Author: Alan Weissberger

GSA: 5G Device Ecosystem June 2023 Summary

Highlights:

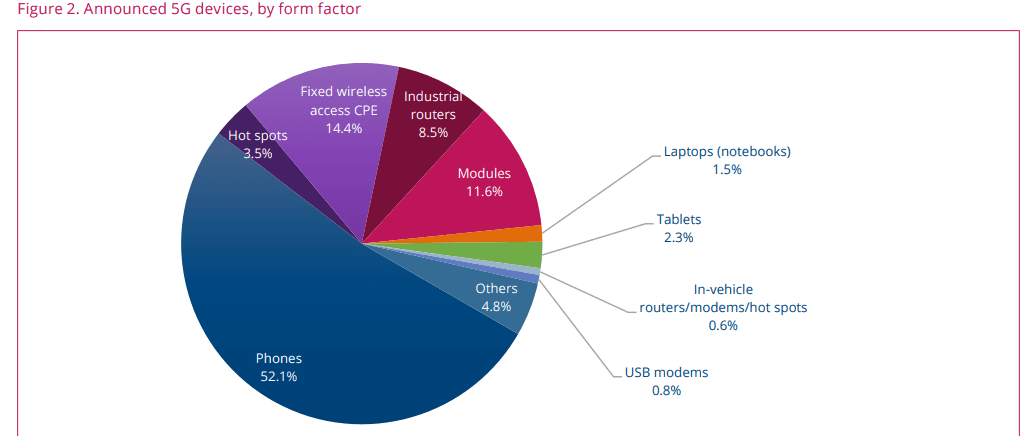

- The number of announced 5G devices rose by 1.2% between April and May 2023, reaching a total of 1,965 devices. Of these, 1,579 are understood to be commercially available, representing 80.4% of all announced 5G devices. This is an increase of 48.7% in the number of commercial 5G devices since the end of May 2022. Highlights this edition include:

- 233 manufacturers with announced available or forthcoming 5G devices

1,965 announced devices, of which at least 1,579 are understood to be commercially available

Not all devices are available immediately and specification details remain limited for some. We expect devices to continue to become more widely available and for more information about announced devices to emerge as they reach the market. - The number of commercially available devices has been growing steadily since the start of the year and should continue in this manner. GSA will continue to track and report on 5G device launches during the coming year. Its GAMBoD database contains important details about device form factors, features and support for spectrum bands. Summary statistics are released in this regular monthly publication.

By the end of May 2023, GSA had identified:

• 26 announced form factors

• 233 manufacturers with announced available or forthcoming 5G devices

• 1,965 announced devices, including regional variants, but excluding operator-branded devices that are essentially rebadged

versions of other phones. Of these, at least 1,579 are understood to be commercially available:

• 1,024 phones (up 15 from April 2023), at least 942 of which are now commercially available (up 14 from April 2023)

• 283 fixed wireless access customer-premises equipment (CPE) devices for indoor and outdoor uses, at least 183 of which are

now commercially available

• 227 modules

• 167 industrial or enterprise routers, gateways or modems

• 68 battery-operated hot spots

• 46 tablets

• 29 laptops or notebooks

• 12 in-vehicle routers, modems or hot spots

• 15 USB terminals, dongles or modems

• 94 other devices, including drones, head-mounted displays, robots, TVs, cameras, femtocells/small cells, repeaters, vehicle

on-board units, keypads, a snap-on dongle/adapter, a switch, a vending machine and an encoder

• 1,063 announced devices with declared support for 5G standalone in sub-6 GHz bands, 864 of which are commercially available.

- Not all devices are available immediately and specification details remain limited for some. We expect devices to continue to become more widely available and for more information about announced devices to emerge as they reach the market.

- The number of commercially available devices has been growing steadily since the start of the year and should continue in this manner.

- GSA will continue to track and report on 5G device launches during the coming year. Its GAMBoD database contains important details about device form factors, features and support for spectrum bands. Summary statistics are released in this regular monthly publication.

References:

GSA FWA Report: 38 commercially launched 5G FWA networks in the EU; Speeds revealed

GSA: 200 global operators offer 5G services; only 20 (Dell’Oro says 13) have deployed 5G SA core network

GSA: 5G Market Snapshot – 5G networks, 5G devices, 5G SA status

Draft new ITU-R recommendation (not yet approved): M.[IMT.FRAMEWORK FOR 2030 AND BEYOND]

Introduction:

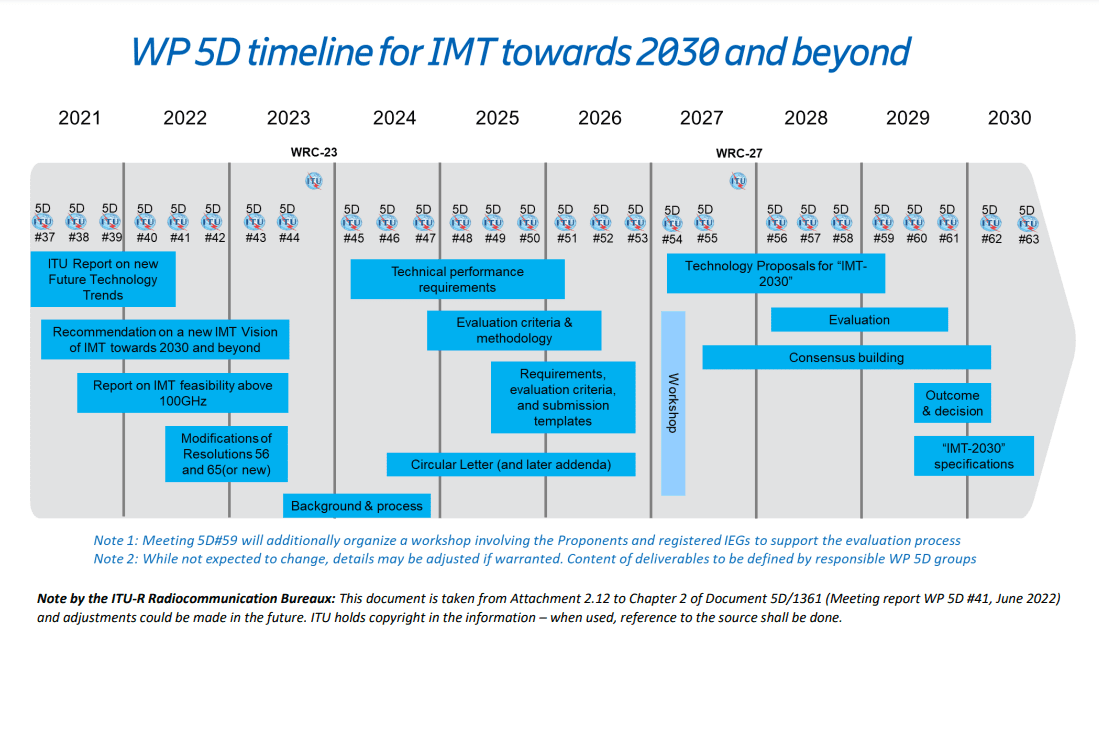

At its 44th meeting in June 2023, ITU-R WP 5D finalized development of a draft new Recommendation ITU-R M.[IMT.FRAMEWORK FOR 2030 AND BEYOND] on “Framework and overall objectives of the future development of IMT for 2030 and beyond.” This draft recommendation is expected to be approved by year end 2023.

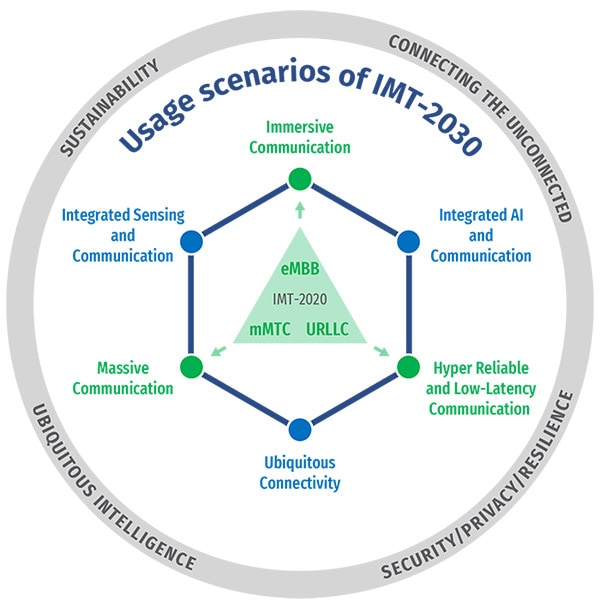

With the evolution of information and communications technologies, IMT-2030 is expected to support enriched and immersive experience, enhanced ubiquitous coverage, and enable new forms of collaboration. Furthermore, IMT-2030 is envisaged to support expanded and new usage scenarios compared to those of IMT-2020, while providing enhanced and new capabilities.

The objective of this Recommendation is to provide guidelines on the framework and overall objectives of the future development of IMT-2030 (aka “6G”).

In the next three years starting from 2024, ITU-R WP 5D will focus on the study of detailed technical performance requirements and the evaluation criteria and methodologies, paving the way for the technology proposal evaluation in the last phase of the IMT-2030 cycle, i.e. from 2027 to 2030.

Relationship between ITU-R (WP 5D) and 3GPP:

ITU-R WP 5D establishes the overall research and development direction, key performance indicators, as well as the standardization, commercialization, and spectrum roadmap for the new generation of IMT through a Framework Recommendation. It then moves on to defining the technical performance requirements to achieve the Framework.

After that, 3GPP develops detailed technical specifications that meet the requirements defined by the ITU-R recommendations and submits their specs to ITU-R WP5D (via ATIS) as a candidate radio interface technology. 5D then evaluates whether the 3GPP defined technology meets the requirements of the ITU-R (for 5G and presumably for 6G too). If it passes the evaluation process, it is approved as ITU-R Recommendation.

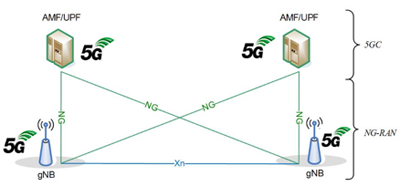

Figure 1. below shows these relationships:

Figure 1. Relationship between ITU-R and 3GPP

………………………………………………………………………………………………………………………….

Motivation and societal considerations:

The motivation for the development of IMT-2030 is to continue to build an inclusive information society and to support the UN’s sustainable development goals (SDGs). To this end, IMT-2030 is expected to be an important enabler for achieving the following goals, among others:

– Inclusivity: Bridging digital divides, to the maximum extent feasible, by ensuring access to meaningful connectivity to everyone.

– Ubiquitous connectivity: To connect unconnected, IMT-2030 is expected to include affordable connectivity and, at minimum, basic broadband services with extended coverage, including sparsely populated areas.

– Sustainability: Sustainability refers to the principle of ensuring that today’s actions do not limit the range of economic, social, and environmental options to future generations. IMT-2030 is envisaged to be built on energy efficiency, low power consumption technologies, reducing greenhouse gas emissions and use of resources under the circular economy model, in order to address climate change and contribute towards the achievement of current and future sustainable development goals.

– Innovation: Fostering innovation with technologies that facilitate connectivity, productivity and the efficient management of resources. These technological advances will improve user experience and positively transform economies and lives everywhere.

– Enhanced security, privacy and resilience: The future IMT system is expected to be secure and privacy-preserving by design. It is expected to have the ability to continue operating during and quickly recover from a disruptive event, whether natural or man-made. Making security, privacy and resilience key considerations in the design, deployment and operation of IMT-2030 systems is fundamental to achieving broader societal and economic goals.

– Standardization and interoperability: To achieve wide industry support for IMT 2030, future IMT systems are expected to be designed from the start to use transparently and member-inclusively standardized and interoperable interfaces, ensuring that different parts of the network, whether from the same or different vendors, work together as a fully functional system.

– Interworking: IMT-2030 is expected to support service continuity and provide flexibility to users via close interworking with non-terrestrial network implementations, existing IMT systems and other non-IMT access systems. IMT-2030 is also expected to support smooth migration from existing IMT systems, where including support of connectivity to IMT-2020 and potentially IMT-Advanced devices will be advantageous for inclusivity.

User and application trends:

Applications and services enabled by IMT-2030 are expected to connect humans, machines and various other things together. With the advances in human-machine interfaces, interactive and high-resolution video systems such as extended reality (XR) displays, haptic sensors and actuators, and/or multi-sensory (auditory, visual, haptic or gesture) interfaces, IMT-2030 is expected to offer humans immersive experiences that are virtually generated or happening remotely. On the other hand, machines are envisaged to be intelligent, autonomous, responsive, and precise due to advances in machine perception, robotics, and artificial intelligence (AI). In the physical world, humans and machines are expected to continuously interact with each other, working with a digital world that extends the real world by using a large number of advanced sensors and AI. Such a digital world not only replicates but also affects the real world by providing virtual experiences to humans, and computation and control to machines.

IMT-2030 is expected to integrate sensing and AI-related capabilities into communication and serve as a fundamental infrastructure to enable new user and application trends. From these trends, it is expected that IMT-2030 provides a wide range of use cases while continuing to provide, inter alia, direct voice support as an essential communication. Furthermore, IMT-2030 technology is expected to drive the next wave of digital economic growth, as well as sustainable far-reaching societal changes, digital equality and universal connectivity. IMT-2030 is expected to further enhance security, privacy, and resilience.

Source: Huawei

…………………………………………………………………………………………………………………………………………………………………..

Technology trends:

Report ITU-R M.2516 provides a broad view of future technical aspects of terrestrial IMT systems considering the timeframe up to 2030 and beyond, characterized with respect to key emerging services, applications trends, and relevant driving factors. It comprises a toolbox of technological enablers for terrestrial IMT systems, including the evolution of IMT through advances in technology and their deployment. In the following sub-sections, a brief overview of emerging technology trends and enablers, technologies to enhance the radio interface, and technologies to enhance the radio network are presented.

Emerging technology trends and enablers:

IMT-2030 is expected to consider an AI-native new air interface that uses AI to enhance the performance of radio interface functions such as symbol detection/decoding, channel estimation etc. An AI-native radio network would enable automated and intelligent networking services such as intelligent data perception, supply of on-demand capability etc. Radio networks that support AI services would be fundamental to the design of IMT technologies to serve various AI applications, and the proposed directions include on-demand uplink/sidelink-centric, deep edge, and distributed machine learning including federated learning.

The integration of sensing and communication functions in IMT-2030 systems would give new capabilities, enable innovative services and applications, and provide solutions with a higher degree of sensing accuracy. It would lead to benefits in enhancing performance and reducing overall cost, size, and power consumption of both systems, when it is combined with technologies such as AI, network cooperation, and multi-nodes cooperative sensing.

Computing services and data services are expected to become an integral component of the IMT 2030 system. It is expected to include processing data at the network edge close to the data source for real-time responses, low data transport costs, high energy efficiency and privacy protection, as well as scaling out device computing capability for advanced application computing workloads.

Device-to-device wireless communication with extremely high throughput, ultra-accuracy positioning and low latency would be an important communication paradigm for IMT-2030. Technologies such as THz technology, ultra-accuracy sidelink positioning, and enhanced terminal power reduction can be considered to support new applications.

Typical use cases for the 6 usage scenarios of IMT-2030:

| Immersive Communication |

|

| Massive Communication |

|

| Hyper Reliable & Low-Latency Communication |

|

| Ubiquitous Connectivity |

|

| Integrated AI and Communication |

|

| Integrated Sensing and Communication |

|

Source: Huawei

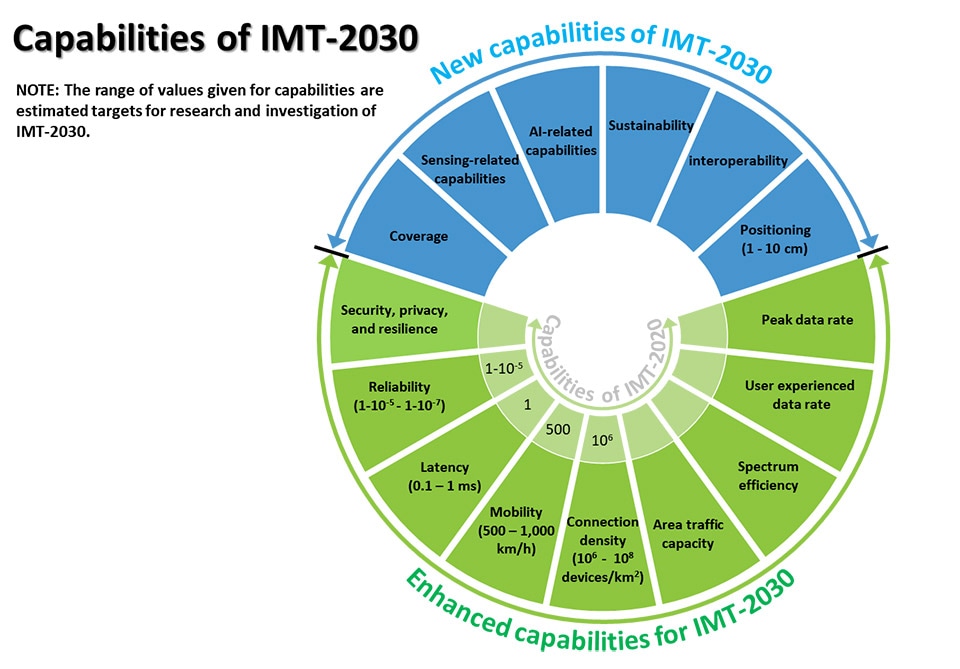

The Figure below summarizes the different dimensions of capabilities for IMT-2030, including 9 enhanced capabilities (peak data rate, user experienced data rate, spectrum efficiency, area traffic capacity, connection density, mobility, latency, reliability, and security/privacy/resilience) and 6 new capabilities (coverage, positioning, sensing-related capabilities, AI-related capabilities, sustainability, and interoperability). The range of values for the capabilities in the figure are estimated targets for research and investigation of IMT-2030. For each usage scenario, single or multiple values within the range would be developed in the future in other ITU-R Recommendations/Reports.

Source: Huawei

IMT-2030 envisages the use of a wide range of frequency bands ranging from sub-1 GHz up to sub-THz bands (low bands, mid bands (centimeterWave), mmWave bands and sub-THz bands). It expects that wider channel bandwidths may be needed to support future applications and services for IMT-2030 in a wide variety of deployments, including wide-area deployments. It is important to ensure that the current spectrum and newly assigned spectrum are harmonized.

References:

https://www.itu.int/md/R19-WP5D-230612-TD-0905/en (RESTRICTED TO TIES USERS)

https://research.samsung.com/blog/All-set-for-6G

IMT Vision – Framework and overall objectives of the future development of IMT for 2030 and beyond

Summary of ITU-R Workshop on “IMT for 2030 and beyond” (aka “6G”)

China’s MIIT to prioritize 6G project, accelerate 5G and gigabit optical network deployments in 2023

ABI Research and CCS Insight: Strong growth for satellite to mobile device connectivity (messaging and broadband internet access)

CCS Insight believes that these enhanced satellite networks have the capability to grow to deliver voice and data services as the constellations evolve. It adds that network operators will be able to offer these satellite services as add-ons to existing subscription packages, catering to the growing demand for ubiquitous connectivity.

As demand for enhanced global connectivity continues to rise, the analyst forecasts that 15% of global mobile subscribers are expected to own a smartphone that supports satellite messaging by 2027 and an additional 10% will benefit from satellite plans provided by their operator. By capitalizing on revenue streams generated through operators and supplementary services, CCCS believes that the direct-to-device satellite market is poised to amass $18bn in revenue by 2027. This market it said represented a “vast opportunity”, with an audience of more than 4.8 billion people who could access satellite services through a compatible smartphone. It calculated that as many as 493 million people worldwide lack any kind of mobile network coverage.

“Bringing satellite capabilities to mass-market smartphones marks a milestone in the telecom industry,” said Luke Pearce, senior analyst at CCS Insight. “This development creates exciting opportunities for consumers, manufacturers and operators and promises to help bridge the digital divide. The projected growth in revenue and subscribers highlights the potential this integration holds for expanding connectivity options – we’re witnessing the start of a new era where satellite services become an integral part of everyday smartphones.”

CCS Insight’s free report, Direct Satellite-to-Device Mobile Services, shares unique insight into the market for satellite-connected phones and unpacks its developing dynamics.

AST SpaceMobile achieves 4G LTE download speeds >10 Mbps during test in Hawaii

FCC Grants Experimental License to AST SpaceMobile for BlueWalker 3 Satellite using Spectrum from AT&T

New ITU report in progress: Technical feasibility of IMT in bands above 100 GHz (92 GHz and 400 GHz)

Introduction:

ITU-R Report R M.2376 contains studies of frequency ranges (6-100 GHz) for International Mobile Telecommunications (IMT) technologies. It is envisioned that future IMT systems will need to support very high throughput data links to cope with the growth of the data traffic, new extremely bandwidth demanding use cases, as well as new capabilities of integrated sensing and communication (ISAC). There has been academic and industry research and development ongoing related to suitability of mobile broadband systems in frequency bands above 92 GHz to enable services requiring tera-bit per second speeds. This has prompted researchers to consider the technical feasibility of higher frequency bands in IMT.

Overview:

This ITU-R preliminary draft new report in progress provides information on the technical feasibility of IMT in bands between 92 GHz and 400 GHz. This Report complements the studies carried in Report ITU-R M.2376. This technical feasibility Report includes information on propagation mechanisms and channel models, as well as newly developed technology enablers such as active and passive components, antenna techniques, deployment architectures, and the results of simulations and performance tests. Aspects of coexistence with incumbent radiocommunications services above 92 GHz are outside the scope of this document, and this report does not presuppose the inclusion of any item on a future World Radio Conference (WRC) agenda nor the decisions of a future WRC.

ITU-R WP5D emphasizes that the further development of the draft new Report ITU-R M.[IMT.ABOVE 100GHz] does not contain propagation prediction methods. It contains only results contributed by industry and academia of propagation measurements and simulation campaigns.

…………………………………………………………………………………………………………………………

From: Experiments bring hope for 6G above 100 GHz:

Channel models for 4G and 5G cannot simply be extended above 100 GHz; engineers must verify and fine-tune knowledge to correctly reflect the impact of the environment for various use cases. We must, for example, understand outdoor scenarios and indoor industrial scenarios where human bodies, vehicles, and environmental conditions such as rain propagation strongly influence signal propagation.

5G pioneered the use of millimeter wave frequencies with bandwidths up to 400 MHz per component carrier to enable transmission rates necessary for demanding real-time applications such as wireless factory automation. 6G technology is aiming at significantly higher transmission rates and lower latencies. Large contiguous frequency ranges for ultra-high data rates with bandwidths of several GHz are only available above 100 GHz.

With sonar, the transmitter and receiver are in the same place. As for channel sounding of electromagnetic waves, the transmitter and receiver are spatially separated. In time domain channel sounding, a modulated pulse signal with excellent autocorrelation properties, such as a Frank-Zadoff-Chu (FZC) sequence [1], serves as a “ping” whose channel impulse response (CIR) is recorded. This propagation-time measurement is very similar to the time-delay measurements performed in a GPS receiver in reference to the GPS satellites (and subsequently inferring the position information), where each satellite transmits its specific correlation sequence. The CIR includes both the direct propagation components (line of sight, LOS) and all reflection and scattering components (non-line-of-sight, NLOS) from objects in the environment (Figure 1). We can derive channel-model parameters and their values from the results.

Figure 1. Operating principle of time domain channel sounding: The channel impulse response (CIR) is measured by emitting an electromagnetic “ping” at the frequency of interest and capturing all returning signal components.

……………………………………………………………………………………………………………………………………………………………….

References:

https://www.itu.int/md/R19-WP5D-C-0679/en (RESTRICTED TO ITU TIES USERS)

https://www.itu.int/md/R1-WP5D-C-1654/en (RESTRICTED TO ITU TIES USERS)

ITU-R WP5D: Studies on technical feasibility of IMT in bands above 100 GHz

Samsung-Mediatek 5G uplink trial with 3 transmit antennas

Samsung Electronics and MediaTek have successfully conducted 5G standalone (SA) uplink tests, using three transmit (3Tx) antennas instead of the typical two, to demonstrate the potential for improved upload experiences with current smartphones and customer premise equipment (CPE).

Until recently, most talk about 5G SA industry firsts have focused on the downlink. However, the demands on uplink performance are increasing with the rise of live streaming, multi-player gaming and video conferences. Upload speeds determine how fast your device can send data to gaming servers or transmit high-resolution videos to the cloud. As more consumers seek to document and share their experiences with the world in real-time, enhanced uplink experiences provide an opportunity to use the network to improve how they map out their route home, check player stats online and upload videos and selfies to share with friends and followers.

While current smartphones and customer premise equipment (CPEs) can only support 2Tx antennas, this industry-first demonstration validated the enhanced mobile capability of 3Tx antenna support. This approach not only improves upload speeds but also enhances spectrum and data transmission efficiency, as well as overall network performance.

The test was conducted in Samsung’s lab, based in Suwon, Korea. Samsung provided its industry-leading 5G network solutions, including its C-Band Massive MIMO radios, virtualized Distributed Unit (vDU) and core. The MediaTek test device featuring its new M80-based CPE chipset began with one uplink channel apiece at 1,900MHz and 3.7GHz, but added an extra uplink flow using MIMO on 3.7GHz. Both companies achieved a peak throughput rate of 363Mbps, an uplink speed that is near theoretical peak using 3Tx antennas.

Source: ZTE

“We are excited to have successfully achieved this industry breakthrough with MediaTek, bringing greater efficiency and performance to consumer devices,” said Dongwoo Lee, Head of Technology Solution Group, Networks Business at Samsung Electronics. “Faster uplink speeds bring new possibilities and have the potential to transform user experiences. This milestone further demonstrates our commitment to improving our customers’ networks using the most advanced technology available.”

“Enhancing uplink performance using groundbreaking tri-antenna and 5G UL infrastructure technologies will ensure next-generation 5G experiences continue to impress users globally,” said HC Hwang, General Manager of Wireless Communication System and Partnership at MediaTek. “Our collaboration with Samsung has proved our combined technical capabilities to overcome previous limits, enhancing network performance and efficiency, opening up new possibilities for service providers and consumers to enjoy faster and more reliable 5G data connectivity.”

“With demands on mobile networks rising, enhancing upload performance is essential to improving consumer and enterprise connectivity, as well as application experiences,” said Will Townsend, VP & Principal Analyst at Moor Insights & Strategy. “Samsung and MediaTek have achieved an important 5G Standalone milestone in a demonstration which underscores a tangible network benefit and does so in a way that can help operators maximize efficiency.”

Samsung has pioneered the successful delivery of 5G end-to-end solutions, including chipsets, radios and core. Through ongoing research and development, Samsung drives the industry to advance 5G networks with its market-leading product portfolio, from virtualized RAN and Core to private network solutions and AI-powered automation tools. The company currently provides network solutions to mobile operators that deliver connectivity to hundreds of millions of users worldwide.

References:

Ericsson and MediaTek set new 5G uplink speed record using Uplink Carrier Aggregation

Nokia achieves extended range mmWave 5G speed record in Finland

Huawei and China Telecom Jointly Release 5G Super Uplink Innovation Solution

https://www.telecomhall.net/t/5g-uplink-enhancement-technology-by-zte-white-paper/20183

Perú’s First Open Access Wholesale Fiber Optic Network

KKR, Telefónica Hispanoamérica, and Entel today announced agreements under which KKR will acquire a majority interest in PangeaCo and the existing fiber optic networks of Telefónica del Perú and Entel Perú to build Perú’s first nationwide open access wholesale fiber optics company with the mission to bring greater access to fiber optics connectivity across the country. The transaction will combine the existing fiber optic networks of PangeaCo, Telefónica del Perú, and Entel Perú into an independent company controlled by KKR. The newly formed network will be open access, allowing usage to all internet service providers for the first time. KKR plans to make approximately US$200 million of additional investment to more than double the ultra-fast fiber network from more than 2 million homes passed today to reach 5.2 million homes passed across 86 provinces by the end of 2026.

Telefonica did not disclose the value of the transaction but said the deal would cut its debt by 200 million euros ($217.8 million). According to a banking source close to the deal, the transaction valued 100% of the unit at about 550 million euros, including debt.

Under the terms of the agreement, KKR will acquire a controlling interest in PangeaCo, which will subsequently acquire the existing fiber optic networks of Telefónica del Perú and Entel Perú. Through the combination of these networks, KKR will establish ON*NET Fibra de Perú as the new name for the platform which will independently build and operate the nation’s largest fiber optic network with world-class quality standards. KKR will own a 54% interest in ON*NET Fibra de Perú alongside Telefónica Hispanoamérica, which will own 36%, and Entel Perú, which will own 10%.

The entire ON*NET Fibra de Perú fiber optic network will be open to use by all internet service providers, increasing competition in the wholesale market. Telefónica del Perú and Entel Perú will be anchor tenants on the expanded open access network, enabling both providers to reach a greater number of customers with ultra-high-speed offerings. The transaction does not impact the services provided by existing customers of PangeaCo, Telefónica del Perú or Entel Perú. Upon closing of the transaction, customers will benefit from the scale of the larger network.

In Perú, approximately 88% of households have mobile or fixed internet service, but less than 35% have access to high-speed fiber optic networks.1 KKR, as the controlling shareholder, intends for ON*NET Fibra de Perú to more than double the households reached by fiber optic network, including reaching municipal areas outside of Lima as well as middle- and low-income households. This transaction demonstrates continued investor confidence in Peruvian infrastructure and the commitment of the companies to contribute to the sustainable development of the digital connectivity in the country.

Today’s announcement builds on KKR’s success in expanding nationwide connectivity and increasing competition in Chile and Colombia. ON*NET Fibra de Chile has expanded access from 2.4 million homes passed to 3.7 million homes passed since KKR signed the acquisition in February 2021 and ON*NET Fibra de Colombia has increased homes passed from 1.2 million to 2.4 million since signing in July 2021.2 Both companies have attracted multiple internet service providers to utilize their open access networks.

KKR is making the investment through its KKR Global Infrastructure Investors III fund and plans to provide operational support to ON*NET Fibra de Perú through NEXO LatAm, a digital infrastructure business supporting KKR’s Infrastructure strategy across Latin America. KKR and NEXO LatAm have significant experience supporting the successful expansion of open access fiber optic investments. The transaction is subject to regulatory approvals, including the approval of the Peruvian antitrust agency (INDECOPI).

…………………………………………………………………………………………………………………………………………………….

From telecoms.com:

When Telefonica first sold a stake in its Chilean fibre business to KKR it had a footprint of 2.4 million homes passed. The deal valued the entire business at $1 billion. The Colombian fiber business that KKR bought into was valued at half that amount and just over half the footprint:1.2 million homes. Admittedly, the Colombia deal was inked two years ago and Chile even longer ago, and a fair bit has changed in the economic situation in that time. However, we can get a sense of the scale of spend we might be looking at.

KKR wants to share the progress made by those Chilean and Colombian ventures. ON*NET Fibra de Chile passed 3.7 million homes as of the end of 2022, while ON*NET Fibra de Colombia had doubled the number of homes passed to 2.4 million, it said, adding that both have attracted multiple ISP customers.

That surely bodes well for the new venture’s aims in Peru, where at present around 88% of households have mobile or fixed internet service, but less than 35% have access to high-speed fibre networks, KKR said, citing data from regulator OSIPTEL and market research firm Omdia (owned by Informa).

It should also help smooth the regulatory process. The deal needs a number of approvals, including that of Peruvian antitrust agency INDECOPI, but it’s hard to foresee any major difficulties, given that this is an established model across the region and one that seems to be working.

References:

https://telecoms.com/522583/telefonica-entel-and-kkr-ink-peru-fibre-deal/

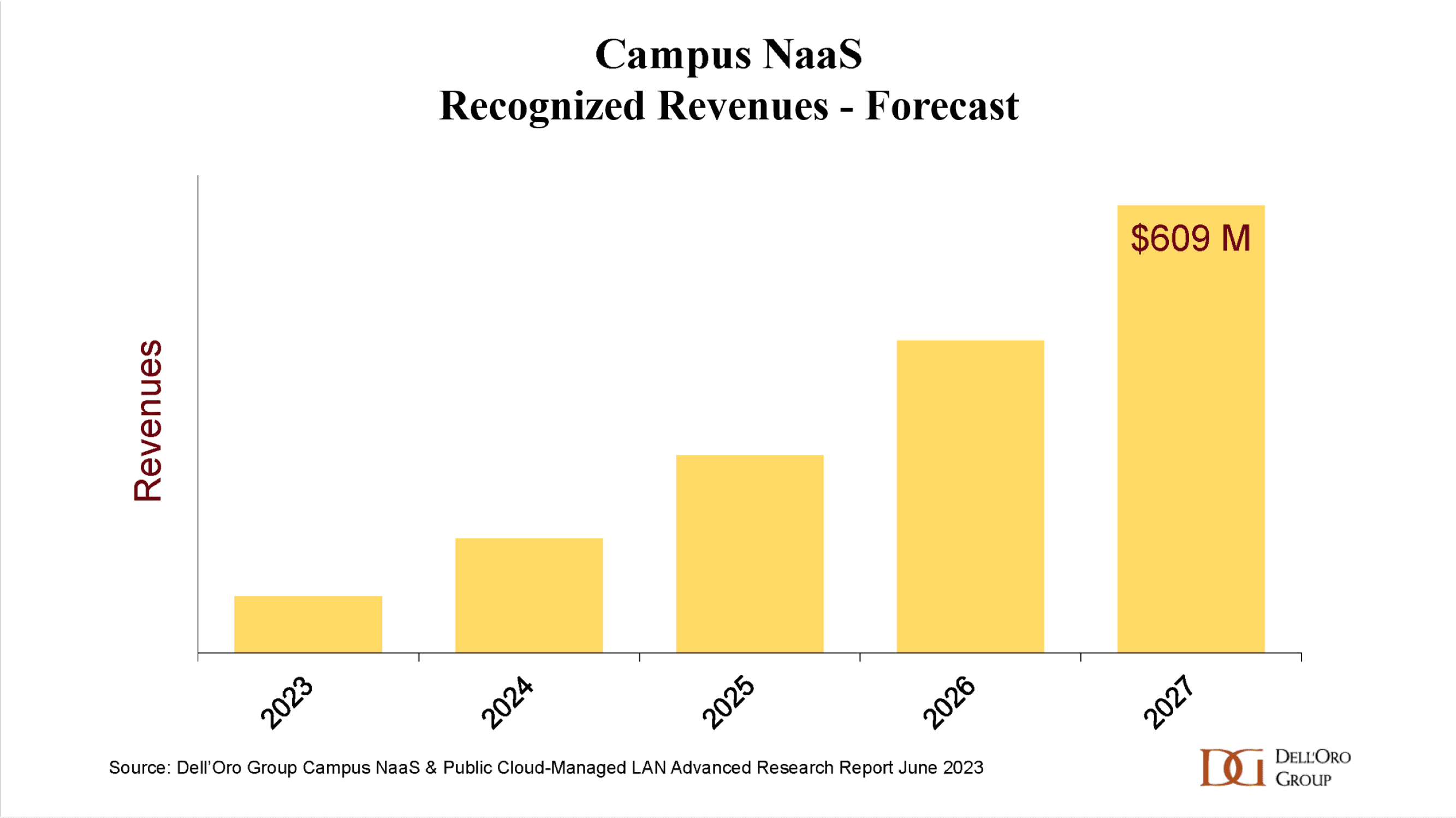

Dell’Oro: Bright Future for Campus Network As A Service (NaaS) and Public Cloud Managed LAN

|

||

|

Reliance Jio to sign $1.5 billion 5G network equipment deal with Nokia (“Home grown 5G” never happened)

Whatever happened to Jio’s claim of “home grown 5G“? Answer: It was a big bold faced lie! Almost 3 years ago, Jio Chairman Mukesh Ambani said his company had developed its own 5G solution “from scratch.” He said at the time, “Jio plans to launch “a world-class 5G service in India…using 100% home grown technologies and solutions,” he said in a statement at the Reliance Industries annual shareholders meeting. “Once Jio’s 5G solution is proven at India-scale, Jio Platforms would be well-positioned to be an exporter of 5G solutions to other telecom operators globally, as a complete managed service,” he added.

…………………………………………………………………………………………………………………………………………………………….

Fast forward to today. Jio, India’s largest telecoms operator, is set to sign a contract at Nokia’s Headquarters in Helsinki, Finland, according to sources speaking to the Economic Times.

The purchase will be financed by several global banks, including HSBC, Citigroup, and JP Morgan, whose combined loans will total around $4 billion. Finnish state-owned export credit agency Finnvera is set to issue guarantees to the lenders. Representatives from the banks are likely to be present at the signing, as well as Senior Executives from Reliance Group.

At the time, financial details of the deals were not disclosed; however, media reports have since suggested that the deal with Ericsson was worth $2.1 billion. Now, this deal with Nokia will see the total 5G investment reach roughly $3.6 billion.

Earlier this year, Jio’s president Mathew Oommen said the company aimed to become “the largest 5G SA (standalone) only network operator in the world in the second half of 2023”, with the company targeting nationwide coverage by the end of the year.

In October 2022, Jio signed 5G equipment contracts with both Nokia and Ericsson.

In related news, earlier this week, Reliance Industries announced the launch of a budget 4G phone, (costing $12), aiming to convert the 250 million 2G users in India to 4G. The company says its goal is to pass the benefits of the internet-capable mobile technology to every Indian.

![]()

References:

https://totaltele.com/indias-jio-to-sign-1-5-billion-5g-equipment-deal-with-nokia/

Reliance Jio’s “Home Grown” 5G? Ericsson and Nokia in multi-year deals with Jio to build a mega 5G network

Reliance Jio claim: Complete 5G solution from scratch with 100% home grown technologies

Do ITU Radio Regulations Matter? China allocates 6 GHz spectrum for 5G and 6G services prior to WRC 23; CTIA objects!

China’s regulators allocated spectrum in the 6 GHz frequency band for 5G and 6G services, asserting it was the first country to reserve the resource expected by the mobile industry to enable future connectivity. In a translated statement, the country’s Ministry of Industry and Information Technology (MIIT) highlighted the band was the only one with sufficiently-large bandwidth in the mid-range frequency band.

In a blog published on the opening day of MWC 2023 Shanghai, GSMA head of spectrum Luciana Camargos highlighted China had identified the upper part of the band for International Mobile Telecommunications (IMT) systems:

“China’s efforts towards the 6GHz band don’t come as a surprise,” Camargos wrote, adding. “Conducive spectrum policies for the mid-bands, especially the 2.6GHz and 3.5GHz, have helped China to deploy the world’s largest 5G networks with over 2.7 million 5G base stations by the end of April 2023 and to be on track to become the first country to reach 1 billion 5G connections in 2025.”

Note: The GSMA has been pushing the case for the use of 6 GHz by the mobile industry ahead of the ITU World Radiocommunication Conference 2023 (IRC 23) in Dubai, UAE in November 2023. WRC 19 did not authorize use of the 6 GHz band for IMT and so it is not in ITU-R M.1036 revision 6 “Frequency arrangements for implementation of the terrestrial component of International Mobile Telecommunications in the bands identified for IMT in the Radio Regulations” which specifies all terrestrial IMT frequencies.

During the Ajit Pai administration, the FCC allocated virtually the entire 6 GHz band – 1,200 megahertz stretching across 5.925 GHz–7.125 GHz – for unlicensed uses, primarily Wi-Fi rather than IMT which uses licensed spectrum.

–>Please refer to References below.

………………………………………………………………………………………………………………………………………………………..

The CTIA was alarmed by China’s decision and posted this on Twitter:

BREAKING NEWS: China announces plans to free up far more #5G spectrum than the United States. Congress must restore @FCC auction authority and identify new spectrum to secure our leadership of the industries and innovations of the future.

“We risk having Chinese networks that are materially better at enabling the industries of the future,” wrote Doug Brake, a policy official at CTIA, the U.S. wireless industry’s main trade association. “If a mobile video platform like TikTok is a national security threat, why should we surrender advantage in a technology like 5G that enables transformation throughout the economy?”

“We need a breakthrough on spectrum policy that prioritizes full-power, licensed, midband spectrum for 5G to secure our industries of the future in the face of increasingly capable Chinese networks and the market dominance of Chinese vendors. This requires a coordinated effort, starting with Congress establishing an auction pipeline, NTIA identifying at least 1500 megahertz of licensed midband spectrum for 5G as part of the National Spectrum Strategy,” Brake wrote.

The NTIA plans to release a U.S. spectrum strategy this November.

…………………………………………………………………………………………………………………………………………………………..

A number of countries in North and South America, and in Asia, have already allocated the 6GHz band for unlicensed uses, according to Dean Bubley of Disruptive Analysis.

Others countries haven’t yet decided what to do with the band. For example, officials in the UK just this week opened an investigation into the possibility of sharing the 6GHz band between Wi-Fi and 5G users.

“Rather than choosing between the two, we believe an alternative approach is possible. We are exploring options that would enable the use of both Wi-Fi and mobile in the band. We are calling this ‘hybrid sharing,'” wrote regulator Ofcom in a post.

According to Disruptive Wireless analyst Bubley, Ofcom’s proposal isn’t that simple. “This would need new technical mechanisms for networks, devices and databases / sensing, and how to manage and enforce any prioritisations,” he wrote in a new LinkedIn post. “There are various options for automation, dynamic vs. fixed sharing and so on. There may be constraints on power or ‘polite’ protocols. Ideally these would be internationally standardized – perhaps just in Europe, but more broad adoption would obviously be preferable.”

Meanwhile, others continue to urge global regulators to allocate the 6GHz band for 5G. For example, the GSMA – the world’s biggest 5G trade association – recently reiterated its position that 6GHz will be necessary for 5G networks to keep pace with demand.

According to Bubley, the debate will likely come to a head later this year at the ITU-R’s 2023 World Radiocommunications Conference (WRC-23) in Dubai, United Arab Emirates (UAE). That’s where global telecom regulators work to harmonize their plans in order to score global economies of scale among equipment suppliers. The result is a set of Radio Regulations which are approved frequencies to be used for IMT and other wireless services.

……………………………………………………………………………………………………………………………………………………………………..

References:

6 GHz band proposed for WiFi/5G in Asia Pacific region, but it’s not in ITU-R M.1036

CTIA commissioned study: U.S. running out of licensed spectrum; 5G FWA to be impacted first by network overloads

GMSA vs ITU-R, FCC & U.S. Tech Companies on use of 6GHz band: Licensed 5G or Unlicensed WiFi?

Broadcom, Cisco and Facebook Launch TIP Group for open source software on 6 GHz Wi-Fi

FCC to open up 6 GHz band for unlicensed use – boon for WiFi 6 (IEEE 802.11ax)

FCC to vote April 23rd to open up 1200 MHz of 6 GHz spectrum for WiFi

U.S. Launches National Spectrum Strategy and Industry Reacts

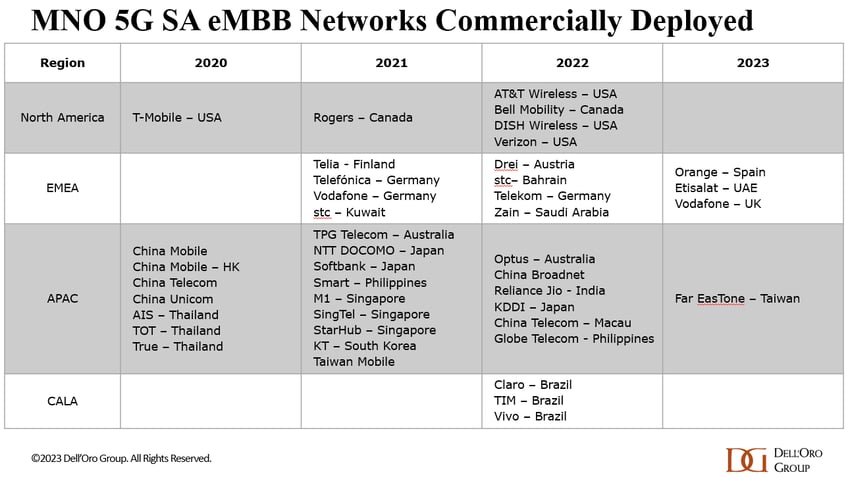

5G SA networks (real 5G) remain conspicuous by their absence

According to a May 2023 report from the Global mobile Suppliers Association (GSA), just 35 network operators in 24 countries and territories “are now understood to have launched or deployed public 5G SA networks.” That’s out of approximately 240 service providers which have now launched commercial 5G services, as per the recent Ericsson Mobility Report.

Dell’Oro’s Dave Bolan said, “Currently we count 43 live 5G SA networks for eMMB [enhanced mobile broadband]. For 2023, four [mobile network operators] have launched 5G SA networks,” he added. It should be noted that Dell’Oro doesn’t factor in fixed wireless access (FWA) or private 5G networks in its SA totals.

In Europe, Vodafone UK and Telefónica Spain join what remains a small set of network operators that have launched 5G SA, including Orange Spain and Vodafone Germany. Spain should provide an interesting study of what happens when two rival operators launch 5G SA service.

There are some glimmers of hope that 5G SA launches will accelerate soon. GSA (aka GSMA) has identified at least 1,063 announced devices with declared support for standalone 5G in sub-6GHz bands, 864 of which are commercially available. Furthermore, it said 116 operators in 53 countries and territories are now investing in 5G SA, including those that have actually deployed a public network. “This equates to 22.1% of the 524 operators known to be investing in 5G licenses, trials or deployments of any type,” the GSA said.

Separately, analysts say that 5G SA branding by network operators is quite confusing (we agree). Vodafone UK’s decision to use 5G Ultra for its 5G SA branding vs Telefonica using 5G+ are examples of that.

Gabriel Brown of Heavy Reading said, “customers don’t really know what it means, other than it denotes some form of technical advance.” He points out that 5G SA “requires a lot of investment and deep engineering expertise; this makes it a useful proxy for network quality. Operators need to take all the technical marketing opportunities they can get.”

“What happens when BT launches? Are they going to call it 5G+ or 5G Super Ultra or something like that? That’s going to make it even more confusing,” said Kester Mann, an analyst with CCS Insight. At the same time, he agrees that 5G standalone is a significant network upgrade and it makes sense that operators would want to gain a marketing edge over rivals that have yet to launch the service.

Notably, neither Vodafone nor Telefónica is charging extra for the more advanced 5G service, and both have focused on the improved speeds and reliability it will bring. They also emphasize eco-friendly aspects, such as lower energy consumption. However, Mann questioned Vodafone’s claim that customers with an eligible 5G Ultra device can expect up to 25% longer battery life. “Twenty-five percent faster than what?” he asked. “It’s a bit unclear.” However, such a claim would certainly be welcome news to consumers. “In a lot of our consumer research, battery life comes out as one of the common bugbears among people using mobile phones,” said Mann.

In the U.S., T-Mobile is the only network operator that’s deployed a 5G SA network. AT&T and Verizon have been talking about it for years, but the time frame for deployment has been pushed back several times.

Deloitte Global said it expects the number of mobile network operators investing in 5G SA networks via trials, planned deployments or rollouts to grow from more than 100 operators in 2022 to at least 200 by the end of this year.

One reason why there are relatively few 5G SA networks deployed is there are no implementation standards. 3GPP 5G Architecture specs, rubber stamped by ETSI, provide several options to realize a 5G cloud-native core network which leads to different implementations. 3GPP decided NOT to liaise their 5G non-radio aspects specs (including 5G Architecture and 5G Security) to ITU-T.

Here are the key 3GPP 5G system specs:

- TS 22.261, “Service requirements for the 5G system”

- TS 23.501, “System architecture for the 5G System (5GS)”

- TS 23.502 “Procedures for the 5G System (5GS)”

- TS 32.240 “Charging management; Charging architecture and principles”

- TS 24.501 “Non-Access-Stratum (NAS) protocol for 5G System (5GS); Stage 3”

The latest 3GPP 5G Architecture spec is System architecture for the 5G System (5GS) (3GPP TS 23.501 version 17.9.0 Release 17), published by ETSI on July 5, 2023.

Source: 3GPP

Hence, the ITU JCA on IMT2020 and Beyond is dependent on other organizations for inputs to their roadmap. “The scope of JCA-IMT2020 is coordination of the ITU-T IMT-2020 standardization work with focus on non-radio aspects and beyond IMT2020 within ITU-T and coordination of the communication with standards development organizations, consortia and forums also working on IMT2020 and beyong IMT-2020 related standards.”

References:

https://www.silverliningsinfo.com/5g/5g-sa-springs-action

ABI Research: Expansion of 5G SA Core Networks key to 5G subscription growth

Orange-Spain deploys 5G SA network (“5G+”) in Madrid, Barcelona, Valencia and Seville

Counterpoint Research: Ericsson and Nokia lead in 5G SA Core Network Deployments

Tech Mahindra and Microsoft partner to bring cloud-native 5G SA core network to global telcos

Omdia and Ericsson on telco transitioning to cloud native network functions (CNFs) and 5G SA core networks

https://urgentcomm.com/2023/01/19/standalone-5g-progress-remains-a-disappointment/

https://www.3gpp.org/technologies/5g-system-overview

https://www.itu.int/en/ITU-T/jca/imt2020/Pages/ToR.aspx