AI RAN

Will “AI at the Edge” transform telecom or be yet another telco monetization failure?

New Telco Opportunity – AI at the Edge:

At MWC 2026 last week, there were a flurry of claims that “AI at the Edge” would transform the telecom industry. One of many examples is an article titled, “The AI edge boom is giving telecom a new strategic role.” In that piece, Jeff Aaron, vice president of product and solutions marketing at Hewlett Packard Enterprise (HPE) spoke with theCUBE’s John Furrier at MWC Barcelona, during an exclusive broadcast on theCUBE, SiliconANGLE Media’s livestreaming studio. They discussed telecom edge AI and why networking is becoming a strategic foundation for data-centric services. Aaron said:

“A big reason for [reignited interest in routing] is AI workloads. They’re moving everywhere now. They have to move to the edge. For them to move to the edge, you’ve got to get them outside of the factory and to all the locations. We’re right in the core of that, and it’s super exciting.”

As AI expands to the edge, data will need to move not only to local compute, but also between many distributed edge sites, making routing paramount. There are four ways AI infrastructure is scaling — inside data centers and across distributed edge locations, according to Aaron.

“There’s scale-out, scale-across, scale-up, and on-ramp. Two are within the data center — scale-out and scale-up — but scale-across and edge on-ramp basically mean you got to figure out how to connect to those areas, and those are just networking,” he added.

Scale-across refers to connecting distributed data centers and edge locations, while edge on-ramp brings remote sites such as factories or branch locations into the network to access AI services. Supporting those distributed environments creates an opportunity for HPE to bring networking and compute together into a more integrated infrastructure stack. At MWC 2026 Barcelona, those trends are clearly coming into focus, according to Aaron.

“Data is moving everywhere right now, and the network is back. The network isn’t just plumbing. The network is how you build a value-added service using an AI workload as a telco infrastructure,” he added.

Telecom carriers are now urgently trying to move from being “dumb data pipes” to becoming “AI performance platforms” by leveraging their geographically distributed infrastructure to host AI closer to the end user. They urgently want to pivot from selling just bandwidth and connectivity to selling outcomes and intelligence with a heavy focus on industrial and enterprise-specific edge deployments. They are considering the following services and business models:

- Infrastructure as a Service (IaaS) & GPUaaS: Offering raw computing power, specifically GPUs, from edge data centers to enterprises that need low-latency processing without building their own facilities.

- Sovereign AI Clouds: Providing AI services that guarantee data remains within national borders, appealing to government and highly regulated sectors like finance and healthcare.

- API Monetization: Exposing real-time network data (e.g., location intelligence, predictive network quality, fraud risk scoring) via APIs that enterprises pay to integrate into their own applications.

- Outcome-Based Pricing: Charging for specific business results, such as a “guaranteed video call quality” or “fraud loss reduction share,” rather than just data usage.

- AI-as-a-Service (AIaaS): Bundling pre-trained models or specialized AI agents (e.g., for customer service or industrial monitoring) with connectivity

Major Carrier AI Edge Deployment Plans:

- AT&T:

- Launched Connected AI for Manufacturing in March 2026, which unifies 5G, IoT, and generative AI to provide real-time fault detection (claiming a 70% reduction in waste).

- Deploying “Edge Zones” in major U.S. cities (Detroit, LA, Dallas) to allow developers to run low-latency, cloud-based software locally.

- Partnering with AWS to link fiber and 5G directly into AWS environments for distributed AI workloads.

- Verizon:

- Unveiled Verizon AI Connect, a suite of products designed to manage resource-intensive AI workloads for hyperscalers like Google Cloud and Meta.

- Trialing V2X (Vehicle-to-Everything) platforms to provide carmakers with standardized APIs for low-latency edge processing in autonomous driving.

- Collaborating with NVIDIA to integrate GPUs into private 5G networks for on-premise AI inferencing in robotics and AR.

- SK Telecom (SKT):

- Announced an “AI Native” strategy at MWC 2026, including a roadmap for AI-RAN (Radio Access Network) that uses GPUs to optimize network performance and host user AI apps simultaneously.

- Building a Manufacturing AI Cloud powered by over 2,000 NVIDIA RTX GPUs to support digital twin simulations and robotics.

- Expanding AI Data Centers (AIDC) across South Korea and Southeast Asia (Vietnam, Malaysia) using energy-optimized LNG-powered facilities.

- Orange & Deutsche Telekom:

- Deploying AI-powered planning tools to cut fiber rollout costs and optimize site power consumption by up to 33% using AI “Deep Sleep” modes.

- Focusing on Sovereign AI strategies to ensure data governance for European enterprise customers.

- Vodafone:

- Utilizing AI/ML applications for daily power reduction at 5G sites and testing autonomous network healing via AI agents

- BT:

- Offers 5G-connected VR for manufacturing design teams (e.g., Hyperbat) to collaborate on 3D models in real-time.

| Product Category | Primary Target | Key Value Proposition |

|---|---|---|

| AI-RAN | Industry 4.0 | Seamless, ultra-low latency for robotics and sensing. |

| Connected AI Platforms | Manufacturing | Real-time predictive maintenance and waste reduction. |

| AI-as-a-Service (AIaaS) | Developers/SMBs | Access to GPU power and pre-trained models via telco edge nodes. |

| Network Slicing APIs | App Developers | Programmatic control over bandwidth for AR/VR and gaming. |

…………………………………………………………………………………………………………………………………………………………………………………………..

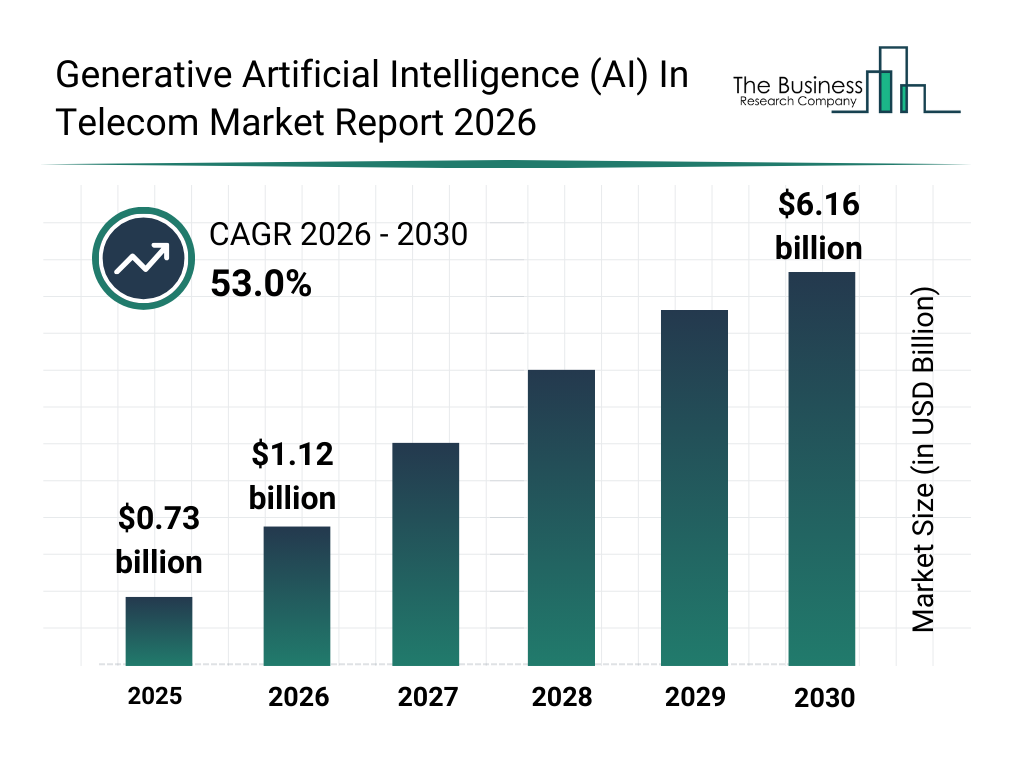

A Dissenting View of “AI at the Edge”:

The global market for AI within the global telecommunications sector is valued at $6.69 billion in 2026, growing at a compound annual rate (CAGR) of 41.9% from 2025. The broader edge AI market—including hardware, software, and services—is forecast to reach $29.98 billion in 2026, according to The Business Research Company. We think those estimates are way too high.

The market research firm states:

………………………………………………………………………………………………………

Author’s Opinion:

Unless telcos change their corporate culture along with slowing the footprint growth of cloud service providers/hyperscalers, we think that AI at the Edge will be yet another telco monetization failure. Just like their failure to monetize: 4G LTE apps, the telco cloud, 5G, multi-access edge computing (MEC), OpenRAN, LPWANs and other telecom technologies that never lived up to their promise and potential.

That’s largely because telcos are very weak: developing IT platforms, compute services, killer applications, and rapid execution of new services (e.g. 5G services require a 5G SA core network which telcos were very slow to deploy). Telecom execs themselves cite cultural and speed‑of‑change issues: the industry is not organized like a software company, so it struggles to iterate products at AI/cloud pace. Also, telcos historically struggle with software. Managing distributed GPU clusters is vastly different from managing cell towers.

After spending billions on 5G with very little or no ROI, investors are skeptical of the increased capex required for AI-grade edge servers which must be maintained by telcos. Those servers will be expensive (especially if they contain clusters of Nvidia GPUs) and consume a lot of power, which is a critical issue at the edge of the carrier’s network.

Many network operators frame AI/edge as “network optimization” or “utilizing underused sites,” not as building monetizable AI platforms with APIs, SDKs, and ecosystems. This mirrors 5G, where huge RAN/core builds were not matched by a clear product and platform strategy, leaving value to OTTs and hyperscalers which are extending their control planes and protocol stacks to the network edge (local zones, operator co‑lo, on‑premises stacks).

Telcos risk becoming “dumb pipes” for AI traffic if they can’t provide a superior developer ecosystem. If they only sell space/power/connectivity, the cloud service providers will continue to own the developer and AI value chain. Analysts warn that edge is a “right to participate, not a right to win.” As such, value accrues to whoever owns the AI platform, tools, marketplace, and pricing power, not the entity that provides connectivity, PoP or cell towers.

Data fragmentation and weak “intelligence” layer:

-

AI monetization depends on high‑quality, cross‑domain data, but telco data is fragmented across OSS, BSS, probes, and partner systems; without unification, it is hard to expose compelling network/edge intelligence services.

-

Analysts emphasize that failure here reduces telcos to generic GPU landlords, while higher‑margin offers (real‑time quality, fraud, identity, mobility/context APIs) remain unrealized.

Narrow internal focus on cost savings:

-

Many operators’ early AI focus is inward (Opex reduction in assurance, planning, customer care) rather than building external, revenue‑generating products, echoing how early 5G was justified mainly on cost/efficiency.

-

Commentators warn that if AI/edge remains a “network efficiency” play, the commercial upside will go to cloud/AI natives that turn similar capabilities into products sold to enterprises.

What analysts say telcos must do differently:

-

Build “Sovereign AI factories” and edge AI clouds: GPU‑enabled sites with cloud‑like developer experience (APIs, self‑service portals, metering, SLAs) and clear sovereign/regional guarantees.

-

Combine differentiated connectivity with AI services (latency‑backed SLAs, AI‑on‑RAN, domain‑specific models for verticals) and use modern, flexible commercial models instead of just selling bandwidth or colocation.

Conclusions:

In summary, the main risk for telcos is to successfully transition from owning and maintaining network infrastructure to owning and operating AI platforms and products at software industry speed. AI at the edge is less of a new service or product and more an architectural upgrade. The two ways telcos can benefit are from:

- Internal cost reduction: If telcos use it to lower their own costs (fraud prevention, risk management, predictive maintenance, fault isolation, self-healing networks, etc.), it’s an automatic win but won’t increase the top line.

- Revenue from new AI -Edge services, e.g. Verizon uses edge-based video analytics in warehouses to improve inventory turnover by up to 40%. If they expect to charge a massive premium for “AI-enabled 5G,” they face the same monetization wall that has doomed them for the past 20 years!

References:

https://siliconangle.com/2026/03/04/telecom-edge-ai-makes-networking-strategic-mwc26/

https://www.nvidia.com/en-us/lp/ai/the-blueprint-for-ai-success-ebook/

AT&T and AWS to deliver last mile connectivity for AI workloads; AT&T Geo Modeler™ AI simulation tool

Analysis: Edge AI and Qualcomm’s AI Program for Innovators 2026 – APAC for startups to lead in AI innovation

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Private 5G networks move to include automation, autonomous systems, edge computing & AI operations

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

Nvidia AI-RAN survey results; AI inferencing as a reinvention of edge computing?

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

CES 2025: Intel announces edge compute processors with AI inferencing capabilities

Ericsson and Intel collaborate to accelerate AI-Native 6G; other AI-Native 6G advancements at MWC 2026

Ericsson and Intel at MWC 2026:

Building on milestones in Cloud RAN, 5G Core, and open network innovation, Ericsson and Intel are showcasing joint technology advancements at the Mobile World Congress (MWC) 2026 in Barcelona this week. Demonstrations can be experienced at the Ericsson Pavilion (Hall 2), Intel Booth (Hall 3, Stand 3E31), and across partner event spaces, highlighting the companies’ shared progress in enabling the next era of AI-driven networks.

The two companies are strengthening their long-standing technology partnership to accelerate ecosystem readiness for AI-native 6G networks and use cases. The expanded collaboration spans next-generation mobile connectivity, cloud infrastructure, and compute acceleration — with a focus on AI-driven RAN and packet core evolution, platform-level security, and scalable cloud-native architectures designed to shorten time-to-market for advanced network solutions.

“6G is not merely an iteration of mobile technology; it will serve as the foundational infrastructure distributing AI across devices, the edge, and the cloud,” said Börje Ekholm, President and CEO of Ericsson. “With our deep history in network innovation and global-scale operator deployments, Ericsson is uniquely positioned to drive practical 6G integration from research to commercialization.”

Lip-Bu Tan, CEO of Intel, added: “Intel’s vision is to lead the industry in unifying RAN, Core, and edge AI to enable seamless deployment of AI-native 6G environments. Together with Ericsson, we are proving that next-generation connectivity can be open, energy-efficient, secure, and intelligent. With future Ericsson Silicon built on Intel’s most advanced process technologies, coupled with Intel Xeon-powered AI-RAN ready Cloud RAN and collaborative multi-year research efforts, we are delivering the performance, efficiency, and supply assurance demanded by leading operators worldwide.”

As 6G transitions from research to commercialization, the industry must align around a mature, standards-based ecosystem. The Ericsson–Intel collaboration aims to accelerate development of high-performance, energy-efficient compute architectures optimized for both AI for Networks and Networks for AI.

AI-native 6G will fuse intelligent, programmable network functions with distributed compute and real-time sensing, bringing processing power closer to the network edge and enabling ultra-responsive, adaptive services. This convergence will enhance network efficiency, agility, and service intelligence across future deployments.

About Ericsson:

Ericsson‘s high-performing networks provide connectivity for billions of people every day. For 150 years, we’ve been pioneers in creating technology for communication. We offer mobile communication and connectivity solutions for service providers and enterprises. Together with our customers and partners, we make the digital world of tomorrow a reality.

About Intel:

Intel is an industry leader, creating world-changing technology that enables global progress and enriches lives. Inspired by Moore’s Law, we continuously work to advance the design and manufacturing of semiconductors to help address our customers’ greatest challenges. By embedding intelligence in the cloud, network, edge and every kind of computing device, we unleash the potential of data to transform business and society for the better.

…………………………………………………………………………………………………………………………………………………………

Related AI-Native 6G Announcements at MWC 2026:

In addition to the Ericsson-Intel collaboration, several vendors and operators announced AI-native 6G advancements or related demos at MWC Barcelona 2026. These initiatives emphasize AI-RAN integration, software-defined architectures, and ecosystem partnerships to bridge 5G-A to 6G.

NVIDIA Multi-Partner Commitment: NVIDIA rallied operators and vendors including Booz Allen, BT Group, Cisco, Deutsche Telekom, Ericsson, Nokia, SK Telecom, SoftBank, and T-Mobile to build open, secure AI-native 6G platforms. The focus is on software-defined wireless with AI embedded in RAN, edge, and core for integrated sensing, communications, and interoperability.

Nokia AI-RAN: Nokia highlighted new partnerships with Dell, Quanta, Red Hat, SuperMicro, NVIDIA, and operators like T-Mobile, Indosat Ooredoo Hutchison, BT, Elisa, NTT DOCOMO, and Vodafone for AI-RAN trials paving the way to cognitive 6G networks. Live demos at Nokia’s Hall 3 Booth 3B20 included Southeast Asia’s first AI-RAN Layer 3 5G call on shared GPU infrastructure and vision AI for immersive services.

T-Mobile & Deutsche Telekom Hub: T-Mobile US and (major shareholder) Deutsche Telekom launched a joint 6G Innovation Hub targeting AI-native autonomous networks, secure sensing/positioning, and connectivity-compute convergence for Physical AI. It builds on agentic AI proofs like network-integrated translation, emphasizing “kinetic tokens” for real-time physical world control.

ZTE GigaMIMO 6G Prototype: ZTE unveiled the world’s first 6G prototype with 2000+ U6G-band antenna elements (GigaMIMO), powered by AI algorithms for 10x capacity over 5G-A, 30% spectral efficiency gains, and AI-driven immersive services. Booth 3F30 demos integrate AI across connectivity, computing, and devices for “AI serves AI” networks.

Qualcomm Agentic AI RAN: Qualcomm announced AI-native RAN management services in its Dragonwing suite for autonomous 6G-grade networks, plus new Open RAN AI features for performance optimization. CEO Cristiano Amon’s keynote focused on “Architecting 6G for the AI Era,” with device-to-data-center transformations.

Huawei U6GHz for 6G Path:

Huawei released all-scenario U6GHz products (macro/micro sites, microwave) with AI-centric solutions for 5G-A capacity (100 Gbps downlink) and low-latency AI apps, enabling smooth 6G evolution. Emphasizes hyper-resolution MU-MIMO and multi-band coordination for indoor/outdoor AI experiences.

Summary Chart:

| Vendor/Operator | Key Focus | Partners/Demos | Booth/Location |

|---|---|---|---|

| NVIDIA | Open AI-native platforms | Multiple operators/vendors | MWC general |

| Nokia | AI-RAN trials & cognitive networks | NVIDIA, T-Mobile, IOH et al. | Hall 3, 3B20 |

| T-Mobile/DT | Physical AI hub | Joint R&D | Announced pre-MWC |

| ZTE | GigaMIMO 6G prototype | China Mobile, Qualcomm | Hall 3, 3F30 |

| Qualcomm | Agentic RAN automation | Open RAN ecosystem | Keynote & demos |

| Huawei | U6GHz AI-centric evolution | Carrier-focused | MWC showcase |

…………………………………………………………………………………………………………………………………………………………………………………….

References:

NVIDIA and global telecom leaders to build 6G on open and secure AI-native platforms + Linux Foundation launches OCUDU

Comparing AI Native mode in 6G (IMT 2030) vs AI Overlay/Add-On status in 5G (IMT 2020)

SKT 6G ATHENA White Paper: a mid-to-long term network evolution strategy for the AI era

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Nokia and Rohde & Schwarz collaborate on AI-powered 6G receiver years before IMT 2030 RIT submissions to ITU-R WP5D

SK Telecom, DOCOMO, NTT and Nokia develop 6G AI-native air interface

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

NVIDIA and global telecom leaders to build 6G on open and secure AI-native platforms + Linux Foundation launches OCUDU

- AI-RAN Integration: Shifting from fixed-function hardware to AI-RAN architecture to turn networks into programmable AI infrastructure.

- Architectural Resilience: Implementing open and trusted principles to ensure interoperability, supply-chain security, and rapid innovation cycles.

- Integrated Sensing & Communication: Leveraging AI-native platforms to enable real-time intelligence and decision-making at the network edge.

- Scalability: Addressing the complexity of 6G to support billions of autonomous endpoints that demand higher security and lower latency than current architectures can provide.

The NVIDIA AI Aerial platform is a software-defined, cloud-native framework for building, training, and deploying AI-native 5G and 6G wireless networks. It transitions traditional fixed-function hardware to a programmable, multi-tenant infrastructure that runs both Radio Access Network (RAN) and AI workloads simultaneously on NVIDIA-accelerated computing.

Image Credit: NVIDIA

Quotes:

“AI is driving the largest infrastructure buildout in history, and telecommunications is the next frontier,” stated Jensen Huang, founder and CEO of NVIDIA. “By building AI-RAN, we are transforming global telecom networks into a ubiquitous AI fabric.”

Allison Kirkby, chief executive of BT Group, said: “Connectivity is the backbone of economic growth, and with this collaboration, we’re helping lay the foundations for a future ecosystem that is intelligent, sustainable and secure. By building on open and trustworthy AI native platforms, we can simplify future technologies like 6G, ensuring they build upon the strengths of today’s 5G networks while still unlocking powerful new capabilities at scale.”

Tim Höttges, CEO of Deutsche Telekom AG, said: “Best network, best customer experience — that remains our promise. With an open, intelligent and trusted 6G infrastructure, we are laying the foundation for the era of physical AI and unlocking new value for our customers, for industry and for society.”

Arielle Roth, Assistant Secretary of Commerce for Communications and Information, and Administrator at the National Telecommunications and Information Administration, said: “America’s 6G leadership will be critical to our nation’s economic prosperity, national security and global competitiveness. Today’s announcement demonstrates that the United States and our allies and partners around the world are leading in this next-generation technology. We look forward to the next steps from this international industry coalition as they advance and implement their shared 6G vision.”

Jung Jai-hun, president and CEO of SK Telecom, said: “SKT is evolving telco infrastructure to serve as the foundation for the AI era, where connectivity serves as a platform for intelligence and innovation. Together, we can build open, trusted infrastructure that drives a global ecosystem of AI innovation.”

Hideyuki Tsukuda, executive vice president and chief technology officer of SoftBank Corp., said: “Al-native 6G will transform wireless networks into secure, software-defined infrastructure that supports the next wave of global innovation. SoftBank Corp. is driving this innovation with NVIDIA by advancing open and trusted platforms that enable interoperability, resilience and continuous evolution at scale.”

Srini Gopalan, CEO of T-Mobile, said: “We’re at a pivotal moment. In the U.S., we’ve laid the foundation with 5G Advanced and AI-native networks where intelligence lives inside the network. As 6G becomes the backbone of the AI era, telecom will serve as the nervous system of the digital economy, enabling autonomous systems and intelligent industries at scale and unlocking new value for customers and businesses alike. T-Mobile is proud to help define what’s next through deep ecosystem collaboration and sustained innovation.”

……………………………………………………………………………………………………………………………………………

Linux Foundation launches OCUDU:

Separately, the Linux Foundation (LF) today announced the formation of the Open Centralized Unit Distributed Unit (OCUDU) Ecosystem Foundation, an open collaboration hub dedicated to building, scaling, and sustaining the OCUDU technical project assets and leveraging them to establish a foundational reference platform for RAN including AI based algorithms and solutions. The OCUDU Ecosystem Foundation provides a critical mechanism for industry vendors to optimally guide OCUDU development to support 5G and early AI Native 6G services.

The OCUDU Ecosystem Foundation brings together an ecosystem across enterprise, telecom operators, cloud providers, equipment vendors, and research institutions to co-develop and integrate critical components required for 5G and early 6G deployments. This community-driven model complements global standards from 3GPP and O-RAN alliance and industry alliances like AI-RAN alliance. This global effort ensures that innovation, transparency, and interoperability remain at the core of global software-defined RAN evolution.

“By aligning global efforts under the Linux Foundation, we’re building an open, trusted, and secure open source platform to power the next decade of wireless innovation,” said Arpit Joshipura, general manager, Networking, Edge and IoT, at the Linux Foundation. “The OCUDU Ecosystem Foundation represents a key step forward in open source RAN, specifically for CU and DU.”

“This initiative brings the best of the open source model to one of the most critical layers of future wireless: the foundation for an interoperable, software-defined radio access network,” said Dr. Tom Rondeau, principal director for FutureG. “By shifting the maintenance of these common components to a collaborative, open-source project, under neutral governance at the Linux Foundation, we enable our industry partners to focus their resources on the innovative and monetizable technologies that are most effective for the nation. We are building a foundation that enables shared success and accelerates progress for the entire ecosystem. We are looking forward to seeing this approach provide a vital platform for strengthening our relationships and collaboration with our allies and international partners.”

“The key to driving innovation in wireless is to leverage a broad ecosystem of experts in networking, radio software, and emerging AI technologies,” said Joe Kochan, CEO of NSC. “What started with a competitive proposal process to elicit the best technology solutions from among NSC’s large and diverse membership is now expanding under the Linux Foundation, and NSC is proud to continue partnering with both LF and the FutureG team to advance OCUDU development efforts and build the next generation of wireless capabilities.”

References:

Comparing AI Native mode in 6G (IMT 2030) vs AI Overlay/Add-On status in 5G (IMT 2020)

SKT 6G ATHENA White Paper: a mid-to-long term network evolution strategy for the AI era

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Nokia and Rohde & Schwarz collaborate on AI-powered 6G receiver years before IMT 2030 RIT submissions to ITU-R WP5D

SK Telecom, DOCOMO, NTT and Nokia develop 6G AI-native air interface

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Analysis: Rakuten Mobile and Intel partnership to embed AI directly into vRAN

Today, Rakuten Mobile and Intel announced a partnership to embed Artificial Intelligence (AI) directly into the virtualized Radio Access Network (vRAN) stack. While vRAN currently represents a small percentage of the total RAN market (Dell’Oro Group recently forecasts vRAN to account for 5% to 10% of the total RAN market by 2026), this partnership could boost increase that percentage as it addresses key adoption hurdles—performance, power, and AI integration. Key areas of innovation include:

- Enhanced Wireless Spectral Efficiency: Optimizing spectrum utilization for superior network performance and capacity.

- Automated RAN Operations: Streamlining network management and reducing operational complexities through intelligent automation.

- Optimized Resource Allocation: Dynamically allocating network resources for maximum efficiency and subscriber experience.

- Increased Energy Efficiency: Significantly reducing power consumption in the RAN, contributing to sustainable network operations.

The partnership essentially aims to make vRAN superior in performance and TCO (Total Cost of Ownership) compared to traditional, proprietary, purpose built RAN hardware.

“We are incredibly excited to expand our collaboration with Intel to pioneer truly AI-native RAN architectures,” said Sharad Sriwastawa, co-CEO and CTO, Rakuten Mobile. “Together, we are validating transformative AI-driven innovations that will not only shape but define the future of mobile networks. This partnership showcases how intelligent RAN can be achieved through the seamless and efficient integration of AI workloads directly within existing vRAN software stacks, delivering unparalleled performance and efficiency.”

Rakuten Mobile and Intel are engaged in rigorous testing and validation of cutting-edge RAN AI use cases across Layer 1, Layer 2, and comprehensive RAN operation and network platform management. A core objective is the seamless integration of AI directly into the RAN stack, meticulously addressing integration challenges while upholding carrier-grade reliability and stringent latency requirements.

Utilizing Intel FlexRAN reference software, the Intel vRAN AI Development Kit, and a robust suite of AI tools and libraries, Rakuten Mobile is collaboratively training, optimizing, and deploying sophisticated AI models specifically tailored for demanding RAN workloads. This collaborative effort is designed to realize ultra-low, real-time AI latency on Intel Xeon 6 SoC, capitalizing on their built-in AI acceleration capabilities, including AVX512/VNNI and AMX.

“AI is transforming how networks are built and operated,” said Kevork Kechichian, Executive Vice President and General Manager of the Data Center Group, Intel Corporation. “Together with Rakuten, we are demonstrating how AI benefits can be achieved in vRAN. Intel Xeon processors power the majority of commercial vRAN deployments worldwide, and this transformation momentum continues to accelerate. Intel is providing AI-ready Xeon platforms that allow operators like Rakuten to design AI-ready infrastructure from the ground up, with built-in acceleration capabilities.”

Rakuten says they are “poised to unlock new levels of RAN performance, efficiency, and automation by embedding AI directly into the RAN software stack, this AI-native evolution represents the future of cloud-native, AI-powered RAN – inherently software-upgradable and built on open, general-purpose computing platforms. Additionally, the extended collaboration between Rakuten Mobile and Intel marks a significant step toward realizing the vision of autonomous, self-optimizing networks and powerfully reinforces both companies’ commitment to open, programmable, and intelligent RAN infrastructure worldwide.”

……………………………………………………………………………………………………………………………………………………………………..

- AI-Native Efficiency & Performance: The collaboration focuses on integrating AI to improve network performance and energy efficiency, which is a major pain point for operators. By embedding AI directly into the vRAN stack, they are enhancing wireless spectral efficiency, reducing power consumption, and automating RAN operations.

- Leveraging High-Performance Hardware: The initiative utilizes Intel® Xeon® 6 processors with built-in vRAN Boost. This eliminates the need for external, power-hungry accelerator cards, offering up to 2.4x more capacity and 70% better performance-per-watt.

- Validation of Large-Scale Commercial Viability: Rakuten Mobile operates the world’s first fully virtualized, cloud-native network. Its continued collaboration with Intel to make the vRAN AI-native provides a proven blueprint for other operators, reducing the perceived risk of adopting vRAN, particularly in brownfield (existing) networks.

- Acceleration of Open RAN Ecosystem: The collaboration supports the broader push towards Open RAN, which is expected to see a significant rise in market share, doubling between 2022 and 2026.

………………………………………………………………………………………………………………………………………………………………

- Market Share Shift: Omdia forecasts that vRAN’s share of the RAN baseband subsector will reach 20% by 2028. That’s a significant jump from its current low single-digit percentage.

- Explosive CAGR: The global vRAN market is projected to grow from approximately $16.6 billion in 2024 to nearly $80 billion by 2033, representing a 19.5% CAGR.

- Small Cell Dominance: By the end of 2026, it is estimated that 77% of all vRAN implementations will be on small cell architectures, a key area where Rakuten and Intel have demonstrated success.

References:

https://corp.mobile.rakuten.co.jp/english/news/press/2026/0210_01/

Virtual RAN gets a boost from Samsung demo using Intel’s Grand Rapids/Xeon Series 6 SoC

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

vRAN market disappoints – just like OpenRAN and mobile 5G

LightCounting: Open RAN/vRAN market is pausing and regrouping

Dell’Oro: Private 5G ecosystem is evolving; vRAN gaining momentum; skepticism increasing

https://www.mordorintelligence.com/industry-reports/virtualized-ran-vran-market

https://www.grandviewresearch.com/industry-analysis/virtualized-radio-access-network-market-report

Comparing AI Native mode in 6G (IMT 2030) vs AI Overlay/Add-On status in 5G (IMT 2020)

Executive Summary:

AI integration in 6G specifications (3GPP) and standards (ITU-R IMT 2030) highlights a strategic shift in the telecom industry towards AI-native networks, with telecom industry heavyweights like Huawei, Samsung, Ericsson, and Nokia actively developing foundational technologies. Unlike 5G, where AI and machine learning were limited applications or add-on features over existing architecture, 6G will incorporate AI from the onset with an “AI native” approach where intelligence will allow the network to be smart, agile, and able to learn and adapt according to changing network dynamics.

This transformation is necessary because future 6G networks will be too complex for human operators to manage, requiring AI-empowered and learning-driven networks that can facilitate zero-touch network management through capabilities including learning, reasoning, and decision-making.

- AI-Native Networks: The industry consensus is that 6G will be “AI-native,” meaning artificial intelligence will be built directly into the core functions of network control, resource management, and service orchestration. This moves AI from an optimization layer in 5G to an foundational element in 6G.

AI Native Image Courtesy of Ericsson

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

- Company Initiatives:

- Huawei is focused on making AI a native element of the network architecture (AI-native 6G) rather than an overlay technology, integrating communication, sensing, computing, and intelligence. This vision, called “Connected Intelligence,” involves two aspects: AI for 6G (network automation) and 6G for AI (AI as a Service, AIaaS). More in Huawei Research Areas below.

- Samsung is a major proponent of AI-RAN (Radio Access Network) technology. The company hosted a summit in November 2025 to showcase working AI-RAN technology that autonomously optimizes network performance and is conducting joint research with SK Telecom (SKT) on AI-supported RAN. Samsung sees vRAN (virtualized RAN) as a key enabler for “AI-native, 6G-ready networks”.

- Ericsson emphasizes the necessity of a strong 5G Standalone (5G SA) foundation for an AI future, using AI to manage and automate current networks in preparation for 6G’s demands. Ericsson is also integrating agentic AI into its platforms for more autonomous network management.

- Nokia is deepening its AI push, licensing software to expand AI use in mobile networks and preparing for early field trials in 2026 by porting baseband software to platforms like NVIDIA’s, which opens the door for more advanced AI use cases.

- Industry Analysis and Trends:

- Standardization: 2026 is crucial as formal 6G specification work begins in earnest within 3GPP with Release 21. In WP5D, the IMT 2030 RIT/SRIT standardization work will commence at the February 2027 meeting with the final deadline for submissions at the February 2029 meeting. More in the ITU-R WP5D section below.

- The AI-RAN Alliance is an industry initiative (not a traditional SDO) focused on accelerating real-world AI applications and integration within the RAN. It works alongside SDOs, providing industry insights and pushing for rapid validation and testing of AI-RAN technologies, with a specific focus on leveraging accelerated computing.

- Automation and Efficiency: AI-native algorithms in 6G are expected to deliver extreme spectrum and energy efficiency, significantly reducing operational costs for telcos while improving reliability and performance.

- Monetization Challenges: Despite the technological promise, analysts caution that 6G remains largely theoretical for now. Some operators are stalling on full 5G SA deployment, waiting to move to 6G-ready cores later in the decade, leading to concerns that 5G SA might become an “odd generation.”

- Infrastructure Constraints: The physical demands of AI infrastructure, particularly energy consumption and construction timelines, are becoming operational realities that may bound the pace of AI growth in 2026, regardless of software advancements.

- ITU-R Working Party (WP) 5D is making AI a native and foundational element of the 6G (IMT-2030) system, rather than the “add-on” or “overlay” status it had in 5G (IMT 2020). This shift is being achieved through the definition of specific AI capabilities and requirements that future 6G technologies must inherently support. In particular:

- Defining AI as a Core Capability: The Recommendation ITU-R M.2160 (“Framework and overall objectives of the future development of IMT for 2030 and Beyond”) officially defines “Artificial Intelligence and Communication” as one of the six major usage scenarios and an overarching design principle for IMT-2030.

- Integrating AI into the Radio Interface: WP 5D is actively developing technical performance requirements (TPRs) and evaluation criteria for proposed 6G radio interface technologies (RITs) that inherently incorporate AI/Machine Learning (ML). This includes work on:

- AI-enabled air interface design: This involves the physical layer, potentially moving towards AI-native physical (PHY) layers that can dynamically adapt waveforms and network parameters in real-time, rather than relying on predefined, static configurations.

- AI-driven resource management: AI/ML algorithms will be crucial for real-time optimization of spectral and energy efficiency, managing complex traffic, and ensuring Quality of Service (QoS).

- Enabling AI-Driven Services: The framework for IMT-2030 is designed to support the full lifecycle of AI components, from data collection and model training to deployment and performance monitoring, enabling new AI-driven services and applications directly within the network infrastructure.

- Establishing a Formal Timeline: WP 5D has established a clear timeline for 6G standardization, with specific stages for vision, requirements, evaluation methodology, and specifications. This structured approach ensures that all proposed RITs/SRITs are evaluated against the new AI-native requirements, promoting global alignment and preventing AI from becoming a fragmented, proprietary solution.

- Stage 1 (Vision): Completed in June 2023.

- Stage 2 (Requirements & Evaluation): Targeted for completion in 2026.

- Stage 3 (Specifications): Expected by the end of 2030.

- Purpose: AI is integral to the entire network lifecycle, from initial design and deployment to autonomous operation and service creation.

- Integration Level: Intelligence is embedded across all layers of the network stack, including the physical layer (air interface), control plane, and data plane.

- Scope: AI enables core functionalities such as real-time self-optimization, self- healing capabilities, and dynamic resource allocation, rather than static, predefined configurations.

- Outcome: The creation of a fully cognitive, self-managing, and highly adaptable “intelligence fabric” capable of supporting advanced use cases like real-time holographic communication, digital twins, and autonomous systems with ultra-low latency.

| Feature | 5G (IMT-2020) | 6G (IMT-2030) |

|---|---|---|

| AI Role | Optimization tool (overlay) | Foundational and native element |

| Network Operation | Manual configuration with AI assistance | Autonomous and self-managing |

| Air Interface | Human-designed with some ML optimization | AI/ML-designed and managed |

| Complexity Management | Relies on standard protocols | Manages complexity through embedded AI/ML |

| Services Supported | Enhanced mobile broadband, basic IoT | Integrated AI & Communication, sensing, holographic comms |

–>By embedding AI into the fundamental design principles and technical requirements of IMT-2030, ITU-R WP 5D is ensuring that 6G is an AI-native network capable of self-management, self-optimization, and supporting a vast ecosystem of AI applications, a significant shift from the supplementary role AI played in 5G.

- Agentic-AI Core (A-Core): Huawei unveiled a blueprint for a 6G core network (which will be specified by 3GPP and NOT ITU) where services are managed by specialized AI agents using a large-scale network AI model called “NetGPT”. This allows the network to program, update, and execute its own control procedures automatically without human intervention, based on natural language instructions.

- Network Architecture Redesign: Huawei proposes the NET4AI system architecture, a service-oriented design that moves beyond the 5G service-based architecture. It introduces a dedicated data plane (DP) to handle the massive volume of data generated by AI and sensing services, enabling flexible and efficient many-to-many data flow for distributed learning and inference.

- Integrated Sensing and Communication (ISAC): A core pillar of Huawei’s 6G work is the native integration of sensing with communication. This allows the network to use radio waves for high-resolution sensing, localization, and imaging, creating a “digital twin” of the physical world. The large volume of data collected from sensing then serves as a source for AI model training and real-time environmental monitoring.

- Distributed Machine Learning: Huawei researches deep-edge architecture to enable massive, distributed, and collaborative machine learning (ML). This includes the development of frameworks like a two-level learning architecture that combines federated learning (FL) and split learning (SL) to optimize computing resources and ensure data privacy by keeping raw data local to devices.

- AI as a Service (AIaaS): The 6G network is designed to provide AI capabilities as a service, allowing the training and inference of large AI models to be distributed across the network (edge and cloud). This offers low-latency performance and access to rich data for AI-driven applications like collaborative robotics and autonomous driving.

- Energy Efficiency and Sustainability: The company is researching how native AI capabilities can improve overall energy efficiency by up to 100 times compared to 5G. This involves smart energy control, dynamic resource scaling, and optimizing communication paths for lower power consumption.

- Standardization and White Papers: Huawei is actively contributing to global 6G discussions and standardization bodies like the ITU-R, sharing its vision through publications such as the book 6G: The Next Horizon – From Connected People and Things to Connected Intelligence and various technical white papers. The goal is to define the technical specifications and use cases for 6G that will drive industry-wide innovation by around 2030.

References:

https://www.ericsson.com/en/reports-and-papers/white-papers/ai-native

Roles of 3GPP and ITU-R WP 5D in the IMT 2030/6G standards process

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

ITU-R WP5D IMT 2030 Submission & Evaluation Guidelines vs 6G specs in 3GPP Release 20 & 21

ITU-R WP 5D Timeline for submission, evaluation process & consensus building for IMT-2030 (6G) RITs/SRITs

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

Highlights of 3GPP Stage 1 Workshop on IMT 2030 (6G) Use Cases

Should Peak Data Rates be specified for 5G (IMT 2020) and 6G (IMT 2030) networks?

GSMA Vision 2040 study identifies spectrum needs during the peak 6G era of 2035–2040

Highlights and Summary of the 2025 Brooklyn 6G Summit

NGMN: 6G Key Messages from a network operator point of view

Nokia and Rohde & Schwarz collaborate on AI-powered 6G receiver years before IMT 2030 RIT submissions to ITU-R WP5D

Verizon’s 6G Innovation Forum joins a crowded list of 6G efforts that may conflict with 3GPP and ITU-R IMT-2030 work

Nokia Bell Labs and KDDI Research partner for 6G energy efficiency and network resiliency

Deutsche Telekom: successful completion of the 6G-TakeOff project with “3D networks”

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Qualcomm CEO: expect “pre-commercial” 6G devices by 2028

Ericsson and e& (UAE) sign MoU for 6G collaboration vs ITU-R IMT-2030 framework

KT and LG Electronics to cooperate on 6G technologies and standards, especially full-duplex communications

Highlights of Nokia’s Smart Factory in Oulu, Finland for 5G and 6G innovation

Nokia sees new types of 6G connected devices facilitated by a “3 layer technology stack”

Rakuten Symphony exec: “5G is a failure; breaking the bank; to the extent 6G may not be affordable”

India’s TRAI releases Recommendations on use of Tera Hertz Spectrum for 6G

New ITU report in progress: Technical feasibility of IMT in bands above 100 GHz (92 GHz and 400 GHz)

AI infrastructure spending boom: a path towards AGI or speculative bubble?

by Rahul Sharma, Indxx with Alan J Weissberger, IEEE Techblog

Introduction:

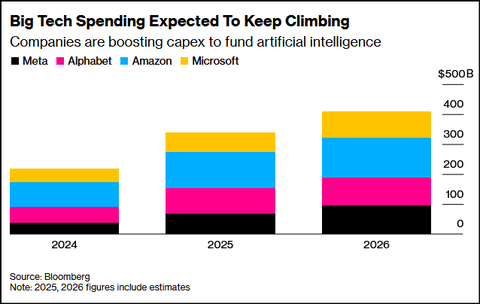

The ongoing wave of artificial intelligence (AI) infrastructure investment by U.S. mega-cap tech firms marks one of the largest corporate spending cycles in history. Aggregate annual AI investments, mostly for cloud resident mega-data centers, are expected to exceed $400 billion in 2025, potentially surpassing $500 billion by 2026 — the scale of this buildout rivals that of past industrial revolutions — from railroads to the internet era.[1]

At its core, this spending surge represents a strategic arms race for computational dominance. Meta, Alphabet, Amazon and Microsoft are racing to secure leadership in artificial intelligence capabilities — a contest where access to data, energy, and compute capacity are the new determinants of market power.

AI Spending & Debt Financing:

Leading technology firms are racing to secure dominance in compute capacity — the new cornerstone of digital power:

- Meta plans to spend $72 billion on AI infrastructure in 2025.

- Alphabet (Google) has expanded its capex guidance to $91–93 billion.[3]

- Microsoft and Amazon are doubling data center capacity, while AWS will drive most of Amazon’s $125 billion 2026 investment.[4]

- Even Apple, typically conservative in R&D, has accelerated AI infrastructure spending.

Their capex is shown in the chart below:

Analysts estimate that AI could add up to 0.5% to U.S. GDP annually over the next several years. Reflecting this optimism, Morgan Stanley forecasts $2.9 trillion in AI-related investments between 2025 and 2028. The scale of commitment from Big Tech is reshaping expectations across financial markets, enterprise strategies, and public policy, marking one of the most intense capital spending cycles in corporate history.[2]

Meanwhile, OpenAI’s trillion-dollar partnerships with Nvidia, Oracle, and Broadcom have redefined the scale of ambition, turning compute infrastructure into a strategic asset comparable to energy independence or semiconductor sovereignty.[5]

Growth Engine or Speculative Bubble?

As Big Tech pours hundreds of billions of dollars into AI infrastructure, analysts and investors remain divided — some view it as a rational, long-term investment cycle, while others warn of a potential speculative bubble. Yet uncertainty remains — especially around Meta’s long-term monetization of AGI-related efforts.[8]

Some analysts view this huge AI spending as a necessary step towards achieving Artificial General Intelligence (AGI) – an unrealized type of AI that possesses human-level cognitive abilities, allowing it to understand, learn, and adapt to any intellectual task a human can. Unlike narrow AI, which is designed for specific functions like playing chess or image recognition, AGI could apply its knowledge to a wide range of different situations and problems without needing to be explicitly programmed for each one.

Other analysts believe this is a speculative bubble, fueled by debt that can never be repaid. Tech sector valuations have soared to dot-com era levels – and, based on price-to-sales ratios, are well beyond them. Some of AI’s biggest proponents acknowledge the fact that valuations are overinflated, including OpenAI chairman Bret Taylor: “AI will transform the economy… and create huge amounts of economic value in the future,” Taylor told The Verge. “I think we’re also in a bubble, and a lot of people will lose a lot of money,” he added.

Here are a few AI bubble points and charts:

- AI-related capex is projected to consume up to 94% of operating cash flows by 2026, according to Bank of America.[6]

- Over $75 billion in AI-linked corporate bonds have been issued in just two months — a signal of mounting leverage. Still, strong revenue growth from AI services (particularly cloud and enterprise AI) keeps optimism alive.[7]

- Meta, Google, Microsoft, Amazon and xAI (Elon Musk’s company) are all using off-balance-sheet debt vehicles, including special-purpose vehicles (SPVs) to fund part of their AI investments. A slowdown in AI demand could render the debt tied to these SPVs worthless, potentially triggering another financial crisis.

- Alphabet’s (Google’s parent company) CEO Sundar Pichai sees “elements of irrationality” in the current scale of AI investing which is much more than excessive investments during the dot-com/fiber optic built-out boom of the late 1990s. If the AI bubble bursts, Pichai said that no company will be immune, including Alphabet, despite its breakthrough technology, Gemini, fueling gains in the company’s stock price.

…………………………………………………………………………………………………………………..

From Infrastructure to Intelligence:

Executives justify the massive spend by citing acute compute shortages and exponential demand growth:

- Microsoft’s CFO Amy Hood admitted, “We’ve been short on capacity for many quarters” and confirmed that the company will increase its spending on GPUs and CPUs in 2026 to meet surging demand.

- Amazon’s Andy Jassy noted that “every new tranche of capacity is immediately monetized”, underscoring strong and sustained demand for AI and cloud services.

- Google reported billions in quarterly AI revenue, offering early evidence of commercial payoff.

Macro Ripple Effects – Industrializing Intelligence:

AI data centers have become the factories of the digital age, fueling demand for:

- Semiconductors, especially GPUs (Nvidia, AMD, Broadcom)

- Cloud and networking infrastructure (Oracle, Cisco)

- Energy and advanced cooling systems for AI data centers (Vertiv, Schneider Electric, Johnson Controls, and other specialists such as Liquid Stack and Green Revolution Cooling).

| Company Name | Core Expertise | Key Solutions for AI Data Centers |

|---|---|---|

| Vertiv | Critical infrastructure (power & cooling) | Offers full-stack solutions with air and liquid cooling, power distribution units (PDUs), and monitoring systems, including the AI-ready Vertiv 360AI portfolio. |

| Schneider Electric | Energy management & automation | Provides integrated power and thermal management via its EcoStruxure platform, specializing in modular and liquid cooling solutions for HPC and AI applications. |

| Johnson Controls | HVAC & building solutions | Offers integrated, energy-efficient solutions from design to maintenance, including Silent-Aire cooling and YORK chillers, with a focus on large-scale operations. |

| Eaton | Power management | Specializes in electrical distribution systems, uninterruptible power supplies (UPS), and switchgear, which are crucial for reliable energy delivery to high-density AI racks. |

- LiquidStack: A leader in two-phase and modular immersion cooling and direct-to-chip systems, trusted by large cloud and hardware providers.

- Green Revolution Cooling (GRC): Pioneers in single-phase immersion cooling solutions that help simplify thermal management and improve energy efficiency.

- Iceotope: Focuses on chassis-level precision liquid cooling, delivering dielectric fluid directly to components for maximum efficiency and reduced operational costs.

- Asetek: Specializes in direct-to-chip (D2C) liquid cooling solutions and rack-level Coolant Distribution Units (CDUs) for high-performance computing.

- CoolIT Systems: Known for its custom direct liquid cooling technologies, working closely with server OEMs (Original Equipment Manufacturers) to integrate cold plates and CDUs for AI and HPC workloads.

–>This new AI ecosystem is reshaping global supply chains — but also straining local energy and water resources. For example, Meta’s massive data center in Georgia has already triggered environmental concerns over energy and water usage.

Global Spending Outlook:

- According to UBS, global AI capex will reach $423 billion in 2025, $571 billion by 2026 and $1.3 trillion by 2030, growing at a 25% CAGR during the period 2025-2030.

Compute demand is outpacing expectations, with Google’s Gemini saw 130 times rise in AI token usage over the past 18 months, highlighting soaring compute and Meta’s infrastructure needs expanding sharply.[9]

Conclusions:

The AI infrastructure boom reflects a bold, forward-looking strategy by Big Tech, built on the belief that compute capacity will define the next decade’s leaders. If Artificial General Intelligence (AGI) or large-scale AI monetization unfolds as expected, today’s investments will be seen as visionary and transformative. Either way, the AI era is well underway — and the race for computational excellence is reshaping the future of global markets and innovation.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Footnotes:

[1] https://www.investing.com/news/stock-market-news/ai-capex-to-exceed-half-a-trillion-in-2026-ubs-4343520?utm_medium=feed&utm_source=yahoo&utm_campaign=yahoo-www

[2] https://www.venturepulsemag.com/2025/08/01/big-techs-400-billion-ai-bet-the-race-thats-reshaping-global-technology/#:~:text=Big%20Tech’s%20$400%20Billion%20AI%20Bet:%20The%20Race%20That’s%20Reshaping%20Global%20Technology,-3%20months%20ago&text=The%20world’s%20largest%20technology%20companies,enterprise%20strategy%2C%20and%20public%20policy.

[3] https://www.businessinsider.com/big-tech-capex-spending-ai-earnings-2025-10?

[4] https://www.investing.com/analysis/meta-plunged-12-amazon-jumped-11–same-ai-race-different-economics-200669410

[5] https://www.cnbc.com/2025/10/15/a-guide-to-1-trillion-worth-of-ai-deals-between-openai-nvidia.html

[6] https://finance.yahoo.com/news/bank-america-just-issued-stark-152422714.html

[7] https://news.futunn.com/en/post/64706046/from-cash-rich-to-collective-debt-how-does-wall-street?level=1&data_ticket=1763038546393561

[8] https://www.businessinsider.com/big-tech-capex-spending-ai-earnings-2025-10?

[9] https://finance.yahoo.com/news/ai-capex-exceed-half-trillion-093015889.html

……………………………………………………………………………………………………………………………………………………………………………………………………………………………

About the Author:

Rahul Sharma is President & Co-Chief Executive Officer at Indxx – a provider of end-to-end indexing services, data and technology products. He has been instrumental in leading the firm’s growth since 2011. Raul manages Indxx’s Sales, Client Engagement, Marketing and Branding teams while also helping to set the firm’s overall strategic objectives and vision.

Rahul holds a BS from Boston College and an MBA with Beta Gamma Sigma honors from Georgetown University’s McDonough School of Business.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………

References:

Curmudgeon/Sperandeo: New AI Era Thinking and Circular Financing Deals

Expose: AI is more than a bubble; it’s a data center debt bomb

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

FT: Scale of AI private company valuations dwarfs dot-com boom

Amazon’s Jeff Bezos at Italian Tech Week: “AI is a kind of industrial bubble”

AI Data Center Boom Carries Huge Default and Demand Risks

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Nokia in major pivot from traditional telecom to AI, cloud infrastructure, data center networking and 6G

Reuters: US Department of Energy forms $1 billion AI supercomputer partnership with AMD

………………………………………………………………………………………………………………………………………………………………………….

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

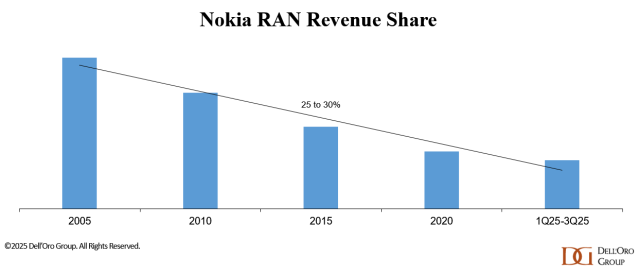

According to Dell’Oro VP Stefan Pongratz, Nokia has outlined a clear plan to arrest its declining RAN revenue share (see chart below), with NVIDIA now a central pillar of that strategy. The partnership is designed to deliver AI RAN [1.] while meeting wireless network operators’ near-term constraints and concerns on performance, power, and TCO (Total Cost of Ownership). IEEE Techblog has noted in many past blog posts that telcos have huge doubts about AI RAN which implies they won’t buy into that new RAN architecture.

This is especially relevant considering the monumental failure of multi-vendor Open RAN which was promoted as a game changer, but has dismally failed to attain that vision.

Note 1. AI RAN is a mobile RAN architecture where AI and machine learning are embedded into the RAN software and underlying compute platform to optimize how the network is planned, configured, and operated. It is being pushed by NVIDIA to get its GPUs into 5G, 5G Advanced and 6G base stations and other wireless network equipment in the RAN.

……………………………………………………………………………………………………………………………………………………..

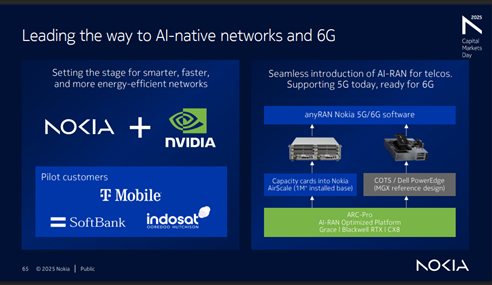

Nokia aims to use collaboration with NVIDIA (which invested $1B in the Finland based company) to stabilize its RAN market share in the near term and create a platform for long-term growth in AI-native 5G-Advanced and 6G networks. The timing—following a dense cadence of disclosures at NVIDIA’s GPU Technology Conference and Nokia’s Capital Markets Day—makes this an ideal time to reassess the scope of the joint announcements, the RAN implications, and Nokia’s broader competitive posture in an increasingly concentrated market.

Both companies share a belief that telecom networks will evolve from best-effort connectivity into a distributed compute fabric underpinning autonomous machines, self-driving vehicles, humanoids, and industrial digital twins. From that perspective, the RAN becomes an “AI grid” that executes and orchestrates AI workloads at the edge, enabling massive numbers of latency-sensitive, bandwidth-intensive AI use cases.

Unlike prior attempts to penetrate the RAN market with its GPUs, NVIDIA is now taking a more pragmatic approach, explicitly targeting parity with incumbent, purpose-built RAN equipment based on performance, power, and TCO rather than leading with speculative multi-tenant or new-revenue narratives. Nokia, acutely aware of wireless telco risk tolerance, is positioning the solution so that the ROI must be justifiable on a pure RAN basis, with additional AI and edge-compute upside treated as optional rather than foundational.

A quick recap of NVIDIA’s entry into RAN: Based on the announcement and subsequent discussions, our understanding is that NVIDIA will invest $1 B in Nokia and that NVIDIA-powered AI-RAN products will be incorporated into Nokia’s RAN portfolio starting in 2027 (with trials beginning in 2026). While RAN compute—which represents less than half of the $30B+ RAN market—is immaterial relative to NVIDIA’s $4+ T market cap, the potential upside becomes more meaningful when viewed in the context of NVIDIA’s broader telecom ambitions and its $165 B in trailing-twelve-month revenue.

With a deployed base of more than 1 million BTS, Nokia is prioritizing three migration vectors to GPU/AI-RAN, in order of expected impact:

-

Purpose-built D-RAN [2.], by inserting a new card into existing AirScale slots.

-

D-RAN vRAN [3.], using COTS servers at the cell site.

-

Cloud RAN [4.] or vRAN, using centralized COTS infrastructure.

This approach aligns with wireless network operators’ desire to sweat existing AirScale assets while minimizing operational disruption.

Note 2. Purpose-built D-RAN is a distributed RAN architecture where the baseband processing runs on dedicated, vendor-specific hardware at or very close to the cell site, rather than on generic COTS servers. It is “purpose-built” because the silicon, boards, and software stack are tightly integrated and optimized for RAN performance, power efficiency, and footprint, not general-purpose compute.

Note 3. vRAN or virtual RAN is a technology that virtualizes the functions of a cellular network’s radio access network, moving them from dedicated hardware to software running on general-purpose servers. This approach makes mobile networks more flexible, scalable, and cost-efficient by replacing proprietary hardware with software on common-off-the-shelf (COTS) hardware.

Note 4. Cloud RAN (C-RAN) is a centralized cellular network architecture that uses cloud computing to virtualize and process radio access network (RAN) functions. This architecture centralizes baseband units in a “BBU hotel,” allowing for more flexible and scalable network management, efficient resource allocation, and improved network performance. It allows operators to pool resources, adjust capacity based on demand, and support new services, which is a key enabler for 5G networks.

………………………………………………………………………………………………………………………………………………

In this model, the Distributed Unit, and often the higher-layer functions, are physically collocated with the radio unit at the site, making each site a largely self-contained RAN node. This contrasts with Cloud RAN or vRAN, where baseband functions are centralized or virtualized on shared cloud infrastructure, and with cloud/AI-RAN approaches that rely on GPUs or other general-purpose accelerators instead of custom RAN hardware.

The macro-RAN market (baseband plus radio) is roughly a $30 billion annual opportunity, with on the order of 1–2 million macro sites shipped per year. In that context, operators have limited appetite to pay more than $10,000 for a GPU per sector, even if software-led benefits accumulate over time, which is why NVIDIA is signaling GPU pricing in line with ARC-Compact, but at roughly double the capacity and Nokia is targeting 48–50% gross margins in Mobile Infrastructure by 2028, slightly above the current run-rate.

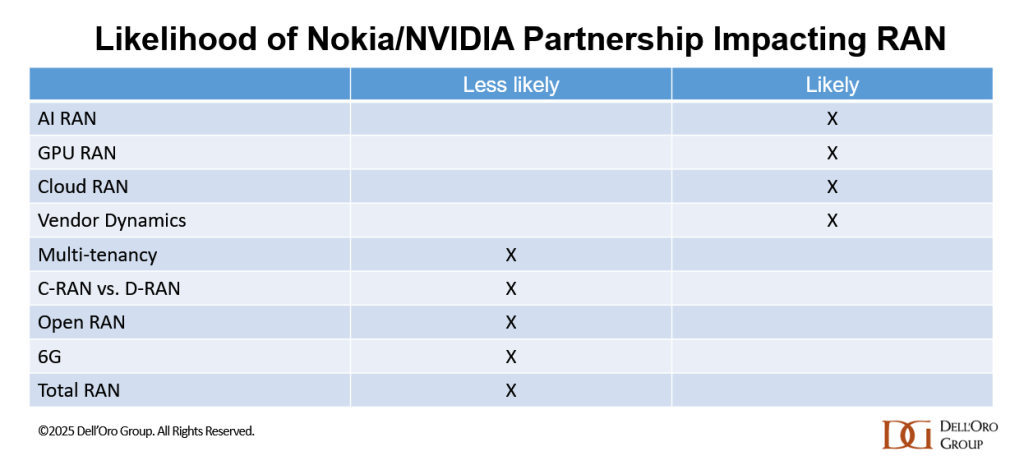

If the TCO and performance-per-watt gap versus custom silicon continues to narrow, the partnership could materially influence AI-RAN and Cloud-RAN trajectories while also supporting Nokia’s margin expansion goals. AI-RAN was already expected to scale to roughly one-third of the RAN market by 2029; Nokia’s decision to lean harder into GPUs amplifies this structural shift without fundamentally changing the long-term 6G direction.

In the near term, GPU-enabled D-RAN using empty AirScale slots is expected to dominate deployments, reflecting operators’ preference for incremental, site-level upgrades. At the same time, the Nokia-NVIDIA partnership is not expected to meaningfully alter the overall Cloud RAN vs. D-RAN mix, Open RAN adoption (slow or non-existent) , or the trajectory of multi-tenant RAN, which remain more dependent on network operator architecture and commercial decisions than on a single vendor–silicon alignment.

Nokia plans to remain disciplined and focus on areas where it can differentiate and unlock value—particularly through software/faster innovation cycles via its recently announced partnership with NVIDIA. The company sees meaningful opportunities to capture incremental share in North America, Europe, India, and select APAC markets. And it is already off to a solid start— we estimate that Nokia’s 1Q25–3Q25 RAN revenue share outside North America improved slightly relative to 2024. Following this stabilization phase, Nokia is betting that its investments will pay off and that it will be well-positioned to lead with AI-native networks and 6G.

Nokia’s objective is clear: stabilize RAN in the short term, then grow by leading in AI-native networks and 6G over the longer horizon. Success now hinges on Nokia’s ability to operationalize the GPU-based RAN roadmap at scale and on NVIDIA’s ability to deliver carrier-grade economics and performance—turning the AI-RAN narrative into production-grade, repeatable deployments.

Nokia sees meaningful opportunities to capture incremental RAN market share in North America, Europe, India, and select APAC markets. And it is already off to a solid start— we estimate that Nokia’s 1Q25–3Q25 RAN revenue share outside North America improved slightly relative to 2024. Following this stabilization phase, Nokia is betting that its investments will pay off and that it will be well-positioned to lead with AI-native networks and 6G.

References:

Nokia in major pivot from traditional telecom to AI, cloud infrastructure, data center networking and 6G

Indosat Ooredoo Hutchison, Nokia and Nvidia AI-RAN research center in Indonesia amongst telco skepticism

Nvidia pays $1 billion for a stake in Nokia to collaborate on AI networking solutions

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

AI RAN Alliance selects Alex Choi as Chairman

Expose: AI is more than a bubble; it’s a data center debt bomb

Nokia and Rohde & Schwarz collaborate on AI-powered 6G receiver years before IMT 2030 RIT submissions to ITU-R WP5D

Nokia and the test and measurement firm Rohde & Schwarz have created and successfully tested a “6G” radio receiver that uses AI technologies to overcome one of the biggest anticipated challenges of 6G network rollouts, coverage limitations inherent in 6G’s higher-frequency spectrum.

–>This is truly astonishing as ITU-R WP5D doesn’t even plan to evaluate 6G RIT/SRITs till February 2027 when the first submissions are invited to be presented.

Nokia Bell Labs developed the receiver and validated it using 6G test equipment and methodologies from Rohde & Schwarz. The two companies will unveil a proof-of-concept receiver at the Brooklyn 6G Summit on November 6, 2025. Nokia says, “the machine learning capabilities in the receiver greatly boost uplink distance, enhancing coverage for future 6G networks. This will help operators roll out 6G over their existing 5G footprints, reducing deployment costs and accelerating time to market.”

Image Credit: Rohde & Schwarz

Nokia Bell Labs and Rohde & Schwarz have tested this new AI receiver under real world conditions, achieving uplink distance improvements over today’s receiver technologies ranging from 10% to 25%. The testbed comprises an R&S SMW200A vector signal generator, used for uplink signal generation and channel emulation. On the receive side, the newly launched FSWX signal and spectrum analyzer from Rohde & Schwarz is employed to perform the AI inference for Nokia’s AI receiver. In addition to enhancing coverage, the AI technology also demonstrates improved throughput and power efficiency, multiplying the benefits it will provide in the 6G era.

“One of the key issues facing future 6G deployments is the coverage limitations inherent in 6G’s higher-frequency spectrum. Typically, we would need to build denser networks with more cell sites to overcome this problem. By boosting the coverage of 6G receivers, however, AI technology will help us build 6G infrastructure over current 5G footprints,” said Peter Vetter, President, Core Research, Bell Labs, Nokia.

“Rohde & Schwarz is excited to collaborate with Nokia in pioneering AI-driven 6G receiver technology. Leveraging more than 90 years of experience in test and measurement, we’re uniquely positioned to support the development of next-generation wireless, allowing us to evaluate and refine AI algorithms at this crucial pre-standardization stage. This partnership builds on our long history of innovation and demonstrates our commitment to shaping the future of 6G,” said Michael Fischlein, VP, Spectrum & Network Analyzers, EMC and Antenna Test, Rohde & Schwarz.

…………………………………………………………………………………………………………………………………………………………………………………………

Last month, Nokia teamed up with rival kit vendor Ericsson to work on video coding standardization in preparation for 6G. The project, which also involved Berlin’s Fraunhofer Heinrich Hertz Institute (HHI), demonstrated a new video codec which they claim has higher compression efficiency than the current standards (H.264/AVC, H.265/HEVC, and H.266/VVC) without significantly increasing complexity, and its wider aim is to strengthen Europe’s role in next generation standardization, we were told at the time.

…………………………………………………………………………………………………………………………………………………………………………………………

About Nokia:

At Nokia, we create technology that helps the world act together.

As a B2B technology innovation leader, we are pioneering networks that sense, think and act by leveraging our work across mobile, fixed and cloud networks. In addition, we create value with intellectual property and long-term research, led by the award-winning Nokia Bell Labs, which is celebrating 100 years of innovation.

With truly open architectures that seamlessly integrate into any ecosystem, our high-performance networks create new opportunities for monetization and scale. Service providers, enterprises and partners worldwide trust Nokia to deliver secure, reliable and sustainable networks today – and work with us to create the digital services and applications of the future

About Rohde & Schwarz:

Rohde & Schwarz is striving for a safer and connected world with its Test & Measurement, Technology Systems and Networks & Cybersecurity Divisions. For over 90 years, the global technology group has pushed technical boundaries with developments in cutting-edge technologies. The company’s leading-edge products and solutions empower industrial, regulatory and government customers to attain technological and digital sovereignty. The privately owned, Munich-based company can act independently, long-term and sustainably. Rohde & Schwarz generated a net revenue of EUR 3.16 billion in the 2024/2025 fiscal year (July to June). On June 30, 2025, Rohde & Schwarz had more than 15,000 employees worldwide.

References:

ITU-R WP5D IMT 2030 Submission & Evaluation Guidelines vs 6G specs in 3GPP Release 20 & 21

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Nvidia pays $1 billion for a stake in Nokia to collaborate on AI networking solutions

Highlights of Nokia’s Smart Factory in Oulu, Finland for 5G and 6G innovation

Verizon’s 6G Innovation Forum joins a crowded list of 6G efforts that may conflict with 3GPP and ITU-R IMT-2030 work

Qualcomm CEO: expect “pre-commercial” 6G devices by 2028

NGMN: 6G Key Messages from a network operator point of view

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

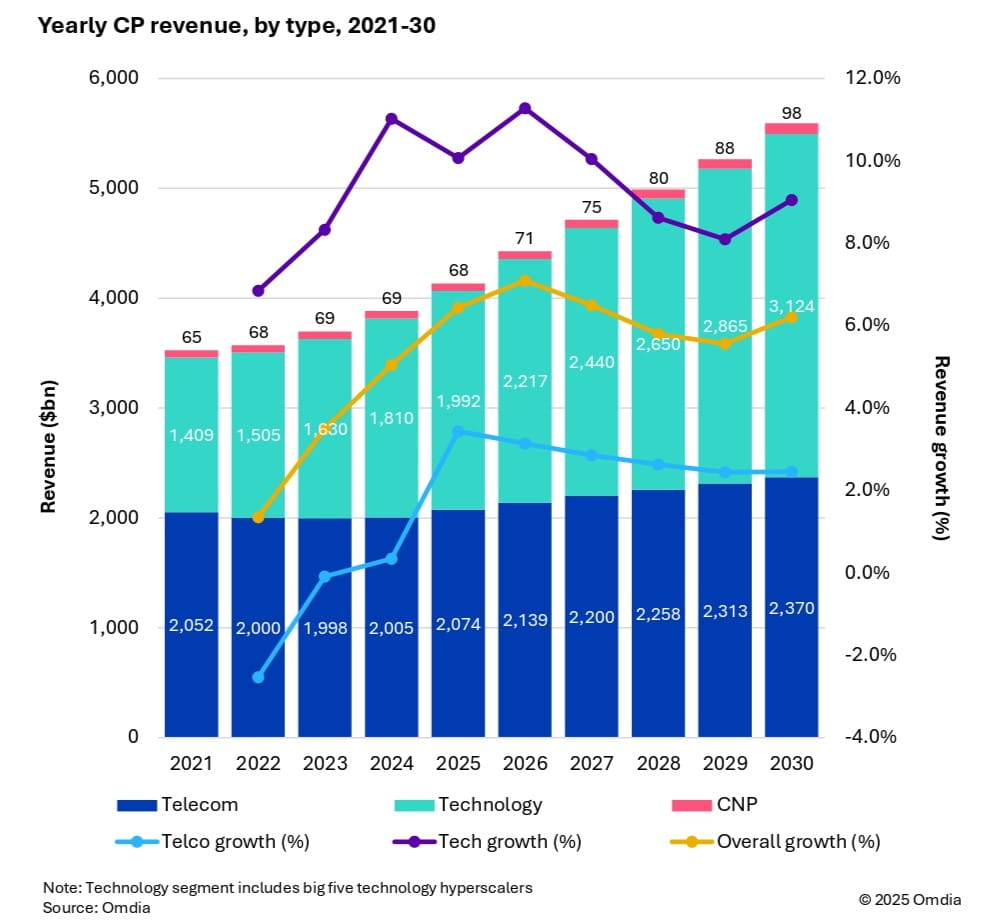

Market research firm Omdia (owned by Informa) this week forecast that 6G and AI investments are set to drive industry growth in the global communications market. As a result, global communications providers’ revenue is expected to reach $5.6 trillion by 2030, growing at a 6.2% CAGR from 2025. Investment momentum is also expected to shift toward mobile networks from 2028 onward, as tier 1 markets prepare for 6G deployments. Telecoms capex is forecast to reach $395 billion by 2030, with a 3.6% CAGR, while technology capex will surge to $545 billion, reflecting a 9.3% CAGR.

Fixed telecom capex will gradually decline due to market saturation. Meanwhile, AI infrastructure, cloud services, and digital sovereignty policies are driving telecom operators to expand data centers and invest in specialized hardware.

Key market trends:

- CP capex per person will increase from $74 in 2024 to $116 in 2030, with CP capex reaching 2.5% of global GDP investment.

-

Capital intensity in telecom will decline until 2027, then rise due to mobile network upgrades.

-

Regional leaders in revenue and capex include North America, Oceania & Eastern Asia, and Western Europe, with Central & Southern Asia showing the highest growth potential.

Dario Talmesio, research director at Omdia said, “telecom operators are entering a new phase of strategic investment. With 6G on the horizon and AI infrastructure demands accelerating, the connectivity business is shifting from volume-based pricing to value-driven connectivity.”

Dario Talmesio, research director at Omdia said, “telecom operators are entering a new phase of strategic investment. With 6G on the horizon and AI infrastructure demands accelerating, the connectivity business is shifting from volume-based pricing to value-driven connectivity.”

Omdia’s forecast is based on a comprehensive model incorporating historical data from 67 countries, local market dynamics, regulatory trends, and technology migration patterns.

…………………………………………………………………………………………………………………………………………………

Separately, Dell’Oro Group sees 6G capex ramping around 2030, although it warns that the RAN market remains flat, “raising key questions for the industry’s future.” Cumulative 6G RAN investments over the 2029-2034 period are projected to account for 55% to 60% of the total RAN capex over the same forecast period.

“Our long-term position and characterization of this market have not changed,” said Stefan Pongratz, Vice President of RAN and Telecom Capex research at Dell’Oro Group. “The RAN network plays a pivotal role in the broader telecom market. There are opportunities to expand the RAN beyond the traditional MBB (mobile broadband) use cases. At the same time, there are serious near-term risks tilted to the downside, particularly when considering the slowdown in data traffic,” continued Pongratz.

Additional highlights from Dell’Oro’s October 2025 6G Advanced Research Report:

- The baseline scenario is for the broader RAN market to stay flat over the next 10 years. This is built on the assumption that the mobile network will run into utilization challenges by the end of the decade, spurring a 6G capex ramp dominated by Massive MIMO systems in the Sub-7GHz/cm Wave spectrum, utilizing the existing macro grid as much as possible.

- The report also outlines more optimistic and pessimistic growth scenarios, depending largely on the mobile data traffic growth trajectory and the impact beyond MBB, including private wireless and FWA (fixed wireless access).

- Cumulative 6G RAN investments over the 2029-2034 period are projected to account for 55 to 60 percent of the total RAN capex over the same forecast period.

Dell’Oro Group’s 6G Advanced Research Report offers an overview of the RAN market by technology, with tables covering manufacturers’ revenue for total RAN over the next 10 years. 6G RAN is analyzed by spectrum (Sub-7 GHz, cmWave, mmWave), by Massive MIMO, and by region (North America, Europe, Middle East and Africa, China, Asia Pacific Excl. China, and CALA). To purchase this report, please contact by email at [email protected].

References:

https://www.lightreading.com/6g/6g-momentum-is-building

6G Capex Ramp to Start Around 2030, According to Dell’Oro Group

https://www.lightreading.com/6g/6g-course-correction-vendors-hear-mno-pleas

https://www.lightreading.com/6g/what-at-t-really-wants-from-6g

Nvidia pays $1 billion for a stake in Nokia to collaborate on AI networking solutions