Samsung and Ciena partner to deliver pre-validated implementations of 5G networks

At 2021 MWC LA, Samsung Electronics and Ciena announced that they are collaborating to deliver 5G solutions (?) by coupling Samsung’s 5G RAN and core network with Ciena’s xHaul routing and switching portfolio. The collaboration will enable the companies to offer hardware and software solutions to telecom operators to support the increasing volume of 5G data traffic at the edge and within an increasingly distributed 5G architecture.

Rafael Francis, senior director of solutions architecture at Ciena, sited the blurring between the RAN, transport and core network as motivation for the partnership with Samsung.

![]()

Image Courtesy of ACG Research

“The domains of RAN, transport and core are becoming more tied in the sense as operators roll out 5G with new architectures and approaches, like virtualized RAN (vRAN) or cloud RAN (cRAN),” Francis told RCR Wireless News. “Effectively, the network becomes an integral part of that because you not only have backhaul networks, but you have fronthaul and mid-haul networks, and these things all need to interoperate.”

5G xHaul transport needs a solution-level approach that includes both a feature-rich box and a well-integrated automation and orchestration platform. Ciena provides a complete yet open solution with its innovative Adaptive IPTM portfolio, which is well integrated with its Blue Planet Automation software. The company has simplified the 5G xHaul transport with a lean and open set of IP protocols driven by analytics focused, multidomain and multivendor closed-loop orchestration layer.

Alok Shah, Samsung’s VP of strategy, business development and marketing for the company’s networks business, agreed with Francis, adding, “Networks used to be a lot easier to understand. The RAN and the core were well defined, and the transport was backhaul for the cell sites.”

Now, though, in the world of vRAN and cRAN, the backhaul is only one means of transport. There is also fronthaul and mid-haul and, according to Shah, each one has a different level of performance requirement; when it comes to the fronthaul, in particular, the link between fronthaul and the RAN equipment has to be “really tight.”

“Because, you want to make sure that if you’re running 25 Gbps from your radio back to baseband unit, you want to make sure you’re getting the full performance out of that link,” Shah added.

Further, the combined offering will help operators accelerate critical 5G capabilities such as network slicing (requires 5G SA Core network), which Francis singled out a perfect example of why coordination across network domains has become more critical in a 5G era.

“Concepts and capabilities brought by 5G such as network slicing that can be used to drive new revenues and services for MNOs (mobile network operators) must be well coordinated across RAN, transport and core to really have the correct impact like ensuring SLAs and partitioning resources,” Shah said.

Wonil Roh, SVP and head of product strategy for Samsung Electronics’ network business said, “In order to deliver more powerful 5G services, the current network architecture needs to evolve. Samsung’s ability to couple our best-in-class 5G solutions with a leader in transport technologies like Ciena will give customers a solution to address this need, and do so with the confidence to scale and evolve their networks to support the future of 5G.”

Dell’Oro Group VP Stefan Pongratz noted that the two vendors have no material overlap. “Ciena’s telecom equipment revenues are primarily driven by its optical transport and SP switch portfolio while Samsung focuses on the RAN and mobile core markets,” he said. Stefan added that “as the backhaul becomes fronthaul, the transport requirements will change, which could impact the value of pre-integrated solutions.”

……………………………………………………………………………………………………………………………………………

References:

Samsung, Ciena partner to address ‘blurring between RAN, transport and core’

Telenor Deploys 5G xHaul Transport Network from Cisco and NEC; xHaul & ITU-T G.8300 Explained

IBM says 5G killer app is connecting industrial robots: edge computing with private 5G

At 2021 MWC-LA, IBM CTO for networking and edge computing Rob High suggested that connecting maintenance robots (one named Spot is pictured below) as the so-called killer application for 5G. citing wide potential benefits for industry. In a keynote presentation made alongside robotics company Boston Dynamics, the IBM CTO (pictured left) highlighted the benefits of systems employing edge computing (more below) technology together with private 5G in industrial scenarios. The two companies highlighted Spot’s role to assess the performance of analog machinery still in use.

“For all my network operator friends in the audience who keep asking what’s the killer app for 5G? This is it,” High said. “It’s around production processes valuable to industries that are needed, and need 5G to accomplish their tasks to maintain operational readiness and efficiencies,” he added.

“That’s where 5G is going to have its biggest benefit,” he added, noting although the maintenance robot did a lot of local processing it needed to be on a communications network as it was programmed to raise urgent issues. However, High did not state what benefits/features 5G has that makes robot connectivity the killer app. In particular, ultra high reliability is required but neither ITU-R M.2150 or 3GPP Release 16 supports that in the 5G RIT/RAN.

Boston Dynamics’ chief sales officer Mike Pollitt highlighted Spot’s ability to assess machinery and other assets across industrial sites in difficult-to-reach areas and those dangerous for humans. Potential applications include taking readings from analog machines, proactive maintenance and general site investigation.

High added with a long asset life on much industrial machinery, these types of technological solutions could fill the “data gap” by assessing sites without the need to retrofit connectivity hardware into every piece of equipment.

The robotics company has been working with IBM on industrial deployments with Spot relying on the latter’s application management system.

IBM says that edge computing with 5G (requires 5G SA core network) creates tremendous opportunities in every industry. It brings computation and data storage closer to where data is generated, enabling better data control, reduced costs, faster insights and actions, and continuous operations. By 2025, 75% of enterprise data will be processed at the edge, compared to only 10% today.

IBM provides an autonomous management offering that addresses the scale, variability and rate of change in edge environments. IBM also offers solutions to help communications companies modernize their networks and deliver new services at the edge.

References:

https://www.mobileworldlive.com/featured-content/top-three/ibm-spots-killer-industrial-5g-app

https://www.ibm.com/cloud/edge-computing

Reuters: FCC revokes authorization of China Telecom’s U.S. unit

The U.S. Federal Communications Commission (FCC) on Tuesday voted to revoke the authorization for China Telecom’s U.S. subsidiary to operate in the United States, citing national security concerns. That despite the fact that the China telecom has a presence in the U.S.

The decision means China Telecom Americas must now discontinue U.S. services within 60 days. China Telecom, the largest Chinese telecommunications company, has had authorization to provide telecommunications services for nearly 20 years in the United States.

The FCC found that China Telecom “is subject to exploitation, influence, and control by the Chinese government and is highly likely to be forced to comply with Chinese government requests without sufficient legal procedures subject to independent judicial oversight.”

The U.S. regulator added that Chinese government ownership and control “raise significant national security and law enforcement risks by providing opportunities” for the company and the Chinese government “to access, store, disrupt, and/or misroute U.S. communications.”

“The FCC’s decision is disappointing. We plan to pursue all available options while continuing to serve our customers,” a China Telecoms America spokesperson told Reuters.

China Telecom served more than 335 million subscribers worldwide as of 2019 and claims to be the largest fixed line and broadband operator in the world, according to a Senate report, and also provides services to Chinese government facilities in the United States.

The U.S. government said in April 2020 China Telecom targets its mobile virtual network to more than 4 million Chinese Americans; 2 million Chinese tourists a year visiting the United States; 300,000 Chinese students at American colleges; and the more than 1,500 Chinese businesses in America.

In April, 2020, the FCC warned it might shut down U.S. operations of three state-controlled Chinese telecommunications companies, citing national security risks, including China Telecom Americas as well as China Unicom Americas, Pacific Networks Corp and its wholly owned subsidiary ComNet (USA) LLC after U.S. agencies raised national security concerns.

FCC Commissioner Brendan Carr, a Republican, said the FCC “must remain vigilant to the threats posed” by China. The Chinese Embassy in Washington did not respond to a request for comment.

U.S. Senators Rob Portman and Tom Carper, who issued a report in 2020 on Chinese telecom companies U.S. operations, praised the FCC decision in a joint statement that cited “substantial and serious national security and law enforcement risks.”

In March, the FCC began efforts to revoke authorization for China Unicom Americas, Pacific Networks and its wholly-owned subsidiary ComNet to provide U.S. telecommunications services.

In May 2019, the FCC voted unanimously to deny another state-owned Chinese telecommunications company, China Mobile the right to provide U.S. services.

The FCC has taken other actions against Chinese telecoms and other companies. Last year, the FCC designated Huawei Technologies Co and ZTE Corp, as national security threats to communications networks – a declaration that barred U.S. firms from tapping an $8.3 billion government fund to purchase equipment from the companies. The FCC in December adopted rules requiring carriers with ZTE or Huawei equipment to “rip and replace” that equipment.

In March, the FCC designated five Chinese companies as posing a threat to national security under a 2019 law, including Huawei, ZTE, Hytera Communications, Hangzhou Hikvision Digital Technology Co and Zhejiang Dahua Technology Co.

Verizon partners with Amazon Project Kuiper to offer FWA in unconnected and underserved areas

Today at the 2021 Mobile World Congress (MWC) Los Angeles CA, Verizon and Amazon announced a strategic collaboration that will combine Verizon’s 5G wireless network with Amazon’s Project Kuiper constellation of low-Earth orbit (LEO) satellites. The first offering from the new partnership will backhaul Verizon’s cell sites through Amazon’s LEO satellites, enabling Verizon to offer fixed wireless access (FWA) in unconnected rural or underserved areas.

As part of the collaboration, Project Kuiper and Verizon have begun to develop technical specifications [1.] and define preliminary commercial models for a range of connectivity services for U.S. consumers and global enterprise customers operating in rural and remote locations around the world.

Note 1. There are no 3GPP specifications or ITU recommendations for the use of LEO satellites for 5G (IMT 2020/ITU-R M.2150) backhaul. Therefore, new carrier specifications are needed for 5G RANs to use LEO satellite networks for backhaul.

However, 3GPP is planning to include non-terrestrial networks (NTN) and to address satellite’s role in the 5G vision in their Release 17 package of specifications, to be released next year. You can read an overview of 3GPP NTN’s here.

ITU-R SG 4 is responsible for Satellite services. That includes Systems and networks for the fixed-satellite service, mobile-satellite service, broadcasting-satellite service and radiodetermination-satellite service. In particular,

ITU-R WP4B carries out studies on performance, availability, air interfaces and earth-station equipment of satellite systems in the FSS, BSS and MSS. This group has paid particular attention to the studies of Internet Protocol (IP)-related system aspects and performance and has developed new and revised Recommendations and Reports on IP over satellite to meet the growing need for satellite links to carry IP traffic. This group has close cooperation with the ITU Telecommunication Standardization Sector. Of particular interest are:

- Terms of Reference for Working Party 4B Correspondence Group on satellite radio interface technologies for the satellite component of IMT-2020.

- Working document towards a preliminary draft new Report ITU-R M.[XYZ.ABC] on Vision and requirements for satellite radio interface(s) of IMT-2020

…………………………………………………………………………………………………………………………………………………….

Amazon’s Project Kuiper is an initiative to increase global broadband access through a constellation of 3,236 satellites in low Earth orbit (LEO) around the planet. The system will serve individual households, as well as schools, hospitals, businesses and other organizations operating in places where internet access is limited or unavailable. Amazon has committed an initial $10 billion to the program, which will deliver fast, affordable broadband to customers and communities around the world.

The Verizon-Amazon partnership seeks to expand coverage and deliver new customer-focused connectivity solutions that combine Amazon’s advanced LEO satellite system and Verizon’s world-class wireless technology and infrastructure. To begin, Amazon and Verizon will focus on expanding Verizon data networks using cellular backhaul solutions from Project Kuiper. The integration will leverage antenna development already in progress from the Project Kuiper team, and both engineering teams are now working together to define technical requirements to help extend fixed wireless coverage to rural and remote communities across the United States.

Verizon Chairman and CEO Hans Vestberg said, “Project Kuiper offers flexibility and unique capabilities for a LEO satellite system, and we’re excited about the prospect of adding a complementary connectivity layer to our existing partnership with Amazon. We know the future will be built on our leading 5G network, designed for mobility, fixed wireless access and real-time cloud compute. More importantly, we believe that the power of this technology must be accessible for all. Today’s announcement will help us explore ways to bridge that divide and accelerate the benefits and innovation of wireless connectivity, helping benefit our customers on both a global and local scale.”

Amazon CEO Andy Jassy said, “There are billions of people without reliable broadband access, and no single company will close the digital divide on its own. Verizon is a leader in wireless technology and infrastructure, and we’re proud to be working together to explore bringing fast, reliable broadband to the customers and communities who need it most. We look forward to partnering with companies and organizations around the world who share this commitment.”

This partnership will also pave the way for Project Kuiper and Verizon to design and deploy new connectivity solutions across a range of domestic and global industries, from agriculture and energy to manufacturing and transportation. The Kuiper System is designed with the flexibility and capacity to support enterprises of all sizes. By pairing those capabilities with Verizon’s wireless, private networking and edge compute solutions, the two will be able to extend connectivity to businesses operating and deploying assets on a global scale.

Betsy Huber, President, The National Grange said: “The agriculture industry is going to see dramatic changes in how it operates and succeeds in the next several years. Smart farms, bringing technology to agriculture, and connecting the last mile of rural America will be at the forefront of helping our industry to provide food for billions around the globe. Ensuring connectivity in rural areas will be key to making these endeavors a success. We’re excited to see the leadership from both companies working together to help take our industry to the next level.”

Financial analysts at New Street Research said the opportunity could be worth billions of dollars to the two companies. Specifically, they argued that Verizon’s wireless network currently does not cover around 7 million Americans. “If 50% of these people become Kuiper/Verizon customers and assuming Verizon’s phone ARPU [average revenue per user] of ~$60, there could be $2.4 billion in annual revenue,” they wrote.

Amazon and Verizon have previously teamed up to serve customers across many industries, including integrating Verizon’s 5G Edge MEC platform with AWS Wavelength and forming the Voice Interoperability Initiative. This collaboration builds on the relationship between the two companies, and lays the groundwork for Amazon and Verizon to serve additional consumer and global enterprise customers around the world.

Executives from Verizon and Amazon hinted that backhaul is only the start of the companies’ new partnership. They noted that Verizon’s plan to use Amazon’s LEO satellites is just the latest in a long line of pairings between the companies stretching from edge computing to private wireless networks.

“We’ve worked with Verizon on many complex projects over the years,” Amazon SVP David Limp said during a keynote presentation at MWC LA. Limp said Amazon continues to design and build its LEO satellites at the company’s Redmond, Washington, offices.

Verizon’s Chief Strategy Officer Rima Qureshi suggested Amazon and Verizon would explore other offerings beyond cell-site backhaul in the future. She said the companies would pursue “joint solutions” for large enterprise customers in industries stretching from agriculture to energy to education. She also said Verizon and Amazon would look for opportunities both domestically and internationally.

Qureshi noted Verizon’s deal with Nokia to deploy a private 5G network for Southampton in the UK – the largest of the 21 Associated British Ports. She suggested an Amazon-powered satellite component to that offering could extend connectivity beyond the port and into the ocean.

A spokesman for Verizon told Bloomberg it’s a global partnership with Amazon and it’s open to exploring similar deals with other companies, but declined to comment on the finances of the deal.

5G wireless telco’s deals with LEO satellite companies:

This new alliance between Verizon and Project Kuiper comes six weeks after AT&T made a similar deal with LEO satellite operator OneWeb. Just like Verizon, AT&T said it would use that agreement LEO (OneWeb) satellites to extend its connectivity reach to hard-to-serve areas that fall outside of AT&T’s fiber footprint or are beyond the reach of AT&T’s cell towers. AT&T said it would use LEO technology to enhance connectivity when connecting to its enterprise, small and medium-sized business and government customers as well as hard-to-reach cell towers.

In January, KDDI in Japan said it would use Starlink – the LEO offering from Elon Musk’s SpaceX – to connect 1,200 of its remote cell towers with backhaul. KDDI said it would begin offering services under that new teaming as soon as next year.

However, Project Kuiper is way behind both Starlink and OneWeb in terms of satellite deployments. As noted by GeekWire, Starlink already counts 1,650 satellites in orbit (and around 100,000 users), while OneWeb’s constellation is now up to around 358 satellites. Amazon, meantime, has received FCC approvals for the operation of more than 3,000 LEO satellites but has yet to launch any of them. Amazon has committed $10 billion toward the construction of its Kuiper LEO satellite network.

References:

https://www.verizon.com/about/news/5g-leo-verizon-project-kuiper-team

https://www.bloomberg.com/news/articles/2021-10-26/amazon-signs-satellite-pact-with-verizon-in-challenge-to-musk

To learn more about partnering with Amazon and the Project Kuiper team, email [email protected]

……………………………………………………………………………………….

Related Articles:

https://news.kddi.com/kddi/corporate/english/newsrelease/2021/09/13/5400.html

Telenor Deploys 5G xHaul Transport Network from Cisco and NEC; xHaul & ITU-T G.8300 Explained

NEC Corp. and Cisco have been selected by Telenor to deploy 5G xHaul transport networks in Norway and Denmark. 5G-xHaul proposes a converged optical and wireless network solution able to flexibly connect Small Cells to the core network.

In April this year, NEC and Cisco entered a Global System Integrator Agreement (GSIA) to expand their partnership for accelerating the deployment of innovative 5G IP transport network solutions worldwide. This project is a flagship initiative in which the two companies take full advantage of the GSIA and collaborate to deliver state-of-the-art networks to the customer.

NEC and Telenor have a well-established history of working together, and this project is an extension of a global frame agreement signed in 2016 for Telenor’s 4G IP / Multi-Protocol Label Switching (MPLS) network in Scandinavia, to deliver next-generation networks to the operator.

For this specific project, Cisco will supply its NCS 540 series as the cell site router and NEC will provide value added services built on its expertise both in the IT and network domain to implement an architecture that enables flexible and highly scalable end-to-end IP/MPLS networks with bandwidth that can support the high-capacity and low-latency communication required by 5G.

“As a One-stop Network Integrator, NEC takes a customer-first approach, providing optimal solutions that match individual requirements based on our best-of-breed ecosystem, consisting of NEC’s own products and those from industry-leading partners such as Cisco. We are excited to contribute to the advancement of Telenor’s 5G network evolution,” said Mayuko Tatewaki, General Manager, Service Provider Solutions Division, NEC Corporation.

“At Cisco, we continue to look for ways we can shape the future of the internet by providing unparalleled value to our customers and our partners,” said Shaun McCarthy, Vice President of Worldwide Sales, Mass Infrastructure Group, Cisco. “Through our partnership with NEC, we can help Telenor connect more people in Norway and Denmark and provide the automation and orchestration necessary to meet future demands on the network.”

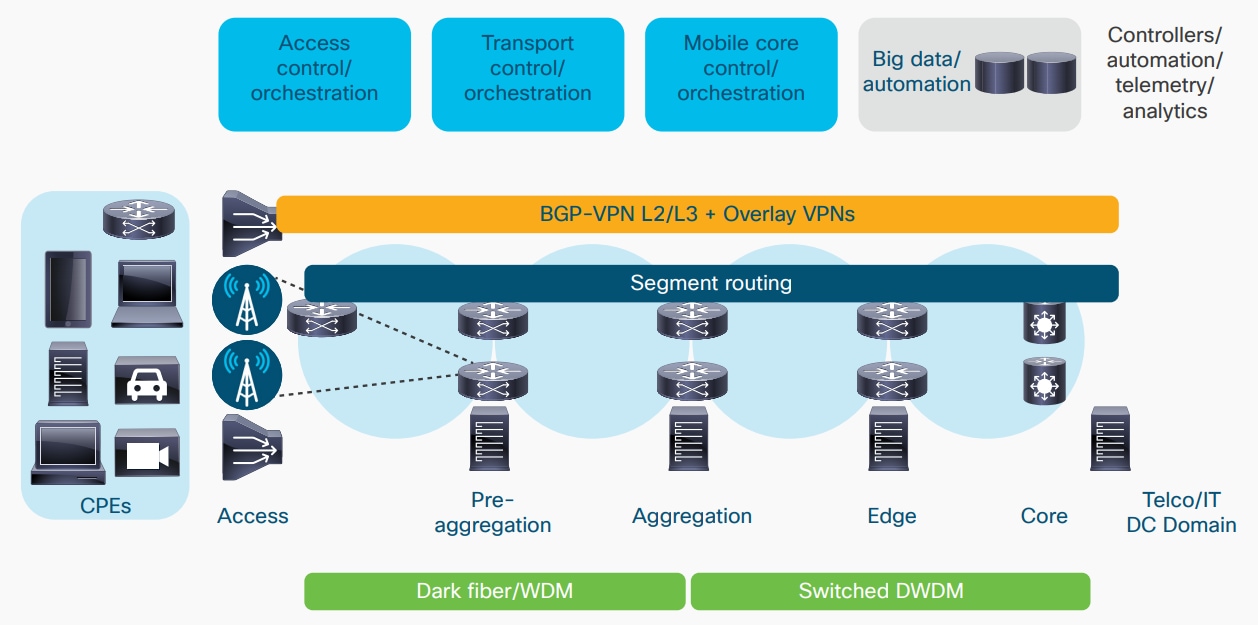

Cisco believes that a converged, end-to-end packet infrastructure, beginning in the access layer and stretching via the network data center all the way to the core, based upon segment routing and packet-based QoS, provides the underlying xHaul transport network (see Figure below). This provides the most flexibility of application placement, the best scalability, the most robust reliability, and the leanest operational costs. On top of this, we layer VPN services, either based on BGP-based VPNs or business software-defined WAN (SD-WAN) technologies, to provide the means to support a multi-service environment capable of supporting strict SLAs.

Overall Architecture for 5G xHaul:

Editor’s Note:

ITU-T G.8300 recommendation “Characteristics of transport networks to support IMT-2020/5G” defines the requirements for the Physical layer transport network support for the 5G fronthaul, midhaul and backhaul networks. The digital clients are the digital streams to/from the 5G entities (e.g., RU, DU, CU, 5GC/NGC) and other digital clients carried in the access, aggregation and core transport networks. The requirements and characteristics are documented for each of the fronthaul, midhaul and backhaul networks as defined in this recommendation.

The factors addressed include:

• Relationship of 5G network architecture to transport network architecture

• Operations, administration, and maintenance (OAM) requirements

• Timing performance and time/synchronization distribution architecture

• Survivability mechanisms

………………………………………………………………………………………………………………………………

NEC and Telenor have worked together before, with this announcement representing an extension of a previous global frame agreement signed in 2016 for Telenor’s 4G IP/Multi-Protocol Label Switching (MPLS) network in Scandinavia. As part of the agreement, the system integrated helped Telenor prepare, enable and perform the migration of services in a turnkey arrangement.

Going forward, NEC and Cisco will continue making collaborative efforts to further enhance their joint solution portfolio and to optimize regional activities for advancing the digital transformation of customers across the globe.

References:

https://newsroom.cisco.com/press-release-content?type=webcontent&articleId=2203825

http://Telenor Deploys 5G xHaul Transport Network from Cisco and NEC

https://www.nec.com/en/press/201603/global_20160331_01.html

Juniper Research: Mobile Roaming and the $2 Billion Revenue Leakage Problem

Juniper Research has found that the inability to distinguish between 4G and 5G data traffic using current standards will result in greater roaming revenue losses as the travel industry returns to pre-pandemic levels and 5G adoption increases. Juniper expects losses from roaming data traffic misidentification will rise to $2.1 billion by 2026 if the industry doesn’t implement the Billing & Charging Evolution Protocol (BCE), an end-to-end industry-wide standard defined by the GSMA that introduces new capabilities that identify roaming data traffic over different network technologies.

In response, the new research, Data & Financial Clearing: Emerging Trends, Key Opportunities & Market Forecasts 2021-2026, cited the support by operators for the BCE (Billing & Charging Evolution) protocol as being a key strategy to minimize the extent of revenue leakage. BCE is an end-to-end industry-wide standard defined by the GSMA that introduces new capabilities that identify roaming data traffic over different network technologies.

This issue of misidentifying roaming data will only be exacerbated by the rising number of 5G subscribers roaming internationally. The report forecasts that there will be over 200 million 5G roaming connections by 2026; rising from 5 million in 2021. This growth is driven by increasing 5G adoption and a return to pre-pandemic levels of international travel. In response, it urged operators to identify emerging areas of potential revenue leakage by leveraging machine learning in roaming analytics tools to efficiently assess roaming behavior and data usage.

In addition, the report found that, to effectively mitigate the growing complexity of clearing processes arising from increased demand for data when roaming, operators must move away from established roaming clearing practices in favor of BCE.

Research author Scarlett Woodford remarked:

“By combining BCE with AI-enabled roaming analytics suites, operators will be ideally positioned to deal with the rise in roaming data. Separating roaming traffic by network connectivity is essential to allow operators to charge roaming partners based on latency and download speed, and maximize overall 5G roaming revenue.”

Steering of Roaming Explained:

Roaming revenue can be drastically affected by regional regulations and pricing decreases; resulting in operators seeking alternative ways of generating profits from roaming traffic. The term ‘Steering of Roaming’ refers to a process in which roaming traffic is redirected to networks with whom an operator has the best wholesale rates. Operators are able to prioritize which network a device connects to when multiple networks are within range. Mobile operators are able to decide which partner network their subscribers will use whilst roaming, in order to reduce outbound roaming costs and ensure that roaming subscribers receive high-quality service.

Operators can rely on third-party enterprises to provide this service, such as BICS, with business analytics used to guide roaming traffic and identify preferential partner networks. If implemented correctly, steering of roaming can help operators increase margins through the reduction of operating costs. Roaming traffic is directed to the partner network offering the best rates, ultimately resulting in operators being able to pass these savings onto their subscribers with lower roaming charges.

References:

https://www.juniperresearch.com/pressreleases/roaming-revenue-losses-to-surpass-$2bn

https://www.juniperresearch.com/whitepapers/mobile-roaming-the-2-bn-revenue-leakage

UK-India research project to progress 5G and future telecom networks

The UK-India Future Networks Initiative (UKI-FNI) is a£1.4 million project, led by the University of East Anglia in collaboration with other UK and Indian universities. Its objective is to build the capability, capacity, and relationships between the two countries in telecoms diversification technologies and research for 5G and beyond. The project will explore hardware and software solutions for future digital networks, as well as develop a joint UK/India vision for Beyond 5G and 5G. The development of Open Radio Access Networks (OpenRAN) will be a key part of the project.

The project is funded by the UK Engineering & Physical Sciences Research Council (EPSRC).

The 5G/6G Innovation Centre (5G/6GIC) at the University of Surrey in the UK will play a key role in a project to examine advanced technologies for future digital telecoms networks. The 5G/6GIC will work with the University of East Anglia (project lead), University College London and the University of Southampton in the UK; and the Indian Institute of Technology (IIT) Delhi and the Indian Institute of Science in (IIS) Bangalore.

The 5G vision of the Centre includes:

- Indoors and outdoors

- Dense urban centres with capacity challenges

- Sparse rural locations where coverage is the main challenge

- Places with existing infrastructure, and areas where there is none

India has an excellent research and innovation base in networking systems software and has the complex testbeds required for proving new technologies. Indeed, under a previous £20 million EPSRC initiative led in the UK by Prof Parr (the India-UK Advanced Technology Centre), the team collaborated for more than 10 years with partners across India – an experience that will be leveraged in the UKI-FNI project.

Prof Parr said: “To those of us who have access to telecommunications services and the Internet, it comes as no surprise how reliant we are on voice, data and web services for email, video conferencing and file sharing, as well as social media for business and personal needs. This has been much more visible during the Covid pandemic. For the telecoms service providers there are important considerations in providing all these systems across regions and nations, including performance, cyber security, energy efficiency, scalability and operational costs for maintenance and upgrades.”

“The consideration on costs is attracting increasing attention when we consider the limited number of global vendors who manufacture and supply the systems over which our data flows across the national and international networks.”

There is a global push to explore innovations that will deliver the infrastructure, systems and services for next-generation mobile communication networks. Part of this drive is coming from network operators who are seeking solutions to reduce the costs for network components by aiming to remove dependence and lock-in to a small group of telecom original equipment manufacturers.

A leading idea is that the 5G infrastructure should be far more demand/user/device centric with the agility to marshal network/spectrum resources to deliver “always sufficient” data rate and low latency to give the users the perception of infinite capacity. This offers a route to much higher-performing networks and a far more predictable quality of experience that is essential for an infrastructure that is to support an expanding digital economy and connected society.

Sanjeev K Varshney, Head of International Cooperation at the DST, said: “The announcement of the India-UK partnership to develop newer research opportunities in future telecom networks is very timely and we look forward to developing new bilateral collaboration in this and other emerging areas of mutual interest.”

Rebecca Fairbairn, Director UKRI India, said: “UKRI India, in collaboration with our partner funders in India, is delighted to announce a drive towards a new Indo-UK research and innovation partnership on future telecom networks.

“Bringing together both our countries’ scientists, engineers, and innovators we will jointly develop new knowledge and high-impact research and innovation in line with our shared 2030 India-UK roadmap.”

Professor Gerard Parr, Principal Investigator for UKI-FNI, University of East Anglia, said: “There are many benefits to be accrued from the UKI-FNI project as we explore new innovative solutions in hardware, software and protocols.

“Ultimately, we will develop a roadmap for a much larger, mutually beneficial and longer-term collaboration between India and the UK in the important digital telecoms sector.”

References:

https://www.surrey.ac.uk/institute-communication-systems/5g-innovation-centre

https://www.uea.ac.uk/news/-/article/uea-leads-on-uk-india-future-telecom-network-partnership-c2-a0

Orange and Nokia deploy 4G LTE private network for Butachimie in Alsace, France

Orange Business Services and Nokia are deploying a redundant and secure 4G-LTE private mobile network that can be upgraded to 5G network at Butachimie’s Chalampé plant in Alsace, France. The network uses the 2.6 GHz spectrum, which French regulator Arcep has designated for mobile networks built to meet businesses’ specific needs. It also uses TDD (Time Division Duplexing) to separate wireless transmit and receive channels.

Butachimie will connect factory equipment and assets to the network, which is expected to allow technicians to geolocate assets with pinpoint accuracy. Nokia will supply a dedicated core network as well as RAN equipment, so that all network data stays onsite. The companies said both the factory equipment and the data it generates will be visible on the network at all times, enabling the manufacturer to prevent failures and ensure continuous production.

This private 4G network allows Butachimie teams to gain controlled and effective access to information system applications; they can also take advantage of new services via wirelessly connected devices (geolocation, intercom, camera, real-time sharing of videos and images, etc.). In addition, the equipment and the data collected ensure a high level of network availability of more than 99.99%, which makes it possible to forecast incipient network failures and guarantee continuous production within the plant.

Stéphane Cazabonne, project manager at Butachimie, said: “Our digital transformation and modernization plan has to meet very stringent challenges in terms of security and availability. Therefore, it is essential for us to be able to rely on reliable partners who can provide us with technological robustness, personalized support, and our business knowledge and related uses. Thanks to Orange Business Services and Nokia, we are taking a new step towards developing the Factory of the Future by offering our operators new tools to increase our performance and competitiveness in our industry. With this scalable network, we can finally benefit from the performance and benefits of the technology, such as 5G, which is already predicted.”

Butachimie’s Chalampé Plant. Photo credit: Butachimie

Butachimie’s Chalampé Plant. Photo credit: Butachimie

Orange Business Services provides advice and technical support on full network management and the use cases around it. Industry 4.0 [1.] current or future. In the design phase, Orange Business Services considered the scalability of the private mobile network, in particular by designing an architecture adapted to the principles of Mobile Edge Computing.

Note 1. Towards Factory 4.0:

Since 2010 Butachimie has been involved in the MIRe project. All the electronics on the site will be completely reviewed and modified by 2022 in order to optimize production. Digitalizing our processes and incorporating digital tools will allow us to improve both performance and competitiveness. It will also speed up process development while following the fundamental rules of safety and sustainability.

…………………………………………………………………………………………………………………………………………………

Denis de Drouâs, director of the private radio networks program at Orange Business Services, said that Butachimie chose a private network that is “totally independent from the public network.” However, other manufacturers may select different solutions.

For example, Schneider Electric is using a hybrid network model that combines private and public 4G and 5G infrastructure. The network uses Orange’s commercial 5G frequencies in the 3.4-3.5GHz bands, but Schneider’s critical data is kept on its campus and can be used for low-latency, edge-based applications.

Orange says it “slices its public network” for enterprise customers, according to de Drouâs. However, that is not the same as “network slicing” (?) which requires a 5G SA core network. Commercial frequencies are used, and the “private slice” guarantees the customer a specific quality of service.

This 4G Private Mobile Network is the backbone for all future applications currently under development as part of the Butachimie digital transformation project.

References:

WSJ: U.S. Wireless Carriers Are Winning 5G Customers for the Wrong Reason

AT&T and Verizon’s heavy promotions lead to booming growth, but value of next-gen networks to users still unclear, by Dan Gallagher

Even before the country’s two largest wireless carriers reported strong quarterly results this week, Morgan Stanley (MS) had a bit of cold water to splash on those carriers.

The investment bank published the results of its ninth annual broadband and wireless survey on Monday. Among the findings were that only 4% of respondents cited “innovative technology” such as 5G as an important factor in their choice of service. That number was unchanged from the previous year’s survey—despite an unremitting onslaught of marketing from wireless carriers and device makers for the next-gen wireless standard. [IEEE Techblog reported the results of the MS survey here]

That would appear inconsistent with the strong growth in wireless services reported by AT&T and Verizon VZ this week. On Wednesday, Verizon reported adding 429,000 postpaid wireless subscribers during the third quarter, which is up 52% from the number added in the same period last year. On Thursday morning, AT&T said it added 928,000 such users to its rolls in the same period—up 44% from the same period last year and the highest number of net new additions in more than a decade of what are considered the industry’s most valuable base of customers.

The two carriers have been selling 5G hard over the past couple of years. That picked up significantly last fall, when Apple Inc. launched its first iPhones compatible with the next-generation wireless technology. Those phones have been in hot demand. Analysts estimate total iPhone sales jumped 25% to a record of 237 million units in Apple’s fiscal year that ended last month, according to consensus estimates on Visible Alpha. The 5G-compatible iPhone 12 and 13 models are expected to account for more than 80% of that number.

But customers appear to be driven more by old-fashion promotions than cutting-edge technology. AT&T, Verizon and T-Mobile —which reports its results on Nov. 2—offered heavy discounts last year for iPhone 12 models paired with new 5G plans. That appears to have continued with the newest crop; wireless analyst Craig Moffett of MoffettNathanson notes that “promotions tied to premium unlimited plans have gotten richer” with the introduction of the iPhone 13 family this year. Indeed, the Morgan Stanley survey found price to be the most compelling driver in choice of a wireless plan, with 44% of respondents citing it as their top factor.

That leaves 5G itself as an uncertain selling point—but one with some big bills attached. The major carriers bid up a total of around $95 billion earlier this year for wireless spectrum licenses auctioned off by the Federal Communications Commission, and Walter Piecyk of Lightshed Partners estimates that a new auction of 3.45 GHz spectrum that kicked off earlier this month will draw total bids of around $30 billion.

These high expenses, coupled with doubts over the consumer appeal of the technology, have helped make AT&T, Verizon and T-Mobile some of the worst-performing large-cap stocks in the S&P 500 this year. All three fell Thursday even after AT&T’s strong report, and they have averaged a decline of 11% so far this year compared with a 21% rise for the main index. This 5G call is still not clear.

Verizon 5G advertisement in New York. PHOTO: John Nacion of ZUMA PRESS

(In the editor’s opinion, it should state “5G built WRONG”)

………………………………………………………………………………………………….

Editor’s Opinion:

We’ve often referred to 5G as “the greatest tech train wreck of all time.” That is because the technology (as it now exists) has over promised and under delivered. The major problems for 5G are the following:

- No ITU recommendations/standard/guidelines or 3GPP implementation specs for 5G SA Core network. That leads to many different carrier implementations, prevents roaming and interoperability. Indeed, <5% of 5G deployed networks are 5G SA. Yet ALL the 5G features and benefits, (e.g. network slicing, automation, MEC, enhanced security, etc) depend on 5G SA core network which separates the data and control planes.

- URLLC (ultra high reliability, ultra low latency) as specified by ITU-R M.2150 (previously known as IMT 2020.specs) and 3GPP release 15 (URLLC is still not complete in 3GPP release 16) do not meet the minimum performance requirements as specified in ITU-R M.2410 +.

- No standard for terrestrial frequencies or frequency arrangements, in particular the three sets of mmWave frequencies approved at the WRC 19 conference. Also, regulatory agencies like the FCC plan to license mmWave frequencies NOT approved by WRC 19 (e.g. 12 GHz). That defeats the goal of global frequency harmonization/roaming.

- Few demonstrated use cases other than Fixed Wireless Access (FWA) and massive machine to machine communication/Internet of Things (but even here URLLC (especially ultra high reliability) is needed.

+ Minimum URLLC requirements:

- Latency: <=1ms latency in the data plane and <=10ms latency in the control plane.

- Reliability: The minimum requirement for the reliability is 1-10−5 success probability of transmitting a layer 2 PDU (protocol data unit) of 32 bytes within 1 ms in channel quality of coverage edge for the Urban Macro-URLLC test environment, assuming small application data (e.g. 20 bytes application data + protocol overhead). Proponents are encouraged to consider larger packet sizes, e.g. layer 2 PDU size of up to 100 bytes.

…………………………………………………………………………………………………

References:

https://techblog.comsoc.org/2021/10/21/1058476/

https://www.itu.int/dms_pub/itu-r/opb/rep/R-REP-M.2410-2017-PDF-E.pdf

FTC Staff Report Finds Many ISPs Collect Troves of Personal Data while Consumers Have No Options

The Federal Trade Commission (FTC) staff report released on Thursday, October 21st found that a group of broadband Internet Service Providers (ISPs), including AT&T, Charter Communications, Comcast and Verizon, collect troves of personal data, and that consumers don’t have much choice on how that data is used.

Question to Ponder: Haven’t we all intuitively known that, just like Big Tech (Amazon, Google, Facebook, Apple, Microsoft) our privacy has been compromised by ISPs in return for “free services,” whereby our personal information is sold to “target advertisers?”

The report was approved unanimously 4-1 by the commission, with FTC chair Lina Khan issuing a separate statement. Khan said the FTC report highlighted:

1) Problems with the notice-and-consent framework for data collection and sharing;

2) The expansion of ISPs into vertically integrated businesses including ones providing content for their broadband “pipes”; and

3) The potential use of “hyper-granular” online dossiers to discriminate against users.

Many ISPs collect and share far more data about their customers than many consumers may expect—including access to all of their Internet traffic and real-time location data—while failing to offer consumers meaningful choices about how this data can be used, according to an FTC staff report on ISPs’ data collection and use practices.

The staff report, which details the expanding scope and some troubling aspects of some ISP data collection practices, stems from orders the FTC issued in 2019 using its authority under 6(b) of the FTC Act to six internet service providers, which make up about 98 percent of the mobile Internet market:

- AT&T Mobility LLC;

- Cellco Partnership, which does business as Verizon Wireless;

- Charter Communications Operating LLC;

- Comcast Cable Communications, which does business as Xfinity;

- T-Mobile US Inc.; and

- Google Fiber Inc.

The FTC also issued orders to three advertising entities affiliated with these ISPs: AT&T’s Appnexus Inc., rebranded as Xandr; Verizon’s Verizon Online LLC; and Oath Americas Inc., rebranded as Verizon Media. The FTC sought information on their data collection and use practices, as well as any tools provided to consumers to control these practices.

As noted in the report, these companies have evolved into technology giants who offer not just internet services but also provide a range of other services including voice, content, smart devices, advertising, and analytics—which has increased the volume of information they are capable of collecting about their customers. The report identified several troubling data collection practices among several of the ISPs, including that they combine data across product lines; combine personal, app usage, and web browsing data to target ads; place consumers into sensitive categories such as by race and sexual orientation; and share real-time location data with third-parties.

At the same time, the report found the privacy protections many of the companies offer raised several concerns. Even though several of the ISPs promise not to sell consumers personal data, they allow it to be used, transferred, and monetized by others and hide disclosures about such practices in fine print of their privacy policies. For example, several news outlets noted that subscribers’ real-time location data shared with third-party customers was being accessed by car salesmen, property managers, bail bondsmen, bounty hunters, and others without reasonable protections or consumers’ knowledge and consent, according to the report.

Many of the ISPs also claim to offer consumers choices about how their data is used and allow them to access such data. The FTC found, however, that many of these companies often make it difficult for consumers to exercise such choices and sometimes even nudge them to share even more information. In addition, while several of the ISPs promise to only keep the data for as long as needed for business purposes, the definition of what constitutes a “business purpose” varies widely among the companies.

The FTC report also found that ISPs use web browsing data and group consumers using “sensitive characteristics such as race and sexual orientation.”

The report concludes that many of the ISPs’ data collection and use practices mirror problems identified in other industries and underscore the importance of restricting data collection and use.

The Commission voted 4-0 to approve and issue the report. Staff presented findings from the report at today’s open virtual Commission meeting. Chair Lina M. Khan issued a separate statementon the report.

Cable Industry Response from the NCTA:

The report drew a sharp rebuke from the cable industry (as represented by the NCTA — The Internet & Television Association), maintaining that it provided a “highly distorted view” that casts them in the same arena as aggressive “Big Tech platforms” which are well known to compromise users privacy via data collected and sold to advertisers.

The NCTA said in a October 21st statement:

The FTC’s report provides a highly distorted view of ISP data collection policies and inappropriately attempts to lump broadband providers into the same category as the Big Tech platforms.

Cable broadband providers take seriously their responsibility to safeguard the personal information of their customers and do not surveil their customers or sell their location data. Viewed objectively, today’s presentation is a broad attack on online advertising generally, not specific ISP actions. And what is further missing from today’s report is the much larger story about Big Tech platforms that are premised on maximizing user attention.

What is needed is a consistent set of privacy rules across the online marketplace on a technology-neutral basis. We look forward to continued engagement with policymakers to forge a strong, consistent framework for privacy protection.

–>What will come of the FTC staff report is not entirely clear. FTC chair Lina Khan said it would be part of an “ongoing conversation” about privacy and data practices that could be “incorporated” into FTC action, according to Multichannel News.

…………………………………………………………………………………………………………………………………………………….

FTC Boilerplate Text:

The Federal Trade Commission works to promote competition and to protect and educate consumers. You can learn more about consumer topics and file a consumer complaint online or by calling 1-877-FTC-HELP (382-4357). For the latest news and resources, follow the FTC on social media, subscribe to press releases and read our blogs.

…………………………………………………………………………………………………………………………………………………….

Separately, Politico reported that tech and telecom companies were among the top 20 spenders for the third quarter of 2021, according to a ranking of lobbying expenditures compiled by POLITICO Influence. Facebook was No. 5 at $5.1 million, with Amazon right behind it with $4.7 million. NCTA — The Internet & Television Association ranked 15th, spending $3.3 million, and Comcast was 18th, with $3.1 million.