RAN market

Dell’Oro: AI RAN revenue forecast: $35B from 2026-to-2030; 3 types of AI RAN explained

According to a new AI RAN Advanced Research Report published by Dell’Oro Group, cumulative AI RAN revenue is projected to reach $35 B over the next five years (2026-2030). However, AI RAN is not expected to expand the overall RAN market.

“Our market assessment and long-term AI RAN position remain unchanged,” said Stefan Pongratz, Vice President at Dell’Oro Group. “AI RAN is already happening and will scale ahead of 6G. At the same time, these tools will enhance the RAN, but they are unlikely to expand the overall RAN market. Even as suppliers introduce new software-based subscription models, we expect AI RAN to generate little, if any, incremental RAN revenue the end of the forecast period,” continued Pongratz.

Additional highlights from the June 2026 AI RAN Advanced Research Report:

- The base-case forecast assumes that AI RAN will not expand the RAN market. Nevertheless, AI RAN is expected to become an important technology enabler as operators incorporate greater virtualization, intelligence, automation, and O-RAN capabilities into their RAN roadmaps.

- GPU RAN projections have been revised upward—GPU RAN is now expected to be a $1 B+ market by the end of the forecast period.

- In the near term, the AI RAN market will remain centered on AI-for-RAN, single-purpose deployments, non-GPU architectures, D-RAN, and 5G.

- Incumbent RAN radio and baseband suppliers are well-positioned in the initial AI RAN phase, driven primarily by AI-for-RAN upgrades leveraging existing hardware. Per Dell’Oro Group’s regular RAN coverage, the top five RAN suppliers contributed approximately 96 percent of 2025 RAN revenue. See charts below.

Dell’Oro Group’s AI RAN Advanced Research Report includes a 5-year forecast for AI RAN by location, tenancy, technology, and region. To purchase this report, please contact us at [email protected].

………………………………………………………………………………………………………………………………………………………………………….

Total & Wireless Telecom Equipment Revenue- top 4 and top 3:

………………………………………………………………………………………………………………………………………………………………………………….

Analysis (Source: Perplexity.ai AND Google Gemini):

There are three versions of AI-RAN which are not mutually exclusive:

- AI for RAN: Embeds AI into the base software stack to automatically manage radio waves, optimize spectrum efficiency, enhance beamforming, and reduce energy consumption in real time. Nokia, Ericsson, NVIDIA.

- AI on RAN: Uses cell towers and base stations as decentralized computing nodes. This allows telecom networks to host AI workloads locally rather than sending all data to distant cloud servers, providing ultra-low latency for applications like robotics, AR/VR, and autonomous vehicles. Nokia, NVIDIA, and operator trial partners like T-Mobile, Indosat, and SoftBank.

- AI and RAN: Combines the two to support “Networks for AI,” where distributed telecom networks act as an active, intelligent backbone to serve end-user AI traffic. AI-RAN Alliance plus Nokia and NVIDIA as the most visible industry champions.

References:

AI RAN to Reach $35 B Over Next Five Years, According to Dell’Oro Group

NVIDIA AI RAN video: youtube.com/watch?v=hwLLBfzoSko&t=26

AI-Era Cloud Network Transformation: A Reference Architecture and Implementation Roadmap

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

AI-RAN Reality Check: hype vs hesitation, shaky business case, no specific definition, no standards?

Analysis: Nvidia’s rumored new 6G AI-RAN – likely features/functions and industry impact

Dell’Oro: 2H2026 Data Center Capex to Accelerate due to massive AI Deployments

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

Dell’Oro: Global RAN market stable (again) in 1Q 2026; top 5 RAN vendors are unchanged

A recently published report from Dell’Oro Group indicates that the stable trends shaping the Radio Access Network (RAN) market in 2025 extended into the first quarter of 2026. Worldwide RAN revenue, excluding services, increased at a low-single-digit year-over-year rate in 1Q 2026, marking the fifth consecutive quarter where the market remained within a relatively narrow range (-4 to +4% year-over-year). However, market fundamentals remain constrained by slower mobile broadband growth.

“This positive start does not alter the fundamentals shaping the growth prospects of this market,” said Stefan Pongratz, Vice President for RAN market research at the Dell’Oro Group. “We attribute the improved conditions primarily to a favorable regional mix and easier comparisons in markets that experienced sharp declines. Meanwhile, RAN remains growth-constrained, and operators are increasingly preparing for a slower mobile broadband growth environment,” Pongratz added.

Additional highlights from the 1Q 2026 RAN report:

- Growth in EMEA and APAC offset weaker activity in North America.

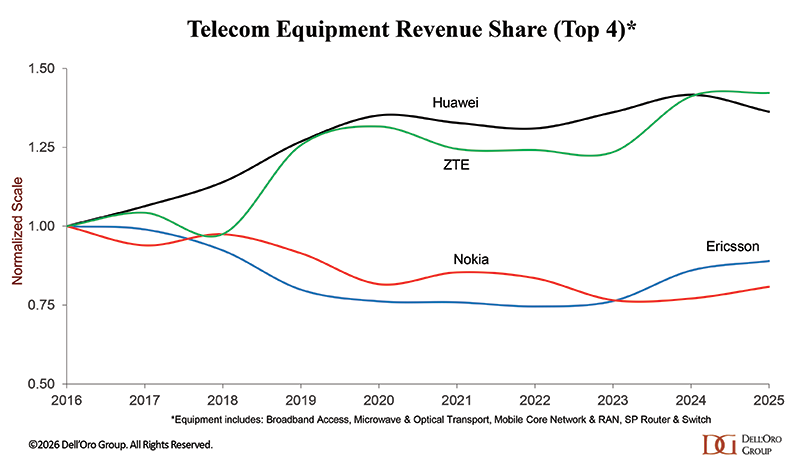

- Revenue rankings were unchanged in 1Q 2026. Based on trailing four-quarter worldwide revenue, the top five RAN suppliers are Huawei, Ericsson, Nokia, ZTE, and Samsung [1.].

- Regional imbalances continue to shape the market recovery trajectory, with APAC excluding China improving while North America and China remain under pressure.

Note 1. There were no significant market share shifts quarter-to-quarter for these five vendors whose ranking remains the same. The ongoing war in Iran, with the Strait of Hormuz closed, has disrupted supply chains for specialized components, while higher energy prices are raising operational costs for infrastructure deployment, creating an increasingly complex environment for network equipment suppliers.

Dell’Oro Group’s RAN Quarterly Report offers a complete overview of the RAN industry, with tables covering manufacturers’ and market revenue for multiple RAN segments including 5G NR Sub-7 GHz, 5G NR mmWave, LTE, Macro BTS, small cells, Massive MIMO, and Cloud RAN. The report also tracks the RAN market by region and includes a four-quarter outlook. To purchase this report, please contact us by email at [email protected]

References:

Worldwide RAN Market Remained Stable in 1Q 2026, According to Dell’Oro Group

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

ABI Research: mobile network spending to fall 29% from 2026-to-2031

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Mulit-vendor Open RAN stalls as Echostar/Dish shuts down it’s 5G network leaving Mavenir in the lurch

ABI Research: mobile network spending to fall 29% from 2026-to-2031

According to ABI Research, global mobile network infrastructure spending is projected to peak at ~$92 billion in 2026–2027 before falling 29% to $65 billion by 2031. This decline reflects the maturation of 5G deployments and a shift in operator focus toward 6G, with reduced demand for traditional Radio Access Network (RAN) equipment.

“5G deployments have seen significant growth over the years, with industry estimates placing the current number of launched 5G networks at over 350 globally,” said Matthias Foo, Principal Analyst at ABI Research. “By the end of 2025, global 5G population coverage is expected to reach 60%, driven in part by rapid deployments in India, where more than 500,000 5G Base Transceiver Stations have been installed within three years.”

As 5G rollouts mature, RAN equipment vendors are beginning to report slower growth. Even as advanced deployments such as 5G-Advanced emerge in markets like the United States, China, and Saudi Arabia, overall infrastructure demand is stabilizing following years of rapid expansion.

Recent financial results from major vendors reinforce this trend.

- Ericsson reported flat RAN growth in 2025 and expects a similar outlook for 2026.

- Nokia also posted flat performance in its Mobile Networks business.

- ZTE reported a 5.9% Year-on-Year decline in its Carriers’ Networks segment in the first half of 2025.

Following the release of their respective financial reports, both Ericsson and Nokia said they expect the RAN market to be more or less flat this year. Nokia is focusing on data center networking, while Ericsson is concentrating on mission critical communications, defense, and enterprise networking.

ABI says some near-term growth is still expected in 2026, supported by ongoing deployments in markets such as Malaysia, India, Argentina, Peru, and Vietnam.

Open RAN adoption is forecast to grow at a 26.5% CAGR through 2031, accounting for approximately 23% of the installed base. However, despite high-profile announcements from operators and vendors, the market is still expected to remain largely dominated by incumbent suppliers rather than new entrants initially expected.

These findings are from ABI Research’s Indoor, Outdoor, and IoT Network Infrastructure market data report, part of its 5G, 6G & Open RAN research service. The report provides detailed forecasts, market share analysis, and insights into key infrastructure investment trends.

Research Highlights:

- mMIMO market tracker across regions and by configurations.

- DAS revenue forecasts by region, technology, and verticals.

- Small cell market tracker for both indoor and outdoor infrastructure.

………………………………………………………………………………………………

Dell’Oro Group is slightly less pessimistic than ABI Research. In January, it forecast that global RAN revenues will grow at a 1% CAGR for the remainder of the 2020s, as ongoing 5G investments. Stefan Pongratz said at the time that downside risks still outweigh the upside potential though, the most notable of those being slowing data growth.

References:

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

RAN Silicon Rethink- Part II; vRAN and General-Purpose Compute

Will “AI at the Edge” transform telecom or be yet another telco monetization failure?

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Omdia: Huawei increases global RAN market share due to China hegemony

Dell’Oro Group: RAN Market Grows Outside of China in 2Q 2025

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

RAN Silicon Rethink- Part II; vRAN and General-Purpose Compute

Overview:

The global Radio Access Network (RAN) market has experienced a significant decline, dropping by nearly $10 billion in annual product revenue between 2022 and 2024, from roughly $45 billion to about $35 billion by the end of last year (source: Omdia).

- As the IEEE Techblog previously reported, Nokia is gradually moving away from its long-held reliance on custom RAN baseband (BBU) silicon from Marvell [1.] as it pivots to use Nvidia’s GPUs, as part of the latter’s $1B investment in Nokia in October 2025.

Note 1. Nokia uses Marvell RAN silicon in its 5G ReefShark portfolio. The companies collaborate to develop custom OCTEON SoC (System-on-a-Chip) and Infrastructure Processors, which are used to boost 5G AirScale base station performance.

- Samsung has long partnered with Marvell Technology on purpose-built 5G baseband silicon. However, rising development costs and a contracting market for proprietary RAN hardware are reshaping that strategy. The economic case for new, custom RAN chipsets is becoming weaker as operators accelerate network virtualization.

- In sharp contrast, Ericsson continues to defend its investment in proprietary silicon architectures while maintaining a flexible approach for operators that prefer virtualized or cloud RAN implementations running on standard central processing units (CPUs). At present, those solutions rely exclusively on Intel processors, though Ericsson notes its software is being engineered with portability in mind to support future hardware diversity.

Samsung’s Silicon Strategy:

Among RAN equipment vendors accessible to operators across North America and much of Europe, Samsung now stands as the principal alternative to the two Nordic RAN equipment suppliers, following the exclusion of Huawei and ZTE from many Western markets.

The South Korean conglomerate has become the global frontrunner in virtualized RAN (vRAN) deployments. Whereas custom silicon once dominated RAN infrastructure design, Samsung’s strategy has notably inverted that paradigm: vRAN is now its mainstream offering, and purpose-built hardware has moved to the periphery.

By the close of last year, Samsung reported supporting approximately 53,000 vRAN sites worldwide — a significant share of which lies within Verizon’s U.S. footprint. The company also disclosed major European developments, including Vodafone’s planned rollout across Germany and other markets, which will rely entirely on vRAN technology. For Samsung, discussions of bespoke, purpose-built 5G infrastructure have become increasingly rare.

According to Alok Shah, Vice President of Network Strategy at Samsung Networks, this transition reflects both the rising cost of developing custom silicon and the performance enhancements achieved by general-purpose CPU platforms.

“We’re still selling our purpose-built BBUs to a number of customers, but I do believe that it’s a matter of time,” Shah told Light Reading during MWC Barcelona, when asked if Samsung envisions an eventual phaseout of its proprietary baseband hardware portfolio.

Virtualized RAN Gains Momentum:

Transitioning to virtualized RAN (vRAN) allows network equipment vendors to capitalize on the scale economies of commercial data-center silicon. Samsung has established commercial vRAN contracts with Verizon and Vodafone, reflecting growing operator confidence in software-defined architectures.

“Virtual RAN performance has reached parity,” Shah said. “I know not all of our competitors feel that way, but that’s certainly how we feel. And the cost of building that modem is pretty high, even for a company like Samsung that’s really good at semiconductors,” he added.

Intel’s Granite Rapids Xeon platform exemplifies this shift to vRAN. The processor’s increased core density enables operators to cut hardware footprints; in many configurations, a single server can now support workloads that previously required two. Several network operators have confirmed this performance improvement during field evaluations.

Samsung and Ericsson continue to explore additional CPU suppliers. AMD’s latest multicore x86 processors offer up to 84 cores, compared with 72 in Intel’s Granite Rapids. However, offloading Forward Error Correction (FEC)—one of the most compute-intensive RAN processes—remains a challenge. Intel’s vRAN Boost feature integrates a dedicated hardware accelerator for FEC, while AMD currently lacks a direct equivalent.

Samsung has also evaluated Arm-based platforms, which increasingly support efficient software migration from x86. Nvidia’s Grace CPU, built on Arm architecture, has emerged as a potential candidate, especially when paired with its GPUs for selective Layer 1 acceleration.

Samsung’s roadmap aligns with a gradual and selective introduction of GPU acceleration. The company demonstrated GPU-based beamforming optimization during MWC, illustrating how AI can refine radio energy targeting. However, Samsung executives maintain that the latest Intel CPUs also provide sufficient capacity to host AI inference workloads directly. “Granite Rapids has plenty of capacity to support AI algorithms on-platform,” noted Shah.

While Nokia is building a GPU-compatible Layer 1 to accelerate computationally intensive baseband functions—including FEC—Samsung’s approach appears incrementally narrower, focusing on targeted AI for RAN optimization rather than complete GPU offload. GPUs may ultimately support AI at the Edge applications—so-called AI and RAN—where telecom operators leverage deployed GPUs for latency-sensitive inference services.

The degree to which such applications will reside within RAN sites remains uncertain. Some operators suggest that edge inference may instead remain within core network clusters that can meet latency requirements more efficiently.

Samsung’s architecture already supports GPU integration through commercial off-the-shelf (COTS) servers from manufacturers such as HPE, Dell, and Supermicro—aligning with broader cloud-native RAN trends. “It’s an off-the-shelf card that can be integrated directly into standard servers,” said Shah.

For now, Intel remains Samsung’s primary compute partner for commercial vRAN products. “We haven’t had an instance where customers are pushing for a second platform—it’s primarily a matter of commercial interest,” Shah added. The direction is clear: Samsung, like other leading vendors, is prioritizing scalable, general-purpose compute over bespoke 5G silicon as vRAN deployment accelerates.

……………………………………………………………………………………………………………………………………………………………………

References:

https://www.lightreading.com/5g/samsung-eyes-death-of-purpose-built-5g-but-has-no-ai-ran-fears

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Marvell shrinking share of the RAN custom silicon market & acquisition of XConn Technologies for AI data center connectivity

Intel FlexRAN™ gets boost from AT&T; faces competition from Marvel, Qualcomm, and EdgeQ for Open RAN silicon

Analysis: Nokia and Marvell partnership to develop 5G RAN silicon technology + other Nokia moves

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

A recently published report from Dell’Oro Group reveals that the Radio Access Network (RAN) market ended the year on a stable note, with stronger than typical 3Q to 4Q seasonality. Fourth-quarter results were consistent with the broader stabilization trend that shaped the RAN market throughout the year, resulting in stable revenue trends for the full year.

“Taking into consideration that the RAN market lost around a fifth of its value between 2022 and 2024, this improved stability in 2025 represents a welcome shift in market conditions,” said Stefan Pongratz, Vice President for RAN market research at the Dell’Oro Group. “Helping to explain the improved sentiment are the more favorable regional mix, easier comparisons, and the weaker USD. Even so, we have not made any material changes to the short-term outlook and still expect the market to be mostly flat in 2026,” continued Pongratz.

Additional highlights from the 4Q 2025 RAN report:

- Revenue rankings did not change in 2025. The top 5 RAN suppliers by worldwide revenue are Huawei, Ericsson, Nokia, ZTE, and Samsung.

- RAN vendor dynamics shifted in 2025—leading vendors strengthened their positions, while smaller suppliers adjusted their strategies. As a result, overall RAN market concentration increased during the year.

- Overall market concentration, as measured by the Herfindahl–Hirschman Index, reached a 10-year high in 2025.

- In 2025, Huawei and Nokia gained ground, Ericsson and Samsung were stable, and ZTE’s RAN revenue share fell.

- The fundamentals that shape the RAN market have not changed, and the long-term trajectory discussed in the most recent 5-year forecast still holds (1% CAGR, 2025-2030).

- The short-term outlook is mostly unchanged, with total RAN expected to remain stable in 2026.

RAN is not a growth market over time (0% CAGR 2020-2025 in nominal US $). However, it can go through periods of higher and lower capital intensity ratios as operators align investment needs with the availability of new spectrum/technologies and demand for capacity. The base case forecast is for stable RAN and capex trends, resulting in further improvements in capital intensity ratios before 6G investments commence towards the end of the forecast period. Worldwide RAN revenue is projected to grow at a 1% CAGR over the next five years, as rapidly declining LTE capex will offset continued 5G and initial 6G investments. RAN as a share of wireless capex is expected to average in the 20 to 25 percentage share range over the forecast period.

Dell’Oro Group’s RAN Quarterly Report offers a complete overview of the RAN industry, with tables covering manufacturers’ and market revenue for multiple RAN segments including 5G NR Sub-7 GHz, 5G NR mmWave, LTE, macro base stations and radios, small cells, Massive MIMO, Open RAN, and vRAN. The report also tracks the RAN market by region and includes a four-quarter outlook. To purchase this report, please contact us by email at [email protected].

…………………………………………………………………………………………………………………………………………………………………………………………..

Editors Opinion:

This author believes that the only RAN growth driver over the next 5 years will be investments in 5G SA core networks, which finally is starting to be deployed more than 5G NSA networks as we noted in today’s companion IEEE Techblog post. Omdia forecasts that 5G SA core network software spending will grow at an 8.8% CAGR between 2025 and 2030, making it a primary driver of investment. Continued 5G investments by global telcos are largely being offset by sharply declining 4G-LTE investments, leading to a “stable” rather than a growing RAN market.

Neither AI RAN, 5G Advanced, or Open RAN will be significant RAN market growth drivers:

- 5G Advanced (5G-A): 5G Advanced is widely considered a key part of the roadmap toward 6G. While some operators are focusing on it, its initial impact on overall global RAN revenue is expected to be more incremental rather than a massive boom in the next 2-3 years. If 5G-Advanced is seen by operators as “incremental” and 6G is legally/technically bound to a 2030/2031 ITU-R standards and 3GPP spec finalization, there is very little “must-have” radio hardware for a network operator to buy before 2030 at the earliest.

- AI-RAN: While AI-RAN is viewed as a key tool for improving efficiency and reducing energy costs (operational expenditure), its immediate impact on capital investment (Capex) in RAN equipment is likely to be slower. However, some, like Samsung, argue that AI-RAN is already driving optimizations in 2026. AI-RAN is primarily an OpEx play. Network operators are buying software and specialized silicon to lower their energy bills and automate frequency management. While this is critical for their survival, it doesn’t create a new “coverage wave” of RAN spending. It’s simply a “treading water” investment.

- Open RAN: has not led to increased RAN sales or multi-vendor equipment in the same RAN. Rather, it is a procurement shift, not a market expander.

There may be pockets of RAN growth in 5G-Advanced for specific performance needs, 5G private networks, and AI-enabled efficiency tools. However, we believe that the global RAN market will continue to stagnate till 6G network are deployed in early 2031.

Stefan had forecast that “cumulative 6G RAN investments over the 2029-2034 period are projected to account for 55 to 60% of the total RAN capex over that time period.” However, 6G capex does not translate into 6G RAN revenue until 6G is actually deployed!

Any earlier 6G deployment will be BEFORE the 5G RAN (IMT 2030 RIT/SRITs) and IMT 2030 Frequency arrangements standards are approved by ITU-R in late 2030 or early 2031 as IMT 2030 recommendations. Note that 3GPP Release 21 marks the official start of its normative 6G work. While the specific milestones for Release 21 are to be decided by June 2026, it is widely expected to produce the first formal 6G RAN technical specifications by late 2028 or early 2029 and submit them to ITU-R WP 5D via ATIS. Therefore, any 6G RAN equipment shipped before the 2030 ITU seal of approval would be based on pre-standardized or early 3GPP specifications that may require later alignment and hardware/software updates.

–>No rational wireless network operator wants to deploy thousands of “6G-ready” sites in 2029 only to find that the ITU-R IMT 2030 RIT/SRITs and/or Frequency Arrangements finalized in late 2030 require a hardware filter change or a different sub-carrier spacing to meet global interference requirements.

Hopefully, 3GPP will have finalized its 6G core network specs during the same time period so that 6G RANs will be complemented with 6G core networks- unlike the initial 5G RAN rollouts which had 4G evolved packet cores (5G NSA).

Potential Repeat Problem of No 6G Core Network Standard:

It’s highly likely that 3GPP will once again (like with 5G) not submit their 6G core network specs to ITU-T which is responsible for non-radio aspects of wireless networks. That means that 3GPP effectively operates as a silo for the 6G Core Network (refusing ITU-T oversight),so there will likely be no unified global regulatory mandate for the “6G system” as a whole—only for the “radio” (ITU-R IMT 2030 recommendations). This might allow operators to delay 6G SA Core deployments indefinitely, which in turn kills the business case for buying new 5G-Advanced or AI-RAN hardware.

Google Gemini: If the 6G Core Network isn’t standardized in a way that allows operators to actually monetize these new radio architectures, it doesn’t matter if the RAN is “Open,” “AI-enabled,” or “Advanced.” It’s still just a cost center on a stagnant balance sheet. If the “brain” (6G Core) doesn’t support the “limbs” (6G RAN), the market may not buy the limbs and 6G RAN sales will disappoint, just as 5G RAN sales did. Many carriers are still struggling to recoup the billions spent on 5G deployment so are seriously concerned about the 6G ROI.

| Feature | 5G Challenge | 6G Challenge |

|---|---|---|

| Spectrum | Mid-band & mmWave (24-52 GHz) | Sub-THz & THz (>100 GHz) |

| Connectivity | Massive IoT (1M devices/km²) | Internet of Senses (10M devices/km²) |

| Architecture | Cloud-native | AI-native & “Cell-free” MIMO |

| Primary Goal | Enhanced Mobile Broadband | Convergence of Physical & Digital worlds |

………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://www.linkedin.com/feed/update/urn:li:activity:7422420902362988544/

6G Capex Ramp to Start Around 2030, According to Dell’Oro Group

Dell’Oro: Mobile Core Networks +15% in 2025; Ookla: Global Reality Check on 5G SA and 5G Advanced in 2026

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Dell’Oro Group: RAN Market Grows Outside of China in 2Q 2025

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Omdia: Huawei increases global RAN market share due to China hegemony

Network equipment vendors increase R&D; shift focus as 0% RAN market growth forecast for next 5 years!

vRAN market disappoints – just like OpenRAN and mobile 5G

Analysis: Rakuten Mobile and Intel partnership to embed AI directly into vRAN

Today, Rakuten Mobile and Intel announced a partnership to embed Artificial Intelligence (AI) directly into the virtualized Radio Access Network (vRAN) stack. While vRAN currently represents a small percentage of the total RAN market (Dell’Oro Group recently forecasts vRAN to account for 5% to 10% of the total RAN market by 2026), this partnership could boost increase that percentage as it addresses key adoption hurdles—performance, power, and AI integration. Key areas of innovation include:

- Enhanced Wireless Spectral Efficiency: Optimizing spectrum utilization for superior network performance and capacity.

- Automated RAN Operations: Streamlining network management and reducing operational complexities through intelligent automation.

- Optimized Resource Allocation: Dynamically allocating network resources for maximum efficiency and subscriber experience.

- Increased Energy Efficiency: Significantly reducing power consumption in the RAN, contributing to sustainable network operations.

The partnership essentially aims to make vRAN superior in performance and TCO (Total Cost of Ownership) compared to traditional, proprietary, purpose built RAN hardware.

“We are incredibly excited to expand our collaboration with Intel to pioneer truly AI-native RAN architectures,” said Sharad Sriwastawa, co-CEO and CTO, Rakuten Mobile. “Together, we are validating transformative AI-driven innovations that will not only shape but define the future of mobile networks. This partnership showcases how intelligent RAN can be achieved through the seamless and efficient integration of AI workloads directly within existing vRAN software stacks, delivering unparalleled performance and efficiency.”

Rakuten Mobile and Intel are engaged in rigorous testing and validation of cutting-edge RAN AI use cases across Layer 1, Layer 2, and comprehensive RAN operation and network platform management. A core objective is the seamless integration of AI directly into the RAN stack, meticulously addressing integration challenges while upholding carrier-grade reliability and stringent latency requirements.

Utilizing Intel FlexRAN reference software, the Intel vRAN AI Development Kit, and a robust suite of AI tools and libraries, Rakuten Mobile is collaboratively training, optimizing, and deploying sophisticated AI models specifically tailored for demanding RAN workloads. This collaborative effort is designed to realize ultra-low, real-time AI latency on Intel Xeon 6 SoC, capitalizing on their built-in AI acceleration capabilities, including AVX512/VNNI and AMX.

“AI is transforming how networks are built and operated,” said Kevork Kechichian, Executive Vice President and General Manager of the Data Center Group, Intel Corporation. “Together with Rakuten, we are demonstrating how AI benefits can be achieved in vRAN. Intel Xeon processors power the majority of commercial vRAN deployments worldwide, and this transformation momentum continues to accelerate. Intel is providing AI-ready Xeon platforms that allow operators like Rakuten to design AI-ready infrastructure from the ground up, with built-in acceleration capabilities.”

Rakuten says they are “poised to unlock new levels of RAN performance, efficiency, and automation by embedding AI directly into the RAN software stack, this AI-native evolution represents the future of cloud-native, AI-powered RAN – inherently software-upgradable and built on open, general-purpose computing platforms. Additionally, the extended collaboration between Rakuten Mobile and Intel marks a significant step toward realizing the vision of autonomous, self-optimizing networks and powerfully reinforces both companies’ commitment to open, programmable, and intelligent RAN infrastructure worldwide.”

……………………………………………………………………………………………………………………………………………………………………..

- AI-Native Efficiency & Performance: The collaboration focuses on integrating AI to improve network performance and energy efficiency, which is a major pain point for operators. By embedding AI directly into the vRAN stack, they are enhancing wireless spectral efficiency, reducing power consumption, and automating RAN operations.

- Leveraging High-Performance Hardware: The initiative utilizes Intel® Xeon® 6 processors with built-in vRAN Boost. This eliminates the need for external, power-hungry accelerator cards, offering up to 2.4x more capacity and 70% better performance-per-watt.

- Validation of Large-Scale Commercial Viability: Rakuten Mobile operates the world’s first fully virtualized, cloud-native network. Its continued collaboration with Intel to make the vRAN AI-native provides a proven blueprint for other operators, reducing the perceived risk of adopting vRAN, particularly in brownfield (existing) networks.

- Acceleration of Open RAN Ecosystem: The collaboration supports the broader push towards Open RAN, which is expected to see a significant rise in market share, doubling between 2022 and 2026.

………………………………………………………………………………………………………………………………………………………………

- Market Share Shift: Omdia forecasts that vRAN’s share of the RAN baseband subsector will reach 20% by 2028. That’s a significant jump from its current low single-digit percentage.

- Explosive CAGR: The global vRAN market is projected to grow from approximately $16.6 billion in 2024 to nearly $80 billion by 2033, representing a 19.5% CAGR.

- Small Cell Dominance: By the end of 2026, it is estimated that 77% of all vRAN implementations will be on small cell architectures, a key area where Rakuten and Intel have demonstrated success.

References:

https://corp.mobile.rakuten.co.jp/english/news/press/2026/0210_01/

Virtual RAN gets a boost from Samsung demo using Intel’s Grand Rapids/Xeon Series 6 SoC

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

vRAN market disappoints – just like OpenRAN and mobile 5G

LightCounting: Open RAN/vRAN market is pausing and regrouping

Dell’Oro: Private 5G ecosystem is evolving; vRAN gaining momentum; skepticism increasing

https://www.mordorintelligence.com/industry-reports/virtualized-ran-vran-market

https://www.grandviewresearch.com/industry-analysis/virtualized-radio-access-network-market-report

Vodafone Spain (Zegona), MasOrange and Telefonica in possible RANco joint venture

In an interview with Expansion published on January 26, 2026, Zegona [1.] CEO Eamonn O’Hare revealed that Vodafone Spain, MasOrange and Telefonica have been holding talks on the possibility of joining their mobile networks together since late last year. “We are talking with Orange and Telefónica to create a RANco,” he said.

Note 1. Zegona owns 100% of Vodafone Spain.

However, Zegona was unable to give the potential joint venture its full attention due to demands of its ongoing fiber projects. Telefonica and Vodafone created their Fiberpass joint venture (JV) in 2025 and agreed to sell a 40% stake to AXA in November. Meanwhile, Vodafone and MasOrange brought in GIC as an investor in their PremiumFiber JV last summer.

Eamonn O’Hare, president and CEO of Zegona

“The whole team was so involved in the fibercos that we didn’t have the time or energy to thoroughly develop the project,” O’Hare told the Expansion. Instead, his staff focused on tying up the fiber optic projects and then took a break over the Christmas period, he explained. “And now we’re back with more energy.”

Why a JV rather than a merger of telcos: “Mergers and acquisitions are not a priority in Spain and the regulatory risk is very high,” he said. Zegona has a greater motivation to make the RANco a reality. “Today there are three companies…that manage three national mobile networks with exactly the same fixed costs, but Orange and Telefónica have twice as many customers as us,” O’Hare explained. “Therefore, our national mobile network is inefficient. Just as our fixed infrastructure was inefficient and unprofitable, [and] that’s why we powered the fibercos.”

“It would be easier to broker a deal with MasOrange to share the network in certain areas, so the synergies would be in urban areas. But we don’t have anything with Telefónica, so there it would all be synergies.” Telefonica already has a mobile network sharing deal in place with Vodafone in sparsely populated areas, and was rumoured to be in talks with the telco on a broader RANco arrangement this time last year.

As a result, a partnership with Telefonica would bring greater synergies as there are no existing arrangements in place in the mobile space, but any deal would be a more difficult deal to hammer out and it would be trickier to bring in an investor, O’Hare added. Zegona has three priorities in Spain: to align its valuation with those of its competitors; to boost its cash flow to €1 billion; and to develop a RANco. “As long as we are in the middle of that transformation, we have no interest in mergers and acquisitions,” he said. And in addition, “the regulatory obstacle is…too big.”

“Historically, these small businesses have grown and then tried to sell themselves to MásMóvil. But MásMóvil no longer buys. Neither do we or Telefónica,” O’Hare said. “No one is buying. So they… will just be devoured by us and by Digi, as in the Pac-Man game.”

Would Huawei network equipment be used in the proposed Spanish RanCo? Vodafone is the mobile operator with the largest network provided by Huawei. Orange is reducing its share, and Telefónica only uses Huawei in part of its core network in Spain and not at all in its radio network. If the Brussels Cybersecurity Act mandates the replacement of this Chinese equipment, what will Vodafone Spain (Zegona) do?

“If Europe is more aggressive on the Huawei issue , I suppose we should accelerate efforts to reduce the amount of Huawei equipment in the network… should we accelerate RANco for this reason? Officially, the answer is no.”

……………………………………………………………………………………………………………….

References:

https://www.expansion.com/empresas/tecnologia/2026/01/26/6973ab17468aebd1418b4590.html

SNS Telecom & IT: Private 5G Market Nears Mainstream With $5 Billion Surge

España hit with major telecom blackout after power outage April 28th

Orange Spain & Ericsson to build 5G Infrastructure for 3 High-Speed Rail Lines

Telefónica and Nokia partner to boost use of 5G SA network APIs

Telefónica launches 5G SA in >700 towns and cities in Spain

Telefónica – Nokia alliance for private mobile networks to accelerate digital transformation for enterprises in Latin America

Ericsson and O2 Telefónica demo Europe’s 1st Cloud RAN 5G mmWave FWA use case

Telecom and AI Status in the EU

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

The global RAN market has been declining for several years, putting pressure on network equipment vendors to cut costs and rethink their commitment to purpose built/custom RAN silicon products or ASICs. In 2022, the market for RAN equipment and software generated about $45 billion in revenues, according to research by Omdia, an Informa company. By 2024, annual revenue had tumbled to $35 billion – a 22.22% drop (and even worse in real dollars when you include inflation). As a result. it has become harder to justify the cost of expensive purpose-built silicon for the shriveling RAN market sector.

The Radio Access Network (RAN) is the segment of the mobile network interfacing the end-users and the mobile core network. In it’s IMT 2020 and IMT 2030 recommendations, ITU-R refers to the interface between a wireless endpoint and RAN equipment (base station or small cell) as the Radio Interface Technology or RIT). The core network specifications all come from 3GPP which has ETSI rubber stamp them.

……………………………………………………………………………………………………………………………………………………………………..

Ericsson and Samsung appear increasingly reliant on Intel for RAN silicon, while Nokia has been dependent on Marvell, but is planning to use NVIDIA GPUs in the near future (much more below). Let’s look at RAN silicon offerings from Intel, Marvell and NVIDIA:

-

Key RAN silicon offerings from Intel include:

- Intel Xeon with Intel vRAN Boost: The primary processors for network and edge applications include specific Intel Xeon 6 SoCs (System-on-Chips) that integrate Intel’s vRAN Boost accelerators directly on the die. This integration helps offload demanding Layer 1 (physical layer) processing, such as forward error correction, from the general-purpose CPU cores.

- Integrated Accelerators: These built-in accelerators are designed to improve performance-per-watt and increase capacity for RAN workloads. Intel’s approach is to provide high performance using common, off-the-shelf hardware with specialized acceleration, contrasting with other approaches that might rely entirely on general-purpose CPUs.

- FPGAs (Field Programmable Gate Arrays): Through its acquisition of Altera, Intel offers FPGAs which can also be used in some RAN applications, allowing for flexible, programmable hardware solutions.

- Intel has a significant market share in 5G base station silicon and its upcoming Granite Rapids processors (part of the Xeon 6 family) are being developed to maintain its strong position in this market, including for Massive MIMO applications. The company faces strong competition, but its next-generation processors aim to improve performance and efficiency for both core and edge computing in 5G networks. massive MIMO into future chips, such as the upcoming Granite Rapids generation.

- OCTEON Fusion Processors: These are baseband processors optimized for cost, power, and programmability, widely used in both traditional and Open RAN (O-RAN) architectures. The latest iteration, the OCTEON 10 Fusion processor, provides comprehensive in-line 5G Layer 1 acceleration, enabling RAN virtualization in cloud data centers.

- OCTEON Data Processing Units (DPUs): The OCTEON TX2 and OCTEON 10 families are multi-core ARM-based processors that handle 5G transport processing, security, and edge inferencing for the RAN Intelligent Controller (RIC). They incorporate hardware accelerators for AI/ML functions, enabling optimized edge processing.

- AtlasOne Chipset: This is a 50Gbps PAM4 DSP (Digital Signal Processor) and TIA (Transimpedance Amplifier) chipset solution for 5G fronthaul, optimized for high performance and power efficiency in integrated, O-RAN, and vRAN architectures.

- Ethernet Switches and PHYs: Marvell’s Prestera switches and Alaska Ethernet physical layer (PHY) devices are used in carrier infrastructure to provide the necessary networking connectivity for 5G base stations and data centers.

- Marvell also works with partners to integrate its technology into accelerator cards, such as the Dell Open RAN Accelerator Card powered by the OCTEON Fusion platform, to provide carrier-grade vRAN solutions. Furthermore, Marvell offers custom ASIC design services for hyper-scalers and telecom customers who need highly optimized, specific silicon solutions for their unique 5G and AI infrastructure requirements.

3. NVIDIA’s new silicon platform for AI Radio Access Networks (AI-RAN) is the NVIDIA Aerial RAN Computer, which is built on the next-generation Blackwell architecture. The primary system for AI-RAN deployment is the NVIDIA Aerial RAN Computer-1, which utilizes the NVIDIA GB200 NVL2 platform.

Key NVIDIA RAN components and features include:

- NVIDIA Blackwell GPU: The core graphics processor that features 208 billion transistors and provides significant performance improvements for AI and data processing workloads compared to previous generations.

- NVIDIA Grace CPU: The GB200 NVL2 platform combines two Blackwell GPUs with two NVIDIA Grace CPUs, connected by a high-speed NVLink-C2C (Chip-to-Chip) interconnect to form a powerful, unified superchip.

- NVIDIA Aerial Software: The hardware runs a full software stack that includes NVIDIA Aerial CUDA-Accelerated RAN libraries and NVIDIA AI Enterprise software for 5G and future 6G networks.

- Specialized Networking: The platform uses NVIDIA BlueField-3 Data Processing Units (DPUs) for real-time data transmission and precision timing, and NVIDIA Spectrum-X Ethernet for high-speed networking, which are critical for RAN performance.

- The goal of this platform is to enable wireless telcos to run both traditional RAN and AI workloads concurrently on a common, energy-efficient, software-defined infrastructure, thereby creating new revenue opportunities and preparing for 6G.

……………………………………………………………………………………………………………………………………………….

To many stakeholders, piggybacking on the general purpose processors used in PCs and data centers might be more sensible, but that would require Virtual RAN (vRAN), which replaces custom silicon with such general-purpose processors. However, it is a very small share of the RAN compute or baseband subsector. Omdia says it was just 10% in 2023, but the market research firm expects that share to more than double by 2028. It that forecast pans out, vRAN could conceivably replace some of the custom RAN silicon business with general purpose processors.

Lat year, Ericsson allocated approximately $5.7 billion of its R & D budget to design and development of ASICs for Layer 1 (PHY), the most demanding part of the baseband. It relies on Intel for other RAN silicon functionality. If virtual RAN claims a bigger share of a low- or no-growth market, Ericsson’s returns on the same level of investment in ASICs would decline because they wouldn’t be needed for vRAN. Also, Intel’s Granite Rapids could markedly narrow the performance and cost gap with purpose-built RAN chips.

“We are doing trials on many platforms,” said Per Narvinger, the head of Ericsson’s mobile networks business group, in reference to that taste testing of different chips. “But the more important thing is that we have actually created this disaggregation of and separation of hardware and software.”

The aim is to have a set of RAN software deployable on multiple hardware platforms. However, that is not achievable with ASICs, which create a tight union between hardware and software (they are inextricably tied together). The general-purpose options identified by Narvinger were AMD, Intel and Nvidia. Currently, Intel remains Ericsson’s sole silicon commercial vendor. Despite Ericsson’s professed enthusiasm for )single vendor) open RAN, its business today is nearly all about purpose-built 5G.

In sharp contrast, Samsung’s retreat from custom RAN silicon has appeared rapid. It is without doubt the biggest mainstream vendor of virtual RAN products, and there is barely interest in the purpose-built 5G technology it has developed with Marvell. The RAN that Samsung has built for Verizon in the US is entirely virtual. It is about to do the same in parts of Europe for Vodafone. Canada’s Telus purchases both virtual and purpose-built 5G products from Samsung. But Bernard Bureau, the operator’s vice president of wireless strategy, says the virtual now outperforms the traditional and is also significantly less expensive. The processors, as in the case of Ericsson, come exclusively from Intel.

- Ericsson’s primary concern likely centers on the hardware architecture utilized for Forward Error Correction (FEC), a resource-intensive Layer 1 function. While Intel’s Granite Rapids and preceding platforms integrate the FEC accelerator directly within the main processor, AMD provides this functionality via an external accelerator card. Ericsson has historically favored integrated solutions, citing the use of separate cards as an added expense.

- Samsung is evaluating virtualized RAN software that potentially obviates the need for a dedicated hardware accelerator when deployed on AMD’s high-core-count processors. Samsung is confident that the increased core density of AMD’s offerings can manage the computational load of a software-only FEC implementation, and a commercial offering may be imminent. Samsung’s transition to AMD processors from Intel would require minimal changes to existing software written for Intel’s x86 instruction set architecture.

Nokia’s situation is more complicated due to NVIDIA’s recent $1 billion investment in the company. An apparent condition is that Nokia will designing 5G and 6G network equipment that uses Nvidia’s GPUs. As we noted in yesterday’s IEEE Techblog post, many telcos regard those GPUs as an expensive and energy-hungry component, which makes using them a risky move by Nokia. Presumably, Nokia cannot use the money it has received from NVIDIA to develop 5G Advanced and 6G software specifically for Marvell’s special purpose RAN silicon. If Nokia develops RAN software that runs on NVIDIA GPUs it conceivably could be repurposed for another GPU platform rather than specialized RAN silicon or an ASIC. And the only viable GPU alternative to NVIDIA at this time (outside of China) is AMD.

References:

https://www.lightreading.com/5g/slow-death-of-custom-ran-silicon-opens-doors-for-amd

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

China gaining on U.S. in AI technology arms race- silicon, models and research

Intel FlexRAN™ gets boost from AT&T; faces competition from Marvel, Qualcomm, and EdgeQ for Open RAN silicon

Analysis: Nokia and Marvell partnership to develop 5G RAN silicon technology + other Nokia moves

Ericsson’s revenue drops, profits soar; deal with Vodafone and partnership with Export Development Canada look promising

Ericsson’s 3rd quarter 2025 results released today showed a 9% drop in revenues, to 56.2 billion Swedish kronor (US$5.9 billion), compared with the same period last year. Ericsson’s gross margin rose 2% to 47.6%. U.S. sales fell by as much as 17% year-over-year for the 3rd quarter, to about SEK22.5 billion ($2.4 billion), after an especially busy period in 2024. And the only region where Ericsson realized any growth was northeast Asia, and that was due to Japan’s new 5G rollout.

At Ericsson’s big mobile networks unit, sales fell 11% year-over-year, to SEK35.4 billion ($3.7 billion), while the decline on a constant-currency basis was just 4%. The division’s operating income also slid by 6%, to SEK7.1 billion ($740 million).

Sales were much better at the company’s cloud software and services group, responsible for the development of Ericsson’s core network software as well as its business and operational support systems. Reported sales rose 3%, to SEK15.3 billion ($1.6 billion), while Ericsson put the organic improvement at 9%. More importantly, it swung from an operating loss of SEK400 million ($42 million) a year earlier to a profit of SEK1.7 billion ($180 million).

Net income soared by an astonishing 191%, to SEK11.3 billion ($1.2 billion). That sharp increase in net income was due to Ericsson’s recent sale of iconectiv, a provider of number-portability and data-exchange services, to a private equity firm. The deal landed Ericsson a capital gain of SEK7.6 billion ($800 million) that flattered its profits at the operating income level. In Stockholm, Ericsson’s share price soared more than 14% in mid-morning trade, although it remained almost 2% below its level at the start of the year.

CEO Börje Ekholm said on today’s earnings call: “The margin expansion reflects actions we’ve taken over the last years to increase operational excellence and efficiency, including the work we’ve done on our cost base. Over the last year, we’ve reduced our headcount by some 6,000, leveraging new ways of working, and that of course includes AI.”

Since the end of 2022, the year Ericsson acquired VoIP software developer Vonage for $6.2 billion, headcount has fallen by more than 15,600, to just 89,898 at the end of June, the company revealed in its latest earnings report.

The Vonage business suffered a 17% drop in sales, to SEK3.2 billion ($330 million), and saw its loss widen by 50%, to SEK600 million ($63 million). It is where Ericsson believes it can monetize the network application programming interfaces (APIs) that will link software apps to networks and hopefully revitalize the 5G market. However, that’s not happening yet.

“The geopolitical situation has required us to shift resources a bit politically. As we went through that transition, we duplicated a large part of the R&D spend. We don’t need to have that anymore as we have relocated R&D,” said Ekholm. “We are not going to jeopardize technology leadership and if we feel there is any risk – and that is a risk I don’t see today – then we would of course need to reassess.”

After years of growth, R&D spending fell by 10% year-over-year for the first nine months of 2025, to SEK35.8 billion ($3.8 billion), prompting concern among analysts that Ericsson could lose competitiveness versus Chinese rivals.

AI is now being used to refine the algorithms that are fed into Ericsson’s software products, said Per Narvinger, the head of Ericsson’s mobile networks business group, on a call with Light Reading. No indication was given if that would reduce headcount any further.

Ericsson hopes the new 5G contract it announced with Vodafone earlier today will boost sales in Europe, where underinvestment in midband 5G coverage and the “standalone” variant of 5G have been constant bugbears for the company. After the rollout of “non-standalone” 5G, which maintains the 4G core, operators just continued to sell a “4G plus” service, Ekholm said.

“It was the established business model of most operators around the world, so it became very natural to take that step and then use 5G almost as a marketing icon on the phone, but, in reality, it didn’t give the extra capabilities,” he added. Standalone features such as low latency and network slicing will be critical in future apps, Ekholm correctly said, arguing that 6G will necessitate edge cloud and AI investments that have also not yet happened.

In summing up, Ericsson said “Increased uncertainty remains on the outlook, both in terms of potential for further tariff changes as well as in the broader macroeconomic environment.”

Looking ahead:

– Continue to invest in technology leadership to strengthen competitive position

– Future-proofed Open RAN-ready portfolio

– New use cases to monetize network investments taking shape

● AI applications becoming a key driver for network investments

● Structurally improving the business through rigorous cost management

……………………………………………………………………………………………………………………………………………………….

Separately,

Ericsson today announced the signing of a USD $3 billion partnership agreement with Export Development Canada (EDC) to expand investment in Canadian research and development, deepen domestic supply chains, and accelerate next-generation technologies including 5G, Cloud RAN, AI, and quantum innovation.

Börje Ekholm, President and CEO, Ericsson, says: “Canada is one of Ericsson’s most important hubs for global research and development, and this partnership with Export Development Canada will allow us to scale that leadership even further. By strengthening our collaboration with Canadian businesses, universities and government partners, we can accelerate breakthroughs in 5G, quantum, and Cloud RAN that will drive growth, create opportunities, and reinforce Canada’s position as a global leader in next generation networks.”

With more than 3,100 employees nationwide and R&D centres in Ottawa, Montreal, and Toronto, Ericsson Canada is at the heart of the company’s global innovation footprint. Canadian teams are driving advancements in 5G, 5G Advanced, and 6G, while also contributing to new research in quantum communications and AI-powered network management.

The three-year partnership will enable Ericsson to expand its Canadian-led innovation and global projects with the support of financial and insurance solutions from EDC. By reinforcing Ericsson’s Canadian supply chain and connecting the company with innovative domestic businesses, the agreement will also amplify Ericsson’s ability to bring Canadian technology to the world, strengthen competitiveness, and create new opportunities for Canadian companies within Ericsson’s global network of partners.

Across all wireless network equipment vendors, annual sales of RAN products fell from $45 billion in 2022 to $35 billion last year, according to Omdia, a Light Reading sister company. Market research firms Omdia and Dell’Oro have encouragingly guided for a more stable market this year.

Most wireless network providers have seen no incentive to spend more on 5G when their returns to date have been so disappointing. And there is skepticism about the business case for low latency services and network slicing. Telcos increasingly sell large bundles of gigabytes to their customers and have struggled to monetize other features.

References:

https://www.lightreading.com/5g/ericsson-says-world-is-flat-amid-us-gloom-and-keeps-cutting

https://www.ericsson.com/en/press-releases/6/2025/ericsson-edc-advance-canadas-technology-leadership

Ericsson integrates agentic AI into its NetCloud platform for self healing and autonomous 5G private networks

Ericsson CEO’s strong statements on 5G SA, WRC 27, and AI in networks

Ericsson completes Aduna joint venture with 12 telcos to drive network API adoption

Ericsson reports ~flat 2Q-2025 results; sees potential for 5G SA and AI to drive growth

Ericsson revamps its OSS/BSS with AI using Amazon Bedrock as a foundation

Ericsson’s sales rose for the first time in 8 quarters; mobile networks need an AI boost

Beyon partners with Ericsson to build energy-efficient wireless networks in Bahrain

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

Ericsson and e& (UAE) sign MoU for 6G collaboration vs ITU-R IMT-2030 framework

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Market research firm Omdia (owned by Informa) says Huawei remains the number one RAN vendor in three out of five large geographical regions. Far from being fatally weakened by U.S. government sanctions, Huawei today looks as big and strong as ever. Its sales last year were the second highest in its history and only 4% less than it made in 2020, before those sanctions took effect. In three out of the five global regions studied by Omdia – Asia and Oceania, the Middle East and Africa, and Latin America and the Caribbean – Huawei was the leading RAN vendor. While third in Europe, it was absent from the top three only in North America where it is banned.

Spain’s Telefónica remains a big Huawei customer in Brazil and Germany, despite telling Krach in 2020 that it would soon have “clean networks” in those markets. Deutsche Telekom and Vodafone, two other European telco giants, are also still heavy users of Huawei. Ericsson and Nokia have noted Europe’s inability to kick out Huawei while alerting investors to “aggressive” competition from Chinese vendors in some regions.

“A few years ago, we were all talking about high-risk vendors in Europe and I think, as it looks right now, that is not an opportunity,” said Börje Ekholm, Ericsson’s CEO, on a call with analysts last month. The substitution of the Nordic vendors for Huawei has not gone as far as they would have hoped. Ekholm warned analysts one year ago about “sharply increased competition from Chinese vendors in Europe and Latin America” and said there was a risk of losing contracts. “I am sure we’ll lose some, but we do it because it is right for the overall gross margin in the company. Don’t expect us to be the most aggressive in the market.”

There are few signs of European telcos replacing one of the Nordic vendors with Huawei, or of big market share losses by Ericsson and Nokia to Chinese rivals. Nokia’s RAN market share outside China did not materially change between the first and second quarters, says Remy Pascal, a principal analyst with Omdia (quarterly figures are not disclosed but Nokia held 17.6% of the RAN market including China last year). Huawei appears to have overtaken it because of gains at the expense of other vendors and a larger revenue contribution from Huawei-friendly emerging markets in the second quarter. Seasonality and the timing of revenue recognition were also factors, says Pascal.

Huawei is still highly regarded by chief technology officers for the quality of its products. It was a pioneer in the development of 5G equipment for time division duplex (TDD) technology, where uplink and downlink communications occupy the same frequency channel, and in massive MIMO, an antenna-rich system for boosting signal strength. It beat Ericsson and Nokia to the commercialization of power amplifiers based on gallium nitride, an efficient alternative to silicon, according to Earl Lum, the founder of EJL Wireless Research.

Sanctions have not held back Huawei’s technology as much as analysts had expected. While the company was cut off from the foundries capable of manufacturing the most advanced silicon, it managed to obtain good-enough 7-nanometer chips in China for its latest smartphones, spurring its resurgence in that market. Network products remain less dependent on access to cutting-edge chips, and sales in that sector do not appear to have suffered outside markets that have imposed restrictions.

Alternatives to Huawei’s dominance have not materialized in a RAN sector that was already short of options. Besides evicting Huawei from telco networks, U.S. authorities hoped “Open RAN” would give rise to American developers of RAN products. That has failed badly.

- Mavenir, arguably the best Open RAN hope the U.S. had, became emblematic of the Open RAN market gloom after it recently withdrew from the market for radio units as part of a debt restructuring. The company has sold its Open RAN software to DISH Network and Vodafone, it has not achieved the market penetration it initially targeted. Mavenir has faced significant financial challenges that led to a restructuring in 2025, significant layoffs and a major shift in strategy away from developing its own hardware.

- Parallel Wireless makes Open RAN software and also provides Open RAN software-defined radios (SDRs) as part of its hardware ecosystem, focusing on disaggregating the radio access network stack to allow operators flexibility and reduced total cost of ownership. Their offerings include a hardware-agnostic 5G Standalone (SA) software stack and the Open RAN Aggregator software, which manages and converges multi-vendor RAN interfaces toward the core network.

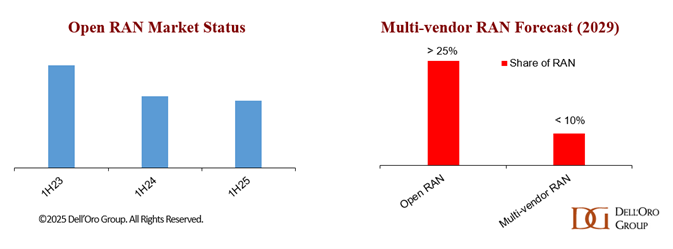

Stefan Pongratz of Dell’Oro Group forecasts annual revenues from multi-vendor RAN deployments – where telcos combine vendors instead of buying from a single big supplier – will have reached an upper limit of $3 billion by 2029, giving multi-vendor RAN less than 10% of the total RAN market by that date. He says five of six tracked regions are now classed as “highly concentrated,” with an Herfindahl-Hirschman Index (HHI) score of more than 2,500. “This suggests that the supplier diversity element of the open RAN vision is fading,” Stefan added.

Preliminary data from Dell’Oro indicate that Open RAN revenues grew year-over-year (Y/Y) in 2Q25 and were nearly flat Y/Y in the first half, supported by easier comparisons, stronger capex tied to existing Open RAN deployments, and increased activity among early majority adopters.

Open RAN used to mean alternatives to Ericsson and Nokia. Today, it looks synonymous with the top 5 RAN vendors (Huawei, Ericsson, Nokia, ZTE, and Samsung). In such an environment of extreme market concentration and failed U.S. sanctions, the appeal of Huawei’s RAN technology is still very much intact.

……………………………………………………………………………………………………………………………………………………………………….

Omdia’s historical data shows that RAN sales fell by $5 billion, to $40 billion, in 2023, and by the same amount again last year. In 2025, it is guiding for low single-digit percentage growth outside China, implying the RAN market has bottomed out. This stabilization suggests the market may be transitioning into a phase of flat-to-modest growth, though risks such as operator capex constraints and uneven regional demand remain. However, concentration of RAN vendors

…………………………………………………………………………………………………………………………………………………………………………

References:

https://www.lightreading.com/5g/huawei-overtakes-nokia-outside-china-as-open-ran-stabilizes-

Omdia: Huawei increases global RAN market share due to China hegemony

Malaysia’s U Mobile signs MoU’s with Huawei and ZTE for 5G network rollout

Dell’Oro Group: RAN Market Grows Outside of China in 2Q 2025

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Network equipment vendors increase R&D; shift focus as 0% RAN market growth forecast for next 5 years!

vRAN market disappoints – just like OpenRAN and mobile 5G

Mobile Experts: Open RAN market drops 83% in 2024 as legacy carriers prefer single vendor solutions

Huawei launches CloudMatrix 384 AI System to rival Nvidia’s most advanced AI system

U.S. export controls on Nvidia H20 AI chips enables Huawei’s 910C GPU to be favored by AI tech giants in China