Author: Alan Weissberger

Dell’ Oro: Huawei still top telecom equipment supplier; optical transport market +1% in 2020

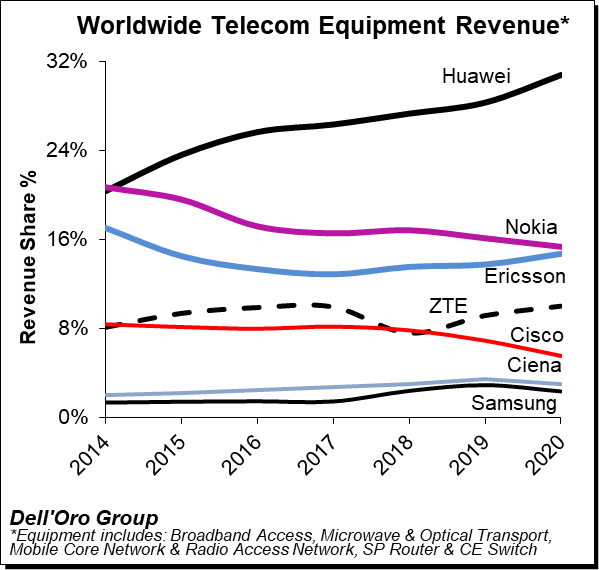

Huawei has increased its lead as the#1 global telecoms network equipment vendor, boosting its revenue share by a three percentage points last year, according to Dell’Oro Group. Nokia lost one percentage point of revenue share year-on-year, as did Cisco, the latter falling to 6%. Ericsson gained one percentage point to match Nokia at 15% of the market and ZTE also saw a 1% uptick to 10% of the global telecom market. (Please refer to chart below).

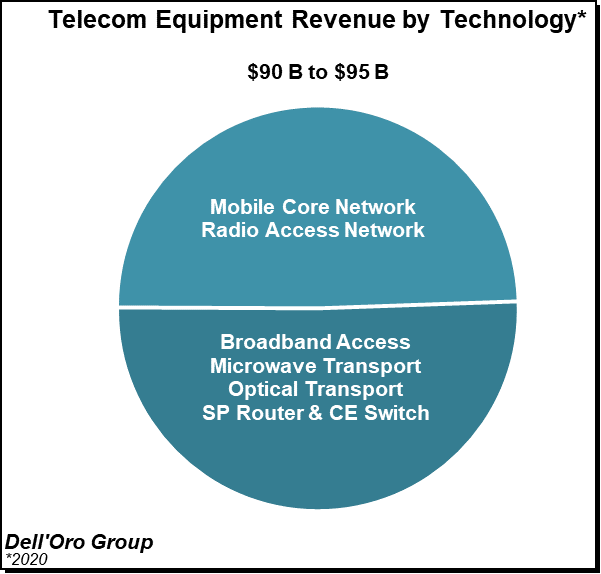

Dell’Oro Group’s preliminary estimates suggest the overall telecom equipment market – Broadband Access, Microwave & Optical Transport, Mobile Core & Radio Access Network, SP Router & Carrier Ethernet Switch (CES) – advanced 7% year-over-year (Y/Y) for the full year 2020, growing at the fastest pace since 2011.

The telecom and networking market research firm suggests revenue rankings remained stable between 2019 and 2020, with Huawei, Nokia, Ericsson, ZTE, Cisco, Ciena, and Samsung ranked as the top seven suppliers, accounting for 80% to 85% of the total market. At the same time, revenue shares continued to be impacted by the state of the 5G rollouts in highly concentrated markets. While both Ericsson and Nokia improved their RAN positions outside of China, initial estimates suggest Huawei’s global telecom equipment market share, including China, improved by two to three percentage points for the full year 2020.

Dell’Oro now estimates the following revenue shares for the top seven suppliers:

| Top 7 Suppliers | Year 2019 | Year 2020 |

| Huawei | 28% | 31% |

| Nokia | 16% | 15% |

| Ericsson | 14% | 15% |

| ZTE | 9% | 10% |

| Cisco | 7% | 6% |

| Ciena | 3% | 3% |

| Samsung | 3% | 2% |

Additional key takeaways from the 4Q2020 reporting period:

- Preliminary estimates suggest that the positive momentum that has characterized the overall telecom market since 1Q-2020 extended into the fourth quarter, underpinned by strong growth in multiple wireless segments, including RAN and Mobile Core Networks, and modest growth in Broadband Access and CES.

- Helping to drive this output acceleration for the full year 2020 is faster growth in Mobile Core Networks and RAN, both of which increased above expectations.

- Covid-19 related supply chain disruptions that impacted some of the telco segments in the early part of the year had for the most part been alleviated towards the end of the year.

- Not surprisingly, network traffic surges resulting from shifting usage patterns impacted the telecom equipment market differently, resulting in strong demand for capacity upgrades with some technologies/regions while the pandemic did not lead to significant incremental capacity in other cases.

- With investments in China outpacing the overall market, we estimate Huawei and ZTE collectively gained around 3 to 4 percentage points of revenue share between 2019 and 2020, together comprising more than 40% of the global telecom equipment market.

- Even with the higher baseline, the Dell’Oro analyst team remains optimistic about 2021 and projects the overall telecom equipment market to advance 3% to 5%.

Dell’Oro Group telecommunication infrastructure research programs consist of the following: Broadband Access, Microwave Transmission & Mobile Backhaul, Mobile Core Networks, Mobile Radio Access Network, Optical Transport, and Service Provider (SP) Router & Carrier Ethernet Switch.

…………………………………………………………………………………………….

Last week, Dell’Oro Group reported that the optical transport equipment revenue increased 1% in 2020 reaching $16 billion. In this period, all regions grew with the exception of North America and Latin America.

“Between concerns on starting new optical builds during the start of the pandemic and aggressive plans on 5G deployments that required a larger share of a service provider’s capital budget, the spending on optical transport dramatically slowed by the end of 2020,” said Jimmy Yu, Vice President at Dell’Oro Group.

“It was a really dramatic drop in optical equipment purchases in the fourth quarter. While we anticipated a slowdown near the end of the year due to concerns around COVID-19, we were surprised by a 29 percent year-over-year decline in WDM purchases in North America as well as a 12 percent decline in China. That said, there was good growth in the other parts of the world, especially Japan,” continued Yu.

| Optical Transport Equipment Market | |

| Regions | Growth Rate in 2020 |

| North America | -6% |

| Europe, Middle East and Africa | 2% |

| China | 1% |

| Asia Pacific excluding China | 13% |

| Caribbean and Latin America | -14% |

| Worldwide | 1% |

The Dell’Oro Group Optical Transport Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, average selling prices, unit shipments (by speed including 100 Gbps, 200 Gbps, 400 Gbps, and 800 Gbps). The report tracks DWDM long haul, WDM metro, multiservice multiplexers (SONET/SDH), optical switch, optical packet platforms, data center interconnect (metro and long haul), and disaggregated WDM. To purchase this report, please email [email protected].

References:

Deutsche Telekom tests 5G standalone video call

“Our goal is to continue to actively shape the future of mobile communications. 5G standalone is important to be able to use technologies such as network slicing or edge computing,” says Claudia Nemat, Board Member Technology and Innovation at Telekom. “We are very proud to have taken the next innovation step in 5G. With this test, we are once again demonstrating our innovation leadership.”

DT first announced tests of its 5G standalone network in February. At the time, Walter Goldenits said the Garching test represented the first step towards the 5G standalone live network, although he also noted that a rollout “will then also depend on the requirements of our customers. Technology and the market will play a joint role in further development.”

Goldenits said more than two thirds of people in Germany are now covered by the operator’s non-standalone 5G network (5G NSA), which is anchored to the existing 4G-LTE infrastructure.

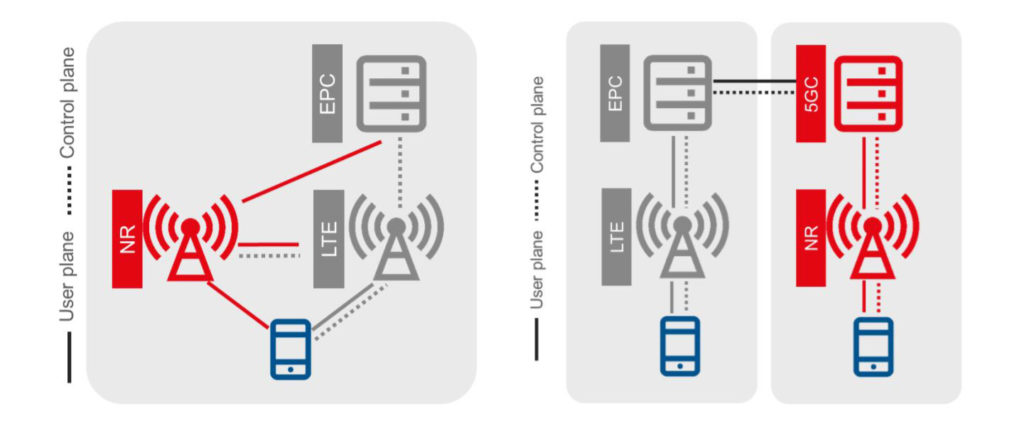

5G NSA (EPC) vs 5G SA (5G Core):

Image Courtesy of GSMA

Important Question:

We wonder how DT is collaborating with T-Mobile US which has already deployed a 5G SA/5G Core network? DT owns 43% of T–Mobile, but the shareholder pact with Softbank assures it of strategic control and allows it to consolidate results of its largest subsidiary at group level. Cooperation is essential to ensure interoperability and 5G SA roaming, because there is no implementation standard or open specification for 5G SA/5G Core network (as we have written so many times).

…………………………………………………………………………………………..

Deutsche Telekom, Orange, Telefónica and Vodafone also recently pledged their support for Open RAN technology in the hope a joint commitment will attract investment, speed up the development of products that can be used in mainstream networks and produce new European wireless network equipment suppliers.

Leichtman Research Group: Top U.S. Broadband Providers Add; PayTV Providers Lose Subscribers in 2020

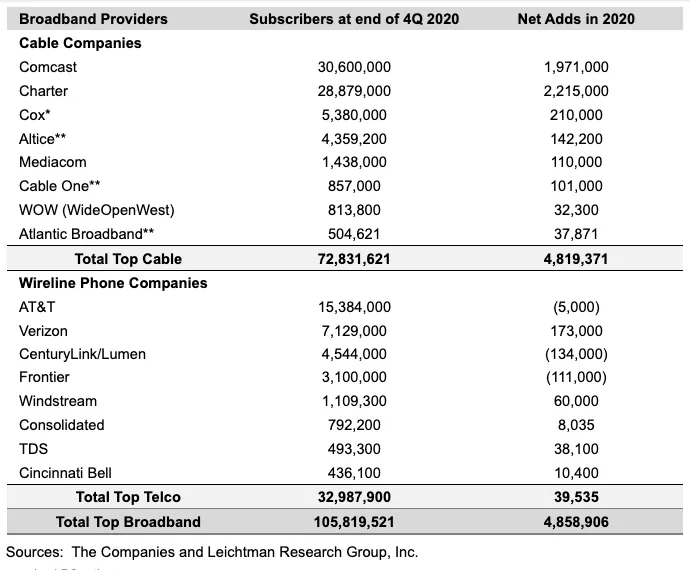

Leichtman Research Group reports that largest U.S. broadband network providers added almost twice as many fixed subscribers in 2020 as they did the previous year, largely due to the Covid-19 pandemic. However, some large broadband providers (like AT&T) lost customers.

The largest cable and wireline phone providers in the U.S. – representing about 96% of the market – acquired about 4,860,000 net additional broadband Internet subscribers in 2020, compared to a pro forma gain of about 2,550,000 subscribers in 2019.

These top broadband providers now account for 105.8 million subscribers, with top cable companies having 72.8 million broadband subscribers, and top wireline phone companies having 33 million subscribers.

Comcast and Charter accounted for 4.19 million, or 86%, of the total number of net additions, with the other six cablecos’ adds coming in significantly lower, ranging from 210,000 for Cox to just under 38,000 for Atlantic Broadband.

For wireline telcos, the best performance came from Verizon, which added a fairly respectable 173,000 fixed broadband customers, but three of the eight posted net customer losses. In particular, AT&T’s net broadband losses came in at 5,000 while CenturyLink and Frontier both lost well over 100,000 customers.

[As per the report below, AT&T’s DirecTV lost more than 3.26 million subscribers which was ~60% of all U.S. pay TV losses in 2020.]

Notes:

* LRG estimate

** Includes recent small acquisitions/sales and LRG pro forma estimates

^ Frontier’s total for 4Q 2020 is an LRG estimate due to later year-end reporting

TDS includes 283,900 wireline broadband subscribers, and 209,400 cable broadband subscribers

…………………………………………………………………………………….

Key findings for the year 2020 include:

- Overall, broadband additions in 2020 were 190% of those in 2019, and more than in any year since 2008

- Top cable and wireline phone companies represent approximately 96% of all subscribers

- The top cable companies added about 4,820,000 subscribers in 2020 – compared to about 3,145,000 net adds in 2019, and the most in any year since 2006

- Charter’s 2,215,000 net broadband additions in 2020 were more than any company had in a year since 2006

- The top wireline telecom companies added about 40,000 subscribers in 2020 – compared to a loss of about 590,000 subscribers in 2019

- Telcos had positive net annual broadband adds for the first year since 2014

- At the end of 2020, cable had a 69% market share vs. 31% for Telcos

“With the impact of the coronavirus pandemic, there were more net broadband additions in 2020 than in any year since 2008,” said Bruce Leichtman, president and principal analyst for Leichtman Research Group, Inc (LRG). “The top cable and Telco broadband providers in the U.S. cumulatively added about 4,860,000 subscribers in 2020, compared to about 5,100,000 subscribers in 2018 and 2019 combined.”

Separately, LRG found that the largest pay-TV providers in the U.S. – representing about 95% of the market – lost about 5,120,000 net video subscribers in 2020, compared to a pro forma net loss of about 4,795,000 in 2019.

The top pay-TV providers now account for about 81.3 million subscribers – with the top seven cable companies having 43.9 million video subscribers, satellite TV services having about 21.8 million subscribers, the top telephone companies having 7.9 million subscribers, and the top publicly reporting Internet-delivered (vMVPD) pay-TV services having 7.7 million subscribers.

AT&T had a net loss of about 3,260,000 subscribers across its four pay-TV services (DIRECTV, AT&T U-verse, AT&T TV, and AT&T TV NOW) in 2020 – compared to a net loss of about 4,095,000 subscribers in 2019.

AT&T “Premium TV” services (not including the vMVPD service AT&T TV NOW) lost 15.3% of subscribers in 2020 – compared to a 4.6% loss among all other traditional pay-TV services.

Key findings for the year include:

- Satellite TV services lost about 3,440,000 subscribers in 2020 – compared to a loss of about 3.700,000 subscribers in 2019

- The top seven cable companies lost about 1,915,000 video subscribers in 2020 – compared to a loss of about 1,560,000 subscribers in 2019

- The top telco TV companies lost about 405,000 video subscribers in 2020 – compared to a loss of about 630,000 subscribers in 2019

- The top publicly reporting Internet-delivered (vMVPD) services (Hulu + Live TV, Sling TV, AT&T TV NOW, and fuboTV) added about 640,000 subscribers in 2020 – compared to about 1,095,000 net adds in 2019

- Traditional pay-TV services (not including vMVPDs) lost about 5,765,000 subscribers in 2020 – compared to a net loss of about 5,890,000 in 2019

“Net pay-TV losses of over 5 million subscribers in 2020 were slightly higher than in 2019, and more than in any previous year,” said Bruce Leichtman, president and principal analyst for Leichtman Research Group, Inc. “Overall, the top pay-TV providers lost 5.9% of subscribers in 2020, compared to 5.2% in 2019.”

About Leichtman Research Group, Inc.

Leichtman Research Group, Inc. (LRG) specializes in research and analysis on broadband, media and entertainment industries. LRG combines ongoing consumer surveys with industry tracking and analysis, to provide companies with a richer understanding of current market conditions, and the potential impact and adoption of new products and services. For more information about LRG, please call (603) 397-5400 or visit www.LeichtmanResearch.com.

References:

https://www.leichtmanresearch.com/about-4860000-added-broadband-from-top-providers-in-2020/

https://www.leichtmanresearch.com/major-pay-tv-providers-lost-about-5120000-subscribers-in-2020/

https://telecoms.com/508907/pandemic-provided-a-shot-in-the-arm-for-us-fixed-broadband/

Verizon is again top U.S. telco brand; AT&T falling behind T-Mobile

According to Brand Finance’s new rankings, Verizon recently widened its lead over AT&T as the world’s most valuable telecoms brand. The firm reported Verizon’s brand rose 8% in its rankings to a value of $68.9 billion.

For the second year in a row Verizon has claimed the title of the world’s most valuable telecoms brand following an 8% increase in brand value to US$68.9 billion. This brand value growth has not only propelled it back into the top 10 most valuable brands globally in the Brand Finance Global 500 2021 ranking, but has meant the brand has continued to widen the lead over second placed AT&T (brand value down 13% to US$51.4 billion). 15 further US brands feature in the Brand Finance Telecoms 150 2021 ranking, with a combined brand value of US$182.8 billion.

Two years since the beginning of Verizon’s business transformation program, Verizon 2.0 – focusing on the transformation of the network, the go-to-market, the brand, and the culture of the business – the brand continues to make leaps and bounds across the industry. The giant is widely recognized to have the best-in-class network and the widest coverage in the US, with the network’s usage surging during the pandemic, handling a staggering 800 million phone calls and 8 billion texts per day.

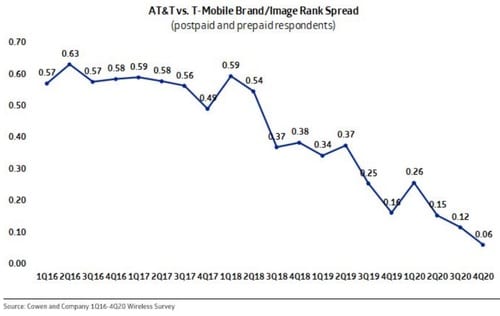

Meanwhile, Cowen and Company sees T-Mobile overtaking AT&T to be the second most popular telecom brand after Verizon. Cowen analysts conduct quarterly surveys of mobile customers, asking them to rank providers for “overall brand/image.”

In the 4th Quarter of 2020, the perceived difference between T-Mobile and AT&T was at its narrowest point since they started conducting their survey. As per the chart below, there was only a 0.06 difference between the two brands (we do not know how Cowen calculated the Rank Spread).

Cowen stated this brand perception issue will be an important to watch during 2021 because “network quality/coverage has historically been one of the main reasons for subscribers to leave their current wireless provider and likely a key driver of brand perception.”

The Cowen Telco Perceptions report (clients only) comes months after T-Mobile boasted that it surpassed AT&T in terms of total number of mobile phone customers.

Analyst Craig Moffett was shocked with AT&T’s $23.4 billion spent at the recently completed C-band auction. He wrote in a note to clients:

“At $23.4B, AT&T spent more than would have been expected a month ago, but expectations for their spend had been rising (notwithstanding the fact that they have only financed half of what they bought, and even that with only short-term debt), so the surprise may not be large there, either. But again, it’s a shock to see the number.”

“AT&T emerges from the auction with leverage of 4.1x EBITDA (assuming all debt financing). Can their dividend be sustained?”

AT&T bought 80 MHz of C-band spectrum in almost all of the top 50 U.S. markets.

How will they be able to finance the buildout of their 5G network to deploy that spectrum?

If you have an opinion on that, please post a comment in the box below this article. Thanks in advance!

References:

TIP OpenRAN project: New 5G Private Networks and ROMA subgroups

The Telecom Infra Project (TIP), one of several industry consortiums creating specifications for open radio access networks (Open RAN), recently announced a new 5G Private Networks subgroup.

Editor’s Note:

We don’t know whether the TIP OpenRAN project or the O-RAN Alliance has (and will have) more industry influence and impact. In addition, there are many splinter partnerships forming; many of them led by Rakuten Mobile. What’s mind boggling is that none of the groups have liaison agreements with either ITU-R WP5D (responsible for all IMT standards, including 4G and 5G) or 3GPP (the prime spec writing organization for mobile networks).

……………………………………………………………………………………

5G Private Networks contribute to improve the quality of experience for 5G connectivity, including better coverage and capacity through on-premise radio equipment, the ability to support low latency and high bandwidth service requirements through edge compute & routing of private traffic, and the potential to support the increasing demand for privacy and localized data analytics.

For network operators, 5G Private Networks also create the opportunity to implement new network management and operational models, enabling full automation of the operation of the enterprise network while improving end customer application experience.

However, to fully capture the benefits of 5G Private Networks, a different approach is required, because traditional network architectures, focused on large scale deployments and operations don’t have the right economics or the operational flexibility to efficiently deliver on the emerging needs of enterprise customers.

The 5G Private Networks Solution Group will develop a new approach to manage and operate 5G Private Networks, based on a cloud-native architecture, and making use of a new class of software management tools, based on the paradigms currently used for the cloud, but adapted to deliver the requirements of a telecom network environment. Telefónica will test the solution in their local TIP Community Lab in Madrid and then move to field trials in Málaga (Spain).

Juan Carlos Garcia, SVP Technology Innovation & Ecosystem, Telefónica, and TIP Board Director said: “This new solution group will enable operators to address the exciting opportunities that 5G is creating in the enterprise segment, both through valuable features for our customers and more efficient network operations. The TIP community is the perfect environment for this innovation, as it will allow us to leverage multiple current project groups (Open Core Networks, OpenRAN) to deliver an end-to-end Minimum Viable Product that we will then test in Telefonica’s TIP Community Lab.”

In particular, the new Solutions Group will leverage previous work contributed to TIP’s OpenRAN Project Group, on a first version of a CI/CD platform that applies traditional IT methodologies to automate integration, testing and deployment of OpenRAN software.

Ihab Tarazi, CTO and SVP, Networking and Solutions, Dell Technologies and TIP Board Director, said: “For open networks to deliver their benefits, the telecom industry needs an abstraction layer that helps integrate different components into end-to-end solutions. New software management tools based on the ones currently used for the cloud can address this need, and this Solution Group is a timely initiative for the industry to collaborate on making this happen.”

Caroline Chan, VP and GM Network Business Incubation Division, Intel and TIP Board Director, said: “Through the recently launched solution groups, TIP is expanding its scope to include the validation of interoperability between different elements across the whole network, and insights and recommendations about how to operate them. The new 5G Private Networks Solution Group is a strong example of this approach. With dedicated local private high-performance network connectivity as a key emerging deployment model for 5G and edge buildout, this group can help foster important ecosystem collaboration.”

As a result, this new solution group will help drive:

- Improved network economics, through the use of commoditized hardware and open source software, and more efficient and flexible network operations and automation, enabled by the adoption of cloud-native technologies.

- Dedicated local high-performance 5G connectivity and edge computing infrastructure, appealing to multiple B2B & B2B2C verticals.

- Better network security and performance.

Telefónica is one of the five European telcos that announced that they will work together on open RANs for mobile networks. The others are Deutsche Telekom, Orange, TIM and Vodafone. A memorandum of understanding (MOU) for that grouping commits the five to the O-RAN Alliance, which has 27 network operator members from AT&T to Vodafone, and to “other industry initiatives, such as the Telecom Infra Project, that contribute to the development of open RAN and that aim to create a healthy and competitive open RAN ecosystem and advance R&D efforts.”

……………………………………………………………………………………………………………….

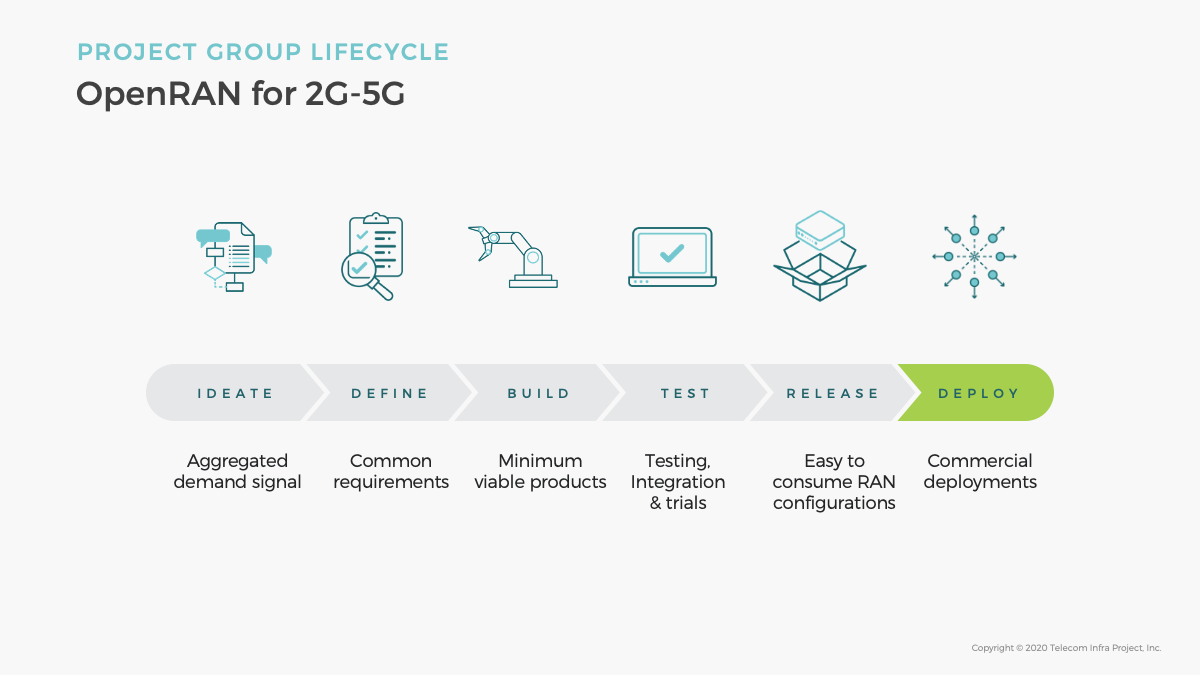

Separately, the charter of the new OpenRAN Orchestration and Management Automation (ROMA) subgroup was approved by the OpenRAN PG. ROMA focuses on aggregating and harmonizing mobile network operators requirements on Open RAN orchestration and lifecycle management automation, fostering ecosystem partners to develop products and solutions that meet ROMA requirements.

The goal of ROMA is to:

· Develop a common set of use cases for OpenRAN lifecycle management automation and orchestration that are agreed across multiple MNO and OpenRAN ecosystem members

· Develop Technical Requirements on products and solutions that support the identified use cases, including interfaces and data models

· Facilitate product and solution development through lab testing, field trials, participating TIP Plugfest and badging on TIP exchange etc.

· Support large scale OpenRAN deployment with lifecycle management automation, including Continuous Integration and Continuous Deployment (CI/CD) frameworks and tool sets.

It will bring better coverage and capacity through on-premise radio equipment, says TIP, and the ability to support low latency and high bandwidth service requirements through edge compute and routing of private traffic, and the potential to support the increasing demand for privacy and localized data analytics.

……………………………………………………………………

About the Telecom Infra Project:

The Telecom Infra Project (TIP) is a global community of companies and organizations that are driving infrastructure solutions to advance global connectivity. Half of the world’s population is still not connected to the internet, and for those who are, connectivity is often insufficient. This limits access to the multitude of consumer and commercial benefits provided by the internet, thereby impacting GDP growth globally. However, a lack of flexibility in the current solutions – exacerbated by a limited choice in technology providers – makes it challenging for operators to efficiently build and upgrade networks.

Founded in 2016, TIP is a community of diverse participants that includes hundreds of companies – from service providers and technology partners, to systems integrators and other connectivity stakeholders. We are working together to develop, test and deploy open, disaggregated, and standards-based solutions that deliver the high-quality connectivity that the world needs – now and in the decades to come.

Find out more: www.telecominfraproject.com

References:

Learn more and join the new 5G Private Networks Solution Group here.

https://telecominfraproject.com/tip-launches-5g-private-networks-solution-group/

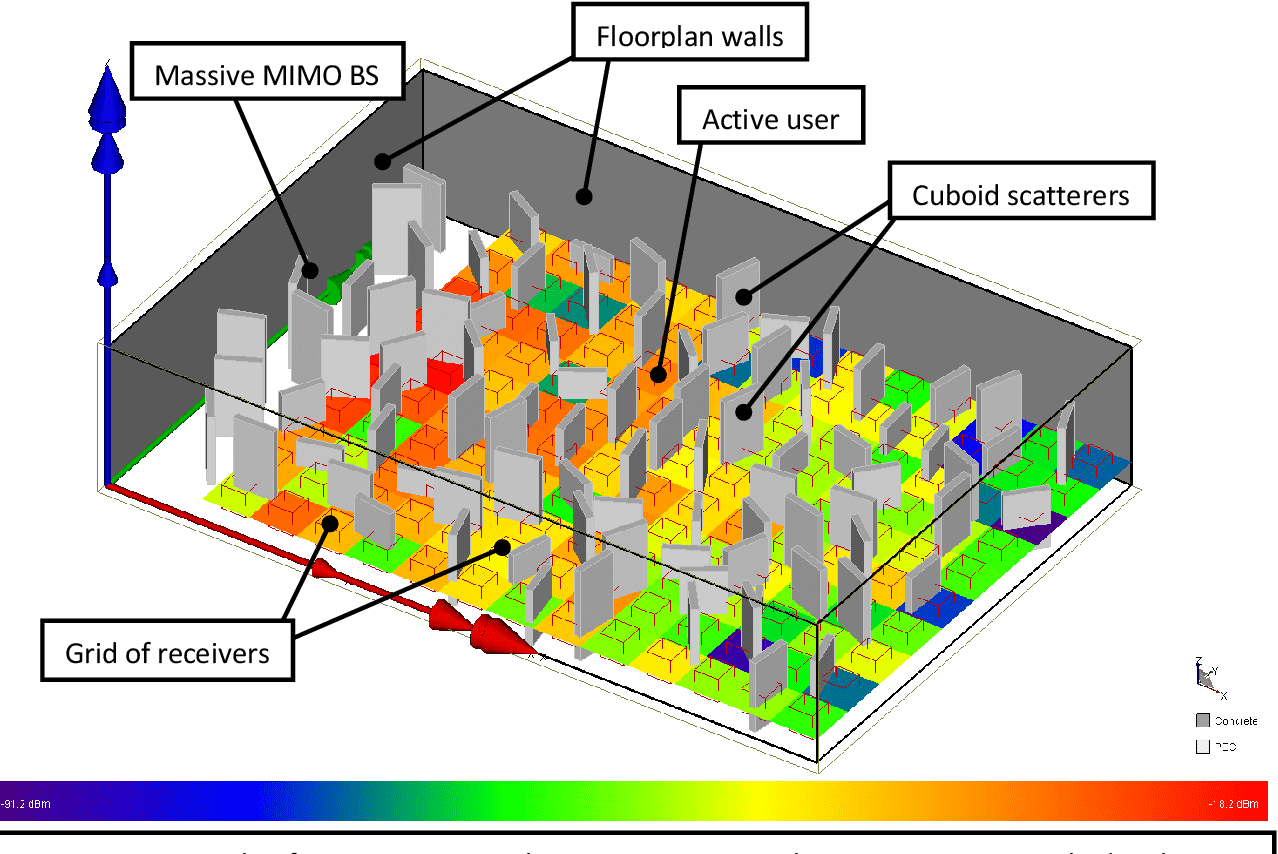

Huawei and China Mobile test 5G indoor Massive MIMO

The pilot was conducted using LampSite, Huawei’s 5G digital indoor network product, based on the 2.6 GHz inter-frequency networking (80 MHz + 80 MHz). Distributed Massive MIMO was enabled in multiple 5G indoor cells to provide the large capacity needed to support 5GtoB (5G to Business) services and meet their high requirements for uplink experience. The peak uplink experience was quadrupled compared with traditional 4T4R cells.

Indoor distributed Massive MIMO introduces Massive MIMO for macro base stations to indoor networks. It is an innovative approach by Huawei to continuously increase the capacity of indoor 5G networks. The technology supports up to 64T64R channels and pools beamforming, MU-MIMO, and other technologies to ensure high capacity in the uplink and consistent user-perceived data speeds. Such a high level of performance makes it perfectly for smart production in which service terminals are frequently relocated for flexible production. Adding another competitive edge to empower 5G to transform industries.

The pilot is of great significance to indoor 5G, providing carriers with a new option to ensure premium uplink experience for emerging industrial services, such as video transfer and AGV operations, and expand 5G to factories, ports, power grids, airports, transportation, security, and many other industrial markets.

Huawei will continue to work with China Mobile Guangdong in innovating 5G to improve 5G performance, build competitive 5G networks, and lead the development of 5G to Business customers.

Huawei will continue to work with China Mobile Guangdong in innovating 5G to improve 5G performance, build competitive 5G networks, and lead the development of 5G to Business customers.

India 4G Spectrum Auction Raises 778 billion Rupees

After much delay, India’s 4G spectrum auction has ended in just two days, raising Indian Rupee (INR) 778 billion (US $10.6 billion) for the government. The auction was held on March 1st and 2nd by India’s Department of Telecommunications. The airwaves acquired will help India’s telecom network operators add 4G capacity and get ready for 5G.

India auctioned spectrum in the 700 MHz, 800 MHz, 900 MHz, 1800 MHz, 2100 MHz, 2300 MHz and 2500 MHz frequency bands. However, the 700MHz spectrum remained unsold because of the high reserve price.

India telecom network operators Reliance Jio, Bharti Airtel, and Vodafone Idea won spectrum in the government’s latest auction.

India’s largest telco, Reliance Jio announced it has acquired the right to use spectrum in all 22 circles across India in the auction. The upstart network operator secured spectrum in the 800 MHz, 1800 MHz and 2300 MHz frequency bands, which increases Jio’s spectrum footprint by 55 percent to 1,717 MHz.

Jio will pay INR 571.23 billion for the right to use this spectrum for a period of 20 years. Payments can be made over a period of 18 years (2-year moratorium plus 16-year repayment period), with interest at 7.3 percent per year.

Reliance Jio now claims to have the highest amount of sub-GHz spectrum with 2×10 MHz contiguous spectrum in most circles. It also has at least 2×10 MHz in the 1800 MHz band and 40 MHz in the 2300 MHz band in each of the 22 circles. The operator also reports it has achieved complete spectrum derisking, with average life of owned spectrum of 15.5 years. Reliance Jio will acquire the spectrum with an effective cost of INR 608 million per MHz. Jio also says the acquired spectrum can be used for provision of 5G services.

“The acquired spectrum can be utilized for transition to 5G services at the appropriate time, where Jio has developed its own 5G stack,” says the Jio press release.

India’s second-largest network service provider, Bharti Airtel acquired 355.45 MHz of spectrum across sub-GHz, mid-band and 2300 MHz bands for a total price of INR 186.99 billion. Airtel will use this spectrum to upgrade its deep indoor and in-building coverage in urban towns. In addition, this spectrum will also help improve its coverage in villages by offering the superior Airtel experience to an additional 90 million customers in India. Airtel also plans to use this spectrum to deliver 5G services in future.

An Airtel statement mentioned that the “the reserve pricing of these bands [700MHz and 3.5GHz] must be addressed on priority in future. This will help the nation to benefit from the digital dividend that will inevitably arise out of this.”

“Airtel has now secured pan-India footprint of sub GHz spectrum that will help improve its deep indoor and in building coverage in every urban town,” as per the company’s statement.

Vodafone Idea entered this spectrum auction “holding the largest quantum of spectrum with a very small fraction, which was administratively allocated and used for GSM services, coming up for renewal”.

As a result, Vodafone Idea acquired spectrum in only five circles for INR 19.93 billion. The operator said it has used this opportunity to optimize spectrum holdings post-merger to create further efficiencies in a few circles. Vodafone Idea expects the spectrum it has acquired in five circles to help it enhance its 4G coverage and capacity.

India’s just completed spectrum auction does not contain any airwaves for 5G

……………………………………………………………………………………………

Reliance Jio’s decision to be the biggest spenders at the auction comes shortly after its holding company, Jio Platforms, reported ₹22,858 crore in revenue during the quarter to December, which was a 30% improvement from the year prior.

Last year, Jio Platforms sold a third of itself to others for ₹152,056 crore. Buyers included Google, Facebook, Silver Lake, Vista Equity Partners, General Atlantic, KKR, Mubadala, ADIA, TPG, L Catterton, PIF, Intel Capital, and Qualcomm Ventures.

References:

https://www.telecompaper.com/news/india-completes-spectrum-auction-raises-inr-778-billion–1374417

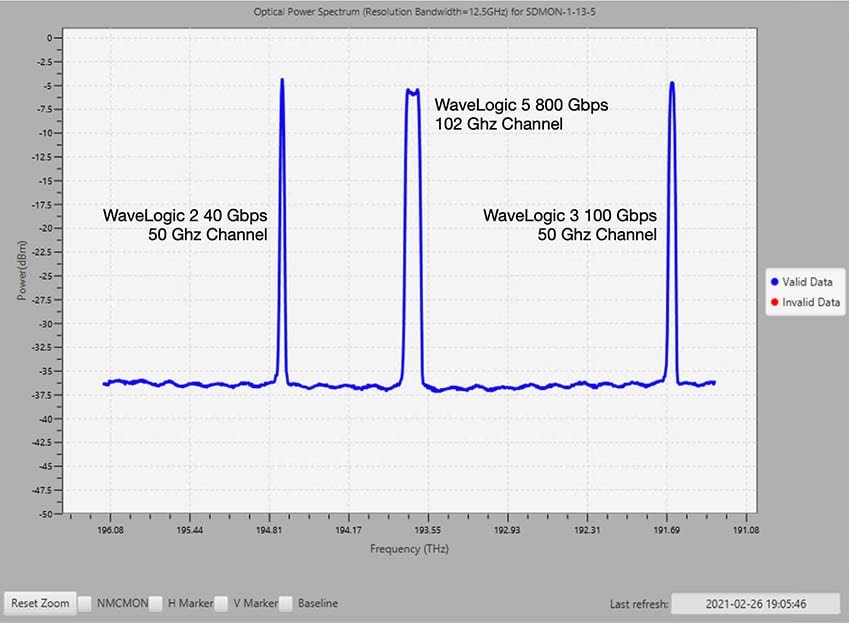

Internet 2’s Next Generation Infrastructure team deploys 800Gbps optical link

On February 26, 2021, Internet2 deployed its first 800 Gbps single-carrier optical circuit between Phoenix and Tucson, AZ as part of its Next Generation Infrastructure (NGI) program.

This milestone marks the first 800G native link to be deployed by a U.S. research and education network. The optical circuit leverages a 102 Ghz carrier generated by a single Ciena Waveserver 5 transponder at each endpoint.

On February 25, 2021, the Internet2 project team completed the upgrade of all Reconfigurable Optical Add-Drop Multiplexers (ROADMs) to flex spectrum on all east-west long-haul routes nationwide. Additionally, the majority of the optical fiber was upgraded from LEAF to SMF28 to better match the coherent transmission technologies being used to convey the new 800 Gbps optical link.

Internet2 plans to rapidly expand its 400G and 800G transmission capabilities along these newly flex-grid enabled routes; more link capacity will come online as our phase 2 hardware deployment team (GDT) continues to move across the country. The Internet2 team is deploying the Cisco 8200 and Ciena Waveserver 5 platform. Completion is targeted for the end of this month (March 2021).

The successful deployment of this initial 800 Gbps optical link is the culmination of thousands of hours of effort from both the Internet2 community and teams in many organizations, including Internet2, GlobalNOC at Indiana University, Ciena, Lumen, and GDT.

Just two weeks ago, Telefonica said it had trialed an 800 Gbps optical link, using Huawei and Nokia network equipment. However, there are no 800 Gps links in any commercial production network, as far as we can determine.

References:

North Carolina School District deploys WiFi 6 from Cambium Networks; WiFi 6 vs 6E Explained

Cambium Networks a leading global provider of wireless networking solutions, today announced its multi-year agreement with the school district of Burke County, N.C., with the addition of Wi-Fi 6 access points to provide multi-gigabit speeds in classrooms.

Using E-Rate funding for education, Burke County will upgrade its network to the latest Wi-Fi 6 technology to improve learning for students. The project, which began in late 2020, is delivering 1,500 multi-gigabit high-density access points to the district’s 27 schools and 12,000 students. This will allow students to simultaneously use Zoom and view streaming videos in the classroom using the latest XV3-8 access points, as well as XMS cloud management that seamlessly integrates with Google G-Suite and other embedded education systems.

“When the technology works, the students win, and so does our community. That is especially important as we navigate the pandemic and students return in March,” said Dr. Melanie Honeycutt, CIO of the Burke County School District. “Cambium is our solution for great performance at an affordable price for high density classrooms, and just in time as COVID accelerated our 1:1 laptop program and the increased use of streaming video.”

Cambium’s Wi-Fi 6 and XMS end-to-end cloud-management solutions provide multi-gigabit Wi-Fi access at a proven low total cost of ownership. With easy integration to existing systems, planning, provisioning, installation and centralized cloud management, Cambium’s solutions can be rapidly deployed to deliver end-to-end multi-gigabit wireless speeds.

“We love to work with visionary and discerning customers,” said Atul Bhatnagar, president and CEO, Cambium Networks. “Dr. Honeycutt and Burke County understand that this is the time to address the digital divide. They have done so in a way that gives students what they require for excellence in education.”

……………………………………………………………………………………..

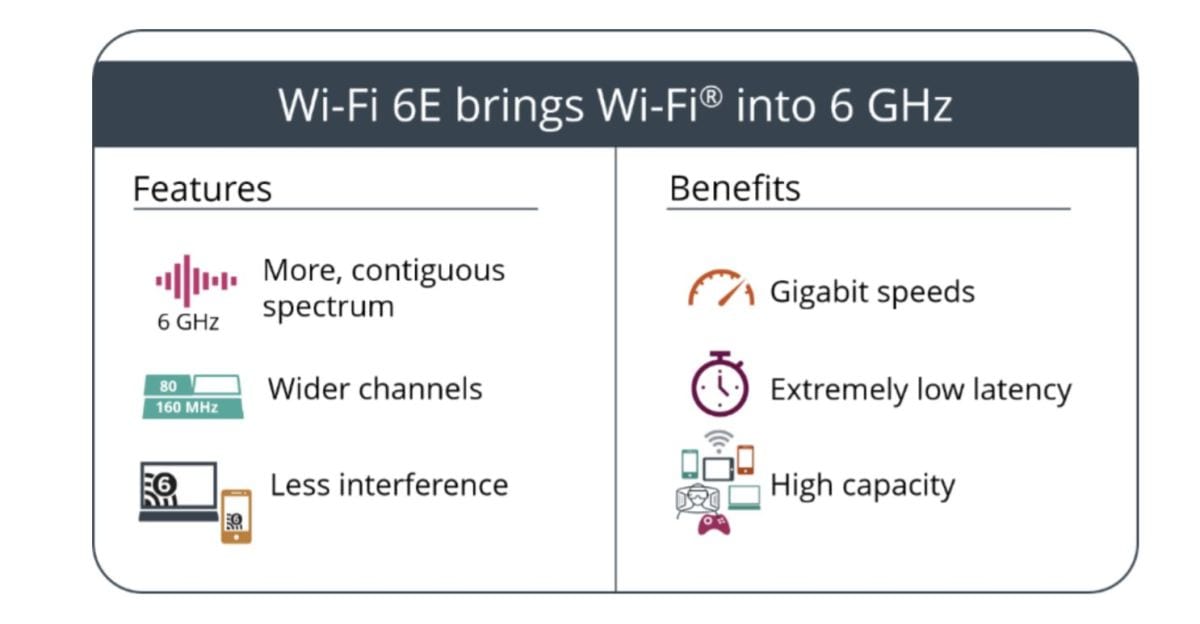

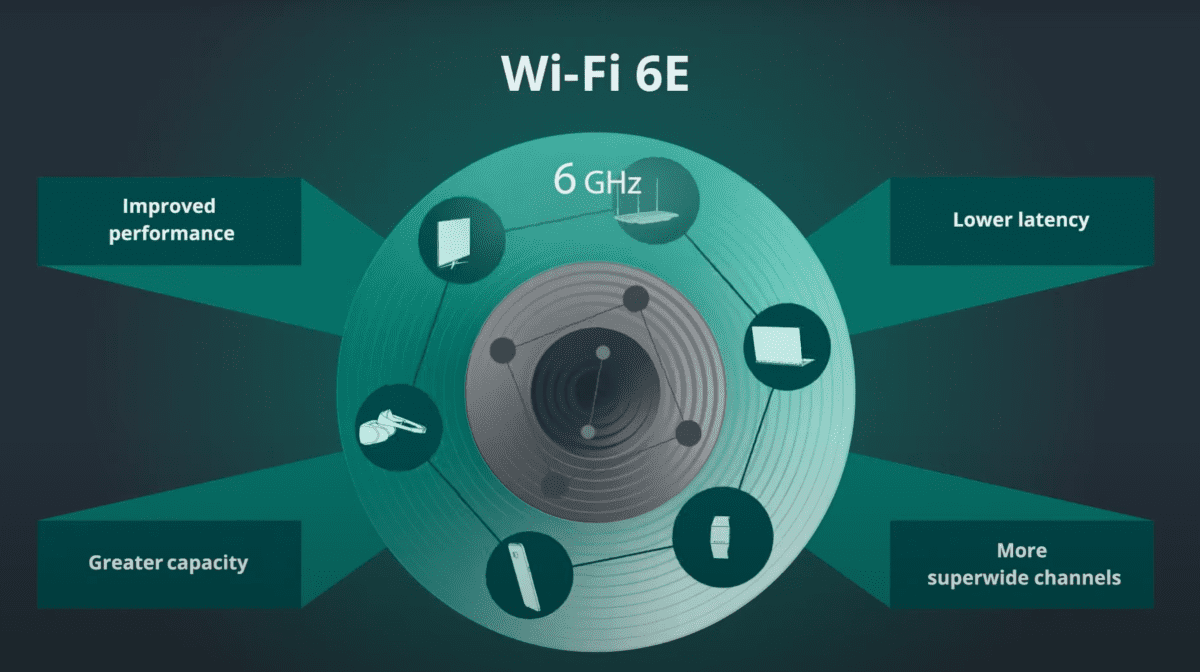

What is WiFi 6 and 6E?

The IEEE 802.11ax standard was dubbed Wi-Fi 6 by the WiFi Alliance. At the time of publication, it was limited by U.S. law to a wireless spectrum that only covered the 2.4GHz and 5GHz bands.

In a 2.4GHz band, there are three non-overlapping channels—and that bandwidth is shared by all users. If too many end point WiFi devices compete for bandwidth on the same wireless channel, then some of those signals will be dropped.

In April of 2020, the Federal Communications Commission (FCC) voted unanimously to open up the 6GHz band for unlicensed use. With that policy change, significantly more airwaves are open that WiFi routers can use. The WiFi Alliance named versions of IEEE 802.11ax that operate at or above 6GHZ as WiFi 6E.

Images Courtesy of WiFi Alliance

…………………………………………………………………………………….

The opening of the 6GHz band is essentially quadruples the amount of airwaves (14 additional 80MHz channels, and seven additional 160MHz channels) available for WiFi routers and smart WiFi devices. That means less signal interference.

Wi-Fi Alliance® is introducing new terminology to distinguish forthcoming Wi-Fi 6 devices that are capable of 6 GHz operation, an important portion of unlicensed spectrum that may soon be made available by regulators around the world. Wi-Fi 6E brings a common industry name for Wi-Fi® users to identify devices that will offer the features and capabilities of Wi-Fi 6 – including higher performance, lower latency, and faster data rates – extended into the 6 GHz band. Wi-Fi 6E devices are expected to become available quickly following 6 GHz regulatory approvals, utilizing this additional spectrum capacity to deliver continuous Wi-Fi innovation and valuable contributions to consumers, businesses and economies.

So, what’s the difference?

Early-adopter devices using Wi-Fi 6 (such as the first batch of Wi-Fi 6 routers) are limited to the 2.4GHz and 5GHz spectrum, while Wi-Fi 6E-compliant devices will have access to all those much richer 6GHz airwaves.

References:

https://www.wi-fi.org/news-events/newsroom/wi-fi-certified-6-delivers-new-wi-fi-era

https://www.wi-fi.org/news-events/newsroom/wi-fi-alliance-brings-wi-fi-6-into-6-ghz

IBM’s Cloud Satellite service in Generally Available Orbit

IBM’s Cloud Satellite service is now in generally available (GA) orbit. The service extends the IBM Cloud control plane to run virtually anywhere, whether that be on commodity hardware, some edge device, or inside another public cloud.

IBM manages Cloud Satellite deployments, which is different than from most other software-defined hybrid cloud platforms. It provides an administrative control plane and as-a-service operation of IBM cloud services using a Kubernetes (K8s) cluster.

IBM explained that the GA push now makes the platform available to all customers. It allows users to run their IBM Cloud service on-premises or in edge locations managed through a single pane of glass in the public cloud.

The first two services for IBM Cloud Satellite will be Cloud Pak for Data and OpenShift as a Service.

IBM’s not alone in looking to data as one of the first services to be offered on hybrid. Amazon Outposts offers RDS for MySQL and PostgreSQL; Azure Arc data services include SQL Managed Instance and PostgreSQL Hyperscale; while Google recently added BigQuery Omni to its Anthos software-defined hybrid cloud as part of a multi-cloud and edge play.

The rationale as to why data services are so elemental to hybrid cloud is that, for many organizations or use cases, data needs to stay local for reasons ranging from latency issues to data residency requirements. OpenShift as a service will provide a route for customers seeking to build their own private cloud K8s environments. IBM is announcing that this will also be early on the list.

As part of this collaboration, customers will be able to:

- Deploy applications across more than 180,000 connected enterprise locations on the Lumen network to provide a low latency experience

- Create cloud-enabled solutions at the edge that leverage application management and orchestration via IBM Cloud Satellite

- Build open, interoperable platforms that give customers greater deployment flexibility and more seamless access to cloud native services like AI, IoT and edge computing

IBM said it has more than 65 “ecosystem partners” building services to run in the Cloud Satellite environment. Partner include Cisco, Dell Technologies, and Intel. They intend to develop cloud services which can run across the multi-cloud and premises platform services include storage, networking, and server options.

“IBM is working with clients to leverage advanced technologies like edge computing and [artificial intelligence], enabling them to digitally transform with hybrid cloud while keeping data security at the forefront,” said Howard Boville, Head of IBM Hybrid Cloud Platform, in a statement. He added that “clients can securely gain the benefits of cloud services anywhere, from the core of the data center to the farthest reaches of the network.”

IBM highlighted three partners, among them Lumen Technologies and Portworx, that are both heavily leveraging 5G to deliver PaaS services for edge computing, and F5, which is developing vertical solutions for banking institutions.

IBM noted that Lumen Technologies (formerly CenturyLink) was using the hybrid cloud platform to deliver its Edge Compute service. That capability relies on Red Hat’s OpenShift that runs within Cloud Satellite to host the applications running close to Lumen’s edge locations. Lumen touts that it has approximately 450,000 route fiber miles in its network spread across more than 60 countries.

Lumen struck a similar deal earlier this year with VMware that will see both vendors “fast-track the design, development, and delivery of edge computing and more secure, work-from-anywhere solutions.”

Does anyone remember IBM’s Satellite Business Systems (SBS) of the late 1970s? It was a pioneer in delivering data services to businesses as a precursor of the Internet.

References:

https://www.ibm.com/cloud/satellite

https://developer.ibm.com/blogs/distributed-cloud-development-ibm-cloud-satellite/

https://www.zdnet.com/article/ibm-cloud-satellite-goes-ga/

https://www.sdxcentral.com/articles/news/ibm-cloud-satellite-boosted-to-ga-orbit/2021/03/

IBM Cloud Satellite: Build faster. Securely. Anywhere. Now generally available. To get started, visit: https://www.ibm.com/cloud/satellite.

For more information on how IBM is working with its ecosystem of partners, visit: www.ibm.com/cloud/blog/ibm-partner-ecosystem-and-cloud-satellite

For more information on IBM Cloud Pak for Data as a Service, visit:

https://www.ibm.com/blogs/journey-to-ai/ibm-cloud-pak-for-data-with-ibm-cloud-satellite

For more information on how IBM is helping developers build on IBM Cloud Satellite, visit:

https://developer.ibm.com/blogs/distributed-cloud-development-ibm-cloud-satellite

For more information on how IBM Cloud Satellite is supported by IBM Storage, visit: www.ibm.com/blogs/systems/improve-it-infrastructure-with-ibm-hybrid-cloud-storage-for-ibm-cloud-satellite

For more information on IBM Global Technology Services capabilities for IBM Cloud Satellite, visit: ibm.biz/PC_IaaS

To learn more about how Lumen has integrated Cloud Satellite across 180K global edge locations, visit: https://blog.lumen.com/speeding-innovation-at-the-edge-with-lumen-technologies-and-ibm-cloud-satellite

About IBM:

For further information visit: www.ibm.com/cloud/