Wipro and Cisco Launch Managed Private 5G Network-as-a-Service Solution

Wipro has announced a managed private 5G-as-a-Service solution in partnership with Cisco. The new offering enables enterprise customers to achieve better business outcomes through the seamless integration of private 5G with their existing LAN/WAN/Cloud infrastructure.

Managed private 5G from Cisco and Wipro supports organizations looking to enjoy the advantages of a private 5G network without having to acquire, run, and maintain one. The as-a-service solution benefits enterprise customers by minimizing the risks associated with upfront capital expenditure (Capex) investments and expedites technology adoption as Wipro and Cisco take on the technical, operational, and commercial risks of implementing the solution.

“Private 5G is already enabling connectivity for a wide range of use cases in factories, supply chains, university and enterprise campuses, entertainment venues, hospitals, and more,” said Masum Mir, Senior Vice President and General Manager, Provider Mobility, Cisco Networking. “We’ve created a simplified and intuitive private 5G solution with Wipro, leveraging the advantages of 5G, IoT, Edge and Wi-Fi6 technologies to improve customer outcomes.”

The managed private 5G solution is built on Cisco’s 4G/5G mobile core technology and Internet of Things (IoT) portfolio – spanning IoT sensors and gateways, device management software, as well as monitoring tools and dashboards. The solution is seamlessly built, run, and managed by Wipro for customers. To support the partnership, Wipro has created a dedicated private 5G lab to build, test, and demonstrate industry use-cases.

“Wipro and Cisco have a long history of building secure networks for enterprises and industries,” said Jo Debecker, Global Head of Wipro FullStride Cloud. “We are both dedicated to the partnership and delivering a secure, cloud-managed private 5G service to our customers. Because it is an as-a-service solution, it provides maximum benefits while minimizing the human resources and costs associated with owning a private network.”

Lourdes Charles, Vice President, 5G / Connectivity Services, Wipro Limited said, “Private 5G integration will put organizations on the cusp of a new revolution. We are delighted to expand our long-standing strategic relationship between Cisco and Wipro to include managed private 5G solutions for enterprise customers. To simplify the customer experience, the solution will validate mission-critical use cases, operations Service-Level Agreements, and lifecycle management. Wipro is fully committed through our 5G Def-i platform, to assist customers with their private 5G networks through best-in-class technology, pricing, and performance.”

“Wipro believes Cisco is very well positioned with extensive products and services to provide the complete stack for enterprise-converged network and security solutions,” the firm noted in an email to SDxCentral. “Cisco also brings integration with enterprise infrastructure and applications.”

IoT Analytics recently ranked Cisco as one of the market’s top software providers, touting its Cisco Edge Intelligence and IoT security offerings. The analyst firm also noted that spending on IoT software hit $53 billion in 2022, with the installed base of connected IoT devices surging to 14.4 billion units. The firm expects that device number to surge to 30 billion units by 2027.

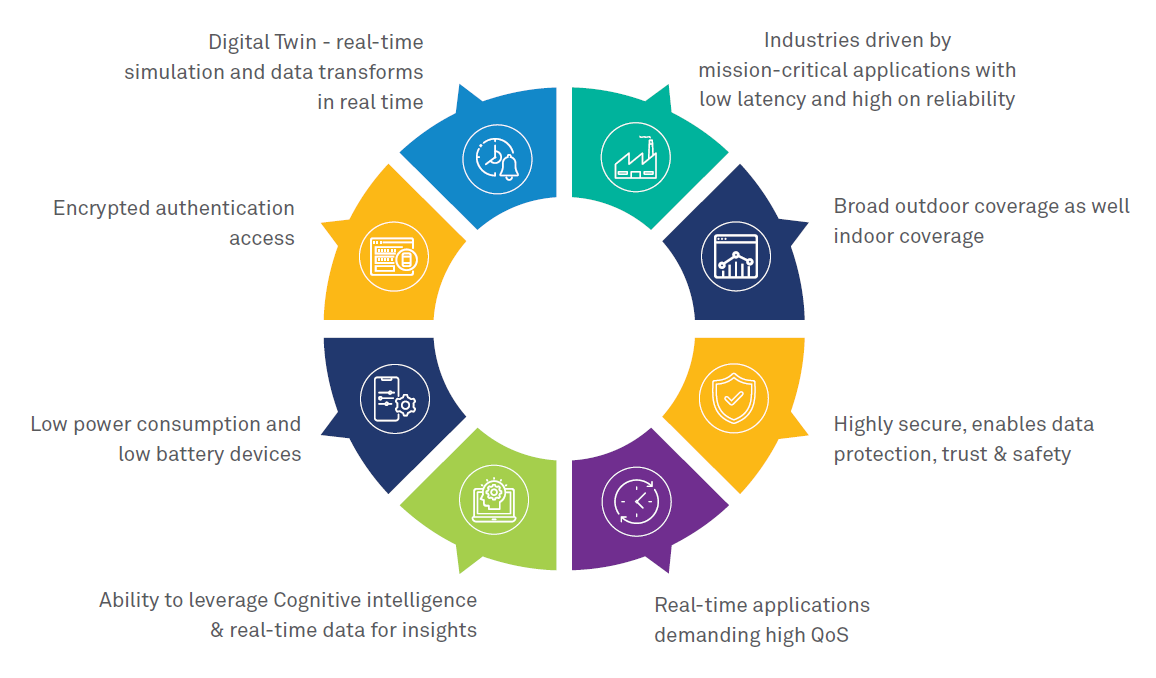

Wipro says that 5G cellular network for enterprise running on both licenses and shared spectrum lays the foundation for:

ABI Research this week reported that more than 1,000 enterprise private networks have been deployed worldwide, despite a slowdown in public proclamations.

“This is actually a good sign for the private networks market,” Leo Gergs, senior analyst for 5G Markets at ABI Research, wrote. “Enterprises are beginning to see the deployment of private cellular connectivity as a competitive advantage and, therefore, do not want to talk about it too openly. Which is important as the market moves from the experimental phase toward commercializing private network deployments.”

Gergs added that this growth has now placed more pressure on the telecommunications industry to ensure those networks can handle increasingly complex and revenue-generating use cases. “The telco industry urgently needs to deliver on promises made to the enterprise community now. Otherwise, enterprise 5G will enter the history books as the technology that always overpromised and under-delivered.”

United Kingdom-based managed service provider Logicalis recently deployed Cisco’s private network with Logicalis overseeing the on-site engineering, including site preparation, ordering of solution components, organization of the spectrum, SIM management, staging, creation of customer profiles and core and RAN installation.

Chris Calvert, VP of private wireless services for Logicalis US, explained that Cisco is providing its Private 5G platform, which includes the 4G/5G core network that Logicalis’s 4G LTE and 5G service requires. That core is available as a single standalone (SA) core or a high-availability three-server cluster.

“Cisco really wanted this to be a managed services-only solution,” Calvert said. “Basically, Logicalis is Cisco’s customer. The combination of the industry expertise and the fact that we have a large managed-services practice were really the driving forces behind Cisco selecting Logicalis as one of only two manufacturers that can actually provide this solution currently.”

About Wipro Limited:

Wipro Limited is a leading technology services and consulting company focused on building innovative solutions that address clients’ most complex digital transformation needs. Leveraging our holistic portfolio of capabilities in consulting, design, engineering, and operations, we help clients realize their boldest ambitions and build future-ready, sustainable businesses. With over 250,000 employees and business partners across 66 countries, we deliver on the promise of helping our customers, colleagues, and communities thrive in an ever-changing world. For additional information, visit us at www.wipro.com.

About Cisco:

Cisco offers an industry-leading portfolio of technology innovations. With networking, security, collaboration, cloud management, and more, we help to securely connect industries and communities. Information about Cisco’s products is here.

References:

Cisco’s Private 5G story: https://www.youtube.com/watch?v=kdsyhsXicNk

FTTH was ~60% of France fixed broadband market in Q1-2023

FTTH lines made up nearly 60% of French fixed broadband market in Q1-2023. FTTH subscriptions across mainland France and the overseas territories reached a 59.4% share of the country’s fixed broadband market at the end-March 2023, up by 10 percentage points from Q1 2022.

Viva La France!

According to the latest update from France regulator Arcep, the FTTH installed base added 895,000 net connections since December for a total of 19.02 million (+965,000 in Q4), representing a 22.8% increase year-on-year. As of March 31, 2023, 35.3 million premises (apartments, houses, offices, etc.) can be connected via FTTH i.e. a little over 80% of premises in the national territory. If you add cable internet that gives us 37.6 million locals who potentially have access to very high speed on wired networks in France. This represents a growth of approximately 3.6 million over the past year.

96% of Paris is connectable to optical fiber, but it’s only 50% in Lille. No explanation is given for this slowdown which is not in line with the France Very High Speed Plan which aims to generalize optical fiber throughout France by 2025.

Other high-speed networks (cable, VDSL and fixed wireless/LTE) continued to see their combined installed base decline quarter-on-quarter (-129,000) to stand at 3.25 million. As a result, the number of overall lines delivering download speeds of at least 30 Mbps reached 22.27 million at end-March.

The ADSL segment maintained its downward trend, leading to a further drop in connections delivering less than 30 Mbps. This brought the installed base across all fixed broadband networks to 32.04 million, up by 99,000 since December. This compares to with 63,000 market net additions in the previous quarter and 133,000 in Q1 2022.

Looking at progress in the ongoing fibre roll-outs, French operators brought FTTH connectivity to 840,000 million additional premises in the three months to March, for an overall footprint of 35.29 million. The pace of deployment slowed down from 1.3 million premises passed with fibre in the December quarter, and 1.1 million in Q1 2022.

On a year-on-year basis, the volume of new premises passed with fibre roughly halved across both densely populated metropolitan areas and mid-sized towns with privately funded roll-outs, while recording a 10% fall in public initiative fibre networks under deployment in rural communities. The latter reached a footprint of 12.8 million premises eligible for FTTH services at end-March, representing 610,000 additional premises since December.

Associated documents:

- Scorecard for fixed broadband and superfast broadband services – figures for Q1 2023

- Maconnexioninternet.arcep.fr, to obtain detailed information on fixed internet access coverage, particularly thanks to FttH rollout maps (which are also still available athttps://cartefibre.arcep.fr/)

- Open data:data on fibreand data on all access technologies

References:

FCC explores shared use of the 42 GHz band

The FCC voted Thursday to launch a proceeding to consider sharing models in 500 megahertz of spectrum in the 42 GHz band. The agency believes its examination could inform how the band might best be used —particularly by smaller wireless service providers— and provide guidance on future uses of sharing models in spectrum management.

FCC Chairwoman Jessica Rosenworcel, who just returned this week from a quick trip to Sharm El-Sheikh, Egypt for an ITU meeting, said that when she took over at the FCC, she believed the agency had overinvested in millimeter wave (mmWave) auctions and done too little to bring mid-band spectrum to market. She set out to change that, launching auctions in the 3.45 GHz and 2.5 GHz bands.

“With those successful mid-band efforts in the rear-view mirror, we are now turning back to millimeter wave,” Rosenworcel said in prepared remarks. “But this time we want to consider something different. In the 42 GHz band we have 500 megahertz of greenfield airwaves with no federal or commercial incumbencies. So we are putting out ideas. We are exploring non-exclusive access models. This could entail using a technology-based sensing mechanism to help operators actively detect and avoid one another. It could involve non-exclusive nationwide licenses that leverage a database to facilitate coexistence. It could also entail site-based licensing. To get even more out of this effort we ask if our approaches could be combined with shared-used models in other spectrum bands, like the lower 37 GHz band.”

“Our goal here is to come up with a new model to lower barriers, encourage competition and maximize the opportunities in millimeter wave spectrum. In short, it’s time to be creative. I look forward to the record that develops—and then look forward to sharing our creativity with the world.”

A Notice of Proposed Rulemaking (NPRM) is in effect where the FCC will build a record on the benefits and drawbacks of implementing a shared licensing approach in the 42 GHz band. The NPRM proposes licensing the 42 GHz band as five 100 megahertz channels and seeks comment on other aspects of implementing a shared licensing approach, including coordination mechanisms, buildout requirements and technical rules.

Michael Calabrese, director of Wireless Future, Open Technology Institute at New America, said his organization agrees that a shared licensing framework is the best use of the 42 GHz band, making this spectrum available to a wide range of fixed wireless ISPs, enterprises and other users.

“Coordinated sharing will be particularly powerful if the FCC adopts a common framework for the lower 37 and 42 GHz bands, giving operators as much as 1100 megahertz of bandwidth,” he said in a statement provided to Fierce. “Fixed wireless deployments are exploding, adding options and competition for high-capacity broadband at lower prices. As open access bands, wide-channel millimeter wave spectrum can fuel and accelerate this positive trend.”

References:

https://www.fcc.gov/document/exploring-shared-use-42-425-ghz-band

https://docs.fcc.gov/public/attachments/DOC-393517A1.pdf

https://www.fiercewireless.com/wireless/fcc-eyes-42-ghz-shared-use

KDDI Deploys DriveNets Network Cloud: The 1st Disaggregated, Cloud-Native IP Infrastructure Deployed in Japan

Israel based DriveNets announced today that Japanese telecommunications provider KDDI Corporation has successfully deployed DriveNets Network Cloud as its internet gateway peering router. DriveNets Network Cloud provides carrier-grade peering router connectivity across the KDDI network, enabling KDDI to scale its network and services quickly, while significantly reducing hardware requirements, lowering costs, and accelerating innovation. Additional applications will be deployed on DriveNets Network Cloud in the future.

“KDDI prides itself on deploying the most advanced and innovative technology solutions that allow us to anticipate and respond to the ever-changing usage trends, while providing considerable value to our customers,” said Kenji Kumaki, Ph.D. General Manager and Chief Architect, Technology Strategy & Planning, KDDI Corporation. “DriveNets Network Cloud enables us to quickly scale our network as needed, while controlling our costs effectively.”

“While many of Japan’s service providers have been aggressively pursuing the virtualization of network functions on their 4G and 5G networks, disaggregation of software and hardware in service providers’ routing infrastructure is just getting started,” said Ido Susan, DriveNets’ co-founder and CEO. “I am extremely proud that our Network Cloud solution was selected by KDDI, a leading innovative service provider, and is already deployed in their network, supporting the needs of KDDI‘s customers.”

![]()

The deployment of DriveNets Network Cloud on the KDDI network is the culmination of several years of testing and verification in KDDI‘s labs. It also reflects the growing adoption of disaggregated network architectures in service provider networks around the world.

“The move to disaggregated networking solutions will continue to be a prevailing trend in 2023 and beyond as savvy service providers try new technologies that can enable them to innovate faster and reduce costs. We are now seeing this technology also adopted in other high-scale networking environments, such as AI infrastructures,” said Susan.

DriveNets Run Almog wrote in an email, “KDDI is using white box devices from Delta. These are the “same” OCP compliant NCP devices which are deployed at AT&T (UFISpace in the AT&T case). they are using it as a peering router (vs. AT&T’s core use case). so this announcement is public indicative to several things: a 2nd Tier #1, another use case, and another ODM vendor, all in commercial deployments with our network cloud.”

DriveNets Inbar Lasser-Raab wrote in an email, “Getting a tier-1 SP to announce is very hard. They are cautious and our solution needs to be working and validated for some time before they are willing to talk about it. We are working on our next PR, but you never know when we’ll get the OK to release” ![]()

Compared to traditional routers that are comprised of software, hardware and chips from a single vendor, a DDBR solution combines software and equipment from multiple vendors, allowing service providers to break vendor lock and move to a new model that enables greater vendor choice and faster scale and introduction of new services through modern cloud design.

In addition to KDDI, DriveNets is already working with other service providers in Asia Pacific to meet the growing interest in its disaggregated networking solutions in the region. In mid-2021, the company established a Tokyo-based subsidiary to enhance its presence in the region.

DriveNets offers an architectural model similar to that of cloud hyperscalers, leading to better network economics and faster innovation. DriveNets Network Cloud includes an open ecosystem with elements from leading silicon vendors and original design manufacturers (ODMs), certified by DriveNets and empowered by our partners, which ensure the seamless integration of the solutions into providers’ networks.

About DriveNets:

DriveNets is a leader in cloud-native networking software and network disaggregation solutions. Founded at the end of 2015 and based in Israel, DriveNets transforms the way service and cloud providers build networks. DriveNets’ solution – Network Cloud – adapts the architectural and economic models of cloud to telco-grade networking. Network Cloud is a cloud-native software that runs over a shared physical infrastructure of white-boxes, radically simplifying the network’s operations, increasing network scale and elasticity and accelerating service innovation. DriveNets continues to deploy its Network Cloud with Tier 1 operators worldwide (like AT&T) and has raised more than $587 million in three funding rounds.

About KDDI:

KDDI is telecommunication service provider in Japan, offering 5G and IoT services to a multitude of individual and corporate customers within and outside Japan through its “au”, “UQ mobile” and “povo” brands. In the Mid-Term Management Strategy (FY23.3–FY25.3), KDDI is promoting the Satellite Growth Strategy to strengthen the 5G-driven evolution of its telecommunications business and the expansion of focus areas centered around telecommunications.

Specifically, KDDI is especially focusing on following five areas: DX (digital transformation), Finance, Energy, LX (life transformation) and Regional Co-Creation. In particular, to promote DX, KDDI is assisting corporate customers in bringing telecommunication into everything through IoT to organize an environment in which customers can enjoy using 5G without being aware of its presence, and in providing business platforms that meet industry-specific needs to support customers in creating businesses.

In addition, KDDI places “sustainability management” that aims to achieve the sustainable growth of society and the enhancement of corporate value together with our partners at the core of the Mid-Term Management Strategy. By harnessing the characteristics of 5G in order to bring about an evolution of the power to connect, KDDI is working toward an era of the creation of new value.

References:

https://drivenets.com/products/

IEEE/SCU SoE May 1st Virtual Panel Session: Open Source vs Proprietary Software Running on Disaggregated Hardware

DriveNets raises $262M to expand its cloud-based alternative to core network routers

AT&T Deploys Dis-Aggregated Core Router White Box with DriveNets Network Cloud software

DriveNets Network Cloud: Fully disaggregated software solution that runs on white boxes

KDDI claims world’s first 5G Standalone (SA) Open RAN site using Samsung vRAN and Fujitsu radio units

Cisco and AT&T to expand connectivity for hybrid workforces

Cisco and AT&T today announced new solutions to enhance connectivity and advance the calling landscape for hybrid workforces. Whether on the shop floor, the top floor, at the branch office, the home office, or the commute in between, the modern workforce is not tethered to a single space, device, or geography. With the new offerings, including Cisco’s Webex Calling and SD-WAN solutions alongside AT&T mobile network, businesses of any size can offer employees a simple, secure, consistent experience to thrive in any setting.

The companies today announced plans that will help ensure a seamless and reliable mobile-first collaboration experience, allowing users the flexibility to take calls across multiple devices while traveling for work, running errands, and more.

With the dramatic increase in the use of mobile phones as the primary business device, enterprises need connectivity solutions that are easy to manage, secure, and provide the flexibility and reliability desired for work from anywhere. This integration addresses this need with key features including:

- Single number mobile identity: Combining the capabilities of an AT&T wireless smartphone with the native integration of Webex Calling will provide greater functionality and flexibility for on-the-go communication.

- Reduce costs: This integration helps enterprise customers lower costs by reducing or eliminating the need for traditional fixed business lines.

- Crystal clear voice: AT&T Cloud Voice with Webex Go allows users to securely make and receive business calls using AT&T’s fast, reliable nationwide mobile network and seamlessly elevate calls to a fully immersive Webex collaboration experience across the Webex App and devices1, with capabilities like closed captioning, noise removal, and white boarding.

- Fast, efficient, and secure collaboration: AT&T and Cisco’s joint solution will increase the ability to effectively and securely collaborate no matter the location, resulting in improved knowledge sharing and faster decision making.

AT&T Cloud Voice with Webex Go2 will be available for all Webex Calling users from Cisco partners in the United States later this year.

SD-WAN Connectivity without Compromise:

Demand for unified experiences over secure connectivity to the cloud and site-to-site continues to surge. Cisco and AT&T are working together to bring secure on-demand connectivity for SD-WAN with add-on services that may include over mobile 5G and fiber broadband to businesses of every size.

For small and medium businesses, AT&T is launching a new self-service option to simplify and accelerate SD-WAN deployment. Businesses can now easily connect, protect, manage, and scale their networks using AT&T Business Wi-Fi with Cisco Meraki.

For larger enterprises, AT&T SD-WAN with Cisco is a fully managed connectivity solution with embedded security and analytics. Enterprises can now confidently connect a user or device to any application in their multicloud using a secure access service edge (SASE)-enabled architecture. This delivers integrated security and application optimization for end-to-end visibility.

Cisco will also provide the ability to embed AT&T wireless connectivity into Cisco devices enabling zero touch provisioning for Cisco and AT&T customers, through AT&T Control Center powered by Cisco.

“The network is at the core of the modern workforce. The ability to get things done is no longer reliant on where you are, but how you are connected,” said Jonathan Davidson, Executive Vice President and General Manager of Cisco Networking. “Hybrid work only works when there is a seamless, consistent, and secure experience for workers, regardless of location. Together with AT&T, we are giving businesses what they need to securely connect everything and everyone—wherever they are. Because when everything is connected, then anything is possible.”

“Mobility is key to enabling hybrid work. Businesses want a seamless and reliable communication experience,” said Mike Troiano, Senior Vice President, Business Products, AT&T. “At the heart of our collaboration with Cisco is a shared vision to empower organizations with secure connectivity, unmatched reliability, and deep network expertise. By deeply integrating our technology, businesses can be assured their communications are built on a solid foundation. Together we are unlocking new levels of productivity, agility, and connectivity— enabling teams to thrive in the modern work landscape.”

Webex Go with AT&T’s Mobile Network

About AT&T:

We help more than 100 million U.S. families, friends and neighbors, plus nearly 2.5 million businesses, connect to greater possibility. From the first phone call 140+ years ago to our 5G wireless and multi-gig internet offerings today, we @ATT innovate to improve lives. For more information about AT&T Inc. (NYSE:T), please visit us at about.att.com. Investors can learn more at investors.att.com.

About Cisco:

Cisco is the worldwide technology leader that securely connects everything to make anything possible. Our purpose is to power an inclusive future for all by helping our customers reimagine their applications, power hybrid work, secure their enterprise, transform their infrastructure, and meet their sustainability goals. Discover more on The Newsroom and follow us on Twitter at @Cisco.

Spark New Zealand partnering with Lynk Global to offer a satellite-to-mobile service

Spark, the leading telco in New Zealand, announced it is collaborating with Lynk Global to offer a satellite-to-mobile service, aiming to enhance connectivity for its customers. Later this year, selected customers will be offered a free trial of the service.

The satellite-to-mobile service will enable periodic text messaging throughout the day during the initial trial. However, as more commercial satellites are deployed, Spark intends to expand the service in 2024 to offer more regular connectivity. The ultimate goal is to provide voice and data services to customers once they become reliably available.

Spark said while satellite coverage cannot reach 100 percent due to the requirement of a clear line of sight to the sky, it offers an additional layer of resilience, especially in light of increasingly severe and frequent weather events caused by climate change. By leveraging satellite connectivity, Spark aims to extend its network reach to areas that are currently underserved by traditional mobile coverage.

According to the Spark press release, the trial period will provide an opportunity to refine and enhance the service in alignment with the increasing number of satellites in orbit. Integration into Spark’s network and regulatory approval are also essential steps before the service can be officially launched.

Photo Credit: Spark New Zealand

The collaboration with Lynk Global and the existing partnership with Netlinkz, which aims to provide satellite broadband services, are part of Spark’s broader strategy to leverage satellite technology as part of its connectivity offering to customers. Spark says it is actively working with various partners to expand the range of services it can deliver.

In a separate announcement last week, Spark revealed its partnership agreement with Netlinkz to provide Starlink business-grade satellite broadband to customers later this year. This initiative follows ongoing trials with a select number of New Zealand businesses.

Spark Product Director, Tessa Tierney, said, “We believe satellite has an important role to play in connecting Aotearoa New Zealand. While satellite can’t provide 100% coverage – as you need a clear line of sight to the sky to get connected2 – it certainly adds an additional layer of resilience, particularly now, as we face increasingly severe and frequent weather events due to climate change. And once there are more satellites launched and the service is available more broadly, it will allow our mobile customers to start to use their phones in more areas that aren’t reached by traditional mobile coverage.”

“We know that our customers will be eager to start using satellite messaging, but the technology is still evolving, so the service and experience will improve and expand as the number of satellites in the sky increases. That’s why we’ve chosen to trial this technology with some of our customers first, to make sure we can offer a great product to our customers when we make it widely available. We also need to integrate the technology into our network and achieve regulatory approval to launch the service. But we are excited to see the possibilities this creates for New Zealanders and will be working hard to make it widely available as soon as we can.

“This partnership with Lynk, and our partnership with NetLinkz to offer a satellite business connectivity service are part of Spark’s broader strategy to use satellite as a part of our connectivity offer to customers. We are continuing to work with these and other potential partners to broaden the services Spark can offer.”

Spark’s introduction of satellite-to-mobile services and business-grade satellite broadband underscores its commitment to enhancing connectivity options for customers across the country, particularly in underserved areas. Spark said further details, including eligibility criteria and timelines, will be disclosed in the coming months.

………………………………………………………………………………………………………………………………………………………………………..

References:

https://www.sparknz.co.nz/news/Spark-to-launch-satellite-to-mobile-service/

Spark New Zealand to Launch Satellite-To-Mobile Service With Lynk Global

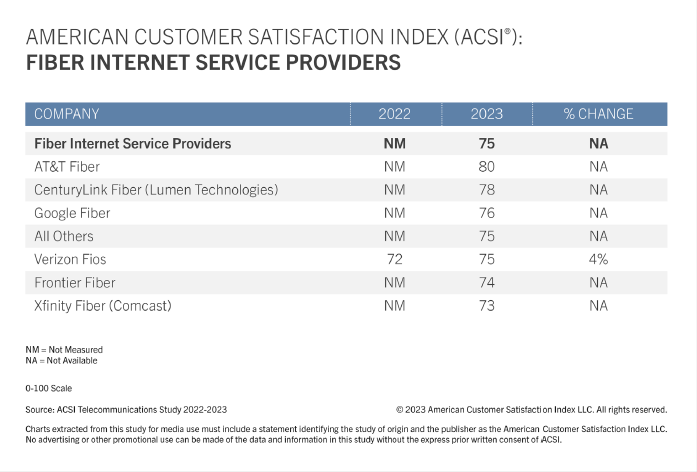

ACSI report: AT&T, Lumen and Google Fiber top ranked in fiber network customer satisfaction

AT&T is #1 in customer satisfaction for fiber optic network providers, according to a new report from the American Customer Satisfaction Index (ACSI). ACSI’s report rates consumer satisfaction for both fiber and non-fiber ISPs as well as for video streaming services and apps. For this study, ACSI interviewed more than 22,000 customers at random between April 2022 and March 2023.

AT&T Fiber tops fiber ISPs — and the entire industry — with a score of 80. CenturyLink (Lumen) Fiber is next at 78, followed by Google Fiber (76). The smaller group of fiber ISPs and Verizon Fios both score 75. Frontier Fiber and Xfinity Fiber round out the fiber ISPs at 74 and 73, respectively.

AT&T is targeting a few cities across Arizona and Nevada with its Gigapower joint venture, in partnership with BlackRock. Whereas Lumen just upped multi-gig coverage in its Quantum Fiber markets and Google Fiber announced several forthcoming builds.

Among non-fiber ISPs, T-Mobile takes the top spot with a score of 73. AT&T Internet finishes second at 72, while ACSI newcomer Sparklight sits in third place at 71. Kinetic by Windstream is next at 70, just outperforming Xfinity (68).

Despite an impressive showing among fiber ISPs, Lumen sits near the bottom in the non-fiber group with a score of 62. Frontier Communications and Optimum round out the non-fiber ISPs at 61 and 58, respectively.

“Across the entire customer experience, fiber service shows a strong advantage — from data transfer speed and service reliability to touchpoints like call centers and websites,” says Forrest Morgeson, Assistant Professor of Marketing at Michigan State University and Director of Research Emeritus at the ACSI. “That said, with well over half of U.S. households lacking access to fiber internet, availability remains a sticking point. As such, non-fiber ISP services remain an attractive option for many customers and should not be overlooked by providers.”

…………………………………………………………………………………………………………………………………………………………………

Fiber sets the pace for in-home Wi-Fi quality:

ACSI also measures key aspects of the in-home Wi-Fi experience for both customers who use equipment from their ISP and those who use third-party equipment that they have purchased.

Fiber ISPs (79) outperform both non-fiber ISPs (73) and third-party equipment providers (70) for overall Wi-Fi quality. The former far exceeds the other two in every customer experience benchmark, including strong marks for the security of its Wi-Fi connection (81) and reliability in terms of avoiding loss of service (80).

References:

No Surprise: AT&T tops leaderboard of commercial fiber lit buildings for 7th year!

AT&T expands its fiber-optic network amid slowdown in mobile subscriber growth

AT&T and BlackRock’s Gigapower fiber JV may alter the U.S. broadband landscape

Charter Communications selects Nokia AirScale to support 5G connectivity for Spectrum Mobile™ customers

Nokia will deliver its AirScale portfolio, including 5G Radio Access Network (RAN), to support Charter Communications’ 5G rollout in trial markets. It marks Nokia’s first win in the cablecos/MSO space for large-scale wireless 5G deployments. Charter will use Nokia’s 5G RAN solutions to deliver wireless 5G connectivity, faster speeds, and increased network capacity to Spectrum Mobile customers in its trial markets in the United States.

Up until now, cablecos have been MVNO rather than actually deploying their own wireless networks. All of the cable companies in the U.S. with mobile aspirations have had to partner with an existing mobile network operator – Verizon, AT&T or T-Mobile – to sell mobile services. And those MVNO partnerships are not cheap. For example, the financial analysts at Wells Fargo estimate that Charter and Comcast pay Verizon $12-$13 per month for each of their mobile customers.

Cable operators have spent more than $1 billion on Citizens Broadband Radio Service (CBRS) spectrum with the intention to build 5G networks to offload traffic from their leased mobile networks and to deliver the fastest wireless service. Using compact and lightweight small cell products, cable operators can more easily and cost-effectively provide 5G wireless connectivity by leveraging their existing DOCSIS infrastructure without having to build additional cell sites.

With 6 million customer lines as of Q1-2023, Charter’s Spectrum Mobile is the nation’s fastest growing mobile network provider. Charter offers its Spectrum Mobile service through an MVNO deal with Verizon but touts its ability to combine that with its Wi-Fi network. It’s also using Citizens Broadband Radio Service (CBRS) spectrum to offload mobile traffic from the leased network. Charter spent more than $464 million in the CBRS auction in 2020.

As Charter continues to grow its mobile customers, the company needed a 5G wireless connectivity solution to offload traffic from its leased mobile network. Charter will deploy Nokia’s 5G RAN products, including strand mounted radios for CBRS, baseband units, and a newly developed 5G CBRS Strand Mount Small Cells All-in-One portfolio on the company’s assets, which will help Charter continue to deliver mobile traffic in strategic locations across its 41-state footprint while providing customers with the best possible 5G service experience.

Justin Colwell, EVP, Connectivity Technology at Charter Communications, said: “Charter is committed to providing our customers a fully converged connectivity experience that combines high value plans with the fastest wired and wireless speeds throughout our footprint. Incorporating Nokia’s innovative 5G technology into our advanced wireless converged network will help us ensure that Spectrum customers in areas with a high concentration of mobile traffic continue to receive superior mobile connectivity, including the nation’s fastest wireless speeds.”

Shaun McCarthy, President of North America Sales at Nokia, said: “This news builds on our more than 20-year relationship working with Charter to enhance its network. We are excited to expand its current trial to additional select metropolitan markets in the US, enabling an enhanced user experience for Spectrum Mobile subscribers. This win strengthens Nokia’s leadership position in the MSO space for 5G wireless deployments.”

Nokia in the U.S.

Nokia is supplying 5G technologies across its portfolio to the major service providers and leading operators, as well as hyperscalers, enterprises, and government organizations in the US. The company has an unrivaled track record of innovation in the U.S. including Nokia Bell Labs, which pioneered many of the fundamental technologies that are being used to develop 5G and broadband standards. Today, more than 90 percent of the U.S. population is connected by Nokia network solutions.

*Based on year end 2022 subscriber data among top 3 cellular carriers.

………………………………………………………………………………………………………………………………………………………

Nokia may have competition in the CBRS/MSO space. Samsung will be introducing a new solution within its already existing CBRS portfolio: a new 5G CBRS Strand Small Cell. Designed to be easily deployed on the MSOs aerial strand assets, it enables use of their existing infrastructure, helping them save on deployment costs.

References:

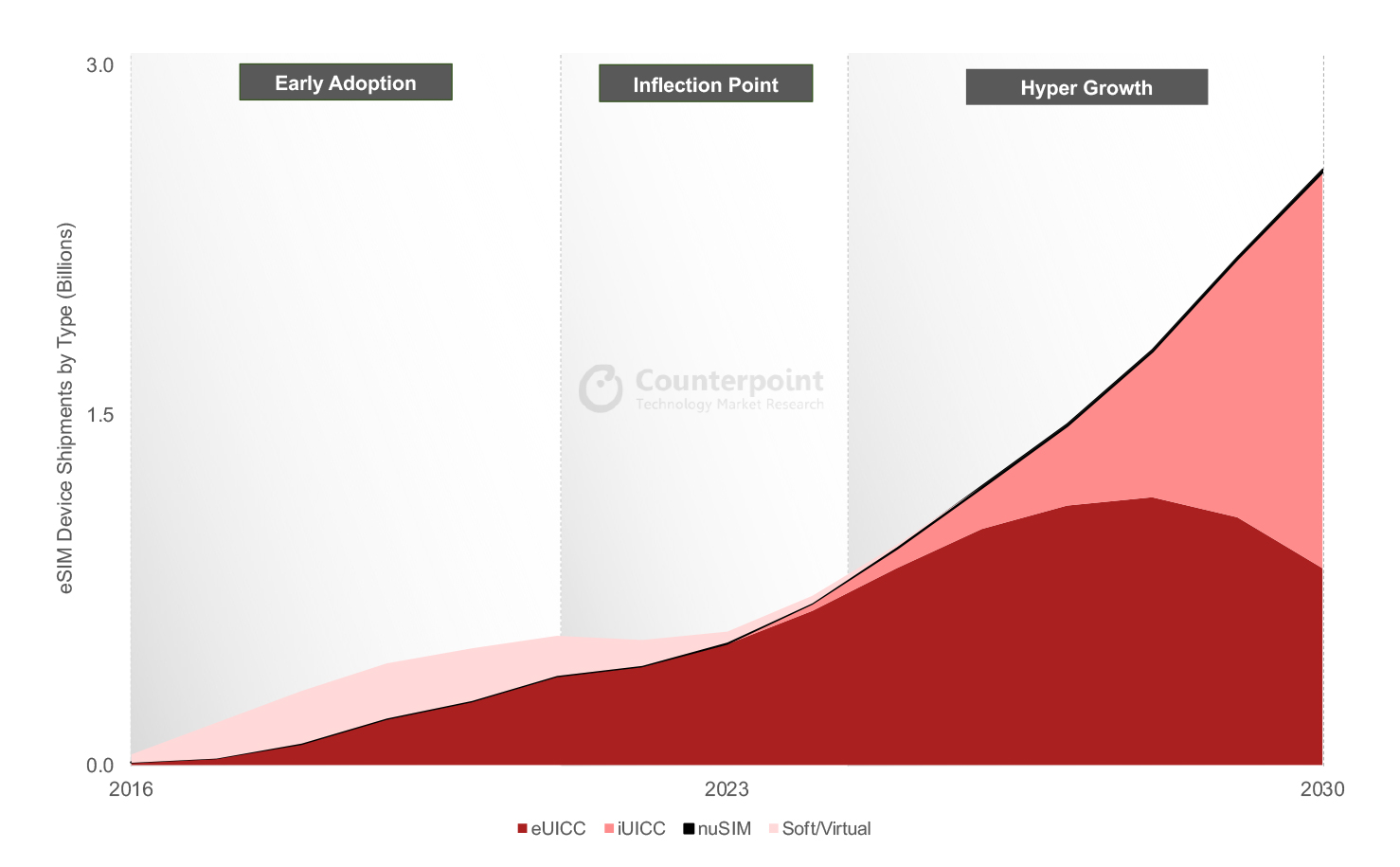

Counterpoint Research: eSIM adoption now entering high-growth phase; +11% YoY in 2022

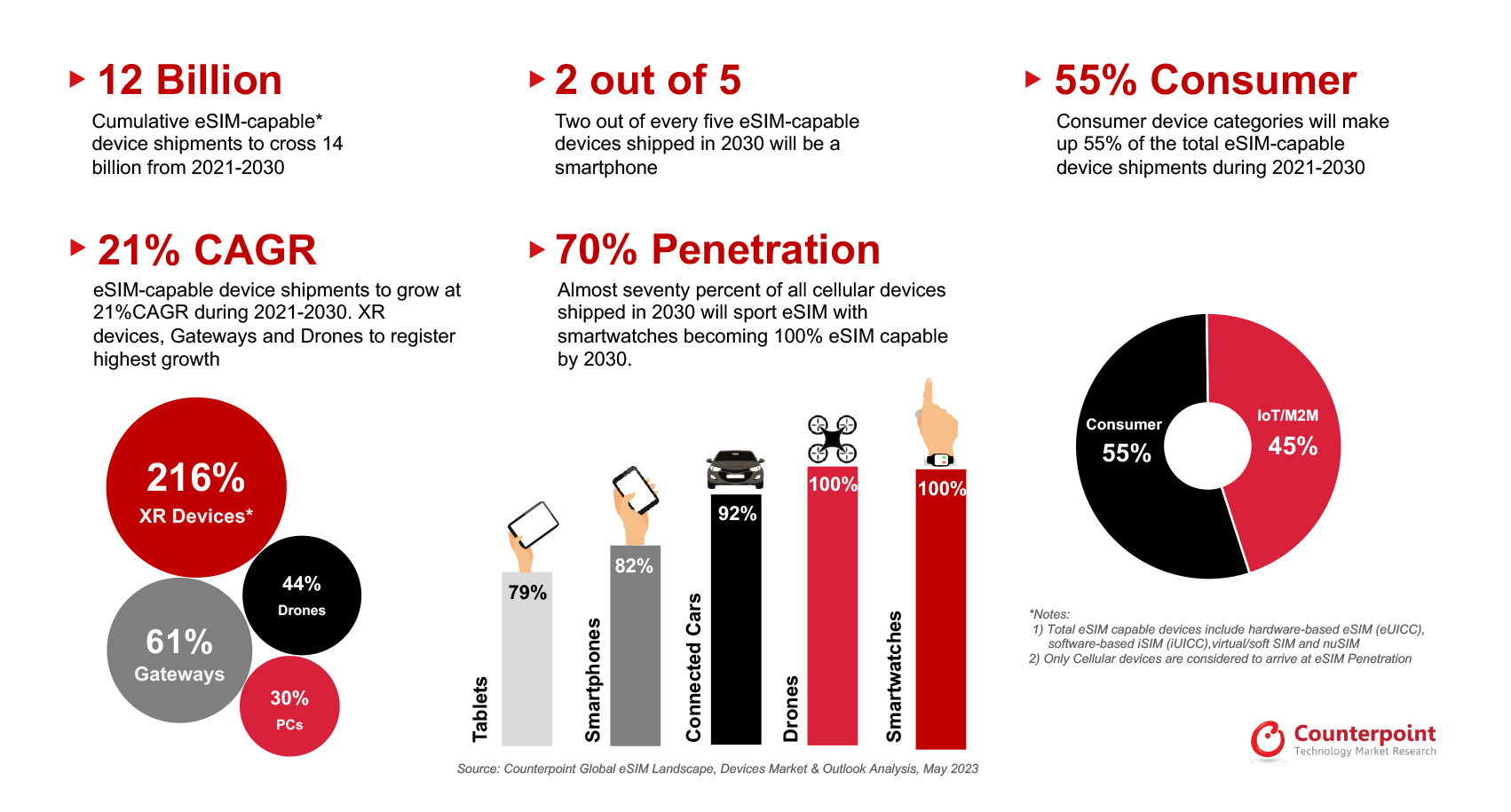

More than 6 billion xSIM (eSIM + iSIM) capable devices will be cumulatively shipped over the next five years, covering all form factors including hardware-based eSIM (eUICC), iSIM (iUICC), nuSIM and Soft SIM, according to Counterpoint’s latest eSIM Devices Market Outlook report.

Editor’s Note: An embedded SIM card – or eSIM – is pre-installed in a device and cannot be physically swapped. Instead, it is programmed remotely and can hold several SIMs at the same time. An integrated SIM (iSIM), meanwhile, is integrated in a device’s main processor, doing away with any form of dedicated hardware.

eSIM adoption has passed the inflection point and is now entering a high-growth phase, driven by the rising adoption of eSIM in smartphones, connected vehicles and cellular IoT applications. The next phase of growth will be driven by greater awareness of eSIM among mobile network operators (MNOs) and device manufacturers, facilitated by the flexibility, cost efficiency, security, cost savings and above all, the key role eSIM is playing in the digital transformation of MNOs.

In 2022, eSIM-capable device shipments grew 11% YoY to reach 424 million units despite a 3% YoY fall in overall cellular-connected device shipments due to weaker demand for smartphones. Globally, more than 275 MNOs support eSIM and provide connections to 30+ different eSIM-capable consumer device models on average. Furthermore, the number of cellular IoT modules and devices is continuously growing.

By 2030, 70% of all cellular devices are expected to support eSIM technology. Adoption will reach 100% in the smartwatch and drone segments; 92% for connected cars; 82% for smartphones; and 79% for tablets. Around 40% of eSIM devices will be smartphones, while 55% of eSIM devices shipped between 2021 and 2030 will be consumer devices.

Commenting on the outlook for xSIM-capable device shipments, Research Vice President Neil Shah said, “The physical MFF2/WLCSP form-factor soldered eSIM chip has been the go-to standard for eSIM implementation alongside the other niche alternative implementations such as soft SIM and nuSIM. Over the next five years, hardware-based eSIM (eUICC) will remain the dominant eSIM form factor and will account for more than half of all shipments.”

“The first wave of mainstream iSIM adoption will be seen across IoT applications driven by leading IoT chipset and module players such as Quectel, Telit, Sequans and Sony Semi (Altair) in partnership with leading xUICC players like Kigen, G+D and Thales. Other key stakeholders driving the adoption of iSIMs would include Qualcomm, IDEMIA, Truphone, Redtea Mobile, Oasis SmartSIM, Apple, Samsung and Nokia. Beyond 2028, iSIM is projected to take over as the dominant SIM form factor, with the shipments of iSIM-capable devices poised to climb to a cumulative 4 billion units by 2030.”

eSIM Has Reached an Inflection Point, Set to Enter a Period of Hyper-Growth

Source: Global eSIM Landscape – Market Outlook and Forecast

Commenting on eSIM adoption across different device categories, Senior Analyst Ankit Malhotra said, “Smartphones have been key in driving primary eSIM awareness among consumers and MNOs, and will continue to be the dominant eSIM-capable device category. Cellular connectivity in smartwatches is growing steadily which is also helping increase the penetration of eSIM-supported smartwatches. The adoption of entitlement servers by MNOs worldwide is a testament to the growing number of smartwatches and other companion devices powered by eSIM. Other cellular-capable consumer devices such as laptops and tablets will also see rapid eSIM adoption in the coming years.”

“The number of IoT/M2M devices equipped with eSIM is poised to grow faster than consumer device categories due to the natural cost, space and remote device management benefits that eSIM offers. The new eSIM IoT specifications SGP.31 by GSMA will accelerate eSIM adoption in the IoT segments potentially eradicating complexities of the existing eSIM Remote Service Provisioning (RSP) platform SM-DP/SM-SR for M2M/IoT segments.”

eSIM Devices Forecast and Analysis

Emerging device categories such as XR, drones and cellular gateways/FWA CPEs will be the fastest-growing categories. 5G-connected drones are another category that will benefit from eSIM technology and drive adoption across several use cases like last-mile delivery, disaster management, search and rescue, education, construction and agriculture. Regulation of beyond-visual-range drones in regions such as Europe will increase the adoption of eSIMs as well.

Automotive and smart mobility are huge growth areas as well. Connected cars are one of the largest and most obvious use cases for eSIMs. Consistent connectivity experience for mobility applications is becoming paramount, particularly for safety use cases such as eCall and the future rise of autonomous driving.

………………………………………………………………………………………………………………………………………………………………………………..

According to Omdia (owned by Informa), there is a compelling business case (subscription required) for eSIMs in the IoT market as they could help resolve connectivity issues plaguing enterprises. Some of the areas that could benefit include energy, healthcare and the financial sector, Omdia says.

Counterpoint forecasts iSIM will become the predominant type of SIM post-2028, with cumulative device shipments to reach 4 billion by 2030. Initial demand will come mainly from IoT applications, it says.

According to Omdia, the iSIM can alleviate issues such as chip shortages, energy and size constraints and increased security concerns. It also notes that cellular service providers such as AT&T, Vodafone and Deutsche Telekom have shown more enthusiasm for iSIMs than eSIMs.

References:

eSIM-Capable Devices Set for Hyper-Growth After Crossing Inflection Point

https://www.t-mobile.com/resources/what-is-an-esim-card

https://www.nytimes.com/2023/03/23/technology/personaltech/esim-sim-cards-travel.html

Orange Spain & Ericsson to build 5G Infrastructure for 3 High-Speed Rail Lines

In a statement, Orange highlighted it had won two of the three lots tendered by the transport infrastructure entity ADIF. It claimed its proposals for the lots received “the highest score” and its bids topped those from Vodafone.

In partnership with Ericsson, which is also supplying kit for Vodafone’s deployment, Orange will provide and maintain 5G infrastructure across the high speed rail corridors.

Announcing the award of its contracts, ADIF said it was part of attempts to “promote the digitisation and efficiency of the railway system” with the entity committing €117.3 million to deployment of 5G on the network and within its assets.

Alongside advantages for passengers, the organisation hailed 5G as a “critical catalyst in the digitisation of the economy in the coming years”.

Within the rail industry, it pointed to use cases including advanced logistics; real-time traffic management; automated vehicles; predictive maintenance; and improved surveillance in stations and on trains.

Orange says it is the first operator to launch 5G+, a network that consumes 90 percent less energy. Some of the notable sustainability initiatives undertaken by Orange include:

- 100% Green Energy Consumption: Since 2014, Orange has exclusively relied on green energy sources to power its operations, reinforcing their dedication to environmental responsibility.

- Device Recycling and Repair Program: Orange has implemented an ambitious program focused on recycling and repairing devices at their points of sale. By extending the lifespan of devices, they actively contribute to reducing electronic waste.

- Eco-Guidelines for Sustainable Practices: Orange has established eco-guidelines to encourage sustainable actions in their day-to-day operations. These guidelines serve as a roadmap, guiding employees in adopting environmentally friendly practices, even in the smallest gestures.

The ongoing efforts of Orange to promote sustainability demonstrate their commitment to mitigating their environmental impact. By integrating green energy, recycling and repair programs, and fostering sustainable practices, Orange is leading by example in its pursuit of a more sustainable future.

…………………………………………………………………………………………………………………………………………..

Separately, Orange Belgium has completed its acquisition of a controlling stake in telco operator, VOO SA. The closing of this deal will give Orange Belgium a 75% stake minus 1 share in VOO SA, with the remaining 25% plus one share retained by Nethys.

This transaction values VOO at an enterprise value of €1.8 billion for 100% of the capital. Orange Belgium will finance this transaction through an intra-Group loan.

Xavier Pichon, CEO of Orange Belgium, comments: “For decades, we developed our telecom skills and pioneering spirit to challenge the market, but as from today, we have the industrial power, tech means and commercial scale to accelerate and Lead the Future of the Belgian telco market in the interest of all consumers, employees and society in general.”

References:

Orange Launches 5G+ Network With Reduced Energy Consumption in Spain