U.S. 4 big cloud companies lead world in hyperscale data centers and capacity

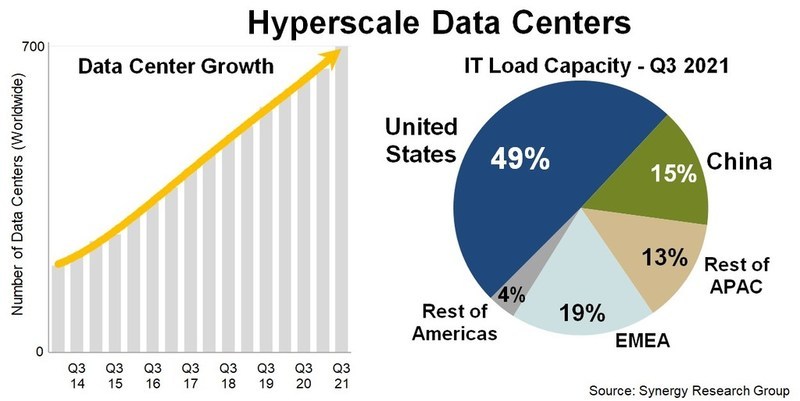

The U.S. continues to lead the world in total hyperscale data centers and worldwide capacity through at least 2026, according to Synergy Research Group. “The United States currently accounts for almost 40% of operational hyperscale data centers and half of all worldwide capacity,” John Dinsdale, chief analyst at Synergy Research Group, wrote in a new report. Synergy’s new hyperscale forecasts show continued rapid growth in the number of large data centers to be used by hyperscale operators in order to support their ever-expanding business operations.

With a current known pipeline of 314 future new hyperscale data centers, the installed base of operational data centers will pass the 1,000 mark in three years’ time and continue growing rapidly thereafter.

The United States currently accounts for almost 40% of operational hyperscale data centers and half of all worldwide capacity. By a wide margin, it is also the country with the most data centers in the future pipeline, followed by China, Ireland, India, Spain, Israel, Canada, Italy, Australia and the UK.

As the installed base of operational data centers continues to grow each year at double-digit percentage rates, the capacity of those data centers will grow even more rapidly as the average size increases and older facilities are expanded.

By data center capacity the leading companies are the usual suspects: Amazon, Microsoft, Google and Facebook, though it is the Chinese hyperscalers that are growing the fastest, most notably ByteDance, Alibaba and Tencent.

The companies that feature most heavily in the future new data center pipeline are Amazon, Microsoft, Facebook and Google. Each has 60 or more data center locations with at least three in each of the four regions – North America, APAC, EMEA and Latin America. Oracle, Alibaba and Tencent also have a notably broad data center presence.

“The future looks bright for hyperscale operators, with double-digit annual growth in total revenues supported in large part by cloud revenues that will be growing in the 20-30% per year range. This in turn will drive strong growth in capex generally and in data center spending specifically,” said John Dinsdale, a Chief Analyst at Synergy Research Group.

“While we see the geographic distribution, build-versus-lease distribution, average data center size and spending mix by data center component all continuing to evolve, we predict continued rapid growth throughout the hyperscale data center ecosystem. Companies who can successfully target that ecosystem with their product offerings have plenty of reasons for optimism.”

Synergy’s Hyperscale Market Tracker research service provides key data and metrics on 19 companies that meet Synergy’s hyperscale definition criteria. The data includes information on the hyperscale data center footprint, a full data center listing, analysis of critical IT load, future data center pipeline, hyperscale operator capex, hyperscale data center spending, company revenues, and five-year forecasts for the key metrics.

Synergy Research Group tracks the data center footprints and expansion plans of 19 of the world’s largest cloud and internet service companies, including the largest providers of infrastructure, platforms, software, search, social media, e-commerce, and gaming.

About Synergy Research Group:

Synergy provides quarterly market tracking and segmentation data on IT and Cloud related markets, including vendor revenues by segment and by region. Market shares and forecasts are provided via Synergy’s uniquely designed online database SIA ™, which enables easy access to complex data sets. Synergy’s Competitive Matrix ™ and CustomView ™ take this research capability one step further, enabling our clients to receive on-going quantitative market research that matches their internal, executive view of the market segments they compete in.

Synergy Research Group helps marketing and strategic decision makers around the world via its syndicated market research programs and custom consulting projects. For nearly two decades, Synergy has been a trusted source for quantitative research and market intelligence.

References:

Synergy Research: Hyperscale Operator Capex at New Record in Q3-2020

Synergy Research: Strong demand for Colocation with Equinix, Digital Realty and NTT top providers

Synergy Research: Ethernet Switch & Router revenues drop to 7 year low in Q1-2020

Synergy Research: Cloud Service Provider Rankings (See Comments for Details)

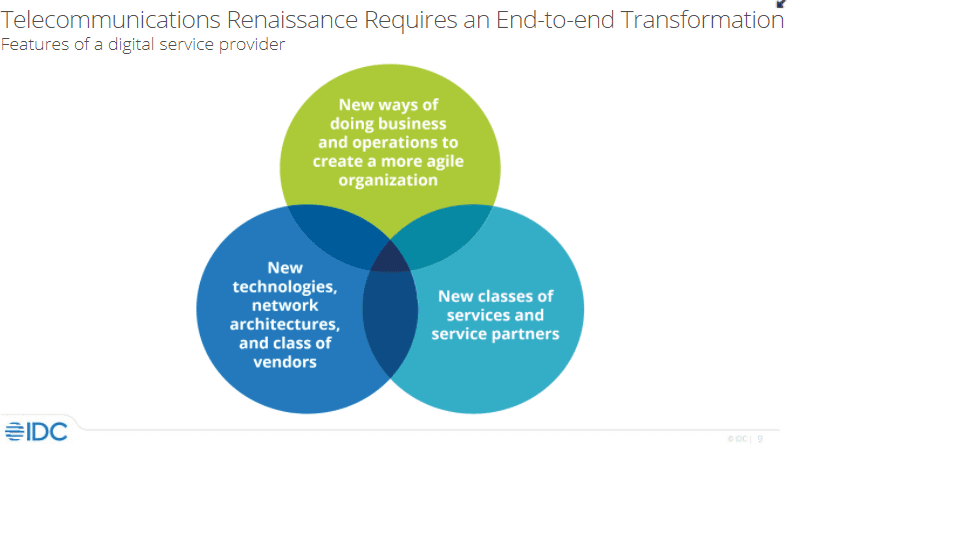

IDC Directions 2022: Telecom Renaissance, by Daryl Schooler

Selected Slides from Daryl Schooler virtual presentation at IDC Directions March 22, 2022, Santa Clara, CA:

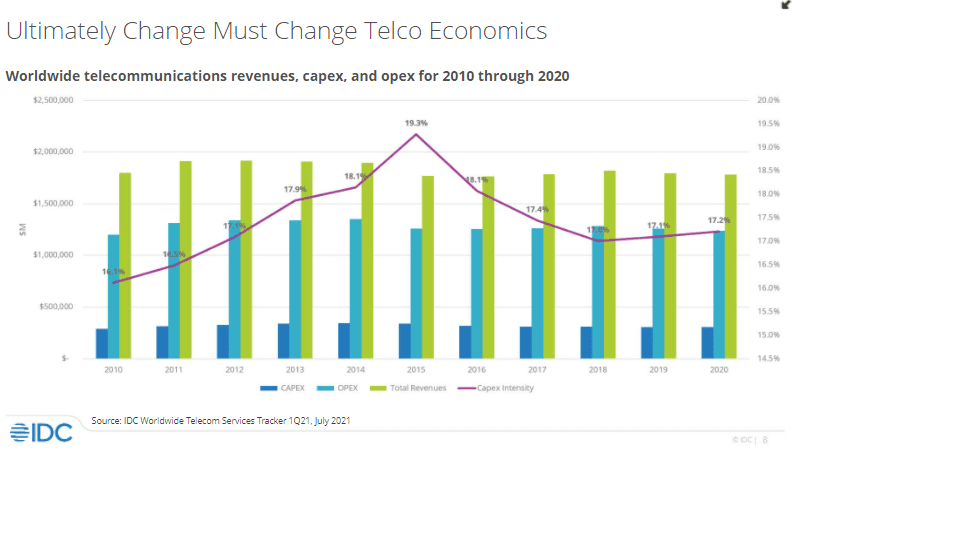

Flat telco revenues for over 10 years!

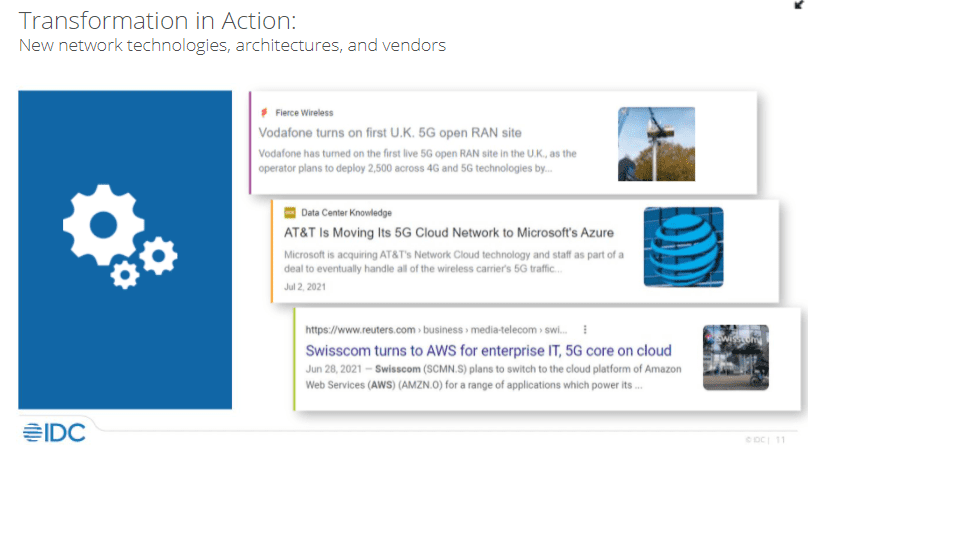

Microsoft is doing 5G SA core networ for AT&T, while AWS is doing 5G SA core for Swisscom (and Dish Network) as shown in this illustration:

Intelsat and PCCW Global combine networks; Intelsat achieves MEF 3.0 Carrier Ethernet (CE) Certification

Intelsat and PCCW Global Combine Networks:

Satellite communications specialist Intelsat and Hong Kong based PCCW Global have announced a new collaboration to extend the reach, resiliency, and quick delivery of on-demand enterprise connectivity offerings.

The integration of Intelsat’s FlexEnterprise global connectivity fabric with PCCW Global’s Console Connect Software Defined Interconnection® platform enables organizations to deliver enterprise connectivity to locations around the globe while leveraging an easy-to-use platform underpinned by one of the world’s largest private MPLS networks.

The combined solution addresses two key obstacles to delivering reliable, agile services across all of an enterprise’s locations: limited local telecom infrastructure that can challenge traditional network deployments in developing or hard-to-reach places, and lengthy lead times typically associated with creating high-performance networks and services. The collaboration brings together FlexEnterprise’s reach and reduced network deployment speed and Console Connect’s real-time quoting, ordering and provisioning of high-performance connectivity.

Mr. Frederick Chui, Chief Commercial Officer, PCCW Global, said, “The collaboration with Intelsat brings together the latest innovations in fixed network and satellite network technologies to deliver more flexible enterprise connectivity solutions. By integrating Intelsat’s FlexEnterprise solution with the Console Connect digital platform, our global customers can access satellite connected locations wherever they need to and effortlessly turn up services across all sites.”

FlexEnterprise leverages the world’s largest and most advanced integrated satellite fleet and ground infrastructure to enable service providers to integrate the reach and reliability of Intelsat services without the need to manage wholesale satellite capacity. The connectivity-as-a-service solution offers packaged service that makes it quicker and more cost-effective to add resiliency to existing sites and extend the reach of enterprise networks to even the most remote areas.

The Console Connect digital platform puts users in control of one of the world’s largest MPLS and Tier 1 IP networks, providing them with private, on-demand connections between over 750 data centres across more than 50 countries worldwide. Console Connect is home to a growing ecosystem of cloud, SaaS, IX, IoT, carrier and enterprise partners, which are directly interconnected by the platform’s private high-performance network, delivering higher levels of network performance, speed, and security. Through the platform’s MeetingPlace feature, users can also directly order and provision partner services, such as remote peering, colocation and business applications, as well as access native services from Console Connect.

Mr. Brian Jakins, General Manager and Vice President of Networks, Intelsat, said, “Our Sales and Product teams work closely with the telecom ecosystem to make satellite services more relevant and easier to adopt for a broader set of customers. With the integration into the Console Connect platform, Intelsat is able to more easily meet customers anywhere on the PCCW Global network, while enterprises leverage the platform to extend applications and services to their most remote users and outposts.”

Intelsat’s Global Network is First to Achieve MEF 3.0 Carrier Ethernet Certification for New Performance Tier:

Intelsat has become the first satellite operator to achieve MEF 3.0 Carrier Ethernet (CE) Certification for services delivered through its integrated space and global terrestrial network. Intelsat’s achievement means that customers can dependably integrate Intelsat’s global network solutions into their network solutions with assurance of performance and security. This also represents continued progress towards Intelsat’s Unified Network vision to enable seamless, end-to-end orchestrated services, driven by our integration of 5G and other open standards.

“Intelsat’s achievement of MEF 3.0 certification ensures that customers can rely on Intelsat to provide Ethernet services that meet the demands of enterprise, government and wholesale use cases with key performance indicators that define the industry standard for high-quality,” said Lance Hassan, Director of Terrestrial Network Innovation at Intelsat. “This achievement also demonstrates Intelsat’s leadership as a satellite communications company and global provider of network solutions.

MEF service definitions help telecom service providers accelerate product development and service implementations, with definitive measures to ensure consistency of the quality of the services they provide. As part of Intelsat’s continued efforts to drive open standards development and adoption across the satellite industry, the company worked with MEF member companies to amend MEF 23 with a new Performance Tier (PT5) that defines new Class of Service performance objectives for satellite-based networks.

“Intelsat, in achieving our industry’s first MEF 3.0 certification for GEO satellite-based Carrier Ethernet services, is adding a dimension to MEF’s important work that will benefit users no matter where they stand on the globe,” said Bob Mandeville, president and founder of Iometrix, MEF’s testing partner for carrier ethernet certifications.

“Companies in the satellite community are crucially important in enabling accessibility of carrier ethernet services anywhere on the planet,” said Kevin Vachon, chief operating officer, MEF. “Achieving MEF 3.0 certification facilitates interoperability with terrestrial networks and lays the groundwork to ultimately achieve service automation with MEF’s Lifecycle Service Orchestration (LSO) framework and APIs. We congratulate Intelsat on their certification achievements.”

Intelsat services are provided by the company’s integrated satellite and terrestrial network. For more information and to check availability, click here.

References:

India Data Center firms seek captive fiber for faster and more efficient connectivity

India data center providers have urged the government to allow them to lay their own captive fiber optic networks to offer faster and more efficient connectivity to companies. India’s current laws around fiber usage require data center operators to depend on telecom service providers for the fiber. That increases prices, makes the process time consuming and impacts ease of business, senior industry executives told ET.

–>The data center sector does not want to be governed by the same rules as telecom operators since it will become expensive and onerous to lay the fiber.

IT industry body Nasscom has also supported the data center industry’s demands through a recent submission to the Telecom Regulatory Authority of India (Trai). Nasscom has called for allowing data center companies to lay their own dark fiber between two or more data centers of the same company, to connect customers’ equipment located within such centers.

The biggest challenge affecting data center operations and services in India is around the telecom licenses to connect data centers that are not part of the same campus, Vimal Kaw, NTT’s head of data center services, told the Economic Times (ET).

“In India, telecom is regulated, and a license is required for data center providers to be able to create a network of connected data centers spanning across locations within a city or across cities. Thus, provisions need to be made by the Department of Telecommunication (DoT) and government in the current regulatory framework to enable data center providers to connect DCs using dark fiber to offer services to DC customers,” Kaw said. Typically, companies pay licensed telecom/internet service providers (TSPs/ISPs) on an annual contract basis.

TSPs, in turn, pay a share of their revenue to the government, irrespective of public or private use of the services. If data center businesses want to set up their own dark fiber networks, they will have to come to a similar revenue share arrangement under current laws, which companies say is not feasible for business-to-business networks.“

Sourcing fiber networks through ISPs/ TSPs can lead to exorbitant prices for data center providers, plus it is a time-consuming process. Meanwhile, getting an ISP license for captive usage is even more expensive. Acknowledging the specific need of the data center ecosystem can go a long way in enabling us to extend our services to newer regions,” said Piyush Somani, CEO of ESDS Software.

Nasscom told Trai that traditional networks operated by TSPs are principally designed for voice or public data services, not for cloud services, which require very high availability, bandwidth, and low latency for extremely high amounts of data.

India IT industry body Nasscom has also supported the data center industry’s demands through a recent submission to the Telecom Regulatory Authority of India (Trai).

………………………………………………………………………………………………………………………….

Data centers depend on captive dark fiber connectivity sourced from telecom operators to expand their presence, Ashish Aggarwal, head of policy, Nasscom told ET. But the process is time consuming and inefficient for the data center ecosystem. “Laying dark fiber is not a TSP activity in the traditional sense because it’s a captive network. For the benefit of ease of business, data centres should be allowed to lay their own fibre networks,” Aggarwal said.

Sunil Gupta, co-founder and CEO of Yotta Infrastructure, said the government can possibly set up a mechanism – either a mandatory obligation or subsidization/incentivization, or both — for this purpose.“ Additionally, data center operators should be allowed to lay their fiber optic cable and develop their own managed network to connect to other data centers, landing stations, and other key buildings of interest like stock exchanges,” he added.

Meanwhile, telecom operator Reliance Jio, in its submission to Trai has urged the regulator to only back fiber connectivity to data centers via licensed entities. Bharti Airtel has said that if right of way issues around fiber connectivity are resolved, the process can become more efficient.

References:

India’s 5G may lag due to low telecom infrastructure growth rate and insufficient fiber for backhaul

ICRA: Indian Telecom Industry Must Migrate from Copper to Dense Fiber Optic Networks

IBD – Controversy over 5G FWA: T-Mobile and Verizon are in; AT&T is out

Two of the three biggest U.S. telecom network providers, T-Mobile US and Verizon Communications, contend that selling 5G FWA (Fixed Wireless Access) broadband services to homes will prove to be a good business. However, AT&T has no plans to make a big push into that space. We wrote about this topic earlier this year, but it remains a conundrum as debate continues.

Whether these 5G FWA services will heat up broadband competition with cable TV companies — who dominate in high-speed internet services — is a controversial issue for telecom stocks. The fixed 5G wireless services also may compete with local phone companies in areas still served by copper line-based “DSL” services.

“Verizon and T-Mobile think the service can be a growth driver and will have attractive economics,” UBS analyst John Hodulik told Investor’s Business Daily (IBD). “FWA (fixed wireless access) is likely to do better where there are limited options for broadband and among subscribers used to lower speeds, so that means legacy DSL subscribers and slower speed cable. The big question is whether FWA has staying power over the next 5 to 10 years given necessary speed increases.”

AT&T has downplayed the potential of fixed 5G wireless. AT&T contends that as data usage surges over time, FWA will become increasingly uneconomic vs. fiber-optic landline alternatives.

“I think it stems from a genuinely different view of the engineering and capacity constraints,” MoffettNathanson analyst Craig Moffett told IBD. “The divergence in views about fixed wireless access between AT&T and Verizon or T-Mobile speaks to a genuine controversy in the telecom industry.” Craig added that telecom companies are scrambling to make money from huge investments in 5G radio spectrum.

Moffett said: “The renewed appetite for FWA may be a sign of a dawning realization that the gee-whizzy use cases of 5G may never materialize. That could be forcing operators to revisit every possible source of incremental revenue in a bid to earn at least some return on their huge investments in 5G spectrum.”

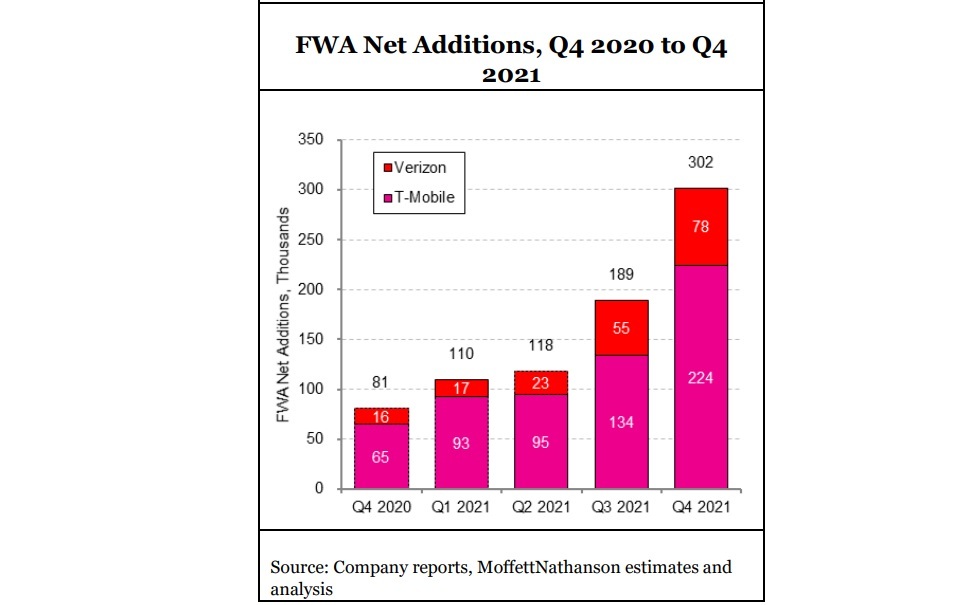

U.S. fixed wireless access (FWA market) captured ~ 38% share of broadband industry net adds in the fourth quarter of 2021. Approximately half of Verizon’s FWA customers are coming from commercial accounts, T-Mobile has indicated that about half its FWA customers are coming from former cable Internet subscribers. FWA’s strong Q4 showing left cable’s flow share at just 66%, about the same as cable’s share of installed US broadband households. “In other words, Cable likely neither gained nor lost share during the quarter, and instead merely treaded water,” Moffett noted. FWA “has gone from low-level background noise to suddenly a major force, with Verizon and T-Mobile alone capturing more than 300K FWA subscribers in the fourth quarter,” Craig noted. However, he isn’t sure that wireless network operators will allocate enough total bandwidth capacity for FWA to fully scale.

In a government auction that ended in early 2021, Verizon spent $45.45 billion on 5G “C-band” airwaves while T-Mobile invested $9.3 billion. AT&T spent $23.4 billion on the auction but it’s putting its 5G investments in areas other than FWA, like industrial 5G applications.

Meanwhile, there are cable TV firms looming with high-speed, coaxial cable. Comcast says it’s not worried about broadband competition from fixed 5G wireless services to homes.

“Time will tell, but it’s an inferior product,” Comcast Chief Executive Brian Roberts said at a recent Morgan Stanley conference. “And today, we can say we don’t feel much impact from (it). It’s lower speeds. And in the long run, I don’t know how viable the technology holds up.”

Cable companies offer hard landlines while 5G wireless services provide high-speed internet to homes mainly via indoor antennae that consumers self-install.

Eighty-seven percent of U.S. households subscribe to an internet service at home, compared with 83% in 2016, according to Leichtman Research Group. Also, cable TV firms comprise 70% of the broadband market, LRG said.

Verizon ended 2021 with 223,000 fixed wireless broadband customers, but most connected via 4G wireless networks. Meanwhile, T-Mobile had 646,000 fixed 5G broadband subscribers.

T-Mobile has told Wall Street analysts it expects to serve in a range of 7 million to 8 million fixed 5G wireless subscribers by 2025. Verizon has projected 3 million to 4 million subscribers over the same period.

T-Mobile charges $50 monthly for its home internet service. Verizon’s pricing starts at $50 or $70 monthly, depending on the data speeds provided. Verizon mobile phone customers with unlimited data plans get a discount.

T-Mobile’s 5G internet to home services provides data speeds up to 115 megabits per second, or Mbps. Verizon plans to provide speeds up to 300 Mbps.

T-Mobile uses mid-band radio spectrum to deliver fixed 5G broadband to homes. Verizon uses a mix of mid-band and high-band radio spectrum. In urban areas, Verizon may be able to deliver higher internet speeds with high-band spectrum, analysts say.

One area of debate remains whether fixed 5G broadband finds more success in suburban/urban markets or in rural areas.

“FWA is definitely a threat to cable companies,” Peter Rysavy, head of Rysavy Research, said in an email. “Particularly with (high frequency) mmWave, 5G can compete directly with cable. Mid-band spectrum is also effective but is best suited for lower density population areas. In these deployments, even T-Mobile limits the number of fixed wireless subscribers it can support in any geographical area.”

At UBS, Hodulik says that even if positioned as a low-end service, fixed 5G broadband still has a potential market of 20 million to 30 million homes.

AT&T, whose forerunner was regional Bell SBC Communications, has a sizable wireline local service area in 22 states. So it will face competition from fixed 5G broadband, just like cable TV firms. Verizon is based mainly in the northeast. T-Mobile doesn’t sell local phone services.

“AT&T has a huge wireline asset base that is only 25% upgraded to fiber,” Oppenheimer analyst Tim Horan told IBD. “So they are very exposed to competition from fixed wireless.”

At an analyst day on March 11, AT&T said it plans to upgrade 50% of its local markets, about 30 million customer locations, to high-speed fiber-optic broadband service by year-end 2025.

Meanwhile, AT&T CEO John Stankey commented on the controversy over FWA. AT&T sees FWA as playing a limited role for mobile small business and enterprise applications as well as in rural areas.

“We’re not opposed to fixed wireless, and I’m sure there’s going to be segments of the market where it’s going to be acceptable and folks are going to find it to be adequate right now,” Stankey said.

Fixed 5G broadband services to homes isn’t the only potential moneymaker for telecom network providers. Verizon, AT&T and T-Mobile aim to upgrade mobile phone users to unlimited data plans. They also plan to sell “private 5G” connections to businesses, Internet of Things (IoT) and 5G connections to industrial devices.

References:

Will 2022 be the year for 5G Fixed Wireless Access (FWA) or a conundrum for telcos?

MoffettNathanson: Robust broadband and FWA growth, but are we witnessing a fiber bubble?

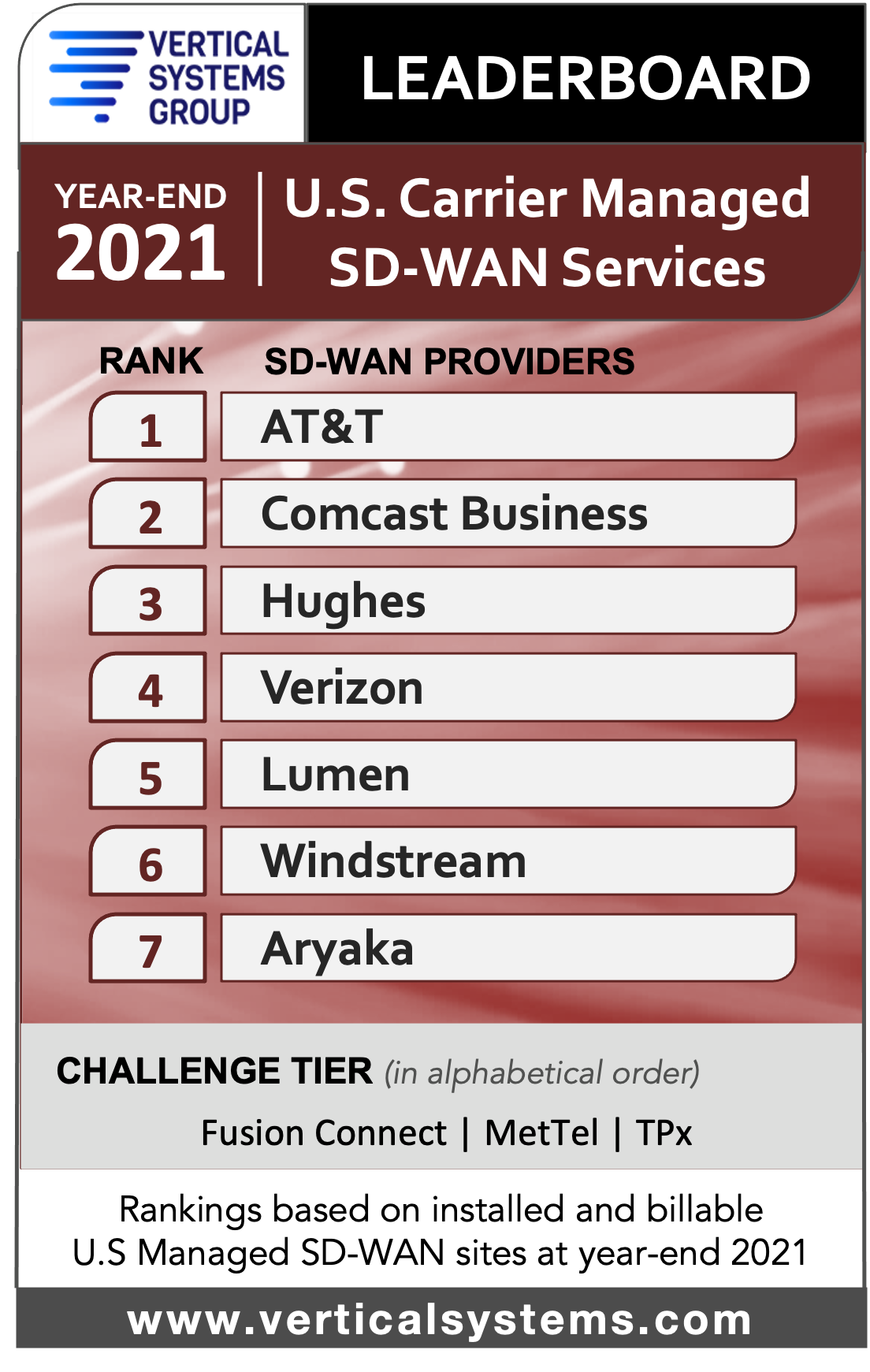

AT&T tops VSG’s U.S. Carrier Managed SD-WAN Leaderboard for 4th year

AT&T continues as the #1 U.S. Carrier Managed SD-WAN provider in 2021 for the fourth consecutive year, as per Vertical Systems Group’s annual SD-WAN Leaderboard. Seven service providers each have 2% or more of the installed and billable Carrier Managed SD-WAN customer sites in the U.S. as of December 31, 2021.

“The U.S. Managed SD-WAN services market emerged from the pandemic in 2021 with solid growth in new site installations, driven by accelerated network transformations and more flexible solutions for customers,” said Rick Malone, principal of Vertical Systems Group. “Competition is heating up as evidenced by the shake up in top provider rankings on our year-end 2021 U.S. LEADERBOARD benchmark.”

Comcast Business rose two places to the No. 2 position on the Leaderboard, bumping down Hughes and Verizon to third and fourth place, respectively. Vertical Systems Group (VSG) says that Comcast Business’s rise on the Leaderboard is due to “organic growth” plus sites added from the acquisition of Masergy.

Three companies attained a Challenge Tier citation for 2021 (in alphabetical order): Fusion Connect, MetTel and TPx. This tier includes service providers with between one percent 1% and 2% share of U.S. Carrier Managed SD-WAN sites.

Research Highlights:

- Rankings changed for five of the seven market leading providers on Vertical’s 2021 U.S. Carrier Managed SD-WAN LEADERBOARD based on latest site share results as compared to the previous year.

- AT&T retains first position overall for the fourth consecutive year.

- Comcast Business rises to second position, up from fourth in 2020 based on site share that includes organic growth plus sites added from its Masergy acquisition.

- Hughes moves to third position, from second overall in 2020. Verizon moves into fourth position, a change from third in the previous year.

- Lumen advances to rank fifth, up from sixth position. Windstream drops to sixth position from fifth in 2020. Aryaka retains seventh position and rounds out the roster of top providers for 2021.

- Additionally, TPx drops into the 2021 Challenge Tier from the Leaderboard.

- MEF 3.0 SD-WAN Service Certification has been attained by five of the 2021 U.S. LEADERBOARD companies: AT&T, Comcast Business, Verizon, Lumen and Windstream. Each of these providers also has employees with MEF SD-WAN Certified Professional training certification.

- Primary technology suppliers to the service providers ranked on the 2021 Carrier Managed SD-WAN LEADERBOARD include Cisco, Fortinet, Versa and VMware. Additionally, SD-WAN providers Aryaka and Hughes utilize internally developed technologies.

Market Players include providers selling Carrier Managed SD-WAN services in the U.S. with site share below 1%, including global network providers that manage U.S. customer sites. For 2021, the Market Player tier includes the following companies (in alphabetical order):

AireSpring, American Telesis, Arelion, Astound Business, Bigleaf, bSimplify, BT Global Services, C Spire Business, CentraCom, Cincinnati Bell, Cogent, Colt, Consolidated Communications, Cox, Crown Castle, DQE Communications, FirstLight, Frontier, Great Plains Communication, GTT, InfoStructure, Intelsat, Lightpath, Logix Fiber Networks, Meriplex, NTT, Orange Business, PCCW Global, PS Lightwave, SDN Communications, Segra, SES, SingTel, Sparklight Business, Spectrum Enterprise, Syringa, T-Mobile, T-Systems, Tata, Telefonica, Telstra, Transtelco, Unite Private Networks, Uniti, Veracity Networks, Virgin Media Business, Vodafone, Zayo and others.

Vertical’s Definition – Carrier Managed SD-WAN Service:

Vertical Systems Group defines a Carrier Managed SD-WAN Service for segment analysis and share calculations as a carrier-grade offering for business customers that is managed by a network operator. Required components and functionality for these offerings include an SDN service architecture that provides dynamic optimization of traffic flows, a purpose-built SD-WAN appliance or CPE-hosted SD-WAN VNF at each customer edge site, support for multiple active underlay connectivity services, automated failover fast enough to maintain active sessions, and centralized network orchestration with traffic and application visibility end-to-end. Security capabilities may be supplied by a managed SD-WAN service provider based on customer requirements.

Telstra to build 3 new teleports for OneWeb in Southern Hemisphere

Telstra is building and maintaining three new dedicated teleports across Australia to provide satellite gateway services for OneWeb in the Southern Hemisphere.

The first of the new teleports, located in Darwin Tivendale, is scheduled to begin installation this month with go-live planned in July. Two further sites – Charlton Toowoomba and Wangara, Perth, WA – are planned for completion later in 2022. Each facility will provide turnkey ground station support for OneWeb’s growing fleet of low-earth orbit (LEO) satellites. These facilities are being delivered as part of a 10-year deal between Telstra and OneWeb.

Telstra’s turnkey approach for OneWeb includes designing, building and activating the teleports with ground station capabilities to meet OneWeb’s requirements. Telstra will also provide 24/7 monitoring and quality assurance services at each location.

“OneWeb had exacting requirements from the outset, and we worked in close partnership with them from site selection through construction,” said Vish Vishwanathan, Vice President Wholesale & Satellite, Telstra Americas. “Teleports are complex sites involving access to secure and resilient infrastructure and on-the-ground expertise, which Telstra has provided to OneWeb throughout this project.”

A new teleport in Darwin, Australia, one of three satellite gateways built by Telstra under a 10-year deal with OneWeb to deliver global connectivity.

…………………………………………………………………………………………………………………

Telecom network providers typically own and operate significant terrestrial and subsea assets, including fiber networks, IP backbones and data centers. These resources provide the critical ground service required to support satellite operators’ growing constellations, reduce their costs of entry into new markets and minimize the need for personnel to maintain their own terrestrial infrastructures.

“Low Earth Orbit satellite technology is transforming the global connectivity landscape, not only by creating new business opportunities, but also giving more businesses, communities and governments the internet access they need for progress,” said Michele Franci, Chief of Delivery and Operations at OneWeb. “More connectivity options benefit everyone and our approach in establishing strategic partnerships with experienced providers like Telstra is core to how we deliver the OneWeb mission.”

OneWeb has 428 satellites in orbit, about two-thirds of its constellation. The satellite internet firm is providing coverage above the 50th parallel North – reaching areas that have historically been hard to connect with distributed communities and challenging terrain. This includes Alaska, Canada, and the wider Arctic Region. Earlier in March, OneWeb signed an MOU with Telstra to explore new connectivity solutions for Australia and the Asia pacific regions.

Earlier this month OneWeb and Telstra announced a memorandum of understanding to look at ways to improve digital connectivity for Telstra customers in Australia and the Asia Pacific region.

“We see lots of opportunities for our consumer, small business and enterprise customers using LEO satellite connectivity – from backhaul to back-up for resiliency, from internet of things to supporting emergency services, from home broadband to supporting agritech,” Andrew Penn, Telstra CEO said in a statement.

…………………………………………………………………………………………………………….

About Telstra:

Telstra is a leading telecommunications and technology company with a proudly Australian heritage and a longstanding, growing international business. We have been operating in the Americas for over 25 years and provide data and IP transit, internet connectivity, network application services such as unified communications and cloud, and managed services to over 500 businesses in 160 cities in the region. Our products and services are supported by one of the largest fiber optic submarine cable systems reaching Asia-Pacific and beyond, with licenses in Asia, Europe and the Americas, and access to more than 2,000 points-of-presence around the world. Through our unparalleled network reach and reliability as well as market-leading customer service and expertise, we connect businesses in the Americas to some of the world’s fastest growing economies, including China, Southeast Asia, North Asia, and Australia. For more information, please visit www.telstra.com/americas.

About OneWeb:

OneWeb is a global communications network powered from space, headquartered in London, enabling connectivity for governments, businesses, and communities. It is implementing a constellation of Low Earth Orbit satellites with a network of global gateway stations and a range of user terminals to provide an affordable, fast, high-bandwidth and low-latency communications service, connected to the IoT future and a pathway to 5G. More at http://www.oneweb.world

References:

https://spacenews.com/telstra-teleports-for-oneweb/

BT in new distribution partner agreement with OneWeb for LEO satellite connectivity

AT&T and OneWeb: Satellite Access for Business in Remote U.S. Areas

OneWeb Launches 36 LEO satellites, 254 in orbit, funding deals & UK coverage too!

Revitalized OneWeb challenges SpaceX/Starlink & Amazon/Kuiper for Broadband Satellite Service

USPTO: No clear winners in 5G patent filings; caution urged when reviewing claims of “5G dominance”

A report published in February 2022 examines which companies have filed for patents at the USPTO (US Patent and Trademark Office) in four technologies: Management of Local Wireless Resources, Multiple Use of Transmission Path, Radio Transmission Systems, and Information Error Detection or Error Correction in Transmission Systems. USPTO says that approach narrowed the focus to patent flings on technologies central to 5G innovation. The report concludes that there’s no clear lead to be seen: “The findings of the report call into question claims that any single firm or country is ‘winning’ the 5G technology race.“

Six companies topped the results, none with any notable lead. They were: Ericsson, Huawei, LG, Nokia, Qualcomm and Samsung. The report notes that while ZTE often is mentioned as a competitor to those six firms, it filed far fewer patents outside of China during the study period. The report authors did a textual analysis of the 22,000-plus patent filings studied to see if any of these competing firms stood out in particular attributes. Here, more subtle differences emerged.

Qualcomm’s patents had the most “legal breadth,” in the sense of making shorter (and therefore generally broader) claims about covered inventions; Ericsson and Nokia ranked higher for “radicalness,” meaning they cited less prior art as references; and Qualcomm and Samsung did well on “technical relevance,” or how often other patents cited their own patents or applications as prior-art references.

The USPTO report references a January 6, 2021 directive from the NTIA (National Telecommunications and Information Administration), the “National Strategy to Secure 5G Implementation Plan,” in which the NTIA sought “an informed understanding of the global competitiveness and economic vulnerabilities of United States 5G manufacturers and suppliers.”

This line from the USPTO report is significant: “Given the complexity of the results, caution is recommended when reviewing media claims of 5G dominance.”

………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Here’s Statista’s take on leading 5G patent holders (as of February 2021):

An IEEE Techblog post from March 2021 examined claims that Huawei and Samsung were the leaders in 5G SEPs (Standard Essential Patents). Earlier related IEEE Techblog posts are listed in the References.

Even though there is no definition of 6G (while 5G standards and frequency arrangements are woefully incomplete), an April 2021 report authored by the Chinese Patent Office states that China currently holds 35% of all 6G patents worldwide. The report urged China to “utilize its technological advantage in 5G to continue staying ahead.”

–>If you believe that, I’d like to sell you a 6G smart phone!

References:

https://www.uspto.gov/sites/default/files/documents/USPTO-5G-PatentActivityReport-Feb2022.pdf

https://www.lightreading.com/5g/uspto-study-everyones-winner-in-5g-patents/d/d-id/776174?

Huawei or Samsung: Leader in 5G declared Standard Essential Patents (SEPs)?

5G Specifications (3GPP), 5G Radio Standard (IMT 2020) and Standard Essential Patents

GreyB study: Huawei undisputed leader in 5G Standard Essential Patents (SEPs)

Wireless Logic’s Conexa network for global IoT has £2 million revenue target in 1st year

Global IoT connectivity platform provider Wireless Logic has launched a new carrier-grade mobile network called Conexa, built to provide connectivity for companies deploying IoT devices and applications worldwide. Will this one succeed while early leader Sigfox failed (and is now in bankruptcy)?

The new cellular network will provide a single SIM for global deployments, offering a range of connectivity solutions, network control and security services for regional, national and global IoT deployments. It offers single and multi-network options, and commercial models for low and high data use.

Conexa provides a suite of connectivity solutions, network control and security services for global, national and regional deployments and is built over an ecosystem of leading mobile network operators (MNOs). It provides single or multi-network options and commercial models suited to both low and high data use according to application type.

“Mobile networks, and the infrastructure around them, were largely developed before the IoT existed, at a time when only the voice and data needs of people needed to be met,” said Oliver Tucker, Co-Founder and CEO, Wireless Logic.

“The IoT has particular requirements and for it to continue to grow, innovate and thrive, companies need a simple way to deploy and manage their solutions. That requires specific on-SIM, on-device and core network IoT services which is why Conexa is built for the IoT and aggregates the world’s best 4G, 5G and LPWAN radio networks.”

“This network has been built for enterprise businesses and those looking to roll out a global IoT deployment. Wireless Logic’s revenue target in year one is £2 million with rapid growth thereafter ahead of industry CAGR.”

Conexa is GSMA-certified and designed to meet the procurement, manufacturing, and logistics challenges that IoT companies face, providing flexible and scalable implementation, integration and day-to-day operation.

Advanced on-SIM applications, distributed networking, real time controls and cloud integration simplify deployments. Unique on-SIM control functions detect and initiate fail-over, as required, to alternative radio and core network infrastructure to protect mission critical applications.

Conexa enables robust, secure and scalable IoT solutions through:

- Global coverage with a range of local connectivity solutions in key G20 markets and beyond, compliant with permanent roaming and data sovereignty regulations

- Always-on connectivity through a dual redundant core network with automatic failover to ensure high-availability needs can be met

- Tailored connectivity solutions according to lifecycle stages, from factory to field, with advanced remote provisioning of eSIM, iSIM and multi-IMSI SIMs, which also help take cost and complexity out of procurement, manufacturing and distribution processes through single product stock keeping units

- Enhanced flexibility and resilience from on-SIM technologies and rules-based remote SIM provisioning

- Security which can be enhanced through on-SIM security applications and network protection features including IMEI locking, white or blacklisting, and private APN and VPN

- SIMPro, an industry leading management platform for SIM and device management, diagnostics and intelligence that provide insight and control of deployments.

“We designed Conexa with flexibility, scalability and usability in mind – as these are fundamental requirements for IoT managers and device manufacturers. For the IoT to continue to grow, innovate and thrive, companies need a simpler way to deploy and manage their solutions. Conexa has been designed to do just that,” Tucker added.

References:

Google’s Equiano cable system will span the west coast of Africa

First announced in 2019, the Equiano system is the third international submarine cable to be owned by Google and their fourteenth submarine cable investment in total. The Equiano cable system is expected to be ready for service by the end of this year.

It is named after Olaudah Equiano, an 18th century writer and abolitionist originally from what is now Nigeria. Enslaved as a child, Equiano purchased his freedom in 1766 and went on to play a major role in the British anti-slave trade movement of the 1780s.

The cable is set to span the West Coast of Africa, travelling from Lisbon, Portugal, down to Cape Town, South Africa, offering a myriad of branching opportunities to neighbouring African countries on the way. Branches already planned include those to Nigeria, St. Helena, Democratic Republic of the Congo, and Namibia, with many more likely to be announced later this year. Please see illustration below.

When previously announced, the system’s first African landing was expected to be at Lagos, Nigeria, but discussions between Google and the Togolese government – particularly surrounding the latter’s Togo Digital 2025 strategy, which aims to make the nation a regional digital hub – saw Togo’s capital Lome jump the queue.

Togo’s minister for digital economy and digital transformation, said her government successfully made the case to Google that it should be Togo instead.

“Togo, which was not on the list of beneficiary countries of the first cohort, was integrated after several months of negotiations and it becomes the first African country to host the cable,” said the Togolese Minister of Digital Economy and Digital Transformation, Cina Lawson.

“As Togo continues to earn its place on the regional and international stage as a digital hub and a favorable ecosystem for innovation and investment, our collaboration with Google and CSquared in successfully landing Equiano further demonstrates Togo’s commitment to enhancing public and social services for all citizens so that they can benefit economically.”

Lome is already a host to two submarine cable systems: the West Africa Cable System (WACS), which spans a similar route to Equiano but continues north to London, UK, and the shorter Maroc Telecom West Africa cable, which travels from Casablanca, Morocco, down to Libreville, Gabon.

The Equiano cable system will be maintained and operated by CSquared Woezon, a joint venture of open access wholesale broadband infrastructure company CSquared and the Société d’infrastructures numériques (SIN), a sovereign entity responsible for holding strategic assets in the telecommunications and ICT sector in Togo. The joint venture, in which CSquared holds a 56% stake, will also manage the related e-Government and Communauté Electrique du Bénin (CEB) terrestrial fibre networks in Togo.

According to Google, the cable system, which comprises 12 fiber pairs and a design capacity of 150 Tbps, should create roughly 37,000 jobs in Togo between 2022 and 2025, as well as boosting the nation’s GDP by $193 million.

References:

https://qz.com/africa/2143897/googles-equiano-cable-is-making-its-first-landing-in-togo/