AI

Telecom operators investing in Agentic AI while Self Organizing Network AI market set for rapid growth

Telecom companies are planning to use Agentic AI [1.] for customer experience and network automation. A recent RADCOM survey shows 71% of network operators plan to deploy agentic AI in 2026, while 14% have already begun, prioritizing areas that directly influence trust and customer satisfaction: security and fraud prevention (57%) and customer service and support (56%). The top use cases are automated customer complaint resolution and autonomous fault resolution.

Operators are betting on agentic AI to remove friction before customers feel it, with the highest-value use cases reflecting this shift, including:

- 57% – automated customer complaint resolution

- 54% – autonomous fault resolution before it impacts service

- 52% – predicting experience to prevent churn

This technology is shifting networks from simply detecting issues to preventing them before customers notice. In contact centers, 2026 is expected to see a rise in human and AI agent collaboration to improve efficiency and customer service.

Note 1. Agentic AI refers to autonomous artificial intelligence systems that can perceive, reason, plan, and act independently to achieve complex goals with minimal human intervention, going beyond simple command-response to manage multi-step tasks, use various tools, and adapt to new information for proactive automation in dynamic environments. These intelligent agents function like digital coworkers, coordinating internally and with other systems to execute sophisticated workflows.

……………………………………………………………………………………………………………………………………………………………………………………………

ResearchAndMarkets.com has just published a “Self-Organizing Network Artificial Intelligence (AI) Global Market Report 2025.” The market research firm says that the self-organizing network AI [2.] is forecast to expand from $5.19 billion in 2024 to $6.18 billion in 2025, at a CAGR of 19.2%. This surge is driven by the integration of machine learning and AI in telecom networks, smart network management investment, and the growing demand for features like self-healing and self-optimization, as well as predictive maintenance technologies.driven by the expansion of 5G, increasing automation demands, and AI integration for network optimization. Opportunities include AI-driven RRM and predictive maintenance. Asia-Pacific emerges as the fast-growing region, boosting telecom innovations amid global trade shifts.

Note 2. Self-organizing network AI leverages software, hardware, and services to dynamically optimize and manage telecom networks, applicable across various network types and deployment modes. The market encompasses a broad range of solutions, from network optimization software to AI-driven planning products, underscoring its expansive potential.

Looking further ahead, the market is expected to reach $12.32 billion by 2029, with a CAGR of 18.8%. Key drivers during this period include heightened demand for automation, increased 5G deployments, and growing network densification, accompanied by rising data traffic and subscriber numbers. Trends such as AI-driven network automation advancements, machine learning integration for real-time optimization, and the rise of generative AI for analytics are reshaping the landscape.

The expansion of 5G networks plays a pivotal role in propelling this growth. These networks, characterized by high-speed data and ultra-low latency, significantly enhance the capabilities of self-organizing network AI. The integration facilitates real-time data processing, supporting automation, optimization, and predictive maintenance, thereby improving service quality and user experience. A notable development in 2023 saw UK outdoor 5G coverage rise to 85-93%, reflecting growing demand and technological advancement.

Huawei Technologies and other major tech companies, are pioneering innovative solutions like AI-driven radio resource management (RRM), which optimizes network performance and enhances user experience. These solutions rely on AI and machine learning for dynamic spectrum and network resource management. For instance, Huawei’s AI Core Network, introduced at MWC 2025, marks a substantial leap in intelligent telecommunications, integrating AI into core systems for seamless connectivity and real-time decision-making.

Strategic acquisitions are also shaping the market, exemplified by Amdocs Limited acquiring TEOCO Corporation in 2023 to bolster its network optimization and analytics capabilities. This acquisition aims to enhance end-to-end network intelligence and operational efficiency.

Leading players in the market include Huawei, Cisco Systems Inc., Qualcomm Incorporated, and many others, driving innovation and competition. Europe held the largest market share in 2024, with Asia-Pacific poised to be the fastest-growing region through the forecast period.

References:

Operator Priorities for 2026 and Beyond: Data, Automation, Customer Experience

https://uk.finance.yahoo.com/news/self-organizing-network-artificial-intelligence-105400706.html

Ericsson integrates agentic AI into its NetCloud platform for self healing and autonomous 5G private network

Agentic AI and the Future of Communications for Autonomous Vehicles (V2X)

IDC Report: Telecom Operators Turn to AI to Boost EBITDA Margins

Omdia: How telcos will evolve in the AI era

Palo Alto Networks and Google Cloud expand partnership with advanced AI infrastructure and cloud security

Sovereign AI infrastructure for telecom companies: implementation and challenges

Sovereign AI infrastructure refers to the domestic capability of a nation or an organization to own and control the entire technology stack for artificial intelligence (AI) systems within its own borders, subject to local laws and governance. This includes the physical data centers, specialized hardware (like GPUs), software, data, and skilled workforce. Sovereign AI infrastructure involves a full “stack” designed to ensure national control and reduce reliance on foreign providers. A few key features:

- Policies and technical controls (e.g., data localization, encryption) to ensure that sensitive data used for training and inference remains within the jurisdiction.

- Development and hosting of proprietary or locally tailored AI models and software frameworks that align with national values, languages, and ethical standards.

- Workforce Development: Investing in domestic talent, including data scientists, engineers, and legal experts, to build and maintain the local AI ecosystem.

- Regulatory Framework: A comprehensive legal and ethical framework for AI development and deployment that ensures compliance with national laws and standards.

Why It’s Important – The pursuit of sovereign AI infrastructure is driven by several strategic considerations for both governments and private enterprises:

- National Security: To ensure that critical systems in defense, intelligence, and public infrastructure are not dependent on potentially adversarial foreign technologies or subject to extraterritorial access laws (like the U.S. CLOUD Act).

- Economic Competitiveness: To foster a domestic tech industry, create high-skilled jobs, protect intellectual property, and capture the significant economic benefits of AI-driven growth.

- Data Privacy and Compliance: To comply with stringent local data protection regulations (e.g., GDPR in the EU) and build public trust by ensuring citizen data is handled securely and according to local laws. Cultural Preservation: To train AI models on local datasets and languages, preserving cultural nuances and avoiding bias found in generalized, globally trained models.

Image Credit: Nvidia

………………………………………………………………………………………………………………………………………………………………………………………………………..

Governments around the world are starting to build sovereign AI infrastructure, and according to a new report from Morningstar DBRS, which opines that major telecommunications companies are uniquely positioned to benefit from that shift. Here are a few take-aways from the report:

- Sovereign AI funding opens a new growth path for telcos – Governments investing in domestic AI infrastructure are increasingly turning to operators, whose network and regulatory strengths position them to capture a large share of this emerging market.

- Telcos’ capabilities align with sovereignty needs – Their expertise in large-scale networks, local presence, and established government relationships give them an edge over hyperscalers for sensitive, sovereignty-focused AI projects.

- Early adopters gain advantage – Operators in Canada and Europe are already moving into sovereign AI, positioning themselves to secure higher-margin enterprise and government workloads as national AI buildouts accelerate.

- Infrastructure Demands: Building robust domestic AI ecosystems requires specialized expertise spanning hardware, software, data governance, and policy.

- Resource Constraints: Dr. Matt Hasan, CEO at aiRESULTS and a former AT&T executive, highlights specific bottlenecks:

- Compute Density at Scale.

- Spectrum Allocation amidst political pressures.

- Energy Demand exceeding existing grid capacity.

- Intensified Reliability Requirements: Sovereign AI implementation places heightened demands on telecom providers for system uptime, reliability, quality, and data privacy. This necessitates a focus on efficient power consumption, resilient routing and backups, robust encryption, and comprehensive cybersecurity measures.

- Supply Chain Vulnerabilities: Geopolitical tensions introduce risks to the supply of critical components such as GPUs and specialized chips, underscoring the interconnected nature of global hardware supply chains.

- The rapid evolution of AI technology mandates continuous investment and technical agility to ensure sovereign deployments remain current.

- The interplay between global hyperscalers and regional telecom operators is expected to shift.

- Hasan predicts a collaborative model, with regional telcos leveraging their position as sovereign partners through joint ventures, rather than an outright displacement of hyperscalers.

References:

Telcos Across Five Continents Are Building NVIDIA-Powered Sovereign AI Infrastructure

https://www.rcrwireless.com/20251202/ai/sovereign-ai-telcos

Subsea cable systems: the new high-capacity, high-resilience backbone of the AI-driven global network

Analysis: OpenAI and Deutsche Telekom launch multi-year AI collaboration

AI infrastructure spending boom: a path towards AGI or speculative bubble?

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Omdia: How telcos will evolve in the AI era

OpenAI announces new open weight, open source GPT models which Orange will deploy

Expose: AI is more than a bubble; it’s a data center debt bomb

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

Custom AI Chips: Powering the next wave of Intelligent Computing

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

IBM and Groq Partner to Accelerate Enterprise AI Inference Capabilities

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

To date, the main benefit of AI for telecom has been to reduce headcount/layoff employees. Light Reading’s Iain Morris wrote, “Telecom operators and vendors, nevertheless, are already using AI as the excuse for thousands of job cuts made and promised. So far, those cuts have not brought any improvement in the sector’s fortunes. Meanwhile, ceding basic but essential skills to systems that hardly anyone understands seems incredibly risky.” Some say that will change with 6G/ IMT 2030, but that’s a long way off. Others point to AI RAN, but that has not gotten any real market traction with wireless telcos.

As Gen AI development accelerates, robust wireless and fiber optic network infrastructure will be essential to accommodate the substantial data and communication volume generated by AI systems. Initially, the existing network ecosystem—encompassing wireless, wireline, broadband, and satellite services—will absorb this traffic load. However, the expanding requirements of AI are anticipated to drive the future emergence of entirely new network architectures and communication paradigms.

For sure, AI needs massive, fast, reliable connectivity to function, driving demand for low latency optical networks and 6G/ IMT 2030, which AI itself will optimize, leading to better efficiency, security, resource management, and new services like real-time AR/VR, ultimately boosting telecom revenue and innovation across the entire digital ecosystem.

![]()

Source: Pitinan Piyavatin/Alamy Stock Photo

……………………………………………………………………………………………………………………………………………………………………..

- AI Backend Scale-Out and Scale-Up Networks: These are specialized, private networks within and across data centers designed to connect numerous GPUs and enable them to function as one massive compute resource. They utilize technologies like:

- InfiniBand: A long-standing high-bandwidth, low-latency technology that has become a top choice for connecting GPU clusters in AI training environments.

- Optimized Ethernet: Ethernet is gaining ground for AI workloads through the development of enhanced, open standards via the Ultra Ethernet Consortium (UEC). These enhancements aim to provide lossless, low-latency fabrics that can match or exceed InfiniBand’s performance at scale.

- High-Speed Optics: The use of 400 Gbps and 800 Gbps (and soon 1.6 Tbps) optical interconnects is critical for meeting the massive bandwidth and power requirements within and between AI data centers.

- Edge AI Networking: As AI inferencing (generating responses from AI models) moves closer to the end-user or device (e.g., in autonomous vehicles, smart hospitals, or factories), specialized edge networks are needed. These networks must ensure low latency and localized processing to enable real-time responses.

- AI-Native 6G Networks: The upcoming sixth-generation (6G) wireless networks are being designed with AI integration as a core principle, rather than an add-on.

- These networks are expected to be fully automated and self-evolving, using AI to optimize resource allocation, predict issues, and enhance security autonomously.

- They will support extremely high data rates (up to 1 Tbps), ultra-low latency (around 1 ms), and new technologies like AI-RAN (Radio Access Network) that integrate AI capabilities directly into the network infrastructure.

- More in next section below.

- Self-Evolving Networks: The ultimate goal is the development of “self-evolving networks” where AI agents manage and optimize the network infrastructure autonomously, adapting to new demands and challenges without human intervention.

……………………………………………………………………………………………………………………………………………………………………..

In IMT 2030/6G networks, AI will shift from being an “add-on” optimization tool (as in 5G) to a native, foundational component of the entire network architecture. This deep integration will enable the network to be self-organizing, highly efficient, and capable of supporting advanced AI applications as a service. Native AI for IMT-2030 (6G) means building AI directly into the network’s core architecture, making it AI-first and pervasive, rather than adding AI as an overlay; this enables self-optimizing, intelligent networks that can autonomously manage resources, provide ubiquitous AI services, and offer seamless, context-aware experiences with minimal human intervention, fundamentally transforming both network operations and user applications by 2030.

- Ubiquitous Intelligence: Embedding AI everywhere, enabling distributed intelligence for AI model training, inference, and deployment directly within the network infrastructure, extending to the network edge.

- Autonomous Operations: AI handles complex tasks like network optimization, resource allocation, and automated maintenance (O&M) in real-time, reducing reliance on manual intervention.

- AI-as-a-Service (AIaaS): The network transforms into a unified platform providing both communication and AI capabilities, making AI accessible for various applications.

- Intelligent Processing: AI drives functions across the air interface, resource management, and control planes for highly efficient operations.

- Data-Driven Automation: Leverages big data and real-time analytics to predict issues, optimize performance, and automate complex decision-making.

- Seamless User Experience: Moves beyond touchscreens to AI-driven interactions, offering more natural and contextual computing.

- Autonomous Operations: AI will enable self-monitoring, self-optimization, and self-healing networks, drastically reducing the need for human intervention in operation and maintenance (O&M).

- Dynamic Resource Management: ML algorithms will analyze massive amounts of network data in real-time to predict traffic patterns and user demands, dynamically allocating bandwidth, power, and computing resources to ensure optimal performance and energy efficiency.

- AI-Native Air Interface: AI/ML models will replace traditional, manually engineered signal processing blocks in the physical layer (e.g., channel estimation, beam management) to adapt dynamically to complex and time-varying wireless environments, improving spectral efficiency.

- Enhanced Security: AI will be critical for real-time threat detection and automated incident response across the hyper-connected 6G ecosystem, identifying anomalies and mitigating security risks that are not well understood by current systems.

- Digital Twins: AI will power the creation and management of real-time digital twins (virtual replicas) of the physical network, allowing for sophisticated simulations and testing of network changes before real-world deployment.

- Pervasive Edge AI: AI model training and inference will be distributed throughout the network, from the cloud to the edge (devices, base stations), reducing latency and enabling real-time, localized decision-making for applications like autonomous driving and industrial automation.

- Support for Advanced Use Cases: The massive data rates (up to 1 Tbps), ultra-low latency, and high reliability enabled by AI in 6G will facilitate new applications such as holographic communication, remote robotic surgery with haptic feedback, and collaborative robotics that were not feasible with 5G.

- Federated Learning: The network will support distributed machine learning techniques, such as federated learning, which allow AI models to be trained on local data across various devices without the need to centralize sensitive user data, thus ensuring data privacy and security.

- Integrated Sensing and Communication (ISAC): AI will process the rich environmental data gathered through 6G’s new sensing capabilities (e.g., precise positioning, motion detection, environmental monitoring), allowing the network to interact with and understand the physical world in a holistic manner for applications like smart city management or augmented reality.

……………………………………………………………………………………………………………………………………………………………………..

AI‑native air interface and RAN:

IMT‑2030 explicitly expects a new AI‑native air interface that uses AI/ML models for core PHY/MAC functions such as channel estimation, symbol detection/decoding, beam management, interference handling, and CSI feedback. This enables adaptive waveforms and link control that react in real time to channel and traffic conditions, going beyond deterministic algorithms in 5G‑Advanced.

At the RAN level, IMT‑2030 envisions “native‑AI enabled” architectures that are simpler but more intelligent, with data‑driven operation and distributed learning across gNBs, edge nodes, and devices. AI/ML will be applied end‑to‑end for resource allocation, mobility, energy optimization, and fault management, effectively turning the RAN into a self‑optimizing, self‑healing system.

Integrated AI and communication services:

The framework defines “Artificial Intelligence and Communication” (often phrased as Integrated AI and Communication) as a specific usage scenario where the network provides AI compute, model hosting, and inference as a service. Example use cases include IMT‑2030‑assisted automated driving, cooperative medical robotics, digital twins, and offloading heavy computation from devices to edge/cloud via the 6G network.

To support this, IMT‑2030 includes “applicable AI‑related capabilities” such as distributed data processing, distributed learning, AI model execution and inference, and AI‑aware scheduling as native capabilities of the system. Computing and data services (not just connectivity) are treated as integral IMT‑2030 components, especially at the edge for low‑latency, energy‑efficient AI workloads.

System intelligence and new use cases:

AI is central to several new IMT‑2030 usage scenarios beyond classic eMBB/mMTC/URLLC, including Immersive Communication, Integrated Sensing and Communication, and Integrated AI and Communication. In integrated sensing, AI fuses multi‑dimensional radio sensing data (position, motion, environment, even human behavior) to provide contextual awareness for applications like smart cities, industrial control, and XR.

Embedding intelligence across air interface, edge, and cloud is seen as necessary to manage 6G complexity and enable “Intelligence of Everything,” including real‑time digital twins and AIGC‑driven services. The vision is for the 6G/IMT‑2030 network to act as a distributed neural system that tightly couples communication, sensing, and computing.

IMT 2030 Goals:

- To create self-healing, self-optimizing networks that can adapt to diverse demands.

- To enable new AI-driven applications, from intelligent digital twins to advanced immersive experiences.

- To build a truly intelligent communication fabric that supports a hyper-connected, AI-enhanced world.

Summary table: AI’s roles in IMT‑2030:

| Dimension | AI role in IMT‑2030 |

|---|---|

| Air interface | AI‑native PHY/MAC for channel estimation, decoding, beamforming, interference control. |

| RAN/core architecture | Native‑AI enabled, data‑driven, self‑optimizing/self‑healing network functions. |

| Compute and data services | Built‑in edge/cloud compute for AI training, inference, and data processing. |

| Usage scenarios | Dedicated “Integrated AI and Communication” plus AI‑rich sensing and immersive use cases. |

| Applications and ecosystems | Support for digital twins, automated driving, robotics, AIGC, and industrial automation. |

In summary, AI in IMT‑2030 is both an internal engine for network intelligence and an exported capability the network offers to verticals, making 6G effectively AI‑native end‑to‑end.

………………………………………………………………………………………………………………………………………………

References:

https://www.lightreading.com/ai-machine-learning/the-lessons-of-pluribus-for-telecom-s-genai-fans

https://www.ericsson.com/en/reports-and-papers/white-papers/ai-native

https://www.5gamericas.org/wp-content/uploads/2024/08/ITUs-IMT-2030-Vision_Id.pdf

ITU-R WP 5D Timeline for submission, evaluation process & consensus building for IMT-2030 (6G) RITs/SRITs

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

Ericsson and e& (UAE) sign MoU for 6G collaboration vs ITU-R IMT-2030 framework

Nokia and Rohde & Schwarz collaborate on AI-powered 6G receiver years before IMT 2030 RIT submissions to ITU-R WP5D

NTT DOCOMO successful outdoor trial of AI-driven wireless interface with 3 partners

Verizon’s 6G Innovation Forum joins a crowded list of 6G efforts that may conflict with 3GPP and ITU-R IMT-2030 work

ITU-R WP5D IMT 2030 Submission & Evaluation Guidelines vs 6G specs in 3GPP Release 20 & 21

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

Highlights of 3GPP Stage 1 Workshop on IMT 2030 (6G) Use Cases

Draft new ITU-R recommendation (not yet approved): M.[IMT.FRAMEWORK FOR 2030 AND BEYOND]

Analysis: OpenAI and Deutsche Telekom launch multi-year AI collaboration

Deutsche Telekom (DT) has formalized a strategic, multi-year collaboration with OpenAI to integrate advanced artificial intelligence (AI) solutions across its internal operations and customer engagement platforms. The partnership aims to co-develop “simple, personal, and multi-lingual AI experiences” focused on enhancing communication and productivity. Initial pilot programs are slated for deployment in Q1 2026. AI will also play a larger role in customer care, internal copilots, and network operations as the Group advances toward more autonomous, self-healing networks.DT plans a company-wide rollout of ChatGPT Enterprise, leveraging AI to streamline core functions including:

- Customer Care: Deploying sophisticated virtual assistants to manage billing inquiries, service outages, plan modifications, roaming support, and device troubleshooting [1].

- Internal Operations: Utilizing AI copilots to increase internal efficiency.

- Network Management: Optimizing core network provisioning and operations.

- Sovereign Cloud (2021): DT’s T-Systems division partnered with Google Cloud to offer sovereign cloud services.

- T Cloud Suite (Early 2025): The launch of a comprehensive suite providing sovereign public, private, and AI cloud options leveraging hybrid infrastructure.

- Industrial AI Cloud (Early 2025): A collaboration with Nvidia to build a dedicated industrial AI data center in Munich, scheduled for Q1 2026 operations.

- Edge AI compute services for enterprises.

- Vertical AI solutions tailored for healthcare, retail, and manufacturing sectors.

- Integrated private 5G and AI bundles for industrial logistical hubs.

“Telcos – if they execute – will have a big play in the edge inferencing space as well as providing hosting and colo services that can host domain specific SLMs that need to be run closer to the user data,” he said. “Furthermore, telcos will play a role in connectivity services across Neocloud providers such as CoreWeave, Lambda Labs, Digital Ocean, Vast.AI etc. OpenAI does not want to lose the opportunity to partner with telcos so they are striking early,” Nag added.

Other Voices:

- Roger Entner notes the model is highly applicable to European incumbents (e.g., Orange, Telefonica) due to the relative scarcity of existing AI data centers in the region, allowing operators to fill a critical infrastructure gap. Conversely, the model is less viable for U.S. operators, where hyperscalers already dominate the extensive data center market.

- AvidThink Founder and colleague Roy Chua cautions that while DT presents a robust “reference blueprint,” replicating this strategy requires significant scale, substantial financial investment, and regulatory alignment—factors not easily accessible to all network operators.

- Futurum Group VP and Practice Lead Nick Patience told Fierce Network, “This deal elevates DT from being a user of AI to being a co-developer, which is pretty significant. DT is one of the few operators building a full-stack AI story. This is an example of OpenAI treating telcos as high-scale distribution and data channels – customer care, billing, network telemetry, national reach and government relationships. This suggests OpenAI is deliberately building an operator channel in key regions (U.S., Korea, EU) but still in partnership with existing cloud and infra providers rather than displacing them.”

OpenAI has established significant partnerships with several telecom network providers and related technology companies to integrate AI into network operations, enhance customer experience, and develop new AI-native platforms. Those deals and collaborations include:

- T-Mobile: T-Mobile has a multi-year agreement with OpenAI and is actively testing the integration of AI (specifically IntentCX) into its business operations for customer service improvements. T-Mobile is also collaborating with Nokia and Nvidia on AI-RAN (Radio Access Network) technologies for 6G innovation.

- SK Telecom (SKT): SK Telecom has an in-house AI company and collaborates with OpenAI and other AI leaders like Anthropic to enhance its AI capabilities, build sovereign AI infrastructure, and explore new services for its customers in South Korea and globally. They are also reportedly integrating Perplexity into their offerings.

- Deutsche Telekom (DT): DT is partnering with OpenAI to offer ChatGPT Enterprise across its business to help teams work more effectively, improve customer service, and automate network operations.

- Circles: This global telco technology company and OpenAI announced a strategic global collaboration to build a fully AI-native telco SaaS platform, which will first launch in Singapore. The platform aims to revolutionize the consumer experience and drive operational efficiencies for telcos worldwide.

- Rakuten: Rakuten and OpenAI launched a strategic partnership to develop AI tools and a platform aimed at leveraging Rakuten’s Open RAN expertise to revolutionize the use of AI in telecommunications.

- Orange: Orange is working with OpenAI to drive new use cases for enterprise needs, manage networks, and enable innovative customer care solutions, including those that support African regional languages.

- Indian Telecoms (Reliance Jio, Airtel): Telecom providers in India are integrating AI tools from companies like Google and Perplexity into their mobile subscriptions, providing millions of users access to advanced intelligence resources.

- Nokia & Nvidia: In a broader industry collaboration, Nvidia invested $1 billion in Nokia to add Nvidia-powered AI-RAN products to Nokia’s portfolio, enabling telecom service providers to launch AI-native 5G-Advanced and 6G networks. This partnership also includes T-Mobile US for testing.

Conclusions:

With more than 261 million mobile customers globally, Deutsche Telekom provides a strong foundation to bring AI into everyday use at scale. The new collaboration marks the next step in Deutsche Telekom’s AI journey – moving from early pilots to large-scale products that make AI useful for everyone

References:

https://www.telekom.com/en/media/media-information/archive/openai-and-telekom-collaborate-1100164

https://www.telekom.com/en/company/companyprofile/company-profile-625808

Deutsche Telekom: successful completion of the 6G-TakeOff project with “3D networks”

Deutsche Telekom and Google Cloud partner on “RAN Guardian” AI agent

Deutsche Telekom offers 5G mmWave for industrial customers in Germany on 5G SA network

Deutsche Telekom migrates IP-based voice telephony platform to the cloud

Open AI raises $8.3B and is valued at $300B; AI speculative mania rivals Dot-com bubble

OpenAI and Broadcom in $10B deal to make custom AI chips

Custom AI Chips: Powering the next wave of Intelligent Computing

OpenAI orders HBM chips from SK Hynix & Samsung for Stargate UAE project

OpenAI announces new open weight, open source GPT models which Orange will deploy

OpenAI partners with G42 to build giant data center for Stargate UAE project

Reuters & Bloomberg: OpenAI to design “inference AI” chip with Broadcom and TSMC

Custom AI Chips: Powering the next wave of Intelligent Computing

by the Indxx team of market researchers with Alan J Weissberger

The Market for AI Related Semiconductors:

Several market research firms and banks forecast that revenue from AI-related semiconductors will grow at about 18% annually over the next few years—five times faster than non-AI semiconductor market segments.

- IDC forecasts that global AI hardware spending, including chip demand, will grow at an annual rate of 18%.

- Morgan Stanley analysts predict that AI-related semiconductors will grow at an 18% annual rate for a specific company, Taiwan Semiconductor (TSMC).

- Infosys notes that data center semiconductor sales are projected to grow at an 18% CAGR.

- MarketResearch.biz and the IEEE IRDS predict an 18% annual growth rate for AI accelerator chips.

- Citi also forecasts aggregate chip sales for potential AI workloads to grow at a CAGR of 18% through 2030.

AI-focused chips are expected to represent nearly 20% of global semiconductor demand in 2025, contributing approximately $67 billion in revenue [1]. The global AI chip market is projected to reach $40.79 billion in 2025 [2.] and continue expanding rapidly toward $165 billion by 2030.

…………………………………………………………………………………………………………………………………………………

Types of AI Custom Chips:

Artificial intelligence is advancing at a speed that traditional computing hardware can no longer keep pace with. To meet the demands of massive AI models, lower latency, and higher computing efficiency, companies are increasingly turning to custom AI chips which are purpose-built processors optimized for neural networks, training, and inference workloads.

Those AI chips include Application Specific Integrated Circuits (ASICs) and Field- Programmable Gate Arrays (FPGAs) to Neural Processing Units (NPUs) and Google’s Tensor Processing Units (TPUs). They are optimized for core AI tasks like matrix multiplications and convolutions, delivering far higher performance-per-watt than CPUs or GPUs. This efficiency is key as AI workloads grow exponentially with the rise of Large Language Models (LLMs) and generative AI.

OpenAI – Broadcom Deal:

Perhaps the biggest custom AI chip design is being done by an OpenAI partnership with Broadcom in a multi-year, multi-billion dollar deal announced in October 2025. In this arrangement, OpenAI will design the hardware and Broadcom will develop custom chips to integrate AI model knowledge directly into the silicon for efficiency.

Here’s a summary of the partnership:

- OpenAI designs its own AI processors (GPUs) and systems, embedding its AI insights directly into the hardware. Broadcom develops and deploys these custom chips and the surrounding infrastructure, using its Ethernet networking solutions to scale the systems.

- Massive Scale: The agreement covers 10 gigawatts (GW) of AI compute, with deployments expected over four years, potentially extending to 2029.

- Cost Savings: This custom silicon strategy aims to significantly reduce costs compared to off-the-shelf Nvidia or AMD chips, potentially saving 30-40% on large-scale deployments.

- Strategic Goal: The collaboration allows OpenAI to build tailored hardware to meet the intense demands of developing frontier AI models and products, reducing reliance on other chip vendors.

AI Silicon Market Share of Key Players:

- Nvidia, with its extremely popular AI GPUs and CUDA software ecosystem., is expected to maintain its market leadership. It currently holds an estimated 86% share of the AI GPU market segment according to one source [2.]. Others put NVIDIA’s market AI chip market share between 80% and 92%.

- AMD holds a smaller, but growing, AI chip market share, with estimates placing its discrete GPU market share around 4% to 7% in early to mid-2025. AMD is projected to grow its AI chip division significantly, aiming for a double-digit share with products like the MI300X. In response to the extraordinary demand for advanced AI processors, AMD’s Chief Executive Officer, Dr. Lisa Su, presented a strategic initiative to the Board of Directors: to pivot the company’s core operational focus towards artificial intelligence. Ms. Su articulated the view that the “insatiable demand for compute” represented a sustained market trend. AMD’s strategic reorientation has yielded significant financial returns; AMD’s market capitalization has nearly quadrupled, surpassing $350 billion [1]. Furthermore, the company has successfully executed high-profile agreements, securing major contracts to provide cutting-edge silicon solutions to key industry players, including OpenAI and Oracle.

- Intel accounts for approximately 1% of the discrete GPU market share, but is focused on expanding its presence in the AI training accelerator market with its Gaudi 3 platform, where it aims for an 8.7% share by the end of 2025. The former microprocessor king has recently invested heavily in both its design and manufacturing businesses and is courting customers for its advanced data-center processors.

- Qualcomm, which is best known for designing chips for mobile devices and cars, announced in October that it would launch two new AI accelerator chips. The company said the new AI200 and AI250 are distinguished by their very high memory capabilities and energy efficiency.

Big Tech Custom AI chips vs Nvidia AI GPUs:

Big tech companies, including Google, Meta, Amazon, and Apple—are designing their own custom AI silicon to reduce costs, accelerate performance, and scale AI across industries. Yet nearly all rely on TSMC for manufacturing, thanks to its leadership in advanced chip fabrication technology [3.]

- Google recently announced Ironwood, its 7th-generation Tensor Processing Unit (TPU), a major AI chip for LLM training and inference, offering 4x the performance of its predecessor (Trillium) and massive scalability for demanding AI workloads like Gemini, challenging Nvidia’s dominance by efficiently powering complex AI at scale for Google Cloud and major partners like Meta. Ironwood is significantly faster, with claims of over 4x improvement in training and inference compared to the previous Trillium (6th gen) TPU. It allows for super-pods of up to 9,216 interconnected chips, enabling huge computational power for cutting-edge models. It’s optimized for high-volume, low-latency AI inference, handling complex thinking models and real-time chatbots efficiently.

- Meta is in advanced talks to purchase and rent large quantities of Google’s custom AI chips (TPUs), starting with cloud rentals in 2026 and moving to direct purchases for data centers in 2027, a significant move to diversify beyond Nvidia and challenge the AI hardware market. This multi-billion dollar deal could reshape AI infrastructure by giving Meta access to Google’s specialized silicon for workloads like AI model inference, signaling a major shift in big tech’s chip strategy, notes this TechRadar article.

- According to a Wall Street Journal report published on December 2, 2025, Amazon’s new Trainium3 custom AI chip presents a challenge to Nvidia’s market position by providing a more affordable option for AI development. Four times as fast as its previous generation of AI chips, Amazon said Trainium3 (produced by AWS’s Annapurna Labs custom-chip design business) can reduce the cost of training and operating AI models by up to 50% compared with systems that use equivalent graphics processing units, or GPUs. AWS acquired Israeli startup Annapurna Labs in 2015 and began designing chips to power AWS’s data-center servers, including network security chips, central processing units, and later its AI processor series, known as Inferentia and Trainium. “The main advantage at the end of the day is price performance,” said Ron Diamant, an AWS vice president and the chief architect of the Trainium chips. He added that his main goal is giving customers more options for different computing workloads. “I don’t see us trying to replace Nvidia,” Diamant said.

- Interestingly, many of the biggest buyers of Amazon’s chips are also Nvidia customers. Chief among them is Anthropic, which AWS said in late October is using more than one million Trainium2 chips to build and deploy its Claude AI model. Nvidia announced a month later that it was investing $10 billion in Anthropic as part of a massive deal to sell the AI firm computing power generated by its chips.

Image Credit: Emil Lendof/WSJ, iStock

Other AI Silicon Facts and Figures:

- Edge AI chips are forecast to reach $13.5 billion in 2025, driven by IoT and smartphone integration.

- AI accelerators based on ASIC designs are expected to grow by 34% year-over-year in 2025.

- Automotive AI chips are set to surpass $6.3 billion in 2025, thanks to advancements in autonomous driving.

- Google’s TPU v5p reached 30% faster matrix math throughput in benchmark tests.

- U.S.-based AI chip startups raised over $5.1 billion in venture capital in the first half of 2025 alone.

Conclusions:

Custom silicon is now essential for deploying AI in real-world applications such as automation, robotics, healthcare, finance, and mobility. As AI expands across every sector, these purpose-built chips are becoming the true backbone of modern computing—driving a hardware race that is just as important as advances in software. More and more AI firms are seeking to diversify their suppliers by buying chips and other hardware from companies other than Nvidia. Advantages like cost-effectiveness, specialization, lower power consumption and strategic independence that cloud providers gain from developing their own in-house AI silicon. By developing their own chips, hyperscalers can create a vertically integrated AI stack (hardware, software, and cloud services) optimized for their specific internal workloads and cloud platforms. This allows them to tailor performance precisely to their needs, potentially achieving better total cost of ownership (TCO) than general-purpose Nvidia GPUs

However, Nvidia is convinced it will retain a huge lead in selling AI silicon. In a post on X, Nvida wrote that it was “delighted by Google’s success with its TPUs,” before adding that Nvidia “is a generation ahead of the industry—it’s the only platform that runs every AI model and does it everywhere computing is done.” The company said its chips offer “greater performance, versatility, and fungibility” than more narrowly tailored custom chips made by Google and AWS.

The race is far from over, but we can expect to surely see more competition in the AI silicon arena.

………………………………………………………………………………………………………………………………………………………………………………….

Links for Notes:

2. https://sqmagazine.co.uk/ai-chip-statistics/

3. https://www.ibm.com/think/news/custom-chips-ai-future

References:

https://www.wsj.com/tech/ai/amazons-custom-chips-pose-another-threat-to-nvidia-8aa19f5b

https://www.wsj.com/tech/ai/nvidia-ai-chips-competitors-amd-broadcom-google-amazon-6729c65a

AI infrastructure spending boom: a path towards AGI or speculative bubble?

OpenAI and Broadcom in $10B deal to make custom AI chips

Reuters & Bloomberg: OpenAI to design “inference AI” chip with Broadcom and TSMC

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

Cisco CEO sees great potential in AI data center connectivity, silicon, optics, and optical systems

Expose: AI is more than a bubble; it’s a data center debt bomb

China gaining on U.S. in AI technology arms race- silicon, models and research

AI infrastructure spending boom: a path towards AGI or speculative bubble?

by Rahul Sharma, Indxx with Alan J Weissberger, IEEE Techblog

Introduction:

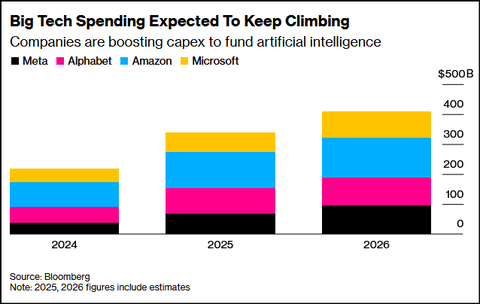

The ongoing wave of artificial intelligence (AI) infrastructure investment by U.S. mega-cap tech firms marks one of the largest corporate spending cycles in history. Aggregate annual AI investments, mostly for cloud resident mega-data centers, are expected to exceed $400 billion in 2025, potentially surpassing $500 billion by 2026 — the scale of this buildout rivals that of past industrial revolutions — from railroads to the internet era.[1]

At its core, this spending surge represents a strategic arms race for computational dominance. Meta, Alphabet, Amazon and Microsoft are racing to secure leadership in artificial intelligence capabilities — a contest where access to data, energy, and compute capacity are the new determinants of market power.

AI Spending & Debt Financing:

Leading technology firms are racing to secure dominance in compute capacity — the new cornerstone of digital power:

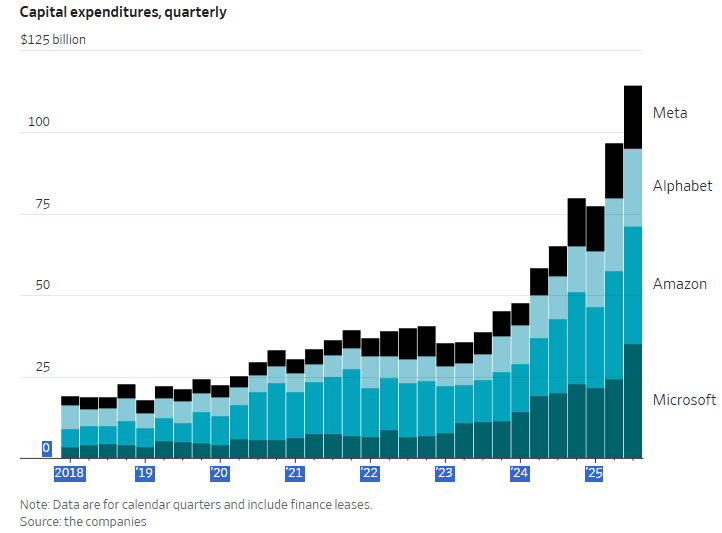

- Meta plans to spend $72 billion on AI infrastructure in 2025.

- Alphabet (Google) has expanded its capex guidance to $91–93 billion.[3]

- Microsoft and Amazon are doubling data center capacity, while AWS will drive most of Amazon’s $125 billion 2026 investment.[4]

- Even Apple, typically conservative in R&D, has accelerated AI infrastructure spending.

Their capex is shown in the chart below:

Analysts estimate that AI could add up to 0.5% to U.S. GDP annually over the next several years. Reflecting this optimism, Morgan Stanley forecasts $2.9 trillion in AI-related investments between 2025 and 2028. The scale of commitment from Big Tech is reshaping expectations across financial markets, enterprise strategies, and public policy, marking one of the most intense capital spending cycles in corporate history.[2]

Meanwhile, OpenAI’s trillion-dollar partnerships with Nvidia, Oracle, and Broadcom have redefined the scale of ambition, turning compute infrastructure into a strategic asset comparable to energy independence or semiconductor sovereignty.[5]

Growth Engine or Speculative Bubble?

As Big Tech pours hundreds of billions of dollars into AI infrastructure, analysts and investors remain divided — some view it as a rational, long-term investment cycle, while others warn of a potential speculative bubble. Yet uncertainty remains — especially around Meta’s long-term monetization of AGI-related efforts.[8]

Some analysts view this huge AI spending as a necessary step towards achieving Artificial General Intelligence (AGI) – an unrealized type of AI that possesses human-level cognitive abilities, allowing it to understand, learn, and adapt to any intellectual task a human can. Unlike narrow AI, which is designed for specific functions like playing chess or image recognition, AGI could apply its knowledge to a wide range of different situations and problems without needing to be explicitly programmed for each one.

Other analysts believe this is a speculative bubble, fueled by debt that can never be repaid. Tech sector valuations have soared to dot-com era levels – and, based on price-to-sales ratios, are well beyond them. Some of AI’s biggest proponents acknowledge the fact that valuations are overinflated, including OpenAI chairman Bret Taylor: “AI will transform the economy… and create huge amounts of economic value in the future,” Taylor told The Verge. “I think we’re also in a bubble, and a lot of people will lose a lot of money,” he added.

Here are a few AI bubble points and charts:

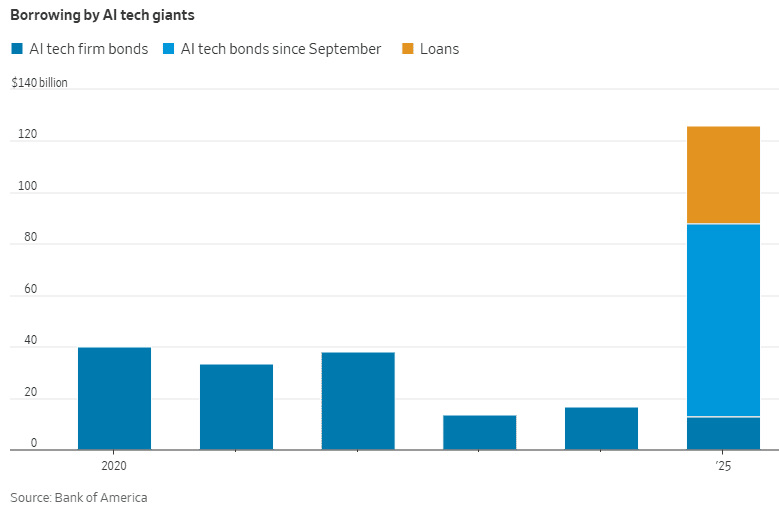

- AI-related capex is projected to consume up to 94% of operating cash flows by 2026, according to Bank of America.[6]

- Over $75 billion in AI-linked corporate bonds have been issued in just two months — a signal of mounting leverage. Still, strong revenue growth from AI services (particularly cloud and enterprise AI) keeps optimism alive.[7]

- Meta, Google, Microsoft, Amazon and xAI (Elon Musk’s company) are all using off-balance-sheet debt vehicles, including special-purpose vehicles (SPVs) to fund part of their AI investments. A slowdown in AI demand could render the debt tied to these SPVs worthless, potentially triggering another financial crisis.

- Alphabet’s (Google’s parent company) CEO Sundar Pichai sees “elements of irrationality” in the current scale of AI investing which is much more than excessive investments during the dot-com/fiber optic built-out boom of the late 1990s. If the AI bubble bursts, Pichai said that no company will be immune, including Alphabet, despite its breakthrough technology, Gemini, fueling gains in the company’s stock price.

…………………………………………………………………………………………………………………..

From Infrastructure to Intelligence:

Executives justify the massive spend by citing acute compute shortages and exponential demand growth:

- Microsoft’s CFO Amy Hood admitted, “We’ve been short on capacity for many quarters” and confirmed that the company will increase its spending on GPUs and CPUs in 2026 to meet surging demand.

- Amazon’s Andy Jassy noted that “every new tranche of capacity is immediately monetized”, underscoring strong and sustained demand for AI and cloud services.

- Google reported billions in quarterly AI revenue, offering early evidence of commercial payoff.

Macro Ripple Effects – Industrializing Intelligence:

AI data centers have become the factories of the digital age, fueling demand for:

- Semiconductors, especially GPUs (Nvidia, AMD, Broadcom)

- Cloud and networking infrastructure (Oracle, Cisco)

- Energy and advanced cooling systems for AI data centers (Vertiv, Schneider Electric, Johnson Controls, and other specialists such as Liquid Stack and Green Revolution Cooling).

| Company Name | Core Expertise | Key Solutions for AI Data Centers |

|---|---|---|

| Vertiv | Critical infrastructure (power & cooling) | Offers full-stack solutions with air and liquid cooling, power distribution units (PDUs), and monitoring systems, including the AI-ready Vertiv 360AI portfolio. |

| Schneider Electric | Energy management & automation | Provides integrated power and thermal management via its EcoStruxure platform, specializing in modular and liquid cooling solutions for HPC and AI applications. |

| Johnson Controls | HVAC & building solutions | Offers integrated, energy-efficient solutions from design to maintenance, including Silent-Aire cooling and YORK chillers, with a focus on large-scale operations. |

| Eaton | Power management | Specializes in electrical distribution systems, uninterruptible power supplies (UPS), and switchgear, which are crucial for reliable energy delivery to high-density AI racks. |

- LiquidStack: A leader in two-phase and modular immersion cooling and direct-to-chip systems, trusted by large cloud and hardware providers.

- Green Revolution Cooling (GRC): Pioneers in single-phase immersion cooling solutions that help simplify thermal management and improve energy efficiency.

- Iceotope: Focuses on chassis-level precision liquid cooling, delivering dielectric fluid directly to components for maximum efficiency and reduced operational costs.

- Asetek: Specializes in direct-to-chip (D2C) liquid cooling solutions and rack-level Coolant Distribution Units (CDUs) for high-performance computing.

- CoolIT Systems: Known for its custom direct liquid cooling technologies, working closely with server OEMs (Original Equipment Manufacturers) to integrate cold plates and CDUs for AI and HPC workloads.

–>This new AI ecosystem is reshaping global supply chains — but also straining local energy and water resources. For example, Meta’s massive data center in Georgia has already triggered environmental concerns over energy and water usage.

Global Spending Outlook:

- According to UBS, global AI capex will reach $423 billion in 2025, $571 billion by 2026 and $1.3 trillion by 2030, growing at a 25% CAGR during the period 2025-2030.

Compute demand is outpacing expectations, with Google’s Gemini saw 130 times rise in AI token usage over the past 18 months, highlighting soaring compute and Meta’s infrastructure needs expanding sharply.[9]

Conclusions:

The AI infrastructure boom reflects a bold, forward-looking strategy by Big Tech, built on the belief that compute capacity will define the next decade’s leaders. If Artificial General Intelligence (AGI) or large-scale AI monetization unfolds as expected, today’s investments will be seen as visionary and transformative. Either way, the AI era is well underway — and the race for computational excellence is reshaping the future of global markets and innovation.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Footnotes:

[1] https://www.investing.com/news/stock-market-news/ai-capex-to-exceed-half-a-trillion-in-2026-ubs-4343520?utm_medium=feed&utm_source=yahoo&utm_campaign=yahoo-www

[2] https://www.venturepulsemag.com/2025/08/01/big-techs-400-billion-ai-bet-the-race-thats-reshaping-global-technology/#:~:text=Big%20Tech’s%20$400%20Billion%20AI%20Bet:%20The%20Race%20That’s%20Reshaping%20Global%20Technology,-3%20months%20ago&text=The%20world’s%20largest%20technology%20companies,enterprise%20strategy%2C%20and%20public%20policy.

[3] https://www.businessinsider.com/big-tech-capex-spending-ai-earnings-2025-10?

[4] https://www.investing.com/analysis/meta-plunged-12-amazon-jumped-11–same-ai-race-different-economics-200669410

[5] https://www.cnbc.com/2025/10/15/a-guide-to-1-trillion-worth-of-ai-deals-between-openai-nvidia.html

[6] https://finance.yahoo.com/news/bank-america-just-issued-stark-152422714.html

[7] https://news.futunn.com/en/post/64706046/from-cash-rich-to-collective-debt-how-does-wall-street?level=1&data_ticket=1763038546393561

[8] https://www.businessinsider.com/big-tech-capex-spending-ai-earnings-2025-10?

[9] https://finance.yahoo.com/news/ai-capex-exceed-half-trillion-093015889.html

……………………………………………………………………………………………………………………………………………………………………………………………………………………………

About the Author:

Rahul Sharma is President & Co-Chief Executive Officer at Indxx – a provider of end-to-end indexing services, data and technology products. He has been instrumental in leading the firm’s growth since 2011. Raul manages Indxx’s Sales, Client Engagement, Marketing and Branding teams while also helping to set the firm’s overall strategic objectives and vision.

Rahul holds a BS from Boston College and an MBA with Beta Gamma Sigma honors from Georgetown University’s McDonough School of Business.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………

References:

Curmudgeon/Sperandeo: New AI Era Thinking and Circular Financing Deals

Expose: AI is more than a bubble; it’s a data center debt bomb

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

FT: Scale of AI private company valuations dwarfs dot-com boom

Amazon’s Jeff Bezos at Italian Tech Week: “AI is a kind of industrial bubble”

AI Data Center Boom Carries Huge Default and Demand Risks

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Nokia in major pivot from traditional telecom to AI, cloud infrastructure, data center networking and 6G

Reuters: US Department of Energy forms $1 billion AI supercomputer partnership with AMD

………………………………………………………………………………………………………………………………………………………………………….

GSMA, ETSI, IEEE, ITU & TM Forum: AI Telco Troubleshooting Challenge + TelecomGPT: a dedicated LLM for telecom applications

The GSMA — along with ETSI, IEEE GenAINet, the ITU, and TM Forum — today opened an innovation challenge calling on telco operators, AI researchers, and startups to build large-language models (LLMs) capable of root-cause analysis (RCA) for telecom network faults. The AI Telco Troubleshooting Challenge is supported by Huawei, InterDigital, NextGCloud, RelationalAI, xFlowResearch and technical advisors from AT&T.

The new competition invites teams to submit AI models in three categories: Generalization to New Faults will assess the best performing LLMs for RCA; Small Models at the Edge will evaluate lightweight edge-deployable models; and Explainability/Reasoning will focus on the AI systems that clearly explain their reasoning. Additional categories will include securing edge-cloud deployments and enabling AI services for application developers.

The goal is to deliver AI tools that help operators automatically identify, diagnose, and (eventually) remediate network problems — potentially reducing both downtime and operational costs. This marks a concrete step toward turning “telco-AI” from pilot projects into operational infrastructure.

As telecom networks scale (5G, 5G-Advanced, edge, IoT), faults and failures become costlier. Automating fault detection and troubleshooting with AI could significantly boost network resilience, reduce manual labor, and enable faster recovery from outages.

“Large Language Models have become instrumental in the pursuit of autonomous, resilient and adaptive networks,” said Prof. Merouane Debbah, General Chair of IEEE GenAINet ETI. “Through this challenge, we are tackling core research and engineering challenges, such as generalisation to unseen network faults, interpretability and edge-efficient AI, that are vital for making AI-native telecom infrastructures a reality. IEEE GenAINet ETI is proud to support this initiative, which serves as a testbed for future-ready innovations across the global telco ecosystem.”

“ITU’s global AI challenges connect innovators with computing resources, datasets, and expert mentors to nurture AI innovation ecosystems worldwide,” said Seizo Onoe, Director of the ITU Telecommunication Standardization Bureau. “Crowdsourcing new solutions and creating conditions for them to scale, our challenges boost business by helping innovations achieve meaningful impact.”

“The future of telecoms depends on the autonomation of network resiliency – shifting from static infrastructure to AI-driven, context-aware, self-optimising networks. TM Forum’s AI-Native Blueprint provides the architectural foundation to make this reality, and the AI Telco Troubleshooting Challenge aligns perfectly to support the industry in moving beyond isolated pilots to production-grade resilient autonomation,” said Guy Lupo, AI and Data Mission lead at TM Forum.

The initiative builds on recent breakthroughs in applying AI to network operations, leveraging curated datasets such as TeleLogs and benchmarking frameworks developed by GSMA and its partners under the GSMA Open-Telco LLM Benchmarks community, which includes a leaderboard that highlights how various LLMs perform on telco-specific use cases.

“Network faults cost operators millions annually and root cause analysis is a critical pain point for operators,” said Louis Powell, Director of AI Technologies at GSMA. “By harnessing AI models capable of reasoning and diagnosing unseen faults, the industry can dramatically improve reliability and reduce operational costs. Through this challenge, we aim to accelerate the development of LLMs that combine reasoning, efficiency and scalability.”

“We are encouraged by the upside of this challenge after our team at AT&T fine-tuned a 4-billion-parameter small language model that topped all other evaluated models on the GSMA Open-Telco LLM Benchmarks (TeleLogs RCA task), including frontier models such as GPT-5, Claude Sonnet 4.5 and Grok-4,” said Andy Markus, Chief Data Officer at AT&T. “This challenge has the right mix of an important business problem and a technical opportunity, and we welcome the industry’s collaboration to take it to the next level.”

The AI Telco Troubleshooting Challenge is open for submissions on the 28th November and it closes on 1st February 2026, with the winners announced at a dedicated prize-giving session at MWC26 Barcelona.

…………………………………………………………………………………………………………………………………………………………………………

Separately, the GSMA Foundry and Khalifa University announced a strategic collaboration to develop “TelecomGPT,” a dedicated LLM for telecom applications, plus an Open-Telco Knowledge Graph based on 3GPP specifications.

-

These assets are intended to help the industry overcome limitations of general-purpose LLMs, which often struggle with telecom-specific technical contexts. PR Newswire+2Mobile World Live+2

-

The plan: make TelecomGPT and related knowledge tools available for operators, vendors and researchers to accelerate AI-driven telco innovations. PR Newswire+1

Why it matters: A specialized “telco-native” LLM could improve automation, operations, R&D and standardization efforts — for example, helping operators configure networks, analyze logs, or build AI-powered services. It represents a shift toward embedding AI more deeply into core telecom infrastructure and operations.

…………………………………………………………………………………………………………………………………………………………………………………..

About GSMA

The GSMA is a global organization unifying the mobile ecosystem to discover, develop and deliver innovation foundational to positive business environments and societal change. Our vision is to unlock the full power of connectivity so that people, industry, and society thrive. Representing mobile operators and organizations across the mobile ecosystem and adjacent industries, the GSMA delivers for its members across three broad pillars: Connectivity for Good, Industry Services and Solutions, and Outreach. This activity includes advancing policy, tackling today’s biggest societal challenges, underpinning the technology and interoperability that make mobile work, and providing the world’s largest platform to convene the mobile ecosystem at the MWC and M360 series of events.

We invite you to find out more at gsma.com

About ETSI

ETSI is one of only three bodies officially recognized by the European Union as a European Standards Organization (ESO). It is an independent, not-for-profit body dedicated to ICT standardisation. With over 900 member organizations from more than 60 countries across five continents, ETSI offers an open and inclusive environment for members representing large and small private companies, research institutions, academia, governments, and public organizations. ETSI supports the timely development, ratification, and testing of globally applicable standards for ICT‑enabled systems, applications, and services across all sectors of industry and society. More on: etsi.org

About IEEE GenAINet

The aim of the IEEE Large Generative AI Models in Telecom Emerging Technology Initiative (GenAINet ETI) is to create a dynamic platform of research and innovation for academics, researchers, and industry leaders to advance the research on large generative AI in Telecom, through collaborative efforts across various disciplines, including mathematics, information theory, wireless communications, signal processing, networking, artificial intelligence, and more. More on: https://genainet.committees.comsoc.org

About ITU

The International Telecommunication Union (ITU) is the United Nations agency for digital technologies, driving innovation for people and the planet with 194 Member States and a membership of over 1,000 companies, universities, civil society, and international and regional organizations. Established in 1865, ITU coordinates the global use of the radio spectrum and satellite orbits, establishes international technology standards, drives universal connectivity and digital services, and is helping to make sure everyone benefits from sustainable digital transformation, including the most remote communities. From artificial intelligence (AI) to quantum, from satellites and submarine cables to advanced mobile and wireless broadband networks, ITU is committed to connecting the world and beyond. Learn more: www.itu.int

About TM Forum

TM Forum is an alliance of over 800 organizations spanning the global connectivity ecosystem, including the world’s top ten Communication Service Providers (CSPs), top three hyperscalers and Network Equipment Providers (NEPs), vendors, consultancies and system integrators, large and small. We provide a place for our Members to collaborate, innovate, and deliver lasting change. Together, we are building a sustainable future for the industry in connectivity and beyond. To find out more, visit: www.tmforum.org

References:

The AI Telco Troubleshooting Challenge Launches to Transform Network Reliability

AI Telco Troubleshooting Challenge global launch webinar

GSMA Vision 2040 study identifies spectrum needs during the peak 6G era of 2035–2040

Gartner: Gen AI nearing trough of disillusionment; GSMA survey of network operator use of AI

Expose: AI is more than a bubble; it’s a data center debt bomb

We’ve previously described the tremendous debt that AI companies have assumed, expressing serious doubts that it will ever be repaid. This article expands on that by pointing out the huge losses incurred by the AI startup darlings and that AI poster child Open AI won’t have the cash to cover its costs 9which are greater than most analysts assume). Also, we quote from the Wall Street Journal, Financial Times, Barron’s, along with a dire forecast from the Center for Public Enterprise.

In Saturday’s print edition, The Wall Street Journal notes:

OpenAI and Anthropic are the two largest suppliers of generative AI with their chatbots ChatGPT and Claude, respectively, and founders Sam Altman and Dario Amodei have become tech celebrities.

What’s only starting to become clear is that those companies are also sinkholes for AI losses that are the flip side of chunks of the public-company profits.

OpenAI hopes to turn profitable only in 2030, while Anthropic is targeting 2028. Meanwhile, the amounts of money being lost are extraordinary.

It’s impossible to quantify how much cash flowed from OpenAI to big tech companies. But OpenAI’s loss in the quarter equates to 65% of the rise in underlying earnings of Microsoft, Nvidia, Alphabet, Amazon and Meta together. That ignores Anthropic, from which Amazon recorded a profit of $9.5B from its holding in the loss-making company in the quarter.

OpenAI committed to spend $250 billion more on Microsoft’s cloud and has signed a $300 billion deal with Oracle, $22 billion with CoreWeave and $38 billion with Amazon, which is a big investor in rival Anthropic.

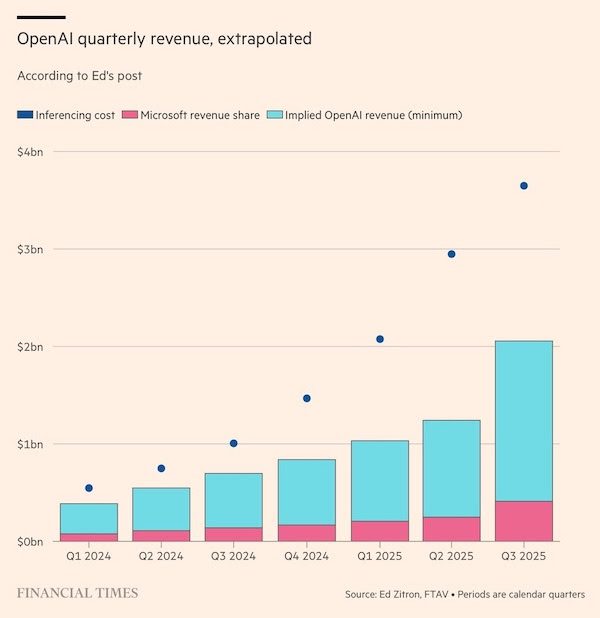

OpenAI doesn’t have the income to cover its costs. It expects revenue of $13 billion this year to more than double to $30 billion next year, then to double again in 2027, according to figures provided to shareholders. Costs are expected to rise even faster, and losses are predicted to roughly triple to more than $40 billion by 2027. Things don’t come back into balance even in OpenAI’s own forecasts until total computing costs finally level off in 2029, allowing it to scrape into profit in 2030.

The losses at OpenAI that has helped boost the profits of Big Tech may, in fact, understate the true nature of the problem. According to the Financial Times:

OpenAI’s running costs may be a lot more than previously thought, and that its main backer Microsoft is doing very nicely out of their revenue share agreement.

OpenAI appears to have spent more than $12.4bn at Azure on inference compute alone in the last seven calendar quarters. Its implied revenue for the period was a minimum of $6.8bn. Even allowing for some fudging between annualised run rates and period-end totals, the apparent gap between revenues and running costs is a lot more than has been reported previously.

The apparent gap between revenues and running costs is a lot more than has been reported previously. If the data is accurate, then it would call into question the business model of OpenAI and nearly every other general-purpose LLM vendor.

Also, the financing needed to build out the data centers at the heart of the AI boom is increasingly becoming an exercise in creative accounting. The Wall Street Journal reports:

The Hyperion deal is a Frankenstein financing that combines elements of private-equity, project finance and investment-grade bonds. Meta needed such financial wizardry because it already issued a $30B bond in October that roughly doubled its debt load overnight.

Enter Morgan Stanley, with a plan to have someone else borrow the money for Hyperion. Blue Owl invested about $3 billion for an 80% private-equity stake in the data center, while Meta retained 20% for the $1.3 billion it had already spent. The joint venture, named Beignet Investor after the New Orleans pastry, got another $27 billion by issuing bonds that pay off in 2049, $18 billion of which Pimco purchased. That debt is on Beignet’s balance sheet, not Meta’s.

Dan Fuss, vice chairman of Loomis Sayles told Barrons: “We are good at taking credit risk,” Dan said, cheerfully admitting to having the scars to show for it. That is, he added, if they know the credit. But that’s become less clear with the recent spate of mind-bendingly complex megadeals, with myriad entities funding multibillion-dollar data centers. Fuss thinks current data-center deals are too speculative. The risk is too great and future revenue too uncertain. And yields aren’t enough to compensate, he concluded.

Increased wariness about monster hyper-scaler borrowings has sent the cost of insuring their debt against default soaring. Credit default swaps (CDS) more than doubled for Oracle since September, after it issued $18 billion in public bonds and took out a $38 billion private loan. CoreWeave’s CDS gapped higher this past week, mirroring the slide of the data-center company’s stock.

According to the Bank Credit Analyst (BCA), capex busts weigh on the economy, which further hits asset prices, the firm says. Following the dot-com bust, a housing bubble grew, which burst in the 2008-09 financial crisis. “It is far from certain that a new bubble will emerge (after the AI bubble bursts) this time around, in which case the resulting recession could be more severe than the one in 2001,” BCA notes.

………………………………………………………………………………………………………………………………………………

The widening gap between the expenditures needed to build out AI data centers and the cash flows generated by the products they enable creates a colossal risk which could crash asset values of AI companies. The Center for Public Enterprise reports that it’s “Bubble or Nothing.”

Should economic conditions in the tech sector sour, the burgeoning artificial intelligence (AI) boom may evaporate—and, with it, the economic activity associated with the boom in data center development.

Circular financing, or “roundabouting,” among so-called hyperscaler tenants—the leading tech companies and AI service providers—create an interlocking liability structure across the sector. These tenants comprise an incredibly large share of the market and are financing each others’ expansion, creating concentration risks for lenders and shareholders.

Debt is playing an increasingly large role in the financing of data centers. While debt is a quotidian aspect of project finance, and while it seems like hyperscaler tech companies can self-finance their growth through equity and cash, the lack of transparency in some recent debt-financed transactions and the interlocked liability structure of the sector are cause for concern.

If there is a sudden stop in new lending to data centers, Ponzi finance units ‘with cash flow shortfalls will be forced to try to make position by selling out position’—in other words to force a fire sale—which is ‘likely to lead to a collapse of asset values.’

The fact that the data center boom is threatened by, at its core, a lack of consumer demand and the resulting unstable investment pathways, is itself an ironic miniature of the U.S. economy as a whole. Just as stable investment demand is the linchpin of sectoral planning, stable aggregate demand is the keystone in national economic planning. Without it, capital investment crumbles.

……………………………………………………………………………………………………………..

Postscript (November 23, 2025):

In addition to cloud/hyperscaler AI spending, AI start-ups (especially OpenAI) and newer IT infrastructure companies (like Oracle) play a prominent role. It’s often a “scratch my back and I’ll scratch yours” type of deal. Let’s look at the “circular financing” arrangement between Nvidia and OpenAI where capital flows from Nvidia to OpenAI and then back to Nvidia. That ensures Nvidia a massive, long-term customer and providing OpenAI with the necessary capital and guaranteed access to critical, high-demand hardware. Here’s the scoop:

- Nvidia has agreed to invest up to $100 billion in OpenAI over time. This investment will be in cash, likely for non-voting equity shares, and will be made in stages as specific data center deployment milestones are met.

- OpenAIhas committed to building and deploying at least 10 gigawatts of AI data center capacity using Nvidia’s silicon and equipment, which will involve purchasing millions of Nvidia expensive GPU chips.

Here’s the Circular Flow of this deal:

- Nvidia provides a cash investment to OpenAI.

- OpenAI uses that capital (and potentially raises additional debt using the commitment as collateral) to build new data centers.

- OpenAI then uses the funds to purchase Nvidia GPUs and other data center infrastructure.

- The revenue from these massive sales flows back to Nvidia, helping to justify its soaring stock price and funding further investments.

What’s wrong with such an arrangement you ask? Anyone remember the dot-com/fiber optic boom and bust? Critics have drawn parallels to the “vendor financing” practices of the dot-com era, arguing these interconnected deals could create a “mirage of growth” and potentially an AI bubble, as the actual organic demand for the products is difficult to assess when companies are essentially funding their own sales.

However, supporters note that, unlike the dot-com bubble, these deals involve the creation of tangible physical assets (data centers and chips) and reflect genuine, booming demand for AI compute capacity although it’s not at all certain how they’ll be paid for.

There’s a similar cozy relationship with the $1B Nvidia invested in Nokia with the Finnish company now planning to ditch Marvell’s silicon and replace it by buying the more expensive, power hungry Nvidia GPUs for its wireless network equipment. Nokia, has only now become a strong supporter of Nvidia’s AI RAN (Radio Access Network), which has many telco skeptics.

………………………………………………………………………………………………………………………………………………….

References:

https://www.wsj.com/tech/ai/big-techs-soaring-profits-have-an-ugly-underside-openais-losses-fe7e3184

https://www.ft.com/content/fce77ba4-6231-4920-9e99-693a6c38e7d5

https://www.wsj.com/tech/ai/three-ai-megadeals-are-breaking-new-ground-on-wall-street-896e0023

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

AI Data Center Boom Carries Huge Default and Demand Risks

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

Gartner: AI spending >$2 trillion in 2026 driven by hyperscalers data center investments

Amazon’s Jeff Bezos at Italian Tech Week: “AI is a kind of industrial bubble”

FT: Scale of AI private company valuations dwarfs dot-com boom

Indosat Ooredoo Hutchison, Nokia and Nvidia AI-RAN research center in Indonesia amongst telco skepticism

Indosat Ooredoo Hutchison (Indosat) Nokia, and Nvidia have officially launched the AI-RAN Research Centre in Surabaya, a strategic collaboration designed to advance AI-native wireless networks and edge AI applications across Indonesia. This collaboration, aims to support Indonesia’s digital transformation goals and its “Golden Indonesia Vision 2045.” The facility will allow researchers and engineers to experiment with combining Nokia’s RAN technologies with Nvidia’s accelerated computing platforms and Indosat’s 5G network.

According to the partners, the research facility will serve as a collaborative environment for engineers, researchers, and future digital leaders to experiment, learn, and co-create AI-powered solutions. Its work will centre on integrating Nokia’s advanced RAN technologies with Nvidia’s accelerated computing platforms and Indosat’s commercial 5G network. The three companies view the project as a foundation for AI-driven growth, with applications spanning education, agriculture, and healthcare.

The AI-RAN infrastructure enables high-performance software-defined RAN and AI workloads on a single platform, leveraging Nvidia’s Aerial RAN Computer 1 (ARC-1). The facility will also act as a distributed computing extension of Indosat’s sovereign AI Factory, a national AI platform powered by Nvidia, creating an “AI Grid” that connects datacentres and distributed 5G nodes to deliver intelligence closer to users.

Nezar Patria, vice minister of communication and digital affairs of the Republic of Indonesia said: “The inauguration of the AI-RAN Research Centre marks a concrete step in strengthening Indonesia’s digital sovereignty. The collaboration between the government, industry, and global partners such as Indosat, Nokia, and Nvidia demonstrates that Indonesia is not merely a user but also a creator of AI technology. This initiative supports the acceleration of the Indonesia Emas 2045 vision by building an inclusive, secure, and globally competitive AI ecosystem.”

Vikram Sinha, president director and CEO of Indosat Ooredoo Hutchison said: “As Indonesia accelerates its digital transformation, the AI-RAN Research Centre reflects Indosat’s larger purpose of empowering Indonesia. When connectivity meets compute, it creates intelligence, delivered at the edge, in a sovereign manner. This is how AI unlocks real impact, from personalised tutors for children in rural areas to precision farming powered by drones. Together with Nokia and Nvidia, we’re building the foundation for AI-driven growth that strengthens Indonesia’s digital future.”

From a network perspective, the project demonstrates how AI-RAN architectures can optimize wireless network performance, energy efficiency, and scalability through machine learning–based radio signal processing.

Ronnie Vasishta, senior vice president of telecom at Nvidia added: “The AI Grid is the biggest opportunity for telecom providers to make AI as ubiquitous as connectivity and distribute intelligence at scale by tapping into their nationwide wireless networks.”