FTC Staff Report Finds Many ISPs Collect Troves of Personal Data while Consumers Have No Options

The Federal Trade Commission (FTC) staff report released on Thursday, October 21st found that a group of broadband Internet Service Providers (ISPs), including AT&T, Charter Communications, Comcast and Verizon, collect troves of personal data, and that consumers don’t have much choice on how that data is used.

Question to Ponder: Haven’t we all intuitively known that, just like Big Tech (Amazon, Google, Facebook, Apple, Microsoft) our privacy has been compromised by ISPs in return for “free services,” whereby our personal information is sold to “target advertisers?”

The report was approved unanimously 4-1 by the commission, with FTC chair Lina Khan issuing a separate statement. Khan said the FTC report highlighted:

1) Problems with the notice-and-consent framework for data collection and sharing;

2) The expansion of ISPs into vertically integrated businesses including ones providing content for their broadband “pipes”; and

3) The potential use of “hyper-granular” online dossiers to discriminate against users.

Many ISPs collect and share far more data about their customers than many consumers may expect—including access to all of their Internet traffic and real-time location data—while failing to offer consumers meaningful choices about how this data can be used, according to an FTC staff report on ISPs’ data collection and use practices.

The staff report, which details the expanding scope and some troubling aspects of some ISP data collection practices, stems from orders the FTC issued in 2019 using its authority under 6(b) of the FTC Act to six internet service providers, which make up about 98 percent of the mobile Internet market:

- AT&T Mobility LLC;

- Cellco Partnership, which does business as Verizon Wireless;

- Charter Communications Operating LLC;

- Comcast Cable Communications, which does business as Xfinity;

- T-Mobile US Inc.; and

- Google Fiber Inc.

The FTC also issued orders to three advertising entities affiliated with these ISPs: AT&T’s Appnexus Inc., rebranded as Xandr; Verizon’s Verizon Online LLC; and Oath Americas Inc., rebranded as Verizon Media. The FTC sought information on their data collection and use practices, as well as any tools provided to consumers to control these practices.

As noted in the report, these companies have evolved into technology giants who offer not just internet services but also provide a range of other services including voice, content, smart devices, advertising, and analytics—which has increased the volume of information they are capable of collecting about their customers. The report identified several troubling data collection practices among several of the ISPs, including that they combine data across product lines; combine personal, app usage, and web browsing data to target ads; place consumers into sensitive categories such as by race and sexual orientation; and share real-time location data with third-parties.

At the same time, the report found the privacy protections many of the companies offer raised several concerns. Even though several of the ISPs promise not to sell consumers personal data, they allow it to be used, transferred, and monetized by others and hide disclosures about such practices in fine print of their privacy policies. For example, several news outlets noted that subscribers’ real-time location data shared with third-party customers was being accessed by car salesmen, property managers, bail bondsmen, bounty hunters, and others without reasonable protections or consumers’ knowledge and consent, according to the report.

Many of the ISPs also claim to offer consumers choices about how their data is used and allow them to access such data. The FTC found, however, that many of these companies often make it difficult for consumers to exercise such choices and sometimes even nudge them to share even more information. In addition, while several of the ISPs promise to only keep the data for as long as needed for business purposes, the definition of what constitutes a “business purpose” varies widely among the companies.

The FTC report also found that ISPs use web browsing data and group consumers using “sensitive characteristics such as race and sexual orientation.”

The report concludes that many of the ISPs’ data collection and use practices mirror problems identified in other industries and underscore the importance of restricting data collection and use.

The Commission voted 4-0 to approve and issue the report. Staff presented findings from the report at today’s open virtual Commission meeting. Chair Lina M. Khan issued a separate statementon the report.

Cable Industry Response from the NCTA:

The report drew a sharp rebuke from the cable industry (as represented by the NCTA — The Internet & Television Association), maintaining that it provided a “highly distorted view” that casts them in the same arena as aggressive “Big Tech platforms” which are well known to compromise users privacy via data collected and sold to advertisers.

The NCTA said in a October 21st statement:

The FTC’s report provides a highly distorted view of ISP data collection policies and inappropriately attempts to lump broadband providers into the same category as the Big Tech platforms.

Cable broadband providers take seriously their responsibility to safeguard the personal information of their customers and do not surveil their customers or sell their location data. Viewed objectively, today’s presentation is a broad attack on online advertising generally, not specific ISP actions. And what is further missing from today’s report is the much larger story about Big Tech platforms that are premised on maximizing user attention.

What is needed is a consistent set of privacy rules across the online marketplace on a technology-neutral basis. We look forward to continued engagement with policymakers to forge a strong, consistent framework for privacy protection.

–>What will come of the FTC staff report is not entirely clear. FTC chair Lina Khan said it would be part of an “ongoing conversation” about privacy and data practices that could be “incorporated” into FTC action, according to Multichannel News.

…………………………………………………………………………………………………………………………………………………….

FTC Boilerplate Text:

The Federal Trade Commission works to promote competition and to protect and educate consumers. You can learn more about consumer topics and file a consumer complaint online or by calling 1-877-FTC-HELP (382-4357). For the latest news and resources, follow the FTC on social media, subscribe to press releases and read our blogs.

…………………………………………………………………………………………………………………………………………………….

Separately, Politico reported that tech and telecom companies were among the top 20 spenders for the third quarter of 2021, according to a ranking of lobbying expenditures compiled by POLITICO Influence. Facebook was No. 5 at $5.1 million, with Amazon right behind it with $4.7 million. NCTA — The Internet & Television Association ranked 15th, spending $3.3 million, and Comcast was 18th, with $3.1 million.

CCS Insights: 5G connections will triple this year to 637M, then to 1.34B in 2022

5G connections (is that the same as 5G subscribers?) will reach well over 1 billion next year, despite the threat of component shortages hitting the supply chain this Christmas, according to a new forecast by CCS Insights. Total 5G connections will triple this year to 637 million, before more than doubling in 2022 to 1.34 billion, CCS Insight predicts. The market research firm says that China will continue to lead in volume terms, at least for the next few years.

Smartphones with 5G capability have until now largely remained sheltered from component shortages affecting the global mobile phone market.

“In another turbulent year for the mobile phone market, supply constraints in low- to mid-tier segments, paired with weak demand in emerging markets, have dampened sales. But 5G-enabled devices have so far continued to find their way to the hands of people in the world’s most advanced markets, with 560 million 5G-capable smartphones projected to sell in 2021”, notes Marina Koytcheva, vice president of forecasting at CCS Insight. But concerns about the supply of high-end devices, including the iPhone, during the Christmas quarter remain and pose a risk to adoption of 5G, even if that risk is temporary.

Telecom operators in Western Europe, North America, China and other advanced markets in Asia continue to roll out 5G networks, overcoming difficulties posed by the Covid-19 pandemic, uncertainties about the role of Chinese network equipment-maker Huawei, and an unstable macroeconomic environment.

In South Korea, 5G is on track to account for 30% of mobile connections by the end of 2021. Strong mobile phone sales in the run-up to Christmas will help the US achieve 25% penetration, surpassing the Chinese market. Although China was an early trailblazer for 5G, shaky demand for smartphones in 2021 means that 5G is forecast to account for only 24% of cellular device connections by the end of the year.

In contrast, Western Europe is still lagging some other markets, limited by delayed spectrum auctions in some countries, slow government decision-making about the role of Huawei, and weakened demand for mobile phones amid the pandemic. Although the speed of 5G roll-out is improving, this relatively gradual start means that 5G won’t account for more than half of cellular device connections in the region until 2024.

Once the spectrum is allocated and telecom operators start deploying 5G networks, how quickly people adopt 5G depends on their willingness to buy 5G-capable devices. “Things are looking up on that front; the global mobile phone market is projected to recover in 2022, and prices of 5G handsets continue to fall steadily. Our forecast for 3.6 billion 5G connections worldwide by 2025 is still firmly on track,” says Koytcheva.

In addition to mobile phones and related devices such as tablets, CCS Insight has identified two other drivers for 5G adoption: industrial cellular Internet of things devices and fixed wireless access (we agree). Both have strong prospects, despite being projected to contribute only 9% of worldwide 5G connections in 2025. Adoption of 5G in industrial applications is seeing positive momentum in China, and is set to get a boost in the US when carriers start switching off their legacy 3G networks.

Fixed wireless access remains a niche technology for now, mostly complementing fibre broadband, but some network operators are increasingly turning their attention to this opportunity with business users, recognizing that the potential revenue per connection could be significantly higher than that from connecting households.

A summary of CCS Insight’s new forecast for 5G connections is presented in the chart below:

Source: CCS Insights

……………………………………………………………………………………………………………………………………………..

The publication of nine-month 5G subscriber numbers from two of China’s three mobile operators is quite revealing (if true?).

- China Mobile is adding 5G customers at a rate of around 11 million per month according to its latest financial report. The world’s biggest mobile operator had 160 million 5G network subscribers at the end of September, up from 127 million three months earlier.

- China Telecom, which is due to report on Friday, had 146.6 million 5G package customers at the end of August. A “back of the envelope” calculation by Mary Lennighan of telecoms.com suggests there are more than a quarter of a billion true 5G subscribers in China.

![]()

CCS Insight predicts that the U.S. will leap ahead of China in 5G on the back of strong smartphone sales in the run-up to Christmas, giving it 25% 5G penetration to China’s 24%, the latter hit by shaky demand for smartphones this year as noted above.

References:

https://telecoms.com/511861/global-5g-connections-set-to-break-the-billion-mark-next-year/

https://telecoms.com/511854/china-mobile-is-adding-11-million-real-5g-users-per-month/

More details of CCS Insight’s extensive 5G service can be found at: https://www.ccsinsight.com/research-areas/5g-networks

AT&T earnings, mobility and consumer broadband grow; stiff competition lies ahead

AT&T today reported a net profit of $5.9 billion in the third quarter, up from $2.8 billion a year ago. Adjusted EPS, excluding the one-time effects of the divestments, reached $0.87 versus $0.76 a year earlier. The company now expects full-year adjusted EPS to be at the high end of the earlier indicated low- to mid-single digit growth range and free cash flow should meet the $26 billion target.

AT&T said it was on track to meet its full-year targets. Revenues for the three months to September were still down 5.7 percent year-on-year to $39.9 billion due to the spin-off its pay-TV business in July, along with other divestments and weaker sales in Business Wireline.

Source: AT&T

…………………………………………………………………………………………………………………………………….

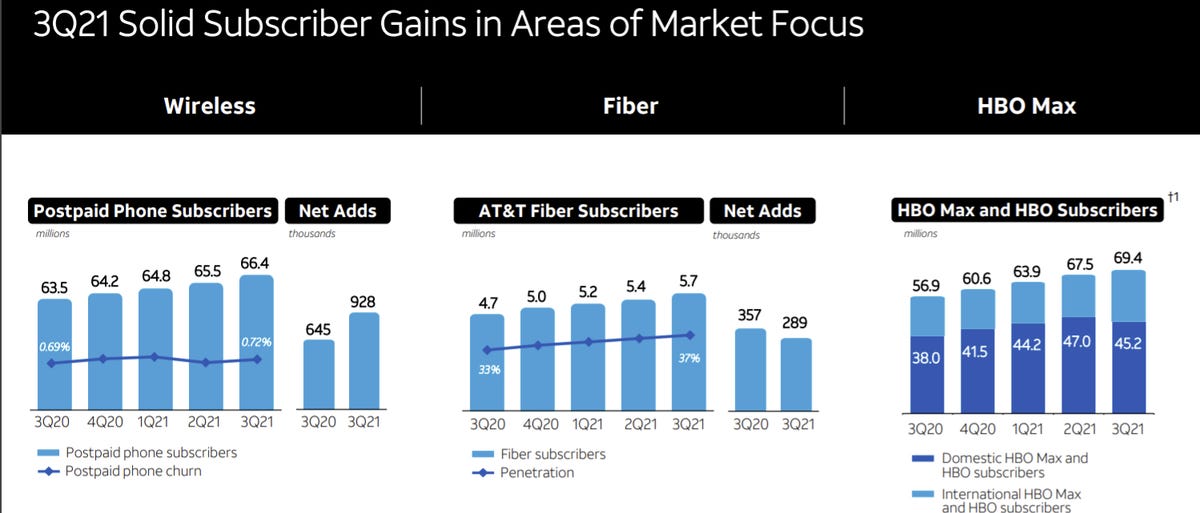

Mobility is AT&T’s largest and most important business, accounting for 48% of consolidated

revenues, and more than two thirds of pro-forma revenues post divestitures. The company’s mobile business did quite well in the third quarter, adding over 1 million postpaid lines. AT&T has now added 4.4 million wireless postpaid subscribers over the past four quarters. Jeff McElfresh, Chief Executive Officer, AT&T Communications said on today’s earnings call (see analyst Craig Moffett’s comments below):

Our (wireless) strategy is working here at AT&T. As we’ve demonstrated, it’s the fifth consecutive quarter where we have driven some momentum and gaining (market) share. Our net add strength here in the quarter at 928,000, that compares to what we had produced back in 2019 in the third quarter of 101,000. And we’re driving strong service revenue growth. And we just posted the largest total EBITDA that we’ve generated out of the wireless business segment. The best part about it, Phil, is that our customers are telling us that we’re doing a good job. These churn levels that are low are a signal to the service and the value that we’re offering and our NPS feedback that we’ve received is the highest that we’ve ever received.

I’d also point to things like our FirstNet program. We’re starting to reach some scale here. Third quarter, we posted the highest net add quarter since launching the program and we’ve arrived at a position of leadership and strength in the law enforcement segment under the public safety sector. And so all in all, it’s been the operational changes that we’ve made at AT&T that has driven really strong momentum in our customer counts.

For comparison, arch rival Verizon added a net 699,000 postpaid subscribers including 429,000 postpaid phones in the third quarter. T-Mobile US will report third quarter results on November 2nd after the stock market closes.

HBO subscribers grew to nearly 70 million by the end of the quarter. Excluding its U.S. video business (to be spun off and merged with Discovery (DISCA) by the middle of next year), revenues rose to $38.1 billion from $36.4 billion in the year-ago quarter, and adjusted operating improved to $8.1 billion from $7.8 billion.

“We continue to execute well in growing customer relationships, and we’re on track to meet our guidance for the year,” said John Stankey, AT&T CEO. “We had our best postpaid phone net add quarter in more than 10 years, our fiber broadband net adds increased sequentially, and HBO Max global subscribers neared 70 million. We also have clear line of sight on reaching the halfway mark by the end of the year of our $6 billion cost-savings goal.”

Third-quarter revenues were $28.2 billion, up 3.8% year over year due to increases in Mobility and Consumer Wireline more than offsetting a decline in Business Wireline. Operating contribution was $7.1 billion, up 0.8% year over year, with operating income margin of 25.2%, compared to 26.0% in the year-ago quarter.

Highlights of AT&T’s Consumer Wireline business:

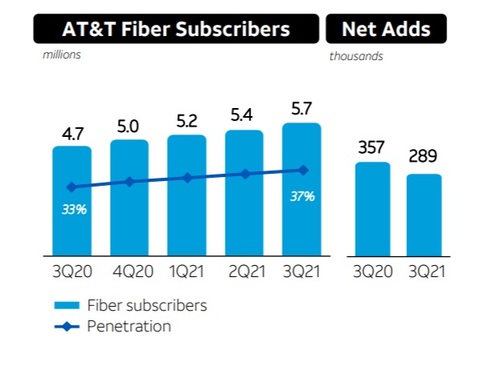

- 289,000 AT&T Fiber net adds; penetration about 37%

- Revenues up 3.4%; broadband revenues up 7.6% with ARPU growth of 5.2%

Growth in fiber broadband is an important part of AT&T’s new strategy, with billions of dollars of capital investment planned to expand its network and win new customers. In the third quarter, broadband internet subscriber growth was underwhelming. The company added a net 5,700 broadband customers, versus the consensus of 52,000. That includes a smaller-than-expected 289,000 fiber adds and a larger-than-expected loss of 261,000 DSL customers. Yet AT&T CFO Pascal Desroches said on today’s earnings call:

Our Fiber growth was solid. We had our highest Fiber gross adds ever and we continue to win share wherever we have Fiber. We added 289,000 Fiber customers in the quarter, and more than 70% of the Fiber net adds are new AT&T broadband customers and this gives us great confidence as we continue to build out our Fiber footprint.

CEO Stankey added a bit more color by saying:

We’re on this path to substantially increase our Fiber footprint and that stretches across both our consumer and our business base. And I think as you’ve known from past history, this is — it’s not uncommon for us to go through these ramps of infrastructure builds. We’ve done that many times before. We’ve recently been through one where we went through a multi-year ramp on fiber builds that we kind of started executing around the 2015 timeframe. They always, as you move through the front end of them, have a few moments where they’re a little bit lumpy and a little bit rocky because that’s the nature of it.

Source: AT&T

…………………………………………………………………………………………………………………………………………..

AT&T said it cut operating expenses by $3.4 billion in the past 12 months, to $32.8 billion. Divestments and lower sports programming costs were offset by higher wireless equipment costs and higher costs for other types of content at WarnerMedia, plus increased sales and marketing expenses. Operating profit was helped also by lower depreciation and amortization following earlier asset write-downs.

Earnings report summary:

- AT&T added 1,218,000 postpaid wireless net additions in the third quarter as well as 249,000 prepaid phone ads and 928,000 postpaid phone net ads.

- AT&T’s mobility unit reported revenue growth of 7% in the third quarter to $19.1 billion and operating income of $6 billion.

- AT&T’s equipment revenue was $4.6 billion, up 15%, due to strong smartphone sales.

- AT&T Fiber added 289,000 net customers and broadband revenue was up 7.6% in the third quarter from a year ago.

- WarnerMedia revenue in the third quarter was $8.4 billion, up 14.2% from a year ago.

“AT&T lays claim to the most hated stock and the most maligned management team in our universe,” wrote New Street analyst Jonathan Chaplin after AT&T’s earnings report on Thursday morning. “…We continue to expect AT&T to struggle as T-Mobile and cable rise. That certainly doesn’t seem to have happened this quarter though, with exceptionally strong net adds in wireless; however, it’s unclear how much credit investors will give AT&T for the newfound resilience in its wireless business, at least in light of everything else.”

With respect to AT&T’s carrier competitors, analyst Craig Moffett wrote in note to clients:

In Wireless, competitor T-Mobile has staked out the rather unusual dual position of lowest cost AND best network. TMobile is expanding its footprint, retail presence, and market share in rural America, and it is targeting market share gains in business wireless. Verizon is planning a march “up the stack,” with a focus on mobile edge compute in the 5G enterprise market. Verizon’s network strategy, somewhat quixotically we would argue, still has a large component of millimeter wave ultra-wideband. But, as a backup, Verizon has amassed a huge trove of C-Band spectrum, and they claim the industry’s densest network.

As we inch toward the finish line of the 3.45 GHz spectrum auction, we will probably learn that AT&T has narrowed, but not fully closed, their spectrum gap versus Verizon (but not T-Mobile). What will its network strategy be? In Business Wireline, it is the nation’s largest incumbent, facing declining share and eroding pricing. What will its Business Wireline strategy be?

………………………………………………………………………………………………………………………………………………….

On October 11th, AT&T awarded a 5 year contract to Ericsson in order to accelerate the expansion of AT&T’s 5G network. This deal helps support deployment of the service provider’s recently acquired C-band spectrum and the launch of 5G Standalone (SA) (which has been outsourced to Microsoft Azure).

Ericsson will help AT&T to bring its 5G network to more consumers, businesses and first responders across key industries – including 5G use cases in sports and venues, entertainment, travel and transportation, business transformation and public safety. AT&T’s network evolution is made possible in part by the Ericsson Radio System portfolio, which includes the Advanced Antenna System (AAS), Advanced RAN Coordination and Carrier Aggregation technologies.

The deployments will support future network enhancements like Cloud RAN, which offers communications services providers increased flexibility, faster delivery of services and greater scalability in networks. The platform supports a centralized RAN architecture enabled by Ericsson Fronthaul Gateway, a new technology that will enable a more efficient transport of the fronthaul interface by converting it to packet (eCPRI).

References:

https://about.att.com/story/2021/q3_earnings.html

https://investors.att.com/financial-reports/quarterly-earnings/2021

Verizon broadband – a combination of FWA and Fios (but not so much pay TV)

Verizon today announced its earnings for the third quarter of 2021, with the company posting net income of $6.6 billion, operating revenue of $32.9 billion, and $1.55 in earnings per share. Verizon now expects total wireless service revenue growth of around 4%, an increase to prior guidance of 3.5% to 4%. It’s earnings guidance was also revised upwards. Verizon adjusted earnings per share of $5.35 to $5.40 is now forecast for the current quarter – an increase from its prior guidance of $5.25 to $5.35.

“We had a strong third quarter, delivering on our strategy and growing in multiple areas,” Verizon Chairman and CEO Hans Vestberg said in the earnings release. “Our disciplined strategy execution demonstrated growth in 5G adoption, broadband subscribers and business applications. We are increasing our 2021 guidance, and we continue to expand our 4G LTE and 5G network leadership. We fully expect to have a strong finish to the year as we accelerate deployment of 5G to our customers across the country,” he added.

“Verizon reported another quarter of strong financial and operating performance,” Verizon Chief Financial Officer Matt Ellis said in the press release. “We are seeing strong demand for connectivity across our Consumer and Business segments as our Mix and Match and Business Unlimited value propositions, network quality and unique partnerships are resonating with both new and existing customers. We grew revenue in the quarter, achieved solid cash flow, completed the sale of Verizon Media and increased the dividend for a 15th consecutive year.”

The #1 wireless telco in the U.S. lost 68,000 net video subscribers from its Fios (FTTH/FTTP) service in the third quarter. “The telecom giant has been shifting its video focus away from Fios TV to partnerships with third-party streaming services as it positions itself as a key distribution platform for them. For example, Verizon has a deal with The Walt Disney Co. for the Disney bundle, which gives customers with select Verizon wireless unlimited plans access to Disney streaming services Disney+, Hulu and ESPN+,” said the Hollywood Reporter.

During the quarter, Verizon sold off its Verizon Media unit, which consisted of formerly dominant tech brands like AOL and Yahoo. The unit was acquired by Apollo Global Management, although Verizon continues to hold a 10 percent stake.

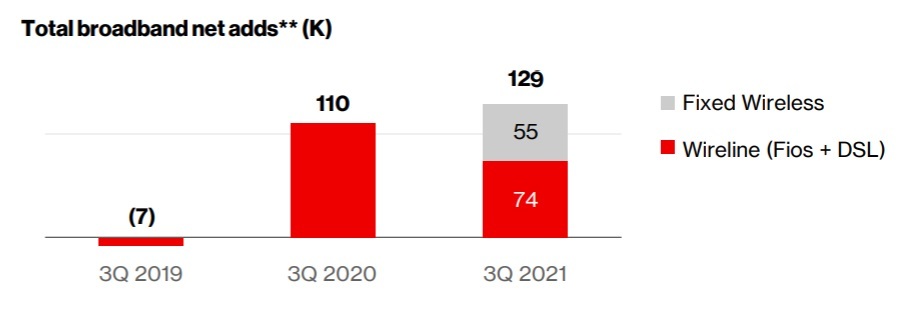

Verizon reported 129,000 broadband net additions in the third quarter, comprised of Fios, DSL and FWA subscribers, during the quarter. Of those, there were 55,000 Fixed Wireless Access (FWA) subscriber adds , which was about 42% of the 129,000 total broadband net adds generated in the quarter. Verizon FWA has a total of ~150,000 subscribers.

Source: Verizon Infographic from 3Q 2021 Earnings Report

Verizon CEO Hans Vestberg said during the earnings call, “We’re on track to meet our fixed wireless access household coverage targets with an expected 15 million homes passed by the end of the year between 4G and 5G. To date, 5G Home is in 57 markets and 4G LTE Home is in over 200 markets across all 50 states.”

Verizon first began offering 4G LTE Home in July 2020 and has really accelerated its rollout. The company has also rolled out 5G Home. Verizon executives on today’s earnings call noted that the FWA subscriber base is a mix of customers getting service from its 4G/LTE network and via Verizon’s 5G millimeter wave (mmWave) network. The company’s FWA base currently is a mix of residential and business customers, but did not break out that ratio. But they did note that there’s about a rough 50/50 split between FWA customers that are coming from Verizon’s existing base and from other service providers. CFO Matt Ellis said Verizon’s FWA customers aren’t solely focused on rural areas, as Verizon is also seeing “good traction” with the product in urban and suburban areas.

Verizon now seems to favor FWA over Fios, probably because of significantly lower installation costs for the former. Yet the company is not giving up on Fios. “In addition to fixed wireless access, we’re pleased with the great performance of Fios and continue to grow the open-for-sale volumes within our footprint.”

Indeed, Fios Internet net adds were 104,000 in the quarter. The telco is increasing its Fios footprint, adding over 400,000 open-for-sale locations this year. One analyst noted that Verizon hasn’t talked about increasing its Fios brand within its ILEC for quite some time.

Chief Financial Officer Matt Ellis said, “On the Fios expansion, we see great opportunity. We have been investing in that for a number of years; maybe haven’t spoken about it quite as much. But it continues to be a very good growth driver for the business.”

The company reported that Fios revenue of $3.2 billion in the quarter was up 4.7% year over year, driven by continued growth in customers as well as Verizon’s effort to increase the value of each customer by encouraging them to step up in speed tiers.

“We remain focused on bringing in high-quality net adds,” said Elllis. “The mix and match pricing structure for both wireless and Fios provides opportunity to migrate customers to higher value tiers and bring in customers on higher value plans. Our strategy is focused on increasing the value we receive from every connection.”

Vestberg said, “Our strategy is becoming a national broadband provider with the best access to the tech for our customers, including Fios, fixed wireless access on 5G, on 4G, mmWave and C-band.”

In a research note to clients, analyst Craig Moffett discussed Verizon’s broadband business:

Verizon’s FiOS service continues to show strength, a product of both more aggressive pricing and a lessening drag from video as the video base shrinks. Notably, Verizon is also beginning to see some contribution from fixed wireless access.

- FiOS internet subscriber gains of 104K were almost spot on with consensus. DSL losses

remained relatively steady (-30K) despite the fact that the base of legacy DSL has been

gradually depleted. Overall broadband net additions came in at 129K, which includes

55K fixed wireless connections. The company reported that it had 150K fixed wireless

broadband customers at the end of Q3. Wireline broadband net additions were strong,

at 74K, but were still weaker than expected. Notably, the company has guided to an

addition of 400K FiOS homes open for sale, the first meaningful expansion of homes

available for sale in some time (note that “open for sale” does not necessarily equate to

new build – particularly in New York, there has long been a large gap between homes

already passed and homes open for sale – but it is likely that there is at least some new

build here. - Like peers, Verizon is losing video subscribers (down 68K, a little worse than the 54K

loss we had expected, and worse than the 62K loss a year ago despite a smaller

denominator). Their decline rate of 7.2% is broadly in line with the rate of decline for the

industry overall.

With respect to Verizon’s 5G strategy and competition (e.g. T-Mobile), Craig wrote:

As we creep up to the 5G epoch, we’re on the brink of a very different industry. Despite a relatively healthy third quarter report – albeit against relatively easy year ago comps – there are reasons for disquiet. A post-COVID service revenue growth recovery has already begun to slow, and incremental revenue streams from 5G are still uncertain. Industry structure, which once appeared to be getting better – we went from four to three with the merger of Sprint and T-Mobile – is now arguably getting worse, as we now arguably go from three to five with the emergence of hybrid MVNO/MNO networks from Cable and Dish. Verizon is on the brink of a very different competitive position.

T-Mobile’s 5G network is increasingly viewed as better than Verizon’s for coverage, speed, and reliability. Verizon’s one-time bid for sustained superiority – millimeter wave “ultra-wideband” service – currently accounts for just one half of one percent of the time 5G users are connected.

Craig notes that Verizon’s initial gambit to retain network superiority in 5G was built on millimeter wave spectrum. The very limited propagation of millimeter wave spectrum, however, demands an incredibly dense wired backhaul network, at enormous cost, lest customers are simply out of range much of the time. Verizon is, anecdotally at least, well ahead of peers in network densification. Still, recent data (once again, from OpenSignal) suggests that, while 5G customers of Verizon’s 5G service are connected to mmWave spectrum much more often than are 5G customers of AT&T or T-Mobile, that is still too trivial a percentage of the time (one half of one percent). That’s hardly the basis of an advantaged network.

T-Mobile has an advantage in both spectrum propagation (coverage) and spectrum depth (speed). And Verizon still charges a premium. Retention and growth will be harder in a world where their network superiority has been ceded to a lower priced service.

In conclusion, Craig states that Verizon enjoyed years as the best network, but it will be harder to maintain that claim in the 5G era, where T-Mobile has a coverage and spectrum depth (speed) advantage. And where TMobile and the company’s Cable MVNO partners charge meaningfully lower prices than Verizon does for the same or better service.

Verizon’s Year End 2021 Priorities:

• Expand 5G leadership (?) and drive adoption; mmWave deployment and C-Band launch

• Customer differentiation and scaling premium experiences

• Transform the business; Tracfone acquisition and Verizon Media Group sale

• Accelerate and amplify 5 vectors of growth; Network-as-a-Service strategy

References:

https://www.lightreading.com/5g/verizon-has-150000-fixed-wireless-access-subs-/d/d-id/772925?

https://www.slashgear.com/verizon-5g-home-internet-expands-to-cover-more-cable-cutters-07694326/

Morgan Stanley finds little interest in 5G; Finland’s Oulu says 5G won’t mature till 2027

Morgan Stanley surveyed 3,500 broadband customers and found that only 4% of respondents said they would switch carriers to access new technologies like 5G. End users had little interest in an “innovative technology” like 5G, according to the survey results.

It should come as no surprise to IEEE Techblog readers that Finnish university researchers are warning that 5G technology won’t actually mature until the year 2027. Ari Pouttu, vice-director of the 6Genesis program at Finland’s University of Oulu, it might be years more before we see 5G’s “killer app.” Oulu is where a lot of cutting-edge network development happens, so readers should pay attention to what their researchers say.

Ari Pouttu, vice-director of the 6Genesis program at Finland’s University of Oulu, it might be years more before we see 5G’s “killer app.”

“5G is now being introduced, but we only have the first part of 5G in the market, and that’s 4G on steroids,” [5G NSA is 5G NR RAN with 4G LTE core and signaling). That’s not the real promise of 5G. The real promise of 5G is connecting all the objects, bringing intelligence into the service,” Pouttu said.

“The appearance of 5G not serving us more than 4G is partially true, partially wrong,” according to Pouttu. “When we go a few years into the future, the capacity of 4G systems comes to the limit, and we need 5G to continue this path.”

Pasi Leipala, CEO of Haltian, followed up with tacit agreement that the 5G era may be about changes in an ambient industrial world you don’t necessarily see. Haltian is an IoT company focused on smart office buildings and inventory sensors.

“If you have a pallet of something, 10,000 units, how do you track where those assets are going? How do you assure that nobody is stealing those, that they’re in the right place at the right time?” Leipala asked. But that kind of sensor density and energy efficiency will take 6G, not the current form of 5G, he said. “You always overestimate the near future and underestimate the far future,” he lamented.

However, all hope is not lost. According to a new Bloomberg article, some believe the metaverse is how wireless network operators will recoup their 5G investments.

Telecommunications companies are looking to build a platform based on the metaverse, an idea that inspired “Ready Player One” and online games by market darlings such as Roblox Corp. Early-stage examples include virtual and augmented reality headsets or glasses that provide immersive experiences. Advanced versions — still years away pending super-fast wireless data speeds — combine multiple technologies like holograms to bring the internet to life: 3D avatars of people working, interacting and relaxing in digital replicas of offices, factories and leisure venues.

Recognizing the business potential, telcos ranging from China Mobile Ltd. to Verizon Communications Inc. and SK Telecom Co. are jumping into the fray — alongside online-game developers — to build a “killer app” that could resemble a blend of today’s social media and e-commerce, but on steroids. Operators could earn a third more in revenue, potentially reaching $712 billion by 2030, if they introduce such innovative 5G applications on top of just laying pipes, according to a research by Ericsson AB’s research arm Consumer & IndustryLab.

Pernilla Jonsson of Ericsson’s Consumer & Industry Lab suggested that the metaverse might be a 5G “killer app” that would help operators avoid becoming dumb pipes.

“The metaverse is our future business model. It will be our core business platform,” Cho Ik-hwan, SK Telecom’s vice president and head of mixed reality development, told the publication. “We want to create a new kind of economic system. A very giant, very virtual economic system.”

“The metaverse will need the speed and capabilities of the faster network to fully optimize futuristic applications and keep pushing progress. It is critical to pay attention to these mind-bending and evolving applications. The metaverse transformation is global. It will impact us all,” according to an article published last year on Verizon’s website titled “The metaverse is coming – it just needed 5G.”

References:

https://www.lightreading.com/5g/is-sun-finally-starting-to-shine-on-5g/a/d-id/772907

https://www.pcmag.com/news/why-you-wont-really-feel-5g-until-2027

https://www.lightreading.com/aiautomation/the-metaverse-will-save-5g-thats-so-cute!/a/d-id/772368?

ETSI DECT-2020 approved by ITU-R WP5D for next revision of ITU-R M.2150 (IMT 2020)

ETSI DECT-2020 NR, the world’s first non-cellular 5G technology standard, will be included in the next revision of ITU-R M.2150, aka IMT-2020 technology recommendation as per the conclusion of ITU-R WP 5D’s 39th (virtual) meeting on Oct 15, 2021.

[Separately, Nufront’s IMT 2020 RIT submission has been withdrawn for consideration in the next M.2150 revision, but maybe submitted in the future. The 5D SWG on Frequency Arrangements could not agree on a revision of ITU-R M.1036 Frequency Arrangements for Terrestrial IMT, which now can’t be approved till November 2022’s ITU-R SG 5 meeting. That means there is no standard for 5G frequencies, which hasn’t bothered the FCC which is considering licensing frequencies that are not being considered for M.1036, e.g. 12GHz.]

The “DECT-2020 NR” Radio Interface Technology (RIT) is designed to provide a slim but powerful technology foundation for wireless applications deployed in various use cases and markets. It utilizes the frequency bands below 6 GHz identified for International Mobile Telecommunication (IMT) in the ITU Radio Regulations.

The DECT-2020 radio technology includes, but is not limited to: Cordless Telephony, Audio Streaming Applications, Professional Audio Applications, consumer and industrial applications of Internet of Things (IoT) such as industry and building automation and monitoring, and in general solutions for local area deployments for Ultra-Reliable Low Latency (URLLC) and massive Machine Type Communication (mMTC) as envisioned by ITU-R for IMT-2020.

According to an email to this author, ETSI supports this DECT RIT mainly because of its URLLC capabilities (3GPP Release 16 URLLC in the RAN has yet to be completed and performance tested).

DECT-2020 NR is claimed by its sponsor to be a technology foundation is targeted for local area wireless applications, which can be deployed anywhere by anyone at any time. The technology supports autonomous and automatic operation with minimal maintenance effort. Where applicable, interworking functions to wide area networks (WAN). e.g. PLMN, satellite, fiber, and internet protocols foster the vision of a network of networks. DECT-2020 NR can be used as foundation for: Very reliable Point-to-Point and Point-to-Multipoint Wireless Links provisioning (e.g. cable replacement solutions); Local Area Wireless Access Networks following a star topology as in classical DECT deployment supporting URLLC use cases, and Self-Organizing Local Area Wireless Access Networks following a mesh network topology, which enables to support mMTC use cases.

Dr. Günter Kleindl, Chair of the ETSI Technical Committee DECT, said:

“With our traditional DECT standard we already received IMT-2000 approval by ITU-R twenty-one years ago, but the requirements for 5G were so much higher, that we had to develop a completely new, but compatible, radio standard.”

Released last year and revised in April 2021, this ETSI standard sets an example of future connectivity: the infrastructure-less and autonomous, decentralized technology is designed for massive IoT networks for enterprises. It has no single points of failure and is accessible to anyone, costing only a fraction of the cellular networks both in dollars and in carbon footprint.

The IoT standard, defined in ETSI TS 103 636 series, brings 5G to the reach of everyone as it lets any enterprise set up and manage its own network autonomously with no operators anywhere in the world. It eliminates network infrastructure, and single point of failure – at a tenth of the cost in comparison to cellular solutions. It also enables companies to operate without middlemen or subscription fees as well as store and consume the data generated in the way they see best fitting for them (on premises, in public cloud or anything in between).

Another democratizing aspect is the frequency. This new ETSI 5G standard supports efficient shared spectrum operation enabling access to free, international spectrums such as 1,9 GHz.

Jussi Numminen, Vice Chair of the ETSI Technical Committee DECT, explains:

“There’s a lot of talk about private networks but this is the first 5G technology which can support shared spectrum operation and multiple local networks in mobile system frequencies. We see this as a fundamental requirement for massive digitalization for everyone. With the ETSI standard you get immediately access to a free, dedicated 1,9 GHz frequency internationally. It is a perfect match for massive IoT.”

Non-cellular 5G is built on completely different principles from cellular 5G. One of the biggest differences – and advantages – is the decentralized network. In a non-cellular 5G network, every device is a node, every device can be a router – as if every device was a base station. The devices automatically find the best route; adding a new device into the network routing works autonomously as well and if one device is down, the devices will re-route by themselves. It means reliable communication eliminating single point of failures.

The standard fulfills both massive machine-type communications (mMTC) and ultra-reliable low latency communications (URLLC) requirements of 5G. Reliably connecting thousands and even millions of devices is one of the cornerstones for demanding industrial 5G systems. DECT-2020 NR supports local deployments without separate network infrastructure, network planning or spectrum licensing agreements making it affordable and easy to access by anyone and anywhere.

A decentralized mesh with short hops and small transmission power also means a significantly lower carbon footprint of the communications system. A recent study in Tampere University in Finland saw an approximately 60% better energy efficiency at system level compared to traditional cellular topology with the same radio energy profile.

The ETSI DECT-2020 NR standard consists of four parts, published in April 2021:

MAC: ETSI TS 103 636-4 V1.2.1 (2021-04)

PHY: ETSI TS 103 636-3 V1.2.1 (2021-04)

Radio reception and transmission requirements: ETSI TS 103 636-2 V1.2.1 (2021-04)

Overview: ETSI TS 103 636-1 V1.2.1 (2021-04)

Note: Updates are being prepared

………………………………………………………………………………………………………………………………………..

This standard is well suited for businesses such as smart meters, Industry 4.0, building management systems, logistics and smart cities. It will assist in the urbanization, building, and energy consumption in the construction of these smart cities. It also opens opportunities for new use cases, scaling at mass the levels of communication for the future. The energy transition from fossil fuels to electricity boost local renewable energy production and consumption market requiring new communication capabilities. This creates a circular economy and allows for the traceability of goods, raw materials and waste.

Finland-based Wirepas received €10 million in funding to develop and bring to market the first technology solutions for non-cellular 5G based on the new DECT-2020 NR wireless connectivity standard announced by ETSI in October 2020. Wirepas said it was the main contributor to the development of the DECT-2020 New Radio (NR) standard.

ETSI DECT-2020 NR in a nutshell:

- No middleman

- No infrastructure

- No subscription fees

- Free dedicated international frequency

- Dense and massive network capabilities

- One tenth of the cost of cellular

- Lowest carbon footprint of large-scale networks

Editor’s Note: We’ve invited ETSI to submit an IEEE Techblog article providing additional information and applications for the ETSI DECT-2020 NR standard.

About ETSI:

ETSI provides members with an open and inclusive environment to support the development, ratification and testing of globally applicable standards for ICT systems and services across all sectors of industry and society. We are a non-profit body, with more than 950 member organizations worldwide, drawn from 64 countries and five continents. The members comprise a diversified pool of large and small private companies, research entities, academia, government, and public organizations. ETSI is officially recognized by the EU as a European Standards Organization (ESO). For more information, please visit us at https://www.etsi.org/

References:

https://www.eetimes.eu/wirepas-receives-e10m-to-develop-first-non-cellular-5g-technology/

EXFO/Heavy Reading Survey: Nearly half of all mobile network operators plan to deploy 5G SA within 1 year

EXFO worked with Heavy Reading to conduct a survey of Mobile Network Operators (MNOs) across North America and Europe to understand their approach to 5G SA core network and the revenue opportunity it presents. 49% of MNOs are planning to deploy 5G SA within the next year, while a further 39% will deploy 5G SA within one to two years. The main drivers for deploying 5G SA are to support enhanced consumer offerings such as virtual reality, augmented reality and mobile gaming; accelerate time to market for new services; and offer network slice-based services.

While 76% of MNOs believe service assurance will be necessary to sell advanced 5G services and meet stringent service level agreements (SLAs), operations teams don’t have real-time visibility into how outages and degradations impact customers—whether they are humans or “machines” (critical, latency-sensitive applications and devices like emergency services or factory floor robots). 65% of MNOs say that this lack of actionable insight is preventing them from automating networks and fault resolution, which are essential to meeting demanding performance expectations in enterprise applications.

Specifically, most MNOs said they need a range of new tools and capabilities to generate revenues from 5G services:

- 86% say they need real-time network, service and quality of experience intelligence

- 85% say they need to be able to monitor per-service and per-device performance.

- 81% say they need AI-driven anomaly and fault detection, as well as root cause analysis.

- 82% say they need monitoring of end-to-end network slices.

“The opportunity to generate revenues from 5G SA lies in automated networks, which means service providers must deliver on enterprise service level agreements. This survey with Heavy Reading reinforces what we hear regularly from our customers: mobile network operators want greater service assurance and analytics to deliver actionable insights into network performance and user experience,” said Philippe Morin, CEO at EXFO. “This is where EXFO’s unique, adaptive approach to service assurance comes into play. By taking a source-agnostic approach to data collection and analytics, combined with a fully cloud-native architecture, our service assurance platform integrates with legacy and new 5G systems to provide a unified, end-to-end view of customer experience, device and network performance.”

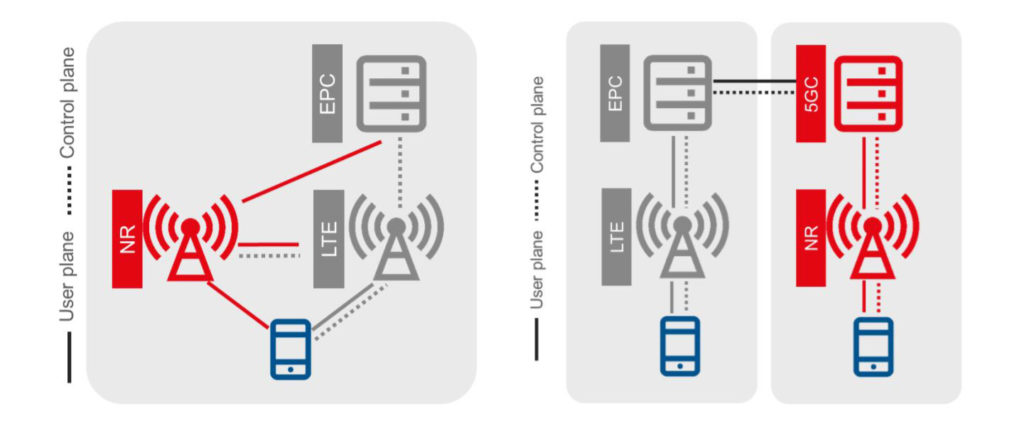

5G NSA (LTE & EPC) 5G SA (NR connected to 5G core)

Benefits of 5G SA core network:

- MNOs can launch new enterprise 5G services such as smart cities, and smart factories

- It is fully virtualized, cloud-native architecture (CNA), which introduces new ways to develop, deploy and manage services

- The architecture enables end to end slicing to logically separate services

- Automation drives up efficiencies while driving down the cost of operating the networks.

- By standardizing on a cloud-native approach, MNOs can also rely on best of breed innovation from both vendors and the open-source communities

“When you look at the number of RFPs that are out there and the dialog we’re having, I think we’re now starting to see the need [to move]from what I would call studying or doing assessment, to potentially now looking at deploying [5G SA],” Morin said. He pointed out that there have been numerous announcements by carriers around 5G private networks and enterprise-based services, which he says are the initial drivers for 5G SA deployment — and are also driving the need for enhanced service assurance capabilities.

“When you’re talking about more business-focused use cases, service-level agreements become even more important and that’s why [there is a]need for service assurance,” Morin said. In contrast to previous network generations, where service assurance was often considered only after a variety of other decisions were made, the expectations of serving enterprise use cases are making service assurance a higher priority. “It’s pretty clear, as you deploy 5G SA, especially in the context of … [having]machines connected to this, IoT devices and so on, and more of an enterprise focus, that service assurance requirements are much more front and center than what we’ve seen in the previous protocols.”

Morin sites two key 5G SA capabilities that offer value:

- The ability to support billions of connections (massive machine-to-machine communications.

- Network slicing to enable differentiated services at scale.

With those opportunities, comes the requirement for MNOs to ensure that they can provide the levels of service and scalability that slicing and massive IoT demand — and that’s where operators will need better monitoring tools, visibility and insights, Morin says, and their acknowledgement of that need is reflected in the survey. EXFO’s joint survey found that 76% of the surveyed MNOs believe that service assurance will be necessary for deploying 5G SA. “I’m pretty sure we would not have the same stats, if you would’ve asked the same questions around 3G and 4G,” Morin added.

“If you’re going to have business use cases that machines are going to be relying on to be able to execute that application, machines won’t be as tolerant as humans, because the service won’t be able to operate. So what this means is that the network operators need a better view of insights on the network performance, that in the past, because it was for humans, maybe was not as required. But clearly, now, for 5G SA and 5G revenues that are going to be driven out of this, getting better visibility on what is happening that is down to the device level– not just the customer; the device, the service and the network — and end-to-end visibility will be really, really critical.”

There’s also the changing nature of service assurance and visibility strategy and tools to consider. As enterprises moved into making use of big data, their strategies and architectures often involved pouring network data into a massive data lake and then retrieving information from there as needed.

“With 5G, and 5G Standalone in particular, we absolutely believe that’s not going to be the architecture of choice. … You cannot wait for the issue to come up, and go into a data lake to try to figure out what happened in the last 15 minutes. We believe that it’s got to be real-time, it’s got to be adaptive — because you can’t start getting information from all the devices and all the IoT. This would have a big impact on your overall cost structure.”

Morin said that 5G SA core network’s cloud-based, orchestrated and automated nature enables the company to support machine-learning and generate insights only when an anomaly or service issue/problem is detected. AI will then determine whether data is needed from the device, service or network layer in order to resolve the issue(s).

“If you’re going to really make 5G SA a success, it will require a higher level of automation, and I do believe that service assurance will be what I would call an automation enabler. If you don’t have that capability to monitor and in an automated way, provide actionable insights to [a specifics]use case and to [a specific]SLA, I think it will be very difficult to go into a high-volume deployment with 5G SA.”

………………………………………………………………………………………………………………………………………………

Author’s Note:

Despite the optimistic results of this 5G SA core network survey, just 13 network operators had launched commercial public 5G SA networks as of the middle of August 2021. Some 45 other operators are planning or deploying 5G SA for public networks, and 23 operators are involved in tests or trials. That’s out of a total of 176 commercial 5G networks launched worldwide (163 of them are 5G NSA networks)!

Note also that there are no ITU standards or 3GPP specifications for how to implement a 5G SA Core network. There are many choices which will lead to different, incompatible implementations of the 5G Core network

References:

https://www.exfo.com/en/products/service-assurance-platform/nova-core/

https://www.exfo.com/en/resources/blog/mobile-private-networks-5g/

https://www.affirmednetworks.com/sa-and-nsa-5g-architectures-the-path-to-profitability/

Open Access Fiber Networks Explained; Underline’s Intelligent Community Network

In Open Access Fiber networks, the same physical network infrastructure is utilized by multiple providers delivering services to subscribers. The Open Access business model has been drawing attention globally as governments and municipalities find the concept of offering competition between providers and the freedom of choice for the subscriber is essential. It has also proved to be a feasible way to connect rural areas where service providers might have a hard time generating enough revenue to justify investing in their own network infrastructure.

Open access fiber networks can be the foundation for distributed healthcare, 5G, and resilient, modernized infrastructure—including responsible energy creation and secure community smart grids.

For subscribers to benefit from the freedom of choice and competition between providers that are delivering services using the same network infrastructure they will need a comprehensive way to browse the assortment of services offered.

Open Access network operators must keep track of:

- Every single subscriber in the network, their physical address, their “technical address” (switch, switch port, etc.).

- Which services they are buying from which provider/s.

- The total number of customers and/or services bought if you’re operating in a three-layer model where you have to report back to the network owners how their network is utilized.

……………………………………………………………………………………………………………………………………….

Already common in Europe with Sweden as the best known example, open access networks are just beginning to gain market traction in the U.S. While U.S. community-wide network operators like SiFi Networks and UTOPIA Fiber (Utah) have adopted a wholesale-like business model, newcomer Underline is taking a bit more of a direct approach.

“When people say open access in this country, they typically mean ISPs can come in and lease fiber and choose to build a given neighborhood that hasn’t been overbuilt yet. We mean something very different,” Underline CEO Robert Thompson told Fierce Telecom. “We are not a wholesale leaser of fiber. We are the fiber network literally to the doorbell.”

Underline isn’t just providing physical fiber-to-the-home infrastructure, but also a unified billing system and cybersecurity layer. The latter will allow the communities it serves to deploy smart city applications over an on-demand Layer 2 (Data Link layer) connection that will never touch the Layer 3 (Network layer) public internet, Thompson said.

“On the one hand, we directly face consumers and businesses, schools and so forth and we provide them network access connectivity and technology for a monthly connection fee. On the other hand, we look like a network infrastructure-as-a-service provider to the ISPs or content community,” Thompson said.

“We don’t provide IP,” he continued. “We’re going to move your traffic from your house ultrafast over fiber and we’re going to hand off you and your traffic to the internet service provider of your choosing. That ISP is then your IP, the routing of your traffic. They’re connecting you to that glorious world wide web,” he added.

Thompson said Underline will charge users directly on a monthly basis for connectivity, with their chosen ISP getting a portion of that cost. So, for instance, in the case where a subscriber takes a $65 per month symmetric gigabit plan, the ISP will get a $15 cut. Underline also plans to charge licensing and per subscriber fees for use of its technology stack.

Underline is now initiating construction in its first market: Colorado Springs, CO. The company will offer residential speeds up to 10 Gbps and enterprise service up to 100 Gbps, with qualifying households eligible to receive a discounted rate on Underline’s bottom tier symmetrical 500 Mbps plan.

The project will be completed in several stages, with a Phase I build set to connect 24,000 homes and 4,000 businesses with 225 route miles of fiber plant. Initial customers will include the the National Cybersecurity Center, the new Space Information Sharing and Analysis Center and Altia Software.

Thompson says that Phase II will cover roughly the same amount of ground and Underline also has a build agreement with an unnamed city “immediately surrounding” Colorado Springs. Taken together, construction in both phases and the second city will amount to “an exercise of approximately $125 million in total capital.”

“We are after this with a vengeance, and we are very thankfully supported by very strong capital,” Thompson said, noting a “drumbeat of steady announcements of drills in the dirt in new communities” is on the way.

Thompson said Underline is targeting communities with populations between 20,000 and 750,000. He noted that such communities have “historically been basically ignored by the incumbents (large telcos) and which by and large will not qualify” for federal support for broadband deployments.

Beyond that, he said Underline’s market assessments include factors like demand point density per fiber route mile, a population productivity ratio, a competition index and a social equity analysis. The latter is a key priority for Underline and “part of our social purpose,” Thompson explained.

“We want to understand and we actually want to target communities that have a significant portion of their demand points that have no internet at all or very poor internet at home because of socio economic status. This country’s got to have internet that’s fast, affordable and fair,” he concluded.

References:

https://www.fiercetelecom.com/operators/underline-has-a-different-vision-for-open-access-fiber-u-s

https://www.cossystems.com/about/open-access/

https://www.foresitegroup.net/what-you-need-to-know-about-open-access-networks-2/

Vodafone Idea to test 5G-based smart city solutions with Larsen & Toubro in Pune, India

India’s struggling telco Vodafone Idea is partnering with engineering and construction conglomerate Larsen & Toubro for a pilot project to test 5G-based smart city solutions, as part of its ongoing 5G trials on government-allocated spectrum.

In the pilot to be conducted in the city of Pune, the companies will collaborate to test and validate 5G use cases built on IoT and video AI technologies leveraging L&T’s Smart City platform, Fusion, to address the challenges of urbanization, safety and security, and offering smart solutions to the citizens.

Vi has deployed its 5G trial in a setup of end-to-end captive network of Cloud Core, new C1 – Vodafone Idea External generation Transport and Radio Access Network.

Abhijit Kishore, chief enterprise business officer at Vodafone Idea, said: “Telecommunications solutions are the backbone of building smart and sustainable cities. The advent of 5G technology opens whole new opportunities to address challenges of urban growth and provide end-to-end solutions to support sustainable creation of Smart Cities, in the future. Vodafone Idea is happy to partner with Larsen & Toubro to test 5G based Smart City solutions and utilize our mutual expertise to find solutions that can help shape cities of the future.”

“In this constantly-evolving world, we are seeing an exponential rise in demand for smarter and more intelligent solutions and L&T Smart World is committed towards leveraging the latest technological innovations in the IoT and Telecommunications areas to benefit society at large. We are excited to partner with Vodafone Idea to bring to the table our experience, of having successfully executed several smart solutions across Indian cities, to develop customized, IoT-driven 5G solutions for various industry and enterprise verticals”, said J. D. Patil, senior executive VP of Defense and smart technologies at L&T.

The partnership between Vodafone Idea and Larsen & Toubro will trial several 5G use cases that cover 5G services such as enhanced Mobile Broadband (eMBB), Ultra Reliable Low Latency Communications (uRLLC) and Multi-Access Edge Computing (MEC). The firms said that the partnership will help to analyze the performance requirements of smart city applications and business models in 5G, design and implement 5G-based “smart and safe city” applications and use data analytics tools to visualize and analyze the trial results.

Vodafone Idea (Vi) has been allocated 26 GHz and 3.5 GHz spectrum in the mmWave band by India’s Department of Telecom (DoT), for their 5G network trials and use cases. In its initial test results Vi has achieved peak speed in excess of 3.7 Gbps with very low latency on the mmWave spectrum band. These speeds were achieved with state-of-the-art equipment in 5G Non-Standalone (NSA) network using 5G NR compliant radios. The Indian telco has also achieved peak download speeds of up to 1.5 Gbps in a 3.5 GHz-band 5G trial network with its original equipment manufacturer (OEM) partners.

The high speed and low latency characteristics of 5G network may enable improved surveillance and video streaming/broadcast to permit the evolution of 5G smart cities and smart factories. Smart City and Industry 4.0 will hopefully accelerate with 5G deployment and usher in new era of Digital India.

As forVi’s two telco competitors:

- Bharti Airtel has recently demonstrated India’s first 5G rural trial using network equipment from Ericsson. It has also showcased 5G cloud gaming.

- India’s wireless network market leader Reliance Jio has trialed 5G VoNR, AI-multimedia chatbot, and immersive high-definition (HD) virtual reality.

The DoT had approved applications of Reliance Jio, Bharti Airtel and Vodafone in May, and MTNL later for 5G trials. The permission has been granted for six-month trials with telecom gear makers Ericsson, Nokia, Samsung and C-DOT.

References:

https://www.vodafoneidea.com/media/press-releases

Vodafone Idea inks partnership to test 5G-based smart city solutions

https://www.businesstoday.in/industry/telecom/story/vodafone-idea-says-achieved-peak-5g-speed-of-over-37-gbps-in-pune-trials-307076-2021-09-19

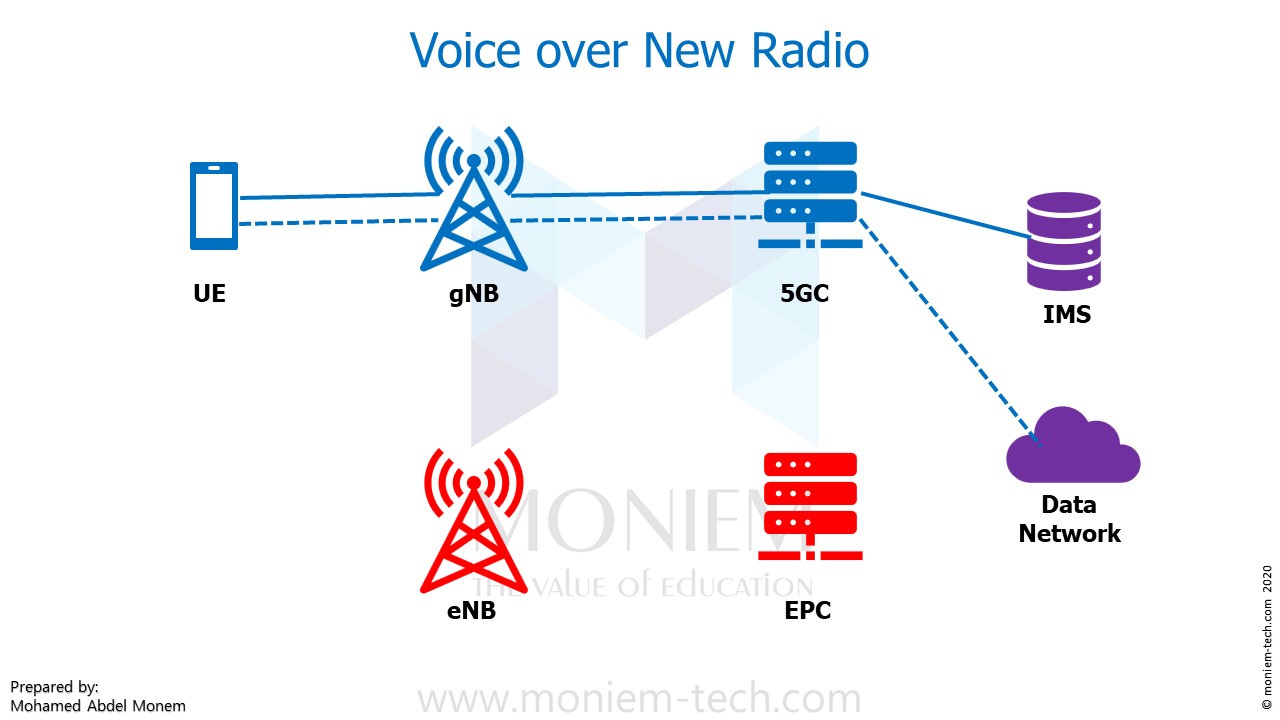

GSM: VoNR progresses, but requires 5G SA core network

5G non-standalone (5G NSA) networks, voice services were enabled by continued use of LTE and 2G/3G infrastructures, but 5G standalone networks (5G SA) – both public and private – require a new approach. They need to be able to carry QoS-guaranteed voice services (as opposed to over-the-top voice applications), but there is no legacy infrastructure to fall back on.

Voice over New Radio (VoNR) [1.] is designed to meet this challenge. VoNR is also expected to bring improvements in latency, call quality and improved integration with applications and services using 5G data at the same time. VoNR is anticipated to drive innovation in conferencing, augmented and virtual reality applications over 5G networks.

Note 1. 5G NR is the essence of standardized 5G RAN as per 3GPP Release 15, 16 and ITU-R M2150 recommendation for 5G RIT/SRIT. However, VoNR requires a 5G SA core network rather than using LTE signaling and core (EPC).

Additionally, there needs to be a mechanism for devices to use to LTE, or 2G/3G voice networks when outside the coverage of a 5G standalone network. EPS Fallback (EPS-FB) is an early introduction step to VoNR until sufficient NR low-band or low mid-band coverage has been deployed.

The Global mobile Suppliers Association (GSA) announced that 42 devices and 40 5G chipsets from four vendors have been announced supporting Voice over New Radio (VoNR) technology. This includes five discrete modems and 35 mobile processors/platforms. Of these, 36 are known to be commercially available, including four discrete modems and 32 mobile processors and platforms. Chipsets are commercially available from Mediatek, Qualcomm, Samsung and Unisoc.

In the GSA’s latest VoNR Market Report, the industry group found that numerous network operators are heavily investing in the new voice technology for their 5G standalone networks. To date, GSA has catalogued 16 operators publicly announced as investing in VoNR in some way or another. Of those, eight are evaluating/testing/trialing, three are understood to be planning to deploy, three

are deploying the technology, one has soft launched VoNR services and one is offering limited VoNR as part of a market trial of its new 5G SA network.

This past June, Deutsche Telekom (DT) and partners announced the successful completion of the world’s first 5G Voice over New Radio (VoNR) call in an end to end multi-vendor environment. T-Mobile, which is majority owned by DT, is also pursuing VoNR as per this article.

References:

GSA Market Report: Global Progress to Voice over New Radio (VoNR) – October 2021

https://www.telekom.com/en/media/media-information/archive/world-first-end-to-end-multivendor-5g-voice-over-nr-call-628746

https://www.fiercewireless.com/tech/t-mobile-chases-voice-5g-verizon-at-t-not-so-much