find itself competing again with its industry rivals.”

References:

http://www.cctime.com/html/2021-6-30/1579416.htm

https://www.lightreading.com/asia/cbn-issues-massive-5g-base-station-tender/d/d-id/770623?

LF Networking 5G Super Blue Print project gets 7 new members

Overview:

LF Networking (LFN), which facilitates collaboration and operational excellence across open source networking projects, today announced seven new member organizations and one associate member have joined the community to collaborate on the 5G Super Blue Print initiative.

The 5G Super Blueprint project covers RAN, Edge, and Core and enables solutions for enterprises and verticals, large institutional organizations, and more. While Networking provides platforms and building blocks across the networking industry that enable rapid interoperability, deployment, and adoption. Participation in this nexus for 5G innovation and integration is open to anyone.

The new members are:

AQSACOM, a leader in Cyber Intelligence software solutions for communications service providers (CSPs) and law enforcement agencies (LEAs);

Radtronics, which provides secure and powerful private wireless network for Maximum Productivity with new applications and services, through Outcome based and cost efficient solutions enabled by strong innovation;

Turnuium, which enables channel partners to connect people, data, and applications through its turnkey multi-carrier managed SD-WAN;

SEMPRE, which secures 5G for critical infrastructure by moving compute to the edge and leveraging military-grade technology—the only HEMP-hardened 5G gNODEB with Edge; and

Wavelabs, a new-age technology company for the Digital, Cognitive & Industry 4.0 Era have joined LFN at the Silver level. New Associate members include: the Oman government’s Ministry of Transportation, Communications & Information Technology;

ICE Group’s (state telecommunications and energy operator of Costa Rica)

ANTTEC (ICE Group’s main union of technicians and engineers); and

High School Technology Services, which offers coding and technology training to students and adults, have joined as Associate members.

“As the center platform for enabling open source 5G building blocks, collaboration and integration is more important than ever for LFN, amplified by our recent developer event in early June,” said Arpit Joshipura, general manager, Networking, Edge and IoT, the Linux Foundation. “This impressive roster of new members across intelligence, government, enterprise and more are welcome additions to the LFN community. We look forward to continued collaboration that enables rapid interoperability, deployment, and adoption of 5G across the ecosystem.”

Leveraging the convergence of major initiatives in the 5G space, and building on a long-running 5G Cloud Native Network demo work stream, LF Networking is leading a community-driven integration and proof of concept involving multiple open source initiatives in order to show end-to-end use cases demonstrating implementation architectures for end users.

In April, the Linux Foundation and the World Bank launched an online course: 5G and Emerging Technologies for Public Service Delivery & Digital Economy Operations – Fundamentals of 5G Networks: Implications for Practitioners. The course is now available on the World Bank’s Open Learning Campus here. Aimed at decision makers and development practitioners, the course provides an introduction to open source and the critical role it plays in today’s networks.

ONE Summit:

Learn more about the 5G Super Blue Print during the Open Networking & Edge (ONE) Summit, the ONE event for end to end connectivity solutions powered by open source and enables the collaborative development necessary to shape the future of networking and edge computing. Taking place October 11-12, 2021 in Los Angeles, Calif., Registration will open soon.

New Member Support:

“With the dramatic growth of Private Wireless LTE and 5G networks over the coming years, the Open Source community will play a transformational role, which is the reason we’re joining the Linux Foundation Networking,” said Peter Lejon, co-founder of RADTONICS AB. “5G technology will have a huge impact on our future, driving positive changes for all of us. With enterprise and regional operators procuring solutions direct from the solutions providers, initiatives like 5G Super Blueprint and Magma Packet Core will be instrumental in serving a rapidly developing market that will include the next billion users on their journey of capturing value through digitalization. We believe that through Open Source and by working together, we can further accelerate the current pace of innovation and development. Change will never be this slow again,” added Lejon.

Marcus Owenby, SEMPRE’s Global CTO, affirmed “SEMPRE’s support for 5G Super Blueprint will enable enterprise and government organizations to leverage open source technology, while also securing 5G using military-grade technology purpose-built to protect critical infrastructure.”

“Wavelabs.ai is an ardent proponent of the ‘OPEN X’ network vision. We work with the entire ecosystems of clients & partners as an engaged, committed, and collaborative partner to realize 5G open and disaggregated ‘White Box’ network as a reality” said Mansoor Khan, CEO of Wavelabs. “LF Networking open-source 5G initiatives address major opportunities today and tomorrow. We believe this partnership will strengthen Wavelabs mission in accelerating the Journey to Future Connectivity by offering the unique blend of next-generation Digital, Cognitive, and Network technology services and solutions”

Resources

AT&T 5G SA Core Network to run on Microsoft Azure cloud platform

AT&T will run its 5G SA Core network on Microsoft’s Azure public cloud computing platform. Microsoft AZURE, which is the second largest cloud computing provider by revenue behind rival Amazon Web Services, has been building out specific cloud computing offering to attract carriers. AT&T is Microsoft’s first major deal in the 5G SA Core network space.

The two giant companies said that Microsoft will purchase software and intellectual property developed by AT&T to help build out its offerings for carriers. The companies did not disclose the terms of the deals, but said that Microsoft will make job offers to several hundred AT&T Network Cloud engineers.

Microsoft will use AT&T’s software and IP to grow its telecom flagship offering, Azure for Operators. Microsoft is acquiring AT&T’s carrier-grade Network Cloud platform technology, which AT&T’s 5G core network (when completed) will run on.

The companies disclosed a few key details about their new deal, but did not provide any firm numbers or any financial arrangements/guidance:

- Microsoft will “assume responsibility for both software development and deployment of AT&T’s Network Cloud immediately,” according to the companies, and will transition AT&T’s existing network cloud operations into Azure over the next three years. Eventually, all of AT&T’s mobile network traffic will run over Microsoft’s Azure.

- The effort will start with AT&T’s 5G core, but will eventually include virtually all of the company’s network operations, including its 4G core.

- Microsoft will be the company to certify all of AT&T’s software-powered network operations for inclusion in the AT&T network. That will include software from other vendors. AT&T has not yet named its 5G core network vendors.

- Microsoft will acquire AT&T’s Network Cloud technology – including its AT&T engineering and lifecycle management software – and its cloud-network operations team. The companies did not disclose exactly how many AT&T employees that transaction might cover, but an AT&T official suggested it will be in the “low hundreds.” Microsoft will then incorporate AT&T’s intellectual property into its Azure for Operators offering, which is for sale to other 5G network operators.

- Microsoft and AT&T did not provide the logistics of their deal, including exactly how many Azure computing locations might be necessary to power AT&T’s network. It’s an important issue considering AT&T’s cellular network spans an estimated 70,000 cell towers across the country, and the operation of the radios on top of those towers might eventually be handled by programs running inside of Microsoft’s cloud. A top Microsoft executive involved in the deal told Light Reading that Microsoft’s Azure software will be installed into some of AT&T’s existing computing locations. Several of those compute server locations are staffed by AT&T technicians.

- AT&T said the company plans to continue to run its network workloads inside of its own data centers and facilities. However, AT&T added that the deal today is focused on AT&T’s 5G core network and that the companies might explore additional elements of the network such as Open Radio Access Network (O-RAN) technology over the course of the agreement.

…………………………………………………………………………………………………………………………………………………

Sidebar: 5G SA Core networks to run on cloud service provider platforms:

- In late April, Dish Network made a similar deal to have Amazon run its 5G core network on AWS.

- In late May, Telefónica said it had validated AWS Outposts as option for 5G SA core deployment in Brazil.

- Earlier this week, TIM said it was building its 5G SA Core network on “Google’s cloud solutions” (whatever that means?)

Do you think the cloud service providers will essentially take over the implementation, operations, and maintenance of 5G SA Core networks, especially since they will likely all be “cloud native.” Please post a comment in the box below this article to express your opinion and why. Thanks!

………………………………………………………………………………………………………………………………………………………………………

“This deal is not exclusive, so I fully expect Azure will try to assert itself as the telecom cloud provider for many carriers around the world,” said Roger Entner of Recon Analytics LLC.

“It’s the first time a Tier One operator has trusted their existing consumer subscriber base to hyper-scaler technology,” Microsoft’s Shawn Hakl, VP of the company’s 5G strategy, told Light Reading. Before joining Microsoft in 2020, Hakl was a longtime Verizon executive.

The deal follows a $2 billion agreement in 2019 in which AT&T said it would start using Microsoft’s cloud for software development and other tasks. At that time, AT&T said it would continue to run its core networking functions in its own private data centers.

Andre Fuetsch, AT&T’s chief technology officer, said that shifting to a public cloud vendor will let AT&T take advantage of a larger ecosystem of software developers who are working on technologies such as wringing more use out of pricey 5G spectrum or creating new features for users. “That’s what we at AT&T want to do, and we think working with Microsoft gives us that advantage,” Fuetsch told Reuters in an interview.

“AT&T has one of the world’s most powerful global backbone networks serving hundreds of millions of subscribers. Our Network Cloud team has proved that running a network in the cloud drives speed, security, cost improvements and innovation. Microsoft’s decision to acquire these assets is a testament to AT&T’s leadership in network virtualization, culture of innovation, and realization of a telco-grade cloud stack,” said Andre Fuetsch, executive vice president and chief technology officer, AT&T. “The next step is making this capability accessible to operators around the world and ensuring it has the resources behind it to continue to evolve and improve. And do it securely. Microsoft’s cloud expertise and global reach make them the perfect fit for this next phase.”

Microsoft intends to use the newly acquired technology – plus the experience gained helping AT&T run the network – to build out a product it calls Azure for Operators, which it will use to pursue 5G core network business from telecommunications companies in the 60 regions of the world where it operates.

https://azure.microsoft.com/en-us/industries/telecommunications/

https://about.att.com/story/2021/att_microsoft_azure.html

https://www.reuters.com/business/media-telecom/att-run-core-5g-network-microsofts-cloud-2021-06-30/

https://www.lightreading.com/the-core/atandt-to-offload-5g-into-microsofts-cloud/d/d-id/770600?