Direct-to-cell service

Ookla on the Global D2D Market

Direct-to-device (D2D) satellite connectivity is emerging as a practical extension of non-terrestrial networks (NTNs), enabling standard smartphones to communicate directly with satellite systems without specialized user equipment. Within the 3GPP ecosystem, NTN capabilities were standardized (3GPP specs become standards by being rubber stamped by ETSI and ITU-R) beginning with 3GPP Release 17, establishing a framework for satellite-terrestrial interoperability and expanding the potential reach of mobile broadband beyond the footprint of terrestrial radio access networks.

D2D services could reduce persistent coverage gaps, especially in rural, maritime, and other underserved environments where terrestrial deployment is constrained by economics or geography. However, commercially available services today remain limited, with most deployments focused on messaging and other low-throughput applications rather than full mobile broadband.

From a market perspective, D2D and NTN have broad implications for mobile network operators (MNOs), satellite operators, equipment vendors, and regulators. That strategic importance helps explain why companies such as Apple, Amazon, SpaceX, and AST SpaceMobile are investing in this segment, alongside broader ecosystem activity around 3GPP-based NTN architectures.

Image Credit: Ookla

Ookla® has contributed to the discussion with a high-resolution poster showing global Speedtest® usage data for D2D services, along with a detailed market study on the D2D landscape. The analysis is based on Android devices that register with D2D-capable satellite systems from Starlink, Skylo, and Lynk, providing an early empirical view of how NTN-based connectivity is being used in practice.

Looking ahead, continued investment in larger satellite constellations and additional spectrum holdings should improve D2D capacity, coverage, and service robustness. As the technology matures, the industry is likely to move from narrowband messaging toward richer data services, with 3GPP NTN providing the standardization path for broader ecosystem scale-up.

For mobile network operators, the long-term effect could be a rebalancing of investment priorities at the edge of network coverage, particularly in sparsely populated regions. That may reduce the incentive for some rural tower builds and alter the demand outlook for parts of the RAN infrastructure supply chain.

Looking ahead, continued investment in next-generation satellite constellations, coupled with expanded spectrum access, is expected to enhance D2D performance and capacity. Key players—including Starlink, AST SpaceMobile, and Amazon’s Project Kuiper—are targeting higher data rates and broader service capabilities, with the objective of extending beyond narrowband messaging to support more data-intensive applications.

For MNOs, the evolution of D2D introduces potential shifts in network planning and capital allocation, particularly at the margins of coverage. Satellite-based augmentation could reduce the economic rationale for terrestrial infrastructure deployment in sparsely populated areas, with downstream implications for tower companies and certain segments of the radio access network (RAN) supply chain.

From a policy perspective, D2D also has the potential to reshape universal service frameworks and coverage obligations. Regulators seeking to expand connectivity may increasingly incorporate NTN-based solutions into their policy toolkits, prompting a reassessment of long-standing assumptions regarding the role of terrestrial infrastructure in achieving nationwide coverage. In that sense, D2D is not just a satellite story. It is becoming a broader telecom architecture shaped by 3GPP specifications and the convergence of terrestrial and non-terrestrial mobile networks.

References:

Analyst firms wide forecasts for the LEO satellite direct-to-device (D2D) market

Ookla: D2D satellite connectivity surged 24.5% during last 9 months; Starlink’s footprint expansion leads the way

Ookla: Starlink a viable competitor for hybrid 5G/NTN services due to network performance improvements and larger coverage area

GSA: 5G Non Terrestrial Networks, 5G SA and 5G Advanced gain momentum

Analysis: Amazon <- Globalstar – a strategic move for D2D and spectrum parity

Direct-to-Device (D2D) satellite network comparison: Starlink V2 (Starlink Mobile) vs “Satellite Connect Europe”

Deutsche Telekom selects Iridium for NB-IoT direct-to-device (D2D) connectivity

Standards are the key requirement for telco/satellite integration: D2D and satellite-based mobile backhaul

MTN Consulting: Satellite network operators to focus on Direct-to-device (D2D), Internet of Things (IoT), and cloud-based services

Analyst firms wide forecasts for the LEO satellite direct-to-device (D2D) market

LEO satellite direct-to-device (D2D) technology looks promising. Telecom analyst firms see D2D as a fast-growing but still early-stage market, with forecasts ranging from roughly 22% to 49% revenue CAGR depending on scope and whether they are measuring total D2D services or smartphone satellite D2D specifically. But that’s not happening now. T-Mobile chief Srini Gopalan, who said the service so far had generated “a lot less usage” than anticipated.

The most common near-term view is that basic D2D will add modest operator revenue at first, but the long-term market could become multi-billion-dollar as broadband and richer services mature. Here are a few analyst forecasts:

- MarketsandMarkets projects the D2D market to rise from USD 0.57 billion in 2025 to USD 2.64 billion by 2030, a 35.6% CAGR.

- Mordor Intelligence projects the direct-to-device satellite connectivity market from USD 4.08 billion in 2025 to USD 13.80 billion by 2031, a 22.37% CAGR.

- Omdia forecasts smartphone satellite D2D revenue to reach USD 11.99 billion by 2030, with a 49.4% revenue CAGR from 2026 to 2030.

- Counterpoint Research expects 46% of all smartphones shipped by 2030 to be D2D-capable. That implies D2D is moving from a niche satellite feature toward a mainstream handset capability, driven by chipset integration and broader device support.

- Juniper Research thinks the number of monthly active users will top 150 million by 2031. The analyst firm suggests a temporary access model, similar to roaming or travel eSIMs, where consumers purchase access in a particular area for a set period. Juniper thinks connectivity alone won’t be enough to attract consumers. It believes operators will have to bundle the satellite service into rewards programs or roaming access.

- Analysys Mason expects operators launching D2D in 2026 to see about a 1% annual revenue uplift from basic services alone, with much larger upside once broadband D2D becomes available.

- TelecomTV reports a similar view from Analyst Brad Grivner, who says D2D could give MNOs around a 1% annual revenue uplift and also improve retention and upsell opportunities.

The spread in forecasts mostly reflects different definitions of the market, different start dates, and whether the analyst counts only current narrowband services or also future broadband D2D. In practical terms, the consensus is that D2D will start as a coverage and messaging feature, then evolve into a broader connectivity platform as device support and satellite capacity scale.

Analysts consistently point to 3GPP NTN standardization (rubber stamped by ETSI and ITU-R), more satellite-ready smartphones, and large-scale LEO deployments as the main catalysts. They also emphasize emergency messaging, rural coverage, IoT, industrial connectivity, and enterprise resilience as the first meaningful demand pools. D2D market growth is being driven by a mix of coverage gaps, new device support, and expanding enterprise use cases. The strongest themes across analyst and industry reports are universal connectivity, IoT demand, LEO satellite buildout, and 3GPP NTN standardization.

Image Credit: Digital Regulation Platform

…………………………………………………………………………………………………………………………………………………………..

Main D2D growth drivers:

-

Coverage expansion. Analysts say D2D is filling a major gap in rural, remote, maritime, and disaster-prone areas where terrestrial networks are weak or unavailable.

-

3GPP NTN standards. Standardized non-terrestrial networking is making satellite connectivity more practical for mainstream devices and accelerating ecosystem adoption.

-

LEO constellation growth. More low-Earth-orbit satellites, along with falling launch costs and better satellite economics, are increasing capacity and improving latency.

-

Smartphone integration. As more phones become satellite-capable, D2D can move beyond niche emergency features into broader consumer usage.

-

Enterprise IoT demand. Logistics, mining, agriculture, utilities, and energy firms want reliable connectivity for remote assets, monitoring, and worker safety.

-

Disaster resilience. Climate-related outages and emergency-response needs are pushing governments and operators toward backup connectivity solutions.

-

Carrier-satellite partnerships. Cooperation between MNOs and satellite operators is speeding commercialization and helping services reach scale.

The D2Dmarket is still starting with messaging, emergency connectivity, and narrowband IoT, but analysts expect growth to broaden as device support and satellite capacity improve. In short, D2D grows fastest where it solves a clear pain point: no coverage, weak resilience, or expensive remote connectivity.

…………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://www.lightreading.com/satellite/making-the-most-of-satellite-d2d

Ookla: D2D satellite connectivity surged 24.5% during last 9 months; Starlink’s footprint expansion leads the way

Ookla: Starlink a viable competitor for hybrid 5G/NTN services due to network performance improvements and larger coverage area

GSA: 5G Non Terrestrial Networks, 5G SA and 5G Advanced gain momentum

Analysis: Amazon <- Globalstar – a strategic move for D2D and spectrum parity

Direct-to-Device (D2D) satellite network comparison: Starlink V2 (Starlink Mobile) vs “Satellite Connect Europe”

Deutsche Telekom selects Iridium for NB-IoT direct-to-device (D2D) connectivity

Standards are the key requirement for telco/satellite integration: D2D and satellite-based mobile backhaul

MTN Consulting: Satellite network operators to focus on Direct-to-device (D2D), Internet of Things (IoT), and cloud-based services

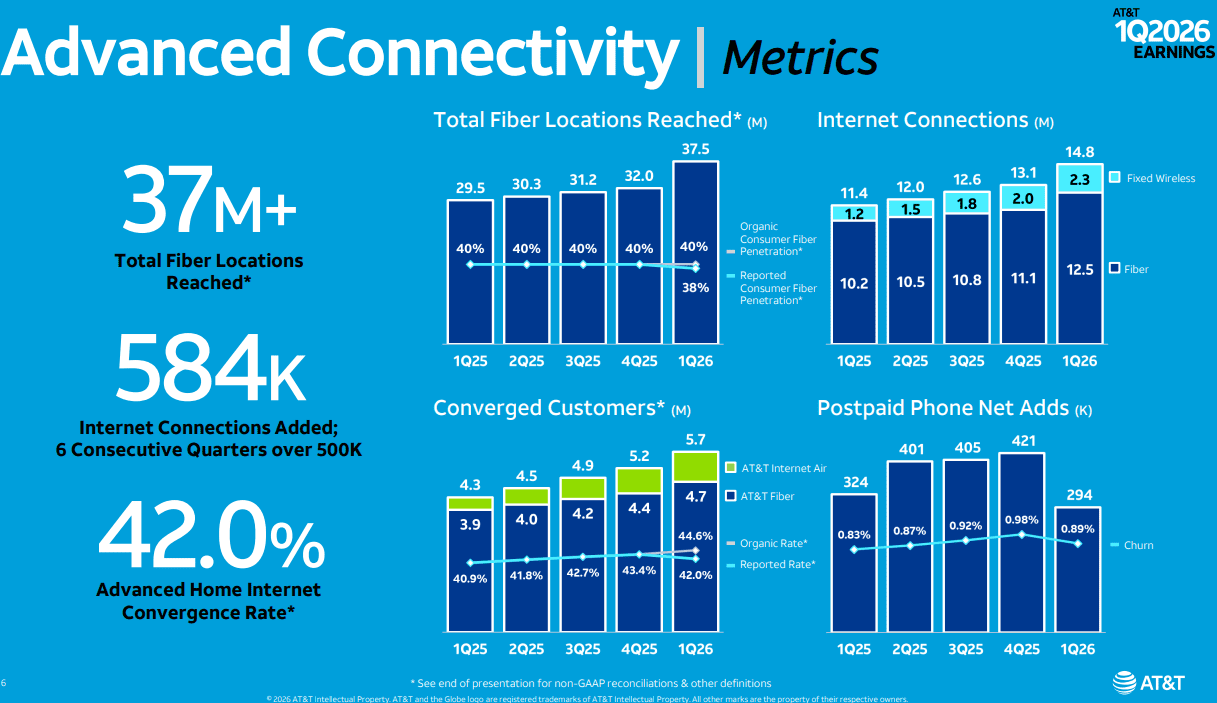

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

AT&T reported first-quarter results today, achieving its fastest-ever year-over-year organic growth in its advanced connectivity convergence rate, with nearly 45% of advanced home internet subscribers also choosing AT&T wireless. Customers are increasingly purchasing their internet and wireless together from AT&T, highlighting the strength of the company’s differentiated, investment-led strategy to drive converged advanced connectivity at scale.

“We saw our best first quarter ever for Advanced Connectivity internet customer net additions, demonstrating the solid foundation of assets we have built,” said John Stankey, AT&T Chairman and CEO. “We’re uniquely positioned to deliver more of what customers want — fiber and 5G all from one provider on the nation’s largest advanced converged network, backed by the AT&T Guarantee. The actions we’ve taken this quarter are evidence of how we are improving the customer value proposition, scaling faster, and accelerating growth.”

AT&T reported $31.5 billion in consolidated operating revenues, representing a 2.9% year-over-year (YoY) increase and outperforming Street estimates of $31.22 billion. This growth was largely driven by the Advanced Connectivity segment, which generated $22.15 billion in consumer revenues, up from $20.97 billion in the prior-year period.

- Wireless Performance: Mobility services posted mostly flat $16.94 billion in revenue, compared to $16.65 billion in Q1 2025.

- Legacy Decommissioning: Legacy revenues fell 25.3% YoY to $1.8 billion. The aggressive copper-to-fiber migration continues, with 85% of wire centers now approved for legacy service cessation.

- Strategic Sunsetting: 30% of these wire centers are slated for total decommissioning by late 2026, coinciding with the loss of 270,000 DSL subscribers this quarter.

The shift toward high-speed, durable connectivity is evidenced by the growth of AT&T’s Fiber and Fixed Wireless Access (FWA) portfolios.

- Fiber Penetration: AT&T recorded 292,000 fiber net additions, bringing the total subscriber base to 12.5 million. The current passings stand at 37.5 million locations, with 32.7 million owned/operated and 4.8 million via joint ventures (JVs).

- FWA Momentum: AT&T Internet Air added 239,000 customers in the quarter (up from 181,000 in Q1 2025), reaching a total of 1.73 million subscribers.

- Roadmap to 60 Million: AT&T remains on track to reach 60 million fiber locations by 2030 through organic expansion, the Gigapower JV, and open-access agreements.

AT&T is evolving its “NetworkCo” model to optimize capital intensity and market reach.

- Lumen Asset Integration: Recently acquired fiber assets from Lumen will be transferred into a JV structure. CFO Pascal Desroches expects to finalize an agreement with an equity partner for these assets in 2H 2026.

- Convergence and “One Connect”: The “One Connect” platform is the cornerstone of AT&T’s converged strategy.

- Bundle Adoption: 42% of advanced home internet customers (5.68 million) also subscribe to mobile services.

- Fiber-Mobile Synergy: Among fiber-specific customers, the mobility bundle penetration rate is 40.2% (4.74 million).

- The “One Connect” Roadmap: CEO John Stankey views the platform as an iterative engine, beginning with BYOD (Bring Your Own Device) and eventually expanding into tailored family plans.

“We made further progress at positioning AT&T as the preferred provider for connecting consumers and businesses to the internet. We closed our transaction with Lumen, ahead of schedule, adding 1.1 million fiber customers, and over 4 million fiber locations. We’re pleased with the progress we’re making as we integrate these assets in several major metro areas and position the business for faster growth. Early indicators are positive. We now offer fiber services throughout our distribution channels in these areas, which has driven sales activity well above pre-transaction trends. We’re executing the steps to scale engineering, construction and service delivery in the acquired geographies, expected as we move into the back half of the year, will achieve steady improvement in fiber and wireless customer growth in these areas. When we focus on customers needs and invest in the experience and products they want, we find success, and in the first quarter, we gave customers more reasons to choose AT&T. We expanded the AT&T guarantee to cover internet Air and launched a new flagship app to deliver a simple digital-first experience to customers.

We also launched AT&T OneConnect, which enables customers to easily connect all their eligible devices at home and on the go, and eliminates the need to buy internet access twice. We refreshed our Unlimited Your Way plans to deliver more value. All these moves are based on a consistent set of principles that drive our approach to serving customers the way they want to be served, with offers that deliver simplicity, value and choice and converged connectivity.

After years of industry-leading investments in our fiber and wireless network, we believe that we have now established a structural advantage that others will not catch. We reached more than 90 million customer locations across the country with our advanced internet services, over either fiber or 5G. We believe this provides us with more scalable reach and converged connectivity than any of our peers, including a meaningful scale and performance advantage in fiber. This is an advantage we’re growing as we ramp our deployment at a faster pace than anyone else. Today, we reach over 37 million customer locations with fiber, and we’re on track to reach 60 million plus locations by the end of the decade.”

NTNs and D2D:

Regarding its choice of AST SpaceMobile for direct-to-device (D2D) connectivity for its smartphones, Stankey said, “I think it’s natural that we work with LEO partners that have the capabilities to solve that problem, to integrate those offerings into our services,” Stankey said Tuesday on AT&T’s Q1 2026 earnings call. “My goal would be that I have a good, strong wholesale relationship, and it may not just be with one of them. It may be with more than one of them.”

Besides AST SpaceMobile, Stankey said he expects SpaceX/Starlink to have a “robust direct-to-device capability,” as well as Amazon Leo and potentially a fourth NTN satellite internet company. SpaceX is developing a next-generation D2D offering with spectrum it’s acquiring from EchoStar, and Amazon plans to introduce a new D2D offering in 2028 amid its recent deal to acquire Globalstar. AT&T has a deal with Amazon Leo to connect business customers that are out of reach of terrestrial wireless and wireline networks, but it has not yet signed a D2D-specific deal with Amazon’s satellite and services unit.

Market Analysis – The Fiber Coverage Gap:

Despite strong growth, analysts remain cautious regarding AT&T’s convergence ceiling. With fiber currently available in only about 20% of the U.S., the primary concern is whether AT&T can maintain competitive parity in non-fiber regions.

- Potential Underperformance Risk: In markets where AT&T relies on legacy copper or wholesale third-party access, it may struggle to match the churn reduction and ARPU (Average Revenue Per User) lift seen in its “Fiber + Wireless” footprint.

- Mitigation Strategy: The success of the “60-million-locations fiber by 2030” roadmap which is the primary driver of AT&Ts increased spending. Also, the scaling of Internet Air as a “bridge” technology will be critical in preventing regional underperformance.

- 2026 Milestone: AT&T expects to exceed 40 million total fiber locations by the end of 2026.

- Build Cadence: The company is targeting an organic deployment pace of 4 million new locations per year by the end of 2026. After 2026, this rate is projected to increase to approximately 5 million additional spots annually.

- Funding Mechanism: To support this acceleration, AT&T plans to reinvest $3.5 billion in cost savings specifically into the fiber build-out over the 2026–2027 period.

- “There’s no path for AT&T to have a fiber footprint that will cover more than a third of the country. Will AT&T be consigned to losing share in the other two thirds?” MoffettNathanson analyst Craig Moffett asked in a research note to clients posted after AT&T’s earnings call.

Despite the high CapEx, AT&T CFO Pascal Desroches reaffirmed that the company remains on track to deliver $18 billion+ in free cash flow (FCF) for 2026.

………………………………………………………………………………………………………………………………………………………………………

References:

https://www.lightreading.com/satellite/at-t-might-look-beyond-ast-spacemobile-for-d2d

Analysis: AT&T’s $250B network investment to advance U.S. connectivity

AT&T and AWS to deliver last mile connectivity for AI workloads; AT&T Geo Modeler™ AI simulation tool

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

AT&T’s convergence strategy is working as per its 3Q 2025 earnings report

AT&T deploys nationwide 5G SA while Verizon lags and T-Mobile leads

AT&T to buy spectrum licenses from EchoStar for $23 billion

AT&T grows fiber revenue 19%, 261K net fiber adds and 29.5M locations passed by its fiber optic network

Ookla: D2D satellite connectivity surged 24.5% during last 9 months; Starlink’s footprint expansion leads the way

Introduction:

Direct-to-device (D2D) satellite connectivity, primarily driven by Starlink deployments, continues to accelerate despite nascent market maturity. Ookla’s latest analysis reveals that while global D2D connections surged 24.5% from July 2025 to March 2026—spurred by Starlink’s expansion into Chile, Ukraine, Peru, and the UK—penetration among mobile subscribers remains under 1.5% in leading markets.

Starlink dominates D2D traffic, accounting for the bulk of connections alongside contributions from Skylo and Lynk Global. Initial use cases center on non-terrestrial network (NTN) extensions for SMS and geolocation in coverage gaps, with next-gen systems eyeing 5G NR integration via acquired spectrum like EchoStar’s holdings. Regional growth offset US/Canada dips, potentially tied to T-Mobile and Rogers introducing D2D surcharges amid seasonal patterns.

Image Credit: Ookla

Market Share Breakdown:

Adoption Barriers:

Terrestrial networks already blanket 96% of the global population per GSMA Intelligence, curbing urgency for D2D beyond edge cases. Low awareness and constrained throughput—versus 5G benchmarks—further limit uptake, though link budgets and multi-orbit architectures promise evolution.

Future Outlook:

Based on the February GSA (Global mobile Suppliers Association) report, Direct-to-Device (D2D) services have achieved commercial launch in 15 markets, with 61 countries currently in the evaluation, testing, or deployment phases of Non-Terrestrial Network (NTN) partnerships. Starlink dominates the landscape with 59 partnerships, followed by AST SpaceMobile at 28. In China—a market excluded from GSA data—ABI Research indicates that China Unicom and China Telecom are already leveraging the Tiantong GEO system for D2D. China Mobile is utilizing the BeiDou constellation while planning integrations with emerging LEO networks. To evolve from narrowband emergency services to full mobile broadband, all three Tier-1 operators are aligning with state-backed LEO mega-constellations, specifically Project Guowang and G60 Qianfan (Spacesail).

For Mobile Network Operators (MNOs), D2D integration significantly alters CAPEX/OPEX strategies. In rural or remote areas, MNOs must now run a cost-benefit analysis: deploy traditional macro sites or utilize satellite-based coverage to eliminate dead zones. While Starlink argues that D2D allows MNOs to reduce terrestrial investment, the technology is largely limited to outdoor environments. Given that approximately 80% of mobile traffic is generated indoors—where satellite link budgets typically fail—terrestrial densification remains critical.

From a regulatory standpoint, the rise of NTN-D2D complicates Universal Service Fund (USF) allocations. In the U.S., the FCC is currently assessing how the $9 billion 5G Fund for Rural America should account for D2D capabilities. Ultimately, while D2D may solve the “dead zone” problem for outdoor mobility, it serves as a complement to, rather than a replacement for, high-capacity terrestrial infrastructure. Enhanced spectrum harmonization and handset chipsets could pivot D2D from supplemental to resilient 5G NTN layer, challenging capex models for rural densification. Network operators must navigate billing handoffs and QoS parity to unlock scale.

References:

https://www.ookla.com/articles/measuring-the-direct-to-device-d2d-marketplace-2026

US Mobile’s new bundle combines its multi-network mobile service with Starlink residential internet

Analysis: Amazon <- Globalstar – a strategic move for D2D and spectrum parity

GSA: 5G Non Terrestrial Networks, 5G SA and 5G Advanced gain momentum

Direct-to-Device (D2D) satellite network comparison: Starlink V2 (Starlink Mobile) vs “Satellite Connect Europe”

Standards are the key requirement for telco/satellite integration: D2D and satellite-based mobile backhaul

Deutsche Telekom selects Iridium for NB-IoT direct-to-device (D2D) connectivity

MTN Consulting: Satellite network operators to focus on Direct-to-device (D2D), Internet of Things (IoT), and cloud-based services

Blue Origin announces TeraWave – satellite internet rival for Starlink and Amazon Leo

China ITU filing to put ~200K satellites in low earth orbit while FCC authorizes 7.5K additional Starlink LEO satellites

Starlink doubles subscriber base; expands to to 42 new countries, territories & markets

Amazon Leo (formerly Project Kuiper) unveils satellite broadband for enterprises; Competitive analysis with Starlink

Analysis: Amazon <- Globalstar - a strategic move for D2D and spectrum parity

Overview:

Amazon said today that it will acquire Globalstar in an $11.57 billion deal, bolstering its fledgling satellite internet business as it tries to catch up with Elon Musk’s Starlink.

Amazon is accelerating its Project Kuiper deployment, aiming to launch approximately 3,200 Low Earth Orbit (LEO) satellites by 2029. To meet regulatory milestones, nearly 50% of the constellation must be operational by the July deadline, with commercial satellite broadband services slated for a soft launch later this year.

The acquisition of Globalstar augments Amazon’s Direct-to-Device (D2D) connectivity offerings. Globalstar’s current architecture is optimized for low-bandwidth, high-reliability mobile links that bypass traditional terrestrial RAN infrastructure. This capability is vital for ubiquitous emergency services and IoT connectivity in non-terrestrial network (NTN) white spaces. Through this deal, Amazon expects to operationalize its own D2D offerings by 2028.

IMPORTANT: It should be noted that ONLY 3GPP is developing the standards for NTNs – ITU-R and ETSI SDOs are simply rubber stamp SDOs for 3GPP NTN specs.

“There are billions of customers out there living, traveling, and operating in places beyond the reach of existing networks, and we started Amazon Leo to help bridge that divide,” said Panos Panay, Senior Vice President of Devices & Services, Amazon. “By combining Globalstar’s proven expertise and strong foundation with Amazon’s customer-obsession and innovation, customers can expect faster, more reliable service in more places—keeping them connected to the people and things that matter most. We’re excited to support Apple users through the Leo D2D system, and look forward to working with mobile network partners to help extend coverage to every corner of the planet,” Panay added.

The Competitive Landscape: Starlink vs. Kuiper:

SpaceX’s Starlink currently maintains a significant lead with over 9 million global subscribers. While Starlink’s core business remains high-throughput fixed wireless via proprietary user terminals, it is aggressively pursuing D2D through spectrum-sharing partnerships with Mobile Network Operators (MNOs) like T-Mobile.

Industry analysts suggest that acquiring Globalstar is a “spectrum play.” Armand Musey of Summit Ridge Group noted that the deal allows Amazon to secure a critical spectrum position and potentially leapfrog Starlink in D2D deployment timelines. Furthermore, Amazon’s proposed data center constellation is engineered for a massive scaling of network capacity, intended to exceed current LEO benchmarks.

“Amazon has been falling behind Starlink on satellite broadband. Acquiring Globalstar allows them to catch up on their D2D spectrum position, and leap ahead on D2D deployment,” said Armand Musey, president & founder of Summit Ridge Group.

Amazon LEO’s proposed data center constellation would dwarf Starlink’s current network by several magnitudes:

The Apple-Globalstar Ecosystem:

Crucially, Globalstar’s existing partnership with Apple remains intact. Globalstar currently provides the L-band connectivity powering Apple’s Emergency SOS and Find My features. Amazon has confirmed it will honor these agreements, maintaining the 2024 framework where Apple invested $1.5 billion for a 20% equity stake to expand the constellation to 54 satellites. See References below.

Market Consolidation and Valuations:

The move follows a broader trend of sector consolidation as players seek the scale required to compete with SpaceX’s vertical integration and launch frequency.

- Deal Metrics: Amazon’s acquisition values Globalstar at approximately $10.8 billion ($90/share), representing a 31% premium over the pre-announcement close.

- Regulatory Path: The merger is expected to close in 2025, pending FCC approval and the achievement of specific deployment KPIs. FCC Chair Brendan Carr indicated the agency remains “open-minded” regarding the consolidation.

Author’s Opinion & Analysis (aided by perplexity.ai):

Amazon’s Globalstar acquisition is a strong strategic move towards D2D, but it is more a spectrum-and-regulatory shortcut than a pure technology leap. The telecom significance is that Amazon is buying not just satellites, but licensed Mobile Satellite Spectrum (MSS), operational know-how, and an immediate path into direct-to-device connectivity that would otherwise take years to assemble.

From a telecom perspective, the key asset is spectrum parity. Globalstar holds licensed MSS spectrum in the L/S-band ranges used for satellite mobile services, and that spectrum is hard to replicate because the FCC has previously rejected or constrained new entrants in those bands. That makes the deal valuable less as a fleet expansion play and more as a way to secure a legally usable radio layer for D2D, which is not at all guaranteed.

Amazon’s stated plan is to combine Globalstar’s spectrum and MSS operations with Amazon Leo to deliver D2D services beginning in 2028, with claims of higher spectrum efficiency than legacy direct-to-cell systems. In telecom terms, that implies Amazon wants to move from “coverage extension” into a more integrated NTN architecture that can support voice, text, and eventually data services at scale. That’s certainly a tall order!

Against Starlink, this is a defensive and offensive move all at the same time. Starlink already has a lead in satellite scale and has commercialized carrier partnerships like T-Mobile’s direct-to-cell offering, so Amazon’s problem has been less launch capacity than spectrum and service readiness. Buying Globalstar narrows that gap by giving Amazon a ready-made regulatory and spectrum base instead of forcing it to negotiate every D2D pathway from scratch.

Against carriers, the move is more nuanced. Amazon is not simply disintermediating mobile operators; its own materials describe D2D as a way to help MNOs extend voice, text, and data beyond terrestrial reach. That suggests a wholesale or partner model, but the long-term competitive risk is obvious: if Amazon owns the satellite layer and the device/service stack, carriers may become optional distribution partners rather than network gatekeepers.

The phrase “spectrum parity” is the real strategic clue. In telecom, constellation size matters, but spectrum rights determine whether a constellation can actually deliver service with usable link budgets, device compatibility, and regulatory clearance. Globalstar’s spectrum therefore acts like a license to compete, not just a frequency block.

This also helps explain why the deal is strategically defensive for Amazon. Without Globalstar, Amazon would face a slower, less certain path through band planning, interference disputes, and NTNspecific regulatory work, especially in crowded MSS allocations. In that sense, the acquisition is a classic telecom play: buy scarce spectrum, then scale the network around it.

The biggest near-term risk to this deal is regulatory. The transaction will need FCC and likely antitrust review, and Amazon will also have to navigate the Apple/Globalstar relationship because Globalstar powers Apple’s Emergency SOS service. That creates both transition risk and potential bargaining leverage for Apple, which could complicate service continuity and deal terms.

Technically, D2D is still constrained by small link budgets, handset antenna limits, and the need to prioritize messaging and emergency services before richer data use cases. Even if Amazon claims better spectrum efficiency, the first commercially meaningful services will likely remain low-throughput, coverage-oriented offerings rather than full terrestrial substitutes. So the real competition is not “satellite internet for phones” in the consumer broadband sense, but who controls the premium coverage layer for dead zones, emergency service, enterprise continuity, and carrier augmentation.

In conclusion, Amazon is making a category-defining infrastructure purchase, not just a corporate acquisition. If approved, it gives Amazon a credible D2D spectrum position, reduces its regulatory latency, and turns Amazon Leo into a more complete and highly competitive NTN platform and D2D service provider.

……………………………………………………………………………………………………………………….

References:

https://www.aboutamazon.com/news/company-news/amazon-globalstar-apple

Amazon Leo (formerly Project Kuiper) unveils satellite broadband for enterprises; Competitive analysis with Starlink

Blue Origin announces TeraWave – satellite internet rival for Starlink and Amazon Leo

NBN selects Amazon Project Kuiper over Starlink for LEO satellite internet service in Australia

Amazon launches first Project Kuiper satellites in direct competition with SpaceX/Starlink

Emergency SOS: Apple iPhones to be able to send/receive texts via Globalstar LEO satellites in November

FCC proposes regulatory framework for space-mobile network operator collaboration

AT&T deal with AST SpaceMobile to provide wireless service from space

Starlink Direct to Cell service (via Entel) is coming to Chile and Peru be end of 2024

Starlink’s Direct to Cell service for existing LTE phones “wherever you can see the sky”

Keysight Technologies Demonstrates 3GPP Rel-19 NR-NTN Connectivity in Band n252

Keysight Technologies, Inc. has demonstrated the first end-to-end New Radio Non-Terrestrial Network (NR-NTN) connection in 3GPP band n252 under Release 19 specifications, achieved in collaboration with Samsung Electronics using Samsung’s next-generation commercial NR modem chipset (part number not stated). The live trial, conducted at CES 2026 in Las Vegas, validated satellite-to-satellite (SAT-to-SAT) mobility and cross-vendor interoperability, establishing a key milestone for direct-to-cell (D2C) satellite communications and NTN commercialization.

The successful validation of band n252 marks the first public confirmation of this spectrum band in an operational NTN system. Band n252 is expected to be a foundational component for upcoming low Earth orbit (LEO) constellations targeting global broadband and IoT coverage. This result demonstrates tangible progress toward large-scale NTN integration supporting ubiquitous, standards-based connectivity for consumers, connected vehicles, IoT devices, and critical communications.

Together with earlier demonstrations in bands n255 and n256, Keysight and Samsung have now validated all major NR-NTN FR1 frequency bands end-to-end. This consolidation enables ecosystem participants—including modem vendors, satellite network operators, and device manufacturers—to analyze cross-band mobility, inter-satellite handovers, and radio performance under consistent, controlled NTN emulation conditions.

The demonstration leveraged Keysight’s NTN Network Emulator Solutions to replicate multi-orbit LEO scenarios, emulate SAT-to-SAT mobility, and execute complete end-to-end routing while supporting live user traffic over the NTN link. When paired with Samsung’s chipset, the setup verified standards compliance, user throughput performance, and multi-vendor interoperability, providing a high-fidelity validation environment that accelerates system testing and time-to-market for NR-NTN deployments targeted for global scaling in 2026.

This integration underscores the readiness of 3GPP Release 19-compliant NTN technologies to transition from proof-of-concept trials to operational field testing, supporting the broader industry goal of realizing seamless terrestrial–non-terrestrial 5G networks within the Rel-19 framework and paving the way for future 6G NTN evolution.

For network operators, device OEMs, and satellite providers, this consolidation of NTN FR1 coverage provides a reference environment to evaluate cross‑band handovers, inter‑satellite mobility, and multi‑vendor interoperability before field deployment. By moving live NR‑NTN testing with commercial‑grade silicon into an emulated LEO constellation environment, the solution is positioned to reduce integration risk, compress trial timelines, and accelerate commercialization of direct‑to‑cell NTN services anticipated to scale from 2026.

Peng Cao, Vice President and General Manager of Keysight’s Wireless Test Group, Keysight, said:

“Together with Samsung’s System LSI Business, we are demonstrating the live NTN connection in 3GPP band n252 using commercial-grade modem silicon with true SAT-to-SAT mobility. With n252, n255, and n256 now validated across NTN, the ecosystem is clearly accelerating toward bringing direct-to-cell satellite connectivity to mass-market devices. Keysight’s NTN emulation environment enables chipset and device makers a controlled way to prove multi-satellite mobility, interoperability, and user-level performance, helping the industry move from concept to commercialization.”

Resources:

About Keysight Technologies:

At Keysight (NYSE: KEYS), we inspire and empower innovators to bring world-changing technologies to life. As an S&P 500 company, we’re delivering market-leading design, emulation, and test solutions to help engineers develop and deploy faster, with less risk, throughout the entire product life cycle. We’re a global innovation partner enabling customers in communications, industrial automation, aerospace and defense, automotive, semiconductor, and general electronics markets to accelerate innovation to connect and secure the world. Learn more at Keysight Newsroom and www.keysight.com.

………………………………………………………………………………………………………………………………………….

References:

https://www.telecoms.com/satellite/samsung-and-keysight-show-off-continuous-ntn-connectivity

Huge significance of EchoStar’s AWS-4 spectrum sale to SpaceX

EchoStar has entered into a definitive agreement to sell its entire portfolio of prized AWS-4 [1.] and H-block spectrum licenses to SpaceX in a deal valued at approximately $19 billion. The spectrum purchase allows SpaceX to start building and deploying upgraded, laser-connected satellites that the company said will expand the cell network’s capacity by “more than 100 times.”

This deal marks EchoStar/Dish Network’s exit as a mobile network provider (goodbye multi-vendor 5G OpenRAN) which once again makes the U.S. wireless market a three-player (AT&T, Verizon, T-Mobile) affair. Despite that operational failure, the deal helps EchoStar address regulatory pressure and strengthen its financial position, especially after AT&T agreed to buy spectrum licenses from EchoStar for $23 billion. ![]()

The companies also agreed to a deal that will enable EchoStar’s Boost Mobile subscribers to access Starlink direct-to-cell (D2C) service to extend satellite service to areas without mobile network service.

……………………………………………………………………………………………………………………………………………………………

Note 1. The AWS-4 spectrum band (2000-2020 MHz and 2180-2200 MHz) is widely considered the “golden band” for D2C services. Unlike repurposed terrestrial spectrum, the AWS-4 band was originally allocated for Mobile Satellite Service (MSS).

…………………………………………………………………………………………………………………………………………………………..

The AWS-4 spectrum acquisition transforms SpaceX from a D2C partner into an owner that controls its dedicated MSS spectrum. The deal with EchoStar will allow SpaceX to operate Starlink direct-to-cell (D2C) services on frequencies it owns, rather than relying solely on those leased from mobile carriers like T-Mobile and other mobile operators it’s working with (see References below).

Roger Entner wrote that SpaceX is now a “kingmaker.” He emailed this comment:

“With 50 MHz of dedicated spectrum, the raw bandwidth that Starlink can deliver increases by 1.5 GBbit/s. This is a substantial increase in speed to customers. The math is 30 bit/s/hz which is LTE spectral efficiency x 50 MHz = 1.5 Gbit/s. “This agreement makes Starlink an even more serious play in the D2C market as it will have first hand experience with how to utilize terrestrial spectrum. It is one thing to have this experience through a partner, this a completely different game when you own it.”

The combination of T-Mobile’s terrestrial network and Starlink’s enhanced D2C capabilities allows T-Mobile to market a service with virtually seamless connectivity that eliminates outdoor dead zones using Starlink’s spectrum.

“For the past decade, we’ve acquired spectrum and facilitated worldwide 5G spectrum standards and devices, all with the foresight that direct-to-cell connectivity via satellite would change the way the world communicates,” said Hamid Akhavan, president & CEO, EchoStar. “This transaction with SpaceX continues our legacy of putting the customer first as it allows for the combination of AWS-4 and H-block spectrum from EchoStar with the rocket launch and satellite capabilities from SpaceX to realize the direct-to-cell vision in a more innovative, economical and faster way for consumers worldwide.”

“We’re so pleased to be doing this transaction with EchoStar as it will advance our mission to end mobile dead zones around the world,” said Gwynne Shotwell, president & COO, SpaceX. “SpaceX’s first generation Starlink satellites with Direct to Cell capabilities have already connected millions of people when they needed it most – during natural disasters so they could contact emergency responders and loved ones – or when they would have previously been off the grid. In this next chapter, with exclusive spectrum, SpaceX will develop next generation Starlink Direct to Cell satellites, which will have a step change in performance and enable us to enhance coverage for customers wherever they are in the world.”

EchoStar anticipates this transaction with SpaceX along with the previously announced spectrum sale will resolve the Federal Communications Commission’s (FCC) inquiries. Closing of the proposed transaction will occur after all required regulatory approvals are received and other closing conditions are satisfied.

The EchoStar-Space X transaction is structured with a balanced mix of cash and equity plus interest payments:

-

Cash and Stock Components: SpaceX will provide up to $8.5 billion in cash and an equivalent amount in its own stock, with the valuation fixed at the time the agreement was signed. This 50/50 structure provides EchoStar with immediate liquidity to address its creditors while allowing SpaceX to preserve capital for its immense expenditures on Starship and Starlink development. A pure stock deal would have been untenable for EchoStar, which is saddled with over $26.4 billion in debt, while a pure cash deal would have strained SpaceX.

-

Debt Servicing: In a critical provision underscoring EchoStar’s dire financial state, SpaceX has also agreed to fund approximately $2 billion of EchoStar’s cash interest payments through November 2027.

-

Commercial Alliance: The deal establishes a long-term commercial partnership wherein EchoStar’s Boost Mobile subscribers will gain access to SpaceX’s next-generation Starlink D2C service. This provides a desperately needed lifeline for the struggling Boost brand. More strategically, this alliance serves as a masterful piece of regulatory maneuvering. It allows regulators to plausibly argue that they have preserved a “fourth wireless competitor,” providing the political cover necessary to approve a deal that permanently cements a three-player terrestrial market.

The move comes amid rapidly increasing U.S. mobile data usage. In 2024, Americans used a record 132 trillion megabytes of mobile data, up 35% over the prior all-time record, industry group CTIA said Monday.

About EchoStar Corporation:

EchoStar Corporation (Nasdaq: SATS) is a premier provider of technology, networking services, television entertainment and connectivity, offering consumer, enterprise, operator and government solutions worldwide under its EchoStar®, Boost Mobile®, Sling TV, DISH TV, Hughes®, HughesNet®, HughesON™, and JUPITER™ brands. In Europe, EchoStar operates under its EchoStar Mobile Limited subsidiary and in Australia, the company operates as EchoStar Global Australia. For more information, visit www.echostar.com and follow EchoStar on X (Twitter) and LinkedIn.

©2025 EchoStar, Hughes, HughesNet, DISH and Boost Mobile are registered trademarks of one or more affiliate companies of EchoStar Corp.

About SpaceX:

SpaceX designs, manufactures, and launches the world’s most advanced rockets and spacecraft. The company was founded in 2002 to revolutionize space technology, with the ultimate goal of making life multiplanetary. As the world’s leading provider of launch services, SpaceX is leveraging its deep experience with both spacecraft and on-orbit operations to deploy the world’s most advanced internet and Direct to Cell networks. Engineered to end mobile dead zones around the world, Starlink’s satellites with Direct to Cell capabilities enable ubiquitous access to texting, calling, and browsing wherever you may be on land, lakes, or coastal waters.

………………………………………………………………………………………………………………………………………………………………………………………………

References:

Mulit-vendor Open RAN stalls as Echostar/Dish shuts down it’s 5G network leaving Mavenir in the lurch

AT&T to buy spectrum Licenses from EchoStar for $23 billion

SpaceX launches first set of Starlink satellites with direct-to-cell capabilities

Starlink’s Direct to Cell service for existing LTE phones “wherever you can see the sky”

Space X “direct-to-cell” service to start in the U.S. this fall, but with what wireless carrier? (T-Mobile)

KDDI unveils AU Starlink direct-to-cell satellite service

Starlink Direct to Cell service (via Entel) is coming to Chile and Peru be end of 2024

Telstra selects SpaceX’s Starlink to bring Satellite-to-Mobile text messaging to its customers in Australia

Telstra partners with Starlink for home phone service and LEO satellite broadband services

One NZ launches commercial Satellite TXT service using Starlink LEO satellites

FCC to investigate Dish Network’s compliance with federal requirements to build a nationwide 5G network

In a letter to Charlie Ergen, the chairman and co-founder of network operator EchoStar, Federal Communications Commission (FCC) chairman Brendan Carr wrote that the agency’s staff would investigate the company’s compliance with requirements to build a nationwide 5G network as per the terms of its federal spectrum licenses. EchoStar owns both Dish Network and Boost Mobile’s wireless service. Dish has said its 5G network covers more than 268 million people and has met all of its regulatory requirements.

In 2019, the U.S. government set several construction milestones for Dish Network to maintain cellular licenses worth billions of dollars. The company agreed to meet specific buildout obligations in connection with a number of spectrum licenses across several different bands. In particular, the FCC agreed to relax some of EchoStar’s then-existing buildout obligations in exchange for EchoStar’s commitment to put its licensed spectrum to work deploying a nationwide 5G broadband network. EchoStar promised—among other things—that its network would cover, by June 14, 2025, at least 70% of the population within each of its licensed geographic areas for its AWS-4 and 700 MHz licenses, and at least 75% of the population within each of its licensed geographic areas for its H Block and 600 MHz licenses.

“The FCC structured the buildout obligations to prevent spectrum warehousing and to ensure that Americans would gain broader access to high-speed wireless services, including in underserved and rural areas.”

Ergen said that the company has worked collaboratively with FCC leaders since it launched its first pay-TV satellite more than 30 years ago. He added that EchoStar’s network creates American jobs and furthers a critical Trump administration priority of ensuring “the United States is at the forefront of wireless leadership and that our infrastructure is free of Chinese vendors.” Full text of his statement is below.

Ergen is reportedly working to pivot his satellite TV business from a declining pay-TV model to a “direct-to-device” business that connects smartphones from space, among other services. Carr laid out plans for the agency to seek public comment on how mobile-satellite services could use some spectrum that EchoStar currently holds. EchoStar is among a group of satellite companies that already hold licenses to provide mobile-device links, though they lack the dense network of modern satellites that Starlink has at its disposal.

SpaceX said in an April letter that EchoStar’s spectrum in the 2 Gigahertz band “remains ripe for sharing among next-generation satellite systems.” The company urged the commission to launch a new rule-making process to add new competitors to the band. EchoStar has accused SpaceX of a spectrum land grab.

Separately, Dish Network has spent years wiring thousands of cellphone towers to help Boost become a wireless operator that could rival AT&T, Verizon and T-Mobile, but the project has been slow-going. Boost’s subscriber base has shrunk in the five years since Ergen bought the brand from Sprint so it is not at all competitive with its big three U.S. cellular rivals.

Dish Network under FCC microscope, Art by Midjourney for Fierce Network

……………………………………………………………………………………………………………………………………………………………….

Charlie Ergen’s Statement in Response to FCC Letter:

“We have worked collaboratively with FCC leaders since we launched our first DBS satellite more than 30 years ago. Today, we are proud to have invested tens of billions to deploy the world’s largest 5G Open RAN network – primarily using American vendors – across 24,000 5G sites, to offer broadband service to over 268 million people nationwide. Through this deployment, which is possible thanks to scores of tower climbers, engineers, and partners, we have met or exceeded all of the commitments we have entered into with the FCC to date. And our work is not yet finished as we continue to deploy and invest in our network. Not only does our network create American jobs and a competitive alternative to incumbent wireless carriers, it also furthers another critical Trump Administration priority: deploying Open RAN to ensure the United States is at the forefront of wireless leadership and that our infrastructure is free of Chinese vendors. Thanks to our nationwide pricing model and agreements with partner carriers, Boost Mobile is available at affordable prices to Americans across the country – including in rural and hard to reach communities. Indeed, our new buildout deadlines – which are consistent with FCC practice under the past two Administrations where the Wireless Bureau granted hundreds of buildout extensions – came with additional, substantial pro-competitive commitments that EchoStar has fulfilled. As we continue to invest in and expand our terrestrial network deployment, we are also working to provide Open RAN direct-to-device satellite technology, bringing additional connectivity to all Americans in the U.S. and around the world.

EchoStar worked tirelessly to establish 3GPP NTN standard for D2D. With D2D 3GPP standards now complete, EchoStar has the global capability in terms of expertise, spectrum, and ITU priority to bring this to fruition. We are now testing new S-band services in both North America and Europe, and this year we launched a LEO satellite with several more planned in the coming months. We look forward to continuing this important work to help the Administration and FCC continue to deliver for the American people.”

References:

https://prod-i.a.dj.com/public/resources/documents/Carr-Ergen-letter.pdf

https://www.fierce-network.com/wireless/fcc-questions-echostar-about-how-its-using-5g-spectrum

https://www.tipranks.com/news/the-fly/echostar-confirms-fcc-letter-to-company-ergen-makes-statement

Dish Network & Nokia: world’s first 5G SA core network deployed on public cloud (AWS)

Dish Network to FCC on its “game changing” OpenRAN deployment

Analysis of Dish Network – AWS partnership to build 5G Open RAN cloud native network

KDDI unveils AU Starlink direct-to-cell satellite service

KDDI-owned AU [1.] launched Japan’s first direct satellite service, connecting 40% of remote island and mountain populations in Japan that terrestrial networks cannot now reach. The new service, called AU Starlink Direct, is also available to subscribers of Okinawa Cellular, a KDDI-owned company serving the group of islands located in southern Japan. KDDI and Okinawa Cellular will start providing AU Starlink Direct, a direct to cell service between satellites and AU smartphones, on April 10, 2025. This is the first Direct to Cell satellite service in Japan.

Note 1. AU is a brand marketed by KDDI in the main islands of Japan and by Okinawa Cellular in Okinawa for their mobile cellular services. acquired au in 2001, initially through a merger of DDI, KDD, and IDO, and subsequently absorbing au’s parent company. KDDI continues to operate the AU brand for its mobile services.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

The service is compatible with 50 smartphone models and is available free of charge to au users from today for the time being without the need to apply. Subscribers of AU and Okinawa Cellular whose iPhone and Android devices support satellite mode can try the service.

Source: Sean Prior/Alamy Stock Photo

Although AU has nearly 100% population coverage, mobile operators’ 4G and 5G networks effectively serve only about 60% of the population because mobile signal cannot reach remote islands and mountainous areas. The new AU Starlink Direct service allows the operator to bridge this digital divide by enabling customers in these dead zones to connect directly to a Starlink satellite using compatible smartphones.

The service can be used to communicate with family members and friends, in emergencies, etc., even in mountainous areas, island areas, and campgrounds and at sea where it is difficult to provide a telecommunications environment. KDDI is expanding the AU coverage area to all of Japan to bring the experience of “Connecting the Unconnected. wherever you see the sky.”

Gwynne Shotwell, President & COO of SpaceX, said: “I’m very excited to bring direct-to-cell phone connectivity to Japan through KDDI, the first in Asia and one of the first in the world. Both Starlink and direct-to-cell are game-changing technologies, making connecting the unconnected simple and bringing potentially life-saving capability to the people of Japan for disaster and other emergency responses.”

KDDI conducted a successful field test of AU Starlink Direct in Kumejima, Okinawa Prefecture, nearly six months ago.

References:

https://newsroom.kddi.com/english/news/detail/kddi_nr-533_3818.html

https://newsroom.kddi.com/english/news/detail/kddi_nr-299_3557.html

KDDI Partners With SpaceX to Bring Satellite-to-Cellular Service to Japan

SpaceX and KDDI to test Satellite Internet in Japan

KDDI Deploys DriveNets Network Cloud: The 1st Disaggregated, Cloud-Native IP Infrastructure Deployed in Japan

AWS Integrated Private Wireless with Deutsche Telekom, KDDI, Orange, T-Mobile US, and Telefónica partners

Samsung and KDDI complete SLA network slicing field trial on 5G SA network in Japan

KDDI claims world’s first 5G Standalone (SA) Open RAN site using Samsung vRAN and Fujitsu radio units

Samsung vRAN to power KDDI 5G network in Japan

One NZ launches commercial Satellite TXT service using Starlink LEO satellites

New Zealand telco One NZ has commercially launched its Satellite TXT service to eligible phone customers [1.] enabling them to communicate via Starlin/SpaceX’s network of Low Earth orbit (LEO) satellites at no extra cost as long as they have a clear line of sight to the sky. The initial TXT service will take longer to send and receive TXT messages. In many cases, TXT messages will take 3 minutes. However, at times it may take 10 minutes or longer, especially during the first few months. As the service matures and more satellites are launched, we expect delivery times to improve. The type of eligible phone you are using, where you are in New Zealand and whether a satellite is currently overhead will all have an impact on whether your TXT is sent or received and how long it takes.

Note 1. There are only four handsets that can currently use of Satellite TXT: Samsung’s Galaxy Z Flip6, Z Fold6, and S24 Ultra, plus the OPPO Find X8 Pro. One NZ said the handset line-up will expand during the course of next year (2025).

“We have lift-off! I’m incredibly proud that One NZ is the first telecommunications company globally to launch a nationwide Starlink Direct to Mobile service, and One NZ customers are among the first in the world to begin using this groundbreaking technology,” exclaimed Joe Goddard, experience and commercial director at One NZ. He said coverage is available across the whole of New Zealand including the 40% of the landmass that isn’t covered by terrestrial networks – plus approximately 20 km out to sea. “Right from the start we’ve said we would keep customers updated with our progress to launch in 2024 and as the technology develops. Today is a significant milestone in that journey,” he added.

April 2023’s partnership with Starlink coincided with the beginning of a new era for One NZ, which up until that point had operated under the Vodafone brand. At the time, One NZ tempered expectations by making it clear the service wouldn’t launch until late 2024.

SpaceX in October finally received permission to begin testing Starlink’s direct-to-cell capabilities with One NZ. Later that same month, One NZ reported that its network engineers in Christchurch were successfully sending and receiving text messages over the network. “We continue to test the capabilities of One NZ Satellite TXT, and this is an initial service that will get better. For example, text messages will take longer to send but will get quicker over time,” said Goddard. He also went to some lengths to point out that Satellite TXT “is not a replacement for existing emergency tools, and instead adds another communications option.”

One NZ offered a few tips to help their customers use the service:

- To TXT via satellite, you need a clear line of sight to the sky. Unlike other satellite services, you don’t need to hold your phone up towards the sky.

- Keeping your TXT short will help. You can also prepare your TXT and press send as soon as you see the One NZ SpaceX banner appear on-screen.

- To check if your TXT has been delivered, check the time stamp next to your TXT. On a Samsung or OPPO, tap on the message.

- Remember to charge your phone or take a battery pack if you are out adventuring.

One NZ vs T-Mobile Direct to Cell Service:

New Zealand’s terrain – as varied and at times challenging as it is – can be covered by far fewer LEO satellites than the U.S. where T-Mobile has announced Direct to Cell service using Starlink LEO satellites. T-Mobile was granted FCC approval for the service in November, and is now signing up customers to test the US Starlink beta program “early next year.”

References:

https://one.nz/why-choose-us/spacex/

https://www.telecoms.com/satellite/one-nz-claims-direct-to-cell-bragging-rights-over-t-mobile-us

Space X “direct-to-cell” service to start in the U.S. this fall, but with what wireless carrier?

Space X “direct-to-cell” service to start in the U.S. this fall, but with what wireless carrier?

Starlink Direct to Cell service (via Entel) is coming to Chile and Peru be end of 2024

Starlink’s Direct to Cell service for existing LTE phones “wherever you can see the sky”

Satellite 2024 conference: Are Satellite and Cellular Worlds Converging or Colliding?