4G

Summary of EU report: cybersecurity of Open RAN

The EU has published a report on the cybersecurity of Open RAN, a 4G/5G (maybe even 2G?) network architecture the European Commission says will provide an alternative way of deploying the radio access part of 5G networks over the coming years, based on open interfaces. The EU noted that while Open RAN architectures create new opportunities in the marketplace, they also raise important security challenges, especially in the short term.

“It will be important for all participants to dedicate sufficient time and attention to mitigate such challenges, so that the promises of Open RAN can be realized,” the report said.

The report found that Open RAN could bring potential security opportunities, provided certain conditions are met. Namely, through greater interoperability among RAN components from different suppliers, Open RAN could allow greater diversification of suppliers within networks in the same geographic area. This could contribute to achieving the EU 5G Toolbox recommendation that each operator should have an appropriate multi-vendor strategy to avoid or limit any major dependency on a single supplier.

Open RAN could also help increase visibility of the network thanks to the use of open interfaces and standards, reduce human errors through greater automation, and increase flexibility through the use of virtualisation and cloud-based systems.

However, the Open RAN concept still lacks maturity, which means cybersecurity remains a significant challenge. Especially in the short term, by increasing the complexity of networks, Open RAN could exacerbate certain types of security risks, providing a larger attack surface and more entry points for malicious actors, giving rise to an increased risk of misconfiguration of networks and potential impacts on other network functions due to resource sharing.

The report added that technical specifications, such as those developed by the O-RAN Alliance, are not yet sufficiently secure by design. This means that Open RAN could lead to new or increased critical dependencies, for example in the area of components and cloud.

The EU recommended the use of regulatory powers to monitor large-scale Open RAN deployment plans from mobile operators and if needed, restrict, prohibit or impose specific requirements or conditions for the supply, large-scale deployment and operation of the Open RAN network equipment.

Technical controls such as authentication and authorization could be reinforced and a risk profile assessed for Open RAN providers, external service providers related to Open RAN, cloud service/infrastructure providers and system integrators. The EU added that including Open RAN components into the future 5G cybersecurity certification scheme, currently under development, should happen at the earliest possible stage.

Following up on the coordinated work already done at EU level to strengthen the security of 5G networks with the EU Toolbox on 5G Cybersecurity, Member States have analysed the security implications of Open RAN.

Margrethe Vestager, Executive Vice-President for a Europe Fit for the Digital Age, said: “Our common priority and responsibility is to ensure the timely deployment of 5G networks in Europe, while ensuring they are secure. Open RAN architectures create new opportunities in the marketplace, but this report shows they also raise important security challenges, especially in the short term. It will be important for all participants to dedicate sufficient time and attention to mitigate such challenges, so that the promises of Open RAN can be realised.”

Thierry Breton, Commissioner for the Internal Market, added: “With 5G network rollout across the EU, and our economies’ growing reliance on digital infrastructures, it is more important than ever to ensure a high level of security of our communication networks. That is what we did with the 5G cybersecurity toolbox. And that is what – together with the Member States – we do now on Open RAN with this new report. It is not up to public authorities to choose a technology. But it is our responsibility to assess the risks associated to individual technologies. This report shows that there are a number of opportunities with Open RAN but also significant security challenges that remain unaddressed and cannot be underestimated. Under no circumstances should the potential deployment in Europe’s 5G networks of Open RAN lead to new vulnerabilities.”

Guillaume Poupard, Director General of France’s National Cyber Security Agency (ANSSI), said: “After the EU Toolbox on 5G Cybersecurity, this report is another milestone in the NIS Cooperation Group’s effort to coordinate and mitigate the security risks of our 5G networks. This in-depth security analysis of Open RAN contributes to ensuring that our common approach keeps pace with new trends and related security challenges. We will continue our work to jointly address those challenges.”

Finally, a technology-neutral regulation to foster competition should be maintained., with EU and national funding for 5G and 6G research and innovation, so that EU players can compete on a level playing field.

References:

https://ec.europa.eu/commission/presscorner/detail/en/IP_22_2881

https://digital-strategy.ec.europa.eu/en/library/cybersecurity-open-radio-access-networks

IEEE/SCU SoE Virtual Event: May 26, 2022- Critical Cybersecurity Issues for Cellular Networks (3G/4G, 5G), IoT, and Cloud Resident Data Centers

This virtual event on ZOOM will be from 10am-12pm PDT on May 26, 2022.

Session Abstract:

IEEE ComSoc and SCU School of Engineering (SoE) are thrilled to have three world class experts discuss the cybersecurity threats, mitigation methods and lessons learned from a data center attack. One speaker will also propose a new IT Security Architecture where control flips from the network core to the edge.

Each participant will provide a 15 to 20 minute talk which will be followed by a lively panel session with both pre-planned and ad hoc/ extemporaneous questions. Audience members are encouraged to submit their questions in the chat and also to send them in advance to [email protected].

Below are descriptions of each talk along with the speaker’s bio:

Cybersecurity for Cellular Networks (3G/4G, 5G NSA and SA) and the IoT

Jimmy Jones, ZARIOT

Abstract:

Everyone agrees there is an urgent need for improved security in today’s cellular networks (3G/4G, 5G) and the Internet of Things (IoT). Jimmy will discuss the legacy problems of 3G/4G, migration to 5G and issues in roaming between cellular carriers as well as the impact of networks transitioning to support IoT.

Note: It’s important to know that 5G security, as specified by 3GPP (there are no ITU recommendations on 5G security), requires a 5G Stand Alone (SA) core network, very few of which have been deployed. 5G Non Stand Alone (NSA) networks are the norm, but they depend on a 4G-LTE infrastructure, including 4G security.

Cellular network security naturally leads into IoT security, since cellular networks (e.g. NB IoT, LTE-M, 5G) are often used for IoT connectivity.

It is estimated that by 2025 we will interact with an IoT device every 18 seconds, meaning our online experiences and physical lives will become indistinguishable. With this in mind it is as critical to improve IoT security as fastening a child’s seatbelt.

The real cost of a security breach or loss of service for a critical IoT device could be disastrous for a business of any size, yet it’s a cost seldom accurately calculated or forecasted by most enterprises at any stage of IoT deployment. Gartner predicts Operational Technologies might be weaponized to cause physical harm or even kill within three years.

Jimmy will stress the importance of secure connectivity, but also explain the need to protect the full DNA of IoT (Device, Network and Applications) to truly secure the entire system.

Connectivity providers are a core component of IoT and have a responsibility to become part of the solution. A secure connectivity solution is essential, with strong cellular network standards/specifications and licensed spectrum the obvious starting point.

With cellular LPWANs (Low Power Wide Area Networks) outpacing unlicensed spectrum options (e.g. LoRa WAN, Sigfox) for the first time, Jimmy will stress the importance of secure connectivity and active collaboration across the entire IoT ecosystem. The premise is that the enterprise must know and protect its IoT DNA (Device, Network & Application) to truly be secure.

Questions from the audience:

I am open to try and answer anything you are interested in. Your questions will surely push me, so if you can let me know in advance (via email to Alan) that would be great! It’s nice to be challenged a bit and have to think about something new.

One item of interest might be new specific IoT legislation that could protect devices and data in Europe, Asia, and the US ?

End Quote:

“For IoT to realize its potential it must secure and reliable making connectivity and secure by design policies the foundation of and successful project. Success in digital transformation (especially where mission and business critical devices are concerned) requires not only optimal connectivity and maximal uptime, but also a secure channel and protection against all manner of cybersecurity threats. I’m excited to be part of the team bringing these two crucial pillars of IoT to enterprise. I hope we can demonstrate that security is an opportunity for business – not a burden.”

Biography:

Jimmy Jones is a telecoms cybersecurity expert and Head of Security at ZARIOT. His experience in telecoms spans over twenty years, during which time he has built a thorough understanding of the industry working in diverse roles but all building from early engineering positions within major operators, such as WorldCom (now Verizon), and vendors including Nortel, Genband & Positive Technologies.

In 2005 Jimmy started to focus on telecom security, eventually transitioning completely in 2017 to work for a specialist cyber security vendor. He regularly presents at global telecom and IoT events, is often quoted by the tech media, and now brings all his industry experience to deliver agile and secure digital transformation with ZARIOT.

…………………………………………………………………………………………………………………………………………………………………………………………………………………….

Title: Flip the Security Control of the Internet

Colin Constable, The @ Company

The PROBLEM:

With the explosion of Internet connected devices and services carrying user data, do current IT architectures remain secure as they scale? The simple and scary answer is absolutely no, we need to rethink the whole stack. Data breaches are not acceptable and those who experience them pay a steep price.

Transport Layer Security (TLS) encrypts data sent over the Internet to ensure that eavesdroppers and hackers are unable to see the actual data being transmitted. However, the Router needs meta data (the IP and Port) to make it work. What meta data does the Data level Router have access to?

We need to discuss how to approach the problem and selectively discard, but learn from previous IT architectures so that we can build a more solid, secure IT infrastructure for the future.

Proposition:

I will provide a glimpse of a future security focused IT architecture.

- We need to move most security control functionality to the edge of the network.

- Cloud data center storage should be positioned as an encrypted cache with encryption keys at the edge.

- No one set of keys or system admin can open all the encrypted data.

When data is shared edge to edge we need to be able to specify and authenticate the person, entity or thing that is sharing the data. No one in the middle should be able to see data in the clear.

Issues with Encryption Keys:

- IT and Data security increasingly rely on encryption; encryption relies on keys; who has them?

- Is there really any point to VPN’s Firewalls and Network segmentation if data is encrypted?

- We use keys for so many things TLS, SSH, IM, Email, but we never tend to think about the keys.

- Do you own your keys? If not someone else can see your data!

- What do we need to flip the way IT is architected?

Recommendations for Keys:

- Keys should be cut at the edge and never go anywhere else.

- You should be able to securely share keys along with the data being transmitted/received.

- There needs to be a new way to think about identity on the Internet.

The above description should stimulate many questions from attendees during the panel discussion.

Biography:

Colin Constable’s passion is networking and security. He was one of the founding members of the Jericho Forum in the 2000s. In 2007 at Credit Suisse, he published “Network Vision 2020,” which was seen by some as somewhat crazy at the time, but most of it is very relevant now. While at Juniper, Colin worked on network virtualization and modeling that blurred the boundaries between network and compute. Colin is now the CTO of The @ Company, which has invented a new Internet protocol and built a platform that they believe will change not just networking and security, but society itself for the better.

……………………………………………………………………………………………………………………….

The Anatomy of a Cloud Data Center Attack

Thomas Foerster, Nokia

Abstract:

Critical infrastructure (like a telecommunications network) is becoming more complex and reliant on networks of inter-connected devices. With the advent of 5G mobile networks, security threat vectors will expand. In particular, the exposure of new connected industries (Industry 4.0) and critical services (connected vehicular, smart cities etc.) widens the cybersecurity attack surface.

The telecommunication network is one of the targets of cyber-attacks against critical infrastructure, but it is not the only one. Transport, public sector services, energy sector and critical manufacturing industries are also vulnerable.

Cloud data centers provide the required computing resources, thus forming the backbone of a telecommunications network and becoming more important than ever. We will discuss the anatomy of a recent cybersecurity attack at a cloud data center, review what happened and the lessons learned.

Questions:

- What are possible mitigation’s against social engineering cyber- attacks?

-Multifactor authentication (MFA)

-Education, awareness and training campaigns

- How to build trust using Operational Technology (OT) in a cloud data center?

Examples:

- Access monitoring

- Audits to international standards and benchmarks

- Security monitoring

- Playbooks with mitigation and response actions

- Business continuity planning and testing

Recommendations to prevent or mitigate DC attacks:

- Privileged Access Management across DC entities

- Individual credentials for all user / device entities

- MFA: One-Time Password (OTP) via text message or phone call considered being not secure 2-Factor Authentication anymore

- Network and configuration audits considering NIST/ CIS/ GSMA NESAS

- Regular vulnerability scans and keep network entities up to date

- Tested playbooks to mitigate security emergencies

- Business continuity planning and establish tested procedures

Biography:

Thomas Foerster is a senior product manager for Cybersecurity at Nokia. He has more than 25 years experiences in the telecommunications industry, has held various management positions within engineering and loves driving innovations. Thomas has dedicated his professional work for many years in product security and cybersecurity solutions.

Thomas holds a Master of Telecommunications Engineering from Beuth University of Applied Sciences, Berlin/ Germany.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Video recording of this event: Critical Cybersecurity Issues for Cellular Networks, IoT, and Cloud-Resident Data Centers – YouTube

Previous IEEE ComSoc/SCU SoE March 22, 2022 event: OpenRAN and Private 5G – New Opportunities and Challenges

Video recording: https://www.youtube.com/watch?v=i7QUyhjxpzE

IDC Worldwide Private LTE/5G Wireless Infrastructure Forecast reveals 4G-LTE Dominates

The global private LTE/5G wireless infrastructure market is forecast to reach revenues of $8.3 billion by 2026, an increase compared to revenues of $1.7 billion in 2021, according to new research from International Data Corporation (IDC). IDC said that this market is expected to achieve a five-year compound annual growth rate (CAGR) of 35.7% over the 2022-2026 forecast period.

The report, Worldwide Private LTE/5G Infrastructure Forecast, 2022-2026 (IDC #US48891622), presents IDC’s annual forecast for the private LTE/5G wireless infrastructure market. The forecast includes aggregated spending on RAN, core, and transport infrastructure as well as spending by region; it excludes services or publicly owned and operated networks that carry shared data traffic. The report also provides a market overview, including drivers and challenges for technology suppliers, communication service providers, and cloud providers.

IDC defines private LTE/5G wireless infrastructure as any 3GPP-based cellular network deployed for a specific enterprise/industry vertical customer that provides dedicated access to private resources. (Yet IDC does not state what 3GPP Release(s) or whether necessary 5G capabilities, like specs for URLLC have been completed and performance tested). This could include dedicated spectrum, dedicated hardware and software infrastructure, and which has the ability to support a range of use cases spanning fixed wireless access, traditional and enhanced mobile broadband, IoT endpoints/sensors, and ultra-reliable, low-latency applications.

“Enterprise or industry verticals, such as manufacturing, retail, utilities, transport, and public safety are leading the charge for private LTE, and eventually private 5G networks, driven by a desire to capture productivity gains, enable automation, and improve customer experience. While the demand metrics are relatively understood, the emerging private cellular ecosystem presents several road maps, each with particular advantages and disadvantages. While an enterprise (within any industry vertical) will eventually need to assess its own needs internally, understanding the implications from each road map can provide a starting point,” said Patrick Filkins, IDC senior research analyst, IoT and Mobile Network Infrastructure.

“The private LTE/5G wireless market showcased in 2021 that although its growth is somewhat immune to macro challenges associated with the global pandemic, it still requires a significant amount of market-level solutioning to address the pain points associated with unlocking the full 5G solution. This includes curating and scaling a robust set of 5G device platforms, which still requires more work across the ecosystem, particularly as it relates to vertical-specific solutioning,” Filkins added.

IDC noted that the worldwide market for private LTE/5G wireless infrastructure continued to gain traction throughout 2021. The research firm highlighted that private 4G-LTE remained the predominant private cellular network revenue generator during 2021. However, Private 5G marketing, education, trials, and new private 5G products and services also began to see market availability. IDC also said that most private 5G projects to date remain as either trials or pre-commercial deployments.

“Heightened demand for dedicated or private wireless solutions that can offer enhanced security, performance, and reliability continue to come to the fore as both current and future applications, particularly those in the industrial sector, require more from their network and edge infrastructure. While private LTE/5G infrastructure continues to see more interest, the reality is 5G itself continues to evolve, and will evolve for the next several years. As such, many organizations are expected to invest in private 5G over the coming years as advances are made in 5G standards, general spectrum availability, and device readiness,” Filkins said.

The report forecasts that the market for 5G private networks will reach $47.5 billion in 2030, up from $221 million last year, while the total market for 4G private networks will go from $3.54 billion in 2021 to $66.88 billion in 2030. IDC also noted that the global spending on smart manufacturing will expand from $345 billion in 2021 to more than $950 billion in 2030.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

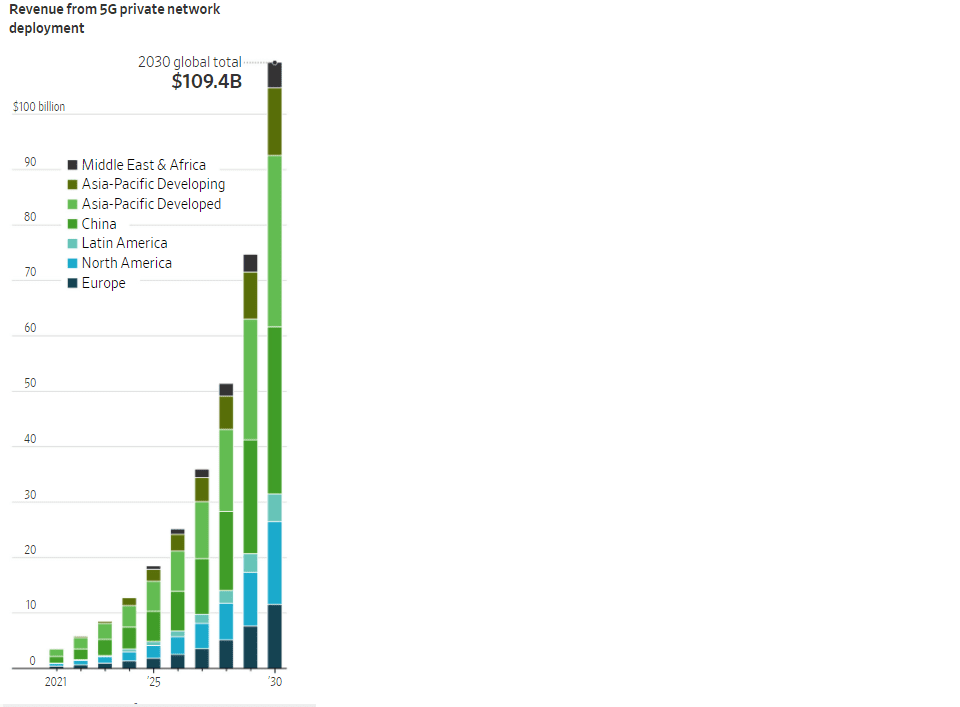

The total addressable market for private networks – including the Radio Access Network, Mobile-access Edge Computing (MEC), core, and professional services – is forecast to increase from $3.7 billion in 2021 to more than $109.4 billion in 2030, according to a recent report by ABI Research. However, a quote in the article introducing that report was dead wrong:

“While the Third Generation Partnership Project (3GPP) has frozen Release 16 (standardizing Ultra-Reliable Low-Latency Communication (URLLC)), Release 16-capable chipsets and devices have not yet emerged in the market. As enterprises require Time-Sensitive Networking (TSN), as well as high availability and reliability of their connection, they are reliant on Release 16 and are, therefore, waiting for compatible chipsets and infrastructure to enter the market. As this is not expected to happen until 2023, enterprise 5G will mature much more slowly than previously anticipate,” ABI Research said.

–>THAT IS BECAUSE EVEN THOUGH 3GPP RELEASE 16 WAS FROZEN IN JUNE 2020, “URLCC IN THE RAN” SPEC WAS NOT COMPLETED AT THAT TIME. Before that spec can be implemented, it must be independently tested to ensure it means the ITU-R M.2410 performance requirements for BOTH ultra high reliability and ultra low latency corresponding to the 5G URLLC use case. As of 16 March 2022 (today), 3GPP Release 16 URLLC in the RAN is only 74% complete!

| 830074 | NR_L1enh_URLLC | Physical Layer Enhancements for NR Ultra-Reliable and Low Latency Communication (URLLC) | 74% | Rel-16 | RP-191584 |

ABI also noted that the global spending on smart manufacturing will expand from $345 billion in 2021 to more than $950 billion in 2030.

Note: 2022 to 2030 are forecasts. Source: ABI Research

“As manufacturers advance their digital transformation initiatives, they drive up spending on smart manufacturing with investments in factories that adopt Industry 4.0 solutions like Autonomous Mobile Robots (AMRs), asset tracking, simulation, and digital twins,” ABI said. ” While most of the revenue today is attributed to hardware, the greater reliance on analytics, collaborative industrial software, and wireless connectivity (Wi-Fi 6, 4G, 5G) will drive value-added services revenue — connectivity, data and analytic services, and device and application platforms — to more than double over the forecast.”

Meanwhile, Dell’Oro Group VP Stefan Pongratz wrote in an email to this author,” We have talked about private cellular for a long time but the reality is that we have not yet crossed the enterprise chasm. Nevertheless, we have a very large market opportunity ($10B to $20B for just the private 4G/5G RAN) that is still up for grabs, hence the high level of interest.”

About IDC:

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,200 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 110 countries. IDC’s analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly owned subsidiary of International Data Group (IDG), the world’s leading tech media, data, and marketing services company.

References:

https://www.idc.com/getdoc.jsp?containerId=prUS48948422

https://www.idc.com/getdoc.jsp?containerId=US48891622

Global market for private networks to exceed $109 billion in 2030: Study

https://www.3gpp.org/DynaReport/GanttChart-Level-2.htm (Release 16)

Strand Consult: MWC 2022 Preview and What to Expect

by John Strand

Tomorrow the Mobile World Congress (MWC) opens physically in Barcelona and also online. Every year for the last 19 years, Strand Consult has published previews of the Mobile World Congress (MWC). After its cancellation in 2020, MWC 2021 was a shadow of its former self, though the hybrid in person/online format brought 30,000 participants. 2022 promises to bring some 50,000, one of the largest gatherings since the pandemic began.

Recall that 2019 MWC had some 110,000 participants and 2400 exhibitors. It’s come a long way from its start 36 years ago in Cannes, cozy enough that attendees to mingle at the Hotel Majestic’s bar following each day’s events.

Like the process for MWC, many people have been returning to normal after Covid. However the world has been gripped by the invasion of Ukraine by Russia, an absurd act against a sovereign, democratic nation which became independent in August 1991. Most democratic countries are united against Russia’s action. GSMA canceled the event’s Russian Pavilion and barred some Russian firms per international sanctions. Consider how Telenor stood up to dictatorship in Myanmar: by selling their assets and leaving the country. Pressure could grow for GSMA to suspend its Russian members.

Covid-19 has had a big impact on how people use mobile telecom services as well as the over-top players like Google, Facebook, Amazon, Apple etc. Historically GSMA kept a low profile on political matters. However that is increasingly difficult in a connected world when people communicate globally and have expectations of their service providers. Mobile operators and trade organizations like GSMA no longer have the luxury to focus solely on short-term profit and remain passive to aggression and autocracy.

MWC Buzzwords: 5G, OpenRAN, AI, Cloud, IoT, Green, and Diversity:

GSMA Director General Mats Granryd will open the conference, and it’s natural that this Swede would look to create consensus among 750 mobile operator members. He has a tough job to tell regulators that the industry needs better conditions while defending his members’ request for subsidies among other industries which have fared far worse than mobile telecommunications. As usual, he will focus on the latest hype and avoid the uncomfortable, which is too bad for journalists who want answers to critical questions.

Granryd will probably make the point that 5G is growing quickly: over 200 5G mobile networks based on 3GPP standards have now been launched around the world. If 4G was about the smartphone app economy, 5G is about disrupting the wireline home broadband market and opportunities for industry to integrate people and machines intelligently. There are hundreds of millions of new 5G customers. It’s an impressive accomplishment, but it’s doubtful that this can be turned into greater revenue for mobile operators’ shareholders. To date, the money has flowed to Big Tech.

Granryd will also tout the greening of the industry, though careful not to point out that the total energy footprint of the industry is growing. More traffic, devices, connections, network sites, and applications means more energy use. Not all of this is green and much is “greenwashing.”

The other hot topic is diversity, which has been moved from the last day of the conference to the first. The new Diversity4Tech replaces what was Women4Tech, an effort ended prematurely without success. Indeed, half of the world’s mobile subscribers are women, but there are still too few female executives in the mobile industry. Only 3 of GSMA’s 26 board members are women. It’s embarrassing that GSMA has not performed better on this metric. The only woman in the mobile leader line up is President & CEO of Telia Allison Kirkby who speaks on the New Tech Order. Tellingly, the session features three Chinese men: Yang Jie, Chairman, China Mobile; Ruiwen Ke, Chairman & CEO, China Telecom; and LieHong Liu, Chairman & CEO, China Unicom. Diversity, equity, and inclusion (DEI) are unlikely to be themes in the remarks of China’s state-owned operators. Moreover, they are unlikely to mention state-sponsored cyberattacks which are growing more frequent, more sophisticated, and more severe.

Oddly enough this MCW features a keynote by FC Barcelona President Joan Laporta. The program text boasts that the European football market is worth over $25 billion dollars and growing. In reality, football (soccer) is not an industry that mobile operators should emulate. Not only is FC Barcelona $1.57 billion in debt, it had to let Lionel Messi go because it couldn’t honor its financial contract. More largely, the salaries for superstars like Messi, Ronaldo and, others are breaking the cable industry. GSMA is probably thanking its lucky stars that it didn’t feature Chelsea FC owner Roman Abramovich, a Russian oligarch and Friend of Putin who invested in the UK’s Truphone in 2006.

In any event, Ukraine is a communication game changer. Look at Germany’s Chancellor Olaf Scholz now committing to pay the full freight of NATO dues, something that former Chancellor Merkel refused do to.

Regulation, the never-ending story:

MWC should be the opportunity for mobile operators take a victory lap. The mobile telecom industry salvaged society from the pandemic, allowing people to work, learn and receive health care from home. Moreover, many operators have commendable plans to be carbon neutral in the near future. Yet GSMA has failed utterly to build on mobile operators’ good citizenship to modernize regulation and kick start much-needed consolidation. Instead many authorities want to double-down on failed regulatory policies like net neutrality and are even-more entrenched against mergers. GSMA lacks a coherent strategy of policy and communication to convince competition authorities and regulators to adopt a modern framework for consolidation, investment, and innovation.

Strand Consult has studied mobile industry consolidation globally for more than 20 years and just published the definitive report on 4 to 3 mobile mergers. It describes why European operators don’t pass the acid test on consolidation and why they fail to succeed.

Strand Consult has published hundreds of research notes, reports, and articles about net neutrality around the world. Notably the leading countries for 5G; Japan, South Korea, China, and USA have no net neutrality rules, or only soft rules. It is no surprise that European countries were late to 5G. Strand Consult has documented how the Body of European Regulators (BEREC) has consistently prioritized the needs of a small cadre of so-called “civil society” advocates over Europeans as whole who want more mobile telecom innovation and investment.

More largely, the measures taken by the European Union to “tame” Big Tech have had the opposite effect. Since Margrethe Vestager became Competition Commissioner in November 2017, Big Tech companies have increased their turnover, market share and earnings.

GSMA promotes Clouds:

Where GSMA fails to communicate the value proposition of mobile operators and demand the needed regulatory update, it does a great job to promote cloud providers. Once again, mobile operators are set up to be the biggest losers while Big Tech firms Google, Apple, Amazon, and Microsoft are poised take the lion’s share of the 5G profits of connectivity, just as they did with 4G.

Few understand what AWS means for Amazon. AWS controls about a third of the global cloud market, substantially more its closest competitors Microsoft Azure and Google Cloud. In Q4 FY 2021 AWS generated net sales of $17.8 billion and operating income of $5.3 billion. Net sales grew 39.5% while operating income rose 48.5% compared to the year ago quarter. The value continues to increase as cloud services are integrated with artificial intelligence (AI) and other services.

Here are some critical questions to help you navigate the “cloudnet” sessions

- Why are clouds, which are fundamental to the running of 5G and 5G services, not subject to regulation, like mobile operators?

- Why do regulators obsess about market power of mobile operators while being oblivious to cloud providers Google, Microsoft, Amazon, and increasingly Huawei?

- What has been governments’ strategic blunder in the focus of restricting Huawei in 5G? (Hint: They forget about Huawei in the cloud. See Strand Consult’s note.

- How easy or difficult is it for customers to migrate from one cloud to another? Is data portable from Amazons AWS to Microsoft´s Azure?

3G, 4G, 5G: Where does the cash flow?

At MWC, there is always discussion about the next generation or G. However there is little discussion of the cash flow. Here are the cold, hard facts to consider.

- Many mobile operators believed in 2000 that 3G would be a gold mine for their revenues. They spent billions of euros on spectrum, but the revenue projections that ARPU will grow from to €36 to €72 per month fell far below expectation, ARPU declined.

- There are very few examples of successful partnerships that mobile operators have realized under 3G and 4G. In general, the revenue has flowed to the OTT or third-party providers, not operators.

- The value created in 4G has flowed to Google’s and Apple’s app stores which take a significant revenue cut of the apps on offer.

- Over the years, operators have attempted to launch various application programming interfaces (APIs) that third parties could integrate into their services. Some of these actions have been successful, like premium SMS. From 1998 onwards, mobile operators have been successful to offer premium SMS to pay for various digital services. Strand Consult was the first to publish research on this market and business models. Many of the world’s mobile operators followed our recommendations when it came to how to implement and operate a market with a short code where mobile customers could use to pay for services. See Strand Consult’s old report and research note about premium SMS

- Later around 2009 at MWC, GSMA launched OneAPI, about which we published a lot of research. Unfortunately, the operators did not know how to operate this market and create an ecosystem. Look at the research note ”One API is good news”. While this was a welcome development at the time, it did not develop into a revenue stream.

- Since that time, operators have been transformed into “dumb pipes”, mainly generating revenue from traffic they sell, not by adding value with better or different services. Mobile operators have little to no ability to monetize their own value-added services. In fact WhatsApp has cannibalized mobile operators’ SMS revenue. For example from 2012 to 2013, KPN´s SMS revenue declined by €100 million as customers switched to WhatsApp for messaging.

- There is only limited experience to reference for mobile operators’ 5G partnerships. The current version of 5G is 3GPP release 14 and 15 which do not have a functionality that is more advanced than 4G. Mobile operators have a dream to make money from 5G in the same way they dreamed it for 3G and 4G.

- Moreover, the EU regulatory environment with hard net neutrality rules and BEREC’s draconian over-interpretation of the rules have created an environment which discourages, if not prohibits, partnerships for mobile operators in 5G. It is not surprising that telecom investment has languished for years in EU.

- At MWC there are likely many PowerPoint presentations which describe proposed partnerships between mobile operators and other technology providers. However the business models are not in place, and many mobile operators have an unrealistic view of their ability to monetize value-added services.

- The reality is that to innovate in 5G, firms like Apple and Google, only need to add a new layer on their existing business. They are a proven partner. However mobile operators are required to do the essential retooling of networks. Mobile operators thus have a higher bar for 5G. They have to build an new ecosystem to convince a partner to join, where as Apple, Google and AWS only need, to extend their ecosystem with 5G services.

The role of mobile operators in the value chain has been decimated in the last two decades. It is not a question how mobile operators will react to 5G, but whether they have the skills at all to execute.

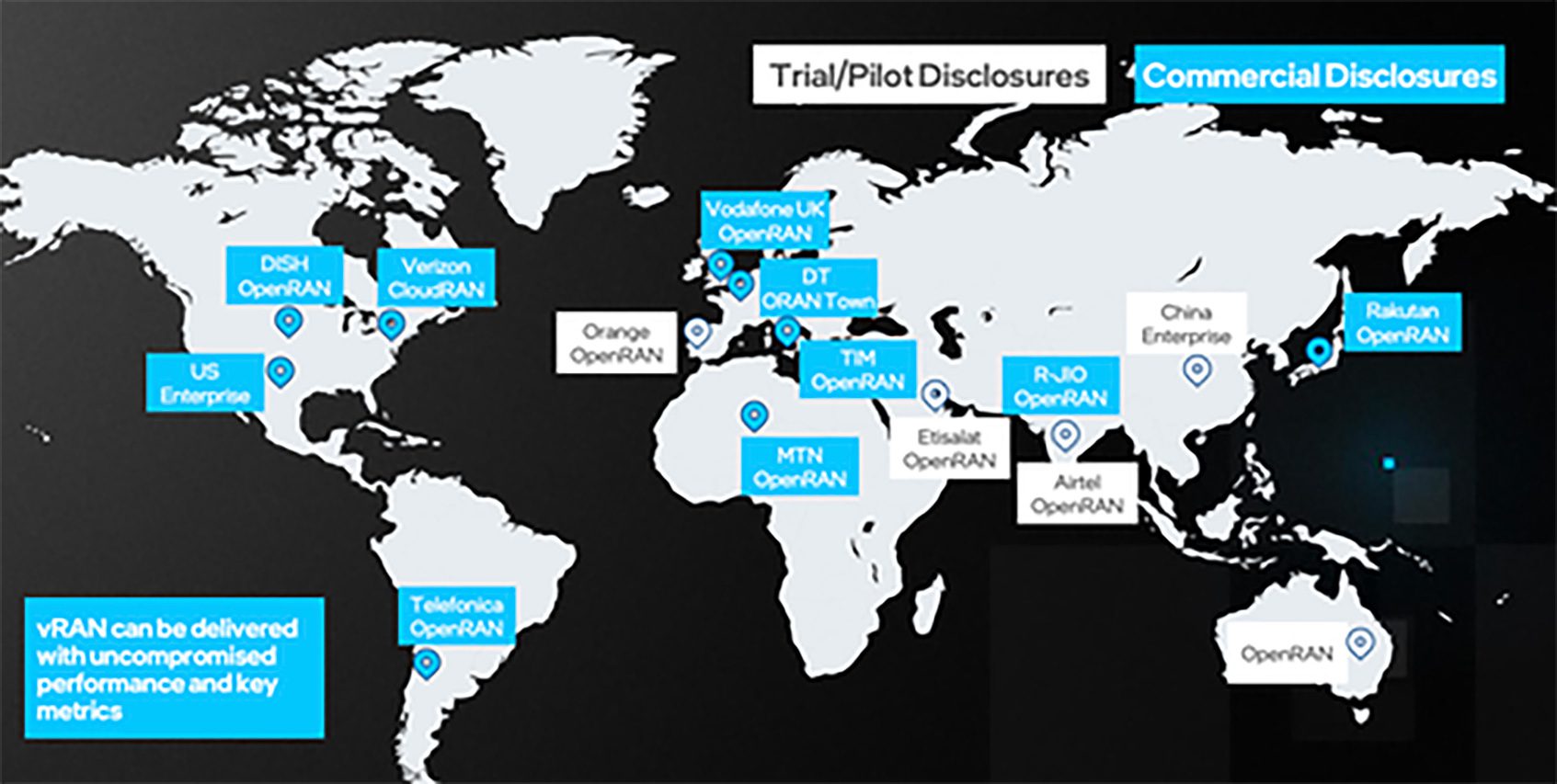

OpenRAN and Vendor Diversity – What does that mean?

The latest MWC hype is OpenRAN and the invented term “vendor diversity”. Much of the hype is driven by OpenRAN players which claim that the market for mobile infrastructure equipment is controlled by Huawei, Ericsson, Nokia and ZTE. However, MWC features some 2000 exhibitors which supply infrastructure equipment to over 750 mobile operators. Note that the need for “vendor diversity” is not addressed with cloud providers.

Many OpenRAN pronouncements sound too good to be true, for example a technology that can reduce mobile operators infrastructure CAPEX and OPEX by 30-40 percent. Investors and other decision makers want objective information about the latest mobile industry hype. Strand Consult’s free report Debunking 25 Myths of OpenRAN examines the claims made by OpenRAN proponents. Strand Consult, having witnessed the launch of WiMax, OneAPI, and the iPhone among other hyped technologies promised to bring windfall revenues to mobile operators, provides critical questions to evaluate OpenRAN in its latest report.

The main challenge for OpenRAN is whether it can be relevant for operators which have very little room for margin of error. OpenRAN is far from being able to replace classic infrastructure on a 1:1 basis.

OpenRAN testing has been launched in a world in which mobile operators buy and build classic RAN at a high rate. There are two reference cases. One is Rakuten in Japan driven by charismatic CEO Tareq Amin. Rakukten gives away free traffic without getting paying customers into the store. It’s solution is proprietary, not open.

The US-based Dish is the second. It faces many challenges which make it hard to see how it can become a serious alternative to Verizon, AT&T and T-Mobile

The Federal Communication Commission (FCC) proceeding on OpenRAN showed few, if any examples, of US mobile operators and their trade associations (CTIA, Rural Wireless Association, and Competitive Carriers Association) testifying that OpenRAN is a serious alternative to classic RAN installations.

MWC offers an opportunity to meeting mobile operators’ Chief Technology Officers. Ask them what they think of OpenRAN why they have launched 5G using classic RAN based on 3GPP standards.

The history of OpenRAN is reminiscent of WiMax. If you have some of the PowerPoints from the early 2000s, you will see how infrastructure vendors talked about why WiMax was so amazing. These points are almost identical to what is asserted about OpenRAN.

To assess claims about vendor diversity, it’s important to look at facts and history. The infrastructure supplier market has consolidated from 20 top tier providers in the 2G market in 1989 to 12 top tier providers in 1999 to 5 top tier providers in 2019. Many of the first-generation enthusiasts did not make it out of the 1G analogue cellular world into the world of 2G digital cellular. Over time the GSM standards family (GSM, WCDMA, LTE etc.) became the de facto basis for the roadmap, the standard for global economies of scale and the industry benefits such as lower unit costs. Those equipment suppliers which focused on CDMA and analog exited the market.

There is also the practical issue of math. The notion of vendor diversity for its own sake challenges operators to reduce complexity and cost in their networks. Operators frequently reduce the number of vendors to improve security (ability to vet vendors and develop trusted relationships) and to lower cost (ability to secure volume discounts). Indeed operators want concentration in part to get better value for money.

Note how Neil McRae, Managing Director and Chief Architect at British Telecom described when he got the question; “The major operators have been telling their shareholders since 2000 that they should reduce suppliers to save money?”. He replied, I have worked with BT for 10 years. When I arrived, BT had a 21 C fixed network with 50 vendors. I reduced it to 4 vendors and saved BT £1 billion in 3 years. The key was reducing complexity, which is the killer in telecommunications. When I hear about Open architectures with 5- 50 vendors, I run for the hills. Reducing vendors was the right thing to do and we would do it again.” RAN, while important, is just one part of an operator’s infrastructure requirements.

Moreover, the consolidation of European infrastructure is the result of many European operators having opted into Huawei and opted out of European suppliers.

The active customer base of Europe’s 102 mobile operators is 673 million subscribers. Huawei’s and ZTE’s share of 4G RAN mobile networks are 44% and 4% respectively, total 48%.This means that 325 million European mobile customers access Chinese infrastructure, primarily from Huawei. Countries are divided into four categories of share of 4G RAN equipment from Chinese suppliers: 75-100%; 50-75%; 25-50%; and less than 25%.In its RAN report Strand Consult has mapped the market for 4G RAN in Europe.

More than 40% of the CAPEX that European operators have used every year for the last 10 years has been shipped to China and Chinese suppliers like Huawei and ZTE. If you look at the American operators, most of their CAPEX has gone to European suppliers Nokia and Ericsson. We thought that the EU should thank the US operators and the US government for their massive support for European manufacturers and for their fight against the use of Chinese equipment from Huawei and ZTE. The five operators Vodafone, TIM, Telefonica, Orange and Deutsche Telekom have for several years opted for Chinese manufacturers at the expense of European vendors. 62% of Vodafone´s 4G RAN in Europe are from Huawei.

The fact is that RAN Capex makes up less than 3 percent of a mobile operator’s ARPU. The global RAN market is today $29 billion and can be pitted against Verizon’s Capex which amounts to $18 billion.

The bottom line for MWC

Strand Consult has limited expectation for mobile operators’ profitability in 5G. Operators may have ambitions, but the question is whether they have the skills to build an ecosystem that can compete with Apple, Google, and AWS. However, operators can do better on the policy front to modernize regulation and promote consolidation.

Under the current frameworks, there is little to no upside for operators. Mobile operators must consolidate to cut cost and increase profitability. They will probably continue to sell off infrastructure. They continually become dumb pipes. There’s nothing wrong with being a dumb pipe; it’s a business model that works quite fine in water and energy. But don’t expect it to be innovative.

In practice, this development means that many functions from telecom regulators have become irrelevant. The primary task of the telecom regulator of the future will be to deal with spectrum.

Technology companies build services on top of US and Chinese platforms. Many of the smaller technology companies are driven by the construction of a business with the aim of being acquired by these tech companies. A good example is Facebook’s purchase of WhatsApp for $16 billion in February 2014.

There will be many interesting discussions on 5G, OpenRAN, IOT and AI, including the need for more security and transparency. In any event, MWC is always a party because of the cool people who attend giving food for thought to those who want to be stimulated intellectually. Moreover Barcelona’s bars and restaurants rarely disappoint.

Strand Consult provides both pre and post review of the Mobile World Congress. Read reviews from the past years.

Meet Strand Consult at the Mobile World Congress:

If you would like to meet with Strand Consult during the MWC, please email your contact details and the details/purpose of the meeting, and we will get back to you. Journalists are most welcome!

………………………………………………………………………………………………………………………………………………………………………

Biography:

John Strand founded Strand Consult in 1995. Since then, hundreds of companies in the telecom, media and technology industries have attended Strand Consult’s workshops, purchased reports, consulted with the company to develop strategy, launch new products, and conduct a dialogue with policymakers.

John Strand sits on the advisory board of a number of Scandinavian and International companies and is a member of the Arctic Economic Council Telecommunications Working Group. He served on the Advisory Board for the 3GSM World Congress, the event known as the Mobile World Congress in Barcelona.

References:

Strand Consult: Open RAN hype vs reality leaves many questions unanswered

O-RAN Alliance tries to allay concerns; Strand Consult disagrees!

Intel FlexRAN™ gets boost from AT&T; faces competition from Marvel, Qualcomm, and EdgeQ for Open RAN silicon

Dell’Oro Group estimates the RAN market is currently generating between $40 billion and $45 billion in annual revenues. The market research firm forecasts that Open RAN will account for 15% of sales in 2026. Research & Markets is more optimistic. They say the Open RAN Market will hit $32 billion in revenues by 2030 with a growth rate of 42% for the forecast period between 2022 and 2030.

As the undisputed leader of microprocessors for compute servers, it’s no surprise that most of the new Open RAN and virtual RAN (vRAN) deployments use Intel Xeon processors and FlexRAN™ software stack inside the baseband processing modules. FlexRAN™ is a vRAN reference architecture for virtualized cloud-enabled radio access networks.

The hardware for FlexRAN™ includes: Intel® Xeon® CPUs 3rd generation Intel® Xeon® Scalable processor (formerly code named Ice Lake scalable processor), Intel® Forward Error Correction Device (Intel® FEC Device), Mount Bryce (FEC accelerator), Network Interface Cards – Intel® Ethernet Controller E810 (code name Columbiaville). Intel says there are now over 100 FlexRAN™ licensees worldwide as per these charts:

Source: Intel

A short video on the FlexRAN™ reference architecture is here.

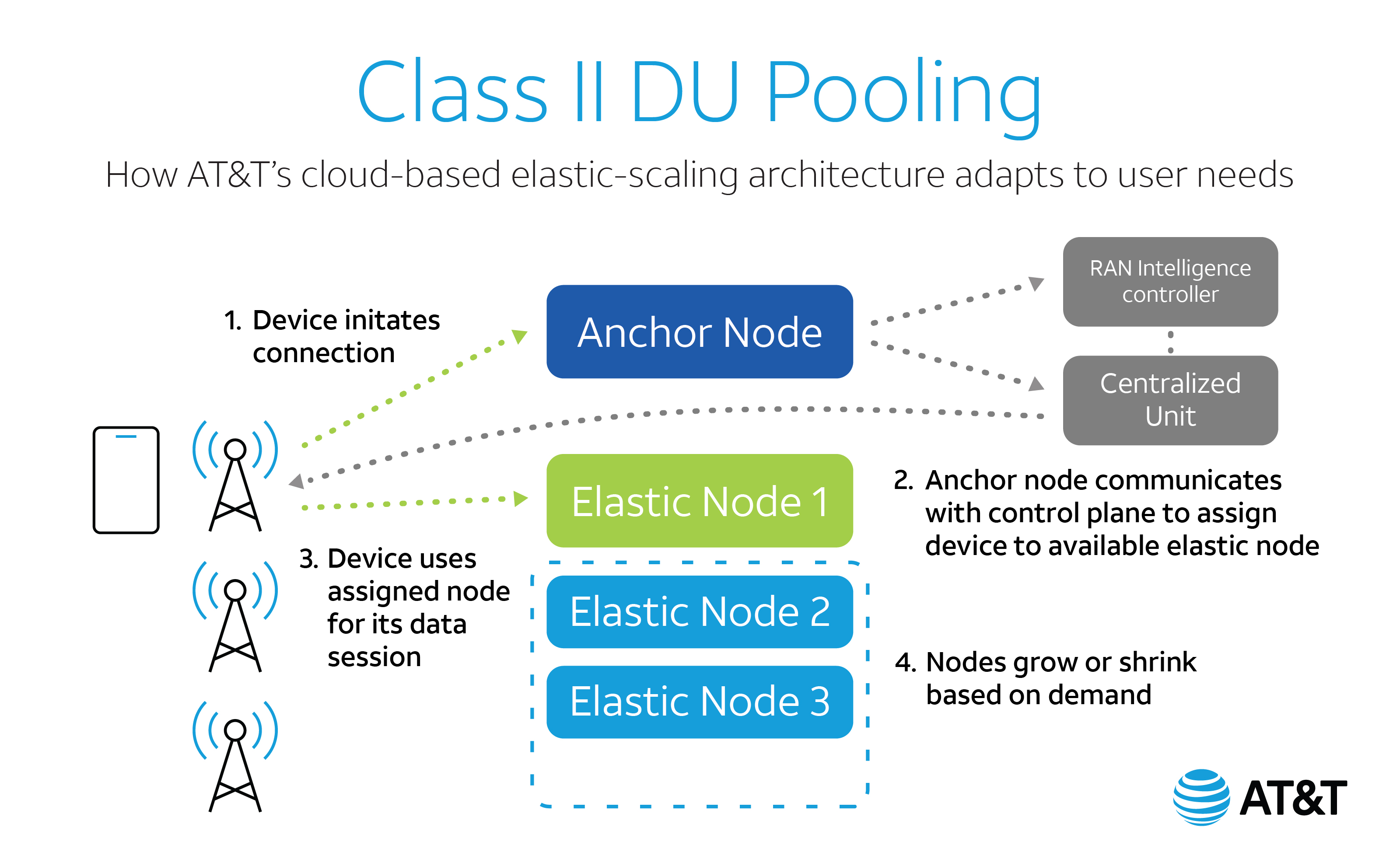

FlexRAN™ got a big boost this week from AT&T. In a February 24, 2022 blog post titled “Cloudifying 5G with an Elastic RAN,” Gordon Mansfield, AT&T VP Mobility Access & Architecture said that “AT&T and Intel had co-developed an industry-leading advanced RAN pooling technology freeing 5G radios from the limitations of dedicated base stations, while enabling more efficient, resilient, and green 5G networks. DU-pooling will eventually be usable by the entire 5G operator community to drive the telecom industry’s goals of green and efficient wireless networks forward.”

DU pooling technology was made possible by combining AT&T’s deep knowledge of Open RAN technologies as one of the co-founders of the O-RAN Alliance with Intel’s expertise in general purpose processors and software-based RAN through its FlexRAN™ software stack running on Intel 3rd generation Intel® Xeon® Scalable processors. The open standards for communications between radios and DUs that were published by O-RAN enabled its development, and the result is a technology demonstrator implemented on FlexRAN™ software.

………………………………………………………………………………………………………………………………………………………………………………..

Intel is now facing new Open RAN competition from several semiconductor companies.

Marvell has just unveiled a new accelerator card that will slot into a Dell compute server (which uses x86 processors). Based on a system called “inline” acceleration, it is designed to do baseband PHY layer processing and do it more efficiently than x86 processors. A Marvell representative claims it will boost open RAN performance and support a move “away from Intel.” Heavy Reading’s Simon Stanley (see below) was impressed. “This is a significant investment by Dell in open RAN and vRAN and a great boost for Marvell and the inline approach,” he said.

Qualcomm, which licenses RISC processors designed by UK-based ARM, has teamed up with Hewlett Packard Enterprise (HPE) on the X100 5G RAN accelerator card. Like Marvel’s offering, it also uses inline acceleration and works – by “offloading server CPUs [central processing units] from compute-intensive 5G baseband processing.”

There is also EdgeQ which is sampling a “Base Station on a Chip” which is targeted at Open RAN and private 5G markets. Three years in the making, EdgeQ has been collaborating with market-leading wireless infrastructure customers to architect a highly optimized 5G baseband, networking, compute and AI inference system-on-a-chip. By coupling a highly integrated silicon with a production-ready 5G PHY software, EdgeQ uniquely enables a frictionless operating model where customers can deploy all key functionalities and critical algorithms of the radio access network such as beamforming, channel estimation, massive MIMO and interference cancellation out of the box.

For customers looking to engineer value-adds into their 5G RAN designs, the EdgeQ PHY layer is completely programmable and extensible. Customers can leverage an extendable nFAPI interface to add their custom extensions for 5G services to target the broad variety of 5G applications spanning Industry 4.0 to campus networks and fixed wireless to telco-grade macro cells. As an industry first, the EdgeQ 5G platform holistically addresses the pain point of deploying 5G PHY and MAC software layers, but with an open framework that enables a rich ecosystem of L2/L3 software partners.

The anticipated product launches will be welcomed by network operators backing Open RAN. Several of them have held off making investments in the technology, partly out of concern about energy efficiency and performance in busy urban areas. Scott Petty, Vodafone’s chief digital officer, has complained that Open RAN vendors will not look competitive equipped with only x86 processors. “Now they need to deliver, but it will require some dedicated silicon. It won’t be Intel chips,” he told Light Reading in late 2021.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Inline vs Lookaside Acceleration:

While Marvell and Qualcomm are promoting the “inline” acceleration concept, Intel is using an alternative form of acceleration called “lookaside,” which continues to rely heavily on the x86 processor, offloading some but not all PHY layer functions. This week, Intel announced its own product refresh based on Sapphire Rapids, the codename for its next-generation server processors.

Simon Stanley, an analyst at large for Heavy Reading (owned by Informa), said there are two key innovations. The first involves making signal-processing tweaks to the Sapphire Rapids core to speed up the performance of FlexRAN™, Intel’s baseband software stack. Speaking on a video call with reporters, Dan Rodriguez, the general manager of Intel’s network platforms group, claimed a two-fold capacity gain from the changes. “In the virtual RAN and open RAN world, the control, packet and signal processing are all done on Xeon and that is what FlexRAN enables,” he said.

The other innovation is the promise of integrated acceleration in future Sapphire Rapids processors. Sachin Katti, who works as chief technology officer for Intel’s network and edge group, said this would combine the benefits of inline acceleration with the flexibility of x86. That is preferable, he insisted, to any solution “that shoves an entire PHY layer into an inflexible hardware accelerator,” a clear knock at inline rivals such as Marvell and Qualcomm. Despite Katti’s reference to inline acceleration, Stanley does not think it is Intel’s focus. “None of this rules out an inline acceleration solution, but it does not seem to be part of the core approach,” he told Light Reading. “The key strategy is to add maximum value to Xeon Scalable processors and enable external acceleration where needed to achieve performance goals.”

Both inline and lookaside involve trade-offs. Inline’s backers have promised PHY layer software alternatives, but Intel has a major head start with FlexRAN™, which it began developing in 2010. That means lookaside may be a lot more straightforward. “The processor is in control of everything that goes on,” said Stanley during a previous conversation with Light Reading. “It is essentially the same software and makes life very easy.”

Larger network operators seemed more enthusiastic about inline during a Heavy Reading survey last year. By cutting out the processor, it would reduce latency, a measure of the delay that occurs when signals are sent over the network. That could also weaken Intel, reducing power needs and allowing companies to use less costly CPUs. “If you use inline, you probably need a less powerful processor and less expensive server platform, which is not necessarily something Intel wants to promote,” Stanley said last year.

References:

https://www.intel.com/content/www/us/en/communications/virtualizing-radio-access-network.html

EdgeQ Samples World’s 1st Software-Defined 5G Base Station-on-a-Chip

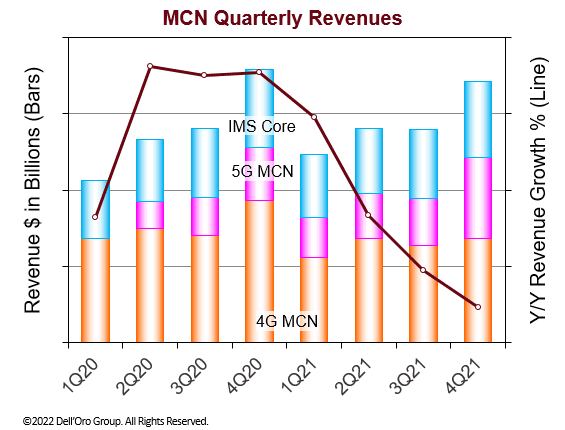

Dell’Oro: Mobile Core Network and MEC Stagnant in 2021; Will Growth in 2022

According to a recently published report from Dell’Oro Group, the total Mobile Core Network (MCN) and Multi-access Edge Computing (MEC) market 2021 revenue growth slowed to the lowest rate since 2017. The growth rate is expected to go higher in 2022 with the expansion of the 21 commercial 5G Standalone (5G SA) MBB networks that were deployed by the end of 2021, coupled with new 5G SA networks readying to launch throughout the year.

“MCN revenues for 2021 were lower than expected due to an unexpectedly poor fourth quarter performance. The revenues for 4Q 2021 were lower than in 4Q 2020. The last time that happened was in 4Q 2017,” stated Dave Bolan, Research Director at Dell’Oro Group. “The poor performance in 4Q 2021 was due to negative year-over-year revenue performance for the China region. The performance for the rest of the world was almost flat but still negative and obviously was not enough to offset the decline in China.

“The growth in 2021 came from the 5G MCN segment and was not enough to offset the decline in 4G MCN and IMS Core. Of the 21 5G SA networks commercially deployed Huawei is the packet core vendor in seven of the networks, including the three largest networks in the world located in China, and Ericsson is the packet core vendor in 10 of the networks. Not surprisingly, of the top five vendors, only Huawei and Ericsson gained overall MCN revenue market share during 2021.

“Looking at the MEC market, MEC is still a fraction of the overall MCN market, but we believe two recent announcements by Ericsson are noteworthy because, in our opinion, Ericsson will accelerate the adoption of MEC and help 5G MNOs monetize their networks by coalescing MEC implementations around the 3GPP standards. Ericsson claims to be the first to leverage recent advancements by the 3GPP standards body for edge exposure, and network slicing all the way through to a smartphone,” continued Bolan.

Additional highlights from the 4Q 2021 Mobile Core Network Report:

- Top-ranked MCN vendors based on revenue in 2021 were Huawei, Ericsson, Nokia, ZTE, and Mavenir.

- The EMEA region was the only region to grow in revenue in 2021.

- The APAC region was the largest region in revenue for 2021.

As of December 31, 2021 there were 21 known 5G SA eMBB networks commercially deployed.

|

5G SA eMBB Network Commercial Deployments |

|

|

Rain (South Africa) |

Launched in 2020 |

|

China Mobile |

|

|

China Telecom |

|

|

China Unicom |

|

|

T-Mobile (USA) AIS (Thailand) True (Thailand) |

|

|

China Mobile Hong Kong |

|

|

Vodafone (Germany) |

Launched in 2021 |

|

STC (Kuwait) |

|

|

Telefónica O2 (Germany) |

|

|

SingTel (Singapore) |

|

|

KT (Korea) |

|

|

M1 (Singapore) |

|

|

Vodafone (UK) |

|

|

Smart (Philippines) |

|

|

SoftBank (Japan) |

|

|

Rogers (Canada) |

|

|

Taiwan Mobile |

|

|

Telia (Finland) |

|

|

TPG Telecom (Australia) |

|

The Dell’Oro Group Mobile Core Network & Multi-Access Edge Computing Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, shipments, and average selling prices for Evolved Packet Core, 5G Packet Core, Policy, Subscriber Data Management, and IMS Core including licenses by Non-NFV and NFV, and by geographic regions. To purchase this report, please contact us at [email protected].

References:

https://www.delloro.com/news/mobile-core-network-stagnant-in-2021-poised-for-growth-in-2022/

https://techblog.comsoc.org/2021/12/01/delloro-5g-sa-core-network-launches-accelerate-14-deployed/

Vi and A5G Networks partner to enable Industry 4.0, Smart Cities in “Digital India” using 4G spectrum

India network operator Vodafone Idea Limited (Vi) today announced its collaboration with Nashua, NH based A5G Networks, Inc. to enable industry 4.0 and smart mobile edge computing in India.

Vi and A5G Networks have together set up a pilot private network in Mumbai utilizing existing 4G spectrum.

Vi’s association with A5G Networks is in line with its commitment to realize Digital India dreams with the latter’s differentiated and unique 4G, 5G, and Wi-Fi autonomous software for distributed Networks. A5G Networks software is fully cloud-native containerized built for hybrid and multi-cloud infrastructure.

“Vi is committed to providing superior services to digital enterprises and consumers to enhance user experiences, empowered by an autonomous network,” said Mr. Jagbir Singh, Chief Technology Officer, Vodafone Idea Ltd. “As part of our digital transformation journey on the 5G roadmap, we are happy to partner with A5G Networks to bring new services enabling industry 4.0 and smart cities in the digital era.”

“We are excited to be a part of this important journey for Digital India with Vi,” said Rajesh Mishra, Founder, and CEO of A5G Networks. “Vi is committed to delivering best-in-class services to their subscribers and driving the Digital India movement. Success depends upon a highly resilient, secure, and flexible network infrastructure.

In November 2020, Mishra told Light Reading he decided to start A5G Networks due to the growth in the Open RAN market, where Parallel Wireless has been a leading player. “When you have a lot of [Open] RANs, what happens then?” Mishra said, explaining that A5G Networks will sell software for network orchestration. “The timing was right,” he said of his departure from Parallel Wireless, citing the status of open RAN in the wider wireless market. “I’ve got to start working and building.”

Vi is partnering with technology leaders and innovators to set up digital networks enabling several low latency applications, private networks, smart cities, and connected cars.

The 5G Open Innovation Lab (“5GOILab”), a global applied innovation ecosystem for corporations, academia and government institutions, selects 15 early- to late-stage companies twice a year to join our enterprise innovation program. Companies are led by founders that have demonstrated a vision and strategy for leveraging 5G networks to achieve digital transformation in the enterprise and advance applications and solutions in artificial intelligence, augmented reality, edge computing and IoT. A5G and Santa Clara CA based EdgeQ (4G/5G base station on a chip) were selected to participate. A5G Networks for enabling distributed and disaggregated network of networks to create autonomous private and public 4G, 5G, and WiFi Networks.

The Lab does not take an equity position in its member companies, rather, companies collaborate with 5G technology experts and business advisors through CEO and CTO roundtables, private working sessions, virtual networking and social events, and opportunities to meet with the Lab’s extensive partner network of venture capital firms.

About Vodafone Idea Limited:

Vodafone Idea Limited is an Aditya Birla Group and Vodafone Group partnership. It is India’s leading telecom service provider. The Company provides pan India Voice and Data services across 2G, 3G, 4G and has a 5G ready platform. With the large spectrum portfolio to support the growing demand for data and voice, the company is committed to deliver delightful customer experiences and contribute towards creating a truly ‘Digital India’ by enabling millions of citizens to connect and build a better tomorrow. The Company is developing infrastructure to introduce newer and smarter technologies, making both retail and enterprise customers future ready with innovative offerings, conveniently accessible through an ecosystem of digital channels as well as extensive on-ground presence.

The company offers products and services to its customers in India under the TM Brand name “Vi”.

For more information, please visit: www.MyVi.in and www.vodafoneidea.com

About A5G Networks Inc:

A5G Networks Inc. is a leader and innovator in autonomous mobile network infrastructure. The company is headquartered in Nashua, NH, USA with offices in Pune MH, India. A5G Networks is pioneering secure and scalable 4G, 5G and Wi-Fi software to enable distributed network of networks. To learn more about A5G Networks, visit www.a5gnet.com

References:

GSA: Private Mobile Networks Summary-2022

Introduction:

The demand for private mobile networks based on 4G LTE (and increasingly 5G) technologies is being driven by the spiralling data, security, digitisation and enterprise mobility requirements of modern business and government entities. Organisations of all types are combining connected systems with big data and analytics to transform operations, increase automation and efficiency or deliver new services to their users. Wireless networking with LTE or 5G enables these transformations to take place even in the most dynamic, remote or highly secure environments, while offering the scale benefits of a technology that has already been deployed worldwide.

The arrival of LTE-Advanced systems delivered a step change in network capacity and throughput, while 5G networks have brought improved density (support for larger numbers of users or devices), even greater capacity, as well as dramatic improvements to latency that enable use of mobile technology for time-critical applications.

Private mobile networks are often part of a broader digital transformation programme in an organisation. This could include the introduction or development of cloud networking and other digital technologies such as artificial intelligence and machine learning, and data analytics. More and more applications of the private mobile network will use these capabilities combined with mobile connectivity.

In addition to companies looking to deploy their own private mobile network for the first time, there is a large group of potential customers that currently operate private networks based on technologies such as TETRA, P25, Digital Mobile Radio, GSM-R and Wi-Fi. Many of these customers are demanding critical broadband services that are simply not available from alternative technologies, so private mobile networks based on LTE and 5G could eventually replace much of this market.

The exact number of existing private mobile network deployments is hard to determine, as details are not often made public. To improve information about this market, GSA is now maintaining a database of private LTE and 5G networks worldwide.

Since the last market update, GSA has been working with Executive Members Ericsson, Huawei and Nokia on harmonising definitions of what counts as a valid private mobile network, and on harmonising sector definitions. That work has led to a restatement of some of GSA’s market statistics.

The definition of a private mobile network used in this report is a 3GPP-based 4G LTE or 5G network intended for the sole use of private entities, such as enterprises, industries and governments. The definition includes MulteFire or Future Railway Mobile Communication System. The network must use spectrum defined in 3GPP, be generally intended for business-critical or mission-critical operational needs, and where it is possible to identify commercial value, the database only includes contracts worth more than €100,000, to filter out small demonstration network deployments.

Private mobile networks are usually not offered to the general public, although GSA’s analysis does include the following: educational institutions that provide mobile broadband to student homes; private fixed wireless access networks deployed by communities for homes and businesses; city or town networks that use local licences to provide wireless services in libraries or public places (possibly offering Wi-Fi with 3GPP wireless backhaul) which are not an extension of the public network.

Non-3GPP networks such as those using Wi-Fi, TETRA, P25, WiMAX, Sigfox, LoRa and proprietary technologies are excluded from the data set. Furthermore, network implementations using solely network slices from public networks or placement of virtual networking functions on a router are also excluded. Where identifiable, extensions of the public network (such as one or two extra sites deployed at a location, as opposed to dedicated private networks), are excluded. These items may be described in the press as a type of private network.

GSA has identified 58 countries and territories with private network deployments based on LTE or 5G, or where private network spectrum licences suitable for LTE or 5G have been assigned. In addition, there are private mobile network installations in various offshore locations serving the oil and gas industries, as well as on ships.

GSA has collated information about 656 organisations known to be deploying LTE or 5G private mobile networks. Since the last update of this report in November 2021, some organisations have been removed from the database and this analysis, owing to a lack of evidence that they met the definition criteria. These examples may be added again in the future.

GSA has counted over 50 equipment vendors that have been involved in the supply of equipment for private mobile networks based on LTE or 5G. Commercial availability of pre-integrated solutions from several equipment providers increased in 2021; these solutions aim to simplify adoption of private networks, which should add market impetus. In addition, GSA has identified more than 70 telecom network operators (counting national operators within the same group as distinct entities) involved with private mobile network projects. Also, global-scale cloud providers (often referred to as “hyperscalers”) are offering private mobile network solutions, sometimes in partnership with mobile operators or network suppliers. Their ability to exploit mass-scale cloud infrastructure and their existing presence in commercial enterprises is likely to drive additional growth in the private mobile network market.

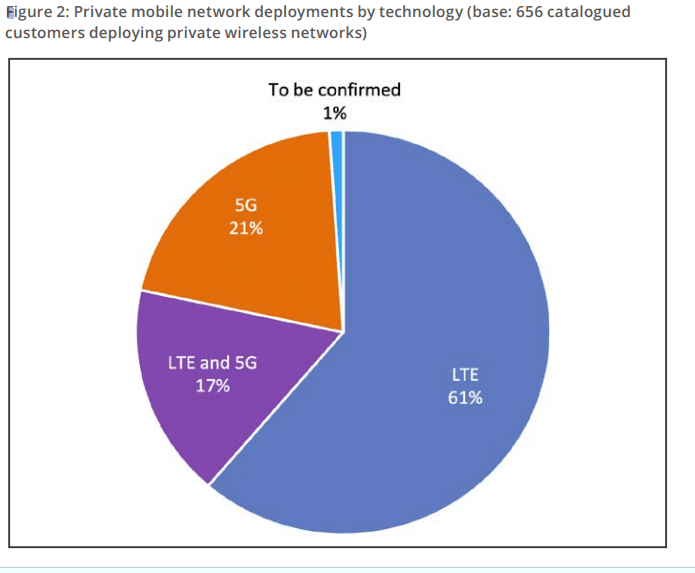

GSA has been able to categorise 656 customers deploying private mobile networks, which as Figure 1 shows, are located all around the world. Where organisations have subsidiaries in different countries or territories deploying their own networks, each subsidiary is counted separately. LTE is used in 78% of the catalogued private mobile network deployments for which GSA has data; 5G is being deployed in 38% of networks.

Dell’Oro Group forecasts a much smaller private wireless market share for 5G. They say LTE is dominating the private market in 2021 and 5G NR still on track to surpass LTE by the outer part of the forecast period, approaching 3 percent to 5 percent of the total 5G private plus public RAN market by 2026.

GSA also tracks the spectrum bands being used for deployments assigned specifically for local or private network purposes. Figure 4 shows that, including known spectrum assignments and deployments, C-band spectrum is the most widely assigned; TDD spectrum at 1.8 GHz comes second and is associated with the greatest number of identified deployments (more than 100 separate metro rail deployments in China). After that comes CBRS spectrum (also technically within the C-band but split out owing to the unusual way it has been assigned in the US).

There are more than 200 CBRS licensees, although they have not all been counted within the licence data, as it is not certain whether the spectrum will be used for public or private networks.

Telecom regulators are also showing signs of making increased allocations of dedicated spectrum available for private mobile networks — typically small tranches in specified locations. This could be acquired directly by organisations instead of by mobile operators, giving industries an alternative deployment model. Dedicated spectrum of this sort has already been allocated in France, the US, Germany and the UK, for example, and GSA expects this trend to be followed in other countries in 2022.

Note that owing to the removal of projects not meeting the new size requirement of at least €100,000, the counts are not directly comparable with those in the previous issue, although the patterns are the same.

GSA will be publishing further statistical updates covering the private mobile sector during 2022.

Acknowledgement: GSA would like to thank its Executive Members Ericsson, Huawei and Nokia for sharing general information about their network deployments to enable this dataset and report to be produced.

References:

https://gsacom.com/paper/private-mobile-networks-summary-february-2022/

Nokia and Mavenir to build 4G/5G public and private network for FSG in Australia

Australian rural carrier Field Solutions Holdings (FSG) has selected Nokia and Mavenir as its primary technology vendors to build Australia’s fourth mobile network.

As part of the deal, the technology partners will supply 4G and 5G radio access networks and the mobile core network. Mavenir will provide 4G/5G Converged Packet core, as well as IMS voice and messaging services.

FSG plans to deliver 4G and 5G services in rural, regional and remote areas of the country. FSG will also be delivering private 4G LTE and 5G service offerings. FSG, has secured 5G spectrum holdings to ensure that rural, regional and remote Australia is not left behind in the rollout of 5G services.

FSG CEO Andrew Roberts, said FSG’s 5G service will cover 85% of Australia’s landmass.

FSG CEO Andrew Roberts, said FSG’s 5G service will cover 85% of Australia’s landmass.

FSG CEO Andrew Roberts, said FSG’s 5G service will cover 85% of Australia’s landmass.“FSG has run a comprehensive 6-month RFP process to select the most appropriate technology partners for the rollout of the Regional Australia Network. FSG has selected these partners to ensure we have the cost-effective, future proof and globally proven technology platform needed to deliver Australia’s 4th mobile network.”

“The demand for private 4G and 5G networks is gaining momentum, FSG will be delivering cost-effective, carrier-grade private solutions for agri-business, mining and government. We expect to be announcing several private 4G and 5G private network deployments in the coming weeks,” said FSG CEO Andrew Roberts.

“Together with our new partners, Nokia and Mavenir, FSG is primed to deliver connectivity to regions, whilst offering capability for carriers to join the solution using Active Neutral host RAN, inbound roaming or ‘old school’ passive co-location on our purpose-built infrastructure,” Roberts added.

By embracing new models, the cost to deliver these solutions can be kept to a minimum, further supporting the committee’s desire to ensure that affordability is not forgotten. FSG are in the process of delivering 19 new place-based networks across Australia. These networks, comprising over 100 sites, each of which will be 4G and 5G capable, Neutral Host and Roaming ready when delivered in FY 23/24. “The Regional Australia Network is a dedicated network supporting rural Australia. Today, we operate Australia’s largest non-NBN fixed wireless network, which delivers fixed wireless broadband across rural, regional and remote Australia. The Regional Australia Network (RAN(TM)) will see these current and all new networks being enabled to delivery 4G and 5G data and voice services, fixed wireless broadband together with NB-IoT and CatM1 services”, Roberts stated.

FSG also said that the company is in the process of delivering 19 new “place-based” networks across Australia. These networks comprise more than 100 sites, each of which will be 4G and 5G capable, neutral host and roaming-ready when delivered in fiscal year 2023/24.

Anna Perrin, Nokia’s managing director for Australia and New Zealand, said, “As a world-leading provider of mobile technology, we have championed the development of Neutral Host networks around the world and we’re excited to bring this global expertise to our partnership with FSG. Supporting the creation of new and innovative solutions and business models for rural and remote coverage across Australia.”

“Mavenir is excited to partner with FSG to deliver a cost-effective, future proof and globally proven 4G/5G Cloud-native Converged Packet Core, IMS and messaging services to enable Australia’s 4th mobile network,” said Dereck Quinlan, Mavenir regional VP.

“Mavenir continues to drive forward with advanced cloud-native solutions that our customers and the industry recognise. Our Cloud-native Converged Packet Core solution embraces a disruptive technology architecture and business model that drive network agility, deployment flexibility, and service velocity,” Quinlan added.

Over the next 18 months, FSG, in partnership with the Australian Federal Government and mobile operator Optus, will be trialing the deployment of what it says is Australia’s first “Active Neutral Host” network. The neutral-host model enables FSG to build and operate infrastructure and a single set of electronics that all mobile network operators in Australia can utilize and will be ready for PSMB services, the company says.

“The more carriers subscribe to the model, the more valuable and impactful it is for Australian Rural communities and Australia as a whole. We look forward to welcoming the other Australian Carriers to the program, to make the neutral host model a reality for rural, regional and remote Australia,” Roberts added.

References:

https://www.bloomberg.com/press-releases/2022-02-20/selects-nokia-and-mavenir-as-technology-partners

FSG selects Nokia, Mavenir to rollout Australia’s fourth mobile network

Nokia delivers private 4G fixed-wireless access (FWA) network for underserved students living in rural California

Nokia completed the first of a two-phase deployment of 4G fixed-wireless access (FWA) network with partner AggreGateway, to provide broadband internet connectivity to underserved students in the Dos Palos Oro Lomo (DPOL) school district of California.

The district comprises five campuses and serves a population of 5,000 residents. The Nokia platform will provide internet access to the homes of 2,400 students using Nokia Private 4.9G/LTE Digital Automation Cloud (NDAC) operating in the CBRS/On-Go GAA spectrum, and customer premises equipment including Nokia FastMile 4G Gateways and WiFi Beacons.

The DPOL technology team will operate its new LTE network through the centrally secure Nokia DAC Cloud monitoring application. DPOL will also provision LTE / Wi-Fi hotspots to students to be used with any standard laptop or tablet to access broadband internet.

The project’s first phase was completed in November 2021. Nokia and AggreGateway will complete the second phase in 2022.

The Federal Communications Commission (FCC) has reported nearly 17 million school children in the USA lack internet access at home, creating a nationwide ‘homework gap’ (Federal Communications Commission). This became even more pronounced during the pandemic as schools closed and distance learning became the new normal.

Image Credit: Nokia

Paoze Lee, Technology Systems Director of the Dos Palos-Oro Loma school district, said: “As we put a plan in place for distance learning during the pandemic we found we could only provide coverage for approximately 50% of DPOL students via commercial wireless network providers. Working with Nokia and AggreGateway, we are taking the next steps to level the field and ensure every student has the same access to our learning facilities.”

Octavio Navarro, President of AggreGateway, said: “Growing up in a rural small town like Dos Palos-Oro Loma, I experienced the digital divide firsthand. Being able to implement a Nokia private wireless solution for the students has been beyond rewarding. The IT staff from DPOL, AggreGateway, and Nokia worked seamlessly together to achieve this goal. We are excited, proud, and look forward to the continued success.”

Matt Young, Head of Enterprise for North America at Nokia, said: “We are pleased to help close the digital divide in the Dos Palos-Oro Loma school district. For many rural areas of the US it’s not commercially viable to build out networks, and often families on the lowest income suffer. Leveraging our DAC and FastMile FWA technologies we can enable the delivery of much needed internet connectivity to students in the area.”

The project’s first phase was completed in November 2021. Nokia and AggreGateway will complete the second phase in 2022.

About Nokia: