“SK Wonderland at CES 2024;” SK Group Chairman: AI-led revolution poses challenges to companies

On Tuesday at CES 2024, SK Group [1.] displayed world-leading Artificial Intelligence (AI) and carbon reduction technologies under an amusement park concept called “SK Wonderland.” It provided CES attendees a view of a world that uses the latest AI and clean technologies from SK companies and their business partners to a create a smarter, greener world. Highlights of the booth included:

- Magic Carpet Ride in a flying vehicle embedded with an AI processor that helps it navigate dense, urban areas – reducing pollution, congestion and commuting frustrations

- AI Fortune Teller powered by next-generation memory technologies that can help computers analyze and learn from massive amounts of data to predict the future

- Dancing Car that’s fully electric, able to recharge in 20 minutes or less and built to travel hundreds of miles between charges

- Clean Energy Train that’s capable of being powered by hydrogen, whose only emission is water

- Rainbow Tube that shows how plastics are finding a new life through a technology that turns waste into fuel

Note 1. SK Group is South Korea’s second-largest conglomerate, with Samsung at number one.

SK’s CES 2024 displays include participation from seven SK companies — SK Inc., SK Innovation, SK Hynix, SK Telecom, SK E&S, SK Ecoplant and SKC. While the displays are futuristic, they’re based on technologies that SK companies and their global partners have already developed and are bringing to market.

SK Group Chairman Chey Tae-won said that companies are facing challenges in navigating the transformative era led by artificial intelligence (AI) due to its unpredictable impact and speed. He said AI technology and devices with AI are the talk of the town at this year’s annual trade show and companies are showcasing their AI innovations achieved through early investment.

“We are on the starting line of the new era, and no one can predict the impact and speed of the AI revolution across the industries,” Chey told Korean reporters after touring corporate booths on the opening day of CES 2024 at the Las Vegas Convention Center in Las Vegas. Reflecting on the rapid evolution of AI technologies, he highlighted the breakthrough made by ChatGPT, a language model launched about a year ago, which has significantly influenced how AI is perceived and utilized globally. “Until ChatGPT, no one has thought of how AI would change the world. ChatGPT made a breakthrough, and everybody is trying to ride on the wave.”

SK Group Chairman Chey Tae-won speaks during a brief meeting with Korean media on the sidelines of CES 2024 at the Las Vegas Convention Center in Las Vegas on Jan. 9, 2024

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

SK Hynix Inc., SK Group’s chipmaking unit, is one of the prominent companies at CES 2024, boasting its high-performance AI chips like high bandwidth memory (HBM). The latest addition is the HBM3E chips, recognized as the world’s best-performing memory product. Mass production of HBM3E is scheduled to begin in the first half of 2024.

SK Telecom Co. is also working on AI, having Sapeon, an AI chip startup under its wing. Chey stressed the importance of integrating AI services and solutions across SK Group’s diverse business sectors, ranging from energy to telecommunications and semiconductors. “It’s crucial for each company to collaborate and present a unified package or solution rather than developing them separately,” Chey said. “But I don’t think it is necessary to set up a new unit for that. I think we should come up with an integrated channel for customers.”

SK Telecom and Deutsche Telekom are jointly developing Large Language Models for generative AI to be used by telecom network providers.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

References:

https://en.yna.co.kr/view/AEN20240110001900320#

https://eng.sk.com/news/ces-2024-sk-to-showcase-world-class-carbon-reduction-and-ai-technologies

SK Telecom inspects cell towers for safety using drones and AI

SK Telecom and Deutsche Telekom to Jointly Develop Telco-specific Large Language Models (LLMs)

SK Telecom and Thales Trial Post-quantum Cryptography to Enhance Users’ Protection on 5G SA Network

Neos Networks launches 10Gbps Managed Dedicated Internet Access (DIA)

UK business network operator Neos Networks today announced a major upgrade of its Managed Dedicated Internet Access (Managed DIA) service to provide capacities up to 10Gbps as standard. Previously available up to 1Gbps, the upgrade provides a fully managed, enterprise-grade fibre solution for UK organisations grappling with ever-increasing bandwidth demand and the need for reliable access to the internet.

The latest upgrade means Neos Networks customers across the UK can access the same bandwidths across its Wires-only DIA, and Managed DIA variants, with a clearer upgrade path. The upgrade also promises to simplify the hardware and support available for customers. Neos Networks manages both the maintenance and break/fix of the router, meaning the customer’s network or IT team can focus on other areas of their business.

Neos Networks’ extensive network infrastructure underpins the UK’s digital economy, powering the UK’s critical infrastructure, and connecting public services, telcos and enterprises of all shapes and sizes. This latest upgrade gives such organisations more flexible and scalable options to meet their unique connectivity needs. Devices are monitored and managed 24/7 by Neos, and the service is also optimised for reduced energy consumption and rack space when combined with services such as Neos Networks access tails.

The UK’s connectivity demands are continuously increasing, spurred by ongoing digital transformation and new technology like 5G, IoT and artificial intelligence. In 2020, Neos Networks launched a 10Gbps Wires-only DIA service in readiness for this increasing customer demand. This latest upgrade of Managed DIA means customers who are currently making use of a large number of 1Gbps circuits can look to scale their bandwidth as part of the same service. Neos is making this easier than ever and is poised to deliver across UK telcos, enterprises and critical and national infrastructure.

Mark Charlesworth, Director of Product, at Neos Networks, said: “Our continued investment in our business internet proposition means Neos Networks is now able to provide the same scalable bandwidth across a range of different service models throughout the UK. This provides a much-simplified upgrade path for customers with increasing bandwidth requirements, delivering the level of service they need in a flexible and scalable way”.

Through Managed DIA, Neos Networks steps closer to the customer’s environment, beyond a traditional wholesale fibre infrastructure role. This includes more proactive monitoring, and advanced analytics to support network maintenance and availability. With the impact of the loss of service only becoming more critical for organisations across the UK, Neos Networks’ MPLS core network also ensures that services via Managed DIA are highly resilient.

Neos Networks offers a Managed DIA service supported by 24/7 technical assistance, providing businesses with a broad selection of last-mile connectivity providers, along with diverse and resilient options. The strength of this service lies in Neos Networks’ extensive network coverage, which includes more than 676 high-speed Ethernet Points of Presence across the nation. This expansive reach enhances the quality of its DIA services, ensuring businesses have reliable access. Importantly, all traffic to and from a business’s network is securely transported over Neos Networks’ robust network and IP platform. This guarantees instantaneous access and a high-quality service experience, making it an ideal choice for businesses with data-intensive, real-time applications.

References:

Neos Networks launches 10Gbps Managed Dedicated Internet Access

Nokia and CityFibre sign 10 year agreement to build 10Gb/second UK broadband network

STELLAR Broadband offers 10 Gigabit Symmetrical Fiber Internet Access in Hudsonville, Michigan

Orange España: commercial deployment of 10 Gbps fiber in 5 cities

Comcast launches symmetrical 10-Gigabit speeds over Ethernet FTTP

Comcast demos 10Gb/sec full duplex with DOCSIS 4.0; TDS deploys symmetrical 8Gb/sec service

T-Mobile US, Ericsson, and Qualcomm test 5G carrier aggregation with 6 component carriers

T-Mobile US, in a partnership with Ericsson and Qualcomm Technologies, has successfully tested the aggregation of six component carriers in sub-6 GHz spectrum in its live production 5G network.

The test involved aggregating two channels of 2.5 GHz, two channels of PCS spectrum and two channels of AWS spectrum, according to T-Mobile US, which produced an “effective 245 MHz of aggregated 5G channels.”

T-Mo said that they were able to “achieve download speeds of 3.6 Gbps in sub-6 GHz spectrum. That’s fast enough to download a two-hour HD movie in less than 7 seconds!”

5G carrier aggregation allows T-Mobile to combine multiple 5G channels (or carriers) to deliver greater speed and performance. In this test, the Un-carrier merged six 5G channels of mid-band spectrum – two channels of 2.5 GHz Ultra Capacity 5G, two channels of PCS spectrum and two channels of AWS spectrum – creating an effective 245 MHz of aggregated 5G channels.

Image Courtesy of Qualcomm Technologies

“We are pushing the boundaries of wireless technology to offer our customers the best experience possible,” said Ulf Ewaldsson, President of Technology at T-Mobile. “With the first and largest 5G standalone network in the country, T-Mobile is the only mobile provider serving 10s of millions of customers to unleash new capabilities like 5G carrier aggregation nationwide, and I am so incredibly proud of our team for leading the way.”

T-Mobile US announced in May of 2023 that it was rolling out four component-carrier aggregation across its 5G Standalone network, which it said at the time can achieve peak speeds of 3.3 Gbps. In that case, T-Mobile US relies on two 2.5 GHz channels, one 1.9 GHz channel and one 600 MHz channel. The first device able to access 4CA capabilities was the Samsung Galaxy S23.

The carrier also touted its testing of five-component-carrier aggregation in sub-6 GHz spectrum at last year’s Mobile World Congress Barcelona. In that trial, working with Nokia and Qualcomm, T-Mo aggregated two FDD and three TDD carriers and achieved peak downlink throughput speeds that exceeded 4.2 Gbps.

T-Mobile claims to be the leader in 5G, delivering the country’s largest, fastest and most awarded 5G network. The Un-carrier’s 5G network covers more than 330 million people across two million square miles — more coverage area than AT&T and Verizon combined. 300 million people nationwide are covered by T-Mobile’s super-fast Ultra Capacity 5G with over 2x more square miles of coverage than similar offerings from the Un-carrier’s closest competitors.

References:

https://www.ericsson.com/en/ran/carrier-aggregation

Ookla: T-Mobile and Verizon lead in U.S. 5G FWA

T-Mobile combines Millimeter Wave spectrum with its 5G Standalone (SA) core network

Verizon, T-Mobile and AT&T brag about C-band 5G coverage and FWA

T-Mobile and Charter propose 5G spectrum sharing in 42GHz band

ABI Research: 5G Network Slicing Market Slows; T-Mobile says “it’s time to unleash Network Slicing”

T-Mobile US at “a pivotal crossroads” CEO says; 5,000 employees laid off

Ookla Q2-2023 Mobile Network Operator Speed Tests: T-Mobile is #1 in U.S. in all categories!

T-Mobile and Google Cloud collaborate on 5G and edge compute

SpaceX launches first set of Starlink satellites with direct-to-cell capabilities

T-Mobile US today said that SpaceX launched a Falcon 9 rocket on Tuesday with the first set of Starlink satellites that can beam phone signals from space directly to smartphones. The U.S wireless carrier will use Elon Musk-owned SpaceX’s Starlink satellites to provide mobile users with network access in parts of the United States, the companies had announced in August 2022. The direct-to-cell service at first will begin with text messaging followed by voice and data capabilities in the coming years, T-Mobile said. Satellite service will not be immediately available to T-Mobile customers; the company said that field testing would begin “soon.”

SpaceX plans to “rapidly” scale up the project, according to Sara Spangelo, senior director of satellite engineering at SpaceX. “The launch of these first direct-to-cell satellites is an exciting milestone for SpaceX to demonstrate our technology,” she said.

Mike Katz, president of marketing, strategy and products at T-Mobile, said the service was designed to help ensure users remained connected “even in the most remote locations”. He said he hoped dead zones would become “a thing of the past”.

Other wireless providers across the world, including Japan’s KDDI, Australia’s Optus, New Zealand’s One NZ, Canada’s Rogers will collaborate with SpaceX to launch direct-to-cell technology.

References:

https://www.theguardian.com/science/2024/jan/03/spacex-elon-musk-phone-starlink-satellites

Starlink Direct to Cell service (via Entel) is coming to Chile and Peru be end of 2024

Starlink’s Direct to Cell service for existing LTE phones “wherever you can see the sky”

Could Transpositional Modulation be used to solve the “spectrum crunch” problem

Transpositional Modulation (TM) permits a single carrier wave to simultaneously transmit two or more signals, unlike other modulation methods. It does this without destroying the integrity of the individual bit streams.

TM Technologies (TMT) is a wireless technology company offering dramatic data throughput increases for existing wireless and wired networks, using TM.

TMT’s In Band Full Duplex (IBFD) is a MIMO-compatible antenna and software technology providing signal interference cancellation via its Adaptive-Array Antenna which allows simultaneous transmit and Receive = Doubling Data Rates. TM-IBFD development has shown a combined 120 db noise reduction in two-way communications, which provides up to a 100% gain in wireless data transport efficiency.

TMT believes that the use of its patented methods can prevent or delay the onset of a wireless “bandwidth crunch” and focuses on developing products for a range of applications. These products will use core technology to provide solutions and create value for customers, the economy, and the global wireless infrastructure. The company says that the TM-IBFD is backwards compatible and complimentary with existing beam forming or beam shaping installations.

Image Courtesy of TM Technologies (TMT)

……………………………………………………………………………………………………………………………………..

Using the latest Xilinx RFSoC devices, TMT has produced a Software Defined Radio (SDR) format with OFDM as primary modulation with multiple TM channel overlays. This is applicable to nearly any access or backhaul radio device with adequate head-space and operating within the 3GPP Rel 16 specifications.

Industry analyst Jeff Kagan wrote: “Spectrum shortage remains a problem that is not going to solve itself. That’s why new solutions like this are necessary….In the case of solving this spectrum crisis, there are two different groups to focus on. One, is the wireless carriers. Two, are wireless network builders. Either, the customer, which is the wireless network needs to demand this from their network builders. Or the network builders need to embrace this as a competitive advantage and as a solution to their customers.”

Jeff Kagan

References:

Kagan: Could TM Technologies help solve wireless spectrum shortage?

IEEE 5G/6G Innovation Testbed for developers, researchers and entrepreneurs

Courtesy of IEEE member David Witkowski (see his bio below the article):

David’s career began in the US Coast Guard where he led deployment and maintenance programs for mission-critical telecom, continuity of government, and data networking systems. After earning his B.Sc. in Electrical Engineering from University of California @ Davis, he held managerial and leadership roles for high technology companies ranging from Fortune 500 multi-nationals to early-stage startups.

David serves as Executive Director of the Civic Technology Program at Joint Venture Silicon Valley, Senior Advisor for Broadband at Monterey Bay Economic Partnership, and is a Fellow of the Radio Club of America and a Senior Member of the IEEE. He previously served as as Co-Chair of the GCTC Wireless SuperCluster at NIST, on the Board of Expert Advisors for the California Emerging Technology Fund.

David’s IEEE activities include:

-

Co-Chair of the Deployment Working Group at IEEE Future Networks (FNTC)

-

Life Member of the IEEE Microwave Theory and Techniques Society (MTT-S)

-

Member of the IEEE International Committee on Electromagnetic Safety (ICES)

-

Member of the IEEE Committee on Man and Radiation (COMAR)

Huawei’s comeback: 2023 revenue approaches $100B with smart devices gaining ground

Huawei expects to report revenue exceeding 700 billion yuan ($98.5 billion) for 2023, according to comments from rotating deputy chairman Ken Hu in an internal new year message seen by Reuters.

Mr. Hu Houkun (Ken Hu), Huawei’s deputy chairman Photo Credit: Huawei

That optimistic forecast offers further evidence that Huawei is rebounding after U.S. sanctions starting in 2019 crippled some of its business lines by restricting access to critical global technologies such as advanced chips.

“Thanks to our partners across the value chain for standing with us through thick and thin. And I’d also like to thank every member of the Huawei team for embracing the struggle – for never giving up,” Hu said.

“After years of hard work, we’ve managed to weather the storm. And now we’re pretty much back on track.”

“In 2023, we expect to wrap up the year with over 700 billion yuan [US$98.9 billion] in revenue,” he added. That would be a 9% increase on sales from 2022, when the comparable rate of global telecom revenue growth was less than 1%.

Indeed, 2023 has been a very difficult year for telecom network equipment makers such as Ericsson and Nokia. Ericsson’s revenues for the first nine months fell 7% on a constant-currency basis. Nokia’s were down 3%.

…………………………………………………………………………………………………….

What sectors might be responsible for the 9% sales growth Huawei expects this year? From the first paragraph of Ken Hu’s commentary.

“Our ICT infrastructure business has remained solid, and results from our device business surpassed expectations. Both our digital power and cloud businesses are growing steadily, and our intelligent automotive solutions have become significantly more competitive.”

Huawei’s improvement might be due to the upbeat performance of its devices business which includes smartphones and smartwatches. In 2020, the company’s consumer unit accounted for about 54% of all Huawei’s revenues, but its sales halved the following year. It was badly hurt by sanctions because smartphones have a greater need than networks do for advanced chips. Huawei was also cut off from Google software that runs on other Android smartphones. Its response to all this included the sale of Honor, a big smartphone subsidiary.

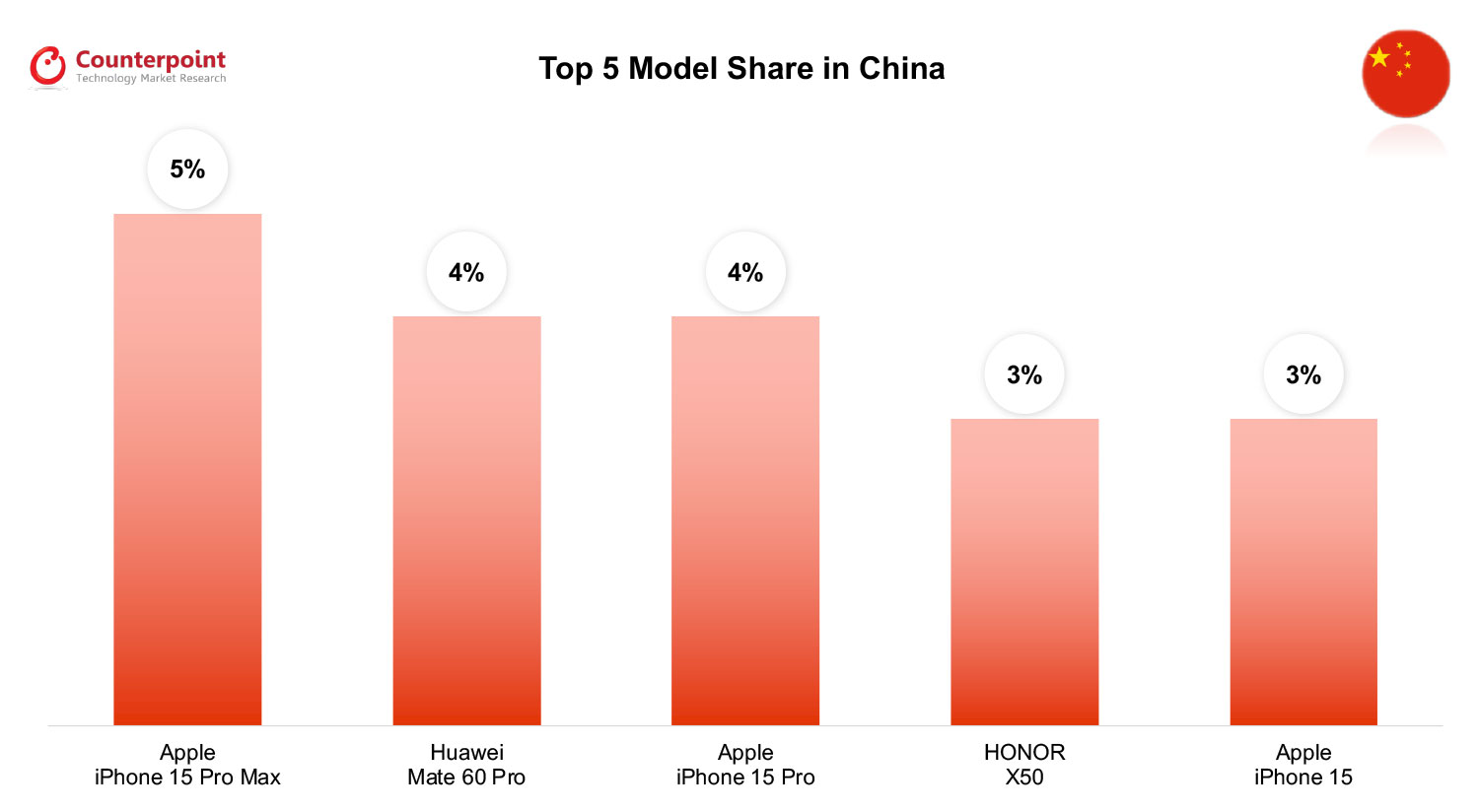

This past August, Huawei launched its Mate 60 series of smartphones, which are believed to be powered by a domestically developed chipset. The release was widely viewed as marking Huawei’s comeback into the high-end smartphone market after years of struggling under U.S. sanctions.

Huawei’s smartphone shipments surged 83% in October year-on-year, helping the overall Chinese smartphone market to grow 11% over the same period, according to Counterpoint Research which wrote:

Huawei’s success and climb in the rankings has been helped by the recent launch of its Mate 60 series 5G phones and popularity of its older P-series 4G devices. “The company is posting some very good growth numbers, but obviously there’s base effects happening,” notes China analyst Archie Zhang. “We expect it will grow by more than half this year, but that still doesn’t bring them close to pre-COVID levels. But it’s signalling a promising 2024.”

Huawei’s smartwatch business is doing very well. Counterpoint’s Woojin Son wrote:

“There is significant value in examining the growth drivers of the global smartwatch market in Q3 2023. Amid a global economic slowdown, most consumer device markets like smartphones are still experiencing stagnation compared to a year ago. In contrast, the smartwatch market has recorded YoY growth for two consecutive quarters in both premium and budget segments. Notably, High-level Operating System (HLOS)* smartwatches, typically featuring higher specification and price, have grown largely driven by Huawei in Q3 2023 as the company posted its highest quarterly performance ever. Most of this surge occurred in the Chinese domestic market, coupled with the launch of new Huawei 5G smartphones.”

……………………………………………………………………………………………………………………..

Looking ahead to 2024, Huawei said in the letter the device business would be one of the major business lines it would focus on for expansion. “Our device business needs to double down on its commitment to developing best-in-class products and building a high-end brand with a human touch,” the letter said.

Missing from Hu’s remarks was any reference to Huawei’s profits, which plummeted 69% last year, to just RMB35.6 billion ($1 billion).

Huawei watchers will probably have to wait until the publication of its 2023 annual report for an update. For sure, the company is cutting costs. “We will continue to streamline HQ, simplify management, and ensure consistent policy, while making adjustments where necessary,” said Huawei’s chairman.

Yet the company will likely continue to ramp up R&D spending. RMB161.5 billion ($22.8 billion) was spent on R&D in 2022, about a quarter of total revenues and a 13% year-over-year increase. Expect a similar increase for 2023 and 2024.

References:

Singles Day Growth Boosts Odds of China Market Smartphone Recovery in Q4 2023

Global Smartwatch Market Rebounds; Huawei and Fire-Boltt Hit New Peaks

Starlink Direct to Cell service (via Entel) is coming to Chile and Peru be end of 2024

Chilean network operator Entel and SpaceX, the company that owns satellite internet provider Starlink, made a commercial agreement to provide satellite-to-mobile services. The agreement will improve broadband coverage for Entel’s LTE customers. It will allow millions of cell phones in Chile and Peru to access satellite coverage starting at the end of 2024.

The first Starlink satellites with Direct to Cell capacity will be launched, providing basic satellite connectivity by the end of 2024. Starlink is a pioneer in providing fixed broadband services through low-orbit satellite networks, which helped it to gain an advantage in the development of direct-to-cell technology.

Starlink satellites with Direct to Cell capabilities enable access to texting, calling, and browsing anywhere on land, lakes, or coastal waters. Direct to Cell will also connect IoT devices which have LTE cellular access.

“One of the great advantages of this proposal is that it will work using the same 4G VoLTE phones that exist in the market today. It does not require any special equipment or special software,” Entel network manager Luis Uribe told BNamericas. “This is an important advantage over traditional satellite solutions. It is a technology that is still evolving, it is being developed. We are going to explore [use cases] as [the technology] advances,” he added.

Although Entel’s mobile networks cover 98% of the populations of Chile and Peru, the Starlink deal will allow it to provide services in maritime territory or in areas that suffered natural disasters.

“It is a technology that has enormous potential as a result of its ability to cover areas that traditional networks cannot achieve,” Uribe said.

A so-called line of sight between device and satellite is required for direct-to-cell to work, meaning the technology might not work indoors or in dense forests. If available, terrestrial coverage will be prioritized.

While other companies are developing similar solutions, they are not as advanced as Starlink. “We see other solutions that also look interesting. To the extent that these do not involve special software or devices, they could be an option,” said Uribe.

Entel is also focused on 5G deployment, achieving a first-stage goal of connecting 270 localities from Arica in the north to Puerto Williams in the south in August.

The company is investing US$350mn in the entire deployment program. In October, Entel enabled NB-IoT at over 6,500 sites to boost connectivity for Internet of Things devices.

“From the point of view of the company’s internal processes, we are incorporating artificial intelligence and generative artificial intelligence tools,” said Uribe. The technologies are being used for automation processes and network optimization, among others.

References:

https://www.bnamericas.com/en/features/spotlight-the-entel-starlink-mobile-coverage-agreement

Starlink’s Direct to Cell service for existing LTE phones “wherever you can see the sky”

SpaceX has majority of all satellites in orbit; Starlink achieves cash-flow breakeven

Bloomberg on Quantum Computing: appeal, who’s building them, how does it work?

1. What’s the appeal of quantum computers?

They can do things that classical computers can’t. Google revealed in April that one of its quantum computers had solved a problem in seconds that would have taken the world’s most powerful supercomputer 47 years. Experimental quantum computers are typically given tasks that a conventional computer would take too long to do, such as simulating the interaction of complex molecules for drug discovery. Their greatest potential is for modeling complex systems involving large numbers of moving parts whose behavior changes as they interact — such as predicting the behavior of financial markets, optimizing supply chains and operating the large language models used in generative artificial intelligence. They’re not expected to be much use in the laborious but simpler work fulfilled by most of today’s computers — processing a more limited number of isolated inputs sequentially on a mass scale.

2. Who’s building them?

Canadian company D-Wave Systems Inc. became the first to sell quantum computers to solve optimization problems in 2011. International Business Machines Corp., Alphabet Inc.’s Google, Amazon Web Services and numerous startups have all created working quantum computers. More recently, companies such as Microsoft Corp. have made progress toward building scalable and practical quantum supercomputers. Intel Corp. started shipping a silicon quantum chip to researchers with transistors known as qubits (quantum bits) that are as much as 1 million times smaller than other types. Microsoft and other companies, including startup Universal Quantum, expect to build a quantum supercomputer within the next ten years. China is building a $10 billion National Laboratory for Quantum Information Sciences as part of a big push in the field.

3. How do quantum computers work?

They use tiny circuits to perform calculations, as do traditional computers. But they make these calculations in parallel, rather than sequentially, which is what makes them so fast. Regular computers process information in units called bits, which can represent one of two possible states — 0 or 1 — that correspond to whether a portion of the computer chip called a logic gate is open or closed. Before a

traditional computer moves on to process the next piece of information, it must have assigned the previous piece a value. By contrast, thanks to the probabilistic aspect of quantum mechanics, the qubits in quantum computers don’t have to be assigned a value until the computer has finished the whole calculation. This is known as “superposition.” So whereas three bits in a conventional computer would only be able to represent one of eight possibilities – 000, 001, 010, 011, 100, 101, 110 and 111 – a quantum computer of three qubits can process all of them at the same time. A quantum computer with 4 qubits can in theory handle 16 times as much information as an equally-sized conventional computer and will keep doubling in power with every qubit that’s added. That’s why a quantum computer can process exponentially more information than a classic computer.

Why Quantum Will Be Quicker

Problems like breaking encryption or mapping a molecule’s structure can require sorting through millions of possibilities.

4. How does it return a result?

In designing a standard computer, engineers spend a lot of time trying to ensure that the status of each bit is independent from those of all the other bits. But qubits are entangled, meaning the properties of one depend on the properties of the qubits around it. This is an advantage, as information can be transferred quicker between qubits as they work together to arrive at a solution. As a quantum algorithm runs, contradictory (and therefore incorrect) results from the qubits cancel each other out, whilst compatible (and therefore likely) results are amplified. This phenomenon, called coherence, allows the computer to spit out the answer it deems most likely to be correct.

5. How do you make a qubit?

In theory, anything exhibiting quantum mechanical properties that can be controlled could be used to make qubits. IBM, D-Wave and Google use tiny loops of superconducting wire. Others use semiconductors and some use a combination of both. Some scientists have created qubits by manipulating trapped ions, pulses of photons or the spin of electrons. Many of these approaches require very specialized conditions, such as temperatures colder than those found in deep space.

6. How many qubits are needed?

Lots. Although qubits can process exponentially more information than classical bits, their inherently uncertain nature makes them heavily prone to errors. Errors creep into qubits’ calculations when they fall out of coherence with each other. Outside the lab, scientists have only been able to keep qubits in coherence for fractions of a second — in many cases, too short a period of time to run an entire algorithm. Theorists are working to develop algorithms that can correct some of these errors. But an inevitable part of the fix is adding more qubits. Scientists estimate that a computer needs millions – if not billions – of qubits to reliably run programs suited for commercial use. Sticking enough of them together is the main challenge. As a computer gets larger in size, it emits more heat, which makes it more likely that qubits will fall out of coherence. The current record for qubits connected is 1,180, achieved by California startup Atom Computing in October 2023 — more than double the previous record of 433, set by IBM in November 2022.

7. When do I get my quantum computer?

It depends on what you want to use it for. Academics are already solving problems on 100-strong qubit machines through the cloud-based IBM Quantum Platform, which the general public is able to try out (if you know how to develop quantum code). Scientists aim to deliver a so-called “universal” quantum computer suitable for commercial applications within the next decade. One caveat of the enormous problem-solving power of quantum computers is their potential for cracking classical encryption systems. Perhaps the best indication of just how close we are to quantum computing is that governments are signing directives and businesses are pouring millions of dollars into securing legacy computing systems against being cracked by quantum machines.

References:

SK Telecom and Thales Trial Post-quantum Cryptography to Enhance Users’ Protection on 5G SA Network

SKT Develops Technology for Integration of Heterogeneous Quantum Cryptography Communication Networks

Research on quantum communications using a chain of synchronously moving satellites without repeaters

China Mobile verifies optimized 5G algorithm based on universal quantum computer

UAE’s “etisalat by e&” announces first software defined quantum satellite network

Can Quantum Technologies Crack RSA Encryption as China Researchers Claim?

Quantum Technologies Update: U.S. vs China now and in the future

ASPI’s Critical Technology Tracker finds China ahead in 37 of 44 technologies evaluated

WiFi 7 and the controversy over 6 GHz unlicensed vs licensed spectrum

Introduction:

Even though the IEEE 802.11be standard is yet to be released officially, there are currently Wi-Fi 7 routers on the market from many major vendors. Wi-Fi 7 provides significantly faster speeds then WiFi 6 (IEEE 802.11ax), with ultra-low latencies and a better communication channel. Thereby, more devices can be connected efficiently.

Wi-Fi 7 routers are capable of delivering wireless data transfer speeds of up to 46 Gbps, which is five times greater than that of Wi-Fi 6E routers. Wi-Fi 7 routers can also operate on multiple bands: carrier frequency operation is between 1 and 7.250 GHz while ensuring backward compatibility and coexistence with legacy IEEE Std 802.11 compliant devices operating in the 2.4 GHz, 5 GHz, and 6 GHz bands. Latency is also lower with a Wi-Fi 7 router and channel connections are more efficient.

Some Wi-Fi 7 routers include the NETGEAR Nighthawk Tri-Band WiFi 7 Router BE19000 Wireless Speed, the TP-Link BE9300 Tri-Band Wi-Fi 7 Router ARCHER BE550, and the ASUS BE96U Tri-Band WiFi 7 Router RT-BE96U.

6 GHz Band Controversy:

As of September 2023, the following countries have adopted the policy of making the entire 6 GHz band available for unlicensed use: U.S., South Korea, Brazil, Saudi Arabia, Costa Rica, Peru. Canada has also made 1200 MHz of 6 GHz spectrum available for unlicensed services. The 6 GHz band is the largest allocation of unlicensed spectrum in the US and South Korea.

Some other countries that have enabled Wi-Fi in the 6 GHz band include: Andorra, Argentina, Australia, Austria, Bahrain, Belgium, CEPT.

China has chosen a licensed approach for the 6 GHz band, using the entire 1,200 MHz for 5G and future 6G services.

The Telecom Regulatory Authority of India (Trai) suggests that the lower end of the 6 GHz spectrum band can be allocated for unlicensed use, such as WiFi, while the upper end can be licensed for telecom use. Netgear said that the India DoT (Department of Telecommunications) is considering to delicense the lower band 6 GHz spectrum.

However, WRC 23 agreed to open up the 6 GHz band for future high-speed mobile communications (instead of for unlicensed WiFi). The 6 GHz band (6.425-7.125 GHz) – was identified for mobile in every ITU Region – EMEA, the Americas and the Asia Pacific. Countries representing more than 60% of the world’s population asked to be included in the identification of this band for licensed mobile at WRC-23. The 6 GHz spectrum is now the harmonized home for the expansion of mobile capacity for 5G-Advanced and beyond.

References:

https://standards.ieee.org/ieee/802.11be/7516/

https://spectrum.ieee.org/what-is-wifi-7

WRC-23 concludes with decisions on low-band/mid-band spectrum and 6G (?)

MediaTek Introduces Global Ecosystem of Wi-Fi 7 Products at CES 2023

Highlights of Qualcomm 5G Fixed Wireless Access Platform Gen 3

Qualcomm FastConnect 7800 combining WiFi 7 and Bluetooth in single chip

Intel and Broadcom complete first Wi-Fi 7 cross-vendor demonstration with speeds over 5 Gbps