Author: Alan Weissberger

Ericsson’s new antenna helps accelerate Vodafone 5G roll-out

Vodafone is rolling out Ericsson’s new compact antenna to bring greater 5G capacity, coverage and performance to locations across the U.K. The Ericsson AIR 3218 combines a radio unit and antenna in a single unit. It can also transmit mobile data over all of the frequencies that Vodafone currently uses in the U.K., without needing additional antenna units, as was the case for previous models.

The combined multiband, Massive MIMO design makes it easier for the operator to add more capacity to a mast without increasing its footprint. It’s also easier to mount on rooftops, towers, walls and poles.

“5G is the UK’s digital future, but we should never underestimate how difficult it is to deliver a future-proofed network at scale across the length and breadth of the UK. Working in partnership with Ericsson, we are constantly exploring new ways to accelerate this transformation, and this is another example of where innovation is delivered through collaboration,” said Ker Anderson, head of Radio and Performance at Vodafone UK, in a statement.

Ker Anderson, Head of Radio and Performance, Vodafone UK, said: “5G is the UK’s digital future, but we should never underestimate how difficult it is to deliver a future-proofed network at scale across the length and breadth of the UK.

“Working in partnership with Ericsson, we are constantly exploring new ways to accelerate this transformation, and this is another example of where innovation is delivered through collaboration.”

Combining equipment in this way can also help improve the design of a site. As there is limited space on a mobile mast for installing equipment, designers must also consider factors such as structural integrity – how much weight can a mast can safely sustain, especially in windy conditions.

Vodafone is using AR 3218 units with its 900MHz, 3.4GHz and 3.6GHz 5G frequencies, which have been carefully selected to meet the increasing demand for mobile data while also improving network efficiency. Those frequencies are already licensed for use in the UK.

The Interleaved AIR 3218 is powered by the latest Ericsson Silicon processor which enables both high performance and energy efficiency. Compared to 4G, it can do more with less – transmitting more gigabytes of data for each watt of energy used (Gbytes/Watt). The integrated design uses energy more efficiently than two separate pieces of equipment. Energy usage is a critically important design consideration for Vodafone engineers, as the company’s network is responsible for the majority of Vodafone’s annual energy consumption.

Ericsson noted that the Interleaved AIR 3218 is powered by the latest Ericsson Silicon technology. It also uses beam-through technology where an arbitrary active antenna can be placed behind the passive antenna, reducing the overall footprint in terms of size, weight and wind load.

So far, they’ve calculated a 30% reduction in site acquisition and build time based on results from the first five sites where deployment has already been completed. The AIR 3218 is expected to be deployed across 50 sites within the Vodafone UK network in 2023.

References:

https://www.vodafone.co.uk/newscentre/news/new-ericsson-antenna-helps-accelerate-vfuk-5g-rollout/

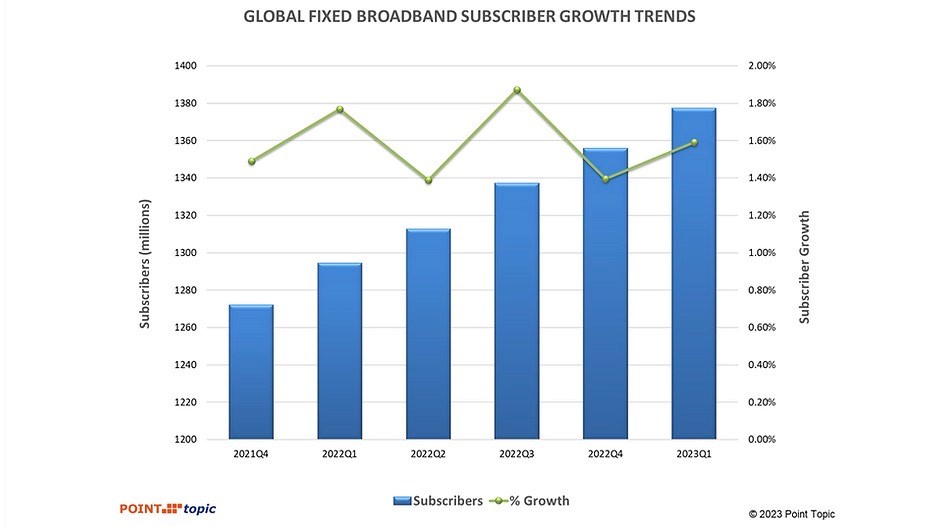

Point Topic Comprehensive Report: Global Fixed Broadband Connections at 1.377B as of Q1-2023

Global fixed broadband connections reached 1.377 billion as of Q1-2023, up by 83 million from a year earlier and reflecting an annual growth rate of 1.59%, according to Point Topic.

There was a decline in fixed broadband subscriptions in 18 countries[1] which mainly include emerging markets, as well as some saturated markets such as Singapore. However, while there were fluctuations in growth rates across regions and markets, the overall trend indicates a steady expansion of global broadband connectivity.

Highlights:

-

Among global regions, Africa, East Asia and America Other saw the fastest growth in broadband connections (2.9%, 2.2% and 1.8%), not least due to healthy increases in broadband subscribers in the vast markets of Egypt, Brazil and China.

-

The share of FTTH/B in the total fixed broadband subscriptions continued to increase and stood at 66.7%. Broadband connections based on other technologies saw their market shares shrink further, with an exception of satellite and wireless (mainly FWA).

-

VDSL subscriber numbers grew in ten countries, while they dropped in at least 22 markets as consumers migrated to FTTH/B.

-

The highest FTTH/B broadband subscriber growth rates in Q1 2023 were in Algeria, Peru and UK.

At 21.6 million, the quarterly net adds were close to the figure we recorded a year ago, though the growth rate (1.59%) was slower, compared to 1.77% in Q1 2022, with global inflation and economic instability having an impact.

East Asia continued to dominate in Q1 2023, maintaining its position as the largest market with a 49.6% share of global fixed broadband subscribers. This substantial market share is primarily driven by China with its vast population.

In Q1 2023, broadband subscriber base grew faster in China, Hong Kong and Korea, compared to Q4 2022. As a result, the region’s net adds share globally went up from 63.2% to 68.8%. Asia Other accounted for 10.8% of the global broadband market, similarly to the previous quarter, though the region’s net adds share went down from 12.8% to 9.4%.

Europe’s market shares remained rather consistent, though Eastern Europe saw their net adds share decline from 3.4% to 0.5%, as a result of slower growth in almost all markets and the decline in broadband subscribers in Russia having an especially significant impact due to its market size.

Similarly, Americas maintained relatively stable market shares of 10.3% and 8.1% respectively, while America – Other’s net adds share increased from 7.8% to 9%, driven by higher growth in such sizeable markets as Brazil, Mexico, Colombia and Chile, to name a few.

Next Point Topic looks at fixed broadband penetration among population, comparing it to growth rates across the regions.

Africa and Asia Other continue to have relatively low fixed broadband penetration rates among their populations. In Q1 2023, this metric in Africa stood at 4.6%, while Asia Other reached 5.6%. These figures indicate the potential for future expansion in these regions. Not surprisingly, Africa also recorded the highest quarterly growth rate of 2.9%.

The markets of East Asia and America Other followed closely with growth rates of 2.2% and 1.8% respectively, despite East Asia already having the highest population penetration at 41.9%. This reflects a widespread adoption of fixed broadband services in East Asia, while America Other showcases steady growth in a region with significant potential, where broadband penetration is among the lowest, at 17.2%.

Eastern Europe displayed a modest growth rate of 0.2% with a population penetration of 24.8%. Some markets in this region still have a lot of headspace when it comes to broadband adoption but the growth was sluggish, likely due to economic pressures. Other European regions showed a slightly higher growth rate, with Europe Other at 0.5%, coupled with the second highest population penetration of 39.4%. These figures indicate a mature market with limited growth opportunities.

Among the largest twenty broadband markets all but one saw fixed broadband subscribers grow in Q1 2023, although in ten of them the growth was slower than in the Q4 2022. There was a slight drop in broadband subscribers in Russia which is under international sanctions.

The less saturated broadband markets of India, Egypt, Brazil and Mexico recorded the highest quarterly growth rates in Q1 2023, all higher than 2%. China recorded an above 2% growth as well. At the other end of the spectrum, the mature markets of Germany, France, Japan, UK, and Italy saw modest growth rates at below 0.5%. At the same time, Italy was among the countries that saw one of the largest improvements in growth rates, from -0.44% in Q4 2022 to 0.04% in Q1 2023, as its GDP growth also went from negative to positive in that period[2]. Mexico, China and Brazil recorded the largest improvements in their growth rates, at +1.14.%, +0.52% and +0.41% respectively.

Between Q4 2022 and Q1 2023, the share of FTTH/B connections in the total fixed broadband subscriptions went up by 0.7% and stood at 66.7%. Broadband connections based on other technologies saw their market shares shrink further, with an exception of satellite and wireless (mainly FWA), which remained stable.

FTTx (mainly VDSL) share stood at 6.7%[3]. VDSL subscriber numbers grew in ten countries (including modest quarterly increase in the large VDSL markets of Turkey, Czech Republic, Greece and Germany, for example), while they fell in 22 other markets as consumers migrated to FTTH/B.

It remains to be seen whether consumers will continue to gravitate toward fibre broadband offerings, particularly as global economies face potential slowdown and inflationary pressures.

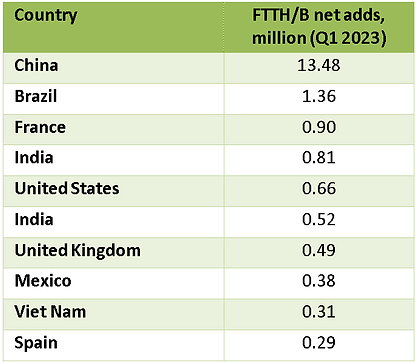

In terms of FTTH/B broadband net additions in Q1 2023, China continued to maintain a significant lead with 13.5 million while Brazil added 1.4 million. Mexico is back in the top ten league, having pushed out Argentina this quarter.

Satellite broadband also saw a modest growth of 1.3% while wireless broadband demonstrated continued relevance with a respectable growth rate of 4.9%. These trends can be attributed to the demand for connectivity in remote or underserved areas where traditional broadband infrastructure is not feasible.

The diverse growth rates among different broadband technologies highlight the dynamic nature of the industry as consumers seek more reliable and high-speed connections. The significant increase in FTTH/B connections and the growth of satellite and wireless broadband underline the ongoing efforts to bridge the digital divide and ensure connectivity for all.

The top ten countries by fixed broadband subscribers remained unchanged (Figure 5). As of Q1 2023, China exceeded 0.6 billion fixed broadband subscribers, having added 14.6 million in the quarter. Also, the country is approaching 1.2 billion 5G subscribers, with the service now being used by 84% of the population.

Overall, the latest fixed broadband subscriber data reveals a clear trend towards advanced, high-speed broadband solutions like FTTH/B, while older technologies such as copper-based broadband (ADSL and VDSL) are experiencing a decline, suggesting that the broadband landscape is continuously evolving to meet the growing demand for faster and more reliable connectivity.

References:

https://www.point-topic.com/post/global-broadband-subscriptions-q1-2023

Point Topic: Global Broadband Tariff Benchmark Report- 2Q-2022

Point Topic: Global fixed broadband connections up 1.7% in 1Q-2022, FTTH at 58% market share

Malaysia’s Maxis agreement with DNB to provide nationwide 5G services

Malaysian telco Maxis executed a 5G access agreement with state-run network operator Digital Nasional (DNB), according to local press reports.

Maxis said it will seek its shareholders’ approval for the execution of the agreement, at an extraordinary general meeting to be carried out in the third quarter. If the agreement is approved, Maxis will become the last of the country’s mobile operators to agree to execute the 5G access agreement with DNB.

Telekom Malaysia, CelcomDigi, YTL Communications and U Mobile have all agreed to the wholesale access agreement with the state-run network operator.

“DNB remains the single neutral wholesale network provider to undertake the deployment of 5G infrastructure and network nationwide as at the latest practicable date. Therefore, the entry into the access agreement with DNB will enable Maxis to provide the 5G services to its customers,” the company said in a filing to the local stock exchange.

The filing also indicated the price to be paid by Maxis to execute the agreement is yet to be determined and may be subject to periodic reviews conducted by the Malaysian Communications and Multimedia Commission as well as a by DNB.

![]()

DNB was set up by the Malaysian government in 2021 as a special purpose vehicle to develop the country’s 5G network infrastructure, which private telecommunications firms would use to offer 5G services to their customers.

However, Malaysia’s 5G roll-out by DNB had raised concerns over pricing and transparency, as well as worries that a single state-run 5G network would result in a nationalized monopoly.

Due to these concerns, the new prime minister, Anwar Ibrahim, had previously announced an overall review of the rollout of the national 5G network due to the lack of transparency. In May, the government announced it will enable the deployment of a second 5G network in 2024, adding that a new entity will be created to manage Malaysia’s second 5G network.

Malaysia’s Communications and Digital Minister Fahmi Fadzil recently said that DNB will continue to roll out 5G network infrastructure in the country until 80% coverage is achieved by the end of this year. The Malaysian government also confirmed that DNB will be taken over by a private entity once it achieves its 5G population coverage target.

Ookla Q2-2023 Mobile Network Operator Speed Tests: T-Mobile is #1 in U.S. in all categories!

Ookla’s U.S. Mobile and Wireline Speed Overview:

T-Mobile was the fastest mobile operator with a median download speed of 164.76 Mbps. T-Mobile also had the fastest median 5G download speed at 220.00 Mbps, and lowest 5G multi-server latency of 51 ms.

Spectrum edged out Cox as the fastest fixed wireline broadband provider with a median download speed of 243.02 Mbps. Verizon had the lowest median multi-server latency on fixed broadband at 15 ms.

Source: Ookla

……………………………………………………………………………………………………………………….

Ookla’s Speedtest Intelligence® reveals T-Mobile was the fastest mobile operator in the United States during Q2 2023 with a median download speed of 164.76 Mbps on modern chipsets, a slight decline from 165.22 Mbps during Q1 2023. Verizon Wireless and AT&T were distant runners up and both saw minor declines in download speed.

T-Mobile had the fastest median upload speed among top mobile operators in the U.S. at 12.16 Mbps during Q2 2023. Verizon Wireless was second and AT&T finished third.

Calculating median multi-server latency for the three top mobile operators in the U.S. during Q2 2023, T-Mobile had the lowest multi-server latency at 54 ms. Verizon Wireless was a close second at 58 ms. AT&T was third at 63 ms. As latency becomes an increasingly important measure, we’ll be sure to watch latency metrics closely.

In measuring the Consistency of each operator’s performance, we found that T-Mobile had the highest Consistency in the U.S. during Q2 2023, with 86.1% of results showing at least 5 Mbps download and 1 Mbps upload speeds. Verizon Wireless and AT&T followed at 81.5% and 79.2%, respectively.

In measuring the Video Score of each mobile operator’s video performance, we found that T-Mobile had the highest Video Score in the U.S. at 74.39 during Q2 2023. Verizon Wireless was a close second at 70.89 and AT&T was third at 68.16.

Looking at the 5G Video Score of each operator’s video performance over a 5G connection, T-Mobile had the highest 5G Video Score in Q2 2023 at 78.70. Verizon Wireless recorded a 5G Video Score of 77.39 and AT&T had a score of 70.40.

Looking only at tests taken on a 5G connection, T-Mobile had the fastest median 5G download speed in the U.S. at 220.00 Mbps during Q2 2023, in line with its performance during Q1 2023. Verizon Wireless remained second and saw a slight increase to 133.50 Mbps in Q2 2023. AT&T remained third at 86.01 Mbps. The bars shown in the chart below are 95% confidence intervals, which represent the range of values in which the true median is likely to be. For a complete view of commercially available 5G deployments in the U.S. to-date, visit the Ookla 5G Map™.

Our mobile 5G multi-server latency results in Q2 2023 showed that among top providers, T-Mobile registered the lowest median 5G multi-server latency in the United States. Latency was a tight race, but our testing showed that with a median value of 51 ms, T-Mobile users saw better multi-server latency values than those of their nearest competitor, Verizon Wireless (53 ms).

In measuring the Consistency of each operator’s performance over a 5G connection in the U.S. during Q2 2023, we found that there was no statistical winner for highest 5G Consistency.

Our analysis of the most popular devices in the U.S. during Q2 2023 showed no statistical winner for fastest median download speed, with the Samsung Galaxy S23 Ultra and Samsung Galaxy Z Fold4 both recording similar speeds, followed by the Google Pixel 7 Pro, the Apple iPhone 14 Pro Max, and the Samsung Galaxy S22 Ultra.

We examined combined performance by major cell phone manufacturers and found that Samsung devices had the fastest median download speed in the U.S. at 90.83 Mbps during Q2 2023. Apple followed at 75.65 Mbps.

Looking at popular chipsets in the U.S., Ookla found no statistical winner for median download performance between Qualcomm’s Snapdragon 8 Gen 2 at 141.58 Mbps and its previous generation Snapdragon 8+ Gen 1 at 136.85 Mbps. Qualcomm’s Snapdragon X65 5G registered a median download speed of 125.05 Mbps, Google’s Tensor G2 was next on the list at 124.77 Mbps, while Qualcomm’s Snapdragon 8 Gen 1 followed at 117.59 Mbps.

Kansas City, Missouri had the fastest median mobile download speed among the 100 most populous cities in the U.S. at 151.15 Mbps during Q2 2023. Scottsdale, Arizona was second; Columbus, Ohio was third; Plano, Texas fourth; and St. Paul, Minnesota was fifth.

Reno, Nevada had the slowest median mobile download speed among the U.S.’s 100 most populous cities during Q2 2023 at 51.06 Mbps. Anchorage, Alaska was second slowest; Lincoln, Nebraska third slowest; Laredo, Texas fourth slowest; and Tulsa, Oklahoma was fifth slowest.

T-Mobile was the fastest operator in 87 of the 100 most populous cities in the U.S. during Q2 2023. Verizon Wireless was the fastest provider in El Paso, Texas, and results were statistically too close to call in 12 cities.

References:

https://www.speedtest.net/global-index/united-states#market-analysis

Ookla: Fixed Broadband Speeds Increasing Faster than Mobile: 28.4% vs 16.8%

Ookla: State of 5G Worldwide in 2022 & Countries Where 5G is Not Available

Ookla Ranks Internet Performance in the World’s Largest Cities: China is #1

Deutsche Telekom Global Carrier Launches New Point-of-Presence (PoP) in Miami, Florida

Wholesale network operator Deutsche Telekom Global Carrier has announced the launch of a new Point-of-Presence (PoP) in Miami, Florida. The PoP, hosted within the Equinix data center, offers bandwidths of 1/10/100 gigabits per second (n x 1, n x 10, n x 100 Gbps). According to the official statement, this expansion aims to strengthen Deutsche Telekom’s global IPX and IP network footprint.

By establishing the new IPX and IP PoP in Miami, Deutsche Telekom Global Carrier says its clients can now enjoy direct access to its Tier 1 IP and IPX network, one of the largest in the world. This move comes in response to the growing demand for high-speed connectivity, as businesses increasingly require efficient implementation of digital applications and emerging technologies.

“The launch of our new IPX PoP in Miami, Florida, is an important step for Deutsche Telekom Global Carrier in addressing customer needs on the American continent. Even with Today’s ever-growing data volumes, users’ expectations continue to rise, and low-latency data roaming is crucial. Our newly implemented IPX PoP addresses the demand increase and helps us provide our customers and partners with premium quality global connectivity.”

Deutsche Telekom Global Carrier emphasized the significance of the Miami PoP: “At Deutsche Telekom Global Carrier, we are always several steps ahead of demand because we’re committed to providing our customers and partners with superior, future-proof connectivity and quality. This new PoP is part of that promise,” said the company in its press release.

With this latest development, Deutsche Telekom Global Carrier ensures businesses have the essential infrastructure required for seamless digital operations.

Image Credit: Deutsche Telekom

Csaba Füzesi, Head of Product Management Voice & Mobile Services at Deutsche Telekom Global Carrier, said: “The launch of our new IPX PoP in Miami, Florida is an important step for Deutsche Telekom Global Carrier in addressing customer needs on the American continent. Even with today’s ever-growing data volumes, expectations of users continue to rise, and low-latency data roaming is crucial. Our newly implemented IPX PoP addresses the increase in demand and helps us to provide our customers and partners with premium quality global connectivity.”

Miles McWilliams, Head of Sales Internet & Content Services at Deutsche Telekom Global Carrier, said: “Today’s ever-growing data volumes match the rising expectations of users. At Deutsche Telekom Global Carrier we are always several steps ahead of demand because we’re committed to providing our customers and partners with superior, future-proof connectivity and quality. This new PoP is part of that promise.”

Deutsche Telekom has extended its autonomous AS 3320 network around the Equinix site in Miami, which is America’s largest data center campus. The MI1 data center is located in downtown Miami, with a colocation area of 255,512 square feet.

References:

https://telecomtalk.info/deutsche-telekom-global-carrier-pop-miami-florida/783941/

Bain & Co, McKinsey & Co, AWS suggest how telcos can use and adapt Generative AI

Generative Artificial Intelligence (AI) uncertainty is especially challenging for the telecommunications industry which has a history of very slow adaptation to change and thus faces lots of pressure to adopt generative AI in their services and infrastructure. Indeed, Deutsche Telekom stated that AI poses massive challenges for telecom industry in this IEEE Techblog post.

Consulting firm Bain & Co. highlighted that inertia in a recent report titled, “Telcos, Stop Debating Generative AI and Just Get Going” Three partners stated network operators need to act fast in order to jump on this opportunity. “Speedy action trumps perfect planning here,” Herbert Blum, Jeff Katzin and Velu Sinha wrote in the brief. “It’s more important for telcos to quickly launch an initial set of generative AI applications that fit the company’s strategy, and do so in a responsible way – or risk missing a window of opportunity in this fast-evolving sector.”

Generative AI use cases can be divided into phases based on ease of implementation, inherent risk, and value:

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Telcos can pursue generative AI applications across business functions, starting with knowledge management:

Separately, a McKinsey & Co. report opined that AI has highlighted business leader priorities. The consulting firm cited organizations that have top executives championing an organization’s AI initiatives, including the need to fund those programs. This is counter to organizations that lack a clear directive on their AI plans, which results in wasted spending and stalled development. “Reaching this state of AI maturity is no easy task, but it is certainly within the reach of telcos,” the firm noted. “Indeed, with all the pressures they face, embracing large-scale deployment of AI and transitioning to being AI-native organizations could be key to driving growth and renewal. Telcos that are starting to recognize this is non-negotiable are scaling AI investments as the business impact generated by the technology materializes.”

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Ishwar Parulkar, chief technologist for the telco industry at AWS, touted several areas that should be of generative AI interest to telecom operators. The first few were common ones tied to improving the customer experience. This includes building on machine learning (ML) to help improve that interaction and potentially reduce customer churn.

“We have worked with some leading customers and implemented this in production where they can take customer voice calls, translate that to text, do sentiment analysis on it … and then feed that into reducing customer churn,” Parulkar said. “That goes up another notch with generative AI, where you can have chat bots and more interactive types of interfaces for customers as well as for customer care agent systems in a call. So that just goes up another notch of generative AI.”

The next step is using generative AI to help operators bolster their business operations and systems. This is for things like revenue assurance and finding revenue leakage, items that Parulkar noted were in a “more established space in terms of what machine learning can do.”

However, Parulkar said the bigger opportunity is around helping operators better design and manage network operations. This is an area that remains the most immature, but one that Parulkar is “most excited about.” This can begin from the planning and installation phase, with an example of helping technicians when they are installing physical equipment.

“In installation of network equipment today, you have technicians who go through manuals and have procedures to install routers and base stations and connect links and fibers,” Parulkar said. “That all can be now made interactive [using] chat bot, natural language kind of framework. You can have a lot of this documentation, training data that can train foundational models that can create that type of an interface, improves productivity, makes it easier to target specific problems very quickly in terms of what you want to deploy.”

This can also help with network configuration by using large datasets to help automatically generate configurations. This could include the ability to help configure routers, VPNs and MPLS circuits to support network performance.

The final area of support could be in the running of those networks once they are deployed. Parulkar cited functions like troubleshooting failures that can be supported by a generative AI model.

“There are recipes that operators go through to troubleshoot and triage failure,” Parulkar said “A lot of times it’s trial-and-error method that can be significantly improved in a more interactive, natural language, prompt-based system that guides you through troubleshooting and operating the network.”

This model could be especially compelling for operators as they integrate more routers to support disaggregated 5G network models for mobile edge computing (MEC), private networks and the use of millimeter-wave (mmWave) spectrum bands.

Federal Communications Commission (FCC) Chairwoman Jessica Rosenworcel this week also hinted at the ability for AI to help manage spectrum resources.

“For decades we have licensed large slices of our airwaves and come up with unlicensed policies for joint use in others,” Rosenworcel said during a speech at this week’s FCC and National Science Foundation Joint Workshop. “But this scheme is not truly dynamic. And as demands on our airwaves grow – as we move from a world of mobile phones to billions of devices in the internet of things (IoT)– we can take newfound cognitive abilities and teach our wireless devices to manage transmissions on their own. Smarter radios using AI can work with each other without a central authority dictating the best of use of spectrum in every environment. If that sounds far off, it’s not. Consider that a large wireless provider’s network can generate several million performance measurements every minute. And consider the insights that machine learning can provide to better understand network usage and support greater spectrum efficiency.”

While generative AI does have potential, Parulkar also left open the door for what he termed “traditional AI” and which he described as “supervised and unsupervised learning.”

“Those techniques still work for a lot of the parts in the network and we see a combination of these two,” Parulkar said. “For example, you might use anomaly detection for getting some insights into the things to look at and then followed by a generative AI system that will then give an output in a very interactive format and we see that in some of the use cases as well. I think this is a big area for telcos to explore and we’re having active conversations with multiple telcos and network vendors.”

Parulkar’s comments come as AWS has been busy updating its generative AI platforms. One of the most recent was the launch of its $100 million Generative AI Innovation Center, which is targeted at helping guide businesses through the process of developing, building and deploying generative AI tools.

“Generative AI is one of those technological shifts that we are in the early stages of that will impact all organizations across the globe in some form of fashion,” Sri Elaprolu, senior leader of generative AI at AWS, told SDxCentral. “We have the goal of helping as many customers as we can, and as we need to, in accelerating their journey with generative AI.”

References:

https://www.bain.com/insights/telcos-stop-debating-generative-ai-and-just-get-going/

Deutsche Telekom exec: AI poses massive challenges for telecom industry

Generative AI in telecom; ChatGPT as a manager? ChatGPT vs Google Search

Generative AI could put telecom jobs in jeopardy; compelling AI in telecom use cases

Generative AI Unicorns Rule the Startup Roost; OpenAI in the Spotlight

Forbes: Cloud is a huge challenge for enterprise networks; AI adds complexity

Qualcomm CEO: AI will become pervasive, at the edge, and run on Snapdragon SoC devices

Bloomberg: China Lures Billionaires Into Race to Catch U.S. in AI

Forbes: Cloud is a huge challenge for enterprise networks; AI adds complexity

Survey data and discussions with enterprise networking professionals reveal they are still grappling with many networking issues spawned by the expansion of the cloud – the most common of which include securing connections for remote work, implementing zero-trust security strategies, and integrating myriad cloud and wide-area networks (WANs).

For example, in Futuriom’s latest survey of 196 enterprise IT and networking professionals, more than 80% said the complexity of connecting the wide variety of networks was a large challenge. At nearly 70% of responses, expertise and knowledge was the second-largest challenge (multiple responses were allowed), and cost was cited by 60%. Please refer to survey highlights below.

Contributing to that complexity is the ephemeral nature of both cloud connectivity and hybrid work. Workers are now moving around more than ever, and cloud services can change and scale nearly every day (or minute).

Survey Highlights:

- Survey respondents indicate strong demand for SD-WAN and SASE managed services. Our survey data and discussions with end users indicate that SD-WAN/SASE technology helps professionals with network and security challenges, including the growing complexity created by distributed applications, cloud connectivity, and sprawling security risks.

- Managing network complexity is the largest challenge driving managed services demand. When asked about the largest challenges in managing WANs, 85% of respondents identified complexity, followed by expertise and knowledge (68%). Rounding out the responses were cost (60%) and time (47%). (Multiple responses were allowed.)

- Hybrid work and the need for zero-trust network access (ZTNA) are key drivers of SD-WAN/SASE technology. In the survey, 98% of respondents said that hybrid work has increased demand for SASE and ZTNA. When we asked respondents if ZTNA is a crucial component of SASE and SD-WAN offerings, 92% said yes.

- Hybrid (cloud/edge deployment) and single-pass architectures will be important components of SASE/SD-WAN services going forward. When respondents were asked if they wanted a hybrid solution that can accommodate networking and security both on premises and using cloud points of presence (PoPs), 98% said yes. In addition, 94% of respondents said they prefer a single-pass architecture.

- There will continue to be a diversity of SD-WAN/SASE deployment models. The two most popular models for deployment are best-of-breed combination (34%) and single-vendor (23%), but survey results show a wide diversity of deployment models.

AI increases complexity as enterprises need to figure out how to store, connect, and move their data in hybrid clouds that will leverage AI.

This complexity, along with the rapid shift to hybrid work spurred by COVID, has triggered a wave of innovation in networking – perhaps more innovation than we have seen in decades. Startups are drawing large funding rounds. Best-of-breed established networking players such as Arista Networks, Extreme Networks, Juniper Networks, and HPE are building new networking and security products and chipping away at the market share of market leader Cisco. Cisco is responding in kind. Sources tell me they think Cisco’s acquisition of Valtix may be the most interesting in years.

All of this sets the stage for the most dynamic networking environment I’ve seen in decades. And it’s only going to get more interesting, as the AI and hybrid work wave makes networking more crucial.

The melding of security and networking remains hot. In the software-defined networking (SD-WAN) and Secure Access Service Edge market, potential Initial Public Offering (IPO) companies such as Aryaka Networks, Cato Networks, and Versa Networks are building our product suites to help secure remote workers and cloud connectivity. These companies will also help enterprises connect to cloud on-ramps and consolidate security functions with a SASE approach. Versa last October tanked up with $120 in funding in what it called a “pre-IPO round.”

Many of the cloud networking startups that are included in the Futuriom 50 list of promising cloud innovators are using this chaotic moment to shore up strategies, raise money — or both.

For example, just this week, cloud-native networking start-up Arrcus announced that Hitachi Ventures would invest additional capital, raising its Series D to $65 million before it closes. Arrcus says its Arrcus Connected Edge (ACE) platform will be more economical for cloud providers and service providers deploying services such as 5G and AI. It claims it is growing revenue 100% year-over-year.

Other cloud networking startups are also going after AI. DriveNets recently announced that its Network Cloud-AI solution, which uses cloud-based Ethernet-based networking to boost the performance of AI clouds, is in trials with major hyperscalers.

Cost optimization, one of the strongest themes of the year in cloud technology, is another focus for cloud networking players. Cloud networking pioneer Aviatrix has beefed up security and cost-optimization features and launched a distributed firewall to help enterprises reduce the costs of cloud networking infrastructure. Prosimo last week made an interesting play to get its application-layer cloud networking suite in the hands of more users by launching a free, introductory-level version of its product called MCN Foundation.

Yes, there is a trend to all these announcements. They are focused on return on investment (ROI) and cost savings. This is the right message for the era we are in. Enterprise tech planners not only want to shift to more flexible cloud-based services, they need to do so to save money.

For example, in its new product release, Prosimo said customers can achieve a 30%-50% reduction in total cost of ownership (TCO) by optimizing cloud network connectivity. With its distributed firewall, Aviatrix says network pros will save money by reducing the expense of additional firewall instances, which many enterprises must buy to support additional cloud connectivity and scaling. (But they may not want to stack firewall upon firewall into the cloud, which after all can function as a firewall itself.) DriveNets says its trials have reduced the idle time of AI clouds by as much as 30%.

Integrating all of this stuff isn’t easy either. That’s the value proposition of Itential, a plucky Georgia-based startup with a set of low-code automation tools that streamline networking for integrations in hybrid networking and cloud environments.

It’s no coincidence that the marketing messages have all shifted toward ROI, which is the mother’s milk of technology. It’s the reason we all use cloud-based software-as-a-service and iPhones instead of minicomputers and rotary dial phones. Innovation is about efficiency.

This makes me very optimistic about cloud networking – and the networking market in general. After decades of stagnation, the cloud has woken up the industry. In addition to innovation, there is also a surge in competition — which will put more efficient and affordable technology into the hands of the users.

References:

Networking Startups Jump On Cloud Costs And AI (forbes.com)

https://www.futuriom.com/articles/news/results-from-our-sd-wan-sase-managed-services-survey/2023/06

Generative AI in telecom; ChatGPT as a manager? ChatGPT vs Google Search

Generative AI could put telecom jobs in jeopardy; compelling AI in telecom use cases

Allied Market Research: Global AI in telecom market forecast to reach $38.8 by 2031 with CAGR of 41.4% (from 2022 to 2031)

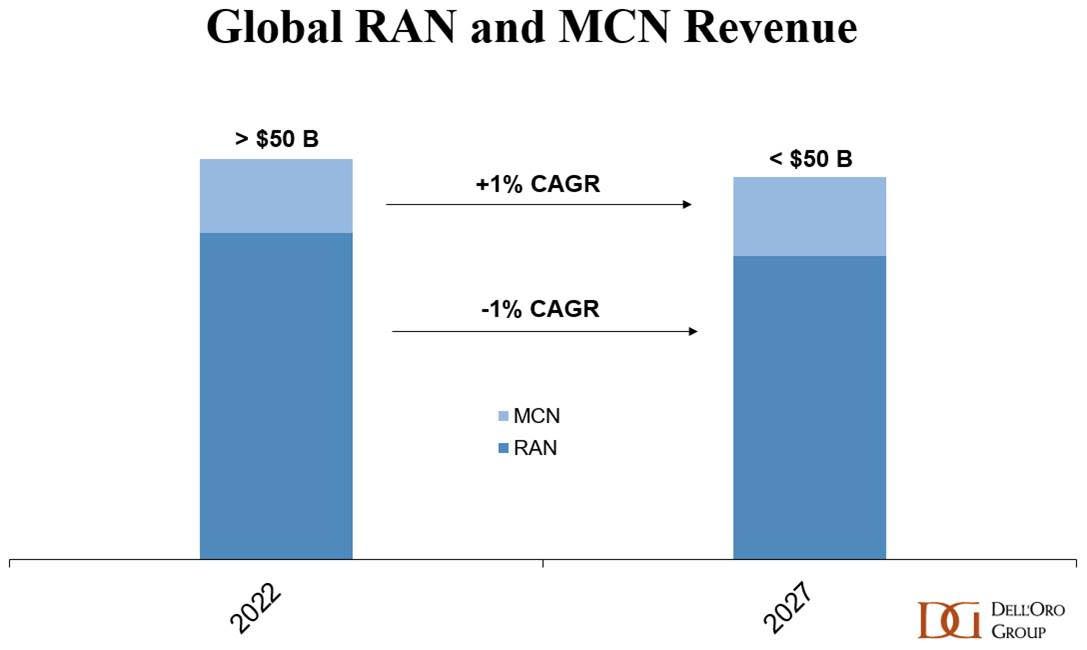

Dell’Oro: RAN Market to Decline 1% CAGR; Mobile Core Network growth reduced to 1% CAGR

According to a newly published forecast report by Dell’Oro Group,the Radio Access Network (RAN) market is done expanding for now. Following the 40% to 50% ascent between 2017 and 2021, RAN revenues flattened out in 2022 and these trends extended to 1Q 2023.

“Even if it is early days in the broader 5G journey, the challenge now is the comparisons are becoming more challenging in the more mature 5G markets and the upside with the slower-to-adopt 5G regions is not enough to extend the growth streak,” said Stefan Pongratz, Vice President at Dell’Oro Group.

“Meanwhile, growth from new revenue streams including Fixed Wireless Access and enterprise LTE/5G is not ramping fast enough to change the trajectory. With 5G-Advanced not expected to trigger a new capex cycle, the question now is no longer whether RAN will grow. The question now is, rather, how much will the RAN market decline before 6G comes along?” Pongratz added.

Additional highlights from the Mobile RAN 5-Year July 2023 Forecast Report:

- Global RAN is projected to decline at a 1 percent CAGR over the next five years.

- The less advanced 5G regions are expected to perform better while the more developed 5G regions, such as North America and China, are projected to record steeper declines.

- LTE is still handling the majority of the mobile data traffic, but the focus when it comes to new RAN investments is clearly on 5G. Even with the more challenging comparisons, 5G is projected to grow another 20 percent to 30 percent by 2027, which will not be enough to offset steep declines in LTE.

- With mmWave comprising a low single-digit share of the RAN market and skepticism growing about the MBB business case, it is worth noting that our position has not changed. We still envision that the mmWave spectrum will play a pivotal role in the long-term capacity roadmap.

……………………………………………………………………………………………………………………….

Separately, Dell’Oro again lowered its forecasts for the Mobile Core Network market (which is now 5G SA core network), this time citing a slowdown in customer growth. It now predicts that the worldwide market for mobile core networks will expand at a CAGR of 1% over the next five years, having previously forecast a 2% CAGR as recently as January.

“We have reduced our forecast for the third consecutive time, primarily caused, this time, by an expected slowdown in subscriber growth,” said Dave Bolan, Research Director at Dell’Oro Group.

Dave said that Dell’Oro has reduced its expectations for the Multi-Access Edge Computing (MEC) market (which requires 5G SA core network). It now anticipates MEC will have a CAGR of 31%, noting that commercially-viable enterprise applications are taking much longer to come to fruition than many had hoped.

“Mobile Network Operators (MNOs) are concerned about inflation, a possible recession, and political conflicts. They are therefore being restrained in their capital expenditures, another factor weighing in on a more conservative forecast,” said Bolan. “As we continue refining our count of MNOs that have launched 5G Standalone (5G SA) eMMB networks, we note that only 4 MNOs have commercially deployed new 5G SA networks compared to six in the first half of 2022,” he added.

Additional highlights from the Mobile Core Network & Multi-Access Edge Computing 5-Year July 2023 Forecast Report:

- Year-over-year MCN revenue growth rates are projected to be flat in 2026 and turn negative in 2027.

- The North America and China regions are expected to have negative CAGRs, while Europe, Middle East, and Africa (EMEA), and Asia Pacific excluding China regions are expected to have the highest positive CAGRs.

Vodafone became one of those first-half 2023 launches, when it brought 5G Ultra to market in the UK in late June. In its latest Mobility Report, published around the same time, Ericsson noted that while around 240 telcos have launched commercial 5G services, only 35 of them have brought standalone 5G to market.

That should bode well for the mobile core market, and indeed it is faring better than the RAN space, in growth potential terms, at least.

Nonetheless, Dell’Oro predicts that year-on-year growth rates in mobile core network revenues will be flat by 2026 and turn negative the following year.

Dell’Oro Group’s Mobile RAN 5-Year Forecast Report offers a complete overview of the RAN market by region – North America, Europe, Middle East & Africa, Asia Pacific, China, and Caribbean & Latin America, with tables covering manufacturers’ revenue and unit shipments for 5GNR, 5G NR Sub 6 GHz, 5G NR mmW and LTE pico, micro, and macro base stations. The report also covers Open RAN, Virtualized RAN, small cells, and Massive MIMO. To purchase this report, please contact us by email at [email protected].

Dell’Oro Group’s Mobile Core Network & Multi-Access Edge Computing 5-Year July Forecast Report offers a complete overview of the market for Wireless Packet Core including MEC for the User Plane Function, Policy, Subscriber Data Management, and IMS Core with historical data, where applicable, to the present. The report provides a comprehensive overview of market trends by network function implementation (Non-NFV and NFV), covering revenue, licenses, average selling price, and regional forecasts for various network functions. To learn more about this report, please contact us at [email protected].

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, security, enterprise networks, and data center infrastructure markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions. For more information, contact Dell’Oro Group at +1.650.622.9400 or visit www.delloro.com.

References:

RAN Market to Decline at a 1 Percent CAGR Through 2027, According to Dell’Oro Group

Slower Subscriber Growth to Cut Mobile Core Network Market Growth, According to Dell’Oro Group

Heavy Reading Survey: 5G services require network automation

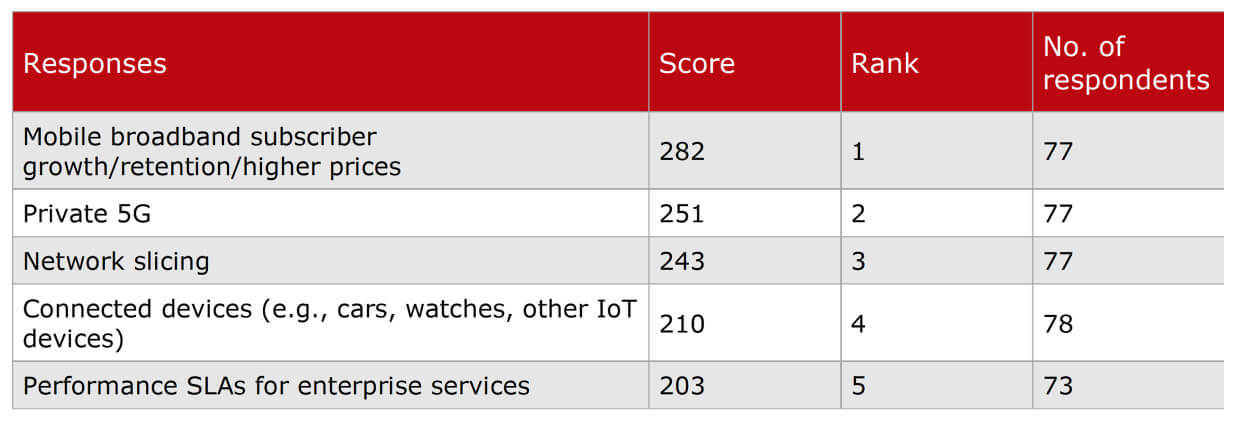

Heavy Reading’s 2023 5G Network Analytics and Automation Operator Survey aims to help the industry better understand the status of network analytics and automation and provide insights into operators’ strategies. (To download a copy, click here.) At the start of the survey, one question looks to understand which 5G services network operators believe to be the most valuable in supporting revenue growth.

Editor’s NOTE: It’s important to understand that ALL 5G SERVICES/FEATURES (such as network slicing) require a 5G SA core network rather than 5G NSA which uses 4G-LTE infrastructure for everything other than the 5G NR RAN.

……………………………………………………………………………………………………………………………

The table below shows the weighted average scores across several 5G services, with operators ranking “mobile broadband subscriber growth/retention/high prices” first and ahead of the other options.

Enhanced mobile broadband (eMBB) is the anchor service for 5G NSA and generates nearly all 5G revenue today. This scoring infers that operators are keen to grow their core businesses, which will involve greater efficiencies and new mobile packages that offer superior or premium features at an added cost.

“Private 5G” and “network slicing” rank second and third, respectively. Heavy Reading expects their importance and popularity to increase as additional operators deploy 5G SA and can support full autonomy. “Performance SLAs for enterprise services” is currently the lowest ranking (fifth) of all service choices but is likely to be a valuable market, especially for network slicing and private 5G.

“Connected devices (e.g., cars, watches, other IoT devices)” ranks just above performance SLAs in fourth. Internet of Things (IoT) is a sizeable market within 4G, but the massive machine-type communications (mMTC) use case has yet to be realized in 5G, as technologies such as RedCap remain underdeveloped.

Smaller network operators have a different opinion than larger operators on the revenue growth question.

For mobile operators with less than 9 million subscribers, private 5G ranks first. This result perhaps indicates that smaller operators feel they are already exploiting eMBB services and see little scope for further revenue growth with 5G SA.

Which services are the most attractive for 5G revenue growth in your organization? (Rank in order, where 1 = the most attractive)

Given the survey results above and the desire for operators to grow their revenue and retain customers, it is evident that automation will play a fundamental role in future 5G services underpinning cost efficiencies and quality of service. Service diversity and the 5G disaggregated cloud native infrastructure will mandate automation across the network (i.e., provisioning, testing, operation, fault resolution and maintenance), specifically for the following aspects:

Automated configuration: Automation tackles the scale and complexity of administration, management and lengthy configuration across large networks with multiple service solutions (e.g., private networks, network slicing, performance SLAs, etc.), offering significant time savings over manual effort.

- End-to-end 5G monitoring and visibility: 5G network visibility requires a dynamic and layered approach to monitor 5G cloud infrastructure, orchestration/containerized environments and the network domains and services. Service insights and SLA monitoring will be more granular. Examples include network slicing visibility per slice, user, session, location, etc., across KPIs like latency, jitter, packet drop and data rate.

- Network probes and testing: Active test agents provide near real-time visibility, making them better equipped to monitor dynamic cloud native environments and workload changes than more traditional reactive methods.

- Lifecycle and test management: Automated software deployment cycles (CI/CD) will be critical due to the increased cadence of software updates across virtual machines or cloud native deployments. In addition, automating network and service testing could enable the validation of services and configuration while assessing the perceived end-user quality of service.

- Artificial intelligence/machine learning (AI/ML): These technologies will contribute heavily to automated processes, optimization and efficiencies, with AIOps processes assuring the network and its services. For example, AI/ML can help forecast network resources, user mobility patterns, RAN optimization, security anomaly prevention, fault prediction, etc.

Operators are highly motivated to deliver advanced services and drive business growth and revenue to recoup the costs of their significant 5G spectrum and network investments. However, supporting a diverse and evolving portfolio of 5G network services will require automation to provide service visibility, efficiencies and network performance excellence.

References:

ABI Research: Expansion of 5G SA Core Networks key to 5G subscription growth

5G SA networks (real 5G) remain conspicuous by their absence

Swisscom, Ericsson and AWS collaborate on 5G SA Core for hybrid clouds

New IEEE 802.11bb standard to significantly boost LiFi market

The IEEE Standards Board has approved IEEE 802.11bb as the latest global light communications standard. The bb standard marks a significant milestone for the LiFi market, as it provides a globally recognized framework for deployment of LiFi technology.

IEEE 802,11, the working group which developed the Wi-Fi standards, formed the Light Communications 802.11bb Task Group in 2018, chaired by pureLiFi and supported by Fraunhofer HHI, two entities that have been at the forefront of LiFi development efforts. LiFi, which stands for “light fidelity,” is a wireless technology that uses light rather than radio frequencies to transmit data. Ratification of the standard was concluded in June 2023.

The IEEE 802.11bb standard defines the physical layer specifications and system architectures for wireless communication using light waves. This new standard sets the foundation for the widespread adoption of LiFi technology and paves the way for the interoperability of LiFi systems with the successful WiFi standard.

The technology has been in development for years now, but the lack of a globally-recognized standard to go with it means there has been little enthusiasm from OEMs to develop and commercialise LiFi-enabled products. That could all change now, thanks to the release of the official LiFi standard.

“The release of the IEEE 802.11bb standard is a significant moment for the wireless communications industry,” said Nikola Serafimovski, VP of standardisation at pureLiFi, in a statement on Wednesday.

LiFi is a wireless technology that uses light rather than radio frequencies to transmit data. By harnessing the light spectrum, LiFi can unleash faster, more reliable wireless communications with unparalleled security compared to conventional technologies such as WiFi and 5G. The Light Communications 802.11bb Task Group was formed in 2018 chaired by pureLiFi and supported by Fraunhofer HHI, two firms which have been at the forefront of LiFi development efforts. Both organisations aim to see accelerated adoption and interoperability not only between LiFi vendors but also with WiFi technologies as a result of these standardisation efforts.

Richard Webb, Director, Network Infrastructure at industry analyst firm CCS Insights, “The IEEE 802.11bb standard is an important milestone for LiFi technology placing LiFi as a complementary and integrated technology alongside the highly successful WiFi standard. This opens-up exciting new opportunities for LiFi to work seamlessly with WiFi and make communications better in a range of applications, from high-speed, secure internet access in the home and office to expanding next generation experiences to wider markets such as XR and spatial computing.”

“The release of the IEEE 802.11bb standard is a significant moment for the wireless communications industry,” said pureLiFi’s VP of Standardisation, Nikola Serafimovski, who chaired the 802.1bb Task Group.

“Through the activity of the 802.11bb task group, LiFi attracted interest from some of the biggest industry players ranging from semiconductor companies to leading mobile phone manufacturers. We worked with these key stakeholders to create a standard that will provide what the industry needs to adopt LiFi at scale. I would like to thank the support of Tuncer Baykas as Vice-Chair, and Volker Jungnickel as technical editor for helping make this process so successful.”

Volker Jungnickel from Fraunhofer HHI, technical editor of the task group, commented on the importance of a global LiFi standard: “The IEEE 802.11bb standard is a critical step to enable interoperability between multiple vendors. It allows for the first time LiFi solutions inside the WiFi ecosystem. This is essential for the development of new and innovative applications. LiFi can replace cables by short-range optical wireless links and connect numerous sensors and actuators to the Internet. We believe that this will create a future mass market. Fraunhofer HHI is looking forward to work with LiFi vendors from lighting and communication industries to make this a reality.”

pureLiFi, a pioneering company in the development of LiFi technology, has already developed the world’s first standards-compliant devices including the recently released Light Antenna ONE.

Analogous to the antenna chain in a radio frequency (RF) system such as WiFi, Light Antenna ONE inherently enables 802.11bb compliance. It can be integrated with existing WiFi chipsets that ship in the billions annually. With Light Antenna ONE, LiFi simply appears to the system as if it were another band of WiFi.

“pureLiFi is delighted to see the release of the IEEE 802.11bb standard,” said Alistair Banham, CEO of pureLiFi. “This is a significant moment for the LiFi industry, as it provides a clear framework for the deployment of LiFi technology on a global scale. We are proud to have played a leading role in its creation and to be ready with the world’s first standards-compliant devices. The existence of a global standard gives confidence to device manufacturers who will deploy LiFi at scale.”

With the release of the IEEE 802.11bb standard, pureLiFi believes that LiFi as a complimentary and additive solution to RF communications is now poised to take its place in the wireless communication market, offering unprecedented speed, security, and reliability to users around the world.”

Fraunhofer HHI is a world leader in the development of mobile and optical communication networks and systems as well as processing and coding of video signals. HHI has studied use cases for indoor and outdoor applications with early adopters and made sustainable contributions to standards. HHI offers all building blocks for state-of-the-art LiFi systems, tailors prototypes for special applications and conducts field trials in real scenarios.

“Fraunhofer HHI welcomes the new IEEE 802.11bb,” said Dominic Schulz, lead of LiFi development at Fraunhofer HHI.

“ LiFi offers high-speed mobile connectivity in areas with limited RF, like fixed wireless access, classrooms, medical, and industrial scenarios. It complements or serves as an alternative to WiFi and 5G. 802.11bb integrates easily with existing infrastructures. Operating in an exclusive optical spectrum ensures higher reliability and lower latency and jitter. Light’s line-of-sight propagation enhances security by preventing wall penetration, reducing jamming and eavesdropping risks, and enabling centimetre-precision indoor navigation.”

With IEEE Std 802.11bb, LiFi has a first solution addressing mass-market requirements, such as low cost, low energy and high volumes. Industry can fully reuse WiFi protocols over the light medium. This will bring traffic offloading, security and navigation capabilities of WiFi to the next level.”

References:

https://telecoms.com/522689/ieee-puts-the-spotlight-on-lifi-tech/

https://www.fiercewireless.com/tech/ieee-standardization-shines-spotlight-lifi