Author: Alan Weissberger

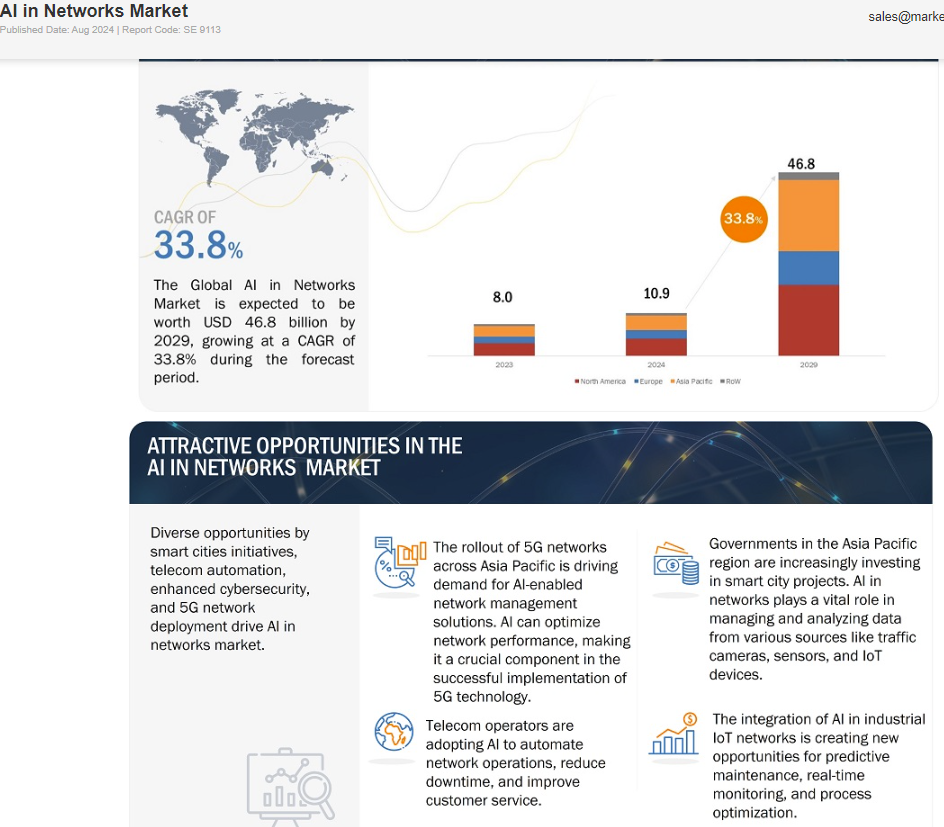

Markets and Markets: Global AI in Networks market worth $10.9 billion in 2024; projected to reach $46.8 billion by 2029

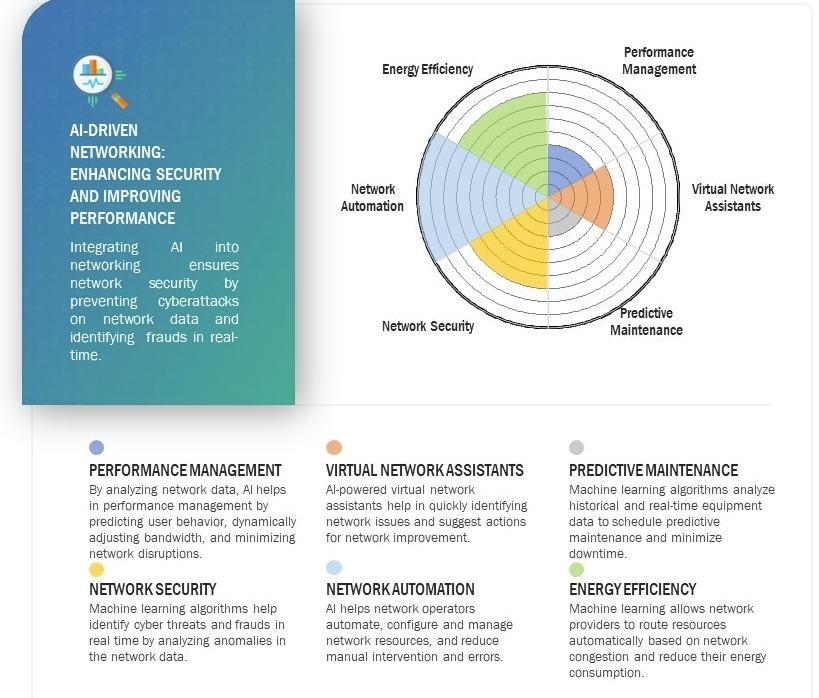

According to research firm Markets and Markets, the global AI in Networks market is expected to be valued at USD 10.9 billion in 2024 and is projected to reach USD 46.8 billion by 2029 and grow at a CAGR of 33.8% from 2024 to 2029. AI in networks market is experiencing high growth driven by increasing adoption of 5G technology, edge computing, IoT connected devices, and expansion of smart cities. Increasing deployment of 5G networks has led to the vast amount of network data, generated by high bandwidth application such as video streaming and online gaming, driving network operators to integrate AI driven solutions to manage network data and allocate resources to reduce network congestion. Network operators are also integrating AI driven solutions to automate network operations and predictive maintenance, to reduce human dependency and errors, leading to efficient network management.

Network operators invest heavily in developing AI-driven solutions to manage and optimize network traffic. AI in networks allows operators to efficiently perform network management tasks such as traffic routing, resource allocation, and network security. As the 5G technology advances, the demand for cybersecurity solutions will also rise, driving the AI in networks market.

Constraint: Data privacy and security concerns in AI in networks

Integration of artificial intelligence technology in the networking leads to various risks affiliated with collecting, storing, and transmitting network traffic data. AI driven network collect users and network operations data information, creating a high risk environment of privacy breaches, due to the rising cyberthreats. These cyberattacks may lead to unauthorized access to network and user data, disrupting network operations. Additionally, data generated by connected and Iot devices such as smartphones, smart home systems, surveillance system is collected by network, leads to concerns regarding unauthorized surveillance and cyberattacks.

Opportunity: Increasing prevalence of smart city initiatives

Rapid urbanization has led to the exapsnion of smart cities globally. Countries around the world are investing heavily towards smart infrastructure by integrating advanced technologies such as artificial intelligence (AI). For instance, smart city ecosystem consist of various sensors and connected and IoT devices, and to ensure efficient transmission and processing of data generated by these sensor and devices. AI driven network solutions play a vital role in collecting and processing of data, identifying anomalies and equipment failure based on present and historical data, helping network operator to schedule maintenance in advance and reduce downtime.

Challenge: Rapid change in the technology landscape

As the technology landscape evolves rapidly, AI presents a major challenge in the network market. As new technologies appear and current technology evolves, companies in the ecosystem must continuously invest in the research and development of changing market demand and advancements. Additionally, intense competition in the market and pressure to offer innovative solutions further restrict companies from maintaining market leadership. Companies’ negligence in identifying the technological shift can result in a decline in market share and revenue.

AI in networks market in North America will hold the highest market share during the forecast period.

The AI in networks market for North America is expected to hold the highest market share during the forecast period. This growth is attributed to the presence of leading AI and network technology companies in the region. These companies are investing heavily towards the advancement of technologies such as AI, 5G, edge computing, due to the high internet penetration rate in the region. The demand for high bandwidth network application such as video streaming and online gaming also on the rise, driving the investments and innovations towards AI driven solutions in network management.

******************************

References:

https://www.marketsandmarkets.com/Market-Reports/ai-in-networks-market-131514910.html

AI adoption to accelerate growth in the $215 billion Data Center market

Allied Market Research: Global AI in telecom market forecast to reach $38.8 by 2031 with CAGR of 41.4% (from 2022 to 2031)

Nvidia enters Data Center Ethernet market with its Spectrum-X networking platform

Will AI clusters be interconnected via Infiniband or Ethernet: NVIDIA doesn’t care, but Broadcom sure does!

Generative AI in telecom; ChatGPT as a manager? ChatGPT vs Google Search

Generative AI could put telecom jobs in jeopardy; compelling AI in telecom use cases

The case for and against AI in telecommunications; record quarter for AI venture funding and M&A deals

2021 U.S. Broadband Infrastructure law has been a colossal failure – who’s to blame?

The 2021 U.S. Investment and Jobs Act (IIJA), AKA the Bipartisan Infrastructure Law was signed into law November 15, 2021. It included $42.5 billion for states to expand broadband to “unserved,” mostly rural, communities. The White House said it would “Ensure every American has access to high-speed internet…. The Bipartisan Infrastructure Deal will deliver $65 billion to help ensure that every American has access to reliable high-speed internet through a historic investment in broadband infrastructure deployment. The legislation will also help lower prices for internet service and help close the digital divide, so that more Americans can afford internet access.”

In his speech at the Democratic National Convention, President Joe Biden trumpeted his broadband program in historic terms, calling it a national build-out “not unlike what Roosevelt did with electricity.” Democratic presidential nominee Kamala Harris helped create and promote the program as vice president, and on the campaign trail it could offer a way to show how the White House has delivered for rural Americans.

Yet almost three years later, ground hasn’t been broken on a single project! The Biden-Harris Administration recently said construction won’t start until next year at the earliest, meaning many projects won’t be up and running until the end of the decade. Who’s to blame?

- NTIA was expected to play a major role in the endeavor to connect every American to high-speed, affordable broadband. They intended to work closely with all stakeholders, including State and local governments, Tribal governments, industry, and community leaders, as well as across the Federal government to ensure that this bold investment is targeted to those who need it most. But they haven’t helped a bit!

- States must submit plans to the U.S. Commerce Department about how they’ll use the funds and their bidding process for providers. The Commerce Dept. has piled on mandates that are nowhere in the law and has rejected state plans that don’t advance progressive goals. Commerce hoped to spread the cash to small rural cooperatives, but the main beneficiaries will be large providers that can better manage the regulatory burden. Bigger businesses always win from bigger government.

- Commerce is all but refusing to fund anything other than fiber broadband, though satellite services like SpaceX’s Starlink and wireless carriers 5G FWA can expand coverage at lower cost. Extending 5G to rural communities costs a couple thousand dollars per connection. Building out fiber runs into the tens of thousands. Fiber networks will require more permits, which delay construction. But fiber will require more union labor to build. Commerce wants grant recipients to pay union-scale wages and not oppose union organizing.

- The Administration has also stipulated hiring preferences for “underrepresented” groups, including “aging individuals,” prisoners, racial, religious and ethnic minorities, “Indigenous and Native American persons,” “LGBTQI+ persons,” and “persons otherwise adversely affected by persistent poverty or inequality.”

- In Virginia, that leaves thousands of mostly rural residents stuck in a long-outdated version of the internet. According to the official state count, there are more than 100,000 homes and offices across Virginia with connection speeds slow enough to qualify for the $1.48 billion in funding. “People need to see it,” said Lynlee Thorne, a political director for Democratic campaign group Rural Ground Ggame, which helps lead campaigns for Virginia state seats. “It’s got to be a lot more concrete. We’re past the point of being able to earn people’s votes based on the status quo or just hope.”

- Last week, Cox Communications last week sued Rhode Island over the state’s plan to “build taxpayer-subsidized and duplicative high-speed broadband internet in affluent areas of Rhode Island like the Breakers Mansion in Newport and affluent areas of Westerly,” where Taylor Swift owns a $17 million vacation home. Cox says there are better ways to spend taxpayer dollars. According to the Federal Communications Commission, 99.97% of U.S. households already have access to high-speed internet.

References:

https://www.politico.com/news/2024/09/04/biden-broadband-program-swing-state-frustrations-00175845

Dell’Oro: Global telecom CAPEX declined 10% YoY in 1st half of 2024

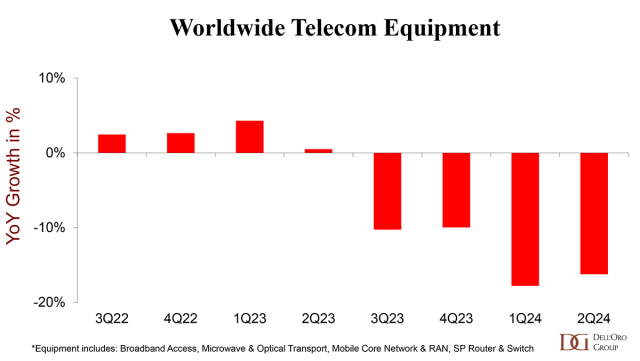

According to a recent report by Dell’Oro Group, telecom operators are now scaling back their investments in 5G and fixed broadband technologies. Of course, that’s nothing new as telco CAPEX has been declining for quite some time (see References below). Preliminary Dell’Oro findings show that the more challenging conditions that shaped the second half of 2023 extended into the first half of 2024.

Worldwide telecom capex, the sum of wireless and wireline/other telecom carrier investments, declined 10% year-over-year (YoY) in the first half of 2024, partly due to built-up inventory, weaker demand in China, India, and US, challenging 5G comparisons, excess capacity, and elevated uncertainty.

“The high-level message is clear. The flattish revenue trajectory and the difficulties with monetizing new technologies and opportunities are impacting the risk appetite and willingness to raise the capital intensity levels for extended periods,” said Stefan Pongratz, Vice President for RAN and Telecom Capex research at Dell’Oro Group. “In addition, the reduced gap between advanced and less advanced regions, when it comes to adopting new technologies, is impacting the investment intensity on the way up and down,” continued Pongratz.

Additional highlights from the September 2024 Telecom Capex report:

- Global carrier revenues are expected to increase at a 1 percent CAGR over the next 3 years.

- Worldwide telecom capex is projected to decline at a mid-single-digit rate in 2024 and at a negative 2 percent CAGR by 2026.

- The mix between wireless and wireline remains largely unchanged, reflecting challenging times still ahead for wireless. Wireless-related capex will decline at a 3 percent CAGR by 2026.

- Capital intensity ratios are modeled to approach 15 percent by 2026, down from 17 percent in 2023.

In a previous Dell’Oro report last month, telecom equipment revenues fell by 17% worldwide during the first half of the year. Dell’Oro described that as ‘abysmal results’ and again blamed excess inventory, weaker demand in China, ‘challenging 5G comparisons’, and elevated uncertainty.

In a previous Dell’Oro report last month, telecom equipment revenues fell by 17% worldwide during the first half of the year. Dell’Oro described that as ‘abysmal results’ and again blamed excess inventory, weaker demand in China, ‘challenging 5G comparisons’, and elevated uncertainty.

The Dell’Oro Group Telecom Capex Report provides in-depth coverage of around 50 telecom operators, highlighting carrier revenue, capital expenditure, and capital intensity trends. The report provides actual and 3-year forecast details by carrier, by region by country (United States, Canada, China, India, Japan, and South Korea), and by technology (wireless/wireline). To purchase this report, please contact by email at [email protected].

References:

Telecom Capex Down 10 Percent in 1H24, According to Dell’Oro Group

Dell’Oro: Abysmal revenue results continue: Ethernet Campus Switch and Worldwide Telecom Equipment + Telco Convergence Moves to Counter Cable Broadband

Analysts: Telco CAPEX crash looks to continue: mobile core network, RAN, and optical all expected to decline

Analysys Mason’s gloomy CAPEX forecast: “there will not be a cyclical recovery”

China Mobile & China Unicom increase revenues and profits in 2023, but will slash CAPEX in 2024

Dell’Oro: RAN market still declining with Huawei, Ericsson, Nokia, ZTE and Samsung top vendors

Highlights of Dell’Oro’s 5-year RAN forecast

Dell’Oro: 2023 global telecom equipment revenues declined 5% YoY; Huawei increases its #1 position

Dell’Oro & Omdia: Global RAN market declined in 2023 and again in 2024

Global 5G Market Snapshot; Dell’Oro and GSA Updates on 5G SA networks and devices

FCC approves EchoStar/Dish request to extend timeline for its 5G buildout

On September 20th, the U.S. FCC has granted EchoStar’s request to extend the deadline for portions of its 5G network buildout into 2026 in exchange for several commitments, including a low-cost offering and a pledge to accelerate build-outs in certain markets.

EchoStar’s request to the FCC was sent to the commission on September 18, 2024. The licenses subject to the requested waiver include EchoStar’s AWS-4, Lower 700MHz E Block, 600MHz, AWS-3, AWS H Block and AWS-3 licenses. Depending on the spectrum, EchoStar generally is asking to move the milestones to December 2026. EchoStar also wants final construction milestones moved from December 14, 2026, to June 14, 2028. The request seemed to make clear that its 2025 deadlines were in jeopardy even if the company could resolve its near-term debt obligations (more below).

Benefits of the FCC’s new framework include:

- Enhancing EchoStar’s Network Build. By the end of this year, EchoStar’s Boost Mobile Network will cover 80% of the U.S. population, an additional 30 million more Americans than EchoStar’s 2023 obligation to cover 70% of the population. EchoStar will also accelerate and expand its final buildout milestones in more than 500 license areas on this same timeline. Because of EchoStar’s wholesale partnerships with AT&T and T-Mobile, consumers in areas where EchoStar has not yet deployed will still be able to sign up for the industry-leading coverage EchoStar’s wireless service – Boost Mobile – offers.

- Requiring a Low-Cost Offering. EchoStar will make a low-cost wireless plan and 5G device available to consumers nationwide, regardless of whether they live in an area where EchoStar has built out its Boost Mobile Network or relies on roaming partners to provide service.

- Enabling a More Efficient Build. The targeted extensions adopted by the FCC will provide a construction timeline that more closely aligns EchoStar’s deployment with its 3.45 GHz spectrum licenses, reducing the resources necessary to install infrastructure twice at each cell site/tower. Small wireless carriers and Tribal nations will also be able to lease EchoStar spectrum licenses in extension areas where the company has not yet deployed.

Blair Levin, a policy analyst at New Street Research and a former FCC official, remarked at the speed at which the FCC approved the petition:

“We can’t think of a faster one. And it is a real tribute to the brilliant strategy and execution by the DISH public policy team,” he explained. “The speed at which the FCC acted – albeit likely with significant pre-negotiation – is an indication that the FCC leadership is willing to act quickly and decisively to increase the odds of DISH succeeding in building out a fourth national facilities-based competitor.” Levin believes a vote is “highly unlikely” if there are three Commissioners willing to push this forward.

“The Bureau has not yet issued the order but as far as we can tell, they simply approved the order. The speed at which the Bureau acted suggests to us that this was pre-negotiated, meaning that the Bureau order is unlikely to make changes,” he added noting that the FCC action could face a lawsuit, but does not expect anyone willing to spend the political capital to pursue one.

EchoStar/Dish hope to be able to offer a nationwide wireless service due to its roaming deals with AT&T and T-Mobile, but will also be able to sign up customers with competitive pricing and plans enabled by its “enhanced presence” in the accelerated buildout markets. “This pro-consumer outcome is in addition to the public interest commitments EchoStar is making in connection with its extension request,” EchoStar said in their FCC petition.

………………………………………………………………………………………………………………………………………….

EchoStar is the parent company of Dish Network which is building a 5G Open RAN based network. The goal is to establish the company as a fourth national carrier after AT&T, T-Mobile and Verizon.

EchoStar pledged to fulfill a range of commitments, including a plan to cover more than 80% of the US population with its open RAN network at the end of 2024. The company, which has MVNO partnerships with AT&T and T-Mobile, said it will also accelerate and expand its final buildout milestones in more than 500 license areas on that same timeline.

EchoStar said it’s also prepared to introduce a nationwide “affordable” 5G plan that will offer at least 30 gigabytes of data per month for no more than $25 per month for both prepaid and postpaid customers.

EchoStar also pledged to deploy 24,000 towers by June 14, 2025 – about 9,000 more than its 15,000 2023 tower obligation, and to offer to load at least 75% of new customers with compatible devices on its MVNO network in the aforementioned accelerated markets.

…………………………………………………………………………………………………………………………………………..

On Monday, EchoStar disclosed in an 8-K filing that its negotiations with certain holders of senior debt securities had concluded without reaching an agreement regarding potential transactions, including new secured notes with an extended maturity date. “The Company remains engaged with various other parties regarding possible financing transactions,” EchoStar said in the filing.

“The failure to resolve the lawsuit limits Dish’s capital raising options, but they still have options. We believe the most likely path to raising capital will be notes secured by the AWS-3 licenses,” New Street Research analyst Jonathan Chaplin said in a note about the new filing.

About EchoStar:

EchoStar Corporation (Nasdaq: SATS) is a premier provider of technology, networking services, television entertainment and connectivity, offering consumer, enterprise, operator, and government solutions worldwide under its EchoStar®, Boost Mobile®, Sling TV, DISH TV, Hughes®, HughesNet®, HughesON™ and JUPITER™ brands. In Europe, EchoStar operates under its EchoStar Mobile Limited subsidiary and in Australia, the company operates as EchoStar Global Australia. For more information, visit www.echostar.com and follow EchoStar on X (Twitter) and LinkedIn.

References:

https://www.fcc.gov/ecfs/document/1091867842711/1

https://www.lightreading.com/regulatory-politics/fcc-greenlights-echostar-s-revised-5g-buildout-plan

https://www.lightreading.com/regulatory-politics/dish-asks-fcc-for-more-time-for-5g-buildout

https://about.dish.com/2024-02-22-DISH-Expands-VoNR-Coverage-to-Over-200-Million-People

Dell’Oro: Abysmal revenue results continue: Ethernet Campus Switch and Worldwide Telecom Equipment + Telco Convergence Moves to Counter Cable Broadband

Dell’Oro Group recently reported that:

1. 2Q 2024 worldwide Ethernet Campus Switch revenues contracted year-over-year for the third quarter in a row. Ethernet campus switch sales hit an all-time high in 2Q 2023 and a year later, vendors are suffering in comparison.

“We expect another year-over-year contraction in sales next quarter, in 3Q 2024,” said Siân Morgan, Research Director at Dell’Oro Group. “However, the outlook is improving, and the Ethernet Campus Switch market is expected to return to growth in 4Q 2024.”

“While the economy in China remains soft, Huawei grew year-over-year campus switch revenues across the rest of Asia Pacific and CALA. Over half of Huawei’s campus switch sales were generated outside China,” added Morgan.

Additional highlights from the 2Q 2024 Ethernet Switch–Campus Report:

- The contraction in Ethernet campus switch sales was broad-based across both modular and fixed form factors, all verticals and regions.

- Sales to North America fell the most of any macro-economic region.

- Cisco grew campus switch revenues on a quarter-over-quarter basis, for the first time in a year.

The Dell’Oro Group’s Ethernet Switch–Campus Quarterly Report offers a detailed view of Ethernet switches built and optimized for deployment outside the data center, to connect users and things to the Local Area Networks. The report contains in-depth market and vendor-level information on manufacturers’ revenue, ports shipped, and average selling prices for both Modular and Fixed, and Fixed Managed and Unmanaged Ethernet Switches (100 Mbps, 1/2.5/5/10/25/40/50/100/400 Gbps), Power-over-Ethernet, plus regional breakouts as well as split by customer size (Enterprise vs. SMB) and vertical segments. To purchase these reports, please contact us by email at [email protected].

……………………………………………………………………………………………………….

2. Preliminary findings indicate that worldwide telecom equipment revenues across the six telecom programs tracked at Dell’Oro Group—Broadband Access, Microwave & Optical Transport, Mobile Core Network (MCN), Radio Access Network (RAN), and SP Router & Switch—declined 16% year-over-year (Y/Y) in 2Q24, recording a fourth consecutive quarter of double-digit contractions. Helping to explain the abysmal results are excess inventory, weaker demand in China, challenging 5G comparisons, and elevated uncertainty.

Regional output deceleration was broad-based in the second quarter of 2024, reflecting slower revenue growth on a Y/Y basis in all regions, including North America, EMEA, Asia Pacific, and CALA (Caribbean and Latin America). Varied momentum in activity in the first half was particularly significant in China – the total telecom equipment market in China stumbled in the second quarter, declining 17% Y/Y.

The downward pressure was not confined to a specific technology, and initial readings show that all six telecom programs declined in the second quarter. In addition to the wireless programs (RAN and MCN), which are still impacted by slower 5G deployments, spending on Service Provider Routers fell by a third in 2Q24.

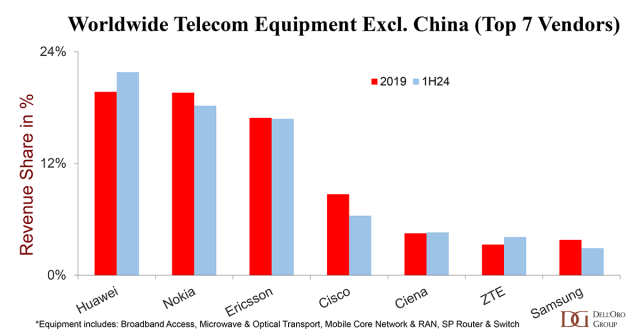

Supplier rankings were mostly unchanged. The top 7 suppliers in 1H24 accounted for 80% of the worldwide telecom equipment market and included Huawei, Nokia, Ericsson, ZTE, Cisco, Ciena, and Samsung. Huawei and ZTE combined gained nearly 3 percentage points of share between 2023 and 1H24.

Supplier positions differ slightly when we exclude the Chinese market. Despite the ongoing efforts by the U.S. government to curb Huawei’s rise, Huawei is still well positioned in the broader telecom equipment market, excluding China, which is up roughly two percentage points relative to 2019 levels.

- Even with the second half of 2024 expected to account for 54% of full-year revenues, market conditions are expected to remain challenging in 2024.

- The Dell’Oro analyst team collectively forecasts global telecom equipment revenues to contract 8 to 10% in 2024, even worse than the 4% decline in 2023.

3. U.S. Telcos Betting on Convergence and Scale To End Cable’s Broadband Reign

U.S. telcos have been very active the past two weeks with deals and partnerships.

- Verizon announced a $20B deal to acquire Frontier Communications and push the combined entity to a fiber footprint of 25 million homes and a fixed wireless footprint of approximately 60 million homes.

- AT&T announced partnerships with four open access network providers to help it expand the reach of its fiber services outside its existing wireline footprint. AT&T will serve as an ISP in these markets, delivering both residential and enterprise services via these partnerships. AT&T is on track to pass a minimum of 30 million homes with fiber by 2025 in its own footprint, as well as an additional 1.5 million homes through its Gigapower joint venture with BlackRock.

- AT&T has also quietly increased the availability of its Internet Air FWA (Fixed Wireless Access) services to over 130 markets, as It potentially positions the service to move beyond just a means of capturing existing DSL subscribers.

These deals follow on the heels of T-Mobile’s proposed acquisition of Lumos Networks, which is slated to pass 3.5 million homes with fiber by the end of 2028. Under the terms of the deal, Lumos will transition to a wholesale model with T-Mobile as the anchor ISP. This is exactly the type of arrangement T-Mobile has established with some of its other infrastructure partners. However, with its partial ownership of Lumos, T-Mobile can presumably generate better returns and healthier margins from its broadband service offerings. The joint venture also is consistent with T-Mobile’s goal of expanding its market presence and footprint without expending a significant amount of capital. In fact, if you take the $1.4B that T-Mobile will ultimately invest in Lumos as it increases its homes passed from 320K to 3.5M by the end of 2028, T-Mobile’s cost per home passed ends up being somewhat less than $500.

That $500 per home passed figure could be even lower should Lumos continue to secure additional American Rescue Plan Act (ARPA) Capital Project Fund grants as well as a portion of the $3.6 B in aggregate BEAD (Broadband Equity, Access, and Development) funding across North Carolina, South Carolina, and Virginia.

The primary reason for T-Mobile’s push into both direct fiber network ownership and partnerships with open access fiber providers is that the operator has over 1 million customers on a waiting list for its fixed wireless service. These customers can’t be served because they are in markets where T-Mobile does not have enough 5G capacity to serve them. As T-Mobile expands the reach of its fiber offering, it can not only provide service to these customers but also existing FWA subscribers. Once an FWA subscriber switches to T-Mobile Fiber, that opens the spectrum for additional FWA subscribers.

US telcos are moving quickly to expand the reach of their fiber, fixed wireless, and ISP services to complement their nationwide mobile networks because they smell blood among the largest cable operators. Telcos are disrupting the broadband market faster and more efficiently right now—a disruption that could very well be amplified by Federal and State subsidies.

With the rollout of 5G networks having had little impact on the profitability of mobile services, fixed wireless has emerged as the most successful use case for mobile network operators (MNOs) can monetize their excess 5G capacity. FWA’s timing couldn’t have been better, with inflation having increased from 2021 on, pushing subscribers to seek out more affordable—but still high quality—broadband service offerings. FWA hit the market providing a powerful combination of affordability, speed, and availability.

The success of FWA combined with overall fiber network expansions has given telcos a potent tool for not only the convergence of mobile and fixed broadband services but also the emergence of these services being offered on an almost nationwide basis. It’s pretty simple math. If you can offer a product or service to a larger number of end customers, the higher the likelihood of continued net subscriber additions, all other things being equal.

Even in markets where there is overlap between fixed wireless and that MNO’s own (or marketed) fiber broadband services, there isn’t really a danger of cannibalization, because the two services will very likely address very different subscribers. As the telcos’ ARPU (average revenue per unit) results have shown, subscribers are willing to pay more for fiber-based connectivity. In 2Q24, for example, AT&T announced that its fiber broadband ARPU is $69 and that the mix shift of its subscribers to fiber has pushed overall broadband ARPU up to $66.17, representing a 6% increase from 2Q23.

Meanwhile, in the second quarter, T-Mobile reported an ARPA figure of $142.54, which was up from $138.94 in 2Q23. Partially fueling that increase was an increase in the number of customers per account, due largely to the adoption of FWA services. Remember, T-Mobile prices and treats its FWA offering as an additional line of service, making it very simple to add to an existing T-Mobile account.

With a starting price point of $50 and typical download speeds ranging from 33-182 Mbps and upload speeds of 6-23 Mbps, T-Mobile is clearly targeting the low-mid cable broadband tiers—and having a great deal of success in converting those subscribers.

Going forward, the 1-2 punch of FWA and fiber will allow the largest telcos to have substantially larger broadband footprints than their cable competitors. Combine that with growing ISP relationships with open access providers and these telcos can expand their footprint and potential customer base further. And by expanding further, we don’t just mean total number of homes passed, but also businesses, enterprises, MDUs (multi-dwelling units), and data centers. Fiber footprint is as much about total route miles as it is about total passings. And those total route miles are, once again, increasing in value, after a prolonged slump.

For cable operators to successfully respond, consolidation likely has to be back on the table. The name of the game in the US right now is how to expand the addressable market of subscribers or risk being limited to existing geographic serving areas. Beyond that, continuing to focus on the aggressive bundling of converged services, which certainly has paid dividends in the form of new mobile subscribers.

Beyond that, being able to get to market quickly in new serving areas will be critical. In this time of frenzied buildouts and expansions, the importance of the first mover advantage can not be overstated.

The push and pull of broadband and wireless subscribers isn’t expected to slow down anytime soon. Certainly, with inflation continuing to put pressure on household budgets, consumers are going to be focused on keeping their communications costs low and looking for value wherever they can find it. That means we are returning to an environment where subscribers take advantage of introductory pricing on services only to switch providers to extend that introductory pricing once the initial offer expires. That shifting and its expected downward pressure on residential ARPU will likely be countered by increasing ARPUs at some providers as they move existing DSL customers to fiber or, in the case of cable operators, move customers to multi-gigabit tiers.

The US broadband market is definitely in for a wild ride over the next few years as the competitive landscape changes across many markets. The net result is certain to be shifts in market share and ebbs and flows in net subscriber additions depending on consumer sentiment. One thing that will remain constant is that value and reliability will remain key components of any subscription decision. The providers that deliver on that consistently will ultimately be the winners.

References:

Ethernet Campus Switch Revenues Plunge by 30 Percent in 2Q 2024, According to Dell’Oro Group

US Telcos Betting on Convergence and Scale To End Cable’s Broadband Reign

Dell’Oro: Private RAN revenue declines slightly, but still doing relatively better than public RAN and WLAN markets

Dell’Oro: Campus Ethernet Switch Revenues dropped 23% YoY in 1Q-2024

Dell’Oro: RAN revenues declined sharply in 2023 and will remain challenging in 2024; top 8 RAN vendors own the market

Dell’Oro: Broadband Equipment Spending to exceed $120B from 2022 to 2027

Dell’Oro: RAN Market to Decline 1% CAGR; Mobile Core Network growth reduced to 1% CAGR

Dell’Oro: Optical Transport market to hit $17B by 2027; Lumen Technologies 400G wavelength market

Dell’Oro: Private RAN revenue declines slightly, but still doing relatively better than public RAN and WLAN markets

Dell’Oro Group reports that Private Wireless Radio Access Network (RAN) revenue growth slowed slightly in the second quarter on a year-over-year basis relative to the ~40 percent increase in 2023. Still, the tapering is in line with expectations and private wireless is performing significantly better on a relative basis than both public RAN and enterprise WLAN. [However, it’s a much smaller market.]

“With public MBB investments slowing, the expectations with new growth opportunities such as Fixed Wireless Access and private wireless are rising,” said Stefan Pongratz, Vice President at Dell’Oro Group. “The results in the quarter and the trends over the past year validate this message that we have communicated now for some time, namely that the enterprise is a very large and mostly untapped opportunity. The market will continue to grow faster than both public RAN and enterprise WLAN, but because of the lower starting point, it will take some time before enterprise RAN revenues are large enough to stabilize public MBB swings,” continued Pongratz.

Additional highlights from the September 2024 Private Wireless Report:

- Contract activity is slowing but the quality of the contracts is improving and increasingly includes larger, multi-site, and even multi-country agreements.

- Regional activity is mostly stable. The three largest regions in 1H24 from a revenue perspective include China, North America, and EMEA.

- Vendor rankings did not change in 1H24. The evolving scope of private wireless taken together with the fact that the $20 B+ enterprise RAN opportunity remains largely untapped is spurring interest from a broad array of participants across the ecosystem. Still, the traditional RAN suppliers are currently well-positioned in this initial phase.

- Top 3 Private Wireless RAN suppliers in 1H24 are Huawei, Nokia, and Ericsson.

- Top 3 Private Wireless RAN suppliers in 1H24 excluding China are Nokia, Ericsson, and Samsung.

- Projections are mostly unchanged. Private wireless RAN revenues are projected to grow at a 21 percent CAGR over the next five years, while public RAN revenues are set to decline at a 3 percent CAGR over the same time period.

Dell’Oro Group’s Private Wireless Advanced Research Report includes both quarterly vendors share data and a 5-year forecast for Private Wireless RAN by RF Output Power, technology, spectrum, and region. To purchase this report, please contact us at [email protected].

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, security, enterprise networks, and data center markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions. For more information, contact Dell’Oro Group at +1.650.622.9400 or visit https://www.delloro.com.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Ericsson and Nokia – Private Wireless Network Initiatives:

- Last week, Ericsson shared details of its enterprise 5G strategy, formulated after its 2020 Cradlepoint acquisition which provides both private 5G and neutral host solutions. “Ericsson’s strategic and comprehensive approach to evolving its private networking portfolio is addressing the growing demand for secure, high-performance connectivity in enterprises,” the vendor quoted Pablo Tomasi, Principal Analyst for Private Networks and Enterprise 5G at Omdia, as saying in its strategy announcement. “Ericsson’s ability to meet customers where they are in their 5G journey with a unified experience will be critical in helping the market scale and enabling enterprises leveraging 5G to transform in a meaningful way,” Tomasi added.

- Nokia has made myriad private networking deal announcements in the past couple of years and recently revealed the results of a market study it commissioned that paints the sector in a very positive light. Early adopters have been scaling up deployments, adding new locations for example, and the vast majority of those surveyed – 93%, to be exact – claimed to have generated a return on investment within a year; almost a quarter did so in just one month. That’s a strong message and one designed to help drive the market forwards.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

References:

Private Wireless RAN Revenues up 24 percent in 2Q 2024, According to Dell’Oro Group

https://www.telecoms.com/telecoms-infrastructure/private-ran-revenues-continue-to-grow-amid-vendor-push

Dell’Oro: RAN market still declining with Huawei, Ericsson, Nokia, ZTE and Samsung top vendors

Highlights of Dell’Oro’s 5-year RAN forecast

Dell’Oro: 2023 global telecom equipment revenues declined 5% YoY; Huawei increases its #1 position

Dell’Oro & Omdia: Global RAN market declined in 2023 and again in 2024

Dell’Oro: Private 5G ecosystem is evolving; vRAN gaining momentum; skepticism increasing

HPE Aruba Launches “Cloud Native” Private 5G Network with 4G/5G Small Cell Radios

SNS Telecom & IT: Private 5G Network market annual spending will be $3.5 Billion by 2027

Ericsson and Vodafone enable Irish rugby team to use Private 5G SA network for 2023 Rugby World Cup

Wipro and Cisco Launch Managed Private 5G Network-as-a-Service Solution

Japan to support telecom infrastructure in South Pacific using Open RAN technology

Japan’s government and private sector will offer support for telecommunications infrastructure in Pacific island countries, starting with a data center and telecom project in Palau, in an effort to improve the security of vital networks connecting Asia and North America. The initiative will be led by Japan’s Ministry of Internal Affairs and Communications and is expected to include telecom company NTT Group, internet service provider Internet Initiative Japan and other companies. It aims to increase Japan’s participation in the South Pacific, a region crisscrossed with undersea communications cables linking East Asia, the U.S., Australia and Southeast Asia. Funding will come from the ministry’s international cooperation budget. Several billion yen (1 billion yen equals $7.1 million) in public-private investment is expected to be mobilized over the first two years.

The infrastructure improvements will use Open Radio Access network (RAN) technology, which Japan has sought to promote as a low-cost way of building wireless networks from components made by different manufacturers.

Japan, the U.S., and Australia — which, along with India, make up the security dialogue known as the Quad — all support improving communications security in Pacific island countries. These island countries are reliant on equipment from Chinese telecom company Huawei Technologies for their land-based networks. The U.S. and others say Huawei has ties to the Chinese military and poses a security risk. Western officials have raised concerns about the potential for eavesdropping on communications and other activities. Huawei denies such accusations.

Quad members have agreed to support the modernization of Palau’s telecommunications infrastructure. Japan’s communications ministry will start putting this initiative to work as early as fiscal 2025, which begins in April. It will then seek to expand aid in fiscal 2026 to other countries in the region. Tuvalu and the Marshall Islands — two of the dwindling number of countries to maintain formal diplomatic relations with Taiwan — are likely to be candidates for such support. The effort will also seek to train cybersecurity personnel. Island countries with understaffed cybersecurity capabilities are seen as a potential vulnerability that can be exploited to launch attacks against Japan, experts say.

Tuvalu-an island country roughly halfway between Australia and Hawaii-is expected to be a candidate to receive Japanese support for telecommunications infrastructure. © Reuters

……………………………………………………………………………………………………………………………………………………………………………………………………..

China has worked to extend its influence in the South Pacific. In recent years, the Solomon Islands, Kiribati and Nauru have all cut diplomatic ties with Taiwan in favor of relations with Beijing. The Solomon Islands also formed a security agreement with China. Including Palau, only three countries in the region still maintain diplomatic relations with Taiwan.

Telecommunications infrastructure is becoming increasingly important for island countries in their own right.

“A stable network connecting a country with the rest of the world is essential for receiving remittances from migrant workers. Better telecommunications infrastructure is of great significance in improving ties between countries,” said Motohiro Tsuchiya, a professor at the Keio University Graduate School of Media and Governance in Japan.

……………………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://market.us/report/open-ran-market/

https://www.o-ran.org/otics/japan-otic

https://www.lowyinstitute.org/the-interpreter/japan-s-5g-ambitions-quad

NTT advert in WSJ: Why O-RAN Will Change Everything; AT&T selects Ericsson for its O-RAN

NTT DOCOMO OREX brand offers a pre-integrated solution for Open RAN

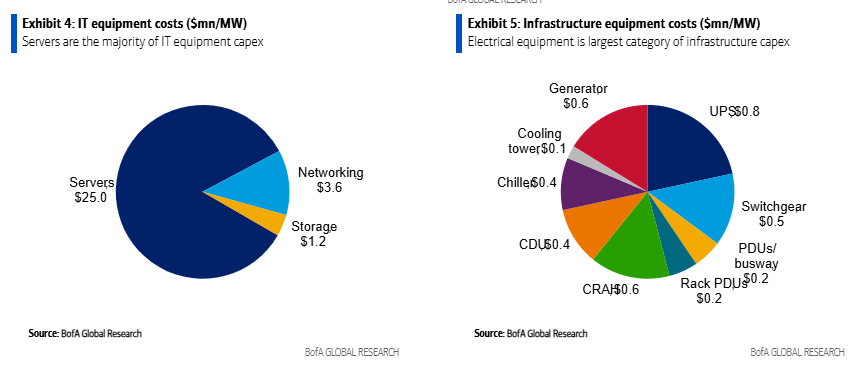

AI adoption to accelerate growth in the $215 billion Data Center market

Market Overview:

Data Centers are a $215bn global market that grew 18% annually between 2018-2023. AI adoption is expected to accelerate data center growth as AI chips require 3-4x more electrical power versus traditional central processing units (CPUs).

AI adoption is poised to accelerate this growth meaningfully over coming years. BofA‘s US Semis analyst, Vivek Arya, forecasts the AI chip market to reach ~$200bn in 2027, up from $44bn in 2023. This has positive implications for the broader data center industry.

AI workloads are bandwidth-intensive, connecting hundreds of processors with gigabits of throughput. As these AI models grow, the number of GPUs required to process them grows, requiring larger networks to interconnect the GPUs. See Network Equipment market below.

The electrical and thermal equipment within a data center is sized for maximum load to ensure reliability and uptime. For electrical and thermal equipment manufacturers, AI adoption drives faster growth in data center power loads. AI chips require 3-4x more electrical power versus traditional CPUs (Central Processing Units).

BofA estimates data center capex was $215bn globally in 2023. The majority of this spend is for compute servers, networking and storage ($160bn) with data center infrastructure being an important, but smaller, piece ($55bn). For perspective, data center capex represented ~1% of global fixed capital formation, which includes all private & public sector spending on equipment and structures.

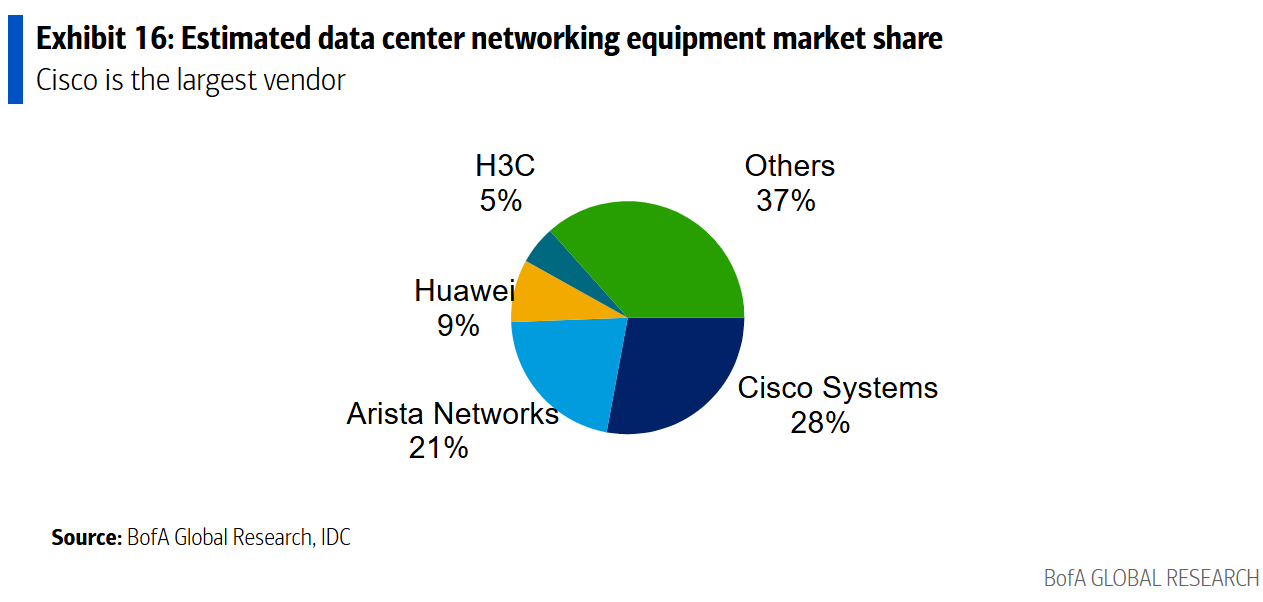

Networking Equipment Market:

BofA estimates a $20bn market size for Data Center networking equipment. Cisco is the market share leader, with an estimated 28% market share.

- Ethernet switches which communicate within the data center via local area networks. Typically, each rack would have a networking switch.

- Routers handle traffic between buildings, typically using internet protocol (IP). Some cloud service providers use “white box“ networking switches (e.g., manufactured by third parties, such as Taiwanese ODMs, to their specifications).

Data center speeds are in a state of constant growth. The industry has moved from 40G speeds to 100G speeds, and those are quickly giving way to 400G speeds. Yet even 400G speeds won’t be fast enough to support some emerging applications which may require 800G and 1.6TB data center speeds.

…………………………………………………………………………………………………………………………………….

Data Centers are also a bright spot for the construction industry. BofA notes that construction spending for data centers is approaching $30bn (vs $2bn in 2014) and accounts for nearly 21% of data center capex. At 4% of private construction spending (vs 2% five years ago), the data center category has surpassed retail, and could be a partial offset in a construction downturn.

Source: BofA Global Research

………………………………………………………………………………………………………………………..

References:

https://www.belden.com/blogs/smart-building/faster-data-center-speeds-depend-on-fiber-innovation#

Proposed solutions to high energy consumption of Generative AI LLMs: optimized hardware, new algorithms, green data centers

Nvidia enters Data Center Ethernet market with its Spectrum-X networking platform

Co-Packaged Optics to play an important role in data center switches

EdgeCore Digital Infrastructure and Zayo bring fiber connectivity to Santa Clara data center

Deutsche Telekom with AWS and VMware demonstrate a global enterprise network for seamless connectivity across geographically distributed data centers

New venture to sell Network Application Programming Interfaces (APIs) on a global scale

Overview:

Some of the world’s largest telecom operators, including América Móvil, AT&T, Bharti Airtel, Deutsche Telekom, Orange, Reliance Jio, Singtel, Telefonica, Telstra, T-Mobile, Verizon and Vodafone, together with network gear maker Ericsson (the largest shareholder) are announcing a new venture to combine and sell network Application Programming Interfaces (APIs) on a global scale to spur innovation in digital services. Network APIs are the way to easily access, use and pay for network capabilities. The venture will drive implementation and access to common APIs from multiple telecom service providers to a broader ecosystem of developer platforms. All the APIs on offer will be based on CAMARA – the open source API project led by the GSMA and the Linux Foundation.

Modern mobile networks have advanced and intelligent capabilities, which have historically been inaccessible to developers. Additionally, it has been impractical for developers to integrate the different capabilities of hundreds of individual telecom operators. The newly formed company will combine network APIs globally, with a vision that new applications will work anywhere and on any network, making it easier and quicker for developers to innovate.

Easily accessible advanced network capabilities will open up the next frontier in app development and empower developers to create new use cases across many sectors. These could include anti-fraud verification for financial transactions and the ability to check device status so streaming providers can dynamically adjust video quality.

The newly formed company will provide network APIs to a broad ecosystem of developer platforms, including hyperscalers (HCPs), Communications Platform as a Service (CPaaS) providers, System Integrators (SIs) and Independent Software Vendors (ISVs), based on existing industry-wide CAMARA APIs (the open-source project driven by the GSMA and the Linux Foundation). Vonage and Google Cloud will partner with the new company, providing access to their ecosystems of millions of developers as well as their partners. The new venture shareholders will bring funding and important assets, including Ericsson’s platform and network expertise, global telecom operator relationships, knowledge of the developer community and each telecom operator’s network APIs, expertise and marketing.

Ericsson-owned Vonage and Google Cloud have already agreed to partner with the new venture, providing access to their respective ecosystems of millions of developers as well as their partners.

“We have a common concern that we’ve made it difficult for developers to program on wireless networks,” said Niklas Heuveldop, CEO of Vonage, stressing that this initiative is all about removing any friction and roadblocks that may be preventing developers taking full advantage of the programmable networks opportunity. He added that, for Vonage, this means a smaller piece of a bigger network API pie.

Closing of the transaction is expected early 2025, subject to regulatory approvals and other customary conditions. Upon closing, Ericsson will hold 50% of the equity in the venture while the telecom providers will hold 50% in total. Built on a deep understanding of developer and enterprise needs and in keeping with the industry-body GSMA Open Gateway principles, the new venture’s platform and partner ecosystem will remain open and non-discriminatory to maximize value creation across the industry.

Comment and Analysis:

Much has already been made of the industry’s decision to open up and (attempt) to monetize network APIs. Optimistic estimates, like the one proffered by McKinsey, claim that network APIs represent a $300 billion opportunity for telcos between now and the end of the decade. However, some like Kearney, have warned that all will be for naught without proper industry coordination and collaboration to drive software developer uptake.

“Today’s announcement is an important step in that direction by addressing one of the major challenges for developers seeking to engage with mobile operators – sector fragmentation,” said Kester Mann, director of consumer and connectivity at CCS Insight. “In the past, the telecom industry – with many competing players each deploying different strategies for their specific regions – has struggled to present a united and coherent front.” Despite their dubious track record, Mann reckons this particular venture stands a better chance of success than most, thanks to the urgent need for operators to earn a return on 5G, and due to the involvement of major technology partners in the form of Google and Ericsson. “There should be fresh optimism that the new company unveiled will enjoy more success than previous failed ventures,” he added.

While open network APIs will work on compatible hardware from any vendor – whether it’s Nokia or Ericsson or Huawei – this new venture represents an opportunity for Ericsson to play a central role in the emerging ecosystem.

Quotes from the partners:

América Móvil

Daniel Hajj, Chief Executive Officer, AMX: “We are very excited to join Ericsson and other key players in our industry in this innovative global platform initiative that will benefit the digital ecosystem as a whole. New API solutions will establish exciting value-added offerings to our customers on the top of our networks’ infrastructure.”

AT&T

Jeremy Legg, Chief Technology Officer, AT&T: “At AT&T, we’ve been creating API tools to empower developers for well over a decade. Now, with a broad-based, interoperable API platform, we’re giving innovators a new global toolbox where the world’s best app developers can create exciting user experiences at scale. This high-performance mobile ecosystem will usher in a new era of greater possibility for customers and mobile users around the world.”

Bharti Airtel

Gopal Vittal, Managing Director and CEO, Bharti Airtel: “Today marks a defining moment as the industry comes together to form a unified platform that will allow more developers and businesses to utilize our networks and explore API opportunities through open gateway principles. This move will enhance network monetization opportunities. Airtel is delighted to partner in this initiative that will help enable the telecom sector to drive growth and innovation across the ecosystem.”

Deutsche Telekom

Tim Höttges, CEO of Deutsche Telekom: “The new company accelerates our leading work with MagentaBusiness APIs to expose our network capabilities for customers and developers. We believe that this company will open up new monetization opportunities for the industry. We encourage and look forward to more telecom operators joining us to expand and develop this ecosystem.”

Ericsson

Börje Ekholm, President and CEO, Ericsson: “Today is a defining moment for the industry and milestone in our strategy to open up the network for increased monetization opportunities. A global platform built on Ericsson’s deep technical capabilities and with a comprehensive ecosystem, that provides millions of developers with a single connection, will enable the telecom industry to invest deeper into the network API opportunity, driving growth and innovation for everyone.”

Orange

Christel Heydemann, Chief Executive Officer, Orange: “This is a critical first step in our innovation journey to fully harness the power of our networks at scale, providing secure access to new on-demand network services and advanced network capabilities. By delivering a common and simple set of network APIs for developers globally, we can unleash this network value for businesses, large and small. This is a definitive gamechanger for businesses, opening up the possibility of a new wave of digital services.”

Reliance Jio

Mathew Oommen, President, Reliance Jio: “We spearheaded the transformation of both mobile and fixed home broadband by delivering affordable, high-quality broadband to everyone, across India. As we rapidly adopt an AI and API-driven technology ecosystem—by collaborating with global leaders, Jio is thrilled to offer a suite of innovative and transformative APIs to enterprises and developers worldwide. Together, we are not just building networks; we are laying the foundation for a smarter, more connected, and inclusive world in the AI era.”

Singtel

Mr Yuen Kuan Moon, Group Chief Executive Officer, Singtel: “This unified platform and global eco-system will enable even more developers and businesses to leverage 5G quality networks to exploit API opportunities using GSMA’s open gateway principles. We look forward to helping even more enterprises and organizations in Asia to use network API solutions to drive growth and innovation through this timely collaboration.”

Telefonica

José María Álvarez-Pallete, Chairman & CEO of Telefónica: “This collaboration will drive the GSMA Open Gateway initiative and provide customers with a consistent set of Camara APIs. Our belief is that this industry movement, which will be open to all networks, can set the stage for unprecedented innovation and value creation for the sector, by unlocking the potential of network capabilities.”

Telstra

Vicki Brady, CEO of Telstra: “This is a groundbreaking initiative for our industry. This new global venture will create an ecosystem that provides developers, partners and customers with access to programmable, advanced network capabilities that will unleash a new wave of innovation in digital services and further unlocks the benefits of our 5G network. We’ve been making good progress locally with Ericsson and other partners, and we look forward to further accelerating digital transformation for our Australian customers and bringing value and simplicity to application developers around the world.”

T-Mobile

Ulf Ewaldsson, President of Technology, T-Mobile: “At T-Mobile, we’ve always been laser focused on championing change across the industry to create the best customer experiences, while fueling growth and innovation across the entire wireless ecosystem. That level of transformation takes unprecedented collaboration and expertise. We are excited about the possibilities this venture will create for developers and wireless customers around the world.”

Verizon

Joe Russo, EVP & President, Global Network and Technology of Verizon: “The depth and value of the services and data insights accessible through Verizon’s renowned 5G network are practically boundless. Verizon has been at the forefront of developing various network APIs to assist developers in enhancing customer security, reducing pain points in customer interactions, and enabling the creation of novel experiences. This exciting collaboration with global partners will broaden the availability of these services and accelerate adoption of APIs worldwide.”

Vodafone

Margherita Della Valle, Vodafone Group Chief Executive, said: “Network APIs are reshaping our industry. This pioneering partnership will enable businesses and developers to use the collective strength of our global networks to develop applications that drive growth, create jobs, and improve public services. Just as 4G and smartphones made apps integral to our everyday life, the power of our 5G network will stimulate the next wave of digital services.”

Google Cloud

Thomas Kurian, CEO of Google Cloud: “We understand the power of an open platform and ecosystem in driving innovation. We are proud to participate in this important partnership in the telco industry to create value for our global customers via network APIs – and ultimately deliver on the promise of the public cloud.”

Vonage

Niklas Heuveldop, CEO Vonage: “This groundbreaking, open industry collaboration effectively removes the single largest barrier for developers to leverage mobile networks to their full potential. Developers across the world’s leading developer platforms will benefit from accessing advanced network capabilities in partner networks globally through common APIs, accelerating the digital transformation of businesses and the public sector. As one of the leading developer platforms, we look forward to engaging our developer community as we grow the network API business.”

……………………………………………………………………………………………………………………………………………………….

References:

Telefónica and Nokia partner to boost use of 5G SA network APIs

Analysts: Telco CAPEX crash looks to continue: mobile core network, RAN, and optical all expected to decline

Analysys Mason Open Network Index: survey of 50 tier 1 network operators

Ericsson expects continuing network equipment sales challenges in 2024

Nvidia enters Data Center Ethernet market with its Spectrum-X networking platform

Nvidia is planning a big push into the Data Center Ethernet market. CFO Colette Kress said the Spectrum-X Ethernet-based networking solution it launched in May 2023 is “well on track to begin a multi-billion-dollar product line within a year.” The Spectrum-X platform includes: Ethernet switches, optics, cables and network interface cards (NICs). Nvidia already has a multi-billion-dollar play in this space in the form of its Ethernet NIC product. Kress said during Nvidia’s earnings call that “hundreds of customers have already adopted the platform.” And that Nvidia plans to “launch new Spectrum-X products every year to support demand for scaling compute clusters from tens of thousands of GPUs today to millions of DPUs in the near future.”

- With Spectrum-X, Nvidia will be competing with Arista, Cisco, and Juniper at the system level along with “bare metal switches” from Taiwanese ODMs running DriveNets network cloud software.

- With respect to high performance Ethernet switching silicon, Nvidia competitors include Broadcom, Marvell, Microchip, and Cisco (which uses Silicon One internally and also sells it on the merchant semiconductor market).

Image by Midjourney for Fierce Network

…………………………………………………………………………………………………………………………………………………………………………..

In November 2023, Nvidia said it would work with Dell Technologies, Hewlett Packard Enterprise and Lenovo to incorporate Spectrum-X capabilities into their compute servers. Nvidia is now targeting tier-2 cloud service providers and enterprise customers looking for bundled solutions.

Dell’Oro Group VP Sameh Boujelbene told Fierce Network that “Nvidia is positioning Spectrum-X for AI back-end network deployments as an alternative fabric to InfiniBand. While InfiniBand currently dominates AI back-end networks with over 80% market share, Ethernet switches optimized for AI deployments have been gaining ground very quickly.” Boujelbene added Nvidia’s success with Spectrum-X thus far has largely been driven “by one major 100,000-GPU cluster, along with several smaller deployments by Cloud Service Providers.” By 2028, Boujelbene said Dell’Oro expects Ethernet switches to surpass InfiniBand for AI in the back-end network market, with revenues exceeding $10 billion.

………………………………………………………………………………………………………………………………………………………………………………

In a recent IEEE Techblog post we wrote:

While InfiniBand currently has the edge in the data center networking market, but several factors point to increased Ethernet adoption for AI clusters in the future. Recent innovations are addressing Ethernet’s shortcomings compared to InfiniBand:

- Lossless Ethernet technologies

- RDMA over Converged Ethernet (RoCE)

- Ultra Ethernet Consortium’s AI-focused specifications

Some real-world tests have shown Ethernet offering up to 10% improvement in job completion performance across all packet sizes compared to InfiniBand in complex AI training tasks. By 2028, it’s estimated that: 1] 45% of generative AI workloads will run on Ethernet (up from <20% now) and 2] 30% will run on InfiniBand (up from <20% now).

………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.fierce-network.com/cloud/data-center-ethernet-nvidias-next-multi-billion-dollar-business

https://www.nvidia.com/en-us/networking/spectrumx/

Will AI clusters be interconnected via Infiniband or Ethernet: NVIDIA doesn’t care, but Broadcom sure does!

Data Center Networking Market to grow at a CAGR of 6.22% during 2022-2027 to reach $35.6 billion by 2027

LightCounting: Optical Ethernet Transceiver sales will increase by 40% in 2024