LEO satellites

Ookla: Starlink a viable competitor for hybrid 5G/NTN services due to network performance improvements and larger coverage area

SpaceX’s Starlink low-Earth orbit (LEO) satellite constellation providing high speed internet service is increasingly positioning itself as a scalable broadband access platform within the global telecom ecosystem. It now has growing relevance for both retail and enterprise connectivity use cases.

Network performance improvements (see below) have occurred alongside substantial subscriber growth. Starlink’s global user base expanded from approximately 4.6 million at the end of 2024 to over 10 million by early 2026, underscoring the LEO satellite platform’s ability to scale capacity while maintaining service quality.

This evolution is exemplified by T-Mobile’s “SuperBroadband” offering, which integrates 5G fixed wireless access (FWA) with Starlink satellite connectivity to deliver hybrid terrestrial–non-terrestrial network (NTN) solutions for business customers. The viability of such architectures is directly dependent on sustained improvements in satellite network throughput, latency, and service consistency.

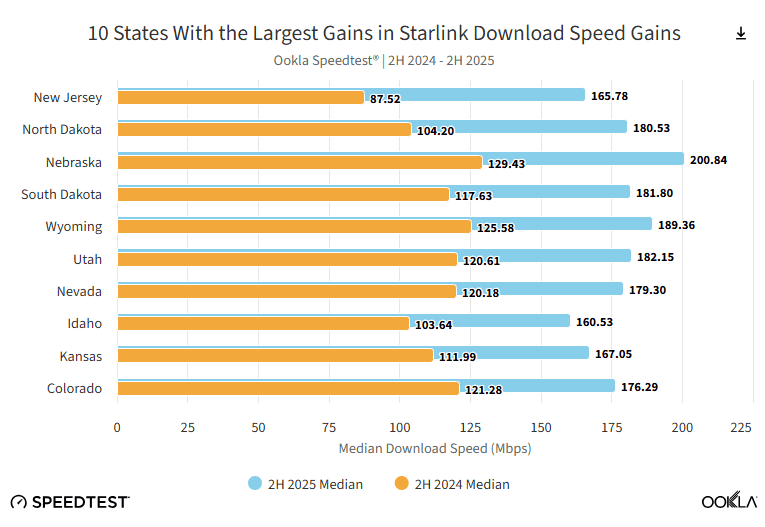

Ookla Speedtest® data for the second half of 2025 indicates significant year-over-year improvements in Starlink’s performance across key network metrics. Median download speeds exceeded 100 Mbps in 49 states, compared to 23 states in 2H 2024, reflecting both increased system capacity and improved spectral efficiency. Performance gains were also observed across the lower quartile of users: 25th percentile download speeds improved in 48 states, with the number of states below 50 Mbps declining from eleven to two (Alaska and Florida). This shift indicates not only higher peak throughput but also improved quality of experience (QoE) consistency across the subscriber base.

Latency performance has also trended positively, driven by both constellation densification and architectural enhancements. While Starlink continues to target ~20 ms median latency, the number of states with median multi-server latency below 40 ms increased from one to ten between 2H 2024 and 1H 2025. By 2H 2025, top-performing regions—including New Jersey, Colorado, Arizona, and Washington, D.C.—achieved median latencies of approximately 37 ms, approaching parity with certain terrestrial broadband deployments and enabling latency-sensitive applications.

There has been a rapid expansion of the Starlink constellation and ongoing satellite technology upgrades. As of February 2026, the constellation exceeded 10,000 satellites in orbit, materially increasing aggregate network capacity and reducing cell congestion through greater spatial reuse. The deployment of Generation 3 (V3) satellites—featuring an order-of-magnitude increase (~10×) in downlink capacity relative to prior generations—has further enhanced throughput. Concurrently, upgrades to inter-satellite laser links have enabled more efficient space-based routing, reducing dependency on terrestrial gateway infrastructure, minimizing bottlenecks, and improving end-to-end latency performance.

Notably, these network enhancements have coincided with rapid subscriber growth. Starlink’s global user base expanded from approximately 4.6 million at year-end 2024 to over 10 million by early 2026, demonstrating the platform’s ability to scale capacity in line with demand while maintaining or improving key performance indicators.

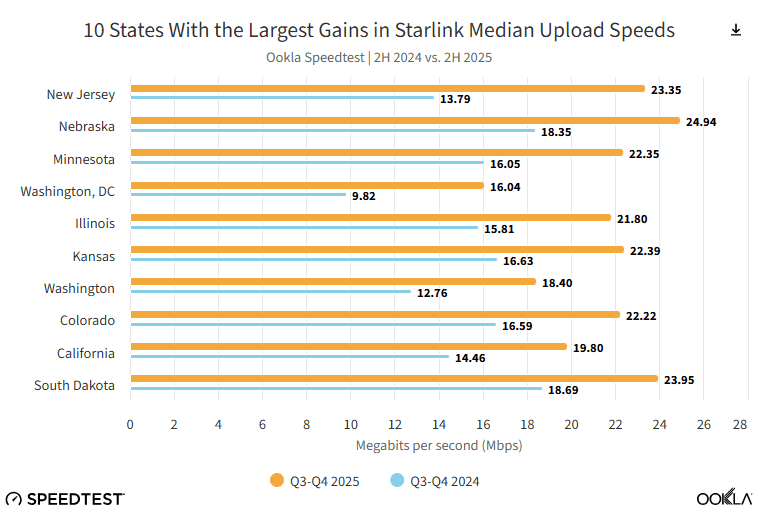

Uplink performance has also improved materially, with 22 states achieving median upload speeds ≥20 Mbps in 2H 2025, compared to zero states in the prior-year period. This threshold is aligned with the FCC’s current broadband definition, underscoring Starlink’s increasing capability to meet regulatory benchmarks for two-way broadband services. Nebraska, New Jersey, and Minnesota recorded the largest gains, with Nebraska leading overall at 24.94 Mbps median upload throughput.

However, performance gains remain uneven across certain geographies. States including Connecticut, Hawaii, and New Hampshire exhibited relatively modest uplink improvements, suggesting localized constraints related to capacity allocation, gateway distribution, or demand density. These variances highlight the continued importance of targeted constellation scaling and ground segment optimization to ensure uniform service quality.

In Q4, 44.7% of Starlink’s user base achieved the FCC’s 100/20 Mbps broadband benchmark, signaling the provider’s transition from a niche rural solution to a high-performance market disruptor. By scaling its LEO constellation to over 10,000 nodes and deploying higher-throughput payloads, Starlink has successfully optimized spectral efficiency and reduced latency, maintaining QoS even as its global subscriber base scaled to 10 million.

While the U.S. remains Starlink’s primary market, the competitive landscape is shifting. Amazon’s Project Kuiper faces significant deployment headwinds; despite an FCC mandate to orbit 1,618 satellites by July 2026, the company has only deployed roughly 240 units and has petitioned for a two-year extension due to launch capacity constraints. This market penetration places legacy GEO operators like Hughesnet and Viasat at a strategic disadvantage. Although these incumbents are leveraging aggressive pricing and CPE (Customer Premises Equipment) refreshes to stem churn, the inherent latency limitations of GEO architecture continue to pose a significant structural barrier to competing with LEO-based performance.

Overall, the data indicates that Starlink is transitioning from a niche rural broadband solution toward a more robust, high-capacity access network capable of supporting hybrid 5G/NTN architectures and enterprise-grade connectivity services.

…………………………………………………………………………………………………………………………………………………………………………………………………………….

Addendum – LEO vs GEO satellite internet:

The technical architectures of Low Earth Orbit (LEO) and Geostationary Earth Orbit (GEO) systems are fundamentally defined by their orbital altitude, which dictates their latency, link budget, and network complexity.

- Orbital Mechanics and Altitude:

- GEO satellites reside at a fixed altitude of approximately 35,786 km. They orbit at the same speed as the Earth’s rotation, appearing stationary from the ground, which allows for simple, fixed-point antenna installations.

- LEO satellites operate at significantly lower altitudes, typically between 160 km and 2,000 km. Because they are closer to Earth, they must travel at much higher velocities (approx. 28,000 km/h) to maintain orbit, completing a full revolution in about 90–128 minutes.

- Latency and Propagation Delay:

- GEO: The extreme distance results in a high propagation delay, with a typical round-trip time (RTT) of 500–600 ms. This is unsuitable for real-time applications like VoIP, gaming, or high-frequency trading.

- LEO: Proximity to Earth reduces latency to 20–50 ms, making the performance comparable to terrestrial fiber.

- Link Budget and Power Requirements:

- GEO: High path loss over 36,000 km requires high-power Traveling Wave Tube Amplifiers (TWTAs) and large, high-gain satellite antennas to maintain signal integrity. However, the terminal transmit power required for low-bitrate applications can actually be lower than LEO due to the stable, optimized architecture of legacy GEO MSS systems.

- LEO: Lower path loss enables the use of lower-power RF systems. However, the rapid movement requires complex phased array antennas at the user terminal to electronically track satellites and manage seamless handoffs between nodes in the constellation.

- Network Resilience and Capacity:

- GEO: A single satellite can cover up to 42% of the Earth’s surface, but capacity is centralized; a single point of failure can impact an entire region.

- LEO: Resilience is achieved through distributed constellations of thousands of satellites. These systems often utilize Intersatellite Links (ISLs)—optical or RF mesh networks in space—to route data between satellites, reducing the need for local ground gateways.

| Feature | LEO Architecture | GEO Architecture |

|---|---|---|

| Altitude | 160 – 2,000 km | ~35,786 km |

| Latency (RTT) | 20 – 50 ms | 500 – 600 ms |

| Coverage | Regional/Global via large constellation | ~1/3 of Earth per satellite |

| Terminal Type | Advanced tracking/Phased array | Fixed parabolic dish |

| Operational Life | ~5 years (due to atmospheric drag) | ~15 years |

…………………………………………………………………………………………………………………………………………………………………………………………………………….

References:

https://www.ookla.com/articles/starlink-hits-new-us-highs

Ookla: D2D satellite connectivity surged 24.5% during last 9 months; Starlink’s footprint expansion leads the way

US Mobile’s new bundle combines its multi-network mobile service with Starlink residential internet

Starlink doubles subscriber base; expands to to 42 new countries, territories & markets

Elon Musk: Starlink could become a global mobile carrier; 2 year timeframe for new smartphones

Direct-to-Device (D2D) satellite network comparison: Starlink V2 (Starlink Mobile) vs “Satellite Connect Europe”

Blue Origin announces TeraWave – satellite internet rival for Starlink and Amazon Leo

Amazon Leo (formerly Project Kuiper) unveils satellite broadband for enterprises; Competitive analysis with Starlink

China ITU filing to put ~200K satellites in low earth orbit while FCC authorizes 7.5K additional Starlink LEO satellites

GEO satellite internet from HughesNet and Viasat can’t compete with LEO Starlink in speed or latency

Analysis: Amazon <- Globalstar - a strategic move for D2D and spectrum parity

Overview:

Amazon said today that it will acquire Globalstar in an $11.57 billion deal, bolstering its fledgling satellite internet business as it tries to catch up with Elon Musk’s Starlink.

Amazon is accelerating its Project Kuiper deployment, aiming to launch approximately 3,200 Low Earth Orbit (LEO) satellites by 2029. To meet regulatory milestones, nearly 50% of the constellation must be operational by the July deadline, with commercial satellite broadband services slated for a soft launch later this year.

The acquisition of Globalstar augments Amazon’s Direct-to-Device (D2D) connectivity offerings. Globalstar’s current architecture is optimized for low-bandwidth, high-reliability mobile links that bypass traditional terrestrial RAN infrastructure. This capability is vital for ubiquitous emergency services and IoT connectivity in non-terrestrial network (NTN) white spaces. Through this deal, Amazon expects to operationalize its own D2D offerings by 2028.

IMPORTANT: It should be noted that ONLY 3GPP is developing the standards for NTNs – ITU-R and ETSI SDOs are simply rubber stamp SDOs for 3GPP NTN specs.

“There are billions of customers out there living, traveling, and operating in places beyond the reach of existing networks, and we started Amazon Leo to help bridge that divide,” said Panos Panay, Senior Vice President of Devices & Services, Amazon. “By combining Globalstar’s proven expertise and strong foundation with Amazon’s customer-obsession and innovation, customers can expect faster, more reliable service in more places—keeping them connected to the people and things that matter most. We’re excited to support Apple users through the Leo D2D system, and look forward to working with mobile network partners to help extend coverage to every corner of the planet,” Panay added.

The Competitive Landscape: Starlink vs. Kuiper:

SpaceX’s Starlink currently maintains a significant lead with over 9 million global subscribers. While Starlink’s core business remains high-throughput fixed wireless via proprietary user terminals, it is aggressively pursuing D2D through spectrum-sharing partnerships with Mobile Network Operators (MNOs) like T-Mobile.

Industry analysts suggest that acquiring Globalstar is a “spectrum play.” Armand Musey of Summit Ridge Group noted that the deal allows Amazon to secure a critical spectrum position and potentially leapfrog Starlink in D2D deployment timelines. Furthermore, Amazon’s proposed data center constellation is engineered for a massive scaling of network capacity, intended to exceed current LEO benchmarks.

“Amazon has been falling behind Starlink on satellite broadband. Acquiring Globalstar allows them to catch up on their D2D spectrum position, and leap ahead on D2D deployment,” said Armand Musey, president & founder of Summit Ridge Group.

Amazon LEO’s proposed data center constellation would dwarf Starlink’s current network by several magnitudes:

The Apple-Globalstar Ecosystem:

Crucially, Globalstar’s existing partnership with Apple remains intact. Globalstar currently provides the L-band connectivity powering Apple’s Emergency SOS and Find My features. Amazon has confirmed it will honor these agreements, maintaining the 2024 framework where Apple invested $1.5 billion for a 20% equity stake to expand the constellation to 54 satellites. See References below.

Market Consolidation and Valuations:

The move follows a broader trend of sector consolidation as players seek the scale required to compete with SpaceX’s vertical integration and launch frequency.

- Deal Metrics: Amazon’s acquisition values Globalstar at approximately $10.8 billion ($90/share), representing a 31% premium over the pre-announcement close.

- Regulatory Path: The merger is expected to close in 2025, pending FCC approval and the achievement of specific deployment KPIs. FCC Chair Brendan Carr indicated the agency remains “open-minded” regarding the consolidation.

Author’s Opinion & Analysis (aided by perplexity.ai):

Amazon’s Globalstar acquisition is a strong strategic move towards D2D, but it is more a spectrum-and-regulatory shortcut than a pure technology leap. The telecom significance is that Amazon is buying not just satellites, but licensed Mobile Satellite Spectrum (MSS), operational know-how, and an immediate path into direct-to-device connectivity that would otherwise take years to assemble.

From a telecom perspective, the key asset is spectrum parity. Globalstar holds licensed MSS spectrum in the L/S-band ranges used for satellite mobile services, and that spectrum is hard to replicate because the FCC has previously rejected or constrained new entrants in those bands. That makes the deal valuable less as a fleet expansion play and more as a way to secure a legally usable radio layer for D2D, which is not at all guaranteed.

Amazon’s stated plan is to combine Globalstar’s spectrum and MSS operations with Amazon Leo to deliver D2D services beginning in 2028, with claims of higher spectrum efficiency than legacy direct-to-cell systems. In telecom terms, that implies Amazon wants to move from “coverage extension” into a more integrated NTN architecture that can support voice, text, and eventually data services at scale. That’s certainly a tall order!

Against Starlink, this is a defensive and offensive move all at the same time. Starlink already has a lead in satellite scale and has commercialized carrier partnerships like T-Mobile’s direct-to-cell offering, so Amazon’s problem has been less launch capacity than spectrum and service readiness. Buying Globalstar narrows that gap by giving Amazon a ready-made regulatory and spectrum base instead of forcing it to negotiate every D2D pathway from scratch.

Against carriers, the move is more nuanced. Amazon is not simply disintermediating mobile operators; its own materials describe D2D as a way to help MNOs extend voice, text, and data beyond terrestrial reach. That suggests a wholesale or partner model, but the long-term competitive risk is obvious: if Amazon owns the satellite layer and the device/service stack, carriers may become optional distribution partners rather than network gatekeepers.

The phrase “spectrum parity” is the real strategic clue. In telecom, constellation size matters, but spectrum rights determine whether a constellation can actually deliver service with usable link budgets, device compatibility, and regulatory clearance. Globalstar’s spectrum therefore acts like a license to compete, not just a frequency block.

This also helps explain why the deal is strategically defensive for Amazon. Without Globalstar, Amazon would face a slower, less certain path through band planning, interference disputes, and NTNspecific regulatory work, especially in crowded MSS allocations. In that sense, the acquisition is a classic telecom play: buy scarce spectrum, then scale the network around it.

The biggest near-term risk to this deal is regulatory. The transaction will need FCC and likely antitrust review, and Amazon will also have to navigate the Apple/Globalstar relationship because Globalstar powers Apple’s Emergency SOS service. That creates both transition risk and potential bargaining leverage for Apple, which could complicate service continuity and deal terms.

Technically, D2D is still constrained by small link budgets, handset antenna limits, and the need to prioritize messaging and emergency services before richer data use cases. Even if Amazon claims better spectrum efficiency, the first commercially meaningful services will likely remain low-throughput, coverage-oriented offerings rather than full terrestrial substitutes. So the real competition is not “satellite internet for phones” in the consumer broadband sense, but who controls the premium coverage layer for dead zones, emergency service, enterprise continuity, and carrier augmentation.

In conclusion, Amazon is making a category-defining infrastructure purchase, not just a corporate acquisition. If approved, it gives Amazon a credible D2D spectrum position, reduces its regulatory latency, and turns Amazon Leo into a more complete and highly competitive NTN platform and D2D service provider.

……………………………………………………………………………………………………………………….

References:

https://www.aboutamazon.com/news/company-news/amazon-globalstar-apple

Amazon Leo (formerly Project Kuiper) unveils satellite broadband for enterprises; Competitive analysis with Starlink

Blue Origin announces TeraWave – satellite internet rival for Starlink and Amazon Leo

NBN selects Amazon Project Kuiper over Starlink for LEO satellite internet service in Australia

Amazon launches first Project Kuiper satellites in direct competition with SpaceX/Starlink

Emergency SOS: Apple iPhones to be able to send/receive texts via Globalstar LEO satellites in November

FCC proposes regulatory framework for space-mobile network operator collaboration

AT&T deal with AST SpaceMobile to provide wireless service from space

Starlink Direct to Cell service (via Entel) is coming to Chile and Peru be end of 2024

Starlink’s Direct to Cell service for existing LTE phones “wherever you can see the sky”

US Mobile’s new bundle combines its multi-network mobile service with Starlink residential internet

MVNO US Mobile has announced a partnership with Starlink to offer customers a bundle which includes its pre-paid wireless service with home internet from the Space X owned LEO satellite internet provider. Ahmed Khattak, CEO of US Mobile, announced the partnership on Reddit, saying their Starlink One service will be offered without data caps. Khattak stated the Starlink bundle will be offered with US Mobile’s unlimited standard or premium plans able to access all three networks, which means customers only need to deal with one bill, one app and “one company that actually picks up the phone.”

“I won’t tease numbers too hard, but imagine a plan for less than $50 a month that spans every major network in the United States, extends across Canada and Mexico, includes internet from space at home,” Khattak wrote. US Mobile has MNVO deals in place with AT&T, Verizon and T-Mobile US and uses a platform which gives customers the ability to switch between networks. This “terrestrial and celestial” unification allows customers to manage their home and mobile connectivity under a single bill and app.

US Mobile and SpaceX have joined forces to redefine convergence. | Image by US Mobile

Details on the exact cost of the bundled tier and Starlink equipment were not available. Wave7 Research analyst Jeff Moore told Mobile World Live Starlink started offering its home broadband service last month in 120 T-Mobile Boost retail stores as part of a pilot program. “If Starlink is working to sell home Internet via Boost and providing mobile connectivity via US Mobile, then Starlink is probably having conversations with other MVNOs about options for becoming channels for internet sales and for mobile satellite connectivity,” he explained.

Meanwhile, Khattak stated he expects similar deals will follow with additional satellite broadband providers such as Amazon Leo. “The endgame is Global Multi-Orbit Convergence. Every major terrestrial network on the ground, every major LEO constellation in the sky, stitched together into a single plan that follows you anywhere on earth,” Khattak added.

- Dynamic Network Switching: Users can access Warp (Verizon), Dark Star (AT&T), and Light Speed (T-Mobile).

- Automatic Handover: While US Mobile previously required manual “Teleporting” between networks, the new Multi-Network Add-on allows phones to automatically switch to the strongest available signal or a backup network if the primary one fails.

- Unified Account: Both the Starlink satellite session and terrestrial cellular lines are managed via a single “unification layer,” which CEO Ahmed Khattak describes as a software infrastructure that’s been a decade in the making.

- Introductory Pricing: Most Starlink discounts revert to standard pricing (an increase of roughly $20/month) after the first six months.

- Availability: The bundle is not available in certain areas subject to Starlink congestion pricing.

- Hardware Requirements: To use dynamic network switching, your device must support multiple active eSIMs.

AT&T recently launched OneConnect, a cellular and fiber bundle providing one mobile line and fiber internet for $90 per month. T-Mobile’s MVNO Mint Mobile countered with a wireless and 5G internet bundle starting at $45 per month.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

References:

https://www.phonearena.com/news/us-mobile-starlink_id179545

Direct-to-Device (D2D) satellite network comparison: Starlink V2 (Starlink Mobile) vs “Satellite Connect Europe”

Blue Origin announces TeraWave – satellite internet rival for Starlink and Amazon Leo

Amazon Leo (formerly Project Kuiper) unveils satellite broadband for enterprises; Competitive analysis with Starlink

Starlink doubles subscriber base; expands to to 42 new countries, territories & markets

Elon Musk: Starlink could become a global mobile carrier; 2 year timeframe for new smartphones

KDDI unveils AU Starlink direct-to-cell satellite service

GEO satellite internet from HughesNet and Viasat can’t compete with LEO Starlink in speed or latency

Open Cosmos introduces global space-based LEO satellite service for IoT monitoring

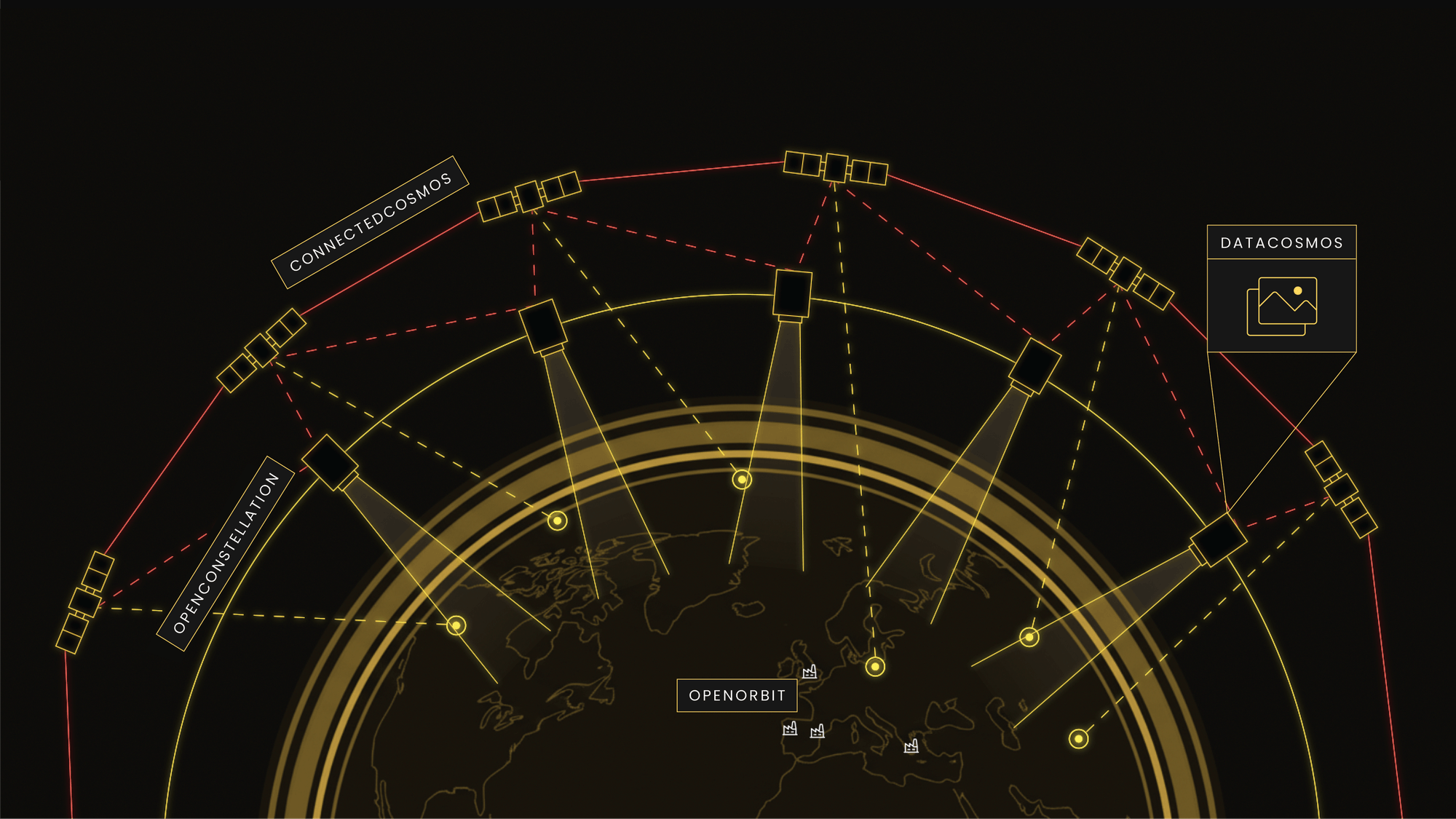

Founded in 2015, UK headquartered Open Cosmos has introduced a new integrated satellite service that combines broadband, earth observation, and IoT capabilities to help organizations monitor critical infrastructure, protect environmental assets, and respond more rapidly to events. The company says the offering is unique in combining global IoT connectivity with real-time Earth observation data to deliver contextual intelligence for governments and institutions.

The service is built on Open Cosmos’ multi-layer satellite architecture, which the company describes as a trilogy of secure broadband connectivity, Earth observation, and IoT. The constellation includes the newly launched Connected Cosmos Low Earth Orbit (LEO) connectivity backbone [1.] and the Open Constellation Earth observation layer [2]. Each satellite carries an IoT payload, integrating functions that are typically deployed as separate systems.

Note 1. Connected Cosmos is a new LEO constellation providing sovereign and secure communications for businesses and government bodies worldwide. It ensures that critical data remains secure, trusted, and immediately usable—even when terrestrial infrastructure is compromised. It uses Optical Inter-Satellite-Links to route data between satellites, physically bypassing subsea cables. Built to withstand interference from jamming and cyber attacks, it’s designed to cut through a contested orbital field for modern critical operations.

Note 2. The Open Constellation is a mutualized satellite infrastructure, created to enable organizations to share the data generated by satellites for improved access to information on our planet. Using this shared capacity reduces overall costs and increases access to better quality, more frequent data. With more satellites in orbit, more areas can be covered more frequently, giving partners of the Open Constellation a greater global coverage.

Open Cosmos Ecosystem:

Image Credit: Open Cosmos

…………………………………………………………………………………………………………………………………………………………………………

The company says this approach is intended to “address the traditionally siloed nature of space-based data services, dramatically accelerating data delivery times and maximizing operational awareness, which will monitor environmental change and support disaster response across the globe – even in the most remote regions.”

Open Cosmos says the result is faster detection of events and a better understanding of what is happening on the ground. Potential applications include monitoring widely distributed assets, overseeing critical infrastructure such as energy, utility, and rail networks, protecting oceans, tracking wildfires, and observing offshore conditions. In this model, imagery and sensor data are combined so that users can not only see that a change has occurred, but also understand the context behind it.

“Our mission at Open Cosmos has always been focused on solving real world issues through space-based services,” said Danielle Edwards, VP for IoT at Open Cosmos. “This is an essential and critical technology service for governments, enterprises and institutions across the globe, helping to monitor and solve real world problems, with the innovative use of technology in space.

“Our existing Earth observation satellites already carry IoT payloads, so we have the experience to integrate further through our ConnectedCosmos LEO constellation, with each satellite being designed and made to carry IoT capabilities. Our aim is to provide a multitude of payload types within a single constellation to give our customers a completely bespoke and unique service.

“We won’t be just providing the data from a sensor; we will provide the visual imagery to explain why that data is changing. As demand for global monitoring and connected infrastructure continues to grow, our integrated approach represents a new model for space-enabled intelligence.”

At MWC earlier this month, Carlos Zamora, VP of Satcom Solutions at Open Cosmos, said the company is not positioning the LEO broadband service as a direct-to-device play.

Zamora elaborated:

“First of all we’re not going direct to device with the broadband. We’re not here to compete with Starlink or Kuiper or of all of these systems – we’re not here to bring internet to the to the masses. We’re here to bring a global secure connectivity to governments, commercial [customers] and actually anyone that is worried about their data resiliency and sovereignty. But we do have IoT capabilities that commercial and other customers could use. So the architecture is also fundamentally different. What we’re selling is a network, not a link in space, but actually a network. And I think what makes the difference beyond just connectivity, which is already a differentiator, is the fact that we can start fusing all of our offerings together. And this is not just about moving bits from one place to another, it is giving you the possibility of accessing a space infrastructure that can give you access to real time Earth observation, to real time computing capabilities in orbit, and basically creating a network of assets that can increase your situational awareness and give you access to a global intelligence backbone.”

Open Cosmos is effectively positioning the platform as a secure, multi-sensor space infrastructure layer rather than a consumer broadband network. The focus is on government, enterprise, and institutional customers that need connectivity, resilience, and situational awareness tied to Earth observation and IoT data.

………………………………………………………………………………………………………………………………………………………………………………….

References:

https://www.open-cosmos.com/leo-satellite-network-connectivity

https://www.open-cosmos.com/news/open-cosmos-earth-observation-iot-real-time-data

https://www.telecoms.com/satellite/open-cosmos-launches-earth-observation-and-iot-satellite-service

Enterprise IoT and the Transformation of UK Telecom Business Models – Part 1

From LPWAN to Hybrid Networks: Satellite and NTN as Enablers of Enterprise IoT – Part 2

Semtech LoRa® PHY technology enables Amazon Sidewalk to expand while supporting fixed and mobile IoT endpoints

ITU-R recommendation IMT-2020-SAT.SPECS from ITU-R WP 5B to be based on 3GPP 5G NR-NTN and IoT-NTN (from Release 17 & 18)

CEA-Leti RF Chip Enables Ultralow-Power IoT Connectivity For Remote Devices Via Astrocast’s Nanosatellite Network

China ITU filing to put ~200K satellites in low earth orbit while FCC authorizes 7.5K additional Starlink LEO satellites

- Purpose: The planned systems are intended to provide global broadband connectivity, data relay, and positioning services, directly competing with U.S. efforts like SpaceX’s Starlink network.

- Filing Entities: The primary filings were submitted by the state-backed Institute of Radio Spectrum Utilization and Technological Innovation, along with other commercial and state-owned companies like China Mobile and Shanghai Spacecom.

- Status: These filings are an initial step in a long international regulatory process and serve as a claim to limited spectrum and orbital slots. They do not guarantee all satellites will ultimately be built or launched. The actual deployment will be a gradual process over many years.

- Context: The move is part of an escalating “space race” to dominate the LEO environment. Early filings are crucial for securing priority access to orbital resources and avoiding signal interference. The sheer scale of the Chinese proposal would, if realized, dwarf most other planned constellations.

- Regulations: Under ITU rules, operators must deploy a certain percentage of the satellites within seven years of the initial filing to retain their rights.

- Shanghai Yuanxin (Qianfan), currently China’s most advanced LEO satellite operator, has submitted a regulatory request for an additional 1,296 satellites.

- Telecommunications giant China Mobile is planning two separate constellations totaling 2,664 satellites.

- ChinaSat, the established state-owned satellite provider, is focusing on a 24-satellite medium-Earth orbit (MEO) system.

- GalaxySpace, a private satellite manufacturer based in Beijing, has applied for 187 satellites, and China Telecom has applied for 12.

Image Credit: Klaus Ohlenschlaeger/Alamy Stock Photo

“This gives SpaceX what they need for the next couple of years of operation. They’re launching a bit over 3,000 satellites a year, so 7,500 satellites being authorized is potentially enough for SpaceX to do what they want to do until late 2027,” said Tim Farrar, satellite analyst and president at TMF Associates.

SpaceX has plans for a larger D2D satellite constellation that would use the AWS-4 and H-block spectrum it is acquiring from EchoStar. It is awaiting FCC approval for the US$17 billion deal, but the spectrum is not expected to be transferred until the end of November 2027.

The FCC noted that the changes will allow the Starlink system to serve more customers and deliver “gigabit speed service.” Along with permission for another tranche of satellites, the FCC has set new parameters for frequency use and lower orbit altitudes. The modified authorizations will also apply to new satellites to be launched.

Starlink’s LEO satellite network competitors are Amazon Leo, OneWeb and AST Space Mobile.

………………………………………………………………………………………………………………………………………………………..

References:

U.S. BEAD overhaul to benefit Starlink/SpaceX at the expense of fiber broadband providers

Huge significance of EchoStar’s AWS-4 spectrum sale to SpaceX

Telstra selects SpaceX’s Starlink to bring Satellite-to-Mobile text messaging to its customers in Australia

SpaceX launches first set of Starlink satellites with direct-to-cell capabilities

SpaceX has majority of all satellites in orbit; Starlink achieves cash-flow breakeven

Amazon Leo (formerly Project Kuiper) unveils satellite broadband for enterprises; Competitive analysis with Starlink

NBN selects Amazon Project Kuiper over Starlink for LEO satellite internet service in Australia

GEO satellite internet from HughesNet and Viasat can’t compete with LEO Starlink in speed or latency

Amazon launches first Project Kuiper satellites in direct competition with SpaceX/Starlink

Vodafone and Amazon’s Project Kuiper to extend 4G/5G in Africa and Europe

Starlink doubles subscriber base; expands to to 42 new countries, territories & markets

Starlink, the satellite internet service by SpaceX, has nearly doubled its internet subscriber base in 2025 to over 9 million global customers. This rapid expansion from approximately 4.6 million subscribers at the end of 2024 has been driven by new service launches in 42 countries and territories, new subscription options, and the company’s focus on bridging the digital divide in remote and underserved areas.

- Total Subscribers: As of December 2025, Starlink connects over 9 million active customers across 155 countries.

- Growth Rate: The company added its most recent million users in just under seven weeks, a record pace of over 20,000 new users daily. Overall internet traffic from users more than doubled in 2025.

- Geographic Expansion: Starlink’s growth is heavily fueled by international markets where traditional broadband is limited. The U.S. subscriber base alone reached over 2 million by mid-2025.

- Infrastructure: SpaceX has focused heavily on scaling its network capacity, operating more than 9,000 active satellites in orbit and investing heavily in ground infrastructure.

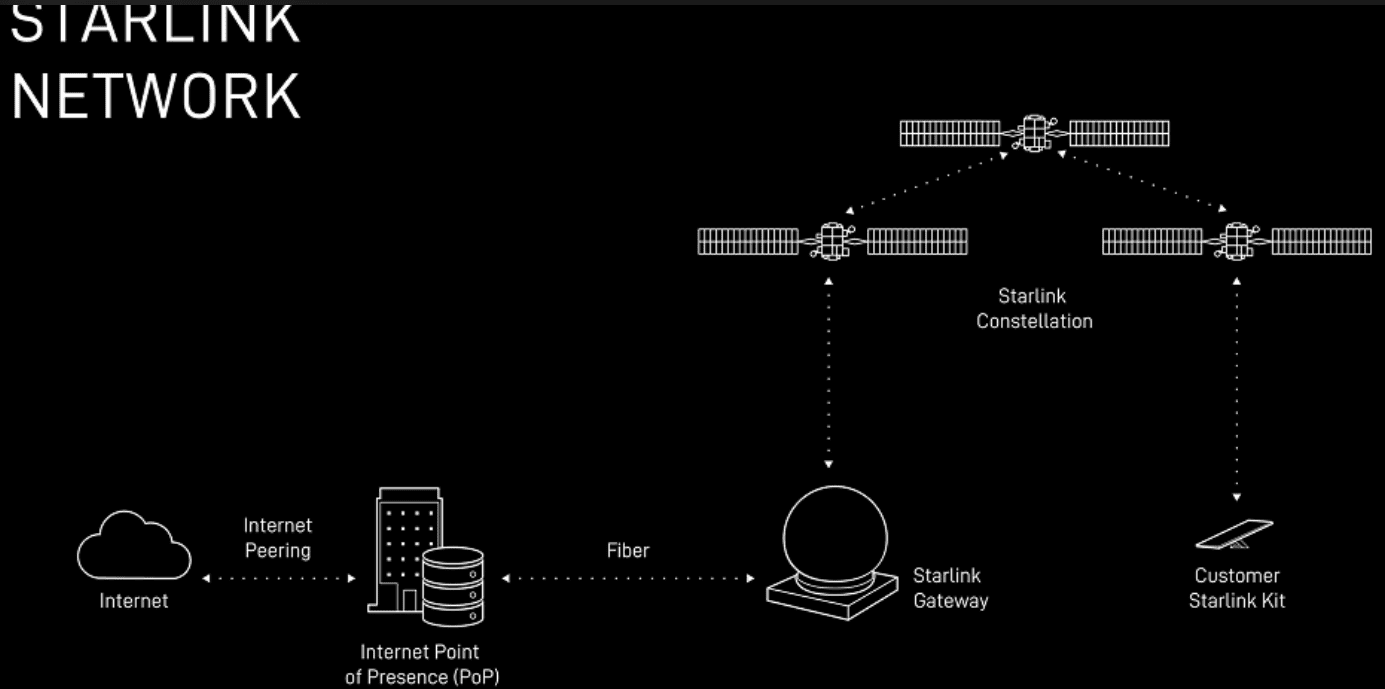

Starlink’s Ground Network:

Starlink has also deployed the largest satellite ground network with more than 100 gateway sites in the United States alone – comprising a total of over 1,500 antennas – are strategically placed to deliver the lowest possible latency, especially for those who live in rural and remote areas.

Starlink produces these gateway antennas at our factory in Redmond, Washington where they rapidly scaled production to match satellite production and launch rate.

Network Resilience:

With more than 7,800 satellites in orbit, Starlink customers always have multiple satellites in view, as well as multiple gateway sites and internet points-of-presence locations (PoPs). As a result, Starlink customers benefit from continuous service even when terrestrial broadband is suffering from fiber cuts, subsea cable damage, and power outages that can deny service to millions of individuals for days.

Additionally, each Starlink satellite is equipped with cutting-edge optical links that ensure they can relay hundreds of gigabits of traffic directly with each other, no matter what happens on the ground. This laser network enables Starlink satellites to consistently and reliably deliver data around the world and route traffic around any ground conditions that affect terrestrial service at speeds that are physically impossible on Earth.

Starlink’s Latency:

To measure Starlink’s latency, the company collects anonymized measurements from millions of Starlink routers every 15 seconds. In the U.S., Starlink routers perform hundreds of thousands of speed test measurements and hundreds of billions of latency measurements every day. This high-frequency automated measurement assures consistent data quality, with minimal sampling bias, interference from Wi-Fi conditions, or bottlenecks from third-party hardware.

As of June 2025, Starlink is delivering median peak-hour latency of 25.7 milliseconds (ms) across all customers in the United States. In the US, fewer than one percent of measurements exceed 55 ms, significantly better than even some terrestrial operators.

- Addressing the Digital Divide: Starlink has positioned itself as a critical solution for rural and remote communities, offering high-speed, low-latency internet where fiber or cable is unfeasible.

- New Services: The company is expanding beyond individual households to include services for airlines, maritime operators, and businesses. There are also plans for a direct-to-cell service in partnership with mobile carriers like T-Mobile.

- Next-Generation Satellites: To manage the growing user base and increasing congestion, SpaceX plans to launch its larger, next-generation V3 satellites in 2026, which are designed to offer gigabit-class connectivity and dramatically increase network capacity.

- IPO Considerations: Starlink’s significant growth and role as SpaceX’s primary revenue driver have positioned the parent company for a potential initial public offering (IPO) in 2026.

Competition:

Starlink’s main LEO competitors are Amazon Leo (Project Kuiper) and OneWeb (Eutelsat), aiming for similar high-speed, low-latency service, while established providers Hughesnet and Viasat (mostly GEO) offer more traditional, affordable satellite options but with higher lag, though they’re adapting. Starlink leads in consumer availability and speed currently, but Amazon and OneWeb are rapidly scaling to challenge its dominance with LEO constellations, offering faster speeds and lower latency than older satellite tech.

……………………………………………………………………………………………………………..

References:

https://starlink.com/updates/network-update

Elon Musk: Starlink could become a global mobile carrier; 2 year timeframe for new smartphones

Amazon Leo (formerly Project Kuiper) unveils satellite broadband for enterprises; Competitive analysis with Starlink

NBN selects Amazon Project Kuiper over Starlink for LEO satellite internet service in Australia

GEO satellite internet from HughesNet and Viasat can’t compete with LEO Starlink in speed or latency

KDDI unveils AU Starlink direct-to-cell satellite service

Telstra selects SpaceX’s Starlink to bring Satellite-to-Mobile text messaging to its customers in Australia

U.S. BEAD overhaul to benefit Starlink/SpaceX at the expense of fiber broadband providers

One NZ launches commercial Satellite TXT service using Starlink LEO satellites

Reliance Jio vs Starlink: administrative process or auction for satellite broadband services in India?

FCC: More competition for Starlink; freeing up spectrum for satellite broadband service

SpaceX launches first set of Starlink satellites with direct-to-cell capabilities

Starlink Direct to Cell service (via Entel) is coming to Chile and Peru be end of 2024

NBN selects Amazon Project Kuiper over Starlink for LEO satellite internet service in Australia

Government-owned wholesale broadband operator NBN Co will become the first major customer of Amazon’s Project Kuiper Low-Earth Orbit (LEO) satellite internet technology in Australia beginning in the middle of 2026. At that time, NBN Co plans to offer wholesale residential-grade fixed LEO satellite broadband services to more than 300,000 premises within our existing satellite footprint via participating Retail Service Providers (RSPs).

The agreement will enable NBN Co to transition from its existing geostationary Sky Muster satellite service over the coming years and will complement NBN Co’s investments in fiber and fixed wireless upgrades for regional Australia.

NBN Co will shortly start consultation with RSPs, regional communities and stakeholders, to help inform what speed tiers are offered, wholesale pricing and the upgrade for customers. The consultation will consider the offer of equipment and professional initial standard installation and assurance at no cost for existing eligible NBN satellite customers, via participating RSPs.

…………………………………………………………………………………………………………………………………………………………………………………………………………

Project Kuiper’s low-latency, high-bandwidth satellite network will provide significant improvements to the quality and reliability of broadband for eligible regional, rural and remote communities. To achieve its goals, Project Kuiper is deploying thousands of satellites in low Earth orbit —connected to each other by high-speed optical links that will create a mesh network in space—and linked to a global network of antennas, fiber, and internet connection points on the ground.

The initial satellite constellation will include more than 3,200 satellites, which began deploying on April 28, 2025 with its first operational launch. That initial launch consisted of 27 production satellites and was carried out by a United Launch Alliance Atlas V rocket, according to the United Launch Alliance. The launch took place from Cape Canaveral Space Force Station in Florida.

There are currently 78 Kuiper satellites in orbit, after three successful launches in less than three months. Amazon is continuing to increase its production, processing and launch rates ahead of an initial service rollout.

…………………………………………………………………………………………………………………………………………………………………………………………………………

In the coming years, LEO satellite services powered by Project Kuiper will replace NBN’s current geostationary orbit Sky Muster satellite service. The company plans to maintain and operate its two geostationary Sky Muster satellites until the transition to the Project Kuiper satellite network is complete. This will ensure continuity for customers in regional, rural, and remote parts of Australia who rely on satellite telecommunications. However, the two Sky Muster satellites are expected to remain operational until approximately 2032.

The agreement between NBN and Amazon is expected to introduce competition to the LEO-based satellite internet services market, particularly in regional Australia. Currently, Starlink dominates this market as the only LEO satellite operator. As of April 2025, Starlink claimed to have more than 350,000 customers in Australia.

Telecom analyst Paul Budde told Reuters that NBN’s decision to partner with Amazon was probably influenced by the need to limit sovereign risk arising from giving control of essential Australian infrastructure to a company aligned with “a very unpredictable America. I am sure total dependence on Starlink would not be seen as a favorable situation,” he added.

Ellie Sweeney, Chief Executive Officer at NBN Co, said:

“LEO satellite broadband, supplied by NBN Co and powered by Amazon’s Project Kuiper, will be a major leap forward for customers in parts of regional, rural and remote Australia.

“This important agreement will complement our other major network upgrades that have involved the rollout of full fibre services across much of our fixed line network and the deployment of the latest 5G millimeter wave technology to improve the speed and capacity of our fixed wireless network.

“Australians deserve to have access to fast, effective broadband regardless of whether they live in a major city, on the outskirts of a country town or miles from their nearest neighbor. That’s what NBN was set up to deliver. By upgrading to next generation LEO satellite broadband powered by Project Kuiper, we are working to bring the best available technology to Aussies in the bush.

“Transitioning from two geostationary satellites to a constellation of Low Earth Orbit satellites will help to ensure the nbn network is future-ready and delivers the best possible broadband experience to customers living and working in parts of regional, rural and remote Australia.

“We plan to bring faster, lower latency broadband to Australians living and working in regional, rural and remote areas, enabling their ongoing participation in the economy for work, study, telehealth, streaming entertainment and connecting with family and friends.

“This new LEO service will eventually replace our geostationary satellites, and we are committed to working with regional communities to ensure we provide continuity of service and make the transition as smooth and seamless as possible.”

Rajeev Badyal, Vice President, Technology at Amazon’s Project Kuiper, said:

“We’ve designed Project Kuiper to be the most advanced satellite system ever built, and we’re combining that innovation with Amazon’s long track record of making everyday life better for customers. We’re proud to be working with NBN to bring Kuiper to even more customers and communities across Australia and look forward to creating new opportunities for hundreds of thousands of people in rural and remote parts of the country.”

References:

https://www.lightreading.com/satellite/nbn-amazon-deal-to-bring-project-kuiper-to-australia-by-2026

https://www.aboutamazon.com/news/innovation-at-amazon/project-kuiper-satellite-internet-first-launch

Amazon launches first Project Kuiper satellites in direct competition with SpaceX/Starlink

Vodafone and Amazon’s Project Kuiper to extend 4G/5G in Africa and Europe

Amazon to Spend Billions on 38 Space Launches for Project Kuiper

Telstra selects SpaceX’s Starlink to bring Satellite-to-Mobile text messaging to its customers in Australia

GEO satellite internet from HughesNet and Viasat can’t compete with LEO Starlink in speed or latency

FCC: More competition for Starlink; freeing up spectrum for satellite broadband service

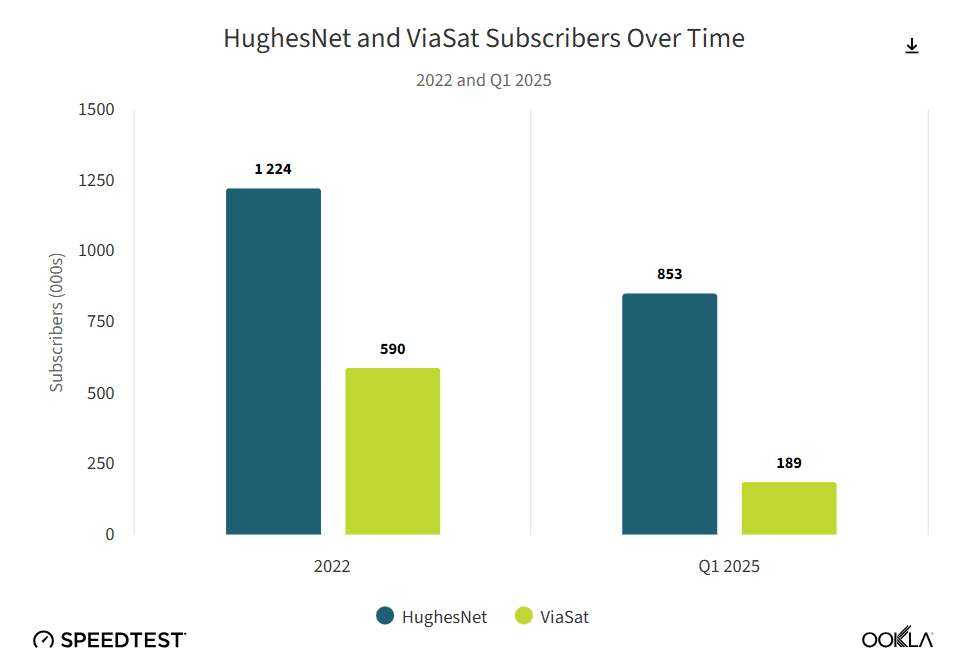

GEO satellite internet from HughesNet and Viasat can’t compete with LEO Starlink in speed or latency

GEO satellite internet providers provide reliable connectivity across large land masses, but their distance from Earth presents challenges to delivering low-latency and high-speed satellite Internet services. HughesNet and Viasat operate stationary satellites 22,000 miles above Earth, whereas LEO satellite operators such as Starlink have satellites orbiting a mere 340 miles above Earth. GEO satellites are also less ubiquitous than LEO satellites – GEO operators have fewer satellites in their constellations.

According to Ookla, GEO satellite providers HughesNet and Viasat can’t compete with Starlink when it comes to latency and download speeds. HughesNet and Viasat are best-known for providing consistent coverage across large land masses. But because they operate in geostationary orbit rather than low-Earth orbit (LEO) and because they have fewer satellites in their constellations, they struggle with speed limitations and latency, making it difficult for them to compete with LEO providers such as SpaceX’s Starlink.

HughesNet and Viasat have three satellites each in their fleet delivering fixed broadband service. Viasat plans to launch its Viasat-3 F2 satellite later this year and the Viasat-3 F3 in 2026. In addition, it owns a fleet of satellites from the company’s Inmarsat acquisition in May 2023 which are primarily used in maritime and mission-critical applications.

The challenges facing these GEO satellite providers have become more pronounced over the past few years, particularly as Starlink has moved aggressively into the U.S. market with promotions such as its recent offer to provide free equipment to new customers in states where it has excess capacity.

“HughesNet and Viasat are losing subscribers at a rapid rate thanks to competition from LEO satellite provider Starlink with its lower latency and faster download speeds,” according to Sue Marek, editorial director and analyst with Ookla.

Ookla’s Key Takeaways:

- HughesNet saw its median multi-server latency improve from 1019 milliseconds (ms) in Q1 2022 to 683 ms in Q1 2025. Viasat’s median latency increased slightly over that time period from 676 ms in Q1 2022 to 684 ms in Q1 2025. But neither are remotely close to matching Starlink with its median latency of just 45 ms in Q1 2025.

- HughesNet more than doubled its median download speeds from 20.87 Mbps in Q1 2022 to 47.79 Mbps in Q1 2025 while Viasat increased its median download speeds from 25.18 Mbps to 49.12 Mbps during that same time period.

- Upload speeds are another area where GEO satellite constellations struggle to compete with Starlink and other low-Earth orbit systems. HughesNet has increased its median upload speeds from 2.87 Mbps in Q1 2022 to 4.44 Mbps in Q1 2025 but that is still far lower than Starlink, which has a median upload speed of 14.84 Mbps in Q1 2025. Viasat saw its median upload speeds decline over that same time period from 3.06 Mbps in Q1 2022 to 1.08 Mbps in Q1 2025.

- HughesNet and Viasat are losing subscribers at a rapid rate thanks to competition from LEO satellite provider Starlink with its lower latency and faster download speeds.

Meanwhile, Starlink has nearly 8,000 satellites in low earth orbit (LEO) as part of its mega-constellation, according to Space.com. Starlink’s median download speeds, according to data from Ookla’s Speedtest users, almost doubled from 53.95 Mbit/s in Q3 2022 to 104.71 Mbit/s in Q1 2025. These latest average download speeds are also nearly twice that of HughesNet and Viasat.

In addition to network performance, Starlink has made strides in the U.S. market with promotions and distribution of free equipment to “new customers in states where it has excess capacity,” said Marek. In May, Starlink offered its Standard Kit, priced at $349, for free to consumers in select areas who agree to a one-year service commitment. But, “high demand” areas would still need to pay a one-time, upfront “demand surcharge” of $100, the company said.

Starlink is making headway teaming up with terrestrial service providers on direct-to-device (D2D) services, which connect smartphones and mobile devices directly to satellite networks in areas of spotty wireless service. Canada’s Rogers Communications launched a beta D2D service this week that initially supports text messaging via Starlink LEO satellites. The Canadian operator is also working with Lynk Global in a multi-vendor approach to D2D. Starlink announced this week that it has over 500,000 customers across Canada.

T-Mobile’s D2D service, T-Satellite with Starlink, will be commercially available later this month and will include SMS texting, MMS, picture messaging and short audio clips. In October, T-Satellite will add a data service to its Starlink-based satellite offering.

However, T-Mobile announced it would bump up the launch of T-Satellite to areas impacted by the recent flooding in central Texas. During a number of recent natural disasters, Starlink has offered free services and/or satellite equipment kits to affected communities.

Starlink is providing Mini Kits, which support 50 gigabyte and unlimited roaming data subscriptions, for search and rescue efforts in central Texas, in addition to one month of free service to customers in the areas impacted by recent flooding. In January, the satellite operator offered about a month of free service to new customers and a one-month service credit to existing customers in areas affected by the Los Angeles wildfires.

Starlink could be facing increasing competition from Project Kuiper, Amazon’s LEO satellite broadband service, as it ramps up deployment of a planned LEO constellation of over 3,000 satellites. However, Project Kuiper has fallen far behind schedule in meeting the FCC’s deadline of having more than 1,600 LEO satellites in orbit by the summer of 2026. Since its initial launch in April, Amazon only has a total of 78 satellites in orbit, according to CNBC. Meanwhile, Starlink has launched over 2,300 satellites in the past year alone.

References:

https://www.ookla.com/articles/hughesnet-viasat-performance-2025

https://www.space.com/space-exploration/launches-spacecraft/spacex-starlink-15-2-b1093-vsfs-ocisly

KDDI unveils AU Starlink direct-to-cell satellite service

Telstra selects SpaceX’s Starlink to bring Satellite-to-Mobile text messaging to its customers in Australia

One NZ launches commercial Satellite TXT service using Starlink LEO satellites

SpaceX launches first set of Starlink satellites with direct-to-cell capabilities

FCC: More competition for Starlink; freeing up spectrum for satellite broadband service

U.S. BEAD overhaul to benefit Starlink/SpaceX at the expense of fiber broadband providers

Starlink’s Direct to Cell service for existing LTE phones “wherever you can see the sky”

ABI Research and CCS Insight: Strong growth for satellite to mobile device connectivity (messaging and broadband internet access)

AST SpaceMobile completes 1st ever LEO satellite voice call using AT&T spectrum and unmodified Samsung and Apple smartphones

PCMag Study: Starlink speed and latency top satellite Internet from Hughes and Viasat’s Exede

China Telecom and China Mobile invest in LEO satellite companies

Two of China’s state-owned telcos have taken stakes in new LEO satellite companies.

- China Telecom has set up a new fully owned subsidiary, Tiantong Satellite Technology Co., registered in Shenzhen with 1 billion Chinese yuan (US$138 million) paid-in capital. China Telecom, which is currently the only operator with a mobile satellite license, operates three Tiantong Geo orbit satellites, launched between 2016 and 2021, covering China, the western Pacific and its neighbors.

- In April China Mobile took a 20% stake in a new RMB4 billion ($551 million) state-owned company, China Shikong Xinxi Co., registered in Xiongan. China Satellite Network Group, the company behind Starnet, China’s biggest LEOsat project, will own 55%, and aerospace contractor Norinco, a 25% shareholder.

China Telecom will shutter its legacy satellite subsidiary, established in 2009, and transfer the assets into the new company.

The other new business, China Shikong, lists its scope as satellite communication, satellite navigation and remote sensing services.

The two investments come as China Starnet is readying to launch its first satellites in the second half of the year. It is aiming to build a constellation of 13,000, with the first 1,300 going into operation over the next five years, local media has reported.

In addition to Starnet, two other mass constellations are planned – the state-owned G60 and a private operator, Shanghai Hongqing. Neither has set a timetable. They will be playing catch up with western operators like Starlink and OneWeb, which are already operating thousands of commercial satellites.

Since foreign operators are forbidden from selling into China, it is not yet clear how China is going to structure its LEO satellite industry and what role precisely the new operators are going to play.

References:

Chinese telcos tip cash into satellite (lightreading.com)

China Mobile launches LEO satellites to test 5G and 6G – Developing Telecoms

Very low-earth orbit satellite market set to reach new heights | TelecomTV

5G connectivity from space: Exolaunch contract with Sateliot for launch and deployment of LEO satellites

LEO operator Sateliot joins GSMA; global roaming agreements to extend NB-IoT coverage

Momentum builds for wireless telco- satellite operator engagements

Satellite 2024 conference: Are Satellite and Cellular Worlds Converging or Colliding?

Satellite 2024 conference: Are Satellite and Cellular Worlds Converging or Colliding?

Converged terrestrial and satellite connectivity is a given, but the path is strewn with unknowns and sizable technological and business challengers, according to satellite operator CEOs. Hopefully, 3GPP Release 18 will contain the necessary specifications for it to be implemented as we explained in this IEEE Techblog post.

During Access Intelligence’s Satellite 2024 conference in Washington DC this week, Viasat CEO Mark Dankberg said satellite operators must start thinking and acting like mobile network operators, creating an ecosystem that allows seamless roaming among them. Terrestrial/non-terrestrial network (NTN) convergence requires “a complete rethinking” of space and ground segments, as well as two to three orders of magnitude improvement in data pricing, Dankberg said. Standards will help get satellite and terrestrial to fit together, but that evolution will happen slowly, taking 10 to 15 years, Iridium CEO Matt Desch said. It remains to be seen how direct-to-device services will make money, he added. Satellite-enabled SOS messaging on smartphones “is becoming free, and our satellites are not free — we need to make money on it some way,” Desch added.

The regulatory environment around satellite has changed tremendously during the past decade, with the FCC very oriented toward mobile networks’ spectrum needs and now satellite matters making up most of the agenda for the 2027 World Radiocommunication Conference, Desch said. However, there will be regulatory challenges to resolve in satellite/terrestrial convergence, he predicted. There are significant synergies in having a 5G terrestrial network and satcom assets under one roof, he said. Blurring the lines between terrestrial and non-terrestrial makes it easier for manufacturers to build affordable equipment that operates in both modes, Desch concluded.

That inevitable convergence is being driven by declining launch costs, maturing technologies and improved manufacturing, all of which make non-terrestrial network connectivity more economically competitive, said EchoStar CEO Hamid Akhavan. He said the EchoStar/Dish Network combination (see 2401020003) was driven in part by that convergence, consolidating EchoStar’s S-band spectrum holdings outside the U.S. with Dish’s S-band holdings inside the country. The deal also melds Dish’s network operator expertise with Hughes’ satellite expertise.

Wednesday Opening General Session: Are Satellite and Cellular Worlds Converging or Colliding?

To ensure space’s sustainability, missions must follow the mantra of “leave nothing behind,” sustainability advocates said. Space operators should have more universal protocols and vocabulary when exchanging space situational awareness data, as well as more uniformity in what content gets exchanged, said Space Data Association Executive Director Joe Chan. When it comes to space sustainability, clutter isn’t necessarily dangerous, and any rules fostering sustainability should avoid restricting the use of space, he said. Space lawyer Stephanie Roy of Perkins Coie said a mission authorization framework covering space operations that fall outside the regulatory domain of the FCC, FAA and NOAA is needed. Space operators and investors see sustainability rules as inevitable and want to ensure they allow flexibility and don’t mandate use of any particular technology, she added. Many speakers called for a “circular economy” in space, with more reuse of materials via refueling, reuse or life extension.

Separately, space sustainability advocates urged a mission authorization regulatory framework and universal use of design features such as docking plates enabling on-orbit serving or towing. Meanwhile, conference organizers said event attendance reached 14,000.

Also, ITU Secretary-General Doreen Bogdan-Martin urged the satellite industry to join ITU’s Partner2Connect digital coalition aimed at addressing digital divide issues, particularly in the least-developed nations and in landlocked and small island developing countries. The digital divide “is right up there” with climate change as a pressing issue for humanity, said Bogdan-Martin. She noted the coalition has received $46 billion in commitments, with a target of $100 billion by 2026.

References:

https://communicationsdaily.com/article/view?BC=bc_65fb60473d5de&search_id=836928&id=1911572

ABI Research and CCS Insight: Strong growth for satellite to mobile device connectivity (messaging and broadband internet access)

SatCom market services, ITU-R WP 4G, 3GPP Release 18 and ABI Research Market Forecasts

https://www.3gpp.org/specifications-technologies/releases/release-18