AI Partnerships

Analysis: Rakuten Mobile and Intel partnership to embed AI directly into vRAN

Today, Rakuten Mobile and Intel announced a partnership to embed Artificial Intelligence (AI) directly into the virtualized Radio Access Network (vRAN) stack. While vRAN currently represents a small percentage of the total RAN market (Dell’Oro Group recently forecasts vRAN to account for 5% to 10% of the total RAN market by 2026), this partnership could boost increase that percentage as it addresses key adoption hurdles—performance, power, and AI integration. Key areas of innovation include:

- Enhanced Wireless Spectral Efficiency: Optimizing spectrum utilization for superior network performance and capacity.

- Automated RAN Operations: Streamlining network management and reducing operational complexities through intelligent automation.

- Optimized Resource Allocation: Dynamically allocating network resources for maximum efficiency and subscriber experience.

- Increased Energy Efficiency: Significantly reducing power consumption in the RAN, contributing to sustainable network operations.

The partnership essentially aims to make vRAN superior in performance and TCO (Total Cost of Ownership) compared to traditional, proprietary, purpose built RAN hardware.

“We are incredibly excited to expand our collaboration with Intel to pioneer truly AI-native RAN architectures,” said Sharad Sriwastawa, co-CEO and CTO, Rakuten Mobile. “Together, we are validating transformative AI-driven innovations that will not only shape but define the future of mobile networks. This partnership showcases how intelligent RAN can be achieved through the seamless and efficient integration of AI workloads directly within existing vRAN software stacks, delivering unparalleled performance and efficiency.”

Rakuten Mobile and Intel are engaged in rigorous testing and validation of cutting-edge RAN AI use cases across Layer 1, Layer 2, and comprehensive RAN operation and network platform management. A core objective is the seamless integration of AI directly into the RAN stack, meticulously addressing integration challenges while upholding carrier-grade reliability and stringent latency requirements.

Utilizing Intel FlexRAN reference software, the Intel vRAN AI Development Kit, and a robust suite of AI tools and libraries, Rakuten Mobile is collaboratively training, optimizing, and deploying sophisticated AI models specifically tailored for demanding RAN workloads. This collaborative effort is designed to realize ultra-low, real-time AI latency on Intel Xeon 6 SoC, capitalizing on their built-in AI acceleration capabilities, including AVX512/VNNI and AMX.

“AI is transforming how networks are built and operated,” said Kevork Kechichian, Executive Vice President and General Manager of the Data Center Group, Intel Corporation. “Together with Rakuten, we are demonstrating how AI benefits can be achieved in vRAN. Intel Xeon processors power the majority of commercial vRAN deployments worldwide, and this transformation momentum continues to accelerate. Intel is providing AI-ready Xeon platforms that allow operators like Rakuten to design AI-ready infrastructure from the ground up, with built-in acceleration capabilities.”

Rakuten says they are “poised to unlock new levels of RAN performance, efficiency, and automation by embedding AI directly into the RAN software stack, this AI-native evolution represents the future of cloud-native, AI-powered RAN – inherently software-upgradable and built on open, general-purpose computing platforms. Additionally, the extended collaboration between Rakuten Mobile and Intel marks a significant step toward realizing the vision of autonomous, self-optimizing networks and powerfully reinforces both companies’ commitment to open, programmable, and intelligent RAN infrastructure worldwide.”

……………………………………………………………………………………………………………………………………………………………………..

- AI-Native Efficiency & Performance: The collaboration focuses on integrating AI to improve network performance and energy efficiency, which is a major pain point for operators. By embedding AI directly into the vRAN stack, they are enhancing wireless spectral efficiency, reducing power consumption, and automating RAN operations.

- Leveraging High-Performance Hardware: The initiative utilizes Intel® Xeon® 6 processors with built-in vRAN Boost. This eliminates the need for external, power-hungry accelerator cards, offering up to 2.4x more capacity and 70% better performance-per-watt.

- Validation of Large-Scale Commercial Viability: Rakuten Mobile operates the world’s first fully virtualized, cloud-native network. Its continued collaboration with Intel to make the vRAN AI-native provides a proven blueprint for other operators, reducing the perceived risk of adopting vRAN, particularly in brownfield (existing) networks.

- Acceleration of Open RAN Ecosystem: The collaboration supports the broader push towards Open RAN, which is expected to see a significant rise in market share, doubling between 2022 and 2026.

………………………………………………………………………………………………………………………………………………………………

- Market Share Shift: Omdia forecasts that vRAN’s share of the RAN baseband subsector will reach 20% by 2028. That’s a significant jump from its current low single-digit percentage.

- Explosive CAGR: The global vRAN market is projected to grow from approximately $16.6 billion in 2024 to nearly $80 billion by 2033, representing a 19.5% CAGR.

- Small Cell Dominance: By the end of 2026, it is estimated that 77% of all vRAN implementations will be on small cell architectures, a key area where Rakuten and Intel have demonstrated success.

References:

https://corp.mobile.rakuten.co.jp/english/news/press/2026/0210_01/

Virtual RAN gets a boost from Samsung demo using Intel’s Grand Rapids/Xeon Series 6 SoC

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

vRAN market disappoints – just like OpenRAN and mobile 5G

LightCounting: Open RAN/vRAN market is pausing and regrouping

Dell’Oro: Private 5G ecosystem is evolving; vRAN gaining momentum; skepticism increasing

https://www.mordorintelligence.com/industry-reports/virtualized-ran-vran-market

https://www.grandviewresearch.com/industry-analysis/virtualized-radio-access-network-market-report

Fiber Optic Boost: Corning and Meta in multiyear $6 billion deal to accelerate U.S data center buildout

Corning Incorporated and Meta Platforms, Inc. (previously known as Facebook) have entered a multiyear agreement valued at up to $6 billion. This strategic collaboration aims to accelerate the deployment of cutting-edge data center infrastructure within the U.S. to bolster Meta’s advanced applications, technologies, and ambitious artificial intelligence initiatives. The agreement specifies that Corning will furnish Meta with its latest advancements in optical fiber, cable, and comprehensive connectivity solutions. As part of this commitment, Corning plans to significantly scale its manufacturing capabilities across its North Carolina facilities.

A key element of this expansion is a substantial capacity increase at its fiber optic cable manufacturing plant in Hickory NC, for which Meta will serve as the foundational anchor customer. The construction and operation of these data centers — critical infrastructure that supports our technologies and moves us toward personalized superintelligence — necessitate robust server and hardware systems designed to facilitate information transfer and connectivity with minimal latency. Fiber optic cabling is a cornerstone component for enabling this high-speed, near real-time connectivity, powering applications from sophisticated wearable technology like the Ray-Ban Meta AI glasses to the global connectivity services utilized by billions of individuals and enterprises.

“This long-term partnership with Meta reflects Corning’s commitment to develop, innovate, and manufacture the critical technologies that power next-generation data centers here in the U.S.,” said Wendell P. Weeks, Chairman and Chief Executive Officer, Corning Incorporated. “The investment will expand our manufacturing footprint in North Carolina, support an increase in Corning’s employment levels in the state by 15 to 20 percent, and help sustain a highly skilled workforce of more than 5,000 — including the scientists, engineers, and production teams at two of the world’s largest optical fiber and cable manufacturing facilities. Together with Meta, we’re strengthening domestic supply chains and helping ensure that advanced data centers are built using U.S. innovation and advanced manufacturing.”

Meta is expanding its commitment to build industry-leading data centers in the U.S. and to source advanced technology made domestically. Here are two quotes from them:

- “Building the most advanced data centers in the U.S. requires world-class partners and American manufacturing,” said Joel Kaplan, Chief Global Affairs Officer at Meta. “We’re proud to partner with Corning – a company with deep expertise in optical connectivity and commitment to domestic manufacturing – for the high-performance fiber optic cables our AI infrastructure needs. This collaboration will help create good-paying, skilled U.S. jobs, strengthen local economies, and help secure the U.S. lead in the global AI race.”

- “As digital tools and generative AI continue to transform our economy — in fields like healthcare, finance, agriculture, and more — the demand for fiber connectivity will continue to grow. By supporting American companies like Corning and building and operating data centers in America, we’re helping ensure that our nation maintains its competitive edge in the digital economy and the global race for AI leadership.”

Key elements of the agreement:

- Multiyear, up to $6 billion commitment.

- Corning to supply latest generation optical fiber, cable and connectivity products designed to meet the density and scale demands of advanced AI data centers.

- New optical cable manufacturing facility in Hickory, North Carolina, in addition to expanded production capacity across Corning’s North Carolina operations.

- Agreement supports Corning’s projected employment growth in North Carolina by 15 to 20 percent, sustaining a skilled workforce of more than 5,000 employees in the state, including thousands of jobs tied to two of the world’s largest optical fiber and cable manufacturing facilities.

…………………………………………………………………………………………………………………………………………………………….

Comment and Analysis:

Corning’s “up to $6 billion” Meta agreement is essentially a long‑term, anchor‑tenant bet that AI‑era data centers will be fundamentally more fiber‑intensive than legacy cloud resident data centers, with Corning positioning itself as the default U.S. optical plant for Meta’s buildout through ~2030. In practice, this deal is a long‑term take‑or‑pay style capacity lock that de‑risks Corning’s capex while giving Meta priority access to scarce, high‑performance data‑center‑grade fiber and cabling.

AI data centers are becoming the new FTTH in the sense that hyperscale AI buildouts are now the primary structural driver of incremental fiber demand, design innovation, and capex prioritization—but with far higher fiber intensity per site and far tighter performance constraints than residential access ever imposed.

Why “AI Data Centers are the new FTTH” for fiber optic vendors:

For fiber‑optic vendors, AI data centers now play the role that FTTH did in the 2005–2015 cycle: the anchor use case that justifies new glass, cable, and connectivity capacity.

-

AI‑optimized data centers need 2–4× more fiber cabling than traditional hyperscalers, and in some designs more than 10×, driven by massively parallel GPU fabrics and east–west traffic.

-

U.S. hyperscale capacity is expected to triple by 2029, forcing roughly a 2× increase in fiber route miles and a 2.3× increase in total fiber miles, a demand shock comparable to or larger than the early FTTH boom but concentrated in fewer, much larger customers.

-

This is already reshaping product roadmaps toward ultra‑high‑fiber‑count (UHFC) cable, bend‑insensitive fiber, and very‑small‑form‑factor connectors to handle hundreds to thousands of fibers per rack and per duct.

In other words, where FTTH once dictated volume and economies of scale, AI data centers now dictate density, performance, and margin mix.

Carrier‑infrastructure: from access to fabric:

From a carrier perspective, the “new FTTH” analogy is about what drives long‑haul and metro planning: instead of last‑mile penetration, it’s AI fabric connectivity and east–west inter‑DC routes.

-

Each new hyperscale/AI data center is modeled to require on the order of 135 new fiber route miles just to reach three core network interconnection points, plus additional miles for new long‑haul routes and capacity upgrades.

-

An FBA‑commissioned study projects U.S. data centers alone will need on the order of 214 million additional fiber miles by 2029, nearly doubling the installed base from ~160M to ~373M fiber miles; that is the new “build everywhere” narrative operators once used for FTTH.

-

Carriers now plan backbone routes, ILAs, and regional rings around dense clusters of AI campuses, treating them as primary traffic gravity wells rather than as just a handful of peering sites at the edge of a consumer broadband network.

The strategic shift: FTTH made the access network fiber‑rich; AI makes the entire cloud and transport fabric fiber‑hungry.

Strategic implications:

-

AI is now the dominant incremental fiber use case: residential fiber adds subscribers; AI adds orders of magnitude more fibers per site and per route.

-

Network economics are moving from passing more homes to feeding more GPUs: route miles, fiber counts, and connector density are being dimensioned to training clusters and inference fabrics, not household penetration curves.

-

Policy and investment narratives should treat AI inter‑DC and campus fiber as “national infrastructure” on par with last‑mile FTTH, given the scale of projected doubling in route miles and more than doubling in fiber miles by 2029.

In summary, the next decade of fiber innovation and capex will be written less in curb‑side PON and more in ultra‑dense, AI‑centric data centers with internal fiber optical fabrics and interconnects.

……………………………………………………………………………………………………………………………………………………………………………………………….

References:

Meta Announces Up to $6 Billion Agreement With Corning to Support US Manufacturing

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

Analysis: Cisco, HPE/Juniper, and Nvidia network equipment for AI data centers

Networking chips and modules for AI data centers: Infiniband, Ultra Ethernet, Optical Connections

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Superclusters of Nvidia GPU/AI chips combined with end-to-end network platforms to create next generation data centers

Lumen Technologies to connect Prometheus Hyperscale’s energy efficient AI data centers

Proposed solutions to high energy consumption of Generative AI LLMs: optimized hardware, new algorithms, green data centers

Hyper Scale Mega Data Centers: Time is NOW for Fiber Optics to the Compute Server

Analysis: OpenAI and Deutsche Telekom launch multi-year AI collaboration

Deutsche Telekom (DT) has formalized a strategic, multi-year collaboration with OpenAI to integrate advanced artificial intelligence (AI) solutions across its internal operations and customer engagement platforms. The partnership aims to co-develop “simple, personal, and multi-lingual AI experiences” focused on enhancing communication and productivity. Initial pilot programs are slated for deployment in Q1 2026. AI will also play a larger role in customer care, internal copilots, and network operations as the Group advances toward more autonomous, self-healing networks.DT plans a company-wide rollout of ChatGPT Enterprise, leveraging AI to streamline core functions including:

- Customer Care: Deploying sophisticated virtual assistants to manage billing inquiries, service outages, plan modifications, roaming support, and device troubleshooting [1].

- Internal Operations: Utilizing AI copilots to increase internal efficiency.

- Network Management: Optimizing core network provisioning and operations.

- Sovereign Cloud (2021): DT’s T-Systems division partnered with Google Cloud to offer sovereign cloud services.

- T Cloud Suite (Early 2025): The launch of a comprehensive suite providing sovereign public, private, and AI cloud options leveraging hybrid infrastructure.

- Industrial AI Cloud (Early 2025): A collaboration with Nvidia to build a dedicated industrial AI data center in Munich, scheduled for Q1 2026 operations.

- Edge AI compute services for enterprises.

- Vertical AI solutions tailored for healthcare, retail, and manufacturing sectors.

- Integrated private 5G and AI bundles for industrial logistical hubs.

“Telcos – if they execute – will have a big play in the edge inferencing space as well as providing hosting and colo services that can host domain specific SLMs that need to be run closer to the user data,” he said. “Furthermore, telcos will play a role in connectivity services across Neocloud providers such as CoreWeave, Lambda Labs, Digital Ocean, Vast.AI etc. OpenAI does not want to lose the opportunity to partner with telcos so they are striking early,” Nag added.

Other Voices:

- Roger Entner notes the model is highly applicable to European incumbents (e.g., Orange, Telefonica) due to the relative scarcity of existing AI data centers in the region, allowing operators to fill a critical infrastructure gap. Conversely, the model is less viable for U.S. operators, where hyperscalers already dominate the extensive data center market.

- AvidThink Founder and colleague Roy Chua cautions that while DT presents a robust “reference blueprint,” replicating this strategy requires significant scale, substantial financial investment, and regulatory alignment—factors not easily accessible to all network operators.

- Futurum Group VP and Practice Lead Nick Patience told Fierce Network, “This deal elevates DT from being a user of AI to being a co-developer, which is pretty significant. DT is one of the few operators building a full-stack AI story. This is an example of OpenAI treating telcos as high-scale distribution and data channels – customer care, billing, network telemetry, national reach and government relationships. This suggests OpenAI is deliberately building an operator channel in key regions (U.S., Korea, EU) but still in partnership with existing cloud and infra providers rather than displacing them.”

OpenAI has established significant partnerships with several telecom network providers and related technology companies to integrate AI into network operations, enhance customer experience, and develop new AI-native platforms. Those deals and collaborations include:

- T-Mobile: T-Mobile has a multi-year agreement with OpenAI and is actively testing the integration of AI (specifically IntentCX) into its business operations for customer service improvements. T-Mobile is also collaborating with Nokia and Nvidia on AI-RAN (Radio Access Network) technologies for 6G innovation.

- SK Telecom (SKT): SK Telecom has an in-house AI company and collaborates with OpenAI and other AI leaders like Anthropic to enhance its AI capabilities, build sovereign AI infrastructure, and explore new services for its customers in South Korea and globally. They are also reportedly integrating Perplexity into their offerings.

- Deutsche Telekom (DT): DT is partnering with OpenAI to offer ChatGPT Enterprise across its business to help teams work more effectively, improve customer service, and automate network operations.

- Circles: This global telco technology company and OpenAI announced a strategic global collaboration to build a fully AI-native telco SaaS platform, which will first launch in Singapore. The platform aims to revolutionize the consumer experience and drive operational efficiencies for telcos worldwide.

- Rakuten: Rakuten and OpenAI launched a strategic partnership to develop AI tools and a platform aimed at leveraging Rakuten’s Open RAN expertise to revolutionize the use of AI in telecommunications.

- Orange: Orange is working with OpenAI to drive new use cases for enterprise needs, manage networks, and enable innovative customer care solutions, including those that support African regional languages.

- Indian Telecoms (Reliance Jio, Airtel): Telecom providers in India are integrating AI tools from companies like Google and Perplexity into their mobile subscriptions, providing millions of users access to advanced intelligence resources.

- Nokia & Nvidia: In a broader industry collaboration, Nvidia invested $1 billion in Nokia to add Nvidia-powered AI-RAN products to Nokia’s portfolio, enabling telecom service providers to launch AI-native 5G-Advanced and 6G networks. This partnership also includes T-Mobile US for testing.

Conclusions:

With more than 261 million mobile customers globally, Deutsche Telekom provides a strong foundation to bring AI into everyday use at scale. The new collaboration marks the next step in Deutsche Telekom’s AI journey – moving from early pilots to large-scale products that make AI useful for everyone

References:

https://www.telekom.com/en/media/media-information/archive/openai-and-telekom-collaborate-1100164

https://www.telekom.com/en/company/companyprofile/company-profile-625808

Deutsche Telekom: successful completion of the 6G-TakeOff project with “3D networks”

Deutsche Telekom and Google Cloud partner on “RAN Guardian” AI agent

Deutsche Telekom offers 5G mmWave for industrial customers in Germany on 5G SA network

Deutsche Telekom migrates IP-based voice telephony platform to the cloud

Open AI raises $8.3B and is valued at $300B; AI speculative mania rivals Dot-com bubble

OpenAI and Broadcom in $10B deal to make custom AI chips

Custom AI Chips: Powering the next wave of Intelligent Computing

OpenAI orders HBM chips from SK Hynix & Samsung for Stargate UAE project

OpenAI announces new open weight, open source GPT models which Orange will deploy

OpenAI partners with G42 to build giant data center for Stargate UAE project

Reuters & Bloomberg: OpenAI to design “inference AI” chip with Broadcom and TSMC

AI infrastructure spending boom: a path towards AGI or speculative bubble?

by Rahul Sharma, Indxx with Alan J Weissberger, IEEE Techblog

Introduction:

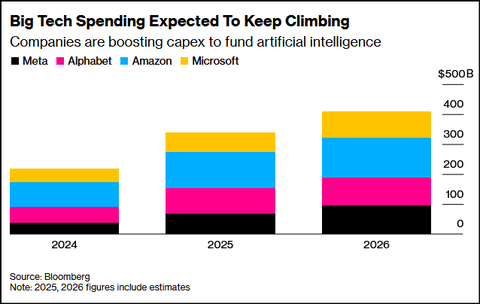

The ongoing wave of artificial intelligence (AI) infrastructure investment by U.S. mega-cap tech firms marks one of the largest corporate spending cycles in history. Aggregate annual AI investments, mostly for cloud resident mega-data centers, are expected to exceed $400 billion in 2025, potentially surpassing $500 billion by 2026 — the scale of this buildout rivals that of past industrial revolutions — from railroads to the internet era.[1]

At its core, this spending surge represents a strategic arms race for computational dominance. Meta, Alphabet, Amazon and Microsoft are racing to secure leadership in artificial intelligence capabilities — a contest where access to data, energy, and compute capacity are the new determinants of market power.

AI Spending & Debt Financing:

Leading technology firms are racing to secure dominance in compute capacity — the new cornerstone of digital power:

- Meta plans to spend $72 billion on AI infrastructure in 2025.

- Alphabet (Google) has expanded its capex guidance to $91–93 billion.[3]

- Microsoft and Amazon are doubling data center capacity, while AWS will drive most of Amazon’s $125 billion 2026 investment.[4]

- Even Apple, typically conservative in R&D, has accelerated AI infrastructure spending.

Their capex is shown in the chart below:

Analysts estimate that AI could add up to 0.5% to U.S. GDP annually over the next several years. Reflecting this optimism, Morgan Stanley forecasts $2.9 trillion in AI-related investments between 2025 and 2028. The scale of commitment from Big Tech is reshaping expectations across financial markets, enterprise strategies, and public policy, marking one of the most intense capital spending cycles in corporate history.[2]

Meanwhile, OpenAI’s trillion-dollar partnerships with Nvidia, Oracle, and Broadcom have redefined the scale of ambition, turning compute infrastructure into a strategic asset comparable to energy independence or semiconductor sovereignty.[5]

Growth Engine or Speculative Bubble?

As Big Tech pours hundreds of billions of dollars into AI infrastructure, analysts and investors remain divided — some view it as a rational, long-term investment cycle, while others warn of a potential speculative bubble. Yet uncertainty remains — especially around Meta’s long-term monetization of AGI-related efforts.[8]

Some analysts view this huge AI spending as a necessary step towards achieving Artificial General Intelligence (AGI) – an unrealized type of AI that possesses human-level cognitive abilities, allowing it to understand, learn, and adapt to any intellectual task a human can. Unlike narrow AI, which is designed for specific functions like playing chess or image recognition, AGI could apply its knowledge to a wide range of different situations and problems without needing to be explicitly programmed for each one.

Other analysts believe this is a speculative bubble, fueled by debt that can never be repaid. Tech sector valuations have soared to dot-com era levels – and, based on price-to-sales ratios, are well beyond them. Some of AI’s biggest proponents acknowledge the fact that valuations are overinflated, including OpenAI chairman Bret Taylor: “AI will transform the economy… and create huge amounts of economic value in the future,” Taylor told The Verge. “I think we’re also in a bubble, and a lot of people will lose a lot of money,” he added.

Here are a few AI bubble points and charts:

- AI-related capex is projected to consume up to 94% of operating cash flows by 2026, according to Bank of America.[6]

- Over $75 billion in AI-linked corporate bonds have been issued in just two months — a signal of mounting leverage. Still, strong revenue growth from AI services (particularly cloud and enterprise AI) keeps optimism alive.[7]

- Meta, Google, Microsoft, Amazon and xAI (Elon Musk’s company) are all using off-balance-sheet debt vehicles, including special-purpose vehicles (SPVs) to fund part of their AI investments. A slowdown in AI demand could render the debt tied to these SPVs worthless, potentially triggering another financial crisis.

- Alphabet’s (Google’s parent company) CEO Sundar Pichai sees “elements of irrationality” in the current scale of AI investing which is much more than excessive investments during the dot-com/fiber optic built-out boom of the late 1990s. If the AI bubble bursts, Pichai said that no company will be immune, including Alphabet, despite its breakthrough technology, Gemini, fueling gains in the company’s stock price.

…………………………………………………………………………………………………………………..

From Infrastructure to Intelligence:

Executives justify the massive spend by citing acute compute shortages and exponential demand growth:

- Microsoft’s CFO Amy Hood admitted, “We’ve been short on capacity for many quarters” and confirmed that the company will increase its spending on GPUs and CPUs in 2026 to meet surging demand.

- Amazon’s Andy Jassy noted that “every new tranche of capacity is immediately monetized”, underscoring strong and sustained demand for AI and cloud services.

- Google reported billions in quarterly AI revenue, offering early evidence of commercial payoff.

Macro Ripple Effects – Industrializing Intelligence:

AI data centers have become the factories of the digital age, fueling demand for:

- Semiconductors, especially GPUs (Nvidia, AMD, Broadcom)

- Cloud and networking infrastructure (Oracle, Cisco)

- Energy and advanced cooling systems for AI data centers (Vertiv, Schneider Electric, Johnson Controls, and other specialists such as Liquid Stack and Green Revolution Cooling).

| Company Name | Core Expertise | Key Solutions for AI Data Centers |

|---|---|---|

| Vertiv | Critical infrastructure (power & cooling) | Offers full-stack solutions with air and liquid cooling, power distribution units (PDUs), and monitoring systems, including the AI-ready Vertiv 360AI portfolio. |

| Schneider Electric | Energy management & automation | Provides integrated power and thermal management via its EcoStruxure platform, specializing in modular and liquid cooling solutions for HPC and AI applications. |

| Johnson Controls | HVAC & building solutions | Offers integrated, energy-efficient solutions from design to maintenance, including Silent-Aire cooling and YORK chillers, with a focus on large-scale operations. |

| Eaton | Power management | Specializes in electrical distribution systems, uninterruptible power supplies (UPS), and switchgear, which are crucial for reliable energy delivery to high-density AI racks. |

- LiquidStack: A leader in two-phase and modular immersion cooling and direct-to-chip systems, trusted by large cloud and hardware providers.

- Green Revolution Cooling (GRC): Pioneers in single-phase immersion cooling solutions that help simplify thermal management and improve energy efficiency.

- Iceotope: Focuses on chassis-level precision liquid cooling, delivering dielectric fluid directly to components for maximum efficiency and reduced operational costs.

- Asetek: Specializes in direct-to-chip (D2C) liquid cooling solutions and rack-level Coolant Distribution Units (CDUs) for high-performance computing.

- CoolIT Systems: Known for its custom direct liquid cooling technologies, working closely with server OEMs (Original Equipment Manufacturers) to integrate cold plates and CDUs for AI and HPC workloads.

–>This new AI ecosystem is reshaping global supply chains — but also straining local energy and water resources. For example, Meta’s massive data center in Georgia has already triggered environmental concerns over energy and water usage.

Global Spending Outlook:

- According to UBS, global AI capex will reach $423 billion in 2025, $571 billion by 2026 and $1.3 trillion by 2030, growing at a 25% CAGR during the period 2025-2030.

Compute demand is outpacing expectations, with Google’s Gemini saw 130 times rise in AI token usage over the past 18 months, highlighting soaring compute and Meta’s infrastructure needs expanding sharply.[9]

Conclusions:

The AI infrastructure boom reflects a bold, forward-looking strategy by Big Tech, built on the belief that compute capacity will define the next decade’s leaders. If Artificial General Intelligence (AGI) or large-scale AI monetization unfolds as expected, today’s investments will be seen as visionary and transformative. Either way, the AI era is well underway — and the race for computational excellence is reshaping the future of global markets and innovation.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Footnotes:

[1] https://www.investing.com/news/stock-market-news/ai-capex-to-exceed-half-a-trillion-in-2026-ubs-4343520?utm_medium=feed&utm_source=yahoo&utm_campaign=yahoo-www

[2] https://www.venturepulsemag.com/2025/08/01/big-techs-400-billion-ai-bet-the-race-thats-reshaping-global-technology/#:~:text=Big%20Tech’s%20$400%20Billion%20AI%20Bet:%20The%20Race%20That’s%20Reshaping%20Global%20Technology,-3%20months%20ago&text=The%20world’s%20largest%20technology%20companies,enterprise%20strategy%2C%20and%20public%20policy.

[3] https://www.businessinsider.com/big-tech-capex-spending-ai-earnings-2025-10?

[4] https://www.investing.com/analysis/meta-plunged-12-amazon-jumped-11–same-ai-race-different-economics-200669410

[5] https://www.cnbc.com/2025/10/15/a-guide-to-1-trillion-worth-of-ai-deals-between-openai-nvidia.html

[6] https://finance.yahoo.com/news/bank-america-just-issued-stark-152422714.html

[7] https://news.futunn.com/en/post/64706046/from-cash-rich-to-collective-debt-how-does-wall-street?level=1&data_ticket=1763038546393561

[8] https://www.businessinsider.com/big-tech-capex-spending-ai-earnings-2025-10?

[9] https://finance.yahoo.com/news/ai-capex-exceed-half-trillion-093015889.html

……………………………………………………………………………………………………………………………………………………………………………………………………………………………

About the Author:

Rahul Sharma is President & Co-Chief Executive Officer at Indxx – a provider of end-to-end indexing services, data and technology products. He has been instrumental in leading the firm’s growth since 2011. Raul manages Indxx’s Sales, Client Engagement, Marketing and Branding teams while also helping to set the firm’s overall strategic objectives and vision.

Rahul holds a BS from Boston College and an MBA with Beta Gamma Sigma honors from Georgetown University’s McDonough School of Business.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………

References:

Curmudgeon/Sperandeo: New AI Era Thinking and Circular Financing Deals

Expose: AI is more than a bubble; it’s a data center debt bomb

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

FT: Scale of AI private company valuations dwarfs dot-com boom

Amazon’s Jeff Bezos at Italian Tech Week: “AI is a kind of industrial bubble”

AI Data Center Boom Carries Huge Default and Demand Risks

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Nokia in major pivot from traditional telecom to AI, cloud infrastructure, data center networking and 6G

Reuters: US Department of Energy forms $1 billion AI supercomputer partnership with AMD

………………………………………………………………………………………………………………………………………………………………………….

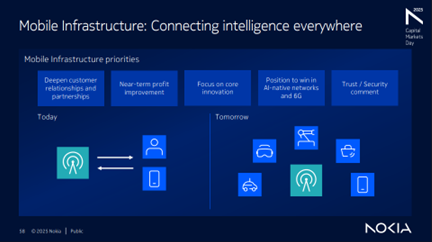

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

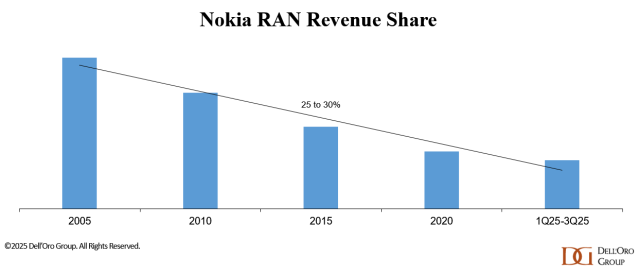

According to Dell’Oro VP Stefan Pongratz, Nokia has outlined a clear plan to arrest its declining RAN revenue share (see chart below), with NVIDIA now a central pillar of that strategy. The partnership is designed to deliver AI RAN [1.] while meeting wireless network operators’ near-term constraints and concerns on performance, power, and TCO (Total Cost of Ownership). IEEE Techblog has noted in many past blog posts that telcos have huge doubts about AI RAN which implies they won’t buy into that new RAN architecture.

This is especially relevant considering the monumental failure of multi-vendor Open RAN which was promoted as a game changer, but has dismally failed to attain that vision.

Note 1. AI RAN is a mobile RAN architecture where AI and machine learning are embedded into the RAN software and underlying compute platform to optimize how the network is planned, configured, and operated. It is being pushed by NVIDIA to get its GPUs into 5G, 5G Advanced and 6G base stations and other wireless network equipment in the RAN.

……………………………………………………………………………………………………………………………………………………..

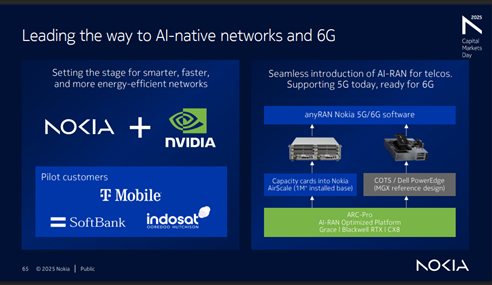

Nokia aims to use collaboration with NVIDIA (which invested $1B in the Finland based company) to stabilize its RAN market share in the near term and create a platform for long-term growth in AI-native 5G-Advanced and 6G networks. The timing—following a dense cadence of disclosures at NVIDIA’s GPU Technology Conference and Nokia’s Capital Markets Day—makes this an ideal time to reassess the scope of the joint announcements, the RAN implications, and Nokia’s broader competitive posture in an increasingly concentrated market.

Both companies share a belief that telecom networks will evolve from best-effort connectivity into a distributed compute fabric underpinning autonomous machines, self-driving vehicles, humanoids, and industrial digital twins. From that perspective, the RAN becomes an “AI grid” that executes and orchestrates AI workloads at the edge, enabling massive numbers of latency-sensitive, bandwidth-intensive AI use cases.

Unlike prior attempts to penetrate the RAN market with its GPUs, NVIDIA is now taking a more pragmatic approach, explicitly targeting parity with incumbent, purpose-built RAN equipment based on performance, power, and TCO rather than leading with speculative multi-tenant or new-revenue narratives. Nokia, acutely aware of wireless telco risk tolerance, is positioning the solution so that the ROI must be justifiable on a pure RAN basis, with additional AI and edge-compute upside treated as optional rather than foundational.

A quick recap of NVIDIA’s entry into RAN: Based on the announcement and subsequent discussions, our understanding is that NVIDIA will invest $1 B in Nokia and that NVIDIA-powered AI-RAN products will be incorporated into Nokia’s RAN portfolio starting in 2027 (with trials beginning in 2026). While RAN compute—which represents less than half of the $30B+ RAN market—is immaterial relative to NVIDIA’s $4+ T market cap, the potential upside becomes more meaningful when viewed in the context of NVIDIA’s broader telecom ambitions and its $165 B in trailing-twelve-month revenue.

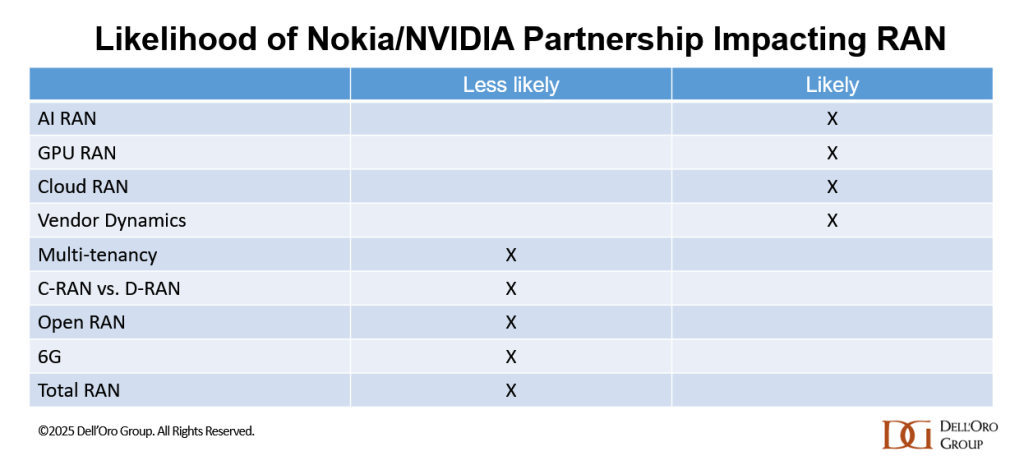

With a deployed base of more than 1 million BTS, Nokia is prioritizing three migration vectors to GPU/AI-RAN, in order of expected impact:

-

Purpose-built D-RAN [2.], by inserting a new card into existing AirScale slots.

-

D-RAN vRAN [3.], using COTS servers at the cell site.

-

Cloud RAN [4.] or vRAN, using centralized COTS infrastructure.

This approach aligns with wireless network operators’ desire to sweat existing AirScale assets while minimizing operational disruption.

Note 2. Purpose-built D-RAN is a distributed RAN architecture where the baseband processing runs on dedicated, vendor-specific hardware at or very close to the cell site, rather than on generic COTS servers. It is “purpose-built” because the silicon, boards, and software stack are tightly integrated and optimized for RAN performance, power efficiency, and footprint, not general-purpose compute.

Note 3. vRAN or virtual RAN is a technology that virtualizes the functions of a cellular network’s radio access network, moving them from dedicated hardware to software running on general-purpose servers. This approach makes mobile networks more flexible, scalable, and cost-efficient by replacing proprietary hardware with software on common-off-the-shelf (COTS) hardware.

Note 4. Cloud RAN (C-RAN) is a centralized cellular network architecture that uses cloud computing to virtualize and process radio access network (RAN) functions. This architecture centralizes baseband units in a “BBU hotel,” allowing for more flexible and scalable network management, efficient resource allocation, and improved network performance. It allows operators to pool resources, adjust capacity based on demand, and support new services, which is a key enabler for 5G networks.

………………………………………………………………………………………………………………………………………………

In this model, the Distributed Unit, and often the higher-layer functions, are physically collocated with the radio unit at the site, making each site a largely self-contained RAN node. This contrasts with Cloud RAN or vRAN, where baseband functions are centralized or virtualized on shared cloud infrastructure, and with cloud/AI-RAN approaches that rely on GPUs or other general-purpose accelerators instead of custom RAN hardware.

The macro-RAN market (baseband plus radio) is roughly a $30 billion annual opportunity, with on the order of 1–2 million macro sites shipped per year. In that context, operators have limited appetite to pay more than $10,000 for a GPU per sector, even if software-led benefits accumulate over time, which is why NVIDIA is signaling GPU pricing in line with ARC-Compact, but at roughly double the capacity and Nokia is targeting 48–50% gross margins in Mobile Infrastructure by 2028, slightly above the current run-rate.

If the TCO and performance-per-watt gap versus custom silicon continues to narrow, the partnership could materially influence AI-RAN and Cloud-RAN trajectories while also supporting Nokia’s margin expansion goals. AI-RAN was already expected to scale to roughly one-third of the RAN market by 2029; Nokia’s decision to lean harder into GPUs amplifies this structural shift without fundamentally changing the long-term 6G direction.

In the near term, GPU-enabled D-RAN using empty AirScale slots is expected to dominate deployments, reflecting operators’ preference for incremental, site-level upgrades. At the same time, the Nokia-NVIDIA partnership is not expected to meaningfully alter the overall Cloud RAN vs. D-RAN mix, Open RAN adoption (slow or non-existent) , or the trajectory of multi-tenant RAN, which remain more dependent on network operator architecture and commercial decisions than on a single vendor–silicon alignment.

Nokia plans to remain disciplined and focus on areas where it can differentiate and unlock value—particularly through software/faster innovation cycles via its recently announced partnership with NVIDIA. The company sees meaningful opportunities to capture incremental share in North America, Europe, India, and select APAC markets. And it is already off to a solid start— we estimate that Nokia’s 1Q25–3Q25 RAN revenue share outside North America improved slightly relative to 2024. Following this stabilization phase, Nokia is betting that its investments will pay off and that it will be well-positioned to lead with AI-native networks and 6G.

Nokia’s objective is clear: stabilize RAN in the short term, then grow by leading in AI-native networks and 6G over the longer horizon. Success now hinges on Nokia’s ability to operationalize the GPU-based RAN roadmap at scale and on NVIDIA’s ability to deliver carrier-grade economics and performance—turning the AI-RAN narrative into production-grade, repeatable deployments.

Nokia sees meaningful opportunities to capture incremental RAN market share in North America, Europe, India, and select APAC markets. And it is already off to a solid start— we estimate that Nokia’s 1Q25–3Q25 RAN revenue share outside North America improved slightly relative to 2024. Following this stabilization phase, Nokia is betting that its investments will pay off and that it will be well-positioned to lead with AI-native networks and 6G.

References:

Nokia in major pivot from traditional telecom to AI, cloud infrastructure, data center networking and 6G

Indosat Ooredoo Hutchison, Nokia and Nvidia AI-RAN research center in Indonesia amongst telco skepticism

Nvidia pays $1 billion for a stake in Nokia to collaborate on AI networking solutions

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

AI RAN Alliance selects Alex Choi as Chairman

Expose: AI is more than a bubble; it’s a data center debt bomb

NTT DOCOMO successful outdoor trial of AI-driven wireless interface with 3 partners

NTT DOCOMO has successfully executed the world’s premier outdoor field trial of real-time transceiver systems leveraging artificial intelligence (AI)-driven wireless technology, a critical advancement for sixth-generation (6G) mobile communications (AKA IMT 2030).

Conducted in collaboration with parent company NTT, Inc. (NTT), Nokia Bell Labs, and SK Telecom Co., Ltd, the field trials were held across three sites in Yokosuka City, Kanagawa Prefecture. The results validated that the application of AI optimized system throughput (transmission speed), achieving up to a 100% improvement over conventional, non-AI methods under identical environmental conditions, effectively doubling communication speeds.

Wireless communication quality can be compromised by fluctuations in radio propagation environments, leading to unstable connections. To mitigate this challenge, the partners developed “AI-AI technology,” which applies AI to both the transmitting and receiving ends of the wireless interface. This system dynamically optimizes modulation and demodulation schemes based on prevailing radio conditions, facilitating stable communication across diverse use cases. The efficacy of this technology had previously been confirmed in indoor environments.

The recent field trials aimed to verify the technology’s stable performance in complex outdoor settings, where radio conditions are subject to greater variability from factors such as temperature, weather, and physical obstructions.

This innovative AI wireless technology was evaluated across three distinct outdoor courses with varying propagation conditions, including the presence of obstacles and terminal mobility:

- Course 1: A public road featuring gentle curves, with a test vehicle traveling up to 40 km/h.

- Course 2: An environment with partial signal obstructions.

- Course 3: A road with minimal obstructions, with a test vehicle traveling up to 60 km/h.

In all test scenarios, the technology demonstrated its ability to compensate for signal degradation, confirming enhanced communication speeds. Specifically, in the highly complex propagation conditions of Course 1, the AI-AI technology yielded an average throughput improvement of 18% and a maximum increase of 100% compared to traditional methods.

These findings enable higher-speed data transmission for users and allow network operators to enhance spectrum efficiency and deliver superior quality of service (QoS). The successful outdoor validation marks a significant milestone toward the practical implementation of 6G systems, which promise a combination of high wireless transmission efficiency and reduced power consumption. NTT DOCOMO remains committed to refining this technology under a wide range of conditions and accelerating R&D efforts toward 6G realization, while simultaneously collaborating with global partners on 6G standardization (in 3GPP and ITU-R WP5D) and deployment.

This new technology will be featured at the NTT R&D FORUM 2025 hosted by NTT, scheduled from November 19–21 and November 25–26, 2025.

These three AI-wireless field trials represent the latest joint effort stemming from the collaborative AI research partnership of DOCOMO, parent NTT, Nokia Bell Labs, and SK Telecom Co, which was established at Mobile World Congress (MWC) in February 2024.

NTT Docomo has forged additional 6G alliances with a range of partners, including Ericsson, domestic Japanese suppliers Fujitsu and NEC, and testing specialists Keysight Technologies and Rohde & Schwarz.

This year has seen an increase in partnerships among Korean and Japanese operators. Earlier this month, KDDI‘s research partnership with Nokia Bell Labs was announced, focusing on achieving 6G energy efficiency and enhanced network resilience. Samsung and SoftBank entered into a memorandum of understanding (MoU) last month to co-develop prospective next-generation technologies, encompassing 6G, AI-driven Radio Access Networks (AI RAN), and Large Telecom Models (LTMs).

In a separate MoU signed in March, KT‘s and Samsung’s collaboration was formalized to jointly advance 6G antenna technology. Additionally, KT has maintained a separate research engagement with Nokia centered on semantic communications research.

About NTT DOCOMO:

NTT DOCOMO, Japan’s leading mobile operator with over 91 million subscribers, is one of the global leaders in 3G, 4G and 5G mobile network technologies.

Under the slogan “Bridging Worlds for Wonder & Happiness,” DOCOMO is actively collaborating with global partners to expand its business scope from mobile services to comprehensive solutions, aiming to deliver unsurpassed value and drive innovation in technology and communications, ultimately to support positive change and advancement in global society.

………………………………………………………………………………………………………………………………………………………………………………………….

References:

https://www.docomo.ne.jp/english/info/media_center/pr/2025/1117_00.html

https://www.docomo.ne.jp/english/

https://www.lightreading.com/6g/ntt-docomo-doubles-6g-throughput-in-ai-trials

NTT DOCOMO OREX brand offers a pre-integrated solution for Open RAN

NTT’s IOWN provides ultra low latency and energy efficiency in Japan and Hong Kong

NTT & Yomiuri: ‘Social Order Could Collapse’ in AI Era

NTT Docomo will use its wireless technology to enter the metaverse

Expose: AI is more than a bubble; it’s a data center debt bomb

We’ve previously described the tremendous debt that AI companies have assumed, expressing serious doubts that it will ever be repaid. This article expands on that by pointing out the huge losses incurred by the AI startup darlings and that AI poster child Open AI won’t have the cash to cover its costs 9which are greater than most analysts assume). Also, we quote from the Wall Street Journal, Financial Times, Barron’s, along with a dire forecast from the Center for Public Enterprise.

In Saturday’s print edition, The Wall Street Journal notes:

OpenAI and Anthropic are the two largest suppliers of generative AI with their chatbots ChatGPT and Claude, respectively, and founders Sam Altman and Dario Amodei have become tech celebrities.

What’s only starting to become clear is that those companies are also sinkholes for AI losses that are the flip side of chunks of the public-company profits.

OpenAI hopes to turn profitable only in 2030, while Anthropic is targeting 2028. Meanwhile, the amounts of money being lost are extraordinary.

It’s impossible to quantify how much cash flowed from OpenAI to big tech companies. But OpenAI’s loss in the quarter equates to 65% of the rise in underlying earnings of Microsoft, Nvidia, Alphabet, Amazon and Meta together. That ignores Anthropic, from which Amazon recorded a profit of $9.5B from its holding in the loss-making company in the quarter.

OpenAI committed to spend $250 billion more on Microsoft’s cloud and has signed a $300 billion deal with Oracle, $22 billion with CoreWeave and $38 billion with Amazon, which is a big investor in rival Anthropic.

OpenAI doesn’t have the income to cover its costs. It expects revenue of $13 billion this year to more than double to $30 billion next year, then to double again in 2027, according to figures provided to shareholders. Costs are expected to rise even faster, and losses are predicted to roughly triple to more than $40 billion by 2027. Things don’t come back into balance even in OpenAI’s own forecasts until total computing costs finally level off in 2029, allowing it to scrape into profit in 2030.

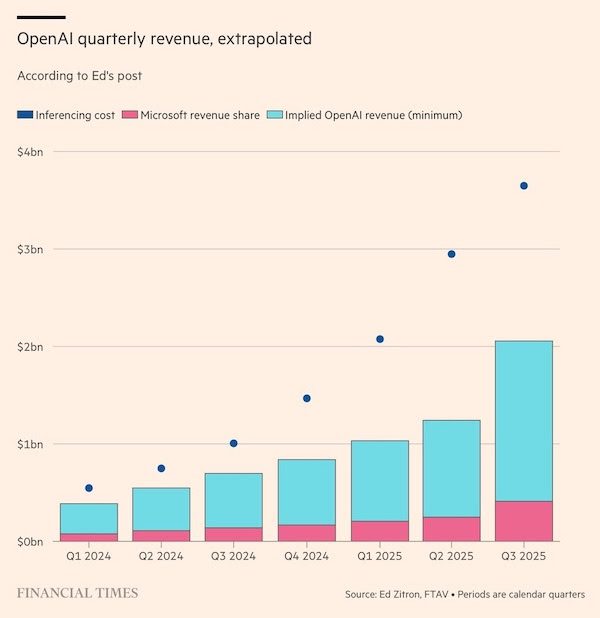

The losses at OpenAI that has helped boost the profits of Big Tech may, in fact, understate the true nature of the problem. According to the Financial Times:

OpenAI’s running costs may be a lot more than previously thought, and that its main backer Microsoft is doing very nicely out of their revenue share agreement.

OpenAI appears to have spent more than $12.4bn at Azure on inference compute alone in the last seven calendar quarters. Its implied revenue for the period was a minimum of $6.8bn. Even allowing for some fudging between annualised run rates and period-end totals, the apparent gap between revenues and running costs is a lot more than has been reported previously.

The apparent gap between revenues and running costs is a lot more than has been reported previously. If the data is accurate, then it would call into question the business model of OpenAI and nearly every other general-purpose LLM vendor.

Also, the financing needed to build out the data centers at the heart of the AI boom is increasingly becoming an exercise in creative accounting. The Wall Street Journal reports:

The Hyperion deal is a Frankenstein financing that combines elements of private-equity, project finance and investment-grade bonds. Meta needed such financial wizardry because it already issued a $30B bond in October that roughly doubled its debt load overnight.

Enter Morgan Stanley, with a plan to have someone else borrow the money for Hyperion. Blue Owl invested about $3 billion for an 80% private-equity stake in the data center, while Meta retained 20% for the $1.3 billion it had already spent. The joint venture, named Beignet Investor after the New Orleans pastry, got another $27 billion by issuing bonds that pay off in 2049, $18 billion of which Pimco purchased. That debt is on Beignet’s balance sheet, not Meta’s.

Dan Fuss, vice chairman of Loomis Sayles told Barrons: “We are good at taking credit risk,” Dan said, cheerfully admitting to having the scars to show for it. That is, he added, if they know the credit. But that’s become less clear with the recent spate of mind-bendingly complex megadeals, with myriad entities funding multibillion-dollar data centers. Fuss thinks current data-center deals are too speculative. The risk is too great and future revenue too uncertain. And yields aren’t enough to compensate, he concluded.

Increased wariness about monster hyper-scaler borrowings has sent the cost of insuring their debt against default soaring. Credit default swaps (CDS) more than doubled for Oracle since September, after it issued $18 billion in public bonds and took out a $38 billion private loan. CoreWeave’s CDS gapped higher this past week, mirroring the slide of the data-center company’s stock.

According to the Bank Credit Analyst (BCA), capex busts weigh on the economy, which further hits asset prices, the firm says. Following the dot-com bust, a housing bubble grew, which burst in the 2008-09 financial crisis. “It is far from certain that a new bubble will emerge (after the AI bubble bursts) this time around, in which case the resulting recession could be more severe than the one in 2001,” BCA notes.

………………………………………………………………………………………………………………………………………………

The widening gap between the expenditures needed to build out AI data centers and the cash flows generated by the products they enable creates a colossal risk which could crash asset values of AI companies. The Center for Public Enterprise reports that it’s “Bubble or Nothing.”

Should economic conditions in the tech sector sour, the burgeoning artificial intelligence (AI) boom may evaporate—and, with it, the economic activity associated with the boom in data center development.

Circular financing, or “roundabouting,” among so-called hyperscaler tenants—the leading tech companies and AI service providers—create an interlocking liability structure across the sector. These tenants comprise an incredibly large share of the market and are financing each others’ expansion, creating concentration risks for lenders and shareholders.

Debt is playing an increasingly large role in the financing of data centers. While debt is a quotidian aspect of project finance, and while it seems like hyperscaler tech companies can self-finance their growth through equity and cash, the lack of transparency in some recent debt-financed transactions and the interlocked liability structure of the sector are cause for concern.

If there is a sudden stop in new lending to data centers, Ponzi finance units ‘with cash flow shortfalls will be forced to try to make position by selling out position’—in other words to force a fire sale—which is ‘likely to lead to a collapse of asset values.’

The fact that the data center boom is threatened by, at its core, a lack of consumer demand and the resulting unstable investment pathways, is itself an ironic miniature of the U.S. economy as a whole. Just as stable investment demand is the linchpin of sectoral planning, stable aggregate demand is the keystone in national economic planning. Without it, capital investment crumbles.

……………………………………………………………………………………………………………..

Postscript (November 23, 2025):

In addition to cloud/hyperscaler AI spending, AI start-ups (especially OpenAI) and newer IT infrastructure companies (like Oracle) play a prominent role. It’s often a “scratch my back and I’ll scratch yours” type of deal. Let’s look at the “circular financing” arrangement between Nvidia and OpenAI where capital flows from Nvidia to OpenAI and then back to Nvidia. That ensures Nvidia a massive, long-term customer and providing OpenAI with the necessary capital and guaranteed access to critical, high-demand hardware. Here’s the scoop:

- Nvidia has agreed to invest up to $100 billion in OpenAI over time. This investment will be in cash, likely for non-voting equity shares, and will be made in stages as specific data center deployment milestones are met.

- OpenAIhas committed to building and deploying at least 10 gigawatts of AI data center capacity using Nvidia’s silicon and equipment, which will involve purchasing millions of Nvidia expensive GPU chips.

Here’s the Circular Flow of this deal:

- Nvidia provides a cash investment to OpenAI.

- OpenAI uses that capital (and potentially raises additional debt using the commitment as collateral) to build new data centers.

- OpenAI then uses the funds to purchase Nvidia GPUs and other data center infrastructure.

- The revenue from these massive sales flows back to Nvidia, helping to justify its soaring stock price and funding further investments.

What’s wrong with such an arrangement you ask? Anyone remember the dot-com/fiber optic boom and bust? Critics have drawn parallels to the “vendor financing” practices of the dot-com era, arguing these interconnected deals could create a “mirage of growth” and potentially an AI bubble, as the actual organic demand for the products is difficult to assess when companies are essentially funding their own sales.

However, supporters note that, unlike the dot-com bubble, these deals involve the creation of tangible physical assets (data centers and chips) and reflect genuine, booming demand for AI compute capacity although it’s not at all certain how they’ll be paid for.

There’s a similar cozy relationship with the $1B Nvidia invested in Nokia with the Finnish company now planning to ditch Marvell’s silicon and replace it by buying the more expensive, power hungry Nvidia GPUs for its wireless network equipment. Nokia, has only now become a strong supporter of Nvidia’s AI RAN (Radio Access Network), which has many telco skeptics.

………………………………………………………………………………………………………………………………………………….

References:

https://www.wsj.com/tech/ai/big-techs-soaring-profits-have-an-ugly-underside-openais-losses-fe7e3184

https://www.ft.com/content/fce77ba4-6231-4920-9e99-693a6c38e7d5

https://www.wsj.com/tech/ai/three-ai-megadeals-are-breaking-new-ground-on-wall-street-896e0023

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

AI Data Center Boom Carries Huge Default and Demand Risks

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

Gartner: AI spending >$2 trillion in 2026 driven by hyperscalers data center investments

Amazon’s Jeff Bezos at Italian Tech Week: “AI is a kind of industrial bubble”

FT: Scale of AI private company valuations dwarfs dot-com boom

IBM and Groq Partner to Accelerate Enterprise AI Inference Capabilities

IBM and Groq [1.] today announced a strategic market and technology partnership designed to give clients immediate access to Groq’s inference technology — GroqCloud, on watsonx Orchestrate – providing clients high-speed AI inference capabilities at a cost that helps accelerate agentic AI deployment. As part of the partnership, Groq and IBM plan to integrate and enhance RedHat open source vLLM technology with Groq’s LPU architecture. IBM Granite models are also planned to be supported on GroqCloud for IBM clients.

………………………………………………………………………………………………………………………………………………….

Note 1. Groq is a privately held company founded by Jonathan Ross in 2016. As a startup, its ownership is distributed among its founders, employees, and a variety of venture capital and institutional investors including BlackRock Private Equity Partners. Groq developed the LPU and GroqCloud to make compute faster and more affordable. The company says it is trusted by over two million developers and teams worldwide and is a core part of the American AI Stack.

NOTE that Grok, a conversational AI assistant developed by Elon Musk’s xAI is a completely different entity.

………………………………………………………………………………………………………………………………………………….

Enterprises moving AI agents from pilot to production still face challenges with speed, cost, and reliability, especially in mission-critical sectors like healthcare, finance, government, retail, and manufacturing. This partnership combines Groq’s inference speed, cost efficiency, and access to the latest open-source models with IBM’s agentic AI orchestration to deliver the infrastructure needed to help enterprises scale.

Powered by its custom LPU, GroqCloud delivers over 5X faster and more cost-efficient inference than traditional GPU systems. The result is consistently low latency and dependable performance, even as workloads scale globally. This is especially powerful for agentic AI in regulated industries.

For example, IBM’s healthcare clients receive thousands of complex patient questions simultaneously. With Groq, IBM’s AI agents can analyze information in real-time and deliver accurate answers immediately to enhance customer experiences and allow organizations to make faster, smarter decisions.

This technology is also being applied in non-regulated industries. IBM clients across retail and consumer packaged goods are using Groq for HR agents to help enhance automation of HR processes and increase employee productivity.

“Many large enterprise organizations have a range of options with AI inferencing when they’re experimenting, but when they want to go into production, they must ensure complex workflows can be deployed successfully to ensure high-quality experiences,” said Rob Thomas, SVP, Software and Chief Commercial Officer at IBM. “Our partnership with Groq underscores IBM’s commitment to providing clients with the most advanced technologies to achieve AI deployment and drive business value.”

“With Groq’s speed and IBM’s enterprise expertise, we’re making agentic AI real for business. Together, we’re enabling organizations to unlock the full potential of AI-driven responses with the performance needed to scale,” said Jonathan Ross, CEO & Founder at Groq. “Beyond speed and resilience, this partnership is about transforming how enterprises work with AI, moving from experimentation to enterprise-wide adoption with confidence, and opening the door to new patterns where AI can act instantly and learn continuously.”

IBM will offer access to GroqCloud’s capabilities starting immediately and the joint teams will focus on delivering the following capabilities to IBM clients, including:

- High speed and high-performance inference that unlocks the full potential of AI models and agentic AI, powering use cases such as customer care, employee support and productivity enhancement.

- Security and privacy-focused AI deployment designed to support the most stringent regulatory and security requirements, enabling effective execution of complex workflows.

- Seamless integration with IBM’s agentic product, watsonx Orchestrate, providing clients flexibility to adopt purpose-built agentic patterns tailored to diverse use cases.

The partnership also plans to integrate and enhance RedHat open source vLLM technology with Groq’s LPU architecture to offer different approaches to common AI challenges developers face during inference. The solution is expected to enable watsonx to leverage capabilities in a familiar way and let customers stay in their preferred tools while accelerating inference with GroqCloud. This integration will address key AI developer needs, including inference orchestration, load balancing, and hardware acceleration, ultimately streamlining the inference process.

Together, IBM and Groq provide enhanced access to the full potential of enterprise AI, one that is fast, intelligent, and built for real-world impact.

References:

FT: Scale of AI private company valuations dwarfs dot-com boom

AI adoption to accelerate growth in the $215 billion Data Center market

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?