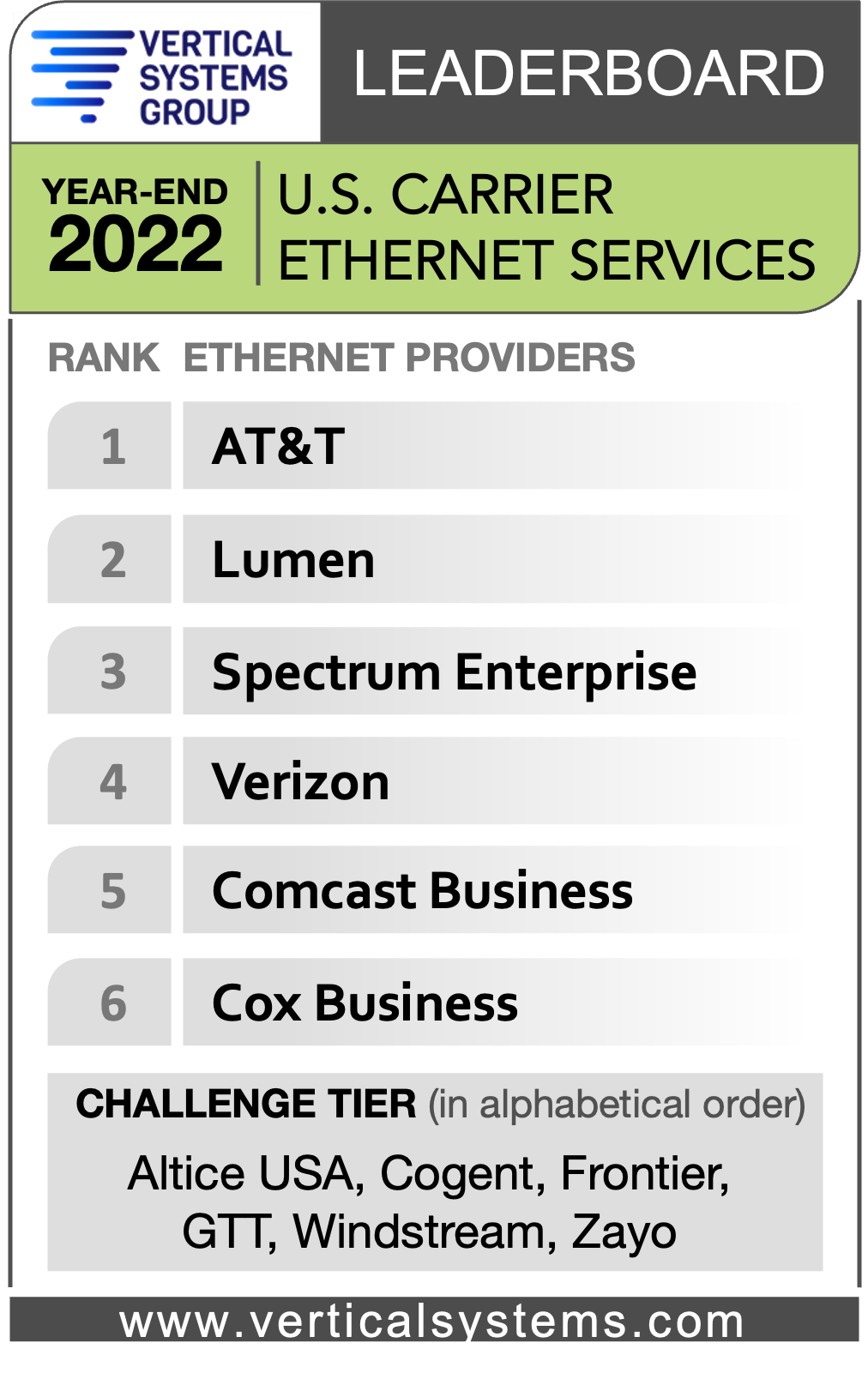

No Surprise: AT&T tops leaderboard of commercial fiber lit buildings for 7th year!

Once again, AT&T ranked #1 in the U.S. Fiber Lit Buildings Leaderboard fromVertical Systems Group (VSG) for a seventh consecutive year. The fiber focused U.S. carrier retained the top spot with the highest number of fiber lit buildings across its footprint in 2022. But there’s a whole lot more AT&T #1 rankings that the carrier has not gotten proper credit for achieving:

- AT&T also holds the #1 ranking in VSG 2022 U.S. Carrier Ethernet LEADERBOARD.

- AT&T ranked #1 for the fifth consecutive year in VSG’s year end 2022 U.S. managed carrier SD-WAN leaderboard.

–>Please see the images below, courtesy of VSG.

Major mobile operators like AT&T and Verizon are actively installing new fiber for their 5G network backhaul, which facilitates new fiber connectivity to nearby commercial sites. T-Mobile no longer has any fiber assets from their Sprint acquisition. They were sold to Cogent along with all other wireline assets in a deal that closed May 1, 2023.

Verizon, Spectrum Enterprise, Lumen, Comcast Business, Cox Business, Zayo, Crown Castle, Frontier, Brightspeed, Breezeline and Optimum followed. Those retail and wholesale fiber providers qualified for the leaderboard with 15,000 or more on-net U.S. fiber lit commercial buildings as of year-end 2022.

-

“Fiber installations at U.S. commercial sites increased in 2022, driven by escalating requirements for gigabit-speed connectivity to support cloud-based services, data centers, 5G rollouts, and other applications,” said Rosemary Cochran, principal of Vertical Systems Group. “New fiber investments in the U.S. will continue to be impacted by pending federal programs and funding initiatives. Opportunities in the commercial segment include monetizing the millions of small buildings underserved.”

U.S. Fiber Lit Buildings LEADERBOARD Highlights:

- The 2022 LEADERBOARD roster increases to twelve commercial fiber providers, up from eleven in 2021.

- AT&T retains the #1 rank on the 2022 U.S. Fiber Lit Buildings LEADERBOARD for the seventh consecutive year.

- Rankings for the top six companies on the 2022 LEADERBOARD are unchanged from 2021, which includes AT&T, Verizon, Spectrum Enterprise, Lumen, Comcast Business, and Cox Business.

- The next six LEADERBOARD provider rankings change as compared to the previous year. Zayo advances to rank seventh ahead of Crown Castle, which dips to eighth. Frontier moves up to ninth position from tenth. Brightspeed debuts in tenth position with fiber assets acquired from Lumen. Breezeline (formerly Atlantic Broadband) falls to eleventh position from ninth. Optimum (Altice USA brand) drops from eleventh to the twelfth and final position.

- The number of 2022 Challenge Tier citations expands from eight to nine with the addition of Ritter Communications.

Market Players include all other fiber providers with fewer than 5,000 U.S. commercial fiber lit buildings. The 2022 Market Players tier covers more than two hundred metro, regional and other fiber providers, including the following companies (in alphabetical order): 11:11 Systems, ACD, Alaska Communications, American Telesis, Armstrong Business Solutions, Astound Business, C Spire, Centracom, Cogent, Conterra, DFN, DQE Communications, Everstream, ExteNet Systems, Fatbeam, FiberLight, First Digital, Flo Networks, Fusion Connect, Google Fiber, GTT, Horizon, Hunter Communications, Logix Fiber Networks, LS Networks, Mediacom Business, MetroNet Business, Midco, Pilot Fiber, PS Lightwave, Shentel Business, Silver Star Telecom, Sonic Business, Sparklight Business, Syringa, T-Mobile, TDS Telecom, TPx, U.S. Signal, Vast Networks, WOW!Business, Ziply Fiber and others.

For this analysis, a fiber lit building is defined as a commercial site or data center that has on-net optical fiber connectivity to a network provider’s infrastructure, plus active service termination equipment onsite. Excluded from this analysis are standalone cell towers, small cells not located in fiber lit buildings, near net buildings, buildings classified as coiled at curb or coiled in building, HFC-connected buildings, carrier central offices, residential buildings, and private or dark fiber installations.

……………………………………………………………………………………………………………………………………..

References:

AT&T expands its fiber-optic network amid slowdown in mobile subscriber growth

https://www.verticalsystems.com/2023/02/15/2022-u-s-ethernet-leaderboard/

AT&T tops VSG’s U.S. Carrier Managed SD-WAN Leaderboard for 4th year

VSG LEADERBOARD : AT&T #1 in Fiber Lit Buildings- Year end 2020

AT&T expands its fiber-optic network amid slowdown in mobile subscriber growth

AT&T is expanding its network of fiber-optic cables to deliver fast internet speeds for customers, including those in places where it doesn’t already provide broadband. The plan will cost billions of dollars over the next several years, a price tag that the company—whose debt load outstrips its annual revenue—will not carry alone. AT&T formed a joint venture with BlackRock to fund the project and also wants to access government funding to accelerate the build-out. AT&T and BlackRock have collectively invested $1.5 billion in the venture—named Gigapower—to date, the company said.

Gigapower plans to provide a state-of-the-art fiber network to internet service providers and other businesses in parts of select metro areas throughout the country using a commercial wholesale open access platform. Both companies believe now is the time to create the United States’ largest commercial wholesale open access fiber network to bring high-speed connectivity to more Americans.

AT&T will serve as the anchor tenant of the Gigapower network, but other companies could also provide internet service over the network. That so-called open-access model has become common throughout Europe, but has yet to be widely embraced in the U.S. Gigapower recently introduced plans to build out fiber in Las Vegas, northeastern Pennsylvania and parts of Arizona, Alabama and Florida.

Doubling down on fiber optics sets AT&T on a different path than its rivals Verizon and T-Mobile US, which are relying on improved technology that beams broadband internet service from the same cellular towers that link their millions of mobile smartphone customers. AT&T is testing a similar fixed wireless access service but on a smaller scale, but executives say fiber remains the long-term focus.

AT&T updated shareholders on its vision for fiber internet and 5G cellular networks at its annual meeting, but the documentation/replay was not available at press time. AT&T spent about $24 billion on its fiber and 5G networks last year, and it forecast a similar level of spending this year. The company is confident it will get a very good return on investment (ROI).

The Dallas-based company and its peers face heightened competition in the cellphone business—their core profit engine. After the Covid-19 pandemic brought a surge in new accounts, the cellphone business has cooled, pushing companies to seek alternate paths for growth. AT&T, which has nearly 14 million consumer broadband customers, has provided internet service for years, and executives say that keeping customers plugged in requires faster connections as more data is used.

“We should be putting more fiber out faster, quicker and in more places than anybody else,” AT&T Chief Executive John Stankey said in a recent interview. “If we do that, that means our network is always going to be ahead of anybody else’s.”

Fiber-optic cables, wired directly to or near Americans’ homes, contain easy-to-upgrade glass strands that can carry much more data than radio waves. That higher capacity is crucial for video calls, streaming, videogames and other services, which use more internet data than most smartphone apps. As of last year, fiber was available at some 63 million homes, or more than half of primary residences, according to the Fiber Broadband Association.

AT&T wants its fiber network to cover more than 30 million homes and businesses within its current service area by the end of 2025. In many cases, fiber will replace internet connections over copper wirelines.

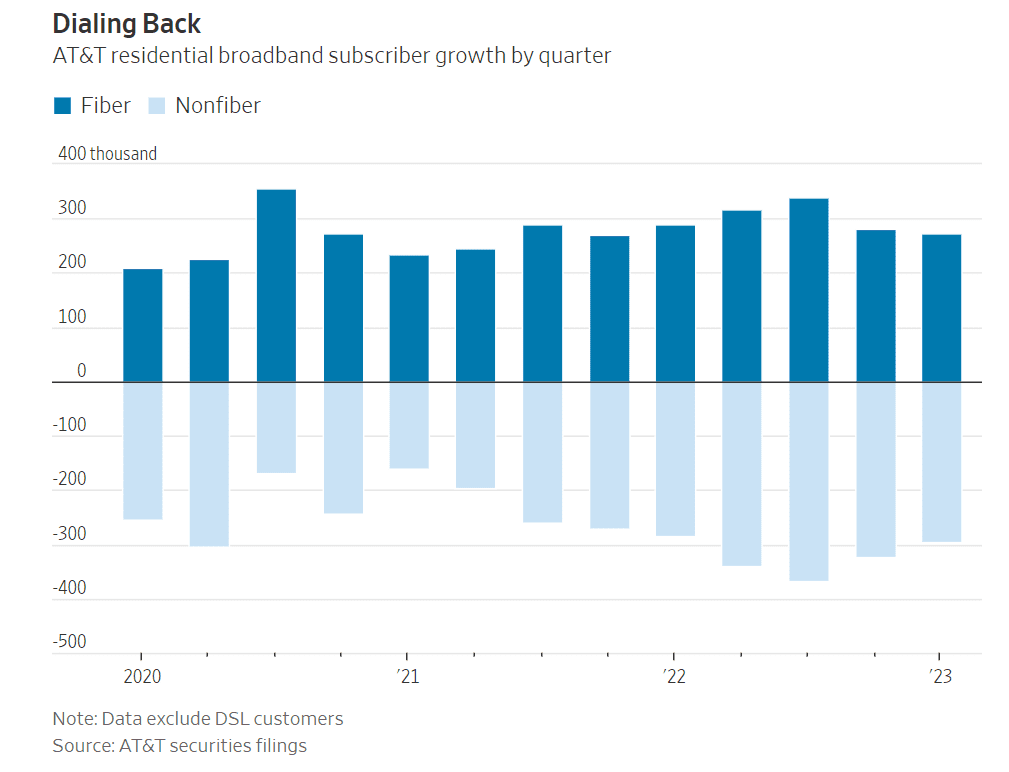

Laying the fiber is one thing, but progress in getting customer sign-ups has been slower than some analysts expected. In the first three months of the year, AT&T signed up 272,000 home fiber subscribers, a deceleration from the December quarter and the same period last year.

The results also marked the fourth straight quarter during which residential fiber sign-ups failed to offset declines in broadband customers overall. Stankey said he isn’t expecting the trend to reverse this year.

AT&T offers its fiber service at various speed tiers, starting at $55 a month for downloads up to 300 megabits a second. Prices run as high as $180 a month for 5-gigabit speeds.

In the March quarter, the average AT&T fiber internet customer paid about $66 a month. That total was up 9% from last year but still slightly less than the sums paid by customers of cable rivals Charter Communications and Comcast, according to Roger Entner, the founder of Recon Analytics.

While AT&T’s fiber build-out continues, it hopes its Internet Air service—which uses cell towers to beam broadband to homes—can stem customer defections in the short term. The service, which costs $55 a month, isn’t yet widely available, said Stankey, who took over as CEO in 2020 and unwound AT&T’s bet on entertainment.

Reuters: Telcos draft proposal to charge Big Tech for EU 5G rollout; Meta offers a rebuttal

Big tech companies accounting for more than 5% of a telecoms provider’s peak average internet traffic should help fund the rollout of 5G and broadband across Europe, according to a draft proposal by the telecoms industry. The proposal is part of feedback to the European Commission which launched a consultation into the issue in February. The deadline for responses is Friday.

Alphabet’s Google, Apple Facebook-owner Meta, Amazon, Netflix and TikTok would most likely be hit with fees, according to industry estimates. Google, Apple, Meta, Netflix, Amazon and Microsoft together account for more than half of data internet traffic.

The document, which was reviewed by Reuters and has not been published, was compiled by telecoms lobbying groups GSMA and ETNO. They represent 160 operators in Europe, including Deutsche Telekom, Orange, Telefonica and Telecom Italia. Telecom operators have lobbied for years for leading technology companies to help foot the bill for 5G and broadband roll-out, saying that they create a huge part of the region’s internet traffic. This is the first time they have tried to define a threshold for who should pay.

“We propose a clear threshold to ensure that only large traffic generators, who impact substantially on operators’ networks, fall within the scope,” the draft stated. “Large traffic generators would only be those companies that account for more than 5% of an operator’s yearly average busy hour traffic measured at the individual network level,” it said. The European Commission declined to comment.

Meta on Wednesday urged Brussels to reject any proposals to charge Big Tech for additional network costs. In a Facebook blog post, Markus Reinisch, Meta’s VP for Public Policy for Europe, described potential fees as a “private sector handout for selected telecom operators” that would disincentivize innovation and investment, and distort competition. “We urge the Commission to consider the evidence, listen to the range of organizations who have voiced concerns, and abandon these misguided proposals as quickly as possible,” he said. Here are Meta’s takeaways:

- Network fee proposals misunderstand the value that content platforms bring to the digital ecosystem.

- We support the Commission’s goal of “ensuring access to excellent connectivity for everyone,” but network fee proposals will hurt European consumers and businesses.

- We urge the Commission to consider the evidence, listen to the range of organizations who have voiced concern, and drop these proposals.

References:

Network Fee Proposals Will Ultimately Hurt European Businesses and Consumers

https://www.euractiv.com/section/5g/news/eu-telcos-call-for-big-tech-to-share-5g-network-costs/

GSMA: Europe’s 5G rollout is too slow at 6% of mobile customer base

European telcos need to address very high 5G energy consumption

Strand Consult: Market for 5G RAN in Europe: Share of Chinese and Non-Chinese Vendors in 31 European Countries

Vodafone Idea (Vi) is worth ZERO; needs additional liquidity support from lenders

While announcing its FY23 earnings, UK telecom company, Vodafone Plc said the Group’s carrying value of investment in Indian listed firm Vodafone Idea (Vi) is Zero. Also, that the Group is recording no further losses related to Vi. The troubled-laden Vi is still in need of additional liquidity and plans to raise funds going forward. In its FY23 report, Vodafone Plc said, “VIL remains in need of additional liquidity support from its lenders and intends to raise additional funding.”

Vodafone seems to be backing away from Vi. The business needs more money, that Vodafone is certainly not willing to provide, and that zero valuation indicates that it will put no more effort into saving it. There are significant uncertainties in relation to Vi’s ability to make payments in relation to any remaining liabilities covered by the mechanism and no further cash payments are considered probable from the Group as at 31 March 2023, it added.

“VIL [Vodafone Idea Ltd] remains in need of additional liquidity support from its lenders and intends to raise additional funding. There are significant uncertainties in relation to VIL’s ability to make payments in relation to any remaining liabilities covered by the mechanism and no further cash payments are considered probable from the Group as at 31 March 2023,” Vodafone said, in the notes to its consolidated financial statements for the 2023 financial year.

Furthermore, Vodafone said, “the carrying value of the Group’s investment in VIL is nil and the Group is recording no further share of losses in respect of VIL.”

It should be noted that Vi is the only Indian telco that has NOT yet deployed 5G services. Since the launch of 5G last October, Reliance Jio’s 5G services have become available in more than 400 cities and towns, while Airtel’s 5G services can be accessed in more than 500. Jio plans to provide all-India 5G coverage by December, with Airtel aiming for blanket availability by March next year.

Recently, Vodafone Idea complained to the Telecom Regulatory Authority of India (TRAI), accusing its rivals of predatory 5G pricing. Although it has been shedding customers for years, there can be little doubt that losses have accelerated since the launch of 5G. Vodafone Idea had lost about 7 million in the four months leading up to 5G’s launch in October last year. In the four months following the introduction of 5G services by Airtel and Jio, its losses soared to about 10 million.

Vodafone Idea is known to have a significant percentage of high-spending customers who have remained loyal to it. These customers typically show limited interest in lower tariffs, but many will have been drawn to 5G services available only from other telcos, with Vodafone Idea’s 5G plan nowhere close to fruition. Airtel and Jio, accordingly, are racing to build 5G networks and attract as many Vodafone Idea subscribers as possible.

………………………………………………………………………………………………………………………………………………………………………………..

When Vodafone and Idea Cellular entered into an merger agreement in 2017, the parties had agreed to a mechanism for payments between the Group and Vodafone Idea, pursuant to the difference between the crystallisation of certain identified contingent liabilitiesin relation to legal, regulatory, tax and other matters, and refunds relating to Vodafone India and Idea Cellular. Cash payments s or cash receipts relating to these matters must have been made or received by Vi before any amount becomes due from or owed to the Group.

Hence, any future future payments by the Group to VIL as a result of this agreement would only be made after satisfaction of this and other contractual conditions. Thereby, the UK-based telco said, “Vodafone Group’s potential exposure to liabilities within VIL is capped by the mechanism described above; consequently, contingent liabilities arising from litigation in India concerning operations of Vodafone India are not reported.”

Vodafone Plc’s potential exposure under this mechanism is capped at ₹64 billion n (€719 million) following payments made under this mechanism from Vodafone to VIL, in the year ended 31 March 2021, totalling ₹19 billion (€235 million).

In FY23, Vodafone Plc’s revenue increased by 0.3% to €45.7 billion driven by growth in Africa and higher equipment sales, offset by lower European service revenue and adverse exchange rate movements. While adjusted EBITDAal declined by 1.3% to €14.7 billion due to higher energy costs, and commercial underperformance in Germany.

References:

https://telecoms.com/521728/vodafone-sees-no-remaining-value-in-indian-operation/

Big 5G Conference: 6G spectrum sharing should learn from CBRS experiences

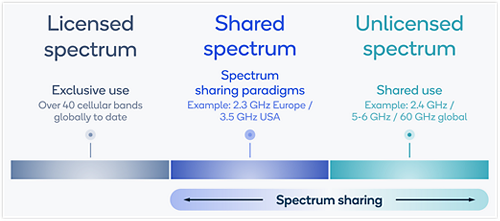

Spectrum sharing is a methodology that allows multiple wireless networks to access the same frequency band dynamically and efficiently. It can reduce the spectrum scarcity issue and enable more wireless applications and services, but also requires careful coordination and management to avoid interference and ensure fair access.

Examples of spectrum sharing techniques include Licensed Shared Access (LSA), which uses a regulatory framework to permit licensed users to share spectrum with incumbent users, Dynamic Spectrum Access (DSA), which enables wireless networks to sense and adapt to the spectrum environment, and Spectrum Aggregation, which combines multiple spectrum bands or channels into a larger bandwidth. LSA can be used by mobile operators to access spectrum that is not used by TV broadcasters, DSA can be employed by cognitive radio networks to detect and avoid channels occupied by primary users, Spectrum Aggregation can be used by 5G networks for coverage and speed.

The wireless telecom industry has to take a “concerted look at revolutionizing spectrum sharing” and to take a closer look at the lessons learned from CBRS spectrum sharing [1.], which took about a decade to be successfully implemented, according to Andrew Thiessen, chair of the spectrum working group at the Next G Alliance who was speaking at the Informa Big 5G conference panel session in Austin, TX. He opined that the industry needs to be pushing ahead with spectrum sharing technologies and techniques at speeds similar to the innovations that are being applied to smartphones.

Note 1. Citizens Broadband Radio Service (CBRS), which allows for dynamic spectrum sharing between the Department of Defense and commercial spectrum users. The DOD users have protected, prioritized use of the spectrum. When the government isn’t using the airwaves, companies and the public can gain access through a tiered licensing arrangement. This means the DOD can use the same spectrum for its critical missions while companies can use it for 5G and high-speed Internet deployment.

“Innovative spectrum sharing frameworks are key to unlocking additional bandwidth for wireless connectivity across the country,” Deputy Assistant Secretary of Commerce for Communications and Information April McClain-Delaney said. “The success and growth of the CBRS band shows the promise of dynamic spectrum sharing to make more efficient use of this finite resource.”

………………………………………………………………………………………………………………………………………………..

Joe Kochan, executive director of the National Spectrum Consortium, agreed that spectrum sharing for 6G does present challenges as it faces a wide range of commercial users, federal users and non-federal users, as well as different types of technologies, such as radar. That elicits a need for the industry to build new tools and to get more creative about how that spectrum can be shared.

The Biden administration’s National Spectrum Strategy will “lay the framework” to get everything moving, said Derek Khlopin, deputy associate administrator, spectrum planning policy, at the NTIA. “We’re tech and application-neutral. But the better we understand, the better we can plan.” he explained.

“We’ve started listening, to be frank,” Khlopin said. “But it’s not necessarily the role of the government to figure all of this out. We need help, so we’re working closely with industry, with academia and others. Spectrum sharing is here to stay between federal and non-federal users,” he added.

Khlopin was asked about NTIA’s exploration of the 7GHz band and its potential for 6G. “It’s a very complicated band,” he said. “There’s a lot there … We’re aware of the industry interest there.”

Thiessen said one challenge for 6G will be a lack of contiguous spectrum. He believes that 6G will likely be made up of a lot of pieces of spectrum, and those pieces will likely need to be targeted to specific use cases. However, that presumption is premature as neither 3GPP or ITU-R WP5D has started any serious work on defining 6G specifications. That is why all the buzz about 6G is irrelevant at this time.

References:

https://www.linkedin.com/advice/1/how-can-wireless-network-coexistence-interference

https://ntia.gov/blog/2023/innovative-spectrum-sharing-framework-connecting-americans-across-country

https://www.lightreading.com/6g/spectrum-sharing-will-be-key-to-unlocking-6g/d/d-id/784884?

Vodafone tests 5G Dynamic Spectrum Sharing (DSS) in its Dusseldorf lab

GSMA: Closing the digital divide in Central Asia and the South Caucasus

The GSMA has published a report – Closing the digital divide in Central Asia and the South Caucasus – which affirms that mobile technology is fundamental to expanding connectivity across the region, with over 40% of the population living in rural areas where mobile connectivity is the primary, and often only, form of internet access. The report assesses the state of mobile adoption and infrastructure availability in Armenia; Azerbaijan; Georgia; Kazakhstan; Kyrgyzstan; Tajikistan; Turkmenistan; and Uzbekistan.

GSMA Intelligence estimated around 45 million people across the eight countries used mobile internet (as of the date of publication). This represented a significant increase from 14.1 million recorded a decade earlier, though it still leaves around 50 million unconnected. Although lack of coverage was cited as still a challenge in parts of Central Asia, where around 10 per cent of the population in some markets lived in underserved areas, it generally noted the pace of adoption was lagging rollout.

GSMA Intelligence noted collaboration as key to addressing the digital divide in the regions, adding there is a need to “increase digital skills and literacy and improve affordability, in addition to investing in local digital ecosystems and an enabling policy environment that can accelerate growth in local content, services and applications”

The new report was launched to mark the opening of M360 Eurasia 2023, which today welcomed global leaders from the mobile ecosystem and adjacent industries for two days of learning, debate and networking at the Four Seasons Hotel in Baku, Azerbaijan.

“Since the first mobile phone call 50 years ago, our industry has evolved, adapted and advanced the world around us, serving 5.4 billion unique customers. As we enter the era of intelligent connectivity, it feels like anything is possible, but it has also never been more important for us to focus on closing the digital divide. Together we must keep working to build a firm foundation for the next generation of intelligent connectivity and ensure that no one is left behind in our global digital economy,” said Mats Granryd, Director General of the GSMA, on stage for the opening ceremony and keynote.

“I am delighted to welcome the global connectivity community to Baku for M360 Eurasia,” said H.E. Rashad Nabiyev, Minister of Digital Development and Transport for the Republic of Azerbaijan. “As we continue our digital transformation journey in Azerbaijan, we look forward to hearing leaders in mobile and technology explore the latest trends in connectivity and the importance of digital resilience.”

As of April 2023, commercial 5G services were only available in Kazakhstan, Tajikistan and Uzbekistan, though GSMA Intelligence noted activities around the latest generation of mobile technology were ramping more widely.

“Although 5G is on the horizon in several markets in Central Asia and the South Caucasus, the focus for many operators in the medium term is to expand 4G capacity in urban areas and 4G coverage to underserved areas, and accelerate uptake among consumers.”

Closing the Digital Divide in Eurasia:

M360 Eurasia comes to Baku, Azerbaijan as progress to build the digitally powered economy of the future continues in the region, driven by ambitious digital transformation initiatives and a general trend towards greater digitisation.

The new report from the GSMA, which evaluates the connectivity landscape of eight countries1 in Central Asia and the South Caucasus, outlines the digital divide and spotlights ongoing initiatives in the region to close it with recommended action points for stakeholders to accelerate progress.

Other key findings from the report include:

- While 45 million people are now using mobile internet across the eight countries evaluated, a digital divide remains with nearly 50 million unconnected people at risk of missing out on the benefits of mobile internet.

- The adoption of mobile internet services has not kept pace with the expansion of network coverage, resulting in a significant usage gap2. As of 2022, the regional usage gap was widest in Georgia (52%) and Turkmenistan (50%), and lowest in Armenia (33%) and Azerbaijan (31%) versus a global average of 41%.

- While 4G is now the dominant technology in Azerbaijan (59%) and Kazakhstan (62%), 3G still accounts for over 40% of total connections across the region versus a global average of 17%.

- The region’s 5G uptake is still in its infancy with commercial 5G services only available in Kazakhstan, Tajikistan and Uzbekistan as of April 2023. The medium-term focus for operators in the region is to expand 4G capacity in urban areas and 4G coverage to underserved areas.

- While 4G coverage has reached 83% of the population in Central Asia, extending coverage to the last frontier can be costly and complex. This has led to operators increasingly turning to alternate technologies, such as satellite backhaul, and innovative partnerships as a means of closing the digital divide.

- Closing the region’s digital divide will require substantial collaborative actions. To this end, governments and policymakers should implement measures that can attract investment in the deployment of network infrastructure in underserved areas; create innovative digital services to stimulate demand; and address the various non-infrastructure barriers to mobile internet adoption.

M360 Series: Regional focus, global impact:

M360 Eurasia marks this year’s first iteration of the M360 Series. Presented by the GSMA, M360 is a series of global events that unifies the regional mobile ecosystem to discover, develop and deliver innovation that is the foundation to positive business environments and societal change.

The events facilitate inspirational keynotes, engaging panel discussions and insightful case studies across mobile technology and adjacent industry verticals.

To download the report, please click here: Closing the digital divide in Central Asia and the South Caucasus

About GSMA:

The GSMA is a global organisation unifying the mobile ecosystem to discover, develop and deliver innovation foundational to positive business environments and societal change. Our vision is to unlock the full power of connectivity so that people, industry, and society thrive. Representing mobile operators and organisations across the mobile ecosystem and adjacent industries, the GSMA delivers for its members across three broad pillars: Connectivity for Good, Industry Services and Solutions, and Outreach. This activity includes advancing policy, tackling today’s biggest societal challenges, underpinning the technology and interoperability that make mobile work, and providing the world’s largest platform to convene the mobile ecosystem at the MWC and M360 series of events.

References:

GSMA REPORT HIGHLIGHTS PIVOTAL ROLE OF MOBILE TECHNOLOGY IN EXPANDING CONNECTIVITY IN EURASIA REGION

EU wants to build a subsea internet cable in the Black Sea

Since 2021, the EU and the nation of Georgia (previously in the USSR) have highlighted a need to install an underwater (subsea) internet cable through the Black Sea to improve the connectivity between Georgia and other European countries.

After the start of war in Ukraine, the project has garnered increased attention as countries in the South Caucasus region have been working to decrease their reliance on Russian resources—a trend that goes for energy as well as communications infrastructure. Internet cables have been under scrutiny because they could be tapped into by hackers or governments for spying.

“Concerns around intentional sabotage of undersea cables and other maritime infrastructure have also grown since multiple explosions on the Nord Stream gas pipelines last September, which media reports recently linked to Russian vessels,” the Financial Times reported. The proposed cable, which will cross international water through the Black Sea, will be 1,100 kilometers, or 684 miles long, and will link the Caucasus nations to EU member states. It’s estimated to cost €45 million (approximately $49 million).

“Russia is one of multiple routes through which data packages move between Asia and Europe and is integral to connectivity in some parts of Asia and the Caucasus, which has sparked concern from some politicians about an over-reliance on the nation for connectivity,” The Financial Times reported.

Across the dark depths of the globe’s oceans there are 552 cables that are “active and planned,” according to TeleGeography. All together, they may measure nearly 870,000 miles long, the company estimates. Take a look at a map showing existing cables, including in the Black Sea area, and here’s a bit more about how they work.

The Black Sea cable is just one project in the European Commission’s infrastructure-related Global Gateway Initiative. According to the European Commission’s website, “the new cable will be essential to accelerate the digital transformation of the region and increase its resilience by reducing its dependency on terrestrial fibre-optic connectivity transiting via Russia. In 2023, the European Investment Bank is planning to submit a proposal for a €20 million investment grant to support this project.”

Currently, the project is still in the feasibility testing stage. While the general route and the locations for the converter stations have already been selected, it will have to go through geotechnical and geophysical studies before formal construction can go forward.

References:

Why the EU wants to build an underwater cable in the Black Sea

China seeks to control Asian subsea cable systems; SJC2 delayed, Apricot and Echo avoid South China Sea

SEACOM telecom services now on Equiano subsea cable surrounding Africa

Bharti Airtel and Meta extend 2Africa Pearls subsea cable system to India

Google’s Equiano subsea cable lands in Namibia en route to Cape Town, South Africa

Google’s Topaz subsea cable to link Canada and Japan

Altice Portugal MEO signs landing party agreement for Medusa subsea cable in Lisbon

2Africa subsea cable system adds 4 new branches

Echo and Bifrost: Facebook’s new subsea cables between Asia-Pacific and North America

Banned in the U.S., China Telecom Americas launches eSurfing Cloud services in Brazil

China Telecom do Brasil (“CTB”) today announced the launch of eSurfing Cloud services in Brazil. Through on-demand purchases that aim to simplify the process for more targeted service, the new offering provides businesses with the flexibility of accessing public and private cloud services, combined with the security and control of private cloud.

CTB’s eSurfing Cloud services enable enterprises in Brazil to take advantage of the latest cloud technologies, with the added benefit of local support and expertise. With this new offering, businesses in Brazil can optimize their cloud environments, reduce costs, and improve efficiency, all while maintaining high levels of security and compliance. The eSurfing Cloud services in São Paulo will allow customers to connect on a global multi-cloud network of more than nine public cloud nodes, 30 proprietary edge cloud nodes, and more than 200 CDN nodes.

“We are excited to bring our world-class cloud solutions to businesses in Brazil,” said Luis Fiallo, the officer of China Telecom do Brasil. “Our eSurfing Cloud services deliver flexible and scalable solutions that can meet the unique evolving needs of businesses in the region. The launch of this new offering is our continued commitment to helping our customers achieve their business goals and succeed in today’s digital landscape.”

Brazil is one of the most active cloud markets in Latin America, with high demand for the critical services that connect LATAM to the global market. Cloud adoption in Brazil has increased nearly 40% since 2019 and is expected to grow nearly 19% by 2033. While eSurfing Cloud provides customers with access to public cloud, private cloud, hybrid cloud, and edge cloud, its advantages in cloud-network integration, security, and extensive customization make it the choice digital transformation accelerator for businesses of any size.

About China Telecom do Brasil:

China Telecom do Brasil is the largest subsidiary of China Telecom Americas in Latin America and a leading provider of Internet and cloud computing services in Brazil. With a focus on customer satisfaction, the company delivers reliable, scalable, and secure solutions that enable businesses to connect their networks within Brazil and internationally, while thriving in today’s digital landscape. The company is the largest Chinese Internet provider in Brazil with network POPs and backbone connecting the state of Sao Paulo, State of Rio De Janeiro, State of Parana and State of Rio Grande do Sul to the China Telecom global network.

SOURCE: China Telecom Americas

………………………………………………………………………………………………………………………………………

China Telecom still banned in U.S.:

The Federal Communications Commission (FCC) has raised mounting concerns about Chinese telecom companies in recent years which had won permission to operate in the United States decades ago. On October 26, 2021 the FCC revoked and terminated China Telecom America’s authority to provide Telecom Services in America. The FCC said that China Telecom (Americas) “is subject to exploitation, influence and control by the Chinese government.”

On December 20, 2022, a U.S. federal appeals court rejected China Telecom Corp’s challenge to the order withdrawing the company’s authority to provide services in the United States.

…………………………………………………………………………………………………………………………………………

References:

https://www.fcc.gov/document/fcc-revokes-china-telecom-americas-telecom-services-authority

Analysis and Implications: China’s 3 Major Telecom Operators to be delisted by NYSE

Deutsche Telekom’s fiber optic expansion in 140 of the 179 municipalities within the Gigabit region of Stuttgart

Deutsche Telekom said it has deployed its fiber optic network in more than 140 of the 179 municipalities covered by its agreement with the “gigabit region” of Stuttgart. The German network operator has developed its network in the districts of Boeblingen, Esslingen, Goeppingen, Ludwigsburg and Rems-Murr districts.With ongoing expansion efforts at over 58 construction sites, the company is making significant progress, particularly in nine districts in Stuttgart, according to the statement from the company.

Since 2019, Telekom has accounted for more than 90 percent of the growth in fiber optic infrastructure. As the sole company expanding into both rural and urban areas, Telekom has established itself as a reliable partner, delivering on all construction projects and cooperation agreements, according to the broadband officer of the region and managing director of Gigabit Region Stuttgart (GRS).

In Ludwigsburg and Esslingen alone, Telekom has already been awarded contracts for 76 funding projects. The recent collaboration with Stadtwerke Nuertingen serves as a prime example of Telekom’s cooperative efforts.

Currently, approximately 30,000 households in expansion areas under this partnership can already subscribe to Telekom’s fibre optic connections. The long-term goal is to enable 185,000 households within cooperative areas with municipal utilities to choose their preferred communication provider for fibre optic connections by 2030.

The combined efforts of self-expansion, collaborations, and subsidized projects have granted around 335,000 households throughout the region access to the fibre optic network, Telekom said.

The core focus of the gigabit project is to expand the ultra-fast fiber optic network through strategic partnerships. Currently, 177 municipalities, including Stuttgart and the neighbouring districts of Boeblingen, Esslingen, Goeppingen, Ludwigsburg, and Rems-Murr, are participating in the expansion program.

The project aims to provide 50 percent of households, all companies, and schools with fiber optic connectivity by 2025. By 2030, the target is to achieve 90 percent household coverage. With a population of approximately 2.8 million in the conurbation, other companies in the Stuttgart region are also actively involved in fiber optic expansion initiatives said Telekom.

Telekom includes provisions for rapidly expanding the performance of its 5G network. Presently, almost 95 percent of households can already access 5G in Telekom’s mobile network, while over 99 percent of the population can utilize 4G/LTE connectivity.

Significance of DT Tower Sales:

Deutsche Telekom said proceeds from the sale of its tower business helped reduce net debt excluding leases by over 10 billion euros compared with the end of 2022, to 93 billion euros. The transaction was also the main factor behind the near quadrupling of net profit, to 15.4 billion euros, compared with the same period last year, the company said.

Deutsche Telekom had agreed in July 2022 to sell 51% of its tower business in Germany and Austria to a consortium of Canada’s Brookfield and U.S. private equity firm DigitalBridge after they made a surprise last-minute bid that valued the unit at 17.5 billion euros ($17.5 billion).

References:

NTT pins growth on IOWN (Innovative Optical and Wireless Network)

NTT Corp has unveiled a plan to invest JPY8 trillion ($59 billion) in growth businesses over the next five years. The core of its new growth will be its self-developed IOWN concept. The Japanese telecom giant is aiming to lift EBITDA (earnings before interest, taxes, depreciation and amortization) from JPY3.3 trillion ($24.3 billion) today to JPY4.0 trillion ($29.5 billion) in 2027.

The IOWN (Innovative Optical and Wireless Network) is an initiative for networks and information processing infrastructure including terminals that can provide high-speed, high-capacity communication utilizing innovative technology focused on optics, as well as tremendous computational resources. This is done in order to overcome the limitations of existing infrastructure with innovative technologies, optimize the individual with the whole based on all available information, and create a rich society that is tolerant of diversity. We have started R&D with the aim of finalizing specifications in 2024 and realizing the initiative in 2030.

IOWN consists of the following three major technical fields:

- APN: All-Photonics Network

Major improvement to information processing infrastructure potential - DTC: Digital Twin Computing

A new world of services and applications - CF: Cognitive Foundation®

Optimal harmonization of all ICT resources

A key concept is Photonic Disaggregated Computing – a new computing architecture that makes the shift from traditional server box-oriented computing infrastructure to boxless computing infrastructure, building on photonics-based data transmission paths.

By enabling each module, such as memory and AI computing devices, with photonic I / O (Input / Output) and connecting modules with a high-capacity and high-speed photonic data network, photonic disaggregated computing achieves highly flexible computing infrastructure. By dynamically combining modules according to computing demand, it also dramatically improves performance. Using NTT’s optoelectronic integration technology, the inter-package and inter-chip data transmission process can be replaced with photonics even inside of modules, while also dramatically improving energy efficiency.

By including data-centric computing technology and photonic disaggregated computing technology into the IOWN concept, we will accelerate creation of a natural cyber space in the era of the Smart World.

For example, AI control done by transmitting a large volume of data with low latency can realize system control that goes beyond the limits of human perception and reflexes. By coordinating a vast number of AI systems, NTT says they can realize overall optimization on the scale of society, as well as prediction of the future through large-scale simulations.

References:

https://group.ntt/en/ir/library/presentation/2022/230512e_2.pdf