U.S. Cellular 5G Phase 2 in 2nd half of 2020; 5G Use Cases described; TDS broadband services profiled

Backgrounder:

U.S. Cellular is 84%-owned by Telephone & Data Systems (TDS). That is why both companies participated in the former’s earnings call on August 7, 2020. It operates the fifth-largest wireless telecommunications network in the United States with 4.9 million connections in 21 states.

Source: U.S. Cellular

……………………………………………………………………………………………………………………….

“My first month at U.S. Cellular has been full of learning and listening – a seamless and effective transition,” said new CEO Laurent C. Therivel (LT).

“I want to thank Ken Meyers for providing sound advice and counsel. Over the past few weeks, I have traveled to various locations and met with many of our associates (in the safest manner possible). I am inspired by our customer-centric culture and high levels of engagement, and I’m inspired by the flexibility and resiliency our associates have displayed throughout this pandemic. It is clear to me that our competitive advantage rests on our focus on the customer and our high-quality network. Our network strength was recently recognized, with U.S. Cellular ranking #1 in the North Central Region in the J.D. Power 2020 Wireless Network Quality Performance Study – Volume 2, making this the 7th time since 2016 that U.S. Cellular has received an award. This recognition validates that our network modernization strategy is working.”

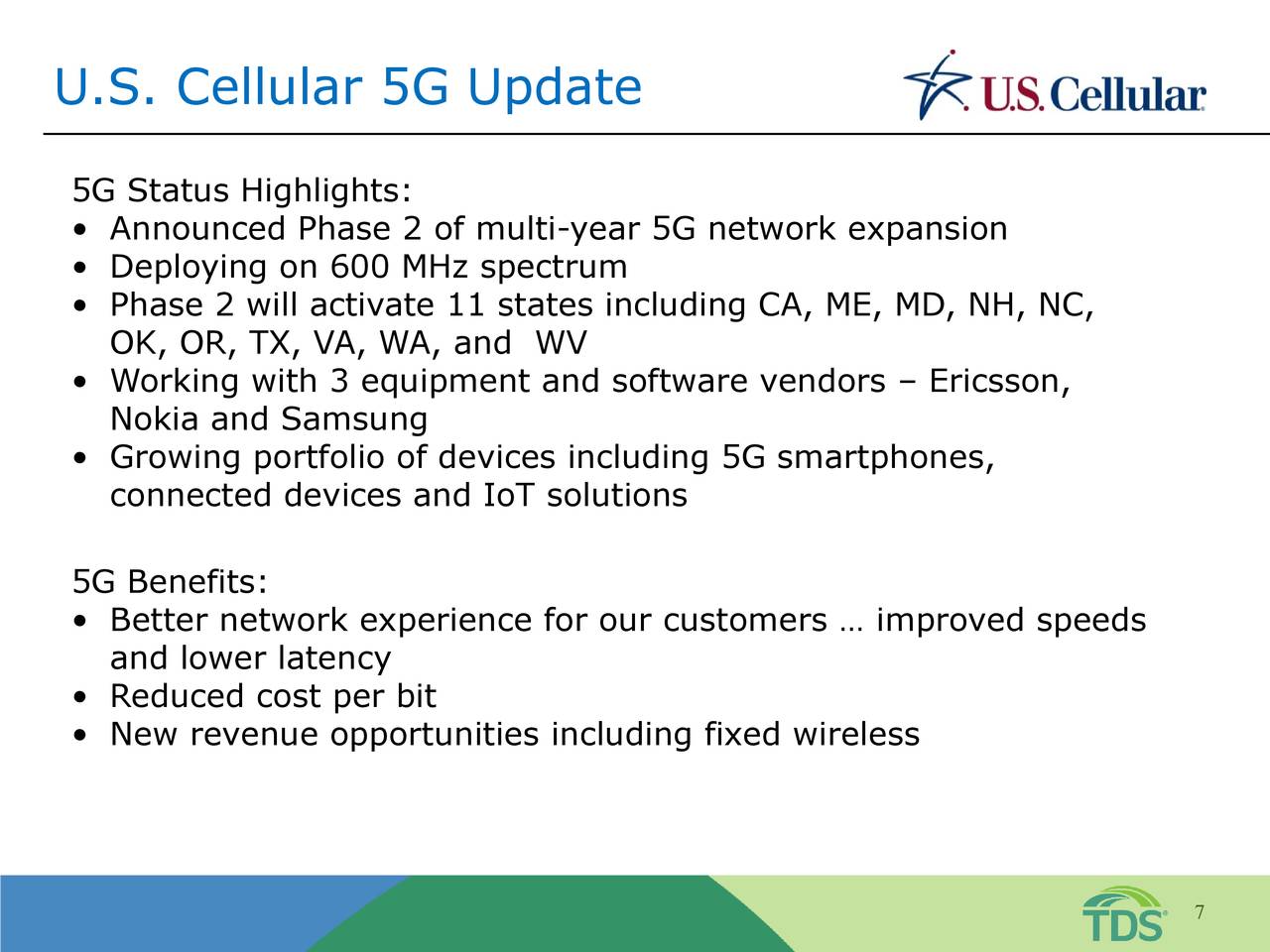

U.S. Cellular CTO Mike Irizzari talked up the company’s 5G deployment experience and future plans during Friday’s earnings call.

“Iowa and Wisconsin were Phase 1 of our multi-year 5G network expansion. And last week, we announced our next phase. Phase 2 will begin in the second half of 2020. We will deploy in 11 states or about 10 million POPs. We are working with 3 equipment vendors, and we are continuing to expand the number of 5G devices.

We have been very pleased with the performance of Phase 1. Customers are receiving an improved customer experience; our 5G deployment improves average and peak speeds for our 5G and our 4G customers. In addition to an improved customer experience and new revenue opportunities, we expect 5G to carry traffic more efficiently, improving the cost to deliver a bit. And this efficiency enables us to get the most out of our spectrum portfolio.

We expect to begin deploying our millimeter wave spectrum in 2021 to improve speed and capacity in denser areas of our footprint. Further, we expect to conduct trials of our millimeter wave fixed wireless service in 2021 in select markets.”

Editor’s Note:

U.S. Cellular acquired roughly $402 million worth of mmWave spectrum licenses in three recent FCC spectrum auctions.

US Cellular CFO Doug Chambers commented:

“From a network standpoint, we engineer our network for peak-usage periods, and the network continues to perform well. To date, COVID-19 has increased data traffic about 20% to 25% and our network has been able to handle that extra demand. Throughout the quarter, we continued our network modernization and 5G efforts, and we will be finishing our VoLTE deployment this year. Our expansion markets in Iowa and Northern Wisconsin are doing well. And as LT highlighted, we won another J.D. Power award.”

Q & A on 5G Use Cases (we don’t believe there are any!):

Ric Prentiss of Raymond James: As we think about 5G, what do you see as some of the top use cases in business cases in U.S. Cellular territory for 5G?

New CEO Laurent (LT) Therivel replied:

“Initially, when you think about 5G, there’s going to be a huge benefit on the cost side. Cost per gig is going to become a lot more efficient to manage traffic. And if I look at just the past quarter with the pandemic, we just briefly covered this in our comments, but I don’t want to leave it unsaid. Data traffic up over 70%. And the mix of that traffic, right, shifting from – if you think about customers want to be covered where they work, live and play, big shifts from work to live and play.

And so managing that traffic and managing the cost of that traffic is going to be critical. And 5G is going to help us a great deal there.

Talking about use cases, initially, you can think about the use cases as being around high-speed Internet (enhanced Mobile Broadband) and providing fixed wireless broadband connections (which is not an IMT 2020 Use Case) to our customers. We think there’s a significant opportunity there. And you can expect to see that portion of the business continue to grow.

If I then fast forward truly long run, autonomous car, AI and facilitating some of those really high speed, low latency use cases are going to be critical (However, URLLC not complete in 3GPP Release 16 and won’t be in IMT-2020.specs).

From that perspective, do we expect to see near-term monetization of those? No, but it’s going to be table stakes, having a strong 5G presence. And then in the midterm, you can expect to see use cases around business and business solutions, think connected health, connected education.

We are going to be ramping up our presence on the business side when we talk – I am sure I will get questions about priorities moving forward and certainly around top line growth business being a component of that top line growth. Those connected manufacturing, connected health, those kinds of use cases are going to be enabled by 5G. I think those will be starting to take shape in the coming years, and I think we are well positioned to take advantage of it.”

LT Therivel replied to Morgan Stanley’s Simon Flannery question about the future US Cellular fixed wireless product and its speed(s):

“We are able to help customers and get customers connected in areas where maybe cable either doesn’t address or has very limited presence. And Mike talked a little bit about the 5G rollout, rolling out millimeter wave. So as we start to densify the network with millimeter wave, that’s going to create incremental opportunities for capacity and excess capacity to go monetize. And so you can expect to see a higher speed product brought to the market price point to be determined.

Editor’s Note:

U.S. Cellular currently provides 25GB of high-speed fixed wireless data for $50 per month via its LTE network; after customers reach that allotment, their speeds are slowed to 2G speeds. The company doesn’t provide any firm speed promises because the company said speeds “vary due to area, coverage, foliage, compression or the network management requirements.”

Verizon is the only U.S. wireless network operator with plans to deploy fixed wireless services on mmWave spectrum. The company currently offers fixed wireless services on its LTE network as does US Cellular. Mike Dano of Light Reading wrote that “CenturyLink, Shentel, Windstream, C Spire, Cable One and Midco, among others, also have plans to offer fixed wireless across a variety of spectrum bands, including potentially mmWave bands.”

………………………………………………………………………………………………………………………..

LT did not answer Flannery’s follow up question: “Any sort of sizing? Is this hundreds of thousands of potential households or what’s the right way to think about the opportunity?”

–>That was a quite reasonable “punt.” U.S. Cellular’s 5G mmWave mobile broadband roll-out won’t be till 2021 (if not delayed by permits for mounting small cells and pandemic induced installation restrictions). There won’t be any excess mmWave bandwidth to monetize till at least 2022. The competitive landscape for fixed broadband access at that future time is completely unknown. We expect to see a pick up of FTTH installations by then.

……………………………………………………………………………………………………………………………………………

Telephone & Data Systems (TDS)

TDS CFO Vicki Villacrez announced an innovative new “cloud TV” service for the wireline telco:

“We are pleased to report that we have expanded our launch of our cloud TV product called TDS TV+ to additional cable and wireline markets, including our Wisconsin out-of-territory clusters and expect to complete those rollouts in the third quarter.

Additionally, we plan to roll out TDS TV+ to our new fiber market, Coeur d’Alene, Idaho, in the fourth quarter. This is a really great product. And while it is still early in its launch, we are focused on ensuring its success across our markets.

From a network perspective, the current crisis continues to reaffirm the importance of high-speed Internet and how important not only our investments have been, but also our continued advocacy on behalf of rural America.

As a result of driving fiber deeper into our markets, we have robust networks, which continue to remain very stable and meet our customers’ needs. From an out-of-territory perspective, pre-sales continue to exceed our expectations.

We are currently installing service in our Wisconsin and Idaho clusters. We remain focused on construction throughout these communities, and we are working towards commencing construction in Spokane, Washington, where we recently launched presale activities. Overall, we remain committed to achieving our strategic priorities through the second half of the year.”

And a status report on broadband wireline Internet and TV services and trends:

“We are now offering up to 1-gig broadband speeds in our fiber markets. Across our wireline residential base, essentially one-third of all broadband customers are now taking 100-megabit speeds or greater compared to 26% a year ago. This is helping to drive a 4% increase in average residential revenue per connection in the quarter.

Wireline residential video connections grew 9% compared to the prior year. Video is important to our customers. Approximately 40% of our broadband customers in our IPTV markets take video, which for us is a profitable product. Our strategy is to increase this metric as we expand into new markets that value these services and through the launch of our new TDS TV+ product. Our IPTV services in total cover one-third of our wireline footprint, leaving opportunity to further leverage our investment in video.

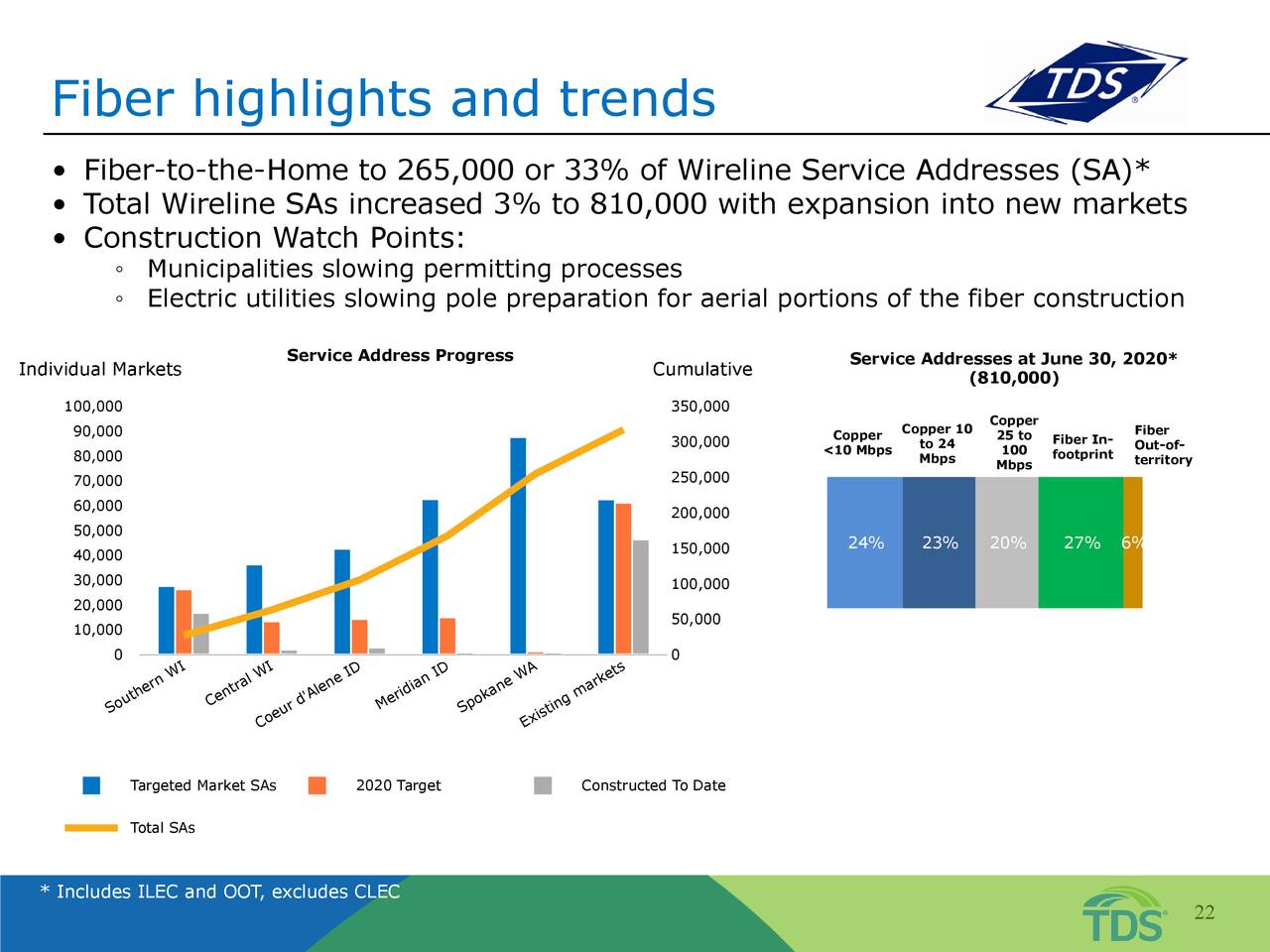

265,000 or 33% of our wireline service addresses are now served by fiber, which is up from 27% a year ago. This is driving revenue growth while also expanding the total wireline footprint, 3% to 810,000. Our current fiber plans include roughly 320,000 service addresses that will be built over a multiyear period. Year-to-date, we have completed construction of 25,000 fiber addresses. And overall take rates are generally exceeding expectations in these areas that we have launched to-date. We are expecting our fiber service address delivery to more than double in the second half of the year as we continue launching new markets.”

References:

Dish Network: 5G O-RAN compliant, multi-vendor network; Boost and Ting on board

5G O-RAN Network Progress, but no deployment schedule:

Dish Network President & CEO W. Erik Carlson said on Friday’s earnings call that the company was making progress in “building the nation’s first O-RAN compliant 5G network and since the last call we’ve named several key vendors including Altiostar, OpenRAN, Mavenir, Fujitsu, and VMware.” However, the completion date and deployment schedule were not revealed.

Charlie Ergen, Dish Co-Founder and Chairman of the Board, added that there’s a lot of excitement about O-RAN radios and the path that Dish is taking there. He said that Mavenir is doing some of the software for the baseband distribution unit and that VMware enables Dish to “stitch together the cloud” with its 5G O-RAN based network. Containers and micro services are being used in this implementation, but exactly how was not revealed or discussed.

Highlighting VMware’s contribution to the 5G O-RAN project, Ergen said:

“But when you put all that together, you got to make it work and you got to make it work on different cloud providers and private clouds, and VMware allows us to horizontally go across the stack and stitch that stuff together. And the way we look at partnerships, VMware has done a lot of work for us already even before we signed the contract with them.

They’re learning a lot about Telco and O-RAN and so they’re getting a real R&D sandbox to play in and they’re making our business better and we’re making their business better. So it’s a really, really good win-win for both companies and they’ve been a tremendous vendor even before we signed a contract with them.

So the big picture thing is there is nothing — there is nothing that stops us from building really the best network in the United States. There is no law of physics — there’s no law of physics, there is no technology that really hasn’t changed. It’s really execution. It’s really execution risk for us and our vendors to make it happen. But we’re not reinventing science, we’re not reinventing anything. We’re just taking really good cloud providers and software providers and making what has been a very clunky, hardware-centered highly operational cost environment, very similar to data centers 20 to 30 years ago.

We’re going to make it (5G O-RAN) into a modern network. So everything exists to do that. And we’re just going to go do it. We don’t spend a lot of time talking about it externally because everybody is going to be skeptical up until we light it up and then people will have their opinion about it. So that’s what we’re going to do.”

………………………………………………………………………………………………………………………………….

Dish’s Other Wireless Network Businesses:

Earlier this week, Dish acquired Ting Mobile and announced a partnership with Tucows on technology services. The company acquired T-Mobile assets including customer relationships and the brand in order to support Ting Mobile customers.

Dish closed the Boost Mobile acquisition (from T-Mo, but actually it was owned by Sprint) on July 1st and will report Boost results for the first time in the third quarter. The company will report Boost results in their Wireless segment and will disclose key metrics such as ARPU and subscriber data at that time. As part of the T-Mo/Sprint merger, Dish also acquired $3.6 billion of 800 MHz spectrum, which was Sprint’s entire 800 MHz spectrum holdings.

Craig Moffett of MoffettNathanson had this comment about Dish’s wireless business:

“Yes, they’ve chosen VMware and few other vendors. And small, private tower operators report some Dish activity – Dish sensibly seems to be focusing on smaller towercos first, as the majors will have more negotiating leverage and will therefore drive a harder bargain. And, sure, they’ve now bought Ting, a small operator to augment their Boost business (these pre-paid businesses were acquired after the end of the just-reported second quarter).

But they still haven’t started materially building. And they still haven’t found a strategic partner. They still haven’t gone to the capital markets for financing. And they still haven’t changed their capex guidance for wireless for this year – a paltry $250 to $500M, excluding capitalized interest.

Nor have they changed their longer term guidance of $10B to build a virtualized network, a number that we no longer have to caveat by saying we don’t believe.

Save for some slowly escalating wireless spending as they continue to gradually hire the people they’ll need to run the business – although even that is going far more slowly than one would expect – we’re left with a satellite business, and only a satellite business (OK, also an OTT business) in Q2 results.”

Craig, along with many analysts (including this author) believe Dish could take steps to unlock value by selling some or all of its significant spectrum assets. Dish has a long history of buying spectrum and doing nothing with it. As FierceWireless wrote last year, “Dish has spent roughly $20 billion over the past decade to amass a significant spectrum portfolio, and has roughly 95 MHz of low-band and mid-band spectrum per market.” That was before Dish bought Sprint’s entire 800 MHz (low band) spectrum assets, which are not included in this graph:

Dish has promised the FCC that it “will deploy a facilities-based 5G broadband network capable of serving 70% of the US population by June 2023 and has requested that its spectrum licenses be modified to reflect those commitments.” Dish would have to pay fines of up to $2.2 billion if it fails to meet its 5G deployment deadlines.

Conclusions:

Dish Network’s massive bet on deploying wireless spectrum it owns overshadows its declining cash-cow satellite television business. Dish reported a net loss of 40,000 net satellite television customers, half the figure a year ago as far fewer accounts deactivated service. The firm’s customer base likely skews towards customers that place less value on live sports and more on news coverage, which has delivered strong ratings during the pandemic and protests. Dish also lost (net) 56,000 Sling customers, better than the 281,000 lost the prior quarter, which had come following a large price increase at the start of the year. Price increases fueled a 7% year-over-year increase in average revenue per customer, roughly offsetting customer losses as total revenue declined 0.8%.

Moreover, Dish isn’t likely to become a full-fledged nationwide wireless network competitor, because Dish’s plan is only to cover 70 percent of the US population by June 2023. That could leave 100 million Americans without the option of a fourth wireless carrier (behind Verizon, AT&T, and the new T-Mo). Finally, the whole O-RAN concept is unproven with no liaison arrangements between the ITU or 3GPP and either of the two O-RAN spec writing entities – the O-RAN Alliance (which Dish is implementing) and the TIP Open RAN project.

Dish’s plan of covering 70 percent of the 327 million people in the U.S. isn’t impressive compared to the major carriers’ current 4G LTE coverage, which is important because carriers admit that 5G won’t be much faster than 4G in rural areas where millimeter-wave deployments aren’t viable. Outside densely populated areas, Verizon says that 5G speeds will merely be like “good 4G.”

We are also of the opinion, that Dish’s physical 5G deployment costs will be much more than Dish has budgeted and can not be financed without Dish having to borrow significant amounts of money from the credit markets or partner companies..

……………………………………………………………………………………………………………………………

References:

https://www.fiercewireless.com/wireless/wake-doj-deal-where-dish-s-spectrum-and-how-much-does-it-have (Dish Spectrum Maps)

Dish’s 5G network plan may be delayed for years as a result of COVID-19

5G Base Station Deployments; Open-RAN Competition & HUGE 5G BS Power Problem

According to Taiwan based market research firm TrendForce, the big three China and European telecom equipment manufacturers captured more than 85% market share in the global mobile base station industry in 2019, with Sweden-based Ericsson, China-based Huawei, and Finland-based Nokia as the three largest suppliers. However, owing to the U.S.-China trade war and the export controls issued by the U.S. government, Huawei subsequently was unable to procure key components from U.S.-based RF-front end manufacturers, in turn affecting the sales performance of its base stations in the overseas markets. As a result, Huawei is expected to focus its base station construction this year primarily in domestic China.

Total 5G base stations in China are projected to exceed 600,000 in 2020, while Japanese and Korean equipment manufacturers aggressively expand in the overseas markets.

By the end of 1st Half of 2020, the three major Chinese mobile network operators, including China Mobile, China Unicom, and China Telecom, had built more than 250,000 5G base stations in China. This number is projected to reach 600,000 by the end of this year, with network coverage in prefecture-level cities in China. In addition, emerging infrastructures such as 5G networks and all-optical networks will generate commercial opportunities for Huawei. According to the GSM Association’s forecasts, by 2025, more than a quarter of cellular devices in China will operate on 5G networks, occupying one-third of all global 5G connections.

On the other hand, thanks to successful 5G commercialization efforts in Korea, Samsung has seen a surge in its base station equipment. The company has provided base stations for the three major mobile network operators in Korea, including SKT, KT, and LG Uplus, in addition to collaborating with U.S. operators, such as AT&T, Sprint, and Verizon.

Open RAN Competitors:

The UK government is now targeting Japan-based NEC and Fujitsu as Huawei replacement suppliers of 5G network equipment. As European and the U.S. governments have implemented sanctions against Huawei, Japanese equipment suppliers now have the perfect opportunity to raise their market shares in Europe and possibly in the U.S. (with upstart 5G network providers that adopt “OpenRAN.” Throw in O-RAN Alliance members Mavenir, Parallel Wireless, Robin, Altiostar and Radisys into the mix and there may be serious competition for the big three base station vendors, especially OUTSIDE OF CHINA (where Huawei and ZTE will surely dominate).

……………………………………………………………………………………………………

Sidebar: 5G Base Station Power Consumption Issue -China article

by 海外风云 (courtesy of Yigang Cai)

A recent news report from China (used Google Translate to convert to English) highlighted the critical issue of network operators shutting down 5G base stations to save electricity bills. Selected 5G base stations in China are being powered off every day from 21:00 to next day 9:00 to reduce energy consumption and lower electricity bills. 5G base stations are truly large consumers of energy such that electricity bills have become one of the biggest costs for 5G network operators.

- Using this method of turning off the 5G base station at night to save power can save 15 Chinese yuan a day in electricity costs. The current 200,000 base stations can save 1.2 billion annually.

- By the end of this year, 1 million 5G base stations will be built, saving 6 billion in a year.

- If there are more than 2 million base stations, 12 billion electricity can be saved a year, which is equivalent to China Unicom’s total profit in one year.

- If there are more than 2 million base stations and they are not turned off for 24 hours, then all the money earned by Unicom will be paid for electricity.

- The more base stations, the greater the loss of revenues.

How many 5G base stations will the future society need? If the transmission speed and coverage rate required by 5G are reached, the total number of base stations may exceed everyone’s imagination.

According to news reports, the North Bund of Shanghai’s Hongqiao District is the world’s first gigabit 5G high-speed demonstration zone, with 26 base stations per square kilometer. According to the plan, the total number of 5G base stations in Shanghai’s Hongqiao District will exceed 1,000 in two years. The total area of Hongqiao District is 23.5 square kilometers.

According to the plan, about 50 base stations are required per square kilometer. If 5G base stations are covered nationwide, 9.6 million x 50=480 million base stations are required.

The electricity bill is equivalent to several hundred times the annual profit of China Unicom. Even if it only covers 1% of the country’s area, electricity bills can bankrupt the three major operators.

This is only the electricity bill and does not include any other costs. How much power does a 5G base station consume? Look at this test data, this is already the world’s top-level base station, produced by the world’s top suppliers, using the most advanced chips from Japan and the United States. 5G base stations consume several times more power than 4G base stations.

Editor’s Note:

A typical 5G base station consumes up to twice or more the power of a 4G base station, writes MTN Consulting Chief Analyst Matt Walker in a new report entitled “Operators facing power cost crunch.” And energy costs can grow even more at higher frequencies, due to a need for more antennas and a denser layer of small cells. Edge compute facilities needed to support local processing and new internet of things (IoT) services will also add to overall network power usage. Exact estimates differ by source, but MTN says the industry consensus is that 5G will double to triple energy consumption for mobile operators, once networks scale.

………………………………………………………………………………………………………………………………………

The total number of 5G base stations must be dozens of times more than that of 4G to achieve high-speed coverage. 02 Why does 5G need so many base stations? Why do we need so much transmit power?

A basic principle of communication: the higher the transmission speed, the greater the signal-to-noise ratio can ensure accurate transmission. In other words, the more you need high-speed propagation, the more power and shorter distances you need.

In order to achieve faster speeds, we must use higher frequencies, above 10 GHz, or even 300 GHz (mmWave). The higher the frequency, the lower the wall penetration ability (implying line of sight required for correct signal reception).

2.4G Hz WiFi is already impenetrable through two walls, and higher frequency penetration is even worse. In order to ensure the signal strength, the power must be increased. In order not to be blocked by walls, many base stations must be densely placed in the cell to avoid being blocked by too many walls.

If you want to enjoy the high speed of the 5G era, you have to increase the number of base stations more than ten times or even hundreds of times. There is no choice.

In the 5G era, everyone will not worry about the harm of electromagnetic radiation to the body, and everyone will no longer oppose the establishment of base stations in communities. Because no matter where you live in any community, there are densely packed base stations. There are 50 base stations in one square kilometer, and you can’t avoid them.

At that time, the street lamps, power poles and billboards you saw were probably 5G base stations in disguise. There is no way to avoid it. A few years later, if you find that not many people are sick due to electromagnetic radiation, you will believe that electromagnetic radiation is actually not harmful.

…………………………………………………………………………………………………………………………………

Early 5G Use Cases and Applications:

According to TrendForce’s latest investigations, 5G use cases have been in telemedicine and industrial IoT during the spread of COVID-19 in 2020. Primary applications of 5G during this period include contactless disinfection robots, remote work, and distance learning.

Currently, China has been most aggressive in developing 5G networks, with more than 400 5G-related innovative applications in transportation, logistics, manufacturing, and health care in 1st Half of 2020. At the same time, the emergence of 5G services has created a corresponding surge in base station demand.

TrendForce research vice president Kelly Hsieh indicates that, from a technical perspective, the growth in mobile data consumption, low-latency applications (such as self-driving cars, remote surgeries, and smart manufacturing), and large-scale M2M (smart cities) requires an increase in 5G base stations for support. Constructing these base stations will likely bring various benefits, such as investment stability, value chain development, and interdisciplinary partnerships between the telecommunication industry and other industries.

References:

https://www.trendforce.com/presscenter/news/20200803-10422.html

CenturyLink Q2-2020 Earnings Beat; Fiber and Low Latency are the Foundation for Emerging Applications

CenturyLink Inc. on Wednesday reported second-quarter net income of $377 million which beat analysts expectations. The global communications and IT services company posted revenue of $5.19 billion in the period compared to $5.375 billion for the second quarter 2019.

The company’s communications services include local and long-distance voice, broadband, Multi-Protocol Label Switching (MPLS), private line (including special access), Ethernet, hosting (including cloud hosting and managed hosting), data integration, video, network, public access, Voice over Internet Protocol (VoIP), information technology, and other ancillary services. CenturyLink also serves global enterprise customers across North America, Latin America, EMEA, and Asia Pacific.

![]()

“We had a solid quarter of both revenue and sales results, highlighted by the performance in Enterprise, iGAM and consumer broadband,” said Jeff Storey, president and CEO of CenturyLink. “We have delivered for our customers in record time, and our agility positions us well to combine our network infrastructure with our cloud, security, edge and collaboration services into a platform that meets our customers’ data and application needs. I’m proud of the CenturyLink team’s response to COVID-19 and how we have worked with our customers, communities and each other, both in the current crisis and for the long-term.”

During CenturyLink’s Q2 2020 earnings call Wednesday afternoon, Storey said:

“The economic effects of the pandemic created uncertainty for our customers, partners, the company, and the market in general. It‘s also highlighted the absolutely essential and durable nature of CenturyLink’s services and infrastructure in an all-digital world. We own the critical infrastructure — everything from the extended fiber network, to the deep interconnection relationships required to deliver customers scalable, secure network that is easily and flexibly consumed.”

“Our customers see that using next generation technologies enabled them to adapt their business models more rapidly and are working to take advantage of tools like artificial intelligence and machine learning across distributed compute resources and high performance networking. This translates into greater demand for transport services, hybrid WAN connectivity, network based security, edge computing and managed services as enterprises adjust to a more data dependent and distributed operating environment. This new normal has also increased consumers’ need for digital services and the demand for data shows no signs of slowing.”

“As our customers moved beyond the first wave of crisis response, we‘ve seen a marked change in their engagement and increased urgency in their dialog around longer-term digital transformation of their work environment.”

………………………………………………………………………………………………………………………………………………

CenturyLink has been pleasantly surprised with the demand for broadband it‘s seeing from the consumer segment right now as many employees continue to work from home as a result of the pandemic. Indeed, 75% of CenturyLink employees are now working from home, Storey said.

Enterprise sales orders grew year-over-year for dynamic, fiber-based services as customers started “buying again” in the second fiscal quarter, Storey said. Enterprise is a market segment that includes CenturyLink‘s high-bandwidth data services, managed services and SD-WAN services. Revenues increased by about 1 percent to $1.43 billion during the carrier’s fiscal second quarter compared to $1.41 billion in Q2-2019.

Small and medium business (SMB) sales fell 6.1 percent during the quarter to $646 million compared to $688 million in Q2 2019. CEO Storey said that CenturyLink will be actively working to grow its SMB customer base in future quarters. The carrier hopes to attract more SMB customers in the same way it‘s gained traction with enterprises, through its fiber-based network offerings, together with services such as embedded security, edge computing, IP enablement and managed services, Storey said.

In addition to COVID-19, the SMB segment continued to be plagued by legacy voice declines, said CenturyLink‘s CFO Neel Dev. “We are monitoring [this segment] and working closely with our customers,” he said. ”Over the long-term, we believe SMB represents a growth opportunity for us … it’s a large addressable market.”

During the quarter, CenturyLink added 42,000 1-gig and above customers, a record since the company began expanding their fiber to the home efforts.

CenturyLink’s Global Network Statistics:

- 450K Fiber Route Miles

- 170K+ On-Net Buildings

- 27M Technical Space (square feet)

- 2,200+ Public Data Centers On-Net

- 100+ Edge Compute Nodes (Enabling > 98% of U.S. Enterprises within latency of 5ms)

–>Most highly connected Internet peering backbone in the world

…………………………………………………………………………………………………………….

Two distinct business models with an all-digital operating mindset:

1. Enterprise:

- Growth-oriented, fiber-based Enterprise services

- Fiber is the enabler for all emerging communications technologies

- Highly scalable, global network

- Services are enhanced by cloud, security, WAN and edge initiatives

2. Consumer and Small Business:

- Coupling Century Link’s extensive footprint with greater digital engagement

- Expand efforts to grow Small Business group of customers

- Investing in growth with fiber-based, high-speed broadband

Fiber and Low Latency are the Foundation for Emerging Applications

• IoT

• Smart manufacturing and retail

• Personalized healthcare and finance

• Robotics

• AI/Big Data

• Augmented Reality/Virtual Reality

• Real-time video analytics

• 5G enablement (fiber backhaul for wireless telco partners)

More from CEO Storey:

“This agility is key to our strategy and is underpinned by our ongoing transformation from a telecom service provider to a leading technology company providing network and network supported technology solutions to today’s digital market.

We all know how well positioned our infrastructure is, that our value proposition is more than having great infrastructure. I frequently talk to employees about how our relationships with customers must be rooted in CenturyLink’s capabilities to drive their success, rather than the mindset of speeds and feeds and circuits of a typical telecom company.

As a technology company, we combine our deep infrastructure strength with a digital operating environment that enables our customers to turn their data and connectivity into a strategic advantage.

We integrate network, compute and operational technologies with managed services to simplify their business operation. Capabilities like orchestration services help them control the thousands of widely distributed devices and digital assets they now have to manage. The COVID-19 crisis didn’t create this need, but it has certainly amplified and accelerated it. And you can see this in our second quarter results with improving revenue trend led by revenue growth in enterprise, solid performance in iGAM on a constant currency basis and growth in consumer broadband.”

CenturyLink says they are well-positioned to capture expanding addressable market opportunities. Some examples are: Manufacturing, Gaming, and Retail. Storey highlighted the company’s change from wireline telecom and and IT services to a digital technologies solutions provider:

“This is the CenturyLink of the future, a company that delivers digital technology solutions to our customers differentiated through our world-class fiber infrastructure. If you consider the increasing demand across all customer verticals to move massive datasets as quickly as possible to widely distributed processing resources, our infrastructure is very well aligned to meet this shift in requirement.

By combining just 100 or so of our existing technical spaces with our deeply distributed fiber network, we can serve around 95% of US enterprise locations within five milliseconds of latency. Further, as operators of one of the largest and most interconnected networks in the world, we enable our customers to efficiently and effectively collect, process and move their data seamlessly across public clouds, private clouds, public data centers, company-owned data centers and the various work locations of the enterprise whether in employee’s homes or in the office. Now I see examples of this in our business every day.”

T-Mobile Announces “World’s 1st Nationwide Standalone 5G Network” (without a standard)

T-Mobile USA claims they are the first wireless network operator in the world to launch a commercial nationwide standalone 5G network (5G SA). The “Un-carrier” is also expanding 5G coverage by 30 percent, now covering nearly 250 million people in more than 7,500 cities and towns across 1.3 million square miles.

“Since Sprint became part of T-Mobile, we’ve been rapidly combining networks for a supercharged Un-carrier while expanding our nationwide 5G footprint, and today we take a massive step into the future with standalone 5G architecture,” said Neville Ray, President of Technology at T-Mobile. “This is where it gets interesting, opening the door for massive innovation in this country — and while the other guys continue to play catch up, we’ll keep growing the world’s most advanced 5G network.”

IEEE Techblog readers know that all previously deployed (pre-standard) “5G” networks focused on delivering new 5G radio (3GPP Rel 15 5G NR) in the data plane while leveraging existing LTE core networks, management and signaling in the control plane. With a new 5G Core network, T-Mobile engineers have already seen up to a 40% improvement in latency during testing. T-Mo claims:

“This is just the beginning of what can be done with Standalone 5G. When coupled with core network slicing in the future, 5G SA will lead to an environment where transformative applications are made possible — things like connected self-driving vehicles, supercharged IoT, real-time translation … and things we haven’t even dreamed of yet.”

In the near-term, 5G SA enables T-Mobile US to unleash its entire 600 MHz footprint for 5G. With non-standalone network architecture (NSA), 600 MHz 5G is combined with mid-band LTE to access the core network, but without SA the 5G signal only goes as far as mid-band LTE. With today’s launch, 600 MHz 5G can go beyond the mid-band signal, covering hundreds of square miles from a single tower and going deeper into buildings than before.

To make the world’s first nationwide commercial SA 5G network a reality, T-Mobile partnered closely with Cisco and Nokia to build its 5G core, and Ericsson and Nokia for state-of-the-art 5G radio infrastructure.

OnePlus, Qualcomm Technologies and Samsung have helped the Un-carrier ensure existing 5G endpoint devices can access 5G SA with a software update, based on compatibility. The 5G SA software update is required to activate the 5G SA functionality. For example, the Samsung Galaxy S20+ 5G requires a software download (available August 4, 2020) to enable 5G SA operation.

For more information about T-Mobile’s 5G vision, visit: www.t-mobile.com/5g. To see all the places you’ll get T-Mobile’s current 5G down to a neighborhood level, check out the map here: www.t-mobile.com/coverage/5g-coverage-map.

……………………………………………………………………………………………………………………………………

Comment and Analysis: Specs for 5G Core (there is no standard)

T-Mo’s launch of standalone 5G is noteworthy considering there are no standards for 5G Core from any SDO! ITU-T IMT 2020 non radio aspects SG’s aren’t even working on it!

Yeah, we know about 3GPP Rel 16 5G Core/Architecture specs:

- TS 23.501 5G Systems Architecture, with annexes which describe 5G core deployment scenarios

- TS 23.502 [3] contains the stage 2 procedures and flows for 5G System

- TS 23.503 [45] contains the stage 2 Policy Control and Charging architecture for 5G System

Collectively, all three of the above referenced 3GPP Rel 16 5G Systems Architecture documents do not specify the detailed mechanisms, protocols and procedures to implement a 5G core network.

For example, there are many software choices for implementing a “cloud native” 5G Core: containers, virtualized network functions, kubernetes, micro-services. Each Network Function (NF) offers one or more services to other NFs via Application Programming Interfaces (APIs). And there is no standard for the APIs associated with a given NF!

The only 5G Core implementation spec we know of is from GSMA. It’s titled: “5G Implementation Guidelines: SA Option 2.” That document provides a checklist for operators that are planning to launch 5G networks in SA (Standalone) Option 2 configuration, technological, spectrum and regulatory considerations in the deployment. The current version of the document currently provides detailed guidelines for implementation of 5G using Option 2, reflecting the initial launch strategy being adopted by multiple operators. There is an implementation guideline for NSA Option 3 already available.

However, as described in “GSMA Operator Requirements for 5G Core Connectivity Options” there is a need for the industry ecosystem to support all of the 5G core connectivity options (namely Option 4, Option 5 and Option 7). As a result, further guidelines for all 5G deployment options will be provided in the future.

GSMA says “5G Stand Alone to Become Reality“:

“The deployment of fully virtualized networks using 5G Stand Alone Cores, thereby facilitating Edge Computing and Network Slicing, will enable enterprises and governments to reap the many benefits from high throughput, ultra-low latency and IoT to improve productivity and enhance services to their customers,” said Alex Sinclair, Chief Technology Officer, GSMA.

………………………………………………………………………………………………………………..

Other Voices on 5G Core Deployments:

1. From Rakuten CTO Tareq Amin via email to this author:

– Containerization/Cloud native 5G Core from Rakuten-NEC:

3GPP specification requires cloud native architecture as the general concept like distributed, stateless, and scalable. However, an explicit reference model is out of scope for 3GPP specification (TS 23.501). Therefore NEC 5GC cloud native architecture is based on 3GPP “openness” concept as well as ETSI NFV treats “container” and “cloud native,” which NEC is also actively investigating to apply its product.

2. Alex Quach, VP of Intel’s Data Platforms Group, said most operators around the world are still leveraging a 4G core network. “The way different service providers implement their 5G core is going to vary,” said Quach. “Every service provider has unique circumstances. The transition to a new 5G core is going to be different for every operator.”

4. Asked if SK Telecom has now completed its 5G Standalone core network, the South Korean carrier was vague in an email reply to FierceWireless. “To commercialize standalone 5G service in Korea, we are currently making diverse R&D efforts including conducting tests in both lab and commercial environment. Our latest achievements include the world’s first standalone (SA) 5G data session on our multi-vendor commercial 5G network.

……………………………………………………………………………………………………………………………

Other References:

https://www.gsma.com/futurenetworks/resources/5g-implementation-guidelines-sa-option-2-2/

3GPP Rel 16 5G Core/Architecture specs:

- TS 23.501 5G Systems Architecture, with annexes which describe 5G core deployment scenarios:

https://www.3gpp.org/ftp/

- TS 23.502 [3] contains the stage 2 procedures and flows for 5G System

https://www.3gpp.org/ftp/

- TS 23.503 [45] contains the stage 2 Policy Control and Charging architecture for 5G System

https://www.3gpp.org/ftp/

Ting Mobile Acquired by DISH; Tucows Enables Mobile Competition Globally

Dish Network has acquired the assets of MVNO Ting Mobile, including its customer relationships, from Tucows, for an undisclosed amount. Under the deal, most Ting Mobile customers across the US will become Dish customers from August. The customers will be able to access the new T-Mobile US network, continue using their own phones and keep their rates and customer experience, Dish said. Tucows remains the owner of the Ting Mobile tech stack.

The deal follows Dish’s recent entry on the mobile market through the acquisition of Sprint’s prepaid brand Boost Mobile. Started eight years ago, Ting also focuses on the prepaid market, targeting cost-conscious mobile users. Ting said it expects the deal to help Dish “disrupt the retail wireless market and become a major competitor in the US mobile industry.”

Here’s what the news means for Ting Mobile customers:

· No data migration, service interruption or billing changes

· The same great customer service with the same Ting Mobile team managing the service/running the business

· A renewed ability for Ting Mobile to innovate on price, staying true to its roots

John Swieringa, Group President, Retail Wireless and DISH COO:

“Today, we welcome Ting Mobile customers to DISH. Ting Mobile is a great brand that stands for better value in wireless, and we are eager to begin delivering our award-winning customer service to Ting subscribers. Our agreement with Tucows will accelerate our digital and operational capabilities in wireless. Elliot and his team have a strong track record as entrepreneurs and innovators, and we are excited to partner with them on our wireless venture.”

……………………………………………………………………………………………………………………………………………..

![]()

Tucows has separately launched Mobile Services Enabler (MSE) services, with Dish as its first customer. Tucows will going forward focus on growing its MSE business, delivering a wide range of functions such as billing, activation, provisioning, and funnel marketing to mobile providers. Tucows has more than 24 million domain names under management on its platform through a global reseller network of over 36,000 web hosts and ISPs.

References:

Gartner: Market Guide for Small Cells- 5G, virtualization, disaggregation and Open RAN

Introduction:

Small cells are increasingly used to boost network densification and expand coverage for both private and public networks. They will be increasingly important in the deployment of 5G mmWave networks because of the very short propagation distances which require many small cells for adequate coverage in a given geographical area.

5G small cell market is gaining momentum due to the higher bands like mmWave limitation, in-depth in-building coverage requirement and strategic area densification. However, despite the hype surrounding 5G, 3G/4G deployments are expected to remain the dominant technology in terms of volume shipments until 2022 when 5G small cell deployment will overtake 3G/4G. Therefore, because small cell densification is moving forward, integrated small cell platforms supporting both 5G and 4G radio are essential for the next five years.

Small cells deployed in strategic areas have also accelerated the new virtualized and disaggregated architecture adoption, aiming for greater cost-efficiency and flexibility. Together with edge computing, they are enablers for enterprise digital services such as manufacturing applications, smart harbor/terminal, local contextual applications and IoT services.

Definition of Small Cells:

-

Femtocells

-

Picocells

-

Carrier-grade Wi-Fi

Gartner’s Key Findings:

-

The small cell solution is shifting from delivering in-build coverage to enable large-scale network densification. Increasing 5G and private network deployments further accelerate the trend.

-

In the small cell market, variety and diversity are replacing uniformity. Introduction of new spectrums, types of cells and architectures, vertical industries use cases, and business models like neutral host act as accelerators in this respect.

-

In addition, diversity increases the cost and complexity of small cell deployment and management, not just access points but also potentially edge computing, localized core and distributed radio units.

-

Traditional proprietary small cell systems are challenged by disaggregated, virtualized architecture. Communications service providers (CSPs) are looking for a more flexible, multivendor, cost-effective solution through breaking apart basebands and radio heads, and virtualizing some or all of the baseband functions in software.

Gartner’s Recommendations for Small Cell Deployment:

-

Build your small cell deployment strategy beyond coverage through prioritized investment in network densification and related digital services. Include 5G small cell and private networking requirements in your product plans.

-

Address diversity challenges through a multivendor approach. There is no one size fits all in the future small cell market, and a scenario-oriented product evaluations process needs to be implemented.

-

Reduce complexity and improve cost-efficiency through prioritizing the deployment feasibility as well as operation intelligence and automation.

-

Work closely with emerging suppliers and establish an objective and structured process to thoroughly evaluate and develop quick prototypes using disaggregated and virtualized architectures.

Small Cells Will Be at the Forefront of Virtualization and Open RAN:

The economic success of 5G is reliant on interoperable multi-vendor networks, which require open interfaces at both the silicon and network levels. Therefore, many CSPs are continually exploring the possibility of moving away from the proprietary hardware to more modern open and interoperable systems.

To support these, CSPs will need to adopt new network topologies such as cloud-RAN, virtualized RAN (vRAN) or open RAN (ORAN), together with integrated edge compute.The key to the open network lies in disaggregation — separating the key elements such as centralized units (CUs) and distributed units (DUs) — and the open reconfiguration — combining components from any suppliers because they are all interconnected in the same way.

For 5G, those central processes will usually be virtualized (run as software on off-the-shelf servers).The move to open network has been more advanced in small cell layer than macro network, and several suppliers already offer architectures in which a number of small cells are clustered around a centralized, virtualized controller. But there are two potential barriers to achieving a real multivendor environment: the need to be in agreement on where the network should be split between the central and the local elements and the need to be a single common interface between the elements in each preferred split.

Split RAN/SC architectures have multiple options, as identified by 3GPP. Of these, 3GPP has focused on Option-2 (RLC-PDCP), ORAN on Option-7.2 (PHY-PHY) and Small Cell Forum (SCF) on Option-6 (PHY-MAC). SCF will develop a 5G version of its networked FAPI spec, which will enable a split MAC and PHY in a disaggregated small cell network, supporting the 3GPP Option-6 split over Ethernet fronthaul and targeting, in particular, cost-effective indoor scenarios. SCF’s work on open interfaces such as nFAPI will play an important role in the market, alongside the work of partners such as O-RAN Alliance and Telecom Infra Project.

Many CSPs expect to take their first steps in their small cell layer, providing valuable experience of how to manage and orchestrate a network in which multiple radio units share common baseband functions, some of them deployed on cloud infrastructure. While there are still challenges in this domain, the disaggregation and virtualized architecture reduce the technology barrier to market and introduce new players into the market including software players as well as OEMs and ODMs.

……………………………………………………………………………………………………………………………………………………….

Small Cell Hardware and Software Vendors:

The table below may be used as a quick reference guide to representative vendors and their 5G small cell solutions. It includes the major vendors who have a long history providing small cell, DAS solutions and also some new emerging vendors who are providing software-based small cell solutions.

Table of Small Cell Vendors:

|

Small Cell Software

|

|

|

Air5G

|

|

|

Virtualized RAN Software

|

|

|

M-RAN Virtual Small Cell

|

|

|

5G Open Platform Small Cell

|

|

|

ONECELL

|

|

|

Enterprise Radio Access Network (E-RAN)

|

|

|

Radio Dot System, Micro Radio, Lightpole Site

|

|

|

LampSite Family, BookRRU, Easy Macro

|

|

|

Viper Platform

|

|

|

Massive MIMO AAS Radio Unit

|

|

|

Flexi Zone, AirScale Indoor Radio system (ASiR), AirScale Micro Remote Radio Head (mRRH), AirScale mmWave Radio (ASMR), Smart Node Femtocells

|

|

|

CellEngine

|

|

|

Samsung 5G Small Cell

|

|

|

Qcell, 5G iMicro, 5G Pad RRU

|

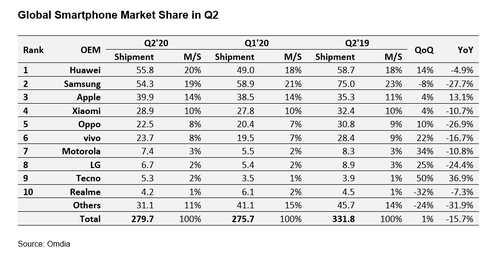

UPDATED: Huawei now #1 global smartphone vendor

Despite the severe U.S. restrictions on Huawei, the company has succeeded in taking the top spot in the global smartphone market, according to figures from Canalys. The market research firm estimates Huawei shipped more smartphones worldwide than any other vendor for the first time in Q2 2020, marking the first quarter in nine years that a company other than Samsung or Apple led the market.

Note, however, that global smartphone sales DECLINED in the second quarter. Huawei shipped an estimated 55.8 million devices in the quarter, down 5 percent year on year. Samsung came second with 53.7 million smartphones, down 30 percent from a year earlier.

Huawei’s resilience was due to its strong position in China, where its shipments rose 8 percent in Q2. This offset an estimated 27 percent fall in its shipments abroad. Canalys estimates over 70 percent of Huawei’s smartphone sales are now in mainland China. That helps explains why the company can be so successful in selling smartphones, despite not being able to use licensed Google Android and associated apps on its latest flagship devices (that’s because Huawei was placed on the U.S. Entity list last year).

Canalys said the situation would likely not have happened without the Covid-19 pandemic. Huawei profited from the strong recovery in the Chinese economy, while Samsung has a very small presence in China, with less than 1 percent market share, and suffered from the restrictions in key markets such as the US, India, Brazil and Europe.

“This is a remarkable result that few people would have predicted a year ago,” said Canalys Senior Analyst Ben Stanton. “If it wasn’t for COVID-19, it wouldn’t have happened. Huawei has taken full advantage of the Chinese economic recovery to reignite its smartphone business. Samsung has a very small presence in China, with less than 1% market share, and has seen its core markets, such as Brazil, India, the United States and Europe, ravaged by outbreaks and subsequent lockdowns.”

“Taking first place is very important for Huawei,” said Canalys Analyst Mo Jia. “It is desperate to showcase its brand strength to domestic consumers, component suppliers and developers. It needs to convince them to invest, and will broadcast the message of its success far and wide in the coming months. But it will be hard for Huawei to maintain its lead in the long term. Its major channel partners in key regions, such as Europe, are increasingly wary of ranging Huawei devices, taking on fewer models, and bringing in new brands to reduce risk. Strength in China alone will not be enough to sustain Huawei at the top once the global economy starts to recover.”

As a result, it will be hard for Huawei to maintain its lead in the long term. Its major channel partners in key regions such as Europe are increasingly wary of stocking Huawei devices, taking on fewer models and bringing in new brands to reduce risk, as per the above Canalys quote from analyst Mo Jia.

Separately, Gartner estimates that 10% of smartphone shipments, or about 220 million units in 2020, will have 5G capability, but they’ll work on “5G” networks with a LTE core (5G NSA).

…………………………………………………………………………………………………………………………………

Addendum:

Huawei’s just announced global licensing agreement with Qualcomm grants Huawei back rights to some of the San Diego-based company’s patents effective Jan. 1, 2020. It remains to be seen if Huawei will design smartphone components that use those patents in their next generation of 5G endpoint devices.

………………………………………………………………………………………………………………………………….

References:

https://www.canalys.com/newsroom/Canalys-huawei-samsung-worldwide-smartphone-market-q2-2020

………………………………………………………………………………………………………………………………………

Update- August 3, 2020:

According to market research firm Omdia, overall Q2-2020 smartphone shipment volume was down a hefty 15.7%, year-on-year, to 229.7 million units.

Samsung will certainly hope there are better times ahead. Omdia figures show the South Korean behemoth lost its #1 position in Q2, dislodged by Huawei. Samsung’s Q2 shipments plummeted nearly 28%, year-on-year, to 54.3 million.

Many of Samsung’s most important markets, were significantly impacted by COVID-19, especially emerging markets, which apparently accounted for more than 70% of Samsung’s overall shipments in 2019.

For its part, Samsung is hopeful of a Q3 smartphone recovery, helped by the launch of new flagship models, including the Galaxy Note and a new foldable phone.

Huawei, helped by a resurgent domestic market in China, snagged a 20% global smartphone share during Q2 (55.8 million units), up from an 18% market share the previous quarter. Year-on-year, Huawei’s Q2 shipment units were down a comparatively modest 4.9%.

Apple was one of the few OEMs to increase Q2 shipment volumes, year-on-year (up 13.1%, to 39.9 million units). The iPhone SE, a model with mid-range pricing, coupled with the iPhone 11, helped Apple expand its unit shipments, and cement its third-spot position with a market share of 14% (up from 11% in Q2 2019).

“With the launch of the iPhone SE in April, Apple has released a long-desired product, with an attractive price,” said Jusy Hong, director of smartphone research at Omdia.

“For existing iPhone users who needed to upgrade their smartphones in the second quarter, the new SE represented an affordable option that does not require a large downpayment or high monthly repayment rates,” added Hong.

Reference:

https://www.lightreading.com/huawei-apple-buck-q2-smartphone-trends—report/d/d-id/762886?

Point Topic Analysis of Fixed Broadband Tariffs from 300 Operators in 90 Countries

|

|

|

|

|

TSDSI’s 5G Radio Interface spec advances to final step of IMT-2020.SPECS standard

Telecommunications Standards Development Society of India (TSDSI)’s 5G Radio Interface Technology (RIT) has met step 7 of an 8 step process of ITU-R WP5D, thereby paving the way for its inclusion in the IMT-2020.SPECS. That impressive accomplishment was achieved at the ITU-R WP5D virtual meeting #35e which concluded on July 9, 2020. From the WP 5D Technology WG meeting report: “The RIT proposed in IMT-2020/19(Rev.1) (TSDSI) also passed Step 7 as “TSDSI RIT.”

As a penultimate step, the description of the TSDSI technology has been included in the draft IMT-2020 specification document. The TSDSI RIT is specified in Annex III. of the draft IMT-2020.SPECS standard, which is expected to be finalized at the WP5D meetings to be held in October and November 2020. Final approval is expected at the ITU-R SG 5 meeting November 23-24, 2020.

The TSDSI 5G RIT specification was described in a July 5, 2019 IEEE Techblog post. The ITU-R had earlier adopted the Low-Mobility-Large-Cell (LMLC) use case proposed by TSDSI as a mandatory 5G requirement in 2017. This test case addresses the problem of rural coverage by mandating large cell sizes in a rural terrain and scattered areas in developing as well as developed countries. Several countries supported this as they saw a similar need in their jurisdictions as well.

LMLC fulfills the requirements of affordable connectivity in rural, remote and sparsely populated areas. Enhanced cell coverage enabled by this spec, will be of great value in countries and regions that rely heavily on mobile technologies for connectivity but cannot afford dense deployment of base stations due to lack of deep fiber penetration, poor economics and challenges of geographical terrain.

Photo Credit: TSDSI

TSDSI successfully introduced an indigenously developed 5G candidate Radio Interface Technology (RIT), compatible with 3GPP’s 5G NR IMT-2020 RIT submission, at the ITU-R WP5D meeting in July, 2019 (as noted in the above referenced IEEE Techblog post). TSDI’s RIT incorporates India-specific technology enhancements that can enable larger coverage for meeting the LMLC requirements. It exploits a new transmit waveform that increases cell range developed by research institutions in India (IIT Hyderabad, CEWiT and IIT Madras) and supported by several Indian tech companies. It enables low-cost rural coverage and has additional features which enable higher spectrum efficiency and improved latency.

From TSDSI: Acceptance of TSDSI RIT as a 5G radio interface standard, a first for India, catapults India into the elite club of countries with expertise in defining global standards. It is a trailblazer that establishes India’s potential to deliver more such solutions that are appropriate to the specific requirements of the developing world and rely on indigenously developed technologies – Design Local, Deploy Global.

…………………………………………………………………………………………………………..

Addendum: Overview of TSDSI RIT

TSDSI RIT is a versatile radio interface that fulfills all the technical performance requirements of IMT 2020 across all the different test environments. This RIT focuses on connecting the next generation of devices and providing services across various sectors. In particular, this RIT focuses on:

1. Enhanced spectral efficiency and broadband access

2. Low latency communication

3. Support millions of IOT devices

4. Power efficiency

5. High speed connectivity

6. Large Coverage (in particular for Rural areas)

7. Support multiple frequency bands including mmWave spectrum

While, the current specifications provide a robust RIT, the specification also provides a framework on which future enhancements can be supported, providing a future-proof technology. In the following sections, we provide a basic description of the RIT. The complete details of the RIT can be found in the specification document IMT-2020/20 (ITU TIES account required for access).

References:

Executive Summary: IMT-2020.SPECS defined, submission status (?), and 3GPP’s 2 RIT submissions

Reliance Jio claim: Complete 5G solution from scratch with 100% home grown technologies