Author: Alan Weissberger

Amazon Leo plans to deploy 5,105 D2D to interoperate with Apple devices

Executive Summary:

Amazon Leo, the #1 competitor to SpaceX’s Starlink for LEO satellite internet, is proposing a new Direct to Device (D2D) constellation comprising 5,105 low-Earth orbit (LEO) satellites that will work in concert with satellites Amazon is acquiring from Globalstar.

Amazon Leo has disclosed additional technical and regulatory detail on its proposed global direct‑to‑device (D2D) low Earth orbit (LEO) constellation, envisioned to comprise 5,105 satellites and to operate in conjunction with D2D capacity obtained via Amazon’s planned acquisition of Globalstar.

System architecture and spectrum use:

According to an FCC application filed by Kuiper Systems LLC on Saturday, July 25, the Amazon Leo D2D system is designed to leverage Mobile‑Satellite Service (MSS) spectrum as well as selected terrestrial mobile bands to deliver “ubiquitous global coverage.” The constellation will employ D2D‑optimized spacecraft using service links in the 1.6–2.4 GHz range, supported by feeder links and TT&C in Ka‑ and V‑band. Outside the US, Amazon plans to utilize additional available L‑band and S‑band allocations for service links to expand geographic reach and regulatory flexibility.

In a Monday technical blog post, Amazon Leo outlined a five‑shell orbital architecture, with three mid‑latitude shells designed to serve densely populated regions and two high‑latitude shells to extend coverage into remote geographies, including polar areas. Amazon reiterated that the D2D constellation is being engineered to interoperate with Apple devices (including iPhone and Apple Watch) and to complement its Kuiper broadband network, which is expected to enter commercial service later this year.

Integration with Globalstar and optical ISLs:

The Amazon Leo D2D constellation will incorporate optical inter‑satellite links (OISLs) to integrate the new D2D system with existing Amazon Leo satellite infrastructure and to “work in close concert” with the Globalstar MSS constellation in the 1.6–2.4 GHz band, assuming timely closing of the transaction. Amazon states that it will mitigate inter‑system interference between the Amazon Leo D2D system and Globalstar’s HIBLEO‑4, HIBLEO‑X, and planned C‑3 MSS operations via unified global network management and coordinated controls.

The proposed $11.5 billion Amazon–Globalstar deal remains under active regulatory review. Amazon Leo has previously indicated that its own D2D constellation is targeted for launch around 2028, positioning the system as a smartphone‑ and device‑centric coverage layer beyond the reach of terrestrial radio access networks and as a competitor or complement to emerging D2D offerings from SpaceX, AST SpaceMobile, and others. Amazon has highlighted canonical D2D use cases, including emergency messaging, in‑vehicle connectivity, and a broad range of IoT applications.

The potential role of Amazon’s D2D platform within the new US rural‑coverage D2D joint venture formed by AT&T, T‑Mobile, and Verizon remains unspecified.

Satellite lifecycle, deorbiting, and debris mitigation:

Each Amazon Leo D2D satellite is designed with a nominal operational life of six to eight years, contingent on orbital shell parameters. Amazon plans active end‑of‑life management and deorbiting, reserving approximately 40% of each satellite’s propellant for “disposal operations” to support controlled removal from orbit.

The FCC filing also provides additional detail on collision‑risk management and debris‑mitigation strategies. To reduce the probability of fragmentation events, Amazon has engineered propellant tanks to leak rather than burst under most failure modes, including micrometeoroid and orbital‑debris impacts, and has characterized tank behavior under high‑velocity impact conditions. The constellation will be monitored on a 24/7 basis for conjunction and collision risk, and each satellite will be equipped with onboard propulsion and maneuvering capability to perform collision‑avoidance maneuvers with respect to other spacecraft and tracked objects.

References:

https://www.lightreading.com/satellite/amazon-leo-files-plan-to-deploy-5-105-d2d-satellites

Cheap Chinese AI Models: Unappreciated Threat to U.S. Hyperscaler AI Dominance

Introduction:

IEEE Techblog readers are keenly aware of the stupendous AI capex that has eliminated most hyperscaler free cash flow. There’s also the ROI question when there’s no “killer app” or a clear way to monetize AI services. And let’s not forget issues like: the competition for AI benchmark bragging rights. price per token, rack density, and power consumption-per-dollar.

Now the next AI battleground will be competition from Chinese open-weight models, which are pushing AI toward commoditization faster than many U.S. hyperscalers expected. That shift could quietly erode the economics of the entire AI infrastructure stack.

Raffi Krikorian, the chief technology officer at Mozilla, which runs the Firefox browser, switched to Chinese AI startup Moonshot’s Kimi K3 for many of his day-to-day activities within days of the new, powerful model’s launch more than a week ago. “It just seems snappier,” Krikorian said of K3, comparing it with the acclaimed, higher-priced Claude Fable chatbot from Anthropic, the San Francisco private AI company with a $1 trillion assessed market value. Earlier, he had been using another strong Chinese model, Z.ai’s GLM-5.2, for everyday tasks such as managing his calendar, documents, and email.

Krikorian is among a growing number of Americans turning to Chinese AI systems, which are gaining traction worldwide because they are more affordable and increasingly efficient. U.S. companies such as cryptocurrency exchange Coinbase have said they are switching to Chinese AI models to help reduce costs. Their growing popularity has frustrated some U.S. tech giants, but barring an outright ban, these models are likely to keep attracting independent software developers in the U.S. and beyond.

The shift from training to inference:

The AI buildout is moving from model training toward sustained inference, and that changes the economics of the stack. Training demands enormous one-time bursts of compute, but inference creates continuous load on accelerators, interconnect, storage, and power systems, which means utilization and token pricing now matter as much as raw model capability.

That is where Chinese open-weight models matter most. Reports indicate that some are 60% to 90% cheaper than leading U.S. AI offerings, while still being “good enough” for a large share of enterprise and developer workloads.

Why open weight matters technically:

Open-weight models reduce deployment friction by allowing organizations to download, modify, and run models on their own infrastructure rather than through a centralized API. NTIA has noted that this can broaden access and accelerate innovation, but it also shifts responsibility for integration, safety, and lifecycle management onto deployment.

From an infrastructure perspective, that means AI demand becomes more distributed. Instead of concentrating in a small number of hyperscale regions, workloads can move into private clouds, regional facilities, enterprise data centers, and even edge-adjacent environments, changing traffic patterns and backend topology.

Impact on hyperscaler design:

The first-order risk for hyperscalers is not loss of raw demand; it is lower monetization per unit of demand. If users route routine inference to cheaper Chinese models, the same physical infrastructure may carry more tokens but generate less revenue, pressuring the economics of GPU clusters, accelerator networking, and power-hungry cooling systems.

That is a serious issue because modern AI facilities are purpose-built systems. They rely on dense GPU racks, low-latency fabrics, liquid cooling, and carefully engineered power distribution, all of which are justified by high utilization and strong margins. If the average workload shifts to lower-value inference, the return on those assets falls even if the machines stay busy.

Network and power consequences:

The networking impact is equally important. More self-hosted and regionally deployed inference increases east-west traffic inside enterprise environments and raises demand for metro transport, interconnect, and secure private connectivity, rather than only for giant centralized AI campuses.

Power and cooling are the other pressure points. AI infrastructure already consumes substantial electrical power and water, and inference-heavy systems can run continuously, making thermal design and power delivery central to total cost of ownership. If cheaper models fragment the market across more sites, the industry may need more distributed capacity without the same revenue density to support it.

The strategic takeaway:

For U.S. AI companies and hyperscalers, the threat from Chinese open-weight models is best understood as commoditization of inference. The frontier race may continue at the top end, but the commercial center of gravity is shifting toward lower-cost, portable models that reduce lock-in and weaken pricing power across the stack. The infrastructure question is no longer whether AI demand will grow; it is whether the industry can preserve enough margin, utilization discipline, and network economics to make that growth pay.

……………………………………………………………………………………………………………………………………………………………………….

Open-weight AI model landscape

- Chinese open-weight models are strongest on cost and deployability. That makes them especially disruptive for inference-heavy workloads, where price per token and operational control matter most.

- U.S. closed models remain strongest on managed-service depth and frontier capability. Their advantage is less about openness and more about product integration, reliability, and enterprise tooling.

- For infrastructure operators, the key issue is workload migration. Open-weight models can move inference from hyperscale APIs into private clouds, regional facilities, and enterprise data centers, changing network and power demand patterns.

- The strategic tradeoff is control versus simplicity. Open models lower vendor lock-in, but they increase responsibility for GPU capacity, MLOps, safety, observability, and lifecycle management.

…………………………………………………………………………………………………………………………………………………………………….

References:

Hyperscaler AI Race: Soaring Capex Wipes Out Free Cash Flow; AGI and Digital Gods

| Company | 2024 (Actual) | 2025 (Actual) | 2026 (Current Guidance / Est) | 2027 (Projected) |

|---|---|---|---|---|

| 📦 Amazon | $53B | $112B | $195B – $210B | $230B – $260B |

| 🔍 Alphabet (Google) | $51B | $104B | $195B – $205B | $240B – $280B |

| 💻 Microsoft | $56B | $108B | $185B – $195B | $220B – $250B |

| ♾️ Meta | $38B | $85B | $125B – $145B | $150B – $180B |

| 🗄️ Oracle | $13B | $25B | $45B – $50B | $55B – $65B |

| 🧮 Combined Aggregate | $211B | $434B | $745B – $805B | $895B – $1,035B |

The huge increase in hyperscaler capex, wipes out their free cash flow (revenues-expenses is now negative for all but Microsoft). The shift in focus by investors from earnings to free cash flow marks a turning point in market perceptions. The correct way to describe free cash flow is the cash flow a company generates during a period of time that is available to be paid to the company’s shareholders and debtholders.Companies with negative free cash flow are only able to cover the interest and principal on their debt by additional borrowing or by issuing new equity. In other words, cash is flowing from investors to the company, not the other way around. In a financial crisis, investors become unwilling to support companies not able to cover interest and principal, with the result being a cascade of defaults and runs on financial institutions.

A major concern with the massive AI-capex which has occurred during the last two years is that much of it is debt financed. As the real cost of generative AI-tokens is becoming clear, lower priced Chinese competitors are emerging, and AI customers are beginning to economize on their use of AI. As a result, investors are becoming increasingly alarmed about whether U.S. AI firms will be able to cover their debt obligations. AI-capex has been the main, and perhaps only driver of U.S. economic growth. If more companies announce negative free cash flows, that increase in magnitude, the financial system and overall economy will move closer to the tipping point.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

But wait, Google/Alphabet co-founder says it’s more about winning AI market share than skyrocketing capex or ROI. On Patrick O’Shaughnessy’s Invest Like the Best podcast, Gavin Baker, Chief Investment Officer for Atreides Management, shared an anecdote about what’s been going on within Google/Alphabet offices. According to Baker, Google co-founder Larry Page has been telling Google employees, “I am willing to go bankrupt rather than lose this race.” That shows how high the person who led Alphabet through its halcyon days thinks the stakes are in AI.

References:

https://www.fool.com/investing/2024/08/31/thinking-of-selling-nvidia-stock-larry-page-quote/

Curmudgeon: Caveat Emptor: Huge Debt and Circular Financing Deals Dominate AI Build-Outs

Merry-go-round of dog chasing its tail: Relationship between U.S. hyperscalers and private Gen AI companies

Ookla: AI platform reliability decreases as outages surge

Nvidia CEO Huang: AI is the largest infrastructure buildout in human history; AI Data Center CAPEX will generate new revenue streams for operators

Hyperscaler capex > $600 bn in 2026 a 36% increase over 2025 while global spending on cloud infrastructure services skyrockets

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

5G infrastructure moves from coverage and speeds to cloud-native, orchestration, automation and AI-assisted networks

The most meaningful 5G infrastructure theme this week is the continued shift toward 5G standalone (SA), cloud-native, and AI-assisted networks. Recent news coverage shows that network operators and vendors pushing 5G SA expansion, automation, and 5G private-network use cases, alongside funding and buildout activity in fiber and rural transport that support 5G subscriber coverage and network capacity growth.

A few developments stand out from the available coverage:

- Google Cloud and Nokia expanded their AI partnership for autonomous networks.

- Ericsson and LG Uplus (Korea) agreed to deepen their strategic partnership to develop and expand network-based voice AI solutions for global markets, and advance AI-native network transformation.

- KDDI (Japan) launched a RAN digital twin initiative.

- CityFibre (UK) extended its 5G SA partnership with VodafoneThree (UK).

- Microamp (Poland) won EU backing for a 5G mmWave AI-RAN platform.

- There is also continuing momentum around mission-critical and industrial 5G, including Nokia Defense/KNDS tactical communications and Telia’s work on critical IoT and advanced 5G SA services.

It’s now crystal clear that 5G infrastructure investment is moving beyond raw radio deployment and into orchestration, automation, and vertical-specific network design. That is the bigger takeaway for telecom analysts: 5G spend is increasingly being justified by software intelligence, private/enterprise monetization, and operational efficiency rather than network coverage or speeds.

Image Credit: Nvidia

…………………………………………………………………………………………………………………………………………………………………………………………………………

The following table and text was generated by Perplexity.ai:

AI-Driven Network Management: Nokia vs. Ericsson vs. KDDI (2026):

An important structural caveat: Nokia and Ericsson are network equipment vendors whose AI tools are deployed across multiple operator customers, while KDDI is a mobile network operator deploying AI within its own live network. Direct comparisons of “commercial deployment” must account for this important distinction.

Comparison Table

Furthest along at vendor/customer commercial scale: Ericsson. The strongest discriminator is deployed EIAP customer adoption (AT&T, Swisscom, Telstra, Vodafone), the ~90-rApp ecosystem with ~90 ecosystem members, and the scale of Ericsson’s AI network-optimization estate (100M+ daily AI inferences across 13M+ sites serving 2B+ subscribers). The #1 ABI Research ranking for RAN automation (February 2026), the commercially scalable AI in RAN software subscription (June 2026), and rApp aaS available on AWS Marketplace (February 2026) further solidify Ericsson’s position as the most commercially mature vendor. Ericsson also has the broadest pre-existing digital twin ecosystem, though its RAN digital twin assets are more fragmented across research initiatives, rApps, and site-level tools compared to Nokia’s unified product launch.

Furthest along as an operator using AI agents in its own live network: KDDI. KDDI’s Fault Recovery Support Agent has been live in commercial operations since February 2026, and its multi-AI agent area optimization technology is deploying nationwide across base stations in FY2026 with confirmed quantitative gains (25% improvement in congested areas, 95%+ reduction in optimization work). This is stronger “own-network production” evidence than Nokia’s or Ericsson’s vendor-side claims, because KDDI is demonstrating autonomous AI agents operating in a live commercial network rather than selling tools for others to deploy. However, KDDI’s RAN Digital Twin remains an early-stage collaboration (prototype target March 2028), and its Gemini on GDC integration is still in trial.

Furthest along in explicit Gemini integration: Nokia. Nokia has the most direct and productized Gemini integration of the three, with six specialized Gemini-powered agents built on Google Cloud’s ADK and Gemini Enterprise Agent Platform, two of which (Router and Event Triage) are already running in Nokia’s environment. However, these agents are not yet commercially deployed with operator customers — the full SaaS package targets Google Cloud Marketplace in September 2026, with additional agents shipping through 2027. Nokia also launched the clearest single RAN Digital Twin product (February 2026, NVIDIA AODT) and has the most explicit vendor-side Gemini story, but its commercial deployment footprint with operators is narrower than Ericsson’s.

Summary:

Ericsson leads in commercial scale and breadth, KDDI leads in live operator-network AI agent deployment, and Nokia leads in depth of Gemini integration and unified RAN digital twin productization.

………………………………………………………………………………………………………………………………………………………………………………………….

References:

Nokia RAN Digital Twin launch (Feb 2026) — primary source for the NVIDIA AODT-powered product (Nokia RAN Digital Twin, a telecommunications simulation system built on the NVIDIA Aerial Omniverse Digital Twin (AODT) platform. It uses accelerated ray tracing and AI to model 5G and 6G wireless network environments)

5 New Digital Twin Products Developers Can Use to Build 6G Networks

RCR Wireless: Nokia Gemini agents in network ops (Jun 2026) — detailed breakdown of all six agents, tech stack, 50-80% efficiency gains, deployment timeline

Nokia autonomous networks portfolio upgrade (Jun 2026) — Agent Library, 60-80% productivity gains, all network layers covered

Ericsson AI in RAN launch (Jun 2026) — commercially scalable software subscription, agentic AI support, Ericsson Silicon

Ericsson #1 ranked by ABI Research for RAN automation (Feb 2026) — EIAP adoption by AT&T, Swisscom, Telstra, Vodafone; ~90 Apps and ecosystem members

Ericsson blog: Network digital twin for safe autonomy (Apr 2026) — Ericsson’s vision for predictive, interactive NDTs in autonomous networks

KDDI RAN Digital Twin launch (Jun 2026) — primary source; NVIDIA, Keysight, Samsung partners; prototype by March 2028, commercial validation by FY2030

KDDI Fault Recovery Support Agent (Feb 2026) — live since Feb 19, 2026; operational digital twin for fault analysis; Autonomous Maintenance Agent planned FY2026

KDDI multi-AI agent area optimization (Feb 2026) — nationwide deployment FY2026; 25% improvement in congested areas; 95%+ work reduction

KDDI Gemini on Google Distributed Cloud trial (Apr 2026) — Gemini on GDC trial at Osaka Sakai Data Center; multi-agent system for network development automation; commercial target 2027

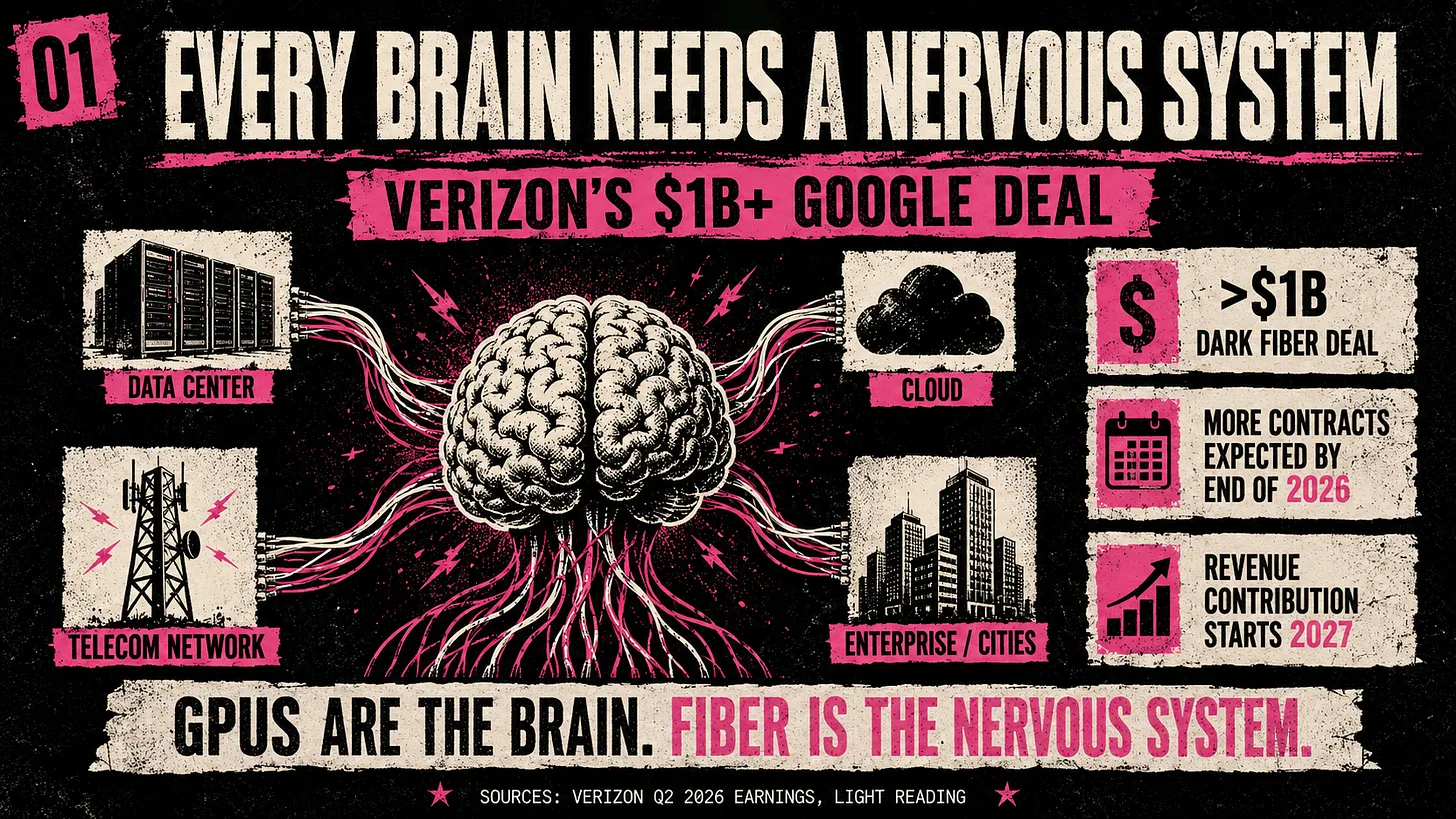

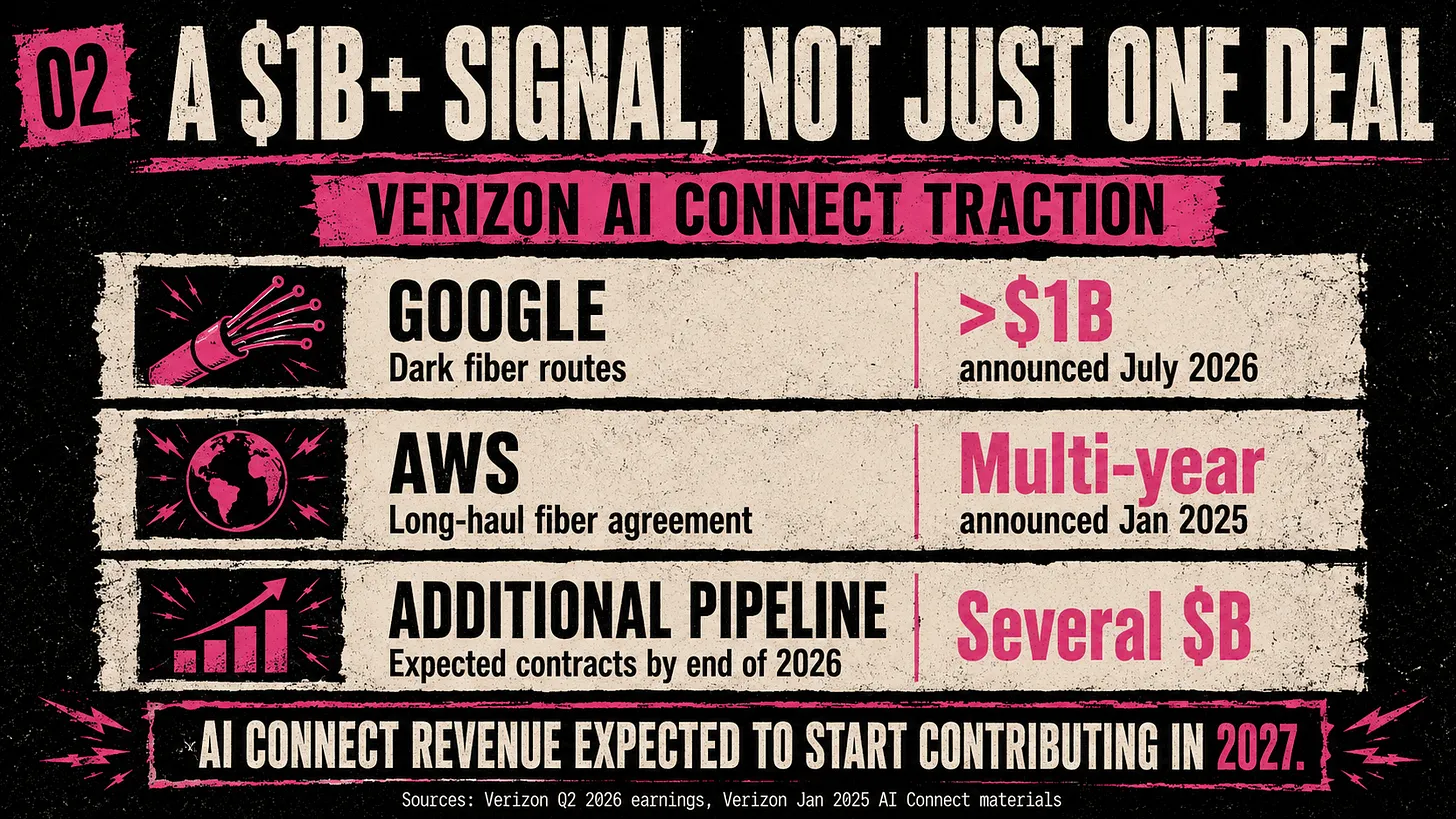

Verizon’s $1 Billion Google Dark Fiber Deal Highlights Importance of Optical Networks

Executive Summary:

Verizon CEO Dan Schulman said on Friday the company had secured a more-than-$1 billion dark fiber agreement with Google. It underscores how hyperscale AI growth is elevating dark fiber, route diversity, and high-capacity optical engineering into core industry priorities and is evidence that the network layer is becoming a central enabler of AI-scale computing. The deal, disclosed during Verizon’s Q2 2026 earnings call, is intended to connect Google data centers and support the transport demands of AI workloads.

“We have other deals that we expect to announce by year end that taken together are expected to be worth multiple billions of dollars in revenue over the next several years,” Schulman said on Verizon’s post-earnings call.

From a telecom perspective, the significance lies in the shift from best-effort connectivity toward engineered optical infrastructure with explicit performance objectives. As hyperscalers expand distributed AI training and inference, the requirements for capacity, latency, route diversity, and operational control increasingly favor dark fiber over shared transport models.blogs.cisco+2

Why This Matters for Network Architecture:

Dark fiber gives the customer direct control over the optical layer, enabling custom design choices for line rates, protection schemes, and traffic engineering. That flexibility is especially relevant for large data-center interconnect environments, where traffic growth can quickly outpace conventional managed services.blogs.cisco+1

The Verizon-Google transaction also reinforces the role of long-haul and metro fiber as strategic infrastructure rather than commodity bandwidth. In practice, this places greater emphasis on fiber route resilience, diverse path design, and the ability to scale toward higher-capacity optical systems as AI clusters expand.blogs.cisco+1

Standards and Industry Implications:

While the deal itself is commercial, its implications touch several standards-adjacent concerns that are increasingly important to operators and vendors. These include high-capacity optical transport, inter-domain coordination, deterministic latency for distributed workloads, and the operational models needed to support AI-driven traffic growth.blogs.cisco+1

For IEEE ComSoc readers, the broader signal is that future network evolution may be shaped as much by AI infrastructure economics as by traditional access or mobility growth. The value proposition is moving toward fiber-based transport layers that can support hyperscale interconnect, cloud adjacency, and resilient backhaul for distributed computing environments.benton+1

Conclusions:

Verizon’s reported dark fiber deal with Google suggests that optical connectivity is no longer a passive enabler but a competitive differentiator in the data-center supply chain. It highlights a broader shift in network economics: AI growth is elevating fiber infrastructure from a supporting asset to a strategic enabler. For carriers, the message is clear — the winners in the AI era may be those that can pair scale, route control, and transport engineering with the capacity demands of hyperscale cloud buildouts.

Text & Images from Sebastian Barros:

Verizon’s billion dollar agreement with Google shows that the AI infrastructure boom is moving beyond chips, data centers and electricity. The next constraint is connecting everything together. Verizon will use existing fiber where possible and construct new routes where necessary. It can provide either dark fiber or managed, lit capacity, depending on what the customer wants.

Google already operates one of the most advanced private networks in the world. Its infrastructure spans more than two million miles of lit fiber, 33 subsea cable investments, more than 200 network edge locations, and thousands of content delivery sites. Yet Google still needs Verizon to provide additional routes.

The (hyperscaler) companies building the largest AI brains cannot build every nerve themselves, as the pace is too fast. The telco opportunity begins when data needs to leave the campus.

Models must be copied between regions; training datasets must be moved from storage locations to computing clusters; companies need private connections to cloud platforms; AI applications must retrieve enterprise information stored across different data centers. Inference results must reach factories, vehicles, hospitals, stores, offices, and consumers.

AI therefore requires two different networks. The first connects processors inside the brain. The second connects different brains with the outside world, and Telcos have a much stronger position in the second.

References:

https://sebastianbarros.substack.com/p/every-brain-needs-a-nervous-system

Verizon to build new, long-haul, high-capacity fiber pathways to connect AWS data centers

Hyper Scale Mega Data Centers: Time is NOW for Fiber Optics to the Compute Server

S&P Global Market Intelligence Surveys: Fiber Deployments in U.S. and Europe + AI Infrastructure Causes Market Shift

Amazon and Corning in Multi-Billion-Dollar Fiber Infrastructure Deal in North Carolina

2026 Fiber Connect Keynote: “The Future of Fiber Optics: AI and the Quantum”

Big Fiber’s $250M financing deal to buildout dark fiber routes for AI Data Center expansion

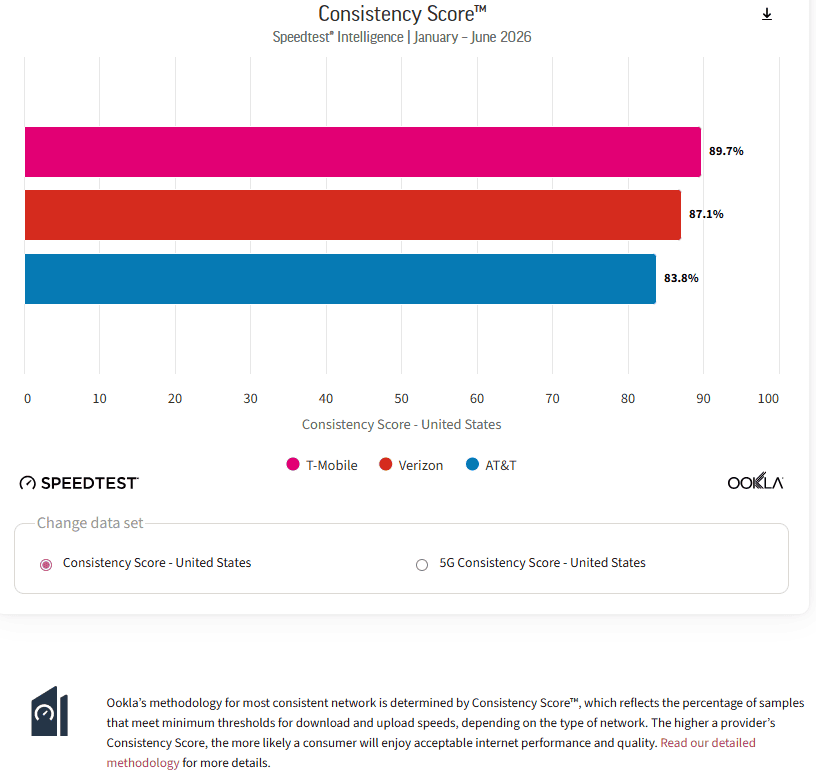

Highlights from Ookla’s U.S. Speedtest Connectivity Report-Mobile & Fixed Networks

Executive Summary:

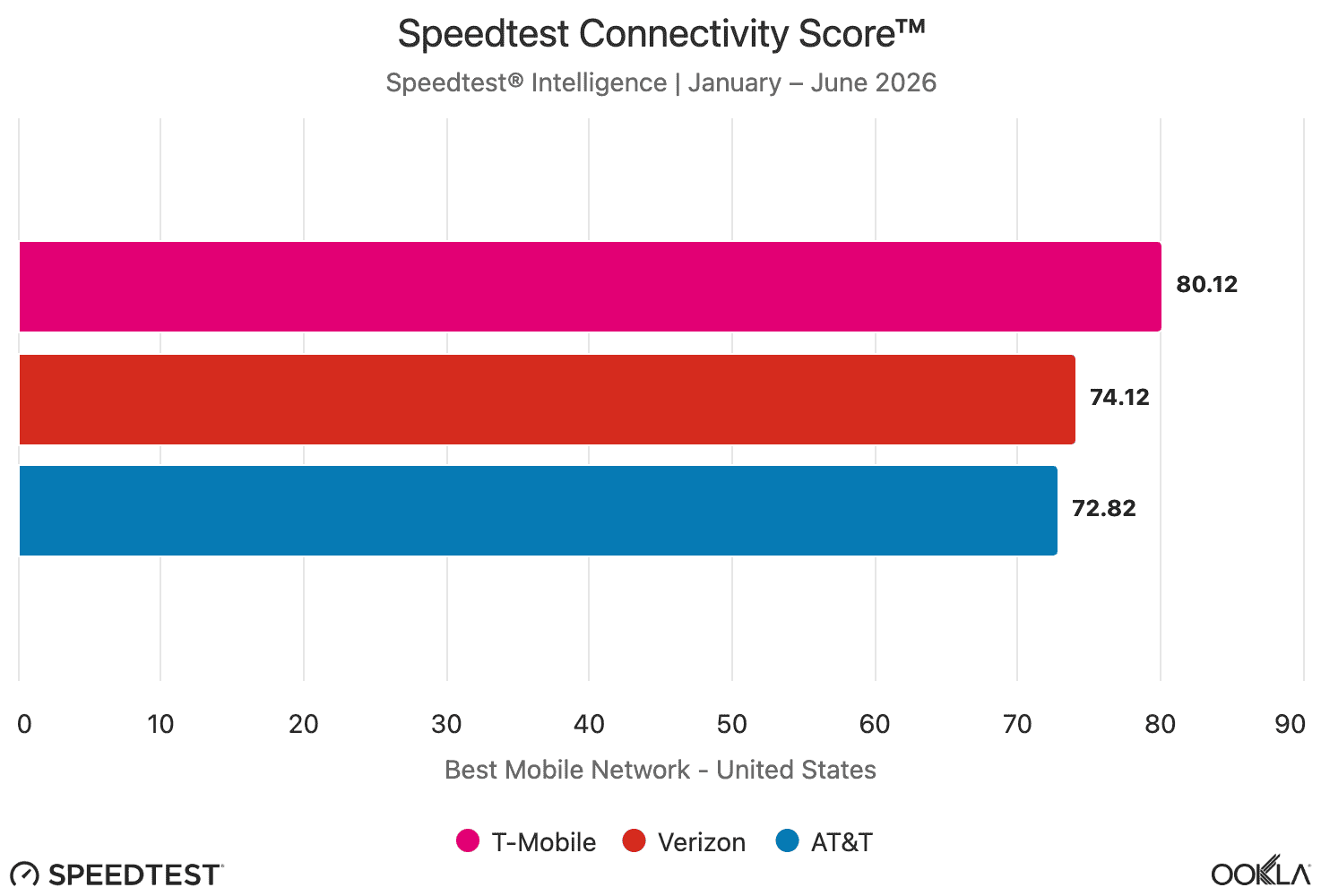

Ookla’s United States Speedtest Connectivity Report H1 2026 provides a detailed snapshot of network performance across the U.S. mobile and fixed broadband markets, based on Speedtest Intelligence data. The findings point to a competitive landscape in which T-Mobile continued to distinguish itself in mobile connectivity, while AT&T Fiber led the fixed broadband segment.

In the mobile network category, T-Mobile was named the Best Mobile Network overall and also claimed the Best 5G Network award for the first half of 2026. The “un-carrier” recorded a median download speed of 275.55 Mbps across all technologies combined, and a median 5G download speed of 314.38 Mbps. These results underscore the strong performance of T-Mobile’s network, particularly in 5G-centric use cases where throughput remains a key differentiator.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

T-Mobile recorded the best mobile network consistency in the United States, for all technologies combined and for 5G. Across all technologies, 89.7% of its samples met or exceeded the threshold of 5 Mbps download and 1 Mbps upload, while 79.3% of its 5G samples met or exceeded the higher threshold of 25 Mbps download and 3 Mbps upload.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

For the fixed line networks, AT&T Fiber was recognized as the Best Internet provider and the Fastest Fixed Network in the United States during the same period. The oldest U.S. network operator posted a median download speed of 374.75 Mbps and a median upload speed of 320.65 Mbps, reflecting the growing importance of high-capacity fiber access in home broadband markets. As fixed and mobile connectivity continue to converge in consumer experience expectations, these metrics highlight the increasingly performance-driven nature of broadband competition.

The report also indicates that T-Mobile delivered the best gaming and video streaming experiences in the United States during 1H 2026, both across all technologies combined and in the 5G-only category. This is notable because it extends the company’s advantage beyond raw speed metrics into application-level quality, where latency sensitivity, jitter, and consistency can be as important as peak throughput.

At the city level, Lincoln, Nebraska recorded the fastest median mobile download speed among the most populous U.S. cities at 395.83 Mbps. In fixed broadband, Durham, NC led the group with a median download speed of 380.47 Mbps. These city-level results reinforce the fact that network performance varies significantly by market, even within a single national assessment, and that local deployment density and backhaul quality can materially influence user experience.

Editorial Analysis & Conclusions:

Taken together, the report suggests that U.S. network leadership in 1H 2026 was shaped by both access technology and service quality. Mobile operators are increasingly being judged not only by coverage and 5G speed, but also by end-user experience across demanding applications, while fiber providers continue to push the upper bounds of fixed-line performance. Ookla’s latest data therefore offers a useful benchmark for understanding where the U.S. connectivity market stands — and where competition is most intense.

- The U.S. mobile market appears to be shifting from a simple coverage contest toward a performance-and-experience contest. T-Mobile’s lead in overall mobile, 5G, gaming, and video-streaming experience suggests that end-user quality is now being shaped by a combination of throughput, consistency, and 5G availability rather than raw coverage alone.

- The results reinforce that 5G leadership is increasingly tied to how well operators can translate spectrum, radio access optimization, and transport capacity into sustained user experience. T-Mobile’s strong median download speeds across both blended and 5G-only measurements indicate that its network engineering is delivering not just peak performance, but performance that is visible in real-world usage patterns.

- The fixed broadband results show that fiber remains the benchmark for high-capacity access in the U.S. AT&T Fiber’s strong download and upload figures illustrate why fiber continues to set the standard for symmetrical, high-throughput residential service, especially as cloud applications, video conferencing, and multi-device home traffic continue to grow.

- Application-centric metrics are becoming more relevant in how networks are evaluated. The fact that T-Mobile led in gaming and video streaming experience suggests that operators are increasingly judged on latency-sensitive and consistency-sensitive workloads, not just speed-test averages. For ComSoc readers, that is a reminder that network KPIs are evolving in step with how people actually use the network.

- At the city level, the report also highlights how uneven performance can be across markets. Lincoln’s leading mobile result and Durham’s leading fixed result suggest that local infrastructure, spectrum conditions, and deployment density still matter significantly even within a mature national market. This is especially relevant for planners and researchers interested in the last mile, metro-area capacity, and regional quality-of-experience gaps.

Overall, the report suggests that U.S. connectivity competition is entering a more mature phase in which operators are differentiated less by whether they can deliver 5G or fiber at all, and more by how well they can optimize those platforms for sustained, application-level performance. For IEEE Techblog readers, that makes the report useful not only for network operator rankings, but as a snapshot of where network engineering priorities are heading.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

References:

https://www.ookla.com/research/reports/united-states-speedtest-connectivity-report-h1-2026

https://www.ookla.com/resources/guides/speedtest-methodology

Ookla: AI workloads will force changes in 5G mobile network infrastructure

Ookla: AI platform reliability decreases as outages surge

Ookla on the Global D2D Market

Ookla: Starlink a viable competitor for hybrid 5G/NTN services due to network performance improvements and larger coverage area

Ookla: D2D satellite connectivity surged 24.5% during last 9 months; Starlink’s footprint expansion leads the way

Nokia to showcase agentic AI network slicing; Ericsson partners with Ookla to measure 5G network slicing performance

Autonomous customer experience required for AI-Native 6G and distributed intelligence at the network edge

Executive Sumary:

Communications service providers (CSPs) have historically competed on network-centric KPIs—coverage, capacity, reliability, and price—anchored in 3GPP performance and management frameworks (e.g., TS 28-series, TS 23.501 QoS models). However, these metrics alone are no longer sufficient to sustain differentiation in increasingly saturated and capital-intensive markets, according to Chantel Cary, Product Marketing Senior Manager at Oracle Communications [1],

“The battleground has shifted,” Cary told Capacity Global. “Today, customer experience is becoming the clearest point of differentiation, and in many cases, the most important driver of growth.”

This shift is unfolding alongside structural constraints: flat ARPU, rising capex associated with 5G standalone, fiber access (FTTx), and edge cloud expansion, and increasing customer acquisition and retention costs. At the same time, customer expectations—benchmarked against hyperscaler-grade digital platforms—are becoming uniformly high across mobile and fixed broadband services.

“They do not compare a telecom provider only to other providers,” she said. “They compare every experience to the best experience they have anywhere.”

…………………………………………………………………………………………………………………………………………………………………………………………………………………..

Note 1. Oracle Communications is a dedicated global business unit and product portfolio fully owned and operated by Oracle. It provides enterprise software and infrastructure designed specifically for telecommunications service providers (like AT&T or Verizon) and large enterprises. Their solutions manage everything from network routing, security, and signaling (including 5G) to back-office billing, revenue management, and customer experience operations,

…………………………………………………………………………………………………………………………………………………………………………………………………………………..

Analysys Mason reports that 97% of operators view AI-powered automation as essential for survival and growth, reinforcing alignment with TM Forum’s Autonomous Networks framework and the broader industry transition toward AI-native system design.

AI-Native Customer Experience Architecture:

Cary’s concept of “autonomous customer experience” maps directly to the emerging paradigm of AI-native networks, where intelligence is embedded across both network and service layers rather than applied as an overlay. “It is not about removing the human element from engagement,” she explained. “It is about using AI to continuously orchestrate the customer lifecycle in ways that humans alone cannot manage at scale.”

In wireless networks, this evolution is reflected in 3GPP-defined enablers such as the Network Data Analytics Function (NWDAF, TS 23.288), which provides real-time analytics to optimize policy control, mobility, and QoS. In parallel, O-RAN Alliance architectures introduce the near-real-time and non-real-time RAN Intelligent Controllers (near-RT RIC, non-RT RIC), enabling AI-driven control loops for radio resource management and service optimization.

Image Credit: Aisera

In wireline and converged networks, similar principles are emerging through SDN-based control planes, broadband network gateways (BNG) with telemetry streaming, and ITU-T frameworks (e.g., Y.3172 for machine learning in future networks), enabling closed-loop optimization across access, aggregation, and core domains.

However, Cary notes that most OSS/BSS environments remain fragmented, limiting the ability to operationalize these capabilities at the customer experience layer. Data silos, batch-oriented processing, and loosely coupled workflows constrain real-time, cross-domain orchestration.

AI Across Commercial and Network Domains:

Cary identifies three primary domains of impact, increasingly converging with network intelligence:

-

Marketing: AI-driven personalization is evolving toward real-time, context-aware engagement informed by both customer behavior and network conditions (e.g., location, QoS state, congestion). This aligns with event-driven architectures and customer data platforms integrated with network analytics (e.g., NWDAF exposure via APIs). “Personalisation shifts from broad audiences to the individual,” she said, adding that relevance is now “a prerequisite for attention.”

-

Sales: AI enables next-best-action and dynamic offer generation, incorporating network-aware insights such as service availability, slice characteristics (in 5G SA), and fiber capacity constraints. Integration with policy control (3GPP TS 23.203) and service orchestration frameworks supports closed-loop order capture and fulfillment. “That combination of higher conversion and lower friction is valuable,” she said.

-

Service: AI-driven assurance is transitioning from reactive fault management to predictive and intent-based service assurance across both wireless and wireline domains. Telemetry from RAN, transport, and fixed access networks feeds AI models that anticipate degradation and trigger remediation before customer impact. “Human agents still play a central role,” Cary said, “but they can be augmented with real-time recommendations, contextual history and autonomous processes that improve both speed and consistency.”

Scaling Challenges in AI-Native Transformation:

Despite progress in AI models and domain-specific analytics, Cary highlights a systemic gap in operationalization.

“What it lacks, in many cases, is the ability to turn fragmented customer data into real-time decisions that can actually be executed across marketing, sales and service,” she said.

Analysys Mason data indicates that only 6% of operators achieve ROI above 25% from AI initiatives, while 60% advance just 20% of proofs of concept into production. This reflects challenges in integrating heterogeneous data sources across OSS, BSS, and network domains, as well as limitations in MLOps and real-time orchestration frameworks.

Fragmentation is compounded in converged networks, where wireless (3GPP-based) and wireline (e.g., Broadband Forum TR-369/USP, TR-383 for disaggregated BNG) ecosystems often evolve independently. Additionally, 93% of operators cite multi-vendor complexity as increasing total cost of ownership, underscoring the need for interoperable, standards-based integration across AI, network, and IT domains.

“That creates an unfortunate pattern across the industry,” she said, “promising AI initiatives that demonstrate value in isolation but fail to scale because they are not connected to the data, systems and processes where real work happens.”

Toward Fully AI-Native Operations:

Cary emphasizes that the target state is not incremental automation but fully AI-native operations, where intelligence is embedded into both network control loops and customer engagement workflows.

“This is why the future of customer experience in communications is not about layering AI onto the edge of the enterprise,” Cary said. “It is about making AI operational at the core of engagement.”

This vision aligns with emerging 6G research directions, where AI is treated as a native design primitive across RAN, core, and service layers, as well as with TM Forum’s Open Digital Architecture (ODA), which promotes composable, API-driven integration between OSS, BSS, and AI components.

Oracle’s approach reflects this convergence by unifying customer data, embedding AI into engagement and orchestration layers, and integrating these capabilities with telecom operational systems across both wireless and wireline domains.

Implementation Suggestions:

Cary said that network providers do not need to transform everything at once. She recommends starting by unifying customer data across touchpoints to establish a trusted, real-time view, before activating high-value AI use cases across marketing, sales and service. From there, providers can embed AI into workflows so insight translates into action rather than sitting in dashboards, eventually connecting those capabilities into end-to-end orchestration.

Indeed, Cary advocates a phased approach consistent with AI-native transformation:

-

Establish a unified, real-time data fabric spanning customer, service, and network domains.

-

Deploy high-value AI use cases (e.g., next-best-action, churn prediction, predictive assurance) leveraging both IT and network telemetry.

-

Embed AI into execution workflows to enable closed-loop, intent-driven orchestration across the customer lifecycle.

This progression reflects the broader industry trajectory toward converged, AI-native networks, where customer experience is no longer an overlay on connectivity, but a direct outcome of tightly coupled intelligence across wireless and wireline infrastructures.

“The communications providers that lead in the years ahead will not be the ones that simply adopt more AI tools. They will be the ones that use AI to rethink how customer engagement works across the enterprise. AI is not just enhancing customer experience,” she added. “It is redefining how customer experience is delivered, and in communications, that shift is likely to separate the providers that keep pace from the ones that set the pace.”

………………………………………………………………………………………………………………………………

Editorial Analysis:

Cary’s vision aligns with IMT 2030/6G’s shift from AI as an overlay to AI as an architectural primitive, spanning the air interface, semantic service handling, and distributed edge intelligence across wireless and wireline domains. The cleanest way to map her suggestions into 6G is to treat “autonomous customer experience” as the service-layer expression of an AI-native network stack: AI decisions would no longer sit only in OSS/BSS, but would be distributed across RAN, transport, core, and edge applications, with closed-loop control spanning wireless and wireline domains. That maps well to current AI-native 6G proposals that emphasize model interdependencies, distributed intelligence, and AI embedded directly in the architecture rather than layered on top.

For the AI native air interface, the link is to AI-assisted radio control, where the network uses learned models to optimize scheduling, mobility, beam management, and QoS-aware policy decisions in real time. In a 6G framing, that extends beyond today’s AI for RAN optimization and toward an AI-native air interface in which the radio stack itself is designed for machine-driven adaptation, including distributed control loops between UE, RAN, and core. For your article, this supports language that customer experience is increasingly shaped by network intelligence at the point of access, not just by back-office engagement systems.ieeexplore.ieee+2

Semantic communications maps to the idea that the network should optimize for meaning or task relevance, not simply bit delivery. In practice, that means a 6G service layer could prioritize the semantic value of an interaction—such as whether a customer is trying to resolve an outage, confirm a move order, or change a plan—and allocate resources accordingly across wireless and wireline paths. The relevance to Cary’s argument is that customer experience becomes more contextual and intent-aware when the network itself can distinguish between low-value traffic and high-importance service interactions.

Distributed intelligence at the network edge is the most direct bridge between CSP operations and 6G design. In a converged wireless-wireline environment, edge AI can fuse RAN telemetry, fixed access metrics, subscriber context, and service history to trigger local decisions such as proactive care, dynamic QoS adjustment, or preemptive fault mitigation. That makes the experience layer more autonomous because the decision point moves closer to where the event occurs, reducing dependence on centralized, slower, batch-oriented processing.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.nokia.com/6g/unlocking-the-full-potential-of-ai-native-6g-through-standards/

Comparing AI Native mode in 6G (IMT 2030) vs AI Overlay/Add-On status in 5G (IMT 2020)

SHIELD-6G with AI-native cyber threat intelligence platform to enhance cybersecurity for Europe’s future 6G networks

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

Ericsson and Intel collaborate to accelerate AI-Native 6G; other AI-Native 6G advancements at MWC 2026

NVIDIA and global telecom leaders to build 6G on open and secure AI-native platforms + Linux Foundation launches OCUDU

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

Jio’s LEO satellite constellation authorized by IN-SPACe: 5 Tbps over India with 3GPP Rel 17 and 18 NTN Alignment

Executive Summary:

India’s space sector has taken another decisive step toward global competitiveness with the Indian National Space Promotion and Authorization Center (IN-SPACe) granting a key technical authorization to Reliance Jio for a proposed Low Earth Orbit (LEO) satellite constellation of approximately 1,600 satellites. The scale and ambition of the program place it firmly within the same category as leading non-terrestrial network (NTN) initiatives such as SpaceX’s Starlink, Amazon’s Project Kuiper, and Eutelsat OneWeb, while signaling India’s intent to build indigenous capability in space-based broadband infrastructure.

Constellation Scale and Architecture:

At ~1,600 satellites, Jio’s planned constellation is smaller than Starlink’s first-generation deployment (~4,400 satellites, with longer-term plans exceeding 10,000), but comparable to Amazon’s Project Kuiper (~3,236 satellites planned) and significantly larger than OneWeb’s first-generation system (648 satellites). This places Jio in an intermediate design space—large enough to deliver meaningful aggregate capacity and coverage, yet potentially more optimized for regional rather than fully global service.

The announced aggregate capacity of up to 5 Tbps suggests a high-throughput satellite (HTS) architecture leveraging aggressive frequency reuse and multi-spot beam designs. By comparison:

-

Starlink is estimated to already deliver tens of Tbps of global capacity, enabled by dense constellation scaling, advanced phased-array antennas, and increasingly, optical inter-satellite links (ISLs) [2.].

-

Kuiper targets multi-Tbps capacity with a strong emphasis on cloud integration via AWS, though it remains pre-commercial as of mid-2026.

-

OneWeb focuses more on enterprise, maritime, and government backhaul, with comparatively lower aggregate throughput but strong QoS guarantees.

Note 1. ISLs (Inter-Satellite Links) are direct communication connections between spacecraft in orbit, allowing them to route data to one another without first sending it down to an Earth station. This creates a dynamic space mesh network, which dramatically reduces data latency, increases coverage, and bypasses the need for costly ground gateways.

……………………………………………………………………………………………………………………………………………………………………………………………………….

A key technical question for Jio will be whether it incorporates optical ISLs in its initial deployment. Starlink’s Gen2 architecture relies heavily on ISLs for mesh networking and latency optimization, reducing dependence on ground gateway density. In contrast, OneWeb’s first-generation system lacks ISLs, relying instead on a dense ground station network. Jio’s architectural choice here will directly influence both latency performance and ground infrastructure cost.

)

Reliance Jio plans to deploy 1,600 LEO satellites to build a space-based communication network. AI-generated image via Business Standard.

…………………………………………………………………………………………………………………………………………………………..

Spectrum Strategy and Link Budget Considerations:

Although Jio has not publicly disclosed its frequency plan, it is likely to align with Ku- and Ka-band allocations, consistent with global LEO broadband systems. Starlink and Kuiper both rely heavily on Ka-band for feeder links and Ku/Ka for user links, while also exploring V-band (40–75 GHz) for future capacity scaling.

For India-specific deployment, spectrum coordination presents both an opportunity and a constraint. Domestic prioritization could streamline regulatory approvals, but coexistence with incumbent satellite operators and terrestrial 5G services will require careful interference management. This is particularly relevant as 3GPP NTN bands increasingly intersect with traditional satellite allocations.

From a link budget perspective, enabling both fixed broadband and direct-to-device (D2D) services within the same constellation introduces competing design requirements. High-throughput broadband favors higher frequencies and larger user terminals, while D2D requires lower link margins, robust coding, and potentially sub-GHz or S-band spectrum to reach handheld devices.

Direct-to-Device and 3GPP NTN Alignment:

Jio’s emphasis on direct-to-device (D2D) connectivity places it at the forefront of a critical industry transition: the integration of NTN into the 3GPP ecosystem. Releases 17 and 18 define the foundational architecture for NTN support, including adaptations for:

-

Large propagation delays and Doppler shifts in LEO systems

-

Modified random access and timing advance procedures

-

Satellite-aware mobility and handover mechanisms

-

Power-efficient waveform adaptations for handheld devices

Starlink has taken an early lead in this domain through its partnership with T-Mobile, leveraging mid-band PCS spectrum to enable D2D messaging services. AST SpaceMobile, while not a direct LEO broadband competitor, has demonstrated high-throughput D2D links using large phased-array satellites. Apple’s emergency SOS feature (via Globalstar) represents a narrower but commercially successful implementation of NTN for consumer devices.

Jio’s differentiation may lie in tighter vertical integration with its terrestrial network. Unlike Starlink, which operates largely as an overlay network, Jio can embed NTN capabilities directly into its 5G—and eventually 6G—core architecture. This opens the door to unified authentication, billing, and service continuity across terrestrial and satellite domains, consistent with the 3GPP vision of seamless TN–NTN convergence.

Latency, Backhaul, and 5G/6G Integration:

Operating in LEO, Jio’s system can achieve round-trip latencies on the order of 20–40 ms, comparable to Starlink and significantly lower than geostationary systems (>500 ms). With ISLs, latency for long-distance routes can even approach or outperform terrestrial fiber in certain scenarios, depending on routing efficiency.

For India, one of the most compelling use cases is satellite-based backhaul for rural and remote base stations. While fiber deployment remains uneven across the country, a LEO-based backhaul layer could enable rapid expansion of 5G coverage without the need for extensive terrestrial infrastructure. This aligns with ongoing 6G research, where integrated TN–NTN architectures are expected to support ubiquitous coverage and network resilience.

In comparison to Jio:

-

OneWeb has already established a strong position in cellular backhaul, including partnerships in emerging markets.

-

Starlink is increasingly targeting enterprise and mobility segments, including aviation and maritime.

-

Kuiper is expected to leverage AWS edge integration for enterprise and cloud-native applications.

Jio’s advantage lies in its domestic scale and control over both access and core network layers, enabling tighter optimization of end-to-end service delivery.

Manufacturing, Launch, and Economic Viability:

Deploying a 1,600-satellite constellation requires industrial-scale manufacturing and launch capabilities. SpaceX’s vertical integration—spanning satellite production and launch via Falcon 9 and Starship—has been a key enabler of Starlink’s rapid deployment. Amazon is pursuing a mixed launch strategy (ULA, Blue Origin, Arianespace), while OneWeb relied heavily on international launch providers.

Jio’s approach will likely depend on partnerships, potentially leveraging ISRO’s launch capabilities alongside commercial providers. However, achieving cost efficiency comparable to Starlink remains a significant challenge, particularly in satellite mass production and user terminal pricing.

User equipment (UE) economics will be especially critical for D2D services. While fixed terminals can subsidize higher costs, mass-market D2D requires integration into standard smartphones without significant cost premiums. This is an area where chipset ecosystem alignment—Qualcomm, MediaTek, and others—will play a निर्ण role.

Strategic and Geopolitical Implications:

Beyond technical considerations, Jio’s LEO initiative reflects broader geopolitical and industrial policy trends. India is positioning itself to reduce dependence on foreign satellite infrastructure while building domestic capability across the space value chain. This aligns with parallel efforts in semiconductor manufacturing, AI infrastructure, and 6G research.

At the same time, the global LEO market is becoming increasingly competitive and capacity-rich. The risk of oversupply, pricing pressure, and regulatory fragmentation is non-trivial. Jio’s success will depend not only on technical execution but also on its ability to carve out a differentiated market position—potentially focusing on South Asia, enterprise services, and tightly integrated telecom offerings.

…………………………………………………………………………………………………………………………………………………………………………………..

LEO Systems Serving India:

Key parameters of LEO constellations relevant to India’s satellite broadband market.

-

Rel‑15 / Rel‑16 – Baseline 5G NR (Terrestrial)

-

Label text: “TN‑only architecture; NR defined for terrestrial cells and standard mobility.”

-

-

Rel‑17 – Initial NTN Support

-

Label text: “Introduction of NR‑NTN for LEO/GEO satellites and HAPS; adaptations for delay, Doppler, and satellite link budget.”

-

-

Rel‑18 – 5G‑Advanced NTN Enhancements

-

Label text: “Improved NTN mobility, QoS, power efficiency; building blocks for direct‑to‑device scenarios and tighter TN–NTN integration.”

-

-

Beyond Rel‑18 / early 6G – Native TN–NTN Convergence

-

Label text: “Unified terrestrial–satellite architecture, AI‑assisted RAN control, ubiquitous coverage; NTN treated as a first‑class component of 6G systems.”

-

………………………………………………………………………………………………………………

References:

European Consortium 5G NTN transmission paves the way for standards based direct to device (D2D) connectivity

Non-Terrestrial Networks (NTN) Tutorial: Architecture, Spectrum, and Technical Foundations

Non-Terrestrial Networks (NTNs): market, specifications & standards in 3GPP and ITU-R

Ookla: Starlink a viable competitor for hybrid 5G/NTN services due to network performance improvements and larger coverage area

From LPWAN to Hybrid Networks: Satellite and NTN as Enablers of Enterprise IoT – Part 2

Telecoms.com’s survey: 5G NTNs to highlight service reliability and network redundancy

Keysight Technologies Demonstrates 3GPP Rel-19 NR-NTN Connectivity in Band n252

ITU-R recommendation IMT-2020-SAT.SPECS from ITU-R WP 5B to be based on 3GPP 5G NR-NTN and IoT-NTN (from Release 17 & 18)

India approves backhaul satellite connectivity via VSAT for telecom services; BharatNet tender coming soon

Deutsche Telekom: Network APIs with RCS to Enhance AI Enterprise Network Engagements

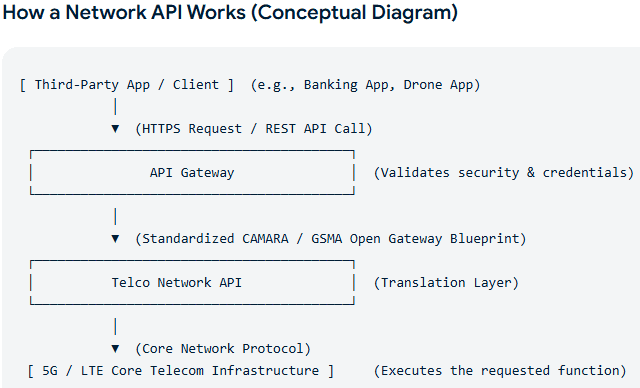

The telecom industry’s network API (Applications Program Interface) journey is transitioning from capability exposure to measurable enterprise value creation. Initial efforts focused on standardizing and exposing network functions through developer-friendly interfaces. The current phase centers on driving adoption and embedding those capabilities into enterprise workflows with demonstrable ROI.

Deutsche Telekom’s Chathurangi Wickramasinghe, SVP Magenta Business API, frames this shift succinctly: “Building APIs is right now not the challenge. But scaling adoption is a challenge.” This reflects a broader industry inflection point where technical feasibility has largely been established through initiatives such as CAMARA (Linux Foundation), GSMA Open Gateway, and TM Forum Open APIs, but commercial scalability remains constrained by integration complexity, fragmented exposure models, and unclear enterprise value propositions.

Deutsche Telekom has been an active contributor to both standardization and commercialization of network APIs. Its MagentaBusiness API platform, launched in Germany in 2023 in collaboration with Vonage, aggregates communications and network APIs into a unified exposure layer. Initial service APIs—Quality-on-Demand (QoD), Device Status–Roaming, and Device Location—align with CAMARA-defined abstractions designed to ensure interoperability across operators and geographies. CAMARA’s northbound API framework, increasingly aligned with 3GPP Service-Based Architecture (SBA) principles, is intended to decouple application logic from underlying network complexity, enabling portability across multi-operator environments.

However, as Wickramasinghe emphasizes, enterprise demand is not driven by APIs per se but by business outcomes. “No customer wakes up in the morning and asks for APIs. They have real business challenges they want to solve.” These challenges increasingly map to identity assurance, fraud mitigation, customer engagement, and operational efficiency—domains where telecom networks possess unique, non-replicable data assets.

A representative use case is the integration of Rich Communication Services (RCS) with network APIs. RCS, specified by GSMA and widely deployed across Android ecosystems, enables branded and interactive messaging for enterprise engagement. When combined with network APIs such as Number Verify and SIM Swap, RCS workflows can incorporate real-time identity validation and fraud detection. This convergence is particularly relevant given persistent vulnerabilities in SMS-based OTP authentication, including SIM swap fraud and phishing attacks.

Deutsche Telekom’s commercial launch of Number Verify in Germany in 2024—implemented in collaboration with Vodafone and O2 Telefónica under GSMA Open Gateway—demonstrates early multi-operator federation. The API enables silent authentication by verifying a user’s MSISDN via network signaling, eliminating reliance on SMS OTP while reducing latency and attack surface. Similarly, the SIM Swap API allows enterprises, particularly in financial services, to query recent SIM change events before authorizing high-risk transactions. GSMA reports indicate that fraud losses linked to account takeover and identity compromise exceed tens of billions of dollars annually, reinforcing the economic rationale for such capabilities.

The relevance of network APIs is further amplified by the emergence of AI-native enterprise architectures. At MWC 2026, Deutsche Telekom positioned network APIs as foundational infrastructure for AI-driven applications, highlighting trusted network signals, real-time context, and programmable QoS as key enablers. This aligns with broader industry trends toward “Network as Code,” where network capabilities are abstracted and consumed dynamically by applications and, increasingly, by AI agents.

Wickramasinghe underscored that enterprise AI adoption is constrained by “trust, security and governance.” Network APIs can address these constraints by providing deterministic, operator-verified signals for identity, location, device state, and session quality. As agentic AI systems begin executing transactions and interacting autonomously with users and services, the integrity of these signals becomes critical. “They rely on trusted signals. They need [them] to carry out their tasks autonomously.”

This framing also clarifies the monetization pathway for operators. Network APIs represent a shift from connectivity-centric revenue models toward exposure of differentiated network intelligence. However, achieving scale requires three conditions: standardized interfaces (e.g., CAMARA-aligned APIs), low-friction developer onboarding (including SDKs and hyperscaler integrations), and direct alignment with high-value enterprise use cases such as fraud prevention, identity verification, and service assurance.

Ecosystem developments in 2026 reinforce this trajectory. Nokia’s Network as Code platform includes Deutsche Telekom among its operator partners and highlights a deployment with Blocksport, where Number Verification enables seamless authentication in sports-oriented super apps. Nokia has also linked network APIs with agentic AI through collaboration with Google Cloud, aiming to make network capabilities programmatically accessible to enterprise AI systems via cloud-native interfaces. Hyperscaler involvement is particularly significant, as it addresses distribution and developer reach—historically a bottleneck for telecom API adoption.

From an architectural perspective, network APIs function as a control plane for trust. They expose network-derived assertions that cannot be replicated at the application layer: subscriber authenticity, SIM lifecycle events, device reachability, and network-validated location. In a zero-trust security paradigm and increasingly automated digital economy, these attributes become foundational primitives for secure transactions and interactions.

The concept of the “agentic network” extends beyond autonomous network operations (e.g., closed-loop assurance in 5G-Advanced and future 6G systems). It encompasses the ability of the network to provide verifiable, real-time context to external AI systems. As AI assumes greater responsibility for decision-making, customer engagement, and service orchestration, telecom operators are positioned to supply high-integrity signals that enhance reliability and reduce risk.

In this context, Wickramasinghe’s central argument is that network APIs achieve mainstream adoption not when they are marketed as technical interfaces, but when they are delivered as embedded, outcome-oriented capabilities. The transition from “API products” to “trusted outcomes”—fraud reduction, seamless authentication, and verified engagement—marks the critical step toward sustainable monetization and strategic relevance in the AI-driven digital ecosystem.

………………………………………………………………………………………………………………………………………………………………………………….

Network API Specifications and Frameworks:

These specifications and frameworks collectively enable the convergence of RCS and network APIs, supporting use cases such as trusted customer engagement, silent authentication, and fraud mitigation in enterprise workflows.

-

CAMARA Project APIs (Linux Foundation)

-

Provides northbound service API definitions aligned with GSMA Open Gateway.

-

As of 2026, over 60 APIs are defined, including stable APIs such as:

-

Number Verification,SIM Swap,SIM Swap Subscriptions -

Quality-on-Demand (QoD),QoS Profiles,QoS Provisioning -

Device Reachability Status,Device Roaming Status,Device Swap -

Location Verification,Location Retrieval,Geofencing Subscriptions -

One Time Password SMS,Customer Insights,KYC (Know Your Customer)APIs -

Simple Edge Discovery,Network Slice Booking,Traffic Influence

-

-

APIs are hosted on GitHub and follow OpenAPI 3.0 schema conventions.telecomtv+2

-

-

GSMA Open Gateway API Descriptions

-

Defines a universal set of northbound APIs for mobile network capabilities.

-

Includes APIs such as

Call Forwarding Signal,Device Identifier,Connected Network Type,Scam Signal, andCarrier Billing. -

Intended to ensure interoperability across operators and geographies, with CAMARA as the technical reference implementation.gsma+1

-

-

3GPP TS 23.222 – Common API Framework (CAPIF)

-

Specifies architecture and procedures for exposing network capabilities via APIs within 5G systems.

-

Defines API invoker, API provider, and CAPIF core functions for discovery, authentication, and logging.

-

3GPP TS 29.222 – Common API Framework for 3GPP Northbound APIs

-

Defines RESTful API design principles and procedures for communication between Application Functions (AFs) and the 5G Core.

-

Includes procedures for monitoring, device triggering, and traffic influence.

-

-

3GPP TS 29.522 – Network Exposure Function (NEF) Services

-

Specifies northbound interfaces between the NEF and external AFs.

-

Covers monitoring, device triggering, background data transfer, PFD management, traffic influence, and QoS session setup.

-

-

ETSI GS OSM 003 – RESTful API Specification and Testing

-

Provides methodology for specifying and testing RESTful APIs in telecom contexts.

-

Aligns with OpenAPI and includes guidelines for versioning, error handling, and security.

-

-

OMA RESTful Network API (OMA-TS-REST_NetAPI)

-

Early specification for RESTful exposure of network services such as messaging, location, and payment.

-

Predecessor to 3GPP CAPIF and NEF-based frameworks.

-

………………………………………………………………………………………………………………………………………………………………………………….

RCS (Rich Communication Services) Specifications:

-

GSMA RCC.71 – RCS Universal Profile Service Definition

-

Defines the baseline service capabilities for RCS Universal Profile, including chat, file transfer, audio/video messaging, and group chat.

-

Current version (v3.0) aligns with 3GPP IMS specifications and Android/Jibe ecosystem requirements.gsma

-

-

GSMA RCC.08 – Rich Communications Suite Endorsement of 3GPP TS 29.311

-

Specifies interworking between RCS and 3GPP messaging services.

-

Endorses relevant sections of 3GPP TS 29.311 for service-level interworking.gsma

-

-

3GPP TS 23.228 – IP Multimedia Subsystem (IMS)

-

Core IMS architecture specification enabling RCS services over LTE and 5G.

-

Defines session control, registration, and service delivery mechanisms.3gpp

-

-

3GPP TS 24.229 – IMS Signaling Flows and Procedures

-

Specifies SIP-based signaling for IMS sessions, including RCS chat and multimedia sessions.3gpp

-

-

3GPP TS 29.311 – Interworking for Messaging Services

-

Defines interworking between IMS messaging and external systems, including SMS and MMS gateways.gsma

-

-

ETSI TS 102 901 – Rich Communication Suite (RCS)

-

European standard specifying RCS service architecture and capabilities.

-

Aligns with GSMA RCS Universal Profile and 3GPP IMS framework.etsi

-

-

GSMA RCS Business Messaging (RBM) Guidelines

-

Defines enterprise messaging use cases, A2P workflows, and brand verification mechanisms.

-

Supports integration with network APIs for authentication and fraud prevention.5gamericas

-

……………………………………………………………………………………………………………………………………………………………………………….

References:

https://www.rcrwireless.com/20260716/carriers/deutsche-telekom-ai-apis

New Linux Foundation white paper: How to integrate AI applications with telecom networks using standardized CAMARA APIs and the Model Context Protocol (MCP)

Telefónica and Nokia partner to boost use of 5G SA network APIs

New venture to sell Network Application Programming Interfaces (APIs) on a global scale

AI-Era Cloud Network Transformation: A Reference Architecture and Implementation Roadmap

Fierce Network Research report examines telcos role in the AI economy and profiles early AI adopters

China’s big 3 telcos offer 5G Rich Communication Services (RCS)

Analysis: Nokia’s new AI-RAN platform and Standalone AI-RAN node with Nvidia GPUs

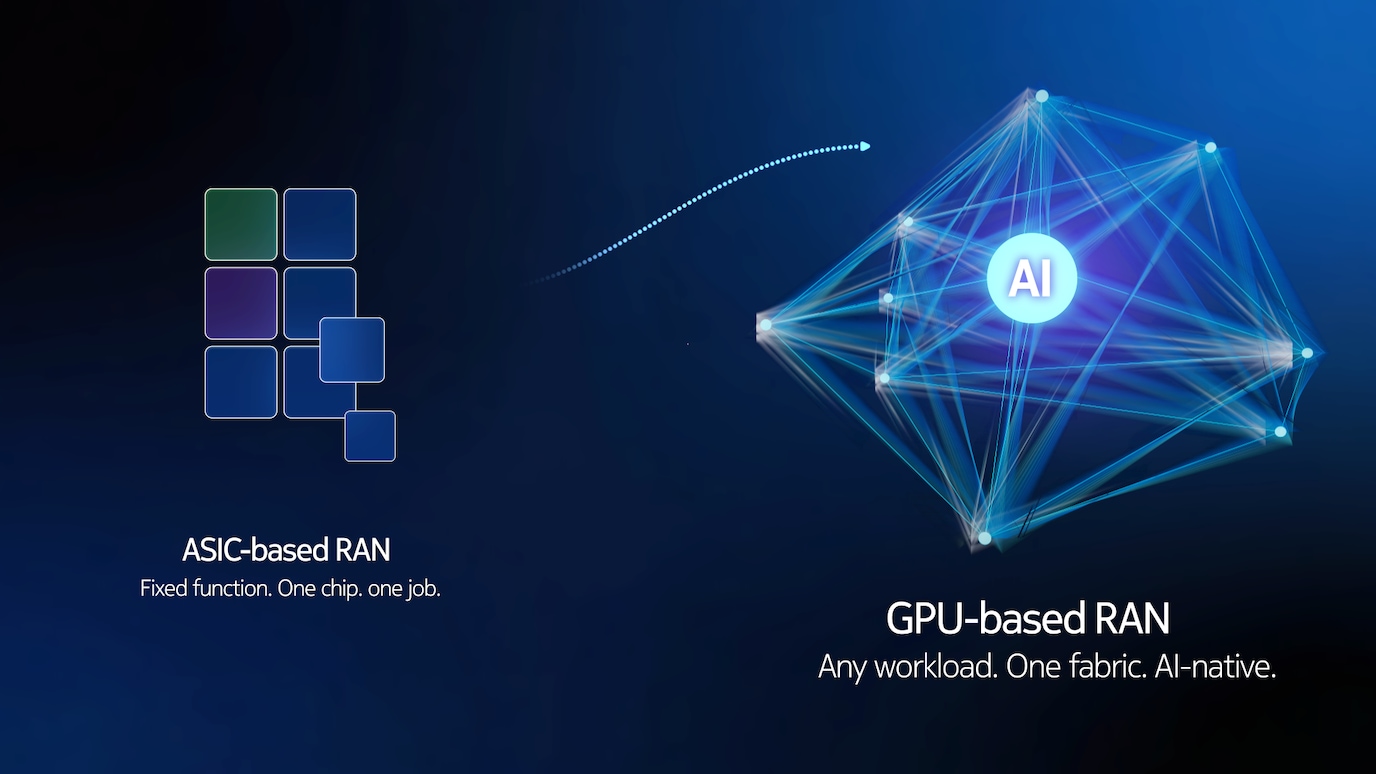

Nokia today announced what it describes as the first commercial AI-RAN platform, signaling a potentially significant inflection point in radio access network architecture. As AI workloads increasingly influence network design and operations, service providers are under pressure to deliver higher capacity, improved cost efficiency, and faster service innovation without depending on traditional hardware refresh cycles. Nokia’s AI-RAN platform is positioned to address these requirements by extracting greater uplink and downlink performance from existing spectrum and radio assets, while enabling a transition toward AI-native network architectures through software-centric evolution. Key take-aways:

- Nokia launches the industry’s first commercial AI-RAN platform, turning AI-RAN from vision into reality and providing a practical path to AI-native networks.

- Built on Nokia’s AI-native anyRAN software and NVIDIA’s Aerial AI-RAN platform, it will deliver more than 100% spectral efficiency gains by 2028, doubling the capacity of existing spectrum assets.

- Nokia’s anyRAN software will support three new accelerated computing baseband platforms. In addition, its existing portfolio will be fully ORAN compliant so operators can modernize at their own pace.

“AI-RAN is the biggest innovation in radio in decades. AI-RAN makes the network intelligent, extends AI into the physical world, and allows telcos to get more from their existing infrastructure, including a software upgrade path to 6G. Nokia’s anyRAN software, powered by NVIDIA’s Aerial AI-RAN platform, unlocks greater performance from the spectrum operators already have and can be deployed with existing Nokia or ORAN-compliant radio units. For operators, that means more performance, better returns and faster delivery of new services,” said Justin Hotard, President and Chief Executive Officer at Nokia.

The platform is built on Nokia’s AI-native network architecture and leverages NVIDIA’s accelerated computing stack to enable AI-driven radio optimization. Initial results indicate spectral efficiency gains exceeding 20% through AI-enhanced radio resource management and signal processing techniques. Nokia’s roadmap targets up to 50% gains by 2027 and greater than 100% by 2028, with the objective of increasing capacity in dense deployments while reducing cost per bit and improving user experience.

“Telecommunications is entering the AI era — the radio access network is the next AI infrastructure,” said Jensen Huang, CEO and founder of NVIDIA. “Together with Nokia, we are bringing NVIDIA CUDA and AI into the baseband, transforming RAN into a planet-scale AI computer. This is a generational shift for operators — unlocking more capacity and efficiency from today’s spectrum while creating the foundation for new AI services and the 6G era.”

Image credit: Nokia

A key element of the offering is a software subscription model that enables operators to access ongoing AI-driven enhancements, feature updates, and performance improvements independent of hardware upgrade cycles. Nokia expects pilot deployments to begin by the end of the year, with broader commercial availability targeted for 2027. The roadmap incorporates NVIDIA’s programmable merchant silicon to support continued performance scaling and feature evolution.

“Nokia’s AI-RAN launch represents an important step in bringing AI-RAN from industry vision to commercial reality. The addition of the new AI-RAN node alongside the AirScale capacity plug-in unit and cloud-native deployment options gives operators practical choices for adopting AI-native networks based on their existing infrastructure and transformation goals. By combining AI-accelerated computing with a software-defined architecture and a clear product roadmap, Nokia is helping operators unlock greater capacity, improve network economics and accelerate the transition toward AI-native RAN,” commented Rémy Pascal, Practice Leader, Mobile Infrastructure at Omdia.

Light Reading’s Iain Morris wrote:

Nokia’s vision, outlined during an exclusive interview with Light Reading, is that the Nvidia-based hardware products announced today and available from next year will potentially last customers deep into the 6G era. That cannot be said of the latest Nokia hardware in commercial use, based on custom silicon provided by Marvell Technology, according to Atkinson. The same would be true of the latest hardware from rival Ericsson, he believes: “It will get them into 6G, but it won’t see them long into 6G.”

The Nokia pivot to GPUs sets up a riveting clash between the two Nordic companies. Ericsson remains firmly attached to its own custom silicon, and its top executives think writing code for CUDA, Nvidia’s software platform, could make Nokia a victim of “vendor lock-in,” imprisoned by a single vendor’s hardware.

For telcos interested in general-purpose processors and the greater freedom they promise, Ericsson instead offers a set of “virtual” RAN products. While based today on Intel’s central processing units (CPUs), the same software can run on CPUs from other chipmakers after minimal tweaks, according to Ericsson. Only a small amount of code remains hardware-dependent, it says.

,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,

Nokia’s AI-RAN platform is based on a common, software-defined architecture integrating its anyRAN software with NVIDIA’s accelerated computing. The platform supports 4G, 5G, and forward evolution toward 6G, while maintaining compliance with Open RAN specifications to enable multi-vendor interoperability. Operators can select from multiple deployment options aligned with their installed base and transformation strategy, while leveraging a unified software roadmap.

For network operators with existing Nokia AirScale deployments, the introduction of a GPU-accelerated capacity plug-in unit provides a relatively low-friction upgrade path. This approach integrates accelerated computing into the current RAN footprint, enabling step-function capacity improvements while preserving prior infrastructure investments. Nokia also highlights support for AI-optimized merchant silicon, including contributions from partners such as Marvell, reflecting a broader ecosystem strategy for AI-RAN evolution.

Nokia is also introducing a GPU-based standalone AI-RAN node designed for flexible deployment across diverse network environments. The platform supports 4G, 5G, and future 6G workloads and can be deployed as a discrete node, in clustered configurations, or integrated with existing AirScale systems as a logical baseband. This enables scalable deployment of AI-native capacity while maintaining architectural flexibility.

For network operators pursuing cloud-native RAN strategies, Nokia’s AI-RAN capabilities extend to GPU-enabled COTS server platforms delivered through ecosystem partners. This approach supports deployment on standardized, accelerated infrastructure while aligning with open and secure supply chain principles. It combines cloud-native operational models with the performance requirements of AI-intensive RAN workloads.

Nokia’s AI-RAN introduces a shift from hardware-centric lifecycle management to a software-driven innovation model. Through its subscription-based framework, operators gain continuous access to evolving AI algorithms, spectral efficiency enhancements, and network optimization capabilities. This model enables ongoing improvements in performance, efficiency, security, and resilience without requiring discrete hardware upgrades, thereby improving total cost of ownership and extending asset lifecycles.

By combining AI-accelerated computing, software-defined RAN architecture, and an open ecosystem approach, Nokia’s AI-RAN platform is intended to provide operators with a scalable pathway to increased capacity, improved economic performance, and continuous innovation as networks evolve toward the 6G era.

References:

https://www.nokia.com/radio-access/ai-ran/

https://www.lightreading.com/6g/nokia-says-long-term-6g-is-not-doable-without-nvidia