Virtual Network Function Orchestration (VNFO) Market Overview: VMs vs Containers

by Kaustubha Parkhi, edited by Alan J Weissberger

Cloud-native network functions (CNF) promise to change the dynamic of telecommunications network function engineering. The advent of 5G has added impetus to this change. Insight Research is at the cutting edge of CNF market analysis. Here are a few excerpts from our new report on the Virtualized Network Function Orchestrator (VNFO) market

Insight Research considers Virtual Machines (VMs) and Containers to be the major Virtual Network Function Orchestration (VNFO) methodologies. Network functions synthesized using VMs and Containers qualify as Virtual Network Functions (VNFs), in our opinion. That latter term has taken on much broader context since it was first introduced in the context of Network Function Virtualization (NFV) at the OpenFlow World Congress in 2012.

VNFs orchestrated by Containers are sometimes referred to as cloud-native NFs (CNFs). Insight Research has also employed this term as early as 2020. Over time however, we have observed that the usage of CNFs is neither consistent nor uniform.

Most ‘traditional’ Management and Orchestration (MANO) schemes such as ONAP, OSM and all proprietary offerings now support Containers and Kubernetes [1.]. Containers are thus one more mean towards achieving the end-objective of VNFs. As such, Insight Research finds it more appropriate to use VNF as an umbrella term and refer to VM or Container as the specific virtualization methodology.

Note 1. Kubernetes, also known as K8s, is an open-source system for automating deployment, scaling, and management of containerized applications.

The question then arises – where would we slot network functions (NFs) orchestrated by containers encapsulated in VMs? Answer is containers. Similarly, NFs orchestrated by VMs encapsulated in containers are slotted under VMs.

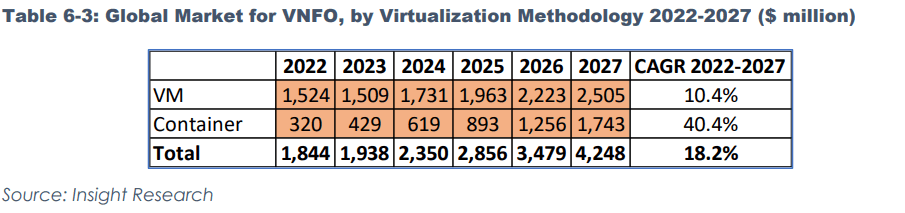

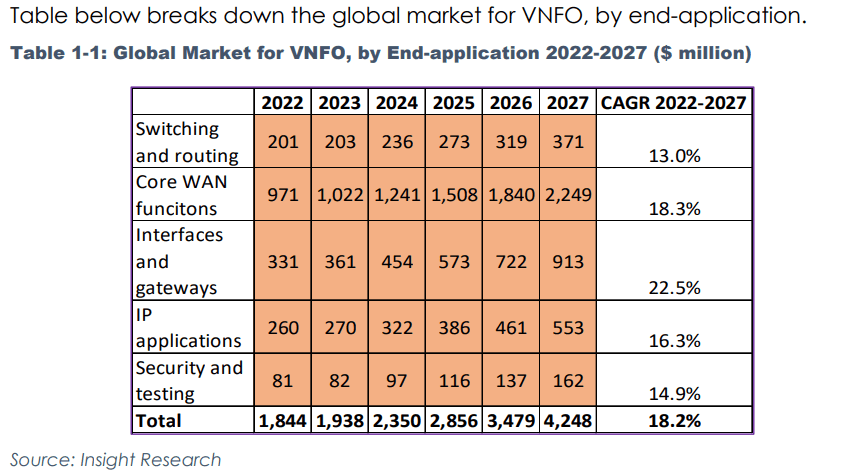

The table below breaks down the VNFO market by virtualization methodology.

We see Containers gaining major market share from VMs such that they are running away with the VNFO market. The advantages of containers over VMs are all well known. Containers are sleeker and when employed with optimal microservice granularity – considerably faster as well.

Additionally, VMs have a head start over containers and have established a solid legacy which will hold good for near to midterm future. However, barriers surrounding container adoption are gradually dissolving with differing momentums across end-applications. The greater the performance differential, the greater is the adoption potential for Containers in end-applications.

Initiatives such Nephio have placed Kubernetes in the center of the VNFO universe. In short, it’s a matter of time before Containers push VMs to be the dominant VNFO virtualization vehicle. However, many question arise.

Here are a few questions for starters:

Is the NFVO the same as service orchestrator?

Is the NFVO the same as SDN controller?

Is Kubernetes an orchestrator?

Since containers and VMs can be embedded inside one another, how do we stamp which virtualization methodology they are using?

If a proprietary MANO uses portions of open source code, should it be considered proprietary?

After picking the brains of numerous experts who were unfailingly patient in unravelling their thinking, Insight Research has been able to arrive at a set of clearcut definitions and assumptions that address the above queries and more.

To buy the report or download an executive summary, please visit:

https://www.insight-corp.com/product/vnfo-ripe-for-change/

Beijing Internet Institute: IPv6 leads Internet into a new era after 12+ years of wavering

Well, it’s certainly about time for IPv6! The transition from IPv4 to IPv6 has been going on for at least 12 years (See New Urgency to Move to IPv6 as Last Block of IPv4 Addresses are Allocated, published Feb 6, 2011!).

IPv6 is the first and might be the last upgrade of the global network in the coming decades. The development of IPv6 and IPv6 derivative and convergence technology standards will meet the objective requirements of the continuous expansion of the future network, facilitate the digital transformation in multiple fields, and become a new track of global digital technology innovation. In light of this, the “Global IPv6 Development and Standard Evolution Symposium and the Release Ceremony of the 2022 IPv6 Support White Paper,” held by the IPv6 Forum and the China Future Internet Engineering Center (CFIEC) on January 5, 2023.

The event accumulates global experts from global organizations from IPv6 Forum, CFIEC, Asia-Pacific Internet Network Information Center (APNIC), China Academy of Information and Communications Technology (CAICT), Internet Engineering Task Force (IETF), China Communication Standardization Association (CCSA), Institute of Electrical and Electronics Engineers (IEEE), European Telecommunications Standardization Association IPv6 Enhanced Innovation Working Group (ETSI IPE). Experts discuss the development vitality and opportunities of IPv6 under the new turning point of digital economy, strengthen the in-depth cooperation between different organizations, establish a perfect IPv6 and derived and fusion technology standards. accelerating large-scale deployment of IPv6 globally in the “global IPv6 development” and “IPv6 standard evolution” dimensions.

IPv6 is leading the development of the Internet

IPv6 provides more innovation capacity and development space for network infrastructure. Wu Hequan, academician of the CAE Member, summarizes the current development trend and characteristics of IPv6 at the meeting. He believes that the global Internet development has entered the dominant period of IPv6, which mainly presents three characteristics: first, the transition from IPv4 to IPv6 is accelerating; Second, from IPv4/IPv6 dual stack to IPv6 only; Third, IPv6 is developing towards IPv6+, with the developing IPv6 address space capabilities and fully integrating with the new generation of IT. IPv6 is playing an active role.

Liu Dong, Vice President of IPv6 Forum, introduced the development of the global IPv6 deployment in general: “The global IPv6 deployment speeds up to a new level in 2022. Countries or regions with a combined IPv6 deployment rate of around 30% or above account for more than half of the world. IPv6 deployment rate in 26 countries exceeded 40%, an increase of 9% compared with 2021; 37 countries have deployment rates exceeding 30%; The deployment rate of 51 countries exceeded 20%. IPv6-only has become a global consensus. The IPv6 applications and users will grow rapidly in the future ”

Sharing the development of IPv6 deployment in the Asia-Pacific region at the conference, Pan Guangliang, Director of Basic Resource Services at the Asia Pacific Internet Network Information Center (APNIC), puts, “The growth of the Internet has not stopped and will not stop. As more and more devices connects to the Internet, IPv6 is the way to go and is growing globally, with Asia seeing strong growth in overall IPv6 capability. According to APNIC statistics, the IPv6 support capacity in Asia exceeds the global average level by nearly 40%. Several countries such as China, India and Malaysia have witnessed rapid IPv6 development. In the next few years, the deployment of IPv6 will continue to improve, and more innovative applications based on IPv6 will appear ”

The development of IPv6 in China is outstanding. Gao Wei, director of the Internet Center of the Standards Institute of the China Academy of Information and Communications Technology, points out at the conference: “China is among the first countries in the world to carry out research, standard setting, application development and large-scale commercialization of IPv6 and next-generation Internet technologies. By December 2022, the number of IPv6 users in China has reached 717.7 million, with IPv6 traffic on fixed networks accounting for 12% and mobile networks 46%, showing a good momentum of development. IPv6 transformation achieves monumental success especially in the cloud platform, to achieve the new era of IPv6 traffic increase to provide strong support.”

IPv6 standard evolves from IPv6-Only to “cloud network”, “computing network” and “security”

In the era of digital economy, the integration of the Internet and the economy continues to deepen, and industrial digitalization with digital industrialization have become opportunities for all industries to score a new chapter. As an important starting point of digital transformation, standard is more conducive to opening up a leading advantage in the changing situation. The research, development and creation of IPv6 and its derived and converged technical standards are closely related to the development and deployment of IPv6. With the accelerated deployment of IPv6, the international standardization of IPv6 has entered a new stage and came across new changes.

Zhao Huiling, chairman of CCSA TC3 Technical Committee of China Communications Standardization Association, says that after 20 years of development, the current IPv6 standards have formed a systematic and standardized trend, covering five categories of standards: resources, networks, applications, security and transition. The standards at this stage can meet the needs of IPv6 network construction, but the security standards and application standards still have a lot to catch up. She also proposes four key directions for the creation of IPv6 industry standards in the new stage:

- First, in the field of cloud network integration, IPv6 supports the deep integration of new resources such as cloud network edge intelligent collaboration and data computing power;

- Second, in the field of IOT, IPv6 supports seamless global coverage, and anyone can communicate with anyone at any place and any time.

- Third, in the field of intelligent operation and maintenance, IPv6 supports end-to-end network quality assurance to ensure that the demands of the cloud on the network in enterprise production scenarios are met.

- Fourth, in the field of security and credibility, IPv6 supports end-to-end security endogenous mechanisms, adaptive security frameworks and security atomic capabilities, security defense, detection, and response prediction.

Li Zhenbin, member of the IETF Internet Architecture Committee (IAB) and Huawei’s chief IP protocol expert, also mentions that, “As the data communication industry moves towards the intelligent connection era of IPv6+, IETF has also gradually carried out various IPv6 standardization work, including the IPv6+1.0 (SRv6) standard, the IPv6+2.0 (5G&Cloud) standard Important achievements have been made in relevant standards. At this stage, IPv6 provides more differentiated service capabilities. Cloud network and computing network become the key applications of IPv6. Through IPv6 expansion and APN and other technologies, personalized networks can be realized and diverse computing power requirements can be met. In terms of APN6, we have signed a standard manuscript with several operators to successfully promote BOF at IETF, which will be the key direction of future technology innovation and standard creation. In addition, the general tunnel encapsulation technology GIP6 based on IPv6 also deserves further attention. ”

After years of deployment and penetration, IPv6 has entered a golden age of IPv6-Only evolution. When introducing the development of IPv6 at ETSI, Xie Chongfeng, Vice Chairman of ISG at ETSI IPE (IPv6 Enhanced innovation) and senior expert on IPv6 at China Academy of Telecommunication Research, says that network infrastructure is multi-domain and multi-scenario. To this end, we should actively promote the multi-domainIPv6-Only network architecture and technical requirements, in the form of a standard in the industry consensus, which will help operators, OTT, and service and devices manufacturers to buildIPv6-Only networks, and promote network infrastructure towards IPv6-Only.

The Release of 2022 Global IPv6 Support White Paper:

This seminar is not only a rare multilateral interaction and exchange between domestic and foreign organizations and experts on IPv6 development and standards, but also a demonstration of the fruitful results achieved in promoting IPv6 globally in the past year. At the meeting, the 2022 Global IPv6 Support White Paper jointly prepared by the IPv6 Forum and CFIEC was officially released. Latif Ladid, the president of the IPv6 Forum, says at the release ceremony that the white paper is based on the latest progress of global IPv6 technology, the number of global users, the network and domain name system, international operators, websites, cloud services Network equipment and other parties elaborate on the global IPv6 support and make multi-dimensional and multi-dimensional statistics to comprehensively, objectively and accurately reflect the global IPv6 development. At the same time, the IPv6 Forum also selected “IPv6 Outstanding Contribution Enterprises” and “IPv6 Pioneer Enterprises” in 2022 based on the white paper. Latif Latid gives awards to five enterprises including Cisco, Huawei, HP, H3C and D-Link, with the “IPv6 Outstanding Contribution Enterprise” award, and ten enterprises, Dell, IBM, TOPSEC, QI-ANXIN, Allied Telesis, Panasonic, Microsoft, ZTE, China Mobile and TP Link, receive the “IPv6 Pioneer Enterprise” award. Yang Wu, chief architect of the H3C Router product line, Zhu Keyi, head of the Huawei Digital Communication Standards and Patent Department, and Han Minglei, an expert on TUPSEC protocol conversion products, also shared the latest IPv6 solutions and products at the meeting.

Liu Dong, Vice President of the IPv6 Forum and director of CFIEC, illustrates: “At the beginning of the year, it is a great pleasure to meet with you online. Through your sharing, we can see that we have made progress in two important dimensions, ‘Global IPv6 Development’ and ‘IPv6 Standard Evolution’, and formed a large number of new achievements. In the future, our various organizations will continue to deepen cooperation and make use of advantages. While moving towards IPv6-Only, the first is to maintain continuous innovation and improve the IPv6 network value; The second is to actively expand the innovative application of IPv6 in the context of the Internet of Everything. The third is to create and improve new technical standards for the sustainable development of IPv6. Let us accelerate the global IPv6 scale deployment, and let IPv6 and the Internet benefit everyone. ”

SOURCE Beijing Internet Institute

References:

https://www.prnewswire.com/news-releases/the-internet-has-entered-the-new-era-led-by-ipv6-301716195.html

Akamai: U.S. Internet speeds increased 22% YoY; IPv6 adoption is a conundrum

New Urgency to Move to IPv6 as Last Block of IPv4 Addresses are Allocated

Can Quantum Technologies Crack RSA Encryption as China Researchers Claim?

Scientists in China claim they have found a way for current-generation quantum computers to crack the RSA algorithm underlying the most common form of online encryption. The researchers said the encryption could be broken with a 372-quantum-bit (qubit) system using hybrid quantum-classical methods to overcome scaling limitations. The Chinese paper “Factoring integers with sublinear resources on a superconducting quantum processor” stated that the algorithm used factored a number with 48 bits on a quantum system with 10 qubits.

The likelihood that quantum computers would be able to crack online encryption was widely believed a danger that could lie a decade or more in the future. But the 24 researchers, from a number of China’s top universities and government-backed laboratories, said their research showed it could be possible using quantum technology that is already available. The quantum bits, or qubits, used in today’s machines are highly unstable and only hold their quantum states for extremely short periods, creating “noise.”

As a result, “errors accumulate in the computer and after around 100 operations there are so many errors the computation fails,” said Steve Brierley, chief executive of quantum software company Riverlane. That has led to a search for more stable qubits as well as error-correction techniques to overcome the “noise,” pushing back the date when quantum computers are likely to reach their full potential by many years. The Chinese claim, by contrast, appeared to be an endorsement of today’s “noisy” systems, while also prompting a flurry of concern in the cyber security world over a potentially imminent threat to online security.

By late last week, a number of researchers at the intersection of advanced mathematics and quantum mechanics had thrown cold water on the Chinese claim:

- Massachusetts Institute of Technology’s Peter Shor pointed out that the team had “failed to address how fast the algorithm will run,” as it could “still take millions of years.” Shor, the American mathematician who first proposed a way for quantum computers to crack encryption, predicted that the inability to run all the computations at once meant it would take “millions of years” for a quantum computer to run the calculation proposed in the paper. The Chinese research comes at a time when many companies working on the technology are in a race to prove that today’s “noisy” systems can reach so-called quantum advantage — the point at which a quantum computer can perform a useful task more efficiently than a traditional, or “classical”, machine, ushering in commercial use of the technology.

- Brierley at Riverlane said it “can’t possibly work” because the Chinese researchers had assumed that a quantum computer would be able to simply run a vast number of computations simultaneously, rather than trying to gain an advantage through applying the system’s quantum properties.

- Four years ago, John Preskill, a professor of theoretical physics at the California Institute of Technology, predicted that quantum systems would start to outperform and might have commercial uses once they reached 50-100 qubits in size. But that moment has come and gone without quantum systems showing any clear superiority. IBM unveiled a 127-qubit computer more than a year ago, and last month announced that a new 433-qubit processor would be available in the first quarter of 2023. These days, Preskill sounds more cautious. “I expect that for practical applications with significant business value we’ll have to wait for error-corrected fault-tolerant quantum computers,” he said, adding that this was likely to be “a ways off.” But he added that today’s systems already had scientific value. One reason that hopes have retreated is that new ways have been found to program classical computers to handle tasks that were once thought to be beyond them.

This has pushed back the quantum frontier, delaying the moment when people building quantum systems can claim an advantage, said Oskar Painter, head of quantum hardware in the cloud computing division at Amazon, one of the tech companies that is building its own quantum computer. “They never finally could say, ‘This will be better,’” he said. After years of rising expectations, the lack of practical uses for the technology has led some experts to warn of a potential “quantum winter” — a period when disappointment about a new technology leads to a waning of interest for a number of years. The term is borrowed from the AI “winters” of the 1970s and 1980s, when a number of promising research avenues turned out to be dead ends, setting the field back for prolonged periods.

“People are worried it will be really harsh,” said Painter at Amazon Web Services. Like many in the field, though, he said that any short-term backlash was unlikely to hit long-term research funding. “I don’t think it will go away.” Receding hopes for early benefits from quantum computing have already contributed to a sharp fall in the stocks of a handful of companies that rode the wave of enthusiasm over the sector to go public since the middle of 2021. Based on their peak share prices soon after they each went public, Arquit, IonQ, D-Wave and Rigetti reached a combined value of $12.5bn. That has since fallen to $1.4bn.

Among the events to batter the quantum companies last year, IonQ was hit by a report from a short seller claiming its technology did not live up to its claims, while Rigetti founder Chad Rigetti was removed as chief executive before quitting the company late in the year.

Part of the problem facing the sector has been an excess of “hype” about the technology, said Constantin Gonciulea, chief technology officer of advanced technology at Wells Fargo. He compared the build-up of expectations around quantum to the crypto industry, as many non-experts have been drawn into the field and promises for the technology have far outgrown its potential in the near term. Despite this, companies working on the first quantum machines and software still insist that practical uses of the technology are just around the corner — while continuing to carefully avoid giving too precise a prediction about exactly when that will be.

David Rivas, head of engineering and product at Rigetti, said that the company still believed it would reach quantum advantage when its computers have “a few hundred to a few thousand qubits.” Even if they cannot match the performance of today’s supercomputers, they will still be useful if they cost much less, or if they can operate faster or with more precision, he said. For some quantum companies, the startling Chinese claim about online encryption was a sign that the technology’s big moment is drawing nearer. But for the doubters, the apparent impracticality of the research will serve as confirmation that quantum computing is still an impressive science experiment rather than a practical technology.

References:

https://arxiv.org/pdf/2212.12372.pdf

https://www.ft.com/content/d64e45b4-692a-429e-bc64-146303ec7fdf

Quantum Technologies Update: U.S. vs China now and in the future

AT&T will be “quantum ready” by the year 2025; New fiber network launched in Indiana

New ITU-T SG13 Recommendations related to IMT 2020 and Quantum Key Distribution

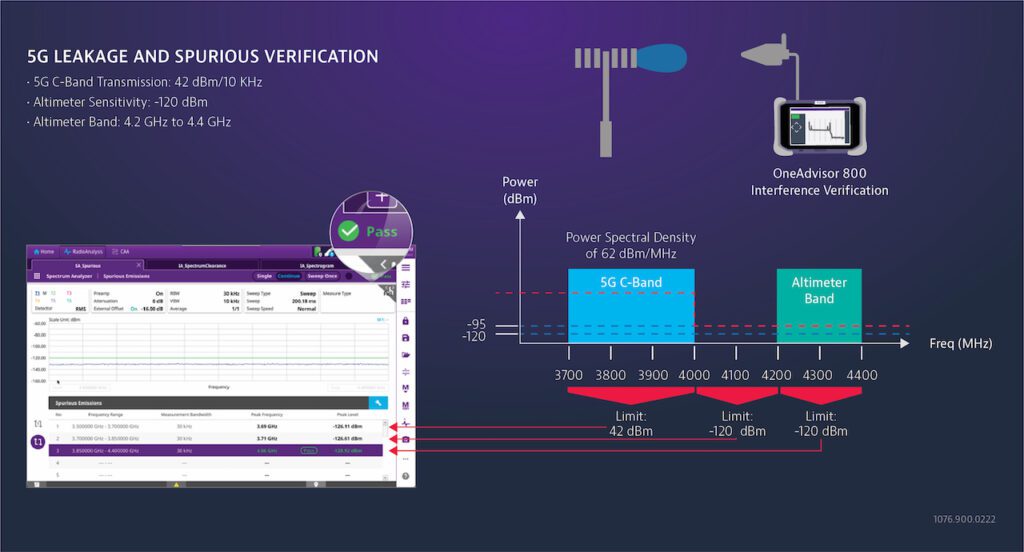

FAA NPRM: Aviation Industry Altimeter Upgrades to Thwart C-Band Interference

The Federal Aviation Administration (FAA) is giving the aviation industry more time to update legacy radio altimeters that could potentially be impacted by terrestrial 5G operations in C-Band spectrum.

In a notice of proposed rulemaking (to be published January 11, 2023), the FAA said that it remains concerned about the impacts of the C-Band operations on flights, including triggering false warnings from flight systems—particularly as more 5G is deployed across the entire band, and with more than 20 additional operators expected to start operating in the band later this year. This new Notice of Proposed Rulemaking (NPRM) lays out a timeline for retrofits by February 2024.

SUMMARY: The FAA proposes to supersede Airworthiness Directive 2021-23-12, which applies to all transport and commuter category airplanes equipped with a radio (also known as radar) altimeter. AD 2021-23-12 requires revising the limitations section of the existing airplane/aircraft flight manual to incorporate limitations prohibiting certain operations requiring radio altimeter data when in the presence of 5G C-Band interference as identified by Notices to Air Missions.

Since the FAA issued AD 2021-23-12, the FAA determined that additional limitations are needed due to the continued deployment of new 5G C-Band base stations whose signals are expected to cover most of the contiguous United States at transmission frequencies between 3.7-3.98 GHz. This proposed AD would require revising the limitations section of the existing airplane/aircraft flight manual to incorporate limitations prohibiting certain operations requiring radio altimeter data, due to the presence of 5G C-Band interference.

This proposed AD would also require modifying certain airplanes to allow safe operations in the United States 5G CBand radio frequency environment. The FAA is issuing this AD to address the unsafe condition on these products.

Originally, the agency had targeted a phased approach that required operators of regional aircraft with the most susceptible altimeters to retrofit them with filters by the end of 2022. AT&T and Verizon, meanwhile, had agreed to delay 5G C-band deployments near airports until July 2023, at which time air carriers were expected to have completed all the retrofits to mitigate possible 5G C-band spectrum interference.

Concerns about the impacts of 5G in C-Band to radio altimeters delayed the initial deployment of C-Band spectrum by AT&T and Verizon roughly a year ago. The worry is that the old altimeters, even though they operate in a completely different spectrum range, were not designed to filter out strong terrestrial cellular signals, leading to out-of-band interference. That interference could lead to the radars not being able to accurately gauge an aircraft’s height-above-ground, which could lead to aircraft crashes—particularly in fog or other situations where pilots would not be able to visually confirm whether height information was correct. As a result, Verizon and AT&T voluntarily agreed to operational tweaks near certain airports, including 5G transmission at reduced power levels, or tilt adjustments to cell sites to direct energy away from protected areas.

The FAA said that it has been able to review data from “dozens of alternative method of compliance (AMOC) requests, demonstrating that these radio altimeters can be relied upon to perform their intended function when operating beyond a certain protection radius around 5G C-Band transmitters.” The agency said that its first related actions on C-Band protection were based on conservative estimates of impacts, and that it initially sought to protect against interference during take-offs and landings within a two-nautical-mile circle around the ends of runways.

“After some time and an improved understanding of the C-Band signals and their effects on specific radio altimeters, the FAA was able to reduce the protected area around the ends of runways,” the agency said int he NPRM—first, by defining a rectangular protected airspace, then shifting that to a trapezoidal protection zone that allowed for expanded neighboring 5G signals. “The FAA is now able to assess the 5G C-Band transmissions’ impact to aviation operations in a specific area, taking into account the particularities of the signal and the airport environment. This assessment process is the Signal in Space (SiS) analysis. It includes a 3-dimensional model for the runway safety zone and considers base station heights and terrain around the airport,” the FAA said.

The FAA said that since it began soliciting reports of potential C-Band interference impacts, it received more than 420 reports of radio altimeter anomalies happening within the areas of known 5G C-band deployments. Most of those—about 315—were ultimately determined to have other causes and resolved through normal operational safety procedures, the agency said. But, it added, “for roughly 100 of the anomaly reports occurring within NOTAM areas, the FAA has excluded other potential causes for the anomaly, but could not rule out 5G C-Band interference as the potential source of the radio altimeter anomalies.”

Those 100 incidents included “erroneous Terrain Awareness and Warning System (TAWS) warnings, erroneous Traffic Collision Avoidance System (TCAS) warnings, erroneous landing gear warnings, and the erroneous display of radio altimeter data. … The FAA is concerned that to the extent 5G C-Band operations contributed to such events, the effects will occur more frequently as telecommunication companies continue to deploy 5G C-Band services throughout the country.”

“The radio altimeter modifications that would not require a substantial system redesign, allowing aircraft operators to readily replace radio altimeters or install filters that allowed the aircraft to operate safely in a mitigated 5G environment,” the agency said, adding that some altimeters will also be able to demonstration that level of performance without any modification. The FAA estimated that the modifications would affect about 7,993 aircraft registered in the U.S.

References:

https://public-inspection.federalregister.gov/2023-00420.pdf

FAA order to avoid interfering with 5G C-Band services; RootMetrics touts coverage vs performance advantages for 5G

AT&T, Verizon Propose C Band Power Limits to Address FAA 5G Air Safety concerns

Vodafone Germany plans to activate 2,700 new 5G cell sites in 1H 2023

Vodafone Germany plans to activate 2,700 new 5G cell sites with a total of 8,000 antennas in the first half of 2023, the telco said today in a press release. The company has so far connected 80% of the German population with 5G. It has activated 5G at 12,000 sites with more than 36,000 antennas altogether. For the 5G expansion, Vodafone Germany is relying on frequencies in the 3.6 GHz, 1.8 GHz and 700 MHz bands in large urban areas, residential areas and suburbs, and rural areas across Germany.

During 2022, Vodafone technicians commissioned 5,450 5G sites with more than 16,000 antennas. In total, Vodafone has already equipped 36,000 antennas with 5G, the company has said. The network operator said its 5G network is already providing coverage to 65 million people across the country, representing nearly 80% of Germany’s population.

Vodafone Germany had previously noted that its 5G Standalone (SA) network is currently available to nearly 20 million people across Germany. Vodafone previously said that 5G SA technology will reach nationwide coverage by 2025. The German telco had already deployed over 3,000 base stations for the provision of 5G SA services. Vodafone initially launched its 5G network in Germany in 2019, using 3.5 GHz frequencies that it acquired from Telefónica in 2018.

The telco also said it will continue to expand its LTE infrastructure across the country. Nationwide, Vodafone said it currently supplies around 98% of households with LTE.

“In 2023, Vodafone will bring the LTE mobile communications standard to even more people and to even more places: almost 1,900 expansion measures are pending in the first half of the year to set up new stations, carry out modernization work and install additional LTE antennas at existing stations,” Vodafone said.

“Together with Altice, Vodafone will start Germany’s largest fiber optic alliance in spring 2023, subject to the approval of the antitrust authorities. The goal is to supply up to 7 million households with new fiber optic connections in the next 6 years,” Vodafone added.

Vodafone Germany had recently successfully completed a field test with Open RAN (O-RAN) technology in Plauen, in the Saxony region.

The German carrier had recently announced that it will carry out comprehensive pilot projects for open 5G radio access networks at several locations in Germany. The first two stations for the operator’s O-RAN technology are located in rural Bavaria. The pilots are scheduled to start in early 2023 and mark the beginning of a broader deployment of O-RAN technology in Vodafone’s European mobile networks.

The pilot projects will use O-RAN hardware and software, which Vodafone successfully tested in the U.K. earlier this year. Samsung is currently supplying mobile technology and software for these O-RAN trials.

Separately, Vodafone has agreed to sell its Hungarian division for €1.7billion (£1.5billion) to local telecoms company 4iG and the Hungarian state. The sale is expected to be completed this month, with the proceeds to be used to pay off some of Vodafone’s debt.

References:

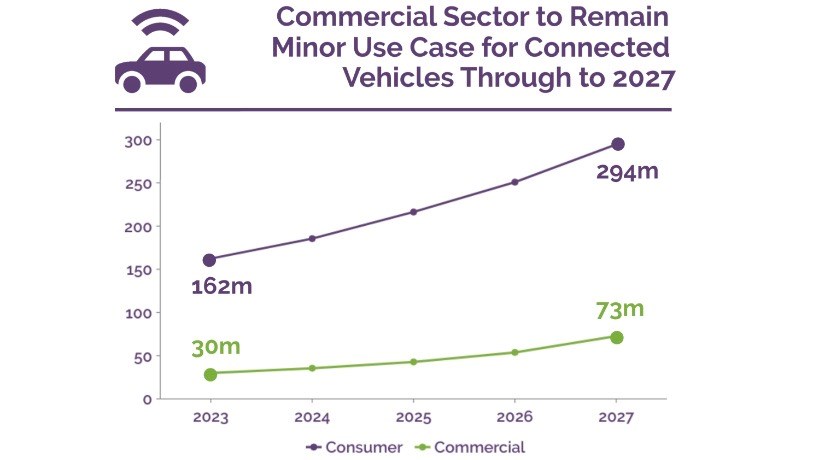

Juniper Research: 5G connectivity opportunity for the connected car market

The number of connected vehicles globally is set to grow from 192 million this year to more than 367 million in 2027, with 5G connectivity set to play a key role in the development of the market, according to a new report from Juniper Research. The company’s new Connected Vehicles research report provides an independent analysis of the future evolution of this fast-paced market and advanced connectivity solutions within the automotive industry. It provides a comprehensive study of the increase in constant connectivity technology features in cars being adopted by automotive original equipment manufacturers, how the rise of 5G is impacting the connected cars market expansion, and the key role mobile network operators have in driving the market forward in order to offer advanced connectivity and an enhanced driving experience.

The analyst firm believes the growth will be driven by improvements in both advanced driver assistance systems (ADAS), the attraction of enhanced in-vehicle infotainment systems, and the transformative potential of 5G’s high-speed and low-latency capabilities. However, maximizing 5G’s potential impact will require “effective collaborations between automotive OEMs and [mobile network] operators,” according to the authors of the report, who believe the 5G connectivity opportunity presented to telcos by the connected vehicle sector will be worth US$3.6bn in 2027.

According to the co-author of the research, Nick Maynard, “5G can allow automotive OEMs [original equipment manufacturers] to upgrade the in-vehicle experience. In a vehicle market transitioning to electric vehicles, improving the user experience is key. Operators hold the critical role in enabling this in a reliable way, making them the partners of choice as their 5G networks rapidly expand.” Connected vehicles utilising 5G will be able to exchange information “between the various elements of the transport system and third-party services.”

| Key Market Statistics | |

| Market size in 2023: | 192 million vehicles in service |

| Market size in 2027: | 367 million vehicles in service |

| 2023 – 2027 Market Growth: | 91% |

The report is upbeat overall, but notes that commercial use cases are proving more difficult to find and justify than those for ordinary automobile drivers. According to the Juniper Research team, by 2027 commercial vehicles will account for no more than 20% of connected vehicles worldwide, only a slight increase from the 16% that commercial vehicles will account for this year.

The research shows that such slow uptake is because commercial vehicle design is not yet fully exploiting the potential of connectivity beyond simple emergency call features and basic connected infotainment systems. The report recommends that automotive OEMs prioritize integrations with common fleet tracking systems out of the factory to maximise the benefits of connectivity, and to enable commercial fleet owners to maximize efficiency in their processes.

All types of connected vehicle technologies are still ‘works in progress,’ according to Juniper Research.

Various types of connected vehicle technologies are being pursued and improved. Vehicle-to-infrastructure (V2I) connectivity is used mainly to ensure vehicle safety as the vehicle communicates with road infrastructure and shares and receives information, such as traffic flows, road and weather conditions, speed limits, accident reports, and so on. Meanwhile, vehicle-to-vehicle (V2V) connectivity primarily permits the real-time exchange of information between vehicles.

Vehicle-to-cloud (V2C) connectivity is enabled via 4G/LTE networks and is mainly used for downloading over-the-air (OTA) vehicle updates, remote vehicle diagnostics or to connect with internet of things (IoT) devices. Vehicle-to-pedestrian (V2P) connectivity is a newer safety technology that uses sensors to detect pedestrians and other ‘obstacles’ and provides collision warning and avoidance guidance. Lastly, vehicle-to-everything (V2X) connectivity is exactly what it says it is – the combination of all the above connectivity systems and methods.

Of course, connected vehicle technology is not solely concerned with conventional automobiles. Self-driving vehicles will also exploit connection technologies to communicate with the road infrastructure and cloud platforms, but as incidents of crashes, injuries and deaths proliferate, self-driving vehicles are getting some bad press and would-be user enthusiasm is waning. Again, much stock is again being placed on the ability of 5G to help make self-driving vehicles not only safer but much more intelligent and responsive – it is very much a work in progress.

References:

Connected Car Market Research: Size, Trends, 2023-27 (juniperresearch.com)

Telcos to play critical 5G role in connected vehicles sector – report | TelecomTV

Verizon deploys Private 5G at Wichita Smart Factory; 5G Radio’s an Issue?

Executive Summary:

Verizon Business announced that its private 5G wireless network is live at The Smart Factory at Wichita, a new immersive, industry experience centre convened by Deloitte. Verizon collaborates with Deloitte and other companies in the Smart Factory ecosystem to advance smart manufacturing deployment and allow manufacturers to quickly adopt cutting-edge Industry 4.0 solutions and technologies that support new business models that improve quality, productivity, and sustainability.

Verizon, as a builder-level collaborator in The Smart Factory at Wichita ecosystem of 20 leading global companies, intends to use this network of companies to help customers from various industries to innovate their approach to better connectivity and use of data to improve real-time coordination between people and assets. Verizon’s private 5G wireless network provides features that will help drive select use cases at The Smart Factory in Wichita, which include:

Select Use Cases at The Smart Factory:

- Improved shop floor visibility: Using predictive maintenance analytics on assets can improve uptime and productivity by addressing up to approximately 50% of the root causes of downtime.

- Improved quality assurance and reduced defects: Detection of potential defects in manufactured products or services before they reach customers, thereby improving the customer experience and reducing waste.

- Material handling automation: Orchestration and management of AGV and AMR fleets can improve the reliability, consistency, safety, and accuracy of moving material across the plant.

- Workplace safety: Reduces human error and manual workloads to minimize injury and productivity loss.

Commenting on the Private 5G Network Deployment, Jennifer Artley, SVP, 5G Acceleration, Verizon Business, said: “The Smart Factory at Wichita is a microcosm of industry 4.0 itself, with a wide range of enterprise partners, suppliers, researchers, and complementary technologies coming together in one ecosystem to make a supercharged impact. 5G brings massive bandwidth and incredibly fast data speeds to the equation to help make these impacts replicable in a plethora of business applications at virtually any scale — customers have the flexibility to dream big and start small.”

“5G is the backbone of Industry 4.0, and we’re so excited to bring it to Deloitte’s The Smart Factory at Wichita to help catalyze scalable, collaborative innovation,” added Jennifer Artley.

The Smart Factory in Wichita:

The Smart Factory at Wichita assists firms through their most difficult manufacturing challenges by showcasing modern manufacturing techniques in a variety of applications on a shop floor. The Factory, located on the Innovation Campus at Wichita State University, includes a fully operational production line and experiential labs for creating and researching smart manufacturing technology and strategy.

Visitors to the facility can explore smart manufacturing concepts that combine the Internet of Things (IoT), cloud, artificial intelligence (AI), computer vision, and more to create interconnected systems that use data to drive real-time, intelligent decision-making.

Verizon Private 5G:

By utilizing Verizon 5G and edge computing to create applications and solutions that drive both the manufacturing and retail industries, this work with Deloitte at The Smart Factory at Wichita strengthens the commitment between the two businesses to co-innovate.

Verizon Business announced that its private 5G wireless network is live at The Smart Factory at Wichita, a new immersive, industry experience centre convened by Deloitte. Verizon collaborates with Deloitte and other companies in the Smart Factory ecosystem to advance smart manufacturing deployment and allow manufacturers to quickly adopt cutting-edge Industry 4.0 solutions and technologies that support new business models that improve quality, productivity, and sustainability.

Commenting on the Private 5G Network Deployment, Jennifer Artley, SVP, 5G Acceleration, Verizon Business, said: “The Smart Factory at Wichita is a microcosm of industry 4.0 itself, with a wide range of enterprise partners, suppliers, researchers, and complementary technologies coming together in one ecosystem to make a supercharged impact. 5G brings massive bandwidth and incredibly fast data speeds to the equation to help make these impacts replicable in a plethora of business applications at virtually any scale — customers have the flexibility to dream big and start small.”

“5G is the backbone of Industry 4.0, and we’re so excited to bring it to Deloitte’s The Smart Factory at Wichita to help catalyze scalable, collaborative innovation,” added Jennifer Artley.

Could 5G Radios be a Problem for Private 5G?

CEO Hans Vestberg told a Citi investor conference this week:

“We need certain radio base stations for private networks, different price ranges. We need modems for certain things. You need more than the handset and the macro sites that is now in there,” Vestberg said at Citi’s 2023 Communications, Media, and Entertainment Conference. “We would now have offerings for cheaper private 5G networks with certain suppliers and more high level, high quality. We didn’t have this optionality, and that’s why we’re now sort of seeing that we’re actually meeting the customer demands of building private 5G networks.”

Vestberg added that the carrier now has “the ecosystem for radios so we are fully committed. We strongly believe in private 5G networks, and that’s a revenue stream we don’t have today because we’re not into Wi-Fi networks and optimization of a manufacturing site. We’re not into that today.”

Verizon Business CEO Sowmyanarayan Sampath during an investor conference in November said it had dozens of private networks already deployed, with accelerating momentum.

“On the private networks, we are very bullish on that opportunity and I think things have gotten a little faster in the last 90 days than they’ve gotten in the last year or so,” Sampath said, adding most of Verizon’s initial private network deals have resulted in incremental spending by customers.

“For example, if we are providing wireline network services – I’ll call it more broadly network services – to 10,000 stores, and if the realtor wants 100 sites or 200 sites of private network, they’re going to come to us because we are already integrated into their service stack, we are integrated into their day-two operating model, we are integrated into their operating system, so when a ticket happens they know what to do and vice versa,” Sampath said. “It’s a very logical extension to our business when you’re managing large portions of the infrastructure to manage their private network piece to it.”

References:

https://www.fiercewireless.com/private-wireless/verizons-arvin-singh-discusses-private-5g

https://www.verizon.com/about/news/verizon-private-5g-network-aircraft-hangar

ITU report: Russia caused severe damage to Ukraine’s telecom infrastructure

Ukraine will need at least $1.79 billion to rebuild its telecommunications infrastructure to function at the pre-war level. International Telecommunication Union (ITU) a U.N. agency published a report showing that Russia had “destroyed completely or seized” telecom infrastructure in several parts of Ukraine. The ITU (formerly CCITT) was ordered to investigate the destruction of Ukraine’s communication networks caused by the Russian aggressors.

The report, which covers the first six months of war, notes significant damage and destruction of telecommunications infrastructure in more than 10 of Ukraine’s 24 regions. At the same time, it is emphasized that the aggressor either completely destroyed or captured telecommunications and critical infrastructure in occupied territories, as well as in the combat zone. In addition, the Russian Federation unilaterally changed Ukrainian telephone codes established by the UN agency to Russian ones.

“Since the beginning of military attacks, with the purpose of using the facilities in its interests and for its own needs, the aggressor either destroyed completely or seized the regular operation of public and private terrestrial telecommunication and critical infrastructure in the temporarily occupied and war-affected territories of Ukraine,” the document said.

According to the report, there had been as many as 1,123 cyber attacks against Ukraine. It also alleged that Moscow unilaterally switched Ukrainian dialling codes, fixed by the U.N. agency, to Russian ones.

Russia has regularly targeted Ukraine with cyberattacks since its annexation of Crimea in 2014. These attacks, perpetrated against government and banking websites, intensified before Moscow sent troops into Ukraine last year. Russia denies being behind those and the other attacks.

The U.N. report, which includes information and data through to August, was quietly posted in a corner of the ITU website in late December. It was brought to Reuters’ attention by a spokesperson on Friday afternoon after requests for information. Western diplomats have privately expressed frustration concerning delays to the report’s publication.

The EU wrote to then ITU Secretary-General, China’s Houlin Zhao, in September calling for its release, a letter seen by Reuters showed. Zhao responded a few days later to say the damage assessment was still underway, the response showed.

The ITU has not publicly commented on the report. Asked about the gap between the reporting period and the report’s publication, ITU told Reuters the report was published on Dec. 23 “after it was judged complete by the management.”

ITU added that the outcomes of its assessment would help mobilise technical assistance for Ukraine.

The Geneva-based agency, founded in 1865, allocates global radio spectrum and satellite orbits and sets standards for artificial intelligence and other new technologies.

Separately, Russia conducted 1,123 cyber attacks on Ukrainian infrastructure.

References:

Bullitt Satellite Connect: Another 2-way Satellite Messaging Service announced at CES 2023

Bullitt Group, the British manufacturer specializing in rugged mobile phones, has revealed a few more details about its two-way satellite messaging service at CES 2023. The service will be commercially available in North America and Europe the first quarter of 2023, the company said. Australia, New Zealand, Africa and Latin America will launch sometime in the first half of 2023, with other regions following the second half of the year.

Bullitt said Motorola, a Lenovo company, will be the first to include Bullitt’s two-way satellite messaging technology. The next device in Motorola Mobility’s Defy phone line-up will be the first smartphone to support Bullitt’s satellite messaging service.

The company previously said it was using telecom chipset supplier MediaTek. It now says it will use Skylo for satellite connectivity. Skylo manages connections to devices over existing licensed GEO satellite constellations, like Inmarsat and others.

Bullitt Satellite Connect solves a real connectivity problem. American’s send 6 billion SMS text messages each day* but, due to the sheer scale and topography of the country, no single carrier covers more than 70% of the US land mass and around 60 million Americans lose coverage for up to 25% of each day**.

That means hundreds of millions of instances where people who want to communicate via their phone cannot. Coverage blackspots persist to a greater and lesser extent the world over. We have a truly international solution. Bullitt Satellite Messenger provides total reassurance that you will have a connection wherever you have a clear view of the sky.

Citing data from Opensignal, Bullit said it’s solving “a real connectivity problem,” where around 60 million Americans lose coverage for up to 25% of each day. Bullitt Satellite Messenger promises to provide a signal wherever there’s a clear view of the sky, similar to the service Qualcomm announced this week with Iridium for Android devices.

The Bullitt service works by combining Bullitt smartphone hardware and an OTT app, Bullitt Satellite Messenger, to send messages to any smartphone. The service will first try to connect via Wi-Fi or cellular, and if neither are available, it will connect via satellite.

Quotes:

Resources:

https://www.fiercewireless.com/wireless/bullitt-taps-motorola-satellite-messaging-phone-launch

Qualcomm and Iridium launch Snapdragon Satellite for 2-Way Messaging on Android Premium Smartphones

Deutsche Telekom to deploy more small cells to solidify its 5G network

Deutsche Telekom plans to deploy more small cells to solidify its 5G network, the company said in a podcast. The carrier explained that small cells improve the quality of the network in areas of high density, such as train or bus stations, markets or shopping arcades.

In late December, Deutsche Telekom said it would repurpose approximately 3,000 old public payphones as 5G small cells by 2025. They will have a range of a few hundred meters and will serve city centres and pedestrian zones using the 3.6 GHz frequency band. Telekom said its 5G small cells serve a 200-metre radius.

Telekom already uses phone box small cells for LTE networks on the 2.6GHz frequency, but will start a 5G rollout using the 3.6GHz band in 2023, having completed a pilot phase.

Telekom stressed its enthusiasm for designs that “fit in with the urban landscape, either by standing out with a decorative design or by harmoniously blending into their surroundings”. The latest roll out of phone box small cells will see 5G connectivity with little to no visual impact on German streets.

Telekom has partnered with Swiss network equipment vendor Huber+Suhner on small cells since 2019, using them to densify its 4G network across a number of German cities. The Huber+Suhner kit is installed in existing street furniture — including phone boxes — operating over a range of frequencies from 1.7GHz to 4.2GHz. When the deal was signed, then-Chief Technology Officer Walter Goldenits said that small cells would form an “important component of our expansion strategy”. He added that the Swiss vendor’s equipment can be converted to support 5G networks “in a few easy steps” (Deutsche Telekomwatch, #87). With this latest phone box small-cell rollout, it appears that this option has not been taken.

5G small cell antennas. © Deutsche Telekom AG

Deutsche Telekom Technik, the operator’s German network deployment and management unit, has been trialling street-level 5G small-cell designs since at least 2019. Then, it highlighted “creative designs” to densify the network, including the use of antenna housings shaped like clocks and birds perching on lampposts.

References:

https://www.telekom.com/en/search-this-website?query=small+cells++

https://www.telekom.com/en/media/media-information/archive/5g-small-cell-antennas-579790