China’s government has selected 6G as one of its priority projects for 2023. At a national conference on industry and information technology, the Ministry for Industry and IT (MIIT) Jin Zhuanglong, said China intends to push forward in “comprehensive” development of 6G this year. In 2023, China will introduce policies and measures to promote coordinated development of new information infrastructure construction and accelerate the construction of 5G and gigabit optical networks, Jin said. MIIT will also improve policies on telecom market development, and strengthen the protection of personal information and users’ rights and interests.

Editor’s Note: Work on 6G has not yet started in either 3GPP or ITU-R WP 5D. The latter SDO is progressing draft reports on the vision of IMT for 2030 and Beyond, but no 6G requirements will be identified.

More than 2.3 million 5G base stations have been put into service, and notable progress has been made in the construction of new data centers, according to the conference.

In recent years, China has intensified efforts to promote the construction of new information infrastructure, deepen the construction of 5G, gigabit optical network and industrial internet, and promote the deep integration of the digital economy and the real economy.

Image Credit: Alan Novelli/Alamy Stock Photo

At the end of last year China Telecom issued a white paper setting out its vision for 6G. Written by the China Telecom Research Institute, the paper proposes a distributed and intelligent programmable RAN (P-RAN) network architecture and what it calls a “three-layer and four-sided” framework. The white paper notes that because of the cost of building out the dense mmWave or terahertz-band networks, it will be essential to provide device-to-device connectivity.

Six months ago, heavyweight China Mobileissued its own 6G vision, calling for “three bodies, four layers and five sides.”

China’s other 6G news is a call for proposals on potential key technologies from the national coordinating body, the IMT-2030 6G Promotion Group. According to an English-language statement posted by CAICT, the main objectives are “to inspire university-academy-industry-association entities for technology innovations, gather and form a rich reserve of 6G potential key technologies, and support 6G research, standardization, and industrial R&D.”

Non-Chinese universities and research organizations are welcome to apply ahead of the deadline in November 2023. The proposed solutions should have “application and promotion value for 6G innovation and development,” and the key technical indicators should be capable of being evaluated and verified, the statement said.

Artificial Intelligence (AI) in telecom uses software and algorithms to estimate human perception in order to analyze big data such as data consumption, call record, and use of the application to improve the customer experience. Also, AI helps telecommunication operators to detect flaws in the network, network security, network optimization & offer virtual assistance. Moreover, AI enables the telecom industry to extract insights from their vast data sets and made it easier to manage the daily business and resolve issues more efficiently and also provide improved customer service and satisfaction.

The growing adoption of AI solutions in various telecom applications is driving market growth. The rising number of AI-enabled smartphones with a number of features such as image recognition, robust security, voice recognition and many as compared to traditional phones is boosting the growth of AI in the telecommunication market. Furthermore, to cater to complex processes or telecom services, AI provides a simpler and easier interface in telecommunication. In addition, growing Over-The-Top (OTT) services, such as video streaming, have transformed the dissemination and consumption of audio and video content. With more consumers turning to OTT services, consumer demand for bandwidth has grown considerably. Carrying such ever-growing traffic from OTT services leads to high operational Expenditure (OpEx) for the telecommunication industry. Hence, AI helps the telecom industry to reduce operational costs by minimizing the human intervention needed for network configuration and maintenance. However, the major restraint of the AI in telecommunication market is the incompatibility between telecommunication systems and AI technology. Contrarily, the increasing penetration of AI-enabled smartphones in the telecommunication industry, and the advent of 5G technology in smartphones are expected to provide major growth opportunities for the growth of the market. Since advancements such as 5G technology in mobile and the rising need to monitor content on the tale communication network to eliminate human error from telecommunication are driving the growth of the market. For an instance, the Chinese government trying to improve its network services and telecommunication services; hence China Telecom Corporation has started a new 5G base station in Lanzhou city. Therefore, these factors are expected to provide numerous opportunities for the expansion of the AI in telecommunication market during the forecast period.

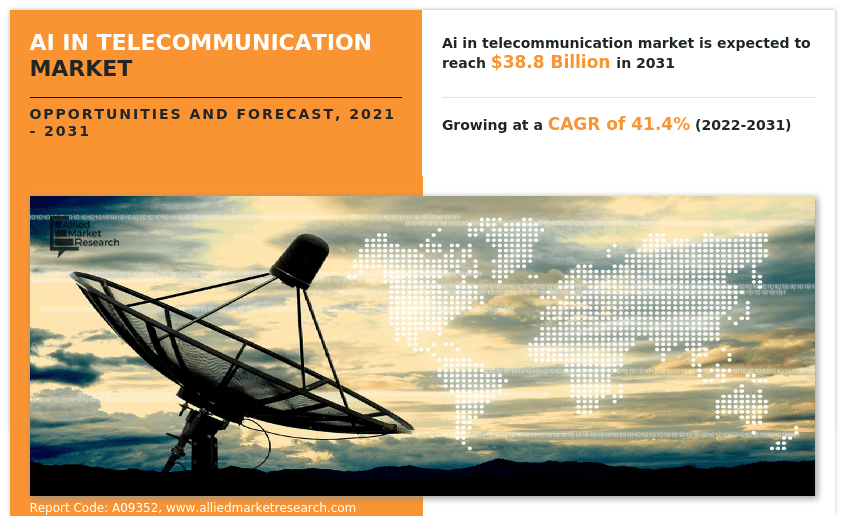

Allied Market Research published a report, titled, “AI in Telecommunication Market by Component (Solution, Service), by Deployment Model (On-Premise, Cloud), by Technology (Machine Learning, Natural Language Processing (NLP), Data Analytics, Others), by Application (Customer Analytics, Network Security, Network Optimization, Self-Diagnostics, Virtual Assistance, Others): Global Opportunity Analysis and Industry Forecast, 2021-2031.”

According to the report, the global AI in telecommunication industry generated $1.2 billion in 2021, and is estimated to reach $38.8 by 2031, witnessing a CAGR of 41.4% from 2022 to 2031. The report offers a detailed analysis of changing market trends, top segments, key investment pockets, value chain, regional landscape, and competitive scenario.

Drivers, Restraints, and Opportunities:

Growing adoption of AI solutions in various telecom applications, the ability of AI to provide a simpler and easier interface in telecommunication and reduce the human intervention needed for network configuration and maintenance, and the growing demand for high bandwidth with more consumers turning to OTT services drive the growth of the global AI in telecommunication market. However, the incompatibility between telecommunication systems and AI technology hampers the global market growth. On the other hand, the increasing penetration of AI-enabled smartphones in the telecommunication industry, and the advent of 5G technology in smartphones likely to create potential opportunities for growth of the global market in the coming years.

Covid-19 Scenario:

The global artificial intelligence in telecommunication market saw a stable growth during the COVID-19 pandemic, owing to the increasing digital penetration and rise in automation.

Moreover, the pandemic led the telecommunications infrastructure to keep businesses, governments, and communities connected and operational. The social and financial disruption caused by the pandemic forced people to depend on technology such as AI for information and remote working.

AI also helped the telecom industry to reinvent customer relationships by identifying personalized needs and engaging with customers through hyper-personalized one-to-one contacts. It also helped configure fixed-line and mobile-network bundles that combine VPN, teleconferencing, and productivity apps.

The solution segment to dominate in terms of revenue during the forecast period:

Based on component, the solution segment was the largest market in 2021, contributing to more than two-thirds of the global AI in telecommunication market, and is expected to maintain its leadership status during the forecast period. This is due to the adoption of solutions by various end users for the automated processes. On the other hand, the service segment is projected to witness the fastest CAGR of 44.9% from 2022 to 2031, due to surge in the adoption of managed and professional services.

The on-premise segment to garner the largest revenue during the forecast period:

Based on deployment model, the on-premise segment held the largest market share of nearly three-fifths of the global AI in telecommunication market in 2021 and is expected to maintain its dominance during the forecast period. This is because it provides added security of data. The cloud segment, however, is projected to witness the largest CAGR of 43.8% from 2022 to 2031, as cloud provides flexibility, scalability, complete visibility, and efficiency to all processes.

The machine learning segment to exhibit a progressive revenue growth during the forecast period:

Based on technology, the machine learning segment held the largest market share of more than two-fifths of the global AI in telecommunication market in 2021, and would maintain its dominance during the forecast period. This is because machine learning algorithms are designed to keep improving accuracy and efficiency. The data analytics segment, however, is projected to witness the largest CAGR of 46.1% from 2022 to 2031, as it helps telecom companies to increase profitability by optimizing network usage and services.

Asia-Pacific to maintain its leadership in terms of revenue by 2031:

Based on region, North America was the largest market in 2021, capturing more than one-third of the global AI in telecommunication market. The growth in the region can be attributed to the infrastructure development and technology adoption in countries like the U.S. and Canada. However, the market in Asia-Pacific is expected to lead in terms of revenue and manifest the fastest CAGR of 45.7% during the forecast period, owing to the growing digital and economic transformation of the region.

Leading Market Players:

Intel Corporation

Nuance Communications, Inc.

AT&T

Infosys Limited

ZTE Corporation

IBM Corporation

Google LLC

Microsoft

Salesforce, Inc.

Cisco Systems, Inc.

The report analyzes these key players of the global AI in telecommunication market. These players have adopted various strategies such as expansion, new product launches, partnerships, and others to increase their market penetration and strengthen their position in the industry. The report is helpful in determining the business performance, operating segments, product portfolio, and developments by every market player.

Gartner defines the network firewall market as the market for firewalls that use bidirectional stateful traffic inspection (for both egress and ingress) to secure networks. Network firewalls are enforced through hardware, virtual appliances and cloud-native controls. Network firewalls are used to secure networks. These can be on-premises, hybrid (on-premises and cloud), public cloud or private cloud networks. Network firewall products support different deployment use cases, such as for perimeters, midsize enterprises, data centers, clouds, cloud-native and distributed offices.

Network firewalls are used to secure networks. These can be on-premises, hybrid (on-premises and cloud), public cloud or private cloud networks. Network firewall products support different deployment use cases, such as for perimeters, midsize enterprises, data centers, clouds, cloud-native and distributed offices.

The network firewall market has evolved to include the following segments, each of which has a specific set of features:

Cloud firewalls: These firewalls from cloud infrastructure vendors are designed for cloud-native deployment as separate virtual instances or in containers. Container firewalls can also secure connections between containers.

Hybrid mesh firewalls: These are platforms that help secure hybrid environments by extending modern network firewall controls to multiple enforcement points, including FWaaS and cloud firewalls, with centralized management via a single cloud-based manager.

Firewall as a service (FWaaS): A FWaaS is a multifunction security gateway delivered as a cloud-based service, often to protect small branch offices and mobile users.

Network firewalls’ capabilities include advanced networking, threat inspection and detection, and web filtering.

Core capabilities:

Networking: This includes support for routing tables with destination network address translation (DNAT) and static network address translation (SNAT) capability.

Stateful inspection: This enables inspection of traffic based on stateful firewall rules.

Threat detection and inspection: This includes intrusion prevention system (IPS) and malware inspection capabilities.

Web filtering: This includes filtering of outbound traffic for HTTP and HTTPS and applications.

Advanced logging and reporting: All actions of firewall administrators can be logged, and reports can be customized and run based on different object types and traffic types. Threat-based and web-filtering-based granular reports can be generated.

Optional capabilities:

Internet of Things (IoT) security: This is achieved either using a module built into threat detection controls or via a dedicated subscription integrated within network firewall offerings. Specific features may include discovery of IoT devices, risk analysis and dedicated rules to block attacks related to these devices. Also, IoT signatures as a part of IPS signature base.

Network sandboxing: Network sandboxing monitors network traffic for suspicious objects and automatically submits them to the sandbox environment, where they are analyzed and assigned malware probability scores and severity ratings.

Zero trust network access (ZTNA): Zero trust network access (ZTNA) makes possible an identity- and context-based access boundary between any user and device to applications.

Operational technology (OT) security: This includes integrated or dedicated features related to protecting an OT environment. Stand-alone OT security offerings are not considered here. Features may include dedicated OT-related threat intelligence, dedicated IPS signatures for OT devices, support for supervisory control and data acquisition (SCADA) applications and threat inspection.

Domain Name System (DNS) security: This secures traffic to DNS by offering monitoring, detection and prevention capabilities against DNS layer attacks.

Software-defined wide-area network (SD-WAN): This provides dynamic path selection, based on business or application policy, centralized policy and management of appliances, virtual private network (VPN), and zero-touch configuration

As network firewalls evolve into hybrid mesh firewalls with the emergence of cloud firewalls and firewall-as-a-service offerings, selecting the most suitable vendor is a challenge. Gartner assessed 17 Network Firewall vendors to help security and risk management leaders make the right choice for their organization.

Fortinet was recognized in 2022 Gartner® Magic Quadrant™ for Network Firewalls for the 13th time. It leads for appliance-based distributed-office use cases, thanks to its offer of mature SD-WAN and firewall capabilities in a single box.

The company’s FortiGate Next-Generation Firewalls deliver seamless AI/ML-powered security and networking convergence over a single operating system (FortiOS) and across any form factor. This includes hardware appliances, virtual machines, and SASE services.

In addition to FortiGate, its firewall product, Fortinet offers SASE, networking and security operations products.

Major firewall-related updates in 2022 have included the introduction of ZTNA, an in-line sandbox and an in-line CASB. Fortinet has also enabled further integration between FortiGate and its network access control (FortiNAC), and introduced a security operations center (SOC) as a service, offered as a bundle with a FortiGate license.

Integrated SD-WAN: Fortinet offers built-in advanced SD-WAN and routing capabilities in FortiGate firewall appliances. Fortinet offers a complete SD-WAN package, with features including forward error correction, packet duplication, and intelligent and dynamic app routing.

Hybrid ZTNA deployment: Fortinet offers flexible ZTNA deployment modes. ZTNA enforcement is part of the FortiGate operating system (FortiOS) and can be deployed on-premises or as a service as part of FortiSASE (a stand-alone offering). The vendor has also introduced an in-line CASB integrated with ZTNA capabilities.

Product portfolio: Fortinet has a large product portfolio. It offers products for networking, network security and security operations. The majority of its products can be managed through a single management interface and offer integration through the Fortinet Security Fabric.

Centralized management: Fortinet offers mature on-premises and cloud-based centralized management through FortiManager and FortiCloud, respectively. These offerings have feature parity and support centralized management of the majority of Fortinet’s devices. FortiGate customers like the ease of management and configuration of Fortinet’s firewalls.

FortiGate NGFWs offer (Source: Fortinet):

Powerful security and networking convergence. Secure networking services like SD-WAN, ZTNA, and SSL decryption are included – no need for extra licensing.

Best price-per-performance. Our unique ASIC architecture delivers the highest ROI plus hyperscale support and ultra-low latency.

AI/ML-poweredthreat protection. Multiple AI/ML-powered security services stop advanced threats and prevent business disruptions.

Palo Alto Networks was among the 17 vendors that Gartner evaluated for its 2022 Magic Quadrant for Network Firewalls, which evaluates vendors’ Ability to Execute as well as their Completeness of Vision. Palo Alto Networks believes its vision of offering best-in-class security as part of an integrated network security platform, combined with its commitment to customer success, has helped the company earn a Leader position for the 11th consecutive year.

“From the industry’s first Next-Generation Firewall in 2007 to the most recently announced PAN-OS 11.0 Nova, Palo Alto Networks relentless innovation helps provide powerful protection for customers. We are honored to be recognized as a Leader in eleven consecutive Gartner Magic Quadrant for Network Firewalls reports,” said Anand Oswal, senior vice president for Products, Network Security. “We believe this recognition by Gartner is a testament to both our innovation, using ML and AI to stop the most evasive threats, and our ability to simplify network security for our customers with a consolidated platform approach.”

Palo Alto Networks believes its leader position in network firewalls is fueled by:

Best-in-class security that prevents zero-day threats: Modern malware is now highly evasive and sandbox-aware. To address this, the recently announced PAN-OS 11.0 Nova introduced the new Advanced WildFire® cloud-delivered security service, which provides unprecedented protection against evasive malware. Advanced Threat Prevention (ATP) now helps protect against zero-day injection attacks in addition to highly evasive command-and-control communications. Additionally, Advanced URL Filtering offers industry-first prevention of zero-day web attacks with inline machine learning capabilities.

Strength in SASE: The industry’s most complete SASE solution, Prisma® SASE simplifies secure access by connecting all users and locations with all apps from a single product. The superior security of ZTNA 2.0 protects both access and data to dramatically reduce the risk of a data breach, while a cloud-native architecture with integrated Autonomous Digital Experience Management (ADEM) provides exceptional user experiences.

Helping customers improve their security posture: Palo Alto Networks AIOps helps customers adopt best practices with guided recommendations, reduce misconfigurations that can lead to security breaches, and predict network-impacting issues before they occur. AIOps, launched earlier this year, now processes 49 billion metrics monthly across 60,000 firewalls and proactively shares 24,000 misconfigurations and 17,000 firewall health and other issues with customers for resolution every month.

A comprehensive product portfolio offered as a platform: Palo Alto Networks offers multiple cloud-delivered security services that work together to prevent attacks at every stage of the attack lifecycle. These security services are offered as part of a network security platform, which makes it easy for customers to consume these services while consistently protecting their data centers, branch offices and mobile workers as well as applications in multicloud and hybrid environments with best-in-class security everywhere.

Since the Gartner evaluation, Palo Alto Networks has further strengthened its NGFW capabilities with the announcement of the latest version of its industry-leading PAN-OS® software, PAN-OS 11.0 Nova. The innovations announced also included the new Advanced WildFire cloud-delivered security service, which brings unparalleled protection against evasive malware, enhancements in the Advanced Threat Prevention service and new fourth-generation ML-powered NGFWs. The company has also taken strides to enhance its customer support experience and grown its Global Customer Service organization.

IDC forecasts that worldwide revenue for enterprise applications will grow from $279.6 billion in 2022 to $385.2 billion in 2026 with a five-year compound annual growth rate (CAGR) of 8.0%. Nearly all this growth will come from investments in public cloud software, which is expected to represent nearly two thirds of all enterprise applications revenue in 2026.

While the process of migrating from on-premises applications to the cloud can take years, enterprise software vendors and their customers will continue the transition to the cloud as this is an essential part of business operations in the digital world. Companies that do not pursue this technology will sustain losses due to profound opportunity costs as their competitors adopt cloud technologies and the use of application programming interfaces (APIs), moving beyond the reach of technological holdouts with on-premises or homemade solutions.

“It’s no longer enough for businesses to sit back and rely on their technological debt of software and hardware assets to keep the company running. In the digital world, enterprise software needs to constantly innovate to keep up with demand for speed, scale, and a resilient business,” said Heather Hershey, research director, Worldwide Digital Commerce at IDC. “Organizations must invest in new tools to keep their application portfolio up to date as they move into the digital era, automating all processes while also leveraging innovation and a wealth of data to become a more creative and resilient company in the digital realm.”

In addition to the ongoing cloud migration, IDC has identified a number of other significant market developments that are driving growth in the enterprise applications market.

SaaS and cloud-based, modular, and intelligent applications are no longer “nice to have” but are instead essential for business. Organizations that want to stay in business need AI-driven software that is cloud enabled, modular, and intelligent.

Application programmable interface technology will continue to be the backbone of the enterprise applications market. APIs will always resonate as a sound investment to companies that understand the pivotal role they play in connecting all the disparate code bases that make up the modern world.

Phasic migration to cloud with TaskApps augmentation will continue, particularly in B2B enterprises. TaskApps and low-code/no-code development tools are being used to close gaps, extend processes, or change up the business at a faster pace throughout the transition to digital first.

New global regulations around data privacy and ethics have changed the way organizations collect and use data, pushing governance to the forefront of the conversation. Compliance has become a differentiating factor for enterprises that prioritize trustworthiness.

“The digital world is completely altering the way software is utilized and incorporated into the organization from modularity to APIs to low code/no code to business process automation to TaskApps and even with innovation,” said Mickey North Rizza, group vice president, Enterprise Software at IDC. “Organizations are stretching their visions from filling technology gaps to optimizing processes globally to going the last mile with complete differentiators for their clients. The business world is finally starting to leverage the opportunity technology brings to it.”

Photo Credit: Unsplash

The enterprise applications market is a competitive market that includes software specific to certain industries as well as software that can handle requirements for multiple industries. Enterprise applications can be delivered as a pre-integrated suite of applications (featuring common data and process models across functional areas) or as standalone applications that automate specific functional business processes, such as accounting, human capital management, or supply chain execution. The enterprise applications market consists of the following secondary markets: enterprise resource management, customer relationship management, engineering applications, supply chain management applications, and production applications.

The IDC report, Worldwide Enterprise Applications Software Forecast, 2022–2026: Digital Era Software on the Rise (Doc #US48563522), presents a five-year forecast for worldwide enterprise applications revenues, including spending by geographic region and deployment type (public cloud and on premises). The report also provides insight into the market’s evolution through 2026, including deployment models, trends, and significant market developments.

In a separate report titled Worldwide Quarterly Enterprise Infrastructure Tracker: Buyer and Cloud Deployment, IDC sas that spending on compute and storage infrastructure products for cloud deployments, including dedicated and shared IT environments, increased 24.7% year over year in the third quarter of 2022 (3Q22) to $23.9 billion. Spending on cloud infrastructure continues to outgrow the non-cloud segment although the latter had strong growth in 3Q22 as well, increasing at 16.5% year over year to $16.8 billion. The market continues to benefit from high demand and large backlogs, coupled with an improving infrastructure supply chain.

Spending on shared cloud infrastructure reached $16.8 billion in the quarter, increasing 24.4% compared to a year ago. IDC expects to see continuous strong demand for shared cloud infrastructure with spending expected to surpass non-cloud infrastructure spending in 2023. The dedicated cloud infrastructure segment grew 25.3% year over year in 3Q22 to $7.1 billion. Of the total dedicated cloud infrastructure, 45.2% was deployed on customer premises.

For the full year 2022, IDC is forecasting cloud infrastructure spending to grow 19.6% year over year to $88.1 billion – a noticeable increase from 8.6% annual growth in 2021. Non-cloud infrastructure is expected to grow 10.7% to $64.7 billion. Shared cloud infrastructure is expected to grow 19.0% year over year to $60.9 billion for the full year while spending on dedicated cloud infrastructure is expected to grow 21.2% to $27.3 billion for the full year.

About IDC:

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,300 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 110 countries. IDC’s analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly owned subsidiary of International Data Group (IDG), the world’s leading tech media, data, and marketing services company. To learn more about IDC, please visit www.idc.com. Follow IDC on Twitter at @IDC and LinkedIn. Subscribe to the IDC Blog for industry news and insights.

ATIS today announced it has executed a memorandum of understanding (MoU) with the O-RAN ALLIANCE to further both organizations’ mutual objectives to advance the industry towards more intelligent, open, virtualized and global standards-compliant mobile networks.

The MoU notes that ATIS and the O-RAN ALLIANCE will collaborate on advancing the state-of-the-art of open radio access network, including Open RAN security and stakeholder requirements for Open RAN. It also addresses the opportunity for ATIS translation of O-RAN ALLIANCE specifications to Open RAN standards to advance the adoption of Open RAN in North America.

“This agreement with the O-RAN ALLIANCE brings the power of ATIS’ 3GPP leadership and its contributions to the continued evolution of 5G, coupled with ATIS’ leadership for 6G and beyond as part of its Next G Alliance, to advance the development of open RAN technologies,” said ATIS President and CEO Susan Miller. “The MoU combines the forces of ATIS and the O-RAN ALLIANCE to connect the present to the future for the open RAN ecosystem, advancing the promise of a robust open RAN marketplace.”

“Continuing the work toward open radio access networks is critical in unlocking the full potential of 5G in North America and will lay the foundation for future generations of wireless technology,” said Igal Elbaz, Chair of ATIS Board of Directors and Network CTO of AT&T. “ATIS and the O-RAN ALLIANCE combining their expertise and resources and ATIS’ adoption of O-RAN specifications to ATIS Open RAN standards will help accelerate the industry’s implementation of open RAN.”

The MoU also addresses participation, by invitation, in meetings of each other’s working groups where appropriate, and promoting and endorsing each other’s events (e.g., conferences and plugfests) or activities (e.g., publication of work results) in areas of mutual interest and with prior consent of the other party.

ATIS’ board is composed of top executives from AT&T, Verizon, T-Mobile, Ciena and Comcast. It’s the group that has previously addressed topics including secure supply chain, robocalls and hearing aid compatibility for cellphones. And it’s also the association behind the new Next G Alliance, which is working to organize a comprehensive U.S. strategy around future 6G technologies.

Also note that ATIS represents 3GPP in ITU-R WP 5D and presents all their IMT contributions on 5G/IMT 2020/ITU-R M.2150. If 3GPP ever includes Open RAN in its specifications, it’s very likely that those will be presented by ATIS to ITU-R for 5G or even 4G LTE.

“Standards-based open RAN will help create a more receptive marketplace for open RAN technology, advance its development and drive adoption in North America,” added ATIS’ VP of technology and solutions, Mike Nawrocki, in a statement to Light Reading.

In the U.S., Dish Network is in the midst of building a nationwide 5G network that adheres to Open RAN specifications. However, it’s unclear whether Dish will be able to profit from its embrace of open RAN. AT&T has told this author they are interested in deploying Open RAN for 5G if it is more economical than legacy RANs. Neither Verizon or T-Mobile has expressed interest in Open RAN.

As a leading technology and solutions development organization, the Alliance for Telecommunications Industry Solutions (ATIS) brings together the top global ICT companies to advance the industry’s business priorities. Our Next G Alliance is building the foundation for North American leadership in 6G and beyond. ATIS’ 160 member companies are also currently working to address 5G, illegal robocall mitigation, quantum computing, artificial intelligence-enabled networks, distributed ledger/blockchain technology, cybersecurity, IoT, emergency services, quality of service, billing support, operations and much more. These priorities follow a fast-track development lifecycle from design and innovation through standards, specifications, requirements, business use cases, software toolkits, open-source solutions and interoperability testing.

ATIS is accredited by the American National Standards Institute (ANSI). The organization is the North American Organizational Partner for the 3rd Generation Partnership Project (3GPP), a founding partner of the oneM2M global initiative, a member of the International Telecommunication Union (ITU) and a member of the InterAmerican Telecommunication Commission (CITEL). For more information, visit www.atis.org. Follow ATIS on Twitter and on LinkedIn.

About O-RAN ALLIANCE:

The O-RAN ALLIANCE is a world-wide community of more than 300 mobile operators, vendors, and research & academic institutions operating in the Radio Access Network (RAN) industry. As the RAN is an essential part of any mobile network, the O-RAN ALLIANCE’s mission is to re-shape the industry towards more intelligent, open, virtualized and fully interoperable mobile networks. The new O-RAN specifications enable a more competitive and vibrant RAN supplier ecosystem with faster innovation to improve user experience. O-RAN based mobile networks at the same time improve the efficiency of RAN deployments as well as operations by the mobile operators. To achieve this, the O-RAN ALLIANCE publishes new RAN specifications, releases open software for the RAN, and supports its members in integration and testing of their implementations.

China will debut the world’s first cruise ship covered by a5G network later this year, due to a collaboration between CSSC Carnival Cruise Shipping Ltd’s own cruise brand Adora Cruises and China Telecom Corp Ltd Shanghai Branch. Adora Cruises [1.] has partnered with Shanghai Telecom, a major 5G network service provider in China, to bring 5G connectivity to its first China-built large cruise ship. This partnership marks a major milestone, as it is the first time a 5G network has been installed on a cruise ship in the world and sets a new standard for connectivity and convenience, according to a press release on Thursday.

Note 1.Adora Cruises is part of CSSC Carnival Cruise Shipping Limited, a joint venture between shipbuilder China State Shipbuilding Corp (CSSC) and U.S.-based leisure travel company Carnival Corporation.

“From network layout, satellite communication, to various digital applications, our goal is to deliver seamless multimedia interactions and consistent mobile connectivity for guests and crew, allowing them to stay connected with loved ones and the world while at sea,” said Chen Ranfeng, Managing Director of CSSC Carnival Cruise Shipping Limited. “By seizing a first-mover advantage in the cruise industry’s 5G market, we hope to set a new standard for digital communication in the marine travel sector.”

Adora Cruises is working towards a future where guests can enjoy an enhanced cruise experience with 5G connectivity and access to all-around multimedia and real-time interaction, the company said.

Image Courtesy of CSSC Carnival Cruise Company

“Combining 5G and satellite technology, we will focus on network communication, digital high-definition, AR/VR and other content services to further improve our guest experience and jointly promote high-quality development of the tourism economy,” said Gong Bo, general manager of Shanghai Telecom. “By seizing a first-mover advantage in the cruise industry’s 5G market, we hope to set a new standard for digital communication in the marine travel sector,” said Ranfeng.

The cruise company’s first two China-built large cruise ships are currently under construction at Shanghai Waigaoqiao Shipbuilding Corp, and will be operated under the brand name of Adora in the future.

The first 135,500-gross-ton Adora cruise ship is expected to start its journey by the end of 2023, while the second vessel is currently still being designed and constructed.

by Geoff Burke, DZS Inc. (a global provider of access networking infrastructure, service assurance and consumer experience software solutions). Edited by Alan J Weissberger

There are a handful of significant trends that will emerge over the next several months as service providers navigate their transformation and seek to find their Competitive EDGE. This post will focus on the increasing shift to multi-gigabit services, the growing importance of the network edge and how service providers are being transformed into “experience providers..

Multi-Gigabit Broadband Services are Becoming the New Standard – The shift to gigabit services was both widespread and well suited for Gigabit Passive Optical Networking (GPON) However, new advanced applications will require symmetrical multi-gigabit speeds. The proliferation of multiple devices using these bandwidth-hungry apps is pushing service providers to begin to think 10 gig services and beyond for both business and residential services. The emergence of the metaverse, with Ultra High Definition (UHD) Augmented Reality/Virtual Reality/Extended Reality (AR/VR/XR) and gaming applications will continue push these boundaries.

The Network Edge Continues to Rise as a Strategic Location – The rise of 10 Gigabit Symmetrical (XGS)-PON and multi-gigabit services that support the above mentioned applications and more is creating new challenges in the network – especially as these apps require symmetrical bandwidth. Service providers realize that they must push equipment as close to the subscriber as possible to optimize traffic management, but also to minimize latency, which is becoming increasingly important in the world of the metaverse and AR/VR/XR apps. Additionally, leveraging intelligence at the edge moves it closer to where data is actually created and consumed and where the subscriber experience is defined giving service providers increased agility in monitoring, managing and optimizing performance.

Service Providers are Rapidly Transforming into Experience Providers – As the network becomes increasingly software defined and intelligent equipment is deployed closer to the edge, the ability for carriers to both gather meaningful information that can reflect and provide actionable insights into user experience grows dramatically. As a result, the concept of a true “experience provider” is emerging where subscriber problems can be anticipated and proactively addressed, and user needs can be addressed remotely and immediately in an extraordinarily personalized manner. This transformation is proving to have profound impacts on carrier performance, with dramatically reduced churn, faster responsiveness, better performance, and higher Average Revenue Per User (ARPU).

India’s Tech Mahindra and Microsoft have announced a collaboration to enable cloud-powered 5G SA core network for telecom operators worldwide. As a part of the collaboration, Tech Mahindra will provide its expertise, comprehensive solutions, and managed services offerings to telecom operators for their 5G SA Core networks. Tech Mahindra will provide its expertise like “Network Cloudification as a Service” and AIOps to global telecom operators for their 5G Core networks. AIOps will help operators combine big data and machine learning to automate network operations processes, including anomaly detection, predicting fault and performance issues.

CP Gurnani, Managing Director and Chief Executive Officer, Tech Mahindra said, “Today, it is critical to leverage next-gen technologies to build relevant and resilient services and solutions for customers across the globe. At Tech Mahindra, we are well-positioned to help telecom operators realize the full potential of their networks and provide innovative and agile services to their customers while also helping them meet their ESG commitments. Our collaboration with Microsoft will further strengthen our service portfolio by combining our deep expertise across the telecom industry with Microsoft Cloud. Further to this collaboration, Tech Mahindra and Microsoft will work together to help telecom operators simplify and transform their operations in order to build green and secure networks by leveraging the power of cloud technologies. At Tech Mahindra, we are well-positioned to help telecom operators realize the full potential of their networks and provide innovative and agile services to their customers while also helping them meet their ESG commitments.”

Tech Mahindra believes the 5G core network will enable use cases such as Augmented Reality (AR), Virtual Reality (VR), IoT (Internet of Things, and edge computing. Of course, 5G URLLC performance requirements, especially ultra low latency, in the RAN and core network must be met first, which they are not at this time. The company will leverage the Microsoft Azure cloud for its sustainability solution iSustain to measure and monitor KPIs across all three aspects of E, S & G. iSustain will help operators address the challenge of measuring and reducing carbon emissions from the networks while meeting demands of the countless energy intense digital technologies, from AR/ VR to IoT.

Anant Maheshwari, President, Microsoft India said, “Harnessing the power of Microsoft Azure, telecom operators can provide more flexibility and scalability, save infrastructure cost, use AI to automate operations, and differentiate their customer offerings. The collaboration between Tech Mahindra and Microsoft will help our customers build green and secured networks with seamless experiences across the Microsoft cloud and the operator’s network. Azure provides operators with cloud solutions that enable them to create new revenue generating services and move existing services to the cloud. Through our collaboration with Tech Mahindra, Microsoft will further help telcos overcome challenges, drive innovation and build green and secured networks that provide seamless experiences by leveraging the power of Microsoft Cloud for Operators.”

The partnership is in line with Tech Mahindra’s NXT.NOWTM framework, which aims to enhance the ‘Human Centric Experience’, Tech Mahindra focuses on investing in emerging technologies and solutions that enable digital transformation and meet the evolving needs of the customer.

About Tech Mahindra:

Tech Mahindra offers innovative and customer-centric digital experiences, enabling enterprises, associates and the society to Rise. We are a USD 6 billion organization with 163,000+ professionals across 90 countries helping 1279 global customers, including Fortune 500 companies. We are focused on leveraging next-generation technologies including 5G, Blockchain, Metaverse, Quantum Computing, Cybersecurity, Artificial Intelligence, and more, to enable end-to-end digital transformation for global customers. Tech Mahindra is the only Indian company in the world to receive the HRH The Prince of Wales’ Terra Carta Seal for its commitment to creating a sustainable future. We are the fastest growing brand in ‘brand strength’ and amongst the top 7 IT brands globally. With the NXT.NOWTM framework, Tech Mahindra aims to enhance ‘Human Centric Experience’ for our ecosystem and drive collaborative disruption with synergies arising from a robust portfolio of companies. Tech Mahindra aims at delivering tomorrow’s experiences today and believes that the ‘Future is Now.’

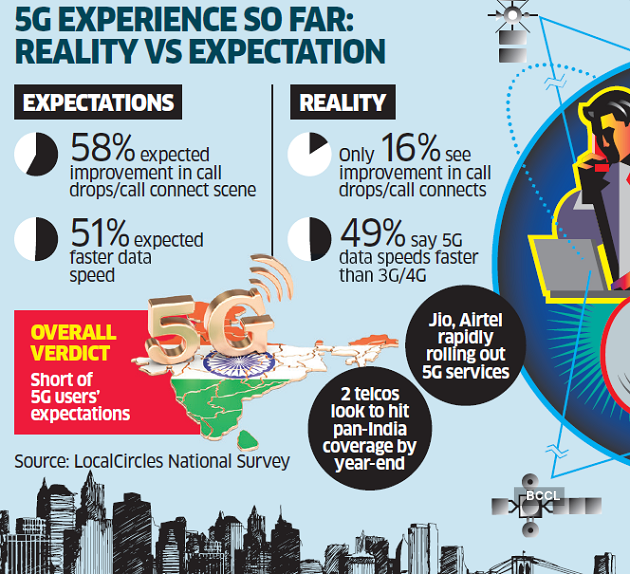

“It’s Not Just You: 5G Is a Big Letdown,” is the title of a Wall Street Journal on-line article published today (January 11, 2023). Author Joanna Stern writes:

I turned off Verizon’s red down pointing triangle 5G on my iPhone—and barely noticed a difference. The 4G LTE performance and coverage felt just about the same.

Three years since the U.S. cellular carriers lit up their next-generation networks and promised to change the game, the game hasn’t changed. And if you’re among the millions of Americans who recently upgraded, you probably already know that. In 2022, 61% of U.S. cellular customers accessed 5G networks, according to Global Wireless Solutions, a network testing and research company.

On Verizon’s Ultra Wideband network, I got 500 Mbps down. But I didn’t notice a difference when streaming Netflix, watching TikTok, loading websites or sending messages. You don’t need a fire hose to extinguish a candle.

Where you might see a difference is during commuting hours and other times of heavy congestion, Chetan Sharma, a telecom-industry analyst, told me. A Verizon spokesman said that 5G’s higher data capacity helps at concerts, sporting events and other crowded areas where everyone is trying to download or upload photos or videos.

“As cars, smart home standards, and so many screens took center stage at this year’s [CES] show, 5G took a back seat,” concludes a Verge article titled, “Where was 5G at CES?” “After years of hype, 5G was seemingly a no-show at CES 2023.” The Verge article continues knocking 5G (and for good reason):

For starters, we’re all sick of hearing about it. And CES has a unique way of rallying around a technology one year and then leaving it for dead the next.

And there was always a time limit on 5G’s newsworthiness — at a certain point, when it becomes the prevailing wireless technology, it’s not going to be “5G the new thing;” it’ll just be “the internet you use when you’re not on Wi-Fi.”

More than any of the above, the time has passed where wireless CEOs feel they need to sell 5G to the general public (and, of course, their shareholders). It’s not a niche new service anymore; it’s the default option (in the U.S. at least). Basically every new phone sold on their shelves is 5G compatible, and mid-band 5G finally exists on all major carriers in large parts of the US. The next time you walk into a wireless store to buy a new phone or sign up for a new service, you’ll have a very hard time leaving without a 5G device and plan, regardless of whether you really wanted them.

So now we have 5G phones in our hands, 5G networks are here, and… not much has changed. Maybe web pages load a little faster — hardly robot surgery. What gives? The thing is, rolling out 5G is a long ongoing process. The hype made it seem like all the good stuff was just around the corner, but truthfully, it was (and still is) years and years away.

So yes, you may have a 5G icon on your phone, but the most transformative aspects of 5G are supposedly still in the works. That’s a tough message to sell in a flashy keynote, especially when everyone in the room has access to the technology you’re talking about.

The IEEE Techblog in general, and this author in particular, have been pounding the table for years that 5G would be a colossal tech train wreck for these reasons:

1. 3GPP Release 16 URLLC in the RAN spec and performance testing have not been completed. Hence the URLLC in 3GPP Release 15 and ITU M.2150 recommendation do not meet the critically important URLLC ITU M.2410 performance requirements for ultra high reliability or ultra low latency. Here is the latest status of URLLC in the RAN in the 3GPP Release 16 specification as of 6 January 2023:

–Physical Layer Enhancements for NR Ultra-Reliable and Low Latency Communication (URLLC) NR_L1enh_URLLC 1 Rel-16 R1 6/15/2018 12/22/2022 96% complete RP-19158

–UE Conformance Test Aspects – Physical Layer Enhancements for NR URLLC NR_L1enh_URLLC-UEConTest 2 Rel-16 R5 12/14/2020 12/22/2022 90% complete RP-202566 RP-221485

2. There is no implementation standard for 5G SA Core network– only 3GPP reference architecture specs which list alternative implementation schemes, most of which are “cloud native.” That resulted in a lot of telco confusion that delayed the roll out of 5G SA networks such that most 5G deployed today is NSA which uses 4G LTE core network and functions. Dell’Oro Group’s Dave Bolan wrote in a white paper:

The 5G Core is the key to monetizing the 5G SA network bringing MNOs (Mobile Network Operators) into the modern cloud era, allowing the MNO to (1) offer new services quickly with Cloud-Native Network Functions, (2) add Network Slices on demand for mobile private networks, and (3) address latency-sensitive applications with MEC. These new opportunities cannot be addressed by 4G or 5G NSA networks, and the sooner an MNO embraces 5G SA networking, the closer it will be to reaping new revenue streams.

3. ALL of the 3GPP defined 5G functions and features, require 5G SA Core network. Those 5G functions include 5G security, network slicing, and automation/virtualization. MEC also needs a 5G SA Core network to work efficiently with a 5G RAN. There are relatively few 5G SA Core networks deployed and for those that are, there are few of the highly touted 5G functions available, e.g. T-Mobile is a case in point.

4. There is no standard for roaming between 5G networks, especially not when there are different versions of 5G SA core networks- each requiring a different software download for 5G endpoint devices. Hence, 5G is not truly mobile in the sense of portability. 5G is probably best used for FWA or local M2M/IoT communications where there are no roaming requirements.

5. There is no standard for 5G Frequency Arrangements (ITU M.1036 revision 6) which are critically important for all the mmWave frequencies specified at WRC 19 for 5G, but frequency arrangements not yet agreed upon by ITU-R WP 5D.

6. 5G base station and endpoint devicepower consumption is very high, especially for the mmWave frequencies which deliver the fastest 5G speeds.

The White House is working through the NTIA to develop a national spectrum strategy that would cover 5G, 6G and other spectrum users.

According to FierceWireless, National Telecommunications and Information Administration (NTIA) chief Alan Davidson said that work would continue throughout this year. Speaking at last week’s CES conference in Las Vegas, Davidson reminded the audience that the NTIA manages federal spectrum use and serves as the President’s advisor on spectrum policy. That means that the NTIA works together with the FCC to manage spectrum when a federal user is involved. From a practical perspective, the Department of Defense has historically held a lot of valuable spectrum for national security use, making the DoD an incumbent user in many spectrum bands.

The NTIA manages federal spectrum use and serves as the President’s advisor on spectrum policy. (Image Credit: Gerd Altmann from Pixabay)

In 2023 NTIA will be working with federal agency partners to develop a national spectrum strategy, which will provide a long-term plan to meet both commercial and federal spectrum needs.

Officials from the National Oceanic and Atmospheric Administration (NOAA) said they’re taking stock of the agency’s spectrum usage in order to potentially release some for commercial uses, according to SpaceNews. “It is an ongoing challenge. We expect to have to fight for maintenance of spectrum. But at the same time, we realize we’re not going to win every fight,” said Steve Volz, NOAA Satellite and Information Service assistant administrator on January 11th at the American Meteorological Society meeting.

Spectrum for 5G and 6G is a critical national policy topic:

“Continuing to meet increasing consumer demand and expectations, ensure continued growth of the US economy, bridge the digital divide, and facilitate global leadership on next-generation technologies requires sufficient spectrum resources,” wrote the CTIA, the US wireless industry’s main trade association. “Accordingly, it is imperative that the commission continually replenish its pipeline of spectrum allocated for commercial mobile and fixed broadband services.”

“America needs a national strategy to make sure there is enough spectrum to build out 5G networks and not fall behind China,” wrote Mike Rogers, a former Congressional representative from Michigan who authored a report critical of China’s Huawei, in The Hill.

Joel Thayer, of the Digital Progress Institute, agreed. “If we cannot get our act together and follow an all-of-the-above spectrum strategy, we cede the race to 5G and even 6G to China. Full stop,” he wrote in The Hill.

Such arguments strongly echo the “race to 5G” rhetoric that wasubiquitous in policy circles in the early days of 5G.

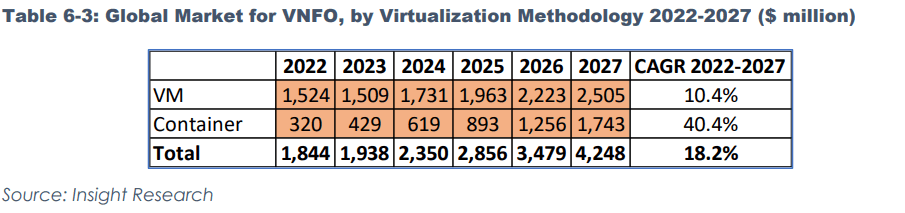

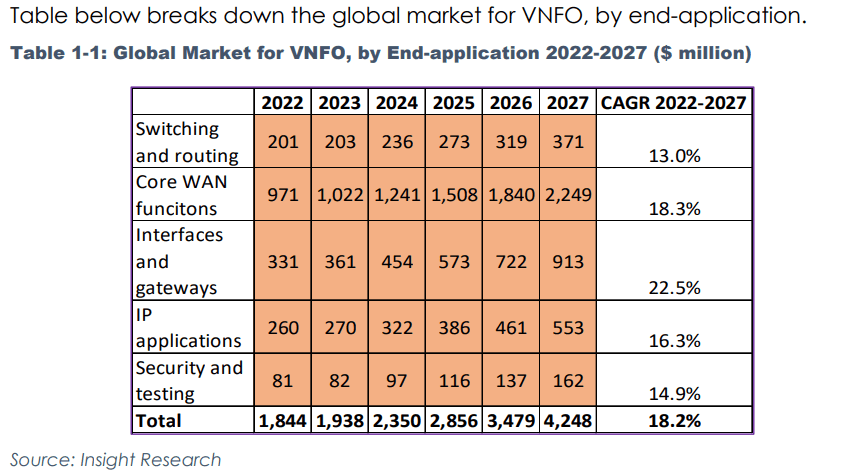

Cloud-native network functions (CNF) promise to change the dynamic of telecommunications network function engineering. The advent of 5G has added impetus to this change. Insight Research is at the cutting edge of CNF market analysis. Here are a few excerpts from our new report on the Virtualized Network Function Orchestrator (VNFO) market

Insight Research considers Virtual Machines (VMs) and Containers to be the major Virtual Network Function Orchestration (VNFO) methodologies. Network functions synthesized using VMs and Containers qualify as Virtual Network Functions (VNFs), in our opinion. That latter term has taken on much broader context since it was first introduced in the context of Network Function Virtualization (NFV) at the OpenFlow World Congress in 2012.

VNFs orchestrated by Containers are sometimes referred to as cloud-native NFs (CNFs). Insight Research has also employed this term as early as 2020. Over time however, we have observed that the usage of CNFs is neither consistent nor uniform.

Most ‘traditional’ Management and Orchestration (MANO) schemes such as ONAP, OSM and all proprietary offerings now support Containers and Kubernetes [1.]. Containers are thus one more mean towards achieving the end-objective of VNFs. As such, Insight Research finds it more appropriate to use VNF as an umbrella term and refer to VM or Container as the specific virtualization methodology.

Note 1. Kubernetes, also known as K8s, is an open-source system for automating deployment, scaling, and management of containerized applications.

The question then arises – where would we slot network functions (NFs) orchestrated by containers encapsulated in VMs? Answer is containers. Similarly, NFs orchestrated by VMs encapsulated in containers are slotted under VMs.

The table below breaks down the VNFO market by virtualization methodology.

We see Containers gaining major market share from VMs such that they are running away with the VNFO market. The advantages of containers over VMs are all well known. Containers are sleeker and when employed with optimal microservice granularity – considerably faster as well.

Additionally, VMs have a head start over containers and have established a solid legacy which will hold good for near to midterm future. However, barriers surrounding container adoption are gradually dissolving with differing momentums across end-applications. The greater the performance differential, the greater is the adoption potential for Containers in end-applications.

Initiatives such Nephio have placed Kubernetes in the center of the VNFO universe. In short, it’s a matter of time before Containers push VMs to be the dominant VNFO virtualization vehicle. However, many question arise.

Here are a few questions for starters:

Is the NFVO the same as service orchestrator?

Is the NFVO the same as SDN controller?

Is Kubernetes an orchestrator?

Since containers and VMs can be embedded inside one another, how do we stamp which virtualization methodology they are using?

If a proprietary MANO uses portions of open source code, should it be considered proprietary?

After picking the brains of numerous experts who were unfailingly patient in unravelling their thinking, Insight Research has been able to arrive at a set of clearcut definitions and assumptions that address the above queries and more.

To buy the report or download an executive summary, please visit: