Month: April 2022

Gartner: Public Cloud End-User Spending to approach $500B in 2022; $600B in 2023

Gartner forecasts that public cloud end user spending will reach nearly $600 billion by the end of 2023. The market research firm says public cloud services will continue in 2022, and nearly capture $494.7 billion in global spending this year – up from $410.9 billion in 2021. That represents a 20.4% increase in spending from 2021.

“Cloud is the powerhouse that drives today’s digital organizations,” said Sid Nag, research vice president at Gartner. “CIOs are beyond the era of irrational exuberance of procuring cloud services and are being thoughtful in their choice of public cloud providers to drive specific, desired business and technology outcomes in their digital transformation journey.”

Infrastructure-as-a-service (IaaS) is forecast to experience the highest end-user spending growth in 2022 at 30.6%, followed by desktop-as-a-service (DaaS) at 26.6% and platform-as-a-service (PaaS) at 26.1% (see Table 1). The new reality of hybrid work is prompting organizations to move away from powering their workforce with traditional client computing solutions, such as desktops and other physical in-office tools, and toward DaaS, which is driving spending to reach $2.6 billion in 2022. Demand for cloud-native capabilities by end-users accounts for PaaS growing to $109.6 billion in spending.

Table 1. Worldwide Public Cloud Services End-User Spending Forecast (Millions of U.S. Dollars)

| 2021 | 2022 | 2023 | |

| Cloud Business Process Services (BPaaS) | 51,410 | 55,598 | 60,619 |

| Cloud Application Infrastructure Services (PaaS) | 86,943 | 109,623 | 136,404 |

| Cloud Application Services (SaaS) | 152,184 | 176,622 | 208,080 |

| Cloud Management and Security Services | 26,665 | 30,471 | 35,218 |

| Cloud System Infrastructure Services (IaaS) | 91,642 | 119,717 | 156,276 |

| Desktop as a Service (DaaS) | 2,072 | 2,623 | 3,244 |

| Total Market | 410,915 | 494,654 | 599,840 |

BPaaS = business process as a service; IaaS = infrastructure as a service; PaaS = platform as a service; SaaS = software as a service. Note: Totals may not add up due to rounding. Source: Gartner (April 2022)

“Cloud native capabilities such as containerization, database platform-as-a-service (dbPaaS) and artificial intelligence/machine learning contain richer features than commoditized compute such as IaaS or network-as-a-service,” said Nag. “As a result, they are generally more expensive which is fueling spending growth.”

SaaS remains the largest public cloud services market segment, forecasted to reach $176.6 billion in end-user spending in 2022. Gartner expects steady growth within this segment as enterprises take multiple routes to market with SaaS, for example via cloud marketplaces, and continue to break up larger, monolithic applications into composable parts for more efficient DevOps processes.

Emerging technologies in cloud computing such as hyperscale edge computing and secure access service edge (SASE) are disrupting adjacent markets and forming new product categories, creating additional revenue streams for public cloud providers.

“Driven by maturation of core cloud services, the focus of differentiation is gradually shifting to capabilities that can disrupt digital businesses and operations in enterprises directly,” said Nag. “Public cloud services have become so integral that providers are now forced to address social and political challenges, such as sustainability and data sovereignty.

“IT leaders who view the cloud as an enabler rather than an end state will be most successful in their digital transformational journeys,” said Nag. “The organizations combining cloud with other adjacent, emerging technologies will fare even better.”

Gartner clients can read more in Forecast: Public Cloud Services, Worldwide, 2020-2026, 1Q22 Update. Lean more in the complimentary Gartner webinar Cloud Computing Scenario: The Future of Cloud.

References:

Gartner: Accelerated Move to Public Cloud to Overtake Traditional IT Spending in 2025

Strong growth for global cloud infrastructure spending by hyperscalers and enterprise customers

Gartner: Global public cloud spending to reach $332.3 billion in 2021; 23.1% YoY increase

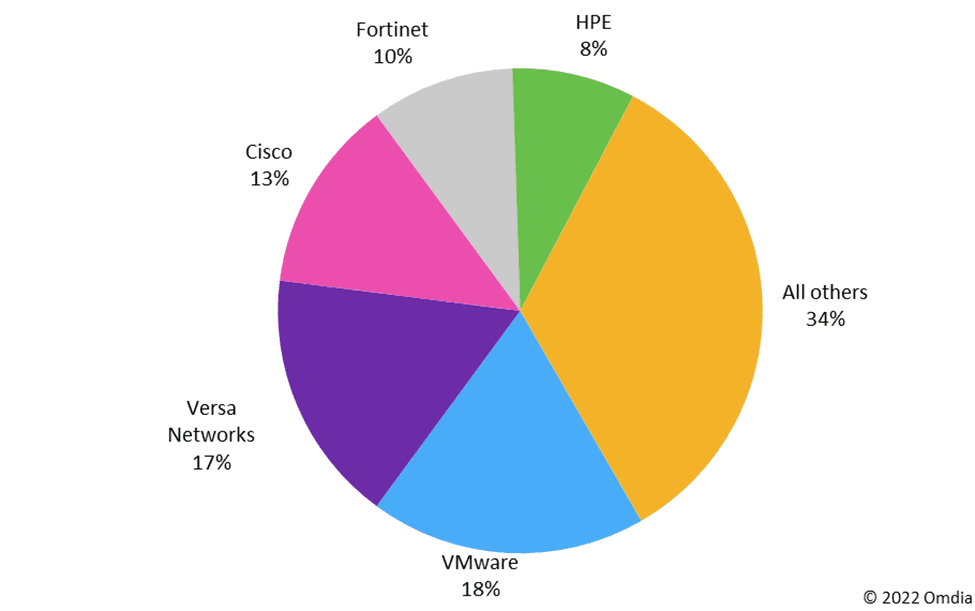

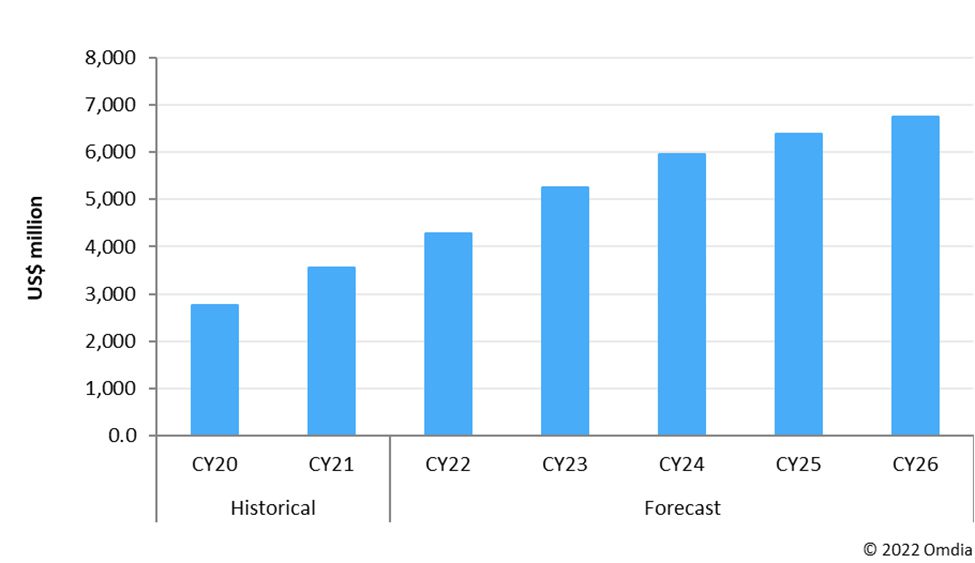

Omdia: VMware and Versa Networks are SD-WAN revenue leaders; SD-WAN market to hit $6.7B by 2026

According to a new report by market research firm Omdia (owned by Informa in the UK ), SD-WAN revenue remained on track with forecasts reaching $3.6 billion in 2021. Edge computing, an increased use of machine learning (ML) and artificial intelligence (AI), and growth in IoT are also increasing demand for SD-WAN services, Omdia said. The SD-WAN market exceeded $1 billion in total revenue for Q4 2021, up 24% year-over-year. Amongst SD-WAN vendors, VMware led in 2021 with 18% market share for Q4, followed closely by Versa Networks (17%) and Cisco (13%). Both VMware and Cisco got to the top through various SD-WAN acquisitions. More importantly, SD-WANs (with application aware routing and an overlay network) seem to have totally replaced classical SDN based WANs (with strict separation of Data and Control place, centralized Network layer routing, and NO overlay networks) as we don’t hear anything about that previously ultra-hyped “pie in the sky” technology.

Omidia says that vendors which managed their supply chain, shipping, logistics or relied heavily on uCPE hardware fared the best in 2021. Power management integrated circuits (PMIC) remain the biggest bottleneck for server vendors; interface integrated circuits (ICs), microcontrollers and networking application-specific ICs (ASICs) are among the components in short supply impacting SD-WAN vendors, said Omdia. There are also growing opportunities for vendors and service providers to work together on delivering SD-WAN as a managed service as customer demand trends away from DIY (do it yourself) SD-WAN.

“There is a new opportunity for vendors and CSPs as the market transitions from providing optimization of application packet streams on single links with WAN optimization appliances to agility and cost savings enabled by virtualizing the WAN across multiple link types with SD-WAN,” added Omdia.

The SD-WAN market has also benefitted from increased deployment of cloud and multi-cloud services as a result of enterprise efforts to support a more distributed workforce. Omdia cites adoption of 5G as another driver for SD-WAN demand to “help deploy and manage network capability, connectivity and security cost-effectively.”

“Service providers are beginning to look to SD-WAN to provide traffic steering over 5G LTE links for use cases such as the Industrial Internet of Things (IIoT),” said Omdia. Security is also front-of-mind to protect remote workers but is frequently viewed more as “an additional layer than a priority when selecting an SD-WAN provider,” Omdia added.

SD-WAN deployments in the healthcare industry have also experienced significant growth due to increased reliance on mobile health devices and telehealth services.

Over the next two years, Omdia predicts that SD-WAN vendors will further integrate services to provide vendor interoperability for enterprise customers, and that AI automation technology will be added to SD-WAN software for automated real-time analysis and network optimization for application traffic.

By 2026, the SD-WAN market will reach $6.7 billion in revenue, according to Omdia’s forecast. That’s up from $3.6 billion revenue in 2021 and results in a CAGR of almost 20%.

References:

https://www.lightreading.com/sd-wan/omdia-sd-wan-boosted-by-5g-edge-computing-growth/d/d-id/776851?

Dell’Oro: SD-WAN market grew 45% YoY; Frost & Sullivan: Fortinet wins SD-WAN leadership award

AT&T tops VSG’s U.S. Carrier Managed SD-WAN Leaderboard for 4th year

India’s Trai: Coexistence essential for efficient use of mmWave band spectrum

India’s telecom regulator (Trai) believes that its suggestion of coexistence between terrestrial network operators and satellite service providers in the millimeter wave (mmWave) band of 27.5- 28.5 GHz is essential for the “optimum use of airwaves.”

Trai has recommended the mmWave band – 24.25 GHz to 28.5 GHz – be put to auction. It has recommended a base price of Rs 7 crore a unit.

“Both International Mobile Telecommunications (IMT) and satellite bands can co-exist. That has to happen for the efficient use of spectrum,” said a senior Telecom regulator who did not want to be identified by name.

“The Satellite Earth Station Gateway (for satcom) should be permitted to be established in the frequency range 27.5-28.5 GHz at uninhabited or remote locations on a case-to-to-case basis, where there is less likelihood of 5G IMT services to come up,” the Trai official said.

Trai said that such a move would encourage buyers – both telcos and satcom players and eliminate the possibility of a major chunk of such airwaves to remain idle.

Editor’s Note:

As we’ve noted many times, the WRC 19 specified 5G mmWave frequency arrangements have yet to be standardized in the ITU-R M.1036 revision. Hence, it’s a 5G frequency free for all.

…………………………………………………………………………………………..

Why are telecom companies upset with TRAI despite its proposal to cut spectrum prices by 40%?

The Telecom Regulatory Authority of India (TRAI) this week released recommendations on auction of spectrum, including those likely to be used for offering 5G services. The telecom regulator has suggested cutting prices of airwaves across various bands by 35-40% from its earlier proposed base price. However, the Cellular Operators Association of India, whose members include the three private telcos, Bharti Airtel, Reliance Jio and Vodafone Idea, has expressed disappointment, given the industry’s demand for a 90% reduction in the prices.

The telecom regulator has recommended that all available spectrum in the existing bands — 700 MHz, 800 MHz, 900 MHz, 1800 MHz, 2100 MHz, 2300 MHz, 2500 MHz — should be put up for auction, along with airwaves in new bands such as 600 MHz, 3300-3670 MHz and 24.25-28.5 GHz. In all, more than 1,00,000 MHz of airwaves have been recommended to be put up for auction. The total spectrum on offer at reserve price is valued at about ₹5 lakh crore for 20 years.

For the 3300-3670 MHz band, which has emerged as the prime spectrum for 5G and is likely to be used for deploying 5G in India, the all-India reserve price has been lowered by about 35.5% to ₹317 crore/MHz, from ₹492 crore/MHz recommended earlier. Similarly, the reserve price for the premium 700 MHz band, which saw no takers in the previous auction, has been cut by 40% to ₹3,927 crore/MHz, from about ₹6,568 crore/MHz.

TRAI has determined the reserve price for spectrum bands based on a 20-year spectrum holding period. The reserve price for the increase in spectrum holding period to 30 years would be 1.5x the recommended reserve price for 20 years.

It has also recommended several options for the uptake of Captive Wireless Private Networks (CWPNs), including private networks through telcos, independent isolated network in an enterprise’s premises using telcos’ spectrum, allowing enterprise to take spectrum on lease from telcos or directly from Department of Telecom (DoT) to establish their own isolated captive private networks. TRAI also suggested that enterprises may obtain the spectrum directly from the government and establish their own isolated CWPN.

Given the financial stress in the sector, the government had in November, written to the regulator emphasising the need to strike a balance between generating revenue and the sustainability of the telecom sector in a way that telecom service providers are in good health with sufficient capacities to make regular and substantial capital expenditure for transitioning to 5G technology. It had also highlighted that spectrum lying idle was a waste for the economy.

Further, in the last spectrum auction, held in March 2021, only 37.1% of the spectrum put to auction was acquired by the telecom services providers, largely due to high prices.

“The inputs received by the Authority during the consultation process also point to the need for further rationalisation of the reserve price,” the regulator said in the recommendation running to more than 400 pages.

In its recommendations, the regulator has asserted that the “valuation exercise (and the setting of the reserve prices) is grounded in a techno-economic methodology that is time-tested. The valuation is intended to elicit spectrum prices that encourage buyers to procure radio frequencies in different bands, while at the same time ensuring that bidders are discouraged from collusive behaviour.”

The telecom services providers have via the industry body COAI expressed disappointment with TRAI’s recommendations for auction of 5G spectrum bands.

In a strongly worded reaction, COAI called the recommendation a “step backwards” than forward towards building a digitally connected India.

COAI maintained that the spectrum pricing recommended by TRAI was too high, and noted that throughout the consultation process, the industry had presented extensive arguments based on global research and benchmarks, for significant reduction in spectrum prices. “Industry recommended 90% lower price, and to see only about 35-40% reduction recommended in prices, therefore is deeply disappointing,” it said.

It added that charging a 1.5x price for spectrum for a 30-year period will nullify the relief provided by the Union Cabinet in 2021. The industry body pointed out that by introducing mandatory rollout obligations for 5G networks without factoring the huge cost of such a rollout, TRAI has “delinked itself from reality and is running counter to the Government’s efforts of enhancing ease of doing business”.

On allowing private captive networks for enterprises, COAI argued that TRAI was dramatically altering the industry dynamics and hurting the financial health of the industry rather than improving it. Private networks would be a disincentive for the telecom industry to invest in networks and continue paying high levies and taxes, it contended.

Reference:

Intel quietly acquires private 5G software provider Ananki

Intel has acquired private 5G network provider Ananki, several months after the startup spun out of the non-profit Open Networking Foundation (ONF) to commercialize open-source network technologies.

The acquisition was confirmed Monday on LinkedIn by Guru Parulkar, PhD, who was co-founder and CEO of Ananki and executive director of the Open Networking Foundation.

–>His ONF successor was not disclosed, despite my LI comment enquiring about it.

Intel declined to comment on the Ananki acquisition and instead only confirmed a development that Parulkar said was related: that the ONF’s development team has joined Intel’s Networking and Edge Group. Intel’s statement echoed a quote provided by top Intel networking executive and former Stanford Professor Nick McKeown, PhD in a press release published by the non-profit. McKeown was previously a part-time Intel Senior Fellow who joined the company after its 2019 acquisition of Barefoot Networks, which he co-founded.

“The addition of these developers will support [Intel’s Network and Edge Group’s] mission to drive the shift toward software-defined and fully programmable infrastructure – from the cloud, through the Internet and 5G networks, all the way out to the Intelligent Edge. Intel intends to continue to support and contribute to ONF’s open-source efforts,” an Intel spokesperson said. No financial terms were disclosed.

Ananki provides an open-source, software-defined service that aims to make private 5G networks “as easy to consume as Wi-Fi” for enterprises working on so-called Industry 4.0 projects. This involves connecting a variety of things, including cameras, sensors, robots, and autonomous vehicles, over high-speed networks in various settings, from factories to retail stores.

Ananki has a diverse range of products, including a SaaS-based 5G software stack, small cell radios, SIM cards, and a dashboard for monitoring and analyzing network activity. These are provided through a subscription-based service that charges organizations based on how much 5G coverage they need.

Source: Ananki

If Intel continues to offer Ananki’s products as a subscription service, it would fall in line with the semiconductor giant’s plan to buoy hardware sales with a significant increase in software revenue, as The Register has previously reported. Less than two weeks ago, The Register reported that Intel plans to offer the cloud optimization software of Granulate, another startup it plans to acquire, in Xeon CPU sales pitches.

The Ananki transaction is part of a broader effort by the Open Networking Foundation to support the increasing commercialization of its open-source, software-defined networking technologies, which it originally developed with the financial support of its more than 100 members. Those include Intel as well as several other prominent tech companies, such as AMD, AT&T, Broadcom, Cisco, Google, Microsoft, Nvidia, and T-Mobile.

The Open Networking Foundation said this new commercialization shift involves open-sourcing the entirety of its production-ready software, which includes private 5G, SD-RAN, SD-Fabric and SD-Core technologies that serve as the basis of Ananki’s products. The nonprofit has also made its software-defined broadband and P4 programmable network technologies available as open source.

“We have built platforms that naysayers said were doomed to fail, we’ve proven what’s possible, and today a number of our platforms have been deployed in production networks and others are now production ready and expected to be broadly adopted,” said Parulkar, who is now vice president of software within Intel’s Network and Edge Group.

The ONF seems to want to move development from internal open source teams to member organizations. As such, the nonprofit is transitioning a majority of its development team to Intel’s Network and Edge Group, which is also the new home of Ananki.

References:

https://www.theregister.com/2022/04/12/intel_ananki_5g/

https://www.intel.com/content/www/us/en/edge-computing/what-is-the-network-edge.html

https://networkbuilders.intel.com/events2022/big-5g-event

ONF Enters a New Era Focused on Growing Adoption and Community for its Leading Open Source Projects

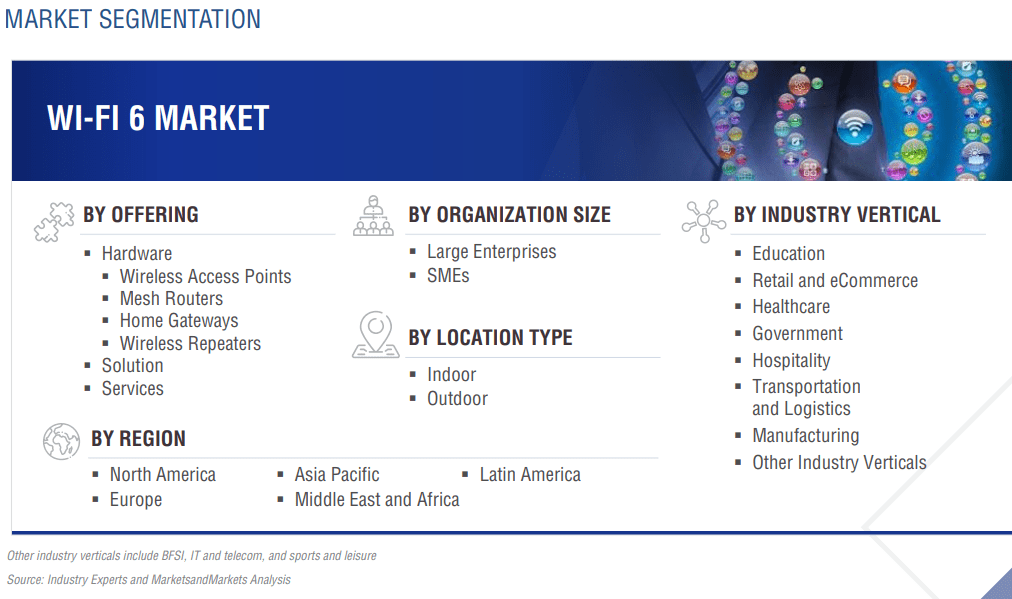

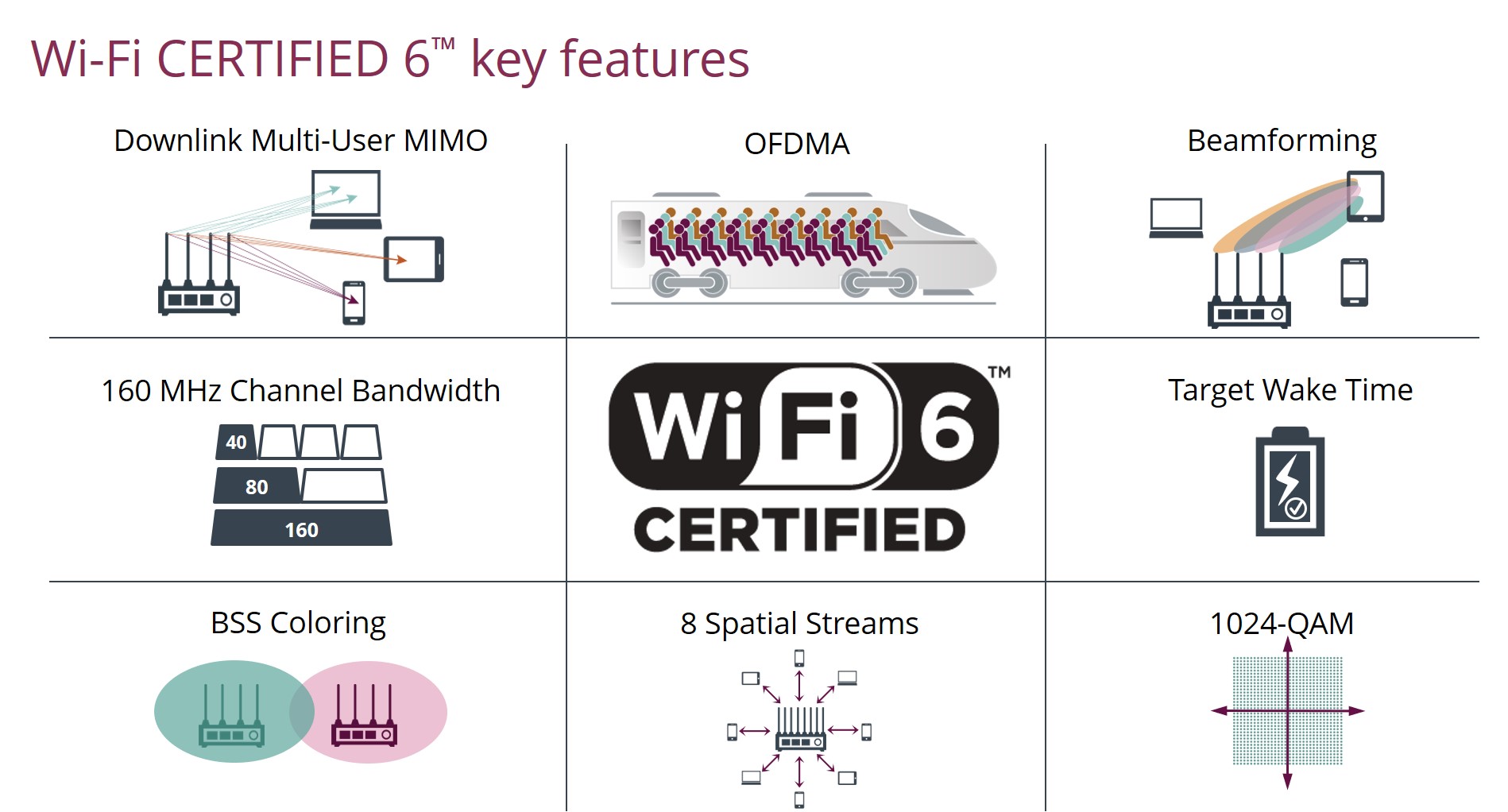

Global Wi-Fi 6 market forecast to grow from $11.5B in 2022 to $26.2B by 2027; CAGR=17.9%

According to a new research report “Wi-Fi 6 Market Global Forecast to 2027,” published by MarketsandMarkets™, the global Wi-Fi 6 market size is expected to grow from $11.5 billion in 2022 to $26.2 billion by 2027, at a Compound Annual Growth Rate (CAGR) of 17.9% during the forecast period.

……………………………………………………………………………………………………………………………………

Editor’s Note:

Wi-Fi 6 is an acronym for the IEEE 802.11ax standard. Prior to the release of Wi-Fi 6, Wi-Fi standards were identified by version numbers ranging from 802.11b to 802.11ac.

…………………………………………………………………………………………………………………….

The managed services Wi-Fi 6 market segment is expected to grow at a higher CAGR than enterprise or consumer Wi-Fi 6 during the forecast period. Managed Service Providers (MSPs) offer are third–party IT service providers that remotely manage the IT infrastructure and systems of clients for backup and recovery of business–critical data. These service providers carry out 24/7 remote monitoring of Wi–Fi 6 networks for their commercial clients. Enterprises opt for managed services to overcome the challenges of budget constraints and technical expertise as managed service providers have skilled human resources, infrastructure, and industry certifications. They offer services to monitor and manage hardware devices and manage the availability and the performance of networks. They also ensure smooth operations and security of networks. The growth of the Wi–Fi 6 market is being driven by the increasing reliance by businesses on the use of IT to improve business productivity, coupled with a continuing rise in demand for specialized MSPs and cloud–based managed Wi–Fi 6 services.

Asia Pacific (APAC) region to record the highest growing region in the Wi-Fi 6 Market. Important countries include Australia, Japan, Singapore, India, China, and New Zealand. The region is expected to witness the fast-paced adoption of Wi-Fi 6 software. The Asia Pacific region is estimated to be the fastest-growing Wi-Fi 6 Market owing to the rise in the adoption of new technologies, high investments for digital transformation, the rapid expansion of domestic enterprises, extensive development of infrastructures, and increasing GDP of various countries. Rapidly growing economies, such as China, Japan, Singapore, and India, are implementing Wi-Fi 6 solutions across multiple business processes to provide effective solutions.

Key and innovative vendors in the Wi-Fi 6 market are:

Cisco Systems (US), Intel Corporation (US), Huawei Technologies (China), NETGEAR (US), Juniper Networks (US), Broadcom (US), Qualcomm Inc. (US), Extreme Networks (US), Ubiquiti Networks (US), Fortinet Inc. (US), Aruba Networks (US), NXP Semiconductors (Netherlands), AT&T (US), Cambium Networks (US), D-Link Corporation (China), Alcatel-Lucent (US), TP-Link (China), MediaTek (China), Telstra (Australia), Murata (Japan), Sterlite Technologies Limited (India), Celeno (Israel), H3C (China), Senscomm Semiconductor (China), XUNISON (Ireland), Redway Networks (UK), VSORA (France), NEWRACOM (US), WILUS Group (South Korea), Federated Wireless (US).

References:

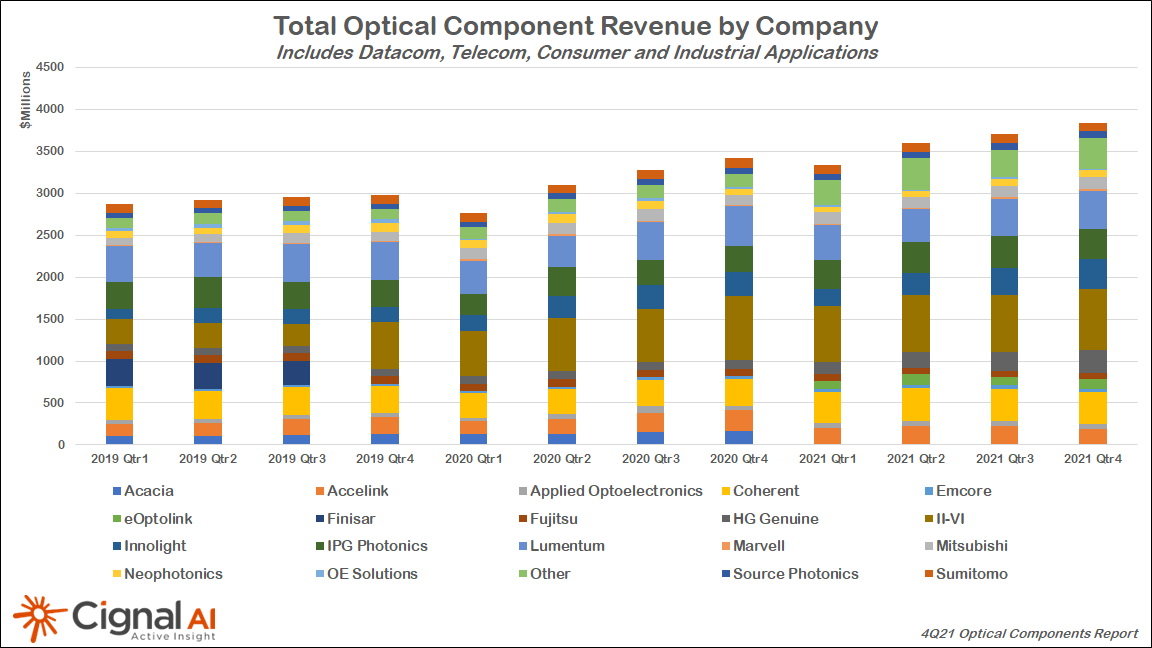

Cignal AI: Datacom optical component revenue +27% to reach $4.7B in 2021

Cignal AI reports that total revenue for optical components, a category that includes optical transceivers, grew 15% in 2021. Components for datacom optical network applications led the way, growing 27% to account for $4.7 billion of the total $14.5 billion component sales registered for the year within the datacom, telecom, industrial, and consumer markets, the market research firm states in its latest Optical Components Report.

A transition by large cloud service providers and some enterprise network operators toward 400-Gbps transmission helped spur this growth. For example, 1.8 million QSFP-DD and OSFP datacom modules shipped during 2021, most of which were DR4 format. Meanwhile, more than 60,000 400G pluggable coherent modules shipped at the same time, with QSFP-DD ZR devices accounting for the majority.

“The transition to 400GbE is well underway, and pluggable coherent 400Gbps technology is revolutionizing the design of the optical networks that connect datacenters,” said Scott Wilkinson, Lead Optical Component Analyst at Cignal AI. “400Gbps speeds will drive spending and bandwidth growth both inside and outside the datacenter in 2022,” Scott added.

More Key Findings from the 4Q21 Optical Components Report:

- Supply chain difficulties limited Telecom optical components market growth the most in 2021. However, the segment is forecast to grow more than 8% in 2022.

- Consumer component revenue for 3D sensing applications was flat YoY as lower-cost components offset higher unit shipments.

- Industrial optical components used for welding and medical applications grew 18% in 2021, following a weak 2020. Following the acquisition of Coherent, II-VI is poised to control over 50% of this market.

- 1.8M QSFP-DD Datacom modules shipped during 2021, most of which were DR4 format. The report also tracks SR4, FR4, and LR4 Datacom transceivers.

- Over 60k 400Gbps pluggable coherent modules shipped last year, the majority of which were QSFP-DD ZR. The report captures the shipment details of all the emerging derivatives of this format, including ZR, ZR+, 0dB ZR+, and CFP2 based ZR+.

- Shipments of 200Gbps coherent CFP2 modules grew 17% to just over 200k units during 2021 as Chinese OEMs ramp this speed (which is less dependent on western technology) for longer distance metro and long haul applications.

References:

U.S. cybersecurity firms seek tech standards to secure critical infrastructure

A group of cybersecurity companies that specialize in securing critical infrastructure said they’ve formed a lobbying group to push for technological standards among the private sector and government.

The Operational Technology Cybersecurity Coalition said it will directly work with government to share feedback on policy proposals and adopt uniform technological standards for securing places such as pipelines and industrial facilities. Founding members include Claroty Inc, Tenable Holdings Inc, Honeywell International Inc, Nozomi Networks Inc and Forescout Technologies Inc.

Editor’s Note: What is Cybersecurity?

Cybersecurity is a subset of information security which aims to defend an organization’s cloud, networks, computers, and data from unauthorized digital access, attack, or damage by implementing various defense processes, technologies, and practices. With the countless sophisticated threat actors targeting all types of organizations, it’s critical that your IT infrastructure is secured at all times to prevent a full-scale attack on your clouds, networks, or endpoints and risk exposing your company to fines, data losses, and damage to reputation.

………………………………………………………………………………………………………………

The new cybersecurity industry initiative comes as experts have placed increased scrutiny on what’s known as Operational Technology (OT), a broad array of computer systems that monitor and control industrial equipment.

In May, the cybersecurity firm Mandiant Inc warned that compromises against Internet-connected OT devices were on the rise.

“This work is essential to protect our country’s critical infrastructure,” said Jeff Zindel, vice president and general manager for cybersecurity at Honeywell.

Information Technology (IT) and Operational Technology (OT) are converging, bringing the promise of improved efficiency and new business models enabled by mass digital transformation and the Industrial Internet of Things (IIoT). However, along with the promise of greater connectivity comes greater risk.

As new technologies are introduced and integrated into legacy operations, OT and IT teams are being challenged from every direction. Security approaches that previously worked for one environment may not apply to the other.

That is why a coalition of industry leaders founded the Operational Technology Cyber Security Alliance (OTCSA) — to provide OT operators and suppliers with resources and guidance to mitigate their cyber risk in a fast-evolving world.

An ecosystem approach to safe and secure industrial operations:

The OTCSA is committed to enabling safe and secure operations for the entire OT spectrum. This includes securing the related interfaces to enable interconnectivity to IT while continuing to support and improve the daily life of citizens and workers in an evolving world.

The OTCSA provides OT operators and their vendor ecosystems with regular technical briefs and implementation guidelines to navigate necessary changes, upgrades and integrations. We will build and support an understanding of OT cyber security challenges and solutions from the board room to the factory floor.

The OTCSA adresses cyber security concerns across the entire range of industrial operations, including:

- Industrial control system equipment, software, and networks

- IT equipment and networks that are used in OT systems or provide functionality to OT systems

- Building management systems

- Facilities and control rooms access control systems

- CCTV systems

- Medical equipment

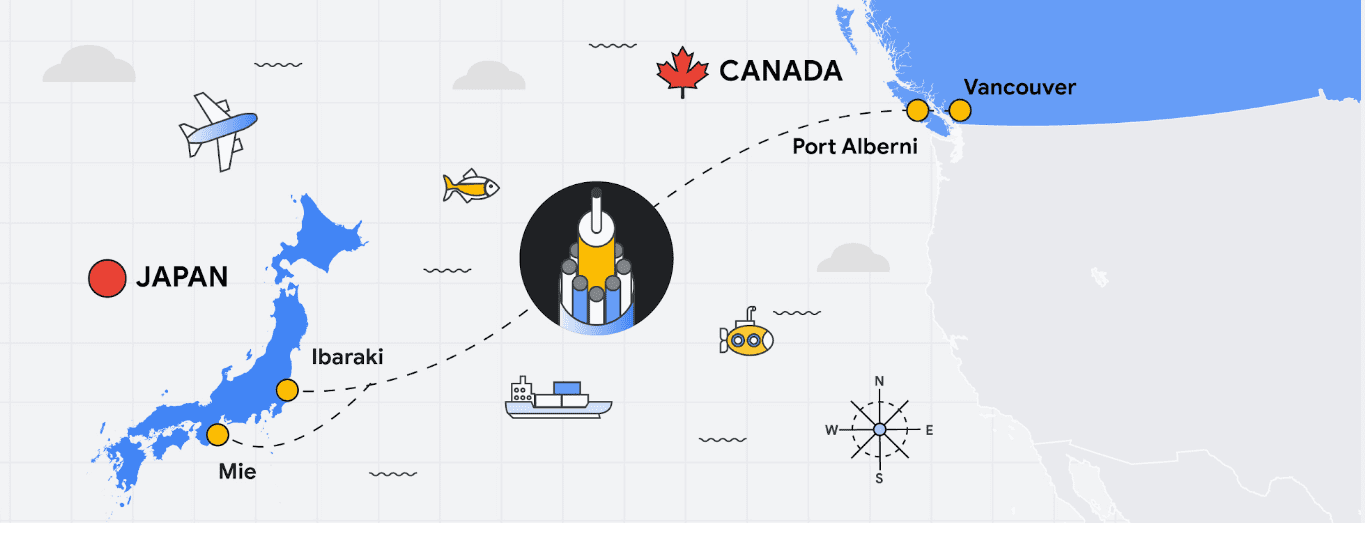

Google’s Topaz subsea cable to link Canada and Japan

The submarine cable system will be the first to link Canada directly to Asia, aiming to provide additional capacity for Google services and to a variety of network operators in Japan and Canada. The cable will be ready for service in 2023.

In August last year, reports were beginning to surface that Canada’s Shaw Communications was building a submarine cable landing station in Port Alberni, on the country’s West coast, despite no new cable systems being formally announced at the time.

It seems that Google was the chairman of this mysterious cable project, announcing the creation of the Topaz system, the first submarine cable set to link Canada directly to Asia. The Topaz cable will take a short hop from Vancouver, Canada, to Port Alberni on Vancouver Island, before travelling West across the Pacific to Japan, where it terminates at the cities of Shima and Takehagi.

In both Port Alberni and Takehagi, landing stations for the cable will need to be built from scratch. Vancouver, on the other hand, having housed the now defunct copper-based Commonwealth Pacific Cable System, built back in 1963, already has a historic landing station available for the project. This facility will be upgraded to meet the needs of the Topaz cable. The final stop, Shima, is already a major hub for submarine cable activity, with three local cable landing stations collectively connecting to around 17 subsea systems.

The Topaz system will comprise 16 fiber pairs with a total capacity of 240 Tbps. It will also make use of Wavelength Selective Switch technology, a software-defined solution that allows greater flexibility when routing traffic on individual fibre pairs.

Google says its intention with the system is not only to allow for low latency access to its own services, like Google Cloud and YouTube, but also to offer capacity for network operators in Canada and Japan.

The company also reportedly intends to swap fiber pair capacity with other submarine cable operators on similar routes, thereby increasing what the company calls “the intercontinental network lattice for network operators”.

Google’s interest and investment in submarine cable projects in recent years cannot be underestimated. The company has announced participation in 20 submarine cable projects, connecting 29 cloud regions, 88 zones, 146 network edge locations across more than 200 countries and territories.

Network infrastructure investments like Topaz bring significant economic activity to the regions where they land. For example, according to a recent Analysys Mason study, Google’s historical and future network infrastructure investments in Japan are forecasted to enable an additional $303 billion (USD) in GDP cumulatively between 2022 and 2026.

The width of a garden hose, the Topaz cable will house 16 fiber pairs, for a total capacity of 240 Terabits per second (not to be confused with TSPs). It includes support for Wavelength Selective Switch (WSS), an efficient and software-defined way to carve up the spectrum on an optical fiber pair for flexibility in routing and advanced resilience. We’re proud to bring WSS to Topaz and to see the technology is being implemented widely across the submarine cable industry.

While Topaz is the first trans-Pacific fiber cable to land on the West Coast of Canada, it’s not the first communication cable to connect to Vancouver Island. In the 1960s, the Commonwealth Pacific Cable System (COMPAC) was a copper undersea cable linking Vancouver with Honolulu (United States), Sydney (Australia), and Auckland (New Zealand), expanding high-quality international phone connectivity. Today, COMPAC is no longer in service but its legacy lives on. The original cable landing station in Vancouver — the facility where COMPAC made landfall on Canadian soil — has been upgraded to fit the needs of modern fiber optics and will house the eastern end of the Topaz cable.

Traditional and treaty rights, and local communities, are deeply important to our infrastructure projects. The Topaz cable is built alongside the traditional territories of the Hupacasath, Maa-nulth, and Tseshaht, and we have consulted with and partnered with these First Nations every step of the way.

“Tseshaht is very proud of this collaboration and our partnership with Google, who has been very respectful and thoughtful in its engagement with our Nation. That’s how we carry ourselves and that’s how we want business to carry themselves in our territory.“ — Tseshaht First Nation – Elected Chief Councillor-Ken Watts

“The five First Nations of the Maa-nulth Treaty Society are pleased that we have concluded an agreement with Google Canada and have consented to the installation of a new, high-speed fiber optic cable through our traditional territories. This agreement, in which both Google Canada and our Nations benefit, is based on respect for our constitutionally protected treaty and aboriginal rights and enhances the process of reconciliation. We would also like to acknowledge the sensitivity that Google Canada expressed during our talks in regard to the pain and trauma experienced by our people as a result of residential school experience. We look forward to a long and mutually beneficial relationship with Google Canada.” —Chief Charlie Cootes, President of the Maa-nulth Treaty Society

“Google’s respect towards our Nation is appreciated and has good energy behind it.” —Hupacasath First Nation – Elected Chief Councilor – Brandy Lauder

With the addition of Topaz, Google has announced investments in 20 subsea cable projects. This includes Curie, Dunant, Equiano, Firmina and Grace Hopper, and consortium cables like Blue, Echo, Havfrue and Raman — all connecting 29 cloud regions, 88 zones, 146 network edge locations across more than 200 countries and territories. Learn about Google Cloud’s network and infrastructure on our website and in the below video.

………………………………………………………………………………………………………

India Telcos say private networks will kill 5G business

India’s top tier wireless network operators have called on the Telecom Regulatory Authority of India (Trai) – India’s telecom sector regulator – to scrap the proposed move to administratively allocate 5G spectrum on demand for private enterprise networks through a publicized online portal-based process, warning that such a step could destroy the 5G business case in the country.

The businesses have mentioned that such a proposal, if accepted by the federal government, might probably rob telcos of their future 5G enterprise revenues – estimated at round 40% of the whole for 5G. Revenue loss to such an extent won’t justify needed capital expenditure in establishing 5G networks, they’ve argued.

In its newest suggestions on 5G spectrum pricing, the Trai has advised that non-public enterprises straight acquire 5G spectrum from the federal government and set up their very own captive wi-fi non-public community (CWPNs). It has additionally beneficial a “gentle contact’ on-line portal-based regime” for buying such permissions/licences for establishing CWPNs. Trai has additionally advised that non-public enterprises have the choice to lease spectrum from telcos to arrange their very own captive non-public 5G networks.

“By permitting non-public captive networks for enterprises, Trai is dramatically altering the trade dynamics and hurting the monetary well being of the telecom trade reasonably than bettering it,” the Mobile Operators Affiliation of India (COAI) said in an announcement Tuesday, April 12th.

The COAI represents Reliance Jio, Bharti Airtel and Vodafone Thought (Vi). It added that “enterprise companies represent 30-40% of the (telecom) trade’s total revenues…non-public networks as soon as once more dis-incentivises the telecom industry to spend money on networks and in addition proceed paying excessive levies and taxes.”

The COAI has urged Trai to revisit its newest suggestions and disallow non-public enterprise networks to make sure monetary viability and orderly progress of the telecom trade that, it mentioned, is greater than able to delivering these companies to companies.

India’s mobile carriers had earlier advised Trai that any proposal to put aside 5G spectrum for personal enterprise networks for captive use both at no cost or at an administrative worth would even be legally untenable.

Trai has beneficial that the spectrum for personal networks be assigned administratively on demand by way of a extensively publicized on-line portal-based course of in a good and clear method. However the regulator has left it to the telecom division to determine whether or not such administrative allocation can be legally tenable or not, based mostly on DoT’s spectrum allocation coverage.

In its 5G dialogue paper, Trai had mentioned the likes of Germany, Finland, UK, Brazil, Australia, Hong Kong and Japan had put aside spectrum within the mmWave band for personal captive 5G networks, whereas Slovenia, Sweden and Korea deliberate to put aside each mmWave and mid-band 5G spectrum for such captive networks.

Subsequently, Tata Communications (TCL), Larsen & Toubro (L&T) and cigarette maker ITC had strongly countered the telcos’ place, and known as on Trai to again earmarking devoted spectrum non-public captive networks and undertake international practices to create a personal 5G ecosystem for enterprises to drive the federal government’s Make in India imaginative and prescient.

However one other high telco government mentioned that if operators’ potential 5G income flows from the profitable enterprise enterprise vertical dry up, they might see little enterprise sense in bidding aggressively for 5G airwaves within the upcoming sale.

Bulk of the bidding urge for food for 5G airwaves, he mentioned, stems from the sturdy income potential of the B2B enterprise enterprise. But when that income stream disappears, telcos gained’t have a viable enterprise case to splurge huge cash on 5G spectrum, particularly as they’ve sufficient spectrum to proceed their current cellular broadband companies operations.”

Know-how corporations, although, have strongly backed Trai’s name to permit non-public enterprises to straight acquire 5G spectrum from the federal government by way of the executive route.

“By way of non-public networks, Trai’s suggestions handle the pursuits of TSPs (telecom service suppliers), enterprises and the general public as extra non-public networks would result in extra employment alternatives and enterprise, and translate into larger financial output and advantages,” mentioned the Broadband India Discussion board (BIF), which counts Cisco, Amazon, Google, Microsoft, Fb-owner Meta, Qualcomm and Intel amongst its key members.

Earmarking unique spectrum for personal 5G networks, it mentioned, would additionally present an “enchancement over common SLAs (service level agreements) of public networks, moreover guaranteeing full lack of interference between them”.

BIF added that Trai’s name for task of spectrum administratively for personal 5G networks “is most acceptable” because it has thought of that captive wi-fi non-public networks should not public networks and don’t have any market prospects, and are restricted to a selected location.”

Trai chairman PD Vaghela termed the 5G spectrum rates “reasonable”, saying they have been arrived at after considering various factors including quantum of spectrum offered, competition in the market and profitability.

……………………………………………………………………………………………………

April 18, 2022 Addendum:

Spectrum users have started squabbling over the telecom regulator’s recommendation to earmark certain bands for captive wireless private networks.

The cellular operators under the COAI have opposed regulator suggestions of allowing enterprises to build their own private 5G networks for captive purposes.

Technology players such as Facebook, Google, Indian Space Association (ISpA) want the 28.5GHz band spectrum to be reserved and allocated exclusively for satellite communications (satcom) services.

The COAI said “by allowing private captive networks for enterprises, telecom regulator Trai is dramatically altering the industry dynamics and hurting the financial health of the industry rather than improving it”.

“Telecom service providers have and going forward will invest lakhs of crore rupees in network rollouts. Enterprise services constitute 30-40 per cent of the industry’s overall revenues. Private networks once again disincentivises the telecom industry to invest in networks and continue paying high levies and taxes.”

The Broadband India Forum (BIF), the industry body of tech players such as Facebook and Google, welcomed the recommendations to allow private networks.

Telcos flay plan for private 5G networks

Spectrum users have started squabbling over the telecom regulator’s recommendation to earmark certain bands for captive wireless private networks.

The cellular operators under the COAI have opposed regulator suggestions of allowing enterprises to build their own private 5G networks for captive purposes.

The suggestion has been welcomed by the Broadband India Forum (BIF).

Technology players such as Facebook, Google, Indian Space Association (ISpA) want the 28.5GHz band spectrum to be reserved and allocated exclusively for satellite communications (satcom) services.

The COAI said “by allowing private captive networks for enterprises, telecom regulator Trai is dramatically altering the industry dynamics and hurting the financial health of the industry rather than improving it”.

“Telecom service providers have and going forward will invest lakhs of crore rupees in network rollouts. Enterprise services constitute 30-40 per cent of the industry’s overall revenues. Private networks once again disincentivises the telecom industry to invest in networks and continue paying high levies and taxes.”

The Broadband India Forum (BIF), the industry body of tech players such as Facebook and Google, welcomed the recommendations to allow private networks.

The Indian Space Association (IsPA) said “we welcome Trai’s recommendation that calls for coexistence of satellite communications and IMT in the 27.5-28.5GHz band. We also appreciate recommending an exclusion zone for satellite earth stations in the 27.5-28.5GHz band.”

IsPA opposed the inclusion of all spectrum in the 24.25-28.5GHz bands along with low and mid bands in the auction as it was a case of oversupply to the telecom operators at the cost of the satellite industry.

“The 24.25-27.5GHz bands along with 3.3-3.67GHz bands would be more than sufficient for 5G. Therefore, in line with the global best practices, the 28GHz band should be allocated exclusively for satellite communications,” it added.

In its recent recommendations, telecom regulator Trai said spectrum in three bands – 3700-3800MHz, 4800-4990MHz and 28.5-29.5GHz band – could be earmarked for captive wireless private networks which, it felt, could co-exist with non-IMT services.

In the 28.5-29.5 MHz band, Trai said: “A software based transparent system should be built to permit the establishment of private networks and satellite earth Stations based on the geo-coordinates of the proposed location on interference free co-existence basis.”

The regulator added: “DoT should develop a digital map with geographic coordinates of all the existing and future satellite earth stations as well as geographic coordinates of the premises of Private Network locations. Based on this database, permissions for establishment of new installations may be provided to the licensees.”

https://www.telegraphindia.com/business/telcos-flay-plan-for-private-5g-networks/cid/1861119

References:

https://economictimes.indiatimes.com/topic/telecom-regulatory-authority-of-india

Related: IEEE/SCU SoE Panel Session on Open RAN and 5G Private Networks:

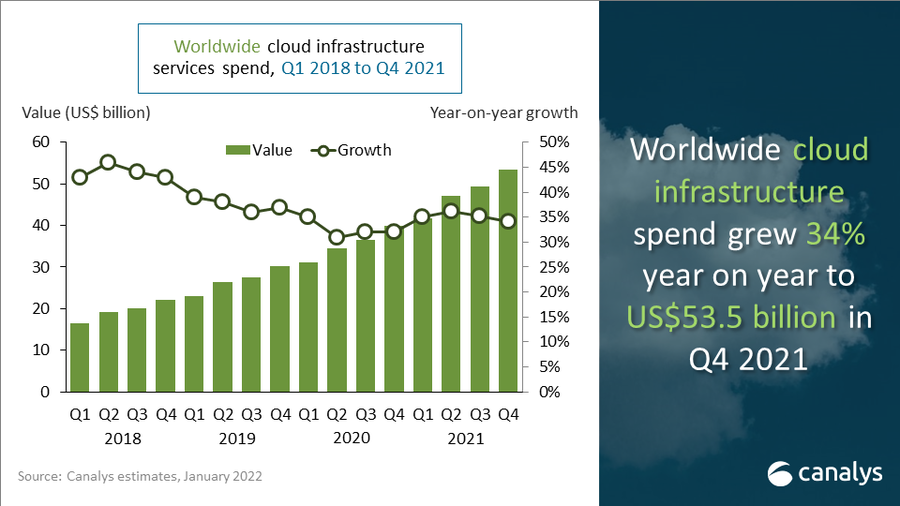

IDC: Cloud Infrastructure Spending +13.5% YoY in 4Q-2021 to $21.1 billion; Forecast CAGR of 12.6% from 2021-2026

According to the International Data Corporation (IDC) Worldwide Quarterly Enterprise Infrastructure Tracker: Buyer and Cloud Deployment, spending on compute and storage infrastructure products for cloud infrastructure, including dedicated and shared environments, increased 13.5% year over year (YoY) in the fourth quarter of 2021 (4Q-2021) to $21.1 billion. This marked the second consecutive quarter of year-over-year growth as supply chain constraints have depleted vendor inventories over the past several quarters. As backlogs continue to grow, pent-up demand bodes well for future growth as long as the economy stays healthy, and supply catches up to demand.

For the full year 2021, cloud infrastructure spending totaled $73.9 billion, up 8.8% over 2020. IDC predicts spending on cloud infrastructure services to increase 21.7% in 2022 to $90.0 billion.

The service provider category includes cloud service providers, digital service providers, communications service providers, and managed service providers. In 4Q21, service providers as a group spent $21.2 billion on compute and storage infrastructure, up 11.6% from 4Q20. This spending accounted for 55.4% of total compute and storage infrastructure spending. For 2021, spending by service providers reached $75.1 billion on 8.5% year over year growth, accounting for 56.2% of total compute and storage infrastructure spending. IDC expects compute and storage spending by service providers to reach $89.1 billion in 2022, growing at 18.7% year over year.

At the regional level, year-over-year spending on cloud infrastructure in 4Q21 increased in most regions.

- Asia/Pacific (excluding Japan and China) (APeJC) grew the most at 59.5% year over year.

- Canada, Central and Eastern Europe, Japan, Middle East and Africa, and China (PRC) all saw double-digit growth in spending.

- The United States grew 5.6%.

- Western Europe and Latin America declined for the quarter.

For 2021, APeJC grew the most at 43.7% year over year. Canada, Central and Eastern Europe, Middle East and Africa, and China all saw double-digit growth in spending. Japan grew in the high single digits, while Western Europe grew in the low single digits. The United States grew 1.5%. Latin America declined for the year. For 2022, cloud infrastructure spending for most regions is expected to grow with the highest growth expected in the United States at 27.8%. Central and Eastern Europe is the only region expected to decline in 2022 with spending forecast to be down 21.7% year over year.

Longer term, IDC expects spending on compute and storage cloud infrastructure to have a compound annual growth rate (CAGR) of 12.6% over the 2021-2026 forecast period, reaching $133.7 billion in 2026 and accounting for 68.6% of total compute and storage infrastructure spend. Shared cloud infrastructure will account for 72.0% of the total cloud amount, growing at a 13.4% CAGR. Spending on dedicated cloud infrastructure will grow at a CAGR of 10.7%. Spending on non-cloud infrastructure will flatten out at a CAGR of 0.5%, reaching $61.2 billion in 2026. Spending by service providers on compute and storage infrastructure is expected to grow at a 11.7% CAGR, reaching $130.6 billion in 2026.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

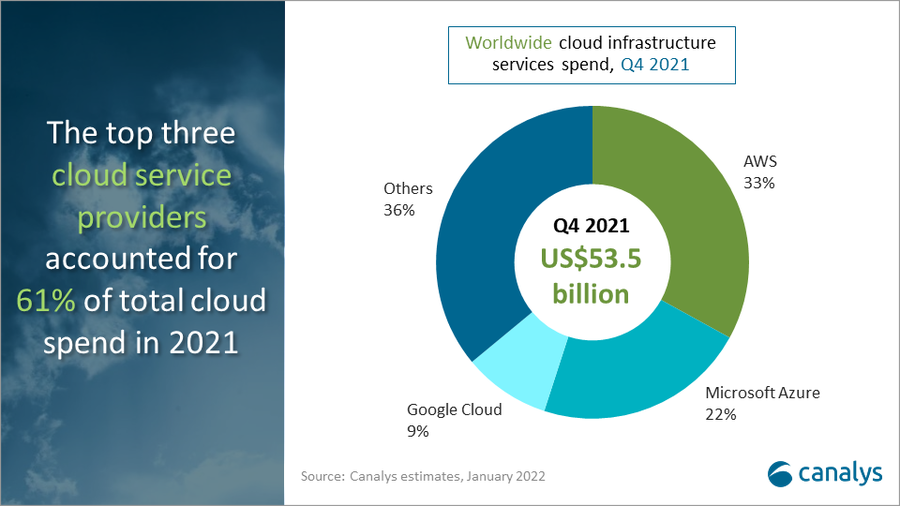

Separately, Amazon Web Services (AWS) led with 33% of spending on cloud infrastructure services in Q4 2021, according to a Feb 3, 2022 blog post from research group Canalys. Meta, previously known as Facebook, recently chose AWS as a long-term strategic cloud service provider and continues to deepen the relationship as Meta begins to move away from social media to become a broader metaverse company over the next five years. AWS also announced key customer wins across retail, healthcare and financial services and emphasized a key agreement with Nasdaq to migrate markets to AWS to become a cloud-based exchange.

Microsoft Azure was second with 22% of spending, followed by Google Cloud with 9%. The three companies accounted for 64% of total cloud investment for 2021.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

IDC’s Worldwide Quarterly Enterprise Infrastructure Tracker: Buyer and Cloud Deployment is designed to provide clients with a better understanding of what portion of the compute and storage hardware markets are being deployed in cloud environments. The Tracker breaks out each vendors’ revenue into shared and dedicated cloud environments for historical data and provides a five-year forecast. This Tracker is part of the Worldwide Quarterly Enterprise Infrastructure Tracker, which provides a holistic total addressable market view of the four key enabling infrastructure technologies for the datacenter (servers, external enterprise storage systems, and purpose-built appliances: HCI and PBBA).

Taxonomy Notes:

IDC defines cloud services more formally through a checklist of key attributes that an offering must manifest to end users of the service.

Shared cloud services are shared among unrelated enterprises and consumers; open to a largely unrestricted universe of potential users; and designed for a market, not a single enterprise. The shared cloud market includes a variety of services designed to extend or, in some cases, replace IT infrastructure deployed in corporate datacenters; these services in total are called public cloud services. The shared cloud market also includes digital services such as media/content distribution, sharing and search, social media, and e-commerce.

Dedicated cloud services are shared within a single enterprise or an extended enterprise with restrictions on access and level of resource dedication and defined/controlled by the enterprise (and beyond the control available in public cloud offerings); can be onsite or offsite; and can be managed by a third-party or in-house staff. In dedicated cloud that is managed by in-house staff, “vendors (cloud service providers)” are equivalent to the IT departments/shared service departments within enterprises/groups. In this utilization model, where standardized services are jointly used within the enterprise/group, business departments, offices, and employees are the “service users.”

For more information about IDC’s Enterprise Infrastructure Tracker, please contact Lidice Fernandez at [email protected].

References:

https://www.idc.com/getdoc.jsp?containerId=prUS48998722

Gartner: Accelerated Move to Public Cloud to Overtake Traditional IT Spending in 2025

Strong growth for global cloud infrastructure spending by hyperscalers and enterprise customers

Gartner: Global public cloud spending to reach $332.3 billion in 2021; 23.1% YoY increase