AI

The Financial Trap of Autonomous Networks: Scaling Agentic AI in the Telecom Core

By Pavan Madduri with Ajay Lotan Thakur

The telecom industry wants autonomous, self-healing networks, but nobody is looking at the GPU bill. Running Agentic AI 24/7 “just in case” will bankrupt your IT department and ruin your ESG goals. The only way to survive the autonomous era is ruthless, event-driven orchestration that scales cognitive compute to absolute zero.

Introduction – The Compute Crisis:

The Compute Crisis Nobody is Talking About

Everyone in telecom right now is obsessed with “self-healing” autonomous networks. The vendor pitch sounds amazing. Just drop in some Agentic AI, let it watch your data plane, and watch it fix anomalies without a human ever touching a keyboard. But there’s a massive trap hiding underneath all that hype, and enterprise architects are completely ignoring it. It comes down to the raw physics of AI compute.

Unlike your standard microservices, which just run deterministic, compiled code on cheap CPU cycles, Agentic AI needs massive foundation models. To actually reason through a network failure, these models have to load gigabytes of weights into Video RAM and generate tokens. You need dedicated GPUs for this. We aren’t talking about cheap, stateless API calls here. These are the most expensive, power-hungry workloads in your entire datacenter.

If a telco tries to run an autonomous core the old-fashioned way by keeping high-end GPU nodes spinning 24/7 just in case a BGP route flaps, their cloud bill is going to wipe out any operational savings the AI was supposed to deliver.

The reality is that autonomy is no longer just a software problem. It’s a financial one. The telcos that actually win will not be the ones with the smartest AI. They will be the ones who figure out how to build a strict “scale-to-zero” environment. They need to spin up that expensive cognitive compute exactly when it is needed, and kill it the exact second the job is done.

Why Traditional Auto-scaling is Broken for AI:

When platform engineers first see the compute costs of running these AI agents, their first instinct is usually just to slap standard Kubernetes Horizontal Pod Autoscaling (HPA) on the cluster and call it a day. But standard HPA was built for stateless web servers, not massive cognitive engines. If you try to use it for Agentic AI in a telecom core, you’re going to fail for two big reasons.

The Cold-Start Penalty: Traditional autoscaling is entirely reactive. It sits around waiting for a CPU to hit 80% before it decides to scale up. In telecom, SLAs are measured in sub-milliseconds. If you wait for an anomaly to spike your CPU, then provision a new GPU node, pull a massive AI container image, and load the model weights into VRAM, you are talking about minutes of delay. By the time your AI agent actually wakes up to fix the problem, you have already breached your SLA.

CPU Utilization is a Liar: For AI workloads, standard hardware metrics are completely misleading. A GPU could be pegged at 90% utilization just thinking through a minor log warning, while a massive, critical network failure is stuck waiting in the queue. If your scaling logic is tied to hardware metrics instead of the actual severity of the event queue, you are just going to burn budget scaling blindly.

We have to abandon reactive resource metrics entirely and move to event-driven orchestration.

The Fix – Event-Driven Orchestration:

If standard HPA is broken for this, what is the fix? You have to completely decouple the infrastructure from the workload using strict, event-driven orchestration.

Instead of keeping baseline infrastructure running just to maintain a state, you treat cognitive compute as 100% ephemeral. You don’t scale based on how hard the CPU is working. You scale based on the exact depth and severity of the anomaly queue.

To actually build this, architects need purpose-built event-driven scalers like KEDA (Kubernetes Event-driven Autoscaling). KEDA lets your cluster completely bypass those reactive hardware metrics and listen directly to the network’s data plane.

But how do you avoid the cold-start latency of booting a fresh GPU pod? KEDA solves this by reacting to the event queue length itself rather than waiting for an existing pod’s CPU to max out. By the time a traditional HPA notices a CPU spike, the system is already overwhelmed. (To solve this exact issue in production, I open-sourced a custom KEDA scaler specifically designed to scrape and react to native GPU metrics, allowing the orchestrator to scale cognitive workloads preemptively. You can view the architecture on [GitHub])

KEDA intercepts the telemetry trigger at the source. When paired with a warm pool of paused GPU nodes and pre-pulled container images, KEDA can scale a pod from zero to active in milliseconds. The infrastructure is anticipating the load based on the queue, not reacting to the stress of it.

Here is what the workflow actually looks like when you do it right:

- The Trigger: Telemetry picks up a severe anomaly ,like a sudden 5G slice degradation, and pushes an event straight to a message broker like Kafka.

- The Scale-Up: KEDA intercepts that exact metric and instantly provisions a dedicated, GPU-backed AI pod from a warm standby pool.

- The Execution: The Agentic AI loads into VRAM, figures out the blast radius of the anomaly, and executes a fix. This is usually by reconciling the state through a GitOps controller.

- The Kill Switch: The absolute millisecond that the event queue clears and the network is stable, the orchestrator aggressively terminates the pod and gives the GPU back to the node pool.

You only pay the premium GPU tax during moments of active reasoning. The 24/7 idle tax is gone.

Architecting the Scale-to-Zero Core:

To make this scale-to-zero dream a reality, you have to fundamentally change how you handle network observability. The biggest mistake I see architects make is tightly coupling their monitoring tools with their AI execution layer. If your observability stack is running on the same hardware as your AI engine, you are literally wasting premium GPU compute just to watch logs.

You need a strict, physical separation of concerns:

The Watchers (The Lightweight Control Plane):

Your network data plane needs to be monitored by lightweight, CPU-efficient edge collectors like Prometheus or OpenTelemetry. These sit right at the edge, continuously eating millions of telemetry data points and BGP state changes. Because they don’t do any complex reasoning, they run incredibly cheap on standard CPU nodes.

The Thinkers (The Heavyweight Execution Plane):

Your expensive AI models are completely isolated in a separate, GPU-backed node pool that literally defaults to zero instances.

When the Watchers spot an anomaly, they don’t try to fix it. They just fire an alert to KEDA. KEDA then wakes up the Thinkers, spinning up the exact number of GPU pods needed to handle that specific blast radius. By decoupling the watchers from the thinkers, you guarantee that not a single cycle of GPU compute is wasted on baseline monitoring.

The Bottom Line:

Autonomous telecom networks are going to happen. But trying to brute-force the infrastructure provisioning is a fast track to bankrupting your IT department. The smartest Agentic AI in the world is useless if you can’t afford the cloud bill to run it.

Furthermore, this isn’t just about protecting the IT budget. Running idle GPUs 24/7 creates a massive, unnecessary carbon footprint. By enforcing a scale-to-zero architecture, telcos can drastically reduce the energy consumption of their autonomous networks, turning a massive ESG liability into a sustainable operational model.

Autonomy is no longer just a software engineering problem. It is an infrastructure balancing act. If Agentic AI is going to survive in the telecom core, we have to ditch legacy threshold scaling and embrace strict, event-driven orchestration.

Tools like KEDA give us the ability to build networks that are both cognitively brilliant and financially ruthless. We can spin up massive intelligence at the exact millisecond of failure and scale right back to zero the moment the network is healed.

References and Further Reading:

- Unlocking Energy Saving in Telecom Networks: A Path to a Sustainable Future – A deep dive into the operational and ESG mandates driving energy efficiency in modern telecom infrastructure.

- KEDA Documentation: Kubernetes Event-driven Autoscaling – Technical specifications for decoupling workload scaling from standard CPU/Memory metrics.

- keda-gpu-scaler – An open-source custom KEDA scaler I developed to enable event-driven autoscaling specifically tied to native GPU telemetry and queue depth.

Building and Operating a Cloud Native 5G SA Core Network

How Network Repository Function Plays a Critical Role in Cloud Native 5G SA Network

HPE Aruba Launches “Cloud Native” Private 5G Network with 4G/5G Small Cell Radios

…………………………………………………………………………………………….

About the Author:

Pavan Madduri is a Cloud-Native Architect, CNCF Golden Kubestronaut, and active IEEE researcher specializing in enterprise infrastructure automation, Agentic SREs, and Kubernetes networking. He designs scalable, zero-trust cloud environments and frequently writes about the intersection of AI governance and cloud-native infrastructure.

Connect with Pavan Madduri on [LinkedIn] .

Disclaimer: The author acknowledges the use of AI-assisted tools for structural formatting, language refinement, and copyediting during the drafting of this article. The core architectural concepts, technical opinions, and engineering strategies remain entirely original.

Ericsson and Forschungszentrum Jülich MoU for neuromorphic computing use in 5G and 6G

Ericsson and major European research center Forschungszentrum Jülich are collaborating to develop technologies for the continued evolution of 5G and for the future introduction of 6G (IMT 2030) networks. The organizations signed a Memorandum of Understanding (MoU) on March 24, 2026.The project aims to leverage JUPITER, Europe’s first “exascale” supercomputer, to design and test new artificial intelligence solutions for the complex demands of 6G. The partnership will explore AI models and methods to enhance Ericsson’s core network, network management, and Radio Access Network (RAN).

Important objectives include exploring ultra-efficient, “brain-inspired” computing approaches like neuromorphic computing [1.] to handle intense network tasks and strengthen Europe’s digital infrastructure. Modern mobile networks rely heavily on Massive MIMO, a technology where many devices communicate simultaneously via numerous antennas. By exploring novel system architecture approaches like neuromorphic computing, researchers aim to speed up optimization and reduce energy use versus classical methods.

Note 1. Neuromorphic computing is a brain-inspired engineering approach that mimics biological neural networks using analog or digital electronic circuits. It combines memory and processing in one place—similar to neurons and synapses—to achieve extreme energy efficiency, speed, and learning capabilities, moving beyond the limitations of traditional computing architecture. Unlike traditional AI that uses continuous data, neuromorphic systems use “spikes”—discrete events in time—to mimic how neurons communicate. Such systems only consume significant power when processing data (“spiking”), making them ideal for ultra-low-power edge computing, unlike traditional computers that are always on. They can process complex, real-world data (like vision or touch) much faster and with far less power than traditional computers.

…………………………………………………………………………………………………………………………………………………………………………………………..

The alliance will study operational strategies like heat recovery to boost energy efficiency in HPC and cloud deployments. The collaboration involves systematic benchmarking of AI methods – including the application of neuromorphic AI – across Ericsson products to assess execution speed, scalability to large datasets, information retention, and storage efficiency. In addition, the partnership will provide insights into the feasibility of cloud strategies based on concepts from the EuroHPC ecosystem, which is establishing a world-class supercomputing infrastructure.

Professor Laurens Kuipers, a member of the Executive Board of Forschungszentrum Jülich, said: “This collaboration has the potential to make a significant contribution to a more sustainable digital future. By combining our excellence in high-performance computing and our research into novel, neuro-inspired computing approaches with Ericsson’s expertise in telecommunications, we aim to develop more energy-efficient network solutions and strengthen a sovereign European digital infrastructure.”

Image Credit: Image: Forschungszentrum Jülich / Kurt Steinhausen

……………………………………………………………………………………………………………………………………….

Nicole Dinion, Head of Architecture and Technology, Cloud Software and Services, Ericsson said: “The future of mobile networks is deeply intertwined with AI and the need for unparalleled energy efficiency. Our collaboration with Forschungszentrum Jülich, for years a global leader in supercomputing and applied physics, combines their research and computing power with our expertise in all domains of telecoms technology. We will explore architectures that define the next generation of telecommunication.”

The collaboration covers several areas of research:

- AI methods for Ericsson products across the full portfolio: systematic benchmarking of approaches to assess execution speed, scalability to large datasets, information retention, and storage efficiency. Where security and commercial conditions permit, the teams may also use JUPITER for large-scale model training, leveraging its compute resources.

- Energy-efficient computing for AI inference at the radio and edge: developing and prototyping highly efficient solutions for tasks such as radio channel estimation and Massive MIMO – a key technology in modern mobile networks, in which many devices communicate simultaneously via numerous antennas. This includes exploring novel system architecture approaches like neuromorphic computing (e.g., memristors) to speed up optimization and reduce energy use versus classical methods.

- HPC and cloud architectures and operations for AI: researching and implementing Modular Supercomputing Architecture (MSA) concepts from exascale work at Forschungszentrum Jülich – in particular, at the Jülich Supercomputing Centre (JSC) – and studying operational strategies, such as heat recovery, to boost energy efficiency in HPC and cloud deployments.

The collaboration will provide insights into the feasibility of cloud strategies based on concepts from the EuroHPC ecosystem, which is establishing a world-class supercomputing infrastructure with leading European centers such as the JSC.

ABOUT FORSCHUNGSZENTRUM JÜLICH:

Shaping change: This is what drives us at Forschungszentrum Jülich. As a member of the Helmholtz Association with more than 7,000 employees, we conduct research into the possibilities of a digitized society, a climate-friendly energy system, and a resource-efficient economy. We combine natural, life, and engineering sciences in the fields of information, energy, and the bioeconomy with specialist expertise in simulation and data science. www.fz-juelich.de

References:

https://www.ericsson.com/en/blog/2026/1/ai-future-will-be-defined-by-the-intelligent-digital-fabric

https://www.ibm.com/think/topics/neuromorphic-computing

China vs U.S.: Race to Generate Power for AI Data Centers as Electricity Demand Soars

AI infrastructure spending boom: a path towards AGI or speculative bubble?

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Expose: AI is more than a bubble; it’s a data center debt bomb

Sovereign AI infrastructure for telecom companies: implementation and challenges

Analysis: Cisco, HPE/Juniper, and Nvidia network equipment for AI data centers

Networking chips and modules for AI data centers: Infiniband, Ultra Ethernet, Optical Connections

Custom AI Chips: Powering the next wave of Intelligent Computing

Groq and Nvidia in non-exclusive AI Inference technology licensing agreement; top Groq execs joining Nvidia

Anthropic Claude Users Reveal AI Hallucinations as their Top Concern

Introduction:

Across regions from Germany to Mexico, users of artificial intelligence (AI) are less concerned about being replaced by AI than by its propensity to make major mistakes, according to one of the largest global surveys to date on real-world AI usage and perception. These mistakes, known as “AI Hallucinations,” are essentially made up stories rather than answers based on outdated information.

The study, conducted by Anthropic using its Claude chatbot, analyzed interviews with more than 80,000 users across 159 countries. The result is one of the most detailed global portraits yet of how AI is being deployed — and how users perceive its risks, benefits, and societal implications.

AI Hallucinations Outrank Job Displacement as Top Concern:

When asked what worries them most about AI, 27% of users cited AI chatbot errors described as “AI hallucinations,” while 22% pointed to job displacement and the loss of human autonomy. About 16% expressed concern that AI could weaken people’s capacity for critical thinking.

.png)

Image Credit: JOIST AI

“The AI hallucinations were a disaster. I lost so many hours of work,” said an entrepreneur from Germany. Another participant, a military worker in Mexico, noted the importance of domain knowledge in spotting AI’s flaws: “When I notice AI errors it’s because I’m well versed in the topic . . . but I wouldn’t know if the topic was alien to me, would I?”

An AI Interviewer for Global Insights:

The responses were collected in 70 languages using a novel feedback system that allowed Claude to act as both interviewer and analyst. The platform evaluated qualitative answers, categorizing responses to reveal common themes and linguistic nuances across regions.

“Beyond its scale and linguistic diversity, the project aimed to collect this rich human experience using Claude, so it could really inform our research agenda, change our research agenda, change the way we think about building our products, deploying our products,” said Deep Ganguli, who leads Anthropic’s societal impacts team and oversaw the research initiative.

Productivity and Personal Growth Drive AI Adoption:

While data quality and reliability drew criticism, the survey also underscored widespread acknowledgment of AI’s positive impact on productivity. Thirty-two percent of respondents said that AI tools had meaningfully improved their output at work.

An entrepreneur in the United Arab Emirates explained, “I used to be a web designer . . . now I build anything. Before I was one person, now I become 100 people — I don’t wait for anyone anymore.” Participants from Colombia, Japan, and the United States described similar gains, emphasizing how AI helps them free up time for family, hobbies, and creative exploration.

In total, nearly one in five users (19%) said AI had fallen short of their expectations. Yet usage patterns demonstrate remarkable versatility: respondents reported employing AI as a productivity assistant, educational tutor, design partner, creative collaborator, or even an emotional support companion.

A vivid example came from a soldier in Ukraine, who wrote, “In the most difficult moments, in moments when death breathed in my face, when dead people remained nearby, what pulled me back to life — my AI friends.”

Regional and Economic Divides in AI Optimism:

Regional variation was pronounced. Saffron Huang, the lead researcher on the project, found that respondents in South America, Africa, and across South and Southeast Asia expressed more optimism than users in Europe, the United States, or East Asia.

“The trend is that maybe more lower and middle-income countries are more optimistic than higher-income countries that have more AI exposure,” said Huang. She added that this optimism might reflect a sample skew toward early adopters in developing markets — individuals inclined to view new technologies as opportunities rather than threats.

“They just divide so cleanly . . . the more western developed countries are significantly more concerned about AI and the economy, [and] much more negative, and then, the reverse is true with the lower and middle-income countries,” she said.

According to Anthropic’s researchers, AI’s limited visibility in daily workflows across lower-income economies may explain the difference. “If AI hasn’t visibly entered your daily work yet, AI displacement likely feels abstract, especially when more immediate economic pressures already exist,” the team wrote in a companion blog post.

Next Steps: Measuring AI’s Real-World Impact:

Anthropic plans to extend its Claude Interviewer research framework into longitudinal studies that track how AI affects users’ lives over time. “The goal is to better measure both the improvements and the harms — and to use those insights to make systemic refinements,” said Ganguli.

The company’s approach — embedding feedback collection directly into an AI platform — represents an emerging model for data-driven, iterative AI development. By combining self-reported user experience data with large-scale text analytics, Anthropic aims to better understand how its models interact with human needs and constraints.

Industry and Research Community Respond:

The study has drawn attention across the AI community for its unprecedented reach and innovative methodology. Nickey Skarstad, director of product at language-learning company Duolingo, praised the work’s ambition. On LinkedIn, she wrote: “For anyone building products right now, this is the future of understanding your users. The what AND the why at a scale we’ve never had access to before.”

Still, several researchers remain cautious about overinterpreting the results. Divy Thakkar, a researcher at Anthropic rival Google DeepMind, expressed reservations on X, saying he was “sceptical” about calling the study a new form of science due to potential selection bias and limitations in survey design. “A human qualitative researcher would take time to build trust with their participants, hold the space for reflection, introspection, contradictions — that’s the whole point of it,” he wrote.

Methodological caveats extend to demographics. Almost half of the survey’s respondents were based in North America or Western Europe, while regions such as Central Asia had only several hundred participants.

Ilan Strauss, an economist and director of the AI Disclosures Project, described the initiative as “an excellent piece of work,” but urged careful interpretation. He noted that the absence of reported confidence intervals — standard practice in survey-based research — makes it difficult to measure uncertainty. Self-reported productivity gains, he added, are inherently prone to bias.

A Global Mirror for Human-AI Relations:

Despite these caveats, the Claude Interviewer study illustrates a broader shift in the relationship between humans and AI systems. As AI technologies proliferate across regions and industries, they are becoming both instruments of empowerment and sources of anxiety — mirroring social, economic, and cultural dynamics in striking ways.

While western economies debate AI-driven labor disruption and ethical alignment, many in emerging markets frame AI as a means of upward mobility and creative expansion. This duality — between apprehension and aspiration — may shape not only AI adoption patterns but also future research and regulatory directions across global contexts.

References:

https://www.ft.com/content/e074d3a9-7fd8-447d-ac0a-e0de756ac5c5?syn-25a6b1a6=1 (PAYWALL)

https://www.joist.ai/post/ai-hallucinations-what-they-are-and-why-it-matters

Sources: AI is Getting Smarter, but Hallucinations Are Getting Worse

Nvidia CEO Huang: AI is the largest infrastructure buildout in human history; AI Data Center CAPEX will generate new revenue streams for operators

Alphabet’s 2026 capex forecast soars; Gemini 3 AI model is a huge success

Analysis & Economic Implications of AI adoption in China

China’s open source AI models to capture a larger share of 2026 global AI market

AWS to deploy AI inference chips from Cerebras in its data centers; Anapurna Labs/Amazon in-house AI silicon products

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Gartner: AI spending >$2 trillion in 2026 driven by hyperscalers data center investments

AWS to deploy AI inference chips from Cerebras in its data centers; Anapurna Labs/Amazon in-house AI silicon products

Amazon Web Services (AWS) announced it plans to integrate AI processors from Cerebras Systems [1.] into its data centers, signaling growing confidence in the AI-focused semiconductor startup. Under a new multiyear partnership announced Friday, AWS will deploy Cerebras’s Wafer-Scale Engine (WSE) to accelerate inference workloads—the stage of AI operations where models generate responses to user queries. Financial details of the agreement were not disclosed.

Note 1. Founded in 2015 and headquartered in Sunnyvale, CA, Cerebras claims to have the world’s fastest AI inference and training platform.

The collaboration reflects a significant realignment in compute infrastructure strategies across the AI ecosystem. While initial industry focus centered on model training, the rapid expansion of deployed AI services is driving demand for optimized inference performance. Traditional GPUs, though unmatched for training, can be suboptimal for inference scenarios that require ultra-low latency and high throughput. Cloud and AI platform providers are therefore diversifying their silicon portfolios to better match workload profiles and to scale capacity efficiently.

AWS, the world’s largest cloud infrastructure provider, has traditionally relied on its in-house semiconductor division, Annapurna Labs, for custom chip design. Annapurna’s Trainium processors compete with GPUs from major suppliers such as Nvidia and AMD, offering cost and performance advantages for AI training workloads. The new partnership introduces Cerebras technology into AWS infrastructure, where it will work alongside Trainium to enhance large-scale inference capabilities.

Cerebras, best known for its wafer-scale architecture, markets its WSE processors as a high-speed inference platform capable of executing the decode phase of generative AI processing—where text, images, or other outputs are generated—at up to 25 times the speed of conventional GPU solutions. The company, valued at approximately $23 billion following a $1 billion funding round in February, has attracted backing from Fidelity, Benchmark, Tiger Global, Atreides, and Coatue.

The Cerebras deal underscores a major shift in the market for computing power. Image Credit: rebecca lewington/cerebras syste/Reuters

The AWS collaboration follows Cerebras’s major compute partnership with OpenAI, which reportedly involves deploying up to 750 MW of computing capacity powered by its chips. AWS and Cerebras will position their joint offering as a premium cloud inference solution, targeting enterprise AI developers requiring high-performance and scalable compute.

“The scale of AI demand is shifting from model creation to global deployment,” said Andrew Feldman, CEO of Cerebras. “Working with AWS aligns our technology with the industry’s largest cloud, giving us reach to a broad enterprise and developer base. If you want slow inference, there will be cheaper ways to go,” Feldman said. “But if you want fast tokens, if speed matters to you, if you’re doing coding or agentic work, not only are we the absolute fastest, but we intend to set the bar. We’re in this to win it.”

AWS and Cerebras will support both aggregated and disaggregated configurations. Disaggregated is ideal when you have large, stable workloads. Most customers run a mix of workloads with different prefill/decode ratios, where the traditional aggregated approach is still ideal. The start-up expects most customers will want access to both and the ability to route workloads to whichever configuration serves them best.

The move intensifies competition in the inference silicon segment, where Nvidia faces growing pressure from purpose-built processor architectures such as Cerebras’s WSE and other emerging alternatives. Nvidia, which recently announced a $20 billion licensing deal with Groq and plans to unveil a new inference-optimized platform, remains the dominant supplier but now contends with an accelerating wave of specialization across the AI compute stack.

AWS vice president and Annapurna Labs co-founder Nafea Bshara emphasized the company’s goal of offering flexible performance tiers. “Our job is to push the speed and lower the price,” he said, noting that AWS will continue to offer cost-optimized Trainium-only options alongside high-performance Cerebras-Trainium configurations.

………………………………………………………………………………………………………………………………………………………………………………………………….

Amazon’s Internally Designed AI Silicon:

Amazon has built a fairly broad internal AI-oriented silicon portfolio through Annapurna Labs, primarily for AWS:

-

Inferentia (Inferentia, Inferentia2) – Custom machine learning accelerators designed for high-throughput, low-cost inference at cloud scale. These power many AWS inference instances and are positioned as an alternative to Nvidia GPUs for production model serving.

-

Trainium (Trainium, Trainium2, Trainium3) – AI training accelerators optimized for large-scale model training (including frontier and foundation models), with Trainium2 and Trainium3 as newer generations offering materially higher performance and better $/compute than the first generation. These are central to projects such as the Rainier supercomputer for Anthropic.

-

Graviton (Graviton, Graviton2/3/4) – Arm-based general-purpose CPUs used heavily across EC2, increasingly in AI-adjacent roles (pre/post-processing, orchestration, model-serving microservices) and as part of cost-optimized AI stacks, even though they are not dedicated accelerators.

-

Nitro system – While not an AI accelerator per se, the Nitro family (offload cards and system) is an internally developed data-plane and virtualization offload architecture that underpins EC2 and works in tandem with Graviton, Inferentia, and Trainium to free CPU cycles and improve I/O for AI/ML workloads.

All of these are designed and iterated internally by Annapurna Labs for exclusive use in AWS data centers, then exposed to customers via AWS services rather than as standalone merchant silicon.

Amazon’s Annapurna Labs is an internal chip design group that has become a core strategic asset for AWS, especially for custom data center and AI silicon.

Origins and acquisition:

-

Annapurna Labs is an Israeli chip design startup founded in 2011 by semiconductor veterans of Intel and Broadcom, including Avigdor Willenz and Nafea Bshara.

- “When we talked with market sources and consulted with experts in the fields of data and servers, at that time only Amazon had a holistic vision and the ability to execute on a large scale,” recalls Bshara about the start of the romance with Amazon. “We were prepared to build the technology and at the same time were open to working with startups. From there we began a journey together with many meetings and shared thinking, among others with James Hamilton (Microsoft’s former data-base product architect and to AWS SVP), and from there within six months we found ourselves inside Amazon.”

-

Amazon began working with the company around 2013 and acquired it in 2015 for an estimated $350–$400 million.

-

Before the deal, Annapurna was in stealth, focusing on low‑power networking and server chips to improve data center efficiency.

Role inside Amazon and AWS:

-

Post‑acquisition, Annapurna was folded into AWS as a specialist microelectronics and custom silicon group, designing chips to reduce cost and power per unit of compute.

-

The group underpins several key AWS technologies: the Nitro system for offloading virtualization and I/O, Arm‑based Graviton CPUs for general compute, and Trainium and Inferentia accelerators for AI training and inference.

-

These chips let AWS optimize performance per watt and per dollar versus x86 servers and third‑party accelerators, improving margins and competitive pricing.

Key products and architectures:

-

Nitro: A combination of custom hardware and software that offloads storage, networking, and security functions from the host CPU, increasing tenant isolation and freeing CPU cycles for workloads.

-

Graviton: A family of Arm‑based server CPUs; by 2018 Graviton was widely adopted on AWS and is now used by most AWS customers for general cloud infrastructure workloads due to better price‑performance and energy efficiency.

-

Inferentia and Trainium: Custom accelerators designed by Annapurna for machine learning inference (Inferentia) and training (Trainium), intended to reduce AWS’s dependence on high‑priced Nvidia GPUs for AI workloads.

Strategic importance and AI focus:

-

Annapurna’s work is central to Amazon’s strategy of vertical integration in the cloud: owning the silicon stack as much as the software and services.

-

The group designs chips that power Amazon’s AI infrastructure, including systems used both by internal teams and external customers such as Anthropic, for which AWS is the primary cloud and silicon provider.

-

Amazon and Anthropic are collaborating on “Project Rainier,” a massive supercomputer built around hundreds of thousands of Annapurna‑designed Trainium2 chips, targeting more than five times the compute used to train current frontier models.

Organization, footprint, and industry impact:

-

Annapurna Labs maintains a significant presence in Israel, employing hundreds of engineers focused on advanced AI and networking processors for AWS.

-

It also operates major engineering hubs such as an Austin, Texas lab where advanced semiconductors and AI systems are designed and tested.

-

Analysts often describe the acquisition as one of Amazon’s most successful, arguing that Annapurna’s custom silicon is a “secret sauce” that helps AWS compete with Microsoft, Google, and others on performance, cost, and energy efficiency.

…………………………………………………………………………………………………………………………………………………………..

References:

https://www.cerebras.ai/company

https://www.cerebras.ai/blog/cerebras-is-coming-to-aws

https://www.wsj.com/tech/amazon-announces-inference-chips-deal-with-cerebras-109ecd31

https://en.globes.co.il/en/article-nafea-bshara-the-israeli-behind-amazons-graviton-chip-1001420744

Intel and AI chip startup SambaNova partner; SN50 AI inferencing chip max speed said to be 5X faster than competitive AI chips

Custom AI Chips: Powering the next wave of Intelligent Computing

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Will “AI at the Edge” transform telecom or be yet another telco monetization failure?

Huawei to Double Output of Ascend AI chips in 2026; OpenAI orders HBM chips from SK Hynix & Samsung for Stargate UAE project

OpenAI and Broadcom in $10B deal to make custom AI chips

U.S. export controls on Nvidia H20 AI chips enables Huawei’s 910C GPU to be favored by AI tech giants in China

Superclusters of Nvidia GPU/AI chips combined with end-to-end network platforms to create next generation data centers

2026 Consumer Electronics Show Preview: smartphones, AI in devices/appliances and advanced semiconductor chips

Networking chips and modules for AI data centers: Infiniband, Ultra Ethernet, Optical Connections

Google announces Gemini: it’s most powerful AI model, powered by TPU chips

Will “AI at the Edge” transform telecom or be yet another telco monetization failure?

New Telco Opportunity – AI at the Edge:

At MWC 2026 last week, there were a flurry of claims that “AI at the Edge” would transform the telecom industry. One of many examples is an article titled, “The AI edge boom is giving telecom a new strategic role.” In that piece, Jeff Aaron, vice president of product and solutions marketing at Hewlett Packard Enterprise (HPE) spoke with theCUBE’s John Furrier at MWC Barcelona, during an exclusive broadcast on theCUBE, SiliconANGLE Media’s livestreaming studio. They discussed telecom edge AI and why networking is becoming a strategic foundation for data-centric services. Aaron said:

“A big reason for [reignited interest in routing] is AI workloads. They’re moving everywhere now. They have to move to the edge. For them to move to the edge, you’ve got to get them outside of the factory and to all the locations. We’re right in the core of that, and it’s super exciting.”

As AI expands to the edge, data will need to move not only to local compute, but also between many distributed edge sites, making routing paramount. There are four ways AI infrastructure is scaling — inside data centers and across distributed edge locations, according to Aaron.

“There’s scale-out, scale-across, scale-up, and on-ramp. Two are within the data center — scale-out and scale-up — but scale-across and edge on-ramp basically mean you got to figure out how to connect to those areas, and those are just networking,” he added.

Scale-across refers to connecting distributed data centers and edge locations, while edge on-ramp brings remote sites such as factories or branch locations into the network to access AI services. Supporting those distributed environments creates an opportunity for HPE to bring networking and compute together into a more integrated infrastructure stack. At MWC 2026 Barcelona, those trends are clearly coming into focus, according to Aaron.

“Data is moving everywhere right now, and the network is back. The network isn’t just plumbing. The network is how you build a value-added service using an AI workload as a telco infrastructure,” he added.

Telecom carriers are now urgently trying to move from being “dumb data pipes” to becoming “AI performance platforms” by leveraging their geographically distributed infrastructure to host AI closer to the end user. They urgently want to pivot from selling just bandwidth and connectivity to selling outcomes and intelligence with a heavy focus on industrial and enterprise-specific edge deployments. They are considering the following services and business models:

- Infrastructure as a Service (IaaS) & GPUaaS: Offering raw computing power, specifically GPUs, from edge data centers to enterprises that need low-latency processing without building their own facilities.

- Sovereign AI Clouds: Providing AI services that guarantee data remains within national borders, appealing to government and highly regulated sectors like finance and healthcare.

- API Monetization: Exposing real-time network data (e.g., location intelligence, predictive network quality, fraud risk scoring) via APIs that enterprises pay to integrate into their own applications.

- Outcome-Based Pricing: Charging for specific business results, such as a “guaranteed video call quality” or “fraud loss reduction share,” rather than just data usage.

- AI-as-a-Service (AIaaS): Bundling pre-trained models or specialized AI agents (e.g., for customer service or industrial monitoring) with connectivity

Major Carrier AI Edge Deployment Plans:

- AT&T:

- Launched Connected AI for Manufacturing in March 2026, which unifies 5G, IoT, and generative AI to provide real-time fault detection (claiming a 70% reduction in waste).

- Deploying “Edge Zones” in major U.S. cities (Detroit, LA, Dallas) to allow developers to run low-latency, cloud-based software locally.

- Partnering with AWS to link fiber and 5G directly into AWS environments for distributed AI workloads.

- Verizon:

- Unveiled Verizon AI Connect, a suite of products designed to manage resource-intensive AI workloads for hyperscalers like Google Cloud and Meta.

- Trialing V2X (Vehicle-to-Everything) platforms to provide carmakers with standardized APIs for low-latency edge processing in autonomous driving.

- Collaborating with NVIDIA to integrate GPUs into private 5G networks for on-premise AI inferencing in robotics and AR.

- SK Telecom (SKT):

- Announced an “AI Native” strategy at MWC 2026, including a roadmap for AI-RAN (Radio Access Network) that uses GPUs to optimize network performance and host user AI apps simultaneously.

- Building a Manufacturing AI Cloud powered by over 2,000 NVIDIA RTX GPUs to support digital twin simulations and robotics.

- Expanding AI Data Centers (AIDC) across South Korea and Southeast Asia (Vietnam, Malaysia) using energy-optimized LNG-powered facilities.

- Orange & Deutsche Telekom:

- Deploying AI-powered planning tools to cut fiber rollout costs and optimize site power consumption by up to 33% using AI “Deep Sleep” modes.

- Focusing on Sovereign AI strategies to ensure data governance for European enterprise customers.

- Vodafone:

- Utilizing AI/ML applications for daily power reduction at 5G sites and testing autonomous network healing via AI agents

- BT:

- Offers 5G-connected VR for manufacturing design teams (e.g., Hyperbat) to collaborate on 3D models in real-time.

| Product Category | Primary Target | Key Value Proposition |

|---|---|---|

| AI-RAN | Industry 4.0 | Seamless, ultra-low latency for robotics and sensing. |

| Connected AI Platforms | Manufacturing | Real-time predictive maintenance and waste reduction. |

| AI-as-a-Service (AIaaS) | Developers/SMBs | Access to GPU power and pre-trained models via telco edge nodes. |

| Network Slicing APIs | App Developers | Programmatic control over bandwidth for AR/VR and gaming. |

…………………………………………………………………………………………………………………………………………………………………………………………..

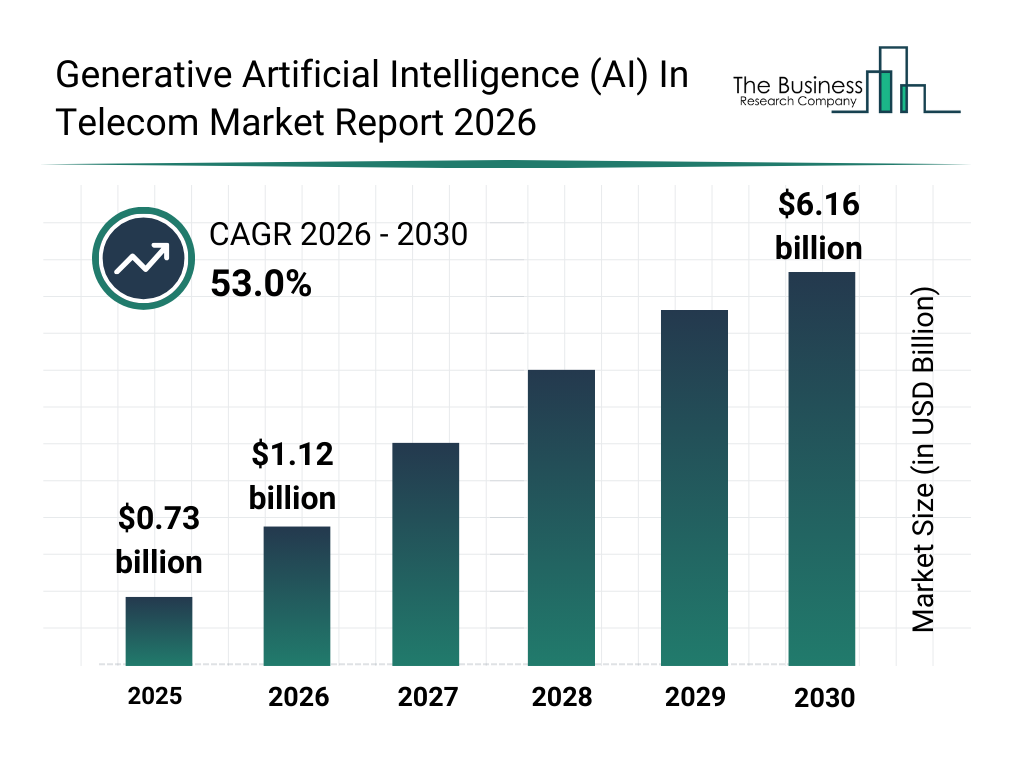

A Dissenting View of “AI at the Edge”:

The global market for AI within the global telecommunications sector is valued at $6.69 billion in 2026, growing at a compound annual rate (CAGR) of 41.9% from 2025. The broader edge AI market—including hardware, software, and services—is forecast to reach $29.98 billion in 2026, according to The Business Research Company. We think those estimates are way too high.

The market research firm states:

………………………………………………………………………………………………………

Author’s Opinion:

Unless telcos change their corporate culture along with slowing the footprint growth of cloud service providers/hyperscalers, we think that AI at the Edge will be yet another telco monetization failure. Just like their failure to monetize: 4G LTE apps, the telco cloud, 5G, multi-access edge computing (MEC), OpenRAN, LPWANs and other telecom technologies that never lived up to their promise and potential.

That’s largely because telcos are very weak: developing IT platforms, compute services, killer applications, and rapid execution of new services (e.g. 5G services require a 5G SA core network which telcos were very slow to deploy). Telecom execs themselves cite cultural and speed‑of‑change issues: the industry is not organized like a software company, so it struggles to iterate products at AI/cloud pace. Also, telcos historically struggle with software. Managing distributed GPU clusters is vastly different from managing cell towers.

After spending billions on 5G with very little or no ROI, investors are skeptical of the increased capex required for AI-grade edge servers which must be maintained by telcos. Those servers will be expensive (especially if they contain clusters of Nvidia GPUs) and consume a lot of power, which is a critical issue at the edge of the carrier’s network.

Many network operators frame AI/edge as “network optimization” or “utilizing underused sites,” not as building monetizable AI platforms with APIs, SDKs, and ecosystems. This mirrors 5G, where huge RAN/core builds were not matched by a clear product and platform strategy, leaving value to OTTs and hyperscalers which are extending their control planes and protocol stacks to the network edge (local zones, operator co‑lo, on‑premises stacks).

Telcos risk becoming “dumb pipes” for AI traffic if they can’t provide a superior developer ecosystem. If they only sell space/power/connectivity, the cloud service providers will continue to own the developer and AI value chain. Analysts warn that edge is a “right to participate, not a right to win.” As such, value accrues to whoever owns the AI platform, tools, marketplace, and pricing power, not the entity that provides connectivity, PoP or cell towers.

Data fragmentation and weak “intelligence” layer:

-

AI monetization depends on high‑quality, cross‑domain data, but telco data is fragmented across OSS, BSS, probes, and partner systems; without unification, it is hard to expose compelling network/edge intelligence services.

-

Analysts emphasize that failure here reduces telcos to generic GPU landlords, while higher‑margin offers (real‑time quality, fraud, identity, mobility/context APIs) remain unrealized.

Narrow internal focus on cost savings:

-

Many operators’ early AI focus is inward (Opex reduction in assurance, planning, customer care) rather than building external, revenue‑generating products, echoing how early 5G was justified mainly on cost/efficiency.

-

Commentators warn that if AI/edge remains a “network efficiency” play, the commercial upside will go to cloud/AI natives that turn similar capabilities into products sold to enterprises.

What analysts say telcos must do differently:

-

Build “Sovereign AI factories” and edge AI clouds: GPU‑enabled sites with cloud‑like developer experience (APIs, self‑service portals, metering, SLAs) and clear sovereign/regional guarantees.

-

Combine differentiated connectivity with AI services (latency‑backed SLAs, AI‑on‑RAN, domain‑specific models for verticals) and use modern, flexible commercial models instead of just selling bandwidth or colocation.

Conclusions:

In summary, the main risk for telcos is to successfully transition from owning and maintaining network infrastructure to owning and operating AI platforms and products at software industry speed. AI at the edge is less of a new service or product and more an architectural upgrade. The two ways telcos can benefit are from:

- Internal cost reduction: If telcos use it to lower their own costs (fraud prevention, risk management, predictive maintenance, fault isolation, self-healing networks, etc.), it’s an automatic win but won’t increase the top line.

- Revenue from new AI -Edge services, e.g. Verizon uses edge-based video analytics in warehouses to improve inventory turnover by up to 40%. If they expect to charge a massive premium for “AI-enabled 5G,” they face the same monetization wall that has doomed them for the past 20 years!

References:

https://siliconangle.com/2026/03/04/telecom-edge-ai-makes-networking-strategic-mwc26/

https://www.nvidia.com/en-us/lp/ai/the-blueprint-for-ai-success-ebook/

AT&T and AWS to deliver last mile connectivity for AI workloads; AT&T Geo Modeler™ AI simulation tool

Analysis: Edge AI and Qualcomm’s AI Program for Innovators 2026 – APAC for startups to lead in AI innovation

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Private 5G networks move to include automation, autonomous systems, edge computing & AI operations

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

Nvidia AI-RAN survey results; AI inferencing as a reinvention of edge computing?

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

CES 2025: Intel announces edge compute processors with AI inferencing capabilities

AT&T and AWS to deliver last mile connectivity for AI workloads; AT&T Geo Modeler™ AI simulation tool

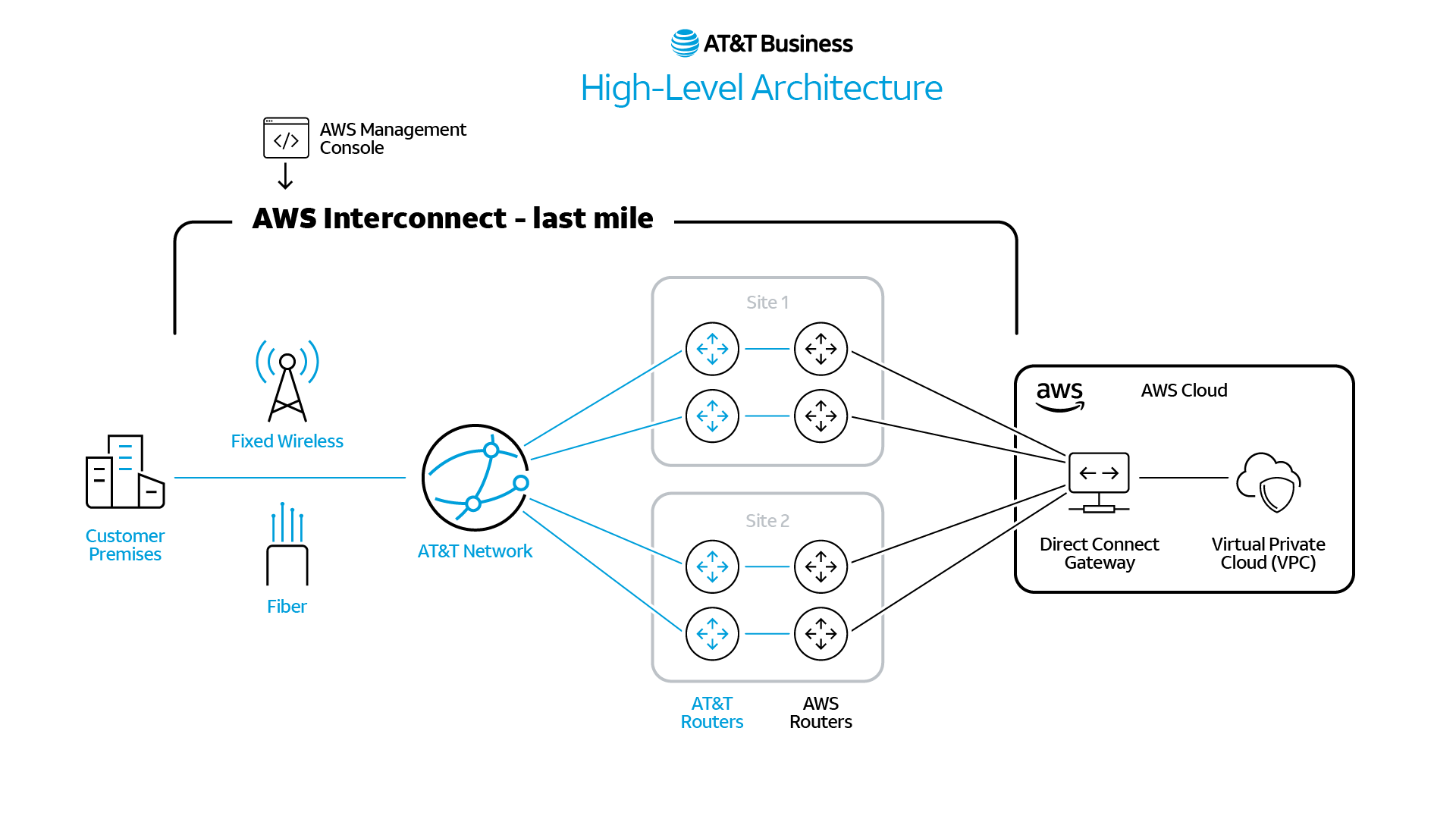

AT&T is strategically re-architecting its infrastructure for the AI era through high-capacity network modernization and deep integration with hyperscale cloud providers.

In addition to its almost six year old deal to run its 5G SA core network in Microsoft Azure’s cloud, AT&T announced at MWC 2026 that it’s now woring with Amazon Web Services (AWS) to extend 5G and fiber connectivity from business customers and locations directly into AWS environments, creating secure, resilient and reliable premises‑to‑cloud architectures for AI workloads. The collaboration is designed to reduce network complexity and latency while supporting real‑time analytics, machine learning, and agentic AI use cases.

This collaboration continues a long-standing relationship between AT&T and AWS and follows recent news outlining broader efforts to modernize the nation’s connectivity infrastructure by providing high-capacity fiber to AWS data centers, migrate AT&T workloads to AWS cloud capabilities and explore emerging satellite technologies.

AWS Interconnect – last mile embeds AT&T‑delivered connectivity directly into AWS workflows, designed to enable customers to provision and manage last‑mile connectivity within the AWS environment and lays the foundation for the use of AI agents to monitor and manage the AI experience from the user to the cloud. This streamlined, self‑managed approach helps enterprises reduce network complexity while maintaining control of their extended enterprise network, allowing businesses to move faster as they scale AI.

High level illustration of the planned AWS Interconnect – last mile architecture, showing how resilient interconnections and AT&T Fiber and fixed wireless access are intended to simplify private connectivity from customer locations into AWS environments.

Diagram Source: AT&T

………………………………………………………………………………………………………

“AI does not just need more compute; it needs flatter networks and faster connections,” said Shawn Hakl, SVP & Head of Product, AT&T Business. “By bringing high‑capacity connectivity closer to cloud platforms, integrating the management of the networks directly into the cloud provisioning process and engineering for resiliency at the metro level, AT&T is helping enterprises streamline their networks, improve performance, security, and scale AI with confidence.”

AT&T says they are building an AI‑ready network (?) designed to scale performance by continuing ongoing network investment, including the growth of capacities up to 1.6Tbps across key metro and long‑haul routes.

AT&T also announced it would work with Nvidia, Microsoft and MicroAI through its Connected AI platform for “smart manufacturing.”

………………………………………………………………………………………………………………..

Finally, AT&T described AT&T Geo Modeler™ which is able to better predict connectivity for emerging technologies like autonomous vehicles, drones, and robotics.

The Geo Modeler is an AI-powered simulation tool that helps predict, in near real time, how a wireless network will perform in the real world. Inspired by the video games Kounev played with his family growing up, the virtual model and simulation is “essentially like a giant video game of the United States” that, infused with AI tools, gives engineers a clearer picture of where potential weak spots may appear. Then issues can be addressed earlier and fixes can roll out faster. In essence, it creates virtual models, similar to the way video games are designed and developed.

“The Geo Modeler helps us see how the real world will shape coverage before we build, so we can deliver connectivity that’s ready for what’s next,” said AT&T scientist Velin Kounev.

Matt Harden, VP of Connected Solutions at AT&T, agrees. “The Geo Modeler is a foundational capability for the connected mobility era,” he said. “By marrying advanced geospatial simulation with AI-driven network orchestration, we can deliver predictable, high-performance connectivity that adapts with the environment. Whether it’s a hurricane, a packed stadium, or a city corridor full of autonomous vehicles, we will be prepared.”

References:

https://about.att.com/story/2026/aws-collaboration-scalable-business-ai.html

https://about.att.com/blogs/2026/150-years-of-connection.html

https://about.att.com/blogs/2025/geo-modeler.html

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

AT&T deploys nationwide 5G SA while Verizon lags and T-Mobile leads

AT&T to buy spectrum licenses from EchoStar for $23 billion

AT&T’s convergence strategy is working as per its 3Q 2025 earnings report

Progress report: Moving AT&T’s 5G core network to Microsoft Azure Hybrid Cloud platform

AT&T 5G SA Core Network to run on Microsoft Azure cloud platform

Huawei unveils AI Centric Network roadmap, U6 GHz products, 5G Advanced strategy and SuperPoD cluster computing platforms

Missing from all the MWC 2026 6G AI alliance announcements, Huawei released a series of all-scenario U6 GHz products to help carriers unlock the full potential of 5G Advanced (5G-A) and set the stage for a seamless transition to 6G. Huawei also showcased its SuperPoD cluster for the first time outside China, which they have created to offer “a new option for the intelligent world.”

- The all-scenario U6 GHz products and solutions Huawei released today use innovative technologies to create a high-capacity, low-latency, optimal-experience backbone designed for mobile AI applications.

- There are already 70 million 5G-A users globally, and 5G-A is increasingly being adopted by carriers at scale. In China, Huawei has helped carriers deliver contiguous 5G-A coverage across 270 cities and launch 5G-A packages that monetize experience in over 30 provinces.

The company also launched enhanced AI-Centric Network solutions [1.] that will help carriers prepare for the agentic era by enabling intelligent services, networks, and network elements (NEs). The company’s plans to build more AI-centric networks and computing backbones that will help carriers and industry customers seize opportunities from the AI era.

Note 1. Huawei’s AI-Centric Network roadmap is designed to integrate intelligence directly into 5G-Advanced (5G-A) infrastructure and accelerate the transition toward Level-4 Autonomous Networks. The company plans to work with global carriers (where its not blacklisted) on the large-scale 5G-A deployment, use high uplink to address surging consumer and industry demand for mobile AI applications, and use the U6 GHz band to unlock the full value of spectrum and pave the way for smooth evolution to 6G.

Photo Credit: Huawei

………………………………………………………………………………………………………………

Three-Layer Intelligence in AI-Centric Networks: Accelerating the Agentic Era:

As mobile network operators transition toward AI-native 5G-Advanced and early 6G architectures, Huawei is positioning its AI-Centric Network portfolio as the blueprint for next-generation intelligent networks. By embedding intelligence across service, network, and network element (NE) layers, Huawei aims to establish the foundation for fully agentic, autonomously managed infrastructures.

- Service Layer: Focuses on multi-agent collaboration platforms to transform core carrier services—such as voice and home broadband—into intelligent service platforms.

- Network Layer: Aims to evolve from single-scenario automation to end-to-end single-domain network autonomy. Huawei officially launched AUTINOps, an AI-native intelligent operations solution designed to replace traditional manual O&M with predictive, preventive “digital employees”.

- Network Element (NE) Layer: Utilizes AI to optimize algorithms for RANs (Radio Access Networks) and core networks, improving spectral efficiency and service awareness.

At the Service layer, Huawei is enabling carriers to operationalize multi-agent collaboration frameworks that embed domain-specific intelligence into key service categories: voice, broadband, and digital experience monetization. These AI agents dynamically manage customer experience and lifecycle value, supporting the transformation of core connectivity services into intelligent, context-aware digital offerings.

At the Network layer, the company’s Autonomous Driving Network Level 4 (ADN L4) initiative focuses on single-scenario automation, delivering measurable improvements in O&M efficiency, service quality, and monetization agility. By the close of 2025, ADN single-scenario deployments were active across more than 130 commercial telecom networks. The next phase targets end-to-end, single-domain autonomy across transport, access, and core networks—an essential step toward zero-touch O&M and intent-driven orchestration in 5G-A and 6G environments.

At the Network Element layer, Huawei is jointly advancing AI-driven innovation across RAN, WAN, and core domains. This includes algorithmic optimization for intelligent RAN scheduling, service-aware traffic identification in WANs, and unified intent modeling across B2C and B2H use cases. Such capabilities enhance spectral and energy efficiency, enable predictive resilience, and provide fine-grained service awareness—all foundational for AI-native air interface and network control in 6G.

Computing Backbone with SuperPoD Clusters:

Supporting this vision, Huawei is introducing its next-generation SuperPoD and cluster computing platforms, designed as high-performance compute backbones for distributed AI model training and inference within telecom and enterprise domains. Featuring the proprietary UnifiedBus interconnect and system-level architecture innovations, the Atlas 950, TaiShan 950, and Atlas 850E SuperPoDs, along with the TaiShan 200–500 servers, deliver ultra-low latency and high throughput optimized for trillion-parameter AI models and real-time agentic operations.

Aligned with its open innovation strategy, Huawei continues to expand an open, collaborative computing ecosystem, supporting open-source frameworks and open-access platforms to accelerate the deployment of intelligent, AI-driven digital infrastructure worldwide.

Intelligent Transformation Across Industry Domains:

At MWC Barcelona 2026, Huawei is highlighting 115 end-to-end industrial intelligence showcases across verticals, underscoring its role in helping enterprises adopt AI-centric operational models. Through the SHAPE 2.0 Partner Framework, 22 co-developed AI and digital infrastructure solutions will demonstrate how vertical industries—from manufacturing and energy to transportation and healthcare—can harness 5G-A and AI integration to deliver measurable business outcomes.

Toward 5G-A Commercialization and 6G Evolution:

With large-scale 5G-Advanced rollouts accelerating, Huawei is collaborating with global carriers and ecosystem partners to realize level-4 autonomous networks and establish the architectural bridge to 6G. Central to this evolution is the convergence of AI, connectivity, and computing—enabling networks that can self-learn, self-optimize, and autonomously orchestrate service intent. These AI-Centric Network initiatives and SuperPoD-based computing backbones form the foundation for value-driven, intelligent networks built for the agentic era.

5G-Advanced and Infrastructure Innovations:

Huawei’s 5G-A strategy, branded as GigaUplink, focuses on delivering the high-uplink capacity and low latency required for mobile AI applications:

- U6 GHz Spectrum: Launched a comprehensive portfolio of all-scenario U6 GHz products to unlock 5G-A’s full potential and provide a smooth evolution path to 6G.

- Agentic Core: Introduced the Agentic Core solution, which integrates intelligence natively into the core network to support ubiquitous AI agent access across devices.

- All-Optical Target Network: Proposed an AI-centric optical roadmap featuring dual strategies: “AI for networks” (optimizing operations) and “networks for AI” (supporting AI workloads with ultra-low latency benchmarks of 1-5ms).

………………………………………………………………………………………………………………………………………………………..

References:

https://www.huawei.com/en/news/2026/3/mwc-ai-centric-network

https://carrier.huawei.com/en/minisite/events/mwc2026/

Huawei FY2025: 2.2% YoY revenue increase; strategic pivot to AI & Automotive

NVIDIA and global telecom leaders to build 6G on open and secure AI-native platforms + Linux Foundation launches OCUDU

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Huawei, Qualcomm, Samsung, and Ericsson Leading Patent Race in $15 Billion 5G Licensing Market

Huawei Cloud Review and Global Sales Partner Policies for 2026

Huawei’s Electric Vehicle Charging Technology & Top 10 Charging Trends

Huawei to Double Output of Ascend AI chips in 2026; OpenAI orders HBM chips from SK Hynix & Samsung for Stargate UAE project

Huawei launches CloudMatrix 384 AI System to rival Nvidia’s most advanced AI system

U.S. export controls on Nvidia H20 AI chips enables Huawei’s 910C GPU to be favored by AI tech giants in China

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

Overview:

AT&T and Ericsson have completed a milestone Cloud RAN test by successfully demonstrating Ericsson’s AI-native Link Adaptation [1.] on a Cloud RAN stack powered by Intel Xeon 6 SoC. The test showed how artificial intelligence (AI) can improve spectral efficiency and network responsiveness in real-world conditions. Conducted over AT&T’s licensed frequency bands, the experiment was the first to use portable Ericsson RAN software running on Intel’s new Xeon 6 system-on-chip (SoC) platform—an architecture designed for high-performance, cloud-native processing of RAN workloads. Engineered specifically for network and edge deployments, Intel Xeon 6 SoC delivers breakthrough AI RAN performance with built-in acceleration. Integrated Intel Advanced Vector Extensions (AVX) and Intel Advanced Matrix Extension (AMX) technologies eliminate the need for discrete accelerators while maximizing capacity, efficiency, and TCO optimization.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Note 1. AI-native Link Adaptation dynamically adjusts to changes in signal quality and interference, boosting RAN performance on purpose-built and cloud-based infrastructure alike.

Other Notes:

-

vRAN: A radio access network (RAN) in which the baseband processing functions run as software on general-purpose processors (mostly from Intel) instead of on dedicated hardware at the cell site. In vRAN, the functional split defines how baseband processing is divided between centralized processors and the radio unit at the site, and that split drives fronthaul bandwidth, latency, and cost.

- Cloud RAN: An evolution of vRAN where those same RAN functions are re-architected as cloud‑native microservices/containers with CI/CD (Continuous Integration and either Continuous Delivery or Continuous Deployment), automation, and orchestrators, optimized for elastic scaling across distributed cloud infrastructure.

- Ericsson Cloud RAN is a cloud native software solution that handles compute functionality in the RAN. It virtualizes RAN functions on Commercial Off The Shelf (COTS) hardware, decoupling software from hardware to enable more flexible, scalable, and efficient network deployments.

- According to Dell’Oro Group, Cloud RAN (often encompassing vRAN) accounted for approximately 5% to 10% of the total global Radio Access Network (RAN) market revenues in 2025. In early 2026, Dell’Oro revised Cloud RAN projections downward. While virtualization remains a “key pillar” for the long term, short-term adoption is being slowed by performance, power, and cost-parity challenges when compared to purpose-built hardware.

- The total RAN market stabilized in late 2025 after losing approximately 20% of its value between 2022 and 2024. Market concentration reached a 10-year high in 2025, with the top five vendors (Huawei, Ericsson, Nokia, ZTE, and Samsung) capturing 96% of the revenue.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Image Credit: Ericsson

In this proof-of-concept setup, Ericsson’s disaggregated and containerized RAN software operated within AT&T’s target Cloud RAN configuration, built on open, commercial off-the-shelf hardware. The test advanced from basic call functionality to validation of feature-rich network behavior in a cloud computing environment. Ericsson’s AI-native Link Adaptation is a learning algorithm that continuously assesses channel state and interference to determine the optimal modulation and coding scheme for each transmission interval. By generating real-time predictions of link quality, the AI model dynamically adjusts data rates to maximize throughput and spectral efficiency.

Early results were promising. Throughput gains reached up to 20% compared with conventional rule-based link adaptation approaches, alongside measurable improvements in spectral efficiency. Ericsson and Intel also used the trial to benchmark various AI inference models, demonstrating performance scalability and energy efficiency on general-purpose compute nodes rather than proprietary hardware accelerators. This suggests a more pragmatic path for deploying AI workloads across distributed RAN architectures.

AI-native Link Adaptation dynamically adjusts to changes in signal quality and interference, boosting RAN performance on purpose-built and cloud-based infrastructure alike.

Ericsson Cloud RAN is a cloud native software solution that handles compute functionality in the RAN. It virtualizes RAN functions on Commercial Off The Shelf (COTS) hardware, decoupling software from hardware to enable more flexible, scalable, and efficient network deployments.

Engineered specifically for network and edge deployments, Intel Xeon 6 SoC delivers breakthrough AI RAN performance with built-in acceleration. Integrated Intel Advanced Vector Extensions (AVX) and Intel Advanced Matrix Extension (AMX) technologies eliminate the need for discrete accelerators while maximizing capacity, efficiency, and TCO optimization.

Beyond the immediate performance improvements, the trial illustrates how open RAN architectures can accelerate innovation. By decoupling RAN software from vendor-specific hardware, AT&T can integrate AI capabilities and update network functions more quickly, avoiding the constraints of lock-in. The portability demonstrated here—running production-grade Ericsson RAN software on Intel Xeon 6 silicon—marks an industry first.

For AT&T, the achievement represents more than a lab milestone. It provides a technical template for scaling AI-native RAN functions into its cloud infrastructure, pointing to a future where machine learning operates natively within radio environments to fine-tune performance in real time. As operators continue balancing cost, flexibility, and efficiency, AI-optimized Cloud RAN deployments could become the next competitive frontier in 5G—and eventually, 6G—network evolution.

………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Quotes:

Rob Soni, Vice President, RAN Technology at AT&T, says: “AT&T is leading the charge toward an open, intelligent, and scalable network future by advancing Open RAN and Cloud RAN with AI-native capabilities at their core. This demo highlights how AI capabilities, powered by our next-generation Cloud RAN platform, can be deployed seamlessly to drive innovation and deliver superior customer experiences.”

Mårten Lerner, Head of Networks Strategy and Product Management, Business Area Networks at Ericsson, says: “Together with AT&T and Intel, Ericsson is demonstrating how our domain expertise combined with AI-native RAN software can drive transformative advancements in both Cloud RAN and purpose-built deployments. Our industry-leading AI-native Link Adaptation serves as the first proof point on this journey. With a hardware-agnostic RAN software stack, Ericsson is committed to offering maximum flexibility and enabling all our customers to benefit from future innovations – regardless of their chosen underlying hardware. This milestone underscores Ericsson’s commitment to helping operators advance their networks by deploying AI functionality across the RAN stack.”

Cristina Rodriguez, VP and GM, Network and Edge at Intel, says: “This successful collaboration with AT&T and Ericsson showcases the power of Intel Xeon 6 SoC to enable and accelerate AI workloads in Cloud RAN environments. Xeon 6 SoC is architected to handle the demanding compute requirements of AI-native network functions, delivering the performance and efficiency operators need to unlock the full potential of intelligent networks. By providing a flexible, standards-based platform, Intel Xeon 6 enables service providers like AT&T to deploy innovative AI capabilities while maintaining the openness and choice that drive industry innovation.”

………………………………………………………………………………………………………………………………………………………………………………………………………………………….

AI-Native Link Adaptation vs. Traditional Methods:

Traditional link adaptation in RAN relies on deterministic, rule-based algorithms that select the Modulation and Coding Scheme (MCS) from predefined lookup tables. These methods primarily use instantaneous Channel Quality Indicator (CQI) reports or estimated Signal-to-Interference-plus-Noise Ratio (SINR) thresholds, often adjusted via Outer Loop Link Adaptation (OLLA) based on ACK/NACK feedback from the UE. This reactive approach applies conservative margins to account for channel estimation errors, prediction lag, and varying interference, which can lead to suboptimal throughput—either underutilizing the link with low MCS or triggering excess HARQ retransmissions with overly aggressive selections.

AI-native Link Adaptation shifts to a predictive, model-driven paradigm using machine learning (typically lightweight neural networks or time-series models) trained on historical channel data. Rather than static thresholds, the AI processes sequences of CQI, beam metrics, mobility patterns, and interference traces to forecast the probable channel state for the next transmission time interval (TTI). This enables precise MCS selection that hugs the Shannon capacity limit more closely, minimizing BLER while maximizing spectral efficiency in dynamic scenarios like high-mobility NLOS or bursty interference.

Key differences include:

| Aspect | Traditional (Rule-Based) | AI-Native (ML-Based) |

|---|---|---|

| Decision Mechanism | Lookup tables, SINR thresholds, OLLA offsets | Real-time inference from ML models |

| Channel Handling | Reactive (past CQI/SINR) | Predictive (time-series forecasting) |

| Adaptation Speed | Step-wise, with feedback lag | Continuous, sub-TTI granularity |

| Performance Gains | Baseline (0% reference) | Up to 20% throughput, 10% spectral efficiency |

| Compute Needs | Low (fixed arithmetic) | Moderate (edge inference on COTS like Xeon 6) |

| Limitations | Struggles with non-stationary channels | Requires training data, retraining overhead |

Analysis: Rakuten Mobile and Intel partnership to embed AI directly into vRAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

vRAN market disappoints – just like OpenRAN and mobile 5G

Nokia and Eolo deploy 5G SA mmWave “Cloud RAN” network

Ericsson and Google Cloud expand partnership with Cloud RAN solution

Ericsson and O2 Telefónica demo Europe’s 1st Cloud RAN 5G mmWave FWA use case

Cloud RAN with Google Distributed Cloud Edge; Strategy: host network functions of other vendors on Google Cloud

vRAN market disappoints – just like OpenRAN and mobile 5G

Ericsson and Intel collaborate to accelerate AI-Native 6G; other AI-Native 6G advancements at MWC 2026

Ericsson and Intel at MWC 2026:

Building on milestones in Cloud RAN, 5G Core, and open network innovation, Ericsson and Intel are showcasing joint technology advancements at the Mobile World Congress (MWC) 2026 in Barcelona this week. Demonstrations can be experienced at the Ericsson Pavilion (Hall 2), Intel Booth (Hall 3, Stand 3E31), and across partner event spaces, highlighting the companies’ shared progress in enabling the next era of AI-driven networks.

The two companies are strengthening their long-standing technology partnership to accelerate ecosystem readiness for AI-native 6G networks and use cases. The expanded collaboration spans next-generation mobile connectivity, cloud infrastructure, and compute acceleration — with a focus on AI-driven RAN and packet core evolution, platform-level security, and scalable cloud-native architectures designed to shorten time-to-market for advanced network solutions.

“6G is not merely an iteration of mobile technology; it will serve as the foundational infrastructure distributing AI across devices, the edge, and the cloud,” said Börje Ekholm, President and CEO of Ericsson. “With our deep history in network innovation and global-scale operator deployments, Ericsson is uniquely positioned to drive practical 6G integration from research to commercialization.”

Lip-Bu Tan, CEO of Intel, added: “Intel’s vision is to lead the industry in unifying RAN, Core, and edge AI to enable seamless deployment of AI-native 6G environments. Together with Ericsson, we are proving that next-generation connectivity can be open, energy-efficient, secure, and intelligent. With future Ericsson Silicon built on Intel’s most advanced process technologies, coupled with Intel Xeon-powered AI-RAN ready Cloud RAN and collaborative multi-year research efforts, we are delivering the performance, efficiency, and supply assurance demanded by leading operators worldwide.”

As 6G transitions from research to commercialization, the industry must align around a mature, standards-based ecosystem. The Ericsson–Intel collaboration aims to accelerate development of high-performance, energy-efficient compute architectures optimized for both AI for Networks and Networks for AI.

AI-native 6G will fuse intelligent, programmable network functions with distributed compute and real-time sensing, bringing processing power closer to the network edge and enabling ultra-responsive, adaptive services. This convergence will enhance network efficiency, agility, and service intelligence across future deployments.

About Ericsson:

Ericsson‘s high-performing networks provide connectivity for billions of people every day. For 150 years, we’ve been pioneers in creating technology for communication. We offer mobile communication and connectivity solutions for service providers and enterprises. Together with our customers and partners, we make the digital world of tomorrow a reality.

About Intel:

Intel is an industry leader, creating world-changing technology that enables global progress and enriches lives. Inspired by Moore’s Law, we continuously work to advance the design and manufacturing of semiconductors to help address our customers’ greatest challenges. By embedding intelligence in the cloud, network, edge and every kind of computing device, we unleash the potential of data to transform business and society for the better.

…………………………………………………………………………………………………………………………………………………………

Related AI-Native 6G Announcements at MWC 2026:

In addition to the Ericsson-Intel collaboration, several vendors and operators announced AI-native 6G advancements or related demos at MWC Barcelona 2026. These initiatives emphasize AI-RAN integration, software-defined architectures, and ecosystem partnerships to bridge 5G-A to 6G.

NVIDIA Multi-Partner Commitment: NVIDIA rallied operators and vendors including Booz Allen, BT Group, Cisco, Deutsche Telekom, Ericsson, Nokia, SK Telecom, SoftBank, and T-Mobile to build open, secure AI-native 6G platforms. The focus is on software-defined wireless with AI embedded in RAN, edge, and core for integrated sensing, communications, and interoperability.

Nokia AI-RAN: Nokia highlighted new partnerships with Dell, Quanta, Red Hat, SuperMicro, NVIDIA, and operators like T-Mobile, Indosat Ooredoo Hutchison, BT, Elisa, NTT DOCOMO, and Vodafone for AI-RAN trials paving the way to cognitive 6G networks. Live demos at Nokia’s Hall 3 Booth 3B20 included Southeast Asia’s first AI-RAN Layer 3 5G call on shared GPU infrastructure and vision AI for immersive services.

T-Mobile & Deutsche Telekom Hub: T-Mobile US and (major shareholder) Deutsche Telekom launched a joint 6G Innovation Hub targeting AI-native autonomous networks, secure sensing/positioning, and connectivity-compute convergence for Physical AI. It builds on agentic AI proofs like network-integrated translation, emphasizing “kinetic tokens” for real-time physical world control.

ZTE GigaMIMO 6G Prototype: ZTE unveiled the world’s first 6G prototype with 2000+ U6G-band antenna elements (GigaMIMO), powered by AI algorithms for 10x capacity over 5G-A, 30% spectral efficiency gains, and AI-driven immersive services. Booth 3F30 demos integrate AI across connectivity, computing, and devices for “AI serves AI” networks.