Year: 2023

Huawei’s comeback: 2023 revenue approaches $100B with smart devices gaining ground

Huawei expects to report revenue exceeding 700 billion yuan ($98.5 billion) for 2023, according to comments from rotating deputy chairman Ken Hu in an internal new year message seen by Reuters.

Mr. Hu Houkun (Ken Hu), Huawei’s deputy chairman Photo Credit: Huawei

That optimistic forecast offers further evidence that Huawei is rebounding after U.S. sanctions starting in 2019 crippled some of its business lines by restricting access to critical global technologies such as advanced chips.

“Thanks to our partners across the value chain for standing with us through thick and thin. And I’d also like to thank every member of the Huawei team for embracing the struggle – for never giving up,” Hu said.

“After years of hard work, we’ve managed to weather the storm. And now we’re pretty much back on track.”

“In 2023, we expect to wrap up the year with over 700 billion yuan [US$98.9 billion] in revenue,” he added. That would be a 9% increase on sales from 2022, when the comparable rate of global telecom revenue growth was less than 1%.

Indeed, 2023 has been a very difficult year for telecom network equipment makers such as Ericsson and Nokia. Ericsson’s revenues for the first nine months fell 7% on a constant-currency basis. Nokia’s were down 3%.

…………………………………………………………………………………………………….

What sectors might be responsible for the 9% sales growth Huawei expects this year? From the first paragraph of Ken Hu’s commentary.

“Our ICT infrastructure business has remained solid, and results from our device business surpassed expectations. Both our digital power and cloud businesses are growing steadily, and our intelligent automotive solutions have become significantly more competitive.”

Huawei’s improvement might be due to the upbeat performance of its devices business which includes smartphones and smartwatches. In 2020, the company’s consumer unit accounted for about 54% of all Huawei’s revenues, but its sales halved the following year. It was badly hurt by sanctions because smartphones have a greater need than networks do for advanced chips. Huawei was also cut off from Google software that runs on other Android smartphones. Its response to all this included the sale of Honor, a big smartphone subsidiary.

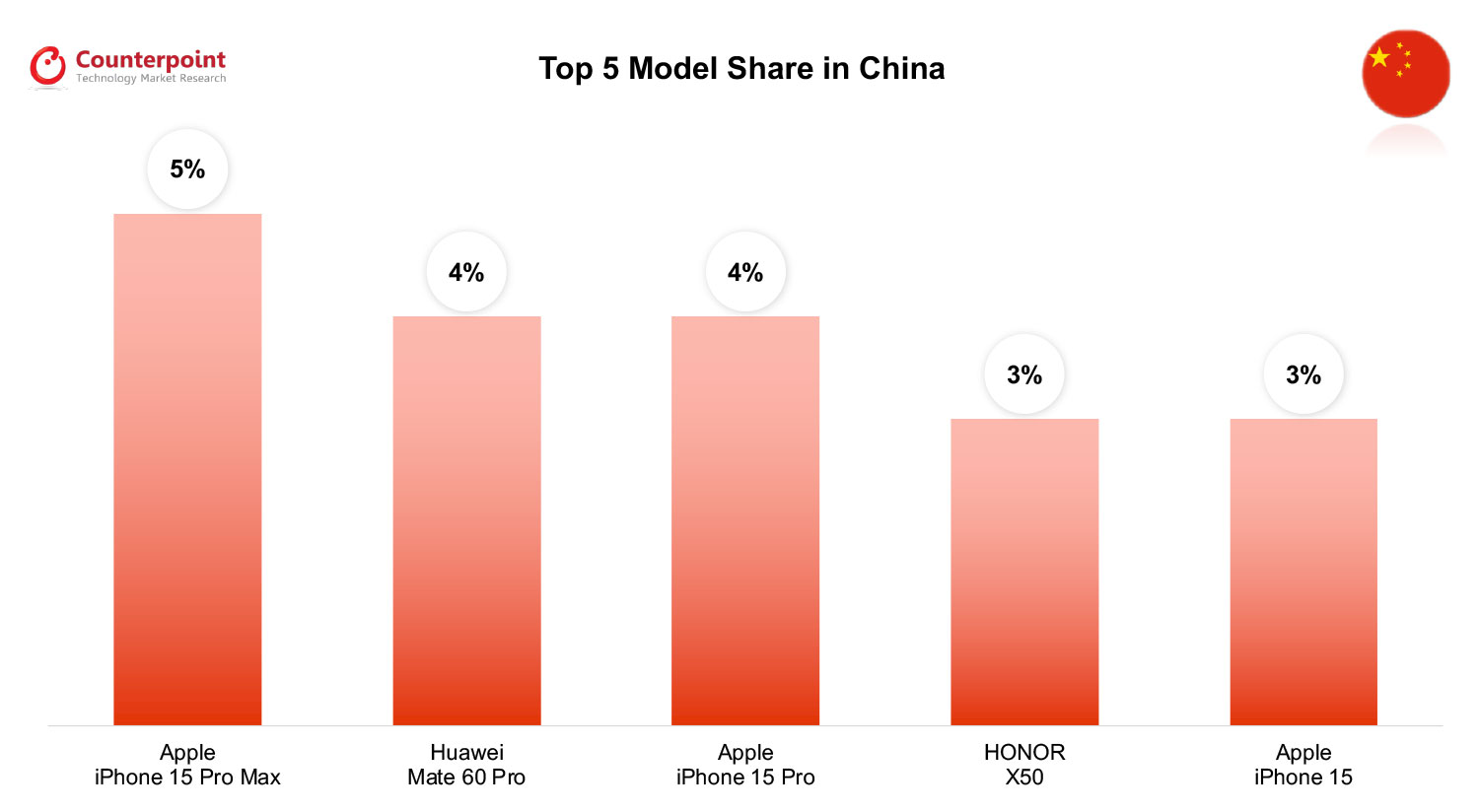

This past August, Huawei launched its Mate 60 series of smartphones, which are believed to be powered by a domestically developed chipset. The release was widely viewed as marking Huawei’s comeback into the high-end smartphone market after years of struggling under U.S. sanctions.

Huawei’s smartphone shipments surged 83% in October year-on-year, helping the overall Chinese smartphone market to grow 11% over the same period, according to Counterpoint Research which wrote:

Huawei’s success and climb in the rankings has been helped by the recent launch of its Mate 60 series 5G phones and popularity of its older P-series 4G devices. “The company is posting some very good growth numbers, but obviously there’s base effects happening,” notes China analyst Archie Zhang. “We expect it will grow by more than half this year, but that still doesn’t bring them close to pre-COVID levels. But it’s signalling a promising 2024.”

Huawei’s smartwatch business is doing very well. Counterpoint’s Woojin Son wrote:

“There is significant value in examining the growth drivers of the global smartwatch market in Q3 2023. Amid a global economic slowdown, most consumer device markets like smartphones are still experiencing stagnation compared to a year ago. In contrast, the smartwatch market has recorded YoY growth for two consecutive quarters in both premium and budget segments. Notably, High-level Operating System (HLOS)* smartwatches, typically featuring higher specification and price, have grown largely driven by Huawei in Q3 2023 as the company posted its highest quarterly performance ever. Most of this surge occurred in the Chinese domestic market, coupled with the launch of new Huawei 5G smartphones.”

……………………………………………………………………………………………………………………..

Looking ahead to 2024, Huawei said in the letter the device business would be one of the major business lines it would focus on for expansion. “Our device business needs to double down on its commitment to developing best-in-class products and building a high-end brand with a human touch,” the letter said.

Missing from Hu’s remarks was any reference to Huawei’s profits, which plummeted 69% last year, to just RMB35.6 billion ($1 billion).

Huawei watchers will probably have to wait until the publication of its 2023 annual report for an update. For sure, the company is cutting costs. “We will continue to streamline HQ, simplify management, and ensure consistent policy, while making adjustments where necessary,” said Huawei’s chairman.

Yet the company will likely continue to ramp up R&D spending. RMB161.5 billion ($22.8 billion) was spent on R&D in 2022, about a quarter of total revenues and a 13% year-over-year increase. Expect a similar increase for 2023 and 2024.

References:

Singles Day Growth Boosts Odds of China Market Smartphone Recovery in Q4 2023

Global Smartwatch Market Rebounds; Huawei and Fire-Boltt Hit New Peaks

Starlink Direct to Cell service (via Entel) is coming to Chile and Peru be end of 2024

Chilean network operator Entel and SpaceX, the company that owns satellite internet provider Starlink, made a commercial agreement to provide satellite-to-mobile services. The agreement will improve broadband coverage for Entel’s LTE customers. It will allow millions of cell phones in Chile and Peru to access satellite coverage starting at the end of 2024.

The first Starlink satellites with Direct to Cell capacity will be launched, providing basic satellite connectivity by the end of 2024. Starlink is a pioneer in providing fixed broadband services through low-orbit satellite networks, which helped it to gain an advantage in the development of direct-to-cell technology.

Starlink satellites with Direct to Cell capabilities enable access to texting, calling, and browsing anywhere on land, lakes, or coastal waters. Direct to Cell will also connect IoT devices which have LTE cellular access.

“One of the great advantages of this proposal is that it will work using the same 4G VoLTE phones that exist in the market today. It does not require any special equipment or special software,” Entel network manager Luis Uribe told BNamericas. “This is an important advantage over traditional satellite solutions. It is a technology that is still evolving, it is being developed. We are going to explore [use cases] as [the technology] advances,” he added.

Although Entel’s mobile networks cover 98% of the populations of Chile and Peru, the Starlink deal will allow it to provide services in maritime territory or in areas that suffered natural disasters.

“It is a technology that has enormous potential as a result of its ability to cover areas that traditional networks cannot achieve,” Uribe said.

A so-called line of sight between device and satellite is required for direct-to-cell to work, meaning the technology might not work indoors or in dense forests. If available, terrestrial coverage will be prioritized.

While other companies are developing similar solutions, they are not as advanced as Starlink. “We see other solutions that also look interesting. To the extent that these do not involve special software or devices, they could be an option,” said Uribe.

Entel is also focused on 5G deployment, achieving a first-stage goal of connecting 270 localities from Arica in the north to Puerto Williams in the south in August.

The company is investing US$350mn in the entire deployment program. In October, Entel enabled NB-IoT at over 6,500 sites to boost connectivity for Internet of Things devices.

“From the point of view of the company’s internal processes, we are incorporating artificial intelligence and generative artificial intelligence tools,” said Uribe. The technologies are being used for automation processes and network optimization, among others.

References:

https://www.bnamericas.com/en/features/spotlight-the-entel-starlink-mobile-coverage-agreement

Starlink’s Direct to Cell service for existing LTE phones “wherever you can see the sky”

SpaceX has majority of all satellites in orbit; Starlink achieves cash-flow breakeven

Bloomberg on Quantum Computing: appeal, who’s building them, how does it work?

1. What’s the appeal of quantum computers?

They can do things that classical computers can’t. Google revealed in April that one of its quantum computers had solved a problem in seconds that would have taken the world’s most powerful supercomputer 47 years. Experimental quantum computers are typically given tasks that a conventional computer would take too long to do, such as simulating the interaction of complex molecules for drug discovery. Their greatest potential is for modeling complex systems involving large numbers of moving parts whose behavior changes as they interact — such as predicting the behavior of financial markets, optimizing supply chains and operating the large language models used in generative artificial intelligence. They’re not expected to be much use in the laborious but simpler work fulfilled by most of today’s computers — processing a more limited number of isolated inputs sequentially on a mass scale.

2. Who’s building them?

Canadian company D-Wave Systems Inc. became the first to sell quantum computers to solve optimization problems in 2011. International Business Machines Corp., Alphabet Inc.’s Google, Amazon Web Services and numerous startups have all created working quantum computers. More recently, companies such as Microsoft Corp. have made progress toward building scalable and practical quantum supercomputers. Intel Corp. started shipping a silicon quantum chip to researchers with transistors known as qubits (quantum bits) that are as much as 1 million times smaller than other types. Microsoft and other companies, including startup Universal Quantum, expect to build a quantum supercomputer within the next ten years. China is building a $10 billion National Laboratory for Quantum Information Sciences as part of a big push in the field.

3. How do quantum computers work?

They use tiny circuits to perform calculations, as do traditional computers. But they make these calculations in parallel, rather than sequentially, which is what makes them so fast. Regular computers process information in units called bits, which can represent one of two possible states — 0 or 1 — that correspond to whether a portion of the computer chip called a logic gate is open or closed. Before a

traditional computer moves on to process the next piece of information, it must have assigned the previous piece a value. By contrast, thanks to the probabilistic aspect of quantum mechanics, the qubits in quantum computers don’t have to be assigned a value until the computer has finished the whole calculation. This is known as “superposition.” So whereas three bits in a conventional computer would only be able to represent one of eight possibilities – 000, 001, 010, 011, 100, 101, 110 and 111 – a quantum computer of three qubits can process all of them at the same time. A quantum computer with 4 qubits can in theory handle 16 times as much information as an equally-sized conventional computer and will keep doubling in power with every qubit that’s added. That’s why a quantum computer can process exponentially more information than a classic computer.

Why Quantum Will Be Quicker

Problems like breaking encryption or mapping a molecule’s structure can require sorting through millions of possibilities.

4. How does it return a result?

In designing a standard computer, engineers spend a lot of time trying to ensure that the status of each bit is independent from those of all the other bits. But qubits are entangled, meaning the properties of one depend on the properties of the qubits around it. This is an advantage, as information can be transferred quicker between qubits as they work together to arrive at a solution. As a quantum algorithm runs, contradictory (and therefore incorrect) results from the qubits cancel each other out, whilst compatible (and therefore likely) results are amplified. This phenomenon, called coherence, allows the computer to spit out the answer it deems most likely to be correct.

5. How do you make a qubit?

In theory, anything exhibiting quantum mechanical properties that can be controlled could be used to make qubits. IBM, D-Wave and Google use tiny loops of superconducting wire. Others use semiconductors and some use a combination of both. Some scientists have created qubits by manipulating trapped ions, pulses of photons or the spin of electrons. Many of these approaches require very specialized conditions, such as temperatures colder than those found in deep space.

6. How many qubits are needed?

Lots. Although qubits can process exponentially more information than classical bits, their inherently uncertain nature makes them heavily prone to errors. Errors creep into qubits’ calculations when they fall out of coherence with each other. Outside the lab, scientists have only been able to keep qubits in coherence for fractions of a second — in many cases, too short a period of time to run an entire algorithm. Theorists are working to develop algorithms that can correct some of these errors. But an inevitable part of the fix is adding more qubits. Scientists estimate that a computer needs millions – if not billions – of qubits to reliably run programs suited for commercial use. Sticking enough of them together is the main challenge. As a computer gets larger in size, it emits more heat, which makes it more likely that qubits will fall out of coherence. The current record for qubits connected is 1,180, achieved by California startup Atom Computing in October 2023 — more than double the previous record of 433, set by IBM in November 2022.

7. When do I get my quantum computer?

It depends on what you want to use it for. Academics are already solving problems on 100-strong qubit machines through the cloud-based IBM Quantum Platform, which the general public is able to try out (if you know how to develop quantum code). Scientists aim to deliver a so-called “universal” quantum computer suitable for commercial applications within the next decade. One caveat of the enormous problem-solving power of quantum computers is their potential for cracking classical encryption systems. Perhaps the best indication of just how close we are to quantum computing is that governments are signing directives and businesses are pouring millions of dollars into securing legacy computing systems against being cracked by quantum machines.

References:

SK Telecom and Thales Trial Post-quantum Cryptography to Enhance Users’ Protection on 5G SA Network

SKT Develops Technology for Integration of Heterogeneous Quantum Cryptography Communication Networks

Research on quantum communications using a chain of synchronously moving satellites without repeaters

China Mobile verifies optimized 5G algorithm based on universal quantum computer

UAE’s “etisalat by e&” announces first software defined quantum satellite network

Can Quantum Technologies Crack RSA Encryption as China Researchers Claim?

Quantum Technologies Update: U.S. vs China now and in the future

ASPI’s Critical Technology Tracker finds China ahead in 37 of 44 technologies evaluated

WiFi 7 and the controversy over 6 GHz unlicensed vs licensed spectrum

Introduction:

Even though the IEEE 802.11be standard is yet to be released officially, there are currently Wi-Fi 7 routers on the market from many major vendors. Wi-Fi 7 provides significantly faster speeds then WiFi 6 (IEEE 802.11ax), with ultra-low latencies and a better communication channel. Thereby, more devices can be connected efficiently.

Wi-Fi 7 routers are capable of delivering wireless data transfer speeds of up to 46 Gbps, which is five times greater than that of Wi-Fi 6E routers. Wi-Fi 7 routers can also operate on multiple bands: carrier frequency operation is between 1 and 7.250 GHz while ensuring backward compatibility and coexistence with legacy IEEE Std 802.11 compliant devices operating in the 2.4 GHz, 5 GHz, and 6 GHz bands. Latency is also lower with a Wi-Fi 7 router and channel connections are more efficient.

Some Wi-Fi 7 routers include the NETGEAR Nighthawk Tri-Band WiFi 7 Router BE19000 Wireless Speed, the TP-Link BE9300 Tri-Band Wi-Fi 7 Router ARCHER BE550, and the ASUS BE96U Tri-Band WiFi 7 Router RT-BE96U.

6 GHz Band Controversy:

As of September 2023, the following countries have adopted the policy of making the entire 6 GHz band available for unlicensed use: U.S., South Korea, Brazil, Saudi Arabia, Costa Rica, Peru. Canada has also made 1200 MHz of 6 GHz spectrum available for unlicensed services. The 6 GHz band is the largest allocation of unlicensed spectrum in the US and South Korea.

Some other countries that have enabled Wi-Fi in the 6 GHz band include: Andorra, Argentina, Australia, Austria, Bahrain, Belgium, CEPT.

China has chosen a licensed approach for the 6 GHz band, using the entire 1,200 MHz for 5G and future 6G services.

The Telecom Regulatory Authority of India (Trai) suggests that the lower end of the 6 GHz spectrum band can be allocated for unlicensed use, such as WiFi, while the upper end can be licensed for telecom use. Netgear said that the India DoT (Department of Telecommunications) is considering to delicense the lower band 6 GHz spectrum.

However, WRC 23 agreed to open up the 6 GHz band for future high-speed mobile communications (instead of for unlicensed WiFi). The 6 GHz band (6.425-7.125 GHz) – was identified for mobile in every ITU Region – EMEA, the Americas and the Asia Pacific. Countries representing more than 60% of the world’s population asked to be included in the identification of this band for licensed mobile at WRC-23. The 6 GHz spectrum is now the harmonized home for the expansion of mobile capacity for 5G-Advanced and beyond.

References:

https://standards.ieee.org/ieee/802.11be/7516/

https://spectrum.ieee.org/what-is-wifi-7

WRC-23 concludes with decisions on low-band/mid-band spectrum and 6G (?)

MediaTek Introduces Global Ecosystem of Wi-Fi 7 Products at CES 2023

Highlights of Qualcomm 5G Fixed Wireless Access Platform Gen 3

Qualcomm FastConnect 7800 combining WiFi 7 and Bluetooth in single chip

Intel and Broadcom complete first Wi-Fi 7 cross-vendor demonstration with speeds over 5 Gbps

China’s telecom industry business revenue at $218B or +6.9% YoY

China’s Ministry of Industry and Information Technology (MIIT) said that in the first eleven months of 2023, the telecommunication industry’s collective business revenue soared to 1.55 trillion yuan, approximately 218 billion U.S. dollars, marking a 6.9% year-on-year increase.

Emerging sectors such as big data, cloud computing, and the Internet of Things (IoT) have shown significant growth. China’s three state owned network providers, China Telecom, China Mobile, and China Unicom have leveraged these technologies to catalyze a 20.1 percent surge in revenue from these areas, amounting to 332.6 billion yuan.

Cloud computing and big data have experienced explosive growth. Revenue from cloud computing surging by 39.7 percent and big data by 43.3 percent compared to the previous year. These figures underscore the central role of data-driven technologies in powering China’s telecom industry forward.

Broadband internet services continue to be a strong revenue stream for the three telecom giants, generating 240.4 billion yuan from January to November, which is an 8.5 percent increase year on year. This growth reflects the increasing demand for high-speed internet across China, as the country continues to embrace digital transformation in all sectors.

In conclusion, China’s telecommunication industry’s growth narrative in 2023 is not just a story of numbers but a chronicle of technological evolution and its integration into the fabric of society. With emerging sectors leading the charge, the industry’s upward trajectory seems poised to continue, as these technologies become increasingly embedded in the everyday lives of businesses and consumers alike.

……………………………………………………………………………………………………………

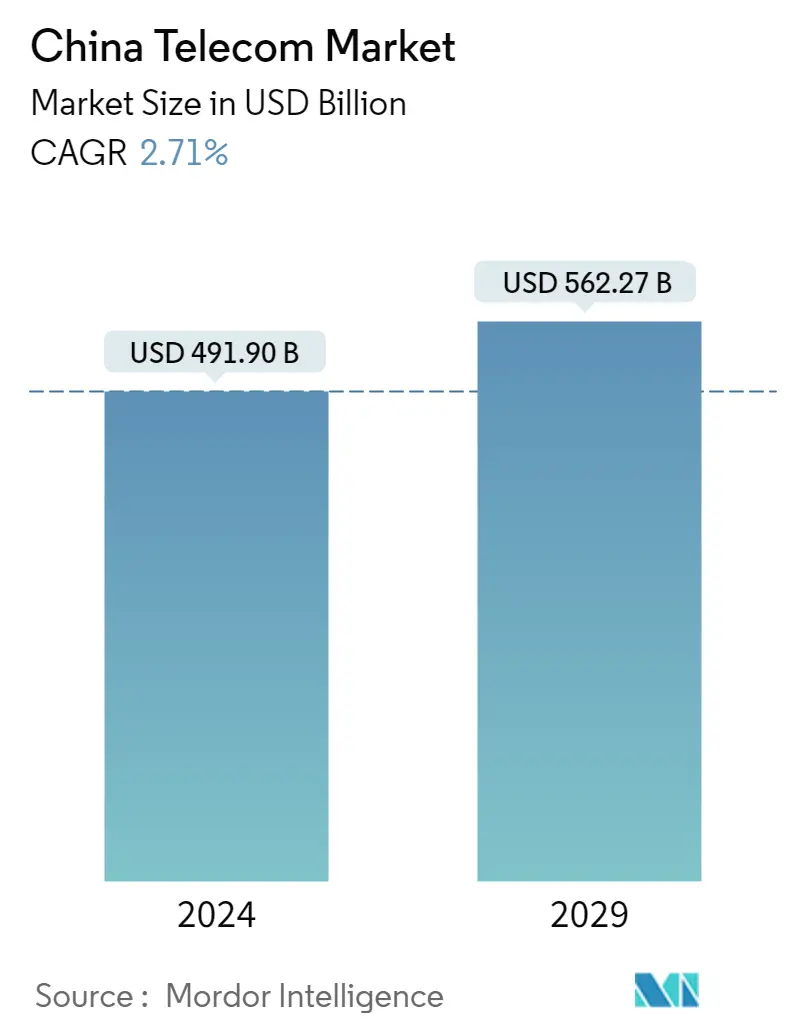

Separately, Mordor Intelligence forecasts the China Telecom Market size is expected to grow from USD 478.92 billion in 2023 to USD 547.43 billion by 2028, at a CAGR of 2.71% during the forecast period (2023-2028).

References:

https://english.news.cn/20231223/36996f5176e24d48a5677ddc160c99a5/c.html

China’s Telecom Sector Soars with Big Data and Cloud Computing Growth

https://www.mordorintelligence.com/industry-reports/china-telecom-market

Strand Consult’s 2024 Telecom Predictions

by John Strand, Founder and CEO of Strand Consult

Introduction:

2024 is poised to be an important year as more than half of the world’s population is poised to vote. Elections create clarity and regime change. They are pivotal because they signal national policy direction for industry and society, not the least being mobile telecom stakeholders. Following are Strand Consult’s hard thoughts on the year ahead. For some holiday mirth and an insightful summary of the challenges facing the telecom industry in 2024, listen to the Telecoms.com podcast featuring telecom legend Denis O’Brien from Digicel in conversation with editors Scott Bicheno (Telecoms.com) and Iain Morris (Light Reading.com).

Geopolitics

2024 is an election year, and more than half of the world’s population are scheduled to vote in 2024. Four critical elections will be held in the Free World: Taiwan on January 23; General elections in India in April-May; the European Parliament on 6 to 9 June; and the US Presidential election on November 5. Separately, a press release notes that a Russian presidential election will be held on 15 to 17 March, and Vladimir Putin will get a fifth term. China canceled free elections again in 2024.

There is limited policymaking in countries during election years, so the policy action is likely to be in the countries in off-election years. However, elections may slow needed action to address conflicts in Ukraine and the Middle East.

Moreover, China continues to partner with dictators, and grow more aggressive. General Secretary Xi Jinping faces limited opposition and critical press. However, many see his reign as a disaster including the mishandling of Covid, the souring economy, and the lost goodwill with other nations, particularly as XI cozies up to Russia’s Putin, North Korea’s Kim Jong Un, and Iran’s Hassan Rouhani.

There still remain mobile telecom operators in the free world which espouse democratic values and yet partner with China’s Huawei and ZTE. The operators reject the claim of security risk and dismiss or downplay the demonstrated control Xi and the party exact on China’s enterprises. The policy secure networks in US and EU has nothing to do with trade, but rather reflects the reality that China has changed fundamentally in the last decade.

2024 will also show the results of the implementation of the EU 5G security toolbox with increased attention on trusted versus non-trusted operators, not just vendors. Nations outside the EU will be inspired by the diplomatic EU approach.

Misguided Regulation

When Strand Consult launched almost 30 years ago, “regulation” had little to no impact on the industry. There were no internet activists trolling telecom regulatory authorities. Today, however, regulation can have a huge impact for both good and ill.

A decade ago Strand Consult published the report The EU’s Broadband and Telecom policy is not working. Europe is falling further behind the US documenting how US operators invested twice as much in infrastructure as their European counterparts over a long period. That trend is ongoing. The US still invests at twice the rate of the EU; the EU is further behind, and the EU gap to close the digital divide has widened from €150 billion to €274 billion.

2024 will be another year in which the EU will publish reports showing that Europe is behind. And yet, European policymakers continue to reject solutions like in-country consolidation which could help firms improve their business case for growth and investment and could ultimately improve the dismal picture for the EU.

Meanwhile the United States, India, and many African nations have completed successful consolidations. The operating results of most telecom firms in these countries are better than those in Europe. EU policymakers accept the status quo of ever-worsening returns and a growing investment deficit.

When it comes to creating better conditions for infrastructure deployment, Europe is also far behind other parts of the world. The only exception in the EU is Denmark, where Strand Consult’s research which started 10 years ago, has made it easier and significantly cheaper to roll out infrastructure in Denmark.

The EU Parliament’s Gigabit Infrastructure Act introduced this year promises faster rollout of gigabit-capable connectivity. It is a solution that helps fixed infrastructure providers. The question remains as to how many years it takes before implementation at the local level. Strand Consult does not expect to see this the effect of this Act in 2024, or even for some years, given rising interest rates. Simply put, the EU bill is too little and about 15 years too late.

The EU’s Digital Markets Act (DMA) proposes to regulate online content and social media platforms. The big question is how to implement it in practice. It will be interesting to see whether Big Tech will censor EU policymakers. There is a similar hubris with the EU’s Artificial Intelligence Act (AI Act) and how it promises “transparency” of algorithms. It’s hard to believe that any European official has the skills to make such an assessment. As AI business models have yet to be proven, the regulation seems premature. No bureaucrat can say whether Google, Microsoft, AWS, ChatGPT, or some other entity has the better AI solution.

Chips, chips, and Chinese chips

All chips matter – whether NVIDIA’s state of the art chips for AI or workhorse memory chips. This has only been heightened by the supply chain shortages driven by Covid-19 and security challenges. Russia, Iran, North Korea and China want advanced chips used for military purposes. Free world nations have imposed restrictions on chips for certain military users; this could only work because firms in the US, Netherlands, Korea, Japan, and Taiwan have the relevant IP.

China is heavily dependent on this advanced chip technology, and indeed firms of all kinds try to work around these rules. Some companies even break them with the expectation that they won’t be caught or fined (See Applied Materials). China has tried for 40 years to get a leadership position in advanced chips with limited success. However, though size and scale, China can impact global chip supply with currency manipulation and by flooding the market with low-end products.

In 2024 China will bombard the media with propaganda saying that if they can’t get an advanced supply of chips, then they will make it themselves. This should be taken with a grain of salt. Strand Consult describes Huawei’s challenges given chip restrictions and its various workarounds and creative messaging. Huawei is diversifying its business and doing an IBM-style transformation, going from a hardware company to a software/service one. It could make Huawei less dependent on its own hardware.

Chip policy will stay salient in 2024.

OpenRAN vs. 3GPP 5G RAN

Strand Consult’s predictions about OpenRAN have been spot on, revealing the stories to be the greater part of hype rather than market value. OpenRAN revenue as a share of the mobile infrastructure market is miniscule, but OpenRAN takes an outsized share of press and policymaker attention owing to Washington policy spin and Hollywood storytelling.

The party version of OpenRAN is to break incumbent vendor lock-in, reduce costs, promote innovation, and simplify network deployment and upgrade. This approach has gained attention and support from some telecommunications industry players, standardization bodies, and regulatory authorities to enhance competition and accelerate the development of 5G and beyond. However compelling a storyline, the reality is that OpenRAN does not provide a meaningful technical and commercial alternative to existing RAN players Huawei, Ericsson, Nokia, ZTE and Samsung.

In other words, you can’t put a hodge podge of virtual elements in a 1:1 matchup for existing RAN solutions. There are a few one-off OpenRAN solutions, but these are sideshows. There are proprietary RAN solutions that can connect to different interfaces. OpenRAN has the same function as a USB cable when connecting an iPhone with a Windows PC. With the new OpenRAN specifications launched in Osaka this summer, it is equivalent to going from using a USB-A to a lightning cable to using a USB-C to a USB-C cable.

Of the 200 3GPP/5G networks deployed globally, just three could be classified as OpenRAN. Of the install base of 5G RAN base stations, OpenRAN has about 1 percent market share of the install 5G base.

2024 could see the O-RAN Alliance folded into 3GPP. Or it could be pushed to 2025. 3GPP already works with many open interfaces, and this will drive the O-RAN Alliance to dismantle itself. The key stumbling block to OpenRAN implementation is operators themselves; they don’t want more complexity in networks. There is still value to the one-stop shop, as AT&T just demonstrated with its 5-year, $14 billion deal with Ericsson.

Business models

Over the last 25 years, the mobile telecom industry has moved from selling volume-based traffic to flat rate, all you can eat models. This has been driven for a variety of reasons. However, we predict 2024 will mark a shift with more flexibility at the high and low end of the market, read high value premium service for gamers and packages with bespoke services for the budget market.

Something’s gotta give. Internet adoption has stalled with 2.6 billion people globally offline for lack of access and affordability. Interest rates are rising, and average revenue per user (ARPU) is falling. Alternatively, we could see some nations allow needed in-market consolidation.

Operators have tried and failed to launch new platforms (think Orange World, Vodafone Live, GSMA’s OneAPI). In the year 2000, there was a 3G dream to double ARPU, from €36 to €72 Euro. Today ARPU is at or below €14 in many European countries. OTT solutions like Skype and WhatApp have proven more successful. Hence Strand Consult is not optimistic for GSMA’s Open Gateway in 2024.

For a deep dive on the state the mobile operators today, read Strand Consult’s latest research note Has the iPhone improved the mobile operators’ business case? which revisits Strand Consult’s groundbreaking report.

Operators have four key challenges:

- Regulation which prevents business model innovation and competition with OTTs

- Competition with other operators

- Customer budget constraint

- Operators’ lack of creativity, innovation, product development, strategy etc.

Connectivity may be the most compelling service on this earth. Just turn off the internet to a 9-year-old boy’s iPhone. The problem is that telecommunications providers have not succeeded to monetize sufficiently the value they provide. Ironically connectivity is increasingly valuable, yet its unit price continues to fall, and consumers expect greater value at a ever falling price point.

Broadband cost recovery and fair share

2024 will likely see the reboot of the Free Ride Prevention Act in South Korea, as firms like Google’s Alphabet which devour more than a quarter of the nation’s bandwidth, refuse to come to the table to negotiate. There is also likely to be progress in the USA, India, and Brazil where proceedings are underway, among other countries. Given recent court cases proving that Big Tech pays for placement, the arguments against fair share have been demolished. Moreover, the court cases have documented systematic Big Tech strong-arming, if not abuse of market power. Expect Big Tech to be more open to dealmaking in lieu of being regulated. Check out Strand Consult’s Global Research Project for Broadband Cost Recovery, Affordability, and Fair Share for more information.

Satellite Industry: Musk vs. Bezos

2024 will see more focus on the use of the low earth orbit (LEO) satellites. The fight between Elon Musk (Starlink) and Jeff Bezos (Kuiper) overshadows the big picture. Musk’s Starlink is lightyear’s ahead of Bezos’ Kuiper and already has 5,420 satellites orbiting the Earth; Kuiper has just two satellites. Bezos and Musk share the same dream; the difference is that Musk has already delivered. Bezos has opened his first satellite burger bar. Musk owns the interstellar McDonald’s.

Starlink has first-mover advantage and some lock-in tech dependence. It has access to cheap lifting capacity to get its satellites into space and to operate ground stations. Even with the FCC’s partisan cancelling of $886 million in subsidies (which appears to be a punishment for Musk buying Twitter and not towing the progressive party line), the company is still likely to succeed as it thrives on overcoming adversity and challenge. Satellite is here to stay as a bona fide broadband technology, and 2024 will only make that clearer.

Wrap up

As some 4 billion people go to the polls in 2024, some important policy may be put on hold, and broadband shortfalls will remain. At the same time, voters have a valuable opportunity to signal a change in leadership and direction. However, many governments will promote policy and legislation to improve access to 5G and broadband.

Rising interest rates will have a negative impact on investment. Fiber will be hit harder than mobile, and emerging markets will have a tougher time than the developed world.

While we don’t expect a business model revolution, we expect many operators to increase prices for connectivity. And indeed, many nations will further their broadband cost recovery and fair share policy solutions to improve access and affordability.

We also predict management cleanup. CEOs who have not delivered will be let go. Consider Vodafone which was Europe’s most capitalized company in year 2000 with well over $300 billion; it has shrunk to $24 billion today. Its main success during this period was to divest Verizon in USA. Its multi billion investment in India was a dismal failure and was written off the balance sheet.

Despite the security and reputational risk, Vodafone continues to work closely with Huawei and uses this equipment across many countries. The company appointed a new CEO in early 2023. Strand Consult observed that Vodafone needs a “cleaner” like Harvey Keitel The Wolf in “Pulp Fiction.” Or they need Meryl Streep from the The Iron Lady, not the Meryl Streep in Mama Mia! Margherita Della Valle’s performance at Vodafone is associated with a falling share price.

Strand Consult does not expect to see results for mobile telecom shareholders driven by GSMA or ENTO. However, these organizations will likely continue to pay their top management high salaries. GSMA CEO Mats Granryd gets $2.4 million in annual salary to hold trade shows featuring increasingly Huawei and Meta while serving on the board of Swedish National TV and chairing Vattenfall AB and Coore AB.

Elections and security of national infrastructure will take center stage in 2024. China will wage a proxy war against those countries which don’t adopt its equipment and service platforms. With growing interest rates and inflation, there is little to make telecom shareholders happy in the coming year.

In 2023 Strand Consult published many research notes and reports and featured cool people on its guest blog. Strand Consult’s analysis was quoted in some 1000 news stories globally. Our work took us to all the continents except Antarctica. Our readership continues to grow. For the last 23 years, Strand Consult has made predictions for the coming year. Our archive shows that we get it right.

Thank you for your support and readership.

Feel free to reach me at [email protected]

References:

StrandConsult Analysis: European Commission second 5G Cybersecurity Toolbox report

StrandConsult: 2022 Year in Review & 2023 Outlook for Telecom Industry

Strand Consult: Open RAN hype vs reality leaves many questions unanswered

O-RAN Alliance tries to allay concerns; Strand Consult disagrees!

Strand Consult: What NTIA won’t tell the FCC about Open RAN

Ookla: T-Mobile and Verizon lead in U.S. 5G FWA

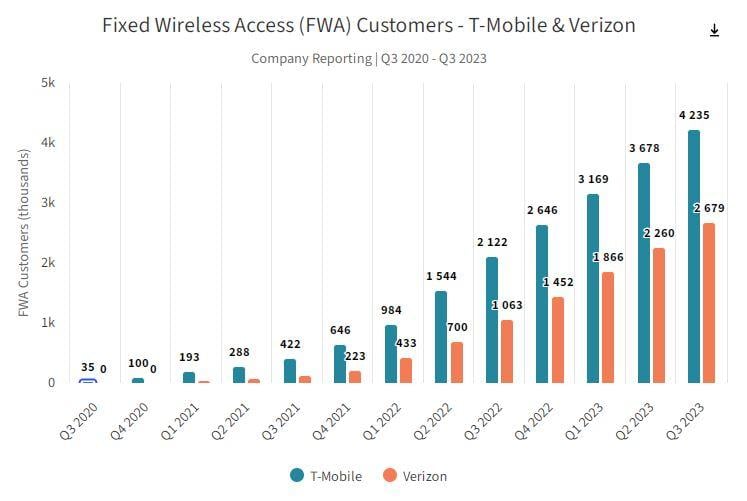

The U.S. is at the forefront of fixed wireless access (FWA) deployments, with many major wireless carriers, including T-Mobile, Verizon, AT&T and UScellular targeting expansion.

T-Mobile has built up a lead in terms of 5G fixed-wireless market share, with Verizon following closely, and AT&T recently launching a new FWA service – AT&T Internet Air. We examined Ookla Speedtest data to understand how FWA performance is evolving in the U.S., and how it is impacting churn in the market.

Key Points:

- T-Mobile & Verizon 5G FWA performance holding up well nationally. Despite strong customer growth, both T-Mobile and Verizon have maintained performance levels over the past year according to Speedtest data. Both ISPs recorded similar median download speeds in Q3 2023, although T-Mobile maintains an edge on median upload performance. Despite this, there are significant differences in performance at a State-level, and for urban versus rural locations.

- Cable & DSL providers bear the brunt of user churn. The FWA value proposition is clearly resonating most with existing cable and DSL customers, which make up the vast bulk of churners to both T-Mobile’s and Verizon’s FWA services. It’s not one-way traffic however, with T-Mobile’s larger user base in particular showing some attrition to cable providers. In rural locations where options are more limited, FWA services are increasingly going head to head, with over 10% of users joining Verizon’s FWA service coming from T-Mobile.

- Clear signs that download performance could be a key contributor to churn in the market. Our analysis of the customers of major ISPs in the US that have churned to T-Mobile’s FWA service shows that their median download performance before churning was below the median performance of all customers of these ISPs, indicating a performance short-fall that is likely contributing towards churn.

- Further C-band spectrum will serve to strengthen FWA’s case. The release and deployment of additional C-band spectrum for all three national cellular carriers, and AT&T’s new FWA service will drive further performance gains, and further competitive pressure in 2024.

T-Mobile and Verizon FWA scaling strongly and national performance holding up well:

Launched during the COVID-19 pandemic, FWA services from T-Mobile and Verizon have seen strong growth over the past three years. Aided by disruptive pricing strategies, no annual contracts, and ease of installation (self-install), net additions remain strong for both ISPs. T-Mobile’s current FWA plan retails for $50/month, but that falls to $30/month for customers subscribing to its Magenta MAX mobile plan. Verizon prices at a slight premium to T-Mobile, with its FWA service currently retailing for $60/month, but falling to $35/month with select 5G mobile plans. On the back of their success we’ve also recently seen AT&T update its FWA strategy, launching AT&T Internet Air in August 2023, with a similar pricing strategy.

Utilizing the same 5G spectrum that its mobile customer base accesses, both T-Mobile and Verizon have been at pains to point out how they manage the on-boarding of new FWA customers, in order to limit any negative impact on performance for both cellular and FWA customers. The release and rollout of additional C-band spectrum for all three operators will provide extra headroom and the potential for improved 5G FWA performance, while T-Mobile has begun testing 5G Standalone mmWave, and has indicated that this could be utilized for 5G FWA in the future.

Performance on T-Mobile’s and Verizon’s 5G FWA services has held up well to date, although it lags behind median download performance of the major cable and fiber ISPs. The median download speed across the US for all fixed providers combined in Q3 2023 was 207.42 Mbps. T-Mobile has recorded consistent median download speed over the past four quarters, reaching 122.48 Mbps in Q3 2023 based on Speedtest data, but saw its median upload performance erode slightly, down from 19.76 Mbps in Q4 2022, to 17.09 Mbps in Q3 2023. Verizon on the other hand improved its median download performance when compared to Q4 2022, reaching a similar level to T-Mobile, of 121.23 Mbps in Q3 2023. However, its upload performance remained lower than T-Mobile’s, at 11.53 Mbps.

Ookla’s Speedtest data was used to identify the number of churned users since Q2 2022, when FWA services really started to scale and impact the rest of the market. The bulk of churn for both T-Mobile’s and Verizon’s 5G FWA services are coming from cable and DSL providers, confirming what the service providers have said.

The market research firm said that performance on T-Mobile’s and Verizon’s 5G FWA services has held up well to date, although it lags behind median download performance of the major cable and fiber ISPs.

Ookla clocked the median download speed across the U.S. for all fixed providers combined in Q3 2023 at 207.42 Mbps. T-Mobile recorded consistent median download speed over the past four quarters, reaching 122.48 Mbps in Q3 2023 based on Speedtest data, but saw its median upload performance erode slightly, from 19.76 Mbps in Q4 2022 to 17.09 Mbps in Q3 2023.

Meanwhile, Verizon improved its median download performance when compared to Q4 2022, reaching a similar level to T-Mobile, of 121.23 Mbps in Q3 2023. However, its upload performance remained lower than T-Mobile’s, at 11.53 Mbps, Ookla said.

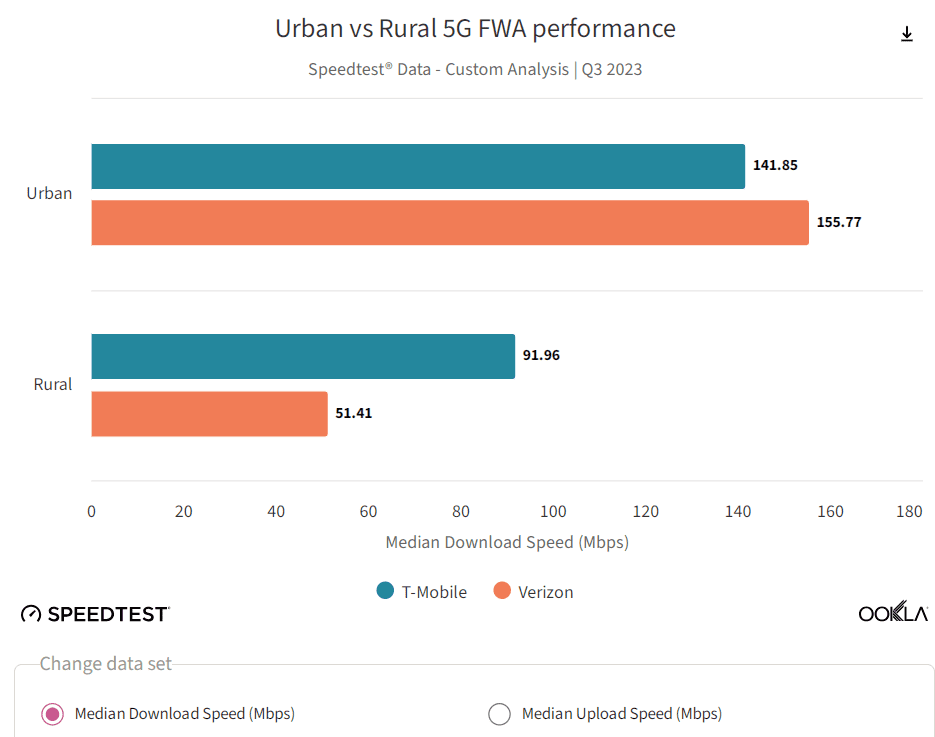

While median performance has remained fairly steady for both operators over the past year, Ookla said it’s a different story when it comes to regional performance and between urban and rural regions.

Rural locations – predictably – fared worse than urban locations for both T-Mobile and Verizon 5G FWA service, given differences in spectrum availability and distance from cell sites, although the difference was starker for Verizon’s FWA service, Ookla said. Verizon’s FWA service recorded a median of 155.77 Mbps in urban locations during Q3 2023, but only 51.41 Mbps in rural locations.

T-Mobile increased rural FWA performance, from 82.20 Mbps in Q4 of 2022 to 91.96 Mbps in Q3 2023. Verizon’s performance in urban locations improved, with the 155.77 Mbps it achieved in Q3 2023 representing a sizable increase on the 125.55 Mbps it recorded in Q4 2022.

All of the big mobile operators, including AT&T with Internet Air, will see improved 5G FWA performance with additional C-band spectrum, and T-Mobile could potentially use millimeter wave on its 5G standalone (SA) network for FWA, Ookla noted.

References:

https://www.ookla.com/articles/fixed-wireless-access-us-q3-2023

https://www.fiercewireless.com/wireless/t-mobile-verizon-5g-fwa-performance-holds-ookla

SK Telecom and Thales Trial Post-quantum Cryptography to Enhance Users’ Protection on 5G SA Network

Korean telco SK Telecom and digital security firm Thales have tested quantum-resistant cryptography based on a 5G standalone (5G SA) network. The trial is focused on encrypting and decrypting identity data on a 5G network to protect user privacy from future quantum threats. It was performed using Thales 5G Post Quantum Cryptography (PQC) SIM cards and a trial 5G standalone network environment from SKT. The test involved cryptographic algorithms designed to resist attacks from quantum computers, as well as ‘classical’ computers.

The end user identity on the 5G SA network is concealed and secured on the device side via the 5G SIM card. The security mechanisms involve cryptographic algorithms designed to resist attacks from future quantum computers, providing a level of security that is considered robust in the post-quantum era.

Photo Credit: rawpixel

The U.S. National Institute of Standards and Technology (NIST) has been leading an initiative to standardize post-quantum cryptographic algorithms, and SKT and Thales have used the Crystals-Kyber one for this successful real condition trial. These post-quantum secure algorithms are being developed to withstand attacks from both classical and quantum computers.

“This collaboration between SKT and Thales highlights our commitment to staying ahead of the curve in terms of cybersecurity and ensuring the safety of our customers’ data. PQC provides enhanced security through the use of cryptographic algorithms that are thought to be secure against quantum computer attacks. Going forward, we will combine PQC SIM with our additional Quantum expertise to achieve end-to-end quantum-safe communications,” said Yu Takki, Vice President and Head of Infra Technology Office of SKT.

“As quantum computers have the potential to break certain existing cryptographic algorithms, there is an emerging need to transition to cryptographic algorithms believed to be secure against quantum attacks. For 5G networks, Thales started to invest on cryptographic algorithms that are quantum-resistant to enhance continued communications security and privacy for users,” said Eva Rudin, SVP Mobile Connectivity & Solutions at Thales.

As quantum computing gets more reliable and presumably starts getting used more widely in the future, this type of security is going to become increasingly important. Nokia recently announced it had completed a proof of concept trial alongside Greek research consortium HellasQCI, demonstrating what it calls quantum-safe connectivity infrastructure.

………………………………………………………………………………………………………………………………………………………………..

Separately, SK Broadband, an internet and paid TV service affiliate of SK Telecom, launched additional personalized internet protocol television (IPTV) services utilizing AI technology to enhance its competitiveness in the country’s paid TV market, the company said Wednesday.

About SK Telecom:

SK Telecom has been leading the growth of the mobile industry since 1984. Now, it is taking customer experience to new heights by extending beyond connectivity. By placing AI at the core of its business, SK Telecom is rapidly transforming into an AI company. It is focusing on driving innovations in areas of telecommunications, media, AI, metaverse, cloud and connected intelligence to deliver greater value for both individuals and enterprises.

For more information, please contact [email protected] or visit SKT’s LinkedIn page www.linkedin.com/company/sk-telecom.

About Thales:

Thales (Euronext Paris: HO) is a global leader in advanced technologies within three domains: Defence & Security, Aeronautics & Space, and Digital Identity & Security. It develops products and solutions that help make the world safer, greener and more inclusive.

References:

https://www.newswire.co.kr/newsRead.php?no=981374

https://www.telecoms.com/5g-6g/sk-telecom-and-thales-trial-quantum-resistant-cryptography-for-5g-sa

https://www.koreatimes.co.kr/www/tech/2023/12/133_365470.html

SKT Develops Technology for Integration of Heterogeneous Quantum Cryptography Communication Networks

SK Telecom and Deutsche Telekom to Jointly Develop Telco-specific Large Language Models (LLMs)

Daryl Schoolar: 5G mmWave still in the doldrums!

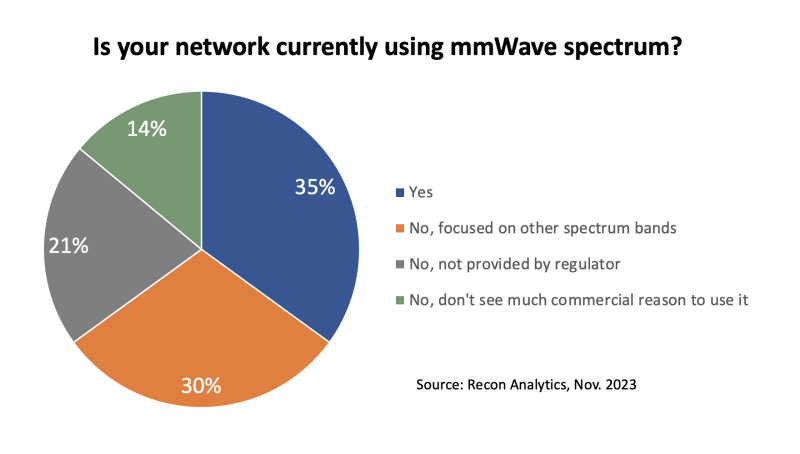

In November Recon Analytics completed a survey of 100 communication service providers (CSP) as part of its “Global Communication Service Provider Pulse” research practice. The survey included questions around the current state of their 5G networks, and their thoughts on 5G Advanced and 6G. Three of those questions are as follows:

- What has been the biggest benefit of deploying 5G?

- In the next phase of 5G’s development, also known as 5G-Advanced, several technological enhancements are under study or being developed. From the list below, which three possible 5G-Advanced technology areas do you think are the most important?

- What are the most important technology areas that you think 6G should focus on?

The most common answers to all three of those questions had to do with increasing network capacity and gaining access to new spectrum. And this is where having lots of water but nothing to drink comes into play. There are mobile operators today who already have large swaths of fallow spectrum in the form of mmWave.

mmWave [1.] provides mobile operators with thousands of megahertz of new capacity, but the majority of 5G operators (with the exception of Verizon) have not started to use it. The limited deployment reflects the coverage and in-building penetration challenges that come with mmWave. Our survey findings underscore this reality. Recon asked mobile operators who currently have a commercial 5G network if they were using mmWave spectrum, below are the responses we got back.

Note 1. 5G mmWave is a set of 5G frequencies that can provide ultra-fast speeds over short distances. It operates on wavelengths between 30 GHz and 300 GHz, which is higher than 4G LTE’s wavelengths of under 6 GHz.

Of the 100 operators we surveyed 66% have a commercial 5G network. Of that group, 35% say they have deployed 5G for mmWave. 44% of the respondents have mmWave spectrum but are either focused on building their network in other spectrum bands, or don’t currently see a commercial reason to use mmWave. The ongoing underutilization of 5G mmWave seems to be impacting the current outlook for future 6G spectrum as well.

When asking mobile network operators about what they thought were the most important areas 6G should focus on, the most common answer given was more capacity through new spectrum. Originally, industry discussions on new 6G spectrum bands were focused on terahertz, which would be even more challenging to work with than mmWave. In the last year there has been a shift. 6G spectrum discussions have moved to the possibility of using bands in the 7 GHz to 24 GHz range. While these bands still have their difficulties when it comes to coverage and in-door penetration, they are not as problematic as terahertz or in many cases mmWave. However, this change in thinking around 6G spectrum does not change the challenges mobile operators must deal with today when it comes to mmWave.

That is where companies like Pivotal Commware and ZTE can be of assistance. Pivotal Commware has pioneered 5G mmWave repeaters that allow a mobile network operator to improve signal range and coverage at a fraction of the cost of an additional mmWave radio. This helps to improve the economics of using mmWave for 5G. Verizon has publicly acknowledged that it is working with the vendor in the U.S. In Asia, ZTE has been working on a solution of its own to overcome line of sight issues with mmWave that it calls RIS 2.0. AIS (Thailand) has trialed RIS 2.0.

Mobile operators’ desire for more capacity is not going away, especially with the emergence of fixed wireless access. The challenge is finding new ways to meet those capacity needs. Operators can continue to milk lower bands and squeeze capacity improvements out of them, but that will only take them so far. mmWave and other higher spectrum bands are well suited to meet growing capacity requirements, but it will require the development of repeaters and reflective services to make those higher bands easier to use for 5G and eventually 6G. It doesn’t help operators to be surrounded by a spectrum they cannot effectively employ, like sailors at sea with no drinkable water in sight.

Daryl Schoolar is a director and analyst at Recon Analytics where he focuses on telecommunication service providers and companies that provide networking communication solutions to those service providers. Some of the topics he covers are digital transformation, 5G, 6G, cloud networking, and telecom service strategies.

UAE network operator “etisalat by e&” achieves 5G mmWave distance milestone

Saudi Arabia’s Stc Achieves 10 Gbps Speeds in 5G mmWave Trials

Verizon Point-To-Multipoint network architecture using mmWave Spectrum

Ericsson and O2 Telefónica demo Europe’s 1st Cloud RAN 5G mmWave FWA use case

Nokia achieves extended range mmWave 5G speed record in Finland

Samsung achieves record speeds over 10km 5G mmWave FWA trial in Australia

Broadband Forum SDN/NFV Work Area launches four new projects at Bangkok Q4-2023 meeting

Introduction:

The Broadband Forum says their open standards and open broadband projects continue to deliver vital importance to companies, both small and large, as we focus on the latest industry trends, and extract most value to consumers, and transition to services-led broadband.

Progress on cloud based SDN/NFV was one of many accomplishments at this December’s meeting in Bangkok, Thailand. SDN and NFV are both software components, but they are different. SDN virtualizes the management of networks, while NFV converts network processes into software applications. SDN separates the data and control planes, allowing operators to manage features from a centralized location. NFV virtualizes network infrastructure, separating functions that typically run in hardware and implementing them as software. We believe the Forum’s SDN/NFV activity is very important as neither SDN or NFV have lived up to their potential and promise, primarily because they were premises based, rather than implemented in the cloud.

From a business perspective, the migration to SDN and NFV in the broadband network facilitates agile deployment of new customized distributed broadband services and applications. This enables new revenues and provider differentiation while managing Capex and OpEx both in the access network and in single and multi-tenant residential and business locations by implementing an agile network and enabling autonomous and automated operations.

![]()

Project Scope: Includes migration to and deployment of SDN/NFV-enabled implementations across all aspects of the broadband network. The scopes are:

- the definition of a new cloud-based environment with its related requirements, called Cloud-based Central Office (CloudCO)

- the architectural requirements, the interface specification among all the components with their related data models including the control-user plane separation interface for disaggregated access nodes

- the specification of virtual network functions and interface with their related data models

- the definition of requirements, interfaces and data models for autonomous and automated networks

Target: Define the Cloud-based Central Office (CloudCO) architecture using SDN, NFV, and cloud technologies to support network functions fundamentally redefining the architecture of access and aggregation networks. Support the migration of SDN and NFV into all aspects of broadband networks, facilitating the agile deployment of new distributed broadband services and applications for operators with greater operational efficiency and lower cost.

Progress: The SDN/NFV Work Area continues to progress the CloudCO project for virtualized network functions, SDN management and control and domain orchestration capabilities in a broadband network. The main activities currently ongoing are related to the disaggregation of the Access Node and defining the related interfaces. The Cloud Component Project Stream is continuing work on Automated Intelligence Management (AIM), Smart SD-WAN and virtual OMCI.

Three key documents near completion. TR-486 is set to be published in December 2023, WT-477 moves to Final Ballot, and WT-386 Issue 2 is currently resolving Straw Ballot comments.

Outcomes:

A productive quarterly meeting for the SDN/NFV Work Area saw four new projects approved. This was WT-403 Amendment 1 ‘PON Abstraction Interface for Time-Critical Applications’, WT-384 Issue 2 ‘CloudCO 2.0’, WT-436 Issue 2 ‘AIM Framework and Architecture’, and a project on Broadband Network Data Collection (BNDC).

A new Open Broadband proposal on CloudCO App SDK was presented to the Broadband Forum Board of Directors.

WT-477 on access node disaggregation has finished Straw Ballot review for both the baseline document and data model. The project has been approved to move to Final Ballot.

WT-413 Issue 2 on ‘SDN Management and Control Interfaces for CloudCO Network Functions’ is progressing. Previously, the SDN/NFV and Common YANG Work Areas reviewed the approach and agreed to report a detailed list of data models, so that vendors can rapidly discover the data models to be implemented for each access network function. The group will discuss the scope regarding the addition of ONU (Optical Network Unit) management and BAA chapter update before the Spring 2024 Meeting. The document is expected to enter Straw Ballot review once WT-477 and WT-486 are completed.

On the Artificial Intelligence and automation fronts, WT-486, which specifies the interfaces for the Automated Intelligence Management (AIM) framework specified in TR-436, has completed Final Ballot and will be published in December 2023. An AIM Tiger Team has completed gap analysis in WT-436 Issue 2 and WT-486 Issue 2. The Tiger Team discussed the Broadband Network Data Collection new project proposal and received approval from the group.

Straw Ballot comment resolution has been completed and WT-386i2 on Fixed Access Network Sharing.

A Tiger Team has been established to review the document on CloudCO interfaces (WT-411i2/WT-454i2) to include the Access SDN Management and Control northbound interface intent-based interactions addressing access network topology and abstraction, including inventory. An update was presented on the discussions held on the data models. The Metamodel needs further review and will be discussed in future weekly meetings.

Together with the Common YANG, the group held a joint session to discuss a new project for BAA – Access Device Abstraction Manager (BAA-ADAM). The groups will continue the discussions offline to clarify the scope and impact on CloudCO interfaces.

The group took part in this year’s CloudCO Demo at Network X in October. Key projects were involved in the demo, including WT-477 reference Disaggregated – Optical Line Terminal (D-OLT) Virtual Network Function, Northbound interface exposure of a L2-L3 network abstraction, Optical Network Terminal (ONT) telemetry over virtualized ONU Management and Control Interface (vOMCI), automation test-suite for OB-BAA, IPFIX adapter framework, and vOMCI Plugfest delta features.

References:

Shaping the future of Broadband – Broadband Forum (broadband-forum.org)

More information about the SDN/NFV Work Area can be found at: https://wiki.broadband-forum.org/display/BBF/SDN+and+NFV.