5G SA/5G Core network

Building and Operating a Cloud Native 5G SA Core Network

By Ajay Thakur with Alan J Weissberger

Abstract:

In this article, we endeavor to clarify some of the critical issues and questions related to implementing a cloud native 5G SA core network and how it differs from the traditional core network composed of hardware devices and software solutions. It’s important to note that NONE of the 3GPP defined 5G features can be realized without a 5G SA core. Those include: Network Automation, Network Function Virtualization, 5G Security, Network Slicing, Multi-Access Edge Computing (MEC), Policy Control, Network Data Analytics, etc.

Communication Service Providers (CSPs) will need to do things differently (than 4G) in order to implement and use a 5G cloud native SA core. Various cloud native 5G SA core aspects include network planning, deployment, software upgrades, network monitoring, hardware and platform upgrades.

These will be examined and contrasted with traditional implementations, such as the 4G Evolved Packet Core (EPC).

Introduction:

3GPP introduced 5G SA core network architecture in release 15. Since then numerous new features (work items) have been introduced to specifications. 3GPP’s 5G SA’s specifications use virtualization and cloud native principles as the foundation. A few key 3GPP Technical Specifications (TSs) for 5G system are the following:

- TS 22.261, “Service requirements for the 5G system”.

- TS 23.501, “System architecture for the 5G System (5GS)”

- TS 23.502 “Procedures for the 5G System (5GS)

- TS 32.240 “Charging management; Charging architecture and principles”.

- TS 24.501 “Non-Access-Stratum (NAS) protocol for 5G System (5GS); Stage 3”

- TS 38.300 “NR; NR and NG-RAN Overall description; Stage-2”

- TS 23.527 “5G System; Restoration procedures Stage-2”

5G SA tries to resolve the challenges faced by network operators in the EPC deployments and how those challenges can be mitigated with new design.

Several important changes in the 5G SA core are support for a Service Based Architecture and Cloud Native implementation of 5G SA core. That will enable new 5G features and functions like Network Slicing, 5G Security, and MEC, among others.

To reap the benefits of Cloud Native SA, CSPs are required to adapt to new cloud native principles of network deployment, operation and monitoring. We shall examine various aspects of Life Cycle Management of 5G SA software and also ask some open ended questions on each aspect.

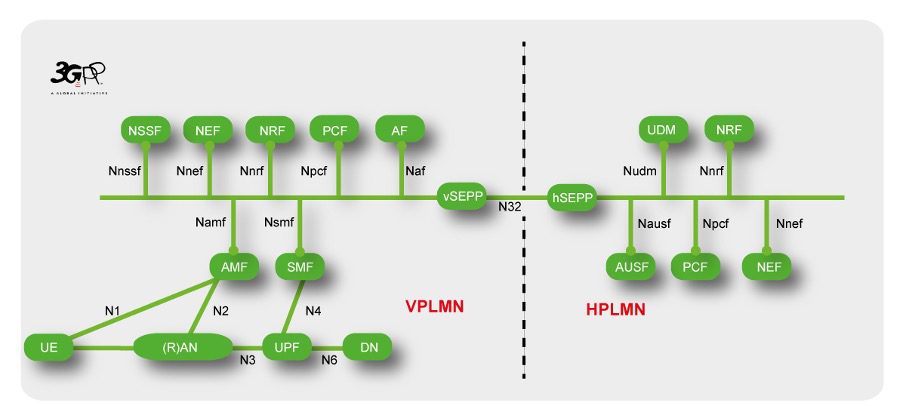

SBA architecture Diagram with multiple Interfaces:

- The Network diagram above shows the SBI interfaces in case of roaming. Each of the individual NF may be composed of one more micro-services. Each NF may come from different vendor. Since these NFs are available in containerized format, they may or may not share the same container orchestration platform.

Network Dimensioning:

- 5G SA solves the network expansion problem since the network can be scaled up/down by adding/removing commercial off the shelf hardware.

- Once we have all the NFs software releases available, operators can gather the compute, memory & network requirements for deployment.

- Operators would rely on auto scaling functionality provided by the 5G NF vendors to avoid over provisioning at the start. This is relatively much simpler compared to adding dedicated hardware for NF in case of EPC.

Deployment Options Selection/Planning

- Operators need to decide the type of deployment for the network like the 5G SA deployment on public cloud or on private cloud.

- Along with Public vs Private cloud decisions, the Operator also needs to decide on a Container orchestration engine. Container orchestration can be managed service or operator managed service. Popular container orchestration engine is Kubernetes (K8s).

- Next step would be to finalize or select one of the CI/CD tools which works for all the vendors and integrate that with the container orchestration platform.

- Also placement of the NFs needs to be decided, e.g. User Plane Function (UPF) could be on-prem close to RAN. It’s possible that the operator may place some of the RAN virtualized components in the cloud.

- These all are important decisions to be made before getting into the real deployment of the software.

- Some of the aspects here are due to Cloud Native 5G SA and were not applicable for EPC.

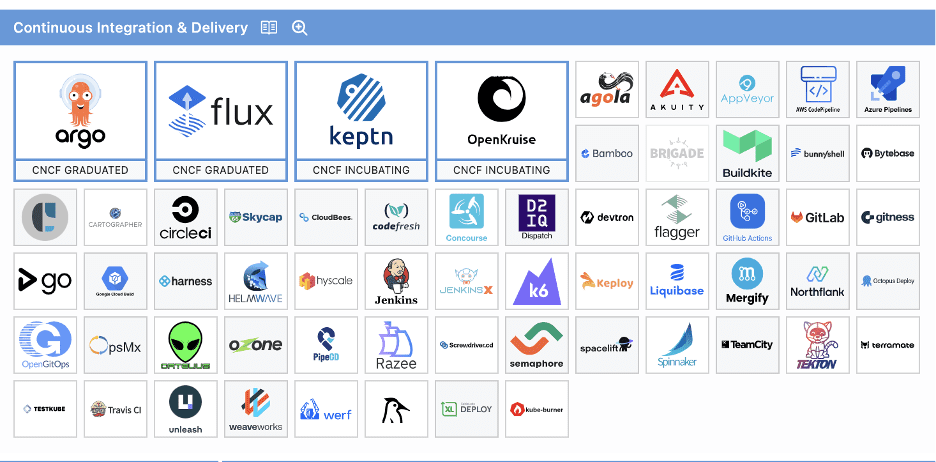

CI/CD:

- CI/CD landscape (https://landscape.cncf.io/) from CNCF shown in below Figure

- It can be seen from the CNCF project that there are many projects which are available for CI/CD

- Irrespective of Public or Private cloud, operators need to follow cloud native CI/CD principles for deploying the Core Network in the Cloud environment. CI/CD involves taking the software release from the vendor and running it against existing network functions and carrying out some minimum tests and once operator is satisfied with evaluation of the release then rollout the release in the network.

- Operators can decide to have a separate staging environments where new releases can soak for a certain period of time while few subscribers use the new release.

- CI/CD gives the option of rolling back the release if the operator is not happy with the performance of the new release.

- Now the challenge here would be, will the operator have single CI/CD tools used for deploying all the vendors’ solution OR would the operator use its own CI/CD tooling and integrate NFs from vendor it in its own environment. This is the decision the operator needs to take.

- Having Automated CI/CD infrastructure which takes the software releases from the vendors and passes it through multiple environments and all the way to the production environment is key.

- Without having an appropriate CI/CD environment it would be very difficult to manage all micro-services and their deployments.

- Public Cloud may come with inbuilt CI/CD solutions and would be easy for operators to start with.

- AWS offers multiple services around CI/CD and those are listed here – https://docs.aws.amazon.com/whitepapers/latest/cicd_for_5g_networks_on_aws/cicd-on-aws.html

- Azure offering can be found here https://learn.microsoft.com/en-us/azure/devops/pipelines/apps/cd/azure/cicd-data-overview?view=azure-devops

- Google Cloud CI/CD services can be found here – https://cloud.google.com/solutions/continuous-integration

Software Upgrade:

- Cloud Native 5G SA allows operator to upgrade some of the components easily instead of complete 5G Core update in one go. CI/CD framework would help in the software upgrades with minimal human intervention.

- Note that with Cloud Native principles the operator would get multiple patch/minor releases and may be some major releases throughout the life cycle of the software. So the traditional approach of pulling down complete hardware & upgrading it with new software is not required for microservice based solutions. But this really works as long as all microservices are truly built stateless and supports live upgrade.

- As an operator, it would be required to know the impact of each upgrade package and prepare for rollback in case something goes wrong during the upgrade cycle.

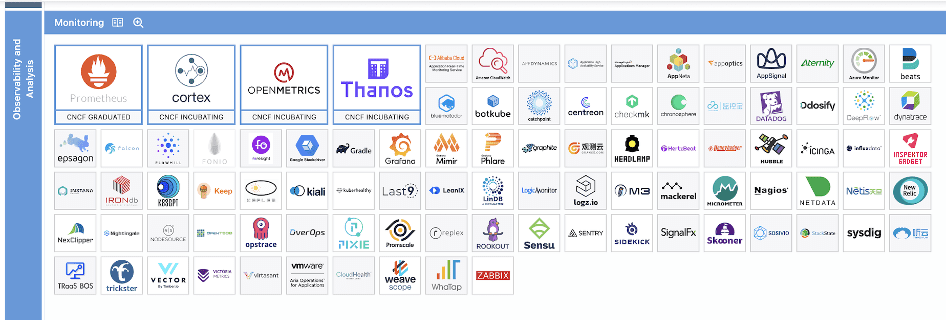

Network Monitoring:

- Traditionally, operators developed their own Network Monitoring solutions to monitor the health of EPC since there was no standard mechanism to get the metrics, statistics from the NFs,

- 5G SA follows Cloud Native principles; it is easy to get the logs, statistics, alerts, alarms from all microservices in a consistent manner. There are common tooling used by most of the cloud native applications and CNCF has multiple projects in these categories.

- CNCF supported Monitoring projects are shown below figure

-

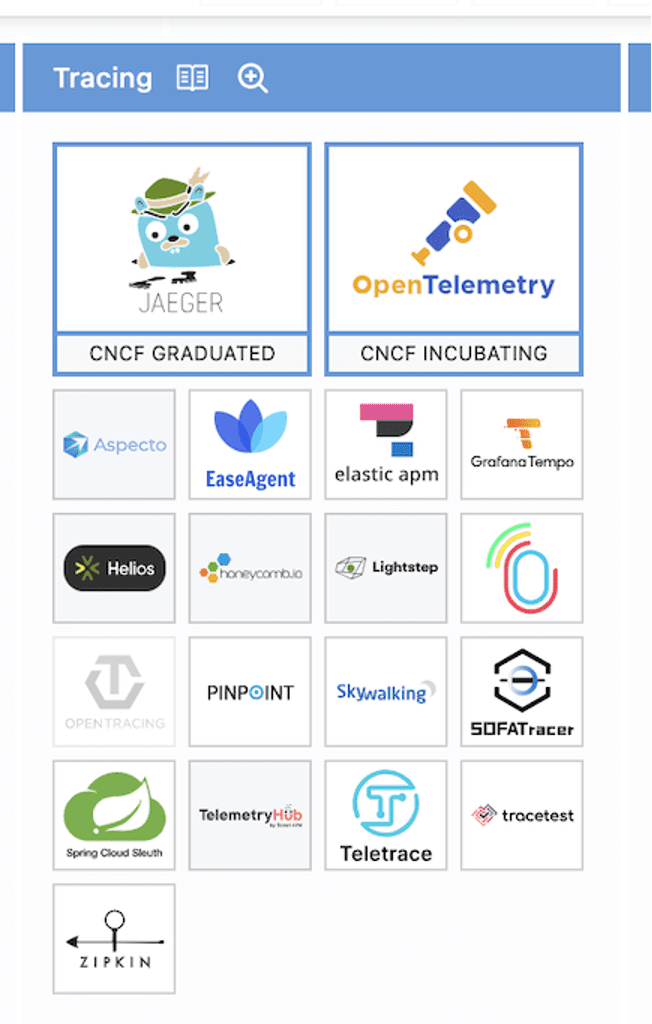

- Tracing is important aspect to find out the bottleneck in the performance.

- Logging has been a traditional approach for debugging network issues. Below are the projects offered by CNCF in the logging area

- Public Cloud providers can extend the monitoring easily by generating Texts or email alerts as per CSPs needs.

- Operators can define their policies to retain the network performance monitoring output for a long time and can take backup of this easily through use of Public Cloud Providers data backup services.

- In the case of EPC these mechanisms were product dependent.

- Challenge in case of 5G SA would be each NF vendor may end up in using different tool and operators would have some challenges to converge all NF vendors to the common tooling.

Hardware & platform upgrade:

- In the traditional approach, providing hardware with updated operating systems and platforms was the responsibility of the equipment vendor. Now this responsibility has gone into either operator’s hand or sometimes in Public Cloud Provider’s hand. It depends on if the 5G SA is deployed on on-prem or on public cloud. Operators need to carefully plan for these upgrades without causing any downtime and of course follow the rolling upgrade patterns to avoid updating multiple entities at a time.

- If managed container orchestration is used, then these upgrades are seamlessly handled by Public Cloud Providers.

Vendor Lock In:

- In the case of EPC, vendor lock in was specific to NF & Radio Vendors. The 3GPP EPC specification allows the operators to swap NFs from one vendor with another and as long as NF supports the required Services. Point to note that this is less costly replacement compared to replacing one vendor with another vendor when NF had associated hardware.

- But with cloud native SA there is a chance that the operator may end up in building the tooling (CI/CD, monitoring etc.) over the period of time and this may lead to cloud provider lock in.

Conclusions:

The 5G SA core network provides a lot of flexibility and automation via cloud native deployments. However, the 3GPP 5G core specs contain a lot of implementation options, which network operators and their vendors must select to properly deploy a 5G core network. Making those decisions will likely require solid experience with operating applications on a cloud native platform. And that may be a reason that 5G SA core network rollouts have been so slow.

In the U.S. AT&T and Verizon have taken a very cautious approach to deploying their long ago promised 5G SA core networks. During the Brooklyn 6G Summit in November 2023, Chris Sambar, EVP for technology at AT&T said, ““I would say we are not moving as quickly as some of the other operators on the 5G standalone core, but we see the use cases that are coming, we understand when they’re coming, so we’re being very purposeful about getting there when we need to get there.” That’s despite AT&T outsourcing its 5G SA core network deployment to Microsoft Azure in June 2021. Yet Microsoft is the world’s second biggest cloud services provider with tons of experience running cloud native applications.

Summing up, Dave Bolan, Research Director at Dell’Oro Group wrote, “The buildout of 5G SA networks is going slower than anticipated which is restraining growth in the marketplace. To date, we count fifty 5G SA eMBB (enhanced Mobile BroadBand) networks that have been commercially deployed worldwide by Mobile Network Operators (MNOs). We counted 18 new 5G SA networks in 2022, but only 12 were launched in 2023. On a positive note, we believe a lot of work has been done in the background, preparing for 5G SA launches by Mobile Network Operators (MNOs) and we expect 2024 to have more launches than 2022.”

Ajay Lotan Thakur, Cloud Software Architect at Intel and IEEE Techblog Editorial Team member

References:

Global 5G Market Snapshot; Dell’Oro and GSA Updates on 5G SA networks and devices

Ericsson Mobility Report touts “5G SA opportunities”

Analysys Mason: 40 operational 5G SA networks worldwide; Sub-Sahara Africa dominates new launches

Samsung and VMware Collaborate to Advance 5G SA Core & Telco Cloud

5G SA networks (real 5G) remain conspicuous by their absence

GSM 5G-Market Snapshot Highlights – July 2023 (includes 5G SA status)

Finland’s Elisa, Ericsson and Qualcomm test uplink carrier aggregation on 5G SA network

With Ericsson and Qualcomm doing the “heavy lifting,” Finland network operator Elisa conducted a live test of uplink carrier aggregation (CA) on its commercial 5G standalone (SA) network. Elisa operates commercial 5G SA networks, starting with its home market of Finland and following it up last year by deploying it in Estonia.

The three partners achieved an upload speed of 230 Mbps in a live 5G network using Uplink Carrier Aggregation. For this test, a 25MHz 2.6 GHz FDD (frequency division duplex) band was combined with a 100MHz 3.5 GHz TDD (time division duplex) band running on a mobile test device powered by Snapdragon® X75 5G Modem-RF System.

Ericsson’s Uplink Carrier Aggregation software combines mid-band FDD and mid-band TDD within the frequency range 1 (FR1), boosting speeds to enable uplink-heavy applications such as live streaming, broadcasts, cloud gaming, extended reality, and video-based use cases.

Uplink-heavy consumer applications on the rise:

According to Ericsson’s most recent Mobility Report, uplink accounted for a modest 8% of total traffic on a sample of four mobile networks analyzed. The applications that generated the largest volume of uplink traffic were personal cloud storage services, followed by comms services and video.

While 8% doesn’t seem like much, Ericsson emphasised that uplink volume is highly context dependent. For instance, there is likely to be more of it at a live event, like a concert or a sporting event, where users enthusiastically film and then share as much action as possible.

A growing amount of data traffic generated today is in the uplink, highlighting the need for new network capabilities to boost uplink speed and capacity and deliver seamless 5G user experience. For instance, concertgoers are recording and streaming videos live on their social media accounts. With fast uplink speeds, they can share their most exciting moments in real-time with friends and family without worrying about lags, congestion, or poor network quality.

In addition to Elisa, Vodafone has also been testing out uplink CA recently, as have Dish, BT and Telefónica.

………………………………………………………………………………………………………………….

Quotes:

Mårten Lerner, Head of Product Area Networks, Ericsson, says: “This latest technology milestone with our partners Elisa and Qualcomm Technologies unlocks high upload speeds in commercial 5G Standalone networks. With this game-changing software capability, we are enabling unparalleled user experience for applications such as live streaming, video conferencing, augmented reality/virtual reality and cloud gaming.”

Sami Rajamäki, Vice President, Network Services, Elisa, says: “We continue as a pioneer of 5G in Finland and develop our network services with our customers’ future needs in mind. The use of augmented reality and development towards metaverse will increase the demand for fast uplink connections. Therefore the top speeds achieved together with Ericsson and Qualcomm are an important step in the development of 5G Standalone network.”

Dino Flore, Vice President, Technology at Qualcomm Europe, Inc. says: “The uplink speed achieved with Elisa and Ericsson is a testament to the breakthrough performance of the Snapdragon X75 5G Modem-RF System. We are excited to see the innovative use cases Elisa can unlock for customers with their 5G Standalone network.”

Ericsson has a robust portfolio of software features that provide a boost in the uplink, and the feature deployed in this demo with Elisa and Qualcomm – FR1 Uplink Carrier Aggregation – became commercially available in the fourth quarter of 2023.

Visit the Ericsson booth in Hall 2 at MWC 2024 in Barcelona to see how a superior uplink performance is being enabled for use cases such as live streaming.

References:

T-Mobile US, Ericsson, and Qualcomm test 5G carrier aggregation with 6 component carriers

Dish Wireless with Qualcomm Technologies and Samsung test simultaneous 5G 2x uplink and 4x downlink carrier aggregation

Ericsson and MediaTek set new 5G uplink speed record using Uplink Carrier Aggregation

BT tests 4CC Carrier Aggregation over a standalone 5G network using Nokia equipment

Global 5G Market Snapshot; Dell’Oro and GSA Updates on 5G SA networks and devices

According to market research firm Omdia, there were 1.8 billion global 5G subscribers at the end of 2023 with 7.9 billion forecast by 2028. This growth trajectory, while substantial, is subject to various influencing factors such as infrastructure development, spectrum availability, device availability, and consumer demand. Kristin Paulin, Principal Analyst at Omdia, has a cautiously optimistic outlook for 5G. She emphasizes that innovation and cooperation are key to unlocking the full potential of 5G and its transformative impact.

Globally, the number of deployed 5G networks is now comparable to 4G LTE deployments. There are currently 296 commercial 5G networks worldwide, a number expected to grow to 438 by 2025.

In North America, 5G deployment was at 176 million connections as of the third quarter of 2023, a 14% increase from the previous quarter. This represents a 26% market share and a 46% penetration rate. However, there were only two U.S. 5G SA network providers – T-Mobile US and Dish Wireless– as of the end of 2023.

in contrast, Latin America and the Caribbean are still in the early stages of 5G adoption. However, the region shows promise with an expected quadrupling of 5G connections in 2023, reaching 46 million. By 2028, it is anticipated that the region will have 492 million 5G connections.

Jose Otero, Vice President of Caribbean and Latin America for 5G Americas, acknowledges the significance of 4G LTE and 5G as vital mobile communication technologies in Latin America. He anticipates more robust opportunities for 5G in the region, driven by upcoming spectrum auctions and wider access to 5G devices in 2024.

“The global 5G landscape shows positive momentum as innovation and collaboration continue to be the mainstays for long term progress.” said Chris Pearson, President of 5G Americas. “With the World Radio Conference wrapping up, it is important that international co-operation and efforts continue to ensure that spectrum and technology standards continue to propel this growth.”

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

According to a recent report by Dell’Oro Group, the Mobile Core Network (MCN) market growth rate has been reduced to less than a 1% CAGR (2023-2028).

“This is the fourth consecutive time we reduced the growth rate of the MCN market as the build-out of 5G Standalone (5G SA) networks continues to wane compared to 5G Non-standalone (5G NSA) networks,” said Dave Bolan, Research Director at Dell’Oro Group. “The buildout of 5G SA networks is going slower than anticipated which is restraining growth in the marketplace. To date, we count fifty 5G SA eMBB (enhanced Mobile BroadBand) networks that have been commercially deployed worldwide by Mobile Network Operators (MNOs). We counted 18 new 5G SA networks in 2022, but only 12 were launched in 2023. On a positive note, we believe a lot of work has been done in the background, preparing for 5G SA launches by Mobile Network Operators (MNOs) and we expect 2024 to have more launches than 2022.”

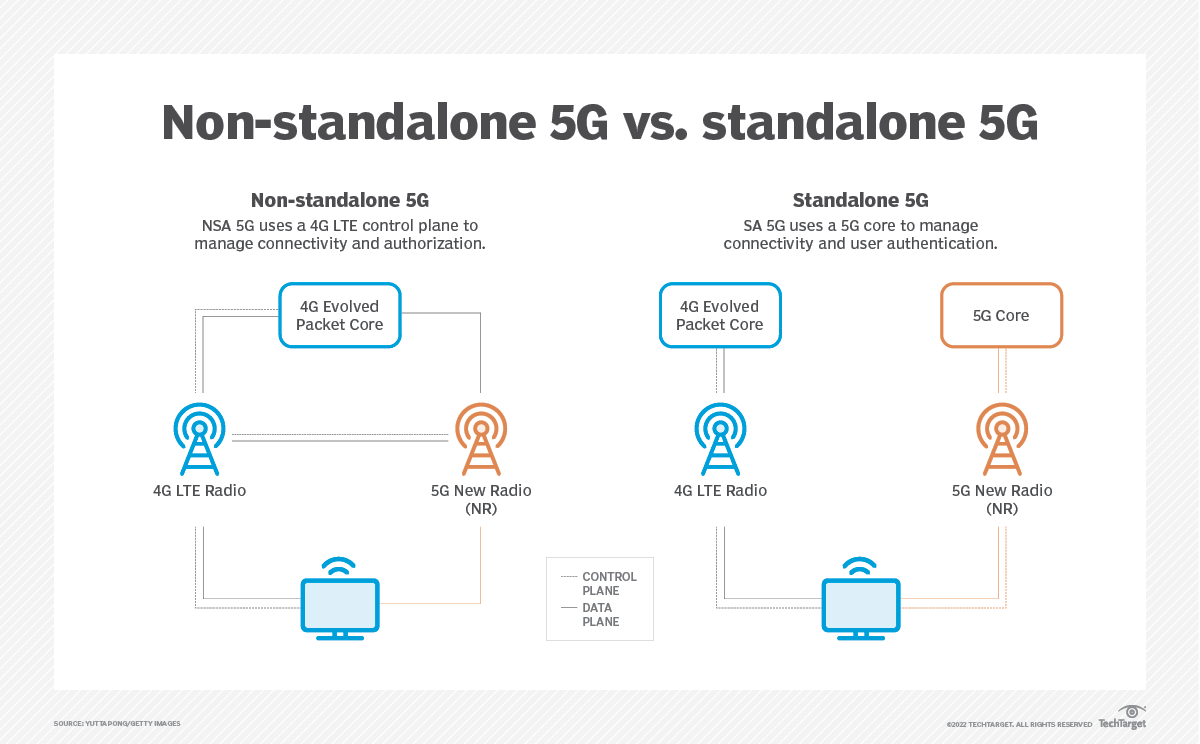

Note 1. Importantly, a 5G SA core network is required to realize 3GPP defined 5G features, like 5G Security, Network Slicing (3GPP’s technical specification (TS) 23.501 defines 5G system architecture with slicing included. TS 22.261 specifies the provisioning of network slices, association of devices to slices, and performance isolation during normal and elastic slice operation).

The 5G SA core network relies on a “Service-Based Architecture” (SBA) framework, where the architecture elements are defined in terms of “Network Functions” (NFs) rather than by “traditional” Network Entities.

5G SA core networks require “cloud-native” hardware and software that has a service-based architecture and decentralized functions. A “cloud-native” 5G core allows for flexible and efficient operation, as well as the effective adoption of new services.

………………………………………………………………………………………………………..

According to Verified Market Research, when the full 5G SA feature set is supported, enterprises can realize the following benefits:

- Further improvements to speed and reach, beyond what 5G NSA brings.

- Support for higher-density deployments of devices.

- Support for low-latency and real-time use cases.

- Support for enhanced enterprise site connectivity via network slicing.

- Better security than 5G NSA (which uses 4G LTE security methods and procedures).

- Simplification of the RAN and core compared to 5G NSA since 5G SA supports only 5G and leaves 4G and older standards behind — and even though the 5G SA core alone is more complex than a pure 4G core alone.

GSA claims that more than 121 network operators in 55 countries and territories have invested in public 5G standalone (SA) networks (but they don’t disclose how many of those have been commercially deployed (for example, AT&T and Verizon have been talking up 5G SA for years, but have yet to deploy it!). We trust Dell’Oro’s number of 5G SA eMBB networks deployed.

Findings from the latest GSA update on the 5G SA ecosystem/devices [2.] include:

- There are 2,130 announced devices with claimed support for 5G SA, up 35.7% from 1,569 at the end of 2022.

- Devices with support for 5G SA account for 90.3% of all 5G devices, as of the end of 2023, up from 35.6% in December 2019.

- 93 modems or mobile processors/platform chipsets state support for 5G SA, 90 of which are understood to be commercially available.

Note 2. It’s crucially important to realize that since all 5G SA core networks are different, a 5G SA device that works on one carrier’s network won’t work on any other without a new 5G SA download.

By the end of December 2023, GSA had identified:

• 28 announced form factors • 261 manufacturers with announced available or forthcoming 5G devices

• 2,358 announced devices, including regional variants, but excluding operator-branded devices that are essentially rebadged versions of other phones. Of these, at least 1,964 are understood to be commercially available:

• 1,255 phones, up 34 from November 2023. At least 1,168 of these are now commercially available, up 56 from November 2023

• 308 fixed wireless access customer-premises equipment (CPE) devices for indoor and outdoor uses, at least 209 of which are now commercially available

• 243 modules • 64 tablets • 33 laptops or notebooks • 77 battery-operated hot spots

• 179 industrial or enterprise routers, gateways or modems

• 13 in-vehicle routers, modems or hot spots

• 29 USB terminals, dongles or modems

• 168 other devices, including drones, head-mounted displays, robots, TVs, cameras, femtocells/small cells, repeaters, vehicle on-board units, keypads, a snap-on dongle/adapter, a switch, a vending machine and an encoder

• 1,098 announced devices with declared support for standalone 5G in sub-6 GHz bands, 904 of which are commercially available.

According to Verified Market Research, the market drivers for the 5G Technology Market can be influenced by various factors. These may include:

- Enhanced Data Speed and Capacity: In comparison to its predecessors (4G/LTE), 5G technology offers far faster data rates and more network capacity. Supporting the increasing need for high-bandwidth applications like virtual reality (VR), augmented reality (AR), and Internet of Things (IoT) devices is imperative.

- Low Latency: The goal of 5G networks is to offer low-latency communication, which shortens the time it takes to send and receive data. This is critical for real-time interactive applications like industrial automation, remote surgery, and driverless cars.

- Growing Need for IoT Devices: One of the main factors driving 5G adoption is the spread of IoT devices across a number of industries, including manufacturing, healthcare, smart cities, and agriculture. 5G is ideally suited for Internet of Things applications due to its low latency and capacity to connect a large number of devices concurrently.

- Rise of Edge Computing: The growth of edge computing is intimately related to 5G networks. Edge computing improves speed and lowers latency by bringing computing resources closer to end users and devices; this makes it a crucial enabler for applications like driverless cars and smart cities.

- Industry 4.0 and Smart Manufacturing: By facilitating effective and dependable communication in smart factories, 5G is anticipated to play a significant role in the fourth industrial revolution, or Industry 4.0. It makes it easier to incorporate technology like automation, robotics, and artificial intelligence into production processes.

- Telecommunications Infrastructure Upgrade: on order to roll out 5G networks, telecommunications service providers are actively spending on infrastructure upgrades. To improve capacity and coverage, new base stations and tiny cells must be installed.

- Government Initiatives and Support: Through legislative frameworks, financial aid, and other means, numerous governments across the globe are actively promoting the rollout of 5G technology. In the global digital landscape, these programmes seek to promote innovation, economic growth, and competitiveness.

- Competitive Environment and Industry Cooperation: Businesses are investing in 5G technology to obtain a competitive advantage due to the highly competitive nature of the telecommunications sector. Furthermore, partnerships between IT firms, telecom service providers, and other relevant parties are quickening the creation and implementation of 5G networks.

Several factors can act as restraints or challenges for the 5G Technology Market. These may include:

- Infrastructure Costs: Given that a large-scale deployment of base stations and small cells is necessary to support 5G, telecom operators may be discouraged by the substantial upfront expenditure necessary for creating and upgrading infrastructure.

- Spectrum Allocation and Availability: The effective operation of 5G networks depends on the allocation and availability of appropriate spectrum bands. Regulatory and geopolitical obstacles can make it difficult to get the necessary spectrum, which can hinder the deployment of 5G services.

- Security Concerns: There are worries about possible cybersecurity attacks due to the vast number of devices connected to 5G networks and the increased connection. Building confidence and promoting wider adoption require overcoming these issues and guaranteeing the security of network infrastructure.

- Interoperability Problems: There are interoperability problems since different generations of cellular technologies coexist. A seamless transition and the prevention of service interruptions depend on the seamless integration of various technologies.

- Regulatory Obstacles: The implementation of 5G networks faces a number of regulatory obstacles, such as spectrum auctions, licence requirements, and local law compliance. Uncertainties surrounding regulations may cause hold-ups and impede the rapid deployment of 5G services.

- Public Health and Safety Concerns: The general public’s reception of 5G networks may be impacted by worries about the possible health impacts of increasing exposure to radiofrequency radiation. Building public trust requires resolving these issues and maintaining clear lines of communication.

- Absence of Killer Applications: The deployment of 5G may be slowed back by the absence of compelling and widely applicable use cases. Creating cutting-edge, impactful apps that take advantage of 5G’s special features is essential to increasing demand.

- Global Economic uncertainty: Businesses’ and operators’ willingness to invest in the rollout of 5G technology can be impacted by economic downturns and uncertainty. Delays in infrastructure upgrades could result from financial considerations and budgetary restrictions.

Charts courtesy of Verified Market Research

References:

5G Continues Robust Momentum Growth and Drives Demand for More Wireless Spectrum

https://www.3gpp.org/technologies/5g-system-overview

https://www.techtarget.com/searchnetworking/definition/5G-standalone-5G-SA

SK Telecom and Thales Trial Post-quantum Cryptography to Enhance Users’ Protection on 5G SA Network

Korean telco SK Telecom and digital security firm Thales have tested quantum-resistant cryptography based on a 5G standalone (5G SA) network. The trial is focused on encrypting and decrypting identity data on a 5G network to protect user privacy from future quantum threats. It was performed using Thales 5G Post Quantum Cryptography (PQC) SIM cards and a trial 5G standalone network environment from SKT. The test involved cryptographic algorithms designed to resist attacks from quantum computers, as well as ‘classical’ computers.

The end user identity on the 5G SA network is concealed and secured on the device side via the 5G SIM card. The security mechanisms involve cryptographic algorithms designed to resist attacks from future quantum computers, providing a level of security that is considered robust in the post-quantum era.

Photo Credit: rawpixel

The U.S. National Institute of Standards and Technology (NIST) has been leading an initiative to standardize post-quantum cryptographic algorithms, and SKT and Thales have used the Crystals-Kyber one for this successful real condition trial. These post-quantum secure algorithms are being developed to withstand attacks from both classical and quantum computers.

“This collaboration between SKT and Thales highlights our commitment to staying ahead of the curve in terms of cybersecurity and ensuring the safety of our customers’ data. PQC provides enhanced security through the use of cryptographic algorithms that are thought to be secure against quantum computer attacks. Going forward, we will combine PQC SIM with our additional Quantum expertise to achieve end-to-end quantum-safe communications,” said Yu Takki, Vice President and Head of Infra Technology Office of SKT.

“As quantum computers have the potential to break certain existing cryptographic algorithms, there is an emerging need to transition to cryptographic algorithms believed to be secure against quantum attacks. For 5G networks, Thales started to invest on cryptographic algorithms that are quantum-resistant to enhance continued communications security and privacy for users,” said Eva Rudin, SVP Mobile Connectivity & Solutions at Thales.

As quantum computing gets more reliable and presumably starts getting used more widely in the future, this type of security is going to become increasingly important. Nokia recently announced it had completed a proof of concept trial alongside Greek research consortium HellasQCI, demonstrating what it calls quantum-safe connectivity infrastructure.

………………………………………………………………………………………………………………………………………………………………..

Separately, SK Broadband, an internet and paid TV service affiliate of SK Telecom, launched additional personalized internet protocol television (IPTV) services utilizing AI technology to enhance its competitiveness in the country’s paid TV market, the company said Wednesday.

About SK Telecom:

SK Telecom has been leading the growth of the mobile industry since 1984. Now, it is taking customer experience to new heights by extending beyond connectivity. By placing AI at the core of its business, SK Telecom is rapidly transforming into an AI company. It is focusing on driving innovations in areas of telecommunications, media, AI, metaverse, cloud and connected intelligence to deliver greater value for both individuals and enterprises.

For more information, please contact [email protected] or visit SKT’s LinkedIn page www.linkedin.com/company/sk-telecom.

About Thales:

Thales (Euronext Paris: HO) is a global leader in advanced technologies within three domains: Defence & Security, Aeronautics & Space, and Digital Identity & Security. It develops products and solutions that help make the world safer, greener and more inclusive.

References:

https://www.newswire.co.kr/newsRead.php?no=981374

https://www.telecoms.com/5g-6g/sk-telecom-and-thales-trial-quantum-resistant-cryptography-for-5g-sa

https://www.koreatimes.co.kr/www/tech/2023/12/133_365470.html

SKT Develops Technology for Integration of Heterogeneous Quantum Cryptography Communication Networks

SK Telecom and Deutsche Telekom to Jointly Develop Telco-specific Large Language Models (LLMs)

Deutsche Telekom Network Day: Fiber, Mobile Network, Open RAN and 5G SA Launch in 2024

2023 Deutsche Telekom (DT) Highlights:

- Fiber offensive: more than 2.5 million new fiber connections made possible in 2023, reaching a total of more than ten million fiber households in 2024

- 5G front-runner: 5G population coverage of 96%, 5G Standalone also for private customers in 2024

- State-of-the-art technologies: Artificial intelligence supports fiber and mobile rollout

- EURO 2024: Deutsche Telekom connects all stadiums, fan zones & team quarters, data gift for all mobile customers

………………………………………………………………………………………………………………………………………

Deutsche Telekom announced that it has successfully enabled more than 2.5 million new fiber connections this year, thereby realizing its fiber plant expansion target. The company invested EUR 2.5 billion in fiber expansion, expanding coverage in almost 3,500 towns and municipalities. According to the announcement, the company projects a total investment of EUR 30 billion in the fiber optic rollout by 2030.

Its Fiber-to-the-home (FTTH) network is set to reach eight million households by the end of the year, with plans to extend this to ten million fiber optic connections by 2024.

………………………………………………………………………………………………………………………………………..

In mobile, Deutsche Telekom currently provides 5G coverage to 96 percent of the population, serving 80 million people through a network of over 80,000 5G antennas, including 10,000 in the 3.5 GHz band spread across more than 800 cities and municipalities. The network delivers download speeds of up to 1 Gbps.

The company aims to achieve 99 percent 5G coverage for the German population by 2025 and plans to launch 5G Standalone (SA) core network for private customers in 2024. DT indicates that 10,000 antennas are compatible with 5G SA in the 3.6 GHz band, covering more than 800 cities and municipalities. This is up from 9,700 antennas in August 2023.

Deutsche Telekom’s business customers are already using 5G SA technology with functions such as network slicing. For example, for live TV transmission of media or in 5G campus networks for industry and research. “In the coming year, 5G SA should then offer all customers real added value,” DT said.

Meanwhile, rival operators Telefónica Deutschland (O2 Germany) and Vodafone Germany already offer standalone 5G services.

…………………………………………………………………………………………………………………………

DT began the deployment of its open radio access network (O-RAN) in Germany in December, in collaboration with Nokia and Fujitsu. The first O-RAN commercial deployment will be in Neubrandenburg. Nokia and Fujitsu are supplying the necessary technology components.

“Open RAN increases the choice of manufacturers and therefore our flexibility. The open access network enables more automation. And makes our networks even more resilient. This benefits the people that our mobile network connects,” says Claudia Nemat.

The German telco expects to have 3,000 O-RAN compatible antennas by the end of 2026.

…………………………………………………………………………………………………………………………

Deutsche Telekom also says it’s using Artificial Intelligence (AI) in network expansion and mobile communications. AI aids in analyzing and evaluating cell usage and capacity utilization, with the ongoing development of a large language model for telco-specific applications in collaboration with SK Telekom. Additionally, AI contributes to enhanced network security through automated pattern recognition, according to the company.

References:

https://www.telekom.com/en/media/media-information/archive/telekom-network-day-2023-1055364

https://www.fiercewireless.com/wireless/deutsche-telekom-plans-5g-standalone-launch-2024

T-Mobile combines Millimeter Wave spectrum with its 5G Standalone (SA) core network

T-Mobile, with the help of with Ericsson and Qualcomm Technologies, Inc., has tested millimeter wave (mmWave) on its production 5G SA network (note that mmWave identifies higher frequencies used on a 5G RAN, while 5G SA refers to a true 5G core network). The Un-carrier aggregated eight channels of mmWave spectrum to reach download speeds topping 4.3 Gbps without relying on low-band or mid-band spectrum to anchor the connection. T-Mobile also aggregated four channels of mmWave spectrum on the uplink, reaching speeds above 420 Mbps.

In the latest revision of ITU-R M.1036- Frequency Arrangements for IMT-the following mmWave bands were approved:

-Frequency arrangements in the band 24.25-27.5 GHz

-Frequency arrangements in the band 45.5-47 GHz

-Frequency arrangements in the band 47.2-48.2 GHz

-Frequency arrangements in the band 66-71 GHz

In the U.S., Verizon has historically been the carrier promoting 5G mmWave, which they dubbed “5G Ultra Wideband.” The telco claims they’ve achieved 1.26 Gbps upload speed using 5G Ultra Wideband. With uploading data becoming increasingly important for video chats, uploading large files or live streaming video. “We have achieved remarkable speed in downloading using various combinations of spectrum in our world-class spectrum portfolio,” said Adam Koeppe, Senior Vice President of Technology Planning at Verizon. “This new achievement indicates how much additional performance we can unleash for our customers on the uplink as we aggregate different combinations of spectrum.”

T-Mobile took the opposite path, focusing on mid and low-band spectrum for its 5G network…until now. 5G mmWave can deliver very fast speeds because it offers massive capacity. But the signal doesn’t travel very well through obstacles, making it less ideal for mobile phone users who aren’t sitting still. That’s why T-Mobile has implemented a multi-band spectrum strategy using low-band to blanket the country and mid-band and high-band (Ultra Capacity) to deliver insanely fast speeds to nearly everyone. Now the Un-carrier is testing 5G mmWave on 5G SA for crowded areas like stadiums and, potentially, for fixed wireless service.

“We’ve been industry leaders – rolling out the first, largest and fastest 5G standalone network across the country – and now we’re continuing to push the boundaries of wireless technology,” said Ulf Ewaldsson, President of Technology at T-Mobile. “We’ve always said we’ll use millimeter wave where it makes sense, and this test allows us to see how the spectrum can be put to use in different situations like crowded venues or to power things like fixed-wireless access when combined with 5G standalone.”

T-Mobile is the U.S. leader in 5G [1.] delivering the largest, fastest and most awarded 5G network in the country. The Un-carrier’s 5G network covers more than 330 million people across two million square miles — more than AT&T and Verizon combined. 300 million people nationwide are covered by T-Mobile’s super-fast Ultra Capacity 5G with over 2x more square miles of coverage than similar mid-band 5G offerings from the Un-carrier’s closest competitors. According to Ookla’s quarterly speed test reports, T-Mobile’s 5G network has consistently outperformed AT&T’s and Verizon’s when it comes to median download speed.

Note 1. AT&T is the leading provider of mobile services in the U.S. with 229.1 subscribers as of Q2 2023, followed by: Verizon: 143.3 million (Q2 2023),,T-Mobile US: 117.9 million (Q3 2023), Dish Wireless: 7.5 million (Q3 2023), and uscellular: 4.6 million (Q3 2023).

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

T-Mobile also offers wireless solutions to connect homes and businesses. 5G Home Internet (FWA) is available to over 50 million homes today, plus Small Business Internet and Business Internet is available across the country. This means millions of homes and businesses can finally ditch traditional ISPs for fast, reliable and hassle-free internet service with T-Mobile. The telco’s FWA customer base increased by 557,000 during Q3, giving it a total of 4.2 million. It has allowed T-Mobile to offer a compelling alternative to fixed broadband, but its service comes with the caveat that speeds will fluctuate depending on demand.

The extra capacity offered by mmWave could help to offer a faster, more consistent connection, making it even more appealing. However, the propagation challenges of mmWave spectrum means customers will have to ensure their FWA hub is sitting on the right shelf or window sill to establish a fast, reliable connection. Addressing complaints as customers struggle to put their hub in the right spot may be a problem for the Un-carrier.

Editor’s Note:

The NTIA will study the following bands in the next two years, noting that the spectrum could support a range of uses, including mobile broadband (IMT), drones and satellite operations:

- 3.1 GHz-3.45 GHz

- 5.03 GHz-5.091 GHz

- 7.125 GHz-8.4 GHz

- 18.1 GHz-18.6 GHz

- 37.0 GHz-37.6 GHz

References:

https://www.t-mobile.com/news/network/t-mobile-revs-up-millimeter-wave-with-5g-standalone

https://www.verizon.com/about/news/verizon-achieves-upload-speeds-surpassing-1-gbps

https://www.telecoms.com/5g-6g/t-mobile-finally-puts-mmwave-to-work-in-5g-sa-network

https://www.telecoms.com/wireless-networking/t-mobile-network-speeds-still-way-ahead-of-verizon-at-t

U.S. Launches National Spectrum Strategy and Industry Reacts

Ericsson Mobility Report touts “5G SA opportunities”

State of 5G SA:

“It’s been exciting to see the industry evolve in the last decade or so, and see first-hand the massive growth of 4G and the arrival of 5G,” said Fredrik Jejdling Executive Vice President and Head of Business Area Networks and Publisher of Ericsson Mobility Report.

The latest edition of Ericsson’s Mobility Report opens with the assertion that “5G standalone brings new opportunities,” which sounds promising, but there’s nothing in the report which shows what those opportunities are.

Ericsson says that 40 service providers have deployed or launched 5G SA in public networks, which agrees with Analysys Mason’s findings. To put that in context, around 280 service providers globally have launched commercial 5G with the overwhelming being 5G NSA.

Dell’Oro counted just seven 5G SA launches to date in 2023, while the GSA – which worked with Ericsson on the stats for its Mobility Report – shared data that also showed little growth in 5G SA this year.

………………………………………………………………………………………………………………………………………….

- 1. 6 bn Global 5G mobile subscriptions are projected to reach 1.6 billion by the end of 2023.

- 30% 5G mid-band population coverage outside mainland China has increased from 10 percent in 2022 to around 30 percent at the end of 2023.

- 56 GB Global mobile data traffic consumption per smartphone is expected to reach 56 GB per month at the end of 2029.

Ericsson predicts that there will be 1.6 billion 5G subs in the world by the end of this year, or 18% of all mobile subscriptions, driven by North America, where 5G penetration will reach 61%. As recently as June, the network equipment vendor forecast that the year-end 5G total would hit 1.5 billion, so clearly the market is increasing faster than expected. In the third quarter there were 163 million 5G subscriber additions taking the total to 1.4 billion by the end of September. As such, the year-end target look eminently achievable.

Ericsson puts total global 5G subscriptions at 5.3 billion by the end of 2029, by which date 5G network coverage should reach 85% of the population, up from 45% at the end of this year.

“With more than 600 million 5G subscriptions added globally this year, and rising in every region, it is evident that the demand for high performance connectivity is strong,” said Fredrik Jejdling, Executive Vice President and Head of Networks, at Ericsson. “The roll-out out of 5G continues and we see an increasing number of 5G standalone networks being deployed, bringing opportunities to support new and more demanding applications for both consumers and enterprises,” he added.

References:

https://www.ericsson.com/en/reports-and-papers/mobility-report

https://www.telecoms.com/5g-6g/5g-subs-exceed-expectations-but-they-re-not-standing-alone

Analysys Mason: 40 operational 5G SA networks worldwide; Sub-Sahara Africa dominates new launches

GSA 5G SA Core Network Update Report

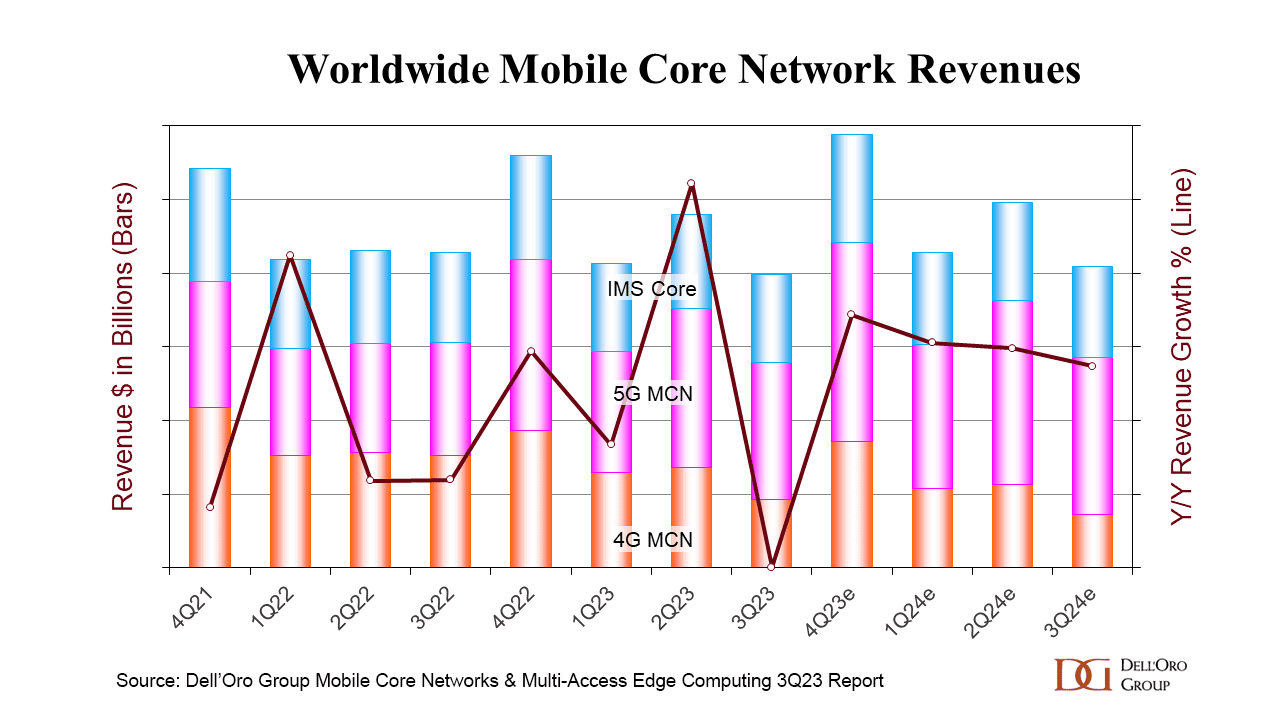

Dell’Oro: Mobile Core Network market has lowest growth rate since 4Q 2017

Dell’Oro: Mobile Core Network market has lowest growth rate since 4Q 2017

The global mobile core network (MCN) market has just turned in its lowest quarterly growth rate for almost six years, hit by a difficult political and economic climate, as well as by slow rollouts of 5G standalone core networks. Dell’Oro Group reports that the MCN market has become erratic, with the lowest growth rate since 4Q 2017. Europe, Middle East, and Africa (EMEA), and China were the weakest performing regions in 3rdQ 2023.

“It has become quite obvious the MCN market has entered into a very unpredictable phase after breaking the highest growth rate in 2ndQ 2023 since 1stQ 2021, and now hitting the lowest performing growth rate in 3rdQ 2023 since 4thQ 2017. Last quarter, EMEA and China were the strongest performing regions and flipped this quarter, becoming the weakest performing regions,” stated Dave Bolan, Research Director at Dell’Oro Group.

“Many vendors state that the market is volatile, attributing this phenomenon to macroeconomic conditions such as the fear of higher inflation rates, unfavorable currency foreign exchange rates, and the geopolitical climate.

“Besides subscriber growth, the growth engine for the MCN market is the transition to 5G Standalone (5G SA), which employs the 5G Core. But after five years into the 5G era, we are still seeing more 5G Non-Standalone (5G NSA) networks being launched than 5G SA, and the pace of 5G SA networks has slowed from 17 launched in 2022 to only seven so far in 2023. However, we expect more 5G SA networks to be deployed in 2024 than in 2023, and we expect 2024’s market performance to be better than 2023,” continued Bolan.

Additional highlights from the 3Q 2023 Mobile Core Network and Multi-Access Edge Computing Report include:

- Two new MNOs launched commercial 5G SA networks in 3Q23: Telefónica O2 in Germany and Etisalat in the UAE.

- Ericsson is the vendor of record for the 5G packet core for all seven 5G SA networks launched in 2023.

- As of 3Q 2023, 45 MNOs have commercially deployed 5G SA eMBB networks.

- The top MCN vendors worldwide for 3Q 2023 [1.] were: Huawei, Ericsson, Nokia, and ZTE.

- The top 5G MCN vendors worldwide for 3Q 2023 were Huawei, Ericsson, ZTE, and Nokia.

Note 1. Dell’Oro did not supply any actual MCN market share percentages or numbers.

……………………………………………………………………………………………………………………………….

In August the Global mobile Suppliers Association (GSA) released Q2 figures that showed just 36 operators worldwide has launched public 5G SA networks, including two soft launches, by the end of June, an increase of just one on the previous quarter.

In total, the GSA said that 115 operators in 52 countries had invested in public 5G SA networks – that includes actual deployments as well as planned rollouts and trials – by the end of Q2, with no new names added during the quarter, and an increase of just three on the end of 2022.

About the Report:

The Dell’Oro Group Mobile Core Network & Multi-Access Edge Computing Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, shipments, and average selling prices for Evolved Packet Core, 5G Packet Core, Policy, Subscriber Data Management, and IMS Core including licenses by Non-NFV and NFV, and by geographic regions. To purchase this report, please contact us at [email protected].

About Dell’Oro Group:

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, security, enterprise networks, and data center infrastructure markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions. For more information, contact Dell’Oro Group at +1.650.622.9400 or visit https://www.delloro.com.

References:

Dell’Oro: RAN market declines at very fast pace while

Mobile Core Network returns to growth in Q2-2023

Dell’Oro: RAN Market to Decline 1% CAGR; Mobile Core Network growth reduced to 1% CAGR

Dell’Oro: Mobile Core Network & MEC revenues to be > $50 billion by 2027

GSA 5G SA Core Network Update Report

5G SA networks (real 5G) remain conspicuous by their absence

Dell’Oro: Market Forecasts Decreased fo

r Mobile Core Network and Private Wireless RANs

Verizon once again delays 5G Standalone (SA) commercial service

Like AT&T, Verizon has promised 5G standalone (SA) core network for a very long time. The mostly wireless U.S. carrier initially said it would launch standalone 5G in 2020. Some in the industry thought it did so in 2022. But the company said the technology ‘is in testing now’ and is still not available commercially.

“We have it in trials only at this point. We don’t have it commercially available for our customers,” Verizon’s chief networking executive, Joe Russo, said on a podcast last month hosted by Recon Analytics. “So more to come in the next several months as Verizon will be entering the standalone core game.”

“It is absolutely a capability that we think will be another enabler to new use cases. But … the reliability and performance of Verizon’s network is what we stand for, and I don’t put technology out into the network that is a step back. It has to be a step forward. And all of the data that I see – both internal testing and with external testing that happens out there in the market – tells me that SA [standalone] needs a little bit more time.”

“We’re doing significant developing and testing to make sure that both the data session and the voice sessions in a standalone world are as good or better than what you would expect in our 4G network today. So we see that in the next several months we’re going to get there, but it was not my goal to be first in deploying standalone. It’s my goal to be best in deploying standalone.”

……………………………………………………………………………………………………………………………..

Verizon spokesperson Kevin King clarified that “we have commercial traffic running on our 5G non standalone core. That is what we announced earlier in the year. Joe was referring to our 5G standalone core which is in testing now.”

That cop-out was contradicted by a statement made during a webinar for analysts on September 29th, which was obtained by Light Reading. “People talk about the standalone core. Just terminology-wise, that’s the 5G core essentially. If you guys have read the stuff we’ve said publicly, certainly we serve some customers on portions of our 5G core,” said Mike Haberman, Verizon’s SVP of strategy and transformation, And then we have some internal stuff going on with other functionality on the core. We’re in the process of rolling out (5G SA) in a very smart fashion.”

“Here’s the deal: When you go to the standalone core, you can’t aggregate your LTE carriers. With the non standalone core I’m aggregating together both 5G and 4G. So when you go standalone you start to bifurcate the spectrum. So that’s the impact to the RAN [radio access network]. So you better be sure that your mobile [customer] distribution, where they are geography, makes sense. Or what will happen is those customers will experience a lower service level. No good. We want to be careful of that. So that’s why, when you do the standalone core, you have to pay very close attention to your radio access network because they are directly attached.”

On April 27th Verizon issued a press release describing the benefits of 5G standalone (SA) technology and how it’s “what sets Verizon apart.” However, the release doesn’t specifically say that Verizon launched the technology. That despite Verizon last year announced it had begun moving traffic onto its new 5G core, which supports both the non standalone (NSA) and standalone (SA) versions of the technology.

Last year, Mobile World Live reported that Verizon was migrating “commercial traffic onto SA 5G core.” The article cited an unnamed Verizon representative. Mobile World Live also reported that Ericsson, Casa Systems, Oracle and Nokia supply Verizon’s 5G core.

Dell’Oro Group, in January 2023, listed Verizon among the few North American wireless providers that had commercially launched the technology.

“This is a moving target,” Recon Analytics analyst Roger Entner told Light Reading. But Entner said Verizon’s position on the standalone version of 5G makes sense. “The benefits you can get today from standalone are limited.”

–>This author totally disagrees with Mr. Entner, because TRUE 5G=5G SA. IN OTHER WORDS, ALL OF THE 3GPP DEFINED 5G FEATURES REQUIRE 5G SA! That includes 5G security and network slicing.

…………………………………………………………………………………………………………………………………

Light Reading’s Mike Dano wrote:

Verizon now appears to be roughly three years behind its initial standalone 5G rollout plans. In the summer of 2020, Verizon said it would begin moving traffic onto its standalone 5G core “in the second half of 2020 with full commercialization in 2021.”

Then, in early 2022, Verizon CTO Kyle Malady suggested that the operator would begin moving some of its fixed wireless access (FWA) traffic onto its standalone 5G core by June of that year. He also said at the time that Verizon would start putting smartphone traffic onto that core in 2023.

………………………………………………………………………………………………………….

T-Mobile US and Dish Wireless are the only two 5G carriers that have launched commercial 5G SA. AT&T has made a lot of noise about it’s 5G SA plans but has yet to launch.

AT&T’s chief networking executive, Chris Sambar, wrote in a September 29th blog post that AT&T was moving some customers to standalone 5G. “Many of the newest mobile devices are ready for 5G standalone, and we continue to move thousands of customers every day. We also recently launched AT&T Internet Air home fixed wireless service, and from the start, this product rides on standalone 5G.”

https://www.lightreading.com/5g/verizon-surprises-with-ongoing-delays-in-5g-standalone-rollout

https://www.verizon.com/about/news/5g-standalone-why-it-matters

https://about.att.com/blogs/2023/network-ready.html

AT&T touts 5G advances; will deploy Standalone 5G when “the ecosystem is ready”- when will that be?

Analysys Mason: 40 operational 5G SA networks worldwide; Sub-Sahara Africa dominates new launches

GSA 5G SA Core Network Update Report

5G subscription prices rise in U.S. without killer applications or 5G features (which require a 5G SA core network)

Analysys Mason: 40 operational 5G SA networks worldwide; Sub-Sahara Africa dominates new launches

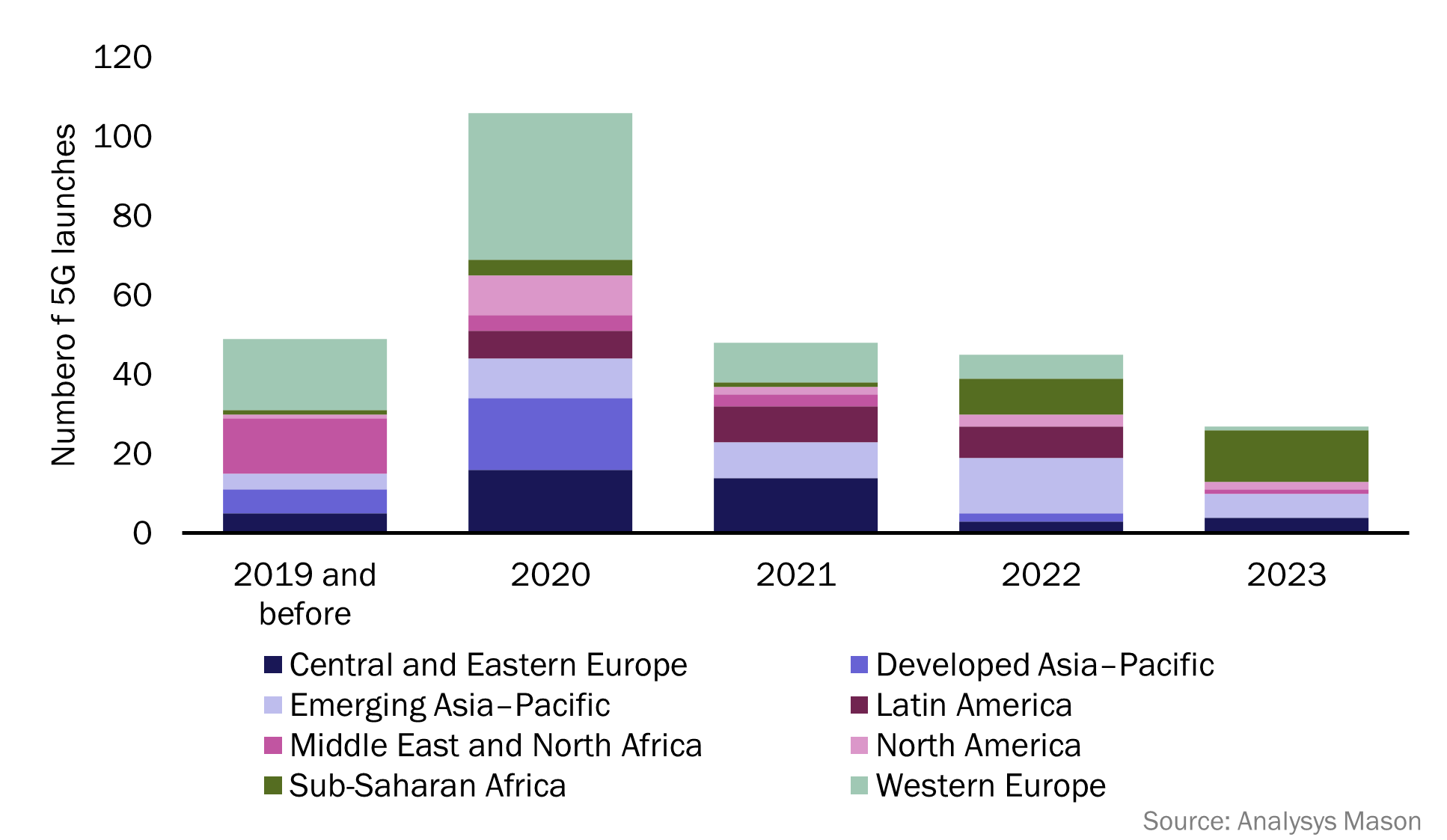

According to the latest edition of Analysys Mason’s 5G deployment tracker, 26 new 5G networks have been commercially launched across 22 countries so far in 2023, with an additional 55 5G networks either in deployment or scheduled for launch later this year.

Sub-Saharan Africa (SSA) has dominated 5G launch figures in 2023, with 13 new launches across 10 countries, accounting for over 48% of 5G launches during the period. Emerging Asia–Pacific (EMAP) has recorded 6 new 5G launches in 2023 so far, while Central and Eastern Europe (CEE) recorded 4 new 5G launches, respectively. Additionally, North America (NA) recorded 2 new 5G launches, while Western Europe (WE) and the Middle East and North Africa (MENA) each reported one new 5G launch in the same period. 5G standalone (SA) launches for the last 12 months (August 2022–2023) have continued to grow steadily, with 11 new operators commercially launching 5G SA networks. Five of these launches have occurred in 2023, with 3 operators launching in WE and 2 launching in MENA.

The market research firm’s 5G deployment tracker includes 338 entries from 2018 to 1H 2023, with 274 confirmed launches of 5G networks and 40 commercial launches of 5G SA networks, worldwide.

According to the latest edition of Analysys Mason’s 5G deployment tracker, 26 new 5G networks have been commercially launched across 22 countries so far in 2023, with an additional 55 5G networks either in deployment or scheduled for launch later this year.

Sub-Saharan Africa (SSA) has dominated 5G launch figures in 2023, with 13 new launches across 10 countries, accounting for over 48% of 5G launches during the period. Emerging Asia–Pacific (EMAP) has recorded 6 new 5G launches in 2023 so far, while Central and Eastern Europe (CEE) recorded 4 new 5G launches, respectively. Additionally, North America (NA) recorded 2 new 5G launches, while Western Europe (WE) and the Middle East and North Africa (MENA) each reported one new 5G launch in the same period. 5G standalone (SA) launches for the last 12 months (August 2022–2023) have continued to grow steadily, with 11 new operators commercially launching 5G SA networks. Five of these launches have occurred in 2023, with 3 operators launching in WE and 2 launching in MENA.

The 5G deployment tracker includes 338 entries from 2018 to 1H 2023, with 274 confirmed launches of 5G networks and 40 commercial launches of 5G SA networks, worldwide.

Figure 1: 5G network launches, worldwide, 2019 (and before)–2023

Network operators in SSA have long prioritised investment in 4G networks over 5G. This is due to the lower cost of 4G devices and infrastructure, and the high number of users on legacy networks, such as 2G and 3G, across the region. As a result, operators have prioritised the migration of these users to 4G networks over new 5G deployments. In 2021, 79.8% of all mobile connections in SSA were 2G or 3G connections, and there were only 6 operational 5G networks in the region. This changed in 2022, with operators launching 9 new 5G networks across the region.1 This number has continued to climb so far in 2023, with a total of 13 new 5G network launches since January.

SSA now accounts for over 48% of all 2023 5G launches, with the region now having more operational 5G networks than MENA, NA, Latin America (LATAM) and developed Asia–Pacific (DVAP). Airtel has launched the most 5G networks in SSA so far in 2023, with the group launching 4 new 5G networks in 4 different countries. These include:

- Kenya: Airtel became the second operator to launch a 5G network in Kenya, following Safaricom’s launch in October 2022. Airtel claims coverage across 370 areas including Mombasa, Nakuru, Nairobi and Kakamega.

- Nigeria: Airtel launched its 5G network in June 2023, with coverage in multiple areas including Abuja, Port Harcourt and Lagos. Airtel is the third operator to launch a 5G network in Nigeria, following MTN (2022) and Mafab (January 2023).

- Uganda: Airtel launched its 5G services in various areas of Kampala in August 2023, one month after MTN launched the first 5G network in Uganda.

- Zambia: Airtel became the second operator to launch a 5G network in Zambia in July 2023, following MT’s 5G launch in November 2022.

Other notable launches across SSA include:

- French Guiana: Orange Caraibe and SFR Caraibe both launched their 5G networks in 2023 in the 3.5GHz band. These are the first 5G networks in French Guiana.

- The Gambia: QCell became the first operator to launch 5G in The Gambia in June 2023, launching in selected areas of the capital city, Banjul.

- South Africa: Telkom South Africa launched their 5G network in 2023, becoming the fourth operator to launch 5G in South Africa after Rain, MTN and Vodacom.

…………………………………………………………………………………………………………………………………

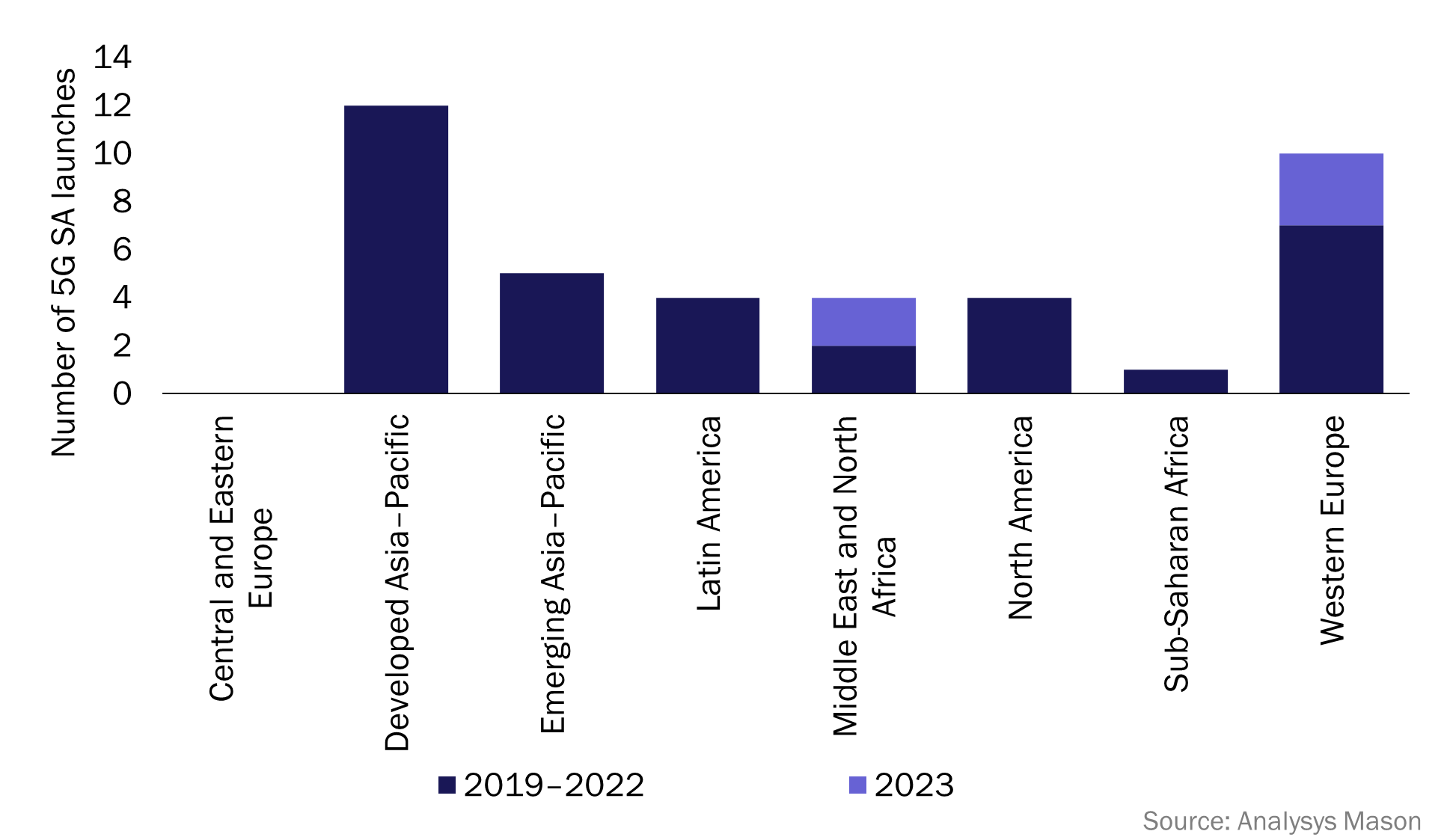

There are now 40 operational 5G SA networks worldwide, spanning 24 countries and 34 different operators. In the previous 12 months (from September 2022 to September 2023) there have been 11 new 5G SA launches, with 5 of these occurring in 2023. These 5 launches were spread across WE (3 new launches) and MENA (2 new launches). More 5G SA launches are expected in 2023, as launch figures have historically peaked in the second half of a calendar year. 5G SA launch figures are expected to accelerate over the next few years, and operators that have already launched 5G SA networks are likely to continue to expand their standalone coverage.

Analysys Mason predicts that by 2024, 5G SA will be the main source of revenue for vendors.

…………………………………………………………………………………………………………………………….

Editor’s Note: We strongly disagree with that 5G SA forecast and we don’t know if the “vendors,” like Ericsson, Nokia, Huawai, ZTE, Samsung, NEC, also provide 5G RAN equipment. Other 5G SA core network vendors, don’t make RAN equipment, e.g. Amazon AWS, Microsoft Azure, Cisco, VMware, Parallel Wireless and Mavenir

In the U.S., only T-Mobile and Dish Network have deployed 5G SA core networks. AT&T and Verizon have been talking the talk about 5G SA core networks but have no commercial deployments. UScellular 5G SA is in test mode. UScellular’s CTO Mike Irizarry said it’s now testing Nokia’s 5G SA core, but doesn’t plan to rush headlong into the SA 5G future.

Also, because there are no specification for 5G SA core network interoperability or roaming, 5G SA endpoint mobility will be extremely limited.

…………………………………………………………………………………………………………………………….

With three new launches so far in 2023, WE is beginning to compete with DVAP for the total number of 5G SA network launches. DVAP has led the total 5G standalone network launch figures since 2021 (see Figure 2), with 11 new launches in the last 2 years across Australia, Japan, Singapore and South Korea. Western Europe now accounts for 25% of all 5G SA networks worldwide, 5 percentage points less than DVAP which accounts for 30%. All regions have now launched at least one 5G SA network, excluding CEE (see Figure 2).

Figure 2: 5G SA launches, worldwide, 2019–2023

In 2023, notable deployments of standalone networks have included:

- Saudi Arabia: Zain launched the first 5G SA network in Saudi Arabia in March 2023, making Saudi Arabia the third country in MENA to have an operational 5G SA network, after Bahrain and Kuwait.

- Spain: Orange and Telefónica both launched 5G SA networks in 2023. These are the first two 5G SA networks in Spain.

- United Arab Emirates (UAE): E& (formerly Etisalat) launched its 5G SA network in February 2023, becoming the fourth operator to launch 5G SA services within MENA and the first in the UAE.

- United Kingdom: Vodafone launched the first 5G SA network in the UK, in June 2023, with coverage across Cardiff, Glasgow, London and Manchester. Vodafone has branded its 5G SA as ‘5G Ultra’.

References:

https://www.analysysmason.com/research/content/articles/5g-deployment-launches-rma18/

GSA 5G SA Core Network Update Report

ABI Research: Expansion of 5G SA Core Networks key to 5G subscription growth

Counterpoint Research: Ericsson and Nokia lead in 5G SA Core Network Deployments

Tech Mahindra and Microsoft partner to bring cloud-native 5G SA core network to global telcos

Omdia and Ericsson on telco transitioning to cloud native network functions (CNFs) and 5G SA core networks

Dell’Oro: RAN market declines at very fast pace while Mobile Core Network returns to growth in Q2-2023

Dell’Oro: RAN Market to Decline 1% CAGR; Mobile Core Network growth reduced to 1% CAGR

Dell’Oro: Mobile Core Network & MEC revenues to be > $50 billion by 2027

Dell’Oro: Market Forecasts Decreased for Mobile Core Network and Private Wireless RANs

Dell’Oro: Mobile Core Network market driven by 5G SA networks in China

Counterpoint Research – 5G SA Core Deployments Decelerate in H1 2023