Author: Alan Weissberger

TM Forum’s DTW Ignite 2026: Open Digital Architecture (ODA); Nokia, Ericsson, IBM and Mavenir AI announcements/cloud partnerships

-

- Shift to Action: TM Forum Vice President Aaron Boasman-Patel and CEO Nik Willetts opened the summit emphasizing that the industry must move past abstract C-suite visions.

- The AI Economy: The flagship keynote officially launched the “Race to 2030,” a direct directive tasking operators to secure their market relevance by deploying high-velocity, production-grade architectures.

-

- On-Stage AI Co-Hosts: In an industry event first, agentic AI systems took the stage alongside human moderators to act as live panel co-hosts, digital analysts, and experts.

- Summit Intelligence Layer: Advanced AI systems recorded and indexed every keynote, panel, and breakout session, functioning as a real-time intelligence layer to deliver daily trend summaries to attendees.

-

- Autonomous Networks (AN): Featuring the largest showcase of live autonomous operating systems to date. Major case studies from carriers like China Mobile, China Telecom, TDC NET, and Telefónica showcased functional solutions for self-optimizing networks, RAN energy efficiency, and fast fault resolution.

- Trustworthy AI and Data: Discussions zeroed in on scaling responsible AI, exploring Models-as-a-Service (MODaaS) frameworks, managing tokenomics, and reinforcing cyber resilience.

- Composable IT and Ecosystems: Demonstrations focused on scaling Open Digital Architecture (ODA) from boardroom design into functional, interoperable engineering realities.

Practical Engineering & Showcases:

- Catalyst Showcases: The exhibition floor hosted over 60 collaborative proof-of-concept Catalyst projects and Innovation Engine live demonstrations.

- New Interactive Hubs: The event debuted dedicated “Mission Garages” for hands-on engineering collaboration, along with a specialized Future Skills program to help tech teams adapt to AI-native workflows. [1]

- Major Tech Partnerships: Industry titans—including IBM, Ericsson, Cisco, and Nokia—used the floor to debut subsea infrastructures, physical AI, and cloud-native automation frameworks.

Note 1. DTW Ignite 2026 is TM Forum’s flagship global connectivity event focused on accelerating AI-native telcos, autonomous networks, and composable IT. The event is from June 23 to June 25 at the Bella Center in Copenhagen, Denmark.

……………………………………………………………………………………………………………………………………………………………….

At the show, the TM Forum and its member alliance of over 850 companies across 180 countries, announced a major structural evolution for the Open Digital Architecture (ODA), shifting it from a cloud-native IT modernization blueprint into an AI-native execution environment. The core focus of these updates is to establish standardized, executable reference frameworks that allow operators to move beyond fragmented AI pilots and build an autonomous enterprise. The primary ODA updates and structural expansions announced at the summit include:

-

- Governed Execution Layer: TM Forum members launched AI-native extensions to the ODA specification, adding a governed execution layer. This allows autonomous AI agents and large language models to run natively within the existing ODA component architecture and Open APIs.

- Project Foundation & AI Canvas: Through the Demo ONE Catalyst project, tech leaders debuted an updated AI-Native ODA Canvas. This cloud-native runtime environment orchestrates data, AI models, and autonomous agents across fragmented BSS, OSS, and network domains to replace rigid legacy systems.

- Model-as-a-Service (MODaaS): To solve the challenge of rising token costs and fragmented model selection, an ODA-aligned MODaaS framework was introduced. It establishes a unified control plane to govern, secure, and manage AI model usage across the carrier architecture.

-

- Space-Telco Interoperability: In a major scope expansion, TM Forum officially launched the ODA for Satellite project. Supported by 16 foundational partners—including Airbus, Terrestar, and Vodacom—the initiative targets multi-billion dollar direct-to-device and space-connectivity markets.

- Unified Non-Terrestrial Frameworks: The project extends standard ODA components to satellite technology providers, standardizing how terrestrial mobile networks and non-terrestrial networks (NTNs) handle cross-industry billing, service delivery, and zero-touch roaming integrations.

- Plug-and-Play Validation: TM Forum rolled out its newly expanded ODA Component Certification. This toolkit gives vendors a programmatic way to verify that their commercial software components are truly plug-and-play ready, lowering custom integration costs for telecom buyers.

- “Running on ODA” Milestones: The alliance celebrated that 18 global Communication Service Providers (CSPs), representing over two billion subscribers globally, have officially achieved “Running on ODA” accreditation—confirming that modular, componentized architecture has reached full scale in production environments.

……………………………………………………………………………………………….

Vendor Announcements:

- Amazon Web Services (AWS) Expansion: Nokia and AWS expanded their partnership to run Nokia’s Autonomous Networks Fabric natively on AWS. The integration brings operators closer to Level 4 network autonomy, enabling networks to orchestrate, analyze, and heal themselves at machine speed.

- Google Cloud Integration: Nokia deepened its alliance with Google Cloud to integrate Gemini models into the Nokia Assurance Center. They unveiled six specialized generative AI agents (including a Router Agent and Event Triage Agent) to automatically process data and isolate the root causes of service faults. It launches as a SaaS offering in September 2026.

- Databricks Proof of Concept: Nokia and Databricks announced the completion of a joint project showing a unified, cloud-agnostic data platform. This resolves a legacy pain point by unifying hundreds of fragmented operational silo data architectures so multi-agent AI can run seamlessly across networks.

- GenAI-Native Operations: Instead of relying on traditional rules-based code, Nokia’s new interfaces allow field engineers to query complex multi-vendor topologies, generate diagnostic code, and run natural-language root-cause analyses on real-time traffic faults.

- Autonomous Network Scaling: Nokia presented multi-party Catalyst project solutions targeting network optimization, zero-touch slicing, and automated enterprise edge deployments tailored for the 5G-Advanced landscape.

……………………………………………………………………………………………………………………………………………………….

- EIAP Core Expansion: The headline announcement from the Ericsson Cloud Software and Services division was the expansion of the Ericsson Intelligent Automation Platform (EIAP). Formerly restricted to RAN operations, the platform now fully integrates and unifies Radio Access Network (RAN) and core network automation systems.

- Introduction of cApps: Ericsson claimed a major industry first by rolling out core-specific automation applications (cApps). These decentralized apps allow operators to run automated routines directly on core architectures, streamlining cross-domain workflows to cut operations costs.

- Business Value Pathways: Ericsson debuted a structured strategic blueprint designed to guide Communication Service Providers (CSPs) through the financial steps of scaling from Level 3 to Level 4 autonomous networks.

…………………………………………………………………………………………………………………………………………………….

- Addressing the “AI Trust Gap”: Responding to a TM Forum study revealing that only 14% of operators can prove their AI systems are fully reliable, IBM presented framework tools at DTW Ignite to address security and model bias.

- B2B2X Monetization: IBM focused its platform showcase on orchestrating automated workflows for multi-enterprise B2B2X networks, enabling secure data federation across third-party hyperscalers and edge servers.

……………………………………………………………………………………………………………………………………………………

- Telco-First Cloud Architecture: Stationed at Booth 334, Mavenir debuted its updated AI-by-design, cloud-native software portfolios built natively around TM Forum’s Open Digital Architecture (ODA) frameworks.

- Closed-Loop Automation: Mavenir demonstrated actionable frameworks that handle real-time resource adjustments, shifting power and processing capacity across base stations based on AI-predicted user demand cycles.

……………………………………………………………………………………………………………………………………………………

References:

https://www.tmforum.org/events/dtw/experience-dtw/new-for-2026

Inside TM Forum’s Catalyst project “Living Networks – Phase III”

Deloitte and TM Forum : How AI could revitalize the ailing telecom industry?

The Financial Trap of Autonomous Networks: Scaling Agentic AI in the Telecom Core

GSMA, ETSI, IEEE, ITU & TM Forum: AI Telco Troubleshooting Challenge + TelecomGPT: a dedicated LLM for telecom applications

SHIELD-6G with AI-native cyber threat intelligence platform to enhance cybersecurity for Europe’s future 6G networks

Verizon’s 6G Innovation Forum joins a crowded list of 6G efforts that may conflict with 3GPP and ITU-R IMT-2030 work

Private 5G networks move to include automation, autonomous systems, edge computing & AI operations

Ericsson integrates Agentic AI into its NetCloud platform for self healing and autonomous 5G private networks

SNS Telecom & IT: Private 5G Market to Reach $6.6 Billion as Physical AI Takes Hold

Private 5G networks are transitioning from limited-scale deployments to a more material segment of the wireless infrastructure market. SNS Telecom & IT estimates that annual spending on private 5G networks will exceed $6.6 billion by 2029, driven by multi-site and multi-national enterprise rollouts supporting industrial automation, “physical AI” systems, and mission-critical communications across both commercial and public-sector domains.

Historically, private cellular deployments remained a niche market during the 2G/3G era, with notable exceptions such as GSM-R for railway communications. The introduction of private LTE in the early 2010s established a foundation for dedicated enterprise connectivity; however, adoption remained constrained by performance limitations and ecosystem maturity. The evolution to 3GPP-defined 5G NPN architectures—both standalone (SNPN) and public network-integrated (PNI-NPN)—is now enabling broader applicability across industrial verticals, with a trajectory that exceeds prior-generation adoption levels. Concurrently, legacy systems such as GSM-R are expected to transition toward 5G-based FRMCS implementations aligned with 3GPP specifications.

From a technical perspective, 5G introduces capabilities that are better aligned with industrial communication requirements than LTE. Enhanced mobile broadband (eMBB), ultra-reliable low-latency communications (URLLC), and massive machine-type communications (mMTC) collectively support higher throughput, sub-10 ms latency targets, improved reliability, and significantly greater device densities. These characteristics enable 5G NPNs to address use cases traditionally served by wired Ethernet or deterministic industrial networks, particularly in scenarios requiring mobility and flexible topology. Additional attributes—including improved coverage per radio node, network slicing, time-sensitive networking (TSN) integration, and enhanced security mechanisms—position private 5G as a viable alternative to interference-prone unlicensed technologies in dense IIoT environments.

Deployment momentum is increasingly visible across manufacturing, logistics, energy, and transportation sectors. Production-grade implementations have demonstrated measurable operational benefits, including reduced downtime, improved safety, and expanded coverage in previously unconnected areas. A common pattern involves the migration of AGV and AMR connectivity from Wi-Fi to private 5G, enabling more deterministic performance and reduced susceptibility to interference. In parallel, private 5G is extending connectivity to challenging industrial zones where wired infrastructure is cost-prohibitive or operationally restrictive. Emerging use cases also include coordinated robotics and edge-controlled automation systems, often described as “physical AI,” where low-latency and reliable connectivity are critical for closed-loop control.

In the public-sector domain, private 5G is gaining traction for mission-critical communications. Applications span defense, public safety, railways, and utilities, where requirements include high availability, secure communications, and support for MCX services (mission-critical push-to-talk, video, and data). The evolution toward 5G-Advanced, as defined in 3GPP Releases 18 through 20, introduces further enhancements relevant to these deployments, including support for reduced channel bandwidth operation in dedicated spectrum, expanded frequency bands, and specific feature sets aligned with FRMCS and mission-critical service requirements.

Geographically, adoption is concentrated in markets with established industrial bases and supportive regulatory frameworks, including North America, Europe, and parts of Asia-Pacific. As enterprises scale digitalization initiatives—encompassing automation, AI-driven operations, and connected workforce applications—private 5G deployments are increasingly moving beyond pilot phases to multi-site, production-grade networks.

SNS Telecom & IT projects a compound annual growth rate of approximately 34% for private 5G investments between 2026 and 2029. Growth is expected to be led by localized enterprise and campus networks, alongside parallel expansion in mission-critical infrastructure. The combination of maturing 3GPP standards, improving device ecosystems, and demonstrated operational benefits is positioning private 5G as a foundational connectivity layer for next-generation industrial and public-sector systems.

References:

https://www.snstelecom.com/private5g

GSA: Global private mobile networks exceed 2,000 worldwide; Ericsson Private 5G from Verizon Business extends beyond U.S.

Private 5G networks move to include automation, autonomous systems, edge computing & AI operations

SNS Telecom & IT: Mission-Critical Networks a $9.2 Billion Market

SNS Telecom & IT: Private 5G Market Nears Mainstream With $5 Billion Surge

SNS Telecom & IT: Private 5G and 4G LTE cellular networks for the global defense sector are a $1.5B opportunity

OneLayer Raises $28M Series A funding to transform private 5G networks with enhanced security

Verizon partners with Nokia to deploy large private 5G network in the UK

AI-RAN and Agentic AI get real: Ericsson, Nokia, Verizon & other operators enter into a new network automation era

Disclaimer: Perplexity.ai was used for research in this article.

Executive Summary:

A cluster of announcements in early-to-mid June 2026 signals a real shift from AI research to commercial AI-driven network automation. Telcos are transitioning from isolated AI pilots to production-grade AI operations deployed across live networks.

-

Ericsson launched its AI in RAN commercial software subscription on June 11th, claiming up to 20% higher downlink throughput and up to 10% better spectral efficiency across more than 15 live deployments using existing baseband silicon.

-

Nokia and Indosat Ooredoo Hutchison (Indonesia) announced a GPU-accelerated AI-RAN partnership in Indonesia on June 8, expanding the Nokia–NVIDIA architecture already adopted by T-Mobile US, SoftBank, and Vodafone.

-

Verizon disclosed that its 60,000-site vRAN is now applying agentic AI to planned configuration changes, service assurance, and network optimization, while publicly calling for industry-wide interoperability standards for agentic systems.

-

Nokia launched an agentic AI framework for IP network operations within its Network Services Platform (NSP), marking its third agentic product announcement in a four-week period.

A growing number of network operators are transitioning from traditional connectivity providers into AI infrastructure operators. SK Telecom (South Korea) announced a gigawatt-scale AI Cloud built on NVIDIA DGX SuperPOD architecture; Deutsche Telekom (Germany) secured the German federal government’s sovereign AI cloud contract; and MTN Group (South Africa) detailed a plan to convert 18,000 African tower locations into a distributed AI inference grid.

Over a six-week window, six major network operators—SK Telecom, Deutsche Telekom, MTN Group, Verizon, SoftBank, and Indosat Ooredoo Hutchison—have converged on a single strategic premise: existing telecommunications infrastructure, including connectivity, physical real estate, and data center capacity, constitutes the foundational footprint for a commercial AI compute business.

………………………………………………………………………………………………………………………………………………………………………………………………

Government’s Buys Into AI Compute:

Government involvement in AI compute is intensifying, with direct implications for telecom strategy. China’s $295 billion program defines the upper bound of state-backed AI compute investment. Beijing announced plans to invest 2 trillion yuan ($295 billion) over five years in AI datacenter infrastructure. China Mobile and China Telecom are designated as the primary operators of a national AI compute network, while Huawei will supply the majority of AI chips—explicitly bypassing NVIDIA. The plan accelerates China’s original 2030 national computing network target to 2028, funded through sovereign debt.

- China’s National Data Administration reported 140 trillion daily AI token flows by March 2026—up 1,400-fold from the start of 2024. China Mobile, China Telecom, and China Unicom launched commercial AI token packages in May, with per-token costs that centralized operations can reduce by approximately 30 percent. China Mobile separately unveiled AI-eSIM, which embeds an autonomous decision layer directly into the SIM.

- Chinese network operators are advancing through the full AI lifecycle—token economy, infrastructure mandate, and sovereign chip supply—at a pace and scale unmatched by any other single market.

Technical Implications for Network Architecture:

The convergence of AI-RAN, agentic AI, and AI infrastructure provision demands architectural evolution across several dimensions:

Standards and Interoperability Gap:

Verizon’s public call for industry-wide interoperability standards for agentic systems highlights a critical bottleneck. Agentic AI frameworks from Ericsson, Nokia, and other vendors must interoperate across multi-vendor networks, yet no standardized protocol exists for agentic command, control, and assurance. This gap mirrors the early RAN interoperability challenges that Open RAN later addressed.

The TM Forum’s Autonomous Networks L4/5 roadmap and the 3GPP 6G standardization process will need to incorporate agentic AI interoperability as a core requirement. Without standards, telcos risk vendor lock-in for AI automation capabilities, undermining the multi-vendor flexibility that has been a telco industry priority for decades.

What This Means for 5G and 6G Roadmaps:

AI-driven automation is becoming a prerequisite for 6G L4/5 autonomous networks. The June 2026 announcements suggest that:

-

5G Advanced deployments will increasingly incorporate AI-RAN as a standard feature, not an optional enhancement.

-

6G specifications (expected by end-2028 per Ericsson) will likely embed agentic AI and autonomous decision layers as core architectural elements.

-

Network economics will shift from bandwidth-centric to compute-centric revenue models, with AI token services and inference grids becoming significant revenue streams.

For network architects, the implication is clear: AI infrastructure must be designed as a first-order network capability, not a second-order application layer. GPU acceleration, agentic orchestration, and token-economy support need to be part of the baseline network architecture from the outset.

Conclusions — The Automation Tipping Point:

June 2026 marks a tipping point where AI-driven network automation transitions from pilot to production. The combination of commercial AI-RAN subscriptions, agentic AI deployments at tens-of-thousands-of-site scale, and telco-led AI infrastructure provision signals that AI is no longer an experimental capability but a core network function.

The critical question for telcos is not whether to adopt AI automation, but how to avoid vendor lock-in while achieving the interoperability required for multi-vendor, multi-domain autonomous networks. Standards bodies, operator consortia, and vendor alliances must address this gap before agentic AI becomes a strategic constraint rather than a competitive advantage.

………………………………………………………………………………………………………………………………………………………………………………………………

References:

https://mtnconsulting.substack.com/p/the-unmanned-network-17-june-2026

Cisco Execs: New “Network Supercycle” as Agentic AI Workloads Reshape Telecom Infrastructure

Cisco Execs: New “Network Supercycle” as Agentic AI Workloads Reshape Telecom Infrastructure

STL Partners webinar: Agentic AI needed for RAN autonomy & efficiency

The Financial Trap of Autonomous Networks: Scaling Agentic AI in the Telecom Core

Nokia to showcase agentic AI network slicing; Ericsson partners with Ookla to measure 5G network slicing performance

T-Mobile US announces new broadband wireless and fiber targets, 5G-A with agentic AI and live voice call translation

Telecom operators investing in Agentic AI while Self Organizing Network AI market set for rapid growth

Ericsson integrates Agentic AI into its NetCloud platform for self healing and autonomous 5G private networks

Agentic AI and the Future of Communications for Autonomous Vehicles (V2X)

Ericsson’s June 2026 Mobility Report Highlights + AI impact on network traffic

Ericsson launches AI in RAN as commercial software subscription:

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

RAN Silicon Rethink- Part II; vRAN and General-Purpose Compute

Analysis: Nvidia’s rumored new 6G AI-RAN – likely features/functions and industry impact

Analysis: Nvidia’s $2 billion investment in Marvell; NVLink Fusion ecosystem & RAN vendor silicon strategy

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Federated Wireless Spectrum AI: Advancing CBRS Efficiency Through AI-Driven RAN Optimization

Introduction:

Recent field trial results from Federated Wireless indicate up to 50% gains in usable CBRS spectrum [1.] and significantly accelerated network planning cycles when using the company’s Wireless Spectrum AI platform [2.]. The field trials were held in markets such as Phoenix and Philadelphia, along with more intensive trials and validations in four counties in Georgia with a tier 1 cable operator and a tier 1 mobile operator, according to Light Reading.

While these results are compelling for operators and enterprise adopters, they warrant careful technical evaluation. This article examines the underlying “Spectrum AI” approach, reviews early performance evidence, and assesses implications for CBRS-based private networks. It also considers deployment risks, regulatory dependencies, and workforce requirements relevant to production-scale adoption.

Note 1. CBRS (Citizens Broadband Radio Service) is a 150 MHz wide broadcast band (3.55 GHz to 3.7 GHz) allocated by the FCC for commercial and private cellular use. Operating in the 3.5 GHz band (Band 48), it utilizes dynamic spectrum sharing to bridge the gap between high-speed 5G/LTE and local Wi-Fi networks.

Note 2. Federated Wireless’ Spectrum AI is a physical AI platform for shared-spectrum planning and coordination in CBRS and 6 GHz environments, designed to improve spectral efficiency, interference management, and deployment speed. It uses real-world propagation and coordination data to help operators unlock more usable capacity without adding spectrum or infrastructure. It’s built to accelerate site planning, refine SAS coordination, and continuously improve with field data and model updates.

…………………………………………………………………………………………………………………………………………………………………………………………………………..

Physical AI for RF Modeling:

Spectrum AI introduces a “physical AI” approach that models radio propagation directly, in contrast to conventional higher-layer traffic analytics used in legacy planning tools. The system is trained on large-scale CBRS propagation datasets, enabling path loss prediction reportedly within 0.5 dB accuracy.

In addition to improved modeling fidelity, Federated claims runtime acceleration on the order of 102–103 compared to Monte Carlo-based simulations. This enables near–real-time spectrum optimization in dynamic environments. The platform interfaces with the Spectrum Access System (SAS), allowing continuous adjustment of grant requests while maintaining regulatory compliance.

A key architectural feature is the use of closed-loop learning: deployment data continuously refines model accuracy, creating a feedback cycle between field performance and planning. Early adopters report up to 90% reductions in planning time, suggesting a transition from static RF design toward adaptive, software-driven control of spectrum resources.

Image Credit: Federated Wireless

…………………………………………………………………………………………………………………………………………………………………..

“We’ve been working on implementing our AI technology for spectrum for the last couple of years,” Federated Wireless President and CEO Iyad Tarazi told Light Reading. “It’s been a long journey with a lot of learnings. … I’m really shocked at the amount of value [AI] is bringing and how it’s changing how I view the business.” “It’s SAS+ with a lot of AI tools,” Tarazi added, noting that it’s designed for large cable operators, mobile carriers and regional wireless network operators.

The original, more rigid, rules-based approach caused operators to use a lot of “conservative buffers” and guardrails because they didn’t have the kind of real-time predictability that AI gives them, Tarazi said. “People were getting frustrated that shared spectrum could do more,” he explained. “Instead of a rules-based [approach], we can do these sorts of massive simulations with a lot of real world data, which is what physical AI is about.”

CBRS Market Context:

CBRS remains the dominant mid-band option for private 5G deployments in the United States. Industry estimates suggest approximately 75% of operational private cellular systems leverage CBRS, with projections exceeding 80% penetration in industrial environments by the early 2030s.

The installed base—hundreds of thousands of CBRS nodes across millions of locations—demonstrates that the ecosystem has moved beyond early trials into scaled deployment. Continued activity from cable operators, system integrators, and neutral-host providers reinforces this momentum. At the same time, the shared-spectrum model remains attractive due to its cost structure and regulatory accessibility.

Within this context, solutions that increase spectral efficiency without requiring additional licensed spectrum are particularly well positioned. Spectrum AI directly targets this requirement.

Reported Capacity and Efficiency Gains:

Federated Wireless reports several performance improvements based on simulations and early field data:

-

Up to 5× capacity gains in dense indoor environments.

-

Approximately 50% increase in usable spectrum across CBRS tiers.

-

102–103× faster RF simulation and planning cycles.

-

Up to 50% reduction in required site count, with estimated capital expenditure savings near 40%.

These metrics, if validated, would materially improve the economics of private 5G. However, all results are currently vendor-reported, and independent benchmarking across diverse deployment scenarios remains limited.

Enterprise Cost Implications:

Private network cost structures are heavily influenced by radio density, site acquisition, and backhaul provisioning. Reductions in node count directly translate into capital and operational savings.

For illustration, consider a 500-site CBRS deployment in a manufacturing environment. A 50% reduction in radios could eliminate approximately 250 nodes, potentially saving on the order of several million dollars in equipment costs while reducing power consumption and maintenance overhead. In parallel, faster planning cycles compress deployment timelines, improving time-to-value for enterprise use cases.

Improved spectral reuse also enables capacity expansion without incremental spectrum costs, enhancing return on investment for existing CBRS allocations.

Deployment Considerations and Risks:

Despite the potential benefits, several risks must be addressed before large-scale adoption:

-

Validation: Performance claims must be independently verified across heterogeneous environments, including industrial, campus, and rural deployments.

-

SAS interoperability: Dynamic spectrum optimization requires robust interaction with SAS platforms; inconsistencies could affect compliance or performance.

-

Regulatory uncertainty: Ongoing FCC proceedings related to CBRS power limits and tiering structures may impact long-term investment assumptions.

-

Security and control: AI-driven RF optimization introduces new attack surfaces and operational risks; explainability and override mechanisms are essential.

These factors underscore the need for phased deployment strategies, rigorous testing, and governance frameworks.

Strategic Implications:

Spectrum AI should be viewed as an incremental but meaningful evolution in RAN optimization rather than a disruptive architectural shift. By increasing effective capacity within existing mid-band allocations, it supports new enterprise and industrial use cases without additional spectrum licensing.

System integrators may incorporate such capabilities into broader solutions that include Wi-Fi 7, edge computing, and security platforms. For operators and neutral-host providers, improved spectral efficiency can reduce infrastructure intensity while expanding serviceable markets.

At a policy level, demonstrated gains in shared-spectrum efficiency could reinforce support for dynamic spectrum access models.

Workforce and Skills Requirements:

The adoption of AI-driven spectrum management increases the demand for interdisciplinary expertise spanning RF engineering, machine learning, and regulatory compliance. Key competencies include:

-

CBRS operational frameworks and SAS interfaces.

-

RF propagation modeling and validation.

-

AI/ML model governance and lifecycle management.

-

Security controls for autonomous network functions.

Structured training and certification programs can help address these requirements, particularly as networks evolve toward greater automation.

Conclusions:

Federated Wireless’ Spectrum AI highlights the growing role of AI in spectrum-aware RAN optimization. Early results suggest meaningful gains in capacity, cost efficiency, and deployment speed within CBRS networks. However, independent validation, regulatory stability, and robust operational controls will be critical to realizing these benefits at scale.

For technical decision-makers, the near-term priority is to evaluate performance claims through controlled trials, assess interoperability with existing SAS and RAN infrastructure, and align organizational capabilities with the demands of AI-driven network operations.

…………………………………………………………………………………………………………………………………………………………………………………………..

References:

Spectrum AI Advances AI Telecom Networks With CBRS Capacity Gains

GSMA Vision 2040 study identifies spectrum needs during the peak 6G era of 2035–2040

Dell’Oro: Fixed Wireless Access revenues +10% in 2025 & will continue to grow 10% annually through 2029

SNS Telecom & IT: Private LTE & 5G Network Ecosystem – CAGR 22% from 2025-2030

SNS Telecom & IT: CBRS Network Infrastructure a $1.5 Billion Market Opportunity

Big 5G Conference: 6G spectrum sharing should learn from CBRS experiences

Analysis: Ericsson’s leading role in French INTENTION 6G project

Ericsson’s R&D center in France is leading INTENTION-6G, a project worth more than €12 million over four years. It’s backed by the France 2030 plan to embed AI into RAN control for energy efficiency and intent-based operation. Partners include Orange, BubbleRAN and CentraleSupélec.

INTENTION 6G aims to optimize energy consumption of the Radio Access Network (RAN) while meeting 5G/6G traffic requirements. At the heart of the project is the integration of artificial intelligence into network control, particularly at RAN level, to improve both performance and energy efficiency. The project has now reached its mid development phase, enabling the first technology building blocks to be defined.

INTENTION 6G is based on a public private partnership approach that combines industrial, academic and entrepreneurial expertise. The project makes it possible to design, test and validate new solutions through demonstrators and experimental platforms, with a view to their gradual integration into tomorrow’s networks.

Several key areas structure the work: advanced automation of network functions, dynamic optimization of energy consumption, and the development of so called “intent based” networks, capable of automatically adjusting their performance to usage and needs thanks to artificial intelligence.

Christian Leon, Head of Ericsson Western Europe, says:

“Mobile networks are evolving to meet ever increasing requirements in terms of performance, energy efficiency and resource optimization. With INTENTION 6G, Ericsson France’s R&D center is actively contributing, alongside leading French partners, to laying today the foundations for the networks that will support tomorrow’s critical use cases and digital transformations.”

-

- Intent-Based Networking (IBN): The project designs networks capable of automatically adjusting performance. Operators issue high-level business goals (intents) via language models, which the system automatically translates into exact technical configurations.

- Advanced Automation: AI takes over network control loops at the Radio Access Network (RAN) level. This shifts management from rigid, manual rules to real-time, zero-touch autonomous domain operations.

- Dynamic Energy Optimization: Mitigating the heavy carbon footprint of next-gen hardware is a priority. AI dynamically monitors traffic demands to initiate micro-sleep and scale down RAN energy use without dropping service quality.

- Standalone Native AI Architecture: It avoids complex legacy radio splitting by prioritizing a standalone architecture. AI components function pervasively across the edge-cloud continuum through a dedicated “AI interconnect”.

- Integrated Sensing and Communication (ISAC): Turning the network into a radar grid to track real-time physical environments.

- Mass-Market Immersive Experiences: Assuring low-latency and continuous data throughput for holographic communications and mixed reality (XR).

- Industry 5.0: Powering dynamic workgroup creation and traffic handling for mobile robot swarms, autonomous delivery drones, and smart factories.

……………………………………………………………………………………………………………………………..

Building on its R&D center in France, opened in 2020, Ericsson says it’s leveraging its expertise in next generation network technologies. The teams involved are particularly specialized in 6G research, AI native networks, critical networks and cybersecurity. The center has already contributed to a portfolio of more than 180 patents in mobile technologies and is part of a strong ecosystem of academic and industrial partners in France.

By mobilizing its innovation capabilities and drawing on a rich and committed ecosystem, Ericsson is helping to prepare a new generation of networks that are smarter, more flexible and more sustainable.

References:

https://www.ericsson.com/en/press-releases/3/2026/intention-6g

https://ieeexplore.ieee.org/document/10942858/

S&P Global Market Intelligence Surveys: Fiber Deployments in U.S. and Europe + AI Infrastructure Causes Market Shift

S&P’s Global Market Intelligence most recent survey showed that 87% of telecom providers in North America and Europe were deploying fiber optics last year, about the same as 2024. That’s according to the firm’s Erik Keith during a webinar hosted June 17th by the Fiber Broadband Association and its president, Gary Bolton. Among the 104 telecom operators surveyed globally, nearly nine out of ten are already using fiber as part of their broadband strategy. On the cable side, more than two-thirds of operators have either deployed fiber-to-the-home or plan to do so.

The Fiber Broadband Association says, “FTTH technology is clearly the “end game” solution for wireline broadband access services, however, the speed and scope of operator migration to full-fiber networks varies widely, depending on factors such as operator roadmaps and competitive landscape conditions.”

- Pervasive Adoption: Among the 104 telecom operators surveyed globally, 87% in North America and Europe utilize or are actively deploying fiber.

- FTTH Dominance: Fiber-to-the-home (FTTH) is widely regarded as the ultimate end-game for wireline broadband, though legacy copper and fixed wireless networks remain a part of some operators’ transition strategies.

- Cable Operator Progress: On the cable side, more than two-thirds of providers have already deployed FTTH or plan to do so as competition intensifies. More than two-thirds of surveyed cable operators have either deployed FTTH or plan to do so in the near future.

- Growing Cable Competition: Fiber overlap now extends across an estimated 75% of the U.S. cable footprint. Because of this, traditional cable operators are experiencing continued broadband subscriber losses and are actively revising their pricing and bundling strategies.

- High Consumer Satisfaction: Consumer surveys show that gigabit-tier fiber subscribers report the highest overall satisfaction rates, while fiber providers—including Verizon, Breezeline, and Frontier—claim the three lowest monthly churn rates in the U.S.

- AI as a Fiber Catalyst: Fiber is increasingly viewed as a dual-use asset capable of supporting both residential users and hyperscalers, as surging artificial intelligence (AI) demands require advanced, high-capacity infrastructure.

……………………………………………………………………………………………………………….

A different S&P Global Market Intelligence report argues that AI infrastructure demand is becoming linked to a larger market shift: constrained energy supply, higher expected earnings for producers and a growing premium for companies that control scarce capacity. For telecom and technology markets, the report adds another layer to the AI infrastructure conversation. The AI buildout is often discussed in terms of chips, models, cloud platforms and data centers. S&P Global Market Intelligence’s analysis suggests the conversation also needs to include energy supply, regional exposure, capex efficiency and the market value of scarce capacity.

……………………………………………………………………………………………………………….

References:

https://www.benton.org/headlines/fiber-breakfast-week-24-fiber-technology-trends

2026 Fiber Connect Keynote: “The Future of Fiber Optics: AI and the Quantum”

Analysis: Fiber Broadband Association (FBA) whitepaper: Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective

Fiber Broadband Association Middle Mile WG: how to use “Digital Infrastructure Networks” for coordinated fiber backbone investments

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

Fiber Optic Boost: Corning and Meta in multiyear $6 billion deal to accelerate U.S data center buildout

Fiber Optic Networks & Subsea Cable Systems as the foundation for AI and Cloud services

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Automating Fiber Testing in the Last Mile: An Experiment from the Field

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

EdgeCore Digital Infrastructure and Zayo bring fiber connectivity to Santa Clara data center

Fiber Connect 2023: Telcos vs Cablecos; fiber symmetric speeds vs. DOCSIS 4.0?

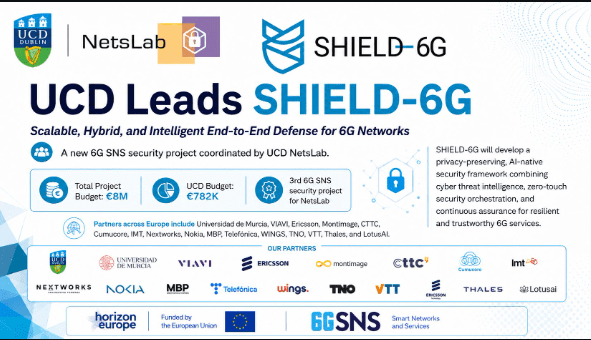

SHIELD-6G with AI-native cyber threat intelligence platform to enhance cybersecurity for Europe’s future 6G networks

The SHIELD-6G (Scalable, Hybrid, and Intelligent End-to-End Defense for 6G Networks) project is exploring ways of strengthening cybersecurity for Europe’s future 6G networks. Backed by an €8 million ($9 million) grant from the European Commission, the 36-month initiative brings together 19 international partners to build an AI-native cyber threat intelligence platform for future networks. Telefónica, Ericsson and Nokia are among 19 companies and research organizations from 10 European countries (Ireland, Spain, Finland, France, the Netherlands, Italy, Greece, Latvia, Estonia, and Turkey) are involved. The project is being coordinated by University College Dublin.

“Future 6G networks are expected to support highly sensitive and mission-critical applications, including connected healthcare, autonomous industrial operations, smart manufacturing, maritime connectivity, and resilient public and private communications,” states the press release.

“6G networks will form the foundation of Europe’s next generation of digital services, but their success will depend on trust, resilience, and security by design,” said Madhusanka Liyanage, Associate Professor/Ad Astra Fellow and Director of Graduate Research at the School of Computer Science, University College Dublin, Ireland. “SHIELD‑6G brings together a strong European consortium to develop intelligent cybersecurity capabilities that can protect critical services and support Europe’s digital sovereignty.”

“6G is way more complex than 5G, because it manages more devices, and there’s more automation, and with automation there come problems,” says Bart Siniarski, director at MBP Network Technology, a Shield-6G member organization. “The attack surface will be extended by a couple of magnitudes. So when we step into 6G — which is, to me, 5G on AI steroids — there are going to be problems at the beginning. And then over time [the goal is that] we are comfortable using 6G in critical infrastructure like hospitals or factories or maybe in shipping and militaries.”

………………………………………………………………………………………………………………………………………………………

The SHIELD-6G project tests and validates its AI-native cyber threat intelligence platform across three primary mission-critical use cases. These scenarios are selected because they require ultra-reliable low latency, mass automation, and high security.

Core AI Security Technologies:

Privacy-Preserving Analytics: Uses federated learning and differential privacy to train threat detection models locally on edge devices. Networks share intelligence without exposing sensitive underlying user data.

Explainable AI (XAI): Ensures complex model decisions are transparent by providing clear, human-readable explanations for network blocks or flags. This prevents false alarms from interrupting critical infrastructure like hospitals or shipping lanes.

Zero-Touch Security Orchestration: Combines automation with secure multi-party computation to isolate and mitigate zero-day network breaches. Responses trigger dynamically with minimal human intervention.

Digital Twin Simulation: Embeds AI models into a network digital twin environment to safely stress-test defenses. The software predicts how an attack will propagate before it affects live network traffic.

………………………………………………………………………………………………………………………………………………………

-

- AI-Native Threat Detection: Developing an automated, real-time cyber defense platform for identifying and mitigating known and unknown threats, including zero-day attacks.

- Privacy & Resilience: Using secure multi-party computation and federated learning to ensure user data remains private while improving systemic network resilience.

- Real-World Validation: Testing the 6G security framework across critical use cases such as connected healthcare, smart manufacturing, and maritime connectivity.

- Coordinating Institution: University College Dublin (UCD).

- Key Partners: Includes multinational companies, specialist SMEs (such as UCD spinout MBP Systems), and the global defense and aerospace giant Thales.

- Funding: Backed by the EU under the Horizon Europe program through the Smart Networks and Services Joint Undertaking (SNS JU).

-

- Remote Medical Operations: Securing ultra-low latency connections required for real-time remote robotic surgeries and critical patient monitoring.

- Data Privacy Compliance: Ensuring that highly sensitive personal health telemetry data remains private during processing.

- Interconnected Medical Devices: Safeguarding thousands of continuous-monitoring hospital IoT devices from unauthorized network penetration.

-

- Autonomous Industrial Operations: Protecting automated, closed-loop machinery and collaborative factory floor robots from data injection or remote hijacking.

- Digital Twin Environments: Modeling and simulating cyberattacks safely inside factory digital twins without disrupting ongoing physical production.

- Supply Chain Automation: Securing end-to-end logistics automation against zero-day vulnerabilities in multi-stakeholder industrial software.

- Autonomous Shipping & Logistics: Defending open-sea navigation, automated port loading systems, and vehicle-to-infrastructure communication channels.

- Critical Coastal Infrastructure: Ensuring stable, tamper-proof communications for offshore installations like deep-sea cargo networks and renewable energy hubs.

- Satellite-Terrestrial Handover: Securing the handoff of tracking data as vessels transition between ground stations and global satellite communication networks.

The SHIELD-6G platform utilizes AI-native, privacy-preserving, and automated technologies to establish a Cyber Threat Intelligence (CTI) pipeline tailored for 6G networks. These technologies allow multi-stakeholder networks to self-heal against cascading vulnerabilities without sharing raw data.

……………………………………………………………………………………………………………………………………………………………

References:

https://www.telecoms.com/5g-6g/european-consortium-launches-shield-6g-security-project

https://www.darkreading.com/cybersecurity-operations/eu-6g-network-security

linkedin.com/posts/bartsiniarski_shield6g-6g-cybersecurity-activity-7467489224217460736-A0yi

Analysis & Implications of the Communications Cybersecurity Information Sharing and Analysis Center (C2 ISAC)

Key Differences Between Network Cybersecurity and Control System Cybersecurity & Why It Matters

Anthropic’s Project Glasswing aims to reshape IT cybersecurity

Emerging Cybersecurity Risks in Modern Manufacturing Factory Networks

Cisco to lay off more than 4,000 as it shifts focus to AI and Cybersecurity

StrandConsult Analysis: European Commission second 5G Cybersecurity Toolbox report

GSA Meetup: Cyber Security Continues as Major Obstacle for IoT Adoption

Demythifying Cyber security: IEEE ComSocSCV April 19th Meeting Summary

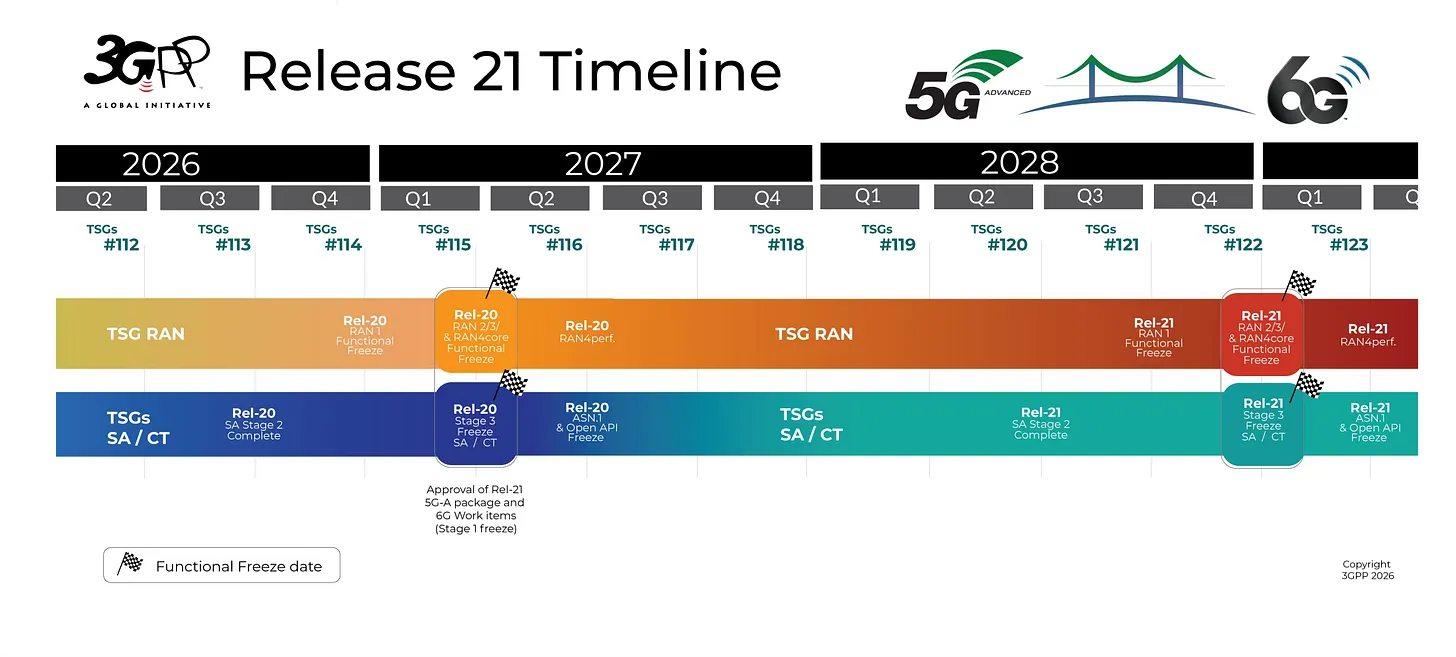

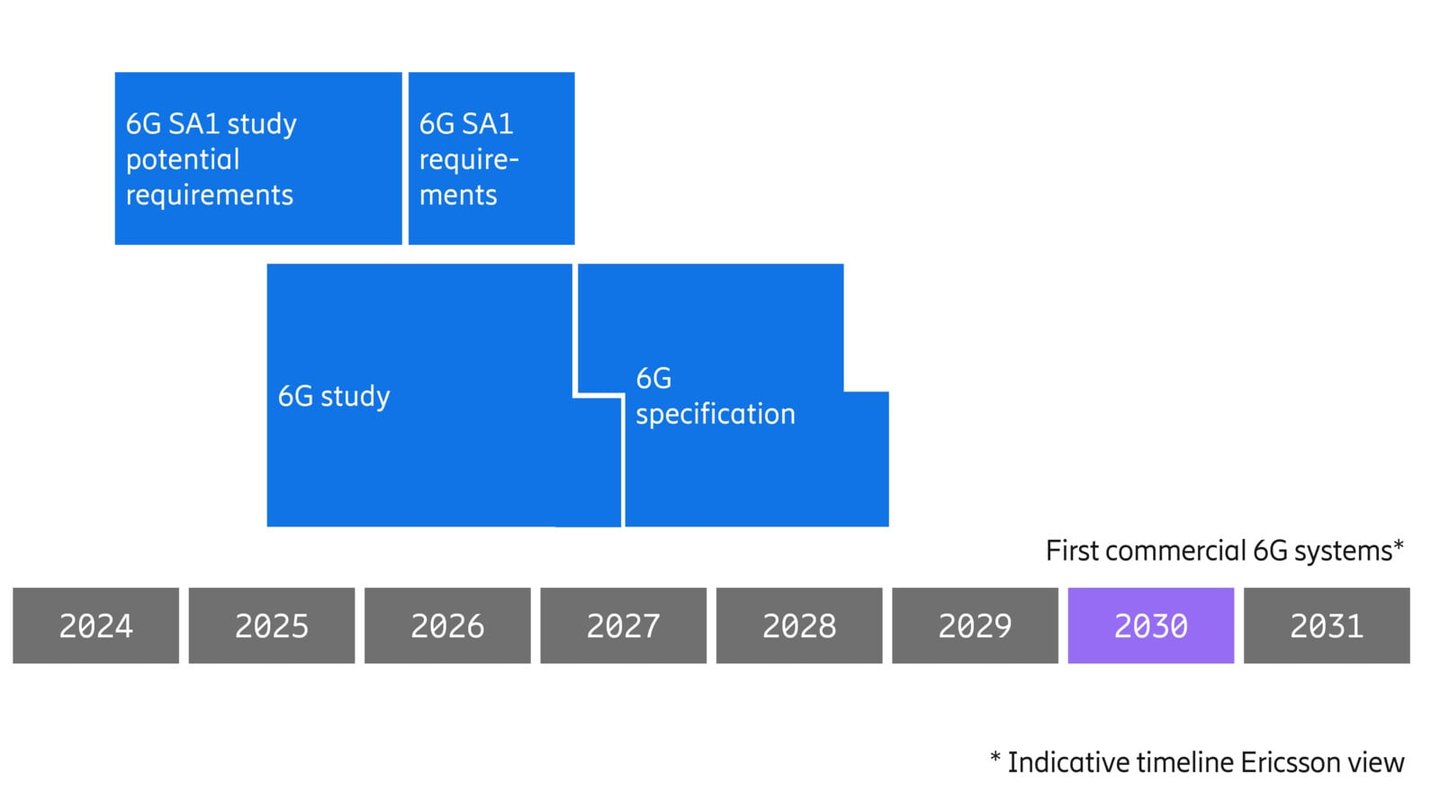

3GPP approves timelines for Release 21 which will specify 6G RAN, Core and 5G Advanced

At 3GPPs meeting last week in Singapore, Technical Specification Group (TSG) RAN #112 approved the full Release-21 timeline jointly proposed by the three TSG Chairs. On June 12th, more than 150 participants from the regions ICT community attended ‘3GPP 6G Standardization: From Study to Specification,’ featuring the combined technical leadership of 3GPP. Topics covered in the summit included the 3GPP Chairs’ analysis of progress this week on 5G Advanced work items and 6G studies across the TSGs. There were also expert overviews on some key topics: AI/ML, ISAC (integrated sensing and communications), Massive MIMO evolution, NTN standards cooperation and security considerations for the 3GPP 6G System.

This formally completes the first 6G study item in 3GPP and sets the stage for the third quarter this year in which 3GPP working groups must settle numerous questions, including the migration architecture that network operators have wanted a decision on for over a year. 3GPP TSG RAN Chairman Younsun Kim, PhD, Samsung, said during a joint session with the other two TSGs (SA and CT) that “no decisions were possible” on migration options, with input now hoped for at TSG RAN#113, scheduled for September 14–17, 2026 in Madrid, Spain. Vodafone warned in a 3GPP contribution titled, “Good migration option decisions in September need hardware impacting decisions now!” that the September decision point only works if the plenary stopped deferring decisions.

Some achievements at this 3GPP Singapore meeting:

- Over 590 standards delegates welcomed by our Hosts to Singapore.

- Social events and a Singapore Industry summit on 3GPP held.

- Singapore Ministry and Government visitors welcomed as guests.

- All Work Items and Study Items for 5G‑Advanced on schedule in Release‑

- 14 Study Items for 6G progressing.

- The TSG RAN Study on 6G Scenarios and requirements (TR 38.914) approved this week.

- First timeline for early 6G specifications approved (Rel-21).

3GPP’s Release 21 will comprise the first 6G specs as well as 5G-Advanced. Release 21 work items for 6G and 5G-Advanced are scheduled to be approved with a first functional freeze in March 2027 and a second freeze in June 2028, with a “checkpoint” in March 2028 for 80% of the work to be done. The stage 3 final freeze is set for December 2028. The full and final code freeze is scheduled for March 2029.

Guy Daniels wrote in a blog post titled, “Analysis of 3GPP RAN #112: Timeline locked but the migration question unanswered“:

There is a 3GPP structural oddity in the details. The March 2027 6G “package approval” is the approval of a placeholder whose RAN2/3/4 content is finalized three months later. This is deliberate concurrency, not an oversight, it’s how the 3GPP works. The normative engineering windows are equally tight: RAN1 runs Q2 2027 to Q3 2028; RAN2/3/4 run Q3 2027 to Q4 2028; six quarters each to specify a new radio generation.”

“The Scenarios and Requirements study is finished, but the political questions it deferred are not. The requirements now say what 6G must do. September begins the fight over what it will be.”

……………………………………………………………………………………………………………………………………………………………………………………………………………………………….

In a blog post summarizing last week’s plenary meeting, Ericsson said 6G standardization “is in full swing” and highlighted some of the early 6G decisions, including choices for waveform, modulation, channel coding, a basic security framework and supported bandwidths. The agreed 6G waveform is to use cyclic-prefix orthogonal frequency-division multiplexing (CP-OFDM) in the downlink. There are two options for uplink: CP-OFDM and discrete Fourier transform spread OFDM (DFT-s-OFDM). Supported bandwidths will range from 3MHz to 400MHz. 3GPP also agreed that 5G channel codes “will be largely reused” in 6G.

Here’s Ericsson’s timeline for 6G:

“6G is coming into focus…We are at a point now where a lot of pieces of the puzzle are starting to come together,” Gabriel Brown, senior principal analyst at Omdia, explained in a recent podcast with colleague and analyst Ruth Brown (no relation). The analysts also presented the 6G state of play at the 6G Summit hosted by ATIS’s Next G Alliance ahead of Network X Americas last month. Gabriel noted there has been a mindset shift among telcos about 6G from being “cautious” to “embracing it.” He said that the World Radiocommunication Conference next year (WRC-27) and the Summer Olympic Games in Los Angeles in 2028 will be important “checkpoints” for the anticipated early 2029 arrival of the 6G standards.

“[The LA Summer Olympics] is going to be an amazing opportunity for the U.S. ecosystem to showcase the potential of next-generation connectivity…It’s a chance to show how wireless can serve all the other industries there,” he added.

It will be important to watch for 3GPP’s September 2026 Madrid meeting output deliverables to get a sense of what functions and features might be in 6G RANs.

……………………………………………………………………………………………………………………………………………………………………………………….

6G Core Network:

The 6G core network architecture (such as signaling, network management, security, 6G specific features, and AI-native core architecture) will be defined in Release 21 Stage-2 (System & Architecture) scheduled to be completed in June 2028. Stage-3 (Protocol Specifications) is slated for December 2028 with ASN.1 & OpenAPI Freeze to be completed in March 2029.

3GPP decided NOT to liaise/contribute their 5G SA core network architecture specs to ITU-T, but ETSI rubber stamped them. Just as they did with IMT-2020 (5G), 3GPP will likely maintain exclusive development and control over all non-radio specifications for IMT-2030 (6G). Instead of formalizing them through ITU-T. 3GPP relies on its own Organizational Partners, e.g. ETSI and ATIS, to adopt the core network framework in their standards. 3GPP decided to bypass ITU-T for the 5G mobile core network, opting to develop 5G SA core network specs directly to ensure rapid, market-driven deployment.

……………………………………………………………………………………………………………………………………………………………………………………………

Addendum – 3GPP specs are NOT standards and have no legal standing:

What most, if not all, telecom trade publications (like this one) get completely wrong is that 3GPP does not produce standards, but specifications via their Releases. Those must be contributed, discussed, debated and approved by official SDOs like ITU-R and ETSI or other 3GPP members.

In the case of 5G/IMT 2020, ATIS presented all 3GPP RIT/SRIT specifications as contributions to ITU-R WP5D, which is 100% responsible for all IMT terrestrial radio interface standards (ITU-R recommendations). It should also be noted that ITU-R WP 5D has sole responsibility for IMT 2030/6G Frequency Arrangements which will be done after 6G frequencies are agreed at the ITU World Radiocommunication Conference (WRC-27),which is scheduled to take place from October 18 to November 12, 2027, in Shanghai, China.

“The 3GPP Technical Specifications and Technical Reports have, in themselves, no legal standing. They only become “official” when transposed into corresponding publications of the Partner Organizations (or the national / regional standards body acting as publisher for the Partner). At this point, the specifications are referred to as UMTS within ETSI and FOMA within ARIB/TTC.”

https://portal.etsi.org/new3g/specs/publications_partners.htm

From Qualcomm:

“3GPP Organization – Fixing three common misconceptions: 3GPP develops technical specifications, not standards. This is a subtle, but important organizational clarification. 3GPP is an engineering organization that develops technical specifications. These technical specifications are then transposed into standards by the seven regional Standards Setting Organizations (SSOs) that form the 3GPP partnership.”

https://www.qualcomm.com/news/onq/2017/08/understanding-3gpp-starting-basics

The Partnership Project is not a legal entity but is a collaborative activity between the following recognized Standards Development Organizations (SDO):

- The Association of Radio Industries and Businesses (ARIB) – Japan

- The Alliance for Telecommunications Industry Solutions (ATIS) – US

- China Communications Standards Association (CCSA) – China

- The European Telecommunications Standards Institute (ETSI) – Europe

- Telecommunications Standards Development Society (TSDSI) – India

- Telecommunications Technology Association (TTA) – South Korea

- Telecommunication Technology Committee (TTC) – Japan

The Partnership Project is entitled the “THIRD GENERATION PARTNERSHIP PROJECT” and may be known by the acronym “3GPP.”

………………………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.3gpp.org/news-events/3gpp-news/tsg112#:~:text=3GPP%20plenaries

https://www.3gpp.org/news-events/3gpp-news/rel21-timeline

https://6gfutures.substack.com/p/analysis-of-3gpp-ran-112-timeline

https://www.ericsson.com/en/blog/2026/6/6g-standardization-key-milestones-and-ran-decisions

https://www.3gpp.org/about-us/legal-matters

https://portal.etsi.org/new3g/specs/publications_partners.htm

https://www.lightreading.com/6g/it-s-official-6g-specs-are-set-for-early-2029

https://www.itu.int/en/ITU-R/study-groups/rsg5/rwp5d/imt-2030/Pages/default.aspx

Roles of 3GPP and ITU-R WP 5D in the IMT 2030/6G standards process

ITU-R M.[IMT-2030.EVAL] & ITU-R M.[IMT-2030.SUBMISSION] reports: Evaluation & Submission Guidelines for 6G RIT/SRITs (6G)

IMT-2030 (“6G”) Minimum Technology Performance Requirements for Radio Interface Technologies

Comparing AI Native mode in 6G (IMT 2030) vs AI Overlay/Add-On status in 5G (IMT 2020)

Analysis: Nvidia’s rumored new 6G AI-RAN – likely features/functions and industry impact

ITU-R WP 5D Timeline for submission, evaluation process & consensus building for IMT-2030 (6G) RITs/SRITs

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

Highlights of 3GPP Stage 1 Workshop on IMT 2030 (6G) Use Cases

Should Peak Data Rates be specified for 5G (IMT 2020) and 6G (IMT 2030) networks?

GSMA Vision 2040 study identifies spectrum needs during the peak 6G era of 2035–2040

Highlights and Summary of the 2025 Brooklyn 6G Summit

NGMN: 6G Key Messages from a network operator point of view

Nokia and Rohde & Schwarz collaborate on AI-powered 6G receiver years before IMT 2030 RIT submissions to ITU-R WP5D

Verizon’s 6G Innovation Forum joins a crowded list of 6G efforts that may conflict with 3GPP and ITU-R IMT-2030 work

Nokia Bell Labs and KDDI Research partner for 6G energy efficiency and network resiliency

Deutsche Telekom: successful completion of the 6G-TakeOff project with “3D networks”

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Qualcomm CEO: expect “pre-commercial” 6G devices by 2028

Ericsson and e& (UAE) sign MoU for 6G collaboration vs ITU-R IMT-2030 framework

Virtualization’s role in 5G Advanced (3GPP Release 18) and a proposed new hardware architecture

Ericsson’s June 2026 Mobility Report Highlights + AI impact on network traffic

Ericsson’s June 2026 Mobility report states that:

- 5G global subscriptions have now passed the 3 billion mark with the addition of 162 million in the first quarter of 2026.

- Half of the world’s mobile data traffic is now carried over 5G vs 48% at the end of 2025. It’s forecast to rise to 85% by the end of 2031.

- Mobile network data traffic growth exceeded expectations, at 22% between Q1 2025 and Q1 2026.

- Fixed Wireless Access (FWA) adoption is also growing, with around 70% of FWA service providers now offering the service over 5G.

- The number of commercial 5G SA network slicing offerings has increased from 65 to 84 in just 6 months.

- Cellular IoT connections are expected to approach 8 billion by the end of 2031

“With the upcoming transition to physical AI, traffic patterns will fundamentally shift as we move from centralized models in data centers to distributed, autonomous AI agents embedded across our device vehicles and cities, commonly connected by 5G,” said Ericsson CTO Erik Ekudden, in a statement accompanying the report.

“Mobile networks are no longer only about providing best-effort connectivity, they are becoming critical, intelligent infrastructure that meets diverse application needs, Reflecting part of this shift is the continued rise in new commercial service offerings based on 5G standalone network slicing and the number of communications service providers deploying 5G SA,” Ekudden said.

Image Credit: Ericsson

……………………………………………………………………………………………………………………………………………………………………….

Impact of Agentic AI workloads on network traffic:

The most critical engineering takeaway from the report is a profound asymmetry in data traffic growth, heavily driven by agentic AI workloads and user-generated content.

Key Insights:

- AI-driven applications – spanning smartphones, AI/AR smart glasses and autonomous vehicles – are inherently uplink heavy, generating continuous data streams that challenge traditional downlink-dominated traffic patterns.

- Uplink traffic growth is already outpacing downlink for many service providers, with field measurements indicating capacity constraints under peak load. Scenario modeling suggests that additional AI traffic will result in uplink traffic being three times higher in 2031 compared to 2025.

- Current networks are not dimensioned for sustained uplink demand, calling for a step change in design – from 5G software and hardware enhancements in the near term to 6G-native uplink innovations over the longer horizon.

- Traffic Inversion: Traditionally, cellular networks are architected and provisioned to handle heavily downlink-centric (DL) traffic patterns. However, the proliferation of multimodal generative AI and uplink-heavy applications is radically flipping this paradigm.

- Field Measurement Data: Out of 55 global operators analyzed, 43 experienced uplink (UL) growth rates outpaces DL growth. Crucially, 17 of those service providers reported UL expansion exceeding DL by a factor of 1.5x or higher.

- Projections: Ericsson’s scenario modeling suggests that cumulative AI-driven traffic could cause UL demands to spike threefold by 2031 compared to 2025 baselines.

- Near-Term: Immediate deployment of 5G RAN software optimizations and hardware refreshes. This includes pushing for 5G Standalone (SA) core migrations, leveraging AI-optimized Massive MIMO beamforming, and utilizing network slicing to guarantee bounded latency for critical UL channels.

- Long-Term: Transitioning to 6G-native uplink innovations. Early 6G standardization, targeted for finalization around 2028–2029, will focus deeply on AI-native architectures, Integrated Sensing and Communication (ISAC), and asymmetric air-interface designs natively optimized for continuous data streams.

Market Outlook:

Resolving these capacity constraints requires immediate, targeted infrastructure capital expenditure. While macro RAN spending has faced recent headwinds, the urgent necessity to re-dimension the air interface for an AI-centric world represents a powerful pipeline catalyst for Ericsson and its infrastructure rivals. Telco spending on RAN products has slumped from $45 billion in 2022 to $35 billion last year, according to analysts at Omdia, while Ericsson’s annual sales have dropped from SEK271.5 billion ($28.8 billion) to SEK236.7 billion ($25.1 billion) over this same period.

References:

https://www.ericsson.com/en/reports-and-papers/mobility-report/reports/june-2026

GSA: Global private mobile networks exceed 2,000 worldwide; Ericsson Private 5G from Verizon Business extends beyond U.S.

Ericsson reports 10% drop in 1st quarter sales; targets network growth

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

Ericsson and Intel collaborate to accelerate AI-Native 6G; other AI-Native 6G advancements at MWC 2026

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Nokia to showcase agentic AI network slicing; Ericsson partners with Ookla to measure 5G network slicing performance

China’s telecom industry rapid growth in 2025 eludes Nokia and Ericsson as sales collapse

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

Ericsson Mobility Report touts “5G SA opportunities”

GSA: Global private mobile networks exceed 2,000 worldwide; Ericsson Private 5G from Verizon Business extends beyond U.S.

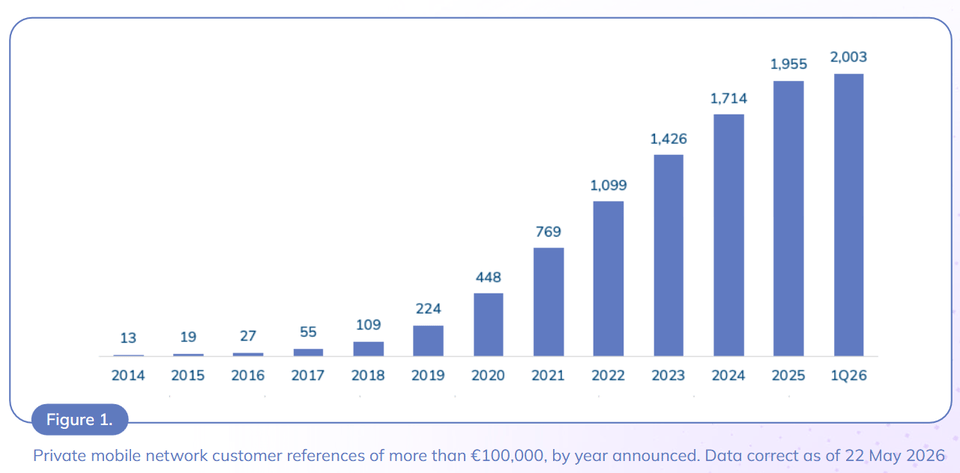

The number of worldwide private mobile networks that are worth more than €100,000 exceeds 2,000, according to the Global mobile Suppliers Association (GSA). Demand is being driven by the growing data, security, digitization and mobility requirements of modern enterprise and government entities. GSA said that at the end of 1Q2026, it had identified 2,003 organizations in 88 countries worldwide that had deployed one or more private mobile networks. The private mobile networks it counted had contract values of more than €100,000 (~$116,000). A further 178 private mobile networks are worth between €50,000 and €100,000, GSA said.

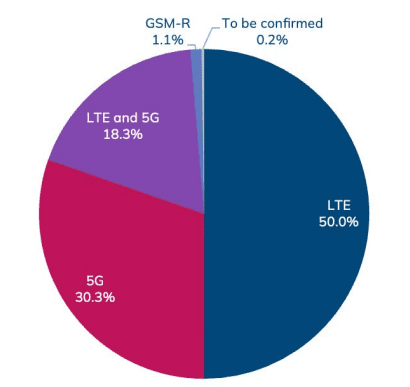

4G-LTE remains the dominant technology, accounting for 1,369 of the customers catalogued by the GSA, but 5G is inching up; 5G is deployed in 974 of the networks, often in conjunction with LTE, but 5G-only networks increased by one percentage point on Q4 2025 to account for 30.3% of customers. GSA said that 76% of the references are non-public and unique. Some industries are cagier than others– in sectors like military and defense, maritime, and the power plants space more than 80% of references are not in the public domain.

Image Source: GSA

Although the proportion of 5G only deployments makes up a significant number of references (30.3%), it must be noted that this number skews toward long-term trials and deployments within educational and test-bed or validation facilities, with a limited number running real operation in industrial situations.

………………………………………………………………………………………………………………………………………………………………………………………………………….

The top five markets are currently the US, Germany, the UK, China and Japan, but those markets were exceeded in growth terms in the first quarter of 2026 by another market in the top 10; Canada saw the number of customers of private mobile networks grow by 5% in Q1. The UK had the next-highest growth rate at 4%, followed by the US at 2% and Germany at 1%.

China is often reported to have a high number of private networks at more than 40,000, the GSA said. But it believes that many of those networks actually use public mobile networks and therefore do not meet its definition for inclusion in its report.

“As the report clearly shows, a large number and varied range of market participants are actively engaged in developing and delivering solutions for private mobile networks,” said GSA president Joe Barrett, in a statement accompanying the group’s latest Private Mobile Networks publication.

“With so much opportunity, and so many regulators planning initiatives to make spectrum available for LTE and 5G private usage, we expect significant market developments over the next couple of years,” Barrett said. Naturally, there is a strong correlation between the number of private mobile networks in a country and the availability of dedicated spectrum there. In addition, private mobile network deployments are mainly in high-income and upper-middle-income countries, according to the GSA.

The GSA did not specifically mention the high-income Middle Eastern markets in its report summary, but it’s probably safe to assume that countries like Oman will help to drive growth going forward. Port of Salalah in the south of Oman announced the launch of the country’s first fully managed private 5G network in partnership with incumbent telecoms operator Omantel. The network will support automation and accelerate the port’s digital transformation, boosting the efficiency of its logistics operations, it said. And both parties indicated that they expect the deal to kick-start the wider use of private enterprise 5G networks in Oman, looking specifically at ports, logistics and industry.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Ericsson Private 5G is now available through Verizon Business beyond U.S. borders. It’s targeted at global enterprises already using Ericsson technology in Verizon Business Private 5G Networks in the U.S., allowing them to extend it to international campuses. It offers a dual mode 4G and 5G network with global spectrum support

“Verizon Business can offer more optionality and flexibility to its private wireless customers who operate across international borders,” states the press release.

Hannes Ekström, Senior Vice President and Head of Customer Unit Verizon, Ericsson Americas, says: “Enterprises are rapidly embracing digital transformation, leveraging secure and high-performing private 5G networks as a key driver of innovation and efficiency. Our multinational customers in the U.S. have already unlocked significant growth through 5G-enabled private networks, and now they seek to replicate this success globally.”

“Through our collaboration with Verizon, we are expanding the reach of our Ericsson Private 5G solution to support Verizon Business’s international deployments, enabling seamless global operations. By simplifying 5G adoption and enhancing reliability, low latency, and security, we are empowering industries to harness next-generation connectivity and drive innovation on a global scale.”

“Verizon Business is proud of our expanding private wireless portfolio, and we’re committed to providing the best possible private wireless experience to our customers around the world,” said Robb Juliano, Vice President of 5G Acceleration, Verizon Business. “By extending the availability of Ericsson Private 5G outside of the U.S., we’re offering enterprises more flexibility in driving innovation, enhancing security, and optimizing operations with private wireless networks on a global scale.”

References:

https://gsacom.com/technology/private-mobile-networks/

https://gsacom.com/paper/private-mobile-networks-june-2026/

https://www.telecoms.com/5g-6g/private-mobile-networks-exceed-2-000-worldwide

https://www.ericsson.com/en/press-releases/2026/6/ericsson-private-5g-for-verizon-business

Private 5G networks move to include automation, autonomous systems, edge computing & AI operations

SNS Telecom & IT: Private 5G Market Nears Mainstream With $5 Billion Surge

SNS Telecom & IT: Private LTE & 5G Network Ecosystem – CAGR 22% from 2025-2030

SNS Telecom & IT: Mission-Critical Networks a $9.2 Billion Market

Verizon partners with Nokia to deploy large private 5G network in the UK

SNS Telecom & IT: Private 5G and 4G LTE cellular networks for the global defense sector are a $1.5B opportunity

HPE Aruba Launches “Cloud Native” Private 5G Network with 4G/5G Small Cell Radios

SNS Telecom & IT: Private 5G Network market annual spending will be $3.5 Billion by 2027

SNS Telecom & IT: Private 5G and 4G LTE cellular networks for the global defense sector are a $1.5B opportunity

Ericsson integrates Agentic AI into its NetCloud platform for self healing and autonomous 5G private networks