Uncategorized

India 5G subscribers top 400 Million with rapid adoption continuing without 5Gi

With over 400 million 5G subscribers, India now ranks #2 globally (China is #1 [1.]). What’s even more remarkable is the speed of adoption after 5G spectrum auctions were repeatedly delayed. Jyotiraditya Scindia, India’s union minister for communications and development of the North Eastern Region, said the country is “setting new global benchmarks in scale, speed and digital transformation.”

According to figures cited by the minister, the country’s 5G subscriber base now exceeds that of other major markets, including the United States with around 350 million users, the European Union with 200 million, and Japan with 190 million. China remains the global leader, with more than 1.2 billion 5G connections.

Note 1. China has over 1.2 billion 5G subscribers as of late 2025, representing over 60% of all mobile connections in the country, driven by massive infrastructure rollout and strong adoption across major operators like China Mobile, China Telecom, and China Unicom, making it the global leader in 5G penetration.

……………………………………………………………………………………………………………………………………………………………………………………………………..

Bharti Airtel and Reliance Jio Infocomm spearheaded the launch, becoming the first carriers to operationalize 5G networks and achieving significant subscriber acquisition, with each surpassing the 50 million user milestone within their initial year of service [1]. Vodafone Idea subsequently entered the 5G market with launches in specific cities during 2025.

State-owned telecom provider BSNL is projected to launch 5G services within the current year [1]. This deployment is slated to exclusively utilize India’s indigenously developed telecom technology stack, a collaborative effort involving the Centre for Development of Telematics (C-DOT), Tejas Networks, and Tata Consultancy Services (TCS).

As of the close of 2025, the national 5G infrastructure comprised 518,854 operational base stations, marking a substantial increase from approximately 464,990 recorded at the start of the year [1]. The Department of Telecommunications (DoT) reported the deployment of 4,112 new 5G base transceiver stations (BTS) in December 2025 alone, contributing to the year-end cumulative total

- Infrastructure Growth: Rapid BTS deployment, exceeding 4,100 new installations in December 2025 alone, demonstrates intense network densification, with coverage now reaching most districts.

- Vodafone Idea’s Entry: Vi, after initial delays, commenced its phased 5G service introduction in select cities during 2025.

- BSNL’s Indigenous Strategy: The state-owned operator is slated to launch 5G using India’s homegrown stack (C-DOT, Tejas, TCS), showcasing self-reliance in telecom technology.

- Market Dynamics: The rapid expansion aims to unlock enterprise and consumer use cases, positioning India as a significant global 5G player, despite ongoing discussions about monetization and infrastructure investment.

Technical & Deployment Highlights:

- Architecture: A mix of 5G SA (Jio) and 5G NSA (Airtel) is prevalent, with SA offering lower latency and true 5G capabilities.

- Spectrum: Operators utilize various bands, including sub-6 GHz (3.3 GHz, 26 GHz) for broad coverage and capacity.

- Deployment Pace: Driven by ministerial targets, operators installed BTS at an accelerated pace, focusing initially on high-revenue urban centers.

This author deeply regrets that the Telecommunications Standards Development Society India (TSDSI)’s 5Gi RIT specification, included as part of the ITU-R M.2150 IMT 2020 RIT/SRIT standard, was not implemented in India. On January 25, 2022, TSDSI told the Telecommunication Engineering Center (TEC) under the DoT not to proceed with the adoption of 5Gi as a national 5G standard. TSDSI added that it “does not intend to further update 5Gi specifications.”

References:

OpenSignal: real world 5G deployment in India, market status & what happened to 5Gi?

Nokia Executive: India to Have Fastest 5G Rollout in the World; 5Gi/LMLC Missing!

LightCounting & TÉRAL RESEARCH: India RAN market is buoyant with 5G rolling out at a fast pace

Nokia’s Bell Labs to use adapted 4G and 5G access technologies for Indian space missions

Reliance Jio in talks with Tesla to deploy private 5G network for the latter’s manufacturing plant in India

Communications Minister: India to be major telecom technology exporter in 3 years with its 4G/5G technology stack

India to set up 100 labs for developing 5G apps, business models and use-cases

Adani Group to launch private 5G network services in India this year

Adani Group planning to enter India’s long delayed 5G spectrum auction

At long last: India enters 5G era as carriers spend $ billions but don’t support 5Gi

5G in India to be launched in 2023; air traffic safety a concern; 5G for agricultural monitoring to be very useful

Bharti Airtel to launch 5G services in India this August; Reliance Jio to follow

5G Made in India: Bharti Airtel and Tata Group partner to implement 5G in India

India government wants “home-grown” 5G; BSNL and MTNL will emerge as healthy

5G in India dependent on fiber backhaul investments

Hindu businessline: Indian telcos deployed 33,000 5G base stations in 2022

Arm Holdings unveils “Physical AI” business unit to focus on robotics and automotive

- Cloud and AI: Focused on data center and AI infrastructure solutions.

- Edge: Encompassing mobile devices, personal computing, and related technologies.

- Physical AI: Integrating its automotive business with robotics initiatives.

- Market Opportunity: Acknowledged the significant growth potential in robotics, from industrial automation to humanoid robots, driven by AI advancements.

- Synergy with Automotive: Combined robotics and automotive within the unit due to shared technical needs, such as power efficiency, safety, and sensor technology.

- Strategic Reorganization: Positioned Physical AI as a third core business line, alongside Cloud & AI and Edge (mobile/PC), to better focus resources and expertise.

- Customer Demand: Responding to existing customers (like automakers and robotics firms such as Boston Dynamics) who are integrating more AI into physical devices.

- Enhancing Real-World Impact: Aims to deliver solutions that fundamentally improve labor, productivity, and potentially GDP, moving AI from data centers to physical interactions

2026 Consumer Electronics Show Preview: smartphones, AI in devices/appliances and advanced semiconductor chips

Marvell shrinking share of the RAN custom silicon market & acquisition of XConn Technologies for AI data center connectivity

Groq and Nvidia in non-exclusive AI Inference technology licensing agreement; top Groq execs joining Nvidia

The Internet of Things (IoT) explained along with ARM’s role in making it happen!

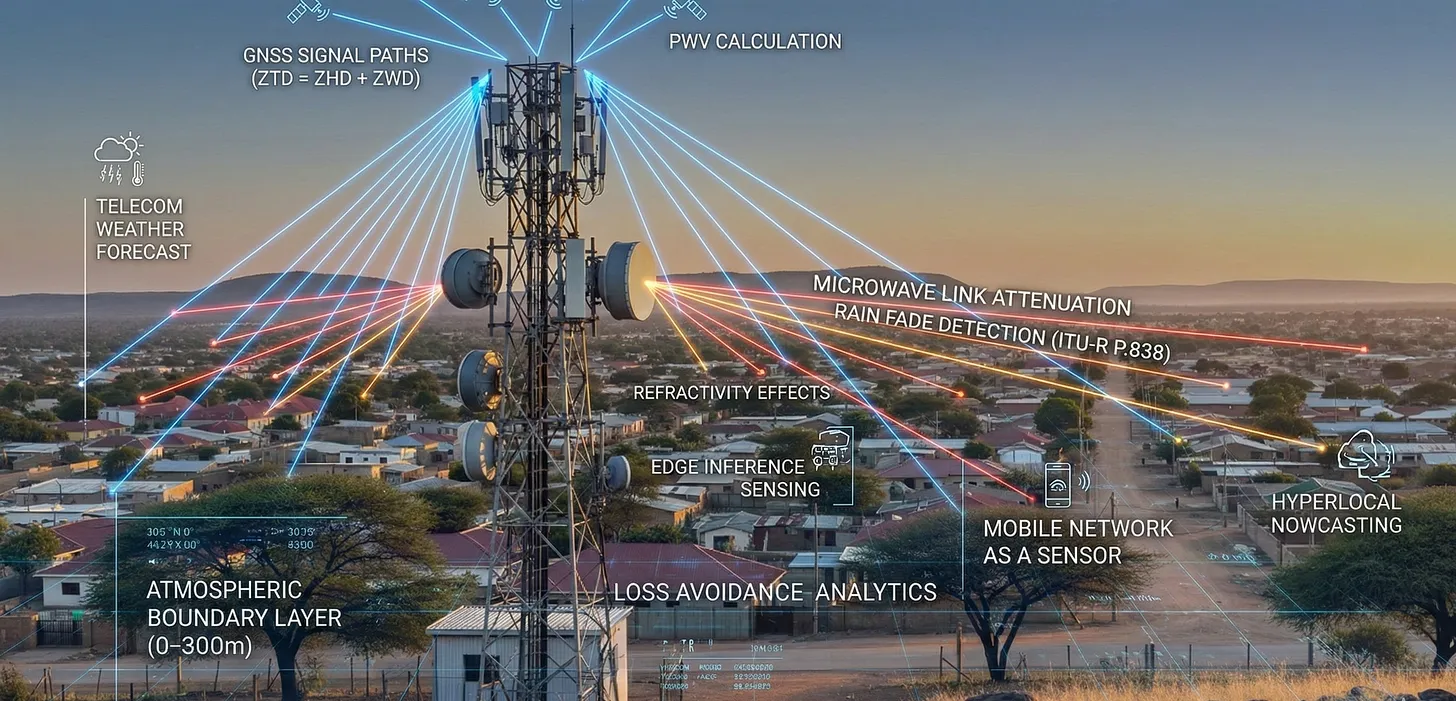

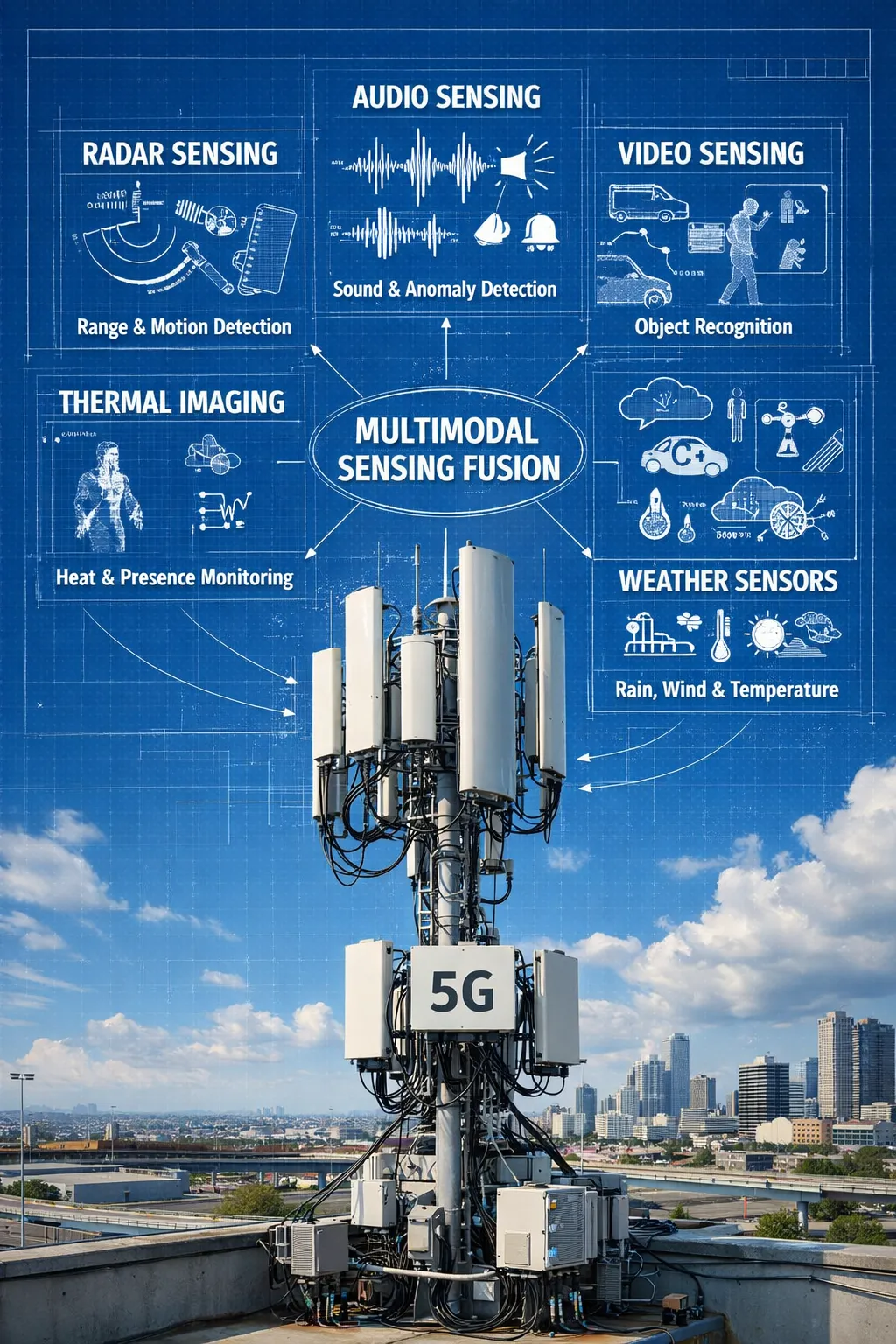

Sebastian Barros: Using telecom networks for weather sensing requires a strategic telco shift from connectivity providers to ecosystem orchestrators

Telecom networks for weather sensing can be facilitated by using existing microwave links and 4G/5G signals as virtual sensors, detecting changes in signal strength and timing caused by rain, humidity, and temperature, effectively turning vast infrastructure into a dense, real-time atmospheric monitoring system for improved forecasting and disaster alerts, notes Sebastian Barros on Substack. By analyzing signal attenuation, telecom networks create high-resolution weather maps, complementing traditional methods like radar. Yet very few network operators or vendors have attempted to use telecommunications infrastructure for dense atmospheric sensing. The data exists but is rarely activated, processed, or disclosed.

Global Navigation Satellite System (GNSS) [1.] based atmospheric estimation, rain attenuation on microwave links, and radio refractivity effects have been studied for more than 20 years. The physics is well understood and already embedded in network planning and synchronization systems. There are eight million radio sites span cities, roads, ports, factories, and borders. Every site has power, compute, backhaul, antennas, timing, and regulatory protection. Today, the network only provides connectivity. Integrated Sensing and Communication (ISAC) starts to change that. It repurposes radio waves for radar-like sensing, including presence detection, velocity, Doppler shift, and range.

……………………………………………………………………………………………………………………………………………………………………………

Note 1. Global Navigation Satellite System (GNSS) is the umbrella term for satellite constellations like the U.S.’s GPS, Russia’s GLONASS, the EU’s Galileo, and China’s BeiDou, which provide global positioning, navigation, and timing (PNT) services. GNSS receivers use signals from these orbiting satellites to calculate precise locations on Earth, offering increased accuracy and reliability compared to relying on a single system, enabling applications from smartphone navigation to autonomous vehicles and precision agriculture.

……………………………………………………………………………………………………………………………………………………………………………

- Receiver: Your end point receiving device (phone, car navigation, etc.) picks up signals from several of these satellites.

- Calculation: By measuring the time it takes for signals to arrive from at least four satellites, the receiver performs complex calculations (trilateration) to pinpoint your exact position.

Telecom networks can expose not just connectivity but structured awareness: object motion, crowd flow, anomalies, risks, and environmental state. In real time, across every continent. The infrastructure already exists. What’s missing is the architecture and the will to build the sensing layer on top of it. With dense, real-time sensing already in place, telecom can expose environmental intelligence through Open Gateway APIs, just as it exposes location or quality today. No new hardware. No new towers. Just activation, inference at the edge, and exposure.

- Data Siloing: The data produced by ISAC currently remains locked within the physical (PHY) and Media Access Control (MAC) layers of the network. It is primarily used for internal network optimization and is not exposed to external applications or platforms.

- Lack of Abstraction and APIs: There are no standard abstraction layers or Application Programming Interfaces (APIs) that would allow external systems (e.g., weather services, autonomous navigation systems, urban infrastructure management) to access and interpret the raw sensing data.

- Absence of Data Fusion Standards: There is no standard methodology to fuse the output from ISAC with data from other sensing modalities (e.g., vision, audio, thermal sensors). This prevents the creation of a comprehensive, multimodal sensing mesh.

- Missing Marketplace: The lack of standardized access and integration means there is no marketplace for this valuable data, which stifles innovation and collaboration across different industries that could benefit from real-world awareness information.

References:

https://sebastianbarros.substack.com/p/telecom-built-the-worlds-best-weather

https://sebastianbarros.substack.com/p/telco-network-as-a-sensor-is-a-huge

https://www.linkedin.com/feed/update/urn:li:activity:7413260481743769600/

https://www.euspa.europa.eu/eu-space-programme/galileo/what-gnss

2025 Year End Review: Integration of Telecom and ICT; What to Expect in 2026

Smart electromagnetic surfaces/RIS: an optimal low-cost design for integrated communications, sensing and powering

Deutsche Telekom: successful completion of the 6G-TakeOff project with “3D networks”

Smart electromagnetic surfaces/RIS: an optimal low-cost design for integrated communications, sensing and powering

Researchers at Xidian University in China have pioneered a smart electromagnetic surface that converts ambient electromagnetic waves into electrical power, marking a potential leap in stealth and wireless technologies. This meta-surface innovation merges advanced electromagnetic engineering with communication principles, enabling self-powered systems for demanding applications. The self-sustaining electronic system integrates wireless information transfer and energy harvesting and has the potential to upend the dynamics of electronic warfare.

The surface facilitates simultaneous energy harvesting and data transmission, drawing power from radar or environmental signals without traditional batteries. Xidian’s team highlights its role in “electromagnetic cooperative stealth,” where networked platforms collaboratively minimize radar cross-sections and sensor detectability. Prototypes demonstrate viability for real-time wave manipulation, building on metasurface designs that dynamically adjust phase and amplitude.

The researchers said this included investigating “electromagnetic cooperative stealth,” where multiple entities work together to reduce their visibility to radar and electromagnetic sensors. In electronic warfare, the technology flips the script on radar threats: stealth aircraft could harvest enemy beams for propulsion or comms, reducing logistical vulnerabilities. This cooperative approach extends to multi-asset formations, enhancing collective invisibility across spectra.

Early tests align with broader Reconfigurable Intelligent Surfaces (RIS), a two-dimensional reflecting surface. RIS advancements facilitate beam steering up to ±45° with low side lobes. According to a paper published in the IEEE Internet of Things magazine last year, RIS could also be used in anti-jamming technology, unmanned aerial vehicle communication and radio surveillance – all of which are difficult to do using older optimization tools.

Reconfigurable intelligent surfaces can also be configured to create intentional radio “dead zones” to mitigate interference and reduce the risk of eavesdropping, according to German electronics manufacturer Rohde & Schwarz. The European Space Agency has further highlighted RIS as a candidate technology for satellite-to-ground communications, where controllable reflection and redirection of signals could help route links around physical obstacles.

For telecommunications, the surface promises 6G breakthroughs like integrated sensing and powering satellites or base stations. China’s lead here could accelerate reconfigurable networks, improving coverage in non-line-of-sight scenarios. Ongoing refinements target complex interactions for higher precision. By including sensing, communication and power into one hardware platform, the device could allow for a range of advanced applications while reducing eavesdropping and interference.

“Ultimately, it is expected to have a broad impact on 6G communications, the Internet of Things, intelligent stealth and other related fields,” the team said in a paper published in the peer-reviewed journal National Science Review last month. Many scientists say that a key area for next-generation wireless communications will be the transmission channel.

Researchers from Fudan University, the University of Sydney and the Commonwealth Scientific and Industrial Research Organization note that, when combined with artificial intelligence (AI), this technology could significantly enhance the security of air-to-ground Internet of Things (IoT) links.

In their latest publication, the Xidian University team describes RIS as a “powerful solution” for future wireless networks, citing its low cost, high programmability and ease of deployment. However, for 6G systems, RIS must support both communication and sensing on a unified hardware platform by integrating data transmission and radar-like functionality to lower cost and optimize spectrum and hardware resource utilization.

Addressing this requirement will demand architectures that can jointly manipulate both scattered electromagnetic waves and actively radiated signals. The researchers propose that an electromagnetic all-in-one radiation–scattering RIS architecture could provide a viable path to meeting this dual-control challenge. “This achieves significant savings in physical space and cost while ensuring multifunctionality across diverse application scenarios,” the team said. The RIS system could also work in a receiver mode to harvest wireless energy to be used to power the meta-surface itself or charge other electronic devices, the paper added.

It could be used for line-of-sight wireless communication, where there is a direct, unobstructed path between a transmitter and receiver, as well as non-line-of-sight wireless communication, in which there is no direct visual link due to physical barriers like buildings.

The proposed RIS “stands out as the optimal low-cost design” for integrated communication and sensing. “In the future, this architecture could enable the development of environment-adaptive integrated sensing and communication systems, micro base stations and relay integrated systems, as well as self-powered sensing systems,” the team said.

………………………………………………………………………………………………………………………………………………………………………………………

References:

https://ieeexplore.ieee.org/document/10907868

Nokia sees new types of 6G connected devices facilitated by a “3 layer technology stack”

Electromagnetic Signal & Information Theory (ESIT): From Fundamentals to Standardization-Part I.

Electromagnetic Signal and Information Theory (ESIT): From Fundamentals to Standardization-Part II.

IMT Vision – Framework and overall objectives of the future development of IMT for 2030 and beyond

ITU-R WP5D: Studies on technical feasibility of IMT in bands above 100 GHz

Summary of ITU-R Workshop on “IMT for 2030 and beyond” (aka “6G”)

Excerpts of ITU-R preliminary draft new Report: FUTURE TECHNOLOGY TRENDS OF TERRESTRIAL IMT SYSTEMS TOWARDS 2030 AND BEYOND

Juniper Research: Global 6G Connections to be 290M in 1st 2 years of service, but network interference problem looms large

Groq and Nvidia in non-exclusive AI Inference technology licensing agreement; top Groq execs joining Nvidia

AI chip startup Groq [1.] today announced that it has entered into a non-exclusive licensing agreement with Nvidia for Groq’s AI inference technology [2.]. The agreement reflects a shared focus on expanding access to high-performance, low cost inference. As part of this agreement, Jonathan Ross, Groq’s Founder, Sunny Madra, Groq’s President, and other members of the Groq team will join Nvidia to help advance and scale the licensed technology. Groq will continue to operate as an independent company with Simon Edwards stepping into the role of Chief Executive Officer. GroqCloud will continue to operate without interruption. It remains to be seen how Groq’s new collaboration with Nvidia will effect its recent partnership with IBM.

Note 1. Founded in 2016, Groq specializes in what is known as inference, where artificial intelligence (AI) models that have already been trained respond to requests from users. While Nvidia dominates the market for training AI models (see Note 2.), it faces much more competition in inference, where traditional rivals such as Advanced Micro Devices have aimed to challenge it as well as startups such as Groq and Cerebras Systems.

Note 2. Training AI models (used by Nvidia GPUs) involves teaching a model to learn patterns from large amounts of data, while AI “inferencing” refers to using that trained model to generate outputs. Both processes demand massive computing power from AI chips.

…………………………………………………………………………………………………………………………………………………………………………………………………….

Groq has achieved a significant financial milestone, elevating its post-money valuation to $6.9 billion from $2.8 billion following a successful $750 million funding round in September. The company distinguishes itself in the competitive AI chip landscape by employing a unique architectural approach that does not rely on external high-bandwidth memory (HBM) chips. This design choice, leveraging on-chip static random-access memory (SRAM), mitigates the supply chain constraints currently impacting the global HBM market.

The LPU (Language Processing Unit) architecture, while enhancing inference speed for applications like chatbots, currently presents limitations regarding the maximum size of AI models that can be efficiently served. Groq’s primary competitor utilizing a similar architectural philosophy is Cerebras Systems, which has reportedly commenced preparations for an initial public offering (IPO) as early as next year. Both companies have strategically secured substantial contracts in the Middle Eastern market.

Nvidia’s investments in AI firms span the entire AI ecosystem, ranging from large language model developers such as OpenAI and xAI to “neoclouds” like Lambda and CoreWeave, which specialize in AI services and compete with its Big Tech customers. Nvidia has also invested in chipmakers Intel and Enfabrica. The company made a failed attempt around 2020 to acquire British chip architecture designer Arm Ltd. Nvidia’s wide-ranging investments — many of them in its own customers — have led to accusations that it’s involved in circular financing schemes reminiscent of the dot-com bubble. The company has vehemently denied those claims.

…………………………………………………………………………………………………………………………………………………………………..

This deal follows a familiar pattern in recent years where the world’s biggest technology firms pay large sums in deals with promising startups to take their technology and talent but stop short of formally acquiring the target.

- A great example of that was Meta which in June invested ~$14.3 billion in Scale AI for a 49% stake in the company. That move valued the startup at around $29 billion. As part of that deal, 28 year old Alexandr Wang resigned as CEO of Scale AI to become Meta’s first-ever Chief AI Officer. He will remain on Scale AI’s board of directors. Wang’s team at the new “superintelligence” lab is tasked with building advanced AI systems that can surpass human-level intelligence.

- In a similar but smaller scale deal, Microsoft agreed to pay AI startup Inflection about $650 million in cash in an unusual arrangement that would allow Microsoft to use Inflection’s models and hire most of the startup’s staff including its co-founders, a person familiar with the matter told Reuters. The high-profile AI startup’s models will be available on Microsoft’s Azure cloud service, the source said. Inflection is using the licensing fee to pay Greylock, Dragoneer and some other investors, the source added, saying the investors will get a return of 1.5 times what they invested.

Bernstein analyst Stacy Rasgon wrote in a note to clients on Wednesday after Groq’s announcement:

“The Nvidia-Groq deal appears strategic in nature for Nvidia as they leverage their increasingly powerful balance sheet to maintain dominance in key areas…..Antitrust would seem to be the primary risk here, though structuring the deal as a non-exclusive license may keep the fiction of competition alive (even as Groq’s leadership and, we would presume, technical talent move over to Nvidia). Nvidia CEO Jensen Huang’s “relationship with the Trump administration appears among the strongest of the key U.S. tech companies.”

…………………………………………………………………………………………………………………………………………………………………………………………………………….

Nvidia CEO Jensen Huang recently dedicated a significant portion of his 2025 GTC 2025 conference keynote speech to emphasize that Nvidia intends to maintain its market dominance as the AI sector increasingly transitions its focus from model training to inference workloads. Huang delivered two major GTC keynotes in 2025: The primary annual conference held in San Jose, California, in March 2025 and a second GTC in Washington, D.C., in October 2025. At these events, he emphasized the rise of “reasoning AI” and “agentic AI” as the drivers for an unprecedented 100x surge in demand for inference computing in just a couple of years. Huang announced that the new Blackwell system, designed as a “thinking machine” for reasoning, was in full production and optimized for both training and large-scale inference workloads.

Huang shared a vision of moving from traditional data centers to “AI factories“—ultra-high-performance computing environments designed specifically to generate intelligence at scale, positioning investment in Nvidia’s infrastructure as an economic necessity.

…………………………………………………………………………………………………………………………………………………………………………………………………………….

References:

https://www.arm.com/glossary/ai-inference

IBM and Groq Partner to Accelerate Enterprise AI Inference Capabilities

Sovereign AI infrastructure for telecom companies: implementation and challenges

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

Custom AI Chips: Powering the next wave of Intelligent Computing

OpenAI and Broadcom in $10B deal to make custom AI chips

Reuters & Bloomberg: OpenAI to design “inference AI” chip with Broadcom and TSMC

Analysis: OpenAI and Deutsche Telekom launch multi-year AI collaboration

Expose: AI is more than a bubble; it’s a data center debt bomb

Will the wave of AI generated user-to/from-network traffic increase spectacularly as Cisco and Nokia predict?

Ookla: FWA Speed Test Results for big 3 U.S. Carriers & Wireless Connectivity Performance at Busy Airports

Ookla just released two new reports based on Speedtest Intelligence data, revealing critical shifts in how Americans connect to the Internet- from their homes and from the country’s 50 busiest airports.

Key findings from the first report:

- T-Mobile, AT&T and Verizon — adding 1.04 million new subscribers in Q3 2025 bringing the total number of FWA customers to 14.7 million, which is slightly more than 12.5% of the 117.4 million U.S. households with broadband, according to the U.S. Census Bureau’s 2024 American Community Survey.

- T-Mobile, Verizon and AT&T all experienced declines in both their median download and upload speeds during Q2 2025 and Q3 2025.

- T-Mobile is the FWA speed leader with median download speed of 209.06 Mbps for Q3 2025, which is approximately double that of AT&T’s median download speed of 104.63 Mbps in the same quarter.

- AT&T and T-Mobile customers in the 10th percentile of users are experiencing speed declines during peak hours in the late afternoon and evening. Verizon subscribers in the 10th percentile don’t have the same sorts of declines, indicating the operator’s enforcement of speed caps may be helping it deliver a more consistent experience to those customers.

- AT&T Internet Air’s latency is higher than its peers but it’s improving. AT&T’s median multi-server latency is ~ 67 milliseconds, “consistently higher” than Verizon (54 ms) and T-Mobile (50 ms) but a notable improvement from 78 ms in Q3 2024.

Separately, the analysts at New Street Research estimated AT&T, T-Mobile and Verizon can currently support up to 32 million FWA customers and they have already added nearly 50% of that number. Operators could potentially increase that load to 36 million following the Federal Communications Commission’s (FCC) upper C-Band auction.

…………………………………………………………………………………………………………………………………………………………………………………

Ookla’s second report analyzes cellular and Wi-Fi performance across the top 50 U.S. airports by passengers. Key findings:

- Cellular network providers had a faster median download speed than Wi-Fi in most airports and more than twice as fast on average. The overall median download speed for cellular was 219.24 Mbps. Note that 5G/4G splits were not explicitly examined.

- Verizon was fastest in the most airports comparing among all mobile providers and airport Wi-Fi including ties.

- Airport Wi-Fi was faster than mobile networks in just over one-third of head-to-head comparisons (including ties), and faster than all mobile providers in five airports.

- Older Wi-Fi technologies may be holding back internet speed in airports with 72.9% of Speedtest samples on Wi-Fi 5 and older generation versus 46.0% in the U.S. overall.

Wi-Fi was faster than any mobile provider in these five airports:

- Cincinnati/Northern Kentucky International

- San Francisco International

- Orlando International

- Hartsfield–Jackson Atlanta International

- Baltimore/Washington International (tie)

Wi-Fi is better by the Bay:

As shown in Wi-Fi’s fastest five airports, Oakland International and Norman Y. Mineta San José International made that list. Rounding out the Bay Area airportstrio, the Wi-Fi speed in San Francisco International comfortably topped the mobile providers.

| Airport | AT&T | T-Mobile | Verizon | Airport Wi-Fi |

| Oakland International | 229.70 | 28.58 | 103.90 | 194.23 |

| Norman Y. Mineta San José International | 103.83 | 211.40 | 251.06 | 176.59 |

| San Francisco International (SFO) | 67.07 | 92.91 | 100.56 | 169.51 |

SFO was the only airport in Ookla’s analysis with Speedtest samples using the 6 GHz band. This was on Wi-Fi 6E – too soon to expect Wi-Fi 7 in airports – with a median download speed of 364.74 Mbps (also remarkable were the median upload speed of 426.04 Mbps and an 8 ms multi-server latency).

References:

https://www.ookla.com/articles/u-s-fwa-report-december-2025

https://www.ookla.com/articles/cellular-faster-than-wi-fi-in-us-airports

Ookla: Global performance of Apple’s in-house designed C1 modem in iPhone 16e

Ookla: Uneven 5G deployment in Europe, 5G SA remains sluggish; Ofcom: 28% of UK connections on 5G with only 2% 5G SA

Ookla: Europe severely lagging in 5G SA deployments and performance

Highlights of Ookla’s 1st Half 2024 U.S. Connectivity Report

Ookla: T-Mobile and Verizon lead in U.S. 5G FWA

Ookla Q2-2023 Mobile Network Operator Speed Tests: T-Mobile is #1 in U.S. in all categories!

Highlights of ITU Global Connectivity Report 2025 and the Baku Action Plan

The ITU Global Connectivity Report 2025, released at the conclusion of the World Telecommunication Development Conference (WTDC-25) in Baku, Azerbaijan, delivers a comprehensive assessment of how global connectivity has evolved from a scarce asset in 1994 into a foundational layer of the digital economy and everyday life, with close to 6 billion users projected to be online by 2025. Its analytical framework is anchored in the policy objective of achieving universal and meaningful connectivity (UMC), structured across six interdependent dimensions: Quality, Availability, Affordability, Devices, Skills, and Security.

The report underscores the socio‑economic gains associated with large‑scale digital transformation, including enhanced productivity, innovation, and service delivery across sectors. At the same time, it emphasizes that progress is constrained by persistent digital divides along income, gender, age, and geographic lines, as well as by escalating exposure to online harms, misinformation, and non‑trivial environmental externalities from ICT infrastructure and usage.

It suggests the era of easy, organic network expansion is over. While 74% of the world is now online, the curve is flattening, and the remaining deficits are structural rather than merely about access.

With an estimated 2.2 billion people still offline, ITU Member States (194) agreed this week on the Baku Action Plan—a four-year roadmap to 2029 designed to close these persistent divides.

The report provides detailed analysis of structural barriers to universal and meaningful connectivity (UMC), notably high connectivity and device costs, gaps in digital skills, and constrained access to appropriate end‑user devices. It translates this analysis into evidence‑based policy guidance focused on regulatory coherence, targeted affordability interventions, and demand‑side enablers to ensure that connectivity translates into effective and inclusive digital usage.

From a network engineering and infrastructure perspective, the report highlights the critical role of resilient, high‑capacity backbones, including submarine cable systems and satellite constellations, as strategic layers of the global connectivity fabric. It stresses the need for coordinated investment, robust redundancy and security models, and integrated planning across terrestrial, subsea, and space‑based networks to support UMC objectives.

The report identifies high service and device costs, insufficient digital skills, and limited device availability as key barriers, and provides evidence‑based policy guidance on regulatory coherence, affordability, and demand‑side enablers. It emphasizes the importance of resilient infrastructure such as submarine cables and satellites, along with stronger national data ecosystems, to support inclusive connectivity strategies and informed digital policy‑making.

Finally, the report calls for strengthening national data ecosystems—covering data collection, governance, sharing, and analytics—as a prerequisite for effective digital inclusion strategies and evidence‑driven policy‑making. It positions mature data capabilities and coherent digital governance frameworks as key enablers for monitoring progress across the six UMC dimensions and for calibrating telecom and ICT policy in line with evolving market and technology dynamics.

References:

https://www.itu.int/itu-d/reports/statistics/global-connectivity-report-2025/

ITU’s Facts and Figures 2025 report: steady progress in Internet connectivity, but gaps in quality and affordability

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

ITU-R report: Applications of IMT for specific societal, industrial and enterprise usages

https://www.itu.int/itu-d/reports/statistics/global-connectivity-report-2022/

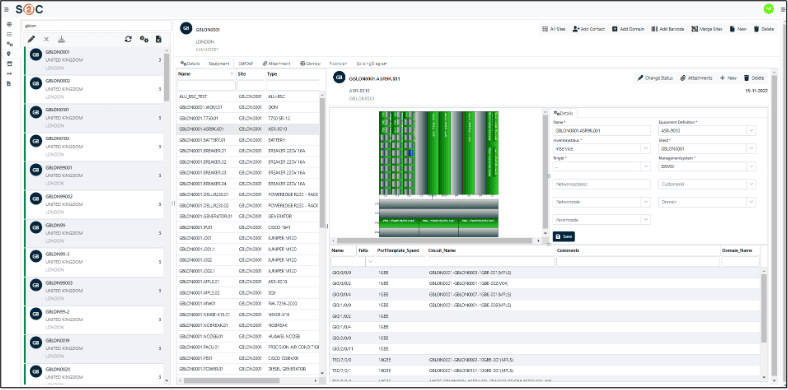

VC4 Advances OSS Transformation with an Efficient and Reliable AI enabled Network Inventory System

By Juhi Rani assisted by IEEE Techblog editors Ajay Lotan Thakur and Sridhar Talari Rajagopal

Introduction:

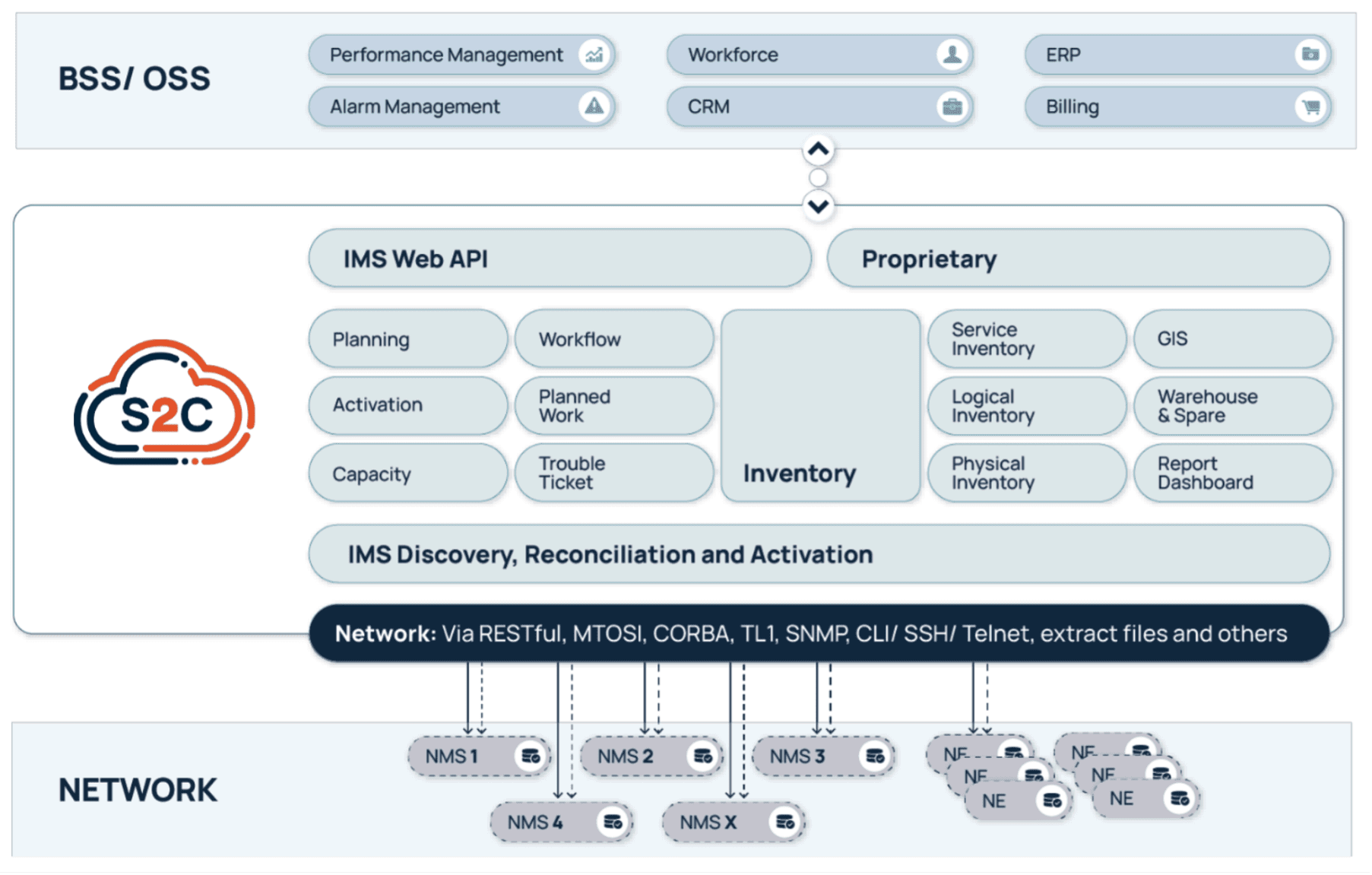

This year, 2025, VC4 [a Netherlands Head Office (H/O) based Operational Support System (OSS) software provider] has brought sharp industry focus to a challenge that many experience in telecom. Many operators/carriers still struggle with broken, unreliable, and disconnected inventory systems. While many companies are demoing AI, intent-based orchestration, and autonomous networks, VC4’s newly branded offering, Service2Create (or S2C as it’s known to some), is refreshingly grounded. Also as we have learnt very quickly, bad data into AI is a “no-no”. None of the orchestration and autonomous networks, will work accurately if your OSS is built on flawed data. The age-old saying “Garbage in, Garbage out” comes to mind.

VC4’s platform, Service2Create (S2C), is a next-generation OSS inventory system that supports the evolving needs of telecom operators looking to embrace AI, automate workflows, and run leaner, smarter operations. Service2Create is built from over two decades of experience of inventory management solutions – IMS. By focusing on inventory accuracy and network transparency, S2C gives operators a foundation they can trust.

Inventory: The Most Underestimated Barrier to Transformation

In a post from TM Forum, we observed that operators across the world are making huge investments in digital transformation but many are slowed by a problem closer to the ground: the inability to know what exactly is deployed in the network, where it is, and how it’s interconnected.

VC4 calls this the “silent blocker” to OSS evolution.

Poor mis-aligned inventory undermines everything. It breaks service activations, triggers unnecessary truck rolls, causes billing mismatches, and frustrates assurance teams. Field engineers often discover real-world conditions that don’t match what’s in the system, while planners and support teams struggle to keep up. The problem doesn’t just stop with network data.

In many cases, customer records were also out of date or incomplete… and unknown inventory can also be a factor. Details like line types, distance from the central office, or whether loading coils were present often didn’t match reality. For years, this was one of the biggest issues for operators. Customer databases and network systems rarely aligned, and updates often took weeks or months. Engineers had to double-check every record before activating a service, which slowed delivery and increased errors. It was a widespread problem across the industry and one that many operators have been trying to fix ever since.

Over time, some operators tried to close this gap with data audits and manual reconciliation projects, but those fixes never lasted long. Networks change every day, and by the time a cleanup was finished, the data was already out of sync again.

Modern inventory systems take a different approach by keeping network and customer data connected in real time. They:

- Continuously sync with live network data so records stay accurate.

- Automatically validate what’s in the field against what’s stored in the system.

- Update both customer and network records when new services are provisioned.

In short, we’re talking about network auto-discovery and reconciliation, something that Service2Create does exceptionally well. This also applies for unknown records, duplicate records and records with naming inconsistencies/variances.

It is achieved through continuous network discovery that maps physical and logical assets, correlates them against live service models, and runs automated reconciliation to detect discrepancies such as unknown elements, duplicates, or naming mismatches. Operators can review and validate these findings, ensuring that the inventory always reflects the true, real-time network state. A more detailed explanation can be found in the VC4 Auto Discovery & Reconciliation guide which can be downloaded for free.

Service2Create: Unified, Reconciled, and AI-Ready

Service2Create is designed to reflect the actual, current state of the network across physical, logical, service and virtual layers. Whether operators are managing fiber rollout, mobile backhaul, IP/MPLS cores, or smart grids, S2C creates a common source of truth. It models infrastructure end-to-end, automates data reconciliation using discovery, and integrates with orchestration platforms and ticketing tools.

To make the difference clearer here is the table below shows how Service2Create compares with the older inventory systems still used by many operators. Traditional tools depend on manual updates and disconnected data sources, while Service2Create keeps everything synchronized and validated in real time.

Comparison between legacy inventory tools and Service2Create (S2C)

| Feature | Legacy OSS Tools | VC4 Service2Create (S2C) |

|---|---|---|

| Data reconciliation | Manual or periodic | Automated and continuous |

| Inventory accuracy | Often incomplete or outdated | Real-time and verified |

| Integration effort | Heavy customization needed | Standard API-based integration |

| Update cycle | It takes days or weeks | Completed in hours |

| AI readiness | Low, needs data cleanup | High, with consistent and normalized data |

What makes it AI-ready isn’t just compatibility with new tools, it’s data integrity. VC4 understands that AI and automation only perform well when they’re fed accurate, reliable, and real-time data. Without that, AI is flying blind.

Built-in Geographic Information System (GIS) capabilities help visualize the network in geographic context, while no/low-code workflows and APIs support rapid onboarding and customization. More than software, S2C behaves like a data discipline framework for telecom operations.

Service2Create gives operators a current, trusted view of their network, improving accuracy and reducing the time it takes to keep systems aligned.

AI is Reshaping OSS… But only if the Data is Right

AI is driving the next wave of OSS transformation from automated fault resolution and dynamic provisioning to predictive maintenance and AI-guided assurance. But it’s increasingly clear: AI doesn’t replace the need for accuracy; it demands it.

In 2025, one common thread across operators and developers was this: telcos want AI to reduce costs, shorten response times, and simplify networks. According to a GSMA analysis, many operators continue to struggle as their AI systems depend on fragmented and incomplete datasets, which reduces overall model accuracy.

VC4’s message is cutting through: AI is only as useful as the data that feeds it. Service2Create ensures the inventory is trustworthy, reconciled daily with the live network, and structured in a way AI tools can consume. It’s the difference between automating chaos and enabling meaningful, autonomous decisions.

Service2Create has been adopted with operators across Europe and Asia. In national fiber networks, it’s used to coordinate thousands of kilometers of rollout and maintenance. In mixed fixed-mobile environments, it synchronizes legacy copper, modern fiber, and 5G transport into one unified model.

Designed for Operational Reality

VC4 didn’t build Service2Create for greenfield labs or ideal conditions. The platform is designed for real-world operations: brownfield networks, legacy system integrations, and hybrid IT environments. Its microservices-based architecture and API-first design make it modular and scalable, while its no/low-code capabilities allow operators to adapt it without long customization cycles. See the diagram below.

S2C is deployable in the cloud or on-premises and integrates smoothly with Operational Support System / Business Support System (OSS/BSS) ecosystems including assurance, CRM, and orchestration. The result? Operators don’t have to rip and replace their stack – they can evolve it, anchored on a more reliable inventory core.

What Industry Analysts are Saying

In 2025, telco and IT industry experts are also emphasizing that AI’s failure to deliver consistent ROI in telecom is often due to unreliable base systems. One IDC analyst summed it up: “AI isn’t failing because the models are bad, it’s failing because operators still don’t know what’s in their own networks.”

A senior architect from a Tier 1 European CSP added, “We paused a closed-loop automation rollout because our service model was based on inventory we couldn’t trust. VC4 was the first vendor we saw this year that has addressed this directly and built a product around solving it.”

This year the takeaway is clear: clean inventory isn’t a nice-to-have. It’s step one.

Looking Ahead: AI-Driven Operations Powered by Trusted Inventory

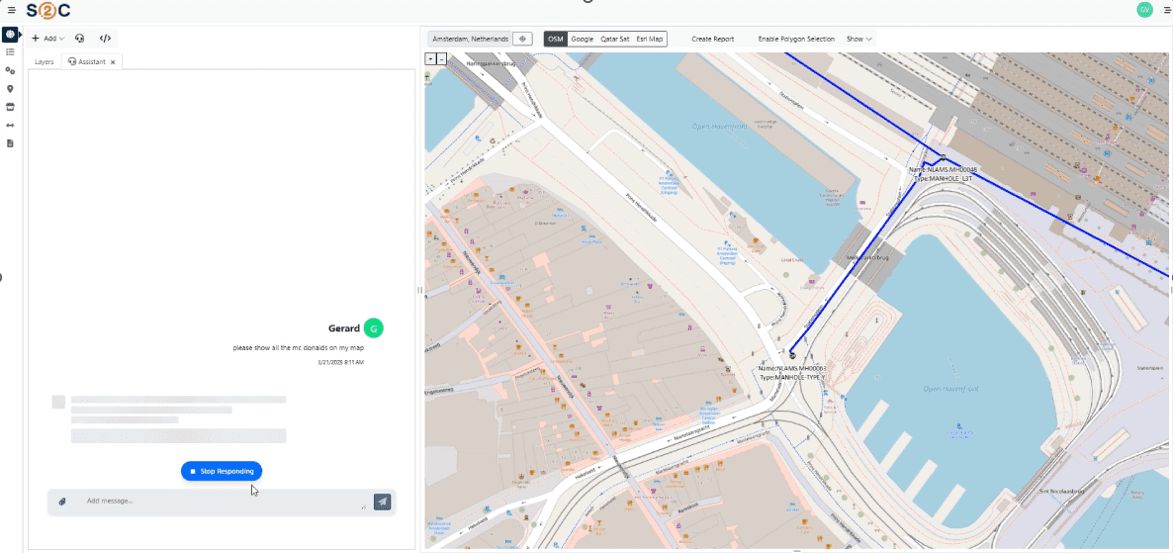

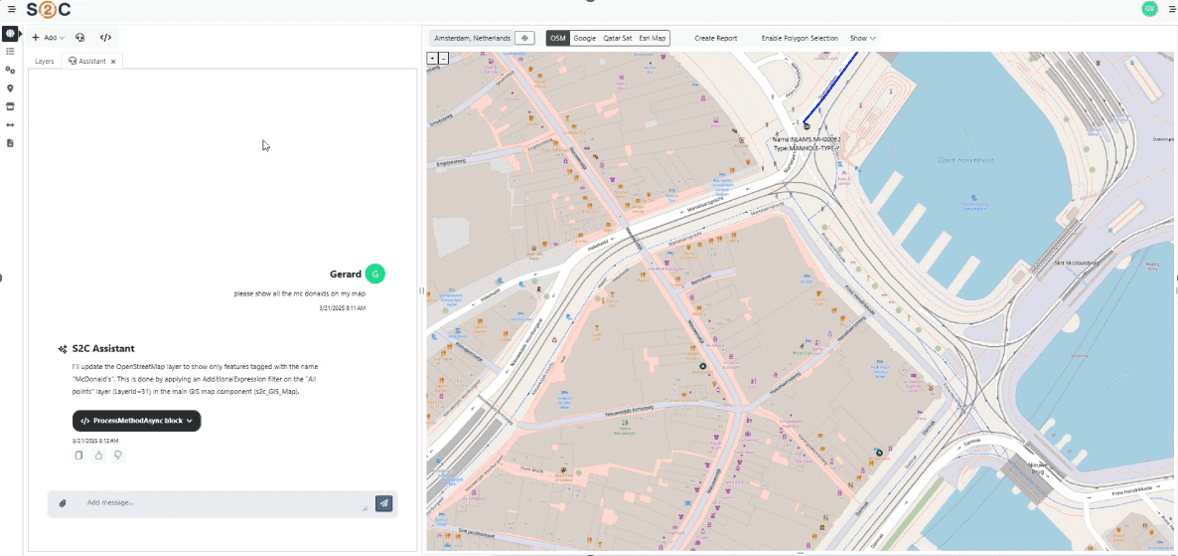

VC4 is continuing to enhance Service2Create with capabilities that support AI-led operations. Currently, S2C is enhanced with AI-powered natural language interfaces through Model Context Protocol (MCP) servers. This creates a revolutionary way for users to access their data and makes it also easier for them to do so. Simply ask for what you need, in plain language, and receive instant, accurate results from your systems of record.

The S2C platform now offers multiple synchronized access methods:

- Natural Language Interface

- Ask questions in plain language: “Show me network capacity issues in Amsterdam”

- AI translates requests into precise system queries

- No training required – productive from day one

- Direct API Access via MCP

- Programmatic access using Language Integrated Query (LINQ) expressions

- Perfect for integrations and automated workflows

- Industry-standard authentication (IDP)

- S2C Visual Platform

- Full-featured GUI for power users

- Parameterized deeplinks for instant component access

- Low/no-code configuration capabilities

- Hybrid Workflows

-

- Start with AI chat, graduate to power tools

- AI generates deeplinks to relevant S2C dashboards

Export to Excel/CSV for offline analysis

-

What It All Comes Down To

Digital transformation sounds exciting on a conference stage, but in the trenches of telecom operations, it starts with simpler questions. Do you know what’s on your network? Can you trust the data? Can your systems work together?

That’s what Service2Create is built for. It helps operators take control of their infrastructure, giving them the confidence to automate when ready and the clarity to troubleshoot when needed.

VC4’s approach isn’t flashy. It’s focused. And that’s what makes it so effective – a direction supported by coverage from Subseacables.net, which reported on VC4’s partnership with AFR-IX, to automate and modernize network operations across the Mediterranean.

………………………………………………………………………………………………………………….

About the Author:

Juhi Rani is an SEO specialist at VC4 B.V. in the Netherlands. She has successfully directed and supervised teams, evaluated employee skills and knowledge, identified areas of improvement, and provided constructive feedback to increase productivity and maintain quality standards.

Juhi earned a B. Tech degree in Electronics and Communications Engineering from RTU in Jaipur, India in 2015.

……………………………………………………………………………………………………………………………………………………………………..

Ajay Lotan Thakur and Sridhar Talari Rajagopal are esteemed members of the IEEE Techblog Editorial Team. Read more about them here.

Nokia Bell Labs and KDDI Research partner for 6G energy efficiency and network resiliency

Nokia Bell Labs and KDDI Research have partnered to advance 6G technology, focusing on improving network energy efficiency and resilience. The collaboration combines KDDI’s real-world network data and operational insights with Nokia Bell Labs’ expertise in energy consumption models and programmable network architectures. This joint research agreement, signed on November 5, 2025, builds on a long history of cooperation and aims to accelerate the development and deployment of sustainable, intelligent 6G networks.

Under this new agreement, the two companies are conducting research in two key areas of 6G:

- mMIMO energy efficiency: New techniques for reducing base-station energy consumption while enhancing communication, specifically targeted at proposed 6G spectrum.

- Distributed programmable core network services for 6G: New mobile core technologies that will ensure continuous communication during infrastructure failures and natural disasters.

KDDI Research and Nokia Bell Labs will demonstrate their initial work in mMIMO energy efficiency at the Brooklyn 6G Summit Nov 5 – 7.

Peter Vetter, President, Core Research, Nokia Bell Labs:

“Tackling the inherent challenges in a new generation of networking requires close collaboration in the industry. Working side by side, KDDI Research and Nokia Bell Labs can advance the state of the art in networking thanks to different perspectives on the problems and possible solutions. Ultimately, the joint outcomes will make 6G a more resilient, efficient and intelligent technology.”

Satoshi Konishi, President and CEO, KDDI Research:

“Through our strategic and close collaboration with Nokia Bell Labs, we aim to accelerate R&D initiatives and further strengthen the ‘Power to Connect’ toward 6G. We strive to continuously deliver new value to our customers and make meaningful contributions to societal progress.”

References:

KDDI unveils AU Starlink direct-to-cell satellite service

KDDI Partners With SpaceX to Bring Satellite-to-Cellular Service to Japan

KDDI Deploys DriveNets Network Cloud: The 1st Disaggregated, Cloud-Native IP Infrastructure Deployed in Japan

AWS Integrated Private Wireless with Deutsche Telekom, KDDI, Orange, T-Mobile US, and Telefónica partners

Samsung and KDDI complete SLA network slicing field trial on 5G SA network in Japan

Nokia’s Bell Labs to use adapted 4G and 5G access technologies for Indian space missions

Nokia and Rohde & Schwarz collaborate on AI-powered 6G receiver years before IMT 2030 RIT submissions to ITU-R WP5D

Highlights of Nokia’s Smart Factory in Oulu, Finland for 5G and 6G innovation

Will the wave of AI generated user-to/from-network traffic increase spectacularly as Cisco and Nokia predict?

Nokia Bell Labs claims new world record of 800 Gbps for transoceanic optical transmission

Nokia Bell Labs sets world record in fiber optic bit rates

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

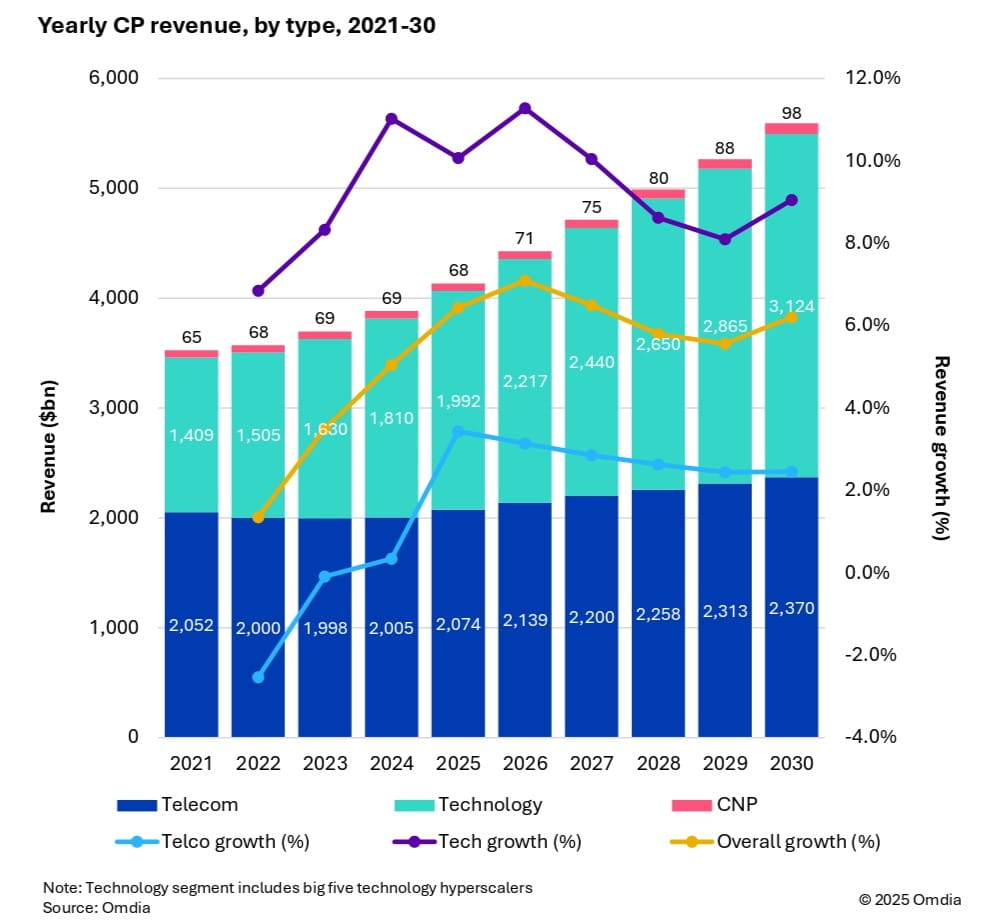

Market research firm Omdia (owned by Informa) this week forecast that 6G and AI investments are set to drive industry growth in the global communications market. As a result, global communications providers’ revenue is expected to reach $5.6 trillion by 2030, growing at a 6.2% CAGR from 2025. Investment momentum is also expected to shift toward mobile networks from 2028 onward, as tier 1 markets prepare for 6G deployments. Telecoms capex is forecast to reach $395 billion by 2030, with a 3.6% CAGR, while technology capex will surge to $545 billion, reflecting a 9.3% CAGR.

Fixed telecom capex will gradually decline due to market saturation. Meanwhile, AI infrastructure, cloud services, and digital sovereignty policies are driving telecom operators to expand data centers and invest in specialized hardware.

Key market trends:

- CP capex per person will increase from $74 in 2024 to $116 in 2030, with CP capex reaching 2.5% of global GDP investment.

-

Capital intensity in telecom will decline until 2027, then rise due to mobile network upgrades.

-

Regional leaders in revenue and capex include North America, Oceania & Eastern Asia, and Western Europe, with Central & Southern Asia showing the highest growth potential.

Dario Talmesio, research director at Omdia said, “telecom operators are entering a new phase of strategic investment. With 6G on the horizon and AI infrastructure demands accelerating, the connectivity business is shifting from volume-based pricing to value-driven connectivity.”

Dario Talmesio, research director at Omdia said, “telecom operators are entering a new phase of strategic investment. With 6G on the horizon and AI infrastructure demands accelerating, the connectivity business is shifting from volume-based pricing to value-driven connectivity.”

Omdia’s forecast is based on a comprehensive model incorporating historical data from 67 countries, local market dynamics, regulatory trends, and technology migration patterns.

…………………………………………………………………………………………………………………………………………………

Separately, Dell’Oro Group sees 6G capex ramping around 2030, although it warns that the RAN market remains flat, “raising key questions for the industry’s future.” Cumulative 6G RAN investments over the 2029-2034 period are projected to account for 55% to 60% of the total RAN capex over the same forecast period.

“Our long-term position and characterization of this market have not changed,” said Stefan Pongratz, Vice President of RAN and Telecom Capex research at Dell’Oro Group. “The RAN network plays a pivotal role in the broader telecom market. There are opportunities to expand the RAN beyond the traditional MBB (mobile broadband) use cases. At the same time, there are serious near-term risks tilted to the downside, particularly when considering the slowdown in data traffic,” continued Pongratz.

Additional highlights from Dell’Oro’s October 2025 6G Advanced Research Report:

- The baseline scenario is for the broader RAN market to stay flat over the next 10 years. This is built on the assumption that the mobile network will run into utilization challenges by the end of the decade, spurring a 6G capex ramp dominated by Massive MIMO systems in the Sub-7GHz/cm Wave spectrum, utilizing the existing macro grid as much as possible.

- The report also outlines more optimistic and pessimistic growth scenarios, depending largely on the mobile data traffic growth trajectory and the impact beyond MBB, including private wireless and FWA (fixed wireless access).

- Cumulative 6G RAN investments over the 2029-2034 period are projected to account for 55 to 60 percent of the total RAN capex over the same forecast period.

Dell’Oro Group’s 6G Advanced Research Report offers an overview of the RAN market by technology, with tables covering manufacturers’ revenue for total RAN over the next 10 years. 6G RAN is analyzed by spectrum (Sub-7 GHz, cmWave, mmWave), by Massive MIMO, and by region (North America, Europe, Middle East and Africa, China, Asia Pacific Excl. China, and CALA). To purchase this report, please contact by email at [email protected].

References:

https://www.lightreading.com/6g/6g-momentum-is-building

6G Capex Ramp to Start Around 2030, According to Dell’Oro Group

https://www.lightreading.com/6g/6g-course-correction-vendors-hear-mno-pleas

https://www.lightreading.com/6g/what-at-t-really-wants-from-6g