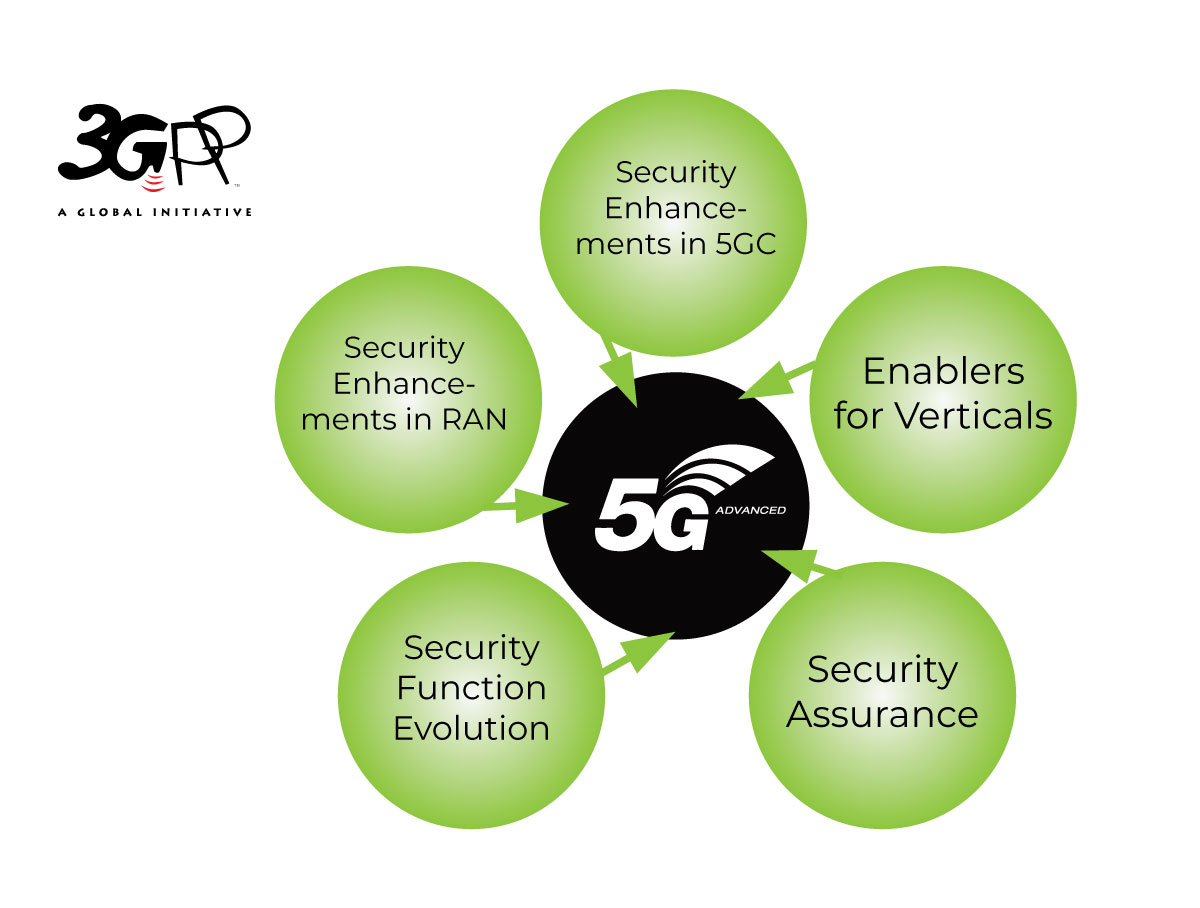

5G Advanced

Huawei unveils AI Centric Network roadmap, U6 GHz products, 5G Advanced strategy and SuperPoD cluster computing platforms

Missing from all the MWC 2026 6G AI alliance announcements, Huawei released a series of all-scenario U6 GHz products to help carriers unlock the full potential of 5G Advanced (5G-A) and set the stage for a seamless transition to 6G. Huawei also showcased its SuperPoD cluster for the first time outside China, which they have created to offer “a new option for the intelligent world.”

- The all-scenario U6 GHz products and solutions Huawei released today use innovative technologies to create a high-capacity, low-latency, optimal-experience backbone designed for mobile AI applications.

- There are already 70 million 5G-A users globally, and 5G-A is increasingly being adopted by carriers at scale. In China, Huawei has helped carriers deliver contiguous 5G-A coverage across 270 cities and launch 5G-A packages that monetize experience in over 30 provinces.

The company also launched enhanced AI-Centric Network solutions [1.] that will help carriers prepare for the agentic era by enabling intelligent services, networks, and network elements (NEs). The company’s plans to build more AI-centric networks and computing backbones that will help carriers and industry customers seize opportunities from the AI era.

Note 1. Huawei’s AI-Centric Network roadmap is designed to integrate intelligence directly into 5G-Advanced (5G-A) infrastructure and accelerate the transition toward Level-4 Autonomous Networks. The company plans to work with global carriers (where its not blacklisted) on the large-scale 5G-A deployment, use high uplink to address surging consumer and industry demand for mobile AI applications, and use the U6 GHz band to unlock the full value of spectrum and pave the way for smooth evolution to 6G.

Photo Credit: Huawei

………………………………………………………………………………………………………………

Three-Layer Intelligence in AI-Centric Networks: Accelerating the Agentic Era:

As mobile network operators transition toward AI-native 5G-Advanced and early 6G architectures, Huawei is positioning its AI-Centric Network portfolio as the blueprint for next-generation intelligent networks. By embedding intelligence across service, network, and network element (NE) layers, Huawei aims to establish the foundation for fully agentic, autonomously managed infrastructures.

- Service Layer: Focuses on multi-agent collaboration platforms to transform core carrier services—such as voice and home broadband—into intelligent service platforms.

- Network Layer: Aims to evolve from single-scenario automation to end-to-end single-domain network autonomy. Huawei officially launched AUTINOps, an AI-native intelligent operations solution designed to replace traditional manual O&M with predictive, preventive “digital employees”.

- Network Element (NE) Layer: Utilizes AI to optimize algorithms for RANs (Radio Access Networks) and core networks, improving spectral efficiency and service awareness.

At the Service layer, Huawei is enabling carriers to operationalize multi-agent collaboration frameworks that embed domain-specific intelligence into key service categories: voice, broadband, and digital experience monetization. These AI agents dynamically manage customer experience and lifecycle value, supporting the transformation of core connectivity services into intelligent, context-aware digital offerings.

At the Network layer, the company’s Autonomous Driving Network Level 4 (ADN L4) initiative focuses on single-scenario automation, delivering measurable improvements in O&M efficiency, service quality, and monetization agility. By the close of 2025, ADN single-scenario deployments were active across more than 130 commercial telecom networks. The next phase targets end-to-end, single-domain autonomy across transport, access, and core networks—an essential step toward zero-touch O&M and intent-driven orchestration in 5G-A and 6G environments.

At the Network Element layer, Huawei is jointly advancing AI-driven innovation across RAN, WAN, and core domains. This includes algorithmic optimization for intelligent RAN scheduling, service-aware traffic identification in WANs, and unified intent modeling across B2C and B2H use cases. Such capabilities enhance spectral and energy efficiency, enable predictive resilience, and provide fine-grained service awareness—all foundational for AI-native air interface and network control in 6G.

Computing Backbone with SuperPoD Clusters:

Supporting this vision, Huawei is introducing its next-generation SuperPoD and cluster computing platforms, designed as high-performance compute backbones for distributed AI model training and inference within telecom and enterprise domains. Featuring the proprietary UnifiedBus interconnect and system-level architecture innovations, the Atlas 950, TaiShan 950, and Atlas 850E SuperPoDs, along with the TaiShan 200–500 servers, deliver ultra-low latency and high throughput optimized for trillion-parameter AI models and real-time agentic operations.

Aligned with its open innovation strategy, Huawei continues to expand an open, collaborative computing ecosystem, supporting open-source frameworks and open-access platforms to accelerate the deployment of intelligent, AI-driven digital infrastructure worldwide.

Intelligent Transformation Across Industry Domains:

At MWC Barcelona 2026, Huawei is highlighting 115 end-to-end industrial intelligence showcases across verticals, underscoring its role in helping enterprises adopt AI-centric operational models. Through the SHAPE 2.0 Partner Framework, 22 co-developed AI and digital infrastructure solutions will demonstrate how vertical industries—from manufacturing and energy to transportation and healthcare—can harness 5G-A and AI integration to deliver measurable business outcomes.

Toward 5G-A Commercialization and 6G Evolution:

With large-scale 5G-Advanced rollouts accelerating, Huawei is collaborating with global carriers and ecosystem partners to realize level-4 autonomous networks and establish the architectural bridge to 6G. Central to this evolution is the convergence of AI, connectivity, and computing—enabling networks that can self-learn, self-optimize, and autonomously orchestrate service intent. These AI-Centric Network initiatives and SuperPoD-based computing backbones form the foundation for value-driven, intelligent networks built for the agentic era.

5G-Advanced and Infrastructure Innovations:

Huawei’s 5G-A strategy, branded as GigaUplink, focuses on delivering the high-uplink capacity and low latency required for mobile AI applications:

- U6 GHz Spectrum: Launched a comprehensive portfolio of all-scenario U6 GHz products to unlock 5G-A’s full potential and provide a smooth evolution path to 6G.

- Agentic Core: Introduced the Agentic Core solution, which integrates intelligence natively into the core network to support ubiquitous AI agent access across devices.

- All-Optical Target Network: Proposed an AI-centric optical roadmap featuring dual strategies: “AI for networks” (optimizing operations) and “networks for AI” (supporting AI workloads with ultra-low latency benchmarks of 1-5ms).

………………………………………………………………………………………………………………………………………………………..

References:

https://www.huawei.com/en/news/2026/3/mwc-ai-centric-network

https://carrier.huawei.com/en/minisite/events/mwc2026/

Huawei FY2025: 2.2% YoY revenue increase; strategic pivot to AI & Automotive

NVIDIA and global telecom leaders to build 6G on open and secure AI-native platforms + Linux Foundation launches OCUDU

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Huawei, Qualcomm, Samsung, and Ericsson Leading Patent Race in $15 Billion 5G Licensing Market

Huawei Cloud Review and Global Sales Partner Policies for 2026

Huawei’s Electric Vehicle Charging Technology & Top 10 Charging Trends

Huawei to Double Output of Ascend AI chips in 2026; OpenAI orders HBM chips from SK Hynix & Samsung for Stargate UAE project

Huawei launches CloudMatrix 384 AI System to rival Nvidia’s most advanced AI system

U.S. export controls on Nvidia H20 AI chips enables Huawei’s 910C GPU to be favored by AI tech giants in China

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

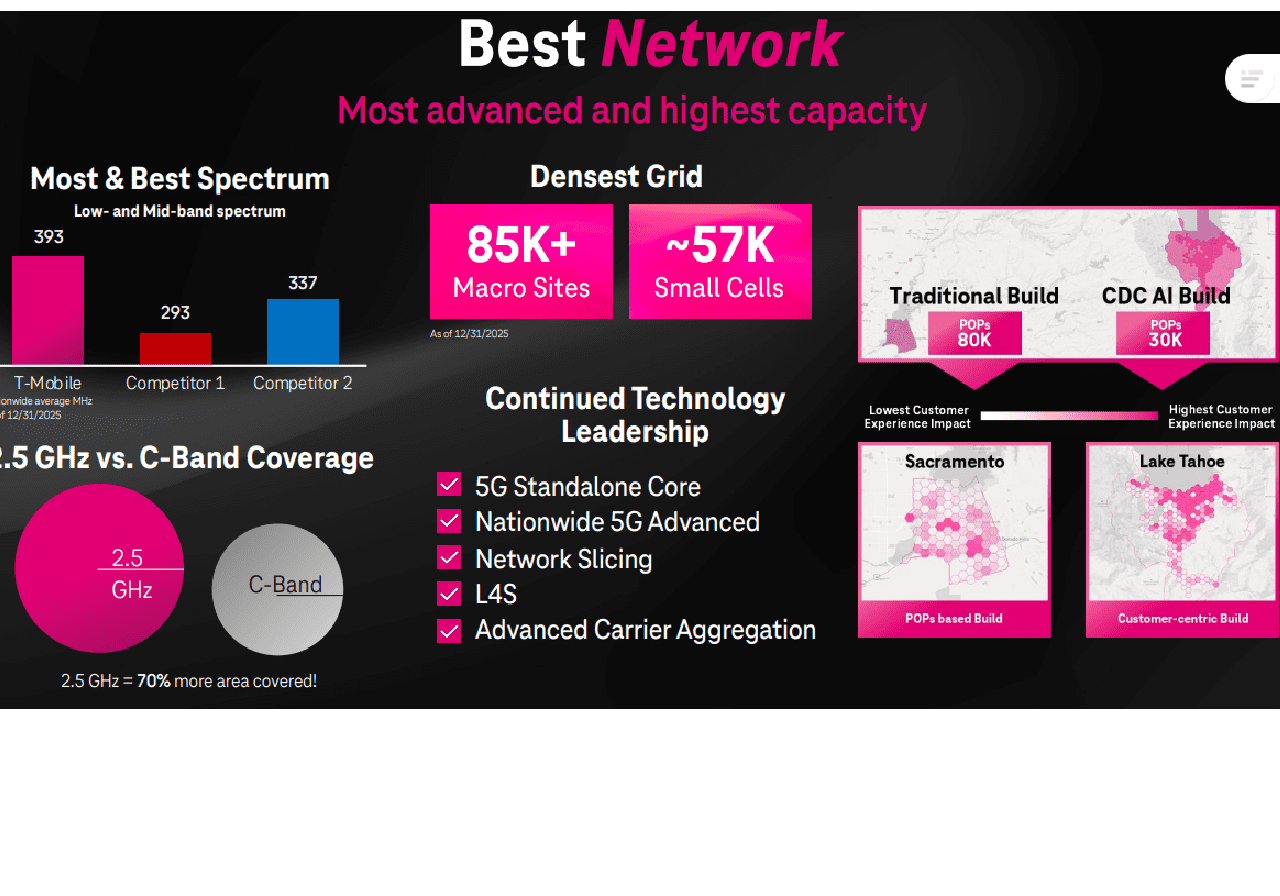

T-Mobile US announces new broadband wireless and fiber targets, 5G-A with agentic AI and live voice call translation

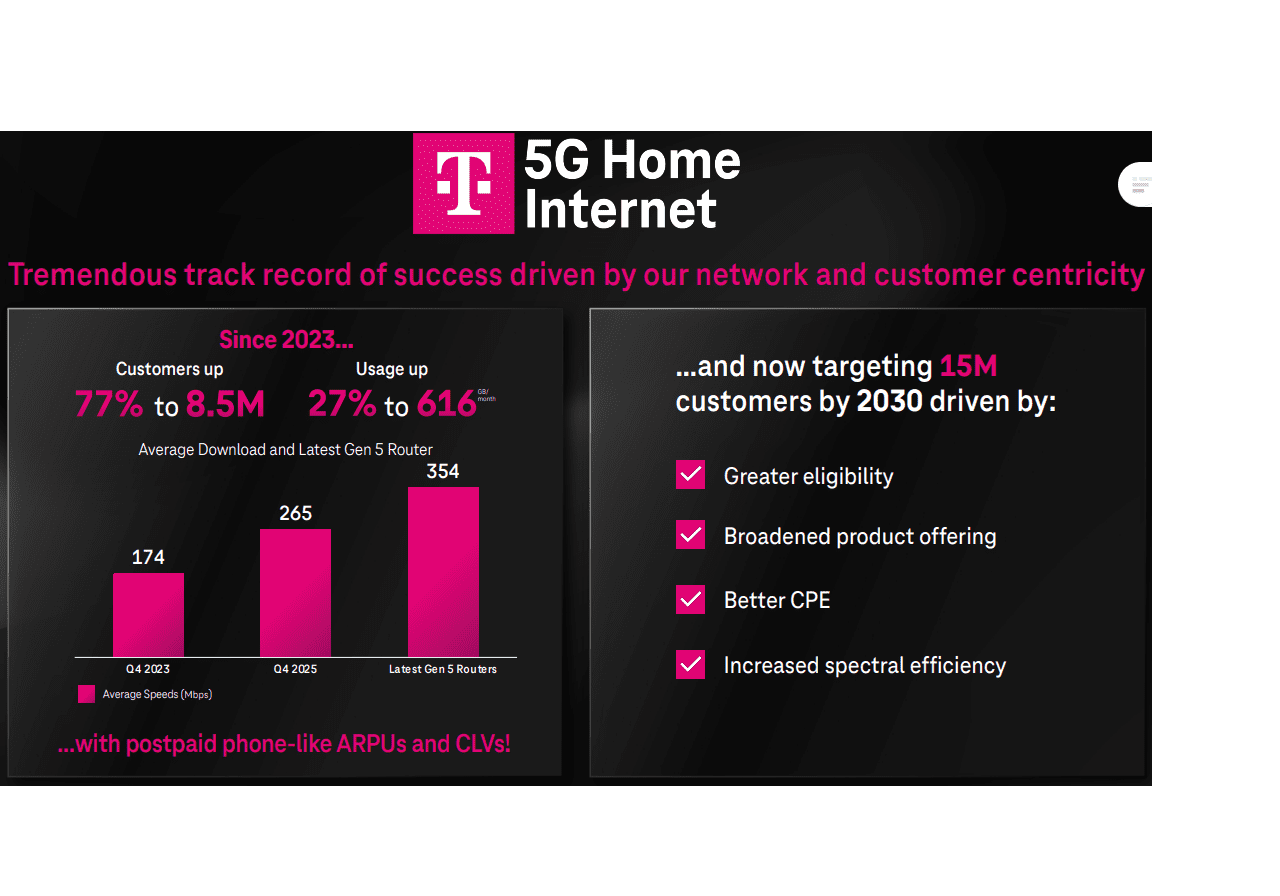

T-Mobile US (the “Un-carrier”) today announced new targets of 15 million 5G broadband customers by 2030, a 25% increase from its previous target of 12 million by the end of 2028, driven by increased spectral efficiency, better CPE technology, increased eligibility including to business customers with complementary usage profiles, and broadened product offerings to continue to meet evolving customer needs. T-Mobile is also leveraging its scale and nationwide 5G Advanced network to expand into new growth areas, including advertising, financial services, and long-term opportunities in edge and physical AI. The top rated U.S. wireless telco is also expecting between 3 and 4 million T-Fiber customers by 2030.

“T-Mobile is raising the bar on what customers, stockholders, and the industry can expect from the Un-carrier. T-Mobile has an unmatched combination of the Best Network, Best Value, and Best Customer Experiences — hallmarks of our unique Un-carrier differentiation — paired with our industry-leading portfolio of assets,” said T-Mobile CEO Srini Gopalan.

“This is why customers bring their connectivity relationship to T-Mobile. Looking ahead, we see an extraordinary runway to further expand this differentiation — through sustained momentum in network perception, digital and AI-driven transformation, and our future-forward innovation in areas like 6G and advanced AI. With this foundation, I’m confident that the future has never been brighter.”

Here are 2 of many impressive slides from T-Mo’s investor presentation referenced below:

The Un-carrier also plans to launch real-time and agentic AI services directly into its 5G-Advanced (5G-A) network by the end of 2026. This initiative, which began with a beta program in early 2026 for postpaid customers, allows for AI-driven features to function natively within the network, meaning users do not need to download specific apps or upgrade their hardware. This 5G-A offering will include live voice call translation in over 50 languages. By integrating AI directly into the 5G-A infrastructure (RAN, core network, and management layers), T-Mobile is enabling features that work on any eligible device, not just smartphones.

New 5G-A Agentic AI Highlights:

- The initial application is a “Live Translation” feature for voice calls, allowing for real-time translation in over 50 languages.

- “Agentic” AI and Automation: The network will use AI to enhance operational efficiency, including predictive optimization and dynamic resource allocation.

- The 5G-Advanced deployment also supports increased data speeds (up to 6.3 Gbps in tests), low-latency applications like XR and cloud gaming, and enhanced location services.

- The forthcoming capability will permit features to be active with only one participant needing to be on the 5G-A network.

- Infrastructure Partners: T-Mobile is collaborating with partners including NVIDIA, Ericsson, and Nokia to build an AI-RAN (Radio Access Network) framework. Telecompaper Telecompaper +3 This move is part of a broader strategy to transition from 5G to 5G-Advanced, with a focus on delivering “intent-driven” AI services and laying the groundwork for 6G (IMT 2030).

……………………………………………………………………………………………………………………………………….

References:

https://www.t-mobile.com/how-mobile-works/innovation/5g-advanced

https://www.t-mobile.com/news/business/t-mobile-capital-markets-day-update-feb-2026

https://www.t-mobile.com/benefits/live-translation

Virtualization’s role in 5G Advanced (3GPP Release 18) and a proposed new hardware architecture

Disclaimer: The author used Google Gemini to provide research contained in this article.

In a February 9, 2026 article, Ji-Yun Seol, Executive VP and Head of Product Strategy, Networks Business at Samsung, says: “The evolution from 5G to 5G-Advanced and 6G hinges on three interconnected pillars: virtualization for flexible networks, AI integration across all network layers, and automation towards autonomous networks.”

As the IEEE Techblog has extensively covered both AI RAN and the use of AI in 6G (IMT 2030), this post focuses on the role of virtualization in 5G Advanced.

In 3GPP Release 18 (5G-Advanced), virtualization is the foundational technology that enables several “software-defined” breakthroughs. 3GPP Release 18 components) have already been submitted to ITU-R WP 5D for inclusion in the next revision of ITU-R M.2150. Any remaining technical issues and the final decision for publication of ITU-R M.2150-3 are expected to be resolved during the WP 5D meeting concluding in Feb 2026.

3GPP Rel 18 features that depend most heavily on a virtualized, cloud-native architecture include:

- Host AI Models: Run complex machine learning algorithms for channel state information (CSI) feedback, beam management, and positioning.

- Automate Optimization: Enable “zero-touch” operations where the network dynamically adjusts power and resource allocation based on predictive traffic patterns.

While slicing existed in earlier releases, 5G-Advanced introduces more sophisticated, automated management. Virtualization is critical for:

Dynamic Resource Partitioning: Using Cloud-native Network Functions (CNFs) to create dedicated virtual networks on demand for specific use cases like Public Safety or industrial automation.

- SLA Assurance: Automatically scaling virtual resources to guarantee the ultra-low latency required for high-bandwidth applications like XR (Extended Reality).

To support lightweight headsets, 5G-Advanced relies on split-rendering.

- Edge Cloud Dependency: Virtualization allows heavy graphical processing to be moved from the headset to a virtualized Edge Cloud. This requires a highly agile, virtualized edge infrastructure to maintain the near-zero delay needed for immersive experiences.

- Infrastructure Visibility: New protocols provide the 3GPP layer with direct visibility into the underlying virtualized platform to detect vulnerabilities in the software-defined infrastructure.

Virtualization enables “self-organizing networks” (SON) where network entities can self-configure.

- Lifecycle Management: Standardized solutions in Rel-18 allow for the automated downloading, activation, and testing of software across virtualized network functions (VNFs).

| Feature | Primary Virtualization Dependency |

|---|---|

| AI/ML for RAN | Hosting and training models on COTS hardware |

| Edge-Based XR | Offloading computation to virtualized edge nodes |

| Automated Slicing | Rapid instantiation of CNFs for specific “slices” |

| Net Energy Saving | Software-driven power-down of virtual resources |

………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

On the hardware side, traditional telecommunications infrastructure was defined by a tight coupling of network functions to proprietary, purpose-built hardware—resulting in siloed environments where routers, baseband units, and security appliances existed as distinct physical appliances. While providing reliable performance, this monolithic model introduced limitations in scalability, creating high demands for space, power, and capital expenditure for functional upgrades.

Virtualization transforms this paradigm by decoupling network functions from dedicated hardware, deploying them as software-defined workloads on commercial off-the-shelf (COTS) servers. This shift toward general-purpose compute platforms drives operational efficiency, enhances flexibility, and enables AI readiness. The industry adoption followed a staged evolution: starting with the virtualization of core networks—migrating packet gateways and subscriber databases to standard servers—followed by Virtualized RAN (vRAN), which disaggregates baseband processing from radio hardware to operate as cloud-native software.

In 5G-Advanced (Release 18), the hardware shifts from proprietary “black boxes” to a disaggregated architecture of General-Purpose Processors (GPPs) and Specialized Accelerators.

The physical infrastructure required to run these virtualized functions generally falls into three categories:

Virtual Network Functions (VNFs) and Cloud-native Functions (CNFs) run on Commercial Off-The-Shelf (COTS) servers designed for high-density environments.

- Processors: Typically

Intel Xeon Scalable or AMD EPYC processors with high CPU core counts (up to 48+ cores) to handle parallelized workloads.

- Memory: Large-scale deployments require 384GB to over 1TB of DDR4/DDR5 RAM to support multiple network “slices” simultaneously.

- Form Factor: Short-depth chassis (300mm to 600mm) to fit into standard telco racks or outdoor cabinets at the network edge.

- Inline vs. Lookaside:

- Lookaside: The CPU sends specific tasks (like Forward Error Correction) to the card and gets them back.

- Inline: The entire L1 data flow passes through the accelerator, reducing the load on the CPU and improving power efficiency.

- Chips: These cards use FPGAs (Field Programmable Gate Arrays), ASICs (Application-Specific Integrated Circuits), or GPUs.

- GPU Integration: Platforms like NVIDIA Aerial use GPUs to accelerate both 5G signal processing and AI workloads on the same hardware.

- DPUs (Data Processing Units): Used to offload networking and security tasks, ensuring that data moves between the radio and the virtualized core with sub-microsecond precision.

| Hardware Component | Function in 5G-Advanced |

|---|---|

| COTS Servers | Host virtualized core and RAN software (vCU, vDU) |

| L1 Accelerators | Handle compute-heavy signal processing (Beamforming, MIMO) |

| SmartNICs / DPUs | Manage high-speed data transfer and timing synchronization |

| GPUs | Power the AI/ML models for network optimization and XR rendering |

…………………………………………………………………………………………………………………………………………………………………..

References:

https://www.3gpp.org/specifications-technologies/releases/release-18

Samsung: Turning legacy infrastructure into AI-ready networks

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Comparing AI Native mode in 6G (IMT 2030) vs AI Overlay/Add-On status in 5G (IMT 2020)

Ericsson announces capability for 5G Advanced location based services in Q1-2026

Ericsson’s 5G Advanced location based services (LBS) offering is a comprehensive suite of innovations designed to redefine location-based services across commercial 5G Standalone (SA) networks. Set for release in Q1 2026, it makes Ericsson the leader in 5G positioning technology, offering a scalable and fully integrated solution on top of Ericsson’s dual-mode 5G Core network.

By embedding positioning as a core 5G SA network capability, Ericsson 5G Advanced location services enables Communications Service Providers (CSPs) to monetize precise location services and expand beyond traditional mobile offerings into verticals such as manufacturing, healthcare, public safety, automotive, drones, and more.

Key benefits:

- High Accuracy: Down to sub-meter for indoor and sub-10 cm for outdoor positioning, enabling precise tracking

- Scalability: Scalable, precise positioning for outdoor applications (automotive, agriculture, drones)

- Seamless Indoor/Outdoor Coverage: Unified 5G positioning technology for both environments.

- Developer & Device Friendliness: No need for device-side apps; improved battery life compared to satellite-based solutions

- Support for Large-Scale Use Cases: Enables massive geofencing, population density analysis, and tracking use cases.

Monica Zethzon, Head of Core Networks, Ericsson, says: “With the launch of 5G Advanced Location Services we are evolving the value of 5G Standalone networks. This innovation gives CSPs the precision and scalability to create differentiated services based on location capabilities.”

Caroline Gabriel, Partner at Analysys Mason, says: “Ericsson’s integrated approach to indoor and outdoor positioning sets a new benchmark in the industry. It addresses critical pain points for operators and enterprises, particularly in sectors where location accuracy is mission-critical.”

The global market for 5G positioning is in its early stages but poised for rapid growth, driven by demand for enhanced precision in diverse sectors. Ericsson’s solution responds to this demand with scalable, developer-friendly capabilities that improve device battery life compared to legacy systems.

This launch further strengthens Ericsson’s location solutions based on Real-Time Kinematics technology, with related devices from Ericsson planned for Q1 2026.

Photo Credit: Ericsson

………………………………………………………………………………………………………………………………………………………….

- Integrated Positioning: Positioning is built into the 5G Standalone (SA) architecture, moving beyond traditional GPS reliance.

- High Accuracy & Efficiency: New techniques improve accuracy (e.g., bandwidth aggregation, carrier-phase measurements) and reduce power consumption for devices.

- AI/ML Integration: Artificial Intelligence/Machine Learning is applied to enhance positioning accuracy, especially for challenging scenarios like beyond-visual-line-of-sight (BVLOS).

- Support for New Devices/Apps: Enables precise tracking for wearables, industrial sensors (RedCap), augmented reality (AR), drone control, and smart grids.

- Beyond-Line-of-Sight (BVLOS): Focus on reliable positioning for industrial and public safety applications where line-of-sight isn’t guaranteed.

- Reduced Power: Solutions target lower power usage, crucial for IoT devices.

- Release 18 (5G Advanced Start): Finalized mid-2024, introduced major LBS enhancements, including RedCap positioning, bandwidth aggregation, and carrier-phase support.

- Release 19 (Ongoing): Continues the evolution, extending LTM (L1/L2-triggered Mobility) and further exploring AI/ML for mobility and positioning.

- Release 20 & Beyond: Will build on these foundations, further evolving towards 6G capabilities.

References:

https://www.ericsson.com/en/press-releases/2026/1/5g-advanced-location-services

5G Advanced offers opportunities for new revenue streams; 3GPP specs for 5G FWA?

What is 5G Advanced and is it ready for deployment any time soon?

Hutchison Telecom is deploying 5G-Advanced in Hong Kong without 5G-A endpoints

China Mobile & ZTE use digital twin technology with 5G-Advanced on high-speed railway in China

Huawei pushes 5.5G (aka 5G Advanced) but there are no completed 3GPP specs or ITU-R standards!

ZTE and China Telecom unveil 5G-Advanced solution for B2B and B2C services

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

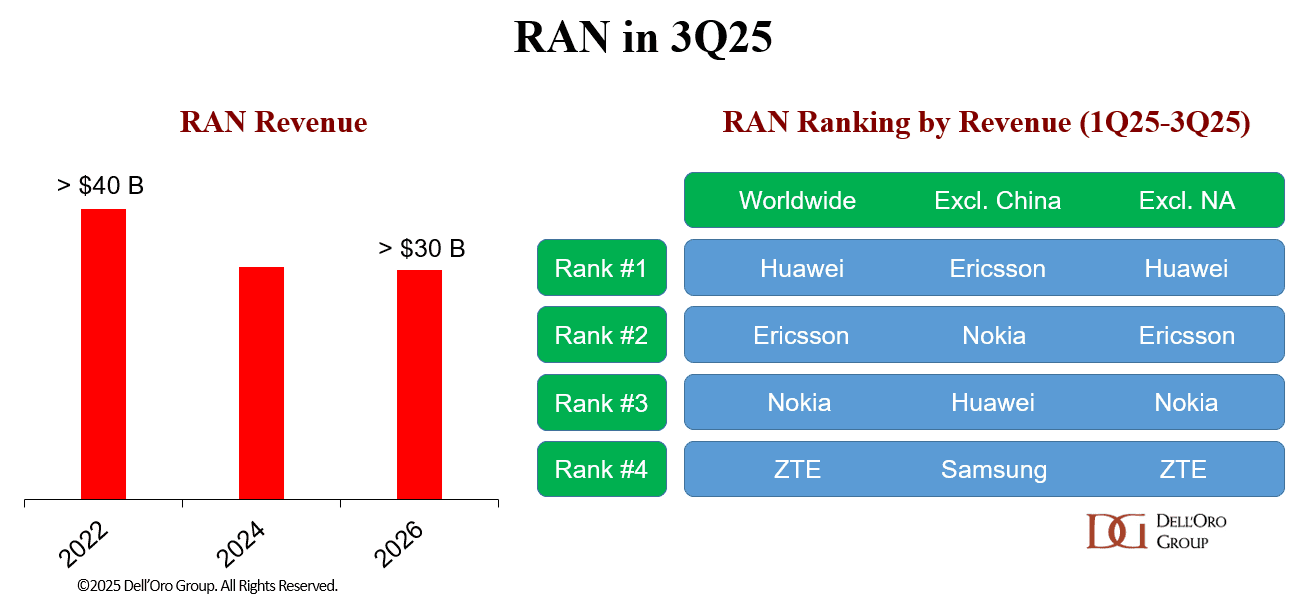

A recently published report from Dell’Oro Group notes that after two years of steep declines, initial estimates show that total Radio Access Network (RAN) revenue—including baseband, radio hardware, and software, excluding services—was flat outside of China and up when excluding North America.

“The nearly stable results for the 1Q25-3Q25 period bolster the flat growth thesis we have communicated for some time, reflecting the current state of the 5G network,” said Stefan Pongratz, Vice President of RAN market research at the Dell’Oro Group. “While near-term RAN expectations remain muted, some of the leading RAN suppliers are still cautiously optimistic that more investments are needed over the long-term to ensure the networks evolve from a connectivity pipe into an intelligence grid. Huawei and Ericsson are the clear #1 and 2 players globally – their combined share makes up nearly two-thirds of the RAN market (see table below).” Pongratz added.

Additional highlights from the 3Q 2025 RAN report:

- In the quarter, growth in EMEA was nearly enough to offset declining revenue in North America and the Asia Pacific regions.

- The top 5 RAN suppliers, based on worldwide revenues for the 1Q25-3Q25 period, are Huawei, Ericsson, Nokia, ZTE, and Samsung.

- Market is becoming more concentrated—the top five suppliers accounted for 96 percent of the 1Q25-3Q25 RAN market, up from 95 percent in 2024.

- Huawei and Ericsson’s worldwide RAN revenue share improved for the 1Q25-3Q25 period relative to 2024.

- Huawei and Nokia’s RAN revenue share outside of North America improved for the 1Q25-3Q25 period relative to 2024.

- The short-term outlook remains unchanged, with total RAN expected to remain mostly stable in 2026.

Dell’Oro Group’s RAN Quarterly Report offers a complete overview of the RAN industry, with tables covering manufacturers’ and market revenue for multiple RAN segments including 5G NR Sub-7 GHz, 5G NR mmWave, LTE, macro base stations and radios, small cells, Massive MIMO, Open RAN, and vRAN. The report also tracks the RAN market by region and includes a four-quarter outlook. To purchase this report, please contact us by email at [email protected].

………………………………………………………………………………………………………………………………………….

Data from Omdia, a Light Reading sister company, shows Ericsson, Huawei and Nokia were even more dominant last year than they were in 2023, growing their combined RAN market share by 2.3 percentage points over this period, to 77.4%. Besides China’s ZTE, the only other contender with more than a percentage point of market share was Samsung.

…………………………………………………………………………………………………………………………………………..

Another recent Dell’Oro Group report reveals that the Mobile Core Network (MCN) market revenue outside China surged 14% year-over-year (Y/Y) in 3Q 2025. Twelve Mobile Network Operators (MNOs) have now selected to move forward with 5G-Advanced (the marketing term used for the next phases of 3GPP’s 5G specs, which started with Release 18 and continues with Release 19 and beyond).

“The Chinese market experienced abnormally high growth in 3Q 2024. As a result, the China market revenue declined 39 percent Y/Y for 3Q 2025,” stated Dave Bolan, Research Director at Dell’Oro Group. “The revenue for all the other regions increased, between 9 percent and 17 percent Y/Y, resulting in a worldwide revenue decline of 2 percent Y/Y. As noted, revenue worldwide excluding China rose 14 percent Y/Y, continuing the trend in subscribers migrating to 5G Standalone (5G SA), and revenue worldwide excluding North America declined 5 percent Y/Y.

“MNOs are moving forward with 5G SA (72 in our last count) and moving forward to take advantage of monetization opportunities. Network Slicing announcements continued. Of note is Reliance Jio (India), which announced 10 network slices with guaranteed service level agreements (SLAs) at scale. In October, T-Mobile launched Edge Control, providing enterprises with what Dell’Oro Group refers to as an MNO-provided Mobile Private Network (MPN). This is in response to the challenges of implementing 5G SA Private Wireless networks in the shared CBRS spectrum in the US.

“We have identified 12 MNOs that have commercially launched 5G-Advanced networks (not all this quarter), to take 5G to the next level with new features and performance. MNOs include: China Mobile, China Telecom, China Unicom, CTM (Macau), Du (UAE), e& (UAE), HKT (Hong Kong), Singtel (Singapore), Telstra (Australia), T-Mobile (USA), YTL (Malaysia), and Zain (Kuwait),” added Bolan.

Additional highlights from the 3Q 2025 Mobile Core Network and Multi-Access Edge Computing Report include:

- Region rankings were: EMEA; Asia Pacific, excluding China; China and North America tied; CALA.

- Vendor rankings (with more than 5 percent share) were: Huawei, Ericsson, Nokia, and ZTE.

The Dell’Oro Group Mobile Core Network & Multi-Access Edge Computing Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, shipments, and average selling prices for Traditional Packet Core, Evolved Packet Core, 5G Packet Core, Policy, Subscriber Data Management, Signaling, Circuit Switched Core, and IMS Core by geographic regions. To purchase this report, please contact us at [email protected].

About Dell’Oro Group:

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, security, enterprise networks, and data center infrastructure markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions.

For more information, contact Dell’Oro Group at +1.650.622.9400 or visit https://www.delloro.com.

References:

MCN Market Up 14 Percent Outside China in 3Q 2025, According to Dell’Oro Group

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Omdia: Huawei increases global RAN market share due to China hegemony

Dell’Oro Group: RAN Market Grows Outside of China in 2Q 2025

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

Dell’Oro: Global RAN Market to Drop 21% between 2021 and 2029

Dell’Oro: RAN market still declining with Huawei, Ericsson, Nokia, ZTE and Samsung top vendors

Highlights of Dell’Oro’s 5-year RAN forecast

Dell’Oro: 2023 global telecom equipment revenues declined 5% YoY; Huawei increases its #1 position

Dell’Oro & Omdia: Global RAN market declined in 2023 and again in 2024

Dell’Oro: Mobile Core Network market has lowest growth rate since 4Q 2017

Dell’Oro: Mobile Core Network market driven by 5G SA networks in China

Dell’Oro: Mobile Core Network Market 5 Year Forecast

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

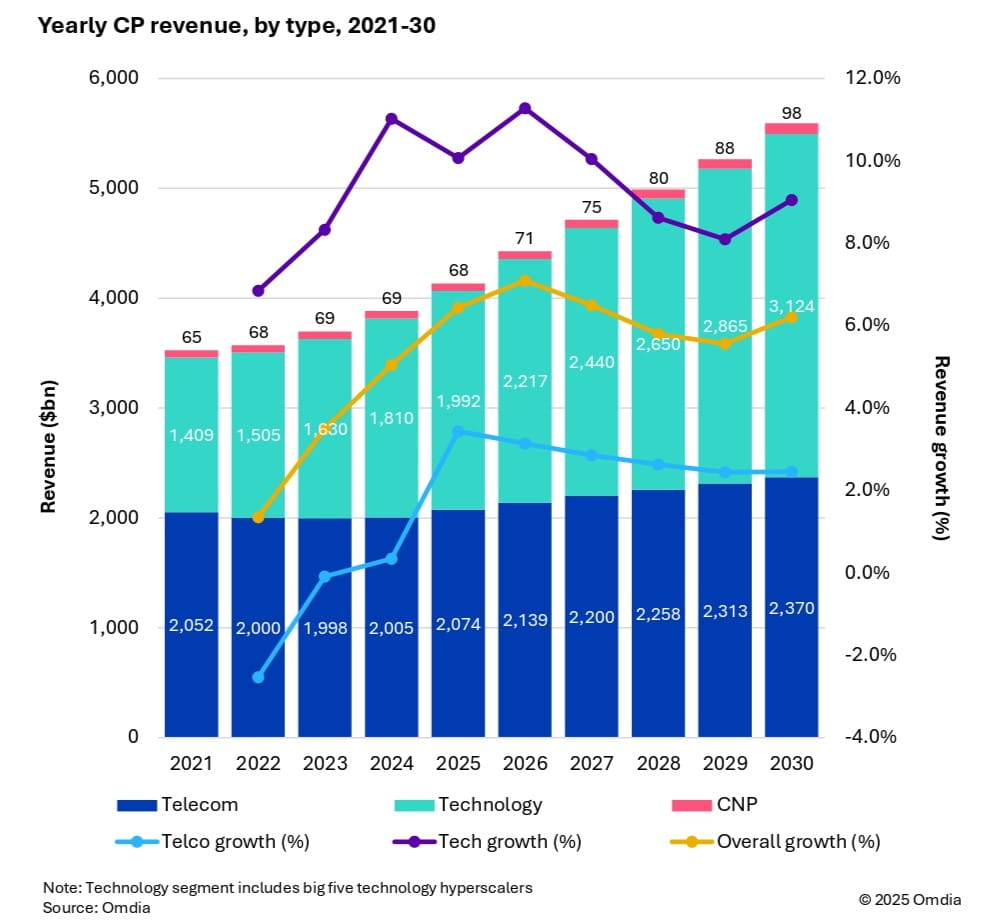

Market research firm Omdia (owned by Informa) this week forecast that 6G and AI investments are set to drive industry growth in the global communications market. As a result, global communications providers’ revenue is expected to reach $5.6 trillion by 2030, growing at a 6.2% CAGR from 2025. Investment momentum is also expected to shift toward mobile networks from 2028 onward, as tier 1 markets prepare for 6G deployments. Telecoms capex is forecast to reach $395 billion by 2030, with a 3.6% CAGR, while technology capex will surge to $545 billion, reflecting a 9.3% CAGR.

Fixed telecom capex will gradually decline due to market saturation. Meanwhile, AI infrastructure, cloud services, and digital sovereignty policies are driving telecom operators to expand data centers and invest in specialized hardware.

Key market trends:

- CP capex per person will increase from $74 in 2024 to $116 in 2030, with CP capex reaching 2.5% of global GDP investment.

-

Capital intensity in telecom will decline until 2027, then rise due to mobile network upgrades.

-

Regional leaders in revenue and capex include North America, Oceania & Eastern Asia, and Western Europe, with Central & Southern Asia showing the highest growth potential.

Dario Talmesio, research director at Omdia said, “telecom operators are entering a new phase of strategic investment. With 6G on the horizon and AI infrastructure demands accelerating, the connectivity business is shifting from volume-based pricing to value-driven connectivity.”

Dario Talmesio, research director at Omdia said, “telecom operators are entering a new phase of strategic investment. With 6G on the horizon and AI infrastructure demands accelerating, the connectivity business is shifting from volume-based pricing to value-driven connectivity.”

Omdia’s forecast is based on a comprehensive model incorporating historical data from 67 countries, local market dynamics, regulatory trends, and technology migration patterns.

…………………………………………………………………………………………………………………………………………………

Separately, Dell’Oro Group sees 6G capex ramping around 2030, although it warns that the RAN market remains flat, “raising key questions for the industry’s future.” Cumulative 6G RAN investments over the 2029-2034 period are projected to account for 55% to 60% of the total RAN capex over the same forecast period.

“Our long-term position and characterization of this market have not changed,” said Stefan Pongratz, Vice President of RAN and Telecom Capex research at Dell’Oro Group. “The RAN network plays a pivotal role in the broader telecom market. There are opportunities to expand the RAN beyond the traditional MBB (mobile broadband) use cases. At the same time, there are serious near-term risks tilted to the downside, particularly when considering the slowdown in data traffic,” continued Pongratz.

Additional highlights from Dell’Oro’s October 2025 6G Advanced Research Report:

- The baseline scenario is for the broader RAN market to stay flat over the next 10 years. This is built on the assumption that the mobile network will run into utilization challenges by the end of the decade, spurring a 6G capex ramp dominated by Massive MIMO systems in the Sub-7GHz/cm Wave spectrum, utilizing the existing macro grid as much as possible.

- The report also outlines more optimistic and pessimistic growth scenarios, depending largely on the mobile data traffic growth trajectory and the impact beyond MBB, including private wireless and FWA (fixed wireless access).

- Cumulative 6G RAN investments over the 2029-2034 period are projected to account for 55 to 60 percent of the total RAN capex over the same forecast period.

Dell’Oro Group’s 6G Advanced Research Report offers an overview of the RAN market by technology, with tables covering manufacturers’ revenue for total RAN over the next 10 years. 6G RAN is analyzed by spectrum (Sub-7 GHz, cmWave, mmWave), by Massive MIMO, and by region (North America, Europe, Middle East and Africa, China, Asia Pacific Excl. China, and CALA). To purchase this report, please contact by email at [email protected].

References:

https://www.lightreading.com/6g/6g-momentum-is-building

6G Capex Ramp to Start Around 2030, According to Dell’Oro Group

https://www.lightreading.com/6g/6g-course-correction-vendors-hear-mno-pleas

https://www.lightreading.com/6g/what-at-t-really-wants-from-6g

Should Peak Data Rates be specified for 5G (IMT 2020) and 6G (IMT 2030) networks?

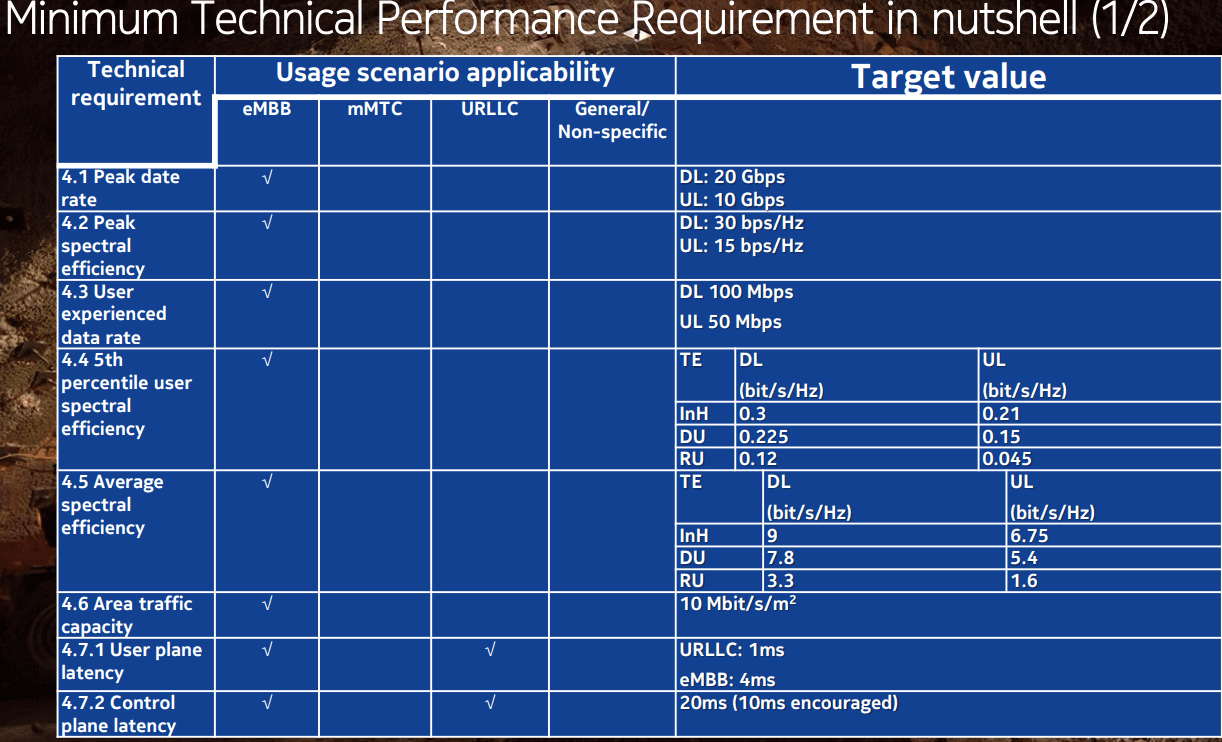

Peak Data Rate [1.] is one of the most visible attributes of IMT (International Mobile Telecommunications) cellular networks, e.g. 3G, 4G and 5G. As a result, it gets significant attention from analysts and reporters that create high expectations for IMT end users which may never be realized in commercially deployed IMT networks.

For example, the peak data rates specified by the ITU-R M.2410 report for IMT-2020 (5G) have not been realized in any 5G production networks under typical conditions. The ITU-R’s 20 Gbps downlink and 10 Gbps uplink targets are theoretical maximums, achievable only in a controlled test environment with ideal conditions. Please refer to the chart below.

……………………………………………………………………………………………………………………………………………………………………..

Note 1. Peak data rate is the theoretical maximum [achievable] data rate under ideal conditions, which is the received data bits assuming error-free conditions assignable to a single mobile station, when all assignable radio resources for the corresponding link direction are utilized (i.e. excluding radio resources that are used for physical layer synchronization, reference signals or pilots, guard bands and guard times).

………………………………………………………………………………………………………………………………………………………………………

5G services are deployed across three main frequency ranges and the speed capability varies dramatically for each.

- Low-band (sub-6 GHz): Offers wide coverage but only a modest speed improvement over 4G, typically delivering a few hundred Mbps at best.

- Mid-band (sub-6 GHz): Provides a balance of speed and coverage, with peak speeds sometimes reaching 1 Gbps, though typical average speeds are much lower.

- High-band (millimeter wave or mmWave): This is the only band capable of reaching multi-gigabit speeds. However, its signal range is very short and it is easily blocked by physical objects, limiting its availability to dense urban areas and specific venues. 5G mmWave base station power consumption is also very high which limits coverage.

- mmWave spectrum: Higher-band millimeter wave spectrum offers massive bandwidth, enabling multi-gigabit speeds. However, its use is limited to dense urban areas and specific venues due to its short range.

- Carrier aggregation: Combining multiple frequency bands (e.g., mmWave with mid-band) significantly increases the total available bandwidth and is crucial for achieving the highest download speeds.

- 5G Advanced (Release 18): New developments in 5G-Advanced technology (also known as 5.5G) enable even higher performance. The Telstra record in 2025 utilized 5G Advanced software.

- Equipment and device capabilities: Peak speeds require cutting-edge network hardware from vendors like Ericsson, Nokia, and Samsung, as well as the latest mobile devices powered by advanced modems from companies like Qualcomm and MediaTek.

The gap between what IMT-2020 (5G) technology can deliver (on paper) and what is actually realized in commercial 5G networks has grown larger and larger over the past few years [2.]. Here’s a summary of speed differences:

| Speed metric | ITU-R specification | Reality in commercial networks |

|---|---|---|

| Peak data rate | 20 Gbps (downlink)

10 Gbps (uplink) |

Reached only in isolated demonstrations, typically using high-band mmWave technology. |

| User experienced rate | 100 Mbps (downlink)

15 to 50 Mbps (uplink) |

The typical average speed for many users, particularly on low- and mid-band deployments. mmWave is higher, but the range is limited. |

Note 2. The gap is even greater for 5G latency! The minimum required latency in ITU-R M.2410 for user plane are:

– 4 ms for eMBB

– 1 ms for URLLC

assumes unloaded conditions (a single user) for small IP packets (e.g. 0 byte payload + IP header), for both downlink and uplink.

The minimum requirement for control plane latency is 20 ms. Proponents are encouraged to consider lower control plane latency, e.g. 10 ms.

However, the average latency experienced in deployed commercial 5G networks is higher, typically ranging between 5 and 20 milliseconds, depending on the network architecture, spectrum, and use case. One reason is that the 3GPP Release 16 spec for 5G-NR enhancements for URLLC in the RAN and Core network were never completed.

5G mmWave spectrum has the potential for the lowest latency, but its limited range and line-of-sight requirements limit restrict deployments to dense urban areas. Therefore, most 5G users connect via mid-band or low-band, which have higher latency.

……………………………………………………………………………………………………………………………………………………………….

For that reason, several companies (Apple, Nokia, TELECOM ITALIA, Deutsche Telekom, SK Telecom, Spark NZ, AT&T) have proposed not to define IMT-2030 peak data rate requirement values in ITU-R M.[IMT-2030.TECH PERF REQ] nor to maintain the IMT-2020 (5G) peak data rate numbers from the ITU-R M.2410 report.

Author’s Note: The IMT-2030 performance requirements in ITU-R M.[IMT-2030.TECH PERF REQ] are to be evaluated according to the criteria defined in Report ITU-R M.[IMT‑2030.EVAL] and Report ITU-R M.[IMT-2030.SUBMISSION] for the development of IMT-2030 recommendations within ITU-R WP5D.

……………………………………………………………………………………………………………………………………………………………………………….

Addendum – Measurements of top 5G network speeds:

- In the first half of 2025, Ookla said e& in the United Arab Emirates was the world’s fastest 5G network, noting a median upload speed of 52.21 Mbps. Other top performers like South Korea, Qatar, and Brazil also see median speeds well above 20 Mbps.

- U.S. performance: In the U.S., major carriers are in a close race. In mid-2024, Opensignal found Verizon with the fastest 5G upload speed at 21.2 Mbps, with T-Mobile close behind. However, as of early 2025, a separate Opensignal report credited T-Mobile with the fastest overall upload experience, at 17.9 Mbps, though that figure includes both 4G and 5G connections.

- European performance: Speeds vary across Europe. Ookla reported that in the first half of 2025, Magenta Telekom in Austria achieved a median 5G upload speed of 35.67 Mbps, while Three in the U.K. recorded a median of 13.07 Mbps.

- Rural vs. urban divide: Average 5G uplink speeds are often higher in urban areas where mid-band spectrum is more prevalent. However, as of mid-2023, Opensignal noted that the rural-urban gap for 5G upload speeds in the U.S. was narrowing due to increased rural investment.

- Dependence on network type: Whether a network uses 5G standalone (SA) or non-standalone (NSA) architecture impacts speeds. In early 2025, an analysis in the U.K. showed that while 5G SA had lower latency, 5G NSA still had a slightly higher proportion of high-speed uplink connections.

…………………………………………………………………………………………………………………………………………………………

References:

https://www.itu.int/pub/r-rep-m.2410-2017

3GPP Release 16 5G NR Enhancements for URLLC in the RAN & URLLC in the 5G Core network

IMT-2030 Technical Performance Requirements (TPR) from ITU-R WP5D

Key Objectives of WG Technology Aspects at ITU-R WP 5D meeting June 24-July 3, 2025

ITU-R WP5D IMT 2030 Submission & Evaluation Guidelines vs 6G specs in 3GPP Release 20 & 21

ITU-R: IMT-2030 (6G) Backgrounder and Envisioned Capabilities

Draft new ITU-R recommendation (not yet approved): M.[IMT.FRAMEWORK FOR 2030 AND BEYOND]

ITU-R M.2150-1 (5G RAN standard) will include 3GPP Release 17 enhancements; future revisions by 2025

Key Objectives of WG Technology Aspects at ITU-R WP 5D meeting June 24-July 3, 2025

ITU-R WP 5D is responsible for the overall radio system aspects of the terrestrial component of International Mobile Telecommunications (IMT) systems, comprising the current IMT-2000, IMT-Advanced and IMT-2020 as well as IMT for 2030 and beyond. Note that 5D’s work is only for terrestrial radio access network interfaces. It does not include 5G or 6G Core network or satellite network access.

ITU-R WP5D Technology Aspects Working Group (WG) consists of several Sub Working Groups (SWGs):

SWG IMT SPECIFICATIONS, SWG EVALUATION, SWG RADIO ASPECTS, SWG IMT UNWANTED EMISSIONS, SWG IMT COORDINATION

Key objectives of WG Technology Aspects at their June 24-July 3, 2025 meeting include:

- Continue revising Recommendation ITU-R M.2150-2 (5G) and Recommendation ITU‑R M.2012-6 (IMT Advanced aka 4G), including consideration of further revision based on contribution;

- Continue working on revision of Document IMT-2030/2 “Process” – submission, evaluation process and consensus building process for IMT-2030;

- Start to work on candidate technology submission template for IMT-2030 (6G);

- Continue working on Report ITU-R M.[IMT-2030.TECH PERF REQ] – minimum requirements related to technical performance for IMT-2030 radio interface(s);

- Continue working on Report ITU-R M.[IMT-2030.EVAL] – Guidelines for evaluation of radio interface technologies for IMT-2030;

- Continue working on Report ITU-R M.[IMT-TROPO DUCT MITIGATION] – Mitigation of interference for IMT network under tropospheric ducting effect;

- Continue working on the documents of unwanted emission characteristics of base/mobile stations using the terrestrial radio interfaces of IMT-2020.

Backgrounder on IMT 2030 (6G):

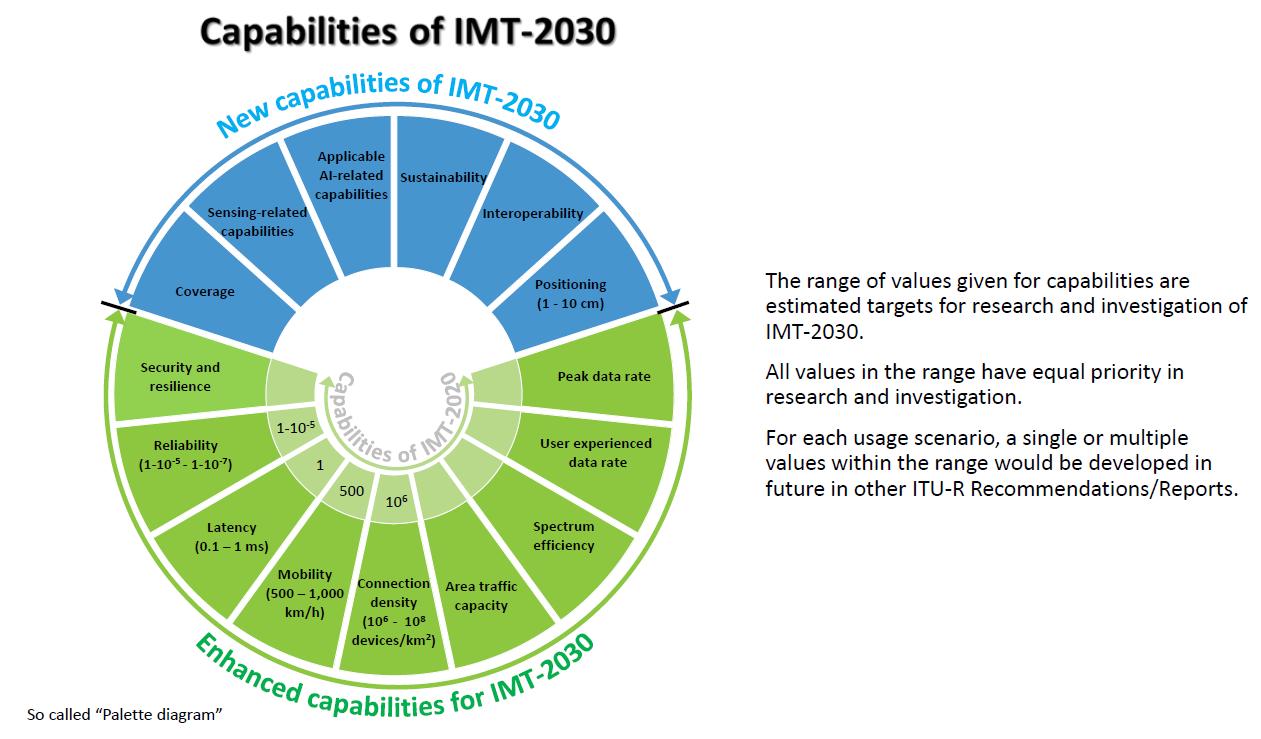

Recommendation ITU R M.2160 ‒ “Framework and overall objectives of the future development of IMT for 2030 and Beyond” identifies IMT-2030 capabilities which aim to make IMT-2030 (6G) more capable, flexible, reliable and secure than previous IMT systems when providing diverse and novel services in the intended six usage scenarios, including immersive communication, hyper reliable and low latency communication (HRLLC), massive communication, ubiquitous connectivity, artificial intelligence and communication, and integrated sensing and communication (ISAC).

IMT-2030 can be considered from multiple perspectives, including users, manufacturers, application developers, network operators, verticals, and service and content providers. Therefore, it is recognized that technologies for IMT-2030 can be applied in a variety of deployment scenarios and can support a range of environments, service capabilities, and technology options.

IMT-2030 is also expected to be built on overarching aspects which act as design principles commonly applicable to all usage scenarios. These distinguishing design principles of the IMT‑2030 are including, but are not limited to sustainability, security and resilience, connecting the unconnected for providing universal and affordable access to all users independent of the location, and ubiquitous intelligence for improving overall system performance.

………………………………………………………………………………………………………………………………………………………………………………………………………….

References:

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

Highlights of 3GPP Stage 1 Workshop on IMT 2030 (6G) Use Cases

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

Ericsson and e& (UAE) sign MoU for 6G collaboration vs ITU-R IMT-2030 framework

ITU-R: IMT-2030 (6G) Backgrounder and Envisioned Capabilities

ITU-R WP5D invites IMT-2030 RIT/SRIT contributions

NGMN issues ITU-R framework for IMT-2030 vs ITU-R WP5D Timeline for RIT/SRIT Standardization

NGMN: 6G Key Messages from a network operator point of view

IMT-2030 Technical Performance Requirements (TPR) from ITU-R WP5D

Draft new ITU-R recommendation (not yet approved): M.[IMT.FRAMEWORK FOR 2030 AND BEYOND]

Hutchison Telecom is deploying 5G-Advanced in Hong Kong without 5G-A endpoints

Hutchison Telecom-Hong Kong is deploying 3GPP’s 5G-Advanced (5G-A) in high-traffic venues in Hong Kong, including the HK Exhibition Center, the West Kowloon Cultural District and the new $3.9 billion Kai Tak Sports Park. However, 5G-A end points [1.] (like smartphones and tablets) aren’t likely to arrive until next year, according to Hutchinson Executive Director and CEO Kenny Koo. Therefore, the 5G-A Hong Kong deployment is mostly symbolic. However, Hutchison is doing some commercial business with 5G-A hotspots.

Hutchinson used the 5G-A modems to provide coverage for the annual Art Basel visual arts fair in March, enabling organizers to offer free Wi-Fi for visitors. It’s also found a little niche in pop-up stores. 5G-A modems registered download and upload speeds of 3.1 Gbit/s and 370 Mbit/s respectively in a demo earlier this month.

Note 1. Only a handful of 5G-A endpoint devices are available in mainland China, where operators are reporting 5G-A commercial networks in hundreds of cities – in the 3.5GHz, 4.9GHz and 2.1GHz bands.

“2025 marks the 5th anniversary of 5G launch. In December 2024, our 5G customer penetration rate reached 54%. At this important stage, we are comprehensively enhancing our 5G coverage and capacity while continuously optimizing user experience. Limited-time upgrade offers are also tailored to encourage customers to upgrade to 5G. Together, we are advancing into the new era of 5.5G (aka 5GA). In support of the development of the Northern Metropolis, we have taken the initiative to actively enhance 5G network coverage in the district as the flow of people and vehicles surges. This ensures that commuters travelling between the northwest New Territories and Kowloon can enjoy a smoother network experience at major transportation hubs, including Tai Lam Tunnel and the Kam Sheung Road section of the MTR Tuen Ma Line. In addition, we are helping to boost the mega event economy by activating 5.5G network hotspots at major event venues in Hong Kong including Kai Tak Sports Park, the West Kowloon Cultural District and the Hong Kong Convention and Exhibition Centre. Customers enjoy an improved experience at high-traffic hotspots compared with the original 5G coverage, with enhanced network speed, increased capacity and low latency performance provided by 5G broadband.”

“We try to position ourselves as a market leader in the technology evolution,” Koo told Light Reading. He said the 5G-A ecosystem “was not yet ready” because of the lack of devices that can support the 26 GHz and 28 GHz bands. “iPhone, Samsung and Huawei handsets do not support 5.5G in those bands,” he said, using the company’s preferred branding of 5G-Advanced.

Author’s Note: Koo did not mention that 5G-A has yet to be standardized by ITU-R as part of IMT 2020 RIT/SRIT aka the ITU-R M.2150 recommendation. 5G Advanced is included in 3GPP Release 18 and is expected to be part of M.2150 issue 3, now being developed by ITU-R WP 5D.

Hutchinson’s subscriber base grew 17% to 4.6 million, mostly due to prepaid gains, while 5G penetration increased 8 percentage points to 54%. Koo said the company has been able to sustain the growth this year because of demand from inbound travelers from mainland China. “They like our prepaid cards,” he added. Last year, Hutchinson’s roaming revenue increased 30% to 684 million Hong Kong dollars (US$87 million) and now accounts for nearly a fifth of total service revenue.

eSim is also a growing market for Hutchinson. There are a lot of travel SIM portals selling eSIM solutions right to consumers,” Koo said. The popularity of its eSIM product means Hutchison’s addressable market has expanded way beyond Hong Kong to reach mobile customers worldwide.

About Hutchison Telecommunications Hong Kong:

Hutchison Telecommunications Hong Kong Limited (“HTHK”) has launched 5G broadband services in both the consumer and enterprise markets, providing high-speed indoor and outdoor internet access. Leveraging a robust 5G network, HTHK has also extended the deployment of 5G solutions including 5G 4K live broadcasting, virtual reality and real-time data transmission to various verticals. HTHK plays a prominent role in developing a new economy ecosystem, channeling the latest technologies into innovations that set market trends and steer industry development.

……………………………………………………………………………………………………………………………………………………………

References:

https://www.lightreading.com/5g/hutchison-joins-5g-advanced-race

https://doc.irasia.com/listco/hk/hthkh/press/p250529.pdf

5G Advanced offers opportunities for new revenue streams; 3GPP specs for 5G FWA?

What is 5G Advanced and is it ready for deployment any time soon?

Huawei pushes 5.5G (aka 5G Advanced) but there are no completed 3GPP specs or ITU-R standards!

Nokia exec talks up “5G Advanced” (3GPP release 18) before 5G standards/specs have been completed

ITU-R recommendation IMT-2020-SAT.SPECS from ITU-R WP 5B to be based on 3GPP 5G NR-NTN and IoT-NTN (from Release 17 & 18)

Nokia wins multi-billion dollar contract from Bharti Airtel for 5G equipment

Nokia has secured a multi-billion dollar contract with India’s Bharti Airtel, one of the country’s leading telecom operators, which is expanding its 5G network. The deal with Airtel would be for Nokia’s latest AirScale mobile radios that support upgrading an existing network to 5G-Advanced and reduces energy costs, according to the sources.

- Ericsson won a multi-billion dollar contract from Bharti Airtel, Reuters reported on Monday. Airtel is also in talks with Samsung about buying 5G equipment, a source told Reuters.

- Samsung has been trying to grow its network equipment business, but has so far lagged Nokia and Ericsson. Samsung won its first 5G contract with Airtel in 2022. India has blocked its mobile carriers from using 5G telecom equipment made by China’s Huawei.

Backgrounder:

India is the world’s second-largest smartphone market where telcos such as Airtel, Reliance Jio and Vodafone Idea have been spending billions of dollars to upgrade their networks to 5G. Bharti Airtel’s 5G market share in India is over 90 million subscribers, as of June 2024. Airtel and Reliance Jio are the only two telcos in India that offer 5G services.

……………………………………………………………………………………………………………………………………..

The Nokia-Bharti Airtel deal is indicative of the intensifying competition among telecom operators and equipment manufacturers in India’s 5G market. For Nokia, the agreement represents a significant rebound and consolidation of its presence in India, amidst previous challenges and the competitive pressures exerted by rivals such as Ericsson and Samsung.As India stands on the cusp of a 5G revolution, the successful execution of this deal could serve as a blueprint for similar agreements, thereby accelerating the pace of 5G deployment across the nation.