Month: November 2021

“There’s nothing like it;” AWS CEO announces Private 5G at AWS re-Invent 2021; Dish Network’s endorsement

Amazon Web Services (AWS) CEO Adam Selipsky kicked off day 2 of AWS re-Invent 2021 today with a keynote presentation loaded with exciting announcements, status updates, and long-term vision-setting for the AWS cloud platform. AWS is now in its 15th year. It currently has 81 Availability Zones, 250+ services, 475 instance types to support virtually any workload. And it has an always-evolving library of solutions designed for highly specific use cases.

The AWS cloud stores more than 3 trillion objects, AWS offers over 200 fully-featured services, with millions of customers around the world,” the CEO said. Of those customers, Netflix, NASA and NTT DoCoMo are highlighted as some of the most innovative use cases for AWS.

“In the last 15 years, cloud has become not just another tech revolution, but a shift in how businesses actually function. There’s no business that can’t be radically disrupted. And we’re just getting started,” Selipsky added, noting that only 5-15% of spending has moved to the cloud, so there’s a big opportunity to come, with 5G and IoT becoming super important too.

“We’re going to keep innovating to keep offering the broadest suite of services,” Selipsky said.

The most import announcement for IEEE Techblog readers was a new AWS Private 5G service that will allow users to launch and manage their own private mobile network in days with automatic configuration, no per-device charges, and shared spectrum operation. AWS provides all the hardware, software, and SIMs needed for Private 5G, making it a one-stop solution that is the first of its kind.

“It’s not easy to set up a private 5G network using offerings from existing 5G providers, according to AWS CEO. “Currently, private mobile network deployments require customers to invest considerable time, money and effort to design their network for anticipated peak capacity, and procure and integrate software and hardware components from multiple vendors. Even if customers are able to get the network running, current private mobile network pricing models charge for each connected device and make it cost prohibitive for use cases that involve thousands of connected devices.”

Selipsky said AWS customers will be able to select where they want to build a mobile network and the network capacity they need. AWS will then deliver and maintain the network’s necessary small cell radio units, servers, 5G core and radio access network (RAN) software, and subscriber identity modules (SIM cards) required for a private 5G network and its connected devices.

“AWS Private 5G automates the setup and deployment of the network and scales capacity on demand to support additional devices and increased network traffic,” the company explained, noting the network will work in “shared spectrum,” likely a reference to the 3.5GHz CBRS spectrum band in the U.S. “There are no upfront fees or per-device costs with AWS Private 5G, and customers pay only for the network capacity and throughput they request.”

“It’s (AWS Private 5G) shockingly easy,” according to Selipsky – AWS sends everything you need, from hardware to software to SIM cards. Automatic configuration makes it ideal for factories and workplaces, and you can ask for as many devices to be connected as you need. He added that the company will sell the service under a pay-as-you-go model, and won’t add any per-device fees. “There’s nothing like AWS Private 5G network out there,” the CEO concluded.

“Many of our customers want to leverage the power of 5G to establish their own private networks on premises, but they tell us that the current approaches make it time-consuming, difficult, and expensive to set up and deploy private networks,” said David Brown, Vice President, EC2 at AWS in a press release. “With AWS Private 5G, we’re extending hybrid infrastructure to customers’ 5G networks to make it simple, quick, and inexpensive to set up a private 5G network. Customers can start small and scale on-demand, pay as they go, and monitor and manage their network from the AWS console.”

Dell’Oro Group’s VP Dave Bolan wrote in an email, “What is new about this announcement, is that we have a new Private Wireless Network vendor (AWS) with very deep pockets that could become a major force in this market segment.”

Immediately after Selipsky keynote speech, Dish Network’s Chief Network Officer Marc Rouanne took the re-Invent stage to tout his own company’s forthcoming 5G network. [Note that AWS is providing the 5G SA cloud native core network for Dish]. Rouanne, touted the appeal of Dish’s planned (but delayed) 5G network for enterprise customers. He said Dish is building a “network of networks” that enterprise customers will be able to adapt to their needs. He said Dish’s 5G customers will be able to customize their services based on parameters such as speed and latency, but didn’t mention that’s based on network slicing which requires the 5G SA core network that Dish has outsourced to AWS.

“Some say we are the AWS of wireless,” Rouanne said, adding that Dish’s 5G will be as flexible as the cloud computing service built by Amazon. “Dish is going to be the enabler of technology that people have not even imagined yet.”

“We’re building the first architecture that is truly optimized for the cloud. It promises tremendous advances, not just for human communications, but also for machine to machine, and of course for humans to control those machines,” he added.

We have previously expressed skepticism that Dish can be an effective telecom/IT systems integrator with no experience whatsoever in that field. We wrote:

Dish said it would use Cisco for routing, IBM for automation, Spirent for testing and Equinix for interconnections – announcements noteworthy considering Dish is mere weeks from its first market launch. The ability to automatically, virtually and in parallel test new 5G Standalone services, slices and software updates in the cloud is key to Dish Network’s network strategy and its differentiation, according to Marc Rouanne, Dish EVP and chief network officer for its wireless business. Rouanne said that the ability to rapidly test and certify network software and services has been part of Dish’s vision for its network. Dish announced more than a year ago that it would use radio management software from both Mavenir and Altiostar, when Rakuten was a major investor in Altiostar (it now owns that company).

–>So it seams that Dish Network’s 5G role will be that of a systems integrator, putting together the many outsourced parts of its 5G greenfield network. It remains to be seen what combination of vendors will supply the Open RAN portion of the 5G network and what development, if any, Dish’s engineers will do for it. And how will Dish’s 5G SA core network via AWS interface with those Open RAN vendors?

In the previously referenced press release from AWS, Stephen Bye, Chief Commercial Officer, DISH said, “Selecting AWS has enabled us to onboard and scale our 5G core network functions within the cloud. They are a key strategic partner in helping us deliver private enterprise networks to our customers. AWS’s innovative platform allows us to better serve our consumer wireless customers, while unlocking new business models for enterprise customers across a wide range of industry verticals. Our ability to support dedicated, private 5G enterprise networks allows us to give customers the scale, resilience and security needed to support a wide variety of devices and services, unlocking the potential of Industry 4.0.”

In conclusion, it looks like the AWS Private 5G network (where Amazon provides the 5G RAN and 5G core) will compete with Dish’s 5G network (where Dish provides the RAN while AWS provides the 5G SA core network) for industrial customers. In that sense, it is a win-win proposition for Amazon as AWS will be competing with AWS (hah, hah!) for the 5G SA core network. It’s also significant that these announcements strengthened the trend to use 5G for industry/factory applications rather than for consumers where there is little or no benefits.

All in all, it send a strong competitive signal to wireless telcos that they’ll be competing with cloud hyperscalers as well as network equipment and software companies in the 5G private network market.

About Amazon Web Services:

For over 15 years, Amazon Web Services has been the world’s most comprehensive and broadly adopted cloud offering. AWS has been continually expanding its services to support virtually any cloud workload, and it now has more than 200 fully featured services for compute, storage, databases, networking, analytics, machine learning and artificial intelligence (AI), Internet of Things (IoT), mobile, security, hybrid, virtual and augmented reality (VR and AR), media, and application development, deployment, and management from 81 Availability Zones (AZs) within 25 geographic regions, with announced plans for 27 more Availability Zones and nine more AWS Regions in Australia, Canada, India, Indonesia, Israel, New Zealand, Spain, Switzerland, and the United Arab Emirates. Millions of customers—including the fastest-growing startups, largest enterprises, and leading government agencies—trust AWS to power their infrastructure, become more agile, and lower costs. To learn more about AWS, visit aws.amazon.com.

References:

https://reinvent.awsevents.com/

https://press.aboutamazon.com/news-releases/news-release-details/aws-announces-aws-private-5g

https://www.techradar.com/news/live/aws-reinvent-2021-keynote-live-blog

https://www.lightreading.com/open-ran/amazon-dish-peddle-dueling-5g-products/d/d-id/773802?

Analysis of Dish Network – AWS partnership to build 5G Open RAN cloud native network

FWA has limited deployments, many supporters, and great potential

Ericsson’s Mobility Report forecasts FWA (fixed wireless access) connections will “show strong growth of 17% annually through 2027.” That compares to anticipated wireline broadband growth over the same period of only 4%. The Ericsson report states that 57 network operators have deployed FWA commercial networks. Finnish telco DNA says FWA is its most popular broadband offering.

Ericsson says Latin America and North America are markets where FWA will play a role in closing the digital divide. Africa may also be promising because of its large rural population and the limited alternatives.

GSMA Intelligence is also enthusiastic about FWA. In a recent blog post it described FWA “as one of the most promising 5G use cases,” providing “an incremental opportunity to maximize the value of existing network assets.”

So is Dell’Oro Group’s Jeff Heynen. He wrote in an IEEE Techblog post, “We estimate that the total number of 5G FWA devices shipping to operators this year will easily exceed 3 million units and could push 4 million units. The vast majority of these units will be to support sub-6Ghz service offerings, though we also expect to see millimeter wave units, as some operators use a combination of those technologies to provide both extensive coverage and fiber-like speeds in areas where the competition from fixed broadband providers is more intense. Overall, however, we expect volumes first from sub-6GHz units this year and into next year, followed by increasing volumes of millimeter wave units beginning in the latter part of 2022 and into 2023.”

Not to be outdone, an Accenture analysis commissioned by the CTIA argues that 5G FWA can serve as many as 43% of rural households.

Light Reading’s Robert Clark writes:

Currently fixed wireless, using either 4G or some other technology, accounts for fewer than 100 million worldwide subscribers.

The challenge for 5G, as for earlier generations, is that wireless doesn’t always deliver the best performance or the strongest business case.

Philippines’ Globe Telecom is a case in point. GSMA Intelligence lauds it as a “great example” largely because it launched its 5G network two years ago with a FWA service called Air Fiber.

But two years is a long time, especially when that period includes COVID-19, and we now find that Globe has shifted away from FWA to actual fiber.

Globe’s total fixed wireless subs fell 17% sequentially in Q3 while FTTH subs grew 35%, the company said in a filing. Total home broadband revenues grew 39% thanks to “the accelerated digital habits of the Filipinos brought about by the pandemic.”

China, the global 5G champion with 450 million users, is also indifferent to the possibilities of fixed wireless. You would think this nation with a rural population of some 530 million and vast sparsely settled regions would be a prime market for FWA, but its home broadband priority is gigabit fiber.

Geography is likely the main reason for limited 5G FWA take-up worldwide. 5G is strong in countries already well-served by fiber. Those markets where operators are likely to grow FWA are still in their early stages.

Opinion:

We believe that 5G FWA has great potential. That is because no standard 5G core network is required and there is no roaming between carriers. As such, non standard/operator specific private 5G SA core networks can be deployed that can deliver a range of 5G core enabled services, e.g. network slicing, automation, security, MEC, enhanced network management.

However, URLLC in the RAN and in the core network must be standardized, performance tested, and implemented in trials. Then deployed in production networks before the various 5G FWA industrial use cases can be effectively deployed.

References:

https://www.lightreading.com/asia/5g-fixed-wireless-how-far-can-it-go/d/d-id/773784?

Dell’Oro: 5G Fixed Wireless Access (FWA) deployments to be driven by lower cost CPE

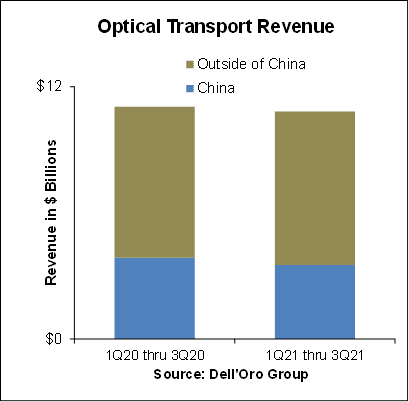

Dell’Oro: Optical Transport Market Down 2% in 1st 9 Months of 2021

According to a recently published report from Dell’Oro Group, the Optical Transport equipment market contracted 2 percent year-over-year in the first nine months of 2021 due to lower sales in China. Outside of China, however, the demand for optical equipment continued to increase, outpacing supply.

“Optical equipment revenue in China took a sharp turn for the worse in 3Q 2021,” said Jimmy Yu, Vice President at Dell’Oro Group. “As a result, optical revenue in China declined at a double-digit rate in the quarter, resulting in a 9 percent decline for the first nine months of 2021. At this rate, we are expecting a full year optical market contraction in the country. Something that has not occurred since 2012. Helping to offset some of this lower equipment revenue from China was the robust demand in North America, Europe, and Latin America.”

“We estimate that Optical Transport equipment revenue outside of China grew 6 percent year-over-year in the third quarter. However, we believe this growth rate could have been higher, closer to 10 percent, if it was not for component shortages and other supply issues plaguing the industry. So, fortunately while optical demand is hitting a rough patch in China, it seems to be accelerating in other parts of the world,” added Yu.

The optical transport market is predicted to reach $18 billion by 2025, primarily as a result of demand for WDM equipment, Dell’Oro reported in July 2021. In addition, Dell’Oro says the ZR pluggable optics market could exceed $500 million in annual sales by 2025.

In a 2Q-2021 report by market research firm Omdia, analysts noted that 5G investment, cloud service growth and demand for “infotainment-at-home” are among the drivers increasing demand in the optical networking market. “The twin dynamics of increasing optical capillarity and increasing end-point capacity continue to drive the optical core,” Omdia wrote in a note to clients.

The Dell’Oro Group Optical Transport Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, average selling prices, unit shipments (by speed including 100 Gbps, 200 Gbps, 400 Gbps, and 800 Gbps). The report tracks DWDM long haul, WDM metro, multiservice multiplexers (SONET/SDH), optical switch, optical packet platforms, data center interconnect (metro and long haul), and disaggregated WDM. To purchase this report, please contact us at [email protected].

Jimmy Yu, Vice President, Dell-Oro Group

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, networks, and data center IT markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions. For more information, contact Dell’Oro Group at +1.650.622.9400 or visit https://www.delloro.com.

References:

Optical Transport Market Down 2 Percent in First Nine Months of 2021, According to Dell’Oro Group

Disaggregated DWDM Equipment Market Up 36 Percent in 2Q 2021, According to Dell’Oro Group

5-Year Forecast: Optical Transport Market Reaches $18 Billion by 2025

Ericsson: 660 million global 5G subscriptions at end of 2021 (?)

In its new Mobility Report, Ericsson has updated its forecast for 5G subscribers at the end of 2021, to a total of close to 660 million. The increase is due to stronger-than-expected demand in China and North America (?), driven in part by falling prices for 5G devices. Ericsson forecasts 5G to become the dominant mobile technology by 2027.

Opinion: For that to happen, this author believes many of the unfinished parts of 5G must be completely standardized and proven in the field. That list includes: URLLC in the RAN, URLLC in the core network, 5G SA core network, 5G security, reduction of very high 5G power consumption, deployment of hundreds of thousands of small cells, frequency arrangements for terrestrial (ITU-R M.1036 revision), industrial and consumer use cases, fiber optics and LEO satellite backhaul, etc.

………………………………………………………………………………………………………….

In Q3 2021, nearly twice as many 5G subscriptions were added around the world as new 4G connections, at respectively 98 million and 48 million. Ericsson expects that 5G networks will cover more than 2 billion people by the end of this year.

Ericsson’s latest forecasts put 5G on track to become the dominant mobile access technology by 2027. 5G is expected to account for around 50 percent of all mobile subscriptions worldwide in 2027, covering 75 percent of the world’s population and carrying 62 percent of the global smartphone traffic by the same date.

Not to be forgotten, Ericsson says fixed wireless access (FWA) will provide broadband access for 800 million people by 2027.

Ericsson’s latest report also looks back on the past ten years of mobile networks. According to the research, around 5.5 billion smartphone users have joined the market in the past ten years, and mobile data traffic has increased almost 300-fold in the same period.

In Q3 2021 alone, there was more mobile data traffic than the entire period up until the end of 2016.

Note that Ericsson has tended to over-estimate total mobile subscriptions but under-estimate the uptake of newer technologies, especially in their early stages. This is shown in the table below:

Fredrik Jejdling, Head of Networks at Ericsson, wrote:

“Mobile communication has had an incredible impact on society and business over the last ten years. When we look ahead to 2027, mobile networks will be more integral than ever to how we interact, live and work. Our latest Ericsson Mobility Report shows that the pace of change is accelerating, with technology playing a crucial role.”

References:

https://www.ericsson.com/en/reports-and-papers/mobility-report

Global 5G subscriptions to hit 660 million this year – Ericsson

https://www.telecompaper.com/news/ericsson-upgrades-global-5g-subscriber-forecasts–1406019

Cowen Analysts: Telcos to lead FTTH buildout; total 82M homes to be passed by 2027

According to a new report titled Fiber to the Home: Navigating the Road to Gigabit America, a multi-sector by Cowen analysts, forecasts that telco fiber-to-the-home (FTTH) lines will pass 82 million American households by 2027, nearly double the 44 million households passed today. The four biggest U.S. wireline telcos (AT&T, Verizon, Frontier and Lumen) will account for the lion’s share of those deployments, together passing more than 71 million homes with fiber.

The Cowen report also projects that cable operators (cablecos or MSOs) will pass another 5 million homes with fiber lines over the next six years, largely because of Altice USA’s current big push in the New York metro area to match Verizon’s Fios rollout. Cable operators already pass about 5 million homes with fiber.

Overall, Cowen estimates that the US now has 50 million homes passed by fiber lines, with the telcos accounting for most of them. Here are a few other highlights from the report:

- Cowen expects state/federal funding of $130B for various broadband initiatives.

- That will close the digital divide and expand the addressable market for broadband access.

- FTTH will gain market share (compared to other fixed broadband access) to take ~70% of the net positive broadband subscriber adds by 2027.

- As a result, 35M FTTH subscribers (26% market share) are expected by 2027; up from 16M (14%) today.

- FTTH subs take speeds that are 54% faster than non-FTTH broadband subs.

- The increase in FTTH subs will lead to exciting next-gen home applications (not specified) and ARPU growth.

- FTTH subs have 13% higher ARPU compared to non-FTTH subs.

Large, midsized and small telcos will all participate in this massive fiber deployment, using FTTH to reverse nearly two decades of broadband market share losses to the cable industry, the Cowen analysts say. For instance, they project the nation’s biggest telcos will add a combined 7.7 million fiber subs over the next five years.

“The next few years will be historic in terms of telco FTTH upgrades, providing consumers speeds of 1 Gbit/s, closing the digital divide, expanding the total addressable market and achieving a ‘Gigabit America’,” the analysts wrote. “After years of hemorrhaging subscribers, we expect Big Telco to stem the tide of losses to Cable…”

However, the report does not say that telcos will be gaining broadband customers from cable operators. Instead, telcos will achieve broadband subscriber gains mainly by upgrading their own remaining 15 million DSL subs to FTTH.

“The cable decade of dominance of DSL-share stealing is over,” the analysts wrote, forecasting that the telcos will overtake the cable companies in broadband sub net gains by 2024. “Cable’s days of stealing DSL subs are over, though only losing modest share (DSL taking the brunt), as the focus will be on defense.”

The Cowen analysts expect cable’s broadband market share to drop very slightly from 61% today to 58% in 2027 while the telcos’ market share creeps up from 25% now to 27% in 2027.

“It’s far from doom-and-gloom for cable operators,” the analysts note. “With cable’s effective marketing plan and speed upgrades, the vast majority of subscriber losses will be from the 15 million DSL subscribers, not cable.”

The analysts expect fixed wireless access (FWA) to play a notable tole in the US broadband market by the middle of the decade, accounting for a small but increasing fraction of high-speed data customers throughout the 2020s. “FWA will establish a solid but niche foothold,” they wrote.

Cowen now expects U.S. service providers to add a collective 17 million broadband subs by 2027, enough to reach 97% penetration of occupied homes and 90% penetration of overall homes, up from 90% and 82% today. The analysts believe that broadband could achieve utility-like penetration levels of 98% or more, like wired phone service did at its peak last century.

All this fiber optic spending will be a boon for optical network equipment vendors. Specifically, the Cowen analysts single out Calix, Adtran, Ciena, Cisco, MasTec, Nokia and Juniper as likely beneficiaries.

The analysts also see potential for further market consolidation. Some scenarios they envision are Charter buying the Suddenlink portion of Altice USA’s footprint and Charter or Altice USA merging with T-Mobile to form a third converged player in the national market.

References:

Telcomp (Brazil): 5G infrastructure (cabling, antennas, small cells, etc) to be ~5x greater than 4G

A few weeks after the 5G auction in Brazil, the industry is calculating the energy demand required to implement this technology. The hope of the market and specialists, is to have a low-impact investment that provides greater efficiency – both in data exchange and in industrial procedures. The infrastructure required for companies to operate 5G – cabling and antennas, etc – should be around five times greater in comparison with 4G, says Luiz Henrique Barbosa da Silva, CEO of Telcomp (Brazilian Association of Competitive Telecom Service Providers). We assume that estimate is for the RAN – not the core network (5G SA core vs 4G EPC).

Vivo’s solar power plant (see photo below) in Quissamã, Rio de Janeiro – Deway Matos/Divulgação The 5G antennas are smaller than the ones currently used and have the average size of a shoe box, according to Conexis, an association that represents telecommunication companies. The number of antennas to be installed depends on different factors, including population density and geographical elements, such as the presence of tunnels and hills, explains Barbosa da Silva, of Telcomp. Spaces with very high population density need more towers.

Vivo’s solar power plant

Despite the need for a larger number of antennas, the network is gaining efficiency. “Imagine a dark room. You put a light in the center: that’s the 1G network. It covers the whole room, but to get good lighting, you need to increase the power. With 2G you put one more bulb in, and when we get to 5G, I have more bulbs on the ceiling, but they are lower wattage. And that is more efficient,” he says. Furthermore, the technology is able to transport data with more efficient energy consumption than 4G, says Marcelo Zuffo, professor at the Polytechnic School at USP (University of São Paulo). In terms of energy consumption, the implementation of the 5G structure does not generate a very different impact from 4G, says Fabro Steibel, executive director of ITS (Institute of Technology and Society). “If you think in terms of carbon [footprint], perhaps the impact is greater, since there is a new standard, a new mesh to be installed,” says Steilbel.

In addition to new antennas, different equipment will need to be installed from those used to operate the 4G frequency, since in Brazil a so-called “standalone” model has been defined for 5G. “We will use a new technology and have to replace equipment because, in theory, companies cannot take what they have today and adapt it to a higher speed. But this is always within the concept of energy efficiency,” says Marcos Ferrari, CEO of Conexis, which represents the operators Algar, Claro, Oi, Sercomtel, Tim and Vivo.

Gains from 5G are not expected to reach the entire population, say experts. “When we compare our investment with other infrastructure sectors, such as highways and airports, we see that it is clean. We are talking about running a robust cabling system in the country. In urban centers, you have to pierce sidewalks to pass a pipeline, but that does not compare to investments that cross, for example, a forest reserve,” he says.

Furthermore, there is an expectation of a reduction in energy waste when devices other than mobile phones are connected to 5G – such as equipment used in a productive plant or in agribusiness, which will allow, for example, activities such as more precise irrigation. Ferrari says it is still too early to have an exact estimate of the impact of energy consumption for the implementation of 5G, but says that operators have environmental commitments both from the point of view of the current technology and the technology to come. According to data from the entity, Claro, for example, one of the winners of the auction of the main bands of the network, has since 2017 a program that provides for the use of clean energy (solar, wind, hydroelectric and biogas) to fuel the company’s operations. With 58 plants and generating plants in states such as Bahia, Minas, Pará, Paraná, Santa Catarina, Rio and São Paulo, the initiative serves more than 50% of the existing antennas with renewable energy. Also according to Conexis data, Algar, which won a regional lot of the auction that covers the Minas Gerais triangle and parts of Mato Grosso do Sul and Goiás, has today 66% of energy consumed originated from renewable sources, with a goal of reaching 85% in 2022 and 95% by 2024.

Vivo is carbon-neutral in direct emissions and since last year has been expanding its distributed energy generation project, which includes the installation of 83 solar, hydro and biogas plants (19 of which are already in operation). The operator’s program will account for 89% of its consumption in low voltage, serving structures such as administrative buildings, base stations and data centers until 2022, when it should be completed.

TIM [1.] states that it intends to extend renewable energy generation to the 5G network when it is already in operation in the country – one of the objectives of the environmental layer of its ESG program (good social, governance and environmental practices) is to increase the ratio between renewable energy use and total energy use. The company has 38 renewable energy plants (including solar, hydroelectric and biogas generators) in operation and wants to reach 60 by the end of 2022.

“Embarking on a new technology is not only a matter of providing a faster Youtube. It is also something I can do with less cost, with industrial efficiency,” says Mario Girasole, vice president of Regulatory and Institutional Affairs of TIM.

For the president of Telcomp, Luiz Henrique Barbosa da Silva, the agenda of clean energy generation is also linked to other issues – for example, hardly companies whose projects are not sustainable will be able to raise funds. Besides the concern with the principles of ESG, a positive impact for companies is the improvement of economic results, he says. “Many operators have invested in renewable energy generation parks. But they are also big consumers. So investing in that is also financially a good business.”

Note 1. TIM started operations in Brazil in 1998 and consolidated ourselves as a national company in 2002, making us the first mobile operator to have a presence in all states of Brazil.

References:

Vodafone Idea to use 5Gi (ITU M.2150-LMLC) in trials

Vodafone Idea (Vi) is working with a “few companies” to prepare for trials using India’s own 5G standard 5Gi, which is included in ITU-R M.2150 as 5G Radio Interface Technology (RIT) for LMLC- Low Mobility Large Cell. The third largest telco in India said that once the telecom equipment is ready, it will conduct trials using the 5G LMLC technology.

“We are already working with a few companies. As and when the product is ready, we will be keen and will be doing trials and deploy accordingly” Jagbir Singh, chief technology officer (CTO) of Vi said on Friday. He didn’t divulge details of the partners are.

5Gi is currently being evaluated by India’s Telecommunication Engineering Center (TEC) for commercial adoption in India. Experts believe that 5Gi is a better option for setting up rural connectivity as it is cost-effective, improves spectral efficiency, and reduces spectrum wastage of up to 11 per cent compared to its global counterpart — the 3GPP approved 5G standard. However, existing telecom operators and equipment vendors are not in favor of adopting the local standard as they say 5Gi is yet to show any of these performance gains at a commercial scale.

Vodafone Idea has partnered with L&T Smart World and Communications, Athornet, Vizzbee Robotics, Tweek labs, Athonet, Nokia and Erricson to provide enterprise solutions. Arvind Nevatia, Chief Enterprise Officer, Vodafone Idea, also said that Vi will be looking to partner with other enterprises now that they have been granted a six month extension on 5G trials.

Vi has been allocated 26 GHz and 3.5 GHz spectrum in the mmWave band by the DoT, for 5G network trials and use cases. Vi has achieved peak speeds in excess of 1.5 Gbps on 3.5 GHz, more than 4.2 Gbps on 26 GHz and up to 9.8 Gbps on backhaul spectrum of E-bands.

Indian telcos, network equipment and chipset vendors along with handset have opposed the incorporation of 5Gi as a national standard citing compatibility issues with 3GPP’s global 5G standard, which has already been adopted globally for commercial live networks. Telcos had urged the Department of Telecom (DoT) and the TEC to merge 5Gi with 3GPP’s global 5G NR spec to achieve scale and bring down costs, but that has not happened yet.

“We follow the 3gpp standards (they are specs- not standards– and have no official standing) for the core network…along with the firewalls. We are going to ensure whatever we do for our IT and network platform specific for the core data protection policy in coordination with 3GPP. Network slicing ensures data protection for each enterprise…all customers are equally protected in terms of security,” he added.

On Friday, Vodafone Idea (Vi) demonstrated some of the 5G technology solutions and use cases as a part of its ongoing 5G trials on government allocated 5G spectrum in Pune, Maharashtra and Gujarat. These tests come at a time when the three rivals -Bharti Airtel, Reliance Jio. and Vi are trying to keep pace with each other in the race towards next generation technology.

Singh added that Vi has 30-35% fiber for backhaul for its wireless network, which it is increasing in urban areas. “5G will be a combination of fiber and E band.”

The company is now preparing to expand the scope of 5G trials and is in talks with its and is in talks with its existing customers and startups. Rival Airtel became the first telco to test 5G technology in the 700Mhz band on Thursday. The telco will be working with start-ups for more use cases.

“We were not aware that we will be getting an extension for trials till 3-4 weeks back. We were not doing that on a very high intensity basis, but now with the clarity we will restart the process of engagement,” Arvind Nevatia, Chief enterprise business officer, Vi.

The telco highlighted new revenue models, as a result of 5G. “What we are seeing is evolving models from fixed commission basis to subscription models whether it is in the consumer space or the SAAS space , a lot of new revenue models are emerging in the country…. ,” said Nevatia.

However, prices of 5G have been a contentious issue between the sector and the government. Chief regulatory officer P Balaji said the decision will be taken by the government, which is setting up the auction process process including consultation on prices with the regulator.

“We see Vodafone Idea as an active partner in the digital vision of the government and as India develops its own 5G plans , we will be happy to participate”, said Balaji.

The current base price of Rs 492 crore for a unit of 5G spectrum in the 3.3-3.6 GHz band has been deemed too expensive by all three Indian telcos.

Many experts believe that adoption of the ITU-R M.2150 5Gi standard in India by the government will enable India to leap-frog in the 5G space, with key innovations introduced by Indian entities accepted as part of global wireless standards for the first time. The nation stands to gain enormously both in achieving the required 5G penetration in rural and urban areas as well as in nurturing the nascent Indian R&D ecosystem to make global impact. TSDSI’s efforts are aligned with the national digital communication policy that promotes innovation, equipment design and manufacturing out of India for the world market. The TSDSI 5G standard also has the potential to make a significant impact in several countries with poor rural broadband wireless coverage. TSDSI remains committed to the development of globally harmonized 5G standards with substantial innovations to address hitherto neglected needs of countries such as India. TSDSI-RIT is a step in the right direction so that our indigenous technologies for rural coverage and connectivity find their rightful place in the 5G eco-system that will be deployed in India and elsewhere.

Vodafone evaluating wind-powered mobile masts for remote area connectivity

UK based network operator Vodafone is examining one solution for connecting remote areas which use mobile masts that power themselves. Vodafone has been working with a company called Crossflow Energy, which has a very interesting clean technology called Transverse Axis Wind Turbines. The turbines look more like something you’d find on a paddle steamer, but they’re apparently more efficient and reliable than regular ones. Vodafone’s plan is to use them, in combination with solar and battery technologies to make self-powering masts.

Vodafone has developed self-powered cell towers and aims to deploy them across the UK. This is the latest part of its plan to expand its reach and offer new services while reducing energy consumption in its future networks, supporting its target of achieving net-zero for UK operations by 2027.

Vodafone regards the adoption of technologies such as the self-powered site as essential to meeting its energy-saving ambitions. As well as reducing Vodafone’s energy consumption, self-powered sites remove the need to connect to the electricity grid, overcoming what the operator says can be an insurmountable civil engineering challenge when building new sites in the most rural parts of the UK.

Other potential benefits of the Eco-Towers cited by Vodafone include: the use of locally generated renewable power to reduce the environmental impact of the site; increased renewable contribution by combining wind and solar with battery storage systems on site, which could remove reliance on diesel generators for back-up power; the quiet, bird-friendly turbine could make the Eco-Tower viable for the most sensitive of sites, including areas of outstanding natural beauty; and on-site power generation that is independent from the electricity grid may improve security of supply.

“We are committed to improving rural connectivity, but this comes with some very significant challenges,” said Andrea Dona, chief network officer at Vodafone UK. “Connecting masts to the energy grid can be a major barrier to delivering this objective, so making these sites self-sufficient is a huge step forward for us and for the mobile industry.

“Our approach to managing our network as responsibly as possible is very simple: we put sustainability at the heart of every decision. There is no silver bullet to reducing energy consumption, but each of these steps forward takes us closer to achieving net-zero for our UK operations by 2027.”

Martin Barnes, CEO at Crossflow Energy, added: “We are really excited to be working with Vodafone. It’s a fantastic opportunity to show how our self-powered Eco-Tower solves the problem of harnessing ‘small wind’ to offer not just that all-important carbon reduction, but also significant commercial benefits.

“In the case of Vodafone, it will help to accelerate the expansion of rural connectivity, transform energy consumption patterns and deliver significant economic and carbon savings. Our turbine technology has equally strong applications for so many other industries, but to have such a high-profile player as Vodafone deploying our Eco-Tower is a major endorsement for us and our technology.”

https://www.computerweekly.com/news/252510074/Vodafone-announces-trial-of-self-powered-mobile-masts

https://telecoms.com/512340/vodafone-looks-into-wind-powered-mobile-masts/

https://www.capacitymedia.com/articles/3830223/vodafone-to-launch-self-powered-mobile-towers

Chile plans submarine cable to Antarctica

Infrastructure association Desarrollo País, Chile telecoms regulator Subtel and Magallanes region have signed an agreement on the deployment of a submarine cable between Antarctica and Chile. The agreement involves a market consultation process for the preparation of a technical, legal, economic, and financial feasibility study.

“As a government we are determined to carry out this enormous project and, in this way, contribute strategically to the concerns of the international community and to expand the development of scientific cooperation,” Chile transport and telecommunications minister Gloria Hutt said in a press release.

Earlier this year, Argentine company Silica Networks had also announced a US$ 2M investment for an Antarctic cable feasibility study that includes its subsidiaries in Brazil and Chile.

The deal paves the way for a market consultation process on the future preparation of a technical, legal, economic and financial feasibility study, said Subtel, adding that the proposed route would cover a distance of around 1,000 kilometers from Puerto Williams to King George Island.

According to Subtel, Chile’s existing infrastructure in Puerto Williams on the Tierra del Fuego archipelago gives it a clear advantage over other continents, in that the facilities already available at the corresponding landing station provide a unique opportunity for the deployment of an undersea fibre-optic cable across the Southern Ocean.

The infrastructure is part of the country’s ‘Fibra Optica Austral‘ backbone project to roll out nearly 4,622 km of fiber-optic infrastructure in the Patagonia region, allowing the construction of a high-capacity digital channel for the development of all types of activities in Antarctica.

In October 2020, Subtel announced that local operator Entel had successfully connected the town of Puerto Williams in the far south of the country to the Fibra Optica Austral (FOA) fiber optic system. Hundreds of inhabitants in the digitally isolated locality in the Tierra del Fuego archipelago can now access reliable mobile broadband services for the first time thanks to the public-private initiative between the operator and Subtel.

The aim of the FOA project is to boost telecommunications for the 300,000 Chileans who live in the underserved Patagonia region, bringing much-needed economic, tourism and trade benefits to around 30 percent of the Chilean territory. A 3,000km submarine cable is being rolled out from Puerto Montt to Puerto Williams with landings at Caleta Tortel and Punta Arenas plus a land-based stretch from Puerto Natales to Porvenir in Magallanes.

Puerto Williams is the second town to be connected to FOA after a 4G base station was activated in Caleta Tortel in the Aysen region earlier this year.

References:

https://www.bnamericas.com/en/news/chile-plans-submarine-cable-to-antarctica

https://www.telecompaper.com/news/chile-consults-on-first-undersea-cable-to-antarctica–1405703

Hyperscalers Outpace Network Operators in Private 5G

Microsoft is the most innovative private network provider globally, according to enterprises already using a private LTE and 5G network, finds a new study from Omdia.

AT&T and Deutsche Telekom are also singled out as industry pace setters, according to Omdia’s latest Private LTE and 5G Networks research which surveyed enterprises globally. Two thirds of enterprises require private network suppliers to demonstrate integration with their existing cloud platform before they will buy. Similar demands apply to enterprises’ IoT and application management platforms.

“Enterprises have needs beyond connectivity when they buy a private network,” advises Omdia principal analyst for Private Networks Pablo Tomasi. “The top two reasons enterprises invest in private networks are better security and digital transformation. They need partners that can service those needs. Telcos may lose out if they don’t step up.”

Enterprises also want these results to be achieved promptly. 55% of enterprises expect a two-year return on their private network investment, but almost a fifth of those already deployed expect ROI in only a year.

Consumption preferences are changing fast: three quarters of enterprises now planning a private network prefer a hybrid model instead of the fully dedicated private networks that dominate 70% of deployments today.

The findings are from an annual survey conducted by Omdia on enterprises using, trialling, or planning to deploy private LTE and 5G networks in six key verticals, part of the Private Networks Intelligence Service. A total of 451 respondents from seven countries participated in the survey.

Full analysis of the survey is available in Omdia’s Private LTE and 5G Network Enterprise Survey Insight – 2021 report.

………………………………………………………………………………………………………………….

What is Private Wireless?

One of the challenges with the private wireless concept is that it is not a specific technology but rather more of a broad term encompassing a wide range of technologies. Marketing departments will have some wiggle room, as the meaning of private wireless varies significantly across the ecosystem.

Some Wi-Fi suppliers, for example, believe they provide private wireless connectivity to enterprises. Smaller radio access network (RAN) suppliers without macro footprints typically associate private wireless with dedicated standalone connectivity for enterprises, while some of the more established macros RAN suppliers envision private wireless as encompassing a broader set of technologies, including both macro and small cell networks.

Suppliers focused on mission-critical and public safety networks see private LTE and NR combined with a new spectrum as an opportunity to upgrade existing private narrowband communications equipment. With the number of LoRa end nodes surpassing 0.2 B, LoRa base station suppliers believe they are dominating the private wireless IoT market.

The operators are also positioning the concept differently, with some focusing on the benefits with broader coverage, while others are capitalizing on some of the new local concepts.

While definitions or interpretations vary widely on the part of both suppliers and operators, there appears to be a greater consensus among customers.

For end-users, private wireless typically means consistent, reliable, and secure connectivity, not accessible by the public, to foster efficiency improvements. For industrial sites, private wireless typically means low latency and high reliability. It is less about the underlying technology, spectrum, or business model and more about solving the connectivity challenge. In other words, end-users don’t care what is under the hood.

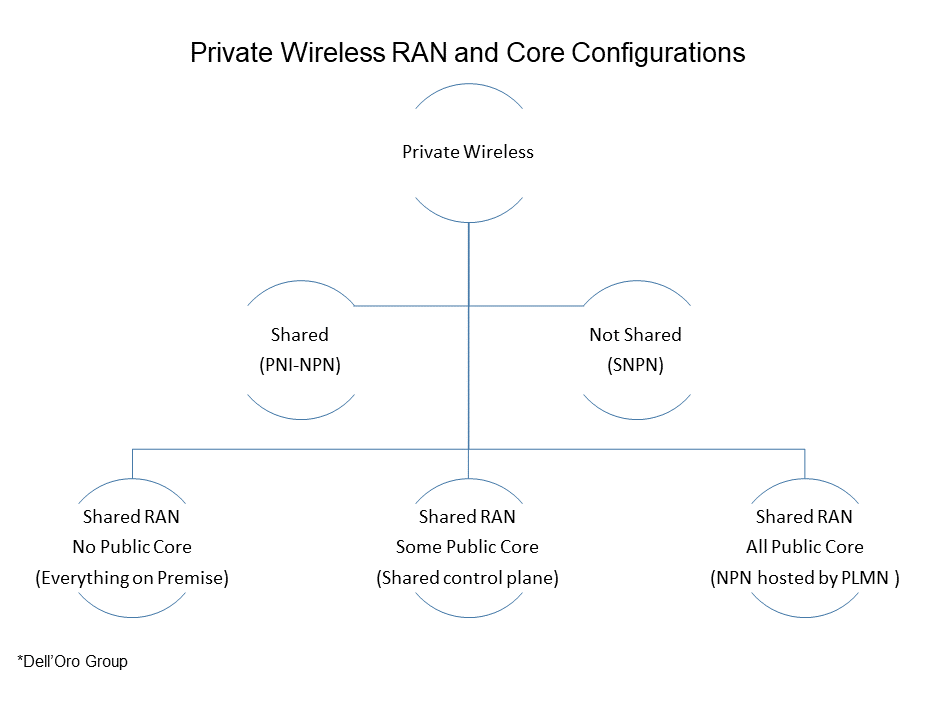

From a Dell’Oro perspective, we consider private wireless as nearly synonymous with 3GPP’s vision for NPNs. According to 3GPP, NPNs are intended for the sole use of a private entity, such as an enterprise. NPNs can be deployed in a variety of configurations, utilizing both virtual and physical elements located either close to or far away from the site. NPNs might be offered as a network slice of a Public Land Mobile Network (PLMN), be hosted by a PLMN, or be deployed as completely standalone networks.

From an end-user perspective, private wireless is also a broader term, generally including not just the RAN but also transport, mobile core network (MCN), Multi-Access Edge Computing (MEC), and corresponding services.

Private Wireless RAN and Core Configurations

There is no one-size-fits-all when it comes to private wireless. We are likely looking at hundreds of deployment options available when we consider all the possible RAN, Core, and MEC technology, architectures, business, and spectrum models.

At a high level, there are two main private wireless deployment configurations, Shared (between public and private) and Not Shared:

- The shared configuration, also known as Public Network Integrated-NPN (PNI-NPN), shares the resources between the private and public networks.

- Not Shared, also known as Standalone NPN (SNPN), reflects dedicated on-premises RAN and core resources. No network functions are shared with the Public Land Mobile Network (PLMN).

Market Status

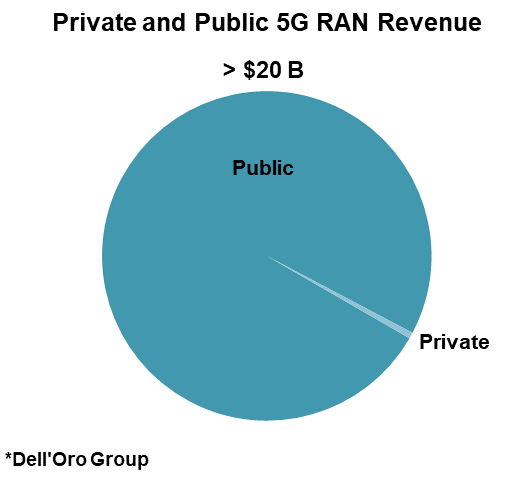

Preliminary 3Q21 estimates suggest the high-level trends remain unchanged with MBB and FWA dominating the 5G capex while private RAN revenues remain small —leading RAN vendors are reporting that private 5G revenues are still negligible relative to the overall public and private 5G RAN market.

Meanwhile, private wireless activity using both macro and local base stations is rising:

- Huawei estimates there are now around 10 K 5G B2B projects globally and the supplier is engaged in thousands of trials focusing on various 5G private use cases.

- Ericsson is currently involved in hundreds of private wireless customer engagements, including pilots with time-critical use cases.

- Even though Nokia’s enterprise business declined year-over-year in 3Q21, Nokia’s private wireless segment continued to gain momentum in the quarter–Nokia now has 380+ private wireless customers.

- ZTE has developed more than 500 cooperative partners in 15 industries, including industrial engineering, transportation, and energy. They have jointly explored 86 innovative 5G application scenarios and successfully carried out more than 60 demonstration projects worldwide supporting multiple 5G IoT use cases.

- Federated Wireless, one of the leading CBRS SAS providers, is working on hundreds of CBRS-based private wireless trials in multiple vertical domains, including warehouse logistics, agriculture, distance learning, and retail applications.

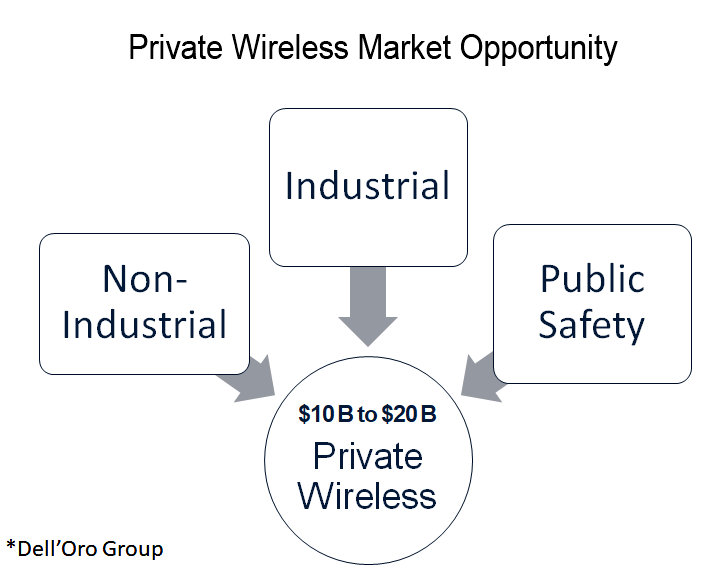

Market Opportunity and Forecast

One of the more compelling aspects with private wireless is that we are talking about new revenue streams, incremental to the existing telco capex. More importantly, the TAM is large, approaching $10–20 B when we include Non-Industrial, Industrial, and Public Safety driven applications.

At the same time, it is important to separate the TAM from the forecast. Here at the Dell’Oro Group, we continue to believe that it will take some time for enterprises to fully conceptualize the value of 5G relative to Wi-Fi. And as much as we want 5G to be as easy to deploy and manage as Wi-Fi, the reality is that we are not yet there.

Still, the uptick in the activity adds confidence the industry is moving in the right direction. And although LTE is dominating the private wireless market today, private 5G NR revenues remain on track to surpass $1 B by 2025.